Filed Pursuant to Rule 424(b)(3)

Registration No. 333-267053

PROSPECTUS

Waldencast plc

Up to 29,533,282 Class A Ordinary Shares (for issuance)

Up to 121,120,063 Class A Ordinary Shares (for resale)

Up to 18,033,332 Warrants to Purchase Class A Ordinary Shares (for resale)

This prospectus relates to the issuance by us of up to 29,533,282 Class A ordinary shares, par value $0.0001 (“Class A ordinary shares”), consisting of: (i) Class A ordinary shares issuable upon the exercise of the private placement warrants (as defined below) and (ii) Class A ordinary shares issuable upon the exercise of the public warrants (as defined below).

This prospectus also relates to the resale by certain of the selling holders named in this prospectus and their pledgees, donees, transferees, assignees and successors (the “Selling Holders”) of: (1) up to 121,120,063 Class A ordinary shares, consisting of (i) 8,545,000 Class A ordinary shares converted from the founder shares (as defined below) held in the aggregate by Burwell Mountain PTC LLC, as trustee of Burwell Mountain Trust (collectively, “Burwell”), Dynamo Master Fund and Waldencast Ventures LP (each, a member of the Waldencast Long-Term Capital LLC, a Cayman Islands limited liability company (the “Sponsor”)), originally issued in a private placement to the Sponsor, for approximately $0.0035 per share, prior to our initial public offering (as defined below); (ii) 80,000 Class A ordinary shares converted from the founder shares held by the Investor Directors (as defined below), issued in a private placement to the Investor Directors, for approximately $0.0035 per share, prior to our initial public offering; (iii) 20,000 Class A ordinary shares issued to Aaron Chatterley, one of our independent directors, in a private placement exempt from registration pursuant to Section 4(a)(2) of the Securities Act, and Rule 506 of Regulation D promulgated thereunder, in connection with the consummation of the Business Combination (as defined below), for no consideration; (iv) 28,237,506 Class A ordinary shares issued in connection with the Business Combination as the equity portion of the merger consideration pursuant to the Obagi Merger Agreement (as defined below) at an acquiror share value of $10.00 per share; (v) 21,104,225 Class A ordinary shares issuable in exchange for 21,104,225 Waldencast LP Common Units (as defined below) (and the redemption by Waldencast of an equivalent number of Class B ordinary shares, par value $0.0001 per share (“Class B ordinary shares”) held by such holder for no additional consideration) issued in connection with the Business Combination as the equity portion of the transaction consideration pursuant to the Milk Equity Purchase Agreement (as defined below) at a common unit value of $10.00 per unit; (vi) 11,800,000 Class A ordinary shares issued in the PIPE Investments (as defined below) pursuant to the Subscription Agreements (as defined below), at a purchase price of $10.00 per share at the closing of the Business Combination; (vii) 33,300,000 Class A ordinary shares issued pursuant the Forward Purchase Agreements (as defined below), which Forward Purchase Securities (as defined below) were issued at a purchase price of $10.00 per Forward Purchase Security at the closing of the Business Combination; and (viii) 18,033,332 Class A ordinary shares issuable upon the exercise of the private placement warrants and (2) up to 18,033,332 private placement warrants, which private placement warrants were issued in a private placement at the time of our initial public offering, at a purchase price of $1.50 per private placement warrant.

This prospectus provides you with a general description of such securities and the general manner in which we and the Selling Holders may offer or sell the securities. More specific terms of any securities that we and the Selling Holders may offer or sell may be provided in a prospectus supplement that describes, among other things, the specific amounts and prices of the securities being offered and the terms of the offering. The prospectus supplement may also add, update or change information contained in this prospectus.

The Class A ordinary shares being offered for resale pursuant to this prospectus by the Selling Holders represent approximately 82.5% of shares outstanding of the Company as of July 27, 2022 (after giving effect to the issuance of shares upon exercise of outstanding public warrants and private placement warrants). Of such shares, 102,366,731 Class A ordinary shares, or approximately 70.0% of shares outstanding of the Company as of July 27, 2022 (after giving effect to the issuance of shares upon exercise of outstanding public warrants and private placement warrants), are subject to Lock-Up agreements pursuant to which certain of the Selling Holders have agreed not to transfer, assign or sell during the respective Lock-Up Periods (as defined below), which range from six months to twelve months from the closing of the Business Combination on June 27, 2022, subject to certain exceptions as described below. Nonetheless, given the substantial number of Class A ordinary shares being registered for potential resale by Selling Holders pursuant to this prospectus, the sale of shares by the Selling Holders, or the perception in the market that the Selling Holders of a large number of shares intend to sell shares, could increase the volatility of the market price of our Class A ordinary shares or result in a significant decline in the public trading price of our Class A ordinary shares. Even if our trading price is significantly below $10.00, the offering price for the Legacy units (as defined below) offered in our initial public offering, the per share price of the shares issued in the PIPE Investment and the per Forward Purchase Security price of the Forward Purchase Security issued pursuant to the Forward Purchase Agreements, certain of the Selling Holders, including Burwell, Dynamo Master Fund and Waldencast Ventures LP, may still have an incentive to sell our Class A ordinary shares because they hold founder shares that were originally purchased by the Sponsor at prices lower than the public investors or the current trading price of our Class A ordinary shares. For example, based on the closing price of our Class A ordinary shares of $8.22 as of October 12, 2022, the holders of the 8,625,000 Class A ordinary shares converted from the founder shares would experience a potential profit of up to approximately $8.22 per share, or up to approximately $70.9 million in the aggregate.

We will not receive any proceeds from the sale of the Class A ordinary shares or warrants by the Selling Holders pursuant to this prospectus. We also will not receive any proceeds from the issuance of the Class A ordinary shares by us pursuant to this prospectus, except with respect to amounts received by us upon exercise of the warrants to the extent such warrants are exercised for cash. We believe the likelihood that warrant holders will exercise their warrants, and therefore the amount of cash proceeds that we would receive, is dependent upon the trading price of our Class A ordinary shares. As of the date of this prospectus, our warrants are “out-of-the money,” which means that the trading price of Class A ordinary shares underlying our warrants is below the $11.50 exercise price of the warrants. For so long as the warrants remain “out-of-the money,” we do not expect warrant holders to exercise their warrants and, therefore, we do not expect to receive cash proceeds from any such exercise. See the risk factor entitled “There is no guarantee that the warrants will ever be in the money, and they may expire worthless” for more information.

We will pay the expenses, other than underwriting discounts and commissions, associated with the sale of securities pursuant to this prospectus. Our registration of the securities covered by this prospectus does not mean that either we or the Selling Holders will issue, offer or sell, as applicable, any of the securities. The Selling Holders may offer and sell the securities covered by this prospectus in a number of different ways and at varying prices. We provide more information in the section entitled “Plan of Distribution.”

You should read this prospectus and any prospectus supplement or amendment carefully before you invest in our securities.

Our Class A ordinary shares and warrants are traded on The Nasdaq Stock Market LLC (“Nasdaq”) under the symbols “WALD” and “WALDW,” respectively. On October 12, 2022, the closing price of our Class A ordinary shares was $8.22 per share and the closing price of our warrants was $0.62 per warrant.

Investing in our securities involves risks. See “Risk Factors” beginning on page 10 and in any applicable prospectus supplement.

None of the U.S. Securities and Exchange Commission or any state securities commission has approved or disapproved of the securities or determined if this prospectus is accurate or adequate. Any representation to the contrary is a criminal offense.

The date of this prospectus is October 13, 2022.

i

This prospectus is part of a registration statement on Form F-1 that we filed with the SEC using a “shelf” registration process. Under this shelf registration process, we and the Selling Holders may, from time to time, issue, offer and sell, as applicable, any combination of the securities described in this prospectus in one or more offerings. We may use the shelf registration statement to issue up to an aggregate of 29,533,282 Class A ordinary shares upon exercise of the public warrants and private placement warrants. The Selling Holders may use the shelf registration statement to sell up to an aggregate of 121,120,063 Class A ordinary shares and up to 18,033,332 warrants from time to time through any means described in the section entitled “Plan of Distribution.” More specific terms of any securities that the Selling Holders offer and sell may be provided in a prospectus supplement that describes, among other things, the specific amounts and prices of the Class A ordinary shares and/or warrants being offered and the terms of the offering.

