UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended June 30, 2023

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from _________ to _________

Commission file number 001-40103

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||

(Address of Principal Executive Offices) | (Zip Code) | ||||

(Registrant's telephone number, including area code)

Not Applicable

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☐ | Accelerated filer | ☐ | ||||||||

| ☒ | Smaller reporting company | ||||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The registrant had outstanding 62,957,660 shares of Class A Common Stock (as defined herein) and 55,032,961 shares of Class B Common Stock (as defined herein) as of August 11, 2023.

Table of Contents

| 77 | |||||

2

Defined Terms

Capitalized terms used herein but not otherwise defined herein shall have the respective meanings ascribed to them in the Amended and Restated Business Combination Agreement, a copy of which is attached to our Annual Report on Form 10-K filed April 17, 2023 (the “Annual Report”).

•“Alvarium” means AlTi Asset Management Holdings 2 Limited, formerly known as Alvarium Investments Limited, an English private limited company.

•“Alvarium Contribution” means the contribution by Cartesian of all the issued and outstanding shares of AlTi Global Topco that it holds to Umbrella.

•“Alvarium Contribution Agreement” means the Contribution Agreement, dated as of January 3, 2023, by and among Cartesian and Umbrella.

•“Alvarium Exchange” means the exchange by each shareholder of AlTi Global Topco of his, her or its (a) ordinary shares of AlTi Global Topco and (b) class A shares of AlTi Global Topco for Class A Common Stock.

•“AlTi” means AlTi Global, Inc., together with its consolidated subsidiaries.

•“Alvarium Reorganization” means a reorganization such that Alvarium is the wholly owned indirect subsidiary of AlTi Global Topco, and AlTi Global Topco is owned solely by the shareholders of Alvarium.

•“Alvarium Shareholders” means the shareholders of Alvarium.

•“Alvarium Tiedemann” means the Company, prior to being renamed “AlTi Global, Inc.”

•“AlTi Global Topco” means AlTi Global Topco Limited, formerly known as Alvarium Topco, an Isle of Man entity which was established by Alvarium and owned by the Alvarium Shareholders.

•“Asset Management” means the Segment that includes the Company's alternatives platform, public and private real estate, co-investment, and strategic advisory (formerly known as merchant banking) businesses.

•“AUA” means assets under advisement.

•“AUM” means assets under management.

•“Board” means the board of directors of the Company.

•“Business Combination” means the transactions contemplated by the Business Combination Agreement.

•“Business Combination Agreement” means the Amended and Restated Business Combination Agreement, dated as of October 25, 2022, by and among Cartesian, Umbrella Merger Sub, TWMH, TIG GP, TIG MGMT, Alvarium and Umbrella.

•“Cartesian” means Cartesian Growth Corporation, a Cayman Islands exempted company, prior to the Business Combination.

•“Cayman Islands Companies Act” means the Cayman Islands Companies Act (as revised) of the Cayman Islands, as the same may be amended from time to time.

•“Charter” means the certificate of incorporation of the Company.

3

•“Class A Common Stock” means the Class A Common Stock, par value $0.0001 per share, of the Company, including any shares of such Class A Common Stock issuable upon the exercise of any warrant or other right to acquire shares of such Class A Common Stock.

•“Class B Common Stock” means the Class B Common Stock, par value $0.0001 per share, of the Company, including any shares of such Class B Common Stock issuable upon the exercise of any warrant or other right to acquire shares of such Class B Common Stock.

•“Class B Units” means the limited liability company interests in Umbrella designated as Class B Common Units in the Umbrella LLC Agreement.

•“Closing” means the closing of the Business Combination.

•“Closing Date” means January 3, 2023, the date on which the Closing occurred.

•“Code” means the Internal Revenue Code of 1986, as amended.

•“Common Stock” refers to shares of the Class A Common Stock and the Class B Common Stock, collectively.

•“Company,” “our,” “we” or “us” means, prior to the Business Combination, Cartesian, as the context suggests, and, following the Business Combination, AlTi.

•“Condensed Consolidated Statement of Financial Position” refers to the consolidated balance sheet of AlTi Global, Inc.

•“Condensed Consolidated Statement of Operations” refers to the consolidated income statement of AlTi Global, Inc.

•“DGCL” refers to the Delaware General Corporation Law, as amended.

•“DLLCA” means the Delaware Limited Liability Company Act, as amended.

•“dollars” or “$” refers to U.S. dollars.

•“Domestication” means the continuation of Cartesian by way of domestication into a Delaware corporation, with the ordinary shares of Cartesian becoming shares of common stock of the Delaware corporation under the applicable provisions of the Cayman Islands Companies Act and the DGCL; the term includes all matters and necessary or ancillary changes in order to effect such Domestication, including the adoption of the Charter consistent with the DGCL and changing the name and registered office of Cartesian.

•"Earn-out” means the contingent additional equity consideration issued by the Company to the Sponsor and the Target Companies’ legacy equityholders.

•“Earn-out Period” means the five years immediately after the Closing Date.

•“Earn-out Securities” means the earn-out shares of Class A Common Stock in the Company and Class B Common Units that may be issued or become tradeable upon the achievement of certain stock price-based vesting conditions in accordance with the terms of the Business Combination Agreement.

•“Employee Stock Purchase Plan” means the AlTi Global, Inc. 2023 Employee Stock Purchase Plan.

•“Equity Incentive Plan” means the AlTi Global, Inc. 2023 Stock Incentive Plan.

•“ESG” means environmental, social and governance.

•“ETFs” means Exchange Traded Funds.

4

•“EU” means European Union.

•“Exchange Act” means the U.S. Securities Exchange Act of 1934, as amended.

•“External Strategic Managers” means global alternative asset managers with whom we partner by making strategic investments in which we actively participate in seeking to leverage the collective resources and synergies of the businesses to facilitate their growth.

•“FINRA” means the Financial Industry Regulatory Authority, Inc.

•“FOS” means Family Office Service.

•“HNWI” means high net worth individual, being an individual having investable assets of $1 million or more, excluding primary residence, collectibles, consumables, and consumer durables.

•“Impact Investing” means investment practices seeking to generate various levels of financial performance together with the generation of positive measurable environmental and social impacts.

•“Investment Company Act” means the Investment Company Act of 1940, as amended, and the rules and regulations promulgated thereunder.

•“Managed Funds” means mutual funds, ETFs, hedge funds, private equity, real estate or other funds.

•“Nasdaq” means The Nasdaq Capital Market.

•“NAV” means net asset value.

•“PIPE Investors” means the subscribers that agreed to purchase shares of Class A Common Stock at the Closing pursuant to the private placements, including without limitation, as reflected in the subscription agreements between Cartesian and each of the PIPE Investors.

•“SEC” means the United States Securities and Exchange Commission.

•“Segment” means collectively, or individually, how the Company manages its business including products and services.

•“Successor” means AlTi.

•“Sponsor” means CGC Sponsor LLC, a Cayman Islands limited liability company.

•“Target Companies” means, collectively, TWMH, TIG GP, TIG MGMT, and Alvarium.

•“Tax Receivable Agreement” means that certain Tax Receivable Agreement, dated as of January 3, 2023, between the Company and the TWMH Members, the TIG GP Members, and the TIG MGMT Members.

•“TIG” means, collectively, the TIG Entities and their subsidiaries and their predecessor entities where applicable.

•“TIG Entities” means, collectively, TIG GP and TIG MGMT and their predecessor entities where applicable.

•“TIG GP” means TIG Trinity GP, LLC, a Delaware limited liability company.

•“TIG GP Members” means the former members of TIG GP.

•“TIG MGMT” means TIG Trinity Management, LLC, a Delaware limited liability company.

5

•“TIG MGMT Members” means the former members of TIG MGMT.

