UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM

(Mark One)

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ___________________ to ___________________

Commission File Number:

(Exact Name of Registrant as Specified in its Charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

(Address of principal executive offices) |

(Zip Code) |

Registrant’s telephone number, including area code: (

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

|

The |

||

|

|

The |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

|

☐ |

|

Accelerated filer |

|

☐ |

|

☒ |

|

Smaller reporting company |

|

||

|

|

|

|

Emerging growth company |

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

As of May 16, 2024, the registrant had

Table of Contents

|

|

Page |

|

|

|

PART I. |

2 |

|

|

|

|

Item 1. |

2 |

|

|

2 |

|

|

3 |

|

|

Condensed Consolidated Statements of Changes In Stockholders’ Equity |

4 |

|

5 |

|

|

Notes to Unaudited Condensed Consolidated Financial Statements |

6 |

Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

26 |

Item 3. |

40 |

|

Item 4. |

40 |

|

|

|

|

PART II. |

42 |

|

|

|

|

Item 1. |

42 |

|

Item 1A. |

42 |

|

Item 2. |

42 |

|

Item 3. |

42 |

|

Item 4. |

42 |

|

Item 5. |

42 |

|

Item 6. |

43 |

|

44 |

||

i

PART I—FINANCIAL INFORMATION

Item 1. Condensed Consolidated Financial Statements (Unaudited).

SAB Biotherapeutics, Inc. and Subsidiaries

Condensed Consolidated Balance Sheets

|

|

March 31, |

|

|

December 31, |

|

||

|

|

(Unaudited) |

|

|

|

|

||

Assets |

|

|

|

|

|

|

||

Current assets |

|

|

|

|

|

|

||

Cash and cash equivalents |

|

$ |

|

|

$ |

|

||

Short-term investments |

|

|

|

|

|

|

||

Accrued interest receivable |

|

|

|

|

|

|

||

Prepaid expenses and other current assets |

|

|

|

|

|

|

||

Total current assets |

|

|

|

|

|

|

||

Deferred issuance cost |

|

|

|

|

|

|

||

Long-term prepaid insurance |

|

|

|

|

|

|

||

Long-term investments |

|

|

|

|

|

|

||

Operating lease right-of-use assets |

|

|

|

|

|

|

||

Financing lease right-of-use assets |

|

|

|

|

|

|

||

Property, plant and equipment, net |

|

|

|

|

|

|

||

Total assets |

|

$ |

|

|

$ |

|

||

Liabilities and Stockholders’ Equity |

|

|

|

|

|

|

||

Current liabilities |

|

|

|

|

|

|

||

Accounts payable |

|

$ |

|

|

$ |

|

||

Notes payable |

|

|

|

|

|

|

||

Operating lease liabilities, current portion |

|

|

|

|

|

|

||

Finance lease liabilities, current portion |

|

|

|

|

|

|

||

Deferred grant income |

|

|

|

|

|

|

||

Accrued expenses and other current liabilities |

|

|

|

|

|

|

||

Total current liabilities |

|

|

|

|

|

|

||

Operating lease liabilities, noncurrent |

|

|

|

|

|

|

||

Finance lease liabilities, noncurrent |

|

|

|

|

|

|

||

Warrant liabilities |

|

|

|

|

|

|

||

Total liabilities |

|

|

|

|

|

|

||

|

|

|

|

|

|

|||

Stockholders’ equity |

|

|

|

|

|

|

||

Preferred stock; $ |

|

|

|

|

|

|

||

Common stock; $ |

|

|

|

|

|

|

||

Treasury stock, at cost; |

|

|

( |

) |

|

|

( |

) |

Additional paid-in capital |

|

|

|

|

|

|

||

Accumulated other comprehensive income (loss) |

|

|

( |

) |

|

|

|

|

Accumulated deficit |

|

|

( |

) |

|

|

( |

) |

Total stockholders’ equity |

|

|

|

|

|

|

||

Total liabilities and stockholders’ equity |

|

$ |

|

|

$ |

|

||

*The condensed consolidated balance sheets' common stock share amounts have been retroactively adjusted to account for the Company's Reverse Stock Split, effective January 5, 2024.

See accompanying notes to the condensed consolidated financial statements

2

SAB Biotherapeutics, Inc. and Subsidiaries

Condensed Consolidated Statements of Operations

(Unaudited)

|

|

For The Three Months Ended March 31, |

|

|||||

|

|

2024 |

|

|

2023 |

|

||

Revenue |

|

|

|

|

|

|

||

|

$ |

|

|

$ |

|

|||

Total revenue |

|

|

|

|

|

|

||

Operating expenses |

|

|

|

|

|

|

||

Research and development |

|

|

|

|

|

|

||

General and administrative |

|

|

|

|

|

|

||

Total operating expenses |

|

|

|

|

|

|

||

Loss from operations |

|

|

( |

) |

|

|

( |

) |

Other income (expense) |

|

|

|

|

|

|

||

Changes in fair value of warrant liabilities |

|

|

|

|

|

|

||

Interest expense |

|

|

( |

) |

|

|

( |

) |

Interest income |

|

|

|

|

|

|

||

Other income |

|

|

|

|

|

— |

|

|

Total other income (expense) |

|

|

|

|

|

|

||

Loss before income taxes |

|

|

( |

) |

|

|

( |

) |

Net loss |

|

$ |

( |

) |

|

$ |

( |

) |

Other comprehensive loss: |

|

|

|

|

|

|

||

Unrealized gain (loss), change in fair value of available-for-sale securities, net of tax |

|

$ |

( |

) |

|

$ |

|

|

Foreign currency translation |

|

|

( |

) |

|

|

— |

|

Total comprehensive loss |

|

$ |

( |

) |

|

$ |

( |

) |

Loss per common share attributable to the Company’s shareholders |

|

|

|

|

|

|

||

Basic and diluted loss per common share |

|

$ |

( |

) |

|

$ |

( |

) |

Weighted-average common shares outstanding – basic and diluted |

|

|

|

|

|

|

||

*The condensed consolidated balance sheets' common stock share amounts have been retroactively adjusted to account for the Company's Reverse Stock Split, effective January 5, 2024.