A prospectus supplement may also add, update or change information included in this prospectus. Any statement contained in this prospectus will be deemed to be modified or superseded for purposes of this prospectus to the extent that a statement contained in such prospectus supplement modifies or supersedes such statement. Any statement so modified will be deemed to constitute a part of this prospectus only as so modified, and any statement so superseded will be deemed not to constitute a part of this prospectus. You should rely only on the information contained in this prospectus, any applicable prospectus supplement or any related free writing prospectus. See “Where You Can Find More Information.”

Neither we nor the Selling Holders have authorized anyone to provide any information or to make any representations other than those contained in this prospectus, any accompanying prospectus supplement or any free writing prospectus we have prepared. We and the Selling Holders take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the securities offered hereby and only under circumstances and in jurisdictions where it is lawful to do so. No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus, any applicable prospectus supplement or any related free writing prospectus. This prospectus is not an offer to sell securities, and it is not soliciting an offer to buy securities, in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus or any prospectus supplement is accurate only as of the date on the front of those documents only, regardless of the time of delivery of this prospectus or any applicable prospectus supplement, or any sale of a security. Our business, financial condition, results of operations and prospects may have changed since those dates.

This prospectus contains summaries of certain provisions contained in some of the documents described herein, but reference is made to the actual documents for complete information. All of the summaries are qualified in their entirety by the actual documents. Copies of some of the documents referred to herein have been filed, will be filed or will be incorporated by reference as exhibits to the registration statement of which this prospectus is a part, and you may obtain copies of those documents as described below under “Where You Can Find More Information.”

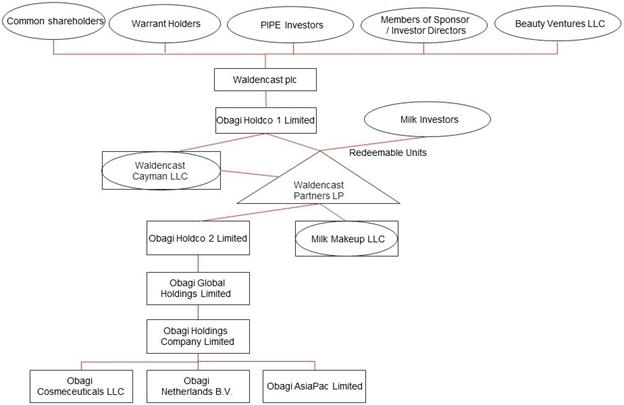

On July 27, 2022 (the “Closing Date”), we consummated the previously announced business combination with Obagi Global Holdings Limited, a Cayman Islands exempted company limited by shares (“Obagi”), and Milk Makeup LLC, a Delaware limited liability company (“Milk”). Pursuant to the Agreement and Plan of Merger, dated as of November 15, 2021 (the “Obagi Merger Agreement”), by and among us, Obagi Merger Sub, Inc., a Cayman Islands exempted company limited by shares and our indirect subsidiary (“Merger Sub”), and Obagi, Merger Sub merged with and into Obagi, with Obagi surviving as our indirect subsidiary (the “Obagi Merger”). Pursuant to the Equity Purchase Agreement, dated as of November 15, 2021 (the “Milk Equity Purchase Agreement” and, together with the Obagi Merger Agreement, the “Transaction Agreements”), by and among us, Obagi Holdco 1 Limited, a limited company incorporated under the laws of Jersey (“Holdco 1”), Waldencast Partners LP, a Cayman Islands exempted limited partnership (“Waldencast LP” and together with Holdco 1, the “Milk Purchasers”), Milk, certain former members of Milk (the “Milk Members”), and Shareholder Representative Services LLC, a Colorado limited liability company, solely in its capacity as representative of the Milk Members (the “Equityholder Representative”), the Milk Purchasers acquired from the Milk Members, and the Milk Members sold to the Milk Purchasers, all of the issued and outstanding membership units of Milk (the “Milk Membership Units”) in exchange for the Milk Cash Consideration (as defined in the Milk Equity Purchase Agreement), the Milk Equity Consideration (as defined in the Milk Equity Purchase Agreement), which consists of partnership units of Waldencast LP (“Waldencast LP Common Units”) exchangeable for our Class A ordinary shares, and our Class B ordinary shares (the “Milk Transaction”).

ii

On July 26, 2022, prior to the Closing Date, with the approval of our shareholders, and in accordance with the Companies Act (As Revised) of the Cayman Islands (“Cayman Act”), the Companies (Jersey) Law 1991, as amended (the “Jersey Companies Law”), and our amended and restated memorandum and articles of association (the “Constitutional Document”), we effected a deregistration under the Cayman Act and a domestication under Part 18C of the Jersey Companies Law, pursuant to which our jurisdiction of incorporation was changed from the Cayman Islands to Jersey and we changed our name from “Waldencast Acquisition Corp.” to “Waldencast plc” (the “Domestication” and, collectively with the Obagi Merger, the Milk Transaction and the other transactions contemplated by the Transaction Agreements, the “Business Combination”).

The Jersey Financial Services Commission (the “JFSC”) has given, and has not withdrawn, its consent under Article 4 of the Control of Borrowing (Jersey) Order 1958 to the issue of the warrants.

The JFSC is protected by the Control of Borrowing (Jersey) Law 1947, as amended, against liability arising from the discharge of its functions under that Law.

A copy of this prospectus has been delivered to the Jersey Registrar of Companies (the “Jersey Registrar”) in accordance with Article 5 of the Companies (General Provisions) (Jersey) Order 2002 and the Jersey Registrar has given, and has not withdrawn, his consent to its circulation.

It must be directly understood that, in giving these consents, neither the Jersey Registrar nor the JFSC takes any responsibility for the financial soundness of the Company or for the correctness of any statements made, or opinions expressed, with regard to it.

The JFSC is protected by the Control of Borrowing (Jersey) Law 1947, as amended, against liability arising from the discharge of its functions under that law.

The directors of the Company have taken all reasonable care to ensure that the facts stated in this prospectus are true and accurate in all material respects, and that there are no other facts the omission of which would make misleading any statement in the document, whether or facts or of opinion. The directors accept responsibility accordingly.

It should be remembered that the price of securities and the income from them can go down as well as up.

If you are in any doubt about the contents of this prospectus, you should consult your stockbroker, bank manager, solicitor, accountant or financial adviser.

Unless the context indicates otherwise, references to the “Company,” “Waldencast,” “we,” “us” and “our” refer, prior to the Business Combination, to Waldencast Acquisition Corp., and, following the Business Combination, to Waldencast plc, including its subsidiaries.