•“TIH” means Tiedemann International Holdings, AG.

•“Transfer Agent” means Continental Stock Transfer & Trust Company.

•“TRA Recipients” means the TWMH Members, the TIG GP Members and the TIG MGMT Members (including certain of our directors and officers) party to the Tax Receivable Agreement.

•“TWMH” means, collectively, Tiedemann Wealth Management Holdings, LLC, a Delaware limited liability company, and its subsidiaries, and their predecessor entities where applicable.

•“TWMH Members” means the former members of TWMH.

•“Warrant Agreement” means the Amended and Restated Warrant Agreement, dated January 3, 2023, by and between the Company and Continental Stock Transfer & Trust Company.

•“Warrants” means the warrants, which were initially issued in the Initial Public Offering, entitling the holder thereof to purchase one of Cartesian’s Class A ordinary shares at an exercise price of $11.50, subject to adjustment.

•“Wealth Management” means the Segment that consists of the Company’s investment management and advisory services, trusts and administrative services, and family office services.

•“Umbrella” means AlTi Global Capital, LLC (formerly known as Alvarium Tiedemann Capital, LLC), a Delaware limited liability company.

•“Umbrella LLC Agreement” means the Third Amended and Restated Limited Liability Company Agreement of AlTi Global Capital, LLC, effective as of July 31, 2023.

•“US GAAP” means United States generally accepted accounting principles, consistently applied.

6

Available Information

We file annual, quarterly and current reports, proxy statements and other information required by the Exchange Act with the SEC. We make available free of charge on our website (www.alti-global.com) our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and other filing as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. We also use our website to distribute company information, including assets under management and performance information, and such information as may be deemed material. Accordingly, investors should monitor our website, in addition to our press releases, SEC filings and public conference calls and webcasts.

Also posted on our website in the “Investor Relations” section are the charters for our Audit, Finance and Risk Committee, Environmental, Social, Governance and Nominating Committee, and Human Capital and Compensation Committee, as well as our Corporate Governance Guidelines and Code of Business Conduct governing our directors, officers, and employees. Information on or accessible through our website is not a part of or incorporated into this Quarterly Report on Form 10-Q for the period ended June 30, 2023 (the “Quarterly Report”) or any other SEC filing. Copies of our SEC filings or corporate governance materials are available without charge upon written request to the Company at its principal place of business. Any materials we file with the SEC are also publicly available through the SEC’s website (www.sec.gov).

No statements herein, available on our website, or in any of the materials we file with the SEC constitute or should be viewed as constituting an offer to sell, or a solicitation of an offer to buy, securities in any jurisdiction.

Cautionary Note Regarding Forward-Looking Statements

This Quarterly Report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Exchange Act, which reflect our current views with respect to, among other things, future events, operations and financial performance. You can identify these forward-looking statements by the use of forward-looking words such as “outlook,” “believes,” “expects,” “potential,” “continues,” “may,” “will,” “should,” “seeks,” “approximately,” “predicts,” “projects,” “intends,” “plans,” “estimates,” “anticipates,” “target” or the negative version of those words, other comparable words or other statements that do not relate to historical or factual matters. The forward-looking statements are based on our beliefs, assumptions and expectations of our future performance, taking into account all information currently available to us. Such forward-looking statements are subject to various risks, uncertainties (some of which are beyond our control) or other assumptions relating to our operations, financial results, financial condition, business prospects, growth strategy and liquidity that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. Some of these factors are described under the headings “Part II. Item 1A. Risk Factors” and “Part 1. Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.” These factors should not be construed as exhaustive and should be read in conjunction with the risk factors and other cautionary statements that are included in this Quarterly Report and in our other periodic filings. If one or more of these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, our actual results may vary materially from those indicated in these forward-looking statements. New risks and uncertainties arise over time, and it is not possible for us to predict those events or how they may affect us. Therefore, you should not place undue reliance on these forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made. We do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law.

7

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements (Unaudited)

8

AlTi Global, Inc.

Condensed Consolidated Statement of Financial Position (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

| (Dollars in Thousands, except share data) | As of June 30, 2023 (Successor) | As of December 31, 2022 (Predecessor) | ||||||||||||

| Assets | ||||||||||||||

| Cash and cash equivalents | $ | $ | ||||||||||||

| Fees receivable, net | ||||||||||||||

| Other receivable, net | ||||||||||||||

| Investments at fair value | ||||||||||||||

| Equity method investments | ||||||||||||||

| Intangible assets, net of accumulated amortization | ||||||||||||||

| Goodwill | ||||||||||||||

| Operating lease right-of-use assets | ||||||||||||||

| Other assets | ||||||||||||||

| Assets held for sale | ||||||||||||||

| Total assets | $ | $ | ||||||||||||

| Liabilities | ||||||||||||||

| Accounts payable and accrued expenses | $ | $ | ||||||||||||

| Accrued compensation and profit sharing | ||||||||||||||

| Accrued member distributions payable | ||||||||||||||

| Earn-out liability, at fair value | ||||||||||||||

| TRA liability | ||||||||||||||

| Delayed share purchase agreement | ||||||||||||||

| Earn-in consideration payable | ||||||||||||||

| Operating lease liabilities | ||||||||||||||

| Debt, net of unamortized deferred financing cost | ||||||||||||||

| Deferred tax liability, net | ||||||||||||||

| Deferred income | ||||||||||||||

| Other liabilities | ||||||||||||||

| Liabilities held for sale | ||||||||||||||

| Total liabilities | $ | $ | ||||||||||||

| Commitments and contingencies (Note 19) | ||||||||||||||

| Shareholders' Equity | ||||||||||||||

Common stock, Class A, $ | ||||||||||||||

Common Stock, Class B, $ | ||||||||||||||

| Additional paid-in capital | ||||||||||||||

| Retained earnings (accumulated deficit) | ( | |||||||||||||

| Accumulated other comprehensive income (loss) | ( | |||||||||||||

| Total AlTi Global, Inc. shareholders' equity | ||||||||||||||

| Non-controlling interest in subsidiaries | ||||||||||||||

| Total shareholders' equity | ||||||||||||||

| Total liabilities and shareholders' equity | $ | $ | ||||||||||||

The accompanying notes are an integral part of these condensed unaudited financial statements.

9

AlTi Global, Inc.

Condensed Consolidated Statement of Operations (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

| For the Period | For the Period | ||||||||||||||||||||||||||||

| (Dollars in Thousands) | April 1, 2023 – June 30, 2023 (Successor) | April 1, 2022 – June 30, 2022 (Predecessor) | January 3, 2023 – June 30, 2023 (Successor) | January 1, 2022 – June 30, 2022 (Predecessor) | |||||||||||||||||||||||||

| Revenue | |||||||||||||||||||||||||||||

| Management/advisory fees | $ | $ | $ | $ | |||||||||||||||||||||||||

| Incentive fees | |||||||||||||||||||||||||||||

| Distributions from investments | |||||||||||||||||||||||||||||

| Other income/fees | |||||||||||||||||||||||||||||

| Total income | |||||||||||||||||||||||||||||

| Operating Expenses | |||||||||||||||||||||||||||||

| Compensation and employee benefits | |||||||||||||||||||||||||||||

| Systems, technology and telephone | |||||||||||||||||||||||||||||

| Sales, distribution and marketing | |||||||||||||||||||||||||||||

| Occupancy costs | |||||||||||||||||||||||||||||

| Professional fees | |||||||||||||||||||||||||||||

| Travel and entertainment | |||||||||||||||||||||||||||||

| Depreciation and amortization | |||||||||||||||||||||||||||||

| Impairment loss on intangible assets | |||||||||||||||||||||||||||||

| General, administrative and other | |||||||||||||||||||||||||||||

| Total operating expenses | |||||||||||||||||||||||||||||

| Total operating income (loss) | ( | ( | |||||||||||||||||||||||||||

| Other Income (Expenses) | |||||||||||||||||||||||||||||

| Gain (loss) on investments | ( | ( | |||||||||||||||||||||||||||

| Gain (loss) on TRA | ( | ( | |||||||||||||||||||||||||||

| Gain (loss) on warrant liability | ( | ||||||||||||||||||||||||||||

| Gain (loss) on earn-out liability | |||||||||||||||||||||||||||||

| Interest and dividend income (expense) | ( | ( | ( | ( | |||||||||||||||||||||||||

