UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________

FORM 10-K

__________________________

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2023

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission file number 001-39835

__________________________

__________________________

(Exact name of Registrant as specified in its Charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of Principal Executive Offices) | (Zip Code) | ||||||||||

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: Warrants, exercisable for one share of Common Stock, $0.0001 par value per share.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act.

Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | o | x | |||||||||

| Non-accelerated filer | o | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. o

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

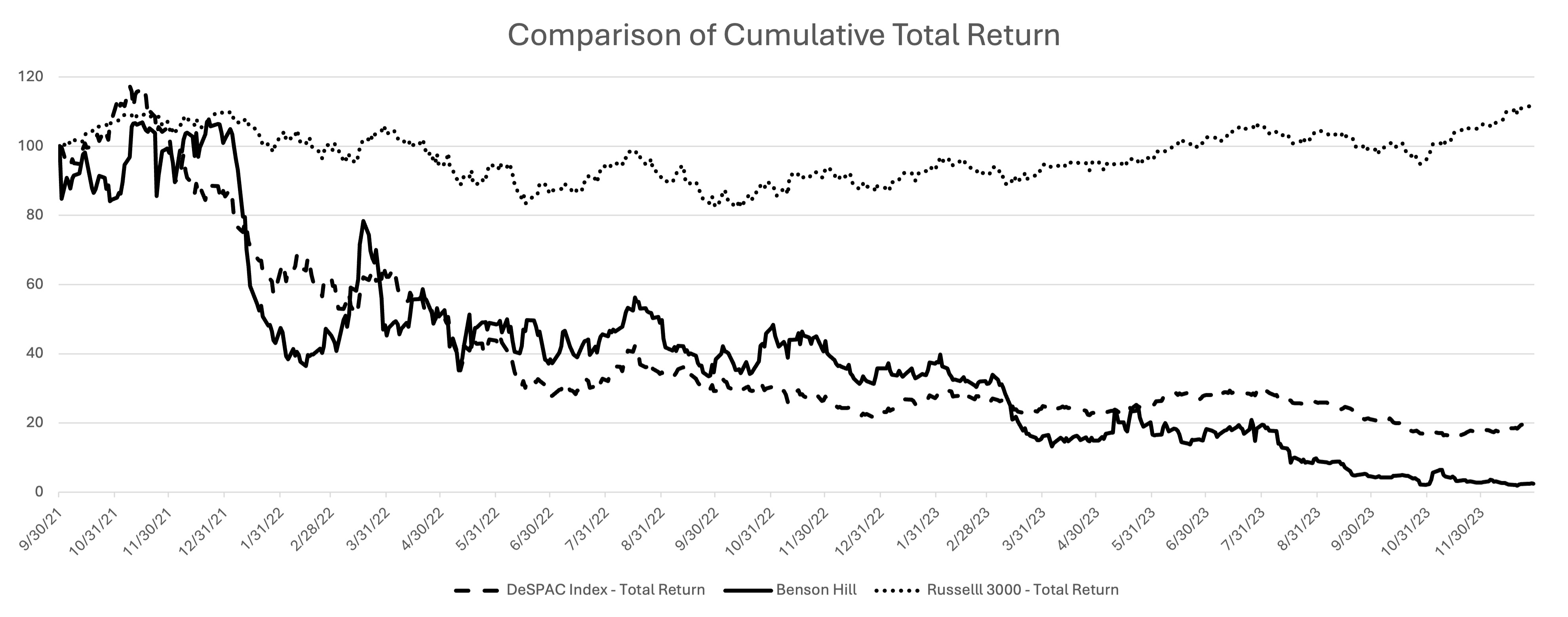

The aggregate market value of voting stock held by non-affiliates of the registrant as of June 30, 2023, the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $247 million based on the closing sales price of $1.30 per share of the registrant’s common stock as reported by the New York Stock Exchange. For purposes of this calculation, shares of common stock beneficially owned by each executive officer, director, and beneficial owner of more than 10% of the registrant’s common stock have been excluded to reflect that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

As of March 12, 2024, 211,099,359 shares of the registrant’s common stock, $0.0001 par value, were issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

TABLE OF CONTENTS

| Page | |||||

i

Cautionary Note Regarding Forward-Looking Statements

Some of the statements contained in this report and documents incorporated by reference herein are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These forward-looking statements are subject to known and unknown risks, uncertainties and assumptions about us that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Given these uncertainties, you should not place undue reliance on these forward-looking statements.

Generally, statements that are not historical facts, including statements concerning possible or assumed future actions, business strategies, events or results of operations, are forward-looking statements. These statements may be preceded by, followed by or include the words “believe,” “estimate,” “expect,” “intend,” “project,” “forecast,” “may,” “will,” “should,” “could,” “would,” “seek,” “plan,” “scheduled,” “anticipate,” “intend,” or similar expressions, as well as the negative of such statements. Forward-looking statements contained in this report include, but are not limited to, statements about our ability to:

•complete and achieve the anticipated benefits of our transition to an asset-light business model with a focused expansion into broadacre animal feed markets, which transition contemplates the sale of our soy processing assets, the payoff of our senior debt, our entry into strategic partnerships and/or licensing arrangements, and procuring additional financing;

•complete the actions associated with, and achieve the anticipated benefits of, the execution of our expanded Liquidity Improvement Plan and other cost-saving measures in a timely manner, or at all;

•continue as a going concern;

•comply with the covenants of our debt financing agreements;

•obtain from the issuance of equity and/or non-dilutive sources the amount of additional capital that we believe may be needed to achieve our financial objectives;

•identify, evaluate and consummate strategic opportunities in ways that maximize stockholder value;

•realize the anticipated benefits of the divestiture of the Seymour, Indiana and Creston, Iowa facilities;

•execute our business strategy, including our business transition and monetization of services provided and expansions in and into existing and new lines of business;

•meet future liquidity requirements and comply with restrictive covenants related to long-term indebtedness;

•maintain our listing on the New York Stock Exchange;

•anticipate the uncertainties inherent in the development of new business lines and business strategies;

•increase brand awareness;

•attract, train and retain effective officers, key employees and directors;

•upgrade and maintain information technology systems;

•acquire and protect intellectual property;

•effectively respond to general economic and business conditions;

•effectively execute our executive leadership transition, including, among others, by maintaining key employee, customer, partner and supplier relationships;

•enhance future operating and financial results;

•anticipate rapid technological changes;

•comply with laws and regulations applicable to our business, including laws and regulations related to data privacy and intellectual property;

•anticipate the impact of, and respond to applicable new accounting standards;

•respond to fluctuations in commodity prices and foreign currency exchange rates and political unrest and regulatory changes in international markets from various events;

•navigate volatile interest rate environments;

•anticipate the significance and timing of contractual obligations;

•maintain key strategic relationships with partners and distributors;

•respond to uncertainties associated with product and service development and market acceptance;

•finance operations on an economically viable basis;

•anticipate the impact of new U.S. federal income tax laws, including the impact on deferred tax assets;

•successfully defend litigation; and

•access, collect and use personal data about consumers.