See accompanying notes to the condensed consolidated financial statements

3

SAB Biotherapeutics, Inc. and Subsidiaries

Condensed Consolidated Statements of Changes In Stockholders’ Equity

(Unaudited)

|

|

|

Common stock |

|

|

Preferred Stock |

|

|

|

|

|

Treasury Stock |

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

Shares |

|

|

Amount |

|

|

Shares |

|

|

|

Amount |

|

|

Additional |

|

|

Shares |

|

|

Amount |

|

|

Accumulated |

|

|

Accumulated Other Comprehensive Income (Loss) |

|

|

Total Stockholders’ |

|

|||||||||||

Balance at December 31, 2022 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

( |

) |

|

|

( |

) |

|

|

( |

) |

|

|

— |

|

|

|

|

|||||||

Issuance of common stock for exercise of stock options |

|

|

|

|

|

|

— |

|

|

|

— |

|

|

— |

|

|

— |

|

|

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

|||

Professional fees settled with warrants |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

— |

|

|

— |

|

|

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

||

Stock-based compensation |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

— |

|

|

— |

|

|

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

||

Net loss |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

— |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

( |

) |

|

|

— |

|

|

|

( |

) |

Balance at March 31, 2023 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

( |

) |

|

|

( |

) |

|

|

( |

) |

|

|

— |

|

|

|

|

|||||||

Balance at December 31, 2023 |

|

|

|

|

|

$ |

|

|

|

|

|

|

$ |

|

|

$ |

|

|

|

( |

) |

|

$ |

( |

) |

|

$ |

( |

) |

|

$ |

|

|

$ |

|

||||||||

Stock-based compensation |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

|||

Issuance of common stock for exercise of stock options |

|

|

|

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

||||

Net loss |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

( |

) |

|

|

— |

|

|

|

( |

) |

|

Foreign currency translation |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

( |

) |

|

|

( |

) |

|

Unrealized gain (loss), change in fair value of available-for-sale securities |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

( |

) |

|

|

( |

) |

|

Balance at March 31, 2024 |

|

|

|

|

|

$ |

|

|

|

|

|

|

$ |

|

|

$ |

|

|

|

( |

) |

|

$ |

( |

) |

|

$ |

( |

) |

|

$ |

( |

) |

|

$ |

|

|||||||

*The condensed consolidated balance sheets' common stock share amounts have been retroactively adjusted to account for the Company's Reverse Stock Split, effective January 5, 2024.

See accompanying notes to the condensed consolidated financial statements.

4

SAB Biotherapeutics, Inc. and Subsidiaries

Condensed Consolidated Statements of Cash Flows

(Unaudited)

|

|

Three Months Ended March 31, |

|

|||||

|

|

2024 |

|

|

2023 |

|

||

Cash flows from operating activities: |

|

|

|

|

|

|

||

Net loss |

|

$ |

( |

) |

|

$ |

( |

) |

Adjustments to reconcile net loss to net cash used in operating activities: |

|

|

|

|

|

|

||

Depreciation and amortization |

|

|

|

|

|

|

||

Amortization of finance right-of-use assets |

|

|

|

|

|

|

||

Stock-based compensation expense |

|

|

|

|

|

|

||

Changes in fair value of warrant liabilities |

|

|

( |

) |

|

|

( |

) |

Accretion of discounts on short-term investments |

|

|

( |

) |

|

|

— |

|

Professional fees settled with equity instruments |

|

|

— |

|

|

|

|

|

Changes in operating assets and liabilities |

|

|

|

|

|

|

||

Accounts receivable |

|

|

— |

|

|

|

|

|

Prepaid expenses and other current assets |

|

|

( |

) |

|

|

|

|

Operating lease right-of-use assets |

|

|

( |

) |

|

|

|

|

Accrued interest receivable |

|

|

( |

) |

|

|

— |

|

Accounts payable |

|

|

|

|

|

( |

) |

|

Deferred grant income |

|

|

( |

) |

|

|

|

|

Accrued expense and other current liabilities |

|

|

( |

) |

|

|

( |

) |

Net cash used in operating activities |

|

|

( |

) |

|

|

( |

) |

|

|

|

|

|

|

|

||

Cash flows from investing activities: |

|

|

|

|

|

|

||

Purchases of equipment |

|

|

( |

) |

|

|

( |

) |

Purchases of investment securities |

|

|

( |

) |

|

|

— |

|

Net cash used in investing activities |

|

|

( |

) |

|

|

( |

) |

|

|

|

|

|

|

|

||

Cash flows from financing activities: |

|

|

|

|

|

|

||

Payment of deferred issuance costs |

|

|

( |

) |

|

|

— |

|

Payments of notes payable |

|

|

( |

) |

|

|

( |

) |

Principal payments on finance leases |

|

|

( |

) |

|

|

( |

) |

Proceeds from exercise of stock options |

|

|

|

|

|

|

||

Net cash used in financing activities |

|

|

( |

) |

|

|

( |

) |

|

|

|

|

|

|

|

||

Effect of exchange rate changes on cash and cash equivalents |

|

|

( |

) |

|

|

— |

|

|

|

|

|

|

|

|

||

Net decrease in cash and cash equivalents |

|

|

( |

) |

|

|

( |

) |

Cash and cash equivalents |

|

|

|

|

|

|

||

Beginning of period |

|

|

|

|

|

|

||

End of period |

|

$ |

|

|

$ |

|

||

Supplemental cash flow information: |

|

|

|

|

|

|

||

Cash paid for interest |

|

$ |

|

|

$ |

|

||

|

|

|

|

|

|

|

||

Supplemental information on non-cash investing and finance activities: |

|

|

|

|

|

|

||

Deferred issuance costs included in accounts payable and accrued expenses |

|

$ |

|

|

$ |

— |

|

|

See accompanying notes to the condensed consolidated financial statements.

5

SAb Biotherapeutics, Inc. and subsidiaries

Notes to condensed consolidated FINANCIAL statements (Unaudited)

(1) Nature of Business

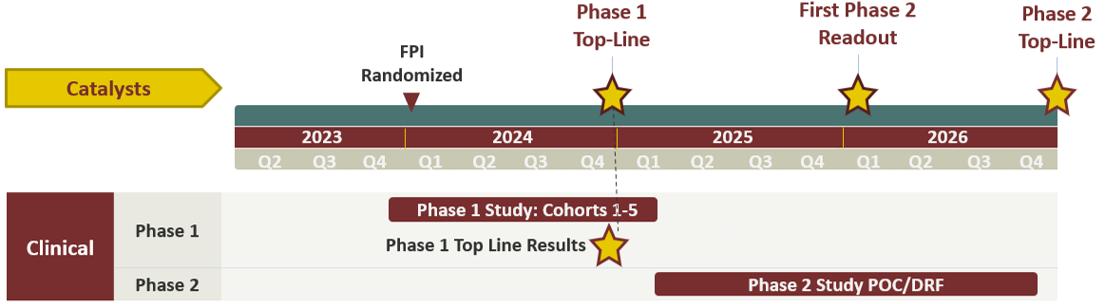

SAB Biotherapeutics, Inc., a Delaware corporation (“SAB” or “SAB Biotherapeutics”, and together with its subsidiaries, the “Company”), is a clinical-stage biopharmaceutical company focused on the development of human polyclonal immunotherapeutic antibodies, or human immunoglobulins (“hIgG”), to address immune system disorders and infectious diseases. The Company’s antibodies are both target-specific and polyclonal, meaning they are comprised of multiple hIgGs and can bind to multiple sites on specific immunogens, making them ideally suited to address the complexities associated with many immune-mediated disorders. The Company’s lead candidate, SAB-142 is a human anti-thymocyte globulin (“ATG”) focused on preventing or delaying the progression of type 1 diabetes (“T1D”).