| Other income (expense) | ( | ( | |||||||||||||||||||||||||||

| Income (loss) before taxes | ( | ||||||||||||||||||||||||||||

| Income tax (expense) benefit | ( | ( | |||||||||||||||||||||||||||

| Net income (loss) | ( | ||||||||||||||||||||||||||||

| Net income (loss) attributed to non-controlling interests in subsidiaries | ( | ( | ( | ( | |||||||||||||||||||||||||

| Net income (loss) attributable to AlTi Global, Inc. | $ | $ | $ | ( | $ | ||||||||||||||||||||||||

| Other Comprehensive (Loss) Income | |||||||||||||||||||||||||||||

| Foreign currency translation adjustments | ( | ( | |||||||||||||||||||||||||||

| Other comprehensive income | ( | ( | |||||||||||||||||||||||||||

| Total comprehensive income (loss) | ( | ||||||||||||||||||||||||||||

| Other income (loss) attributed to non-controlling interests in subsidiaries | ( | ( | ( | ( | |||||||||||||||||||||||||

| Comprehensive income (loss) attributable to AlTi Global, Inc. | ( | ||||||||||||||||||||||||||||

| Net Income (Loss) Per Share | |||||||||||||||||||||||||||||

| Basic | $ | $ | $ | ( | $ | ||||||||||||||||||||||||

| Diluted | $ | $ | $ | ( | $ | ||||||||||||||||||||||||

| Weighted Average Shares of Class A Common Stock Outstanding | |||||||||||||||||||||||||||||

| Basic | |||||||||||||||||||||||||||||

| Diluted | |||||||||||||||||||||||||||||

The accompanying notes are an integral part of these condensed unaudited financial statements.

10

AlTi Global, Inc.

Condensed Consolidated Statement of Changes in Shareholders’ Equity (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

| (Dollars in Thousands, except share data) | Class A Common Stock | Class B Common Stock | Additional paid-in-capital | Retained earnings (accumulated deficit) | Accumulated other comprehensive income | Non-controlling interest in subsidiaries | Total Shareholders' Equity | |||||||||||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at March 31, 2023 (Successor) | $ | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||

| Net income (loss) | — | — | — | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||

| Currency translation adjustment | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Cancellation of AHRA call option | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income | — | — | — | — | — | — | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||

| Payment for partner’s tax | — | — | — | — | ( | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||

| Share based compensation | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||

| AHRA deconsolidation | — | — | — | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of shares - exercise of warrants | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at June 30, 2023 (Successor) | $ | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||

| (Dollars in Thousands, except share data) | Class A Common Stock | Class B Common Stock | Additional paid-in-capital | Retained earnings (accumulated deficit) | Accumulated other comprehensive income | Non-controlling interest in subsidiaries | Total Shareholders' Equity | |||||||||||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | |||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at January 3, 2023 (Successor) | $ | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of shares to Alvarium Employee Benefit Trust | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income (loss) | — | — | — | — | — | ( | — | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||

| Currency translation adjustment | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Cancellation of AHRA call option | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income | — | — | — | — | — | — | ( | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||

| Payment for partner’s tax | — | — | — | — | ( | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||

| AHRA deconsolidation | — | — | — | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||

| Share based compensation | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of shares - exercise of warrants | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Balance at June 30, 2023 (Successor) | $ | $ | $ | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||

11

AlTi Global, Inc.

Condensed Consolidated Statement of Changes in Shareholders’ Equity (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

The accompanying notes are an integral part of these condensed unaudited financial statements.

| (Dollars in Thousands, except share data) | Class A | Class B | Total Members' Capital | Accumulated other comprehensive income (loss) | Non-controlling interest | Total Equity | ||||||||||||||||||||||||||||||||

| Balance at March 31, 2022 (Predecessor) | $ | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||||||

| Member capital distributions | ( | ( | ( | — | — | ( | ||||||||||||||||||||||||||||||||

| Member tax distributions | — | ( | ( | — | — | ( | ||||||||||||||||||||||||||||||||

| Restricted unit compensation | — | — | — | |||||||||||||||||||||||||||||||||||

| Net income (loss) for the period | — | — | ( | |||||||||||||||||||||||||||||||||||

| Other comprehensive income (loss) for the period | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||

| Balance at June 30, 2022 (Predecessor) | $ | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||||||

| (Dollars in Thousands, except share data) | Class A | Class B | Total Members' Capital | Accumulated other comprehensive income (loss) | Non-controlling interest | Total Equity | ||||||||||||||||||||||||||||||||

| Balance at January 1, 2022 | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Member capital distributions | ( | ( | ( | — | — | ( | ||||||||||||||||||||||||||||||||

| Member tax distributions | ( | ( | ( | — | — | ( | ||||||||||||||||||||||||||||||||

| Restricted unit compensation | — | — | — | |||||||||||||||||||||||||||||||||||

| Net income (loss) for the period | — | — | ( | |||||||||||||||||||||||||||||||||||

| Other comprehensive income (loss) for the period | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||

| Balance at June 30, 2022 (Predecessor) | $ | $ | $ | $ | ( | $ | $ | |||||||||||||||||||||||||||||||

The accompanying notes are an integral part of these condensed unaudited financial statements.

12

AlTi Global, Inc.

Condensed Consolidated Statement of Cash Flows (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

| For the Period | ||||||||||||||

| (Dollars in Thousands) | January 3, 2023 – June 30, 2023 (Successor) | January 1, 2022 – June 30, 2022 (Predecessor) | ||||||||||||

| Cash Flows from Operating Activities | ||||||||||||||

| Net income (loss) | $ | ( | $ | |||||||||||

| Adjustments to reconcile net income (loss) to net cash provided by (used in) operating activities: | ||||||||||||||

| Depreciation and amortization | ||||||||||||||

| Amortization of debt discounts and deferred financing costs | ( | |||||||||||||

| Unrealized (gain) loss on investments | ||||||||||||||

| Impairment loss on intangible assets | ||||||||||||||

| Gain (loss) on TRA | ||||||||||||||

| (Income) loss on equity method investments | ( | |||||||||||||

| Restricted unit compensation | ||||||||||||||

| Fair value of warrant liability | ||||||||||||||

| Fair value of earn-out liability | ( | |||||||||||||

| Deferred income tax (benefit) expense | ( | ( | ||||||||||||

| Equity-settled share-based payments | ||||||||||||||

| Unrealized foreign currency (gains)/losses | ||||||||||||||

| (Gain) loss from retirement of debt | ( | |||||||||||||

| Forgiveness of debt shareholder loan | ||||||||||||||

| Forgiveness of debt of notes receivable from members | ||||||||||||||

| Fair value of interest rate swap | ( | |||||||||||||

| Cash flows due to changes in operating assets and liabilities | ||||||||||||||

| Fees receivable | ||||||||||||||

| Other assets | ( | ( | ||||||||||||

| Operating cash flow from operating leases | ||||||||||||||

| Accounts payable and accrued expenses | ( | ( | ||||||||||||

| Accrued compensation and profit sharing | ( | ( | ||||||||||||

| Distributions due to former TIG members | ||||||||||||||

| Other liabilities | ( | |||||||||||||

| Other operating activities | ( | |||||||||||||

| Net cash provided by (used in) operating activities | ( | |||||||||||||

| (Continued on the following page) | ||||||||||||||

13

AlTi Global, Inc.