iii

This document contains references to trademarks and service marks belonging to other entities. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ® or ™ symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

iv

Unless stated in this prospectus or the context otherwise requires, references to:

| ● | “affiliate” or “Affiliate” means, with respect to any specified Person, any Person that, directly or indirectly, controls, is controlled by, or is under common control with, such specified Person, whether through one or more intermediaries or otherwise. The term “control” (including the terms “controlling,” “controlled by” and “under common control with”) means the possession, directly or indirectly, of the power to direct or cause the direction of the management and policies of a Person, whether through the ownership of voting securities, by contract or otherwise; |

| ● | “Beauty FPA Investor” means the Sponsor, in its capacity as managing member of Beauty Ventures; |

| ● | “Beauty Ventures” means Beauty Ventures LLC, a Cayman Islands limited liability company, that is managed by the Sponsor; |

| ● | “Board” means our board of directors; |

| ● | “Business Combination” means the Obagi Merger, the Milk Transaction, the other transactions contemplated by the Transaction Agreements and the Domestication; |

| ● | “Cedarwalk” means Cedarwalk Skincare Ltd., a Cayman Islands exempted company limited by shares; |

| ● | “Class A ordinary shares” means our Class A ordinary shares, par value $0.0001 per share; |

| ● | “Class B ordinary shares” means our Class B ordinary shares, par value $0.0001 per share; |

| ● | “Closing Date” means the date of the Obagi Closing and the date of the Milk Closing, together; |

| ● | “Code” means the U.S. Internal Revenue Code of 1986, as amended; |

| ● | “Constitutional Document” means our memorandum and articles of association; |

| ● | “Continental” means Continental Stock Transfer & Trust Company; |

| ● | “COVID-19” means SARS-CoV-2 or COVID-19, and any evolutions or mutations thereof or related or associated epidemics, pandemics or disease outbreaks; |

| ● | “Dollars” or “$” means lawful money of the U.S.; |

| ● | “Domestication” means the domestication by way of continuance of Waldencast as a Jersey public limited company and deregistration in the Cayman Islands in accordance with Part 18C of the Jersey Companies Law and the Cayman Islands Companies Act; |

| ● | “DTC” means The Depository Trust Company; |

| ● | “Exchange Act” means the Securities Exchange Act of 1934, as amended; |

| ● | “Forward Purchaser” means each of Burwell, Dynamo Master Fund, and Beauty Ventures; |

| ● | “Forward Purchase Agreements” means the Third-Party Forward Purchase Agreement and the Sponsor Forward Purchase Agreement, together; |

| ● | “Forward Purchase Securities” means the Class A ordinary shares and warrants issued pursuant to the Forward Purchase Agreements; |

v

| ● | “founder shares” means the Waldencast Acquisition Corp. Class B ordinary shares purchased by the Sponsor in a private placement prior to the initial public offering, and the Class A ordinary shares issued upon the conversion thereof; |

| ● | “GAAP” means generally accepted accounting principles in the U.S.; |

| ● | “Governmental Authority” means any federal, state, provincial, municipal, local or foreign government, governmental authority, regulatory or administrative agency, governmental commission, department, board, bureau, agency or instrumentality, court or tribunal, or arbitrator; |

| ● | “Holdco 1” means Obagi Holdco 1 Limited, a private limited company incorporated under the laws of Jersey; |

| ● | “Holdco 2” means Obagi Holdco 2 Limited, a private limited company incorporated under the laws of Jersey; |

| ● | “initial public offering” means our initial public offering that was consummated on March 18, 2021; |

| ● | “Investor Directors” means Sarah Brown, Juliette Hickman, Lindsay Pattison and Zach Werner; |

| ● | “Investor Rights Agreement” means the Investor Rights Agreement, dated July 27, 2022, entered into by and among us, Cedarwalk, the Sponsor and CWC Skincare Ltd., the guarantor of Cedarwalk’s obligations thereunder; |

| ● | “IRS” means the U.S. Internal Revenue Service; |

| ● | “Jersey Companies Law” means the Companies (Jersey) Law 1991, as amended; |

| ● | “JOBS Act” means the Jumpstart Our Business Startups Act of 2012; |

| ● | “Legacy units” means the units of Waldencast Acquisition Corp., each unit representing one Class A ordinary share and one-third of one redeemable warrant to acquire one Class A ordinary share; |

| ● | “Lock-Up Agreements” means the Obagi Lock-Up Agreement and the Milk Lock-Up Agreement, together; |

| ● | “Merger Sub” means Obagi Merger Sub, Inc., a Cayman Islands exempted company limited by shares; |

| ● | “Milk” means Milk Makeup LLC, a Delaware limited liability company; |

| ● | “Milk Closing” means the closing of the transactions contemplated by the Milk Equity Purchase Agreement; |

| ● | “Milk Equity Purchase Agreement” means the Equity Purchase Agreement, dated as of November 15, 2021, by and among us, Waldencast LP, Holdco 1, Milk, the Milk Members and the Equityholder Representative; |

| ● | “Milk Lock-Up Agreement” means each of the lock-up agreements, dated as of July 27, 2022, entered into by each of the Milk Members; |

| ● | “Milk Members” means the preferred and common members of Milk; |

| ● | “Milk Membership Units” mean the issued and outstanding membership units of Milk; |

| ● | “Milk Transaction” means the Milk Purchasers’ acquisition from the Milk Members, and the Milk Members’ sale to the Milk Purchasers, of the Milk Membership Units in exchange for the Milk Cash Consideration (as defined in the Milk Equity Purchase Agreement), the Milk Equity Consideration (as defined in the Milk Equity Purchase Agreement), which consists of Waldencast LP Common Units exchangeable for our Class A ordinary shares, and our Class B ordinary shares; |

| ● | “Nasdaq” means The Nasdaq Stock Market LLC; |

vi

| ● | “Obagi” means Obagi Global Holdings Limited, a Cayman Islands exempted company limited by shares; |

| ● | “Obagi Closing” means the closing of the transactions contemplated by the Obagi Merger Agreement; |

| ● | “Obagi Common Stock” means the shares in the capital of Obagi of par value US $0.50 each per share; |

| ● | “Obagi Holdco” means Obagi Holdings Company Limited, a Cayman Islands exempted company limited by shares; |

| ● | “Obagi Hong Kong” means Obagi Hong Kong Limited; |

| ● | “Obagi Lock-Up Agreement” means each of the lock-up agreements, dated as of July 27, 2022, entered into by each of the Obagi Shareholders; |

| ● | “Obagi Merger” means the merger of Merger Sub with and into Obagi, with Obagi surviving the merger as a wholly owned subsidiary of Holdco 2; |

| ● | “Obagi Merger Agreement” means that certain Agreement and Plan of Merger, dated as of November 15, 2021, by and among us, Merger Sub and Obagi; |

| ● | “Obagi Shareholders” means the shareholders of Obagi; |

| ● | “Obagi Worldwide” means Obagi Cosmeceuticals LLC, a Delaware limited liability company, and Obagi Holdings Company Limited, a Cayman Islands exempted company limited by shares; |

| ● | “ordinary shares” means our Class A ordinary shares and our Class B ordinary shares, collectively; |

| ● | “Person” means any individual, firm, corporation, partnership, exempted limited partnership, limited liability company, exempted company, incorporated or unincorporated association, joint venture, joint stock company, Governmental Authority or instrumentality or other entity of any kind; |

| ● | “PFIC” means a passive foreign investment company; |

| ● | “PIPE Investment” means the purchase of our shares pursuant to the PIPE Subscription Agreements; |

| ● | “PIPE Investors” means those certain investors participating in the purchase of our shares pursuant to the PIPE Subscription Agreements; |

| ● | “private placement warrants” means those certain private placement warrants issued (i) in connection with the consummation of our initial public offering in a private placement to our Sponsor; and/or (ii) in connection with the consummation of our Business Combination in a private placement (A) pursuant to the Forward Purchase Agreements and (B) as a result of the conversion of $1,500,000 working capital loans, at the price of $1.50 per warrant; |

| ● | “public warrants” means the redeemable warrants (including those underlying the units) that were offered and sold by us in our initial public offering and registered pursuant to the initial public offering registration statement or our redeemable warrants issued as a matter of law upon the conversion thereof at the time of the Domestication, as context requires; |

| ● | “Registration Rights Agreement” means the Amended and Restated Registration Rights Agreement, dated as of July 27, 2022, entered into by and among us, the Sponsor and certain of our shareholders, Obagi and Milk and certain of their respective affiliates; |

| ● | “Sarbanes-Oxley Act” means the Sarbanes-Oxley Act of 2002, as amended; |

| ● | “SEC” means the U.S. Securities and Exchange Commission; |

vii

| ● | “Securities Act” means the Securities Act of 1933, as amended; |

| ● | “Sponsor” means Waldencast Long-Term Capital LLC, a Cayman Islands limited liability company; |

| ● | “Stockholder Support Agreement” means that certain Support Agreement, dated November 15, 2021, by and among us, Cedarwalk and Obagi, as amended and modified from time to time; |

| ● | “Transaction Agreements” means the Obagi Merger Agreement together with the Milk Equity Purchase Agreement; |

