Exhibit 99.1

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

This Management’s Discussion and Analysis (‘‘MD&A’’) is intended to help the reader understand Triple Flag Precious Metals Corp. (‘‘TF Precious Metals’’), its operations, financial performance and the present and anticipated future business environment. This MD&A, which has been prepared as of November 7, 2023, should be read in conjunction with the unaudited condensed interim consolidated financial statements of TF Precious Metals as at and for the three and nine months ended September 30, 2023 (the “Interim Financial Statements”), which have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”), applicable to the preparation of interim financial statements, including International Accounting Standard (“IAS”) 34, Interim Financial Reporting. The unaudited condensed consolidated interim financial statements have been prepared on a basis consistent with the audited consolidated financial statements of TF Precious Metals as at December 31, 2022 and for the years ended December 31, 2022 and 2021 (the “Annual Financial Statements”), which have been prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”). Certain notes to the Annual Financial Statements are specifically referred to in this MD&A. All amounts in this MD&A are in U.S. dollars unless otherwise indicated. References to “US$”, “$” or “dollars” are to United States dollars, references to “C$” are to Canadian dollars and references to “A$” are to Australian dollars. In this MD&A, all references to ‘‘Triple Flag’’, the ‘‘Company’’, ‘‘we’’, ‘‘us’’ or ‘‘our’’ refer to TF Precious Metals together with its subsidiaries, on a consolidated basis.

This MD&A contains forward-looking information. Forward-looking information is necessarily based on a number of opinions, estimates and assumptions that we considered appropriate and reasonable as of the date such statements were made, and are subject to known and unknown risks, uncertainties, assumptions and other factors that may cause the actual results, level of activity, performance or achievements to be materially different from those expressed or implied by such forward-looking information, including but not limited to the risk factors described in the ‘‘Risk Factors” section of the Company’s most recent annual information form (“AIF”) available from time to time on SEDAR+ at www.sedarplus.ca and on EDGAR at www.sec.gov. There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. Accordingly, users should not place undue reliance on forward-looking information, which speaks only as of the date made. See ‘‘Forward-Looking Information’’ in this MD&A.

Non-IFRS Financial Performance Measures

We use certain non-IFRS financial performance measures in our MD&A. For a detailed description of each of the non-IFRS financial performance measures used in this MD&A and a detailed reconciliation to the most directly comparable measure under IFRS, please refer to the “Non-IFRS Financial Performance Measures” section of this MD&A. The non-IFRS financial performance measures set out in this MD&A are intended to provide additional information to investors and do not have any standardized meaning under IFRS, and therefore may not be comparable to other issuers, and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

3 | |

3 | |

5 | |

6 | |

7 | |

7 | |

Portfolio of Streaming and Related Interests and Royalty Interests | 9 |

10 | |

12 | |

17 | |

17 | |

19 | |

23 | |

24 | |

24 | |

27 | |

27 | |

28 | |

29 | |

32 | |

32 | |

33 |

2

Triple Flag is a precious metals-focused streaming and royalty company offering bespoke financing solutions to the metals and mining industry. Our mission is to be a preferred funding partner to mining companies throughout the commodity cycle by providing customized streaming and royalty financing, while offering value beyond capital as partners via our networks, capabilities and sustainability support.

Since our inception in 2016, we have invested in and systematically developed a long-life, low-cost, high-quality diversified portfolio of streams and royalties providing exposure primarily to gold and silver. We acquired Maverix Metals Inc. (“Maverix”), a royalty and streaming company, earlier this year and our portfolio is now comprised of 234 assets, consisting of 15 streams and 219 royalties. These investments are tied to mining assets at various stages of the mine life cycle.

Asset Count |

| |

Producing |

| 32 |

Development & Exploration |

| 202 |

Total |

| 234 |

Our portfolio is underpinned by a stable base of cash flow generating streams and royalties and is designed to grow intrinsically over time through exposure to potential mine life extensions, exploration success, new mine builds and throughput expansions. In addition, we are focused on further enhancing portfolio quality by executing accretive investments to grow the scale and quality of our portfolio of precious metal streams and royalties. We believe we have a differentiated approach to deal origination and due diligence, increasing the applicability of stream and royalty financing to an underserved mining sector, expanding the application of this form of financing through bespoke deal generation for miners while creating a high-quality, precious metals-focused portfolio of streams and royalties for our investors. We focus on ‘‘per share’’ metrics with the objective that accretive new investments are pursued with careful management of the capital structure to effectively compete for quality assets without incurring long-term financial leverage.

The market prices of gold and silver are the primary, uncontrollable drivers of our profitability and ability to generate free cash flow.

The following table sets forth the average gold and silver prices, and the average exchange rate between the Canadian and U.S. dollars, for the periods indicated.

| | Three months ended | | Nine months ended | ||||

| | September 30 | | September 30 | ||||

Average Metal Prices/Exchange Rates |

| 2023 |

| 2022 | | 2023 | | 2022 |

Gold (US$/oz)1 |

| 1,928 |

| 1,729 | | 1,930 | | 1,824 |

Silver (US$/oz)2 |

| 23.57 |

| 19.23 | | 23.40 | | 21.92 |

Exchange rate (US$/C$)3 |

| 1.3415 |

| 1.3056 | | 1.3456 | | 1.2828 |

| 1. | Based on the London Bullion Market Association (“LBMA”) PM fix. |

| 2. | Based on the LBMA fix. |

| 3. | Based on the Bank of Canada daily average exchange rate. |

Gold

The market price of gold is subject to volatile price movements over short periods of time and can be affected by numerous macroeconomic factors including, but not limited to, the value of the U.S. dollar; the sale or purchase of gold by central banks and financial institutions, interest rates, inflation or deflation, global and regional supply and demand, as well as global political and economic conditions. The market price of gold is a significant contributor to the performance of our gold streams and royalty portfolio.

