UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended March 31, 2024

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from _________ to _________

Commission file number 001-40103

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

(Address of Principal Executive Offices) | (Zip Code) | ||||

(Registrant's telephone number, including area code)

Not Applicable

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☒ | |||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The registrant had outstanding 71,742,444 shares of Class A Common Stock (as defined herein) and 48,265,195 shares of Class B Common Stock (as defined herein) as of May 10, 2024.

Table of Contents

Condensed Consolidated Statement of Comprehensive Income (Loss) (Unaudited) | |||||

| 77 | |||||

2

Defined Terms

Capitalized terms used herein but not otherwise defined herein shall have the respective meanings ascribed to them in the Amended and Restated Business Combination Agreement, a copy of which is attached as Exhibit 2.1 to our Current Report on Form 8-K filed October 26, 2022.

•“AFM UK” means Alvarium Fund Managers (UK) Limited, an English private limited company.

•“AHRA” means “Alvarium Home REIT Advisors Limited”, an English private limited company.

•“Alvarium” means AlTi Asset Management Holdings 2 Limited, formerly known as Alvarium Investments Limited, an English private limited company.

•“AlTi” means AlTi Global, Inc., together with its consolidated subsidiaries.

•“Alvarium Shareholders” means the shareholders of Alvarium.

•“Alvarium Tiedemann” means the Company, prior to being renamed “AlTi Global, Inc.”

•“AlTi Global Topco” means AlTi Global Topco Limited, formerly known as Alvarium Topco, an Isle of Man entity which was established by Alvarium and owned by the Alvarium Shareholders.

•“ARE” means AlTi RE Limited, formerly known as Alvarium RE Limited, an English private limited company.

•“AUA” means assets under advisement.

•“AUM” means assets under management.

•“Business Combination” means the transactions contemplated by the Business Combination Agreement.

•“Business Combination Agreement” means the Amended and Restated Business Combination Agreement, dated as of October 25, 2022, by and among Cartesian, Umbrella Merger Sub, TWMH, TIG GP, TIG MGMT, Alvarium and Umbrella.

•“Business Combination Earn-out” means the Sponsor and the selling shareholders of TWMH, TIG, and Alvarium became entitled to receive earn-out shares contingent on various share price milestones upon Closing under the terms of the Business Combination.

•“Business Combination Earn-out Period” means the five years immediately after the Closing Date.

•“Business Combination Earn-out Securities” means the earn-out shares of Class A Common Stock in the Company and Class B Common Units that may be issued or become tradeable upon the achievement of certain stock price-based vesting conditions in accordance with the terms of the Business Combination Agreement.

•“Cartesian” means Cartesian Growth Corporation, a Cayman Islands exempted company, prior to the Business Combination.

•“Cayman Islands Companies Act” means the Cayman Islands Companies Act (as revised) of the Cayman Islands, as the same may be amended from time to time.

•“Class A Common Stock” means the Class A Common Stock, par value $0.0001 per share, of the Company, including any shares of such Class A Common Stock issuable upon the exercise of any warrant or other right to acquire shares of such Class A Common Stock.

3

•“Class B Common Stock” means the Class B Common Stock, par value $0.0001 per share, of the Company, including any shares of such Class B Common Stock issuable upon the exercise of any warrant or other right to acquire shares of such Class B Common Stock.

•“Class B Paired Interest” means a Class B Unit together with a share of Class B Common Stock.

•“Class B Units” means the limited liability company interests in Umbrella designated as Class B Common Units in the Umbrella LLC Agreement.

•“Closing” means the closing of the Business Combination.

•“Closing Date” means January 3, 2023, the date on which the Closing occurred.

•“Common Stock” refers to shares of the Class A Common Stock and the Class B Common Stock, collectively.

•“Company,” “our,” “we” or “us” means, prior to the Business Combination, Cartesian, as the context suggests, and, following the Business Combination, AlTi.

•“Condensed Consolidated Statement of Financial Position” refers to the consolidated balance sheet of AlTi Global, Inc.

•“Condensed Consolidated Statement of Operations” refers to the consolidated income statement of AlTi Global, Inc.

•“DGCL” refers to the Delaware General Corporation Law, as amended.

•“dollars” or “$” refers to U.S. dollars.

•“Domestication” means the continuation of Cartesian by way of domestication into a Delaware corporation, with the ordinary shares of Cartesian becoming shares of common stock of the Delaware corporation under the applicable provisions of the Cayman Islands Companies Act and the DGCL; the term includes all matters and necessary or ancillary changes in order to effect such Domestication, including the adoption of the Company’s certificate of incorporation consistent with the DGCL and changing the name and registered office of Cartesian.

•“Exchange Act” means the U.S. Securities Exchange Act of 1934, as amended.

•“External Strategic Managers” means global alternative asset managers with whom we partner by making strategic investments in which we actively participate in seeking to leverage the collective resources and synergies of the businesses to facilitate their growth.

•“Federal Reserve” means the Board of Governors of the Federal Reserve System.

•“FOS” means Family Office Service.

•"HLIF” means “Home Long Income Fund”, a private fund regulated by the UK FCA.

•“HNWI” means high net worth individual, being an individual having investable assets of $1 million or more, excluding primary residence, collectibles, consumables, and consumer durables.

•“Holbein” means Holbein Partners, LLP.

•“Home REIT” means “Home REIT plc”, a real estate investment trust listed on the London Stock Exchange.

4

•“Impact Investing” means investment practices seeking to generate various levels of financial performance together with the generation of positive measurable environmental and social impacts.

•“Nasdaq” means the Nasdaq Capital Market.

•“NAV” means net asset value.

•“PIPE Investors” means the subscribers that agreed to purchase shares of Class A Common Stock at the Closing pursuant to the private placements, including without limitation, as reflected in the subscription agreements between Cartesian and each of the PIPE Investors.

•“SEC” means the United States Securities and Exchange Commission.

•“SHIA” means Social Housing Income Advisors Limited, an English private limited company.

•“Sponsor” means CGC Sponsor LLC, a Cayman Islands limited liability company.

•“Strategic Alternatives” means the segment that includes the Company's alternatives platform, public and private real estate, and co-investment business, formerly known as Asset Management.

•“Target Companies” means, collectively, TWMH, TIG GP, TIG MGMT, and Alvarium.

•“Tax Receivable Agreement” or “TRA” means that certain Tax Receivable Agreement, dated as of January 3, 2023, by and among the Company and the TWMH Members, the TIG GP Members, and the TIG MGMT Members.

•“TIG” means, collectively, the TIG Entities and their subsidiaries and their predecessor entities where applicable.

•“TIG Entities” means, collectively, TIG GP and TIG MGMT and their predecessor entities where applicable.

•“TIG GP” means TIG Trinity GP, LLC, a Delaware limited liability company.

•“TIG GP Members” means the former members of TIG GP.

•“TIG MGMT” means TIG Trinity Management, LLC, a Delaware limited liability company.

•“TIG MGMT Members” means the former members of TIG MGMT.

•“TIH” means Tiedemann International Holdings, AG.

•“TRA Exchange” means the series of transactions in which certain holders of Class B Units and Class B Common Stock exchanged a portion of such interests to the Company, in exchange for Class A Common Stock.

•“TWMH” means, collectively, Tiedemann Wealth Management Holdings, LLC, a Delaware limited liability company, and its subsidiaries, and their predecessor entities where applicable.

•“TWMH Members” means the former members of TWMH.

•“UHNW” means ultra high net worth individual, being an individual having investable assets of $30 million or more, excluding primary residence, collectibles, consumables, and consumer durables.

•“UK FCA” means the United Kingdom’s Financial Conduct Authority.