Australian Research and Development Tax Credit

In June 2023, the Company formed a new subsidiary in Australia, SAB BIO PTY LTD, a proprietary limited company (“SAB Australia”), primarily to conduct preclinical and clinical activities for product candidates. SAB Australia’s research and development activities qualify for the Australian government’s tax credit program, which provides a

Liquidity

The accompanying unaudited condensed consolidated financial statements have been prepared assuming the Company will continue as a going concern, which contemplates continuity of operations, realization of assets and the satisfaction of liabilities and commitments in the normal course of business. The Company has experienced net losses, negative cash flows from operations and, as of March 31, 2024, had an accumulated deficit of $

On September 29, 2023, the Company entered into a securities purchase agreement with certain accredited investors (the “September 2023 Purchase Agreement”), pursuant to which the Company agreed to issue and sell shares of preferred stock and warrants, in a private placement which provides for up to $

Based on the Company’s current level of operating expenses, existing resources will be sufficient to cover operating cash needs through the twelve months following the date of this report. In the future, the Company may seek additional funding through a combination of equity or debt financings, or other third-party financing, collaborative or other funding arrangements. Should the Company seek additional financing from outside sources, the Company may not be able to raise such financing on terms acceptable to the Company or at all. If the Company is unable to raise additional capital when required or on acceptable terms, the Company may be required to scale back or discontinue the advancement of product candidates, reduce headcount, liquidate assets, file for bankruptcy, reorganize, merge with another entity, or cease operations.

(2) Summary of Significant Accounting Policies

A summary of the significant accounting policies applied in preparation of the accompanying condensed consolidated financial statements is set forth below.

Basis of presentation

The financial statements have been prepared in conformity with U.S. Generally Accepted Accounting Principles (“GAAP”) and include all adjustments necessary for the fair presentation of the Company’s financial position for the periods presented.

Emerging growth company status

The Company is an “emerging growth company,” as defined in Section 2(a) of the Securities Act of 1933, as amended (the “Securities Act”), as modified by the Jumpstart our Business Startups Act of 2012, (the “JOBS Act”), and it may take advantage of certain

6

exemptions from various reporting requirements that are applicable to other public companies that are not emerging growth companies including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in its periodic reports and proxy statements, and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved.

Further, Section 102(b)(1) of the JOBS Act exempts emerging growth companies from being required to comply with new or revised financial accounting standards until private companies (that is, those that have not had a Securities Act registration statement declared effective or do not have a class of securities registered under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) are required to comply with the new or revised financial accounting standards. The JOBS Act provides that a company can elect to opt out of the extended transition period and comply with the requirements that apply to non-emerging growth companies but any such election to opt out is irrevocable. The Company has elected not to opt out of such extended transition period which means that when a standard is issued or revised and it has different application dates for public or private companies, the Company, as an emerging growth company, can adopt the new or revised standard at the time private companies adopt the new or revised standard. This may make comparison of the Company’s financial statements with another public company which is neither an emerging growth company nor an emerging growth company which has opted out of using the extended transition period difficult or impossible because of the potential differences in accounting standards used.

Principles of consolidation

The accompanying condensed consolidated financial statements include the results of the Company and its wholly owned subsidiaries, SAB Sciences, Inc., SAB Capra, LLC, Aurochs, LLC, and SAB Australia. Intercompany balances and transactions have been eliminated in consolidation.

Significant risks and uncertainties

The Company’s operations are subject to a number of factors that can affect its operating results and financial condition. Such factors include, but are not limited to, the results of research and development efforts, clinical trial activities of the Company’s product candidates, the Company’s ability to obtain regulatory approval to market its product candidates, competition from products manufactured and sold or being developed by other companies, and the Company’s ability to raise capital.

The Company currently has no commercially approved products and there can be no assurance that the Company’s research and development will be successfully commercialized. Developing and commercializing a product requires significant time and capital and is subject to regulatory review and approval as well as competition from other biotechnology and pharmaceutical companies. The Company operates in an environment of rapid change and is dependent upon the continued services of its employees and obtaining and protecting intellectual property.

Funding from government grants is not guaranteed to cover all costs, and additional funding may be needed to cover operational costs as the Company moves forward to with its efforts to develop a commercially approved product.

Use of estimates

The preparation of financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenue and expenses and the disclosure of contingent assets and liabilities in the financial statements. The Company has used significant estimates in its determination of stock-based compensation assumptions, determination of the fair value of the Private Placement Warrant liabilities, determination of the incremental borrowing rate (“IBR”) used in the calculation of the Company’s right of use assets and lease liabilities, estimation of clinical and other accruals and the valuation allowance on deferred tax assets. Actual amounts realized may differ from these estimates.

Fair Value Measurements

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability (an exit price) in the principal or most advantageous market for the asset or liability in an orderly transaction between market participants on the measurement date. The following fair value hierarchy classifies the inputs to valuation techniques that would be used to measure fair value into one of three levels:

Level 1: Unadjusted quoted prices in active markets for identical assets or liabilities.

Level 2: Inputs other than quoted prices that are observable for the asset or liability, either directly or indirectly. These include quoted prices for similar assets or liabilities in active markets and quoted prices for identical or similar assets or liabilities in markets that are not active.

7

Level 3: Unobservable inputs that reflect the reporting entity’s own assumptions.

Certain of the Company’s financial instruments are not measured at fair value on a recurring basis but are recorded at amounts that approximate their fair value due to the short-term nature of their maturities, such as cash and cash equivalents, accrued interest receivable, accounts payable, notes payable and accrued expenses.

The Company accounts for warrants to purchase its common stock pursuant to Accounting Standards Codification (“ASC”) Topic 470, Debt (“ASC 470”), and ASC Topic 480, Distinguishing Liabilities from Equity (“ASC 480”), and classifies warrants for common stock as liabilities or equity. The warrants classified as liabilities are reported at their estimated fair value (see Note 13, Fair Value Measurements) and any changes in fair value are reflected in other income and expense. The warrants classified as equity are reported at their estimated relative fair value with no subsequent remeasurement. The Company’s outstanding warrants are discussed in more detail in Note 12, Warrants.

Deferred Issuance Costs

The Company capitalizes certain legal, professional accounting and other third-party fees that are directly associated with in-process equity financings as deferred issuance costs until such financings are consummated. After consummation of the equity financing, these costs are recorded in shareholders’ equity as a reduction of additional paid-in capital generated as a result of the issuance.