During the three months ended September 30, 2023, the gold price ranged from $1,871 to $1,976 per ounce, averaging $1,928 per ounce for the period, a 12% increase from the same period in the prior year. During the nine months ended September 30, 2023, the gold price ranged from $1,811 to $2,048 per ounce, averaging $1,930 per ounce for the period, a 6% increase from the same period in the prior year. As at September 30, 2023, the gold price was $1,871 per ounce (based on the LBMA PM fix). Notably, the gold price decreased

3

towards the end of the third quarter of 2023 due to a combination of rising real yields and a stronger US dollar, while a buoyant economy negatively weighed on investment demand for gold. Also during the quarter, physically-backed global gold ETFs saw net outflows with September being the fourth straight month of outflows mainly due to investors’ intensifying expectations of rates staying “higher for longer”.

Silver

The market price of silver is also subject to volatile price movements. Silver, often considered a proxy for gold with a high level of correlation to the metal, is predominantly used in industrial applications. Accordingly, a rebound of manufacturing activity is expected to have a positive effect on silver. The market price of silver is driven by factors similar to those influencing the market price of gold, as stated above. The market price of silver is a significant contributor to the performance of our silver streams.

During the three months ended September 30, 2023, the silver price ranged from $21.62 to $25.18 per ounce, averaging $23.57 per ounce for the period, a 23% increase from the same period in the prior year. During the nine months ended September 30, 2023, the silver price ranged from $20.09 to $26.03 per ounce, averaging $23.40 per ounce for the period, with a 7% increase from the same period in the prior year. As at September 30, 2023, the silver price was $23.08 per ounce (based on the LBMA fix). Similar to gold, silver was influenced by rising bond yields, the US dollar, and exchange traded fund flows.

Currency Exchange Rates

We are subject to minimal currency fluctuations as all our revenue and cost of sales are denominated in U.S. dollars, with the majority of general administration costs denominated in Canadian dollars. The Company monitors foreign currency risk as part of its risk management program. As at September 30, 2023, there were no hedging programs in place for non-U.S. dollar expenses.

4

Financial and Operating Highlights

Three and nine months ended September 30, 2023 compared to three and nine months ended September 30, 2022

| | Three months ended | | Nine months ended |

| ||||||||

| | September 30 | | September 30 | | ||||||||

($ thousands except GEOs, per share metrics and asset margin) |

| 2023 | | 2022 | | 2023 |

| 2022 |

| ||||

IFRS measures: | | | | | | | | | | | | | |

Revenue | | $ | 49,425 | | $ | 33,754 | | $ | 152,285 | | $ | 107,999 | |

Gross Profit | |

| 25,809 | | | 19,720 | | | 75,629 | |

| 62,546 | |

Depletion | |

| 16,811 | | | 10,817 | | | 48,479 | |

| 35,481 | |

General administration costs | |

| 4,440 | | | 3,627 | | | 15,296 | |

| 11,084 | |

Impairment charges | | | 27,107 | | | — | | | 27,107 | | | — | |

Net (Loss) Earnings | |

| (6,041) | | | 12,815 | | | 26,527 | |

| 39,626 | |

Net (Loss) Earnings per Share – basic and diluted | |

| (0.03) | | | 0.08 | | | 0.13 | |

| 0.25 | |

Operating Cash Flow | |

| 36,750 | | | 25,356 | | | 116,494 | |

| 81,655 | |

Operating Cash Flow per Share | |

| 0.18 | | | 0.16 | | | 0.59 | |

| 0.52 | |

| | | | | | | | | | | | | |

Non-IFRS measures1: | |

|

| | | | | | | |

|

| |

GEOs | |

| 25,629 | | | 19,523 | | | 78,844 | |

| 59,143 | |

Adjusted Net Earnings | |

| 17,337 | | | 13,258 | | | 48,512 | |

| 43,583 | |

Adjusted Net Earnings per Share | |

| 0.09 | | | 0.09 | | | 0.24 | |

| 0.28 | |

Adjusted EBITDA | |

| 38,804 | | | 26,054 | | | 117,524 | |

| 84,655 | |

Free Cash Flow | |

| 36,750 | | | 25,356 | | | 116,494 | |

| 81,655 | |

Asset Margin | |

| 90 | % | | 90 | % | | 90 | % |

| 91 | % |

| 1. | GEOs, adjusted net earnings, adjusted net earnings per share, adjusted EBITDA, free cash flow and asset margin as presented above and in the following discussion are non-IFRS financial performance measures with no standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. For further information and a detailed reconciliation of each non-IFRS measure to the most directly comparable IFRS measure, see ‘‘Non-IFRS Financial Performance Measures’’ in this MD&A. |