Forward-looking statements represent our estimates and assumptions only as of the date of this report. Factors that could cause actual results to differ materially from those implied by the forward-looking statements in this report are more fully described under the heading “Risk Factors” and elsewhere in this report. The risks described under the heading “Risk Factors” are not exhaustive. Other sections of this report describe additional factors that could adversely affect our business, financial condition or results of operations. New risk factors emerge from time to time and it is not possible to predict all such risk factors, nor can we assess the impact of all such risk factors on our business, or the extent to which any factor or combination of factors may

1

cause actual results to differ materially from those contained in any forward-looking statements. Except as otherwise required by law, we expressly disclaim any obligation or undertaking to release publicly any updates or revisions to any forward-looking statement contained in this report to reflect any change in our expectations or any change in events, conditions or circumstances on which any of our forward-looking statements are based. We qualify all of our forward-looking statements by these cautionary statements.

Item 1. Business

Overview

Benson Hill is an ag-tech company on a mission to lead the pace of innovation in soy protein through differentiated and advantaged genetics. Leveraging downstream insights and demand, we utilize our CropOS® technology platform to design and deliver food and feed that’s better from the beginning: more nutritious, and more functional, while enabling efficient production and delivering novel sustainability benefits to food and feed customers. We are headquartered in St. Louis, Missouri, where most of our research and development activities are managed. In February 2024, as part of our acceleration to an asset-light business model, we divested our soy-crushing and food-grade white flake and soy flour manufacturing operation in Creston, Iowa, which followed the October 2023 divestiture of our soy crushing facility in Seymour, Indiana. We continue to process dry peas in North Dakota through our Dakota ingredients facility, and we sell our products throughout North America, in Europe and in several countries globally.

We believe that moving to an asset-light business model should enable us to focus on our research and development competitive advantage while participating across the value chain through partnerships that are more efficient to scale acreage, require less operating expense and are more capital efficient. This model maintains our ability to solve end user challenges with seed innovation. As we analyze the asset-light business model across the value chain, we have identified three opportunities to monetize Benson Hill’s technology. First, by licensing our germplasm to seed companies. Second, by direct seed and grain sales to farmers. And third, through technology access fees and value-based royalties from seed companies, processors and end users. In the future, we plan to enter the animal feed market and secure partnerships and licensing agreements to scale our product offerings.

The emergence of significant market headwinds in the food, aquaculture, and specialty oil markets is a factor in our decision to reshape our business to best position our proprietary product portfolio and future product pipeline for significant growth. Recent advances in our soybean breeding program will drive significant expansion of our seed portfolio offer by 2025. The latest field evaluations on our third generation of Ultra High Protein Low Oligosaccharides (“UHP-LO”), non-GMO soybean varieties showed protein gains of two percent over the previous generation and achieved a yield gap of only three to five bushels per acre, compared with commodity GMO soybeans. Our herbicide-tolerant Ultra High Protein (“UHP”) soybean varieties are on track for commercial release in 2025, with acreage and further portfolio expansion expected in 2026. This is a major step in providing farmers with options for weed control and enabling lower-cost, broadacre production of already advantaged UHP soybeans for the animal feed industry.

Evolving Food and Feed Industry

By combining proprietary data with artificial intelligence (“AI”) capabilities, coupled with advances in plant genomics and our asset-light strategy, we believe we can accelerate the development and delivery of better food and feed options from the beginning—with a focus on both quantity and quality. Genomics has been used for decades to develop crops for our food and feed system, but most agricultural companies have focused almost exclusively on increasing the yield of a few crops, resulting in commodity ingredients. While focus on quantity is important, it often comes with trade-offs in areas such as nutrient density.

By leveraging deep insights on our proprietary soybean germplasm, Benson Hill is strategically positioned to drive seed innovation in broadacre opportunities for the aquaculture, pet food, swine and poultry markets – some 90 percent of the soy market. These steps allow for speed to market with solution-based products, allowing us to recommoditize soybeans for animal feed and food.

Business Transition

On October 31, 2023, we announced plans to improve our financial position and accelerate our transition to an asset-light business model with a focused expansion into broadacre animal feed markets, intended to complement our accomplishments in human food ingredients. Under this transition plan, we intend to serve the animal feed market through an asset-light business model and secure partnership and licensing agreements to scale our product innovations. In connection with this transition plan, and of our expanded Liquidity Improvement Plan as described in Part II, Item 7 in this report, we divested certain of our soy processing assets, the proceeds of which improved our liquidity position while we seek to secure partnership and licensing agreements to help us execute on our long-term strategy. The execution of our transition to an asset-light business model and our expanded Liquidity Improvement Plan are subject to significant business, financial, operational, timing, market and other

2

risks. We can provide no assurance that we will be able to successfully execute our plans. Please see Part I, Item 1A of this report for a description of our “Risk Factors” that may impact our ability to execute our plans.

Sale of Seymour, Indiana and Creston, Iowa Facilities

In connection with the execution of our transition to an asset-light business model and our expanded Liquidity Improvement Plan, on October 31, 2023, we entered into an asset purchase agreement (the “Asset Purchase Agreement”) with White River Soy Processing, LLC (“White River”), pursuant to which, among other things, on October 31, 2023, we sold our soybean processing facility located in Seymour, Indiana, together with certain related assets, for approximately $35.4 million of total gross proceeds, which includes $25.9 million for the facility assets and the remainder for net working capital, subject to certain adjustments, including an adjustment for inventory (the “Seymour Sale”). See Item 1.01 of our Current Report on Form 8-K filed with the SEC on October 31, 2023 for additional information.

On February 13, 2024, we entered into a membership interest purchase agreement (the “MIPA”) with an affiliate of White River, pursuant to which, among other things, we sold all of our interests in our wholly-owned subsidiary, Benson Hill Ingredients, LLC (“Ingredients”), for approximately $52.5 million, plus a working capital adjustment estimated to be approximately $19.5 million, subject to certain deferred payments, holdbacks and other adjustments (the “Creston Sale”).

The Creston Sale and the Seymour Sale (collectively, the “Transactions”) represent the completion of an expected milestone as we implement cost and operational improvements as part of our expanded Liquidity Improvement Plan. These actions align with Benson Hill’s commitment to disciplined liquidity management and asset efficiency as we transition to an asset-light business model backed by world-class soybean germplasm and competitively advantaged technology. We used the proceeds from the Transactions to improve our liquidity position, by fully retiring our high cost debt, and reducing our operating and working capital costs. Refer to Note 25—Subsequent Events in this report for further details on the Creston Sale and see Item 1.01 of our Current Report on Form 8-K filed with the SEC on February 14, 2024 for additional information.

The Transactions were separately marketed, negotiated, executed, and closed, and neither of the Transactions was conditioned upon the other. The Transactions were executed to leverage our core competencies as a technology-enabled seed innovation company as we transition from a vertically integrated business model to an asset-light business model with an expanded focus on animal feed markets. Exiting the soybean processing business is intended to strengthen our balance sheet as we seek to continue to commercialize our core business and intellectual property assets through partnerships and licensing arrangements to scale our product innovations. Following the Creston Sale, we exited the ownership and operation of soybean processing assets and, therefore, the Transactions collectively met the criteria for transactions required to be accounted for as discontinued operations.