5

•“Umbrella” means AlTi Global Capital, LLC (formerly known as Alvarium Tiedemann Capital, LLC), a Delaware limited liability company.

•“Umbrella LLC Agreement” means the Third Amended and Restated Limited Liability Company Agreement of AlTi Global Capital, LLC, effective as of July 31, 2023.

•“Umbrella Merger Sub” means Rook MS, LLC, a Delaware limited liability company.

•“US GAAP” means United States generally accepted accounting principles, consistently applied.

•“Warrants” means the warrants, which were initially issued in Cartesian’s initial public offering of its units pursuant to its registration statement on Form S-1 declared effective by the SEC on February 23, 2021, entitling the holder thereof to purchase one of Cartesian’s Class A ordinary shares at an exercise price of $11.50, subject to adjustment.

•“Wealth Management” means the segment that consists of the Company’s investment management and advisory services, trusts and administrative services, and family office services.

6

Available Information

We file annual, quarterly and current reports, proxy statements and other information required by the Exchange Act with the SEC. We make available free of charge on our website (www.alti-global.com) our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and other filings as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. We also use our website to distribute company information, including assets under management and performance information, and such information as may be deemed material. Accordingly, investors should monitor our website, in addition to our press releases, SEC filings and public conference calls and webcasts.

Also posted on our website in the “Investor Relations” section are the charters for our Audit, Finance and Risk Committee, Environmental, Social, Governance and Nominating Committee, and Human Capital and Compensation Committee, as well as our Corporate Governance Guidelines and Code of Business Conduct governing our directors, officers, and employees. Information on or accessible through our website is not a part of or incorporated into this Quarterly Report on Form 10-Q for the period ended March 31, 2024 (the “Quarterly Report”) or any other SEC filing. Copies of our SEC filings or corporate governance materials are available without charge upon written request to the Company at its principal place of business. Any materials we file with the SEC are also publicly available through the SEC’s website (www.sec.gov).

No statements herein, available on our website, or in any of the materials we file with the SEC constitute or should be viewed as constituting an offer to sell, or a solicitation of an offer to buy, securities in any jurisdiction.

Cautionary Note Regarding Forward-Looking Statements

This Quarterly Report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Exchange Act, which reflect our current views with respect to, among other things, future events, operations and financial performance. You can identify these forward-looking statements by the use of forward-looking words such as “outlook,” “believes,” “expects,” “potential,” “continues,” “may,” “will,” “should,” “seeks,” “approximately,” “predicts,” “projects,” “intends,” “plans,” “estimates,” “anticipates,” “target” or the negative version of those words, other comparable words or other statements that do not relate to historical or factual matters. The forward-looking statements are based on our beliefs, assumptions and expectations of our future performance, taking into account all information currently available to us. Such forward-looking statements are subject to various risks, uncertainties (some of which are beyond our control) or other assumptions relating to our operations, financial results, financial condition, business prospects, growth strategy and liquidity that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. Some of these factors are described under the headings “Part II. Item 1A. Risk Factors” and “Part I. Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.” These factors should not be construed as exhaustive and should be read in conjunction with the risk factors and other cautionary statements that are included in this Quarterly Report and in our other periodic filings. If one or more of these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, our actual results may vary materially from those indicated in these forward-looking statements. New risks and uncertainties arise over time, and it is not possible for us to predict those events or how they may affect us. Therefore, you should not place undue reliance on these forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made. We do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law.

7

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements (Unaudited)

AlTi Global, Inc.

Condensed Consolidated Statement of Financial Position (Unaudited)

| (Dollars in Thousands, except share data) | As of March 31, 2024 | As of December 31, 2023 | |||||||||

| Assets | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

Fees receivable, net (includes $ | |||||||||||

| Investments at fair value | |||||||||||

| Equity method investments | |||||||||||

| Intangible assets, net of accumulated amortization | |||||||||||

| Goodwill | |||||||||||

| Operating lease right-of-use assets | |||||||||||

| Other assets, net | |||||||||||

| Contingent consideration receivable | |||||||||||

| Assets held for sale | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities | |||||||||||

| Accounts payable and accrued expenses | $ | $ | |||||||||

| Accrued compensation and profit sharing | |||||||||||

| Accrued member distributions payable | |||||||||||

| Warrant liabilities, at fair value | |||||||||||

| Earn-out liability, at fair value | |||||||||||

TRA liability (includes $ | |||||||||||

| Delayed share purchase agreement | |||||||||||

| Earn-in consideration payable | |||||||||||

| Operating lease liabilities | |||||||||||

| Debt, net of unamortized deferred financing cost | |||||||||||

| Deferred tax liability, net | |||||||||||

| Deferred income | |||||||||||

| Other liabilities, net | |||||||||||

| Liabilities held for sale | |||||||||||

| Total liabilities | $ | $ | |||||||||

| Commitments and contingencies (Note 19) | |||||||||||

| Mezzanine Equity | |||||||||||

Series C Redeemable Cumulative Convertible Preferred stock, $ | |||||||||||

| Shareholders' Equity | |||||||||||

Common stock, Class A, $ | |||||||||||

Common stock, Class B, $ | |||||||||||

| Additional paid-in capital | |||||||||||

| Retained earnings (accumulated deficit) | ( | ( | |||||||||

| Accumulated other comprehensive income (loss) | |||||||||||

| Total AlTi Global, Inc. shareholders' equity | |||||||||||

| Non-controlling interest in subsidiaries | |||||||||||

| Total shareholders' equity | |||||||||||

| Total liabilities, mezzanine equity, and shareholders' equity | $ | $ | |||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

8

| For the Three Months Ended | |||||||||||

| (Dollars in Thousands) | March 31, 2024 | March 31, 2023 | |||||||||

| Revenue | |||||||||||

| Management/advisory fees | $ | $ | |||||||||

| Incentive fees | |||||||||||

| Distributions from investments | |||||||||||

| Other income/fees | |||||||||||

| Total income | |||||||||||

| Operating Expenses | |||||||||||

| Compensation and employee benefits | |||||||||||

| Systems, technology and telephone | |||||||||||

| Sales, distribution and marketing | |||||||||||

| Occupancy costs | |||||||||||

| Professional fees | |||||||||||

| Travel and entertainment | |||||||||||

| Depreciation and amortization | |||||||||||

| General, administrative and other | |||||||||||

| Total operating expenses | |||||||||||

| Total operating income (loss) | ( | ( | |||||||||

| Other Income (Expenses) | |||||||||||

| Gain (loss) on investments | ( | ||||||||||

| Gain (loss) on TRA | |||||||||||

| Loss on warrant liability | ( | ( | |||||||||

| Gain (loss) on earnout liability | ( | ||||||||||

| Interest expense | ( | ( | |||||||||

| Interest income | |||||||||||

| Other income (expense) | ( | ||||||||||

| Income (loss) before taxes | ( | ||||||||||

| Income tax (expense) benefit | ( | ( | |||||||||

| Net income (loss) | ( | ||||||||||

| Net loss (income) attributed to non-controlling interests in subsidiaries | ( | ( | |||||||||

| Net income (loss) attributable to AlTi Global, Inc. | $ | $ | ( | ||||||||

| Net Income (Loss) Per Share | |||||||||||

| Basic | $ | $ | ( | ||||||||

| Diluted | $ | $ | ( | ||||||||

| Weighted Average Shares of Class A Common Stock Outstanding | |||||||||||

| Basic | |||||||||||

| Diluted | |||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

9

AlTi Global, Inc.