| ● | “Transactions” means the Obagi Merger together with the Milk Transaction; |

| ● | “transfer agent” means Continental, acting as transfer agent; |

| ● | “U.S. Holder” means a beneficial owner of our Class A ordinary shares who or that is, for U.S. federal income tax purposes: (a) an individual citizen or resident of the U.S., (b) a corporation (or other entity that is treated as a corporation for U.S. federal income tax purposes) that is created or organized (or treated as created or organized) in or under the laws of the U.S. or any state thereof or the District of Columbia, (c) an estate whose income is subject to U.S. federal income tax regardless of its source, or (d) a trust if (i) a U.S. court can exercise primary supervision over the administration of such trust and one or more U.S. persons have the authority to control all substantial decisions of the trust or (ii) it has a valid election in place to be treated as a U.S. person; |

| ● | “Waldencast” and the “Registrant” mean Waldencast Acquisition Corp., a Cayman Islands exempted company limited by shares, prior to the Domestication, and Waldencast plc, a public limited company incorporated under the laws of Jersey, after the Domestication; |

| ● | “Waldencast LP” means Waldencast Partners LP, a Cayman Islands exempted limited partnership; |

| ● | “Waldencast LP Common Units” means limited partnership units of Waldencast LP that, in the case of such units issued as part of, or in respect of, the Milk Equity Consideration (as defined in the Milk Equity Purchase Agreement), are redeemable at the option of the holder of such units and, if such option is exercised, exchangeable for Class A ordinary shares or cash in accordance with the terms of the Amended and Restated Waldencast Partners LP Agreement; |

| ● | “warrants” means the public warrants and the private placement warrants; and |

| ● | “Working Capital Loans” means any loan made to Waldencast by any of the Sponsor, an affiliate of the Sponsor, or any of Waldencast’s officers or directors, and evidenced by a promissory note, for the purpose of financing costs incurred in connection with a Business Combination. |

Unless otherwise stated in this prospectus or the context otherwise requires, all references in this prospectus to our warrants include such Class A ordinary shares underlying the warrants.

viii

Cautionary Note Regarding Forward-Looking Statements

This prospectus contains statements that are forward-looking and as such are not historical facts. This includes, without limitation, statements regarding our financial position, business strategy and the plans and objectives of management for future operations. These statements constitute forecasts and forward-looking statements, and are not guarantees of performance. Such statements can be identified by the fact that they do not relate strictly to historical or current facts. When used in this prospectus, words such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “strive,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. When we discuss our strategies or plans, we are making forecasts or forward-looking statements. Such statements are based on the beliefs of, as well as assumptions made by and information currently available to, our management.

Forward-looking statements in this prospectus and in any document incorporated by reference in this prospectus may include, for example, statements about:

| ● | the inability to recognize the anticipated benefits of the transactions with Obagi and Milk; |

| ● | changes in general economic conditions, including as a result of the COVID-19 pandemic; |

| ● | the ability to continue to meet Nasdaq’s listing standards; |

| ● | volatility of our securities due to a variety of factors, including our inability to implement its business plans or meet or exceed its financial projections and changes; |

| ● | the ability to implement business plans, forecasts, and other expectations, and identify and realize additional opportunities; |

| ● | the ability of Waldencast to implement its strategic initiatives and continue to innovate Obagi’s and Milk’s existing products and anticipate and respond to market trends and changes in consumer preferences; and |

| ● | other factors detailed in the section entitled “Risk Factors.” |

The forward-looking statements contained in this prospectus and in any document incorporated by reference in this prospectus are based on current expectations and beliefs concerning future developments and their potential effects on us. There can be no assurance that future developments affecting us will be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described in the section entitled “Risk Factors” beginning on page 10 of this prospectus. Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

ix

This summary highlights, and is qualified in its entirety by, the more detailed information and financial statements included elsewhere in this prospectus. This summary does not contain all of the information that may be important to you in making your investment decision. You should read this entire prospectus carefully, including our financial statements and the related notes included in this prospectus and the information set forth under the headings “Risk Factors,” “Waldencast’s Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Obagi’s Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Milk’s Management’s Discussion and Analysis of Financial Condition and Results of Operations,” before deciding to invest in our Class A ordinary shares or warrants.

Overview

Waldencast

Founded by Michel Brousset and Hind Sebti, our ambition is to build a global best-in-class beauty and wellness operating platform by developing, acquiring, accelerating, and scaling conscious, high-growth purpose-driven brands. Our vision is fundamentally underpinned by our brand-led business model that ensures proximity to our customers, business agility and market responsiveness, while maintaining each brand’s distinct DNA. The first step in realizing our vision was the business combination with Obagi and Milk. As part of the Waldencast platform, our brands will benefit from the operational scale of a multi-brand platform; the expertise in managing global beauty brands at scale; a balanced portfolio to mitigate category fluctuations; asset light efficiency; and the market responsiveness and speed of entrepreneurial indie brands.

We were incorporated on December 8, 2020 as a Cayman Islands exempted company and a blank check company solely for the purpose of effecting the Business Combination, which was consummated on July 27, 2022. On July 26, 2022, with the approval of our shareholders, and in accordance with the Cayman Act, the Jersey Companies Law and the Constitutional Document, we effected the Domestication, pursuant to which our jurisdiction of incorporation was changed from the Cayman Islands to Jersey and our name was changed from Waldencast Acquisition Corp. to Waldencast plc, a public limited company incorporated under the laws of Jersey. Upon the closing of the Business Combination, we acquired the businesses of Obagi and Milk, which are now indirect subsidiaries of Waldencast.

Our Professional Skincare Segment: Obagi

Our professional skincare segment consists of the Obagi business. Obagi is currently headquartered in Long Beach, California, but will begin operating out of new headquarters in Houston, Texas in the third quarter of 2022. Obagi is a pioneer of the professional skincare category and its products are rooted in research and skin biology. Obagi develops, markets and sells innovative skin health products in more than 60 countries around the world. The Obagi® collection of products includes the following brands, with more than 200 products sold throughout the medical, spa and retail channels: Obagi Medical®, Obagi Clinical®, Obagi Professional™ and Skintrinsiq™. While the product portfolio consists predominantly of cosmetic and over-the-counter (“OTC”) drug products, Obagi does offer prescription-strength drug products, which require approval from the U.S. Food and Drug Administration (the “FDA”) prior to marketing. We have not sought or obtained FDA pre-market approval or foreign regulatory authorities’ authorization for any Obagi products, including the Skintrinsiq device, which we believe does not require marketing authorization from the FDA. These prescription-strength products include the Obagi Nu-Derm® System and related products, some of which contain a 4% concentration of the ingredient hydroquinone (“HQ”). These products are marketed as prescription-use only drugs but have not received marketing authorization from the FDA or other regulatory authorities. The FDA has historically utilized a risk-based enforcement approach with respect to drugs marketed without the required New Drug Application (“NDA”) in accordance with a Compliance Policy Guide (“CPG”) it issued in 2006 and subsequently amended in 2011, in which the FDA announced a drug safety initiative to remove unapproved drugs from the market, and established enforcement priorities and a policy of enforcement discretion with respect to marketed unapproved products. We believe Obagi’s prescription-only HQ products do not fall within the categories of unapproved drugs for which the FDA has indicated it prioritizes enforcement. We have not received any communications from the FDA or any similar regulatory authorities regarding its HQ or any of its other products. However, whether due to safety concerns or otherwise, in the future the FDA may choose to pursue an enforcement action against us and determine that Obagi HQ products should be removed from the market until we obtain FDA approval of the required NDA. Although Obagi prescription-only HQ products are made with 4% HQ, the FDA has historically expressed concerns regarding the safety of 2% HQ products sold on an OTC basis. In addition, the CARES Act implemented a number of changes to regulation of OTC drugs, one of which prohibited the sale of HQ (at any concentration level) from being marked in the U.S. as an OTC drug without FDA approval effective September 2020. On April 19, 2022, the FDA announced that it had issued warning letters to 12 companies for continuing to sell 2% HQ products on an OTC basis in violation of the CARES Act. The FDA’s announcement also cited reports describing serious side effects associated with the use of skin lightening products containing HQ, including reports of skin rashes, facial swelling, and ochronosis (discoloration of the skin). The FDA’s safety concerns regarding these lower-concentration OTC HQ products could prompt the FDA to assert that Obagi’s higher-concentration, prescription-only HQ products represent a higher priority for enforcement pursuant to the active CPG. In addition, Obagi’s prescription-only products are not currently available in pharmacies. Certain states, including Massachusetts, Montana, New Hampshire, New York and Texas, prohibit physicians from dispensing prescription products without a pharmacy or other license or authorization, permitting dispensing of such products only in certain limited circumstances. For these states we offer alternate products under our Obagi Nu-Derm Fx® and Obagi-C Fx product lines that contain the skin brightening ingredient arbutin rather than 4% HQ. Further, we are aware that the state of Texas and Puerto Rico, as well as certain credit card authorization vendors, have taken action against physician customers who sell Obagi’s prescription products to patients over the Internet. Most of these physicians ceased selling the prescription products online, offering them only in office to patients, and/or chose to sell Obagi’s alternate arbutin products online instead. These actions have not had a material impact on our or Obagi’s sales or net revenue. The Obagi Nu-Derm System and related products accounted for approximately 24.5% and 32.6% of our net revenue for the years ended December 31, 2021 and 2020, respectively, and 31.9% and 27.1% of our net revenue for the six months ended June 30, 2022 and 2021, respectively. For further details, see the section entitled “Our Business—Information About Obagi — The Skincare Market — Obagi Medical.”

