As filed with the Securities and Exchange Commission on January 8, 2021

Registration No. 333-

Delaware | | | 6162 | | | 47-1776572 |

(State or other jurisdiction of incorporation or organization) | | | (Primary Standard Industrial Classification Code Number) | | | (I.R.S. Employer Identification Number) |

Joseph H. Kaufman, Esq. Simpson Thacher & Bartlett LLP 425 Lexington Avenue New York, NY 10017 (212) 455-2000 | | | Michael Kaplan, Esq. Shane Tintle, Esq. Davis Polk & Wardwell LLP 450 Lexington Avenue New York, NY 10017 (212) 450-4000 |

Large accelerated filer | | | ☐ | | | Accelerated filer | | | ☐ |

Non-accelerated filer | | | ☒ | | | Smaller reporting company | | | ☐ |

| | | | | Emerging growth company | | | ☒ |

Title of Each Class of Securities to be Registered | | | Proposed Maximum Aggregate Offering Price(1)(2) | | | Amount of Registration Fee |

Common stock, par value $0.01 per share | | | $100,000,000 | | | $10,910 |

(1) | Includes additional shares of common stock that the underwriters have the option to purchase. See “Underwriting (Conflicts of Interest).” |

(2) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(o) of the Securities Act of 1933, as amended. |

| | | Per Share | | | Total | |

Price to the public | | | $ | | | $ |

Underwriting discounts and commissions(1) | | | $ | | | $ |

Proceeds to us (before expenses) | | | $ | | | $ |

Proceeds to the selling stockholders (before expenses) | | | $ | | | $ |

(1) | See “Underwriting (Conflicts of Interest)” for additional information regarding underwriter compensation. |

Goldman Sachs & Co. LLC | | | Wells Fargo Securities | | | Morgan Stanley | | | UBS Investment Bank |

Credit Suisse | | | J.P. Morgan | | | BofA Securities |

JMP Securities | | | Piper Sandler | | | R. Seelaus & Co., LLC | | | SPC Capital Markets LLC |

Wedbush Securities | | | Zelman Partners LLC |

| | | Page | |

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | | ||

| | |

• | “An Agency” or “Agencies” refers to Ginnie Mae, the FHA, the VA, the USDA and/or GSEs. |

• | “CFPB” refers to the Consumer Financial Protection Bureau. |

• | “Fannie Mae” refers to the Federal National Mortgage Association. |

• | “FHA” refers to the Federal Housing Administration. |

• | “Freddie Mac” refers to the Federal Home Loan Mortgage Corporation. |

• | “Ginnie Mae” refers to the Government National Mortgage Association. |

• | “GSE” refers to Government-Sponsored Enterprises, such as Fannie Mae and Freddie Mac. |

• | “Holdings” refers to Home Point Capital LP, a Delaware limited partnership, the direct parent of Home Point Capital Inc. |

• | “HUD” refers to the U.S. Department of Housing and Urban Development. |

• | “MBS” refers to mortgage-backed securities—a type of asset-backed security that is secured by a group of mortgage loans. |

• | “MSRs” refers to mortgage servicing rights—the right and obligation to service a loan or pool of loans and to receive a servicing fee as well as certain ancillary income. MSRs may be bought and sold, resulting in the transfer of loan servicing obligations. MSRs are designated as such when the benefits of servicing the loans are expected to adequately compensate the servicer for performing the servicing. |

• | “Sponsor” or “Stone Point Capital” refers to Stone Point Capital LLC. |

• | “Trident Stockholders” refers, collectively, to one or more investment entities directly or indirectly managed by Stone Point Capital, including Trident VI, L.P., Trident VI Parallel Fund, L.P., Trident VI DE Parallel Fund, L.P. and Trident VI Professionals Fund, L.P. |

• | “USDA” means the U.S. Department of Agriculture. |

• | “VA” means the U.S. Department of Veterans Affairs. |

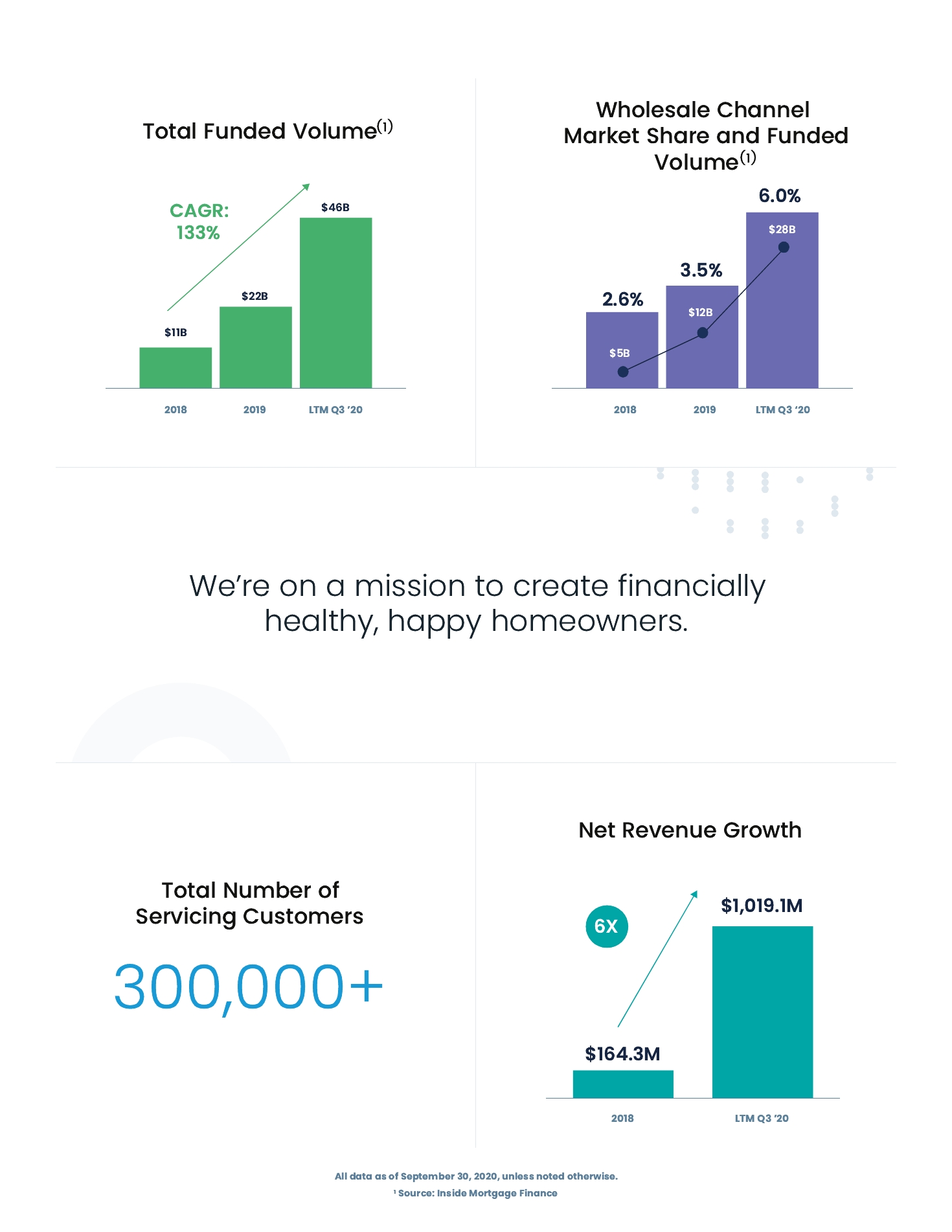

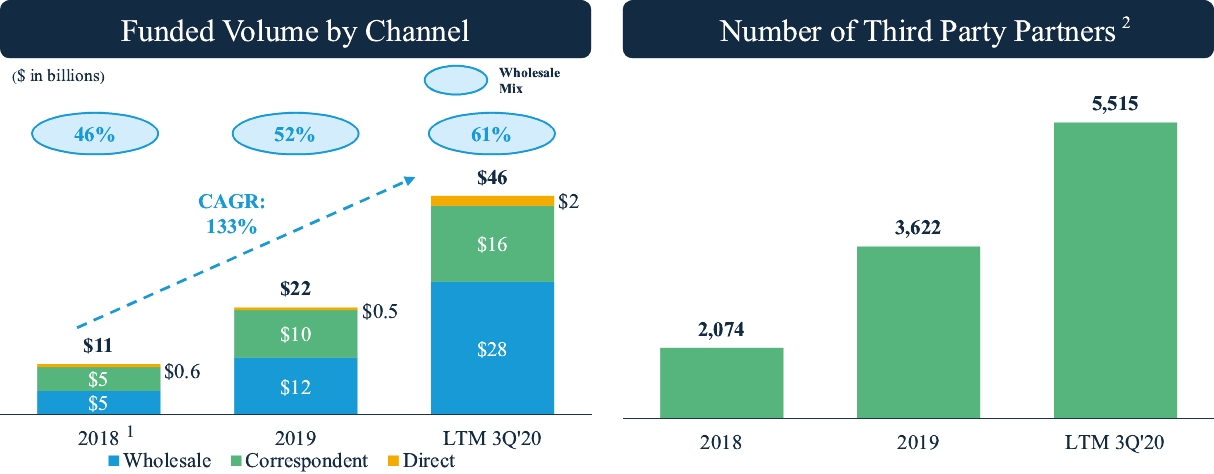

(1) | Total origination volume excludes origination volume from the Distributed Retail channel, which was included in discontinued operations in our results of operations for the year ended December 31, 2018. |

(2) | Origination volume figures used to calculate market share include $1.0 billion of Distributed Retail originations in our results of operations for the year ended December 31, 2018. |

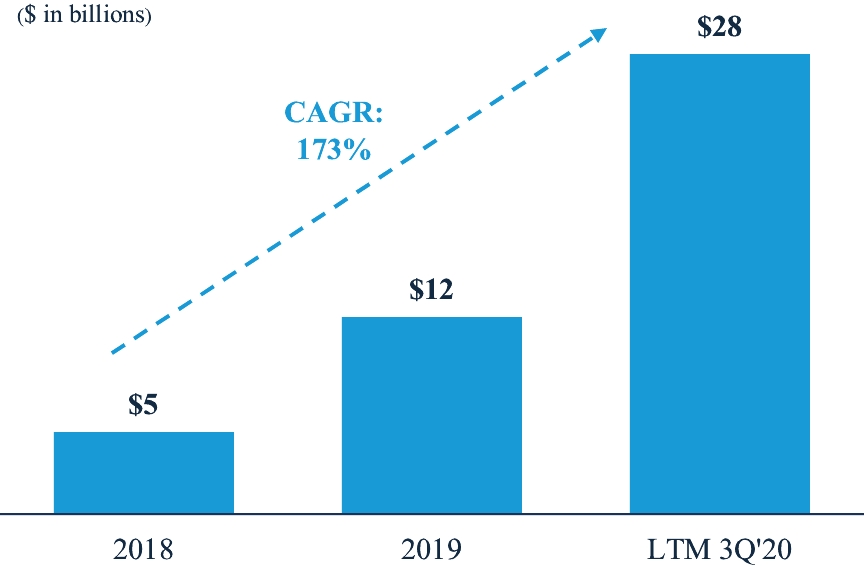

* | LTM 3Q’20 represents the twelve months ended September 30, 2020. |

* | LTM 3Q’20 represents the twelve months ended September 30, 2020. |

* | LTM 3Q’20 represents the twelve months ended September 30, 2020. |

• | provide us efficient access to both purchase and refinance transactions throughout market cycles; |