Condensed Consolidated Statement of Cash Flows (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

| (Continued from the previous page) | For the Period | |||||||||||||

| (Dollars in Thousands) | January 3, 2023 – June 30, 2023 (Successor) | January 1, 2022 – June 30, 2022 (Predecessor) | ||||||||||||

| Cash Flows from Investing Activities | ||||||||||||||

| Cash acquired from consolidation of variable interest entity | ||||||||||||||

| Cash payment for acquisition of TWMH and TIG historical equity | ( | |||||||||||||

| Receipt of payments of notes receivable from members | ||||||||||||||

| Loans to members | ( | |||||||||||||

| Cash receipts from the repayment of advances and loans | ||||||||||||||

| Purchases of investments | ( | ( | ||||||||||||

| Distributions from investments | ||||||||||||||

| Purchase of TIH shares | ( | |||||||||||||

| Purchase of Holbein | ( | |||||||||||||

| Payment of Payout Right | ( | |||||||||||||

| Acquisition of AL Wealth Partners, net of cash acquired | ( | |||||||||||||

| Sales of investments | ||||||||||||||

| Purchases of fixed assets | ( | ( | ||||||||||||

| Net cash provided by (used in) investing activities | ( | ( | ||||||||||||

| Cash Flows from Financing Activities | ||||||||||||||

| Member contribution (distribution) | ( | ( | ||||||||||||

| Payments on term notes and lines of credit | ( | ( | ||||||||||||

| Borrowings on term notes and lines of credit | ||||||||||||||

| Increase (decrease) in distributions due to former TIG members | ( | |||||||||||||

| Cash payment for purchase of shares to be transferred as part of Alvarium share compensation | ( | |||||||||||||

| Cash receipts from exercise of Warrants | ||||||||||||||

| Other financing activities | ||||||||||||||

| Net cash provided by (used in) financing activities | ||||||||||||||

| Effect of exchange rate changes on cash | ( | ( | ||||||||||||

| Net increase (decrease) in cash | ( | ( | ||||||||||||

| Cash and cash equivalents at beginning of the period | ||||||||||||||

| Cash and cash equivalents at end of the period | $ | $ | ||||||||||||

| Reconciliation of balance sheet cash and cash equivalents to cash flows: | ||||||||||||||

| Cash and cash equivalents on balance sheet | $ | $ | ||||||||||||

| Cash and cash equivalents included in Assets held for sale (Note 3) | $ | |||||||||||||

| Cash and cash equivalents, including cash in Assets held for sale | $ | $ | ||||||||||||

| Supplemental Disclosure of Cash Flow Information | ||||||||||||||

| Cash Paid During the Period for: | ||||||||||||||

| Income taxes | $ | |||||||||||||

| Interest payments on term notes and lines of credit | ||||||||||||||

The accompanying notes are an integral part of these condensed unaudited financial statements.

14

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

(1)Description of the Business

AlTi Global, Inc. (the “Registrant”), a Delaware corporation, together with its consolidated subsidiaries (collectively, the “Company”, “AlTi” or “Successor”) is a multi-disciplinary financial services business, with a diverse array of investment, advisory, and administrative capabilities. The Company is a global organization that manages or advises approximately $68.9 billion in combined assets as of June 30, 2023 (Successor). The Company provides holistic solutions for Wealth Management clients through a full spectrum of Wealth Management services, including discretionary investment management services, non-discretionary investment advisory services, trust services, administration services, and family office services. It also structures, arranges, and provides a network of investors with co-investment opportunities in a variety of alternative assets which are either managed intra-group or by carefully selected managers in the relevant asset class. The Company manages and advises both public and private investment funds and also provides strategic advisory, corporate advisory, brokerage and placement agency services to entrepreneurs, “late stage” companies (particularly in the media, technology and innovation sectors), asset managers, private equity sponsors, and investment funds.

Business Combination

The Registrant was initially incorporated in the Cayman Islands as Cartesian Growth Capital, a special purpose acquisition company (“Cartesian SPAC”). In anticipation of the business combination:

•The holders of the equity of Tiedemann Wealth Management Holdings, LLC, a Delaware limited liability company (“TWMH” or “Predecessor”), TIG Trinity GP, LLC, a Delaware limited liability company (“TIG GP”), TIG Trinity Management, LLC, a Delaware limited liability company (“TIG MGMT” and, together with TIG GP, the “TIG Entities”) contributed their TWMH and TIG equity to AlTi Global Capital, LLC, formerly known as Alvarium Tiedemann Capital, LLC, (“Umbrella”) making TWMH and the TIG wholly owned subsidiaries of Umbrella.

•AlTi Asset Management Holdings 2 Limited, formerly known as Alvarium Investments Limited, an English private limited company (“Alvarium”) reorganized such that it became the wholly owned indirect subsidiary of AlTi Global Topco Limited (“AlTi Global Topco”).

•Cartesian SPAC formed Rook MS, LLC, a Delaware limited liability company (“Umbrella Merger Sub”)

Pursuant to the Business Combination on January 3, 2023 (“Business Combination Date”):

•The Registrant was redomiciled as a Delaware corporation and changed its name to Alvarium Tiedemann Holdings, Inc. Effective April 19, 2023, Alvarium Tiedemann Holding, Inc. changed its name to AlTi Global, Inc.

•The Registrant acquired all the outstanding share capital of AlTi Global Topco.

•Umbrella Merger Sub, LLC merged into Umbrella with AlTi Global Capital, LLC, formerly known as Alvarium Tiedemann Capital, LLC as the surviving entity.

•The Company acquired 51 % of the equity interests of Umbrella, while the existing TWMH and TIG rollover shareholders hold a 49 % economic interest in Umbrella. Umbrella holds 100 % of the equity interests of TWMH, TIG, and Alvarium.