1

Our “Clean” Makeup Segment: Milk

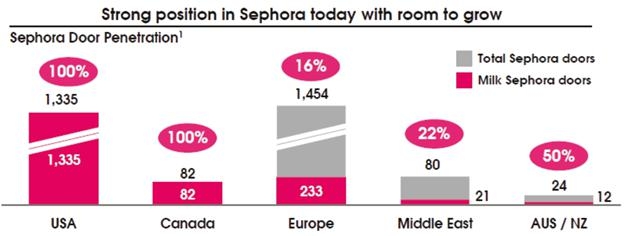

Our “clean” makeup segment consists of the Milk business. Milk is a leading, award-winning clean prestige makeup brand with unique products, a dedicated following among Gen-Z consumers and an emerging global presence. Milk has achieved significant growth thus far but believes even more significant growth opportunities remain in terms of building awareness, product and category expansion, channel expansion and regional expansion.

We believe that Milk’s inclusive brand values, “clean” product philosophy and commitments to sustainability and philanthropy are at the zeitgeist of what will motivate the next generation of beauty consumers around the world, and that these values and product attributes will only become more relevant. We believe that Milk’s ability to authentically connect with youth culture while developing unique, effective and easy to use products that are also 100% vegan, clean and cruelty-free sets Milk apart from other brands.

Milk was launched in 2016 with the goal of building a global movement to challenge and broaden the definition of beauty. Community and self-expression are at the heart of everything Milk does, believing that it’s not how you wear your makeup, it’s what you do in it that matters. This ethos is captured in Milk’s brand signature, “Live Your Look.”

Background

Domestication and Business Combination

On the Closing Date, we consummated the previously announced business combination with Obagi and Milk.

Pursuant to the Obagi Merger Agreement, by and among us, Merger Sub, and Obagi, Merger Sub merged with and into Obagi, with Obagi surviving as our indirect subsidiary.

Pursuant to the Milk Equity Purchase Agreement, by and among us, Holdco Purchaser, Waldencast LP, Milk, the Milk Members, and the Equityholder Representative, the Milk Purchasers acquired from the Milk Members, and the Milk Members sold to the Milk Purchasers, the Milk Membership Units in exchange for the Milk Cash Consideration (as defined in the Milk Equity Purchase Agreement), the Milk Equity Consideration (as defined in the Milk Equity Purchase Agreement), which consists of Waldencast LP Common Units exchangeable for our Class A ordinary shares, and our Class B ordinary shares.

On July 26, 2022, prior to the Closing Date, with the approval of our shareholders, and in accordance with the Cayman Act, the Jersey Companies Law, and the Constitutional Document, we effected a deregistration under the Cayman Act and a domestication under Part 18C of the Jersey Companies Law (by means of filing a memorandum and articles of association with the Registrar of Companies in Jersey), pursuant to which our jurisdiction of incorporation was changed from the Cayman Islands to Jersey and we changed our name from “Waldencast Acquisition Corp.” to “Waldencast plc.”

In connection with the Domestication: (i) each of the then issued and outstanding Waldencast Acquisition Corp. Class A ordinary shares, par value $0.0001 per share, converted automatically, on a one-for-one basis, into our Class A ordinary shares, par value $0.0001 per share, (ii) each of the then issued and outstanding Waldencast Acquisition Corp. Class B ordinary shares, par value $0.0001 per share, converted automatically, on a one-for-one basis, into our Class A ordinary shares, (iii) each of the then issued and outstanding Waldencast Acquisition Corp. warrants converted automatically, on a one-for-one basis, into our warrants, pursuant to the Warrant Agreement, dated March 15, 2021 (the “Warrant Agreement”), between us and Continental Stock Transfer & Trust Company, as warrant agent (the “Warrant Agent”), and (iv) each of the then issued and outstanding Waldencast Acquisition Corp. units were cancelled and the holders thereof were entitled, on a one-for-one basis, to one Class A ordinary share and one-third of one warrant.

The Business Combination was consummated on July 27, 2022. The transaction was unanimously approved by our Board and was approved at the extraordinary general meeting of our shareholders held on July 25, 2022 (the “Extraordinary General Meeting”). Our shareholders also voted to approve all other proposals presented at the Extraordinary General Meeting. As a result of the Business Combination, Obagi and Milk have become indirect subsidiaries of the Company.

The foregoing description of the Business Combination does not purport to be complete and is qualified in its entirety by the full text of the Obagi Merger Agreement, which is incorporated by reference hereto as Exhibit 2.1, and the full text of the Milk Equity Purchase Agreement, which is incorporated herein by reference hereto as Exhibit 2.2.

2

PIPE Investments & Forward Purchase Agreements

In connection with the execution of the Transaction Agreements, we entered into certain subscription agreements, executed on or prior to November 14, 2021 (the “Initial Subscription Agreements”), pursuant to which certain investors (the “Initial PIPE Investors”) agreed to purchase, in the aggregate, 10,500,000 Class A ordinary shares at $10.00 per share for an aggregate commitment amount of $105.0 million (the “Initial PIPE Investment”).

The Transaction Agreements provided that we could enter into additional subscription agreements with investors to participate in the purchase of our shares after November 15, 2021 but prior to the Closing Date. On June 14, 2022, we entered into subsequent subscription agreements (the “June Subsequent Subscription Agreements”) with certain investors (collectively, the “June Subsequent PIPE Investors”) on the same terms as the Initial PIPE Investors, pursuant to which the June Subsequent PIPE Investors collectively subscribed for 800,000 Class A ordinary shares for an aggregate purchase price equal to $8.0 million (the “June Subsequent PIPE Investment”).

On July 15, 2022, we further entered into subsequent subscription agreements (the “July Subsequent Subscription Agreements” and together with the Initial Subscription Agreements and the June Subsequent Subscription Agreements, the “PIPE Subscription Agreements”) with certain investors (collectively, the “July Subsequent PIPE Investors” and, together with the Initial PIPE Investors and the June Subsequent PIPE Investors, the “PIPE Investors”) on the same terms as the Initial PIPE Investors and the June Subsequent PIPE Investors. Pursuant to, and on the terms and subject to the conditions of the applicable July Subsequent Subscription Agreement, the July Subsequent PIPE Investors collectively subscribed for 500,000 Class A ordinary shares for an aggregate purchase price equal to $5,000,000 (the “July Subsequent PIPE Investment” and together with the Initial PIPE Investment and the June Subsequent PIPE Investment, the “PIPE Investment”).

