As filed with the Securities and Exchange Commission on June 28, 2024.

Registration Number 333-280071

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

TO

FORM

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter)

| 3790 | 85-3844872 | |||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

730 Broadway

Redwood City, CA 94063

(818) 860-1352

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Ali Kashani

Chief Executive Officer

730 Broadway

Redwood City, California 94063

(818) 860-1352

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Albert Vanderlaan, Esq.

Orrick, Herrington & Sutcliffe LLP

222 Berkeley St., Suite 2000

Boston, MA 02116

(617) 880-2219

From time to time after this registration statement is declared effective.

(Approximate date of commencement of proposed sale to the public)

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided pursuant to Section 7(a)(2)(B) of the Exchange Act.

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. The selling stockholders may not sell these securities pursuant to this prospectus until the registration statement filed with the Securities and Exchange Commission becomes effective. This preliminary prospectus is not an offer to sell these securities and is not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JUNE 28, 2024

PRELIMINARY PROSPECTUS

4,813,041 Shares of Common Stock

This prospectus relates to the registering and resale by the selling stockholders named under the heading “Selling Stockholders” in this prospectus (which term as used in this prospectus includes their respective transferees, pledgees, distributees, donees and successors-in-interest, each a “selling stockholder” and, collectively, the “selling stockholders”) of up to 4,813,041 shares of common stock, par value $0.0001 per share, of Serve Robotics Inc. (the “Company”), which includes: (i) 2,104,562 shares of our common stock issued upon conversion of certain convertible promissory notes (the “Convertible Promissory Notes”); (ii) 500,000 shares of our common stock issuable upon exercise of the warrant (the “Underwriter Warrant”) issued to Aegis Capital Corp. (“Aegis”) in connection with the public offering and uplisting of our common stock, as more fully described herein (the “Public Offering”); (iii) 63,479 shares of our common stock issuable upon exercise of the warrants (the “Network 1 Warrants”) issued to Network 1 Financial Securities, Inc. (“Network 1”) at the closing of the Public Offering for their service as placement agent for the Convertible Promissory Notes; and (iv) 2,145,000 shares of our common stock issuable upon exercise of the warrant (the “Magna Warrant” and, together with the Underwriter Warrant and the Network 1 Warrants, the “Warrants”) issued to Magna New Mobility USA (“Magna”) in connection with our strategic partnership with Magna.

We will not receive any proceeds from the sale of the shares of common stock by the selling stockholders. However, we will receive the proceeds of any cash exercise of the Warrants. The selling stockholders may sell the shares of common stock offered by this prospectus from time to time through the means described in this prospectus under the caption “Plan of Distribution.”

We will bear all costs, expenses and fees in connection with the registration of the shares of common stock. The selling stockholders will bear all discounts, concessions, commissions and similar selling expenses, if any, attributable to their respective sales of the shares of common stock.

Our common stock is currently traded on The Nasdaq Capital Market, LLC (“Nasdaq”) under the ticker symbol “SERV”. On June 27, 2024, the last reported sale price of our common stock on Nasdaq was $2.00 per share.

We may amend or supplement this prospectus from time to time by filing amendments or supplements as required. You should read the entire prospectus and any amendments or supplements carefully before you make your investment decision.

We are an “emerging growth company” and a “smaller reporting company” as defined under the federal securities laws and, as such, are eligible for reduced public company reporting requirements. See “Prospectus Summary — Implications of Being an Emerging Growth Company and a Smaller Reporting Company.”

Investing in our common stock involves a high degree of risk. Before making an investment decision, please read “Risk Factors” on page 7 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Prospectus dated , 2024.

Table of Contents

i

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form S-1 that we filed with the U.S. Securities and Exchange Commission (“SEC”) pursuant to which the selling stockholders may, from time to time, offer and sell or otherwise dispose of the shares of our common stock covered by this prospectus. We will not receive any proceeds from the sale by the selling stockholders of the securities offered by them described in this prospectus.

We have not, and the selling stockholders have not, authorized anyone to give you any information other than the information contained in this prospectus, the information incorporated by reference herein, any applicable prospectus supplement or any free writing prospectus filed with the SEC. We and the selling stockholders take no responsibility for, and can provide no assurances as to the reliability of, any other information that others may give you. Neither we nor the selling stockholders have authorized anyone to provide you with additional information or information different from that contained in this prospectus filed with the SEC. The selling stockholders are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted. You should assume that the information appearing in this prospectus, the applicable prospectus supplement and any related free writing prospectus is accurate only as of the respective dates of those documents. Our business, financial condition, results of operations and prospects may have changed since those dates.

For Non-U.S. Investors

Neither we nor the selling stockholders have done anything that would permit this offering or possession or distribution of this prospectus, any prospectus supplement or free writing prospectus filed with the SEC, in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus, any prospectus supplement or free writing prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of common stock and the distribution of this prospectus, any prospectus supplement or free writing prospectus outside the United States.

ii

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus, including the sections entitled “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Description of our Business,” includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements relate to, among others, our plans, objectives and expectations for our business, operations and financial performance and condition, and can be identified by terminology such as “may,” “should,” “expect,” “intend,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “will,” “could,” “project,” “target,” “potential,” “continue” and similar expressions that do not relate solely to historical matters. Forward-looking statements are based on management’s belief and assumptions and on information currently available to management. Although we believe that the expectations reflected in forward-looking statements are reasonable, such statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by forward-looking statements.

Forward-looking statements include, but are not limited to, statements about:

| ● | our ability to protect and enforce our intellectual property and the scope and duration of such protection; | |

| ● | our reliance on third parties, including suppliers, delivery platforms, brand sponsors, software providers and service providers; | |

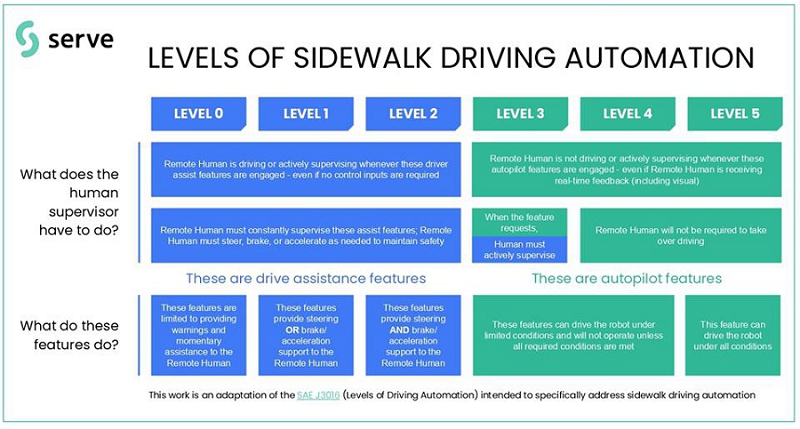

| ● | our ability to operate in public spaces and any errors caused by human supervisors, network connectivity or automation; | |

| ● | our robots’ reliance on sophisticated software technology that incorporates third-party components and networks to operate and our ability to maintain licenses for this software technology; | |

| ● | our ability to commercialize our products at a large scale; | |

| ● | the competitive industry in which we operate which is subject to rapid technological change; | |

| ● | our ability to raise additional capital to develop our technology and scale our operations; | |

| ● | developments and projections relating to our competitors and our industry; | |

| ● | our ability to adequately control the costs associated with our operations; | |

| ● | the impact of current and future laws and regulations, especially those related to personal delivery devices; | |

| ● | potential cybersecurity risks to our operational systems, infrastructure and integrated software by us or third-party vendors; | |

| ● | our ability to continue as a going concern; and | |

| ● | other risks and uncertainties, including those listed under the caption “Risk Factors.” |