15

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

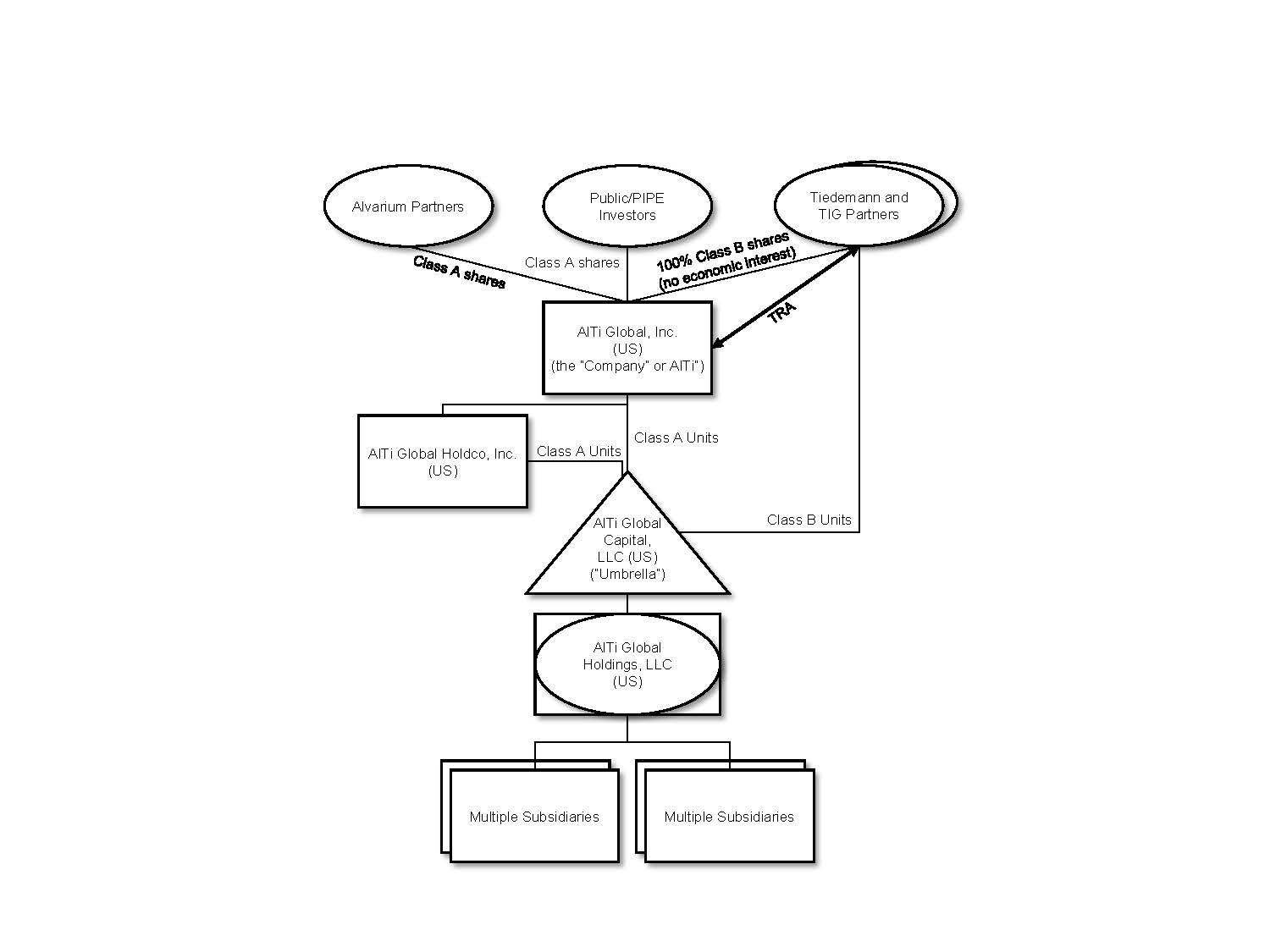

•Through a series of intercompany transactions, AlTi was restructured to reflect the final structure depicted below:

Capital Structure

The Registrant has the following classes of shares and other instruments outstanding:

•Class A Shares – Shares of Class A common stock that are publicly traded. Class A Shareholders are entitled to declared dividends from Class A shares. As of June 30, 2023 (Successor), the Class A Shares represent 53 % of the total voting power of all shares.

•Class B Shares – Shares of Class B common stock that are not publicly traded. Class B shareholders are entitled to distributions declared by the Board. As of June 30, 2023 (Successor), the Class B Shares represent 47 % of the total voting power of all shares.

•Warrants – Prior to the Business Combination, the Company issued warrants to purchase Class A Shares at a price of $11.50 per share. Throughout the period from January 3, 2023 to March 31, 2023 (Successor), 428,626 warrants were exercised. On April 3, 2023, 78,864 warrants were exercised. On June 7, 2023, the Company closed an offer and consent solicitation and entered into a warrant amendment, pursuant to which the remaining 19,892,387 warrants were exchanged for Class A Shares. The exercises and exchanges throughout the period from January 3, 2023 to June 30, 2023 (Successor)

16

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

resulted in an increase in Additional Paid-in-Capital amount of $29.5 million. Following the exchanges, none of the warrants were outstanding as of June 30, 2023 (Successor).

The following table presents the number of shares of the Registrant that were outstanding as of June 30, 2023 (Successor):

| As of June 30, 2023 (Successor) | |||||

| Class A shares | |||||

| Class B shares | |||||

Segments

Our business is organized into two operating segments: Wealth Management and Asset Management. Described below are the segments and the revenue generated by each, which broadly fall into three categories: recurring management, advisory, or administration fees; performance or incentive fees; and transaction fees.

Wealth Management

Our Wealth Management services principally consist of investment management and advisory services, trusts and administrative services, and family office services. Our Wealth Management client base includes high net worth individuals, families, single family offices, foundations, and endowments globally. Investment management or advisory fees are the primary source of revenue in our Wealth Management segment. These fees are generally calculated based on a percentage of the value of each client’s billable assets under management (“AUM”) or assets under advisement (“AUA”) (as applicable). As of June 30, 2023 (Successor), this segment had $48.6 billion in AUM/AUA.

Investment Management and Advisory Services

In our investment management and advisory services teams, we diversify our clients’ portfolios across risk factors, geographies, traditional asset classes such as money markets, equities and fixed income, and alternative asset classes including private equity, private debt, hedge funds, real estate, and other assets through highly experienced, and hard to access, third-party managers.

Trusts and Administration Services

The trusts and administration services that we provide include entity formation and management, creating or modifying trust instruments and/or administrative practices to meet beneficiary needs, full corporate, trustee-executor, and fiduciary services. We also offer provision of directors and company secretarial services, administering entity ownership of intellectual property (“IP”) rights, advice and administration services in connection with investments in marine and aviation assets, and administering entity ownership of fine art and collectibles.

Family Office Services (FOS)

Our family office services are tailored outsourced family office solutions and administrative services which we provide primarily to our larger clients. These services include bookkeeping and back-office services, private foundation management and grantmaking, oversight of trust administration, financial tracking and reporting, cash flow management and bill pay, and other financial services.

17

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

Asset Management

Our Asset Management services include alternatives platform, public and private real estate (including co-investment), and strategic advisory businesses.

Alternatives Platform

Our alternatives platform represents our legacy TIG business which is an alternative asset manager. This platform includes our TIG Arbitrage strategy and funds managed by our External Strategic Managers. Our alternatives platform client base is predominantly comprised of institutional investors. The TIG Arbitrage strategy is our event-driven strategy based in New York through which management fees and incentive fees based on performance are received from the underlying funds and accounts. The strategies of our External Strategic Managers include Real Estate Bridge Lending, European Equities and Asian Credit and Special Situations. We receive distributions from our External Strategic Managers through our profit or revenue sharing arrangements that are generated through their management and incentive fees based on performance of the underlying investments. As of June 30, 2023 (Successor), this platform had $7.9 billion in AUM/AUA.

Real Estate - Public and Private

Our real estate business includes fund management services as well as co-investment solutions. As of June 30, 2023 (Successor), this business had approximately $12.4 billion of AUM/AUA.

Fund Management

Our real estate fund management business manages two funds based in the United Kingdom, LXi REIT plc, a publicly traded real estate investment trust, and Home Long Income Fund, a private fund. Fees from our real estate fund management business are earned from management and advisory services.

Prior to the Business Combination, AlTi RE Limited, formerly known as Alvarium RE Limited (“ARE”), an indirect wholly owned subsidiary of Alvarium, entered into an agreement to sell 100 % of the equity of Alvarium Home REIT Advisors Ltd. (“AHRA”), the advisor to the publicly-traded fund Home REIT Plc (“Home REIT”), to a newly formed entity (“NewCo”) owned by the management of AHRA, for aggregate consideration approximately equal to $29 million. The consideration comprised a promissory note maturing December 31, 2023, subject to extension if mutually agreed upon by the parties thereto. Additionally, ARE was granted a call option pursuant to which ARE had the right to repurchase AHRA prior to the repayment of the note for a purchase price equal to the note balance then outstanding thereunder.

Subsidiaries are companies over which a company has the power indirectly and/or directly to control the financial and operating policies so as to obtain benefits. In assessing control for accounting purposes, potential voting rights that are presently exercisable or convertible (including rights which may arise on the exercise of an option) are taken into account. With respect to the AHRA, the above arrangements resulted in AHRA continuing to be consolidated by AlTi after its legal disposal to NewCo. Due to this consolidation, after the Business Combination, an intangible asset was recognized related to the investment advisory agreement between AHRA and Home REIT.