As of March 31, 2024, the Company had $

Cash, cash equivalents, and restricted cash

Cash and cash equivalents are comprised of cash and highly liquid investments with original maturities of 90 days or less at the date of purchase. Cash equivalents consist primarily of exchange-traded money market funds.

The Company is exposed to credit risk in the event of default by the financial institutions or the issuers of these investments to the extent the amounts on deposit or invested are in excess of amounts that are insured.

Short and long-term investments

The Company accounts for short-term investments in accordance with Accounting Standard Codification (ASC) Topic 320, Investments - Debt and Equity Securities. Management determines the appropriate classification of its investments at the time of purchase and reevaluates such determinations at each reporting period.

At March 31, 2024, the Company’s short and long-term investments consisted of U.S. treasury securities with original maturity exceeding 90 days and investments in exchange traded mutual funds. The Company classifies these securities as both current and non-current depending on their time to maturity.

Trading securities are measured at fair value with unrealized gains and losses reported within other income in the condensed consolidated statement of operations. Available-for-sale debt securities are measured at fair value with unrealized gains and losses reported in accumulated other comprehensive income (loss) in the condensed consolidated statement of operations. The Company considers all of its securities for which there is a determinable fair market value, and there are no restrictions on the Company’s ability to sell within the next twelve months, as available-for-sale securities.

The Company reviews its investments at each reporting date to identify and evaluate whether a decline in fair value below the amortized cost basis of available-for-sale securities is due to credit-related factors and determines if such unrealized losses are the result of credit losses that require impairment. Factors considered in determining whether an unrealized loss is the result of a credit loss or other factors include the extent to which the fair value is less than the cost basis, any changes to the rating of the security by a rating agency, the financial condition and near-term prospects of the issuer, any historical failure of the issuer to make scheduled interest or principal payments, any adverse legal or regulatory events affecting the issuer or issuer’s industry, any significant deterioration in economic condition and the Company’s intent and ability to hold the investment for a period of time sufficient to allow for any anticipated recovery in market value.

The Company did

Concentration of credit risk

The Company maintains its cash and cash equivalent balances in the form of business checking accounts and money market accounts, the balances of which, at times, may exceed federally insured limits. Although the Company currently believes that the financial

8

institutions with whom it does business will be able to fulfill their commitments to the Company, there is no assurance that those institutions will be able to continue to do so. The Company has not experienced any credit losses associated with its balances in such accounts for the three months ended March 31, 2024 and 2023.

Lease liabilities and right-of-use assets

The Company is party to certain contractual arrangements for equipment, lab space, and an animal facility, which meet the definition of leases under Financial Accounting Standards Board (“FASB”) ASC Topic 842, Leases (“ASC 842”). In accordance with ASC 842, the Company recorded right-of-use assets and related lease liabilities for the present value of the lease payments over the lease terms. The Company’s IBR was used in the calculation of its right-of-use assets and lease liabilities.

The Company elected not to apply the recognition requirements of ASC 842 to short-term leases, which are deemed to be leases with a lease term of twelve months or less. Instead, the Company recognized lease payments in the Condensed Consolidated Statements of Operations on a straight-line basis over the lease term and variable payments in the period in which the obligation for these payments was incurred. The Company elected this policy for all classes of underlying assets.

Research and development expenses

Expenses incurred in connection with research and development activities are expensed as incurred. These include licensing fees to use certain technology in the Company’s research and development projects, fees paid to consultants and various entities that perform certain research and testing on behalf of the Company, and expenses related to animal care, research-use equipment depreciation, salaries, benefits, and stock-based compensation granted to employees in research and development functions.

During the three months ended March 31, 2024 and 2023, the Company had contracts with multiple contract research organizations (“CRO”) to complete studies as part of research grant agreements. These costs include upfront, milestone and monthly expenses as well as reimbursement for pass through costs. All research and development costs are expensed as incurred except when the Company is accounting for nonrefundable advance payments for goods or services to be used in future research and development activities. In these cases, these payments are capitalized at the time of payment and expensed in the period the research and development activity is performed. As actual costs become known, the Company will adjust the accrual; such changes in estimate may be a material change in the Company’s clinical study accrual, which could also materially affect reported results of operations. For the three months ended March 31, 2024 and 2023, there were no material adjustments to the Company’s prior period estimates of accrued expenses for clinical trials.

Property, Plant and Equipment

The Company records property, plant, and equipment at cost less depreciation and amortization. Depreciation is calculated using straight-line methods over the following estimated useful lives:

Animal facility equipment |

|

Laboratory equipment |

|

Leasehold improvements |

|

Office furniture and equipment |

|

Vehicles |

Repairs and maintenance expenses are expensed as incurred.

Impairment of long-lived assets

The Company reviews the recoverability of long-lived assets, including the related useful lives, whenever events or changes in circumstances indicate that the carrying amount of a long-lived asset may not be recoverable. If necessary, the Company compares the estimated undiscounted future net cash flows to the related asset’s carrying value to determine whether there has been an impairment. If an asset is considered impaired, the asset is written down to fair value, which is based either on discounted cash flows or appraised values in the period the impairment becomes known. The Company believes that long-lived assets are recoverable, and

Stock-based compensation

FASB ASC Topic 718, Compensation– Stock Compensation, prescribes accounting and reporting standards for all share-based payment transactions in which employee and non-employee services are acquired. The Company recognizes compensation cost relating to stock-based payment transactions using a fair-value measurement method, which requires all stock-based payments to

9

employees, directors, and non-employee consultants, including grants of stock options, to be recognized in operating results as compensation expense based on fair value over the requisite service period of the awards. The Company determines the fair value of common stock based on the closing market price at closing on the date of the grant.

In determining the fair value of stock-based awards, the Company utilizes the Black-Scholes option-pricing model, which uses both historical and current market data to estimate fair value. The Black-Scholes option-pricing model incorporates various assumptions, such as the value of the underlying common stock, the risk-free interest rate, expected volatility, expected dividend yield, and expected life of the options. For awards with performance-based vesting criteria, the Company estimates the probability of achievement of the performance criteria and recognizes compensation expense related to those awards expected to vest. No awards may have a term in excess of

Income taxes

Deferred income taxes reflect future tax effects of temporary differences between the tax and financial reporting basis of the Company’s assets and liabilities measured using enacted tax laws and statutory tax rates applicable to the periods when the temporary differences will affect taxable income. When necessary, deferred tax assets are reduced by a valuation allowance, to reflect realizable value, and all deferred tax balances are reported as long-term on the condensed consolidated balance sheet. Accruals are maintained for uncertain tax positions, as necessary.