These statements relate to future events or our future operational or financial performance, and involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by these forward-looking statements. Factors that may cause actual results to differ materially from current expectations include, among other things, those listed under the section titled “Risk Factors” and elsewhere in this prospectus, in any applicable prospectus supplement and in any related free writing prospectus.

Any forward-looking statement in this prospectus, in any applicable prospectus supplement and in any related free writing prospectus reflects our current view with respect to future events and is subject to these and other risks, uncertainties and assumptions relating to our business, results of operations, industry and future growth. Given these uncertainties, you should not place undue reliance on these forward-looking statements. No forward-looking statement is a guarantee of future performance. You should read this prospectus, any applicable prospectus supplement and any related free writing prospectus and the documents that we reference therein and have filed with the SEC as exhibits thereto completely and with the understanding that our actual future results may be materially different from any future results expressed or implied by these forward-looking statements. Except as required by law, we assume no obligation to update or revise these forward-looking statements for any reason, even if new information becomes available in the future.

This prospectus contains, and any applicable prospectus supplement and any related free writing prospectus may contain, estimates, projections and other information concerning our industry, our business and the markets for certain robotics. Information based on estimates, forecasts, projections or similar methodologies is inherently subject to uncertainties and actual events or circumstances may differ materially from events and circumstances reflected in this information. Unless otherwise expressly stated, we obtained these industry, business, market and other data from reports, research surveys, studies and similar data prepared by third parties, industry, medical and general publications, government data and similar sources that we believe to be reliable. In some cases, we do not expressly refer to the sources from which such data are derived.

iii

PROSPECTUS SUMMARY

This summary highlights certain information about us, this offering and selected information contained elsewhere in this prospectus. This summary is not complete and does not contain all of the information that you should consider before deciding whether to invest in the securities covered by this prospectus. For a more complete understanding of the Company and this offering, we encourage you to read and consider carefully the more detailed information in this prospectus, any related prospectus supplement and any related free writing prospectus, including the information set forth in the section titled “Risk Factors” in this prospectus, any related prospectus supplement and any related free writing prospectus in their entirety before making an investment decision.

All references to “Serve” refer to Serve Operating Co. (formerly known as Serve Robotics Inc.), a privately held Delaware corporation and our direct, wholly-owned subsidiary. Unless otherwise stated or the context otherwise indicates, references to the “Company,” “we,” “our,” “us” or similar terms refer to Serve Robotics Inc. (formerly named Patricia Acquisition Corp.) together with its wholly-owned subsidiary, Serve. Serve holds all material assets and conducts all business activities and operations of Serve Robotics Inc.

This prospectus includes a number of technical terms. Please see “Glossary of Terms and Abbreviations” beginning on page 47.

Our Company

We are on a mission to deliver a sustainable future by transforming how goods move among people.

We have developed an advanced, AI-powered robotics mobility platform, with last-mile delivery in cities as its first application. According to the U.S. Bureau of Transportation Statistics in 2017, 45% of car trips in the United States are taken for shopping and errands, and in 2019, FedEx stated that over 60% of merchants’ customers live within three miles of a store location. By eliminating unnecessary car traffic, and by reducing the cost of last-mile transportation, we aim to reshape cities into sustainable, safe and people-friendly environments, with thriving local economies.

Our first product is a low-emissions robot that serves people in public spaces, starting with last-mile food delivery. In 2017, our core technology development began with our co-founders and a growing product and engineering team. In 2020, the team launched a fleet of sidewalk delivery robots (hereafter simply referred to as “delivery robots”) in Los Angeles performing contactless deliveries during the COVID-19 pandemic shutdowns. By the end of that year, our robots had successfully completed over 10,000 commercial deliveries for Postmates Inc. (collectively with its affiliated entities, “Postmates”) in California, augmenting Postmates’ fleet of human couriers.

Postmates was acquired by Uber Technologies, Inc. (“Uber”) in 2020, and in February of 2021, Uber’s leadership team agreed to contribute the intellectual property developed by the team and assets relating to this project to Serve. In return for this contribution and an investment of cash into the Company, Uber acquired a minority equity interest in the business. By the end of the first quarter of 2021, the majority of the team that had worked on this project at Postmates joined us as full-time employees.

After spinning off from Uber in 2021, we established a commercial partnership with Uber, with deliveries starting in January 2022 on a small scale. In May 2022, Uber announced a pilot program with us, and by June, it executed a commercial-scale agreement with us to deploy up to 2,000 of our robots across the United States.

Our current fleet consists of over 100 robots, and we plan to expand our fleet by building and deploying hundreds of new robots in the coming years after raising additional capital. We have platform-level integrations with the Uber Eats division of Uber and 7-Eleven, Inc. Our strategic investors include NVIDIA, Uber, 7-Ventures and Delivery Hero’s corporate venture units, alongside other world-class investors.

Because we started within a food delivery company, our team comes with a depth of expertise in food delivery. Additionally, our engineering team has extensive experience in AI, automation and robotics. Our leadership team includes veterans from Uber, Postmates, Waymo, Apple Inc., Blue Origin, LLC, GoPro, Inc., GoDaddy Inc. and Anki, Inc. We believe our expertise positions us to service the ever-growing on-demand delivery market, including food delivery.

Based on our proprietary historical delivery data, approximately half of all food delivery distances in the United States are less than 2.5 miles, making these deliveries well-suited to delivery by sidewalk robots. We provide a robotic delivery experience that can delight customers, improve reliability for merchants and reduce traffic congestion and vehicle emissions. Moreover, at scale with full utilization and high autonomy, we believe our robots have the potential to reduce average delivery cost to under $1.00, lower than delivery cost by human couriers today, making on-demand delivery more affordable and accessible in the areas in which we operate. In fact, according to a 2024 ARK Invest report, by using automation to reduce delivery costs, the potential market for food and parcel delivery by robots and drones may grow to as much as $450 billion globally in 2030.

1

Recent Developments

Magna Delivery Vehicle Production Scaling and Purchase Agreement

On April 24, 2024, we entered into a Delivery Vehicle Production Scaling and Purchase Agreement with Magna, under which we appointed Magna as our sole and exclusive partner for the assembly of our automated sidewalk/off-road goods delivery vehicles, pursuant to our previously announced strategic partnership with Magna, as more fully described below.