Our Strengths and Solution: Technology and CropOS® Platform

Navigating the pressures on our food and feed system will require innovation. Technology is an essential enabler as innovation cycles in food and feed are not measured in weeks or months; they’re measured in years.

At our core Benson Hill is a leader in AI driven seed innovation utilizing proprietary genetics. Our CropOS® innovation engine is a proprietary, continuously learning and expanding product design and development platform that uses predictive breeding and other advanced tools like CRISPR gene editing technology to tap into the vast potential within the genome. We believe that the combination of our world-leading proprietary soy and yellow-pea protein germplasm, the predictive capability of the CropOS® platform, the precision of our genomic tools, our Crop Accelerator (a controlled environment research facility), and our extensive field-testing network will further enable us to develop differentiated products with targeted attributes much more quickly and cost effectively than traditional methods.

We are developing products leveraging our CropOS® platform through a three-step, iterative “Design, Build, Test” process that improves in precision and intelligence with each turn of the flywheel. The key inputs to our approach are twofold. The first is an unparalleled data library comprising genotypic, phenotypic, and agronomic data on our crops, consumer insight data on our ingredients, and environmental data on our growing sites. The second is a robust machine learning capability, which leverages our data library to design before we build. We believe this combination of relevant data and advanced simulation lets us get our products to market more efficiently, faster, and on timelines that can more effectively respond to evolving consumer preferences and farmer needs.

In our Design step, the CropOS® platform employs a diverse array of simulations and predictions to execute the most efficient and cost-effective path to novel product development. The platform can consider billions of data points in millions of pipeline configurations to identify the starting parental plant breeding combinations, predict gene targets, and analyze optimal farm management and environmental conditions. These state-of-the-art platform capabilities and enabling technologies allow us to assess the probability of success early in the research and development process, focusing resources and avoiding potentially expensive late-stage failures. In turn, this allows for a larger breadth of products to be designed.

3

Once an optimal path is identified, we enter our Build step. In this stage of our development process, candidate products are created through predictive breeding and gene editing. Our proprietary suite of gene editing technologies and intellectual property portfolio enable us to edit the plant’s own genome predictably and precisely, which we consider an advance form of seed breeding. We can leverage our knowledge of plant gene functions to unlock and restore lost or muted genetic variation that is within the natural diversity of the plant or knock out genes that are unwanted. This approach is distinguished from transgenic, or “GMO” technology, in that we are advancing natural genetic variation that could be achieved using traditional breeding approaches rather than introducing genes foreign to the species.

Through our Crop Accelerator, opened in October 2021, in St. Louis, Missouri, the Build step of our process is sped up within our controlled environment, indoor product development facility. This 47,000-square-foot facility features dynamically adaptive Conviron® growth houses and chambers, equipped with sophisticated sensor and environmental controls, including multi-channel LEDs, imaging capabilities, additive carbon dioxide, and temperature, humidity, and lighting controls. The Crop Accelerator enables rapid testing and target candidate selection over multiple growth cycles. Insights and data points gathered during each growing cycle further enhance the predictive capabilities of the CropOS® platform. We believe this cycle of feedback will accelerate our ability to develop new offerings, including continued expansion of our proprietary portfolio of soy ingredients.

After a potential commercial product is built, it then enters our Test step where it is evaluated within our network (comprised of internal and third-party sites and capabilities) of hundreds of field-level testing research and production sites. We believe our predictive optimization capabilities have the potential to maximize the return on our genetics by using proprietary placement models, which are built on environmental and performance data to predict where to contract acres to lift protein content. We then use digital agriculture technology to collect on-farm data through our grower data partnership program and other relationships to enhance the CropOS® platform, further feeding our data flywheel.

Environmental, Social and Governance Strategy

Environmental and social impact strategy guides our work and is a competitive advantage that helps to inform decisions and work across our company. We believe our ESG strategy is fundamental to achieving our vision and long-term profitability. We are striving to optimize the environmental impact of our operations, and we recognize the greatest potential for impact is through our product development process of designing seeds, ingredients, and food that generates social and environmental benefit throughout the food value chain for all stakeholders.

At the farm level, we help identify additional revenue opportunities for farmers through potential input efficiencies and regenerative farming practices through industry partners. At the manufacturing level, we are designing products that we believe will reduce water and energy intensive processing steps. At the seed level, we believe we can enable improved scaling, accessibility, and adoption of end products with environmental and social benefits, with markets ranging from broadacre animal feed and aquaculture to plant-based protein and pet food.

Benson Hill has developed an internal strategy including foundational policies and processes to manage and assess our ESG success and impact. As an organization, some of our primary ESG goals are the following:

Develop seed innovations that deliver nutrient-rich and sustainable protein options for food and feed manufacturers. Driven by growing consumer demand and climate-related risks, many manufacturers have set ESG measurement and reporting programs, such as reporting on their own greenhouse gas (“GHG”) emission production. Benson Hill is positioned to assist in meeting feed and food manufacturers’ goals of reducing GHG emissions in their scope 3 supply chains by developing genetic innovations/seed innovations with reduced environmental impact. For example, Benson Hill has conducted a consultant-led life cycle assessment of an ingredient derived from our UHP soybeans, and our results show a significant reduction in required GHG emissions and water use due to the reduction, or elimination, of a protein-concentration processing step that is used to create commodity soy protein concentrate today. The reduction or elimination of this concentration step is possible due to the high protein in the soybeans before processing, leading to a high protein ingredient with less processing. We believe this reduction in GHG emissions and water, among other environmental impact indicators, will support downstream ESG objectives.

Improve farm cost-effectiveness and sustainability. Our farmer partners are critical to our success, and we value these relationships greatly. Benson Hill’s on-farm ESG strategy is to directly collect agronomic performance data from the farm and provide recommendations for regenerative practices, as well as enable profitable opportunities through input reduction or alternative revenue streams. Agronomic data collection can inform data-driven decision making in our product life cycle assessments, GHG emissions assessments, product development and other business functions.

Recruit and retain purpose-driven talent. Current research suggests employees are increasingly interested in working for companies that have an integrated ESG mission and purpose. Benson Hill has developed processes and internal programs for

4

our team, such as employee-led committees, that promote working together and re-thinking how we do business within our company, with our partners, and across the supply chain. We are working to develop teams that are grounded in a spirit of diversity, equality, and inclusion, and encouraged to think more innovatively, boldly, and transparently. Our goal is a workplace that is not just productive, but also one of mutual respect and an environment for team members to continuously develop as professionals.

Benson Hill’s ESG strategy and business objectives will continue to progress and evolve based on industry shifts and stakeholders’ needs. We believe our long-term profitability goals and our ESG strategy are mutually inclusive concepts.

Business Segments, Growth Strategies, and Products

Our business is comprised of one operating and reportable segment, Benson Hill, Inc., which combines seed innovation through our world-leading proprietary soy and yellow-pea germplasm, our CropOS® platform which aggregates proprietary protein, genomic, and strategic data layers for predictive breeding using AI and machine learning (“ML”) and our Crop Accelerator, an indoor year-round speed breeding and rapid prototyping facility. The result is a complete and market leading toolbox that will deliver our seed innovations in the future. We are currently developing a diversified seed portfolio spanning the following key markets—protein ingredients, aquaculture and specialty animal feed, and vegetable oils. For each product, our research and development efforts are focused on quality-centric traits, such as nutrient density, carbohydrate profiles, functionality, amino acid content, and sustainability, as well as yield potential and agronomic improvements.