The Company uses a recognition threshold and measurement attribute for the financial statement recognition and measurement of a tax position taken, or expected to be taken, in a tax return. The Company has elected to treat interest and penalties related to income taxes, to the extent they arise, as a component of income taxes.

Revenue recognition

The Company’s revenue is primarily generated through grants from government and other (non-government) organizations.

Grant revenue is recognized during the period that the research and development services occur, as qualifying expenses are incurred, or conditions of the grants are met. Deferred grant income represents grant proceeds received by the Company prior to the period in which the research and development services occur, as qualifying expenses are incurred, or conditions of the grants are met. The Company concluded that payments received under these grants represent conditional, nonreciprocal contributions, as described in ASC 958, Not-for-Profit Entities, and that the grants are not within the scope of ASC 606, Revenue from Contracts with Customers, as the organizations providing the grants do not meet the definition of a customer. Expenses for grants are tracked by using a project code specific to the grant, and the employees also track hours worked by using the project code.

Foreign Currency Translations and Transactions

Assets and liabilities of the Company's foreign subsidiary are translated at the year-end exchange rate. Operating results of the Company's foreign subsidiary are translated at average exchange rates during the period. Translation adjustments have no effect on net loss and are included in “Accumulated other comprehensive loss, net” in the accompanying Consolidated Balance Sheets.

Comprehensive income (loss)

Comprehensive income (loss) includes net loss as well as other changes in stockholders’ equity that result from transactions and economic events other than those with stockholders. The Company’s foreign currency translation adjustments of $

Litigation

From time to time, the Company is involved in legal proceedings, investigations and claims generally incidental to its normal business activities. In accordance with U.S. GAAP, the Company accrues for loss contingencies when it is probable that a liability has been incurred and the amount of the loss can be reasonably estimated. Legal costs in connection with loss contingencies are expensed as incurred.

10

Earnings per share

In accordance with ASC 260, Earnings per Share (“ASC 260”), basic net income (loss) per share attributable to common stockholders is computed by dividing net income (loss) attributable to common stockholders by the weighted-average number of common stock outstanding during the period. Diluted net income (loss) per share attributable to common stockholders is computed by dividing the diluted net income (loss) attributable to common stockholders by the weighted-average number of common stock outstanding for the period including potential dilutive common shares such as stock options.

Segment reporting

In accordance with ASC 280, Segment Reporting, the Company’s business activities are organized into

Australian Research and Development Tax Credit

The Company recognizes other income from Australian research and development incentives when there is reasonable assurance that the income will be received, the relevant expenditure has been incurred, and the consideration can be reliably measured. The research and development incentive is one of the key elements of the Australian Government’s support for Australia’s innovation system and is supported by legislative law primarily in the form of the Australian Income Tax Assessment Act 1997, as long as eligibility criteria are met. Under the program, a percentage of eligible research and development expenses incurred by the Company through its subsidiary in Australia are reimbursed.

Management has assessed the Company’s research and development activities and expenditures to determine which activities and expenditures are likely to be eligible under the research and development incentive regime described above. At each period end, management estimates the refundable tax offset available to the Company based on available information at the time and it is included in other income in the condensed consolidated statements of operations.

Retroactive Adjustments for Common Stock Reverse Split

On January 5, 2024, the Company completed a reverse stock split of the Company’s Common Stock. As a result of the Reverse Stock Split, every ten of the Company’s issued shares of Common Stock were automatically combined into one issued share of Common Stock, without any change to the par value per share. All share and per share numbers in this Form 10-Q have been adjusted to reflect the Reverse Stock Split.

(3) New accounting standards

Recently Issued Accounting Standards

On March 29, 2024, the FASB issued ASU 2024-02 “Codification Improvements” (“ASU 2024-02”) which amends the Codification to remove references to various concepts statements and impacts a variety of topics in the Codification. The amendments apply to all reporting entities within the scope of the affected accounting guidance, but in most instances the references removed are extraneous and not required to understand or apply the guidance. Generally, the amendments in ASU 2024-02 are not intended to result in significant accounting changes for most entities. ASU 2024-02 is effective January 1, 2025 and is not expected to have a significant impact on the Company’s financial statements.

(4) Revenue

During the three months ended March 31, 2024 and 2023, the Company recognized revenue from the following grants:

Government grants

Total revenue recognized from government grants was approximately $

National Institute of Health - National Institute of Allergy and Infectious Disease (“NIH-NIAID”) (Federal Award #1R41AI131823-02) – this grant was for approximately $

11

NIH-NIAID through Geneva Foundation (Federal Award #1R01AI132313-01, Subaward #S-10511-01) – this grant was for approximately $

US Department of Defense (“DoD”), Joint Program Executive Office for Chemical, Biological, Radiological and Nuclear Defense Enabling Biotechnologies (“JPEO”) through Advanced Technology International – this grant was for a potential of $

The grants for the Company’s Rapid Response contract with JPEO (the “JPEO Rapid Repsonse Contact”) are cost reimbursement agreements, with reimbursement of qualified direct research and development expense (labor and consumables) with an overhead charge (based on actual, reviewed quarterly) and a fixed fee (

On August 3, 2022, the Company received notice from the DoD terminating the JPEO Rapid Response contract (the “JPEO Rapid Response Contract Termination”). The Company engaged in negotiations with the DoD to compensate the Company for services provided prior to the JPEO Rapid Response Contract Termination and costs the Company would be expected to bear in future periods. A termination and settlement proposal was submitted to the DoD on September 9, 2022; the Company submitted a final invoice on December 15, 2022; and received payment from the DoD on or about January 12, 2023. The terms of the arrangement provide for a cost-reimbursable structure, and state that the parties will work in good faith equitable reimbursement for work performed toward accomplishment of the tasks provided in the agreement. At this time, other than certain deferred obligations (presented within deferred grant income within the Company’s condensed consolidated unaudited balance sheet) potentially payable to the DoD solely due to subsequent negotiations with third-party vendors, the Company believes and has been advised there is a reasonable, good faith basis for the position that no present or future obligations exist. Revenue recognized subsequent to the JPEO Rapid Response Contract Termination relates to satisfaction of residual obligations under the termination and settlement agreement—see Note 2, Summary of Significant Accounting Policies for further information about the Company’s established revenue recognition process.

(5) Earnings per share

The following is a reconciliation of the numerator and denominator used to calculate basic earnings per share and diluted earnings per share for the three months ended March 31, 2024 and 2023:

|

|

For The Three Months Ended March 31, |

|

|||||

|

|

2024 |

|

|

2023 |

|

||

Calculation of basic and diluted loss per share |

|

|

|

|

|

|

||

Net loss attributable to the Company’s shareholders |

|

$ |

( |

) |

|

$ |

( |

) |

Weighted-average common shares outstanding – |

|

|

|

|

|

|

||

Net loss per share, basic and diluted |

|

$ |

( |

) |

|

$ |

( |

) |

The Company’s potentially dilutive securities, which include stock options, restricted stock awards, common stock warrants, earnout shares, and contingently issuable earnout shares have been excluded from the computation of diluted net loss per share as the effect would be to reduce the net loss per share. Therefore, the weighted average number of common shares outstanding used to calculate both basic and diluted net loss per share attributable to common stockholders is the same.