On June 30, 2023, the Company entered into a series of agreements that resulted in the deconsolidation of AHRA from the Asset Management segment with immediate effect. The agreements removed ARE’s potential controlling voting rights in AHRA (previously ascertainable on the exercise of the option), and terminated other residual contractual relationships between AHRA and ARE. As a result, these agreements removed AlTi’s control of AHRA from an accounting perspective. AHRA’s results were included in the Company’s Condensed Consolidated Statement of Operations for the period from January 3, 2023 to June 30, 2023 (Successor), but its accounts were removed from the Consolidated Statement of Financial Position as of June 30, 2023 (Successor). The deconsolidation resulted in an intangible asset impairment charge of $29.4 million, which is recorded as an

18

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

Impairment loss on intangible assets in the Condensed Consolidated Statement of Operations. Assets managed by AHRA, however, have been excluded from the Company’s AUM/AUA metrics since January 3, 2023.

Co-Investment

Our real estate co-investment business, which was part of the legacy Alvarium business, oversees deal origination, due diligence, documentation, and structuring from inception to exit for a variety of strategies, including forward funding, development, income, value-add and planning. Investors are typically HNWIs, single family offices, and institutional investors. Fees earned related to our real estate co-investment business include private market, incentive fees, management and advisory fees, and placement and brokerage fees. As of June 30, 2023 (Successor), our real estate co-investment platform had deployed more than $7.8 billion of capital (inclusive of capital raised for our public and private real estate funds), of which approximately 14 % has been invested by legacy Alvarium shareholders and senior employees.

Strategic Advisory

(2)Summary of Significant Accounting Policies

(a)Basis of Presentation

(b)Use of Estimates

19

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

(c)Consolidation

The Company consolidates those entities in which it has a direct or indirect controlling financial interest based on either a variable interest model or voting interest model. The Company determines whether an entity should be consolidated by first evaluating whether it holds a variable interest in the entity. Entities that are not VIEs are further evaluated for consolidation under the voting interest model (“VOE” model).

An entity is considered to be a VIE if any of the following conditions exist: (a) the total equity investment at risk is not sufficient to permit the entity to finance its activities without additional subordinated financial support, (b) the holders of equity investment at risk, as a group, lack either the direct or indirect ability through voting rights or similar rights to make decisions that have a significant effect on the success of the entity or the obligation to absorb the expected losses or right to receive the expected residual returns, or (c) the voting rights of some equity investors are disproportionate to their obligation to absorb losses of the entity, their rights to receive returns from an entity, or both and substantially all of the entity’s activities either involve or are conducted on behalf of an investor with disproportionately few voting rights.

Fees that are customary and commensurate with the level of services provided by the Company, and where the Company does not hold other economic interests in the entity that would absorb more than an insignificant amount of the expected losses or returns of the entity, are not considered a variable interest. The Company factors in all economic interests, including proportionate interests through related parties, to determine if fees are considered a variable interest. Where the Company’s interests in funds are primarily management fees and insignificant direct or indirect equity interests through related parties, the Company is not considered to have a variable interest in such entities.

The Company consolidates all VIEs for which it is the primary beneficiary. An entity is determined to be the primary beneficiary if it holds a controlling financial interest, which is defined as having (a) the power to direct the activities of the VIE that most significantly impact the entity’s economic performance and (b) the obligation to absorb losses of the entity or the right to receive benefits from the entity that could potentially be significant to the VIE. The Company does not consolidate any of the products it manages as it does not hold any direct or indirect interests in such entities that could expose the Company to an obligation to absorb losses of an entity or the right to receive benefits from an entity that could potentially be significant to such entities.

The Company determines whether it is the primary beneficiary of a VIE at the time it becomes involved with a VIE and continuously reconsiders that conclusion. In evaluating whether the Company is the primary beneficiary, the Company evaluates its direct and indirect economic interests in the entity. The consolidation analysis is generally performed qualitatively, however, if the primary beneficiary is not readily determinable, a quantitative analysis may also be performed. This analysis requires judgment, including: (1) determining whether the equity investment at risk is sufficient to permit the entity to finance its activities without additional subordinated financial support, (2) evaluating whether the equity

20

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

holders, as a group, can make decisions that have a significant effect on the success of the entity, (3) determining whether two or more parties’ equity interests should be aggregated, (4) determining whether the equity investors have proportionate voting rights to their obligations to absorb losses or rights to receive returns from an entity and (5) evaluating the nature of relationships and activities of the parties involved in determining which party within a related-party group is most closely associated with a VIE and therefore would be deemed the primary beneficiary.

Under the voting interest model, the Company consolidates those entities it controls through a majority voting interest. The Company will generally not consolidate those voting interest entities where a single investor or simple majority of third-party investors with equity have the ability to exercise substantive kick-out or participation rights.

(d)Revenue Recognition

The Company recognizes revenue in accordance with ASC 606, Revenue from Contracts with Customers. Revenue is recognized when the Company transfers promised goods or services to customers in an amount that reflects the consideration to which the Company expects to be entitled to in exchange for those goods or services. ASC 606 includes a five-step framework that requires an entity to: (i) identify the contract(s) with a customer, which includes assessing the collectability of the consideration to which it will be entitled in exchange for the goods or services transferred to the customer, (ii) identify the performance obligation in the contract, (iii) determine the transaction price, (iv) allocate the transaction price to the performance obligation in the contract, and (v) recognize revenue when the entity satisfies a performance obligation.

Management/Advisory Fees

Revenues from contracts with customers consist of investment management, trustee, and custody fees. Pursuant to ASC 606, the Company recognizes revenue at the time of transfer of promised goods or services to customers in an amount that reflects the consideration to which the Company expects to be entitled in exchange for those goods or services. Under this standard, revenue is based on a contract with a determinable transaction price and a distinct performance obligation with probable collectability. Revenues cannot be recognized until the performance obligation is satisfied and control is transferred to the customer.

Investment management, trustee and custody fees are recognized over the period in which the investment management services are performed, using a time-based output method to measure progress. The amount of revenue varies from one reporting period to another as levels of AUA change (from inflows, outflows, and market movements) and the number of days in the reporting period change.

For services provided to each client account, the Company charges an investment management fee, inclusive of custody and/or trustee fees, based on the fair value of the AUA of such account representing a single performance obligation. For assets for which valuations are not available on a daily basis, the most recent valuation provided to the Company is used as the fair value for the purpose of calculating the quarterly fee. In certain circumstances, fixed fees are charged to customers on a monthly basis. The nature of the Company’s performance obligation is to provide a series of distinct services in which the customer receives the benefits of the services over time. The Company’s performance obligation is satisfied at the end of each month or quarter, as applicable to the contract with the customer.

Fees are charged on a mixture of methodologies that include quarterly in arrears based upon the market value at the end of the quarter, quarterly based on the average daily balance, or monthly.

21

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

Receivable balances from contracts with customers are included in the fees receivable line in the Condensed Consolidated Statement of Financial Position. There were no

Our FOS business is also included in this line item. FOS fees are generally structured to reflect an annual agreed upon fee or they can be structured on a project/time-based fee. FOS fees are typically billed quarterly in arrears. We also generate FOS project/time-based fees arising from accounting, administration fees, set up, FATCA, and other non-investment advisory services.

Incentive Fees

The Company is entitled to incentive fees if targeted returns have been achieved in accordance with customer contracts. Incentive fees are calculated using a percentage of net profit from the amount the customers earn. Incentive fees are variable consideration that is generally calculated as applicable to the contract with the customer. We recognize our incentive fees when it is no longer probable that a significant reversal of revenue will occur. Our incentive fees are not subject to clawback provisions.

