UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2022

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ______ to ______

Commission file number 001-40031

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of Principal Executive Offices) | (Zip Code) | |||||||

( | ||||||||

| Registrant's telephone number, including area code | ||||||||

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or and emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| Large accelerated filer | o | Accelerated filer | o | ||||||||

x | Smaller reporting company | ||||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

The aggregate market value of voting stock held by non-affiliates of the Registrant on June 30, 2022, based on the closing price of $5.66 per share for shares of the Registrant’s common stock as reported by the New York Stock Exchange, was approximately $37.8 million. Shares of common stock beneficially owned by each executive officer, director, and holder of more than 10% of our common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

There were 141,477,297 shares of our common stock, $0.0001 par value per share, outstanding as of March 24, 2023.

DOCUMENTS INCORPORATED BY REFERENCE

Items 10, 11, 12, 13 and 14 of Part III of this Annual Report on Form 10-K are incorporated by reference from the registrant’s amendment to this Form 10-K to be filed on Form 10-K/A with the Securities and Exchange Commission no later than 120 days after the end of the registrant’s fiscal year covered by this report.

2

BIGBEAR.AI HOLDINGS, INC.

Annual Report on Form 10-K

December 31, 2022

TABLE OF CONTENTS

| Item | Page | |||||||

3

Part I

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the Securities Act of 1933, as amended (the “Securities Act”), the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and the Private Securities Litigation Reform Act of 1995. All statements contained in this Annual Report on Form 10-K other than statements of historical fact, including statements regarding our future operating results and financial position, our business strategy and plans and our objectives for future operations, are forward-looking statements. Forward-looking statements generally are accompanied by words such as “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect,” “should,” “would,” “plan,” “predict,” “potential,” “seem,” “seek,” “future,” “outlook,” and similar expressions that predict or indicate future events or trends or that are not statements of historical matters. These forward-looking statements include, but are not limited to, statements regarding BigBear’s industry, future events, and other statements that are not historical facts. These forward-looking statements are based on current expectations and beliefs concerning future developments and their potential effects on us and should not be relied upon as representing BigBear’s assessments as of any date subsequent to the date of this Annual Report on Form 10-K. There can be no assurance that future developments affecting us will be those that we have anticipated. These forward-looking statements are subject to a number of risks and uncertainties, including those relating to: changes in domestic and foreign business, market, financial, political, and legal conditions; delays caused by factors outside of our control, including changes in fiscal or contracting policies or decreases in available government funding; changes in government programs or applicable requirements; budgetary constraints, including automatic reductions as a result of “sequestration” or similar measures and constraints imposed by any lapses in appropriations for the federal government or certain of its departments and agencies; influence by, or competition from, third parties with respect to pending, new, or existing contracts with government customers; changes in our ability to successfully compete for and receive task orders and generate revenue under Indefinite Delivery/Indefinite Quantity (“IDIQ”) contracts; potential delays or changes in the government appropriations or procurement processes, including as a result of events such as war, incidents of terrorism, natural disasters, and public health concerns or epidemics, such as the recent coronavirus outbreak; the identified material weaknesses in our internal controls over financial reporting (including the timeline to remediate the material weaknesses); increased or unexpected costs or unanticipated delays caused by other factors outside of our control, such as performance failures of our subcontractors; the rollout of the business and the timing of expected business milestones; the effects of competition on our future business; our ability to obtain and access financing in the future; and other factor detailed below under “Risk Factors”

Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. In addition, statements that contain “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based on information available to us as of the date of this Annual Report on Form 10-K. While we believe that this information provides a reasonable basis for these statements, this information may be limited or incomplete. Our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all relevant information. These statements are inherently uncertain, and investors are cautioned not to unduly rely on these statements.

Some of these risks and uncertainties may in the future be amplified by the ongoing COVID-19 pandemic and there may be additional risks that we consider immaterial or which are unknown. It is not possible to predict or identify all such risks. Accordingly, undue reliance should not be placed upon the forward-looking statements. We do not undertake any obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

Item 1. Business

Company Overview

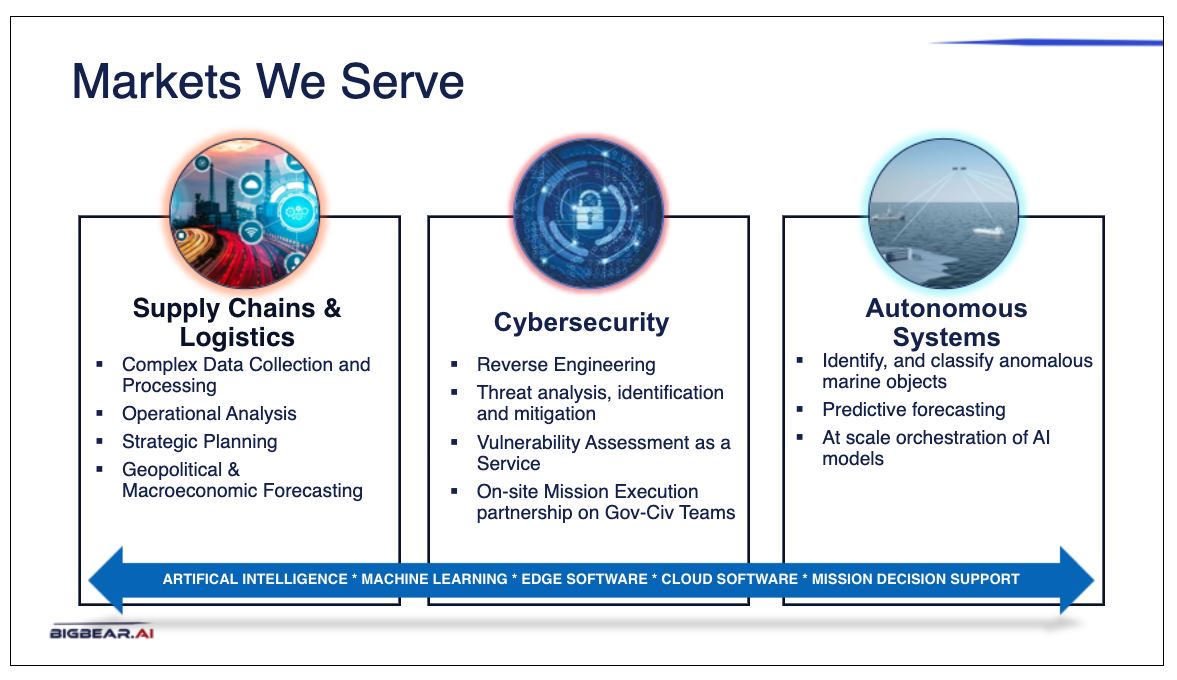

BigBear.ai Holdings, Inc.’s (“BigBear.ai” or the “Company”) mission is to help deliver clarity for our clients as they face their most complex decisions. BigBear.ai’s AI-powered decision intelligence solutions are leveraged across our Cyber & Engineering and Analytics business segments and in three primary markets—global supply chains & logistics, autonomous systems and cybersecurity. Our Cyber & Engineering segment provides high-end technology and management consulting services to our customers, focusing on cloud engineering and enterprise IT, cybersecurity, computer network operations and wireless, systems engineering, as well as strategy and program planning. Our Analytics segment provides high-end technology and consulting services to our customers, focusing on big data computing and analytical solutions, including predictive and prescriptive analytics solutions. BigBear.ai’s customers, including federal defense and intelligence agencies, manufacturers, third party logistics

1

providers, retailers, healthcare, and life sciences organizations, rely on BigBear.ai’s solutions to empower leaders to decide on the best possible course of action by creating order from complex data, identifying blind spots, and building predictive outcomes. We are a technology-led solutions organization, providing both software and services to our customers.

