As filed with the Securities and Exchange Commission on December 13, 2023

Registration No. 333-274947

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 6163 | 93-3029990 | ||||||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) 3 World Trade Center 175 Greenwich Street, 57th Floor New York, NY 10007 Telephone: (415) 522-8837 | (I.R.S. Employer Identification Number) | ||||||

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Copies to:

Jared M. Fishman

Alan J. Fishman

Sullivan & Cromwell LLP

125 Broad Street

New York, NY 10004

Tel: (212) 558-4000

Approximate date of commencement of proposed sale of the securities to the public: From time to time after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the box: ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | ||||||||

☒ | Smaller reporting company | ||||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The information in this preliminary prospectus is not complete and may be changed. The Selling Securityholders may not sell the securities described in this preliminary prospectus until the registration statement filed with the Securities and Exchange Commission is declared effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED DECEMBER 13, 2023

Primary Offering of

Up to 9,808,405 Shares of Better Home & Finance Class A Common Stock Issuable Upon Exercise of Warrants

Secondary Offering of

Up to 53,665,365 Shares of Better Home & Finance Class A Common Stock

Up to 360,774,686 Shares of Better Home & Finance Class A Common Stock Issuable Upon Conversion of Better Home & Finance Class B Common Stock and Better Home & Finance Class C Common Stock

Up to 3,733,358 Shares of Better Home & Finance Class A Common Stock Issuable Upon Exercise of Warrants

Up to 3,733,358 Warrants to Purchase Better Home & Finance Class A Common Stock

This prospectus relates to the issuance by us of up to an aggregate of 9,808,405 shares of Better Home & Finance Class A common stock, par value $0.0001 per share (“Better Home & Finance Class A common stock”), which consists of (i) 6,075,047 shares of Better Home & Finance Class A common stock issuable upon exercise of Public Warrants (as defined below) and (ii) 3,733,358 shares of Better Home & Finance Class A common stock issuable upon exercise of Private Warrants (as defined below, together with Public Warrants, “Warrants”). We will receive proceeds from any Warrants exercised in the event that such Warrants are exercised for cash.

This prospectus also relates to the offer and sale from time to time by the selling securityholders identified in this prospectus, or their permitted transferees (the “Selling Securityholders”), of up to an aggregate of 418,173,409 shares of Better Home & Finance Class A common stock, which consists of

(i) 53,665,365 shares of Better Home & Finance Class A common stock, of which:

a.40,000,000 shares were issued pursuant to the Novator Exchange Agreement to Novator Capital Sponsor Ltd. (“Novator”) at an effective purchase price of $2.50 per share;

b.1,700,000 shares were issued pursuant to the Sponsor Purchase Subscription Agreement to Novator at an effective purchase price of $10.00 per share;

c.3,471,946 shares were issued pursuant to the Merger Agreement (as defined below) to Novator on a one-for-one basis in exchange for Class B ordinary shares of Aurora, which were initially issued at an effective purchase price of $0.004 per share before Aurora’s initial public offering;

d.636,240 shares were issued pursuant to the Merger Agreement to Novator on a one-for-one basis in exchange for Class A ordinary shares underlying the Private Units of Aurora (with each Private Unit consisting of one Class A ordinary share of Aurora and one-fourth of a Public Warrant), which were

initially issued at an effective purchase price of $10.00 per Private Unit and for which Aurora, at the time of its initial public offering, valued the underlying shares at $9.785 per share and the underlying warrants at $0.86 per warrant;

e.1,159,375 shares were issued pursuant to the Merger Agreement to Unbound Holdco Ltd. on a one-for-one basis in exchange for Class B ordinary shares of Aurora, which were initially issued at an effective purchase price of $0.004 per share before Aurora’s initial public offering;

f.1,000,000 shares were issued pursuant to the Merger Agreement to Unbound Holdco Ltd. on a one-for-one basis in exchange for Class A ordinary shares underlying the Private Units of Aurora, which were which were initially issued at an effective purchase price of $10.00 per Private Unit and for which Aurora, at the time of its initial public offering, valued the underlying shares at $9.785 per share and the underlying warrants at $0.86 per warrant;

g.1,242,188 shares were issued pursuant to the Merger Agreement to Arnaud Massenet on a one-for-one basis in exchange for Class B ordinary shares of Aurora, which were initially issued at an effective purchase price of $0.004 per share before Aurora’s initial public offering;

h.150,000 shares were issued pursuant to the Merger Agreement to Arnaud Massenet on a one-for-one basis in exchange for Class A ordinary shares underlying the Private Units of Aurora, which were initially issued at an effective purchase price of $10.00 per Private Unit and for which Aurora, at the time of its initial public offering, valued the underlying shares at $9.785 per share and the underlying warrants at $0.86 per warrant;

i.124,219 shares were issued pursuant to the Merger Agreement to Michael Edelstein (Michael Edelstein September 16, 2020 Revocable Trust) on a one-for-one basis in exchange for Class B ordinary shares of Aurora, which were initially issued at an effective purchase price of $0.004 per share before Aurora’s initial public offering;

j.828,125 shares were issued pursuant to the Merger Agreement, to Prabhu Narasimhan on a one-for-one basis, in exchange for Class B ordinary shares of Aurora, which were initially issued at an effective purchase price of $0.004 per share before Aurora’s initial public offering;

k.50,000 shares were issued pursuant to the Merger Agreement to Prabhu Narasimhan on a one-for-one basis in exchange for Class A ordinary shares underlying the Private Units of Aurora, which were initially issued at an effective purchase price of $10.00 per Private Unit and for which Aurora, at the time of its initial public offering, valued the underlying shares at $9.785 per share and the underlying warrants at $0.86 per warrant;

l.124,219 shares were issued pursuant to the Merger Agreement to Sangeeta Desai on a one-for-one basis in exchange for Class B ordinary shares of Aurora, which were initially issued at an effective purchase price of $0.004 per share before Aurora’s initial public offering;

m.3,176,553 shares were issued to Zachary Frankel, in exchange for Better Home & Finance Class B common stock (defined below), that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, which were initially issued at a weighted average effective purchase price of $0.00003 per share; and

n.2,500 shares were issued to Caroline Harding at an effective purchase price of $10.28 per unit and for which Aurora, at the time of its initial public offering, valued the underlying shares at $9.785 per share and the underlying warrants at $0.86 per warrant,

(ii)288,897,403 shares of Better Home & Finance Class A common stock issuable upon conversion of Better Home & Finance Class B common stock, par value $0.0001 per share (“Better Home & Finance Class B common stock”), of which:

a.61,306,253 shares are issuable upon conversion of 61,306,253 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to entities affiliated with Activant Capital Group LLC at a weighted average effective purchase price of $1.73 per share;

b.55,188,435 shares are issuable upon conversion of 55,188,435 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to SVF Beaver II (DE) LLC at a weighted average effective purchase price of $8.01 per share;

c.27,141,628 shares are issuable upon conversion of 27,141,628 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to Better Portfolio Holdings 1 LLC at a weighted average effective purchase price of $0.00003 per share;

d.23,203,001 shares are issuable upon conversion of 23,203,001 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to LCG4 Best LP at a weighted average effective purchase price of $3.84 per share;

e.25,704,813 shares are issuable upon conversion of 25,704,813 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to 1/0 Mortgage Investment LLC at a weighted average effective purchase price of $0.03 per share;

f.6,522,761 shares are issuable upon conversion of 6,522,761 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to 1/0 Real Estate LLC at a weighted average effective purchase price of $0.32 per share;

g.527,961 shares are issuable upon conversion of 527,961 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to Kevin Ryan at a weighted average effective purchase price of $1.66 per share;

h.5,978,074 shares are issuable upon conversion of 5,978,074 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to Nicholas Calamari at a weighted average effective purchase price of $0.02 per share;