Our partnerships with farmers are an essential part of our supply chain. Within the traditional agriculture industry, farmers typically sell to elevators or processors who operate a high volume/low margin business to store commodity crops and convert them into largely aquaculture and specialty animal feed and industrial products. Benson Hill’s UHP non-GMO soybeans have the potential to transform farmers’ operations and are a key ingredient in transforming our food system.

Our historic growth strategy, or “growth playbook,” was developed as a repeatable process to enable us to remain at the forefront of agriculture innovation.

•Step 1: Create the foundation — At this initial step, we focused on entering the market through owned or controlled channels, selling non-proprietary products to agrifood manufacturers, food and ingredient companies, aquaculture and specialty animal feed customers, and retailers. We used this time to build relationships across the value chain and invest in the data to inform our CropOS® platform with low capital investment.

•Step 2: Integrated route to market — We introduced our proprietary products in the channel to prove the product concept, scale, and catalyze customer demand for our differentiated products. This stage included the use of owned or third-party processing capabilities, and exploring strategic partnerships that could further expand production capacities.

•Step 3: Broad adoption — This is our current and most asset-light step of our strategy where we intend to focus on maximizing the benefit and scale of our proprietary seed portfolio by building partnerships and licensing relationships. In this step, it is envisioned that we will grow beyond our proving ground acreage and eventually increase commercial and supply chain efficiencies by leveraging others’ existing infrastructure.

In 2024, we will begin the shift towards 100% proprietary products through an asset-light business model. Accessing the animal feed markets requires an acre acquisition strategy. As our acre acquisition targets grow in the coming years towards an estimated 6.5 million acres by 2030, we expect broadacre licensing of our germplasm to be the catalyst to get us there. Other sources of future revenues and margins will include direct seed sales and technology access fees from soy ingredient processors and customers.

Yellow Pea Seed Innovations

We are in Step 1 of our growth playbook for yellow pea, and over the near term we expect to enter Step 2 with the start of commercialization of our first proprietary yellow pea protein ingredient products through our existing supply chain infrastructure, including premium texturized and un-texturized yellow pea protein concentrates.

Despite being one of the fastest growing protein ingredients for plant-based meats, yellow pea has received comparatively little genomic innovation to date. The pea-based protein ingredient primarily used today by many plant-based companies, is pea protein isolate (“PPI”). The PPI production process, similar to soy protein concentrate, is expensive as well as water- and energy-intensive; however, such processing is necessary to concentrate protein to higher levels and help ameliorate native off-putting flavors of yellow peas.

5

We have sequenced and assembled a reference genome for yellow pea—a high resolution “genomic map”—that, in combination with our CropOS® platform, is enabling us to accelerate our yellow pea breeding program. As a result, we believe we will develop differentiated varieties of yellow pea for first commercial plantings in the near term. We are working on a pipeline of products that has the potential to significantly reduce off-flavors, increase the protein content of the plant, and ultimately reduce or displace the need for expensive, water- and energy-intensive processing steps typically required for ingredients used in plant-based meat alternatives.

Our subsidiary Dakota Dry Bean Inc., an upper Midwest-based yellow pea processor, has an established channel with commodity pea protein concentrate, split peas, pea flour and pea fiber. We have expanded and upgraded the capabilities of Dakota Ingredients to better serve the pet and human food markets. Through our elite grower program and integrated production capabilities, the operation can now test premium yellow pea varieties and supply ingredients that are traceable and meet certain food-grade, kosher, and non-GMO certification standards.

Our proprietary and non-proprietary revenues were as follows for the years ended December 31, 2023, 2022 and 2021:

Year Ended December 31, | |||||||||||||||||

| (In Thousands USD) | 2023 | 2022 | 2021 | ||||||||||||||

| Proprietary | $ | 109,984 | $ | 72,578 | $ | 38,043 | |||||||||||

| Non-Proprietary | 363,352 | 308,655 | 52,902 | ||||||||||||||

| Total Revenues | $ | 473,336 | $ | 381,233 | $ | 90,945 | |||||||||||

Competitors

We believe that our technology platform coupled with our proprietary germplasm is unique to Benson Hill and sets us apart from others in the agriculture and food markets, but we do compete with others in certain areas of our business. For example, we compete with seeds and trait companies as well as smaller biotechnology and ag-tech companies, particularly for grower contracting and access to acres. Key competitors in this space include Bayer, Corteva, Syngenta, and Pairwise. For our ingredients that are commercialized, we compete with food and feed ingredient companies. Key competitors in these industries include Archer-Daniels-Midland Company (“ADM”), CHS, Inc., and Cargill, Inc. In addition, advancements in fields such as gene editing, biologics, digital agriculture, data science, and artificial intelligence may enable disruptive technology that could alter the competitive landscape for food and agriculture.

Intellectual Property

Our success depends in part on our ability to obtain and maintain intellectual property and proprietary protection for our product candidates and technology related to our business, defend and enforce our intellectual property rights, in particular, our patent rights, preserve the confidentiality of our trade secrets, and operate without infringing valid and enforceable intellectual property rights of others. We seek to protect our proprietary position by, among other things, licensing and filing U.S. and certain non-U.S. patents and patent applications related to our technology, products and product candidates, and improvements that are important to the development of our business, where patent protection is available. We also rely on trade secrets, plant breeders’ rights, and/or contractual provisions to develop and maintain our proprietary position and protect aspects of our business that are not amenable to, or that we do not consider appropriate for, patent protection. We seek to protect our proprietary technologies, in part, by confidentiality agreements with our employees, consultants, scientific advisors, and contractors. Notwithstanding these efforts, we cannot be sure that patents will be granted with respect to any patent applications we have licensed or filed or may license or file in the future, and we cannot be sure that any patents we have licensed or patents that may be licensed or granted to us in the future will not be challenged, invalidated, or circumvented or that such patents will be commercially useful in protecting our product candidates and technology. Moreover, trade secrets can be difficult to protect. While we have confidence in the measures we take to protect and preserve our trade secrets, such measures can be breached, and we may not have adequate remedies for any such breach. In addition, our trade secrets may otherwise become known or be independently discovered by competitors. For more information regarding the risks related to our intellectual property, please see “Risk Factors—Risks Relating to Our Intellectual Property in this report.

As of December 31, 2023, we have approximately 245 pending or issued patents. Approximately 94 of those are for plant varieties, 81% of which have issued. Approximately 81 are product-related, 33% of which have issued. Approximately 70 are enabling technologies, 14% of which have issued. All patents or applications filed on our plant varieties are in the U.S., while 29% and 35% of the product-related or enabling technology patents are in the U.S., respectively. We also have approximately 54 pending applications for plant breeders’ rights on our plant varieties, divided among the U.S. and other countries. In addition to these patents and patent applications, we also hold licenses from other parties related to certain products and activities.