• | benefit from the premise that in-market advisors will continue to be a cornerstone of the mortgage origination process; |

• | are highly scalable and flexible; and |

• | provide an optimized experience for our customers. |

(1) | Total origination volume excludes origination volume from the Distributed Retail channel, which was included in discontinued operations in our results of operations for the year ended December 31, 2018. |

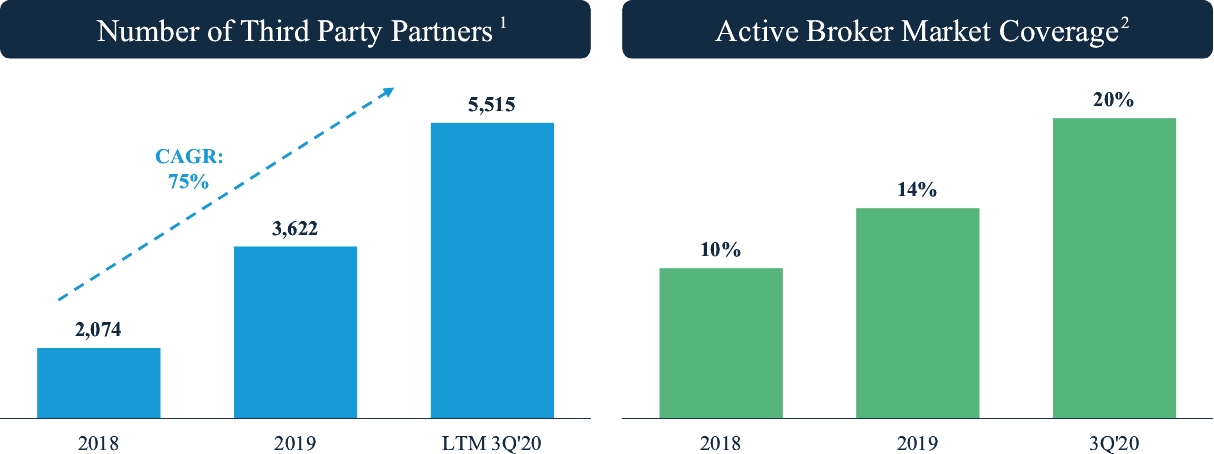

(2) | Third Party Partners includes both Broker Partners and Correspondent Partners. |

* | LTM 3Q’20 represents the twelve months ended September 30, 2020. |

* | LTM 3Q’20 represents the twelve months ended September 30, 2020. |

Activation Rate by Broker Partner Cohort | | | Wallet Share Growth by Broker Partner Cohort Following Initial Onboarding |

* | LTM 3Q’20 represents the twelve months ended September 30, 2020. |

(1) | Third Party Partners includes both Broker Partners and Correspondent Partners. |

(2) | Active broker market coverage is calculated as the total number of active brokers at Home Point divided by the total number of brokers in the market. |

* | LTM 3Q’20 represents the twelve months ended September 30, 2020. |

* | LTM 3Q’20 represents the twelve months ended September 30, 2020. |

* | LTM 3Q’20 represents the twelve months ended September 30, 2020. |

* | LTM 3Q’20 represents the twelve months ended September 30, 2020. |

* | LTM 3Q’20 represents the twelve months ended September 30, 2020. |

• | economies of scale: allows brokers to benefit from the scale of a larger organization while being able to run their business at a size that can be most responsive to their customers; |

• | optimal choice: rather than needing to work with one originator, brokers have the ability to partner with multiple lenders to determine the best financing alternative for their customers; and |

• | scalability of cost structure: reduce cost per loan and limited overhead. |

• | the spread of the COVID-19 (as defined below) outbreak and severe disruptions in the U.S. and global economy and financial markets it has caused; |

• | our reliance on our financing arrangements to fund mortgage loans and otherwise operate our business; |

• | the dependence of our loan origination and servicing revenues on macroeconomic and U.S. residential real estate market conditions; |

• | the requirement to repurchase mortgage loans or indemnify investors if we breach representations and warranties; |

• | counterparty risk; |

• | the requirement to make servicing advances that can be subject to delays in recovery or may not be recoverable in certain circumstances; |

• | competition for mortgage assets that may limit the availability of desirable originations, acquisitions and result in reduced risk-adjusted returns; |

• | our ability to continue to grow our loan origination business or effectively manage significant increases in our loan production volume; |

• | competition in the industry in which we operate; |

• | our ability to acquire loans and sell the resulting MBS in the secondary markets on favorable terms in our production activities; |

• | our being a “controlled company” within the meaning of rules and, as a result, qualifying for exemptions from certain corporate governance requirements; and |

• | our Sponsor controlling us and its interests conflicting with ours or yours in the future. |

• | the last day of the year following the fifth anniversary of this offering; |

• | the last day of the first year in which our annual gross revenues exceed an amount specified by regulation (currently $1.07 billion); |

• | the day we are deemed to be a “large accelerated filer” as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended, or the Exchange Act, which would occur if the market value of our common stock held by non-affiliates exceeded $700.0 million as of the last business day of the second quarter of such year; and |

• | the date on which we have issued more than $1.0 billion in non-convertible debt securities during the preceding three-year period. |

• | no exercise of the underwriters’ option to purchase additional shares of our common stock; |

• | an initial public offering price of $ per share of common stock, which is the midpoint of the estimated price range set forth on the cover page of this prospectus; |

• | the filing and effectiveness of our amended and restated certificate of incorporation and the adoption of our amended and restated bylaws immediately prior to the consummation of this offering; |

• | the -for-one stock split of our common stock, which we intend to effectuate prior to the effectiveness of the registration statement of which this prospectus forms a part; and |

• | the merger of Holdings with and into the Company concurrent with the consummation of this offering, with the Company as the surviving entity. |

• | shares of common stock issuable upon exercise of outstanding options, (i) of which are vested, with a weighted-average exercise price of $ per share, and (ii) of which are not vested, with a weighted-average exercise price of $ per share, in each case, issued under our 2015 Option Plan. See “Executive Compensation—Narrative Disclosure to Summary Compensation Table—Equity Awards”; and |

• | shares of common stock reserved for future issuance under the 2021 Incentive Plan and shares of common stock reserved for future issuance under the 2021 Employee Stock Purchase Plan, each of which we intend to adopt in connection with this offering. See “Executive Compensation—Actions in Connection with this Offering.” |

| | | Nine months ended September 30, | | | Year ended December 31, | |||||||

(In thousands, except shares and per share amounts) | | | 2020 | | | 2019 | | | 2019 | | | 2018 |

| | | (unaudited) | | | (audited) | |||||||

Statement of Operations Data | | | | | | | | | ||||

Gain on loans, net | | | $962,778 | | | $135,495 | | | $199,501 | | | $84,068 |

Loan fee income | | | 60,630 | | | 19,829 | | | 32,112 | | | 19,603 |

Interest income | | | 42,370 | | | 35,101 | | | 51,801 | | | 35,179 |

Interest expense | | | (47,845) | | | (41,933) | | | (57,942) | | | (47,486) |

Interest loss, net | | | (5,475) | | | (6,832) | | | (6,141) | | | (12,307) |

Loan servicing fees | | | 133,904 | | | 104,089 | | | 144,228 | | | 119,049 |

Change in fair value of mortgage servicing rights | | | (230,524) | | | (151,168) | | | (173,134) | | | (47,312) |

Other income | | | 1,022 | | | 1,591 | | | 3,159 | | | 1,156 |

Total net revenue | | | 922,335 | | | 103,004 | | | 199,725 | | | 164,257 |

| | | | | | | | | |||||

Compensation and benefits | | | 251,462 | | | 104,571 | | | 156,197 | | | 109,577 |

Loan expense | | | 28,581 | | | 10,182 | | | 15,626 | | | 16,882 |

Loan servicing expense | | | 22,742 | | | 15,781 | | | 20,924 | | | 18,488 |

Occupancy and equipment | | | 17,006 | | | 12,567 | | | 16,768 | | | 20,521 |

General and administrative | | | 28,373 | | | 14,687 | | | 21,407 | | | 29,165 |

Depreciation and amortization | | | 4,222 | | | 4,394 | | | 5,918 | | | 7,612 |

Other expenses | | | 12,087 | | | 2,770 | | | 4,296 | | | 4,060 |

Total expenses | | | 364,473 | | | 164,952 | | | 241,136 | | | 206,305 |

| | | | | | | | | |||||

Income (loss) from continuing operations before income tax | | | 557,862 | | | (61,948) | | | (41,411) | | | (42,048) |

Income tax expense (benefit) from continuing operations | | | 149,306 | | | (14,080) | | | (9,500) | | | (10,485) |

Income from equity method investment | | | 14,050 | | | 2,591 | | | 2,701 | | | 209 |

Net income (loss) from continuing operations | | | 422,606 | | | (45,277) | | | (29,210) | | | (31,354) |

Net income from discontinued operations before tax | | | — | | | — | | | — | | | 9,707 |

Income tax provision | | | — | | | — | | | — | | | 2,550 |

Income from discontinued operations, net of tax | | | — | | | — | | | — | | | 7,157 |

Total net income (loss) | | | $422,606 | | | $(45,277) | | | $(29,210) | | | $(24,197) |

| | | Nine months ended September 30, | | | Year ended December 31, | |||||||

(In thousands, except shares and per share amounts) | | | 2020 | | | 2019 | | | 2019 | | | 2018 |

| | | (unaudited) | | | (audited) | |||||||

Basic and diluted earnings per share | | | | | | | | | ||||

Basic and diluted income (loss) per share from continuing operations | | | $4,226 | | | $(453) | | | $(292) | | | $(314) |

Basic and diluted earnings per share from discontinued operations | | | — | | | — | | | — | | | 72 |

Basic and diluted total net income (loss) per share | | | $4,226 | | | $(453) | | | $(292) | | | $(242) |

Weighted average shares of common stock outstanding | | | | | | | | | ||||

Basic and diluted | | | 100 | | | 100 | | | 100 | | | 100 |

| | | September 30, | | | December 31, | ||||

(In thousands, except shares and per share amounts) | | | 2020 | | | 2019 | | | 2018 |

| | | (unaudited) | | | (audited) | ||||

Balance Sheet Data: | | | | | | | |||

Assets: | | | | | | | |||

Cash and cash equivalents | | | $271,483 | | | $30,630 | | | $44,010 |

Restricted cash | | | 41,907 | | | 51,101 | | | 38,234 |

Cash and cash equivalents and restricted cash | | | 313,390 | | | 81,731 | | | 82,244 |

Mortgage loans held for sale (at fair value) | | | 2,281,835 | | | 1,554,230 | | | 421,754 |

Mortgage servicing rights (at fair value) | | | 583,263 | | | 575,035 | | | 532,526 |