i.1,222,903 shares are issuable upon conversion of 1,222,903 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to The Nicholas J Calamari Family Trust at a weighted average effective purchase price of $0.00003 per share;

j.246,515 shares are issuable upon conversion of 246,515 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to Paula Tuffin at a weighted average effective purchase price of $0.20 per share;

k.822,125 shares are issuable upon conversion of 822,125 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to Technology Stock Holding Master Trust/Series Tuffin 2021 Trust at a weighted average effective purchase price of $0.01 per share;

l.5,973,526 shares are issuable upon conversion of 5,973,526 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to Sigurgeir Jonsson at a weighted average effective purchase price of $0.32 per share;

m.3,103,721 shares are issuable upon conversion of 3,103,721 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to The Sigurgeir Orn Jonsson 2020 Family Trust at a weighted average effective purchase price of $0.00003 per share;

n.1,222,903 shares are issuable upon conversion of 1,222,903 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to The Anika G Austin Descendants Trust at a weighted average effective purchase price of $0.00003 per share;

o.69,968,642 shares are issuable upon conversion of 69,968,642 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to Vishal Garg at a weighted average effective purchase price of $0.00003 per share; and

p.764,142 shares are issuable upon conversion of 764,142 shares of Class B Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to Unnamed Selling Securityholders at a weighted average effective purchase price of $1.66 per share,

(iii)71,877,283 shares of Better Home & Finance Class A common stock issuable upon conversion of Better Home & Finance Class C common stock, par value $0.0001 per share (“Better Home & Finance Class C common stock”), of which:

a.6,877,283 shares are issuable upon conversion of 6,877,283 shares of Class C Common Stock that were issued based on an exchange ratio of approximately 3.06 shares per share of Better common stock pursuant to the Merger Agreement, to SVF Beaver II (DE) LLC at a weighted average effective purchase price of $8.01 per share and

b.65,000,000 shares are issuable upon conversion of 65,000,000 shares of Class C Common Stock that were issued pursuant to the conversion of the Pre-Closing Bridge Note (as defined herein) held by SB Northstar, to BHFHC Distribution Trust at an effective purchase price of $10.00 per share,

and (iv) 3,733,358 shares of Better Home & Finance Class A common stock issuable upon exercise of Private Warrants, of which:

a.1,715,015 shares are issuable upon exercise of 1,715,015 Private Warrants at $11.50 per share that were issued on a one-for-one basis in exchange for Aurora Private Warrants pursuant to the Merger Agreement, which were initially issued to Novator at an effective purchase price of $1.50 per Private Warrant;

b.575,000 shares are issuable upon exercise of 575,000 Private Warrants at $11.50 per share that were issued in exchange for Aurora Private Warrants underlying Private Units of Aurora pursuant to the Merger Agreement, which were initially issued to Novator at an effective purchase price of $10.00 per Private Unit and for which Aurora, at the time of its initial public offering, valued the underlying shares at $9.785 per share and the underlying warrants at $0.86 per warrant;

c.1,143,343 shares are issuable upon exercise of 1,143,343 Private Warrants at $11.50 per share that were issued on a one-for-one basis in exchange for Aurora Private Warrants pursuant to the Merger Agreement, which were initially issued to Unbound Holdco Ltd at an effective purchase price of $1.50 per Private Warrant;

d.250,000 shares are issuable upon exercise of 250,000 Private Warrants at $11.50 per share that were issued in exchange for Aurora Private Warrants underlying Private Units of Aurora pursuant to the Merger Agreement, which were initially issued to Unbound Holdco Ltd at an effective purchase price of $10.00 per Private Unit and for which Aurora, at the time of its initial public offering, valued the underlying shares at $9.785 per share and the underlying warrants at $0.86 per warrant;

e.37,500 shares are issuable upon exercise of 37,500 Private Warrants at $11.50 per share that were issued on a one-for-one basis in exchange for Aurora Private Warrants underlying Private Units of Aurora pursuant to the Merger Agreement, which were initially issued to Arnaud Massenet at an effective purchase price of $10.00 per Private Unit and for which Aurora, at the time of its initial public offering, valued the underlying shares at $9.785 per share and the underlying warrants at $0.86 per warrant; and

f.12,500 shares are issuable upon exercise of 12,500 Private Warrants at $11.50 per share that were issued on a one-for-one basis in exchange for Aurora Private Warrants underlying Private Units of Aurora pursuant to the Merger Agreement, which were initially issued to Prabhu Narasimhan at an effective purchase price of $10.00 per Private Unit and for which Aurora, at the time of its initial public offering, valued the underlying shares at $9.785 per share and the underlying warrants at $0.86 per warrant,

and of up to 3,733,358 Private Warrants, of which:

a.1,715,015 were issued on a one-for-one basis in exchange for Aurora Private Warrants pursuant to the Merger Agreement, to Novator at an effective purchase price of $1.50 per Private Warrant;

b.575,000 were issued in exchange for Aurora Private Warrants underlying Private Units of Aurora pursuant to the Merger Agreement, to Novator at an effective purchase price of $10.00 per Private Unit and for which Aurora, at the time of its initial public offering, valued the underlying shares at $9.785 per share and the underlying warrants at $0.86 per warrant;

c.1,143,343 were issued on a one-for-one basis in exchange for Aurora Private Warrants pursuant to the Merger Agreement, to Unbound Holdco Ltd at an effective purchase price of $1.50 per Private Warrant;

d.250,000 were issued in exchange for Aurora Private Warrants underlying Private Units of Aurora pursuant to the Merger Agreement, to Unbound Holdco Ltd at an effective purchase price of $10.00 per Private Unit and for which Aurora, at the time of its initial public offering, valued the underlying shares at $9.785 per share and the underlying warrants at $0.86 per warrant;

e.37,500 were issued in exchange for Aurora Private Warrants underlying Private Units of Aurora pursuant to the Merger Agreement, which were initially issued to Arnaud Massenet at an effective purchase price of $10.00 per Private Unit and for which Aurora, at the time of its initial public offering, valued the underlying shares at $9.785 per share and the underlying warrants at $0.86 per warrant; and

f.12,500 were issued in exchange for Aurora Private Warrants underlying Private Units of Aurora pursuant to the Merger Agreement, which were initially issued to Prabhu Narasimhan at an effective purchase price of $10.00 per Private Unit and for which Aurora, at the time of its initial public offering, valued the underlying shares at $9.785 per share and the underlying warrants at $0.86 per warrant.

Effective purchase price is calculated, if securities were acquired from Aurora or by its affiliates before or in connection with the Business Combination, based on the transaction acquisition cost or, if securities were acquired by holders of Better capital stock, based on the weighted-average purchase price of such Better capital stock.

We will not receive any proceeds from the sale of Class A common stock or Private Warrants by the Selling Securityholders pursuant to this prospectus. We will bear all costs, expenses and fees in connection with the registration of the shares of Better Home & Finance Class A common stock and Private Warrants. The Selling Securityholders will bear all commissions and discounts, if any, attributable to their respective sales of the shares of Better Home & Finance Class A common stock and Private Warrants.

Our registration of the securities covered by this prospectus does not mean that either we or the Selling Securityholders will issue, offer or sell, as applicable, any of the securities. The Selling Securityholders may offer and sell the securities covered by this prospectus in a number of different ways and at varying prices. We provide more information about how the Selling Securityholders may sell the securities in the section entitled “Plan of Distribution.”

You should read this prospectus and any prospectus supplement or amendment carefully before you invest in our securities.