6

These patents expire at varying times depending on the jurisdiction and filing date. Individual patent terms extend for varying periods of time, depending upon the date of filing of the patent application, the date of patent issuance, and the legal term of patents in the countries in which they are obtained. In most countries in which patent applications are filed, including the U.S., the patent term is 20 years from the date of filing of the first non-provisional application to which priority is claimed. Under certain circumstances, a patent term can be extended. For example, in the U.S., a patent’s term may be lengthened by patent term adjustment, which compensates a patentee for administrative delays by the U.S. Patent and Trademark Office in reviewing and granting a patent or may be shortened if a patent is terminally disclaimed over an earlier-filed patent. However, the actual protection afforded by a patent varies on a product-by-product basis, from country-to-country, and depends upon many factors, including the type of patent, the scope of its coverage, the availability of legal remedies in a particular country, and the validity and enforceability of the patent.

As of December 31, 2023, we had 18 U.S. trademarks, six pending U.S. trademark applications, 99 registered non-U.S. trademarks, and five pending non-U.S. trademark applications.

Benson Hill is a registered trademark of Benson Hill, Inc. Other trademarks, logos, and slogans registered or used by Benson Hill and our subsidiaries include, but are not limited to, the following: CropOS® and Veri™.

All other brand names or trademarks appearing in this report are the property of their respective owners. Benson Hill’s use or display of other parties’ trademarks, trade dress or products in this report does not imply that Benson Hill has a relationship with, or endorsement or sponsorship of, the trademark or trade dress owners.

Research and Development

As of December 31, 2023, we had approximately 118 employees dedicated to our product and platform development. This team has technical expertise in data science, ML software, genome engineering, molecular biology, biochemistry, genetics and genetic engineering, plant physiology, and plant breeding. The activities of this team are conducted principally at our St. Louis, Missouri facilities. We have made, and will continue to make, substantial investments in this capability. Our research and development expenses were $40.3 million, $47.5 million and $40.6 million for the years ended December 31, 2023, 2022 and 2021, respectively.

Employees

As of December 31, 2023, we employed approximately 270 full-time employees.

Regulatory

We are subject to laws and regulations in the jurisdictions in which we operate. This includes laws and regulations governing biotechnology and food companies related to the development, approval, manufacturing, import, marketing, and sale of our products.

Regulation of Plant Biotechnology Products

The three primary agencies with responsibility for regulation of plant biotechnology products in the U.S. are the U.S. Department of Agriculture’s (“USDA”) Animal and Plant Health Inspection Services (“APHIS”), the U.S. Environmental Protection Agency (“EPA”), and the U.S. Food and Drug Administration (“FDA”). The APHIS regulates plant biotechnology products to ensure that they do not pose a plant pest risk under the Plant Protection Act (“PPA”). The EPA regulates pesticides (including plant-incorporated protectants) pursuant to the Federal Insecticide, Fungicide, and Rodenticide Act (“FIFRA”). The FDA regulates food and animal feed under the Federal Food, Drug, and Cosmetic Act (“FDCA”).

Plant gene editing uses relatively new technology and the regulatory landscape continues to evolve in this area. Under the USDA’s recently revised regulations, certain categories of our products currently in development using gene editing may be exempt from certain regulations related to genetic engineering under the PPA because they could otherwise have been developed through conventional breeding techniques, which may include gene edited soybeans or yellow peas. Other plant biotechnology products currently in development may be subject to certain regulations related to genetic engineering under the PPPA in the future. The FDA offers a voluntary consultation process to determine whether foods derived from plant biotechnology products would require regulatory review and approval before marketing such products.

Other countries also have laws and regulations that apply to plant biotechnology products. The regulatory landscape around gene edited plant biotechnology products varies in each country and continues to evolve.

7

Regulation of Food and Ingredient Products

We are also subject to laws and regulations administered by various federal, state and local government agencies in the U.S., such as the FDA, the Federal Trade Commission, the EPA, the Occupational Safety and Health Administration, and the USDA, related to the processing, packaging, distribution, sale, marketing, labeling, quality, safety, and transportation of our products, as well as our occupational safety and health practices.

Among other things, the facilities in which our products are grown, packed or processed may be required to register with the FDA, and comply with regulatory schemes including the Food Safety Modernization Act (“FSMA”), among other laws and regulations implemented by the FDA, the USDA, and other regulators. We are also subject to parallel state and local food safety regulations, including registration and licensing requirements for our facilities, enforcement of standards and label registration for our products and facilities by state and local health agencies, and regulation of our trade practices in connection with selling our products. We are also subject to labor and employment laws, laws governing advertising, privacy laws, safety regulations and other laws, including consumer protection regulations that regulate retailers or govern the promotion and sale of merchandise.

Merger with Star Peak Corp II

On September 29, 2021 (the “Closing Date”), Star Peak Corp II (“STPC”), a special purpose acquisition company, consummated a merger (the “Closing”) pursuant to that certain Agreement and Plan of Merger, dated May 8, 2021 (the “Merger Agreement”), by and among STPC, STPC Merger Sub Corp., a Delaware corporation and wholly owned subsidiary of STPC (“Merger Sub”), and Benson Hill, Inc., a Delaware corporation (“Legacy Benson Hill”). Pursuant to the terms of the Merger Agreement, a business combination between STPC and Legacy Benson Hill was affected through the merger of Merger Sub with and into Legacy Benson Hill, with Legacy Benson Hill surviving the transaction as a wholly owned subsidiary of STPC (the “Merger”). On the Closing Date, STPC changed its name to Benson Hill, Inc. and Legacy Benson Hill changed its name to Benson Hill Holdings, Inc. As a consequence of the Merger, we became the successor to a company registered with the Securities and Exchange Commission (the “SEC”) and listed on the New York Stock Exchange (the “NYSE”). Our future results of consolidated operations and financial position may not be comparable to historical results as a result of the Merger.

Available Information

Our internet website address is www.bensonhill.com. Through our website, we make available, free of charge, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports, as well as proxy statements, and, from time to time, other documents as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. These SEC reports can be accessed through the investor relations section of our website. The information found on our website is not part of this or any other report we file with or furnish to the SEC.

The SEC maintains an internet website that contains reports, proxy and information statements, and other information regarding Benson Hill and other issuers that file electronically with the SEC. The SEC’s internet website address is www.sec.gov.

Item 1A. Risk Factors

An investment in our securities involves a high degree of risk. In evaluating our business, you should consider carefully the risks described below, as well as the other information contained in this report and in our other filings with the SEC. Additional risks not presently known to us or that we currently deem immaterial may also adversely affect our business. The occurrence of any of these events or circumstances could individually or in the aggregate have a material adverse effect on our business, financial condition, cash flow or results of operations. In that event, the trading price of our securities could decline, and you could lose all or part of your investment. This report contains forward-looking statements; please refer to the cautionary statements made under the heading “Cautionary Note Regarding Forward-Looking Statements” for more information on the qualifications and limitations on forward-looking statements. References in this section to “we,” “our,” or “us” generally refer to Benson Hill, unless otherwise specified.

Risk Factors Summary

Risks Relating to Our Business

•While our audited consolidated financial statements have been prepared on a going concern basis, we believe that our recurring net losses, negative cash flows from operations, accumulated deficit and other factors have raised substantial doubt about our ability to continue as a going concern.

