As confidentially submitted to the Securities and Exchange Commission on August 12, 2022

This draft registration statement has not been publicly filed with the Securities and Exchange Commission

and all information herein remains strictly confidential.

and all information herein remains strictly confidential.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

CONFIDENTIAL DRAFT SUBMISSION NO. 1

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

UNDER

THE SECURITIES ACT OF 1933

BKV CORPORATION

(Exact name of registrant as specified in its charter)

| |

Delaware

(State or other jurisdiction of incorporation or organization) |

| |

1311

(Primary Standard Industrial Classification Code Number) |

| |

85-0886382

(I.R.S. Employer Identification Number) |

|

1200 17th Street, Suite 2100

Denver, Colorado 80202

(720) 375-9680

Denver, Colorado 80202

(720) 375-9680

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Christopher P. Kalnin

Chief Executive Officer

BKV Corporation

1200 17th Street, Suite 2100

Denver, Colorado 80202

(720) 375-9680

Chief Executive Officer

BKV Corporation

1200 17th Street, Suite 2100

Denver, Colorado 80202

(720) 375-9680

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| |

Samantha H. Crispin

M. Preston Bernhisel Adorys Velazquez Baker Botts L.L.P. 2001 Ross Avenue, Suite 900 Dallas, Texas 75201 (214) 953-6500 |

| |

Michael Chambers

Monica E. White Latham & Watkins LLP 811 Main Street, Suite 3700 Houston, Texas 77002 (713) 546-5400 |

|

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this registration statement.

As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| |

Large accelerated filer

☐

|

| |

Accelerated filer

☐

|

|

| |

Non-accelerated filer

☒

|

| |

Smaller reporting company

☐

|

|

| | | | |

Emerging growth company

☒

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☒

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

![[MISSING IMAGE: lg_bkv-4c.jpg]](lg_bkv-4c.jpg)

TABLE OF CONTENTS

| | | |

Page

|

| |||

| | | | | 1 | | | |

| | | | | 25 | | | |

| | | | | 74 | | | |

| | | | | 76 | | | |

| | | | | 77 | | | |

| | | | | 78 | | | |

| | | | | 80 | | | |

| | | | | 81 | | | |

| | | | | 110 | | | |

| | | | | 112 | | | |

| | | | | 152 | | | |

| | | | | 159 | | | |

| | | | | 173 | | | |

| | | | | 175 | | | |

| | | | | 181 | | | |

| | | | | 189 | | | |

| | | | | 192 | | | |

| | | | | 194 | | | |

| | | | | 198 | | | |

| | | | | 205 | | | |

| | | | | 205 | | | |

| | | | | 205 | | | |

| | | | | F-1 | | | |

Dealer Prospectus Delivery Obligation

Through and including , 2022 (the 25th day after the date of this prospectus), all dealers that effect transactions in our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to unsold allotments or subscriptions.

You should rely only on the information contained in this prospectus or in any free writing prospectus that we authorize to be distributed to you. We and the underwriters have not authorized anyone to provide you with any information other than that contained in this prospectus or in any free writing prospectus prepared by or on behalf of us or to which we have referred you, and neither we, nor the underwriters take responsibility for any other information others may give you. We are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where such offers and sales are permitted. The information in this prospectus or any free writing prospectus is accurate only as of its date, regardless of its time of delivery or the time of any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

i

Industry and Market Data

In this prospectus, we present certain market and industry data. This information is based on third-party sources which we believe to be reliable as of their respective dates. Neither we nor the underwriters have independently verified any third-party information. Some data is also based on our good faith estimates. Expectations of our and our industry’s future performance are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Risk Factors.” These and other factors could cause future performance to differ materially from our expectations. See “Cautionary Statement Regarding Forward-Looking Statements.”

Presentation of Financial, Reserve and Operating Data

Unless indicated otherwise, the historical financial information presented in this prospectus is that of BKV Corporation and its consolidated subsidiaries as of December 31, 2021.

The historical natural gas, NGL and oil reserves data presented in this prospectus as of June 30, 2022 and December 31, 2021 and 2020 is based on the reserve reports prepared by Ryder Scott Company, L.P., independent petroleum engineers.

In addition, unless indicated otherwise, the operational data presented in this prospectus is that of BKV Corporation and its consolidated subsidiaries on a consolidated basis as of and for the periods presented.

As a result of our acquisition transactions in recent years, our historical operating, financial and reserve data may not be comparable between periods presented in this prospectus. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Factors that Affect Comparability of Our Results of Operations.”

Trademarks and Trade Names

We own or have rights to various trademarks, service marks and trade names that we use in connection with the operation of our business. This prospectus may also contain trademarks, service marks and trade names of third parties, which are the property of their respective owners. Our use or display of third parties’ trademarks, service marks, trade names or products in this prospectus is not intended to, and does not imply a relationship with, or endorsement or sponsorship by us. Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus may appear without the ®, ™ or SM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensor to these trademarks, service marks and trade names.

Rounding and Percentages

The financial information and certain other information presented in this prospectus have been rounded to the nearest whole number or the nearest decimal. Therefore, the sum of the numbers in a column may not conform exactly to the total figure given for that column in certain tables in this prospectus. In addition, certain percentages presented in this prospectus reflect calculations based upon the underlying information prior to rounding and, accordingly, may not conform exactly to the percentages that would be derived if the relevant calculations were based upon the rounded numbers or may not sum due to rounding.

Other Considerations

This prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. See “Risk Factors” and “Cautionary Statement Regarding Forward-Looking Statements” for additional information regarding these risks.

You should read this prospectus and any written communication prepared by us or on our behalf in connection with this offering, together with the additional information described in the section of this prospectus titled “Where You Can Find More Information.” We have not authorized anyone to provide you with information or to make any representation in connection with this offering other than those contained

ii

herein. If anyone makes any recommendation or gives any information or representation regarding this offering, you should not rely on that recommendation, information or representation as having been authorized by us, the underwriters or any other person on our behalf. The information contained in this prospectus is accurate only as of the date of which it is shown, or if no date is otherwise indicated, the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our shares of common stock. We are offering to sell, and seeking offers to buy, shares of common stock only in jurisdictions where offers and sales are permitted. Our business, financial condition, results of operations and prospects may have changed since that date. Information contained on our website is not part of this prospectus.

No action is being taken in any jurisdiction outside the United States to permit a public offering of shares of common stock or possession or distribution of this prospectus in that jurisdiction. Persons who come into possession of this prospectus in jurisdictions outside the United States are required to inform themselves about and to observe any restrictions as to this offering and the distribution of this prospectus applicable to that jurisdiction.