Property and equipment, net | | | 18,595 | | | 12,051 | | | 10,075 |

Accounts receivable, net | | | 79,320 | | | 57,872 | | | 44,422 |

Derivative assets | | | 314,794 | | | 40,544 | | | 18,990 |

Goodwill and intangibles | | | 11,083 | | | 11,935 | | | 10,957 |

GNMA loans eligible for repurchase | | | 2,919,881 | | | 499,207 | | | 451,209 |

Other assets | | | 65,745 | | | 76,162 | | | 64,214 |

Total assets | | | $6,587,906 | | | $2,908,767 | | | $1,636,391 |

| | | | | | | ||||

Liabilities and Shareholder’s equity: | | | | | | | |||

Liabilities: | | | | | | | |||

Warehouse lines of credit | | | $2,092,477 | | | $1,478,183 | | | $404,237 |

Term debt and other borrowings, net | | | 374,090 | | | 424,958 | | | 276,277 |

Accounts payable and accrued expenses | | | 269,016 | | | 39,739 | | | 21,243 |

GNMA loans eligible for repurchase | | | 2,919,881 | | | 499,207 | | | 451,209 |

Other liabilities | | | 189,700 | | | 56,368 | | | 44,654 |

Total liabilities | | | $5,845,164 | | | 2,498,455 | | | 1,197,620 |

| | | | | | | ||||

Shareholder’s equity: | | | | | | | |||

Common stock (100 shares issued and outstanding, par value $0.01 per share) | | | — | | | — | | | — |

Additional paid-in-capital | | | 519,177 | | | 454,861 | | | 454,110 |

Accumulated deficit | | | 223,565 | | | (44,549) | | | (15,339) |

Total shareholder’s equity | | | 742,742 | | | 410,312 | | | 438,771 |

Total liabilities and shareholder’s equity | | | $6,587,906 | | | $2,908,767 | | | $1,636,391 |

| | | Nine months ended September 30, | | | Year ended December 31, | |||||||

| | | 2020 | | | 2019 | | | 2019 | | | 2018 | |

Other financial data | | | | | | | | | ||||

Adjusted revenue(1) | | | $1,034,687 | | | $190,522 | | | $276,907 | | | $154,118 |

Adjusted net income (loss)(1) | | | 494,598 | | | 20,347 | | | 28,185 | | | (32,006) |

Adjusted EBITDA(1) | | | 688,847 | | | 52,288 | | | 69,410 | | | (19,613) |

| | | Nine Months Ended September 30, | | | Year Ended December 31, | |||||||

($ in thousands) | | | 2020 | | | 2019 | | | 2019 | | | 2018(2) |

Origination Segment KPIs | | | | | | | | | ||||

| | | | | | | | | |||||

Origination Volume by Channel | | | | | | | | | ||||

Wholesale(3) | | | $23,772,112 | | | $7,023,411 | | | $11,564,971 | | | $4,889,220 |

Correspondent(3) | | | 12,696,815 | | | 6,676,458 | | | 10,215,300 | | | 5,081,719 |

Direct(3) | | | 1,576,959 | | | 291,302 | | | 487,322 | | | 608,148 |

Origination volume(3) | | | $38,045,886 | | | $13,991,171 | | | $22,267,593 | | | $10,579,087 |

| | | | | | | | | |||||

Gain on sale margin | | | | | | | | | ||||

Gain on sale margin (bps)(4) | | | 253.1 | | | 96.8 | | | 89.6 | | | 79.5 |

| | | | | | | | | |||||

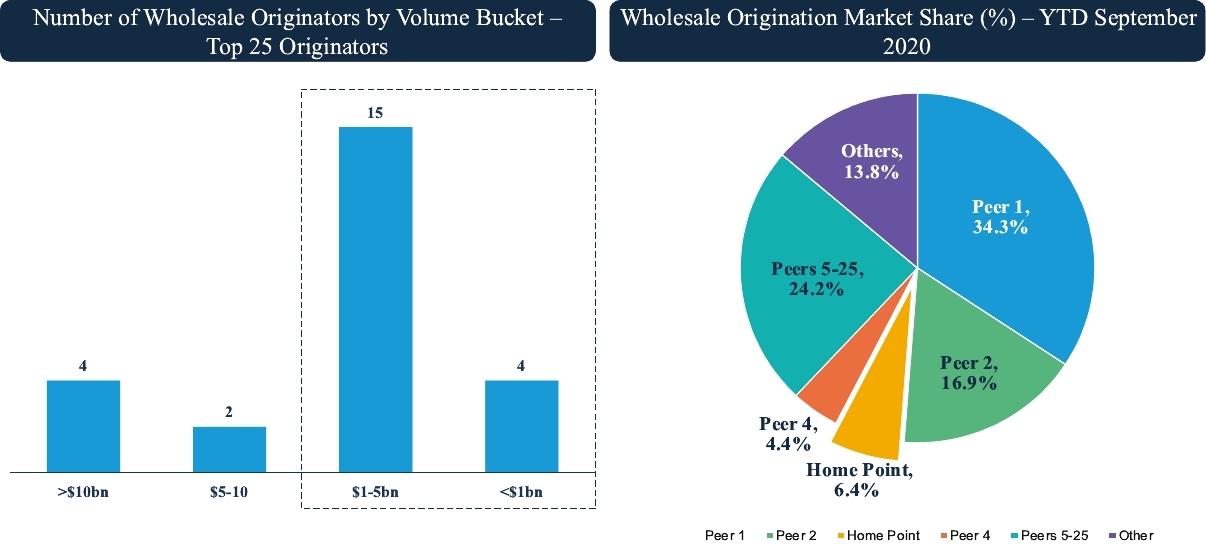

Market Share | | | | | | | | | ||||

Overall share of origination market(5) | | | 1.4% | | | 0.9% | | | 1.0% | | | 0.7% |

Share of wholesale channel(6) | | | 6.4% | | | 3.0% | | | 3.5% | | | 2.6% |

| | | | | | | | | |||||

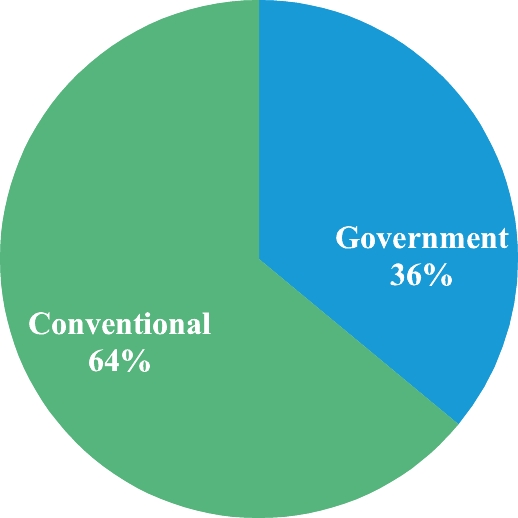

Origination Volume by Purpose(7) | | | | | | | | | ||||

Purchase | | | 31.7% | | | 54.4% | | | 50.6% | | | 66.5% |

Refinance | | | 68.3% | | | 45.6% | | | 49.4% | | | 33.5% |

| | | | | | | | | |||||

Third Party Partners | | | | | | | | | ||||

Number of Broker Partners(8) | | | 4,921 | | | 2,684 | | | 3,085 | | | 1,623 |

Number of Correspondent Partners(9) | | | 594 | | | 516 | | | 537 | | | 451 |

| | | Nine Months Ended September 30, | | | Year Ended December 31, | |||||||

($ in thousands) | | | 2020 | | | 2019 | | | 2019 | | | 2018(2) |

Servicing Segment KPIs | | | | | | | | | ||||

| | | | | | | | | |||||

Mortgage Servicing | | | | | | | | | ||||

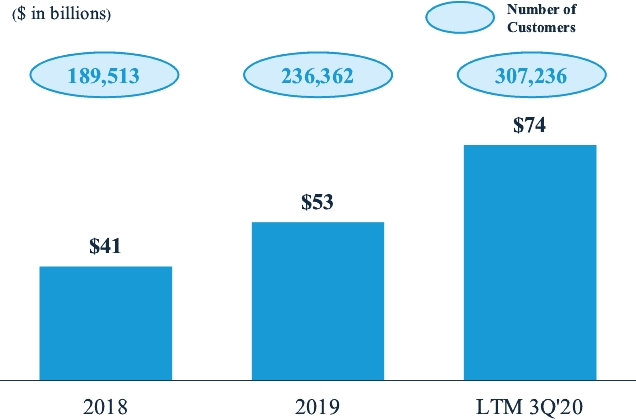

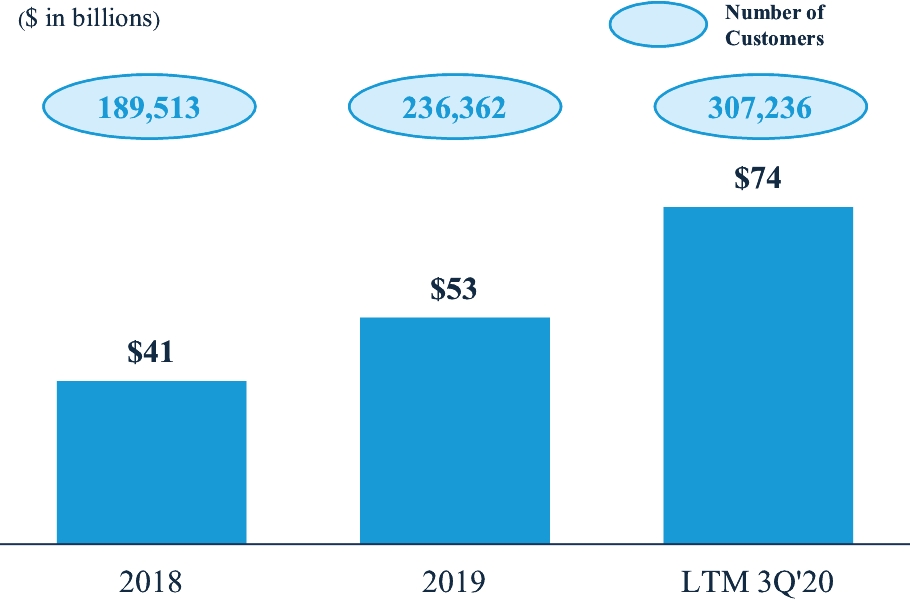

MSR servicing portfolio - UPB(10) | | | $73,951,042 | | | $47,887,643 | | | $52,600,546 | | | $41,423,825 |

Servicing portfolio - Units(11) | | | 307,236 | | | 217,558 | | | 236,362 | | | 189,513 |

| | | | | | | | | |||||

60 days or more delinquent(12) | | | 6.6% | | | 2.0% | | | 1.7% | | | 2.3% |

| | | | | | | | | |||||

MSR Portfolio | | | | | | | | | ||||

MSR multiple(13) | | | 2.6x | | | 3.2x | | | 3.4x | | | 4.3x |

(1) | We define Adjusted revenue as Total net revenue exclusive of the impact of the change in fair value of MSRs related to changes in valuation inputs and assumptions, net of MSRs hedge and adjusted for Income from equity method investment. |

| | | Nine Months Ended September 30, | | | Year Ended December 31, | |||||||

($ in thousands) | | | 2020 | | | 2019 | | | 2019 | | | 2018 |

Total net revenue | | | $922,335 | | | $103,004 | | | $199,725 | | | $164,257 |

Income from equity method investment | | | 14,050 | | | 2,591 | | | 2,701 | | | 209 |