Condensed Consolidated Statement of Comprehensive Income (Loss) (Unaudited)

| For the Three Months Ended | |||||||||||

| (Dollars in Thousands) | March 31, 2024 | March 31, 2023 | |||||||||

| Net income (loss) | ( | ||||||||||

| Other Comprehensive Income (Loss) | |||||||||||

| Foreign currency translation adjustments | ( | ||||||||||

| Other comprehensive income (loss) | ( | ||||||||||

| Total comprehensive income (loss) | ( | ||||||||||

| Other loss attributed to non-controlling interests in subsidiaries | ( | ( | |||||||||

| Comprehensive income (loss) attributable to AlTi Global, Inc. | ( | ||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

10

AlTi Global, Inc.

Condensed Consolidated Statement of Changes in Mezzanine Equity and Shareholders’ Equity (Unaudited)

| Mezzanine Equity | Shareholders’ Equity | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in Thousands, except share data) | Preferred Stock | Class A Common Stock | Class B Common Stock | Additional paid-in-capital | Retained earnings (accumulated deficit) | Accumulated other comprehensive income | Non-controlling interest in subsidiaries | Total Shareholders' Equity | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Shares | Amount | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at January 1, 2024 | $ | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income (loss) | — | — | — | — | — | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Currency translation adjustment | — | — | — | — | — | — | — | — | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income | — | — | — | — | — | — | — | — | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Payment for partner's tax | — | — | — | — | — | — | ( | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of preferred shares, net of issuance costs | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Preferred share dividend | — | — | — | — | ( | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of shares for business combination | — | — | — | — | — | — | ( | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Share based compensation | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shares issued to employees on vesting of equity awards | — | — | — | — | — | ( | — | — | — | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| TRA Exchange | — | — | — | ( | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| LXi deconsolidation | — | — | — | — | — | — | — | — | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at March 31, 2024 | $ | $ | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shareholders’ Equity | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in Thousands, except share data) | Class A Common Stock | Class B Common Stock | Additional paid-in-capital | Retained earnings (accumulated deficit) | Accumulated other comprehensive income | Non-controlling interest in subsidiaries | Total Shareholders' Equity | |||||||||||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at January 1, 2023 | $ | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of shares to Alvarium Employee Benefit Trust | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income (loss) | — | — | — | — | — | ( | — | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||

| Currency translation adjustment | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of shares - exercise of warrants | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at March 31, 2023 | $ | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

11

| For the Three Months Ended | |||||||||||

| (Dollars in Thousands) | March 31, 2024 | March 31, 2023 | |||||||||

| Cash Flows from Operating Activities | |||||||||||

| Net income (loss) | $ | $ | ( | ||||||||

| Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Amortization of debt discounts and deferred financing costs | |||||||||||

| Unrealized (gain) loss on investments | ( | ||||||||||

| Impairment loss on goodwill and intangible assets | |||||||||||

| Gain (loss) on TRA | ( | ( | |||||||||

| (Income) loss on equity method investments | ( | ||||||||||

| Fair value of warrant liability | |||||||||||

| Fair value of earn-out liability | ( | ||||||||||

| Deferred income tax (benefit) expense | ( | ||||||||||

| Equity-settled share-based payments | |||||||||||

| Unrealized foreign currency (gains)/losses | |||||||||||

| (Gain) loss from retirement of debt | ( | ||||||||||

| Forgiveness of debt shareholder loan | |||||||||||

| Fair value of interest rate swap | |||||||||||

| Cash flows due to changes in operating assets and liabilities | |||||||||||

| Fees receivable | |||||||||||

| Other assets | ( | ( | |||||||||

| Operating cash flow from operating leases | |||||||||||

| Accounts payable and accrued expenses | ( | ( | |||||||||

| Accrued compensation and profit sharing | ( | ( | |||||||||

| Other liabilities | ( | ||||||||||

| Other operating activities | |||||||||||

| Net cash provided by (used in) operating activities | ( | ( | |||||||||

| (Continued on the following page) | |||||||||||

12

| (Continued from the previous page) | For the Three Months Ended | ||||||||||

| (Dollars in Thousands) | March 31, 2024 | March 31, 2023 | |||||||||

| Cash Flows from Investing Activities | |||||||||||

| Cash payment for acquisition of TWMH and TIG historical equity | ( | ||||||||||

| Receipt of payments of notes receivable from members | |||||||||||

| Cash receipts from the repayment of advances and loans | |||||||||||

| Purchases of investments | ( | ( | |||||||||

| Cash payment for delayed share purchase agreement | ( | ||||||||||

| Payment of Payout Right | ( | ||||||||||

| Sales of investments | |||||||||||

| Proceeds from sale of LXi REIT Advisors | |||||||||||

| Purchases of fixed assets | ( | ( | |||||||||

| Net cash provided by (used in) investing activities | ( | ||||||||||

| Cash Flows from Financing Activities | |||||||||||

| Proceeds from issuance of preferred stock and warrants | |||||||||||

| Member contribution (distribution) | ( | ( | |||||||||

| Payments on term notes and lines of credit | ( | ( | |||||||||

| Borrowings on term notes and lines of credit | |||||||||||

| Payments of debt issuance costs | ( | ||||||||||

| Tax payments related to vesting of RSUs | ( | ||||||||||

| Increase (decrease) in distributions due to former TIG members | ( | ||||||||||

| Cash payment for purchase of shares to be transferred as part of Alvarium share compensation | ( | ||||||||||

| Cash receipts from exercise of Warrants | |||||||||||

| Payment of preferred stock issuance costs | ( | ||||||||||

| Other financing activities | |||||||||||

| Net cash provided by (used in) financing activities | ( | ||||||||||

| Effect of exchange rate changes on cash | ( | ||||||||||

| Net increase (decrease) in cash | ( | ||||||||||

| Cash and cash equivalents at beginning of the period | |||||||||||

| Cash and cash equivalents at end of the period | $ | $ | |||||||||

| Reconciliation of balance sheet cash and cash equivalents to cash flows: | |||||||||||

| Cash and cash equivalents on balance sheet | $ | $ | |||||||||

| Cash and cash equivalents included in Assets held for sale (Note 3) | $ | ||||||||||

| Cash and cash equivalents, including cash in Assets held for sale | $ | $ | |||||||||

| Supplemental Disclosure of Cash Flow Information | |||||||||||

| Cash Paid During the Period for: | |||||||||||

| Income taxes | |||||||||||

| Interest payments on term notes and lines of credit | |||||||||||

The accompanying notes are an integral part of these unaudited condensed consolidated financial statements.

13

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(1)Description of the Business

AlTi Global, Inc. is a multi-disciplinary financial services business, with a diverse array of investment, advisory, and administrative capabilities. The Company is a global organization that manages or advises approximately $71.0 billion in combined assets as of March 31, 2024. The Company provides holistic solutions for wealth management clients through a full spectrum of wealth management services, including discretionary investment management services, non-discretionary investment advisory services, trust services, administration services, and family office services. It also structures, arranges, and provides a network of investors with co-investment opportunities in a variety of alternative assets which are either managed intra-group or by carefully selected managers in the relevant asset class.

Business Combination

The Registrant was initially incorporated in the Cayman Islands as Cartesian Growth Capital, a special purpose acquisition company. In anticipation of the Business Combination:

•The holders of the equity of the TIG Entities contributed their TWMH and TIG equity to Umbrella making TWMH and the TIG wholly owned subsidiaries of Umbrella.

•Alvarium reorganized such that it became the wholly owned indirect subsidiary of AlTi Global Topco.

•Cartesian SPAC formed Umbrella Merger Sub.

Pursuant to the Business Combination on January 3, 2023:

•The Registrant was redomiciled as a Delaware corporation and changed its name to Alvarium Tiedemann Holdings, Inc. Effective April 19, 2023, Alvarium Tiedemann Holdings, Inc. changed its name to AlTi Global, Inc.