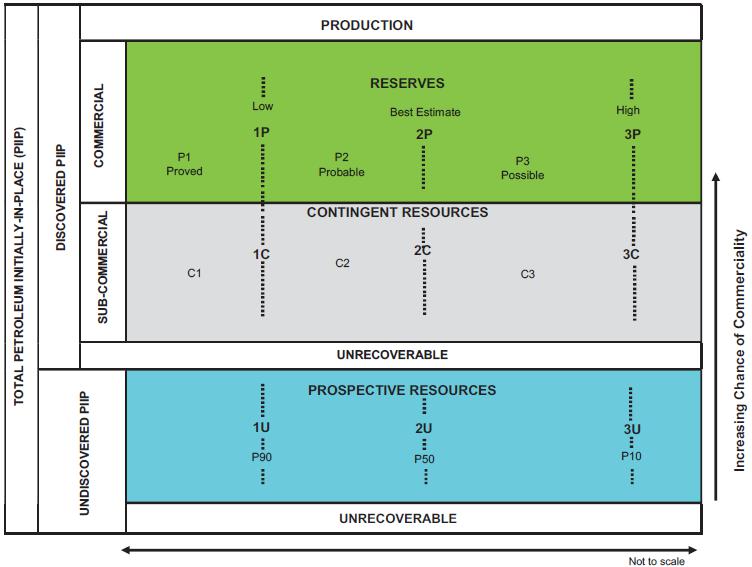

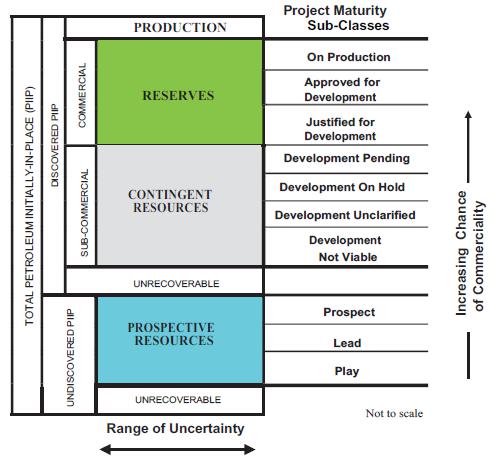

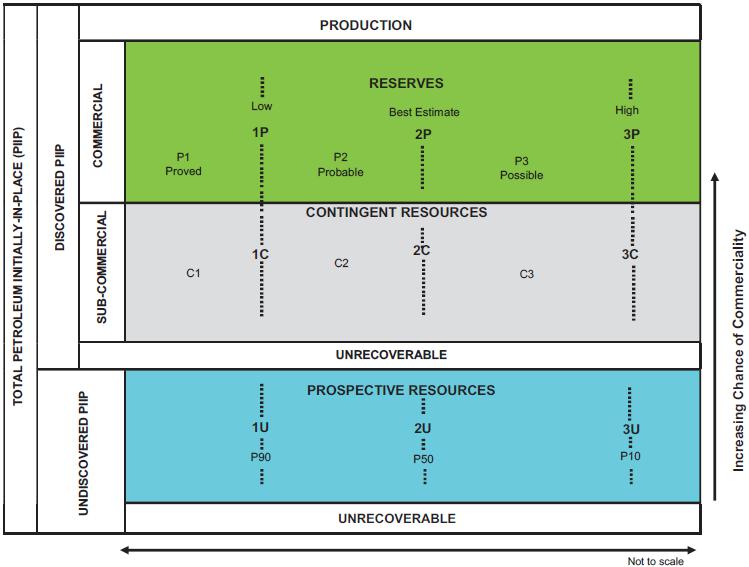

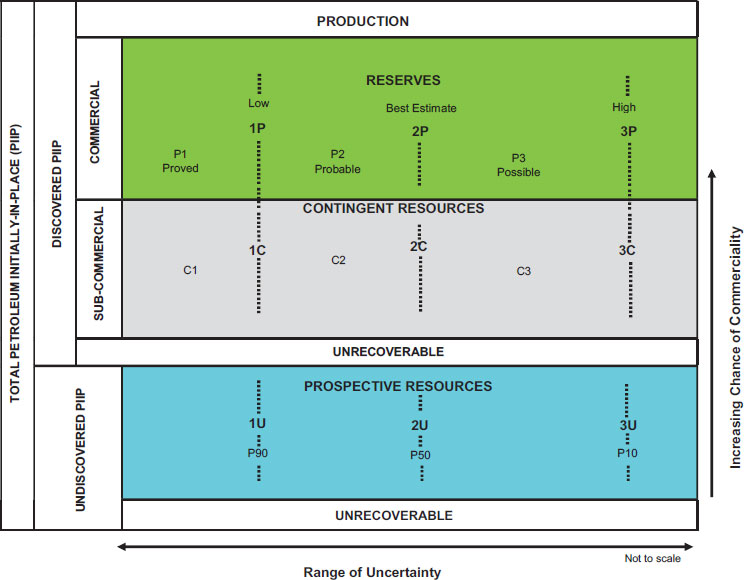

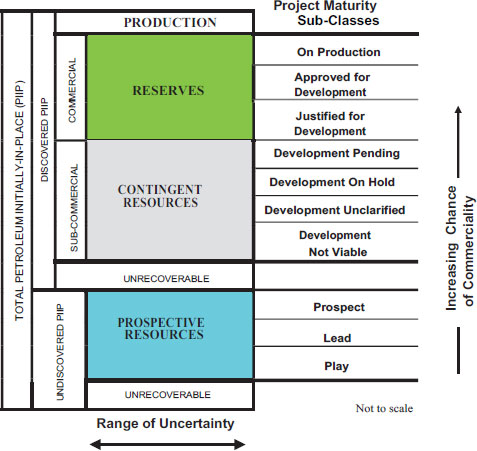

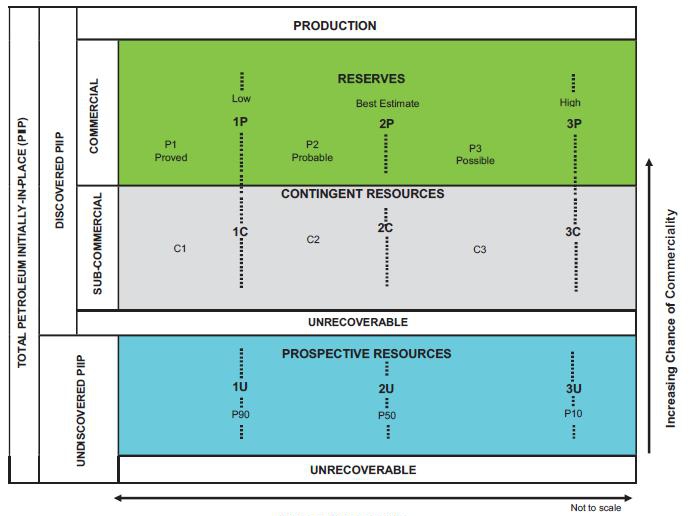

Glossary of Oil and Natural Gas Terms

The following are abbreviations and definitions of certain terms used in this prospectus, which are commonly used in the oil and natural gas industry:

“3P” refers to proven, probable and possible reserves.

“Bbl” refers to one stock tank barrel, of 42 U.S. gallons liquid volume, used in this prospectus in reference to crude oil or other liquid hydrocarbons.

“Bcf” refers to one billion cubic feet of natural gas or CO2.

“Bcfe” refers to one billion cubic feet of natural gas equivalent.

“Btu” refers to British thermal unit, which is the heat required to raise the temperature of one pound of liquid water by one degree Fahrenheit.

“CCUS” refers to carbon capture, utilization and sequestration.

“CO2” refers to carbon dioxide.

“CO2e” refers to carbon dioxide equivalent.

“Developed acreage” refers to the number of acres that are allocated or assignable to productive wells or wells capable of production.

“dry hole” refers to a well found to be incapable of producing hydrocarbons in sufficient quantities such that proceeds from the sale of such production exceed production expenses and taxes.

“Gross acres” or “gross wells” refers to the total acres or wells, as the case may be, in which a working interest is owned.

“lean gas” refers to natural gas that contains a few or no liquefiable liquid hydrocarbons.

“LNG” refers to liquefied natural gas.

“MBbls” refers to one thousand barrels of crude oil or other liquid hydrocarbons.

“Mcf” refers to one thousand cubic feet.

“Mcf/d” refers to one thousand cubic feet per day.

“Mcfe” refers to one thousand cubic feet of natural gas equivalent.

“MMBtu” refers to one million Btus.

“MMcf” refers to one million cubic feet.

iii

“MMcf/d” refers to one million cubic feet per day.

“MMcfe” refers to one million cubic feet of natural gas equivalent.

“MMcfe/d” refers to one million cubic feet of natural gas equivalent per day.

“Mtpa” refers to million tonnes of LNG per year.

“Net acres” refers to the percentage of total acres an owner has out of a particular number of acres, or a specified tract. For example, an owner who has 50% interest in 100 acres owns 50 net acres.

“NGL” refers to natural gas liquids.

“NYMEX” refers to the New York Mercantile Exchange.

“OPEC” refers to the Organization of the Petroleum Exporting Countries.

“Proved developed reserves” or “PDP reserves” refers to reserves that can be expected to be recovered through existing wells with existing equipment and operating methods.

“Proved reserves” refers to the estimated quantities of oil, natural gas and NGLs which geological and engineering data demonstrate with reasonable certainty to be commercially recoverable in future years from known reservoirs under existing economic and operating conditions and prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether deterministic or probabilistic methods are used for the estimation. The project to extract the hydrocarbons must have commenced or the operator must be reasonably certain that it will commence the project within a reasonable time. For a complete definition of proved crude oil and natural gas reserves, refer to the SEC’s Regulation S-X, Rule 4-10(a)(22).

“Proved undeveloped reserves” or “PUD reserves” refers to proved reserves that are expected to be recovered from new wells on undrilled acreage or from existing wells where a relatively major expenditure is required for recompletion. Undrilled locations can be classified as having proved undeveloped reserves only if a development plan has been adopted indicating that such locations are scheduled to be drilled within five years, unless specific circumstances justify a longer time.