Better Home & Finance Class A common stock and Warrants are listed on the Nasdaq Global Market and the Nasdaq Capital Market, respectively, under the ticker symbols “BETR” and “BETRW”. On December 1, 2023, the closing price of Better Home & Finance Class A common stock was $0.453 per share and the closing price of Warrants was $0.07 per warrant. The sale of substantial amounts of Better Home & Finance Class A common stock being offered in this prospectus, or the perception that such sales could occur, could have the effect of increasing the volatility in the prevailing market price or putting significant downward pressure on the price of Better Home & Finance Class A common stock and harm the prevailing market price of Better Home & Finance Class A common stock. Notwithstanding any changes in the prevailing market price, certain Selling Securityholders may still experience a positive rate of return on their securities due to the lower effective purchase price at which they purchased such securities. See “The Offering” and “Risk Factors – Certain existing stockholders purchased securities in the Company at a price below the current trading price of such securities, and may experience a positive rate of return based on the current trading price. Future investors in our Company may not experience a similar rate of return.” You may not experience a similar rate of return should you invest in our securities, as the price at which you purchase our securities may differ from that of these Selling Securityholders.

Each Warrant entitles the holder thereof to purchase one share of Better Home & Finance Class A common stock at a price of $11.50 per share. We believe the likelihood that the holders will exercise their Warrants, and therefore the amount of cash proceeds that we would receive, is dependent upon the trading price of Better Home & Finance Class A common stock. If the trading price of Better Home & Finance Class A common stock is less than the exercise price thereof, we believe the holders are unlikely to exercise their Warrants. Conversely, the holders are more likely to exercise their Warrants the higher the price of Better Home & Finance Class A common stock is above the exercise price thereof. As of December 1, 2023, the closing price of Better Home & Finance Class A common stock as reported on Nasdaq was $0.453 per share, which is below the $11.50 exercise price of the Warrants. For so long as the Warrants remain “out-of-the-money,” we do not expect warrant holders to exercise their Warrants. See “Risk Factors – There is no guarantee that the exercise price of the Warrants will ever be less than the trading price of Better Home & Finance Class A Common Stock on Nasdaq, and they may expire worthless; and the terms of the Warrants may be amended in a manner adverse to a holder if holders of at least 50% of the then outstanding Warrants approve of such amendment.”

We are an “emerging growth company,” as that term is defined under the federal securities laws and, as such, are subject to certain reduced public company reporting requirements.

Investing in our securities involves risks that are described in the “Risk Factors” section beginning on page 17 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued under this prospectus or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2023.

TABLE OF CONTENTS

| Page | |||||

i

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form S-1 that we filed with the Securities and Exchange Commission (the “SEC”) using the “shelf” registration process. Under this shelf registration process, the Selling Securityholders may, from time to time, sell the securities offered by them described in this prospectus. We will not receive any proceeds from the sale by such Selling Securityholders of the securities offered by them described in this prospectus.

Neither we nor the Selling Securityholders have authorized anyone to provide you with any information or to make any representations other than those contained in this prospectus, any applicable prospectus supplement, or any free writing prospectuses prepared by or on behalf of us or to which we have referred you. Neither we nor the Selling Securityholders take responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. Neither we nor the Selling Securityholders will make an offer to sell these securities in any jurisdiction where the offer or sale is not permitted.

We may also provide a prospectus supplement or post-effective amendment to this registration statement to add information to, or update or change information contained in, this prospectus. You should read both this prospectus and any applicable prospectus supplement or post-effective amendment to the registration statement together with the additional information to which we refer you in the section of this prospectus entitled “Where You Can Find More Information.” You should assume that the information appearing in this prospectus or any prospectus supplement is accurate only as of the date on the front of those documents, regardless of the time of delivery of this prospectus or any applicable prospectus supplement, or any sale of a security. Our business, financial condition, results of operations and prospects may have changed since those dates.

This prospectus contains summaries of certain provisions contained in some of the documents described herein, but reference is made to the actual documents for complete information. All of the summaries are qualified in their entirety by the actual documents. Copies of some of the documents referred to herein have been filed, will be filed or will be incorporated by reference as exhibits to the registration statement of which this prospectus is a part, and you may obtain copies of those documents as described below under “Where You Can Find More Information.”

As previously announced, Aurora Acquisition Corp. (“Aurora” and, after the Domestication as described below, “Better Home & Finance” or the “Company”), a Cayman Islands exempted company with limited liability, entered into an Agreement and Plan of Merger, dated as of May 10, 2021, as amended as of October 27, 2021, November 9, 2021, November 30, 2021, August 26, 2022, February 24, 2023 and June 23, 2023 (as amended, the “Merger Agreement”) by and among Aurora, Better Holdco, Inc., a Delaware corporation (“Better”), and Aurora Merger Sub I, Inc., formerly a Delaware corporation and wholly owned subsidiary of Aurora (“Merger Sub”).

On August 21, 2023, as contemplated by the Merger Agreement, and as described in the section titled “Domestication Proposal” beginning on page 248 of the final prospectus and definitive proxy statement, dated July 27, 2023 (the “Proxy Statement/Prospectus”), filed with the U.S. Securities and Exchange Commission (the “SEC”), Aurora filed a notice of deregistration with the Cayman Islands Registrar of Companies, together with the necessary accompanying documents, and filed a certificate of incorporation and a certificate of corporate domestication with the Secretary of State of the State of Delaware, under which Aurora was transferred by way of continuation from the Cayman Islands and domesticated as a Delaware corporation (the “Domestication”). Following the Domestication, on August 22, 2023, as previously announced and as contemplated by the Merger Agreement, and as described in the section titled “BCA Proposal” beginning on page 198 of the Proxy Statement/Prospectus, Merger Sub merged with and into Better, with Better surviving the merger (the “First Merger”) and Better merged with and into Aurora, with Aurora surviving the merger and changing its name to “Better Home & Finance Holding Company” (such merger, the “Second Merger,” and together with the First Merger and the Domestication, the “Business Combination”).

Unless the context indicates otherwise, references in this prospectus to the “Company,” “Better Home & Finance,” “we,” “us,” “our” and similar terms refer to Better prior to the Business Combination and Better Home & Finance Holding Company and its consolidated subsidiaries following the Business Combination. References to “Better” refer to our predecessor company prior to the consummation of the Business Combination.

1

SELECTED DEFINITIONS

Unless otherwise stated in this prospectus or the context otherwise requires, references to:

•“2023 Plan” are to the Better Home & Finance 2023 Incentive Equity Plan;

•“Amended and Restated Charter” are to the Amended and Restated Certificate of Incorporation of Better Home & Finance adopted on August 22, 2023, in connection with the closing of the Business Combination;

•“Amended and Restated Insider Letter Agreement” are to that certain Letter Agreement, dated May 10, 2021, by and between the Sponsor and certain individuals, each of whom is a member of the board of directors and/or management team of Aurora;

•“Aurora” are to Aurora Acquisition Corp. prior to its domestication as a corporation in the State of Delaware;

•“Better” are to, unless otherwise specified or the context otherwise requires, Better Holdco, Inc. and/or its subsidiaries, or any of them;

•“Better Awards” are to Better Options, Better RSUs and Better Restricted Stock Awards outstanding prior to the consummation of the Business Combination;

•“Better Capital Stock” are to the shares of the Better common stock and the Better preferred stock outstanding prior to the consummation of the Business Combination;

•“Better common stock” are to shares of Better common stock, par value $0.0001 per share, outstanding prior to the consummation of the Business Combination;

•“Better Founder and CEO” are to Vishal Garg;

•“Better Holder Support Agreement” are to that certain Company Holder Support Agreement, dated May 10, 2021, by and among certain holders of Better Capital Stock, certain directors and all executive officers of Better;

•“Better Home & Finance” are to Aurora after the Domestication and/or the Business Combination, including its name change from Aurora to “Better Home & Finance Holding Company,” as applicable;

•“Better Home & Finance Class A common stock” are to shares of Better Home & Finance Class A common stock, par value $0.0001 per share, which are entitled to one vote per share;