•The Registrant acquired all the outstanding share capital of AlTi Global Topco.

•Umbrella Merger Sub, LLC merged into Umbrella with AlTi Global Capital, LLC, formerly known as Alvarium Tiedemann Capital, LLC, as the surviving entity.

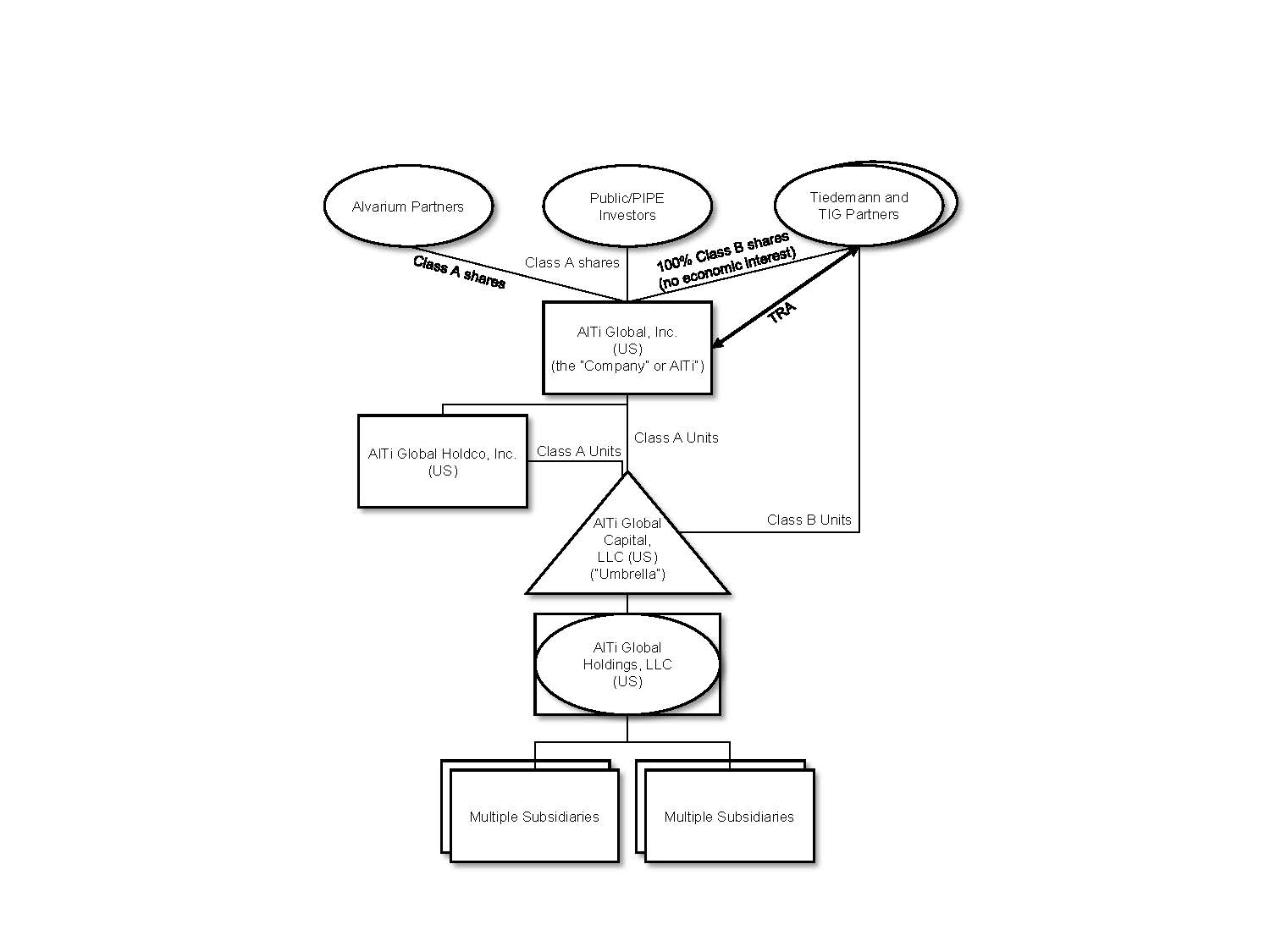

•The Company acquired 51 % of the equity interests of Umbrella, while the existing TWMH and TIG rollover shareholders hold a 49 % economic interest in Umbrella. Umbrella holds 100 % of the equity interests of TWMH, TIG, and Alvarium.

14

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

•Through a series of intercompany transactions, AlTi was restructured to reflect the below:

The Registrant has the following classes of shares and other instruments outstanding:

•Class A Common Stock – Shares of Class A Common Stock that are publicly traded. Class A shareholders are entitled to dividends on shares of Class A Common Stock declared by the Company’s board of directors. As of March 31, 2024, the shares of Class A Common Stock represent 55.1 % of the total voting power of all Common Stock.

•Class B Common Stock – Shares of Class B Common Stock that are not publicly traded. Class B shareholders are entitled to distributions declared by the Company’s board of directors. The distributions are paid by Umbrella. As of March 31, 2024, the shares of Class B Common Stock represent 37.4 % of the total voting power of all shares.

•Prior to the Business Combination, the Company issued warrants to purchase shares of Class A Common Stock at a price of $11.50 per share. Throughout the period from January 1, 2023 to March 31, 2023, 428,626 Warrants were exercised. On April 3, 2023, 78,864 Warrants were exercised. On June 7, 2023, the Company closed an offer and consent solicitation and entered into a warrant amendment, pursuant to which the remaining 19,892,387 Warrants were exchanged for 4,962,147 shares of Class A Common Stock. The exercises and exchanges throughout the period from January 1,

15

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

2023 to June 30, 2023 resulted in an increase in Additional Paid-in-Capital amount of $29.5 million. As of March 31, 2024, none of such Warrants were outstanding.

•Series C Cumulative Convertible Preferred Stock (the “Series C Preferred Stock”) – Shares of Series C Preferred Stock that are not publicly traded issued in connection with the sale (the “Transaction”) to CWC AlTi Investor LLC, an affiliate of Constellation Wealth Capital, LLC (“Constellation”) (combined with the Transaction, the “Constellation Transaction”). The Series C Preferred Stock will receive cumulative, compounding dividends at a rate of 9.75 % per year, subject to annual adjustments based on the stock price of the Class A Common Stock during the fourth quarter of each applicable year (subject to a maximum rate of 9.75 %) on the sum of (i) $1,000 per share plus, (ii) once compounded, any compounded dividends thereon ($1,000 per share plus accumulated compounded dividends and accrued but unpaid dividends through any date of determination). Dividends will be paid (at the option of the Company) as a payment in kind increase in the stated value of the issued shares of Series C Preferred Stock or in cash. The Series C Preferred Stock will also participate with any dividends or distributions declared on the Class A Common Stock. As of March 31, 2024, the shares of Series C Preferred Stock represent 7.5 % of the total voting power of all shares.

•In connection with the Constellation Transaction, the Company issued warrants (the “Constellation Warrants”) to purchase 1,533,333 shares of the Company’s Class A Common Stock at an exercise price of $7.40 per share. These warrants have been classified as a liability as of March 31, 2024. No Constellation Warrants were exercised during the current reporting period.