Distributions from Investments

The Company has equity interests in three entities pursuant to which it is entitled to distributions based on the terms of the respective arrangements. Distributions from each investment will be recorded upon receipt of the distribution. These distributions are recurring under investment agreements and are structured as either a profit or revenue share of the investment’s management and incentive fees.

Other Fees and Income

The Company generates fees for advising on capital market transactions such as mergers and acquisitions and capital raising as part of its strategic advisory division. Strategic advisory fees are primarily success-based fees that are typically a percentage of the financial outcome or target achieved in the merger, acquisition, or capital raising. Revenue is recognized at a point in time upon closing of the transaction or upon the final deliverable. Additionally, the Company may receive upfront non-refundable retainer fees to provide future services to clients, which are recognized over the course of the service period.

The Company generates arrangement fees in its co-investment division by arranging private debt or equity financing, generally in connection with an acquisition or an investment. Arrangement fees are typically 50 to 100 basis points of equity value contributed into a transaction. Acquisition fees are typically payable where there are no agency fees or where there is an off-market transaction sourced by the team. Such acquisition fees are usually in the range of 50 to 100 basis points of the purchase price of the relevant acquisition. The equity structures are long-term ( to ten years ) closed-ended structures with fees normally ranging between 50 and 175 basis points of the equity value committed or drawn. The debt structure terms are generally between 12 and 36 months. The investment adviser, general partner or other entity entitled to fees in respect of each of our co-investments receives such fees either monthly, quarterly or annually.

(e)Cash and Cash Equivalents

22

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

(f)Compensation and Employee Benefits

Cash-Based Compensation

Compensation and benefits consist of salaries, bonuses, commissions, benefits and payroll taxes. Compensation is accrued over the related service period.

Equity-Based Compensation

Equity-based compensation awards are reviewed to determine whether such awards are equity-classified or liability-classified. Compensation expense related to equity-classified awards is equal to their grant-date fair value and generally recognized on a straight-line basis over the awards’ requisite service period. When certain settlement features require an award to be liability-classified, compensation expense is recognized over the service period, and such amount is adjusted at each statement of financial position date through the settlement date to the then current fair value of such award.

The Company recognizes equity-based award forfeitures in the period they occur as a reversal of previously recognized compensation expense. The reduction in compensation expense is determined based on the specific awards forfeited during that period. Furthermore, the Company recognizes all excess tax benefits and deficiencies as income tax benefit or expense in the Condensed Consolidated Statement of Operations.

(g)Foreign Currency and Transactions

(h)Income Taxes

23

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

(i)Other assets

(j)Investments

Investments in Debt Securities. The Company classifies debt investments as held-to-maturity or trading based on the Company’s intent and ability to hold the debt security to maturity or its intent to sell the security. The Company does not have any held-to-maturity debt investments.

Trading securities are those investments that are purchased principally for the purpose of selling them in the near term. Trading securities are carried at fair value on the Condensed Consolidated Statement of Financial Position with changes in fair value recorded in nonoperating income (expense) on the Condensed Consolidated Statement of Operations.

Investments in Equity Securities. Equity securities are generally carried at fair value on the Condensed Consolidated Statement of Financial Position in accordance with ASC 321, “Investments – Equity Securities.” Changes in fair value are recorded in net gains (losses) in the Condensed Consolidated Statement of Operations.

Equity Method. The Company applies the equity method of accounting for equity investments where the Company does not consolidate the investee but can exert significant influence over the financial and operating policies of the investee. The evaluation of whether the Company exerts control or significant influence over the financial and operational policies of its investees is based on the facts and circumstances surrounding each individual investment. The Company’s share of the investee’s underlying net income or loss is recorded as net gain (loss) on investments within current period earnings. The Company’s share of net income of the investee is recorded based upon the most current information available at the time, which may precede the date of the Condensed Consolidated Statement of Financial Position. Due to the nature and size of its investees, the Company has adopted a lag in reporting for certain equity method investees for which the Company cannot reliably obtain financial information on a regular basis. Distributions received reduce the Company’s carrying value of the investee and the cost basis if deemed to be a return of capital. For certain investments, the Company may apply the alternative fair value option to the investment at initial measurement. The fair value measurement of investments in which the option is elected will be measured in accordance with ASC 825.

For equity method investments and nonmarketable investments, impairment evaluation considers qualitative factors, including the financial conditions and specific events related to an investee, which may indicate the fair value of the investment is less than the carrying value. For held-to-maturity investments, impairment is evaluated using market values, when available, or the expected cash flows of the investment.

(k)Leases

24

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

to determine if they are to be accounted for as an operating lease or a finance lease. A lease is accounted for as a finance lease if it meets one of the following five criteria: (i) the lease has a purchase option that is reasonably certain of being exercised, (ii) the present value of the future cash flows is substantially all of the fair market value of the underlying asset, (iii) the lease term is for a significant portion of the remaining economic life of the underlying asset, (iv) the title to the underlying asset transfers at the end of the lease term, or (v) if the underlying asset is of such a specialized nature that it is expected to have no alternative uses to the lessor at the end of the term. Leases that do not meet the finance lease criteria are accounted for as an operating lease. At the inception of a finance lease, an asset and finance lease obligation are recorded at an amount equal to the lesser of the present value of the minimum lease payments and the property’s fair market value. Finance lease obligations are classified as either current or long-term based on the due dates of future lease payments, net of interest. The Company’s lease portfolio primarily consists of operating leases for office space in various countries around the world. The Company also has operating leases for office equipment and vehicles, which are not significant. The Company does not separate non-lease components from lease components for its office space and equipment operating leases and instead accounts for each separate lease component and its associated non-lease component as a single lease component. Right-of-use assets represent the Company’s right to use an underlying asset for the lease term and lease liabilities represent the Company’s obligation to make lease payments arising from the leases. The Company’s right-of-use assets and lease liabilities are recognized at lease commencement based on the present value of lease payments over the lease term. Lease right-of-use assets include initial direct costs incurred by the Company and are presented net of deferred rent and lease incentives. Absent an implicit interest rate in the lease, the Company uses its incremental borrowing rate, adjusted for the effects of collateralization, based on the information available at commencement in determining the present value of lease payments. The Company’s lease terms may include options to extend or terminate the lease when it is reasonably certain that the Company will exercise those options. Lease expense for lease payments is recognized on a straight-line basis over the lease term. Lease right-of-use assets are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount of the asset may not be recoverable.

The Company does not recognize a lease liability or right-of-use asset on the balance for short-term leases. Instead, the Company recognizes short-term lease payments as an expense on a straight-line basis over the lease term. A short-term lease is defined as a lease that, at the commencement date, has a lease term of 12 months or less and does not include an option to purchase the underlying asset that the lessee is reasonably certain to exercise. When determining whether a lease qualifies as a short-term lease, the Company evaluates the lease term and the purchase option in the same manner as all other leases.

(l)Intangible assets other than goodwill, net

The Company recognized certain finite-lived intangible assets as a result of the Business Combination. The Company’s finite-lived intangible assets consist of Trade Names, Customer Relationships, Investment Management Agreements and Backlog. Finite-lived intangible assets are amortized on a straight-line basis over their estimated useful lives.

The Company tests finite-lived intangible assets for impairment if certain events occur or circumstances change indicating that the carrying amount of the intangible asset may not be recoverable. The Company evaluates impairment by comparing the estimated fair value attributable to the intangible asset with its carrying amount. If an impairment exists, the Company adjusts the carrying value to equal the fair value by taking a charge through earnings.