5

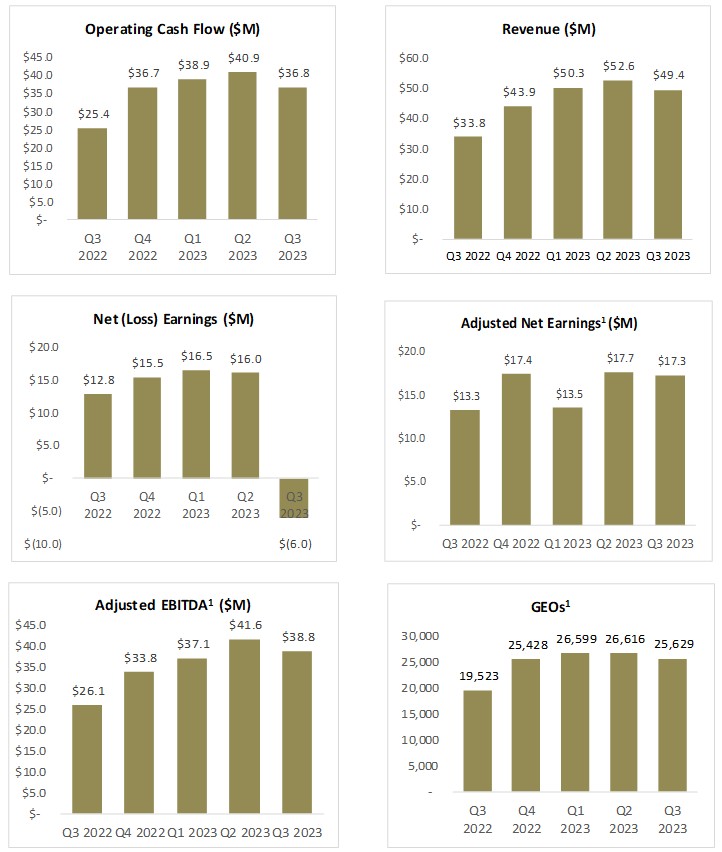

The following charts highlight our recent quarterly performance.

1GEOs, adjusted EBITDA and adjusted net earnings as presented above are non-IFRS financial performance measures with no standardized meaning under IFRS and, therefore, may not be comparable to similar measures presented by other issuers. For further information and a detailed reconciliation of each non-IFRS measure to the most directly comparable IFRS measure, see ‘‘Non-IFRS Financial Performance Measures’’ in this MD&A.

6

The following contains forward-looking information. Reference should be made to the “Forward-Looking Information” and “Technical and Third-Party Information” sections at the end of this MD&A.

The following table provides our full year 2023 guidance, which remains unchanged.

|

| 2023 Guidance |

GEOs1 |

| 100,000 to 115,0002 |

Depletion | | $65 million to $71 million |

| | $21 million to $22 million comprising: |

| | Cash: $16 million to $17 million |

General administration costs | | Non-Cash: ~$5 million |

Australian Cash Tax Rate3 | | ~25% |

1. | GEOs as presented above and in the following discussion is a non-IFRS financial performance measure with no standardized meaning under IFRS and therefore may not be comparable to similar measures presented by other issuers. For further information and a detailed reconciliation of GEOs to the most directly comparable IFRS measure, see ‘‘Non-IFRS Financial Performance Measures’’ in this MD&A. |

2. | Assumed commodity prices of $1,850/oz gold, $22.00/oz silver, $4.00/lb copper and $100/carat for diamonds. |

3. | Australian Cash Taxes are payable for Triple Flag’s Australian royalty interests. |

Our 2023 outlook on stream and related interests and royalty interests is based on publicly available forecasts of the owners or operators of properties on which we have stream and royalty interests and which we believe to be reliable. When publicly available forecasts on properties are not available, we obtain internal forecasts from the owners or operators, or use our own best estimate. We conduct our own independent analysis of this information to reflect our expectations based on an operator’s historical performance and track record of replenishing Mineral Reserves and the operator’s publicly disclosed guidance on future production, the conversion of Mineral Resources to Mineral Reserves, timing risk adjustments, drill results, our view on opportunities for mine plan optimization and other factors. We may also make allowances for the risk of uneven stream deliveries to factor in the potential for timing differences risking the attainment of public guidance ranges. Achievement of the GEOs and the other metrics set forth in the guidance above is subject to risks and uncertainties, including changes in commodity prices and the ability of operators to attain the results set out in their forecasts. Accordingly, we can provide no assurance that the actual GEOs and such other metrics for 2023 will be in the ranges set forth above. In addition, we may revise our guidance during the year to reflect more current information. If we are unable to achieve our anticipated guidance, or if we revise our guidance, our future results of operations may be adversely affected and our share price may decline.

For the fourth quarter of 2023, gold, silver, copper and royalty revenues have been converted to GEOs using commodity prices of $1,900 per ounce of gold and $23.00 per ounce of silver.

We strongly believe that sustainability is integral to our long-term success, the mining industry, and host communities. Robust sustainability performance, measured across multiple time horizons, ensures responsible development, worker safety, environmental protection, social responsibility, and benefits all stakeholders. Triple Flag, as a long-term-focused organization, recognizes the value of responsible practices. We support our mining partners in their decarbonization efforts while maintaining carbon neutrality across both our financed and corporate emissions.

We do not invest in oil, gas, or coal, instead focusing on green metals like copper and nickel in the non-core portion of our portfolio. Green metals are essential for the effective transition to a low-carbon economy driven by renewable energy. We conduct thorough due diligence, leveraging our experienced ESG team and external experts to identify and mitigate transitional and climate-related financial risks. Our goal is to achieve net-zero emissions by 2050, and we are actively pursuing pathways to attain this target.

7

Recognition and Achievements

In late July 2023, we received our inaugural rating of AA in the MSCI ESG Ratings assessment. MSCI ESG Research provides ratings on global public companies on a scale of AAA (leader) to CCC (laggard), according to exposure to industry-specific ESG risks and the ability to manage those risks relative to peers. Triple Flag falls into the highest scoring range for corporate governance relative to peers, reflecting governance practices that are well aligned to investor interests. In the environment and social categories, we performed higher than the industry average, excelling in community relations and health & safety metrics.