Public Offering

On April 18, 2024, we consummated the Public Offering of an aggregate of 10,000,000 shares of common stock pursuant to a registration statement on Form S-1, as amended (File No. 333-274547) under the Securities Act at a price to the public of $4.00 per share, for aggregate gross proceeds of $40 million, prior to deducting underwriting discounts and offering expenses, with net proceeds of approximately $35.7 million. We intend to use the net proceeds of the Public Offering to fund research and development of the next generations of our robots, manufacturing activities, geographic expansion, and for working capital and other general corporate purposes.

In connection with the Public Offering, on April 17, 2024, we issued the Underwriter Warrant, subject to adjustments as provided therein, at an initial exercise price of $5.00 per share. The Underwriter Warrant is exercisable at any time, in whole or in part, commencing October 14, 2024, and expires on April 17, 2029.

In connection with the Public Offering, our common stock commenced trading on Nasdaq under the ticker symbol “SERV” on April 18, 2024. Prior to the Public Offering, our common stock was quoted on the OTCQB Marketplace under the ticker symbol “SBOT”.

License and Services Agreement with Magna

On February 20, 2024, we entered into a License and Services Agreement (the “LSA”) with Magna as a part of a strategic partnership with Magna.

Pursuant to the LSA, we, as an independent contractor of Magna, agreed to (i) grant a non-exclusive license to our Serve AMR Technology in the Licensed Fields of Use (each as defined in the LSA) to Magna and its affiliates and (ii) provide all reasonable engineering, technical and related support services that Magna may request from time to time in writing and in furtherance of commercialization of the Serve AMR Technology and products (including software) using, practicing or incorporating the Serve AMR Technology, and manufactured using, practicing or incorporating our AMR Technology (such services and support, the “Development Services”). Except as expressly set forth in the LSA, any Development Services shall be provided under the MSA (as defined below) and, if expired or terminated, under terms and conditions that are consistent with the terms therein. The term of the LSA will continue unless terminated by either party pursuant to and in accordance with the terms and conditions set forth in the LSA.

Master Services Agreement

On February 1, 2024, we entered into a Master Services Agreement (the “MSA”) with Magna, retroactively effective as of January 15, 2024 (the “MSA Effective Date”). Pursuant to the MSA, we agreed to provide certain services to Magna as described in one or more statements of work (“SOWs”). Such SOWs will contain a description of the scope, the time to be spent on performance, the fees to be paid to Serve, the functional requirements and technical specifications and, to the extent applicable, the timetable, schedule or milestones for the performance of the requested services. We entered into the first SOW with Magna on the MSA Effective Date. The term of the MSA commenced on the MSA Effective Date and will continue for a term of three months, unless terminated earlier or mutually extended in accordance with its terms.

In connection with our strategic partnership with Magna, on February 7, 2024, we issued the Magna Warrant to purchase up to 2,145,000 shares of our common stock, subject to adjustments as provided therein, at an exercise price of $0.01 per share.

The Magna Warrant is exercisable in two equal tranches: (i) the first tranche became exercisable on May 15, 2024, subject to certain conditions; and (ii) the second tranche will become exercisable upon Magna’s achievement of a certain manufacturing milestone as set forth in a production and purchase agreement to be entered into with respect to the contract manufacturing of our autonomous delivery robots by Magna or its affiliates. Notwithstanding the foregoing, the shares issued upon exercise of the Magna Warrant will vest and become exercisable upon any “change of control” (as defined in the Magna Warrant).

2

Convertible Promissory Notes Offering

At an initial closing on January 2, 2024 and subsequent closings on January 12, 2024, January 22, 2024 and January 26, 2024, we issued to certain accredited investors convertible promissory notes (the “Convertible Promissory Notes Offering”), for which the Company received an aggregate of $5.0 million in proceeds. In connection with the Public Offering, the convertible promissory notes converted into 2,104,562 shares of our common stock. Prior to conversion, the convertible promissory notes bore interest at a rate of 6.00% per year, compounded annually, due and payable upon request by each investor on or after the 12-month anniversary of the original issuance date of each note, if they had not converted.

On April 22, 2024, for Network 1’s service as placement agent for the Convertible Promissory Notes Offering in connection with the Public Offering, we issued the Network 1 Warrants to purchase up to 63,479 shares of common stock, subject to adjustments as provided therein, at an initial exercise price of $2.42 per share. The Network 1 Warrants became exercisable on April 17, 2024 and expire on April 17, 2029.

Summary Risk Factors

Investing in our common stock involves substantial risk. Our ability to execute our strategy is also subject to certain risks. The risks described under the heading “Risk Factors” included elsewhere in this prospectus may cause us not to realize the full benefits of our strengths or may cause us to be unable to successfully execute all or part of our strategy. Some of the most significant challenges and risks include the following:

| ● | Because we are an early-stage company with minimal revenue and a history of losses and we expect to continue to incur substantial losses for the foreseeable future, we cannot assure you that we can or will be able to operate profitably. |

| ● | We have a limited operating history, which may make it difficult to evaluate our business and prospects. |

| ● | If we fail to effectively manage our growth, we may not be able to design, develop, manufacture, market and launch new generations of our robotic systems successfully. |

| ● | A significant portion of our revenue is concentrated with a limited number of customers. |

| ● | Our future revenue plans rely on partnering with third-party delivery platforms, brand sponsors and/or direct sales to merchants. |

| ● | Failure of our service providers or disruptions to our outsourcing relationships might negatively impact our ability to conduct our business. |

| ● | Our robots operate in public spaces and any errors caused by human supervisors, network connectivity issues, third-party software or automation may adversely affect our commercial relationships. |

| ● | Our robots rely on sophisticated software technology that incorporates third-party components and networks to operate, and the inability to maintain licenses for this software technology, errors in the software we license or the terms of open-source licenses could result in increased costs or reduced service levels, which would adversely affect our business. |

| ● | The benefit of our products could be supplanted by other technologies or solutions or competitors’ products that utilize similar technology to ours in a more effective way. |

| ● | We have limited experience commercializing our products at a large scale and may not be able to do so efficiently or effectively. |

| ● | We are substantially reliant on our relationships with suppliers and service providers for the parts and components in our robots, as well as for the manufacture of our robots. If any of these suppliers or service partners choose to not do business with us, we would have significant difficulty in procuring and producing our robots and our business prospects would be significantly harmed. |

| ● | The evolving regulations around personal delivery devices (“PDDs”) could materially impact our business and growth prospects in new markets. |

| ● | Defects, glitches or malfunctions in our products or the software that operates them, failure of our products to perform as expected, connectivity issues or operator errors may result in product recalls, lower than expected return on investment for customers and could cause significant safety concerns, each of which could adversely affect our results of operations, financial condition and our reputation. |