•“Better Home & Finance Class B common stock” are to shares of Better Home & Finance Class B common stock, par value $0.0001 per share, which are entitled to three votes per share;

•“Better Home & Finance Class C common stock” are to shares of Better Home & Finance Class C common stock, par value $0.0001 per share, which carry no voting rights except as required by applicable law or as provided in the Amended and Restated Charter;

•“Better Home & Finance common stock” are to shares of Better Home & Finance Class A common stock, Better Home & Finance Class B common stock and Better Home & Finance Class C common stock;

•“Better Home & Finance Options” are to options to purchase shares of Better Home & Finance common stock;

•“Better Home & Finance Restricted Stock Awards” are to restricted shares of Better Home & Finance common stock;

•“Better Home & Finance RSUs” are to restricted stock units based on shares of Better Home & Finance common stock;

2

•“Better Options” are to options to purchase shares of Better common stock;

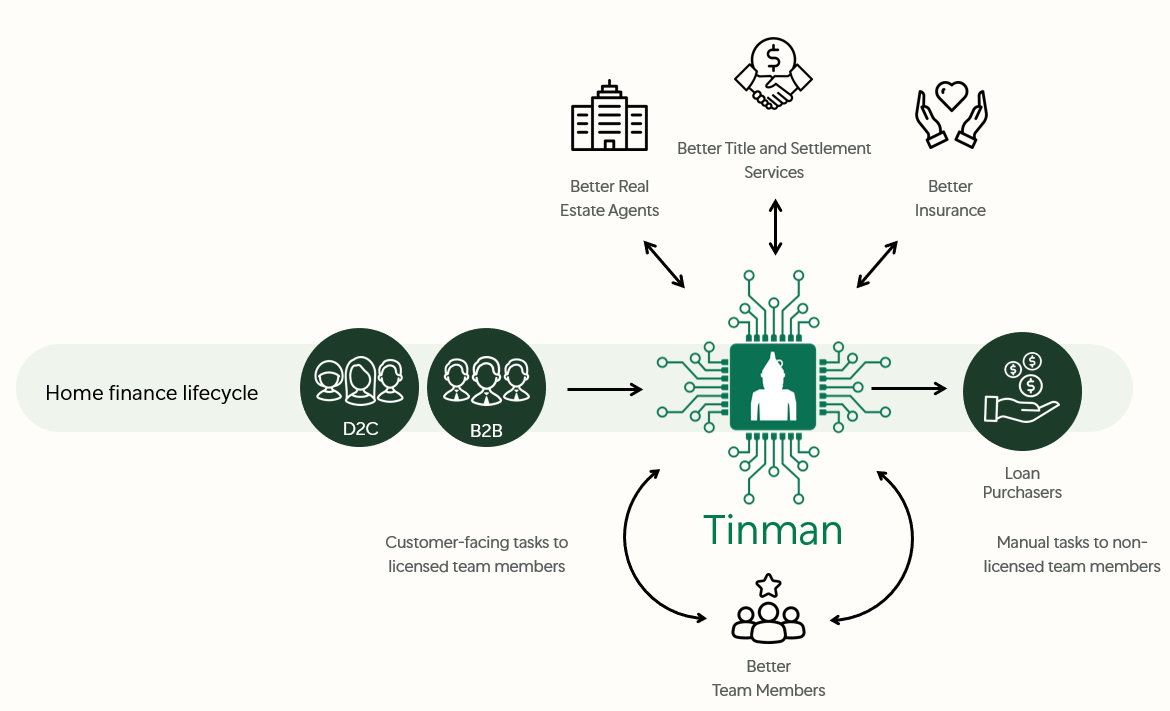

•“Better Plus” are to our non-mortgage business line, which includes Better Settlement Services (title insurance and settlement services), Better Cover (homeowners insurance) and Better Real Estate (real estate agent services);

•“Better Restricted Stock Awards” are to restricted shares of Better common stock;

•“Better RSUs” are to restricted stock units based on shares of Better common stock;

•“Better Stockholders” are to the common and preferred stockholders of Better and holders of Better Awards prior to the consummation of the Business Combination;

•“Better Warrants” are to warrants to purchase shares of Better Capital Stock;

•“Business Combination” are to the Domestication together with the Mergers;

•“Bylaws” are to the Bylaws of Better Home & Finance adopted on August 22, 2023;

•“Closing Date” are to August 22, 2023;

•“CFPB” are to the Consumer Financial Protection Bureau;

•“Convertible Notes” are to the subordinated unsecured 1% convertible notes issued in an aggregate principal amount of $528,585,444 pursuant to an Indenture, dated as of August 22, 2023, between the Company and GLAS Trust Company LLC, as trustee, which are convertible, at the option of the holder into shares of Better Home & Finance Class A common stock.

•“DGCL” are to the General Corporation Law of the State of Delaware;

•“Domestication” are to the domestication of Aurora as a corporation incorporated in the State of Delaware;

•“ESPP” are to the 2023 Employee Stock Purchase Plan;

•“Exchange Act” are to the Securities Exchange Act of 1934, as amended;

•“Fannie Mae” are to the U.S. Federal National Mortgage Association;

•“FCPA” are to the United States Foreign Corrupt Practices Act;

•“FHA” are to the U.S. Federal Housing Administration;

•“First Novator Letter Agreement” are to that certain Letter Agreement, dated August 26, 2022, by and among Aurora, Better and the Sponsor;

•“Freddie Mac” are to the Federal Home Loan Mortgage Corporation;

•“FTC” are to the Federal Trade Commission;

•“Funded Loan Volume” are to the aggregate dollar amount of loans funded in a given period based on the principal amount of the loan at funding;

•“GAAP” are to accounting principles generally accepted in the United States of America;

•“Gain on Sale Margin” are to mortgage platform revenue, net, as presented on our statements of operations and comprehensive income (loss), divided by Funded Loan Volume. For clarity, Gain on Sale Margin represents the difference in value of loan production compared to the price received on the sale of such loan production, net of any mark-to-market revenue impact from fluctuating interest rates on certain loan and

3

financial assets that is reflected in mortgage platform revenue, net, and is not a measure of profitability based on the cost to produce such loans;

•“GSEs” are to government-sponsored enterprises, including Fannie Mae and Freddie Mac;

•“Home Finance” are to our mortgage business line, which is conducted by Better Mortgage Corporation;

•“HUD” are to the U.S. Department of Housing and Urban Development;

•“Insiders” are to those certain individuals, each of whom was a member of the board of directors and/or management team of Aurora, who are party to the Amended and Restated Insider Letter Agreement, with each such individual an “Insider”;

•“IRS” are to the U.S. Internal Revenue Service;

•“JOBS Act” are to the Jumpstart Our Business Startups Act of 2012;

•“Limited Waiver” are to that certain Limited Waiver to the Amended and Restated Insider Letter Agreement, dated February 23, 2023, by and among Aurora, Better, the Sponsor, and the Insiders party to the Amended and Restated Insider Letter Agreement;

•“Merger Agreement” are to the Agreement and Plan of Merger, dated as of May 10, 2021, by and among Aurora, Merger Sub and Better, including, where applicable, as amended by (i) the first amendment to the Merger Agreement, dated October 27, 2021, (ii) the second amendment to the Merger Agreement, dated November 9, 2021, (iii) the third amendment to the Merger Agreement, dated November 30, 2021, (iv) the fourth amendment to the Merger Agreement, dated August 26, 2022, (v) the fifth amendment to the Merger Agreement, dated February 24, 2023 and (vi) the sixth amendment to the Merger Agreement, dated June 23, 2023;

•“Merger Sub” are to Aurora Merger Sub I, Inc., a Delaware corporation and a direct, wholly owned subsidiary of Aurora;