In September 2023, we were awarded Best Company for Social Responsibility (Mid-Cap) by ESG Investing. This award recognizes intentional and impactful community outreach, highlighting our commitment to serve our local and partner communities through active engagement. In addition, we were finalists for Best in Climate Reporting by ESG Investing, which recognizes excellence in climate-related disclosure and methodology.

Subsequent to quarter-end, we received our second Morningstar Sustainalytics rating, resulting in a 3rd percentile finish – 3rd of 117 across the precious metals industry with an absolute risk rating of 8.9 (negligible risk), improving on our rating from last year. Sustainalytics is a global leader in the fields of responsible investing and sustainable finance. Supported by a robust materiality framework, Sustainalytics’ ESG Risk Ratings provide a quantitative and absolute measure of unmanaged ESG Risk.

Giving Back to Our Community

Throughout the summer, wildfires raged across Canada, devastating communities and cutting off key supply routes. To aid in getting critical supplies to the front lines, we contributed C$10,000 to the Atlantic Canada Wildfire Fund organized by the Canadian Red Cross, which offered targeted support to residents of Quebec and Nova Scotia.

In July 2023, Katy Board, our VP of Talent & ESG, visited the Northparkes mine in New South Wales, Australia to attend the Frontline Ball, in support of Ronald McDonald House Charities in nearby Orange. Over A$100,000 was raised in support of local charities. The event was sponsored in part by Triple Flag, and Katy hosted our bursary award winners at the event, giving her the opportunity to meet the recipients (past and present) and site management in person. The Central West Ronald McDonald House supports rural and regional families from Western NSW Health District families, and for Child and Adolescent Mental Health Unit (“CAMHS”). The CAMHS unit in Orange is the only dedicated child and adolescent mental health unit in NSW outside of Sydney. The majority of the families utilizing the house come from rural communities surrounding the minesite.

In August 2023, our team spent a day at a Habitat for Humanity construction site, meeting partner families and working on the building of a 20-unit townhome complex. In addition to contributing labor, we donated C$15,000 to the Habitat fund for the construction of affordable housing in Toronto. In September 2023, Triple Flag sponsored a table at the 2023 Reasons for Hope Dinner (previously known as the Miner’s Lamp Dinner). This event raised over C$1.5 million for the University of Toronto’s Department of Psychiatry to support research into the prevention and early detection of mental illness in children and youth. Triple Flag is proud to be a continuing supporter of Reasons for Hope and mental health initiatives across Canada. Further, to commemorate the National Day for Truth and Reconciliation, our team attended an education session on the United Nations Declaration on the Rights of Indigenous Peoples to further our awareness of Indigenous law.

We currently support 15 engineering-related students through a full bursary program in partnership with Impala Bafokeng (“Implats”, formerly Royal Bafokeng). It is anticipated that 8 of these students will graduate at the end of 2023 and have the opportunity to join Implats’s graduate employment program. We will begin recruiting new and continuing students throughout Q4 and early into Q1 2024 (note the school year in South Africa is on a calendar year schedule).

8

Portfolio of Streaming and Related Interests and Royalty Interests

The following tables present our revenue and GEOs sold by asset for the periods indicated. GEOs are based on stream and related interests as well as royalty interests and are calculated on a quarterly basis by dividing all revenue from such interests for the quarter by the average gold price during that quarter. The gold price is determined based on the LBMA PM fix. For periods longer than one quarter, GEOs are summed for each quarter in the period.

Three and nine months ended September 30, 2023 compared to three and nine months ended September 30, 2022

| | Three months ended September 30 | | Nine months ended September 30 | ||||||||

Revenue ($000s) |

| 2023 |

| 2022 |

| 2023 |

| 2022 | ||||

Streaming and Related Interests | | | | | | | | | | | | |

Cerro Lindo | | $ | 10,563 | | $ | 8,024 | | $ | 32,550 | | $ | 30,426 |

Northparkes | |

| 7,559 | | | 5,351 | | | 21,754 | |

| 18,561 |

ATO | |

| 4,130 | | | 5,183 | | | 15,857 | |

| 10,799 |

RBPlat | |

| 3,148 | | | 3,027 | | | 9,185 | |

| 10,636 |

Buriticá | | | 3,029 | | | 1,449 | | | 8,646 | | | 5,084 |

Moss | |

| 2,340 | | | — | | | 8,286 | |

| — |

Auramet | |

| 2,358 | | | — | | | 7,208 | |

| — |

Renard | |

| 1,710 | | | 2,348 | | | 5,834 | |

| 6,978 |

Other1 | |

| 2,553 | | | 196 | | | 8,221 | |

| 1,402 |

| | $ | 37,390 | | $ | 25,578 | | $ | 117,541 | | $ | 83,886 |

Royalty Interests | |

|

| | | | | | | |

|

|

Fosterville | | $ | 3,108 | | $ | 3,486 | | $ | 8,144 | | $ | 12,073 |

Beta Hunt | |

| 2,328 | | | — | | | 7,015 | |

| — |

Young-Davidson | |

| 1,319 | | | 1,266 | | | 3,888 | | | 4,202 |

Camino Rojo | | | 1,079 | | | — | | | 3,118 | | | — |

Florida Canyon | | | 1,554 | | | — | | | 2,979 | | | — |

Other2 | |

| 2,647 | | | 3,424 | | | 9,600 | |

| 7,838 |

| | | 12,035 | | | 8,176 | | | 34,744 | | | 24,113 |

Total | | $ | 49,425 | | $ | 33,754 | | $ | 152,285 | | $ | 107,999 |

| | Three months ended September 30 | | Nine months ended September 30 | ||||||||