12

|

|

For The Three Months Ended March 31, |

|

|||||

|

|

2024 |

|

|

2023 |

|

||

Stock options and awards |

|

|

|

|

|

|

||

Convertible Debt |

|

|

|

|

|

|

||

Common Stock Warrants (1) |

|

|

|

|

|

|

||

Series A Preferred Stock (2) |

|

|

|

|

|

— |

|

|

Preferred Stock Warrants (3) |

|

|

|

|

|

— |

|

|

Contingently issuable Earnout Shares from unexercised Rollover |

|

|

|

|

|

|

||

Total |

|

|

|

|

|

|

||

(6) Property, plant and equipment

As of March 31, 2024 and December 31, 2023, the Company’s property, plant and equipment was as follows:

|

|

March 31, |

|

|

December 31, |

|

||

Laboratory equipment |

|

$ |

|

|

$ |

|

||

Animal facility leasehold improvements |

|

|

|

|

|

|

||

Animal facility equipment (1) |

|

|

|

|

|

|

||

Construction-in-progress |

|

|

|

|

|

|

||

Leasehold improvements (1) |

|

|

|

|

|

|

||

Vehicles |

|

|

|

|

|

|

||

Office furniture and equipment (1) |

|

|

|

|

|

|

||

Total Property, plant and equipment, gross |

|

|

|

|

|

|

||

Less: accumulated depreciation and amortization |

|

|

( |

) |

|

|

( |

) |

Property, plant and equipment, net |

|

$ |

|

|

$ |

|

||

(1) The Company re-classed $

Depreciation and amortization expense was $

All tangible personal property with a useful life of at least

(7) Leases

The Company has an operating lease for lab space from Sanford Health, under a lease that started in June 2014 and initially ended in June 2019, at which time the lease was extended through August 2024. This lease can be terminated with

13

notice. This lease was amended again in October 2022 to reduce the Company’s leased area to

The Company entered into a lease for office, laboratory, and warehouse space in November 2020, which was amended in July 2022 to add additional administrative and lab space. This amended lease has a

The Company has the following finance leases:

The lease agreements do not require material variable lease payments, residual value guarantees or restrictive covenants.

The amortizable lives of the operating lease assets are limited by their expected lease terms. The amortizable lives of the finance lease assets are limited by their expected lives, as the Company intends to exercise the purchase options at the end of the leases. The following is the estimated useful lives of the finance lease assets:

Animal Facility |

|

Equipment |

|

Land |

Indefinite |

The Company’s weighted-average remaining lease term and weighted-average discount rate for operating and finance leases as of March 31, 2024 are:

|

|

Operating |

|

|

Finance |

|

||

Weighted-average remaining lease term |

|

|

|

|

||||

Weighted-average discount rate |

|

|

% |

|

|

% |

||

14

The table below reconciles the undiscounted future minimum lease payments under non-cancelable leases with terms of more than one year to the total lease liabilities recognized on the condensed consolidated balance sheets as of March 31, 2024:

|

|

Operating |

|

|

Finance |

|

||

2024 — remaining |

|

$ |

|

|

$ |

|

||

2025 |

|

|

|

|

|

|

||

2026 |

|

|

|

|

|

|

||

2027 |

|

|

— |

|

|

|

|

|

2028 |

|

|

— |

|

|

|

|

|

Thereafter |

|

|

— |

|

|

|

|

|

Undiscounted future minimum lease payments |

|

|

|

|

|

|

||

Less: Amount representing interest payments |

|

|

( |

) |

|

|

( |

) |

Total lease liabilities |

|

|

|

|

|

|

||

Less current portion |

|

|

( |

) |

|

|

( |

) |

Noncurrent lease liabilities |

|

$ |

|

|

$ |

|

||

Operating lease expense was approximately $

Finance lease costs for the three months ended March 31, 2024 and 2023 included approximately $

Cash payments under operating and finance leases were approximately $

(8) Accrued Expenses and Other Current Liabilities

As of March 31, 2024 and December 31, 2023, accrued expenses and other current liabilities consisted of the following:

|

|

March 31, |

|

|

December 31, |

|

||

Payroll and employee-related costs |

|

$ |

|

|

$ |

|

||

Accrued research and development expenses |

|

|

|

|

|

|

||

Accrued legal fees |

|

|

|

|

|

|

||

Accrued financing fees payable |

|

|

|

|

|

|

||

Accrued interest |

|

|

|

|

|

|

||

Other accrued expenses |

|

|

|

|

|

|

||

|

|

$ |

|

|

$ |

|

||

(9) Notes Payable

8% Unsecured Convertible Note

Pursuant to the fourth amendment to the Company’s lease with Sanford Health, the Company and Sanford Health agreed to a period of abated rent (the “Abated Rent”) from October 1, 2022 to September 30, 2023. In exchange for the Abated Rent, effective as of October 1, 2022, the Company issued to Sanford Health an

Pursuant to the 8% Unsecured Convertible Note, the Company shall pay the sum of approximately $

15

The Company evaluated the treatment of the 8% Unsecured Convertible Note under ASC 470 and determined the Principal in its entirety would be allocated to debt. The Company’s condensed consolidated balance sheet as of March 31, 2024 includes accrued interest relating to the 8% Unsecured Convertible Note of approximately $

Insurance Financing

The Company obtained financing for certain Director & Officer liability insurance policy premiums. The agreement assigns First Insurance Funding (“Lender”) a first priority lien on and security interest in the financed policies and any additional premium required in the financed policies including (a) all returned or unearned premiums, (b) all additional cash contributions or collateral amounts assessed by the insurance companies in relation to the financed policies and financed by Lender, (c) any credits generated by the financed policies, (d) dividend payments, and (e) loss payments which reduce unearned premiums. If any circumstances exist in which premiums related to any Financed Policy could become fully earned in the event of loss, Lender shall be named a loss-payee with respect to such policy.