Change in fair value of MSR (due to inputs and assumptions), net of hedge | | | 98,302 | | | 84,927 | | | 74,481 | | | (10,348) |

Adjusted revenue | | | $1,034,687 | | | $190,522 | | | $276,907 | | | $154,118 |

| | | Nine Months Ended September 30, | | | Year Ended December 31, | |||||||

($ in thousands) | | | 2020 | | | 2019 | | | 2019 | | | 2018 |

Total net income (loss) | | | $422,606 | | | $(45,277) | | | $(29,210) | | | $(24,197) |

Change in fair value of MSR (due to inputs and assumptions), net of hedge | | | 98,302 | | | 84,927 | | | 74,481 | | | (10,348) |

Income tax effect of change in fair value of MSR (due to inputs and assumptions), net of hedge | | | (26,310) | | | (19,303) | | | (17,086) | | | 2,539 |

Adjusted net income (loss) | | | $494,598 | | | $20,347 | | | $28,185 | | | $(32,006) |

| | | Nine Months Ended September 30, | | | Year Ended December 31, | |||||||

($ in thousands) | | | 2020 | | | 2019 | | | 2019 | | | 2018 |

Total net income (loss) | | | $422,606 | | | $(45,277) | | | $(29,210) | | | $(24,197) |

Income from discontinued operations, net of tax | | | — | | | — | | | — | | | (7,157) |

Interest expense on corporate debt | | | 14,411 | | | 22,324 | | | 27,721 | | | 24,962 |

Income tax expense (benefit) from continuing operations | | | 149,306 | | | (14,080) | | | (9,500) | | | (10,485) |

Depreciation and amortization | | | 4,222 | | | 4,394 | | | 5,918 | | | 7,612 |

Change in fair value of MSR (due to inputs and assumptions), net of hedge | | | 98,302 | | | 84,927 | | | 74,481 | | | (10,348) |

Adjusted EBITDA | | | $688,847 | | | $52,288 | | | $69,410 | | | $(19,613) |

(2) | Unless otherwise indicated, our Distributed Retail channel was included in discontinued operations in our results of operations for the year ended December 31, 2018 and as such it has been excluded from our key performance indicators for the year ended December 31, 2018. |

(3) | Origination dollar value of new loans funded by channel. Origination volume excludes Origination volume from the Distributed Retail channel, which was included in discontinued operations in our results of operations for the year ended December 31, 2018. |

(4) | Calculated as Gain on sale, net divided by Origination volume. |

(5) | Calculated as the Company’s originations dollar value for the year divided by the total residential originations in the United States of America per Inside Mortgage Finance, a third party provider of residential mortgage industry news and statistics each year. Origination volume figures used to calculate market share include $1 billion of Distributed Retail originations in our results of operations for the year ended December 31, 2018. |

(6) | Calculated as the Company’s originations dollar value for the year divided by the total wholesale originations in the United States of America per Inside Mortgage Finance, each year. |

(7) | Origination volume excludes Origination volume from the Distributed Retail channel, which was included in discontinued operations in our results of operations for the year ended December 31, 2018. |

(8) | Number of Broker Partners with whom the Company sources loans from. |

(9) | Number of Correspondent Partners from whom the Company purchases loans from. |

(10) | The unpaid principal balance of loans we service on behalf of Ginnie Mae, Fannie Mae, Freddie Mae and others, at period end. |

(11) | Number of loans in our serving portfolio at period end. |

(12) | Total balances of outstanding loan principals for which installment payments are at least 60 days past due as a percentage of the outstanding loan principal as of a specified date. |

(13) | Calculated as the MSR fair market value as of a specified date divided by the related UPB divided by the weighted average service fee. |

• | a general decline in business activity; |

• | negatively impacting demand for our mortgage loan products, as well as borrowers’ ability to fulfill their loan obligations leading to an increase in delinquency rates, which could have a significant impact on the value of our mortgage assets; |

• | the requirement for us to advance material amounts of cash for delinquent principal, interest, taxes and insurance typically paid by borrowers, which may not be reimbursed for an extended period of time; |

• | the costs of preserving and liquidating defaulted properties, as a result of increased serious delinquencies and defaults; |

• | the destabilization of the real estate and mortgage markets, which could negatively impact fair value of our assets, reduce our loan production volume, reduce the profitability of servicing mortgages or adversely affect our ability to sell mortgage loans; |

• | difficulty accessing the capital markets on attractive terms, or at all, and a severe disruption and instability in the global financial markets, including the MBS market, or deteriorations in credit and financing conditions which could affect our access to capital necessary to fund business operations or address maturing liabilities on a timely basis; |

• | the inability to promptly foreclose on defaulted mortgage loans and liquidate the underlying real property due to the rapidly changing regulatory and administrative climate, including the suspension of foreclosures and evictions as mandated by governmental bodies; |

• | the potential negative impact on the health of our highly qualified personnel, in particular skilled managers, loan servicers, debt default specialists and underwriters, especially if a significant number of them are impacted; and |

• | a deterioration in our ability to ensure business continuity during a disruption. |

• | restrictive covenants and borrowing conditions in our existing or future financing arrangements that may limit our ability to raise additional debt; |

• | a decline in the liquidity in the credit markets; |

• | prevailing interest rates; |

• | the financial strength of our lenders; |

• | the decisions of lenders from whom we borrow to reduce their exposure to mortgage loans; and |

• | accounting changes that impact the calculations of covenants in our debt agreements. |

• | an increase in the number of similar loans available for sale; |

• | conditions in the loan securitization market or in the secondary market for loans in general or for our loans in particular, which could make our loans less desirable to potential investors; |

• | defaults under loans in general; |

• | loan-level pricing adjustments imposed by Fannie Mae and Freddie Mac, including the recently imposed adjustments for the purchase of loans in forbearance and, although deferred for later implementation, refinancing loans; |

• | the types and volume of loans being originated or sold by us; |

• | the level and volatility of interest rates; and |

• | the quality of loans previously sold by us. |

• | loss of our licenses and approvals to engage in our servicing and lending/loan purchasing businesses; |

• | damage to our reputation in the industry; |

• | governmental investigations and enforcement actions; |

• | administrative fines and penalties and litigation; |

• | civil and criminal liability, including class action lawsuits; |

• | diminished ability to sell loans that we originate or purchase, requirements to sell such loans at a discount compared to other loans or repurchase or address indemnification claims from purchasers of such loans, including the GSEs; |

• | inability to raise capital; and |

• | inability to execute on our business strategy, including our growth plans. |

• | underwriting standards and credit standards for mortgage loans; |

• | our staffing levels and other servicing practices; |

• | the servicing and ancillary fees that we may charge; |

• | our modification standards and procedures; |

• | the amount of reimbursable and non-reimbursable advances that we may make; and |

• | the types of loan products that are eligible for sale or securitization. |

• | a majority of our board of directors consist of “independent directors” as defined under the rules of NASDAQ; |

• | our director nominees be selected, or recommended for our board of directors’ selection by a nominating/governance committee comprised solely of independent directors; and |

• | the compensation of our executive officers be determined, or recommended to our board of directors for determination, by a compensation committee comprised solely of independent directors. |

• | we will not be required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act, |

• | we will be subject to reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and |

• | we will not be required to hold nonbinding advisory votes on executive compensation or stockholder approval of any golden parachute payments not previously approved. |

• | results of operations that vary from the expectations of securities analysts and investors; |

• | results of operations that vary from those of our competitors; |

• | changes in expectations as to our future financial performance, including financial estimates and investment recommendations by securities analysts and investors; |

• | changes in economic conditions for companies in our industry; |

• | changes in market valuations of, or earnings and other announcements by, companies in our industry; |

• | declines in the market prices of stocks generally, particularly those of companies in our industry; |

• | additions or departures of key management personnel; |

• | strategic actions by us or our competitors; |

• | announcements by us, our competitors, our suppliers of significant contracts, price reductions, new products or technologies, acquisitions, dispositions, joint marketing relationships, joint ventures, other strategic relationships or capital commitments; |

• | changes in preference of our customers and our market share; |

• | changes in general economic or market conditions or trends in our industry or the economy as a whole; |

• | changes in business or regulatory conditions; |

• | future sales of our common stock or other securities; |

• | investor perceptions of or the investment opportunity associated with our common stock relative to other investment alternatives; |

• | changes in the way we are perceived in the marketplace, including due to negative publicity or campaigns on social media to boycott certain of our products, our business or our industry; |

• | the public’s response to press releases or other public announcements by us or third parties, including our filings with the SEC; |

• | changes or proposed changes in laws or regulations or differing interpretations or enforcement thereof affecting our business; |

• | announcements relating to litigation or governmental investigations; |

• | guidance, if any, that we provide to the public, any changes in this guidance or our failure to meet this guidance; |

• | the development and sustainability of an active trading market for our common stock; |

• | exchange rate fluctuations; |

• | tax developments; |

• | changes in accounting principles; and |

• | other events or factors, including those resulting from informational technology system failures and disruptions, epidemics, pandemics, natural disasters, war, acts of terrorism, civil unrest or responses to these events. |

• | a classified board of directors, as a result of which our board of directors will be divided into three classes, with each class serving for staggered three-year terms; |

• | the ability of our board of directors to issue one or more series of preferred stock; |

• | advance notice requirements for nominations of directors by stockholders and for stockholders to include matters to be considered at our annual meetings; |

• | certain limitations on convening special stockholder meetings; |

• | the removal of directors only for cause and only upon the affirmative vote of the holders of at least 66 2/3% of the shares of common stock entitled to vote generally in the election of directors if our Sponsor and its affiliates cease to beneficially own at least 40% of shares of common stock entitled to vote generally in the election of directors; and |

• | that certain provisions may be amended only by the affirmative vote of at least 66 2/3% of shares of common stock entitled to vote generally in the election of directors if our Sponsor and its affiliates cease to beneficially own at least 40% of shares of common stock entitled to vote generally in the election of directors. |

• | the spread of the COVID-19 outbreak and severe disruptions in the U.S. and global economy and financial markets it has caused; |

• | our reliance on our financing arrangements to fund mortgage loans and otherwise operate our business; |

• | the dependence of our loan origination and servicing revenues on macroeconomic and U.S. residential real estate market conditions; |

• | the requirement to repurchase mortgage loans or indemnify investors if we breach representations and warranties; |

• | counterparty risk; |

• | the requirement to make servicing advances that can be subject to delays in recovery or may not be recoverable in certain circumstances; |

• | competition for mortgage assets that may limit the availability of desirable originations, acquisitions and result in reduced risk-adjusted returns; |

• | our ability to continue to grow our loan origination business or effectively manage significant increases in our loan production volume; |

• | competition in the industry in which we operate; |

• | our success and growth of our production and servicing activities and the dependence upon our ability to adapt to and implement technological changes; |

• | the effectiveness of our risk management efforts; |

• | our ability to detect misconduct and fraud; |

• | any failure to attract and retain a highly skilled workforce, including our senior executives; |

• | our ability to obtain, maintain, protect and enforce our intellectual property; |