Solutions and Services

BigBear.ai is a leader in the use of Artificial Intelligence (AI) and Machine Learning (ML) for decision support. We provide our customers with a competitive advantage in a world driven by data that is growing exponentially in terms of volume, variety, and velocity. We believe data—when leveraged effectively—can be a strategic asset for any organization.

Through our supply chain & logistics, autonomous systems and cybersecurity solutions, we help our customers make sense of the world in which they operate, understand how known and previously unforeseen forces impact their operations, and determine which decision and course of action will best achieve their objectives. With all of our solutions, as needed by each customer, we offer specialized consulting services to design, customize, deploy, operate, and support our solutions for federal and commercial customers. Due to the breadth and depth of experience and expertise in our team, many of our customers rely on BigBear.ai resources to supplement their technical and operational staff for long-term engagements as well.

Supply Chains & Logistics Solutions

Our supply chain & logistics solutions include our Observe Data-as-a-Service (“DaaS”) solution, our ProModel discrete event simulator and our Dominate forecasting tool.

Observe DaaS—Data Conflation at Scale. Observe is a near-real time data collection and curation tool designed to collect and process enormous volumes of data from multiple domains, including BigBear.ai data collections, customer proprietary data, and third-party data, to create more holistic insights. Observe captures and distills data to identify relevant information, forming a more coherent and continuously updated view of the situations that matter to our customers anywhere across the globe. Our collections cover many subjects, including facilities, locations, news, events, social media, public communications, internet services and more. For situations that require a more customized solution, Observe collections can be used to enrich the customer’s proprietary data and analytics via modern, robust application programming interfaces (APIs). Our Observe DaaS solution is live in production, with over 25 sources, across more than 100 countries, and 140 million records processed daily.

ProModel Discrete Event Simulator—Course of Action Analysis & Digital Twin. ProModel is a robust discrete-event simulation technology that captures the behavior of complex interdependent processes and enables rapid course-of-action analysis through a “what if” user interface that allows customers to alter various parameters without changing the model directly. The ProModel

2

digital twin modeling platform is used to plan, design and improve new or existing manufacturing, logistics, business processes and other operational systems, and has been implemented in multiple vertical use cases including shipyard planning (Shipyard AI), patient flow optimization in hospitals (Future Flow) and complex portfolio management (Enterprise Portfolio Simulator). Because our Discrete Event Simulator is built and deployed as foundational technology, it can be tailored to many use cases for customers based on specific needs and embedded in existing platforms for an optimal user experience.

Dominate—Macroeconomic & Geopolitical Forecasting. Dominate is a decision support engine that provides customers goal-oriented advice to help them determine the right decision or course of action to best achieve their desired results. Using technology derived from our battlefield expertise, Dominate forecasts future outcomes based on different decision options, assigns a likelihood to each of those outcomes, and allows users to understand potential impacts for each of these decision options. Dominate is based on a resilient analytical architecture specifically designed to make sense of data sets that are periodically dirty, erroneous, or full of gaps. Customers can easily manipulate constraints or modify outcome goals through an interactive interface to quickly reveal the impacts of different decisions. Even in complex environments, Dominate helps customers reveal unexpected insights and develop innovative courses of action.

Cybersecurity Solutions

“BEARCLAW”—AI-Powered, Machine Accelerated Binary Analysis and SpaceCREST—Vulnerability Assessment & Monitoring, Digital Twin. Our cybersecurity offerings include our Binary Extraction Analysis Repository / Customizable Logic Automated Workflow (“BEARCLAW”) engine and the Space Cyber Resiliency through Evaluation and Security Testing (“SpaceCREST”) laboratory environment. Our BEARCLAW engine is a modular framework that incorporates AI/ML to assess vulnerabilities using automation and our data collections to conduct analysis on binaries and better, more quickly inform analysts to help them rapidly identify and/or respond to threats.

SpaceCREST is a laboratory environment designed to study and evaluate vulnerabilities of space assets in a cyber-physical system, develop cyber resiliency, and provide situational awareness and monitoring of those assets. The SpaceCREST initiative leverages Redwire Corporation’s digital engineering ecosystem, including its Hyperion Operational Space Simulation (“HOSS”) Lab and Advanced Configurable Open-system Research Network (“ACORN”) capabilities. Using HOSS and the ACORN platform, BigBear.ai develops tools and technologies to perform vulnerability research on space infrastructure hardware components, identify potential vulnerabilities that could compromise space systems, and provide tools and techniques that demonstrate how to mitigate and protect against the potential vulnerabilities identified. SpaceCREST’s digital twin helps operators rapidly identify when an attack or system failure is occurring. SpaceCREST also performs catastrophic testing without physically destroying the space asset or interrupting operations and our team of specialists then develops cyber security to mitigate the risk of cyber-attacks for our customers.

Our specialists also provide ongoing offensive and defensive cybersecurity analysis services to certain key customers and our mission operators often partner with government teams to contribute to missions for the intelligence community and the Department of Defense (the “DoD”).

Autonomous Systems Solutions

We are well positioned to address the need for scaled cyber-physical systems for complex customers in the federal government, and in the future, the private sector. Our autonomous systems solutions currently in use by the DoD provide geospatial tracking, anomaly detection, computer vision capabilities, and AI at the edge. By conflating millions of data points using AI/ML, our autonomous systems benefit from increased situational awareness, enable predictive forecasts, and can alert both analysts and decision-makers of potential threats. Analysts can combine data sets, including traditional and nontraditional sources, including social media, traditional news media and event data (e.g., GDELT), SIGINT (e.g., X-band, Lband, AIS), SAR, weather and enterprise data sources, to improve situational awareness. Currently, our algorithms run against a myriad of sensors in a maritime environment to support forces who may be operating in disadvantaged or disconnected environments. We believe that this can be leveraged in ground, space, and air combat force contexts in the future.