The total premiums, taxes and fees financed is approximately $

(10) Stockholders’ Equity

Authorized and Outstanding Capital Stock

The total number of shares of the Company’s authorized capital stock is

Series A Preferred Stock

On September 29, 2023, the Company entered into a securities purchase agreement (the “September 2023 Purchase Agreement”) with certain accredited investors, pursuant to which the Company agreed to issue and sell, in a private placement (the “September 2023 Offering”), (i)

On October 3, 2023, the Company closed on the issuance of the

The Company recorded $

Subject to the terms and limitations contained in the Certificate of Designation of Preferences, Rights and Limitations of the Series A Convertible Voting Preferred Stock (the “Certificate of Designation”):

16

Prior to the extended mandatory exercise time of certain Preferred Tranche A Warrants, certain investors informed the Company that they would not exercise such warrants. Certain other investors in the offering agreed to assume and exercise

Pursuant to the Certificate of Designation, all shares of Series A-1 Preferred Stock, subject to the Stockholder Approval obtained in November 2023, were automatically converted into an aggregate of

Following Shareholder Approval of the September 2023 Offering, on November 22, 2023, the Company issued

For information pertaining to the Company’s outstanding warrants to purchase shares of the Company’s preferred stock, see Note 12, Warrants.

Earnout Shares

On October 22, 2021 (the “Closing Date”), the Company consummated the business combination (the “Business Combination”) contemplated by the agreement and plan of merger, dated as of June 21, 2021, as amended on August 12, 2021, made by and among Big Cypress Acquisition Corp., a Delaware corporation (“BCYP”), Big Cypress Merger Sub Inc., a Delaware corporation (“Merger Sub”), the Company, and Shareholder Representative Services LLC, a Colorado limited liability company, solely in its capacity as the representative, agent and attorney-in-fact of the SAB Stockholders (the “Business Combination Agreement ”). Upon closing of the Business Combination, Merger Sub merged with SAB Biotherapeutics, with SAB Biotherapeutics as the surviving company of the merger. Upon closing of the Business Combination, BCYP changed its name to “SAB Biotherapeutics, Inc.”.

Additionally, the Business Combination Agreement included an earnout provision whereby the shareholders of SAB Biotherapeutics shall be entitled to receive additional consideration (“Earnout Shares”) if the Company meets certain Volume Weighted Average Price (“VWAP") thresholds, or a change in control with a per share price exceeding the VWAP thresholds within a five-year period immediately following the Closing.

The Earnout Shares shall be released in four equal increments as follows:

17

Pursuant to the terms of the Business Combination Agreement, SAB Biotherapeutics’ securityholders (including vested option holders) who own SAB Biotherapeutics securities immediately prior to the Closing Date will have the contingent right to receive their pro rata portion of (i) an aggregate of

The Earnout Shares are indexed to the Company’s equity and meet the criteria for equity classification. On the Closing Date, the fair value of the

Sales Agreement

As previously disclosed, on January 26, 2024, the Company entered into a Controlled Equity Offering Sales Agreement (the “Sales Agreement”) with Cantor Fitzgerald & Co. (“Cantor”), relating to shares of common stock. In accordance with the terms of the Sales Agreement, the Company may offer and sell shares of our common stock having an aggregate offering price of up to $

(11) Stock Option Plans

On August 5, 2014, the Company approved a stock option grant plan (the “2014 Equity Incentive Plan”) for employees, directors, and non-employee consultants, which provides for the issuance of options to purchase common stock. As of March 31, 2024, there were

The Company adopted the 2021 Omnibus Equity Incentive Plan (the “2021 Equity Incentive Plan”, and collectively with the 2014 Equity Incentive Plan, the “Equity Compensation Plans”), which reserved

The expected term of the stock options was estimated using the “simplified” method, as defined by the SEC’s Staff Accounting Bulletin No. 107, Share-Based Payment. The volatility assumption was determined by examining the historical volatilities for industry peer companies, as the Company does not have sufficient trading history for its common stock. The risk-free interest rate assumption is based on the U.S. Treasury instruments whose term was consistent with the expected term of the options. The dividend assumption is based on the Company’s history and expectation of dividend payouts. The Company has never paid dividends on its common stock and does not anticipate paying dividends on its common stock in the foreseeable future. Therefore, the Company has assumed no dividend yield for purposes of estimating the fair value of the options.

18

Stock Options

Stock option activity for employees and non-employees under the Equity Compensation Plans for the three months ended March 31, 2024 was as follows:

|

|

Options |

|

|

Weighted |

|

|

Weighted Average Remaining Contractual Life (periods) |

|

|

Aggregate Intrinsic Value |

|

||||

Outstanding options, December 31, 2023 |

|

|

|

|

$ |

|

|

|

|

|

$ |

|

||||

Granted |

|

|

|

|

$ |

|

|

|

|

|

|

|

||||

Forfeited |

|

|

( |

) |

|

$ |

|

|

|

|

|

|

|

|||

Exercised |

|

|

( |

) |

|

$ |

|

|

|

|

|

|

|

|||

Expired |

|

|

( |

) |

|

$ |

|

|

|

|

|

|

|

|||

Outstanding options, March 31, 2024 |

|

|

|

|

$ |

|

|

|

|

|

$ |

— |

|

|||

Options vested and exercisable, March 31, 2024 |

|

|

|

|

$ |

|

|

|

|

|

$ |

— |

|

|||

Total unrecognized compensation cost related to non-vested stock options as of March 31, 2024 was approximately $

The weighted average grant date fair value of options granted during the three months ended March 31, 2024 and 2023, was $

The estimated fair value of stock options granted to employees and consultants during the three months ended March 31, 2024 and 2023, were calculated using the Black-Scholes option-pricing model using the following assumptions:

|

|

For The Three Months Ended March 31, |

||||||||

|

|

2024 |

|

2023 |

||||||

Expected volatility |

|

|

% |

|

|

% |

||||

Weighted-average volatility |

|

|

|

% |

|

|

|

% |

||

Expected dividends |

|

— |

|

% |

|

— |

|

% |

||

Expected term (in periods) |

|

|

|

|

|

|

||||

Risk-free rate |

|

|

% |

|

|

% |

||||

Restricted Stock

Stock award activity for employees and non-employees under the Equity Compensation Plans for the three months ended March 31, 2024 was as follows:

|

|

Number of shares |

|

|

Weighted |

|

||

Unvested as of December 31, 2023 |

|

|

|

|

$ |

|

||

Vested |

|

|

( |

) |

|

$ |

|

|

Unvested as of March 31, 2024 |

|

|

|

|

$ |

|

||

At March 31, 2024, the Company had an aggregate of $

19

Stock-based compensation expense

Stock-based compensation expense for the three months ended March 31, 2024 and 2023 was as follows:

|

|

For The Three Months Ended March 31, |

|

|||||

|

|

2024 |

|

|

2023 |

|

||

Research and development |

|

$ |

|

|

$ |

|

||

General and administrative |

|

|

|

|

|

|

||

Total |

|

$ |

|

|

$ |

|

||

(12) Warrants

Public Warrants

Each whole Public Warrant entitles the holder to purchase

Once the warrants become exercisable, the Company may call the warrants for redemption:

If the Company calls the warrants for redemption as described above, management will have the option to require any holder that wishes to exercise its warrant to do so on a “cashless basis.” If management takes advantage of this option, all holders of warrants would pay the exercise price by surrendering their warrants for that number of shares of common stock equal to the quotient obtained by dividing (x) the product of the number of shares of common stock underlying the warrants, multiplied by the excess of the “fair market value” (defined below) over the exercise price of the warrants by (y) the fair market value. The “fair market value” shall mean the average reported last sale price of the common stock for the 10 trading days ending on the third trading day prior to the date on which the notice of redemption is sent to the holders of warrants.