• | any cybersecurity risks, cyber incidents and technology failures; |

• | material changes to the laws, regulations or practices applicable to reverse mortgage programs operated by FHA and HUD; |

• | our vendor relationships; |

• | our failure to deal appropriately with various issues that may give rise to reputational risk, including legal and regulatory requirements; |

• | any employment litigation and related unfavorable publicity; |

• | exposure to new risks and increased costs as a result of initiating new business activities or strategies or significantly expanding existing business activities or strategies; |

• | any failure to comply with the significant amount of regulation applicable to our new investment management subsidiary; |

• | the impact of changes in political or economic stability or by government policies on our material vendors with operations in India; |

• | our ability to fully utilize our NOL and other tax carryforwards; |

• | any challenge by the IRS of the amount, timing and/or use of our NOL carryforwards; |

• | possible changes in legislation and the effect on our ability to use the tax benefits associated with our NOL carryforwards; |

• | the impact of other changes in tax laws; |

• | the impact of interest rate fluctuations; |

• | risks associated with hedging against interest rate exposure; |

• | the impact of any prolonged economic slowdown, recession or declining real estate values; |

• | risks associated with financing our assets with borrowings; |

• | risks associated with a decrease in value of our collateral; |

• | the dependence of our operations on access to our financing arrangements, which are mostly uncommitted; |

• | risks associated with the financial and restrictive covenants included in our financing agreements; |

• | our exposure to volatility in the London Inter-Bank Offered Rate; |

• | our ability to raise the debt or equity capital required to finance our assets and grow our business; |

• | risks associated with higher risk loans that we service; |

• | risks associated with derivative financial instruments; |

• | our ability to foreclose on our mortgage assets in a timely manner or at all; |

• | our ability to obtain and/or maintain licenses and other approvals in those jurisdictions where required to conduct our business; |

• | the impact of revised rules and regulations and enforcement of existing rules and regulations by the CFPB; |

• | legislative and regulatory changes that impact the mortgage loan industry or housing market; |

• | changes in regulations or the occurrence of other events that impact the business, operations or prospects of government agencies such as Ginnie Mae, the FHA or the VA, the USDA, or GSEs such as Fannie Mae or Freddie Mac, or such changes that increase the cost of doing business with such entities; |

• | the Dodd-Frank Act and its implementing regulations and regulatory agencies, and any other legislative and regulatory changes that impact the business, operations or governance of mortgage lenders; |

• | the CFPB, and its issued and future rules and the enforcement thereof; |

• | changes in government support of homeownership; |

• | changes in government or government sponsored home affordability programs; |

• | changes in governmental regulations, accounting treatment, tax rates and similar matters; |

• | risks associated with our acquisition of MSRs; |

• | the impact of our counterparties terminating our servicing rights under which we conduct servicing activities; and |

• | our failure to deal appropriately with issues that may give rise to reputational risk. |

• | on an actual basis; |

• | on a pro forma basis, giving effect to the Debt Transaction; and |

• | on a pro forma as adjusted basis, giving effect to the Debt Transaction, as well as (i) the stock split and the merger of Holdings into the Company described elsewhere in this prospectus and (ii) this offering and the use of proceeds received by us therefrom, assuming an initial public offering price of $ per share of common stock, which is the mid-point of the estimated offering price range set forth on the cover page of this prospectus, and after deducting the underwriting discounts and commissions and estimated offering expenses. |

| | | September 30, 2020 | |||||||

(Unaudited) (In thousands, except shares and per share data) | | | Actual | | | Pro Forma for Debt Transaction | | | Pro Forma As Adjusted for the Debt Transaction and this Offering |

Cash and cash equivalents(1) | | | $271,483 | | | $ (3) | | | $ |

| | | | | | | ||||

Debt | | | | | | | |||

Warehouse lines of credit | | | $2,092,477 | | | $ | | | $ |

Operating line of credit | | | 1,000 | | | | | ||

Advance facilities | | | 18,250 | | | | | ||

Term debt, net(2) | | | 354,840 | | | | | ||

Senior Unsecured Notes | | | — | | | | | ||

Total debt | | | $2,466,567 | | | $ | | | |

| | | | | | | ||||

Stockholder’s equity | | | | | | | |||

Common stock, par value $0.01 per share (100 shares authorized, issued and outstanding, actual and pro forma; and shares authorized, shares issued and outstanding, pro forma as adjusted) | | | $— | | | $ | | | $ |

Additional paid in capital | | | 519,177 | | | | | ||

Retained earnings | | | 223,565 | | | | | ||

Total stockholder’s equity | | | 742,742 | | | $ | | | $ |

| | | | | | | ||||

Total capitalization | | | $3,209,309 | | | $ | | | $ |

(1) | Does not include Restricted cash. Also excludes the impact of the cash dividend declared by our board of directors on September 30, 2020 in the amount of $154.5 million, which was paid to Holdings, the sole stockholder, on October 5, 2020. See “Prospectus Summary—Recent Developments—Payment of Cash Dividend.” |

(2) | Net of issuance costs. |

(3) | A $1.00 increase (decrease) in the assumed initial public offering price of $ per share would increase (decrease) the amount of net proceeds to us from this offering by $ , assuming the number of shares of common stock offered by us, as set forth on the cover page of this prospectus, remains the same, and after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

Assumed initial public offering price per share of common stock | | | $ |

Pro forma net tangible book value (deficit) per share of common stock as of September 30, 2020 before this offering | | | |

Increase in pro forma net tangible book value per share of common stock attributable to investors in this offering | | | |

Pro forma net tangible book value (deficit) per share of common stock after this offering | | | |

Dilution per share of common stock to investors in this offering | | | $ |

| | | Shares Purchased | | | Total Consideration | | | Average Price Per Share | |||||||

Name of Beneficial Owners | | | Number | | | Percent | | | Amount | | | Percent | | ||

Existing owners | | | | | | | | | | | |||||

New investors in this offering | | | | | | | | | | | |||||

Total | | | | | | | | | | | |||||

• | the issuance in January 2021 of $ aggregate principal amount of Senior Unsecured Notes; |

• | the use of approximately $ of the net proceeds from the issuance of the Senior Unsecured Notes to repay outstanding amounts under our MSR Facility; |

• | the use of approximately $ of the net proceeds from the issuance of the Senior Unsecured Notes to fund a distribution to our existing shareholders; and |

• | this offering and the application of the estimated net proceeds from this offering received by us as described under “Use of Proceeds”. |

| | | As Reported | | | Pro Forma Adjustments Related to Debt Transaction | | | Footnotes | | | Pro Forma for Debt Transaction | | | Pro Forma Adjustments Related to This Offering | | | Footnotes | | | Pro Forma As Adjusted | |

Assets: | | | | | | | | | | | | | | | |||||||

Cash and cash equivalents | | | $271,483 | | | | | (A) | | | | | | | (F) | | | ||||

Restricted cash | | | 41,907 | | | | | | | | | | | | | ||||||

Cash and cash equivalents and restricted cash | | | 313,390 | | | | | | | | | | | | | ||||||

Mortgage loans held for sale (at fair value) | | | 2,281,835 | | | | | | | | | | | | | ||||||

Mortgage servicing rights (at fair value) | | | 583,263 | | | | | | | | | | | | | ||||||

Property and equipment, net | | | 18,595 | | | | | | | | | | | | | ||||||

Accounts receivable, net | | | 79,320 | | | | | | | | | | | | | ||||||

Derivative assets | | | 314,794 | | | | | | | | | | | | | ||||||

Goodwill and intangibles | | | 11,083 | | | | | | | | | | | | | ||||||

GNMA loans eligible for repurchase | | | 2,919,881 | | | | | | | | | | | | | ||||||

Other assets | | | 65,745 | | | | | | | | | | | (G) | | | |||||

Total assets | | | $6,587,906 | | | | | | | | | | | | | ||||||

| | | | | | | | | | | | | | | ||||||||

Liabilities and Shareholders’ Equity: | | | | | | | | | | | | | | | |||||||

Liabilities: | | | | | | | | | | | | | | | |||||||

Warehouse lines of credit | | | $2,092,477 | | | | | | | | | | | | | ||||||

Term debt and other borrowings, net | | | 374,090 | | | | | (C) | | | | | | | | | |||||

Accounts payable and accrued expenses | | | 269,017 | | | | | (B) | | | | | | | (H) | | | ||||

GNMA loans eligible for repurchase | | | 2,919,881 | | | | | | | | | | | | | ||||||

Other liabilities | | | 189,700 | | | | | | | | | | | | | ||||||

Total liabilities | | | $5,845,165 | | | | | | | | | | | | | ||||||

| | | | | | | | | | | | | | | ||||||||

Shareholders’ Equity: | | | | | | | | | | | | | | | |||||||

Common stock (100 shares issued and outstanding, par value $0.01 per share) | | | — | | | | | | | | | | | (F) | | | |||||

Additional paid-in capital | | | 519,177 | | | | | (E) | | | | | | | (I) | | | ||||

Retained earnings (accumulated deficit) | | | 223,565 | | | | | (D) | | | | | | | (H) | | | ||||

Total shareholders' equity | | | 742,742 | | | | | | | | | | | | | ||||||

Total liabilities and shareholders' equity | | | $6,587,906 | | | | | | | | | | | | |

| | | As Reported | | | Pro Forma Adjustments Related to Debt Transaction | | | Footnotes | | | Pro Forma for Debt Transaction | | | Pro Forma Adjustments Related to This Offering | | | Footnotes | | | Pro Forma As Adjusted | |

Revenue: | | | | | | | | | | | | | | | |||||||

Gain on loans, net | | | $962,778 | | | | | | | | | | | | | ||||||

Loan fee income | | | 60,630 | | | | | | | | | | | | | ||||||

Interest income | | | 42,370 | | | | | | | | | | | | | ||||||

Interest expense | | | (47,845) | | | | | (A) | | | | | | | | | |||||

Interest loss, net | | | (5,476) | | | | | | | | | | | | | ||||||

Loan servicing fees | | | 133,904 | | | | | | | | | | | | | ||||||

Change in fair value of mortgage servicing rights | | | (230,524) | | | | | | | | | | | | | ||||||

Other income | | | 1,022 | | | | | | | | | | | | | ||||||

Total net revenue | | | 922,335 | | | | | | | | | | | | | ||||||

| | | | | | | | | | | | | | | ||||||||

Expenses: | | | | | | | | | | | | | | | |||||||

Compensation and benefits | | | 251,462 | | | | | | | | | | | | | ||||||

Loan expense | | | 28,581 | | | | | | | | | | | | | ||||||

Loan servicing expense | | | 22,742 | | | | | | | | | | | | | ||||||

Occupancy and equipment | | | 17,006 | | | | | | | | | | | | | ||||||

General and administrative | | | 28,373 | | | | | | | | | | | | | ||||||

Depreciation and amortization | | | 4,222 | | | | | | | | | | | | | ||||||

Other expenses | | | 12,087 | | | | | | | | | | | | | ||||||

Total expenses | | | 364,473 | | | | | | | | | | | | | ||||||

| | | | | | | | | | | | | | | ||||||||

Income (loss) before income tax | | | 557,862 | | | | | | | | | | | | | ||||||

Income tax expense (benefit) | | | 149,306 | | | | | (B) | | | | | | | | | |||||

Income from equity method investment | | | 14,050 | | | | | | | | | | | | | ||||||

| | | | | | | | | | | | | | | ||||||||

Total net income (loss) | | | $422,606 | | | | | | | | | | | | | ||||||

| | | | | | | | | | | | | | | ||||||||

Earnings Per Share: | | | | | | | | | | | | | | | |||||||

Basic and diluted earnings per share | | | | | | | | | | | | | (C) | | | — |

| | | As Reported | | | Pro Forma Adjustments Related to Debt Transaction | | | Footnotes | | | Pro Forma for Debt Transaction | | | Pro Forma Adjustments Related to This Offering | | | Footnotes | | | Pro Forma As Adjusted | |