“rich gas” refers to natural gas containing heavier hydrocarbons than a lean gas.

“Scope 1 emissions” refers to direct GHG emissions that occur from sources that are controlled or owned by an organization.

“Scope 2 emissions” refers to indirect GHG emissions associated with the purchase of electricity, steam, heat or cooling.

“Scope 3 emissions” refers to GHG emissions that result from the end use of an organization’s products, as well as emissions from other business activities from assets not owned or controlled by the organization but that the organization indirectly impacts in its value chain.

“Tcfe” refers to one trillion cubic feet of natural gas equivalent.

“Undeveloped acreage” refers to acreage under lease on which wells have not been drilled or completed such that there is not production of commercial quantities of hydrocarbons.

“Working interest” refers to the right granted to the lessee of a property to explore for and to produce and own natural gas or other minerals. The working interest owners bear the exploration, development, and operating costs on either a cash, penalty, or carried basis.

Commonly Used Defined Terms

As used in this prospectus, unless the context indicates or otherwise requires, the terms listed below have the following meanings:

“Banpu” refers to our sponsor, Banpu Public Company Limited, a public company listed on the Stock Exchange of Thailand and the ultimate parent company of BKV Corporation, Banpu, Banpu Power and BPPUS.

iv

“Banpu Power” refers to Banpu Power Public Company Limited, a public company listed on the Stock Exchange of Thailand. Banpu owns approximately 78.66% of Banpu Power as of December 31, 2021.

“Barnett” refers to the Barnett Shale in the Fort Worth Basin of Texas.

“BKV Barnett” refers to BKV Barnett LLC, a Delaware limited liability company and wholly owned subsidiary of BKV O&G.

“BKV Chaffee” refers to BKV Chaffee Corners, LLC, a Delaware limited liability company and wholly owned subsidiary of BKV O&G.

“BKV Chelsea” refers to BKV Chelsea, LLC, a Delaware limited liability company and wholly owned subsidiary of BKV O&G.

“BKV dCarbon Ventures” refers to BKV dCarbon Ventures, LLC, a Delaware limited liability company and the CCUS business of BKV Corporation.

“BKV Midstream” refers to BKV Midstream, LLC, a Delaware limited liability company and wholly owned subsidiary of BKV Corporation.

“BKV O&G” refers to BKV Oil and Gas Capital Partners, L.P., a Delaware limited partnership and wholly owned subsidiary of BKV Corporation.

“BKV Operating” refers to BKV Operating, LLC, a Delaware limited liability company and wholly owned subsidiary of BKV O&G.

“BKV-BPP Power” or “BKV-BPP Power Joint Venture” refers to BKV-BPP Power LLC, a Delaware limited liability company and the joint venture between BKV Corporation and BPPUS, in which we own a 50% interest.

“BNAC” refers to Banpu North America Corporation, a subsidiary of Banpu, our sponsor, and the majority stockholder of BKV Corporation.

“BPPUS” refers to Banpu Power US Corporation, a wholly owned subsidiary of Banpu Power and the owner of a 50% interest in the BKV-BPP Power Joint Venture.

“bylaws” refers to the amended and restated bylaws of BKV Corporation to be adopted in connection with the consummation of this offering.

“certificate of incorporation” refers to the second amended and restated certificate of incorporation of BKV Corporation to be adopted in connection with the consummation of this offering.

“Data Lake” refers to a centralized cloud, large data technology that stores all company data and enables dashboards, visualizations, and analytics from a variety of systems and inputs.

“ERCOT” refers to the Electric Reliability Council of Texas.

“ESG” refers to environmental, social and governance.

“GAAP” refers to generally accepted accounting principles in the United States.

“GHG” refers to greenhouse gases.

“governing documents” refers to our certificate of incorporation and our bylaws.

“HRCO” refers to a contract for the financial purchase and sale of power based on a floating price of natural gas at a predetermined location using a predetermined conversion factor, or heat rate, required to turn the fuel input into electricity.

“Kalnin Ventures” refers to Kalnin Ventures LLC, a Colorado limited liability company and wholly owned subsidiary of BKV Corporation.

“NEPA” refers to the Marcellus Shale in the Appalachian Basin of Northeast Pennsylvania.

v

“Net zero” refers to the full elimination and/or offset of Scope 1 and Scope 2 emissions in our owned and operated upstream businesses.

“Ryder Scott” refers to Ryder Scott Company, L.P., independent petroleum engineers.

“Ryder Scott Pricing” refers to Ryder Scott’s estimate of future hydrocarbon price parameters, as of June 30, 2022, based on Ryder Scott’s survey of future hydrocarbon price parameters used by financial institutions and others in the oil and gas industry, as well as NYMEX futures prices. Ryder Scott Pricing also includes a cost escalation model, as further described in Ryder Scott’s reports.

“Temple I” refers to the combined gas turbine and steam turbine power plant located in Temple, Texas and owned by the BKV-BPP Power Joint Venture.

vi

PROSPECTUS SUMMARY

This summary highlights certain information about us and this offering contained elsewhere in this prospectus, but it is not complete and does not contain all of the information you should consider before making an investment decision. In addition to this summary, you should read this entire prospectus carefully, including the sections titled “Risk Factors,” “— Summary Historical Financial Information,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our historical financial statements and the related notes thereto included elsewhere in this prospectus, before making an investment decision. This summary contains forward-looking statements that involve risks and uncertainties. See “Cautionary Statement Regarding Forward-Looking Statements.” References in this prospectus to “BKV,” the “Company,” “we,” “us,” “our” and like terms are to BKV Corporation, a Delaware corporation, and its wholly owned subsidiaries, unless the context otherwise requires or we otherwise state.

Our Company

Overview

We are a forward thinking, growth driven, vertically integrated energy company focused on creating value for our stockholders through the organic development of our properties as well as accretive acquisitions. Our core business is to produce natural gas from our owned and operated upstream businesses, which we expect to achieve net zero Scope 1 and Scope 2 emissions by the end of 2025. We maintain a “closed-loop” approach to our net zero emissions goal with our four business lines: natural gas production, natural gas gathering, processing and transportation (our “natural gas midstream business”), power generation and carbon capture, utilization and sequestration (“CCUS”). We believe that the safe production of low impact, sustainable energy is not simply a good idea, it is good business. To that end, we believe that our differentiated business model, net zero emissions focus, highly experienced management team and technology-driven approach to operating our business will enable us to create stockholder value.

![[MISSING IMAGE: tm2217921d1-org_verview4c.jpg]](tm2217921d1-org_verview4c.jpg)

We are dedicated to making advancements in the production of sustainable energy and being a force for good in our society. We understand the impact climate change has on our community, the world and

1

future generations, which is why addressing these impacts in how energy is produced is a top priority. In particular, it is one of our core values, “Be One BKV,” to create a unified team with a shared vision to achieve our ESG goals.

![[MISSING IMAGE: tm2217921d1-pg_bkvass4c.jpg]](tm2217921d1-pg_bkvass4c.jpg)

2

Our Operations

Natural Gas Production

We are engaged in the acquisition, operation and development of natural gas and NGL properties primarily located in the Barnett Shale in the Fort Worth Basin of Texas (the “Barnett”) and in the Marcellus Shale in the Appalachian Basin of Northeastern Pennsylvania (“NEPA”). Our upstream assets are the core of our business and provide us with substantial Adjusted Free Cash Flow, which we expect will be sufficient to fund our capital expenditure program, enhance stockholder value and support future acquisitions across our four business lines while maintaining a conservative balance sheet. We have a balanced portfolio of low decline producing properties and undeveloped inventory, primarily in the Barnett. Additionally, our focus on operational efficiencies, access to BKV-owned and third-party midstream systems, and proximity to natural gas demand markets along the Gulf Coast and Northeast corridor allow us to generate high margins.