The following table presents the number of shares of the Registrant that were outstanding as of March 31, 2024 and December 31, 2023:

| As of March 31, 2024 | As of December 31, 2023 | ||||||||||

| Class A Common Stock | |||||||||||

| Class B Common Stock | |||||||||||

| Series C Preferred Stock | |||||||||||

Segments

Our business is organized into two operating segments: Wealth Management and Strategic Alternatives. Described below are the segments and the revenue generated by each, which broadly fall into three categories: recurring management, advisory, or administration fees; performance or incentive fees; and transaction fees.

Wealth Management

Within our Wealth Management segment, services provided principally consist of investment management and advisory services, trusts and administrative services, and family office services. The wealth management client base includes high net worth individuals, families, single family offices, foundations, and endowments globally. Investment management or advisory fees are the primary source of revenue in our Wealth Management segment. These fees are generally calculated based on a percentage of the value of each client’s billable AUM or AUA (as applicable). As of March 31, 2024 and December 31, 2023, this segment had $53.5 billion and $51.0 billion, respectively, in AUM/AUA.

Investment Management and Advisory Services

In our investment management and advisory services teams, we diversify our clients’ portfolios across risk factors, geographies, traditional asset classes such as money markets, equities and fixed income, and alternative

16

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

asset classes including private equity, private debt, hedge funds, real estate, and other assets through highly experienced third-party managers.

Trusts and Administration Services

The trust and administration services that we provide include entity formation and management, creating or modifying trust instruments and/or administrative practices to meet beneficiary needs, full corporate, trustee-executor, and fiduciary services. We also offer provision of directors and company secretarial services, administering entity ownership of intellectual property rights, advice and administration services in connection with investments in marine and aviation assets, and administering entity ownership of fine art and collectibles.

FOS

Family office services are tailored outsourced family office solutions and administrative services which we provide primarily to our larger clients. These services include bookkeeping and back-office services, private foundation management and grantmaking, oversight of trust administration, financial tracking and reporting, cash flow management and bill pay, and other financial services.

Strategic Alternatives

Strategic alternatives services include the alternatives platform and public and private real estate (including co-investment) businesses.

Alternatives Platform

The alternatives platform embodies our legacy TIG business, which is an alternative asset manager and includes our TIG Arbitrage strategy and funds managed by our External Strategic Managers, predominantly for institutional investors. The TIG Arbitrage strategy is an event-driven strategy fund that earns management fees and incentive fees based on the performance of its underlying funds and accounts. The investment strategies of the External Strategic Managers include Real Estate Bridge Lending, European Equities and Asian Credit and Special Situations. Distributions are received from the External Strategic Managers through profit or revenue sharing arrangements that are generated through management and incentive fees based on the performance of the underlying investments. As of March 31, 2024 and December 31, 2023, this platform had $7.5 billion and $7.6 billion, respectively, in AUM/AUA.

Co-Investment

Real estate co-investment oversees deal origination, documentation, and structuring from inception to exit for a variety of strategies, including development, income, value-add, and planning. Investors are typically HNWIs, single family offices, and institutional investors. Fees earned include private market, incentive fees, management and advisory fees, and placement and brokerage fees. As of March 31, 2024 and December 31, 2023, our real estate co-investment platform had deployed more than $7.7 billion and $7.8 billion, respectively, of capital (inclusive of capital raised for our private real estate funds), of which approximately 14

Real Estate - Public and Private

The real estate business includes fund management services as well as co-investment solutions. As of March 31, 2024 and December 31, 2023, this business had approximately $10.0 billion and $12.7 billion, respectively, of AUM/AUA.

Fund Management

Our real estate fund management business manages two funds based in the United Kingdom, LXi, a publicly traded real estate investment trust, and HLIF, a private fund, however, we are in the process of exiting this

17

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

business. Fees from our real estate fund management business are earned from management and advisory services. On January 9, 2024, AlTi RE Public Markets Limited entered into heads of terms to sell 100 % of the equity of LXi REIT Advisors Limited (“LRA”), the advisor to the publicly-traded fund LXi REIT plc (“LXi”), to LondonMetric Property Plc (“LondonMetric”) for fixed consideration of approximately $33.1 million and up to an estimated $5.1 million of contingent consideration based on the exchange rate as of the balance sheet date, as applicable. The contingent consideration meets the definition of a derivative and is recorded as Contingent consideration receivable on the Condensed Consolidated Statement of Financial Position as of March 31, 2024. This contingent consideration will be remeasured at fair value at each reporting date in accordance with ASC 820, Fair Value Measurement, with changes in fair value recognized in the Condensed Consolidated Statement of Operations in the period of change.

This disposal was completed on March 6, 2024. As a result, the Company recognized an intangible asset impairment charge of $23.5 million, which is recorded in Impairment loss on goodwill and intangible assets in the Consolidated Statement of Operations during the year ended December 31, 2023. In addition, as of December 31, 2023, the major classes of assets and liabilities of LRA were presented as held for sale in the Consolidated Statement of Financial Position. As of the three months ended March 31, 2024, a gain on disposal of $0.2 million was recognized in Gain (loss) on investments in the Condensed Consolidated Statement of Operations. See Note 3 (Business Combinations and Divestitures) for further information.

On February 26, 2024, AFM UK and SHIA served notice to terminate their contracts with HLIF. We are in discussions with a third-party manager to take over the management of HLIF and termination of these contracts will become effective once the transition process has completed.

Alvarium Home REIT Advisors Limited

Prior to the Business Combination, ARE, an indirect wholly owned subsidiary of Alvarium, entered into an agreement to sell 100 % of the equity of AHRA, the investment advisor to the publicly-traded fund Home REIT, to a newly formed entity (“NewCo”) owned by the management of AHRA, for aggregate consideration approximately equal to $29 million. Consequently, AHRA has never been part of AlTi. The consideration comprised a promissory note maturing December 31, 2023, subject to extension if mutually agreed upon by the parties thereto. Additionally, ARE was granted a call option pursuant to which ARE had the right to repurchase AHRA prior to the repayment of the note for a purchase price equal to the note balance then outstanding thereunder.

Subsidiaries are companies over which a company has the power indirectly and/or directly to control the financial and operating policies so as to obtain benefits. In assessing control for accounting purposes, potential voting rights that are presently exercisable or convertible (including rights which may arise on the exercise of an option) are taken into account. With respect to the AHRA, the above arrangements resulted in AHRA continuing to be consolidated by AlTi after its legal disposal to NewCo. Due to this consolidation, after the Business Combination, an intangible asset was recognized related to the investment advisory agreement between AHRA and Home REIT.

AlTi was formed on January 3, 2023, through a business combination transaction that included certain legacy Alvarium companies. While the sale of AHRA occurred prior to the Business Combination, under GAAP, its results were required to be consolidated in our financial statements until June 30, 2023, when it was deconsolidated. On June 30, 2023, the Company entered into a series of agreements that resulted in the deconsolidation of AHRA from the Strategic Alternatives segment with immediate effect. The agreements removed ARE’s potential controlling voting rights in AHRA (previously ascertainable on the exercise of the option) and terminated other residual contractual relationships between AHRA and ARE. As a result, these agreements removed AlTi’s control of AHRA from an accounting perspective. AHRA’s results are included in the Company’s Condensed Consolidated Statement of Operations for the period from January 1, 2023 to June 30, 2023, and it was removed from the Consolidated Statement of Financial Position as of June 30, 2023. The deconsolidation resulted in an intangible asset impairment charge of $29.4 million, which was recorded in Impairment loss on goodwill and intangible assets in the Condensed Consolidated Statement of Operations

18

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

during the year ended December 31, 2023. Assets managed by AHRA, however, have been excluded from the Company’s AUM/AUA metrics since January 1, 2023.