•“Mergers” are to, collectively, the merger of Merger Sub with and into Better, with Better surviving the merger as a wholly owned subsidiary of Aurora, and the merger of Better with and into Aurora, with Aurora surviving the merger;

•“MSRs” are to mortgage-servicing rights;

•“Nasdaq” are to the Nasdaq Global Market, the Nasdaq Capital Market, and The Nasdaq Stock Market, LLC, as applicable;

•“Pre-Closing Bridge Note Purchase Agreement” are to that certain agreement, dated November 30, 2021, by and among Aurora, Better, SB Northstar and the Sponsor;

•“Pre-Closing Bridge Notes” are to the subordinated 0% bridge promissory notes, issued in an aggregate principal amount of $750,000,000 pursuant to the Pre-Closing Bridge Note Purchase Agreement, that converted into or were exchanged for Better Home & Finance Class A common stock and Better Home & Finance Class C common stock on the Closing Date;

•“Restricted Stock Awards” are to restricted shares of Better Home & Finance common stock;

•“RSUs” are to restricted stock units based on shares of Better Home & Finance common stock;

•“Private Warrants” are to the certain warrants that are “Private Placement Warrants” or “Novator Private Placement Warrants” as defined in the Amended and Restated Insider Letter Agreement;

•“Public Warrants” are to warrants to purchase shares of Better Home & Finance Class A common stock at an exercise price of $11.50 per share (other than the Private Warrants);

4

•“Purchase Loan Volume” are to the aggregate dollar amount of purchase loans funded in a given period based on the principal amount of the loan at funding;

•“Refinance Loan Volume” are to the aggregate dollar amount of refinance loans funded in a given period based on the principal amount of the loan at funding;

•“Registration Rights Agreement” are to the Amended and Restated Registration Rights Agreement, dated as of August 22, 2023, by and among Better Home & Finance, Sponsor, and certain other persons;

•“Sarbanes-Oxley Act” are to the Sarbanes-Oxley Act of 2002;

•“SB Northstar” are to SB Northstar LP, a Cayman Islands exempted limited partnership and an affiliate of SoftBank Group Corp. and party to the SB Northstar Subscription Agreement;

•“SEC” are to the United States Securities and Exchange Commission;

•“Second Novator Agreement” refer to that certain Letter Agreement, dated February 7, 2023, by and among Aurora, Better and the Sponsor;

•“Securities Act” are to the Securities Act of 1933, as amended;

•“Softbank Subscription Agreement” are to certain Subscription Agreement, dated May 10, 2021, by and between Aurora and SB Northstar;

•“Sponsor” are to Novator Capital Sponsor Ltd., a Cyprus limited liability company;

•“Sponsor Subscription Agreement” are to certain Subscription Agreement, dated May 10, 2021, by and among Aurora, Sponsor and BB Trustees SA;

•“Subscription Agreements” are to, collectively, the Softbank Subscription Agreement and the Sponsor Subscription Agreement, in each case as amended;

•“SVF Beaver” are to SVF II Beaver (DE) LLC, an affiliate of SoftBank Group Corp., which was a Better Stockholder prior to the Business Combination and entered into a contribution agreement with Better and a letter agreement and irrevocable voting proxy with the Better Founder and CEO, each dated as of April 7, 2021, as amended;

•“Total Loans” are to the total number of loans funded in a given period;

•“VA” are to the U.S. Department of Veterans Affairs;

•“Warrant Agreement” are to that certain Warrant Agreement, dated March 3, 2021, by and between Aurora and Continental Stock Transfer & Trust Company, as warrant agent; and

•“Warrants” are to, collectively, the Private Warrants and the Public Warrants.

5

TRADEMARKS

This prospectus contains references to trademarks and service marks belonging to other entities. Solely for convenience, in some cases, the trademarks, trade names and service marks referred to in this prospectus are listed without the applicable ®, ™ and SM symbols, but they will assert, to the fullest extent under applicable law, their rights to these trademarks, trade names and service marks.

6

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus and the information and documents incorporated by reference herein include “forward-looking statements” within the meaning of federal securities laws. These statements include, without limitation, statements regarding the financial position, business strategy and the plans and objectives of management for future operations. These statements constitute forward-looking statements, and are not guarantees of performance. Such statements can be identified by the fact that they do not relate strictly to historical or current facts. When used in this prospectus, the words “could,” “should,” “will,” “may,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project,” the negative of such terms and other similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. Such forward-looking statements are based on management’s current expectations and assumptions about future events and are based on currently available information as to the outcome and timing of future events. Except as otherwise required by applicable law, the Company disclaims any duty to update any forward-looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this prospectus. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. Forward-looking statements in this prospectus and in any information and document incorporated by reference in this prospectus, and the associated risks, uncertainties, assumptions and other important factors may include, but are not limited to:

•Factors relating to our business, operations and financial performance, including:

◦Our ability to operate under and maintain or improve our business model;

◦The effect of interest rates on our business, results of operations, and financial condition;

◦Our ability to expand our customer base, grow market share in our existing markets and enter into new markets;

◦Our ability to respond to general economic conditions, particularly elevated interest rates and lower home sales and refinancing activity;

◦Our ability to restore our growth and our expectations regarding the development and long-term expansion of our business;

◦Our ability to comply with laws and regulations related to the operation of our business, including any changes to such laws and regulations;

◦Our ability to achieve and maintain profitability in the future;

◦Our ability and requirements to raise additional financing in the future;

◦Our estimates regarding expenses, future revenue, capital and additional financing requirements;

◦Our ability to maintain, expand and be successful in our strategic relationships with third parties;

◦Our ability to remediate existing material weaknesses and implement and maintain an effective system of internal controls over financial reporting;

◦Our ability to develop new products, features and functionality that meet market needs and achieve market acceptance;

◦Our ability to retain, identify and hire individuals for the roles we seek to fill and staff our operations appropriately;

◦The involvement of our CEO in litigation related to prior business activities, our business activities and associated negative media coverage;

7

◦Our ability to recruit and retain additional directors, members of senior management and other team members, including our ability in general, and our CEO’s ability in particular, to maintain an experienced executive team in operating as a public company;

◦Our ability to maintain and improve morale and workplace culture and respond effectively to the effects of negative media coverage; and

◦Our ability to maintain, protect, assert and enhance our intellectual property rights.

•Factors relating to our capital structure, governance and the market for our securities, including:

◦The existence of multiple classes of common stock and its impact on the liquidity and value of Better Home & Finance Class A common stock;

◦The limited experience of our directors and management team in overseeing a public company;

◦Our ability to maintain the listing of the Better Home & Finance Class A common stock and Warrants on the Nasdaq Global Market and the Nasdaq Capital Market, respectively

◦Our ability to maintain certain lines of credit and obtain future financing on commercially favorable terms to fund loans and otherwise operate our business;

◦The liquidity and trading of Better Home & Finance Class A common stock and Warrants; and

The forward-looking statements contained in this prospectus and in any document incorporated by reference into this prospectus are based on current expectations and beliefs concerning future developments and their potential effects on us. There can be no assurance that future developments affecting us will be those that we have anticipated These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the section entitled “Risk Factors” beginning on page 17 of this prospectus. Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements.

8

PROSPECTUS SUMMARY

This summary highlights selected information from this prospectus and does not contain all of the information that is important to you. You should read this entire document and the other documents to which we refer before you decide to invest in our securities. Unless otherwise indicated or the context otherwise requires, references to the “Company,” “Better Home & Finance”, “we,” “us,” or “our” and similar other terms refer to Better before the Business Combination and Better Home & Finance and its consolidated subsidiaries after the Business Combination.