Revenue ($000s) |

| 2023 |

| 2022 |

| 2023 |

| 2022 | ||||

Gold | | $ | 29,149 | | $ | 20,605 | | $ | 89,473 | | $ | 61,205 |

Silver | |

| 18,321 | | | 10,605 | | | 56,070 | |

| 39,159 |

Other3 | |

| 1,955 | | | 2,544 | | | 6,742 | |

| 7,635 |

Total | | $ | 49,425 | | $ | 33,754 | | $ | 152,285 | | $ | 107,999 |

| 1. | Includes revenue from El Mochito, La Colorada, Gunnison and Pumpkin Hollow. |

| 2. | Includes revenue from Dargues, Eagle River, Hemlo, Henty, Stawell and other royalties, including royalties acquired pursuant to the Maverix acquisition. |

| 3. | Includes copper and diamonds. |

9

| | Three months ended September 30 | | Nine months ended September 30 | ||||

GEOs (ounces) |

| 2023 |

| 2022 |

| 2023 |

| 2022 |

Streaming and Related Interests | | | | | | | | |

Cerro Lindo |

| 5,477 | | 4,640 | | 16,925 |

| 16,592 |

Northparkes |

| 3,919 | | 3,095 | | 11,223 |

| 10,144 |

ATO |

| 2,142 | | 2,998 | | 8,218 |

| 5,999 |

RBPlat |

| 1,632 | | 1,751 | | 4,754 |

| 5,810 |

Buriticá | | 1,570 | | 838 | | 4,478 | | 2,777 |

Moss |

| 1,214 | | — | | 4,291 |

| — |

Auramet |

| 1,222 | | — | | 3,734 |

| — |

Renard |

| 887 | | 1,358 | | 3,023 |

| 3,829 |

Other1 |

| 1,324 | | 113 | | 4,257 |

| 757 |

|

| 19,387 | | 14,793 | | 60,903 |

| 45,908 |

Royalty Interests | | | | | | | | |

Fosterville |

| 1,612 | | 2,016 | | 4,199 |

| 6,599 |

Beta Hunt |

| 1,207 | | — | | 3,621 |

| — |

Young-Davidson |

| 684 | | 733 | | 2,011 |

| 2,300 |

Camino Rojo | | 560 | | — | | 1,615 | | — |

Florida Canyon | | 806 | | — | | 1,538 | | — |

Other2 |

| 1,373 | | 1,981 | | 4,957 |

| 4,336 |

|

| 6,242 | | 4,730 | | 17,941 |

| 13,235 |

Total |

| 25,629 | | 19,523 | | 78,844 |

| 59,143 |

| | Three months ended September 30 | | Nine months ended September 30 | ||||

GEOs (ounces) |

| 2023 |

| 2022 |

| 2023 |

| 2022 |

Gold |

| 15,115 | | 11,918 | | 46,254 |

| 33,587 |

Silver |

| 9,500 | | 6,134 | | 29,100 |

| 21,368 |

Other3 |

| 1,014 | | 1,471 | | 3,490 |

| 4,188 |

Total |

| 25,629 | | 19,523 | | 78,844 |

| 59,143 |

| 1. | Includes revenue from El Mochito, La Colorada, Gunnison and Pumpkin Hollow. |

| 2. | Includes revenue from Dargues, Eagle River, Hemlo, Henty and Stawell and other royalties, including royalties acquired pursuant to the Maverix acquisition. |

| 3. | Includes copper and diamonds. |

For the nine months ended September 30, 2023

Acquisition of an additional royalty interest in Stawell Gold Mines Pty Ltd .

On September 25, 2023, the Company entered into an agreement with Stawell Gold Mines Pty Ltd (“Stawell”) for the acquisition of an additional 2.65% net smelter returns (“NSR”) royalty. This is in addition to the pre-existing 1.0% NSR royalty on gold that Triple Flag previously held. Both royalties cover future production at the Stawell gold mine in Victoria, Australia. Triple Flag acquired the additional royalty interest for cash consideration of $16.6 million. The additional royalty interest was recorded as mineral interest.

10

Impairment Charges

In accordance with the Company’s accounting policy, non-current assets are tested for impairment or impairment reversals when events or changes in circumstances suggest that the carrying amount may not be recoverable or is understated. Impairments in the carrying value of each cash-generating unit (“CGU”) are measured and recorded to the extent that the carrying value of each CGU exceeds its estimated recoverable amount, which is the higher of fair value less costs of disposal (“FVLCD”) and value-in-use (“VIU”), which is generally calculated using an estimate of future discounted cash flows. Impairment charges are included in the ‘‘Impairment charges’’ line within the condensed interim consolidated statements of income (loss).

Loans receivable and receivables are written off when there is no reasonable expectation of recovery. Indicators that there is no reasonable expectation of recovery include, among others, the failure of a debtor to engage in a repayment plan, and a failure to make contractual payments for a period of greater than 120 days past due. Impairment losses on loans receivable and receivables are presented as impairment charges within operating income. Subsequent recoveries of amounts previously written off are credited against the same line item.

| i. | Renard |

During the three months ended September 30, 2023, the Renard mine, operated by the Stornoway Diamond Corporation (“Stornoway”), experienced financial difficulties due to adverse market conditions, such as increased operational costs due to inflationary pressures, and the continued decline of diamond prices due to lower demand. On September 27, 2023, this was further exacerbated by India’s diamond trade bodies urging its members to halt imports of rough diamonds from mid-October to mid-December to manage supplies. As a result of the prolonged softening of the diamond market over the third quarter, Triple Flag concluded that an indicator of impairment existed. Management performed an impairment analysis for the Renard stream in accordance with IAS 36 Impairment of Assets, and for the Bridge Financing under IFRS 9 Financial Instruments.