•If we fail to successfully manage and execute our transition to an asset-light business model with a focused expansion into broadacre animal feed markets, which will require us to secure partnership and licensing agreements to generate and scale our product innovations, our results of operations could be harmed.

8

•We will need to raise additional capital in the future to fund our operations and we may be unable to raise such funds when needed and on acceptable terms.

•The actions associated with the execution of our expanded Liquidity Improvement Plan could be insufficient to achieve our financial objectives and could have negative consequences on our business and growth.

•We cannot assure you that our evaluation of potential strategic alternatives to enhance value for stockholders will be successful; and there may be negative impacts on our business and stock price as a result of the process of exploring strategic alternatives.

•Any collaboration arrangements that we have or may enter into may not be successful, which could adversely affect our anticipated revenues and our ability to develop and commercialize our product candidates.

•The divestiture of assets presents risks and challenges that could negatively impact our business, financial condition, and results of operations.

•We have a history of net losses and we may not achieve or maintain profitability.

•We face significant competition and many of our competitors have substantially greater financial, technical and other resources than we do.

•To compete effectively, we must introduce new products that achieve market acceptance.

•If we are unable to effectively apply our CropOS® platform, effectively obtain and integrate new technologies into the platform or to create new platforms, our results of operations, client relationships, and growth could be adversely affected.

•Our ability to contract for sufficient acreage with the appropriate nutrient profile on a cost-effective basis presents challenges.

•Cybersecurity vulnerabilities, threats and more sophisticated and targeted computer crimes pose a risk to our systems, networks, products and data.

•We have recognized goodwill and long-lived asset impairment charges for the year ended December 31, 2023, and we could be required to record additional material impairment charges on intangible assets and long-lived assets in the future.

•We have a limited operating history, which makes it difficult to evaluate our current business and prospects and may increase the risk of investment.

•If we are unable to identify and remediate any material weaknesses in our internal control over financial reporting or otherwise fail to maintain an effective system of internal control over financial reporting, this may result in material misstatements of our consolidated financial statements or failure to meet our periodic reporting obligations.

•The overall agricultural industry is susceptible to commodity price changes and we are exposed to market risks from changes in commodity prices.

•Adverse weather conditions, natural disasters, crop disease, pests and other natural conditions can impose significant costs and losses on our business.

•Our business activities are currently conducted at a limited number of locations, which makes us susceptible to damage or business disruptions caused by natural disasters or acts of vandalism.

•If we fail to manage our future growth effectively, our business could be materially adversely affected.

•If our early testing of pipeline products is unsuccessful, we may be unable to complete the development of product candidates on a timely basis or at all.

•The successful commercialization of our products depends on our ability to produce high-quality products cost-effectively on a large scale and to accurately forecast demand for our products, and we may be unable to do so.

•Products that we develop, and food and feed containing our products, may fail to meet standards established by third-party non-GMO verification organizations, which could reduce the value of our products to customers.

•If we are sued for defective products and if such lawsuits were determined adversely, we could be subject to substantial damages, for which insurance coverage is not available.

•Our risk management strategies may not be effective.

•We rely on information technology systems and any inadequacy, failure, interruption or security breaches of those systems may harm our ability to effectively operate our business.

•We use artificial intelligence in our business, and challenges with properly managing its use could result in reputational harm, competitive harm, and legal liability, and adversely affect our results of operations.

•We depend on key management personnel and attracting, training and retaining other qualified personnel, and our business could be harmed if we lose key management personnel or cannot attract, train and retain other qualified personnel.

•We incur substantial costs as a result of operating as a public company and our management devotes substantial time to maintaining compliance with applicable rules and regulations.

•Disruptions in the worldwide economy may adversely affect our business, results of operations and financial condition.

Risks Relating to Our Capital Structure

•We have borrowed and may be required to borrow funds in the future.

9

•Failure to obtain capital when needed on acceptable terms, or at all, may force us to delay, limit, reduce or terminate our product development efforts or other operations.

Risks Relating to Our Common Stock

•The NYSE may delist our securities from trading on its exchange, which could limit investors’ ability to make transactions in our securities and subject us to additional trading restrictions.

•Future sales, or the perception of future sales, by us or our stockholders in the public market could cause the market price of our common stock to decline, and any issuance of additional common stock, or securities convertible into common stock, could dilute common stockholders.

•The market price of our common stock is highly volatile, which could lead to losses by investors and costly securities litigation.

•If securities analysts do not publish research or reports about our business or if they downgrade our common stock or our sector, our common stock price and its trading volume could decline.

•We qualify as an “emerging growth company” within the meaning of the Securities Act, and because we take advantage of certain exemptions from disclosure requirements available to emerging growth companies, it could make our securities less attractive to investors and may make it more difficult to compare our performance to the performance of other public companies.

•Because there are no current plans to pay cash dividends on our common stock for the foreseeable future, you may not receive any return on your investment unless you sell your common stock for a price greater than that which you paid for it.

•Anti-takeover provisions in our organizational documents could delay or prevent a change of control.

Risks Relating to Our Outstanding Warrants

•Our outstanding warrants are exercisable for common stock, which would increase the number of shares eligible for future resale in the public market and result in dilution to stockholders.

•We may amend the terms of the Public Warrants in a manner that may be adverse to holders of Public Warrants with the approval by the holders of at least 65% of the then-outstanding Public Warrants.

•We may redeem unexpired Public Warrants prior to their exercise at a time that is disadvantageous to you, thereby making the Public Warrants worthless.

•Holders of our warrants will have no rights as a common stockholder until such holders exercise their warrants and acquire our common stock.

•Almost all of our outstanding warrants are accounted for as liabilities and the changes in value of the warrants could have a material effect on our financial results.

•The NYSE has delisted our Public Warrants from trading on its exchange, which could limit investors’ ability to make transactions in our securities and subject us to additional trading restrictions.

Risks Relating to Our Intellectual Property

•Patents and patent applications involve highly complex legal and factual questions, which, if determined adversely to us, could negatively impact our competitive position.

•We will not seek to protect our intellectual property rights in all jurisdictions throughout the world and we may not be able to adequately enforce our intellectual property rights even in the jurisdictions where we seek protection.

•Third parties may assert rights to inventions we develop or otherwise regard as our own.

•We may be unsuccessful in developing, licensing or acquiring intellectual property that may be required to develop and commercialize our product candidates.

Risks Relating to Regulatory and Legal Matters

•The regulatory environment in the U.S. for our current and future products is uncertain and evolving.

•The regulatory environment outside the U.S. varies greatly from jurisdiction to jurisdiction and there is less certainty how our products will be regulated.

•Government policies and regulations, particularly those affecting the agricultural sector and related industries, could adversely affect our operations and profitability.

•We are subject to numerous environmental, health and safety laws and regulations relating to our use of biological materials and our food production operations. Compliance with such laws and regulations could be time consuming and costly.

•Litigation or legal proceedings could expose us to significant liabilities and have a negative impact on our reputation or business.

•Our ability to use net operating loss carryforwards and other tax attributes may be limited in connection with the Merger or other ownership changes.

10

Risks Relating to Our Business

While our audited consolidated financial statements have been prepared on a going concern basis, we believe that our recurring net losses, negative cash flows from operations, accumulated deficit and other factors have raised substantial doubt about our ability to continue as a going concern.