As of June 30, 2022, our total acreage position was approximately 505,000 net acres, 99% of which was held by production. As of June 30, 2022, our net daily production (after giving effect to the Exxon Barnett Acquisition) averaged 878 MMcfe/d, consisting of approximately 79% natural gas and approximately 21% NGLs. As of June 30, 2022, our total proved reserves of 6,305 Bcfe had an estimated 7% year-over-year average base decline rate over the next 10 years. We have more than 10 years of core inventory remaining, with attractive returns, based on a 1 to 1.5 rigs per year pace, including 515 horizontal locations and more than 1,700 refracture (“refrac”) candidates. Based on current commodity prices, the capital investment required to hold production flat year-over-year is less than approximately 30% of our annual Adjusted EBITDAX. Adjusted EBITDAX is not a financial measure calculated in accordance with GAAP. See “— Summary Historical Financial Information — Non-GAAP Financial Measures” for a description of this measure and a reconciliation to the most directly comparable GAAP measure.

We entered the Barnett in October 2020 with our acquisition of more than 289,000 net acres and 3,850 producing operated wells and related upstream assets from Devon Energy Corporation (“Devon Energy”). On June 30, 2022, we further scaled our Barnett position by acquiring approximately 175,000 net acres, 2,100 operated wells and related upstream and other assets in the Exxon Barnett Acquisition. As of June 30, 2022, our Barnett acreage position was approximately 468,000 net acres, which is approximately 99% held by production. Our average daily Barnett production of approximately 740 MMcfe/d for the six months ended June 30, 2022 consisted of 75% natural gas and 25% NGLs. We had an average working interest in our operated wells in the Barnett of approximately 96% as of June 30, 2022.

We are the largest natural gas producer by gross operated volume in the Barnett. Based on information published by the Texas Railroad Commission (“TRRC”), the chart below illustrates our gross operated production volumes in the Barnett (including the Exxon Barnett Acquisition), which represent approximately 29% of the total Barnett production, and nearly double that of the next largest producer in the Barnett for the month of March 2022.

3

![[MISSING IMAGE: tm2217921d1-bc_top104c.jpg]](tm2217921d1-bc_top104c.jpg)

We entered NEPA in 2016 and have subsequently scaled our position through 12 acquisitions. As of June 30, 2022, our acreage position was approximately 37,000 net acres, which is approximately 94% held by production. Our average net daily production of 138 MMcfe/d for the six months ended June 30, 2022 consisted entirely of natural gas. We had an average working interest in our operated wells in NEPA of 89% as of June 30, 2022.

Natural Gas Midstream

Through our ownership in midstream systems, we are engaged in the gathering, processing and transportation of natural gas (which we refer to as our natural gas midstream business) that supports our upstream assets and third-party producers in the Barnett and NEPA. Our midstream assets improve our overall corporate returns by enhancing our margins and lowering our break-even operating costs while allowing us to manage the timing, development and optimization of production of our upstream assets. In the Barnett, as of June 30, 2022, approximately 220 MMcf/d of our gross production (approximately 25% of our total gross Barnett production) was gathered and processed by our owned Barnett midstream system, which includes approximately 778 miles of gathering pipeline, 65 midstream compressors and one amine processing unit. Additionally, our owned Barnett midstream system has over 200 MMcf/d in unutilized pipeline and processing capacity, providing room to increase throughput (from our own production and for third-party volumes) while maintaining optimal operating pressure with limited additional capital investment required. We also believe we have ample dedicated capacity on third party midstream systems for our expected production and future development. In NEPA, as of June 30, 2022, we had an approximate 29.4% non-operated ownership interest in a midstream system, which is operated by subsidiaries of Repsol Oil & Gas (“Repsol”), with throughput of approximately 174 MMcf/d, and we separately own and operate approximately 16 miles of natural gas gathering pipelines, 14 miles of freshwater distribution pipelines and six gas compression units.

Power Generation

We have a 50% ownership interest in the BKV-BPP Power Joint Venture, which owns Temple I, a newly-constructed, modern combined cycle gas and steam turbine power plant located in the Electric Reliability Council of Texas (“ERCOT”) North Zone in Temple, Texas. The remaining 50% interest is owned by BPPUS, a wholly owned subsidiary of Banpu Power and an affiliate of our sponsor, Banpu. Temple I has an annual average power generation capacity of 755 MW and delivers power to customers on the ERCOT power network in Texas. Temple I is among the most efficient generators supplying power to ERCOT, with a baseload design heat rate of approximately 6,950 Btu/kWh, which is well below the ERCOT Combined

4

Cycle Gas Turbines (“CCGT”) average. Temple I’s modern technology enables it to respond to rapidly changing market signals in real time, making it well-suited to serve the various needs of the ERCOT market. We expect our power generation assets will be synergistic with our base upstream business. In the near term, we will seek to establish midstream contracts that allow us to supply our own natural gas directly to Temple I and its firm intrastate natural gas storage service at the Bammel storage facility. Once implemented, supplying our own natural gas to Temple I will reduce gas transportation costs and create reciprocal natural hedges for both businesses via vertical integration. Additionally, we leverage our existing organization to provide marketing, engineering, finance, accounting and other administrative services to the BKV-BPP Power Joint Venture for an annual fee plus expenses. We intend to continue to build out our power generation business through opportunistic acquisitions of power generation assets and to expand into retail power, which would enable us to ultimately provide net zero wellhead-to-household energy to the end-consumer.

Carbon Capture, Utilization and Sequestration

We are committed to capturing CO2 that is separated from natural gas power generation and compression and from various high concentration industrial and natural gas processing CO2 sources with existing infrastructure, and then compressing and injecting the CO2 into underground injection control (“UIC”) wells. We launched our CCUS business, BKV dCarbon Ventures, in March 2022 and reached a final investment decision (“FID”) on our first high concentration CCUS project in the Barnett in June 2022 with EnLink Midstream, LLC (“EnLink”). This CCUS project will separate CO2 from substantially all of our EnLink-gathered natural gas production, which we expect to achieve a maximum injection rate of up to 185,000 tons of CO2 per year. This represents more than 8% of our Scope 1 and 2 upstream emissions from our owned and operated upstream businesses, with the first injection scheduled for the second half of 2023. We intend to continue to develop our CCUS business and expect to use this project as a prototype for modular, smaller-scale projects that can be repeated and quickly scaled. We are targeting the development of five to ten high-concentration, and potentially some low-concentration, CCUS projects in the near-term based on economics supported by the current carbon tax credit policy in Section 45Q of the Internal Revenue Code of 1986, as amended (the “Code” and such tax credit policy, “Section 45Q”). Although these potential projects are in different stages of the evaluation process, we have identified a CCUS project pipeline of nearly 30 million metric tons of CO2 per year, which is nearly two times the size of our Scope 1, 2 and 3 emissions combined. We seek to execute projects with attractive standalone economics for high and low CO2 concentration streams that contribute to our near-term goal of net zero emissions, which we consider to be full elimination and/or offset of the Scope 1 and 2 emissions in our upstream businesses, by the end of 2025. We believe we are well positioned to achieve this goal through our integrated business model, CCUS operations, operational excellence, carbon-negative initiatives and capital discipline. We further aspire to offset the Scope 3 emissions impact of our owned and operated upstream businesses by the early 2030s, with what we believe is a clear and credible path to these net zero goals through the expansion of our CCUS business.

The chart below reflects our owned and operated upstream Scope 1 and 2 emissions as of June 30, 2022, including Scope 1 and 2 emissions estimates from the Exxon Barnett Acquisition, as well as our intended path to net zero Scope 1 and 2 emissions by 2025 for our owned and operated upstream businesses.

5

![[MISSING IMAGE: tm2217921d1-pc_bkvspla4c.jpg]](tm2217921d1-pc_bkvspla4c.jpg)

(1)

Based on 2021 emission calculations based on EPA Subpart W and best estimates of acquired Exxon Barnett assets based on 2020 Subpart W submissions and does not factor in production decline.

(2)

Emissions surveys assumption to accomplish a 1-2 month leakage period versus 12-month period which must have regulatory updates (current proposed OOO.b,c) to include continuous/flyover/satellite technology sensitivities.

(3)

Solar will offset Scope 2 emissions through a 5-10 MW build out.

We believe our approach to reducing the emissions of our direct operations is repeatable for most similar assets and would enable us to achieve net zero Scope 1 and 2 emissions with respect to future assets within three to four years after taking over control.

Business Strategy

Our strategy is to create value for our stockholders by managing and growing our integrated asset base and delivering sustainable energy focused on our net zero objectives. Our strategy has the following principal elements:

•

Deliver robust returns to stockholders. We intend to prioritize delivering strong returns to our stockholders through our dividend policy and focus on creating stockholder value. See “Dividend Policy.” We believe our operational expertise in successfully drilling and refracturing wells, acquiring and integrating assets purchased at attractive valuations and maintaining financial discipline will underpin our ability to meet our stockholder return goals. Our integrated businesses and natural gas-weighted, low-decline PDP reserves collectively reduce our downside risk while providing asymmetric upside returns from the confluence of commodity price uplift potential, operational improvement and development opportunities, and future accretive acquisition opportunities.