3

| ● | Even if our products perform properly and are used as intended, if operators sustain any injuries while using our products, we could be exposed to liability and our results of operations, financial condition and our reputation may be adversely affected. |

| ● | We operate in a competitive industry that is subject to rapid technological change, and competitors may have or attain more resources and/or greater market recognition than we do. |

| ● | If we cannot protect, maintain and, if necessary, enforce our intellectual property rights, our ability to develop and commercialize products will be adversely impacted. |

| ● | Security breaches and other disruptions could compromise our proprietary information and expose us to liability, which would cause our business and reputation to suffer. |

| ● | Our business plans require a significant amount of capital. Our future capital needs may require us to sell additional equity or debt securities that may dilute our stockholders or contain terms unfavorable to us or our investors. |

| ● | We will be required to raise additional capital in order to develop our technology and scale our commercial delivery operations. However, we may be unable to raise additional capital needed to fund and grow our business. |

| ● | If use of the internet via websites, mobile devices and other platforms, particularly with respect to online food ordering, does not continue, our business and growth prospects will be harmed. |

| ● | Our products and services are disruptive to the delivery services industries, and important assumptions about the market demand, pricing, adoption rates and sales cycle, for our current and future products and services may be inaccurate. |

| ● | Even if we successfully market our products and services, the purchase or subscription, adoption and use of the products and services may be materially and negatively impacted if our customers resist the use and adoption of the products and services. |

| ● | Our systems, products, technologies and services and related equipment may have shorter useful lives than we anticipate. |

| ● | We, any manufacturing partners, and suppliers may rely on complex machinery for production, which involves a significant degree of risk and uncertainty in terms of operational performance and costs. |

| ● | We may be unable to adequately control the costs associated with our operations. |

| ● | Our ability to manufacture products of sufficient quality on schedule in the future is uncertain, and delays in the design, production and launch of our products could harm our business, prospects, financial condition and operating results. |

| ● | We are subject to cybersecurity risks to our operational systems, security systems, infrastructure, integrated software in our products and data processed by us or third-party vendors. |

| ● | We do not intend to pay dividends for the foreseeable future and, as a result, your ability to achieve a return on your investment will depend on appreciation in the price of our common stock. |

Implications of Being an Emerging Growth Company and a Smaller Reporting Company

We qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, as amended (the “JOBS Act”). An “emerging growth company” may take advantage of reduced reporting requirements that are otherwise applicable to public companies. These provisions include, but are not limited to:

| ● | being permitted to present only two years of audited financial statements and only two years of related “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure in our periodic reports and registration statements, including this prospectus; |

| ● | not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act, as amended (the “Sarbanes-Oxley Act”), on the effectiveness of our internal controls over financial reporting; |

| ● | reduced disclosure obligations regarding executive compensation arrangements in our periodic reports, proxy statements and registration statements, including this prospectus; and |

| ● | exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. |

4

We may use these provisions until December 31, 2028, which is the last day of the fiscal year following the fifth anniversary of the first sale of our common stock pursuant to an effective registration statement in 2023. However, if certain events occur prior to the end of such five-year period, including if we become a “large accelerated filer,” our annual gross revenues exceed $1.235 billion or we issue more than $1.00 billion of non-convertible debt in any three-year period, we will cease to be an emerging growth company prior to the end of such five-year period.

We have elected to take advantage of certain of the reduced disclosure obligations in the registration statement of which this prospectus is a part and may elect to take advantage of other reduced reporting requirements in future filings. As a result, the information that we provide to our stockholders may be different than you might receive from other public reporting companies in which you hold equity interests.

The JOBS Act provides that an emerging growth company can take advantage of an extended transition period for complying with new or revised accounting standards, until those standards apply to private companies. We have elected to take advantage of the benefits of this extended transition period and, therefore, we will not be subject to the same new or revised accounting standards as other public companies that are not emerging growth companies. Our financial statements may therefore not be comparable to those of companies that comply with such new or revised accounting standards. Until the date that we are no longer an emerging growth company or affirmatively and irrevocably opt out of the exemption provided by Section 7(a)(2)(B) of the Securities Act upon issuance of a new or revised accounting standard that applies to our financial statements and that has a different effective date for public and private companies, we will disclose the date on which we will adopt the recently issued accounting standard.

We are also a “smaller reporting company,” meaning that the market value of our stock held by non-affiliates is less than $700 million and our annual revenue is less than $100 million during the most recently completed fiscal year. We may continue to be a smaller reporting company if either (i) the market value of our stock held by non-affiliates is less than $250 million or (ii) our annual revenue is less than $100 million during the most recently completed fiscal year and the market value of our stock held by non-affiliates is less than $700 million. If we are a smaller reporting company at the time we cease to be an emerging growth company, we may continue to rely on exemptions from certain disclosure requirements that are available to smaller reporting companies. Specifically, as a smaller reporting company we may choose to present only the two most recent fiscal years of audited financial statements in our Annual Report on Form 10-K and, similar to emerging growth companies, smaller reporting companies have reduced disclosure obligations regarding executive compensation.

Corporate Information

We were incorporated in the State of Delaware as Patricia Acquisition Corp. on November 9, 2020. On July 31, 2023, Serve Acquisition Corp. merged with and into Serve (the “Merger”). Following the Merger, Serve was the surviving entity and became our wholly-owned subsidiary, and all of the outstanding stock of Serve was converted into shares of our common stock. The business of Serve became our business as a result of the Merger. Following the consummation of the Merger, Serve changed its name to “Serve Operating Co.” and we changed our name to “Serve Robotics Inc.”

Prior to the Merger, Patricia Acquisition Corp. was a “shell” company registered under the Exchange Act, with no specific business plan or purpose until it began operating the business of Serve following the closing of the Merger.

Our principal executive offices are located at 730 Broadway, Redwood City, California 94063. Our telephone number is (818) 860-1352. Our website address is http://www.serverobotics.com. Information contained on, or that can be accessed through, our website is not a part of this prospectus.

All trademarks, service marks and trade names appearing in this prospectus are the property of their respective holders. Use or display by us of other parties’ trademarks, trade dress, or products in this prospectus is not intended to, and does not, imply a relationship with, or endorsements or sponsorship of, us by the trademark or trade dress owners.