There is substantial doubt about our ability to continue as a going concern, as we currently do not have adequate financial resources to meet our forecasted operating costs as they come due in the ordinary course of business for at least twelve months from the filing of this report. For the year ended December 31, 2023, we incurred a net loss from continuing operations of $111.2 million, negative cash flows from operating activities of $73.1 million and capital expenditures of $11.8 million. As of December 31, 2023, we had cash and cash equivalents and marketable securities of $48.7 million. As of December 31, 2023, we had an accumulated deficit of $523.8 million and term debt and notes payable of $60.5 million, which are subject to repayment terms and covenants further described in Note 14—Debt in this report. We have incurred significant losses since our inception, primarily to fund investment into technology and costs associated with early-stage commercialization of products and we expect to continue generating operating losses in the near term. These matters raise substantial doubt about our ability to continue as a going concern.

Our potential inability to continue as a going concern may materially adversely affect our share price and our ability to raise new capital, enter into agreements with third parties, meet our obligations as they become due and otherwise execute our business strategy. If we are unable to generate sustainable operating profit and sufficient cash flows, then our future success will depend on our ability to raise capital. We cannot be certain that additional capital, whether through selling additional debt or equity securities or obtaining a line of credit or other loan, will be available to us or, if available, will be on terms acceptable to us. If we are unable to raise additional financing and increase revenue or reduce expenses, we may be unable to continue to fund our operations, develop our products, realize value from our assets, or discharge our liabilities in the normal course of business. If we become unable to continue as a going concern, we could have to liquidate our assets, and potentially realize significantly less than the values at which they are carried on our financial statements, and stockholders could lose all or part of their investment in our shares.

If we fail to successfully manage and execute our transition to an asset-light business model with a focused expansion into broadacre animal feed markets, which will require us to secure partnership and licensing agreements to generate revenue and scale our product innovations, our results of operations could be harmed.

On October 31, 2023, we announced plans to improve our financial position and accelerate our transition to an asset-light business model with a focused expansion into broadacre animal feed markets. We cannot provide any assurance that we will be able to manage and execute these plans successfully or in a timely manner, or that, even if we do, we will have sufficient liquidity to pursue our long-term strategy. Our ability to accomplish these plans is subject to significant business, financial, operational, timing, market, and other risks, including necessary participation of third parties. For example, execution of our asset-light business model and our expanded Liquidity Improvement Plan resulted in the divestiture of our processing assets, as a result of which our ability to generate revenue from product sales has been substantially diminished. We must secure new partnership and licensing agreements to generate revenues and scale our product innovations. There is no assurance that we will be able to secure the necessary partnership and licensing agreements to generate revenues or achieve our acreage goals in the coming years. If we are unable to identify and realize new sources of revenue, including from collaborative arrangements, joint operating activities, partnerships and licensing opportunities, our ability to execute our long-term strategy will be harmed. We may not be successful in our efforts to execute our transition to an asset-light business model, generate revenue from partnership and licensing arrangements, or attain and maintain profitable operations. Our ability to successfully manage and execute this transition is subject to a variety of conditions and factors, some of which are beyond our control, including our ability to secure new partnership and licensing agreements. If we are unsuccessful in these efforts, our cash balances and operating cash flow alone will be insufficient to fund our longer-term capital and liquidity needs.

If we are unable to successfully manage and execute our transition to an asset-light business model and our expanded Liquidity Improvement Plan, we may not realize the expected benefits of these plans, and our results of operations could be harmed.

The actions associated with the execution of our expanded Liquidity Improvement Plan could be insufficient to achieve our financial objectives and could have negative consequences on our business and growth.

On March 27, 2023, our Board committed to the Liquidity Improvement Plan, which together with subsequent cost-saving measures, is intended to improve liquidity by an estimated $65 million to $85 million by the end of 2024. We subsequently expanded our cost-cutting efforts under the Liquidity Improvement Plan. Through the combination of cash on hand, savings driven by our expanded Liquidity Improvement Plan, and net proceeds from our completed and any future asset dispositions,

11

and securing additional financing, we expect to improve our liquidity position. We plan to use this anticipated liquidity runway while we seek to secure partnership and licensing agreements to help us execute our long-term strategy.

While we expect the actions associated with the execution of our expanded Liquidity Improvement Plan to be substantially complete by the end of the fourth quarter of 2024, there can be no assurance that such actions or any other cost reduction initiatives will be successfully or timely implemented, or that they will materially and positively impact our ability to achieve our financial objectives, or that they will leave us sufficient liquidity to pursue our plans or remain a going concern. Because the Liquidity Improvement Plan involves restructuring certain parts of our organization, the associated cost reductions could adversely impact productivity, product innovations and sales to an extent we have not anticipated. In addition, divestiture of our processing assets and our exploration of strategic alternatives, could adversely impact our ability to generate revenues. Our ability to complete the actions associated with the execution of our expanded Liquidity Improvement Plan and achieve the anticipated benefits within the expected timeframe is subject to estimates and assumptions, and actual results may vary materially from our expectations, including as a result of factors that are beyond our control. Our efforts to create a more cost-efficient organization and enhance our capital structure to execute on our strategic priorities may not be successful. Even if we successfully execute these actions in a timely manner and they generate the anticipated cost savings, our expanded Liquidity Improvement Plan may have other unforeseeable or unintended consequences that could materially adversely impact our profitability and business, including our research and development initiatives and our ability to commercialize our product candidates. To the extent that we do not achieve the intended benefits of the actions associated with the execution of our expanded Liquidity Improvement Plan or suffer negative consequences as a result of its implementation, our business and results of operations may be materially adversely affected.

We will need to raise additional capital in the future to fund our operations and we may be unable to raise such funds when needed and on acceptable terms.

We fully repaid the Convertible Notes Payable on February 13, 2024. We currently intend to obtain new financing. We can make no assurances that we will be able to secure any new financing, or that the terms of any new financing will be more favorable to us than our prior indebtedness. If we are unable to obtain new financing on favorable terms, in a timely manner, or at all, in an amount sufficient to meet our liquidity needs, our business, financial condition, results of operations, prospects, and ability to continue as a going concern could be adversely affected.

If we elect to raise additional funds or additional funds are required, we may raise such funds from time to time through public or private equity offerings, debt financings, corporate collaboration and licensing arrangements or other financing alternatives. Additional equity or debt financing or corporate collaboration and licensing arrangements may not be available on acceptable terms, if at all. If we are unable to raise additional capital in sufficient amounts or on terms acceptable to us, we will be prevented from pursuing licensing, development, acquisition and commercialization efforts and our ability to generate revenues and achieve or sustain profitability will be substantially harmed.

If we raise additional funds by issuing equity securities, our stockholders will experience dilution. Debt financing, if available, would result in increased fixed payment obligations and may involve agreements that include covenants limiting or restricting our ability to take specific actions, such as incurring additional debt, making capital expenditures or declaring dividends. Any debt financing or additional equity that we issue may contain terms, such as liquidation preferences, superior voting rights or the issuance of derivative securities, which could have a further dilutive effect on or subordinate the rights of our current investors. If we raise additional funds through collaboration and licensing arrangements with third parties, it may be necessary to relinquish valuable rights to our technologies, future revenue streams or product candidates or to grant licenses on terms that may not be favorable to us. Should the financing we require to sustain our working capital needs be unavailable or prohibitively expensive when we require it, our business, operating results, financial condition and prospects could be materially and adversely affected and we may be unable to continue our operations.