Revenue: | | | | | | | | | | | | | | | |||||||

Gain on loans, net | | | $199,501 | | | | | | | | | | | | | ||||||

Loan fee income | | | 32,112 | | | | | | | | | | | | | ||||||

Interest income | | | 51,801 | | | | | | | | | | | | | ||||||

Interest expense | | | (57,942) | | | | | (A) | | | | | | | | | |||||

Interest loss, net | | | (6,141) | | | | | | | | | | | | | ||||||

Loan servicing fees | | | 144,228 | | | | | | | | | | | | | ||||||

Change in fair value of mortgage servicing rights | | | (173,134) | | | | | | | | | | | | | ||||||

Other income | | | 3,159 | | | | | | | | | | | | | ||||||

Total net revenue | | | 199,725 | | | | | | | | | | | | | ||||||

| | | | | | | | | | | | | | | ||||||||

Expenses: | | | | | | | | | | | | | | | |||||||

Compensation and benefits | | | 156,197 | | | | | | | | | | | | | ||||||

Loan expense | | | 15,626 | | | | | | | | | | | | | ||||||

Loan servicing expense | | | 20,924 | | | | | | | | | | | | | ||||||

Occupancy and equipment | | | 16,768 | | | | | | | | | | | | | ||||||

General and administrative | | | 21,407 | | | | | | | | | | | | | ||||||

Depreciation and amortization | | | 5,918 | | | | | | | | | | | | | ||||||

Other expenses | | | 4,296 | | | | | | | | | | | | | ||||||

Total expenses | | | 241,136 | | | | | | | | | | | | | ||||||

| | | | | | | | | | | | | | | ||||||||

Income (loss) before income tax | | | (41,411) | | | | | | | | | | | | | ||||||

Income tax expense (benefit) | | | (9,500) | | | | | (B) | | | | | | | | | |||||

Income from equity method investment | | | 2,701 | | | | | | | | | | | | | ||||||

| | | | | | | | | | | | | | | ||||||||

Total net income (loss) | | | $(29,210) | | | | | | | | | | | | | ||||||

| | | | | | | | | | | | | | | ||||||||

Earnings Per Share: | | | | | | | | | | | | | | | |||||||

Basic and diluted earnings per share | | | | | | | | | | | | | (C) | | | — |

(A) | Represents the net adjustment to Cash and cash equivalents to reflect (i) the net cash proceeds of $ million received from the issuance of the Senior Unsecured Notes and the payment of $ million to repay a portion of the MSR Facility as discussed in note (C), (ii) $ million distributed to our existing shareholder, (iii) $ million used to pay debt issuance costs related to the issuance of the Senior Unsecured Notes; and (iv) $ million used to pay accrued interest related to the MSR Facility as discussed in note (B). |

(B) | Represents the adjustment to Accounts payable and accrued expenses to reflect the payment of $ million of accrued interest associated with the repayment of a portion of the MSR Facility. |

(C) | Represents the issuance of $ million aggregate principal amount of Senior Unsecured Notes, a portion of the net proceeds of which was used to pay down $ million of the MSR Facility. As a result, Term debt and other borrowings, net decreased by $ million. |

Issuance of the Senior Unsecured Notes | | | $ |

Debt issuance costs of Senior Unsecured Notes | | | |

Repayment of portion of the MSR Facility | | | |

Net adjustment to Term debt and other borrowings, net | | | $ |

(D) | Represents the adjustment to reduce retained earnings to zero to reflect the $ million of the total $ million distribution paid to our existing shareholder from the net proceeds of the Senior Unsecured Notes. The remainder of the distribution, $ million, has been reflected as a decrease to Additional paid-in capital as discussed in note (E). |

(E) | Represents the adjustment to reduce Additional paid-in capital in excess of Retained earnings balance by $ million as a result of the distribution paid to our existing shareholder from the net proceeds of the Senior Unsecured Notes. |

(F) | Represents the estimated net proceeds received by us in the offering, approximately $ million based on an assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, after deducting $ of assumed underwriting discounts and commissions. We intend to use the net proceeds received by us from this offering for general corporate purposes. We will not receive any proceeds from the sale of shares by the selling stockholders. Of the total proceeds received by us of $ million, $ million will be reflected as an increase to our Common stock with the remaining $ increasing Additional paid-in capital. See “Use of Proceeds” for further information. |

Gross proceeds from the offering | | | $ | | | |

Underwriting discounts and commissions | | | | | ||

Change in pro forma cash from the offering | | | $ | | |

(G) | Represents an adjustment in Other assets to reflect certain deferred costs related to the offering which are primarily related to legal, accounting and other direct costs. Upon completion of this offering, these deferred costs will be charged against the proceeds from this offering with a corresponding reduction to Additional paid-in capital as discussed in note (I). As of September 30, 2020, on an actual basis, $ million of deferred offering costs were recorded in Other assets. |

(H) | Subsequent to September 30, 2020, an additional $ million of capitalizable costs were incurred which were recorded in Accounts payable and accrued expenses with a corresponding reduction to Additional paid-in capital as discussed in note (I). After September 30, 2020, the Company incurred an additional $ million of costs associated with this offering that were not eligible for capitalization. These costs were expensed as incurred and were recorded to Accounts payable and accrued expenses and Retained earnings. |

(I) | The following table is a reconciliation of the adjustments impacting Additional paid-in-capital after giving effect to the Pro Forma Transactions (in thousands): |

Net proceeds from offering of common stock | | | $ | | | (F) |

Reclassification of deferred costs incurred in this offering to Additional paid-in capital | | | | | (G), (H) | |

Net Additional paid-in capital pro forma adjustment | | | $ | | |

(A) | Represents the net adjustment to Interest expense associated with the payment of a portion of the MSR Facility and the issuance of the Senior Unsecured Notes (in thousands): |

| | | Nine months ended September 30, 2020 | | | Year ended December 31, 2019 | |

Interest expense — Senior Unsecured Notes | | | | | ||

Interest expense — MSR Facility | | | | | ||

Net adjustments to Interest expense | | | | |

(B) | Represents a reduction of $ million and $ million in Income tax expense for the nine months ended September 30, 2020 and for the year ended December 31, 2019, respectively. The adjustment was based on the statutory tax rate of %. The adjustment is the result of the net increase in pro forma Interest expense arising from the issuance of the Senior Unsecured Notes partially offset by the repayment of a portion of the MSR Facility. |

(C) | Pro forma Basic and diluted earnings per share has been calculated based on the number of shares assumed to be outstanding, assuming such shares were outstanding for the full periods presented and reflects shares of common stock outstanding. The following table sets forth the computation of unaudited pro forma Basic and diluted earnings per share (in thousands, except for share and per share data): |

| | | Nine months ended September 30, 2020 | | | Year ended December 31, 2019 | |

Numerator | | | | | ||

Pro forma net income (basic and diluted) | | | | | ||

Denominator | | | | | ||

Weighted average of common stock outstanding | | | | | ||

Assumed shares sold in this offering sufficient to pay dividends in excess of current year earnings | | | | | ||

Assumed shares sold in this offering sufficient to partially repay debt | | | | | ||

Weighted average shares of common stock outstanding (basic and dilutive) | | | | | ||

Pro forma net income per share (basic and dilutive) | | | | |

| | | Nine Months Ended September 30, | | | Year Ended December 31, | |||||||

(In thousands, except shares and per share amounts) | | | 2020 | | | 2019 | | | 2019 | | | 2018 |

| | | (unaudited) | | | (audited) | |||||||

Statement of Operations Data | | | | | | | | | ||||

Gain on loans, net | | | $962,778 | | | $135,495 | | | $199,501 | | | $84,068 |

Loan fee income | | | 60,630 | | | 19,829 | | | 32,112 | | | 19,603 |

Interest income | | | 42,370 | | | 35,101 | | | 51,801 | | | 35,179 |

Interest expense | | | (47,845) | | | (41,933) | | | (57,942) | | | (47,486) |

Interest loss, net | | | (5,475) | | | (6,832) | | | (6,141) | | | (12,307) |

Loan servicing fees | | | 133,904 | | | 104,089 | | | 144,228 | | | 119,049 |

Change in fair value of mortgage servicing rights | | | (230,524) | | | (151,168) | | | (173,134) | | | (47,312) |

Other income | | | 1,022 | | | 1,591 | | | 3,159 | | | 1,156 |

Total net revenue | | | 922,335 | | | 103,004 | | | 199,725 | | | 164,257 |

| | | | | | | | | |||||

Compensation and benefits | | | 251,462 | | | 104,571 | | | 156,197 | | | 109,577 |

Loan expense | | | 28,581 | | | 10,182 | | | 15,626 | | | 16,882 |

Loan servicing expense | | | 22,742 | | | 15,781 | | | 20,924 | | | 18,488 |

Occupancy and equipment | | | 17,006 | | | 12,567 | | | 16,768 | | | 20,521 |

General and administrative | | | 28,373 | | | 14,687 | | | 21,407 | | | 29,165 |

Depreciation and amortization | | | 4,222 | | | 4,394 | | | 5,918 | | | 7,612 |

Other expenses | | | 12,087 | | | 2,770 | | | 4,296 | | | 4,060 |

Total expenses | | | 364,473 | | | 164,952 | | | 241,136 | | | 206,305 |

| | | | | | | | | |||||

Income (loss) from continuing operations before income tax | | | 557,862 | | | (61,948) | | | (41,411) | | | (42,048) |

Income tax expense (benefit) from continuing operations | | | 149,306 | | | (14,080) | | | (9,500) | | | (10,485) |

Net income (loss) from continuing operations | | | 408,556 | | | (47,868) | | | (31,911) | | | (31,563) |

Net income from discontinued operations before tax | | | — | | | — | | | — | | | 9,707 |

Income tax provision | | | — | | | — | | | — | | | 2,550 |

Income from discontinued operations, net of tax | | | — | | | — | | | — | | | 7,157 |

Income from equity method investment | | | 14,050 | | | 2,591 | | | 2,701 | | | 209 |

Total net income (loss) | | | $422,606 | | | $(45,277) | | | $(29,210) | | | $(24,197) |

| | | Nine Months Ended September 30, | | | Year Ended December 31, | |||||||

(In thousands, except shares and per share amounts) | | | 2020 | | | 2019 | | | 2019 | | | 2018 |

| | | (unaudited) | | | (audited) | |||||||

Basic and diluted loss earnings per share: | | | | | | | | | ||||

Basic and diluted income (loss) per share from continuing operations | | | $4,226 | | | $(453) | | | $(319) | | | $(316) |