5

THE OFFERING

| Common stock offered by | 4,813,041 shares of common stock | |

| selling stockholders | ||

| Common stock | 37,098,653 shares of common stock | |

| outstanding | ||

| Use of proceeds | We will not receive any proceeds from the sale of the shares of common stock offered by the selling stockholders. However, we will receive the proceeds of any cash exercise of the Warrants. See “Use of Proceeds” for additional information. | |

| Offering price | The selling stockholders may sell their shares of common stock pursuant to this prospectus through public transactions at prevailing market prices or at privately negotiated prices. | |

| Risk factors | You should read the “Risk Factors” section of this prospectus for a discussion of factors to consider carefully before deciding to invest in shares of our common stock. | |

| Nasdaq trading symbol | “SERV” |

The number of shares of common stock outstanding is based on an aggregate of 37,098,653 shares outstanding as of May 31, 2024, and excludes:

| ● | 1,501,341 shares of common stock issuable upon the exercise of stock options outstanding as of March 31, 2024 that were subject to options originally granted under the Serve Robotics Inc. 2021 Stock Plan (the “2021 Plan”), with a weighted-average exercise price of $0.61 per share; |

| ● | 1,327,994 shares of common stock available for issuance under the Serve Robotics Inc. 2023 Equity Incentive Plan (the “2023 Plan”) as of March 31, 2024 with a weighted-average exercise price of $0.61 per share; |

| ● | outstanding Bridge Warrants (as defined herein) to purchase an aggregate of 468,971 shares of our common stock with an exercise price of $3.20 per share as of March 31, 2024; |

| ● | outstanding Bridge Broker Warrants (as defined herein) to purchase an aggregate of 74,662 shares of our common stock with an exercise price of $3.20 per share as of March 31, 2024; |

| ● | outstanding Placement Agent A Warrants (as defined herein) to purchase an aggregate of 153,909 shares of our common stock with an exercise price of $4.00 per share as of March 31, 2024; |

| ● | outstanding Placement Agent B Warrants (as defined herein) to purchase an aggregate of 125,000 shares of our common stock with an exercise price of $0.001 per share as of March 31, 2024; and |

| ● | outstanding warrants to purchase an aggregate of 142,730 shares of our common stock at the exercise price of $3.89 per share as of March 31, 2024 assumed by us in connection with the Merger. |

Except as otherwise indicated, all information in this prospectus:

| ● | reflects the issuance of 10,000,000 shares of our common stock in the Public Offering in April 2024; |

| ● | assumes no exercise of outstanding options subsequent to March 31, 2024; and |

| ● | assumes no vesting of restricted stock unit awards subsequent to March 31, 2024. |

6

RISK FACTORS

Investing in our common stock involves a high degree of risk. In addition to the other information set forth in this prospectus, you should carefully consider the risk factors discussed below when considering an investment in our common stock and any risk factors that may be set forth in the applicable prospectus supplement, any related free writing prospectus, as well as the other information contained in this prospectus, any applicable prospectus supplement and any related free writing prospectus. If any of the following risks occur, our business, financial condition, results of operations and prospects could be materially and adversely affected. In that case, the market price of our common stock could decline, and you could lose some or all of your investment. Additional risks and uncertainties not presently known to us or that we currently deem immaterial also may impair our business operations.

Risks Related to Our Business and Industry

Because we are an early-stage company with minimal revenue and a history of losses and we expect to continue to incur substantial losses for the foreseeable future, we cannot assure you that we can or will be able to operate profitably.

We are an early-stage company. We were formed and commenced operations in January 2021. We face all the risks faced by newer companies, including significant competition from existing and emerging competitors, some of which are established and have better access to capital. In addition, as a new business, we may encounter unforeseen expenses, difficulties, complications, delays and other known and unknown factors. We will need to transition from an early-stage company to a company capable of supporting larger scale commercial activities. If we are not successful in such a transition, our business, results and financial condition will be harmed.

We have not been profitable to date, and we expect operating losses for the near future. During the three months ended March 31, 2024, we generated $0.9 million in revenue and incurred a net loss of $9.0 million. During the years ended December 31, 2023 and 2022, we generated revenue of $0.21 million and $0.11 million, respectively, and we incurred net losses of approximately $24.81 million and $21.86 million, respectively. There can be no assurance that we will not continue to incur net losses in the future. We may not succeed in expanding our customer base and product offerings and even if we do, we may never generate revenue that is significant enough to achieve profitability. Even if we do achieve profitability, we may not be able to sustain or increase profitability on a quarterly or annual basis. Furthermore, we may not be able to control overhead expenses even where our operations successfully expand. Our failure to become and remain profitable would depress our value and could impair our ability to raise capital, expand our business, diversify our product offerings or even continue our operations.

We have a limited operating history, which may make it difficult to evaluate our business and prospects.

We face the risks associated with businesses in their early stages, with limited operating histories and whose prospects are hard to evaluate. Any evaluation of our business and our prospects must be considered in light of the uncertainties, delays, difficulties and expenses commonly experienced by companies at this stage, which generally include unanticipated problems and additional costs relating to the development and testing of products, product approval or clearance, regulatory compliance, production, product introduction and marketing and competition. For example, we have incurred losses for each of the past few years, driven mainly by our investments in research and development costs. Many of these factors are beyond the control of our management. In addition, our performance will be subject to other factors beyond our control, including general economic conditions and conditions in the robotics industry. Accordingly, our business and success face risks from uncertainties faced by developing companies in a competitive environment. There can be no assurance that our efforts will be successful or that we will ultimately be able to attain profitability.

Our auditor has issued a “going concern” opinion.

Our auditor has issued a “going concern” opinion on our financial statements, which means they are not sure that we will be able to succeed as a business without additional financing. For the year ended December 31, 2023, the date of our last audited financial statements, we generated $0.21 million in revenue, and we sustained a net loss of $24.81 million. We had an accumulated deficit of $68.33 million as of December 31, 2023. Our ability to continue as a going concern until we reach profitability is dependent upon our ability to generate cash from operating activities and to raise additional capital to fund our operations. While we were successful in raising a cumulative total of approximately $45.0 million in debt and equity financing from January 1, 2024 through May 31, 2024, our ongoing operational expenses are now approximately $2.4 million per month without yet generating any material corresponding revenue. Our failure to raise additional capital could have a negative impact on not only our financial condition but also our ability to execute our business plan.

7

If we fail to effectively manage our growth, we may not be able to design, develop, manufacture, market and launch new generations of our robotic systems successfully.

We intend to invest significantly in order to expand our business. Any failure to manage our growth effectively could materially and adversely affect our business, prospects, financial condition and operating results. We intend to expand our operations significantly. We expect our expansion to include:

| ● | expanding the management, engineering and product teams; |

| ● | identifying and recruiting individuals with the appropriate relevant experience; |

| ● | hiring and training new personnel; |

| ● | launching commercialization of new products and services; |

| ● | forecasting production and revenue; |

| ● | entering into relationships with one or more third-party design manufacturing partners and third-party contract manufacturers and/or expanding our internal manufacturing capabilities; |

| ● | controlling expenses and investments in anticipation of expanded operations; |

| ● | carrying out acquisitions and entering into collaborations, in-licensing arrangements, joint ventures, strategic alliances or partnerships; |

| ● | expanding and enhancing internal information technology, safety and security systems; |

| ● | conducting demonstrations; |

| ● | entering into agreements with suppliers and service providers; and |

| ● | implementing and enhancing administrative infrastructure, systems and processes. |

Should achieved market penetration warrant, we intend to continue to hire a significant number of additional personnel, including engineers, design, production, operations personnel and service technicians for our robotic systems and services. Because of the innovative nature of our technology, individuals with the necessary experience may not be available to hire, and as a result, we will need to expend significant time and expense, to recruit and retain experienced employees and appropriately train any newly hired employees. Competition for individuals with experience designing, producing and servicing robots and their software is intense, and we may not be able to attract, integrate, train, motivate or retain additional highly qualified personnel. The failure to attract, integrate, train, motivate and retain these additional employees could seriously harm our business, prospects, financial condition and operating results.