•

Optimize the value of our core businesses. We utilize technology and data analysis to enhance our assets and operations, which we believe improves operational efficiencies, reduces our emissions and helps us realize our operational and financial goals as we continue to scale our business. For example, our “Pad of the Future” program, which includes conversion of natural gas-powered instrument pneumatics to compressed air-powered instruments on existing pads, combined with emission and leak surveys, reduces our GHG emissions by 72%, based on current Scope 1 and 2 emissions from production in our owned and operated natural gas upstream business. Our Pad of the Future application also improves pad efficiencies and operating revenue. Employing technology and operational excellence, by June 30, 2022 we had reduced our lease operating costs in the Barnett, excluding the impact of the Exxon Barnett Acquisition, by over 14% since October 2020 and in NEPA by over 26% since January 2019. Additionally, our refrac and long lateral drill programs have allowed us to organically grow our reserves base. As of June 30, 2022, our Barnett refrac program

6

has added 512 Bcfe of proved reserves since its inception in early 2021, with an estimated 1.13 Tcfe net proved, probable and possible (“3P”) reserves at less than an average $0.70/Mcfe finding and development costs during 2021. This refrac program employs specifically designed perforating technology and a suite of innovative refrac techniques, as well as advanced refrac designs and diversion methods to maximize reserve recovery and economics from legacy Barnett wells. Our Barnett new well drilling program has added 1.08 Tcfe of proved reserves since our entry into the Barnett with a total estimate of approximately 2.1 Tcfe 3P reserves. By combining these reserves into a growing vertically integrated asset base, we believe we can enhance margins and create a “closed loop” business that reduces Scope 1 and 2 emissions in our owned and operated upstream businesses and captures margin across the value chain.

•

Grow through opportunistic, synergistic acquisitions. A significant element of our business strategy is gaining scale through accretive acquisitions. We have a track record of growth through acquisitions, which we believe have been at attractive valuations. Since 2016, we have completed 19 acquisitions, resulting in greater than a 100% compound annual growth rate of Adjusted EBITDAX as of June 30, 2022. We believe our business model, management team experience and application of technology enable us to quickly and efficiently integrate additional upstream, midstream and power assets into our business. We also plan to acquire and/or build CO2 transport pipelines and infrastructure to grow our CCUS business, which is the critical link in our integrated business model chain that we believe will allow us to ultimately eliminate and/or offset Scope 3 emissions.

•

Maintain a disciplined financial strategy. We believe we can execute on our business plan and grow our business while continuing to generate substantial Adjusted Free Cash Flow with total capital expenditures, excluding acquisitions, of less than 40% of our annual Adjusted EBITDAX. We are focused on our goal of maintaining a conservative financial profile, with a long-term leverage target of less than 1.0x total net debt to Adjusted EBITDAX. Although we may allow our leverage ratio to exceed our target in connection with a strategic acquisition, we would seek to return our leverage level to below 1.0x as soon as reasonably possible thereafter through Adjusted Free Cash Flow and, if needed, reduced activity levels. To support the generation of future Adjusted Free Cash Flow, we have a policy of hedging approximately 25% to 60% of our production volumes over a given 12 to 24‑month period. We believe our capital efficient project inventory, low-decline natural gas production and multiple, integrated business lines will provide consistent returns through varying business cycles. We intend to apply our cash flows to manage our indebtedness in line with our leverage target, fund our capital expenditure program, enhance stockholder value and execute opportunistic acquisitions across our four business lines. Adjusted EBITDAX is not a financial measure calculated in accordance with GAAP. See “— Summary Historical Financial Information — Non-GAAP Financial Measures” for a description of this measure and a reconciliation to the most directly comparable GAAP measure.

•

Deliver sustainable energy focused on our net zero objectives. We expect to apply our integrated business model, CCUS projects, operational excellence, carbon-negative initiatives, capital discipline and use of technology to realize Scope 1 and 2 net zero upstream owned and operated emissions by the end of 2025. According to the U.S. Energy Information Administration (the “EIA”), lower CO2 emissions realized in the United States have largely been a result of the shift from the use of coal to natural gas for electricity generation. While we believe that switching from coal to natural gas substantially lowers emissions, we believe that emissions can be reduced substantially further through carbon capture on natural gas production, power plants, processing facilities and other energy and industrial infrastructure. As such, in addition to lowering emissions in our direct operations, CCUS for third parties has become a core focus of our business that we expect to represent a meaningful portion of our budgeted capital expenditures going forward as we advance our long-term goal of eliminating and/or offsetting Scope 3 emissions.

•

Encourage innovation. Our distinctive culture encourages innovation with a value-driven focus that feeds into our competitive advantage. For example, our emphasis on the efficient application of modern technology led to the development of our “Pad of the Future” program, our advancements in Barnett refracs and other operational improvements. We intend to continue to develop, retain and add to our already talented, experienced and forward-thinking employees. Our unified team and

7

mantra of “Being a force for good” underpin our core values and provides us with confidence in our ability to successfully manage and grow our business.

Competitive Strengths

We have a number of strengths that we believe will help us successfully execute our business strategy, including:

•

Integrated asset base well positioned for sustainable growth. Our upstream, midstream and power asset bases reside in geographically concentrated areas with numerous asset acquisition opportunities in close proximity. Our proven ability to successfully negotiate, close and integrate these acquisition opportunities quickly and cost effectively will allow us to continue to grow our portfolio of assets synergistically. We believe that scale and the continued application of technological developments and operational excellence, combined with stable, low-decline production profiles, will continue to generate significant capital efficient development opportunities in the Barnett and NEPA.

•

High quality, low decline assets serving key demand markets. Through a series of accretive acquisitions we have established an extensive and largely contiguous acreage position in two key markets, the Barnett and NEPA. Our Barnett assets cover approximately 468,000 net acres and are located in close proximity to key Gulf Coast industrial and LNG demand centers. Our NEPA assets consist of 37,000 net acres in one of the most prolific parts of the Marcellus Shale and are located within less than 200 miles to key demand markets in the U.S. Northeast. We believe the geologic, operational and engineering risks associated with our leasehold acreage have been significantly mitigated through historical development activity. Our PDP reserves had an estimated 7% year-over-year average base decline rate over the next 10 years as of June 30, 2022. Additionally, we have an inventory of over 10 years of refrac and new drill locations within our core acreage that give us the flexibility to maintain or slightly grow current production levels, depending on the commodity cycle.

•

Low emissions energy production. In addition to our focus on owned and operated upstream production of Scope 1 and 2 net zero natural gas by 2025, our long-term goals include eventual Scope 1, 2 and 3 net zero owned and operated natural gas production, which we expect to accomplish via CCUS. We believe we have a comprehensive ESG program, which is overseen and directed by an executive ESG steering committee. In 2021, we certified our NEPA production and achieved a Gold rating with Project Canary’s TrustWell environmental assessment (Project Canary is an environmental certification and ESG data company). This is the second highest rating a company can receive for its production, qualifying our NEPA natural gas production as Responsibly Sourced Gas (“RSG”), which we believe could command a premium in the marketplace. Additionally, we have a plan to achieve net zero Scope 1 and 2 upstream emissions by the end of 2025 based on our “Pad of the Future” emissions reductions, emissions surveys, installing up to 10 MW of solar power, executing CCUS projects which generate offset credits and utilizing offsets to reduce our carbon footprint. We believe BKV dCarbon Ventures will be able to capture over one million metric tons of CO2 per year, beyond our direct asset footprint, by the end of 2025, which exceeds the balance of our current Scope 1 and 2 emissions required to achieve net zero upstream emissions.

•

Efficient use of capital. Our deep, high-graded inventory of refrac opportunities coupled with our inventory of new drill locations allow us to create meaningful additional cash flow with comparatively modest additional capital investments. We utilize operational improvements such as operational process and procurement efficiencies, use of existing field infrastructure, innovative and cost-effective refrac techniques and designs (including diversion methods), drilling long laterals in the Barnett, and optimizing available midstream capacity to further maximize our capital efficiency. Through our midstream, power and CCUS business lines, we are capturing margin across the value chain.