Private Placement Warrants

The Private Placement Warrants and the common stock issuable upon the exercise of the Private Placement Warrants were not transferable, assignable or saleable until after the completion of the Company's merger transaction in 2021. Additionally, the Private Placement Warrants are exercisable on a cashless basis and will be non-redeemable as long as they are held by the initial purchasers or their permitted transferees. If the Private Placement Warrants are held by someone other than the initial purchasers or their permitted transferees, the Private Placement Warrants will be redeemable by the Company and exercisable by such holders on the same basis as the Public Warrants.

PIPE Warrants and PIPE Placement Agent Warrants

In December 2022, the Company entered into a securities purchase agreement with certain institutional and accredited investors for the sale by the Company of

20

2023 Ladenburg Agreement Warrants

On March 21, 2023, the Company entered into a settlement agreement with Ladenburg Thalmann & Co. Inc. (“Ladenburg”), effective March 23, 2023 (the “2023 Ladenburg Agreement”, regarding the action brought by Ladenburg, the “Ladenburg Action”). In connection with the 2023 Ladenburg Agreement, on March 24, 2023, the Company (i) issued the Ladenburg Warrants to purchase up to

September 2023 Purchase Agreement Warrants

As of March 31, 2024, the Company had outstanding

Both the Tranche B Warrants and Tranche C Warrants were classified as derivative liabilities because they are redeemable for cash upon occurrence of a Fundamental Transaction, (as defined in the Forms for such warrants), which may be outside the control of the Company.

Preferred PIPE Placement Agent Warrant

On November 21, 2023, the Company issued to Chardan Capital Markets LLC, the placement agent for the September 2023 Offering, a warrant to purchase

The following table summarizes warrant activity for the three months ended March 31, 2024:

|

|

Outstanding |

|

|

Warrants Issued |

|

|

Warrants Exercised |

|

|

Warrants Forfeited |

|

|

Outstanding |

|

|||||

Transaction |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Business Combination Public Warrants |

|

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

||

Private Placement Warrants |

|

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

||

PIPE Warrants |

|

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

||

PIPE Placement Agent Warrants |

|

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

||

Ladenburg Warrants |

|

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

||

Tranche B Warrants |

|

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

||

Tranche C Warrants |

|

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

||

Preferred PIPE Placement Agent Warrants |

|

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

||

Presentation and Valuation of the Warrants — Liability Classified Warrants

Public Warrants and Private Placement Warrants

The Public Warrants and Private Placement Warrants are accounted for as liabilities in accordance with ASC 815-40, Derivatives and Hedging—Contracts in Entity’s Own Equity and were presented within warrant liabilities on the condensed consolidated balance sheets as of March 31, 2024 and December 31, 2023. The initial fair value of the warrant liabilities was measured at fair value at the Closing Date, and changes in the fair value of the warrant liabilities were presented within changes in fair value of warrant liabilities in the condensed consolidated statements of operations for three months ended March 31, 2024 and 2023.

21

On the Closing Date, the Company established the fair value of the Private Placement Warrants utilizing both the Black-Scholes Merton formula and a Monte Carlo Simulation (the “MCS”) analysis. Specifically, the Company considered an MCS to derive the implied volatility in the publicly-listed price of the Public Warrants. The Company then considered this implied volatility in selecting the volatility for the application of a Black-Scholes Merton model for the Private Placement Warrants. The Company determined the fair value of the Public Warrants by reference to the quoted market price.

The Public Warrants were classified as a Level 1 fair value measurement, due to the use of the quoted market price, and the Private Placement Warrants held privately by assignees of Big Cypress Holdings LLC, were classified as a Level 3 fair value measurement, due to the use of unobservable inputs. See Note 13, Fair Value Measurements, for changes in fair value of the Private Placement Warrants.

The key inputs into the valuations as of March 31, 2024 and December 31, 2023 were as follows:

|

|

March 31, |

|

|

December 31, |

|

||

Risk-free interest rate |

|

|

% |

|

|

% |

||

Expected term remaining (periods) |

|

|

|

|

|

|

||

Implied volatility |

|

|

% |

|

|

% |

||

Closing common stock price on the measurement date |

|

$ |

|

|

$ |

|

||

Preferred Warrants

Should the Company enter into or be party to a fundamental transaction, the Company will be required to purchase all outstanding Warrants from the holders by paying cash in an amount equal to the Black Scholes Value of the unexercised portion of each Preferred Warrant. As a result, the Preferred Warrants are accounted for as derivative liabilities in accordance with ASC 480 and ASC 815-40, Derivatives and Hedging—Contracts in Entity’s Own Equity and were presented within warrant liabilities on the condensed consolidated balance sheet as of March 31, 2024 and December 31, 2023. The initial fair value of the warrant liabilities was measured at fair value at the Closing Date, and changes in the fair value of the warrant liabilities were presented within changes in fair value of warrant liabilities in the condensed consolidated statement of operations for the three months ended March 31, 2024 and 2023.

The Company established the fair value of the Preferred Warrants utilizing the Black-Scholes Merton formula.

All tranches of the Preferred Warrants were classified as Level 3 fair value measurements, due to the use of unobservable inputs. See Note 13, Fair Value Measurements, for changes in fair value of the Preferred Warrants.

The key inputs utilized in determining the fair value of each Tranche B Warrants as of March 31, 2024 and December 31, 2023 were as follows:

|

|

March 31, |

|

|

December 31, |

|

||

Risk-free interest rate (1) |

|

|

% |

|

|

% |

||

Expected term remaining (periods) (1) |

|

|

|

|

|

|

||

Implied volatility |

|

|

% |

|

|

% |

||

Underlying Stock Price (Preferred Series A) |

|

$ |

|

|

$ |

|

||

The key inputs utilized in determining the fair value of each Tranche C Warrants as of March 31, 2024 and December 31, 2023 were as follows:

|

|

March 31, |

|

|

December 31, |

|

||

Risk-free interest rate (1) |

|

|

% |

|

|

% |

||

Expected term remaining (periods) (1) |

|

|

|

|

|

|

||

Implied volatility |

|

|

% |

|

|

% |

||

Underlying Stock Price (Preferred Series A) |

|

$ |

|

|

$ |

|

||

22

Equity Classified Warrants