In connection with our initial public offering; (i) on February 22, 2021, we, the Sponsor and Dynamo Master Fund (a member of the Sponsor) entered into a Forward Purchase Agreement (the “Sponsor Forward Purchase Agreement”), which was subsequently amended by the assignment and assumption agreement entered into by and between the Sponsor and Burwell on December 20, 2021, under which the Sponsor assigned, and Burwell assumed, all of the Sponsor’s rights and benefits under the Sponsor Forward Purchase Agreement, pursuant to which, Burwell and Dynamo Master Fund committed to subscribe for and purchase 16,000,000 Class A ordinary shares and 5,333,333 warrants for an aggregate commitment amount of $160.0 million; and (ii) we and Beauty Ventures LLC (“Beauty Ventures” and, together with Dynamo Master Fund and Burwell, the “Forward Purchasers”) entered into a Forward Purchase Agreement on March 1, 2021 (“the Third-Party Forward Purchase Agreement” and, together with the Sponsor Forward Purchase Agreement, the “Forward Purchase Agreements”), pursuant to which Beauty Ventures committed to subscribe for and purchase 17,300,000 Class A ordinary shares and up to 5,766,666 warrants for an aggregate commitment amount of $173.0 million. Members of our Sponsor or their affiliates will begin to receive a twenty percent (20%) performance fee allocation on the return of the forward purchase securities in excess of the hurdle rate, calculated on the total return generated from forward purchase securities (whether by dividend, transfer or increase in value as measured from date of issuance), when the return of such securities (less the expenses of Beauty Ventures) underlying the Third-Party Forward Purchase Agreement exceeds a hurdle rate of five percent (5%) accrued annually until the fifth anniversary of the issuance of such securities. In the event of a transfer and subsequent sale of any forward purchase securities prior to such fifth anniversary, the performance fee for the period between such transfer and such fifth anniversary will be calculated based on the proceeds generated by such sale.

We granted the PIPE Investors and the Forward Purchasers certain registration rights in connection with the PIPE Subscription Agreements and the Forward Purchase Agreements.

3

Lock-Up Restrictions

Pursuant to a Letter Agreement, dated March 15, 2021, between us and our initial shareholders (as amended, the “Letter Agreement”), such shareholders have agreed not to transfer, assign or sell any of their founder shares until the earlier to occur of: (A) July 27, 2023 (one year after the completion of our initial business combination); and (B) subsequent to our initial business combination (x) if the last reported sale price of our Class A ordinary shares equals or exceeds $12.00 per share (as adjusted for share sub-divisions, share dividends, rights issuances, consolidations, reorganizations, recapitalizations and other similar transactions) for any 20 trading days within any 30-trading day period commencing at least 150 days after our initial business combination or (y) the date on which we complete a liquidation, merger, share exchange, reorganization or other similar transaction that results in all of our public shareholders having the right to exchange their ordinary shares for cash, securities or other property (except with respect to permitted transferees). Any permitted transferees would be subject to the same restrictions and other agreements of our initial shareholders with respect to any founder shares.

In addition, pursuant to the Sponsor Forward Purchase Agreement, Burwell and Dynamo Master Fund agreed not to transfer, assign or sell any of their respective Forward Purchase Securities until the earlier to occur of: (A) July 27, 2023 (one year after the completion of our initial business combination); and (B) subsequent to our initial business combination (x) if the last reported sale price of our Class A ordinary shares equals or exceeds $12.00 per share (as adjusted for share sub-divisions, share dividends, rights issuances, consolidations, reorganizations, recapitalizations and other similar transactions) for any 20 trading days within any 30-trading day period commencing at least 150 days after our initial business combination or (y) the date on which we complete a liquidation, merger, share exchange, reorganization or other similar transaction that results in all of our public shareholders having the right to exchange their ordinary shares for cash, securities or other property (except with respect to permitted transferees). Any permitted transferees would be subject to the same restrictions and other agreements as a purchaser under the Sponsor Forward Purchase Agreement with respect to any such Forward Purchase Securities.

Further, pursuant to the Transaction Agreements, at the Closing Date, certain of the Obagi Shareholders entered into lock-up agreements (the “Obagi Lock-Up Agreement”) and certain of the Milk Members entered into lock-up agreements (the “Milk Lock-Up Agreement” and together with the Obagi Lock-Up Agreement, the “Lock-Up Agreements”), pursuant to which they agreed not to transfer, assign or sell during the respective Lock-Up Period (as defined below), (I) in the case of any of our Class A ordinary shares and the Waldencast LP Common Units, as applicable, received as consideration in connection with the Business Combination, until the earlier of (A) one year after the Closing and (B) (x) if the last reported sale price of our Class A ordinary shares equals or exceeds $12.00 per share (as adjusted for share sub-divisions, share dividends, rights issuances, reorganizations, recapitalizations and the like) for any 20 trading days within any 30-trading day period commencing at least 150 days after the date of the Closing or (y) the date on which we complete a liquidation, merger, share exchange, reorganization or other similar transaction that results in all of our shareholders having the right to exchange their Class A ordinary shares for cash, securities or other property; and (II) in the event that a certain portion of the Obagi Cash Consideration (as defined therein) or the Milk Cash Consideration (as defined therein) is paid in our equity of Waldencast as a result of the occurrence of certain events set forth in the Obagi Merger Agreement and the Milk Equity Purchase Agreement, as applicable, such equity of Waldencast received by Obagi or Milk, for the same period as set forth in clause (I) above, provided that solely for the purpose of this clause (II), the term “one-year” in clause (I)(A) shall be replaced with the term “six months.”

Corporate Information

We were incorporated as a Cayman Islands exempted company on December 8, 2020 under the name Waldencast Acquisition Corp. Upon the closing of the Business Combination, with the approval of our shareholders, and in accordance with the Cayman Act, the Jersey Companies Law, and the Constitutional Document, we effected a deregistration under the Cayman Act and a domestication under Part 18C of the Jersey Companies Law (by means of filing a memorandum and articles of association with the Registrar of Companies in Jersey), pursuant to which our jurisdiction of incorporation was changed from the Cayman Islands to Jersey and we changed our name from Waldencast Acquisition Corp. to Waldencast plc, a public limited company incorporated under the laws of Jersey. Our Class A ordinary shares and our warrants are listed on Nasdaq under the symbols “WALD” and “WALDW,” respectively. Our registered office is 2nd Floor Sir Walter Raleigh House, 48-50 Esplanade, St. Helier, Jersey JE2 3QB and our principal executive office is 10 Bank Street, Suite 560, White Plains, NY 10606, and our telephone number is (917) 546-6828. Our register of members is kept at our registered office. Our secretary is Maples Company Secretary (Jersey) Limited of 2nd Floor, Sir Walter Raleigh House, 48-50 Esplanade, St Helier, JE2 3QB, Jersey. Maples Company Secretary (Jersey) Limited is regulated to conduct trust company business by the JFSC pursuant to the Financial Services (Jersey) Law 1998. Our website address is www.waldencast.com. Our website and the information contained on, or that can be accessed through, our website is not deemed to be incorporated by reference in, and is not considered part of, this prospectus.

4

Emerging Growth Company

We are an “emerging growth company,” as defined in Section 2(a) of the Securities Act, as modified by the JOBS Act, and it may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies, including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved.

Further, Section 102(b)(1) of the JOBS Act exempts emerging growth companies from being required to comply with new or revised financial accounting standards until private companies (that is, those that have not had a Securities Act registration statement declared effective or do not have a class of securities registered under the Exchange Act) are required to comply with the new or revised financial accounting standards. The JOBS Act provides that a company can elect to opt out of the extended transition period and comply with the requirements that apply to non-emerging growth companies but any such election to opt out is irrevocable. We have elected not to opt out of such extended transition period, which means that when a standard is issued or revised and it has different application dates for public or private companies, we, as an emerging growth company, can adopt the new or revised standard at the time private companies adopt the new or revised standard. This may make comparison of our financial statements with certain other public companies difficult or impossible because of the potential differences in accounting standards used.