Research & Development

Our team has more than 20 years of combined experience developing and deploying software products. Historically, much of our research and development has been funded and directed by defense and intelligence customers for their specific needs and objectives. In 2022, we increased hiring and headcount in our innovations lab as well as investment in various research projects aimed at continuing to develop and refine our solutions, including enhancing features and functionality, adding new modules, and improving the application of the latest AI/ML technologies in the solutions we deliver to our customers.

3

One area of our research and development efforts has focused on contributing to the Joint All-Domain Command and Control (“JADC2”)—the DoD’s strategy to connect sensors globally from all branches of the armed forces into a unified network, powered by AI. JADC2 is one of the Pentagon’s top priorities, and we are aiming to play a major role in the realization of this concept by delivering the operating system for its delivery.

Customers

BigBear.ai’s customers include U.S. defense and intelligence agencies, manufacturing, distribution and logistics, healthcare and life sciences. To date, BigBear.ai has predominantly served federal, military, and intelligence agencies of the U.S. government. We are proud of the trusted, multi-decade relationships we have with several U.S. defense and intelligence agencies, including the Joint Staff, U.S. Army, U.S. Air Force, and Department of Homeland Security (“DHS”). These customers entrust us with their most critical data and operations and represent most of our historical growth.

Our capabilities are also used extensively by the private sector, with hundreds of complex manufacturing, retail, and logistics clients. Our process simulation and modeling solutions help companies manage massive and complex physical and information environments and gain clarity on facility, equipment and personnel systems, forecasting requirements, and simulating real-world situations.

We are continuing to grow our customer base in our three markets: supply chains & logistics, cybersecurity, and autonomous systems. This is a focus area for us in 2023 as we find ways to apply our existing technology to new use cases and meet growing customer demand. As new use cases are onboarded, we expand our capabilities by adding new data sources, analysis tools, and integrated services to our platform to support new industries and decision scenarios. Thus, every new engagement expands our capability baseline and opens the door to a pipeline of new opportunities within that market and within adjacent markets.

Revenue Mix

We derive a significant portion of our revenue from contracts with the federal government and government agencies. Due to the sensitive and oftentimes classified nature of our work with these customers, a significant portion of BigBear.ai’s contracts still require our data scientists and software engineers to co-locate on-premises to tailor our solutions for these unique environments and use cases. However, as we have continued to amass knowledge and intellectual property (“IP”), our proprietary products now require less customization, and our pipeline has begun to reflect our customers’ desire to more rapidly integrate our capabilities into their current operating environments.

Competitive Advantage

BigBear.ai’s principle competitive advantage is that we are an organization built on a culture of recruiting and retaining talent that we believe attracts the brightest talent in the industry. BigBear.ai is made up of hundreds of employees with domain expertise and hands-on experience in the environments that we build and deliver solutions for. We are focused on creating technology that solves real customer problems, and our team is a critical part of understanding the challenges our customers face.

Additionally, BigBear.ai has been a trusted partner to federal, military, and intelligence agencies of the U.S. government for decades—we take that trust seriously and we work every day to keep it. Because of our history in complex systems integration and AI orchestration, we are well positioned to support the current wave of excitement regarding artificial intelligence, as key decision makers and leaders across government and industry are recognizing the necessity of at-scale, production-grade augmented decision intelligence. Specifically, we believe we are well positioned because of our team’s ability to deploy innovative solutions quickly, offering our customer’s competitive pricing and robust support while leveraging our track record of success in complex environments.

Market Opportunity

BigBear.ai serves multiple large, diverse and rapidly growing addressable markets, delivering AI/ML-powered solutions in supply chains & logistics, cybersecurity, and autonomous systems. Our suite of technology solutions and expertise allows us to target a total addressable market (“TAM”) of more than $68 billion, growing to $315 billion by 2028, based upon third-party industry reports on the current and projected markets for government and commercial customers in the following areas: AI in logistics and supply chain, military AI and autonomous systems, AI orchestration, digital twins, AI in computer vision, and cybersecurity.

4

Growth Strategy

BigBear.ai has multiple growth tactics, including performing on our existing backlog of approximately $222 million as of December 31, 2022, adding new customers, expanding relationships with existing customers, and scaling our direct and indirect sales channels. Given the continued uncertainty in the global economy associated with macroeconomic and geopolitical conditions, we believe in a diversified growth strategy and are actively pursuing multiple plays in each area.

Company Footprint and Management

As of December 31, 2022, we had 649 employees, the vast majority of which hold an active security clearance. Approximately 46% of our workforce is comprised of software engineers, data scientists, cloud/systems engineers, analysts, and cyber subject-matter experts.

BigBear.ai has headquarters in Columbia, MD, with additional office locations in Ann Arbor Michigan; Chantilly, Virginia and Charlottesville, Virginia. In addition, many of our team members work at secure customer facilities across the U.S.

The BigBear.ai executive team is a driving force behind the company’s success. With strong industry experience and knowledge of both government and commercial markets, our diverse executives are shaping the Company’s vision and market penetration strategies, while ensuring operational excellence. Further, the leadership team is committed to maintaining a corporate culture and employee value proposition that attracts and retains the brightest talent in the industry.

Competition

Our competitors include software companies that develop horizontal solutions in the supply chain & logistics, cybersecurity and autonomous systems markets, as well as vertically focused analytics tools within our target markets. We also face competition from government contractors and system integrators who are building custom solutions to enter this market. In many cases, we are competing with the internal software development efforts of our potential customers. Organizations frequently attempt to build their own decision support and analytics platforms using a patchwork of custom development, outside consultants, IT services companies, packaged and open-source software, and significant internal IT resources, before turning to BigBear.ai.

The principal competitive factors in the markets in which we operate include:

•platform agility and product functionality

•data security, privacy, and regulatory compliance

•ease and speed of adoption, use, and deployment

•product innovation and roadmap

•pricing and cost structures

•customer experience, including technical support and education

•brand awareness and reputation

•track record of success in complex environments

While we compete favorably on these factors, some of our competitors have greater name recognition, longer operating histories, broader customer bases, larger sales and marketing budgets, more technology, channel, and distribution partners, wider geographic presence, greater focus in specific vertical markets, lower labor and research and development costs, larger and more mature intellectual property portfolios, and substantially greater financial, technical, and other resources to provide support, make acquisitions, and develop and introduce new products.

Seasonality

We generally experience seasonality in the timing of recognition of revenue as a result of the timing of the execution of our contracts, as we have historically executed many of our contracts in the third and fourth quarters due to the fiscal year ends and procurement cycles of our customers. See “Risk Factors—Risks Related to Our Business and Industry—Our sales efforts involve considerable time and expense and our sales cycle is often long and unpredictable” and “Risk Factors—Risks Related to Our Business and Industry—Our results of operations and our key business measures are likely to fluctuate significantly on a quarterly basis in future periods and may not fully reflect the underlying performance of our business, which makes our future results difficult to predict and could cause our results of operations to fall below expectations.” Additionally, recurring delays in the federal government’s budgeting process can adversely affect the award of new contracts or growth on existing contracts during continuing resolutions.