•

Well capitalized and conservative balance sheet. As of December 31, 2021, we had a 0.10x ratio of total net debt to Adjusted EBITDAX. Subsequent to December 31, 2021, we incurred $570.0 million of unsecured debt in connection with the consummation of the Exxon Barnett Acquisition and for working capital. Following the completion of this offering, we intend to continue to maintain a strong balance sheet and fund our operations predominantly with internally generated cash flows. We believe that the low decline, predictable nature of our upstream production profile, combined with our hedging plan and reinvestment rate target, will allow us to successfully meet our leverage goals.

8

•

High caliber and proven management team. We maintain a highly experienced and knowledgeable management team with an average of over 25 years of experience among our senior management team. Our leadership team has significant experience managing integrated energy and power assets for large-scale enterprises, including companies such as PTT Exploration and Production Public Company Limited (“PTT Exploration”) and BP p.l.c. (“BP”). Furthermore, our sponsor, Banpu, one of Asia Pacific’s largest integrated energy companies, provides us with unique and valuable insights into optimizing our integrated energy business.

Recent Developments

CCUS Project with EnLink

On June 8, 2022, BKV dCarbon Ventures and EnLink reached a Phase I FID to develop our first CCUS project and entered into an agreement to dispose of and geologically sequester CO2 generated as a byproduct of the production of our natural gas in the Barnett. This CCUS project will separate CO2 from substantially all of our EnLink-gathered natural gas production, which we expect to achieve a maximum injection rate of up to 185,000 tons of CO2 per year. We currently estimate the total project cost to us to be between $15.0 and $20.0 million. We are targeting commencement of CO2 injection activities by the second half of 2023, subject to our ability to secure all required permits, at which point we expect this project to be one of the first permanent commercial CO2 disposal and sequestration projects to come online in the United States. We expect this project to offset our current Scope 1 and 2 annual emissions by approximately 8%, bringing us closer to our goal of reaching net zero across Scope 1 and 2 upstream emissions by 2025.

Exxon Barnett Acquisition

On June 30, 2022, we closed the acquisition (the “Exxon Barnett Acquisition”) of natural gas upstream and associated midstream infrastructure in the Barnett from XTO Energy, Inc. and Barnett Gathering LLC, subsidiaries of Exxon Mobil Corporation, for a cash purchase price of $750.0 million, plus additional contingent consideration of up to $50.0 million depending on future natural gas prices. Pursuant to the Exxon Barnett Acquisition, we acquired approximately 175,000 total net acres that are approximately 99% held by production, primarily in Tarrant, Johnson and Parker counties, and additional smaller positions in Jack, Wise, Denton, Erath, Hood and Ellis counties, Texas (our “2022 Barnett Assets”). These upstream assets include low decline wells, ideal for delivering consistent cash flow, and high average working interests of approximately 94% in over 2,100 operated wells. The Exxon Barnett Acquisition also included approximately 778 miles of gathering pipelines and compression and processing midstream infrastructure with, as of June 30, 2022, over 450 MMcf/d of throughput capacity and approximately 28 MMcf/d of third-party production being gathered on the system. In connection with the Exxon Barnett Acquisition, we entered into the Term Loan Credit Agreement (as defined herein) with a syndicate of banks and Bangkok Bank Public Company Limited (New York Branch), as the administrative agent. The Term Loan Credit Agreement includes up to $600.0 million of commitments for term loans to be used solely to fund a portion of the purchase price for the Exxon Barnett Acquisition and other costs and expenses associated with the acquisition. As of June 30, 2022, there was $570.0 million in aggregate principal amount outstanding under the Term Loan Credit Agreement. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources — Loan Agreements and Credit Facilities — Term Loan Credit Agreement” for more information.

Amendment to Derivative Agreement

On August 4, 2022, we entered into an amendment to our ISDA Master Agreement with a counterparty to our derivative contracts pursuant to which we have agreed to terminate or novate, at our election, $100.0 million of our derivative contracts. To the extent we elect to terminate any such derivative contracts, we will be required to make cash payments in the applicable amount to the counterparty, which payments would be due in the aggregate by November 30, 2022. We intend to make any such payments with cash flows from operations. See “Note 20 — Subsequent Events” to our consolidated financial statements included elsewhere in this prospectus for additional information regarding this agreement.

9

Corporate Values, Management Team and Sponsor

We believe in making concrete and transparent progress for the future of sustainability in every action we take today and in the future. These beliefs are confirmed by “The BKV Values” that underpin our corporate culture and decision-making and include the following core values: Deliver on Promises, Have Grit, Embrace Change, Show Courage, Solve Problems, Do Good and Be One BKV, all of which are focused on ensuring that “BKV is a force for good.”

Our management team is led by our Chief Executive Officer and founder, Christopher P. Kalnin, who has approximately 22 years of experience in exploration and production (“E&P”) (PTT Exploration & Production), management consulting (McKinsey & Company) and finance (Credit Suisse First Boston). Eric Jacobsen serves as our Chief Operating Officer with over 28 years of energy operational experience, including 16 years of experience at BP and its predecessors and six years of experience at Noble Energy, Inc. John Jimenez serves as our Chief Financial Officer with over 30 years of international energy experience working with BP and Reliance Industries Limited.

BNAC, our majority stockholder, is an indirect, wholly owned subsidiary of Banpu, our ultimate parent company. Banpu is a multi-billion U.S. dollar market cap energy company publicly traded in Thailand. With nearly four decades of experience in business operations covering 10 countries across the Pacific Rim region and the United States, Banpu is an international versatile energy provider committed to its Greener & Smarter strategy, which prioritizes environmentally sustainable businesses and leverages smart technologies and innovations. Upon completion of this offering, Banpu will beneficially own approximately % of our common stock (or approximately % if the underwriters exercise in full their option to purchase additional shares of our common stock). Banpu has informed us that although it may reduce a portion of its ownership position over time, it intends to remain a long-term stockholder and supporter of BKV.

10

Our Structure

The chart below displays a summary of our ownership structure after giving effect to this offering.

![[MISSING IMAGE: tm2217921d1-fc_ourstru4c.jpg]](tm2217921d1-fc_ourstru4c.jpg)

(1)

Consists of management, directors and other employee and non-employee stockholders.

The information in the chart above does not include additional shares of our common stock reserved for future awards pursuant to the BKV Corporation 2022 Equity and Incentive Compensation Plan (the “2022 Plan”), including shares of common stock that may be issued upon vesting of outstanding equity awards, and shares of our common stock available for purchase by employees pursuant to the BKV Corporation Employee Stock Purchase Plan (the “ESPP”).

11

Implications of Being an Emerging Growth Company

We qualify as an “emerging growth company” as defined in Section 2(a)(19) of the Securities Act of 1933, as amended (the “Securities Act”), including as modified by the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). As a result, for so long as we qualify as an emerging growth company, we are eligible to take advantage of certain exemptions from various reporting requirements applicable to other public companies that are not emerging growth companies. These exemptions include:

•

being permitted to present only two years of audited financial statements and only two years of related “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus;

•

not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, as amended (the “Sarbanes-Oxley Act”);

•

reduced disclosure obligations regarding executive compensation in our periodic reports, proxy statements and registration statements, including in this prospectus;

•

not being required to comply with any new requirements adopted by the Public Company Accounting Oversight Board (“PCAOB”) requiring mandatory audit firm rotation or a supplement to the auditor’s report in which the auditor would be required to provide additional information about the audit and the financial statements of the issuer; and

•

exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved.

We have elected to take advantage of certain of the reduced disclosure obligations in this prospectus and may elect to take advantage of other reduced reporting requirements in our future filings with the Securities and Exchange Commission (the “SEC”). As a result, the information that we provide to our stockholders may be different than you might receive from other public reporting companies in which you hold equity interests.

The JOBS Act also provides that an emerging growth company can take advantage of an extended transition period for complying with new or revised accounting standards, but we have elected not to avail ourselves of this exemption. Rather, we will adopt new or revised accounting standards on the relevant dates in which adoption of such standards is required for other public companies.