(2)Summary of Significant Accounting Policies

(a)Basis of Presentation

The accompanying unaudited condensed consolidated financial statements comprise the financial statements of the Company and its subsidiaries. These condensed consolidated financial statements have been prepared under the accrual basis of accounting in accordance with U.S. GAAP and conform to prevailing practices within the financial services industry, as applicable to the Company, and should be read in conjunction with the annual financial statements included in the Annual Report.on Form 10-K filed by the Company on March 22, 2024 (as amended by the Company on Form 10-K/A filed with the SEC on April 5, 2024, the “Annual Report”). The notes are an integral part of the Company’s condensed consolidated financial statements. In the opinion of management, all adjustments necessary for a fair presentation of the Company’s condensed consolidated financial statements have been included and are of a normal and recurring nature.

(b)Prior Period Immaterial Corrections

Following an analysis of quantitative and qualitative factors in accordance with SEC Staff Accounting Bulletin 99, Materiality, the Company concluded that the errors below were immaterial to the previously issued consolidated financial statements, and thus, no restatement of any of the Company’s previously issued financial statements is necessary. The Company revised the reported balances to correct for the immaterial errors accordingly.

During the second quarter reporting period in 2023, the Company identified and corrected an immaterial error concerning the classification of cash outflows associated with distributions due to former TIG members in the Condensed Consolidated Statement of Cash Flows. In the Company’s previously filed Quarterly Report on Form 10-Q for the period ended March 31, 2023, these cash outflows of $7.1 million were categorized under operating activities. In accordance with ASC 230-10, the Company determined that all cash flows related to distributions due to former TIG members should be classified under financing activities in the Condensed Consolidated Statement of Cash Flows. This item had no impact on the reported net change in cash for the three months ended March 31, 2023. The Company has revised its consolidated statements of cash flows for the period ended March 31, 2023 to present the distributions as noted above.

Additionally, during the current reporting period, the Company identified and corrected immaterial errors impacting the December 31, 2023 balances previously reported related to Accrued compensation and profit sharing, Goodwill, Accounts payable and accrued expenses and certain other balances reported within Other liabilities. These revisions resulted in an adjustment to the opening retained earnings balance for the current reporting period of $(3.0 ) million, a $4.2 million increase in Accrued compensation and profit sharing, a $0.3 million decrease in Goodwill, a $0.6 million increase in Other liabilities, and a $0.3 million increase in Accounts payable and accrued expenses. In conjunction with the prior period immaterial error correction, certain reclassifications have been made to prior period amounts between our Non-controlling interest in subsidiaries and Additional paid-in capital which relate to the TRA exchange of our Class B Units for shares of Class A Common Stock. These reclassifications resulted in an adjustment of $13.3 million and are reflected in our Condensed Consolidated Statement of Changes in

19

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

Mezzanine Equity and Shareholders’ Equity. These prior period reclassifications have no impact on the Company’s cash flows, net income, or total shareholders’ equity.

(c)Reclassifications

(d)Use of Estimates

The preparation of financial statements in conformity with US GAAP requires management to make assumptions and estimates that affect the amounts reported in the condensed consolidated financial statements of the Company. The most critical of these estimates are related to (i) the fair value of the investments included in the Billable Assets within AUM/AUA, as this impacts the amount of revenues the Company recognizes each period; (ii) the fair values of the Company’s investments and liabilities with respect to the TRA, and Earn-out Securities, as changes in these fair values have a direct impact on the Company’s consolidated net income (loss); (iii) the estimate of future taxable income, which impacts the realizability and carrying amount of the Company’s deferred income tax assets; (iv) the qualitative and quantitative assessments of whether impairments of equity method investments, carried interest vehicles, acquired intangible assets, and goodwill exist; and (v) the determination of whether to consolidate a variable interest entity (“VIE”); and (vi) fair value of assets acquired and liabilities assumed in business combinations, including assumptions with respect to future cash inflows and outflows, discount rates, assets’ useful lives, market multiples, the allocation of purchase price consideration in the business combination valuation of acquired assets and liabilities, the estimated useful lives of intangible assets, goodwill impairment testing, assumptions used to calculate equity-based compensation, and the realization of deferred tax assets. Inherent in such estimates are judgements relating to future cash flows, which include the Company’s interpretation of current economic indicators and market valuations, and assumptions about the Company’s strategic plans with regard to its operations. While management believes that the estimates utilized in preparing the condensed consolidated financial statements are reasonable and prudent, actual results could differ materially from those estimates.

(e)Consolidation

The Company consolidates those entities in which it has a direct or indirect controlling financial interest based on either a variable interest model or voting interest model. The Company determines whether an entity should be consolidated by first evaluating whether it holds a variable interest in the entity. Entities that are not VIEs are further evaluated for consolidation under the voting interest model (“VOE” model).

An entity is considered to be a VIE if any of the following conditions exist: (a) the total equity investment at risk is not sufficient to permit the entity to finance its activities without additional subordinated financial support, (b) the holders of equity investment at risk, as a group, lack either the direct or indirect ability through voting rights or similar rights to make decisions that have a significant effect on the success of the entity or the obligation to absorb the expected losses or right to receive the expected residual returns, or (c) the voting rights of some equity investors are disproportionate to their obligation to absorb losses of the entity, their rights to receive returns from an entity, or both and substantially all of the entity’s activities either involve or are conducted on behalf of an investor with disproportionately few voting rights.

Fees that are customary and commensurate with the level of services provided by the Company, and where the Company does not hold other economic interests in the entity that would absorb more than an

20

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

insignificant amount of the expected losses or returns of the entity, are not considered a variable interest. The Company factors in all economic interests, including proportionate interests through related parties, to determine if fees are considered a variable interest. Where the Company’s interests in funds are primarily management fees and insignificant direct or indirect equity interests through related parties, the Company is not considered to have a variable interest in such entities.

The Company consolidates all VIEs for which it is the primary beneficiary. An entity is determined to be the primary beneficiary if it holds a controlling financial interest, which is defined as having (a) the power to direct the activities of the VIE that most significantly impact the entity’s economic performance and (b) the obligation to absorb losses of the entity or the right to receive benefits from the entity that could potentially be significant to the VIE. The Company does not consolidate any of the products it manages as it does not hold any direct or indirect interests in such entities that could expose the Company to an obligation to absorb losses of an entity or the right to receive benefits from an entity that could potentially be significant to such entities.

The Company determines whether it is the primary beneficiary of a VIE at the time it becomes involved with a VIE and continuously reconsiders that conclusion. In evaluating whether the Company is the primary beneficiary, the Company evaluates its direct and indirect economic interests in the entity. The consolidation analysis is generally performed qualitatively, however, if the primary beneficiary is not readily determinable, a quantitative analysis may also be performed. This analysis requires judgment, including: (1) determining whether the equity investment at risk is sufficient to permit the entity to finance its activities without additional subordinated financial support, (2) evaluating whether the equity holders, as a group, can make decisions that have a significant effect on the success of the entity, (3) determining whether two or more parties’ equity interests should be aggregated, (4) determining whether the equity investors have proportionate voting rights to their obligations to absorb losses or rights to receive returns from an entity and (5) evaluating the nature of relationships and activities of the parties involved in determining which party within a related-party group is most closely associated with a VIE and therefore would be deemed the primary beneficiary.

Under the voting interest model, the Company consolidates those entities it controls through a majority voting interest. The Company will generally not consolidate those voting interest entities where a single investor or simple majority of third-party investors with equity have the ability to exercise substantive kick-out or participation rights.