About Better Home & Finance

Better Home & Finance principally operates a digital-first homeownership company with services including mortgage financing, real estate services, title, and homeowners’ insurance. We have combined technology innovation and fresh thinking with a deep customer focus with the goal to revolutionize a homeownership industry. We started by redesigning the mortgage manufacturing process, and, since then, have built toward a broader vision of revolutionizing homeownership.

Background

As previously announced, Aurora, a Cayman Islands exempted company incorporated with limited liability, entered into an Agreement and Plan of Merger, dated as of May 10, 2021, as amended as of October 27, 2021, November 9, 2021, November 30, 2021, August 26, 2022, February 24, 2023 and June 23, 2023 (as amended, the “Merger Agreement”) by and among Aurora, Better Holdco, Inc., a Delaware corporation, and Merger Sub.

On August 21, 2023, as contemplated by the Merger Agreement, and as described in the section titled “Domestication Proposal” beginning on page 248 of the final prospectus and definitive proxy statement, dated July 27, 2023 (the “Proxy Statement/Prospectus”), filed with the U.S. Securities and Exchange Commission (the “SEC”), Aurora filed a notice of deregistration with the Cayman Islands Registrar of Companies, together with the necessary accompanying documents, and filed a certificate of incorporation and a certificate of corporate domestication with the Secretary of State of the State of Delaware, under which Aurora was transferred by way of continuation from the Cayman Islands and domesticated as a Delaware corporation (the “Domestication”).

Following the Domestication, on August 22, 2023 (the “Closing Date”), as previously announced and as contemplated by the Merger Agreement, and as described in the section titled “BCA Proposal” beginning on page 198 of the Proxy Statement/Prospectus, Merger Sub merged with and into Better, with Better surviving the merger (the “First Merger”) and Better merged with and into Aurora, with Aurora surviving the merger and changing its name to “Better Home & Finance Holding Company” (hereinafter referred to as “Better Home & Finance” or the “Company”) (such merger, the “Second Merger,” and together with the First Merger and the Domestication, the “Business Combination” and the completion thereof, the “Closing”).

In connection with the consummation of the Business Combination, the Company issued an aggregate of 40,601,825 shares of Better Home & Finance Class A common stock, 574,407,420 shares of Better Home & Finance Class B common stock and 6,877,283 shares of Better Home & Finance Class C common stock. Each share of Better Home & Finance Class B common stock and Better Home & Finance Class C common stock may be converted to a share of Better Home & Finance Class A common stock at any time by the holder thereof and upon certain other transfers that are not permitted transfers provided by the Amended and Restated Charter. In addition, in connection with other transactions contemplated by the Merger Agreement and related documentation, including the conversion or exchange of certain bridge notes, the Company issued an aggregate of 41,700,000 shares of Better Home & Finance Class A common stock and 65,000,000 shares of Better Home & Finance Class C common stock.

Better Home & Finance Class A common stock and Warrants are listed on the Nasdaq Global Market and the Nasdaq Capital Market, respectively, under the ticker symbols “BETR” and “BETRW.”

The Business Combination has been accounted for as a reverse recapitalization in accordance with GAAP, with no goodwill or other intangible assets recorded. Under this method of accounting, Aurora was treated as the “acquired” company for financial reporting purposes. Accordingly, for accounting purposes, the Business

9

Combination was treated as the equivalent of Better issuing stock for the net assets of Aurora, accompanied by a recapitalization. The net assets of Aurora were stated at historical cost, with no goodwill or other intangible assets recorded.

The rights of holders of Better Home & Finance Class A common stock, Better Home & Finance Class B common stock and Better Home & Finance Class C common stock are governed by our Amended and Restated Charter, our Bylaws, and the DGCL.

Corporate Information

Better Home & Finance Holding Company is a Delaware corporation. Our principal executive offices are located at 3 World Trade Center, 175 Greenwich Street, 57th Floor, New York, NY 10007 and our telephone number at that address is (415) 523-8837. Our website is located at www.better.com. We do not incorporate the information contained on, or accessible through, our corporate website into this prospectus, and you should not consider it part of this prospectus. We have included our website address only as an inactive textual reference and do not intend it to be an active link to our website.

Emerging Growth Company and Smaller Reporting Company Status

We are an “emerging growth company,” as defined in Section 2(a) of the Securities Act, as modified by the JOBS Act, and we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies, including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved.

Further, Section 102(b)(1) of the JOBS Act exempts emerging growth companies from being required to comply with new or revised financial accounting standards until private companies (that is, those that have not had a registration statement under the Securities Act declared effective or that do not have a class of securities registered under the Exchange Act) are required to comply with the new or revised financial accounting standards. The JOBS Act provides that a company can elect to opt out of the extended transition period and comply with the requirements that apply to non-emerging growth companies but any such election to opt out is irrevocable. We have elected not to opt out of such extended transition period which means that when a standard is issued or revised and it has different application dates for public or private companies, we, as an emerging growth company, can adopt the new or revised standard at the time private companies adopt the new or revised standard. This may make comparison of our financial statements with another public company which is not an emerging growth company or is an emerging growth company that has opted out of using the extended transition period difficult or impossible because of the potential differences in accounting standards used.

We will remain an emerging growth company until the earlier of: (1) the last day of the fiscal year (a) following the fifth anniversary of the closing of Aurora’s initial public offering, (b) in which we have total annual gross revenue of at least $1.235 billion or (c) in which we are deemed to be a large accelerated filer, which means the market value of our common equity that is held by non-affiliates exceeds $700.0 million as of the end of the prior fiscal year’s second fiscal quarter; and (2) the date on which we have issued more than $1.0 billion in non-convertible debt securities during the prior three-year period. References to “emerging growth company” have the meaning ascribed to it in the JOBS Act.

We are also a smaller reporting company, as defined in the Exchange Act. Even after we no longer qualify as an emerging growth company, we may still qualify as a smaller reporting company, which would allow us to continue taking advantage of many of the same exemptions from disclosure requirements, including reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements. In addition, for so long as we continue to qualify as a non-accelerated filer, we will not be required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act.

10

Warrants

Each Warrant entitles the holder thereof to purchase one share of Better Home & Finance Class A common stock at a price of $11.50 per share. We believe the likelihood that the holders will exercise their Warrants, and therefore the amount of cash proceeds that we would receive, is dependent upon the trading price of Better Home & Finance Class A common stock. If the trading price of Better Home & Finance Class A common stock is less than the exercise price thereof, we believe the holders are unlikely to exercise their Warrants. Conversely, the holders are more likely to exercise their Warrants the higher the price of Better Home & Finance Class A common stock is above the exercise price thereof. As of December 1, 2023, the closing price of Better Home & Finance Class A common stock as reported on Nasdaq was $0.453 per share, which is below the $11.50 exercise price of the Warrants. For so long as the Warrants remain “out-of-the-money,” we do not expect warrant holders to exercise their Warrants. See “Risk Factors – There is no guarantee that the exercise price of the Warrants will ever be less than the trading price of Better Home & Finance Class A Common Stock on Nasdaq, and they may expire worthless; and the terms of the Warrants may be amended in a manner adverse to a holder if holders of at least 50% of the then outstanding Warrants approve of such amendment.”