The Company also recognized certain indefinite-lived intangible assets as a result of the Business Combination consisting of certain investment management agreements. These indefinite-lived intangibles are not subject to amortization, but are evaluated for impairment at least annually. In assessing its indefinite-lived intangible assets for impairment, the Company has the option to first perform a qualitative

25

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

(m)Goodwill

(n)Fixed Assets, Net

(o)Debt Obligations, Net

26

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

(p)Tax Receivable Agreement

(q)Warrant Liability

(r)Earn-out Liability

27

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

(s)Delayed share purchase agreement

Prior to the Business Combination, TWMH entered into an agreement to purchase a remaining non-controlling interest in its consolidated subsidiary representing 51.1 % of shares in Tiedemann International Holdings, AG (“TIH”). This arrangement was agreed upon for a fixed consideration of $1,818,440 and is accounted for as a liability until it is settled.

(t)Non-controlling Interests

(u)Derivative Financial Instruments

(v)Segment Reporting

Our business is organized into two operating segments: Wealth Management and Asset Management. Described below are the segments and the revenue generated by each, which broadly fall into three categories: recurring management, advisory, or administration fees; performance or incentive fees; and transaction fees.

Wealth Management

Our Wealth Management services principally consist of investment management and advisory services, trusts and administrative services, and family office services. Our Wealth Management client base includes HNWIs, families, single family offices, foundations, and endowments globally. Investment management or advisory fees are the primary source of revenue in our Wealth Management segment. These fees are generally calculated based on a percentage of the value of each client’s AUM or AUA (as applicable). As of June 30, 2023 (Successor), this segment had $48.6 billion in AUM/AUA.

Investment Management and Advisory Services

In our investment management and advisory services teams, we diversify our clients’ portfolios across risk factors, geographies, and asset classes including private equity, private debt, hedge funds, real estate, and other assets through highly experienced third-party managers, who may be hard to access.

Trusts and Administration Services

The trusts and administration services that we provide include entity formation and management, creating or modifying trust instruments and/or administrative practices to meet beneficiary needs, full corporate, trustee-executor, and fiduciary services. We also offer provision of directors and company secretarial services, administering entity ownership of IP rights, advice and administration services in connection

28

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

with investments in marine and aviation assets, and administering entity ownership of fine art and collectibles.

Family Office Services

Our family office services are tailored outsourced family office solutions and administrative services which we provide primarily to our larger clients. These services include bookkeeping and back-office services, private foundation management and grantmaking, oversight of trust administration, financial tracking and reporting, cash flow management and bill pay, and other financial services.

Asset Management

Our Asset Management services include alternatives platform, public and private real estate, co-investment, and strategic advisory businesses.

Alternatives Platform

Our alternatives platform represents our legacy TIG business which is an alternative asset manager. This platform includes our TIG Arbitrage strategy and funds managed by our External Strategic Managers. Our alternatives platform client base is predominantly comprised of institutional investors. The TIG Arbitrage strategy is our event-driven strategy based in New York through which management fees and incentive fees based on performance are received from the underlying funds and accounts. The strategies of our External Strategic Managers include Real Estate Bridge Lending, European Equities and Asian Credit and Special Situations. We receive distributions from our External Strategic Managers through our profit or revenue sharing arrangements that are generated through their management and incentive fees based on performance of the underlying investments. As of June 30, 2023 (Successor), this platform had $7.9 billion in AUM/AUA.

Real Estate - Public and Private

Our real estate business includes fund management services as well as co-investment solutions. As of June 30, 2023 (Successor), this business had approximately $12.4 billion of AUM/AUA.

Fund Management

Our real estate fund management business manages two funds based in the United Kingdom, LXi REIT, a publicly traded REIT, and Home Long Income Fund, a private fund. Services offered through these funds include investments, financial planning and strategy, sales and marketing, and back and middle office infrastructure/administration. The funds are marketed primarily in the United Kingdom to institutional investors, primarily pension funds, as well as to retail investors. Fees from our real estate fund management business are earned from management and advisory fees.

Co-Investment

Our real estate co-investment business, which was part of the legacy Alvarium business, oversees deal origination, due diligence, documentation, and structuring from inception to exit for a variety of strategies including forward funding, development, income, value-add and planning. Investors are typically HNWIs, single family offices, and institutional investors. Fees earned related to our real estate co-investment business include private market, incentive fees, management and advisory fees, and placement and brokerage fees. As of June 30, 2023 (Successor), our real estate co-investment platform has deployed more than $7.8 billion of capital (inclusive of capital raised for our public and private real estate funds), of which approximately 14 % has been invested by legacy Alvarium shareholders and senior employees.

29

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

(w)Other Income / Expenses

Other income and expenses is comprised of unrealized gains (losses) on investments, interest and dividend income (expense), income from equity method investees, and other items.

The Company holds investments in common stock, mutual funds, exchange-traded funds, and exchange-traded notes, which represent investments in equity and debt securities. The Company earns realized and unrealized gains and losses which depend on investment performance.

Interest income is earned through its investments in exchange-traded notes. These generally include debt securities held on a short- or medium-term basis when the Company has excess cash. The Company recognizes and records interest income using the effective interest method.

Dividend income is earned through investments in common stock, mutual funds, and exchange-traded funds. Dividend income is recorded on the ex-dividend date.

(x)Held for Sale Accounting

(y)Recent Accounting Pronouncements

30

AlTi Global, Inc.

Notes to Condensed Consolidated Financial Statements (Unaudited)

(Prior to January 3, 2023, Tiedemann Wealth Management Holdings)

Company adopted this guidance on January 1, 2022 and applied the guidance prospectively to business combinations that occurred after this date. The adoption of this guidance did not have a material effect on the Company’s condensed consolidated financial statements.

In June 2022, the FASB issued ASU 2022-03, Fair Value Measurement (Topic 820): Fair Value Measurement of Equity Securities Subject to Contractual Sale Restrictions. The amendments in this update clarify the guidance in ASC 820 when measuring the fair value of an equity security subject to contractual sale restrictions and introduce new disclosure requirements related to such equity securities. The amendments are effective for fiscal years beginning after December 15, 2023, with early adoption permitted. The Company does not expect the impact of this guidance to be material to its condensed consolidated financial statements.

The Company has considered all newly issued accounting guidance that is applicable to its operations and the preparation of its unaudited condensed consolidated statements, including those it has not yet adopted. The Company does not believe that any such guidance has or will have a material effect on its financial position or results of operations.

(3)Business Combinations and Divestitures

On January 3, 2023, the Company entered into the Business Combination described in Note 1 (Description of the Business). The primary purpose of the Business Combination was to combine established high-growth companies that can benefit from access to capital and public markets and continue value-creation by management.

The Business Combination is a forward merger and is accounted for using the acquisition method of accounting. The Company is the accounting acquirer and Umbrella, including the Target Companies, is the accounting acquiree. The Company has been determined to be the accounting acquirer because Umbrella meets the definition of a VIE, and the Company is the primary beneficiary of Umbrella. ASC 805 requires the primary beneficiary of a VIE to be identified as the accounting acquirer. The Company is the primary beneficiary because it controls all activities of Umbrella, and the non-managing members of Umbrella do not have substantive kick-out or participating rights.

The Business Combination met the requirements to be considered a business combination under ASC 805. The assets and liabilities acquired from the Target Companies, affected for preliminary adjustments to reflect fair market values assigned to assets purchased and liabilities assumed, and results of operations, are included in the Company’s condensed consolidated financial statements from the date of acquisition. The Company has allocated the purchase price to the tangible and identifiable intangible assets based on their estimated fair market values at the acquisition date as required under ASC 805. The excess of the purchase price over the fair value of the net identifiable tangible and intangible assets was recorded as goodwill and is deductible for tax purposes.

The Business Combination resulted in the Company acquiring 51 % of the equity interests of Umbrella which holds 100 % of the equity interests of Alvarium, TWMH, and TIG. The remainder of Umbrella is held by the historical equity holders of TWMH and TIG through their ownership of Class B Units, which are presented as non-controlling interest on the Company’s Condensed Consolidated Statement of Financial Position.