We may take advantage of these provisions until the last day of our fiscal year following the fifth anniversary of the date of the first sale of our common equity securities pursuant to an effective registration statement under the Securities Act. Such fifth anniversary will occur in 2027. However, if certain events occur prior to the end of such five-year period, including if we become a “large accelerated filer,” our gross revenues for any fiscal year equal or exceed $1.07 billion or we issue more than $1.0 billion of non-convertible debt in any three-year period, we will cease to be an emerging growth company prior to the end of such five-year period.

Controlled Company

We intend to apply to list our common stock on the NYSE. Upon completion of this offering, BNAC will hold approximately % of our total outstanding shares of common stock (or approximately % if the underwriters exercise in full their option to purchase additional shares), comprising more than 50% of the voting power of our outstanding common stock. As a result, we will be a “controlled company” within the meaning of the corporate governance rules of the NYSE. As a “controlled company,” we will be eligible to rely on exemptions from the obligation to comply with certain NYSE corporate governance requirements, including the requirements that:

•

a majority of our board of directors consist of independent directors;

•

we have a corporate governance and nominating committee that is composed entirely of independent directors with a written charter addressing the committee’s purpose and responsibilities; and

•

we have a compensation committee that is composed entirely of independent directors with a written charter addressing the committee’s purpose and responsibilities.

12

These exemptions do not modify the independence requirements for our audit committee. As a controlled company, we will remain subject to the rules of the Sarbanes-Oxley Act and the NYSE that require us to have an audit committee composed entirely of independent directors. Under these rules, we must have at least one independent director on our audit committee by the date our common stock is listed on the NYSE, at least two independent directors on our audit committee within 90 days of the listing date, and at least three independent directors on our audit committee within one year of the listing date. We expect to have independent directors upon the closing of this offering.

While BNAC continues to control more than 50% of the voting power of our outstanding common stock, we qualify for, and intend to rely on, these exemptions. Accordingly, you will not have the same protections afforded to stockholders of companies that are subject to all of the corporate governance requirements of the NYSE.

If we cease to be a controlled company within the meaning of the applicable rules of the NYSE, we will be required to comply with these requirements after specified transition periods.

Contact Information

Our principal executive offices are located at 1200 17th Street, Suite 2100, Denver, Colorado 80202, and our telephone number at such address is (720) 375-9680. Our website address is www.bkvcorp.com. The contents of our website are not incorporated by reference herein and are not a part of, and shall not deemed to be a part of, this prospectus.

13

The Offering

Issuer

BKV Corporation, a Delaware corporation

Securities offered

Common stock, par value $0.01 per share (“common stock”)

Common stock offered by us

shares (or shares if the underwriters exercise in full their option to purchase additional shares)

Underwriters’ option to purchase additional shares

The underwriters have an option for a period of 30 days to purchase up to an additional shares of our common stock.

Common stock outstanding immediately after this offering

shares (or shares if the underwriters exercise in full their option to purchase additional shares)

Use of proceeds

We estimate that the net proceeds to us from the sale of our common stock in this offering, after deducting underwriting discounts and commissions and estimated offering expenses payable by us, will be approximately $ million (or approximately $ million if the underwriters exercise in full their option to purchase additional shares), based on an assumed initial public offering price of $ per share (the midpoint of the price range set forth on the cover page of this prospectus).

We intend to use the net proceeds we receive from the sale of our common stock in this offering to fund our capital expenditures and for other general corporate purposes. See “Use of Proceeds.”

Dividend policy

At or prior to the closing of this offering, our board of directors will adopt a policy pursuant to which we intend to pay dividends to stockholders. See “Dividend Policy.”

Voting rights

Each share of common stock will entitle the holder to one vote per share. Generally, matters to be voted on by stockholders must be approved by a majority of the votes entitled to be cast at a meeting by holders of all shares of common stock present in person or represented by proxy.

In addition, pursuant to the stockholders’ agreement to be entered into upon the completion of this offering between BNAC and us (our “Stockholders’ Agreement”), for so long as BNAC and Banpu beneficially own 10% or more of our voting stock, BNAC will be entitled to designate for nomination to our board of directors a number of individuals approximately proportionate to such beneficial ownership, provided that (i) from the completion of this offering until the first anniversary of the completion of this offering, at least three board seats will not be BNAC designees, (ii) from and after the first anniversary of the completion of this offering until the first date on which BNAC and Banpu beneficially own 50% or less of our voting stock, at least four board seats will not be BNAC designees, and (iii) from and after the first date on which BNAC and Banpu beneficially own 50% or less of our voting stock, a number of board seats equal to the minimum number of directors that would constitute a majority of the total number

14

of directors comprising our board of directors will not be BNAC designees. See “Management,” “Principal Stockholders,” “Description of Capital Stock” and “Certain Relationships and Related Party Transactions” for additional information.

Risk factors

You should read the section of this prospectus titled “Risk Factors” and other information included in this prospectus for a discussion of factors to carefully consider before deciding to invest in shares of our common stock.

Controlled company

We will be a “controlled company” within the meaning of the corporate governance rules of the NYSE. Upon completion of this offering, BNAC will hold % of our common stock (or approximately % if the underwriters exercise in full their option to purchase additional shares), comprising more than 50% of the voting power of our outstanding common stock. See “Management — Controlled Company.”

Listing and stock exchange symbol

We intend to list our common stock on the NYSE under the symbol “BKV.”

The number of shares of common stock that will be outstanding immediately after the completion of this offering is based on shares of our common stock to be issued pursuant to this offering (assuming the underwriters do not exercise their option to purchase additional shares), and excludes up to shares of our common stock reserved for future issuance under our equity compensation plans, which will become effective upon the completion of this offering.

Unless otherwise indicated and except for our historical financial statements and related notes included elsewhere in this prospectus, the information in this prospectus:

•

assumes the execution of our Stockholders’ Agreement, as further described under “Certain Relationships and Related Party Transactions”;

•

assumes the amendment and restatement of our existing certificate of incorporation and the amendment and restatement of our existing bylaws in connection with the consummation of the offering;

•

assumes an initial public offering price of $ per share of common stock (the midpoint of the price range set forth on the cover page of this prospectus); and

•

assumes that the underwriters do not exercise their option to purchase additional shares of common stock.

Risk Factors Summary

Investing in our common stock involves risks, including those highlighted in the section titled “Risk Factors” immediately following this prospectus summary, of which you should be aware before making a decision to invest in our common stock. These risks may offset our competitive strengths or have a negative effect on our strategy or operating activities, which could cause a decrease in the price of our common stock and a loss of all or part of your investment. These risks include, among others, the following:

Risks Related to Our Upstream Business and Industry

•

the volatility of natural gas and NGL prices due to factors beyond our control;

•

our reliance on a single third party for all of our natural gas marketing and another third party for substantially all of our natural gas and NGL midstream services in the Barnett;

•

our reserve estimates are based on assumptions that may prove to be inaccurate;

15

•

our ability to find or acquire additional natural gas and NGL reserves that are economically recoverable, including development of our proved undeveloped reserves and associated capital expenditures;

•

uncertainties in evaluating the expected benefits and potential liabilities of recoverable reserves;

•

risks and uncertainties related to drilling operations, which are high-risk and operationally complex;

•

the availability or cost of water, equipment, supplies, personnel and oilfield services;

•

our limited control over activities on properties we do not operate;

Risks Related to Our Power Generation Business

•

the operation of our power generation business through a joint venture which we do not control;

•

risks and hazards related to the operation or maintenance of electric generation facilities;

•

the lack of long-term power sales agreements for Temple I;

•

the disruption of the fuel supplies necessary to generate power at Temple I;

Risks Related to Our CCUS Business

•

our ability to pursue and develop our CCUS business and the associated material capital investments;

Risks Related to Our Midstream Business

•

risks and hazards related to midstream operations as complex activities;

•

our ability to fulfill our business plan to supply our own natural gas to Temple I and our dependence on our natural gas midstream system for the gathering and processing of our natural gas production;

Risks Related to Our Business Generally

•

the geographical concentration of substantially all of our oil and gas and midstream properties;

•

the effect of a deterioration in general economic, business or industry conditions and COVID-19 (including any variants thereof, “COVID-19”);

•

our ability to achieve net zero Scope 1 and Scope 2 emissions in our upstream business;

•

our ability to generate cash flow to meet our debt obligations or fund our other liquidity needs;

•

risks related to our debt and debt agreements, the lack of a committed working capital facility and hedging arrangements that expose us to risk of financial losses and counterparty credit risk;