11

The Offering

Issuer | Better Home & Finance Holding Company (f/k/a/ Aurora Acquisition Corp.). | |||||||

Issuance of Better Home & Finance Class A common stock | ||||||||

Shares of Better Home & Finance Class A common stock offered by us | Up to an aggregate of 9,808,405 shares of Better Home & Finance Class A common stock, par value $0.0001 per share, which consists of (i) 6,075,047 shares of Better Home & Finance Class A common stock issuable upon exercise of Public Warrants and (ii) 3,733,358 shares of Better Home & Finance Class A common stock issuable upon exercise of Private Warrants. | |||||||

Shares of Better Home & Finance Class A common stock outstanding prior to exercise of Public Warrants and Private Warrants | 359,001,627 shares as of the close of business on December 1, 2023. | |||||||

Shares of Better Home & Finance Class A common stock outstanding assuming exercise of all Public Warrants and Private Warrants | 368,810,032 shares (based on total shares outstanding as of the close of business on December 1, 2023). | |||||||

Exercise price of Public Warrants and Private Warrants | $11.50 per share, subject to adjust as described herein. | |||||||

Use of proceeds | We will receive up to an aggregate of approximately $112.8 million from the exercise of the Public Warrants and the Private Warrants, assuming the exercise in full of all of the such warrants for cash. We expect to use the net proceeds from the exercise of such warrants for general corporate purposes. As of December 1, 2023, the closing price of Better Home & Finance Class A common stock as reported on Nasdaq was $0.453 per share, which is below the $11.50 exercise price of the Warrants. For so long as the Warrants remain “out-of-the-money,” we do not expect warrant holders to exercise their Warrants. See “Use of Proceeds” for further discussion. | |||||||

12

Offering and Resale of Better Home & Finance Class A common stock and Private Warrants | ||||||||

| Shares of Better Home & Finance Class A common stock offered by the Selling Securityholders | Up to an aggregate of 418,173,409 shares of Better Home & Finance Class A common stock, par value $0.0001 per share, which consists of (i) 53,665,365 shares of Better Home & Finance Class A common stock, acquired by the Selling Securityholders at prices ranging from $0.00003 per share to $10.00 per share, (ii) 288,897,403 shares of Better Home & Finance Class A common stock issuable upon conversion of Better Home & Finance Class B common stock, par value $0.0001 per share, acquired by the Selling Securityholders at prices ranging from $0.00003 per share to $8.01 per share, (iii) 71,877,283 shares of Better Home & Finance Class A common stock issuable upon conversion of Better Home & Finance Class C common stock, par value $0.0001 per share, acquired by the Selling Securityholders at prices ranging from $8.01 per share to $10.00, and (iv) 3,733,358 shares of Better Home & Finance Class A common stock issuable upon exercise of Private Warrants, acquired by the Selling Securityholders at prices ranging from $0.86 per warrant to $1.50 per warrant. The effective purchase price is calculated, if securities were acquired from Aurora or by its affiliates in connection with the Aurora IPO or before the Closing, based on the transaction acquisition cost or, if securities were acquired by holders of Better capital stock prior to the Business Combination, based on the weighted-average purchase price of such Better capital stock on an as-exchanged basis. | |||||||

Private Warrants offered by the Selling Securityholders | Up to 3,733,358 Private Warrants | |||||||

| Shares of Better Home & Finance Class A common stock outstanding | 359,001,627 shares as of the close of business on December 1, 2023. | |||||||

| Use of proceeds | We will not receive any proceeds from the sale of shares of Better Home & Finance Class A Common Stock or Private Warrants by the Selling Securityholders. | |||||||

Lock-up restrictions | ||||||||

Nasdaq ticker symbols | “BETR” and “BETRW” for Better Home & Finance Class A common stock and Warrants, respectively. | |||||||

The following table includes information relating to the Better Home & Finance Class A common stock and Warrants offered hereby, including the price each selling securityholder paid for its securities and the potential profit relating to such securities. The following table is derived in part from our internal records and is for illustrative purposes only. The table should not be relied upon for any purpose outside of its illustrative nature.

| Name of Selling Securityholder | Number of Offered Shares | Effective Purchase Price per Offered Share or Warrant | Potential Aggregate Profit of Offered Shares (1) | |||||||||||||||||

| Novator Capital Sponsor Ltd. | ||||||||||||||||||||

| Novator Exchange Agreement | 40,000,000 | $2.50 | * | |||||||||||||||||

| Sponsor Purchase Subscription Agreement | 1,700,000 | $10.00 | * | |||||||||||||||||

13

Merger Agreement | 3,471,946 | $0.004 | $1,558,904 | |||||||||||||||||

Merger Agreement | 636,240 | $9.785 | * | |||||||||||||||||

Merger Agreement (PublicWarrants) | 575,000 | $0.86 | * | |||||||||||||||||

Merger Agreement (Private Warrants) | 1,715,015 | $1.50 | * | |||||||||||||||||

| Unbound Holdco Ltd. | ||||||||||||||||||||

Merger Agreement | 1,159,375 | $0.004 | $520,559 | |||||||||||||||||

Merger Agreement | 1,000,000 | $9.785 | * | |||||||||||||||||

Merger Agreement (Private Warrants) | 1,143,343 | $1.50 | * | |||||||||||||||||

Merger Agreement (Public Warrants) | 250,000 | $0.86 | * | |||||||||||||||||

Entities Affiliated with Activant Capital Group LLC | 61,306,253 | $1.73 | * | |||||||||||||||||

| SVF Beaver II (DE) LLC | ||||||||||||||||||||

Merger Agreement | 55,188,435 | $8.01 | * | |||||||||||||||||

Merger Agreement | 6,877,283 | $8.01 | * | |||||||||||||||||

| Better Portfolio Holdings 1 LLC | 27,141,628 | $0.00003 | $12,294,343 | |||||||||||||||||

| LCG4 Best LP | 23,203,001 | $3.84 | * | |||||||||||||||||

| 1/0 Mortgage Investment LLC | 25,704,813 | $0.03 | $10,873,136 | |||||||||||||||||

| 1/0 Real Estate LLC | 6,522,761 | $0.32 | $867,527 | |||||||||||||||||

| BHFHC Distribution Trust | 65,000,000 | $10.00 | * | |||||||||||||||||

| Arnaud Massenet | ||||||||||||||||||||

Merger Agreement | 1,242,188 | $0.004 | $557,742 | |||||||||||||||||

Merger Agreement | 150,000 | $9.785 | * | |||||||||||||||||

Merger Agreement (Public Warrants) | 37,500 | $0.86 | * | |||||||||||||||||

| Michael Edelstein | 124,219 | $0.004 | $55,774 | |||||||||||||||||

| Prabhu Narasimhan | ||||||||||||||||||||

Merger Agreement | 828,125 | $0.004 | $371,828 | |||||||||||||||||

Merger Agreement | 50,000 | $9.785 | * | |||||||||||||||||

Merger Agreement | 12,500 | $0.86 | * | |||||||||||||||||

| Sangeeta Desai | 124,219 | $0.004 | $55,774 | |||||||||||||||||

| Zachary Frankel | 3,176,553 | $0.00003 | $1,438,883 | |||||||||||||||||

| Caroline Harding | 2,500 | $10.28 per unit | * | |||||||||||||||||

| Kevin Ryan | 527,961 | $1.66 | * | |||||||||||||||||

| Nicholas Calamari | 5,978,074 | $0.022 | $2,576,550 | |||||||||||||||||

| The Nicholas J Calamari Family Trust | 1,222,903 | $0.00003 | $553,938 | |||||||||||||||||

| Paula Tuffin | 246,515 | $0.20 | $62,368 | |||||||||||||||||

Technology Stock Holding Master Trust/Series Tuffin 2021 Trust | 822,125 | $0.01 | $364,201 | |||||||||||||||||

| Sigurgeir Jonsson | 5,973,526 | $0.32 | $794,479 | |||||||||||||||||

| The Sigurgeir Orn Jonsson 2020 Family Trust | 3,103,721 | $0.00003 | $1,405,893 | |||||||||||||||||

| The Anika G Austin Descendants Trust | 1,222,903 | $0.00003 | $553,938 | |||||||||||||||||

| Vishal Garg | 69,968,642 | $0.00003 | $31,693,696 | |||||||||||||||||

| Unnamed Selling Securityholder | 764,142 | $1.66 | * | |||||||||||||||||

_______________

*Represents no potential profit per share or a potential loss per share based on illustrative market price.