Triple Flag considered a variety of factors to determine the recoverable amount of the Renard stream and the recoverability of the loan receivable, including cash flows expected to be generated from the Renard mine over the estimated life of mine under different mine plans and diamond price scenarios.

On October 27, 2023, the Renard mine was placed in care and maintenance and Stornoway filed for creditor protection under the Companies’ Creditors Arrangement Act (“CCAA”) in Quebec.

As a result, Triple Flag concluded that there is no reasonable expectation of recovery of the loan receivable and determined that the recoverable amount of the Renard stream was nil as at September 30, 2023, resulting in a total impairment charge of $20.2 million.

| ii. | Beaufor |

In the second half of 2022, Monarch Mining Corporation (“Monarch”), owner of the Beaufor mine, suspended its operations at the Beaufor mine due to financial and operational challenges. On September 27, 2022, the mine was put on care and maintenance for an indefinite period. Due to the continued suspension of operations at the Beaufor mine, the Company concluded that this was a triggering event. As a result, management performed an impairment analysis for the Beaufor royalty investment as at December 31, 2022, resulting in the Beaufor royalty being written down to its estimated recoverable amount of $6.8 million.

During the three months ended September 30, 2023, management concluded that the continued suspension of operations at the Beaufor Mine, now exceeding twelve months, coupled with the market activity and financial position of Monarch disclosed in their 2023 consolidated financial statements, which was released on September 28, 2023, is a triggering event. Triple Flag considered a variety of factors to determine the recoverable amount of the Beaufor royalty, including cash flows expected to be generated from the Beaufor mine over the estimated life of mine.

On November 3, 2023, Monarch announced that one of its creditors, Investissement Québec (“IQ”), had provided notice of its intention to exercise certain rights in respect of the security for its loans totaling C$10.1 million to Monarch. IQ’s loans are secured by all assets of Monarch.

11

As a result, Triple Flag determined the recoverable amount of the Beaufor royalty investment to be nil and therefore recorded an impairment charge of $6.8 million.

Acquisition of Agbaou Royalty

On June 23, 2023, the Company entered into an agreement with Auramet Capital Partners, L.P. (“Auramet”) for the acquisition of the 2.5% NSR royalty it held on the Agbaou mine in Côte d’Ivoire, operated by Allied Gold Corp (“Agbaou Royalty”). The Agbaou royalty provides Triple Flag with an entitlement to 2.5% of net smelter returns from future production at the Agbaou mine. Triple Flag acquired the Agbaou Royalty for a total consideration of $15.5 million of which $13.5 million was paid in cash and remaining paid through an in-kind contribution of an asset held by the Company. The Agbaou Royalty was recorded as mineral interest.

Acquisition of Maverix

On January 19, 2023, the Company acquired all of the issued and outstanding common shares of Maverix pursuant to the terms of an arrangement agreement dated November 9, 2022 (the “Agreement”). Pursuant to the Agreement, Maverix shareholders had the option to receive either 0.36 of a TF Precious Metals common share or $3.92 in cash per Maverix common share, in each case subject to pro-ration such that the aggregate cash consideration would not exceed 15% of the total consideration and the aggregate share consideration does not exceed 85% of the total consideration. In addition, (i) holders of options to acquire Maverix Shares received fully vested replacement options to acquire Triple Flag Shares; and (ii) the restricted share units (“RSUs”) of Maverix outstanding immediately prior to the effective time of the transaction, whether vested or unvested, were assigned and transferred by the holder to Maverix in exchange for a cash payment and each RSU was immediately cancelled. The outstanding Maverix warrants (the “Maverix Warrants”) (5,000,000 Maverix share warrants outstanding with an exercise price of $3.28 per Maverix Share outstanding as of the closing date) were automatically adjusted in accordance with their terms, such that if and when exercised, Maverix warrant holders would receive a total of 1,800,000 Triple Flag shares at an exercise price of $9.11 per Triple Flag Share. The Maverix Warrants were exercised on April 12, 2023.

In connection with the closing, Triple Flag paid $86.7 million and issued 45,097,390 common shares to all former Maverix shareholders, and incurred $5.8 million of transaction costs. The transaction was accounted for as an asset acquisition on January 19, 2023. Following the completion of the acquisition, Maverix Metals Inc. became a wholly-owned subsidiary of Triple Flag.

The transaction was accounted for as an asset acquisition on January 19, 2023, with mineral interests of $587.8 million and is described in Note 4 of the Interim Financial Statements. The other net assets acquired in the transaction included cash and cash equivalents, amounts receivable, prepaid gold interests and loans receivable of approximately $68.9 million, amounts payable and other liabilities, lease liabilities and income tax payable of $11.9 million. The other liabilities included change of control under the terms of Maverix’s employment agreements.

Operating Assets – Performance

Our business is organized into a single operating segment, consisting of acquiring and managing precious metals and other high-quality streams and royalties. Our chief operating decision-maker, the CEO, makes capital allocation decisions, reviews operating results and assesses performance.

Asset Performance — Streams and related assets (producing)

1. | Cerro Lindo (Operator: Nexa Resources S.A.) |

Under the stream agreement with Nexa Resources S.A. (“Nexa”), we receive 65% of payable silver produced from the Cerro Lindo mine until 19.5 million ounces have been delivered and 25% thereafter. Typically, deliveries under the stream lag production by up to 4 months. As at September 30, 2023, 13.6 million ounces of silver had been delivered under the stream agreement with Nexa since inception.

For the three months ended September 30, 2023, we sold the 452,685 ounces of silver delivered under the agreement, a 7% increase from the ounces of silver sold for the same period in the prior year, driven by higher deliveries. GEOs sold were 5,477 for the three months ended September 30, 2023, compared to 4,640 for the same period in the prior year.