•

our dependence, as a holding company, on our subsidiaries and our joint venture for cash;

•

operating hazards that could result in substantial losses or liabilities for which we may not have adequate insurance coverage;

•

our ability to make accretive acquisitions or successfully integrate acquired businesses or assets;

•

our substantial capital requirements and our ability to obtain financing or fund working capital needs;

•

the intense competition in the energy industry and our ability to compete with other companies;

•

cybersecurity or physical security threats or disruptions or loss of our information systems;

•

increased activism and negative investor sentiment regarding upstream activities and companies;

•

the loss of our executive officers and technical personnel and our ability to retain technical personnel;

•

exemptions from certain reporting requirements for as long as we are an emerging growth company;

16

Risks Related to Environmental, Legal Compliance and Regulatory Matters

•

complex laws, regulations and initiatives related to our operations and the use of hydraulic fracturing;

•

reductions in demand for natural gas, NGL and oil due to conservation measures and technological advances;

•

the effect of increased attention to ESG matters, conservation measures and technological advances;

•

risks related to climate change, including transitional, legal, political, financial and physical risks;

•

significant costs and liabilities related to federal, state and local environmental, health and safety laws and regulations;

•

potential tax law changes;

•

complex and evolving laws and regulations regarding privacy and data protection;

Risks Related to Our Relationship with Banpu and its Affiliates

•

the substantial influence of Banpu, our controlling stockholder, over us;

•

our historical reliance on Banpu for capital investments to fund our business operations;

•

we expect to be a “controlled company” within the meaning of the NYSE rules and, as a result, will qualify for and could rely on exemptions from certain corporate governance requirements;

•

conflicts of interest between Banpu and us or our other stockholders or conflicts of interest of our directors as a result of their positions with, or ownership of common stock of, Banpu;

Risks Related to the Offering and Our Common Stock

•

our actual operating results and activities could differ materially from our estimates;

•

risks related to payment of dividends on our common stock, including the lack of sufficient available cash, the discretion of our board of directors, and restrictions in our debt agreements, with respect to payment of dividends and the impact of our dividend policy on our ability to grow;

•

the costs of, and our ability to comply with, the requirements of being a public company;

•

we have identified material weaknesses in our internal control over financial reporting;

•

the lack of an existing market for our common stock;

•

provisions in our governing documents and Delaware law that could discourage acquisition bids or merger proposals; and

•

future sales of our common stock in the public market, or the perception that such sales may occur, could reduce our stock price.

17

Summary Historical Financial Information

The following table shows our summary historical consolidated financial information for the periods and as of the dates indicated. The summary historical consolidated financial information as of and for the years ended December 31, 2021 and 2020 was derived from our audited historical financial statements, included elsewhere in this prospectus. The summary historical consolidated financial data is qualified in its entirety by, and should be read in conjunction with, the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” section included in this prospectus and the consolidated financial statements and related notes and other financial information included in this prospectus. Historical results are not necessarily indicative of results that may be expected for any future period.

| | | |

Year Ended December 31,

|

| |||||||||

| | | |

2021

|

| |

2020

|

| ||||||

| | | |

(in thousands, except share and

per share data) |

| |||||||||

| Revenues and other operating income: | | | | | | | | | | | | | |

|

Natural gas sales

|

| | | $ | 597,050 | | | | | $ | 101,758 | | |

|

NGL sales

|

| | | | 225,135 | | | | | | 11,952 | | |

|

Oil sales

|

| | | | 7,560 | | | | | | 1,333 | | |

|

Non-operated midstream revenues, net

|

| | | | 6,917 | | | | | | 7,458 | | |

|

Derivatives (losses) gains, net

|

| | | | (383,847) | | | | | | 20,755 | | |

|

Marketing revenues

|

| | | | 52,616 | | | | | | — | | |

|

Other

|

| | | | 251 | | | | | | 33 | | |

|

Total revenues and other operating income

|

| | | | 505,682 | | | | | | 143,289 | | |

| Operating Expenses: | | | | | | | | | | | | | |

|

Lease operating and workover

|

| | | | 88,105 | | | | | | 31,260 | | |

|

Taxes other than income

|

| | | | 45,650 | | | | | | 5,151 | | |

|

Gathering and transportation

|

| | | | 173,587 | | | | | | — | | |

|

Accretion of asset retirement obligations

|

| | | | 10,030 | | | | | | 3,211 | | |

|

Depreciation, depletion and amortization

|

| | | | 81,986 | | | | | | 83,388 | | |

|

Exploration and impairment

|

| | | | 34 | | | | | | 560 | | |

|

General and administrative

|

| | | | 85,740 | | | | | | 29,442 | | |

|

Accretion of right of use liabilities(1)

|

| | | | 227 | | | | | | 184 | | |

|

Total operating expenses

|

| | | | 485,359 | | | | | | 153,196 | | |

|

Income (loss) from operations

|

| | | | 20,323 | | | | | | (9,907) | | |

| Other income (expense): | | | | | | | | | | | | | |

|

(Loss) gain on contingent consideration liabilities(2)

|

| | | | (194,968) | | | | | | 7,135 | | |

|

Interest expense

|

| | | | (2,134) | | | | | | (1,713) | | |

|

Other income

|

| | | | 872 | | | | | | — | | |

|

Income from equity affiliates

|

| | | | 910 | | | | | | — | | |

|

Interest income

|

| | | | 8 | | | | | | 121 | | |

|

Loss before income taxes

|

| | | | (174,989) | | | | | | (4,364) | | |

|

Income tax benefit (expense)

|

| | | | 40,526 | | | | | | (38,982) | | |

|

Net loss and comprehensive loss attributable to BKV Corporation

|

| | | $ | (134,463) | | | | | $ | (43,346) | | |

|

Less accretion of preferred stock to redemption value

|

| | | | (3,745) | | | | | | — | | |

|

Less preferred stock dividends

|

| | | | (9,900) | | | | | | (460) | | |

|

Less deemed dividend on redemption of preferred stock

|

| | | | (22,606) | | | | | | — | | |

|

Net loss and comprehensive loss attributable to common stockholders

|

| | | $ | (170,714) | | | | | $ | (43,806) | | |

18

| | | |

Year Ended December 31,

|

| |||||||||

| | | |

2021

|

| |

2020

|

| ||||||

| | | |

(in thousands, except share and

per share data) |

| |||||||||

| Net loss and comprehensive loss per common share: | | | | | | | | | | | | | |

|

Basic and diluted

|

| | | $ | (1.46) | | | | | $ | (0.42) | | |

| Weighted average number of common shares outstanding: | | | | | | | | | | | | | |

|

Basic and diluted

|

| | | | 116,904 | | | | | | 105,275 | | |

| Balance Sheet Information (at period end): | | | | | | | | | | | | | |

|

Cash and cash equivalents

|

| | | $ | 134,667 | | | | | $ | 17,445 | | |

|

Total natural gas properties, net

|

| | | $ | 1,176,117 | | | | | $ | 1,169,297 | | |

|

Total liabilities

|

| | | $ | 865,889 | | | | | $ | 262,424 | | |

|

Total mezzanine equity

|

| | | $ | 83,847 | | | | | $ | 137,212 | | |

|

Total stockholders’ equity

|

| | | $ | 671,092 | | | | | $ | 942,856 | | |

| Statement of Cash Flows Information: | | | | | | | | | | | | | |

|

Net cash provided by (used in) operating activities

|

| | | $ | 358,133 | | | | | $ | (7,405) | | |

|

Net cash used in investing activities

|

| | | $ | (161,858) | | | | | $ | (513,992) | | |

|

Net cash (used in) provided by financing activities

|

| | | $ | (79,053) | | | | | $ | 442,723 | | |

| Other Financial Data (unaudited)(3): | | | | | | | | | | | | | |

|

Adjusted EBITDAX

|

| | | $ | 303,748 | | | | | $ | 65,148 | | |

|

Upstream reinvestment rate

|

| | | | 22% | | | | | | 16% | | |

|

Adjusted Free Cash Flow

|

| | | $ | 165,090 | | | | | $ | 41,794 | | |

|

Adjusted Free Cash Flow Margin

|

| | | | 19% | | | | | | 34% | | |

|

Total Net Leverage Ratio

|

| | | | 0.10x | | | | | | 0.10x | | |

(1)

Represents right of use liabilities related to office space, a pipe yard, and compressor leases.

(2)