We will remain an emerging growth company until the earlier of: (1) the last day of the fiscal year (a) following the fifth anniversary of the closing of our initial public offering, (b) in which we have total annual gross revenue of at least $1,070.0 million or (c) in which we are deemed to be a large accelerated filer, which means the market value of its common equity that is held by non-affiliates exceeds $700.0 million as of the end of the prior fiscal year’s second fiscal quarter; and (2) the date on which we have issued more than $1,000 million in non-convertible debt securities during the prior three-year period. References herein to “emerging growth company” shall have the meaning associated with it in the JOBS Act.

Foreign Private Issuer

We are a “foreign private issuer” under SEC rules and will report under the Exchange Act as a non-U.S. company with “foreign private issuer” status and will be subject to the reporting requirements under the Exchange Act applicable to foreign private issuers. This means that, even after e no longer qualify as an “emerging growth company,” as long as we qualify as a “foreign private issuer” under the Exchange Act, we will be exempt from certain provisions of and intend to take advantage of certain exemptions from the Exchange Act that are applicable to U.S. public companies. Such exemptions include the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations in respect of a security registered under the Exchange Act and the sections of the Exchange Act requiring insiders to file public reports of their stock ownership.

Additionally, we will not be required to file our annual report on Form 20-F until 120 days after the end of each fiscal year and we will furnish reports on Form 6-K to the SEC regarding certain information required to be publicly disclosed by us in Jersey or that is distributed or required to be distributed by us to our shareholders. Further, based on our foreign private issuer status, we will not be required to file periodic reports and financial statements with the SEC as frequently or as promptly as a U.S. company whose securities are registered under the Exchange Act. We will also not be required to comply with Regulation FD, which addresses certain restrictions on the selective disclosure of material information. In addition, among other matters, our officers, directors and principal shareholders will be exempt from the reporting and “short-swing” profit recovery provisions of Section 16 of the Exchange Act and the rules under the Exchange Act with respect to their purchases and sales of our ordinary shares.

We may take advantage of these reporting exemptions until such time as it is no longer a “foreign private issuer.” We could lose our status as a “foreign private issuer” under current SEC rules and regulations if more than 50% of our outstanding voting securities become directly or indirectly held of record by U.S. holders and any one of the following is true: (i) the majority of our directors or executive officers are U.S. citizens or residents; (ii) more than 50% of our assets are located in the U.S.; or (iii) our business is administered principally in the U.S.

We may choose to take advantage of some but not all of these reduced burdens. We have taken advantage of reduced reporting requirements in this prospectus. Accordingly, the information contained in this prospectus may be different from the information you receive from our competitors that are public companies, or other public companies in which you have made an investment.

5

Risk Factors

You should consider carefully the risks and uncertainties described in this prospectus before investing in our securities. These risks are discussed more fully in the section titled “Risk Factors” following this summary. If any of these risks actually occur, our business, financial condition or results of operations would likely be materially adversely affected. These risks include, but are not limited to, the following:

Risks Related to Our Professional Skincare Segment: Obagi

| ● | The loss of a significant customer in our Obagi segment could materially and adversely affect our business, financial condition and results of operations. |

| ● | Our revenues and financial results depend significantly on sales of our Obagi Nu-Derm products. If we are unable to manufacture or sell the Nu-Derm products in sufficient quantities and in a timely manner, or maintain physician and/or patient acceptance of Nu-Derm products, our business will be materially and adversely impacted. |

| ● | We are dependent on third parties to manufacture products for our Obagi segment which entails several risks we would not face if we manufactured the products ourselves. | |

| ● | We rely on third parties to distribute Obagi products and the failure of these parties to provide their services on a timely basis or to comply with our quality standards and controls could materially and adversely affect our business |

| ● | The regulatory approval processes of the FDA and comparable foreign authorities for drugs are lengthy, time-consuming and inherently unpredictable, and if we are required to seek and obtain any regulatory approvals that may be required for our Obagi products, we may be unable to obtain or maintain such regulatory approvals, which would substantially harm our business. |

| ● | Our Obagi products containing the active ingredient, hydroquinone, are marketed as prescription-use only drugs but have not received required premarket authorization from the FDA or other regulatory authorities, and the FDA could require us to remove these products from the market until we obtain approval of the required NDA, and we could be found to be marketing and selling these products in violation of the law. |

| ● | Our Obagi products may cause adverse events or side effects, or could be associated with safety issues, that could result in recalls, withdrawals, or regulatory enforcement action. For example, the FDA has historically expressed concerns regarding the safety of HQ products, including risks for potentially serious side effects, including skin rashes, facial swelling, skin discoloration, carcinogenicity and reproductive toxicity. |

| ● | Failure to obtain regulatory approvals or to comply with regulations in foreign jurisdictions would prevent us from marketing our Obagi products internationally. |

6

Risks Related to Our “Clean” Makeup Segment: Milk

| ● | Our Milk segment has a history of net losses and may experience future losses. |

| ● | The loss of a significant reseller could materially and adversely affect our Milk segment’s business, financial condition and results of operations. |

| ● | We rely on a number of third-party suppliers, distributors and other vendors, and they may not continue to produce products or provide services that are consistent with our standards or applicable regulatory requirements, which could harm our brand. |

| ● | A negative reputation event to any of our Milk segment’s retail partners or beauty industry could cause a decline in our net revenues or a reduction in our earnings. |

| ● | We have growing operations in China, which exposes us to risks inherent in doing business in that country. |

| ● | We are involved, and may become involved in the future, in disputes and other legal or regulatory proceedings, including an ongoing legal proceeding involving our founders, that, if adversely decided or settled, could materially and adversely affect our business, financial condition and results of operations. |

General Business Risks and Risks Related to Our Financial Condition and Operations

| ● | We may make investments into or acquire other companies, which could divert our management’s attention, result in dilution to our shareholders and otherwise disrupt our operations, and we may have difficulty integrating any such acquisitions successfully or realizing the anticipated benefits therefrom, any of which could have an adverse effect on our business, financial condition and results of operations. |

| ● | We may face risks related to companies in the beauty and skincare industries. |

| ● | We face intense competition, in some cases from companies that have significantly greater resources than we do, which could limit our ability to generate sales and/or render our products obsolete. If we are unable to compete effectively, our results will suffer. |

| ● | A disruption in our operations could materially and adversely affect our business.

| |

| ● | Our new product introductions may not be as successful as we anticipate.

| |

| ● | Global or regional conditions may adversely affect our business. |

| ● | Your rights and responsibilities as a shareholder will be governed by Jersey law, which differs in some material respects with respect to the rights and responsibilities of shareholders of U.S. companies. |

| ● | Our only material asset is our indirect interest in Waldencast LP, and we are accordingly dependent upon distributions from Waldencast LP to pay dividends, taxes and other expenses. |

| ● | Any damage to our reputation or brands may materially and adversely affect our business, financial condition and results of operations. |

Risks Related to Ownership of our Class A ordinary shares and warrants

| ● | We are currently an emerging growth company within the meaning of the Securities Act, and to the extent we have taken advantage of certain exemptions from disclosure requirements available to emerging growth companies, this could make our securities less attractive to investors and may make it more difficult to compare our performance with other public companies. |

7

We are registering the issuance by us of up to 29,533,282 Class A ordinary shares that may be issued upon exercise of warrants to purchase Class A ordinary shares, including the public warrants and the private placement warrants. We are also registering the resale by the Selling Holders or their permitted transferees of (i) up to 121,120,063 Class A ordinary shares and (ii) up to 18,033,332 warrants. Any investment in the securities offered hereby is speculative and involves a high degree of risk. You should carefully consider the information set forth under “Risk Factors” on page 10 of this prospectus.

The following information is as of August 15, 2022 and does not give effect to issuances of our Class A ordinary shares or warrants after such date, or the exercise of warrants after such date.