(f)Revenue Recognition

Revenue is recognized when the Company transfers promised goods or services to customers in an amount that reflects the consideration to which the Company expects to be entitled in exchange for those goods or services. A five-step framework is utilized that requires an entity to: (i) identify the contract(s) with a customer, which includes assessing the collectability of the consideration to which it will be entitled in exchange for the goods or services transferred to the customer, (ii) identify the performance obligation in the contract, (iii) determine the transaction price, (iv) allocate the transaction price to the performance obligation in the contract, and (v) recognize revenue when the entity satisfies a performance obligation.

Management/Advisory Fees

Revenues from contracts with customers consist of investment management, trustee, and custody fees. The Company recognizes revenue at the time of transfer of promised goods or services to customers in an amount that reflects the consideration to which the Company expects to be entitled in exchange for those goods or services. Revenue recognized is calculated based on contractual terms, including the transaction price, whether a distinct performance obligation has been satisfied

21

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

and control is transferred to the customer, and when collection of the revenue is assessed as probable.

Investment management, trustee and custody fees are recognized over the period in which the investment management services are performed, using a time-based output method to measure progress. The amount of revenue varies from one reporting period to another as levels of AUA change (from inflows, outflows, and market movements) and the number of days in the reporting period change.

For services provided to each client account, the Company charges an investment management fee, inclusive of custody and/or trustee fees, based on the fair value of the AUA of such account representing a single performance obligation. For assets for which valuations are not available on a daily basis, the most recent valuation provided to the Company is used as the fair value for the purpose of calculating the quarterly fee. In certain circumstances, fixed fees are charged to customers on a monthly basis. The nature of the Company’s performance obligation is to provide a series of distinct services in which the customer receives the benefits of the services over time. The Company’s performance obligation is satisfied at the end of each month or quarter, as applicable to the contract with the customer.

Fees are charged on a mixture of methodologies that include quarterly in arrears based upon the market value at the end of the quarter, quarterly based on the average daily balance, or monthly. Receivable balances from contracts with customers are included in the fees receivable line in the Condensed Consolidated Statement of Financial Position.

Our FOS business is also included in the Management/advisory fees line item. FOS fees are generally structured to reflect an annual agreed upon fee or they can be structured on a project/time-based fee. FOS fees are typically billed quarterly in arrears. We also generate FOS project/time-based fees arising from accounting, administration fees, set up, the Foreign Account Tax Compliance Act (“FATCA”), and other non-investment advisory services.

Incentive Fees

The Company is entitled to incentive fees if targeted returns have been achieved in accordance with customer contracts. Incentive fees are calculated using a percentage of net profit from the amount the customers earn. Incentive fees are variable consideration that is generally calculated as applicable to the contract with the customer. We recognize our incentive fees when it is no longer probable that a significant reversal of revenue will occur. Our incentive fees are not subject to clawback provisions.

Other Fees/Income

The Company generates arrangement fees in its co-investment division by arranging private debt or equity financing, generally in connection with an acquisition or an investment. Arrangement fees are typically 50 to 100 basis points of equity value contributed into a transaction, and are payable upon closing of the transaction. Acquisition fees are typically payable where there are no agency fees or where there is an off-market transaction sourced by the team. Such acquisition fees are usually in the range of 50 to 100 basis points of the purchase price of the relevant acquisition. The equity structures are long-term ( to ten years ) closed-ended structures with fees normally ranging between 50 and 175 basis points of the equity value committed or drawn. The debt structure terms are generally between 12 and 36 months. The investment adviser, general partner or

22

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

other entity entitled to fees in respect of each of our co-investments receives such fees either monthly, quarterly or annually.

(g)Distributions from Investments

The Company has equity interests in three entities pursuant to which it is entitled to distributions based on the terms of the respective arrangements. Distributions from each investment will be recorded upon receipt of the distribution. These distributions are recurring under investment agreements and are structured as either a profit or revenue share of the investment’s management and incentive fees.

(h)Cash and Cash Equivalents

Cash and cash equivalents primarily consist of cash and money market funds. Cash balances maintained by consolidated VIEs are not considered legally restricted and are included in cash and cash equivalents on the Condensed Consolidated Statement of Financial Position.

(i)Restricted Cash and Cash Equivalents

Restricted cash and cash equivalents consist of balances that are restricted as to withdrawal or usage.

As of March 31, 2024 and December 31, 2023, restricted cash and cash equivalents amounted to $4.2 million and $5.4 million, and are included in the line item Cash and cash equivalents on the Condensed Consolidated Statement of Financial Position and Consolidated Statement of Financial Position, respectively. These amounts represent the level of liquidity to be maintained by Company’s certain subsidiaries to meet regulatory requirements. Failing to meet the requirement could lead to censure, fines and ultimately a loss of license.

(j)Compensation and Employee Benefits

Cash-Based Compensation

Compensation and benefits consist of salaries, bonuses, commissions, benefits and payroll taxes. Compensation is accrued over the related service period.

Equity-Based Compensation

Equity-based compensation awards are reviewed to determine whether such awards are equity-classified or liability-classified. Compensation expense related to equity-classified awards is equal to their grant-date fair value and generally recognized on a straight-line basis over the awards’ requisite service period. When certain settlement features require an award to be liability-classified, compensation expense is recognized over the service period, and such amount is adjusted at each statement of financial position date through the settlement date to the then current fair value of such award.

The Company recognizes equity-based award forfeitures in the period they occur as a reversal of previously recognized compensation expense. The reduction in compensation expense is determined based on the specific awards forfeited during that period. Furthermore, the Company recognizes all excess tax benefits and deficiencies as income tax benefit or expense in the Condensed Consolidated Statement of Operations.

23

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(k)Foreign Currency and Transactions

The Company has multiple functional currencies across various consolidated entities. All functional currencies that are not the U.S. dollar are converted upon consolidation at the reporting date. Monetary assets and liabilities denominated in foreign currency are remeasured into U.S. dollars at the closing rates of exchange on the date of the Condensed Consolidated Statement of Financial Position. Non-monetary assets and liabilities denominated in foreign currencies are remeasured into U.S. dollars using the historical exchange rate. The profit or loss arising from foreign currency transactions is remeasured using the rate in effect on the date of the relevant transaction. Gains and losses on transactions denominated in foreign currencies due to changes in exchange rates are recorded within Foreign currency translation adjustments. Gains and losses on certain financing transactions which the Company intends to repay in the foreseeable future are recorded in net income.

(l)Income Taxes

The Company accounts for income taxes under the asset and liability method in accordance with ASC 740. Under this method, deferred tax assets and liabilities are determined based on differences between the condensed consolidated financial statement carrying amounts and tax bases of assets and liabilities and operating loss and tax credit carryforwards and are measured using the enacted tax rates that are expected to be in effect when the differences reverse. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in the Condensed Consolidated Statement of Operations in the period that includes the enactment date. Valuation allowances are established when necessary to reduce deferred tax assets to an amount that, in the opinion of management, is more likely than not to be realized, meaning the likelihood of realization is greater than 50%.

The Company accounts for uncertain tax positions by reporting a liability for unrecognizable tax benefits resulting from uncertain tax positions taken or expected to be taken in a tax return. The Company recognizes interest and penalties, if any, related to unrecognized tax benefits in income tax expense.

(m)Other Assets, Net and Other Liabilities, Net

Other assets, net include prepaid expenses, miscellaneous receivables, current income taxes receivable, fixed assets, and software licenses. The Company amortizes assets over their respective useful lives, as applicable.

Other liabilities, net include the AlTi Wealth Management (Switzerland) SA, formerly known as Alvarium Investment Managers (Suisse) SA, (“AWMS”) deferred cash consideration (see Note 3 (Business Combinations and Divestitures)), accrued payroll and payroll related taxes, accrued legal fees, and corporate taxes payable, among other miscellaneous payables.