5

Regulatory

Our business activities are subject to various federal, state, local, and foreign laws, rules, and regulations. Compliance with these laws, rules, and regulations has not had, and is not expected to have, a material effect on our capital expenditures, results of operations and competitive position as compared to prior periods. Nevertheless, compliance with existing or future governmental regulations, including, but not limited to, those pertaining to global trade, consumer and data protection, and taxes, could have a material impact on our business in subsequent periods.

For more information on the potential impacts of government regulations affecting our business, see the section titled “Risk Factors” contained in this Annual Report on Form 10-K

Intellectual Property

We believe that our intellectual property rights are valuable and important to our business. We rely on a combination of patents, copyrights, trademarks, trade secrets, know-how, contractual provisions, and confidentiality procedures to protect our intellectual property rights.

We seek to protect our proprietary inventions relevant to our business through patent protection in the United States and abroad; however, we are not dependent on any particular patent or application for the operation of our business. In addition to the protection provided by our intellectual property rights, we enter into proprietary information and invention assignment agreements or similar agreements with our employees, consultants, and contractors. We further control the use of our proprietary technology and intellectual property rights through provisions in our agreements with customers.

Legal Proceedings

We are subject to litigation, claims, investigations and audits arising from time to time in the ordinary course of business. Although legal proceedings are inherently unpredictable, we believe that we have valid defenses with respect to any matters currently pending against us and we intend to vigorously defend against such matters. The outcome of these matters, individually and in the aggregate, is not expected to have a material impact on our consolidated balance sheets, statements of operations or cash flows.

Human Capital

Our employees are critical to the success of our business. As of December 31, 2022, we had 649 full-time employees, substantially all of which are employed in the United States. We also engage part-time employees, independent contractors, and third-party personnel to supplement our workforce.

None of our employees is represented by a labor union. We have not experienced any work stoppages due to employee disputes, and we believe that our employee relations are strong.

Our human capital resources objectives include recruiting, retaining, training, and motivating our personnel. The principal purposes of our incentive compensation policies are to attract, retain, and reward personnel through the granting of equity-based and cash-based compensation awards, in order to increase stockholder value and the success of our company by motivating such individuals to perform to the best of their ability and achieve our objectives. We strive to foster a diverse and inclusive culture and environment that encourages active dialogue and robust engagement on the issues most salient to employee satisfaction and believe our employees are empowered to play a significant role in shaping the direction and success of the company.

Item 1A. Risk Factors

You should carefully review and consider the following risk factors and the other information contained in this Annual Report on Form 10-K, including the audited consolidated financial statements and notes to the consolidated financial statements included herein.

These risk factors are not exhaustive. You should carefully consider the following risk factors in addition to the other information included in this Annual Report on Form 10-K, including matters addressed in the section entitled “Cautionary Note Regarding Forward-Looking Statements.” The Company may face additional risks and uncertainties that are not presently known to it, or that BigBear.ai currently deems immaterial, which may also impair the Company’s business or financial condition.

6

The following discussion should be read in conjunction with the audited consolidated financial statements and notes to those financial statements included herein. Additional risks, beyond those summarized below may apply to our activities or operations as currently conducted or as we may conduct them in the future or in the markets in which we operate or may in the future operate. Consistent with the foregoing, we are exposed to a variety of risks, including risks associated with:

•a significant portion of our business being dependent on sales to the public/government sector, including the risk that we may not receive or maintain government contracts or may not receive the full benefit of such contracts;

•our limited operating history as a combined company, which makes it difficult to evaluate our current business and future prospects;

•our ability to sustain our revenue growth in the future;

•our ability to execute our strategy to grow our business and increase our sales and the number and types of markets we compete in;

•the length of our sales cycle and the time and expense associated with it;

•our ability to grow our customer base and to expand our relationships with our existing customers, including with our government customers;

•our reliance on customers in the public/government sector;

•the market and our customers accepting and adopting our products, including future new product offerings;

•the impact of health epidemics, including the COVID-19 pandemic, on our business, financial condition, growth and the actions we may take in response thereto;

•competition in our industry;

•our ability to gain contracts on favorable terms, including with our government customers;

•our ability to grow, maintain and enhance our brand and reputation;

•risks related to security and our technology, including cybersecurity;

•our ability to maintain competitive pricing for our products;

•our ability to secure financing necessary to operate and grow our business as planned, including through acquisitions;

•the high degree of uncertainty of the level of demand for, and market utilization of, our solutions and products;

•our estimates and projections may prove to be inaccurate and certain of our assets may be at risk of future impairment;

•substantial regulation and the potential for unfavorable changes to, or failure by us to comply with, these regulations, which could substantially harm our business and operating results;

•our dependency upon third-party service providers for certain technologies;

•increases in costs, disruption of supply or shortage of materials, which could harm our business;

•developments and projections relating to our competitors and industry;

•the unavailability, reduction or elimination of government and economic incentives, which could have a material adverse effect on our business, prospects, financial condition and operating results;

•our existing debt and our ability to refinance it on more favorable terms;

•our management team’s limited experience managing a public company;

•our ability to hire, retain, train and motivate qualified personnel and senior management and ability to deploy our personnel and resources to meet customer demand;

•our ability to successfully execute future joint ventures, channel sales relationships, platform partnerships, strategic

7

alliances and subcontracting opportunities;

•our ability to grow through acquisitions and successfully integrate any such acquisitions;

•our ability to successfully maintain, protect, enforce and grow our intellectual property rights;

•our compliance with governmental laws, trade controls, customs requirements and other regulations we are subject to;

•the possibility of our need to defend ourselves against fines, penalties and injunctions if we are determined to be promoting products for unapproved uses or otherwise found to have violated a law or regulation;

•concentration of ownership among our existing executive officers, directors and their respective affiliates, which may prevent new investors from influencing significant corporate decisions;

•the effect of economic downturns, depressions and recessions;

•the benefits of the Business Combination not being achieved or meeting the expectations of investors or securities;

•our significant increased expenses and administrative burdens as a public company;

•the volatility of the market for our securities, including our common stock;

•our ability to satisfy the continued listing requirements of the NYSE in the future;

•our internal controls over financial reporting, including our current material weaknesses and any potential future material weaknesses; and

•other factors detailed below.

Risks Related to Our Business and Industry

We have a limited operating history, which makes it difficult to evaluate our prospects and future results of operations.