Our revenues and profits are subject to fluctuations.

It is difficult to accurately forecast our revenues and operating results, and these could fluctuate in the future due to a number of factors. These factors may include adverse changes in companies’ interests in our robotic delivery and branding services, companies’ available dollars to invest in our services, general economic conditions, our ability to market our company to companies, headcount and other operating costs and general industry and regulatory conditions and requirements. Our operating results may fluctuate from year to year due to the factors listed above and others not listed. At times, these fluctuations may be significant and could impact our ability to operate our business.

A significant portion of our revenue is concentrated with a limited number of customers.

A significant portion of our revenue is concentrated with a limited number of customers. During the three months ended March 31, 2024, one customer accounted for 90% of the Company’s revenue and accounted for 83% of the Company’s accounts receivable. In the same period in 2023, a different customer accounted for 50% of the Company’s revenue. There are inherent risks whenever a large percentage of total revenues are concentrated with a limited number of customers. If either of our significant customers were to breach, cancel or amend our agreements with them, it may have an outsized effect on our revenue, cash on hand and profitability. In addition, we may have an increased interest in accepting less favorable terms of any amendment as a result.

8

We are dependent on general economic conditions.

Our business model is dependent on companies purchasing our robotic delivery and branding services. Our business model is thus dependent on national and international economic conditions. Uncertain economic conditions have created volatility in the U.S. Such adverse national and international economic conditions may reduce the future availability of dollars companies have to spend on our services, which would negatively impact our revenues and possibly our ability to continue operations. For example, rising labor costs in recent years have led to increased interest in last-mile automation, while higher interest rates have resulted in a decrease in investment activity and overall capital allocation to hardware startups. The worsening of global economic conditions has in the past adversely affected, and could in the future, adversely affect our business, financial condition or results of operations, and the worsening of economic conditions in certain specific regions of the country could impact the expansion and success of our business in such areas.

Our directors may be engaged in a range of business activities that could result in conflicts of interest.

We may be subject to various potential conflicts of interest because some of our officers and directors may be engaged in a range of business activities. In addition, our executive officers and directors may devote time to their outside business interests, so long as such activities do not materially or adversely interfere with their duties owed to us. In some cases, our executive officers and directors may have fiduciary obligations associated with these business interests that interfere with their ability to devote time to our business and affairs and that could adversely affect our operations. These business interests could require significant time and attention of our executive officers and directors. In addition, we may also become involved in other transactions which conflict with the interests of our directors and the officers who may from time-to-time deal with persons, firms, institutions or companies with which we may be dealing, or which may be seeking investments similar to those desired by us. The interests of these persons could conflict with our interests. For example, one of our directors, James Buckly Jordan, currently serves as a director, officer or advisor to multiple companies, including Miso Robotics and Vebu Labs, that compete in our industry, robotics and automation.

Unfavorable changes in interest rates and foreign currency exchange rates may adversely affect our financial condition, liquidity and results of operations.

Fluctuations in interest rates and foreign exchange rates may negatively impact our business. These rates are highly sensitive to many factors beyond our control, including general economic conditions, both domestic and foreign, and the monetary and fiscal policies of various governmental and regulatory authorities. Any of such widespread economic conditions could negatively impact our supply chain partners and the industry as a whole, which could materially decrease our profits and cash flow. We have experienced increased costs in acquiring parts for our robots as a result of the global semiconductor industry facing shortages in supply as well as inflation and increased interest rates. We, or our supply chain partners, could continue to increase prices as a result of other adverse macroeconomic conditions.

The inability of our supply chain to deliver certain key electrical components, such as semiconductors, could materially adversely affect our business, financial condition and results of operations.

Certain highly complex components used to manufacture our robots are obtained from single or limited sources that we may have to compete for with other participants in the robotics, consumer electronics and automotive markets. If our supply chain fails to deliver products to us in sufficient quality and quantity on a timely basis, we will be challenged to meet our target production and development timelines and could incur significant additional expenses for expedited freight and other related costs. Our supply chain may also be adversely impacted by events outside of our control, including macroeconomic events, trade restrictions and economic recessions. For example, throughout 2022 and 2023, we experienced delays in supply chain deliveries, extended lead times and shortages of key components. Supply chain disruptions have delayed, and may continue to delay the timing of production and maintenance of our robots, which in turn could negatively impact our business, results of operations and financial condition.

Our robots are reliant on semiconductors. In recent years, there has been an ongoing shortage of semiconductors. The semiconductor supply chain is complex, with capacity constraints occurring throughout. We have and will continue to work closely with our suppliers to minimize any potential adverse impacts of the global semiconductor chip shortage and monitor the availability of semiconductor chips and other key components and any other supply chain inefficiencies that may arise. In an effort to mitigate these risks, in some cases, we may have to incur higher costs due to investment in supply chain resiliency and to secure available inventory or make non-cancellable purchase commitments with semiconductor suppliers, which introduce inventory risk if our forecasts and assumptions prove inaccurate. Furthermore, if we are not able to mitigate the impact of the semiconductor chip shortage, any direct or indirect supply chain disruptions may have a material adverse impact on our business, financial condition and results of operations.

9

Our failure to attract and retain highly qualified personnel in the future could harm our business.

We are an innovative technology company. We may not be able to locate or attract qualified individuals for important positions, such as software engineers, robotics engineers, machine vision and machine learning experts and others, which could affect our ability to grow and expand our business. We may also face intense competition for qualified individuals from numerous other companies, including other similarly situated technology companies, many of whom have greater financial and other resources than we do.

In addition, new hires often require significant training and, in many cases, take significant time before they achieve full productivity. For example, we recently appointed a new Chief Financial Officer, effective April 29, 2024, and there may be future changes to our executive management team resulting from the hiring or departure of executives, which could disrupt our business. We may incur significant costs to attract and retain qualified personnel, including significant expenditures related to salaries and benefits and compensation expenses related to equity awards, and we may lose new employees to our competitors or other companies before we realize the benefit of our investment in recruiting and training them. Moreover, new employees may not be or become as productive as we expect, as we may face challenges in adequately or appropriately integrating them into our workforce and culture. If we are unable to attract, integrate and retain suitably qualified individuals who can meet our technical, operational and managerial requirements, on a timely basis or at all, our business, results of operation and financial condition could be adversely affected.

Litigation or legal proceedings could expose us to significant liabilities, occupy a considerable amount of our management’s time and attention and damage our reputation.