(n)Investments

Investments in Debt Securities. The Company classifies debt investments as held-to-maturity or trading based on the Company’s intent and ability to hold the debt security to maturity or its intent to sell the security. The Company does not have any held-to-maturity debt investments.

Trading securities are those investments that are purchased principally for the purpose of selling them in the near term. Trading securities are carried at fair value on the Condensed Consolidated Statement of Financial Position with changes in fair value recorded in Loss on investments on the Condensed Consolidated Statement of Operations.

Investments in Equity Securities. Equity securities are generally carried at fair value on the Condensed Consolidated Statement of Financial Position in accordance with ASC 321, Investments – Equity

24

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

Securities. Changes in fair value are recorded in Loss on investments on the Condensed Consolidated Statement of Operations.

Equity Method. The Company applies the equity method of accounting for equity investments where the Company does not consolidate the investee but can exert significant influence over the financial and operating policies of the investee. The evaluation of whether the Company exerts control or significant influence over the financial and operational policies of its investees is based on the facts and circumstances surrounding each individual investment. The Company’s share of the investee’s underlying net income or loss is recorded as Loss on investments within current period earnings. The Company’s share of net income of the investee is recorded based upon the most current information available at the time, which may precede the date of the Condensed Consolidated Statement of Financial Position. Due to the nature and size of its investees, the Company has adopted a lag in reporting for certain equity method investees for which the Company cannot reliably obtain financial information on a regular basis. Distributions received reduce the Company’s carrying value of the investee and the cost basis if deemed to be a return of capital. For certain investments, the Company may apply the alternative fair value option to the investment at initial measurement. The fair value measurement of investments in which the fair value option is elected will be measured in accordance with ASC 825.

For equity method investments and nonmarketable investments, impairment evaluation considers qualitative factors, including the financial conditions and specific events related to an investee, which may indicate the fair value of the investment is less than the carrying value. For held-to-maturity investments, impairment is evaluated using market values, when available, or the expected cash flows of the investment. These losses in value may be considered other than temporary impairment losses.

(o)Leases

The Company determines if an arrangement is a lease at inception of the arrangement and primarily enters into operating leases, as the lessee, for office space. The Company accounts for its leases in accordance with ASC 842, Leases, and recognizes a lease liability and right-of-use asset in the Condensed Consolidated Statement of Financial Position for contracts that it determines are leases or contain a lease. The Company evaluates leases at their inception to determine if they are to be accounted for as an operating lease or a finance lease. A lease is accounted for as a finance lease if it meets one of the following five criteria: (i) the lease has a purchase option that is reasonably certain of being exercised, (ii) the present value of the future cash flows is substantially all of the fair market value of the underlying asset, (iii) the lease term is for a significant portion of the remaining economic life of the underlying asset, (iv) the title to the underlying asset transfers at the end of the lease term, or (v) if the underlying asset is of such a specialized nature that it is expected to have no alternative uses to the lessor at the end of the term. Leases that do not meet the finance lease criteria are accounted for as an operating lease. At the inception of a finance lease, an asset and finance lease obligation are recorded at an amount equal to the lesser of the present value of the minimum lease payments and the property’s fair market value. Finance lease obligations are classified as either current or long-term based on the due dates of future lease payments, net of interest. The Company’s lease portfolio primarily consists of operating leases for office space in various countries around the world. The Company also has operating leases for office equipment and vehicles, which are not significant. The Company does not separate non-lease components from lease components for its office space and equipment operating leases and instead accounts for each separate lease component and its associated non-lease component as a single lease component. Right-of-use assets represent the Company’s right to use an underlying asset for the lease term and lease liabilities represent the Company’s obligation to make lease payments arising from the leases. The Company’s right-of-use assets and lease liabilities are recognized at lease commencement based on the present value of lease payments over the lease term. Lease right-of-use assets include initial direct costs incurred by the Company and are presented net of deferred rent and lease incentives. Absent an implicit interest rate in the lease, the Company uses its incremental borrowing rate, adjusted for the effects of collateralization, based on the information available at commencement in determining the present value of lease payments.

25

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

The Company’s lease terms may include options to extend or terminate the lease when it is reasonably certain that the Company will exercise those options. Lease expense for lease payments is recognized on a straight-line basis over the lease term. Lease right-of-use assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of the asset may not be recoverable.

The Company does not recognize a lease liability or right-of-use asset on the balance for short-term leases. Instead, the Company recognizes short-term lease payments as an expense on a straight-line basis over the lease term. A short-term lease is defined as a lease that, at the commencement date, has a lease term of 12 months or less and does not include an option to purchase the underlying asset that the lessee is reasonably certain to exercise. When determining whether a lease qualifies as a short-term lease, the Company evaluates the lease term and the purchase option in the same manner as all other leases.

(p)Intangible Assets Other Than Goodwill, Net

The Company recognized certain finite-lived intangible assets as a result of the Business Combination. The Company’s finite-lived intangible assets consist of Trade Names, Customer Relationships, Investment Management Agreements, and Backlog. Finite-lived intangible assets are amortized on a straight-line basis over their estimated useful lives.

The Company tests finite-lived intangible assets for impairment if certain events occur or circumstances change indicating that the carrying amount of the intangible asset may not be recoverable. The Company evaluates impairment by comparing the estimated fair value attributable to the intangible asset with its carrying amount. If an impairment exists, the Company adjusts the carrying value to equal the fair value by taking a charge through earnings.

There were no indicators of impairment, and no impairment charges were recognized for the three months ended March 31, 2024. As of December 31, 2023, the Company recognized intangible asset impairment charges of $52.9 million. See Note 10 (Intangible assets, net) for further detail.

(q)Goodwill

Goodwill represents the excess of the purchase price in a business combination over the fair value of the tangible and intangible assets acquired and the liabilities assumed. Under ASC 350, Intangibles—Goodwill and Other, goodwill is not amortized, but rather is subject to an annual impairment test. Goodwill represents the excess of consideration over identifiable net assets of an acquired business. Goodwill is allocated at a reporting unit level. The Company has two reporting units, Strategic

26

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

Alternatives and Wealth Management, and tests goodwill annually for impairment at each reporting unit. If, after assessing qualitative factors, the Company believes that it is more-likely-than-not that the fair value of the reporting unit inclusive of goodwill is less than its carrying amount, the Company will perform a quantitative assessment to determine whether an impairment exists. If an impairment exists, the Company adjusts the carrying value of goodwill so that the carrying value of the reporting unit is equal to its fair value by taking a charge through earnings. The Company also tests goodwill for impairment in other periods if an event occurs or circumstances change such that it is more-likely-than-not to reduce the fair value of the reporting unit below its carrying amount. The Company concluded that the estimated fair value of the Strategic Alternatives and Wealth Management reporting units were greater than their carrying values, and as such, no impairment charges were required for the three months ended March 31, 2024. As of December 31, 2023, the Company recognized goodwill impairment charges of $(153.9 ) million for the Strategic Alternatives segment and no goodwill impairment charges for the Wealth Management segment. See Note 13 (Goodwill, net).

(r)Fixed Assets, Net

Fixed assets are recorded at cost, less accumulated depreciation and amortization, and are included in the “Other assets” line item in the Company’s Condensed Consolidated Statement of Financial Position. Fixed assets are depreciated or amortized on a straight-line basis, with the corresponding depreciation and amortization expense included within general, administrative and other expenses in the Company’s Condensed Consolidated Statement of Operations. The estimated useful life for leasehold improvements is the lesser of the remaining lease term and the life of the asset, while other fixed assets are generally depreciated over a period of to seven years . Fixed assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable.

(s)Debt Obligations, Net

(t)Tax Receivable Agreement