Since we commenced operations, our business has expanded organically through the delivery of enhanced solutions and expanded product offerings to our customers and through acquisitions. As a result of our limited operating history and evolving business, our ability to forecast our future results of operations is limited and subject to several uncertainties, including our ability to plan for and model future growth. Our historical revenue growth should not be considered indicative of our future performance. Further, in future periods, our revenue growth could slow. We have encountered and will encounter risks and uncertainties frequently experienced by growing companies in rapidly changing industries, such as the risks and uncertainties described herein. If our assumptions regarding these risks and uncertainties, which we use to plan our business, are incorrect or change, or if we do not address these risks successfully, our business could be adversely affected.

We may not be able to sustain our revenue growth rate in the future.

Although our revenue has increased in recent periods, there can be no assurances that revenue will continue to grow or do so at current rates, and you should not rely on the revenue of any prior quarterly or annual period as an indication of our future performance. Our revenue growth rate may decline in future periods. Many factors may contribute to declines in our revenue growth rate, including increased competition, slowing demand for our products and services from existing and new customers, a failure by us to continue capitalizing on growth opportunities including expansion into the commercial marketplace, strategic acquisitions, terminations of existing contracts or failure to exercise existing options by our customers, our failure to execute on the existing backlog of customer contracts, the maturation of our business, and a contraction of our overall market, among others. If our revenue growth rate declines, our business, financial condition, and results of operations could be adversely affected.

Our results of operations and cash flows are substantially affected by our mix of fixed-price and time-and-material type contracts. Our profits may decrease and/or we may incur significant unanticipated costs if we do not accurately estimate the costs of these engagements.

We generate most of our revenue through various time-and-material and fixed-price contracts. Some of our arrangements with our customers are on fixed-price contracts, rather than contracts in which payment to us is determined on a time and materials or other basis. These fixed-price contracts allow us to benefit from cost savings, but subject us to the risk of potential cost overruns, particularly for firm fixed-price contracts because we assume all of the cost burden. If our initial estimates are incorrect, we can lose money on these contracts. U.S. government contracts can expose us to potentially large losses because the U.S. government

8

can hold us responsible for completing a project or, in certain circumstances, require us to pay the entire cost of its replacement by another provider regardless of the size or foreseeability of any cost overruns that occur over the life of the contract. Because many of these contracts involve new technologies and applications and can last for years, unforeseen events, such as technological difficulties, fluctuations in the price of raw materials, a significant increase in inflation in the U.S. or other countries, problems with our suppliers and cost overruns, can result in the contractual price becoming less favorable or even unprofitable to us over time. Our failure to estimate accurately the resources and schedule required for a project, or our failure to complete our contractual obligations in a manner consistent with the project plan upon which our fixed-price contract was based, could adversely affect our overall profitability and could have a material adverse effect on our business, financial condition, and results of operations. We are consistently entering into contracts for large projects that magnify this risk. We have been required to commit unanticipated additional resources to complete projects in the past, which has occasionally resulted in losses on those contracts. We could experience similar situations in the future. In addition, we may fix the price for some projects at an early stage of the project engagement, which could result in a fixed price that is too low. Therefore, any changes from our original estimates could adversely affect our business, financial condition, and results of operations.

Our sales efforts involve considerable time and expense and our sales cycle is often long and unpredictable.

Our results of operations may fluctuate, in part, because of the intensive nature of our sales efforts and the length and unpredictability of our sales cycle. As part of our sales efforts, we invest considerable time and expense evaluating the specific organizational needs of our potential customers and educating these potential customers about the technical capabilities and value of our products and services. In the “land” phase of our business model, we often deploy prototype capabilities to potential customers at no or minimal cost initially to them for evaluation purposes, and there is no guarantee that we will be able to convert these engagements into long-term sales arrangements. In addition, we currently have a limited direct sales force, and our sales efforts have historically depended on the significant involvement of our senior management team. The length of our sales cycle, from initial demonstration to sale of our products and services, tends to be long and varies substantially from customer to customer. Our sales cycle often lasts six to nine months but can extend to a year or more for some customers. Because decisions to purchase our software involve significant financial commitments, potential customers generally evaluate our software at multiple levels within their organization, each of which often have specific requirements, and typically involve their senior management.

Our results of operations depend on sales to enterprise customers, which make product purchasing decisions based in part or entirely on factors, or perceived factors, not directly related to the features of the software, including, among others, that customer’s projections of business growth, uncertainty about economic conditions (including as a result of the ongoing COVID-19 outbreak and the escalation of hostilities between Russia and Ukraine), capital budgets, anticipated cost savings from the implementation of our software, potential preference for such customer’s internally-developed software solutions, perceptions about our business and software, more favorable terms offered by potential competitors, and previous technology investments. In addition, certain decision makers and other stakeholders within our potential customers tend to have vested interests in the continued use of internally developed or existing software, which may make it more difficult for us to sell our software and services. As a result of these and other factors, our sales efforts typically require an extensive effort throughout a customer’s organization, a significant investment of human resources, expense and time, including by our senior management, and there can be no assurances that we will be successful in making a sale to a potential customer. If our sales efforts to a potential customer do not result in sufficient revenue to justify our investments, our business, financial condition, and results of operations could be adversely affected.

Historically, existing customers have expanded their relationships with us, which has resulted in a limited number of customers accounting for a substantial portion of our revenue. If existing customers do not make subsequent purchases from us or renew their contracts with us, if those renewals are otherwise delayed, or if our relationships with our largest customers are impaired or terminated, our revenue could decline, and our results of operations would be adversely impacted.

We derive a significant portion of our revenue from existing customers that expand their relationships with us. Increasing the size and number of the deployments of our existing customers is a major part of our growth strategy. We may not be effective in executing this or any other aspect of our growth strategy. For example, revenue earned from customers contributing in excess of 10% of consolidated revenues were derived from three customers comprising 49% of revenue for the twelve months ended December 31, 2022 (Successor). As of December 31, 2022, we have supported these customers for more than five years.

Each of our contracts with these customers includes termination for convenience provisions whereby the customer can unilaterally elect to terminate the contract. In the event of a termination, we may generally recover only our incurred or committed costs and settlement expenses and profit on work completed prior to the termination. Our 2022 revenues from these significant customers were mainly earned from large multi-year contracts. As of December 31, 2022, about $118 million of our approximate $218

9

million of total backlog is attributable to these significant customers. The estimated completion dates for these contracts range from 2023 to 2026. Of the $118 million of backlog related to these significant customers as of December 31, 2022 we expect to recognize approximately 20% of that amount as revenue by the end of 2023, with the remainder to be recognized as revenue by the end of 2026.