We may, from time to time, be a party to various litigation claims and legal proceedings. We will evaluate these claims and proceedings to assess the likelihood of unfavorable outcomes and estimate, if possible, the amount of potential losses. Claims made or threatened by our suppliers, distributors, customers, competitors or current or former employees could adversely affect our relationships, damage our reputation or otherwise adversely affect our business, financial condition or results of operations. The costs associated with defending legal claims and paying damages could be substantial. Our reputation could also be adversely affected by such claims, whether or not successful.

Our future revenue plans rely on partnering with third-party delivery platforms, brand sponsors and/or direct sales to merchants.

Our largest stream of projected revenue comes from maximizing utilization of our robots to perform deliveries. We may be unable to maximize utilization due to a variety of reasons, including insufficient merchant participation, platform partner matching algorithms, failure to deliver a commercial grade product and a lack of product acceptance by merchants and/or delivery recipients. To date, we have been able to continually increase our robot utilization in our partnership with Uber driven by the continued improvement in our integration, high merchant participation and widespread product acceptance by users of the Uber platform. We have not yet achieved such levels of utilization with our other partners because those integrations are less complete. To best achieve profitability, we would need to continue to improve our utilization targets with Uber above current levels and maintain those levels with other partners as well. As this requires cooperation by third parties, there is no guarantee that it will be achieved within a specific timeframe.

Our financial projections also anticipate generating revenues from brand sponsors who would pay to place their branding on our robots as a form of out-of-home (“OOH”) branding. OOH branding on robots is a new phenomenon and as such, an unproven model. To date, for our limited number of robots, we have been able to run periodic OOH advertising campaigns with several brands in varying sectors including real estate, fashion and entertainment, with 22% and 50% of our revenues for the years ended December 31, 2023 and December 31, 2022, respectively, coming from OOH advertising. In the future, if we are unable to realize these sales, our business model and go-to-market strategy will be jeopardized.

10

Failure of our service providers or disruptions to our outsourcing relationships may negatively impact our ability to conduct our business.

Certain of our remote piloting services are currently provided by third-party vendors, and sometimes from service centers outside of the United States. Services provided pursuant to arrangements with these third-party vendors could be disrupted due to events outside of their control such as power failures, cybersecurity incidents, internet traffic congestion or increased latency or deterioration in their economic condition. Similarly, the expiration of agreements associated with such arrangements or the transition of services between providers could lead to loss of institutional knowledge or service disruptions. While we have not experienced material impact of such disruptions to date, our reliance on others as service providers could have a material adverse effect on our business, financial condition, results of operations and cash flows in the future.

Our robots operate in public spaces and any errors caused by human supervisors, network connectivity issues, third-party software or automation may adversely affect our commercial relationships.

Our ability to attract and retain customers (including merchants, platform partners and brand sponsors) is heavily dependent on our ability to provide a safe and reliable service. Our safety and security track record has been instrumental in helping us attract and retain our existing customers. Because we operate on public sidewalks, the performance of our robots is highly visible and we have to maintain the highest standards for public safety. Our operating procedures and automated systems are designed to ensure that our robots yield the right of way to vehicles, pedestrians, and other sidewalk and road users. Examples include only crossing controlled intersections during a pedestrian “walk” signal and slowing down or stopping if a pedestrian approaches the robot from any direction. Our partners, such as Uber, require timely reporting of any material safety incidents, and if they are not able to ascertain our ability to maintain safe operations, our commercial relationships may be jeopardized. To date, we have not experienced material safety incidents nor have our partners raised any concerns about our safety standards and track record. However, any actual or perceived public safety incidents that may be caused by our human supervisors, network connectivity issues, third-party software or automation may put our commercial relationships and financial viability at risk.

Our robots rely on sophisticated software technology that incorporate third-party components and networks to operate, and the inability to maintain licenses for software technology, errors in the software we license or the terms of open-source licenses could result in increased costs or reduced service levels, which would adversely affect our business.

Our robots require certain third-party software and networks to function safely and effectively, and our business relies on certain third-party software obtained under licenses from other companies. We anticipate that we will continue to rely on such third-party software in the future. Although we believe that there are commercially reasonable alternatives to the third-party software we currently license, this may not always be the case, or it may be difficult or costly to replace. In addition, integration of new third-party software may require significant work and require substantial investment of our time and resources. Our use of additional or alternative third-party software would require us to enter into license agreements with third parties, which may not be available on commercially reasonable terms or at all. Many of the risks associated with the use of third-party software cannot be eliminated, and these risks could negatively affect our business. Furthermore, performance degradation or lack of access to such software and networks can result in poor delivery performance or even grounding of our entire fleet until it is resolved, which could adversely impact our ability to continue our operations.

Additionally, the software powering our technology systems incorporates software covered by open-source licenses. The terms of many open-source licenses have not been interpreted by U.S. courts, and there is a risk that the licenses could be construed in a manner that imposes unanticipated conditions or restrictions on our ability to operate our systems. In the event that portions of our proprietary software are determined to be subject to an open-source license, we could be required to publicly release the affected portions of our source code or re-engineer all or a portion of our technology systems, each of which could reduce or eliminate the value of our technology systems. Such risk could be difficult or impossible to eliminate and could adversely affect our business, financial condition and results of operations.

11

The benefits to customers of our products could be supplanted by other technologies or solutions or competitors’ products that utilize similar technology to ours in a more effective way.

The benefits to customers of our products could be supplanted by other technologies or solutions or competitors’ products that utilize similar technology to ours in a more effective way. We cannot be sure that alternative technologies or improvements to artificial intelligence, industrial automation or other technologies, processes or industries will not match or exceed the benefits of our products or be more cost effective than our products. The development of any alternative technology that can compete with or supplant our products may materially and adversely affect our business, prospects, financial condition and operating results, including in ways we do not currently anticipate. Any failure by us to develop new or enhanced technologies or processes, or to react to changes in existing technologies, could materially delay our development and introduction of new and enhanced products, which could result in the loss of competitiveness of our robotic systems and solutions, decreased revenue and a loss of market share to competitors. Our research and development efforts may not be sufficient to adapt to new or changing technologies. While we plan to upgrade and adapt our robotic systems and solutions as we or others develop new technology, our robotic systems and solutions may not compete effectively with alternative products if we are not able to source and integrate the latest technology into our systems and solutions.

We have limited experience commercializing our products at a large scale and may not be able to do so efficiently or effectively.

We have limited experience commercializing robotic systems at a large scale and may not be able to do so efficiently or effectively. A key element of our long-term business strategy is the continued growth in sales, marketing, training, customer service and maintenance and servicing operations, including hiring personnel with the necessary experience. Managing and maintaining these operations is expensive and time consuming, and an inability to leverage such an organization effectively or at all could inhibit potential sales or subscriptions and the penetration and adoption of our products into new markets. In addition, certain decisions we make regarding staffing in these areas in our efforts to maintain an adequate spending level could have unintended negative effects on our revenues, such as by weakening the sales, marketing and maintenance and servicing infrastructures or lowering the quality of customer service.