Issuance of Class A Ordinary Shares

| Class A ordinary shares to be issued upon exercise of all public warrants and private placement warrant |

29,533,282 Class A ordinary shares. | |

| Class A ordinary shares outstanding prior to exercise of all public warrants and private placement warrants |

86,460,560 Class A ordinary shares. | |

| Use of proceeds | We will receive up to an aggregate of approximately $339.6 million from the exercise of all public warrants and private placement warrants assuming the exercise in full of all such warrants for cash. Unless we inform you otherwise in a prospectus supplement or free writing prospectus, to the extent we elect the exercise of such warrants for cash, we intend to use the net proceeds from such exercise for general corporate purposes. To the extent the warrants are exercised on a “cashless” basis, we will receive no proceeds. | |

| We believe the likelihood that warrant holders will exercise their warrants, and therefore the amount of cash proceeds that we would receive, is dependent upon the trading price of our Class A ordinary shares. Our warrants are currently out-of-the money, which means that the trading price of the Class A ordinary shares underlying our warrants is below the $11.50 exercise price of the warrants. For so long as the warrants remain “out-of-the money,” we do not expect warrant holders to exercise their warrants and, therefore, we do not expect to receive cash proceeds from any such exercise. See the risk factor entitled “There is no guarantee our warrants will ever be in the money, and they may expire worthless” for more information. |

8

Resale of Class A Ordinary Shares and Warrants

| Class A ordinary shares offered by the Selling Holders | 121,120,063 Class A ordinary shares. |

| Warrants offered by the Selling Holders | 18,033,332 warrants. |

| Exercise price for warrants | $11.50 |

| Redemption | The warrants are redeemable in certain circumstances. See “Description of Share Capital—Redeemable Warrants” for further discussion. |

| Use of proceeds | We will not receive any proceeds from the sale of the Class A ordinary shares and warrants to be offered by the Selling Holders. With respect to Class A ordinary shares underlying the warrants, we will not receive any proceeds from such shares except with respect to amounts received by us upon exercise of such warrants to the extent such warrants are exercised for cash. We believe the likelihood that warrant holders will exercise their warrants, and therefore the amount of cash proceeds that we would receive, is dependent upon the trading price of our Class A ordinary shares. Our warrants are currently out-of-the money, which means that the trading price of the Class A ordinary shares underlying our warrants is below the $11.50 exercise price of the warrants. For so long as the warrants remain “out-of-the money,” we do not expect warrant holders to exercise their warrants and, therefore, we do not expect to receive cash proceeds from any such exercise. See the risk factor entitled “There is no guarantee our warrants will ever be in the money, and they may expire worthless” for more information. |

| Lock-up agreements | Certain securities that are owned by the Selling Holders are subject to the lock-up provisions pursuant to the Letter Agreement, the Sponsor Forward Purchase Agreement or the Lock-Up Agreements, as applicable, which provide for certain restrictions on transfer until the termination of applicable lock-up periods. See the Letter Agreement, the Sponsor Forward Purchase Agreement and the Form of Lock-Up Agreement, which are filed as exhibits to the registration statement of which this prospectus forms a part. |

| Risk factors | See the section titled “Risk Factors” beginning on page 10 of this prospectus and other information included in this prospectus for a discussion of factors that you should consider carefully before deciding to invest in our Class A ordinary shares and warrants. |

| Nasdaq symbol for our Class A ordinary shares | “WALD.” |

| Nasdaq symbol for our warrants | “WALDW.” |

9

An investment in our Class A ordinary shares and warrants involves a high degree of risk. You should consider carefully the following risks, together with the financial and other information contained in this prospectus, including “Waldencast’s Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Obagi’s Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Milk’s Management’s Discussion and Analysis of Financial Condition and Results of Operations,” before you decide to purchase our Class A ordinary shares or warrants. If any of the following risks actually occur, our business, financial condition and operating results could be materially and adversely affected. In that case, the market price of our Class A ordinary shares and warrants could decline and you may lose all or a part of your investment. The risks discussed below are not the only risks we face. Additional risks or uncertainties not currently known to us, or that we currently deem immaterial, may also have a material adverse effect on our business, financial condition and operating results. See “Cautionary Note Regarding Forward-Looking Statements.”

Risks Related to Our Professional Skincare Segment: Obagi

The loss of a significant customer in our Obagi segment could materially and adversely affect our business, financial condition and results of operations.

Our Obagi products are sold in the U.S. to healthcare professionals through an authorized wholesale distributor, Boxout Health. Under this model, we sell the products to Boxout Health, which then sells the products through to our physician customers when they order them. As a result, Boxout Health accounted for approximately 34.8% and 54.1% of Obagi’s net revenue in the years ended December 31, 2021 and 2020, respectively, and approximately 32.7% and 41.0% of its net revenue for the six months ended June 30, 2022 and 2021, respectively. Our agreement with Boxout Health does not contain any minimum purchase requirements on its part. Accordingly, we do not have any guarantees regarding the quantity of each of our products that Boxout Health will order each quarter. We provide Boxout Health with forecasts of demand for our products from our physician customers, however, our forecasts may not always accurately assess demand for one or more products during any given quarter, which many affect subsequent orders for the affected products from them. Our e-commerce partners and international distributors purchase our products directly from us. One of our distributors in Southeast Asia, Gevie, Inc. together with its affiliate, Lemed, Inc. (collectively, the “SA Distributor”), accounted for approximately 28.0% and 8.1% of Obagi’s net revenue in the years ended December 31, 2021 and 2020, respectively, and 38.4% and 23.9% of its net revenue for the six months ended June 30, 2022 and 2021, respectively. Our agreement with the SA Distributor grants the SA Distributor a non-exclusive right to distribute our products in Vietnam and South Korea, contains minimum purchase requirements and has a term that expires on December 31, 2026. In January 2022, we executed an amendment with the SA Distributor to expand the countries within Southeast Asia in which it may distribute our products. Accordingly, our sales to such distributor may comprise an even greater proportion of our net revenue in the future. We are currently in discussions with the SA Distributor to expand the countries in Southeast Asia in which it may distribute our products. In the event that we do grant the SA Distributor the right to distribute products in additional countries, our sales to such distributor may comprise an even greater proportion of our net revenue in the future.

10

Our revenues and financial results depend significantly on sales of our Obagi Nu-Derm products. If we are unable to manufacture or sell the Nu-Derm products in sufficient quantities and in a timely manner, or maintain physician and/or patient acceptance of Nu-Derm products, our business will be materially and adversely impacted.

To date, a substantial portion of Obagi’s revenues have resulted from sales of our principal product line, the Obagi Nu-Derm System and related products. Nu-Derm products accounted for approximately 24.5% and 32.6% of Obagi’s net revenue for the years ended December 31, 2021 and 2020, respectively, and 31.9% and 27.1% of its net revenue for the six months ended June 30, 2022 and 2021, respectively. Although we currently offer other products such as Obagi-C Rx, Professional-C, ELASTIderm, CLENZIderm, Blue Peel products and our Obagi Clinical line, and intend to introduce additional new products, we still expect sales of our Obagi Nu-Derm System and related products to account for a substantial portion of our sales for the foreseeable future. Because our business is highly dependent on Nu-Derm products, factors adversely affecting the pricing of, or demand for, these products could have a material and adverse effect on our business.

Sales of our Obagi Nu-Derm products also experience seasonality. We believe this is due to variability in patient compliance that relates to several factors such as a tendency to travel and/or engage in other disruptive activities during the summer months. Additionally, our commercial success depends in large part on our ability to sustain market acceptance of the Nu-Derm System. If existing users of our products determine that our products do not satisfy their requirements, if our competitors develop a product that is perceived by patients or physicians to better satisfy their respective requirements, or if state or federal regulations or enforcement actions prohibit sales of the Nu-Derm System, individual products within the system, or any related products, sales of these products may decline, and our total net revenue may correspondingly decline. We cannot assure you that we will be able to continue to manufacture these products in commercial quantities at acceptable costs. Our inability to do so would adversely affect our operating results and cause our business to suffer.