There are inherent risks whenever a large percentage of total revenues are concentrated with a limited number of customers. Our concentration of revenue among a few of our customers increases the risk of quarterly fluctuations in our operating results and our sensitivity to any material, adverse developments experienced by our significant customers. Further, it is not possible for us to predict the future level of demand for our products and services that will be generated by these customers. As previously described, the terms of our contracts with these significant customers permit them to unilaterally terminate our arrangement at any time (subject to notice and certain other provisions). In addition, the terms and conditions under which we do business generally do not include commitments by those customers to purchase any specific quantities of products or services from us or to renew their contracts after the initial period. Even in those instances where we enter into an arrangement under which a significant customer agrees to purchase an agreed portion of its product or service needs from us (provided we meet our contractual obligations), the arrangement often includes pricing schedules with substantial price concessions that may apply regardless of the volume of products or services purchased, and those material customers may not purchase the volume of products or services we expect. If any of these major customers experience declining or delayed sales due to market, economic or competitive conditions, we could be pressured to reduce the prices we charge for our products and services or we could lose the customer. Any such development could have an adverse effect on our margins and financial position, and would negatively affect our sales and results of operations and/or trading price of our common stock. There can be no assurance that our sales will not continue to be sufficiently concentrated among a limited number of customers.

Certain customers, including customers that represent a significant portion of our business, have in the past reduced their spend with us as a result of budgetary pressure, which has reduced our anticipated future payments or revenue from these customers. It is not possible for us to predict the future level of demand from our larger customers for our software and applications.

While we generally engage customers through contracts with terms up to five years in length, our customers sometimes enter into shorter-term contracts, such as six-month engagements for specific capability developments or enhancements, which may not provide for automatic renewal and may require the customer to opt-in to extend the term. Our customers have no obligation to renew, upgrade, or expand their agreements with us after the terms of their existing agreements have expired. In addition, many of our customer contracts permit the customer to terminate their contracts with us with little or no notice required. If one or more of our customers terminate their contracts with us, whether for convenience, for default in the event of a breach by us, or for other reasons specified in our contracts, as applicable; if our customers elect not to renew their contracts with us; if our customers renew their contractual arrangements with us for shorter contract lengths or for a reduced scope; or if our customers otherwise seek to renegotiate terms of their existing agreements on terms less favorable to us, our business and results of operations could be adversely affected. This adverse impact would be even more pronounced for customers that represent a material portion of our revenue or business operations.

Our ability to renew or expand our customer relationships may decrease or vary due to a number of factors, including our customers’ satisfaction or dissatisfaction with our software and services, the frequency and severity of software and implementation errors, our software’s reliability, our pricing, the effects of general economic conditions and budgets, competitive offerings or alternatives, or reductions in our customers’ spending levels. Achieving such renewal or expansion of our customer contracts may require us to increasingly engage in sophisticated and costly sales efforts that may not result in additional sales. If our customers do not renew or expand their agreements with us or if they renew their contracts for shorter lengths or on other terms less favorable to us, our revenue may decline or grow more slowly than expected, and our business could suffer. Additionally, if the contract awards process for our government customers is delayed due to budgetary constraints, political instability or other governmental delays in the awards process, expected revenues could be delayed, which could have a material adverse effect on our business. Our business, financial condition, and results of operations would also be adversely affected if we face difficulty collecting our accounts receivable from our customers or if we are required to refund customer deposits.

We may not realize the full deal value of our customer contracts, which may result in lower than expected revenue.

As of December 31, 2022 and December 31, 2021, the total remaining deal value of the contracts that we had been awarded by, or entered into with, commercial and government customers, including existing contractual obligations and contract options available to those customers was approximately $218 million and $322 million, respectively.

The majority of these contracts contain termination for convenience provisions. Additionally, the U.S. federal government is prohibited from exercising contract options more than one year in advance. As a result, there can be no guarantee that our

10

customer contracts will not be terminated or that contract options will be exercised.

We may not realize all of the revenue from the full deal value of our customer contracts. This is because the actual timing and amount of revenue under contracts included are subject to various contingencies, including exercise of contractual options, customers terminating their contracts, and renegotiations of contracts. For example, the U.S. Federal government has increasingly relied upon multi-year contracts with pre-established terms and conditions, such as IDIQ contracts, which generally require those contractors who have previously been awarded the IDIQ to engage in an additional competitive bidding process before a task order is issued. In addition, delays in the completion of the U.S. government’s budgeting process, the use of continuing resolutions, and a potential lapse in appropriations, or similar events in other jurisdictions, could adversely affect our ability to timely recognize revenue under certain government contracts.

Our results of operations and our key business measures are likely to fluctuate significantly on a quarterly basis in future periods and may not fully reflect the underlying performance of our business, which makes our future results difficult to predict and could cause our results of operations to fall below expectations.

Our quarterly results of operations, including cash flows, have fluctuated significantly in the past and are likely to continue to do so in the future. Accordingly, the results of any one quarter should not be relied upon as an indication of future performance. Our quarterly results, financial position, and operations are likely to fluctuate as a result of a variety of factors, many of which are outside of our control, and as a result, may not fully reflect the underlying performance of our business. Fluctuation in quarterly results may negatively impact the value of our common stock.

The timing of our sales cycles is unpredictable and is impacted by factors such as government budgeting and appropriation cycles, varying commercial fiscal years, and changing economic conditions. This can impact our ability to plan and manage margins and cash flows. Our sales cycles are often long, and it is difficult to predict exactly when, or if, we will make a sale with a potential customer or how quickly we can move them from the “land” phase into the profitable “expand” phase. As a result, large individual sales have, in some cases, occurred in quarters subsequent to those we anticipated, or have not occurred at all. The loss or delay of one or more large sales transactions in a quarter would impact our results of operations and cash flow for that quarter and any future quarters in which revenue from that transaction is lost or delayed. In addition, downturns in new sales may not be immediately reflected in our revenue because we generally recognize revenue over the term of our contracts. The timing of customer billing and payment varies from contract to contract. A delay in the timing of receipt of such collections, or a default on a large contract, may negatively impact our liquidity for the period and in the future. Because a substantial portion of our expenses are relatively fixed in the short-term and require time to adjust, our results of operations and liquidity would suffer if revenue falls below our expectations in a particular period.