Basic and diluted earnings per share from discontinued operations | | | — | | | — | | | — | | | 72 |

Basic and diluted total net income (loss) per share | | | $4,226 | | | $(453) | | | $(292) | | | $(242) |

Weighted average shares of common stock outstanding | | | | | | | | | ||||

Basic and diluted | | | 100 | | | 100 | | | 100 | | | 100 |

| | | September 30, | | | December 31, | ||||

(In thousands, except shares and per share amounts) | | | 2020 | | | 2019 | | | 2018 |

| | | (unaudited) | | | (audited) | ||||

Balance Sheet Data | | | | | | | |||

Assets: | | | | | | | |||

Cash and cash equivalents | | | $271,483 | | | $30,630 | | | $44,010 |

Restricted cash | | | 41,907 | | | 51,101 | | | 38,234 |

Cash and cash equivalents and restricted cash | | | 313,390 | | | 81,731 | | | 82,244 |

Mortgage loans held for sale (at fair value) | | | 2,281,835 | | | 1,554,230 | | | 421,754 |

Mortgage servicing rights (at fair value) | | | 583,263 | | | 575,035 | | | 532,526 |

Property and equipment, net | | | 18,595 | | | 12,051 | | | 10,075 |

Accounts receivable, net | | | 79,320 | | | 57,872 | | | 44,422 |

Derivative assets | | | 314,794 | | | 40,544 | | | 18,990 |

Goodwill and intangibles | | | 11,083 | | | 11,935 | | | 10,957 |

GNMA loans eligible for repurchase | | | 2,919,881 | | | 499,207 | | | 451,209 |

Other assets | | | 65,745 | | | 76,162 | | | 64,214 |

Total assets | | | $6,587,906 | | | $2,908,767 | | | $1,636,391 |

| | | | | | | ||||

Liabilities and Shareholder’s equity: | | | | | | | |||

Liabilities: | | | | | | | |||

Warehouse lines of credit | | | $2,092,477 | | | $1,478,183 | | | $404,237 |

Term debt and other borrowings, net | | | 374,090 | | | 424,958 | | | 276,277 |

Accounts payable and accrued expenses | | | 269,016 | | | 39,739 | | | 21,243 |

GNMA loans eligible for repurchase | | | 2,919,881 | | | 499,207 | | | 451,209 |

Other liabilities | | | 189,700 | | | 56,368 | | | 44,654 |

Total liabilities | | | $5,845,164 | | | 2,498,455 | | | 1,197,620 |

| | | | | | | ||||

Shareholder’s equity: | | | | | | | |||

Common stock (100 shares issued and outstanding, par value $0.01 per share) | | | — | | | — | | | — |

Additional paid-in-capital | | | 519,177 | | | 454,861 | | | 454,110 |

Accumulated deficit | | | 223,565 | | | (44,549) | | | (15,339) |

Total shareholder’s equity | | | 742,742 | | | 410,312 | | | 438,771 |

Total liabilities and shareholder’s equity | | | $6,587,906 | | | $2,908,767 | | | $1,636,391 |

| | | Nine Months Ended September 30, | | | Year Ended December 31 | |||||||

($ in thousands) | | | 2020 | | | 2019 | | | 2019 | | | 2018(a) |

Origination Volume by Channel | | | | | | | | | ||||

Wholesale(b) | | | $23,772,112 | | | $7,023,411 | | | $11,564,971 | | | $4,889,220 |

Correspondent(b) | | | 12,696,815 | | | 6,676,458 | | | 10,215,300 | | | 5,081,719 |

Direct(b) | | | 1,576,959 | | | 291,302 | | | 487,322 | | | 608,148 |

Origination volume(b) | | | $38,045,886 | | | $13,991,171 | | | $22,267,593 | | | $10,579,087 |

| | | | | | | | | |||||

Gain on sale margin | | | | | | | | | ||||

Gain on sale margin (bps)(c) | | | 253.1 | | | 96.8 | | | 89.6 | | | 79.5 |

| | | | | | | | | |||||

Market Share | | | | | | | | | ||||

Overall share of origination market(d) | | | 1.4% | | | 0.9% | | | 1.0% | | | 0.7% |

Share of wholesale channel(e) | | | 6.4% | | | 3.0% | | | 3.5% | | | 2.6% |

| | | | | | | | | |||||

Origination Volume by Purpose(f) | | | | | | | | | ||||

Purchase | | | 31.7% | | | 54.4% | | | 50.6% | | | 66.5% |

Refinance | | | 68.3% | | | 45.6% | | | 49.4% | | | 33.5% |

| | | | | | | | | |||||

| | | Nine Months Ended September 30, | | | Year Ended December 31 | |||||||

($ in thousands) | | | 2020 | | | 2019 | | | 2019 | | | 2018(a) |

Third Party Partners | | | | | | | | | ||||

Number of Broker Partners(g) | | | 4,921 | | | 2,684 | | | 3,085 | | | 1,623 |

Number of Correspondent Partners(h) | | | 594 | | | 516 | | | 537 | | | 451 |

| | | Nine Months Ended September 30, | | | Year Ended December 31 | |||||||

($ in thousands) | | | 2020 | | | 2019(a) | | | 2019 | | | 2018(a) |

Mortgage Servicing | | | | | | | | | ||||

MSR Servicing Portfolio - UPB(i) | | | $73,951,042 | | | $47,887,643 | | | $52,600,546 | | | $41,423,825 |

MSR Servicing Portfolio - Units(j) | | | 307,236 | | | 217,558 | | | 236,362 | | | 189,513 |

| | | | | | | | | |||||

60 days or more delinquent(k) | | | 6.6% | | | 2.0% | | | 1.7% | | | 2.3% |

| | | | | | | | | |||||

MSR Portfolio | | | | | | | | | ||||

MSR multiple(l) | | | 2.6x | | | 3.2x | | | 3.4x | | | 4.3x |

(a) | Unless otherwise indicated, our Distributed Retail channel was included in discontinued operations in our results of operations for the year ended December 31, 2018 and as such it has been excluded from our key performance indicators for the year ended December 31, 2018. |

(b) | Origination dollar value of new loans funded by channel. Origination volume excludes Origination volume from the Distributed Retail channel, which was included in discontinued operations in our results of operations for the year ended December 31, 2018. |

(c) | Calculated as Gain on sale, net divided by Origination volume. |

(d) | Calculated as the Company’s originations dollar value for the year divided by the total residential originations in the United States of America per Inside Mortgage Finance, a third party provider of residential mortgage industry news and statistics each year. Origination volume figures used to calculate market share include $1 billion of Distributed Retail originations in our results of operations for the year ended December 31, 2018. |

(e) | Calculated as the Company’s originations dollar value for the year divided by the total wholesale originations in the United States of America per Inside Mortgage Finance, each year. |

(f) | Origination volume excludes Origination volume from the Distributed Retail channel, which was included in discontinued operations in our results of operations for the year ended December 31, 2018. |

(g) | Number of Broker Partners with whom the Company sources loans from. |

(h) | Number of Correspondent Partners from whom the Company purchases loans. |

(i) | The unpaid principal balance of loans we service on behalf of Ginnie Mae, Fannie Mae, Freddie Mae and others, at period end. |

(j) | Number of loans in our serving portfolio at period end. |

(k) | Total balances of outstanding loan principals for which installment payments are at least 60 days past due as a percentage of the outstanding loan principal as of a specified date. |

(l) | Calculated as the MSR fair market value as of a specified date divided by the related UPB divided by the weighted average service fee. |

| | | Nine Months Ended September 30, | | | Year Ended December 31, | |||||||

($ in thousands) | | | 2020 | | | 2019 | | | 2019 | | | 2018 |

Total net revenue | | | $922,335 | | | $103,004 | | | $199,725 | | | $164,257 |

Income from equity method investment | | | 14,050 | | | 2,591 | | | 2,701 | | | 209 |

Change in fair value of MSR (due to inputs and assumptions), net of hedge(a) | | | 98,302 | | | 84,927 | | | 74,481 | | | (10,348) |

Adjusted revenue | | | $1,034,687 | | | $190,522 | | | $276,907 | | | $154,118 |

| | | Nine Months Ended September 30, | | | Year Ended December 31, | |||||||

($ in thousands) | | | 2020 | | | 2019 | | | 2019 | | | 2018 |

Total net income (loss) | | | $422,606 | | | $(45,277) | | | $(29,210) | | | $(24,197) |

Change in fair value of MSR (due to inputs and assumptions), net of hedge(a) | | | 98,302 | | | 84,927 | | | 74,481 | | | (10,348) |

Income tax effect of change in fair value of MSR (due to inputs and assumptions), net of hedge(b) | | | (26,310) | | | (19,303) | | | (17,086) | | | 2,539 |

Adjusted net income (loss) | | | $494,598 | | | $20,347 | | | $28,185 | | | $(32,006) |

| | | Nine Months Ended September 30, | | | Year Ended December 31, | |||||||

($ in thousands) | | | 2020 | | | 2019 | | | 2019 | | | 2018 |

Total net income (loss) | | | $422,606 | | | $(45,277) | | | $(29,210) | | | $(24,197) |

Income from discontinued operations, net of tax | | | — | | | — | | | — | | | (7,157) |

Interest expense on corporate debt | | | 14,411 | | | 22,324 | | | 27,721 | | | 24,962 |

Income tax expense (benefit) from continuing operations | | | 149,306 | | | (14,080) | | | (9,500) | | | (10,485) |

Depreciation and amortization | | | 4,222 | | | 4,394 | | | 5,918 | | | 7,612 |

Change in fair value of MSR (due to inputs and assumptions), net of hedge(a) | | | 98,302 | | | 84,927 | | | 74,481 | | | (10,348) |

Adjusted EBITDA | | | $688,847 | | | $52,288 | | | $69,410 | | | $(19,613) |

(a) | MSR fair value changes due to valuation inputs and assumptions are measured using a stochastic discounted cash flow model that includes assumptions such as prepayment speeds, delinquencies, discount rates, and effects of changes in market interest rates. Refer to “Note 2, Basis of Presentation and Significant Accounting Policies” and “Note 5, Mortgage Servicing Rights” to our unaudited condensed consolidated financial statements included elsewhere in this prospectus and to “Note 2, Basis of Presentation and Significant Accounting Policies” and “Note 7, Mortgage Servicing Rights” to our audited consolidated financial statements included elsewhere in this prospectus. The change in the value of the MSR hedge is measured based on third party market values and cash settlement. Refer to “Note 14, Fair Value Measurements”, to our unaudited condensed consolidated financial statements included elsewhere in this prospectus and “Note 18, Fair Value Measurements” to our audited consolidated financial statements included elsewhere in this prospectus. We exclude changes in fair value of MSRs, net of hedge from Adjusted revenue as they add volatility and we believe that they are not indicative of the Company’s operating performance or results of operations. This adjustment does not include changes in fair value of MSRs due to realization of cash flows, which remain in Adjusted EBITDA. Realization of cash flows occurs when cash is collected as customers make scheduled payments, partial prepayments of principal, or pay their mortgage in full. |