(1)The potential aggregate profits are calculated assuming that all shares of Better Home & Finance Class A common stock were sold at a price of $0.453 per share (the closing prices of Better Home & Finance Class A common stock on December 1, 2023). Shares underlying warrants are not reflected in the table above because the exercise price of $11.50 is greater than the closing price of Better Home & Finance Class A common stock on December 1, 2023. The trading price of Better Home & Finance Class A common stock may be different at the time a selling securityholder decides to sell its securities.

14

SUMMARY RISK FACTORS

You should consider all the information contained in this prospectus in deciding to invest in our securities offered under this prospectus. In particular, you should consider the risk factors described under “Risk Factors.” Such risks include, but are not limited to:

Risks relating to our history, business model, growth and financial condition, including:

•We have a history of operating losses, including very significant losses in 2022 and for the nine months ended September 30, 2023, have not been able to maintain profitability achieved in 2020 and early 2021, and may not achieve and maintain profitability in the future.

•We may be unable to effectively restore or manage our growth, including being able to fill certain senior management roles with suitable candidates, which could have a material adverse effect on our business, financial condition and results of operations.

•We may be unable to effectively maintain and develop certain relationships with third-party vendors and key commercial partners, which could have a material adverse effect on our ability to attract customers and grow our business.

•We depend on our ability to sell loans and MSRs in the secondary market to a limited number of loan purchasers, including government-sponsored enterprises and other secondary market participants for each relevant product.

•Better has identified three material weaknesses in its internal control over financial reporting and may identify additional material weaknesses in the future or otherwise fail to implement or maintain an effective system of internal control, which may result in material misstatements of financial statements on our part or cause us to fail to meet our periodic reporting obligations.

•Our compliance and risk management policies, procedures, and techniques may not be sufficient to identify all of the financial, legal, regulatory, and other risks to which we are exposed, and failure to identify and address such risks could result in substantial losses and materially and adversely disrupt our business operations.

•The Better Founder and CEO is involved in litigation that could have a material adverse effect on our revenues, financial condition, cash flows and results of operations.

Risks relating to our market, industry, and general economic conditions, including:

•Our business is significantly impacted by interest rates. Changes in prevailing interest rates or U.S. monetary policies that affect interest rates have and may in the future have a material adverse effect on our business, financial condition, results of operations, and prospects.

•We operate in a heavily regulated industry, and our loan production and servicing activities, real estate brokerage activities, title and settlement services activities and homeowners insurance agency activities expose us to risks of noncompliance with a large and increasing body of complex laws and regulations at the U.S. federal, state and local levels, which, at times, may be inconsistent.

•Our business is highly dependent on Fannie Mae and Freddie Mac and certain other U.S. government agencies, and any changes in these entities or agencies or their current roles could have a material adverse effect on our business.

Risks relating to our global operations, including:

•We have operations in the United Kingdom and India, which subject us to certain operational challenges, laws and regulations, and political or economic risks that we have limited experience in navigating; our

15

business and financial condition could be materially and adversely affected if we are unable to effectively manage these variables.

Risks relating to our products and customers, including:

•We face intense competition from other companies with more well established brands, and may not be able to retain or expand our customer base.

•Our failure to accurately predict demand or growth of new or existing product lines could materially and adversely affect our business, financial condition, results of operations, and prospects.

Risks relating to our technology and intellectual property, including:

•Our products use third-party software, hardware and services that may be difficult to replace or cause errors or failures of our products that could materially and adversely affect our business, financial condition, liquidity, results of operations, or prospects.

•We may not be able to effectively maintain and enforce our intellectual property and proprietary rights and may face allegations of infringement of the intellectual property rights of third parties, which could have a material adverse effect on our business, financial condition, results of operations, and prospects.

Risks relating to our indebtedness and warehouse lines of credit, including:

•We rely on our warehouse lines to fund loans and otherwise operate our business. If one or more facilities are terminated or otherwise become unavailable to use, we may be unable to find replacement financing at commercially favorable terms, or at all, which could have a material adverse effect on our business.

•Fluctuations in the interest rate of our facilities or the value of the collateral underlying certain of these facilities could have a material adverse effect on our liquidity.

Risks relating to the regulatory environment, including:

•The laws and regulations to which we are subject are constantly evolving, together with the scope of supervision, and we may be unable to comply with new laws and regulations effectively or in a timely manner, which could have a material adverse effect on our business.

•We are, and may in the future be, subject to government or regulatory investigations, litigation, or other disputes, including litigation by former senior employees. If the outcomes of these matters are adverse to us, it could materially and adversely affect our business, revenues, financial condition, results of operations, and prospects.

Risks related to ownership of Better Home & Finance common stock and Better Home & Finance operating as a public company, including:

•We may not recognize the anticipated benefits of the Business Combination and related transactions.

•We have received a notice from the listing qualifications staff of Nasdaq that we are currently not in compliance with the minimum bid price requirement set forth in Nasdaq Listing Rule 5450(a)(1) for continued listing. If we are unable to regain compliance, our common stock could be delisted, which could affect the price of our common stock and liquidity and reduce our ability to raise capital.

•Our management team has limited experience managing a public company.

•The existence of multiple classes of common stock may materially and adversely impact the value and liquidity of Better Home & Finance Class A common stock.

•Because we became a public reporting company by means other than a traditional underwritten initial public offering, our stockholders may face additional risks and uncertainties.

16

RISK FACTORS

You should carefully consider the risks and uncertainties described below and the other information in this prospectus before making an investment in Better Home & Finance Class A common stock or Warrants. Our business, financial condition, results of operations, or prospects could be materially and adversely affected if any of these risks occurs, and as a result, the market price of Better Home & Finance Class A common stock could decline and you could lose all or part of your investment. This prospectus also contains forward-looking statements that involve risks and uncertainties. See “Cautionary Statement Regarding Forward-Looking Statements.” Our actual results could differ materially and adversely from those anticipated in these forward-looking statements as a result of certain factors, including those set forth below.

RISKS RELATED TO BETTER HOME & FINANCE’S BUSINESS

Risks Related to Our Operating History, Business Model, Growth and Financial Condition

Since the third quarter of 2021, increased interest rates have negatively impacted our Funded Loan Volume, Gain on Sale Margin, revenue and profitability, which has resulted in significant strain on our business, results of operations and financial condition, which we have had limited success in managing.

We experienced rapid growth and increased demand for our product offerings through the first half of 2021, with a 393% increase in Funded Loan Volume in 2020 compared to 2019 and a 139% increase in Funded Loan Volume in 2021 compared to 2020, which significantly declined in 2022 and 2023 to date as described elsewhere in this section. During this period, our loan production was comprised more heavily of refinancing loans than home purchase loans (refinancing loans comprised approximately 85%, 80% and 45% of Funded Loan Volume in the years ended December 31, 2020, 2021 and 2022), which is more heavily weighted towards refinancing loans than the overall loan production market (based on industry averages of approximately 58% and 30% refinancing loans during the years ended December 31, 2021 and 2022, according to Fannie Mae).

In April 2021, the United States began experiencing what has become a significant rise in interest rates, which increased for a variety of reasons, including inflation, market capacity constraints and other factors. Accordingly, during 2021 and continuing in 2022 and 2023, we experienced both a significant decline in Funded Loan Volume as refinancing loans became less attractive as interest rates increased. Higher interest rates that initially materialized in the secondary market, including in our loan purchaser network, were not initially borne by our customers as increased mortgage rates, but rather reduced our Gain on Sale Margin as we sought to continue increasing our market share by offering more competitive pricing to customers in a more challenging market. Since the second quarter of 2021, our Gain on Sale Margin and later our Funded Loan Volume have remained depressed as a result of elevated interest rates, reduced loan market activity and increased competition in the market.