Other factors that may cause fluctuations in our quarterly results of operations and financial position include, without limitation, those listed below:

•the success of our sales and marketing efforts, including the success of pilot deployments;

•our ability to increase our margins;

•the timing of expenses and revenue recognition;

•the timing and amount of payments received from our customers;

•termination of one or more large contracts by customers, including for convenience;

•the time and cost-intensive nature of our sales efforts and the length and variability of sales cycles;

•the amount and timing of operating expenses related to the maintenance and expansion of our business and operations;

•the timing and effectiveness of new sales and marketing initiatives;

•changes in our pricing policies or those of our competitors;

•the timing and success of new products, features, and functionality introduced by us or our competitors;

11

•cyberattacks and other actual or perceived data or security breaches;

•our ability to hire and retain employees, in particular, those responsible for the development, operations and maintenance, and selling or marketing of our software; and our ability to develop and retain talented sales personnel who are able to achieve desired productivity levels in a reasonable period of time and provide sales leadership in areas in which we are expanding our sales and marketing efforts;

•the amount and timing of our stock-based compensation expenses;

•changes in the way we organize and compensate our sales teams;

•changes in the way we operate and maintain our software;

•changes in the competitive dynamics of our industry;

•the cost of and potential outcomes of future claims or litigation, which could have a material adverse effect on our business;

•changes in laws and regulations that impact our business, such as the Federal Acquisition Streamlining Act of 1994 (“FASA”);

•indemnification payments to our customers or other third parties;

•ability to scale our business with increasing demands;

•the timing of expenses related to any future acquisitions; and

•general economic, regulatory, and market conditions, including the impact of the COVID-19 pandemic and international affairs such as the escalation of hostilities between Russia and Ukraine which may cause financial market volatility.

In addition, our contracts generally contain termination for convenience provisions, and we may be obligated to repay prepaid amounts or otherwise not realize anticipated future revenue should we fail to provide future services as anticipated. These factors make it difficult for us to accurately predict financial metrics for future periods.

The variability and unpredictability of our quarterly results of operations, cash flows, or other operating metrics could result in our failure to meet our expectations or those of analysts that may cover us or investors with respect to revenue or other key metrics for a particular period. If we fail to meet or exceed such expectations for these or any other reasons, the trading price of our common stock could fall, and we could face costly lawsuits, including securities class action suits.

Our software is complex and may have a lengthy implementation process, and any failure of our software to satisfy our customers or perform as desired could harm our business, results of operations, and financial condition.

Our software and services are complex and are deployed in a wide variety of environments. Implementing our software can be a complex and lengthy process since we often configure our existing software for a customer’s unique environment. Inability to meet the unique needs of our customers may result in customer dissatisfaction and/or damage to our reputation, which could materially harm our business. Further, the proper use of our software may require training of the customer and the initial or ongoing services of our technical personnel over the contract term. If training and/or ongoing services require more of our expenditures than we originally estimated, our margins will be lower than projected.

In addition, if our customers do not use our software correctly or as intended, inadequate performance or outcomes may result. It is possible that our software may also be intentionally misused or abused by customers or their employees or third parties who obtain access and use of our software. Similarly, our software is sometimes used by customers with smaller or less sophisticated IT departments, potentially resulting in sub-optimal performance at a level lower than anticipated by the customer. Because our customers rely on our software and services to address important business goals and challenges, the incorrect or improper use or configuration of our software, failure to properly train customers on how to efficiently and effectively use our software, or failure to properly provide implementation or analytical or maintenance services to our customers may result in contract terminations or non-renewals, reduced customer payments, negative publicity, or legal claims against us. For example, as we continue to expand

12

our customer base, any failure by us to properly provide these services may result in lost opportunities for follow-on expansion sales of our software and services.

Furthermore, if customer personnel are not well trained in the use of our software, customers may defer the deployment of our software and services, may deploy them in a more limited manner than originally anticipated, or may not deploy them at all. If there is substantial turnover of the company or customer personnel responsible for procurement and use of our software, our software may go unused or be adopted less broadly, and our ability to make additional sales may be substantially limited, which could negatively impact our business, results of operations, and growth prospects.

If we do not successfully develop and deploy new technologies to address the needs of our customers, our business and results of operations could suffer.

Our success has been based on our ability to design software that enables the integration of large amounts of data to facilitate advanced data analysis, knowledge management, and decision support in real-time. We spend substantial amounts of time and money researching and developing new technologies and enhanced versions of existing features to meet our customers’ and potential customers’ rapidly evolving needs. There is no assurance that our enhancements to our software or our new product features, capabilities, or offerings, including new product modules, will be compelling to our customers or gain market acceptance. If our research and development investments do not accurately anticipate customer demand or if we fail to develop our software in a manner that satisfies customer preferences in a timely and cost-effective manner, we may fail to retain our existing customers or increase demand for our software.

The introduction of new products and services by competitors or the development of entirely new technologies to replace existing offerings could make our software obsolete or adversely affect our business, financial condition, and results of operations. We may experience difficulties with software development, design, or marketing that delay or prevent our development, introduction, or implementation of new software, features, or capabilities. We have in the past experienced delays in our internally planned release dates of new features and capabilities, and there can be no assurance that new software, features, or capabilities will be released according to schedule. Any delays could result in adverse publicity, loss of revenue or market acceptance, or claims by customers brought against us, any of which could harm our business. Moreover, the design and development of new software or new features and capabilities to our existing software may require substantial investment, and we have no assurance that such investments will be successful. If customers do not widely adopt our new software, experiences, features, and capabilities, we may not be able to realize a return on our investment and our business, financial condition, and results of operations may be adversely affected.

Our new and existing software and changes to our existing software could fail to attain sufficient market acceptance for many reasons, including:

•our failure to predict market demand accurately in terms of product functionality and to supply offerings that meet this demand in a timely fashion;

•product defects, errors, or failures or our inability to satisfy customer service level requirements;

•negative publicity or negative private statements about the security, performance, or effectiveness of our software or product enhancements;

•delays in releasing to the market our new offerings or enhancements to our existing offerings, including new product modules;

•introduction or anticipated introduction of competing software or functionalities by our competitors;

•inability of our software or product enhancements to scale and perform to meet customer demands;

•receiving qualified or adverse opinions in connection with security or penetration testing, certifications or audits, such as those related to IT controls and security standards and frameworks or compliance;

•poor business conditions for our customers, causing them to delay software purchases;

•reluctance of customers to purchase proprietary software products;

13

•reluctance of our customers to purchase products hosted by our vendors and/or service interruption from such providers; and

•reluctance of customers to purchase products incorporating open source software.

If we are not able to continue to identify challenges faced by our customers and develop, license, or acquire new features and capabilities to our software in a timely and cost-effective manner, or if such enhancements do not achieve market acceptance, our business, financial condition, results of operations, and prospects may suffer and our anticipated revenue growth may not be achieved.

Because we derive, and expect to continue to derive, a substantial percentage of our revenue from customers purchasing our software, market acceptance of these products, and any enhancements or changes thereto, is critical to our success.

The competitive position of our software depends in part on its ability to operate with third-party products and services, and if we are not successful in maintaining and expanding the compatibility of our software with such third-party products and services, our business, financial condition, and results of operations could be adversely impacted.