12

For the nine months ended September 30, 2023, we sold the 1,419,442 ounces of silver delivered under the agreement, largely in line with the silver sold for the same period in the prior year. GEOs sold were 16,925 for the nine months ended September 30, 2023, compared to 16,592 for the same period in the prior year.

As expected and previously disclosed, deliveries from Cerro Lindo improved sequentially in the third quarter of 2023 following the rainfall-related shutdown in mid-March due to Cyclone Yaku, which temporarily restricted access to higher-grade zones in the second quarter.

During the quarter, the exploration program at Cerro Lindo focused on extensions of known orebodies to the southeast of Cerro Lindo. Drilling also began at the Patahuasi Millay expansion target, which is within Triple Flag’s stream area and is located 500 meters to the northwest of Cerro Lindo.

2. | Northparkes (Operator: China Molybdenum Co., Ltd) |

Under the stream agreement with China Molybdenum Co., Ltd (“CMOC”), we receive 54% of payable gold until an aggregate of 630,000 ounces have been delivered and 27% of payable gold thereafter. We also receive 80% of payable silver until an aggregate of 9 million ounces of silver have been delivered, and 40% of payable silver thereafter for the remainder of the life of mine. Typically, deliveries under the stream lag production by 2 months. As at September 30, 2023, 37,794 ounces of gold and 680,842 ounces of silver had been delivered under the stream agreement with CMOC since inception.

For the three months ended September 30, 2023, we sold the 3,254 ounces of gold and 55,098 ounces of silver delivered to the Company. This compares to 2,544 ounces of gold and 48,707 ounces of silver delivered and sold for the same period in the prior year. GEOs sold were 3,919 for the three months ended September 30, 2023, compared to 3,095 for the same period in the prior year.

For the nine months ended September 30, 2023, we sold the 9,184 ounces of gold and 171,255 ounces of silver delivered to the Company. This compares to 8,460 ounces of gold and 148,571 ounces of silver delivered and sold for the same period in the prior year. GEOs sold were 11,223 for the nine months ended September 30, 2023, compared to 10,144 for the same period in the prior year.

E31 and E31N are higher gold grade open pit deposits at Northparkes, which are expected to contribute to significant near-term production growth at this operation. Development continues to advance, with the first blast successfully completed at E31N during August 2023. Mining of transitional ore commenced at both open pits during the month, with sulfide ore mined from E31 in September. Ore from E31 and E31N is expected to contribute to mill feed blend starting in the fourth quarter of 2023 , which should drive GEOs sales growth starting in 2024.

Separately, the E22 blockcave feasibility study continued to advance during the third quarter of 2023 and is expected to be completed in the first half of 2024. A boxcut and decline development from surface is expected to commence in the third quarter of 2024. Of note, this study is expected to include an evaluation of a regrind ball mill which, if approved, could be installed by 2025 to improve concentrate grade and marketability.

3. | Impala Bafokeng Operations (Operator: Impala Platinum Holdings Limited) |

Under the stream agreement with Royal Bafokeng Platinum Limited (“RBPlat”), we receive 70% of payable gold until 261,000 ounces are delivered and 42% of payable gold thereafter from the RBPlat PGM Operations. Typically, deliveries under the stream lag production by 5 months. As at September 30, 2023, 26,523 ounces of gold had been delivered under the stream agreement with RBPlat since inception.

For the three months ended September 30, 2023, we sold the 1,631 ounces of gold delivered by RBPlat under the stream agreement, a 6% decrease from the ounces delivered and sold for the same period in the prior year. GEOs sold were 1,632 for the three months ended September 30, 2023, compared to 1,751 for the same period in the prior year.

For the nine months ended September 30, 2023, we sold the 4,767 ounces of gold delivered by RBPlat under the stream agreement, a 17% decrease from the ounces delivered and sold for the same period in the prior year. GEOs sold were 4,754 for the nine months ended September 30, 2023, compared to 5,810 for the same period in the prior year.

13

Impala Platinum Limited (“Implats”) has completed the acquisition of RBPlat and is now implementing plans to integrate and optimize the asset. As contiguous operations, the combined asset base of Impala Rustenburg and RBPlats is expected to result in a more secure and sustainable Rustenburg operating complex. It has a premier production base, well-capitalized infrastructure and long-term competitive positioning, and an integrated processing capability which will assist with achievement of material potential synergies. We are encouraged by the outlook for this asset, particularly as the Styldrift mine ramps up to nameplate hoisting capacity of 230kt per month.

4. | Altan Tsagaan Ovoo (“ATO”) (Operator: Steppe Gold) |

Under the stream agreement with Steppe Gold, we receive 25% of the payable gold until 46,000 ounces of gold have been delivered and 25% of payable gold thereafter, subject to an annual cap of 7,125 ounces. We also receive 50% of the payable silver until 375,000 ounces of silver have been delivered and 50% of payable silver thereafter, subject to an annual cap of 59,315 ounces. As at September 30, 2023, 24,529 ounces of gold and 67,159 ounces of silver had been delivered under the stream agreement with Steppe Gold since inception.

For the three months ended September 30, 2023, we sold the 1,995 ounces of gold and 11,922 ounces of silver delivered to the Company under stream and related interests, compared to the 2,927 ounces of gold and 9,214 ounces of silver sold for the same period in the prior year, respectively. GEOs sold were 2,142 for the three months ended September 30, 2023, compared to 2,998 for the same period in the prior year.