We cannot guarantee that we will be able to meet existing financial covenants or that any new financing will be available to us on favorable terms, in a timely manner, or at all, and the failure to procure any new financing we obtain may make it more difficult for us to operate our business, implement our growth plans, or achieve our financial objectives. If this were to occur, we could be required to delay, limit, reduce or terminate our manufacturing, research and development activities, growth and expansion plans, establishment of strategic partnership and licensing relationships, sales and marketing capabilities or other activities that may be necessary to generate revenue and achieve profitability, any of which could have significant negative consequences for our business, financial condition and results of consolidated operations.

12

We cannot assure you that our evaluation of potential strategic alternatives to enhance value for stockholders will be successful; and there may be negative impacts on our business and stock price as a result of the process of exploring strategic alternatives.

On August 9, 2023, our Company announced the commencement of a process to explore strategic alternatives, which could include, but not be limited to, a sale of all or parts of our Company, a merger, joint venture, or other transaction. Our Board of Directors (“Board”) has not set a timetable for the completion of this review process and there can be no assurance that it will result in any transaction or outcome. Whether the process will result in any additional transactions, will depend on numerous factors, some of which are beyond our control. Such factors include the interest of potential acquirers or strategic partners in a potential transaction, the value potential acquirers or strategic partners attribute to our businesses and their respective prospects, our stock price, market conditions, interest rates and industry trends.

Our stock price may be adversely affected if the evaluation does not result in additional transactions or if one or more transactions are agreed to or consummated on terms that investors view as unfavorable to us. Even if one or more additional transactions are completed, there can be no assurance that any such transactions will be successful or have a positive effect on stockholder value. Our Board may also determine that no additional transaction is in the best interest of our stockholders. In addition, our financial results and operations could be adversely affected by the strategic process and by the uncertainty regarding its outcome. The attention of management and our Board could be diverted from our core business operations. We have diverted capital and other resources to the process that otherwise could have been used in our business operations, and we intend to do so. We could incur substantial expenses associated with identifying and evaluating potential strategic alternatives, including those related to employee retention payments, equity compensation, severance pay and legal, accounting and financial advisor fees. In addition, the process could lead us to lose or fail to attract, retain and motivate key employees, and to lose or fail to attract strategic partners, licensees, customers, suppliers or other business partners. Furthermore, it could expose us to litigation. The public announcement of a strategic alternative may also yield a negative impact on our stock price and operating results if prospective or existing counter-parties are reluctant to commit to new or renewal contracts or if existing customers decide to move their business to a competitor. We do not intend to disclose developments or provide updates on the progress or status of the strategic process until our Board deems further disclosure is appropriate or required. Accordingly, speculation regarding any developments related to the review of strategic alternatives and perceived uncertainties related to the future of our Company could cause our stock price to fluctuate significantly.

Any collaboration arrangements that we have or may enter into may not be successful, which could adversely affect our anticipated revenues and our efforts to commercialize our product candidates.

We have entered into collaboration arrangements with third parties for the development or commercialization of our products, such as our collaboration agreement with ADM, and intend to enter in additional such agreements in the future. To the extent that we decide to enter additional collaboration arrangements, we will face significant competition in seeking appropriate partners, and we will likely have limited control over the amount and timing of resources that any future collaborators dedicate to the development or commercialization of our product candidates. In addition, future collaborators may have significantly greater financial resources than we do and may compete with our business, as ADM does, which could enable such competitors to use our technologies to develop their own products that would compete with our products. Our ability to generate revenue from these arrangements depends in part on our collaborators’ abilities to successfully perform the functions assigned to them and our ability to work together. If our collaborations do not result in the successful development and commercialization of products, or if any of our collaborators terminates its agreement with us, we may not receive some of all of any milestone, royalty or other payments provided for under the collaboration agreements. If we do not receive the payments we expect under these agreements, our development of product candidates could be delayed and we may need additional resources to develop our product candidates. In addition, if any collaborator terminates its agreement with us, our revenue generation efforts would be harmed, and we may find it more difficult to attract new collaborators and our reputation among the business and financial communities could be adversely affected. Macroeconomic trends, including those that played a factor in our decision to transition to an asset-light business model, also impact our ability to realize the anticipated benefits of, and to maintain, our collaboration agreements, and could impact our ability to enter into new collaboration agreements. These macroeconomic trends include, without limitation, the emergence of significant market headwinds in the food, aquaculture, and specialty oil markets, and acreage acquisition costs.

Moreover, collaboration arrangements are complex and time-consuming to negotiate, document, implement and maintain. To the extent that we seek to enter into additional collaboration agreements, we may not be successful in our efforts to establish and implement such collaboration or other alternative arrangements in a timely manner, on favorable terms, or at all. If we are unable to do so, we may have to curtail the development of the product candidate for which we are seeking to collaborate, or increase our expenditures and undertake development or commercialization activities at our own expense. If we elect to increase our expenditures to fund development or commercialization activities on our own, we may need to obtain additional capital, which may not be available to us on acceptable or timely terms, or at all. If we do not have sufficient funds, we may not be able to further develop our product candidates or bring them to market and generate product revenue.

13

The divestiture of assets presents risks and challenges that could negatively impact our business, financial condition and results of operations.

Following the divestiture of the Creston and Seymour processing facilities, our ability to generate revenue from product sales has been substantially diminished. As of December 31, 2023, we had cash and marketable securities of $48.7 million from continuing operations, and cash of $0.3 million from discontinued operations. We have had recurring net losses from operations and an accumulated deficit of $524 million as of December 31, 2023. Given our net losses and with only these funds, we will need to seek significant additional funds in the future through equity or debt financings, or strategic alliances with third parties, either alone or in combination, to fund our business plan and to complete our transition to an asset-light operating company. In addition, our transition to an asset-light business model requires that we secure new partnership and licensing agreements to generate revenues and scale our product innovations. There is no assurance that we will be able to secure the necessary partnership and licensing agreements to generate revenues or achieve our acreage goals in the coming years. If we are unable to sufficiently and timely license, sell-to-market or otherwise monetize our intellectual property and food and feed inventory, we may fail to generate enough revenue to continue as a going concern, including making required debt service payments and paying our general and administrative expenses.

These divestitures present risks relating to the availability and use of proceeds generated from the divestitures in light of contractual restrictions under the transaction documents. We may also encounter challenges relating to the separation of operations, products, services or personnel, and as a result of any future liabilities we may retain after completing the divestitures. Any difficulties that we face in connection with the divestitures may result in management’s attention being diverted from our continuing business operations. Significant time and expenses have been incurred to divest the assets described above, which may adversely affect operations as dispositions have required and may in the future require our continued financial involvement, such as through transition service agreements, guarantees, and indemnities or other current or contingent financial obligations and liabilities.

We have a history of net losses and we may not achieve or maintain profitability.