(b) | The income tax effect of change in fair value of MSR (due to inputs and assumptions), net of hedge is calculated as the MSR valuation change, net of hedge multiplied by the quotient of Income tax expense (benefit) divided by Income (loss) before income tax. |

| | | Nine Months Ended September 30, | | | | | ||||||

($ in thousands) | | | 2020 | | | 2019 | | | $ Change | | | % Change |

Gain on loans, net | | | 962,778 | | | 135,495 | | | 827,283 | | | 610.6% |

Loan fee income | | | 60,630 | | | 19,829 | | | 40,801 | | | 205.8% |

Interest income | | | 42,370 | | | 35,101 | | | 7,269 | | | 20.7% |

Interest expense | | | (47,845) | | | (41,933) | | | (5,912) | | | 14.1% |

Interest loss, net | | | (5,475) | | | (6,832) | | | 1,357 | | | 19.9% |

Loan servicing fees | | | 133,904 | | | 104,089 | | | 29,815 | | | 28.6% |

Change in fair value of mortgage servicing rights | | | (230,524) | | | (151,168) | | | (79,356) | | | 52.5% |

Other income | | | 1,022 | | | 1,591 | | | (569) | | | (35.8)% |

Total net revenue | | | 922,335 | | | 103,004 | | | 819,331 | | | 795.4% |

| | | | | | | | | |||||

Compensation and benefits | | | 251,462 | | | 104,571 | | | 146,891 | | | 140.5% |

Loan expense | | | 28,581 | | | 10,182 | | | 18,399 | | | 180.7% |

Loan servicing expense | | | 22,742 | | | 15,781 | | | 6,961 | | | 44.1% |

Occupancy and equipment | | | 17,006 | | | 12,567 | | | 4,439 | | | 35.3% |

General and administrative | | | 28,373 | | | 14,687 | | | 13,686 | | | 93.2% |

Depreciation and amortization | | | 4,222 | | | 4,394 | | | (172) | | | (3.9)% |

Other expenses | | | 12,087 | | | 2,770 | | | 9,317 | | | 336.4% |

Total expenses | | | 364,473 | | | 164,952 | | | 199,521 | | | 121.0% |

| | | | | | | | | |||||

Income (loss) before income tax | | | 557,862 | | | (61,948) | | | 619,810 | | | 1,000.5% |

Income tax expense (benefit) | | | 149,306 | | | (14,080) | | | 163,386 | | | 1,160.4% |

Income from equity method investment | | | 14,050 | | | 2,591 | | | 11,459 | | | 442.3% |

Total net income (loss) | | | 422,606 | | | (45,277) | | | 467,883 | | | 1,033.4% |

| | | Nine Months Ended September 30, | ||||

($ in thousands) | | | 2020 | | | 2019 |

Gain on sales, net(a) | | | $657,355 | | | $(37,127) |

Origination of mortgage service rights | | | 352,118 | | | 175,756 |

Change in fair value of loans held for sale, IRLCs, and related hedges | | | 301,173 | | | 55,599 |

Realized and unrealized gain (loss) from derivative financial instruments | | | (330,851) | | | (56,569) |

Provision for losses relating to representations and warranties | | | (17,017) | | | (2,164) |

Gain on loans, net | | | $962,778 | | | $135,495 |

(a) | The Gain on sales, net includes income related to originations of mortgage servicing rights. |

Nine Months Ended September 30, | | |||||

(in thousands) | | | 2020 | | | 2019 |

Origination volume | | | 38,045,886 | | | 13,991,171 |

Originated MSR - UPB | | | 37,066,235 | | | 12,678,916 |

Gain on sale margin(a) | | | 253.1 | | | 96.8 |

Retained servicing (UPB)(b) | | | 99.2% | | | 96.2 % |

(a) | Gain on sale margin represents the margin on loans sold, including the realized and unrealized gains and losses on sales of mortgage loans, as well as the changes in fair value of all loan-related derivatives, including interest rate lock commitments, freestanding loan-related derivatives, and representation and warranty reserve, and is calculated as the ratio of Gain on loans, net to the Sales volume UPB. |

(b) | Represents the percentage of our loan sales UPBs for which we retained the underlying servicing UPB during the period. |

| | | Nine Months Ended September 30, | ||||

($ in thousands) | | | 2020 | | | 2019 |

Retained servicing fees, net of guarantees | | | $135,813 | | | $101,138 |

Late fees and other | | | (1,909) | | | 2,951 |

Loan servicing fees | | | $133,904 | | | $104,089 |

| | | Nine Months Ended September 30, | ||||

($ in thousands) | | | 2020 | | | 2019 |

MSR Servicing Portfolio - UPB | | | $73,951,042 | | | $47,887,643 |

Average MSR Servicing Portfolio - UPB | | | $63,275,795 | | | $44,655,734 |

MSR Servicing Portfolio – units | | | 307,236 | | | 217,558 |

MSRs Fair Value Multiple (x) | | | 2.57x | | | 3.15x |

Delinquency Rates (%) | | | 12.6% | | | 2.2% |

Weighted average credit score | | | 734 | | | 721 |

Weighted average servicing fee, net (bps) | | | 0.3 | | | 0.3 |

| | | Nine Months Ended September 30, | ||||

($ in thousands) | | | 2020 | | | 2019 |

Realization of cash flows | | | $(132,222) | | | $(66,241) |

Valuation inputs and assumptions | | | (211,667) | | | (163,025) |

Hedge | | | 113,365 | | | 78,098 |

Change in fair value of MSRs | | | (230,524) | | | (151,168) |

| | | Nine Months Ended September 30, | ||||

($ in thousands) | | | 2020 | | | 2019 |

Interest income | | | 42,370 | | | 35,101 |

Interest expense | | | (47,845) | | | (41,933) |

Interest loss, net | | | (5,475) | | | (6,832) |

• | Our Origination segment consists of a combination of retail and third-party loan production operations. The increase in revenues for the Origination segment was primarily driven by an increase in loan Origination volume. |

• | Our Servicing segment consists of servicing loans the Company had initially originated and subsequently sold, for which the Company retained servicing rights as well as MSRs the Company occasionally purchases from others. The decrease in revenues for the Servicing segment was primarily driven by a decrease in interest rates. |

| | | Nine Months Ended September 30, | ||||

($ in thousands) | | | 2020 | | | 2019 |

Gain on loans, net | | | 962,778 | | | 135,853 |

Loan fee income | | | 60,630 | | | 19,788 |

Loan servings fees | | | (1,982) | | | (459) |

Interest income | | | 1,804 | | | 2,237 |

Change in FV of MSRs | | | — | | | — |

Other income | | | — | | | — |

Total Origination segment revenue | | | 1,023,230 | | | 157,419 |

Directly attributable expense | | | 231,315 | | | 97,041 |

Contribution margin | | | 791,915 | | | 60,378 |

| | | Nine Months Ended September 30, | ||||

($ in thousands) | | | 2020 | | | 2019 |

Gain on loans, net | | | $— | | | $(358) |

Loan servicing fees | | | 135,886 | | | 104,548 |

Change in fair value of mortgage servicing rights | | | (230,524) | | | (151,168) |

Interest income | | | 7,130 | | | 13,255 |

Other income | | | 205 | | | 4 |

Total Servicing segment revenue | | | (87,303) | | | (33,719) |

Change in mortgage servicing rights due to valuation, net of hedge | | | (98,302) | | | (84,927) |

Directly attributable expense | | | 42,664 | | | 29,754 |

Contribution margin | | | $(31,665) | | | $21,454 |

| | | Year Ended December 31, | | | | | ||||||

($ in thousands) | | | 2019 | | | 2018 | | | $ Change | | | % Change |

Gain on loans, net | | | $199,501 | | | $84,068 | | | $115,433 | | | 137.3% |

Loan fee income | | | 32,112 | | | 19,603 | | | 12,509 | | | 64.0% |

Interest income | | | 51,801 | | | 35,179 | | | 16,622 | | | 47.2% |

Interest expense | | | (57,942) | | | (47,486) | | | (10,456) | | | 22.0% |

Interest loss, net | | | (6,141) | | | (12,307) | | | 6,166 | | | -50.1% |

Loan servicing fees | | | 144,228 | | | 119,049 | | | 25,179 | | | 21.2% |

Change in fair value of mortgage servicing rights | | | (173,134) | | | (47,312) | | | (125,822) | | | 265.9% |

Other income | | | 3,159 | | | 1,156 | | | 2,003 | | | 173.3% |

Total net revenue | | | 199,725 | | | 164,257 | | | 35,468 | | | 21.6% |

| | | | | | | | | |||||

Compensation and benefits | | | 156,197 | | | 109,577 | | | 46,620 | | | 42.5% |

Loan expense | | | 15,626 | | | 16,882 | | | (1,256) | | | -7.4% |

Loan servicing expense | | | 20,924 | | | 18,488 | | | 2,436 | | | 13.2% |

Occupancy and equipment | | | 16,768 | | | 20,521 | | | (3,753) | | | -18.3% |

General and administrative | | | 21,407 | | | 29,165 | | | (7,758) | | | -26.6% |

Depreciation and amortization | | | 5,918 | | | 7,612 | | | (1,694) | | | -22.3% |

Other expenses | | | 4,296 | | | 4,060 | | | 236 | | | 5.8% |

Total expenses | | | 241,136 | | | 206,305 | | | 34,833 | | | 16.9% |

| | | | | | | | | |||||

Loss from continuing operations before income tax | | | (41,411) | | | (42,048) | | | 637 | | | -1.5% |

Income tax benefit from continuing operations | | | (9,500) | | | (10,485) | | | 985 | | | -9.4% |

Income from equity method investments | | | 2,701 | | | 209 | | | 2,492 | | | 1,192.3% |

Net loss from continuing operations | | | (29,210) | | | (31,354) | | | 2,144 | | | -6.8% |

Net income from discontinued operations before tax | | | — | | | 9,707 | | | (9,707) | | | N/M |

Income tax provision from discontinued operations | | | — | | | 2,550 | | | (2,550) | | | N/M |

Income from discontinued operations, net of tax | | | — | | | 7,157 | | | (7,157) | | | N/M |

Total net loss | | | $(29,210) | | | $(24,197) | | | $(5,013) | | | 20.7% |

| | | Year Ended December 31, | ||||

($ in thousands) | | | 2019 | | | 2018 |

Gain on sales, net(a) | | | $209,261 | | | $80,536 |

Change in fair value of loans held for sale, IRLCs, and related hedges | | | 54,723 | | | (17,818) |

Realized and unrealized gain (loss) from derivative financial instruments | | | (60,290) | | | 22,717 |

Provision for losses relating to representations and warranties | | | (4,193) | | | (1,367) |

Gain on loans, net | | | $199,501 | | | $84,068 |

(a) | The Gain on sales, net includes income related to originations of mortgage servicing rights. |

| | | Year Ended December 31, | ||||

(in thousands) | | | 2019 | | | 2018 |

Origination volume(a) | | | 22,267,593 | | | 10,579,087 |

Originated MSR UPB | | | 20,484,918 | | | 11,690,884 |

Gain on sale margin(a)(b) | | | 89.6 | | | 79.5 |

Retained servicing (UPB)(c) | | | 96.8% | | | 97.4% |