We are substantially reliant on our relationships with suppliers and service providers for the parts and components in our robots, as well as for the manufacture of our robots. If any of these suppliers or service partners choose to not do business with us, we would have significant difficulty in procuring and producing our robots and our business prospects would be significantly harmed.

Our robots contain hundreds of components which are assembled by third-party manufacturing partners. Collaboration with third parties for the manufacturing of robots is subject to risks with respect to operations that are outside our control. Global supply chain problems directly impact our ability to obtain these components cost-effectively. We could experience delays to the extent our current or future partners do not continue doing business with us, meet agreed upon timelines, experience capacity constraints or otherwise are unable to deliver components or manufacture robots as expected. For example, we have had to delay increasing the number of robots in our fleet due to previous third-party supply restraints. Serve has an agreement with a leading LIDAR vendor to purchase LIDARs at highly competitive prices within a limited timeframe. Failure to leverage this agreement, or secure similar supplier agreements for components that may face availability constraints due to supply chain disruptions could result in higher prices for those components, which in turn could increase the cost of manufacturing robots and result in an adverse financial impact to our delivery economics.

There is risk of potential disputes with partners, and we could be affected by adverse publicity related to our partners whether or not such publicity is related to their collaboration with us. Our ability to successfully build a premium brand could also be adversely affected by perceptions about the quality of our partner manufacturers’ robots or other robots manufactured by the same partner. In addition, although we intend to be involved in material decisions in the supply chain and manufacturing process, given that we also rely on our partners to meet our quality standards, there can be no assurance that we will be able to maintain high quality standards.

We may in the future enter into strategic alliances, including joint ventures or minority equity investments, with various third parties to further our business purpose. These alliances could subject us to a number of risks, including risks associated with sharing proprietary information, non-performance by the third party and increased expenses in establishing new strategic alliances, any of which may materially and adversely affect our business.

12

The evolving regulations around PDDs could materially impact our business and growth prospects in new markets.

Sidewalk robots, as opposed to autonomous vehicles operating on public streets, are not by default prohibited from operations in most jurisdictions. But there is no guarantee that the current permissive environment will not change in the future, especially as more sidewalk robots get deployed. While we currently have the requisite permits and support from local municipalities in areas we operate, any change in regulations or permit requirements could adversely impact our business. Therefore, we proactively engage with lawmakers, academics, standards-setting organizations, urban planning nonprofits, disability rights advocates, senior citizen organizations and regional bicycle coalitions to anticipate and mitigate potential regulatory challenges.

Over a dozen states across the United States have enacted legislation regulating PDDs, using a definition that includes sidewalk robots such as ours. While these regulations have been largely industry-friendly and intended to streamline the rollout of PDDs in those jurisdictions, they are not yet uniform and may present some challenges as we seek to deploy in new markets. For example, Washington State and the District of Columbia have a 100-pound unladen weight restriction and the City of Santa Monica prohibits the operation of autonomous devices on sidewalks, that would require amending in order for us to expand into those jurisdictions.

Furthermore, the cellular network and radio systems contained in our robots are regulated by the Federal Communications Commission (the “FCC”), which allocates cellular and wireless bandwidth to ensure minimal conflict between operators. And the battery packs within our robots use custom lithium-ion cells. The transportation and effective storage of lithium-ion batteries is tightly regulated by the U.S. Department of Transportation (the “DOT”) and other regulatory bodies. Any failure to comply with the DOT’s storage and transport requirements or the FCC’s regulations on wireless communications could result in fines, loss of permits and licenses or other regulatory consequences, which could limit our ability to manufacture and deliver our robotic systems and negatively affect our business, prospects, financial condition, results of operations and cash flows.

Content-based restrictions on outdoor advertising, which may include advertising featured on our sidewalk robots, by regulators may restrict the categories of content that we can display on our sidewalk robots.

Restrictions on outdoor advertising of certain products, services or other content are or may be imposed by laws and regulations in cities, counties or states. For example, tobacco products have been effectively banned from outdoor advertising in most U.S. jurisdictions. Further, certain municipalities may limit outdoor advertising. Content-based restrictions could cause a reduction in our content revenues by limiting the content partners we are able to provide advertising services to and, more broadly, such restrictions or any expanded restrictions could limit our ability to advertise on our sidewalk robots, which could have an adverse effect on our business, financial condition and results of operations.

Defects, glitches or malfunctions in our products or the software that operates them, failure of our products to perform as expected, connectivity issues or operator errors may result in product recalls, lower than expected return on investment for customers and could cause significant safety concerns, each of which could adversely affect our results of operations, financial condition and our reputation.

The design, manufacture and marketing of our products involve certain inherent risks. Manufacturing or design defects, glitches, malfunctions, connectivity issues between the central processing unit and peripheral vehicle subsystems, operator errors, unanticipated use of our robotic systems and inadequate disclosure of risks relating to the use of sidewalk robots, among other inherent risks, can lead to injury, property damage or other adverse events. We conduct extensive testing of our units, in some instances in collaboration with our customers, to ensure that any such issues can be identified and addressed in advance of commercial launch of the products. However, there can be no assurance that we will be able to identify all such issues or that, if identified, efforts to address them will be effective in all cases.

13

In addition, if the manufacturing of our products is outsourced, we may not be aware of manufacturing defects that could occur. Such adverse events could lead to unexpected failures in our products and could result, in certain cases, in the removal of our products from the market. A product recall could result in significant costs. To the extent any manufacturing defect occurs, our agreement with the third-party manufacturer may contain a limitation on the third-party manufacturer’s liability, and therefore we could be required to incur the majority of related costs. Product defects or recalls could also result in negative publicity, damage to our reputation or, in the event of regulatory developments, delays in new product acceptance.

Our products incorporate sophisticated computer software. Complex software frequently contains errors, especially when first introduced. Our software may experience errors or performance problems in the future. If any part of our products’ hardware or software were to fail, the service mission could be compromised. Additionally, users may not use our products in accordance with safety protocols and training, which could amplify the risk of failure. Any such occurrence could cause delay in market acceptance of our products, damage to our reputation, product recalls, increased service and warranty costs, product liability claims and loss of revenue relating to such hardware or software defects.

We anticipate that as part of our ordinary course of business we may be subject to product liability claims alleging defects in the design or manufacture of our products. A product liability claim, regardless of our merit or eventual outcome, could result in significant legal defense costs and high punitive damage payments. Although we maintain product liability insurance, the coverage is subject to deductibles and limitations, and may not be adequate to cover future claims. Additionally, we may be unable to maintain our existing product liability insurance in the future at satisfactory rates or adequate amounts.

Even if our products perform properly and are used as intended, if operators sustain any injuries while using our products, we could be exposed to liability and our results of operations, financial condition and our reputation may be adversely affected.