The competitive position of our software depends in part on its ability to operate with products and services of third parties, software services, and infrastructure, including but not limited to, in connection with our joint ventures, channel sales relationships, platform partnerships, strategic alliances, and other similar arrangements where applicable. As such, we must continuously modify and enhance our software to adapt to changes in, or to be integrated or otherwise compatible with, hardware, software, networking, browser, and database technologies. In the future, one or more technology companies may choose not to support the operation of their hardware, software, or infrastructure, or our software may not support the capabilities needed to operate with such hardware, software, or infrastructure. In addition, to the extent that a third-party were to develop software or services that compete with ours, that provider may choose not to support one or more of our offerings. We intend to facilitate the compatibility of our software with various third-party hardware, software, and infrastructure by maintaining and expanding our business and technical relationships. If we are not successful in achieving this goal, our business, financial condition, and results of operations could be adversely impacted.

If we fail to manage future growth effectively, our business could be harmed.

Since our founding, we have experienced rapid growth. We operate in a growing market and have experienced, and may continue to experience, significant expansion of our operations. This growth has placed, and may continue to place, a strain on our employees, management systems, operational, financial, and other resources. As we have grown, we have increasingly managed larger and more complex deployments of our software and services with a broader base of government and commercial customers. As we continue to grow, we face challenges of integrating, developing, retaining, and motivating a rapidly growing employee base. In the event of continued growth of our operations, our operational resources, including our information technology systems, our employee base, or our internal controls and procedures may not be adequate to support our operations and deployments. Managing our growth may require significant expenditures and allocation of valuable management resources, improving our operational, financial, and management processes and systems, and effectively expanding, training, and managing our employee base. If we fail to achieve the necessary level of efficiency in our organization as it grows, our business, financial condition, and results of operations would be harmed. As our organization continues to grow, we may find it increasingly difficult to maintain the benefits of our traditional company culture, including our ability to quickly respond to customers, and avoid unnecessary delays that may be associated with a formal corporate structure. This could negatively affect our business performance or ability to hire or retain personnel in the near or long-term.

In addition, our rapid growth may make it difficult to evaluate our future prospects. Our ability to forecast our future results of operations is subject to a number of uncertainties, including our ability to effectively plan for and model future growth. We have encountered in the past, and may encounter in the future, risks and uncertainties frequently experienced by growing companies in rapidly changing industries. If we fail to achieve the necessary level of efficiency in our organization as it grows, or if we are not able to accurately forecast future growth, our business, financial condition, and results of operations would be harmed.

If we are unable to hire, retain, train, and motivate qualified personnel and senior management and deploy our personnel and resources to meet customer demand around the world, our business could suffer.

Our ability to compete in the highly competitive technology industry depends upon our ability to attract, motivate, and retain qualified personnel. We are highly dependent on the continued contributions of our management team, including their customer relationships, expertise in science and technology, business development experience, and innovative management in both public

14

and private sectors. These contributions are integral to our growth and would be difficult to replace. Some of our executive officers and key personnel are at-will employees and may terminate their employment relationship with us at any time. The loss of the services of our key personnel and any of our other executive officers, and our inability to find suitable replacements, could result in a decline in sales, delays in product development, and harm to our business and operations.

At times, we have experienced, and we may continue to experience, difficulty in hiring and retaining personnel with appropriate qualifications, and we may not be able to fill positions in a timely manner or at all. Potential candidates may not perceive our compensation package, including our equity awards, as favorably as personnel hired prior to our listing. In addition, our recruiting personnel, methodology, and approach may need to be altered to address a changing candidate pool and profile. We may not be able to identify or implement such changes in a timely manner. In addition, we may incur significant costs to attract and recruit skilled personnel, and we may lose new personnel to our competitors or other technology companies before we realize the benefit of our investment in recruiting and training them. As we move into new geographies, we will need to attract and recruit skilled personnel in those geographic areas, but it may be challenging for us to compete with traditional local employers in these regions for talent. If we fail to attract new personnel or fail to retain and motivate our current personnel who can meet our growing technical, operational, and managerial requirements on a timely basis or at all, our business may be harmed. In addition, certain personnel may be required to receive various security clearances and substantial training to work on certain customer engagements or to perform certain tasks. Necessary security clearances may be delayed or unsuccessful, which may negatively impact our ability to perform on our U.S. and non-U.S. government contracts in a timely manner or at all.

Our success depends on our ability to effectively source and staff people with the right mix of skills and experience to perform services for our customers, including our ability to transition personnel to new assignments on a timely basis. If we are unable to effectively utilize our personnel on a timely basis to fulfill the needs of our customers, our business could suffer.

We face intense competition for qualified personnel, especially software engineers and data scientists, in major U.S. markets, where a large portion of our personnel are based. We incur costs related to attracting, relocating, and retaining qualified personnel in these highly competitive markets, including leasing real estate in prime areas in these locations. Further, many of the companies with which we compete for qualified personnel have greater resources than we have. Additionally, laws and regulations, such as restrictive immigration laws, may limit our ability to recruit outside of the United States. If we fail to attract new personnel or to retain our current personnel, our business and operations could be harmed.

We seek to retain and motivate existing personnel through our compensation practices, company culture, and career development opportunities. We may need to invest significant amounts of cash and equity for new and existing employees, and we may never realize returns on these investments. If the perceived value of our equity awards declines, or if the mix of equity and cash compensation that we offer is less attractive than that of our competitors, it may adversely affect our ability to recruit and retain highly skilled personnel. Employees may also be more likely to leave us if the shares of our capital stock they own or the shares of our capital stock underlying their equity incentive awards have significantly reduced in value or the vested shares of our capital stock they own or vested shares of our capital stock underlying their equity incentive awards have significantly appreciated. In addition, many of our employees may receive significant proceeds from sales of our equity in the public markets at some point after the Closing, which may reduce their motivation to continue to work for us. Any of these factors could harm our business, financial condition, and results of operations.

If we are unable to successfully deploy our marketing and sales organization in a timely manner, or at all, or to successfully hire, retain, train, and motivate our sales personnel, our growth and long-term success could be adversely impacted.

We currently have a growing, but limited, direct sales force and our sales efforts have historically depended on the significant direct involvement of our senior management team. The successful execution of our strategy to increase our sales to existing customers, identify and engage new customers, and enter new markets will depend, among other things, on our ability to successfully build and expand our sales organization and operations. Identifying, recruiting, training, and managing sales personnel requires significant time, expense, and attention, including from our senior management and other key personnel, which could adversely impact our business, financial condition, and results of operations in the short and long term.

In order to successfully scale our unique sales model, we must, and we intend to continue to, increase the size of our direct sales force, both in the United States and outside of the United States, to generate additional revenue from new and existing customers while preserving the cultural and mission-oriented elements of our company. If we do not hire enough qualified sales personnel, our future revenue growth and business could be adversely impacted. It may take a significant period of time before our sales personnel are fully trained and productive, particularly in light of our unique sales model, and there is no guarantee we will be successful in adequately training and effectively deploying our sales personnel. In addition, we may need to invest significant resources in our sales operations to enable our sales organization to run effectively and efficiently, including supporting sales

15