For the nine months ended September 30, 2023, we sold the 7,891 ounces of gold and 26,928 ounces of silver delivered to the Company under stream and related interests (2,500 ounces were from the prepay arrangement), compared to the 5,905 ounces of gold and 12,728 ounces of silver sold for the same period in the prior year, respectively. GEOs sold were 8,218 for the nine months ended September 30, 2023, compared to 5,999 for the same period in the prior year.

Steppe Gold has indicated that current operations at ATO are on track to achieve their target of 25,000 to 30,000 ounces of gold for 2023. On July 11th, 2023, Steppe Gold announced it had signed a binding term sheet for $150 million in financing to fully fund the construction and completion of the Phase 2 mine and mill expansion at ATO (“Phase 2”). In October 2023, Steppe Gold announced an initial drawdown of $9.6 million from the $150 million financing package for the development of Phase 2. As per disclosures from the operator, Phase 2 is expected to generate a total of 1,237,000 ounces of gold equivalent (“Au Eq”) recovered over 12 years, at an average of over 100,000 gold equivalent ounces per annum over 12 years. First concentrate production from Phase 2 is expected in late 2025 or early 2026.

Exploration continues at ATO with a focus on expanding oxide mineralization. Steppe Gold has explored less than 10% of the license area.

5. | Buriticá (Operator: Zijin Mining Group Co.) |

Under the stream agreement with Zijin Mining Group Co., we receive 100% of payable silver based on a fixed silver-to-gold ratio of 1.84 over the life of the asset. On average, deliveries under the stream lag production by 3 months.

For the three months ended September 30, 2023, we sold the 129,771 ounces of silver delivered under the agreement, a 67% increase from the same period in the prior year. GEOs sold were 1,570 for the three months ended September 30, 2023, compared to 838 for the same period in the prior year.

For the nine months ended September 30, 2023, we sold the 376,636 ounces of silver delivered under the agreement, a 60% increase from the same period in the prior year. GEOs sold were 4,478 for the nine months ended September 30, 2023, compared to 2,777 for the same period in the prior year.

Through the third quarter of 2023, Buriticá was able to maintain steady operations, however due to the ongoing presence of illegal miners, certain areas of the mine were avoided as a precautionary measure. The mine site continues to engage closely with the surrounding community on illegal mining and is supported by the National Army and National Police.

14

6. | Renard (Operator: Stornoway Diamond Corporation) |

Under the stream agreement with Stornoway Diamond Corporation, we receive 4% of payable carats over the life of the asset.

For the three months ended September 30, 2023, there were 19,050 diamond carats attributable to the Company under the agreement, in line with the same period in the prior year. GEOs sold were 887 for the three months ended September 30, 2023, compared to 1,358 for the same period in the prior year, largely driven by a higher ratio of gold prices to diamond prices.

For the nine months ended September 30, 2023, there were 56,567 diamond carats attributable to the Company under the agreement, an 5% increase from the same period in the prior year. GEOs sold were 3,023 for the nine months ended September 30, 2023, compared to 3,829 for the same period in the prior year, largely driven by a higher ratio of gold prices to diamond prices.

During the three months ended September 30, 2023, the Renard mine, operated by the Stornoway, experienced financial difficulties due to adverse market conditions, such as increased operational costs due to inflationary pressures, and the continued decline of diamond prices due to lower demand. On September 27, 2023, this was further exacerbated by India’s diamond trade bodies urging its members to halt imports of rough diamonds from mid-October to mid-December to manage supplies. As a result of the prolonged softening of the diamond market over the third quarter, Triple Flag concluded that an indicator of impairment existed. Management performed an impairment analysis for the Renard stream in accordance with IAS 36 Impairment of Assets, and for the Bridge Financing under IFRS 9 Financial Instruments.

Triple Flag considered a variety of factors to determine the recoverable amount of the Renard stream and the recoverability of the loan receivable, including cash flows expected to be generated from the Renard mine over the estimated life of mine under different mine plans and diamond price scenarios. On October 27, 2023, the Renard mine was placed in care and maintenance and Stornoway filed for creditor protection under the Companies’ Creditors Arrangement Act in Quebec. As a result, Triple Flag concluded that there is no reasonable expectation of recovery of the loan receivable and determined that the recoverable amount of the Renard stream was nil as at September 30, 2023, resulting in a total impairment charge of $20.2 million.

7. | Moss (Operator: Elevation Gold Mining Corporation) |

Pursuant to the Maverix acquisition, the Company acquired a silver stream on the Moss mine, located in Arizona, USA. Under the agreement, we receive 100% of payable silver produced from the Moss mine until 3.5 million ounces have been delivered under the agreement and 50% thereafter. As at September 30, 2023, 1.1 million ounces of silver had been delivered under the stream agreement since inception.

For the three and nine months ended September 30, 2023, GEOs earned were 1,214 and 4,291, respectively.

The 3A Phase 2 gold and silver leach pad expansion at Moss continues to progress on budget and is expected to be completed in the fourth quarter of 2023.

Subsequent to quarter-end, the Company entered into an agreement with the operator to receive 1,125 ounces of gold by December 15, 2023 in exchange for an advance of $2 million.

Asset Performance — Royalties (Producing)

1. | Fosterville Gold Mine (Operator: Agnico Eagle Mines Limited, effective February 8, 2022) |

We own a 2% NSR royalty interest in Agnico Eagle Mines Limited’s (“Agnico Eagle") Fosterville mine in Australia. On October 25, 2023, Agnico Eagle reported results for the third quarter of 2023. For the three months ended September 30, 2023, Fosterville milled 144 thousand tonnes of ore at an average grade of 13.22 g/t Au resulting in gold production of 59,790 ounces, compared to 172 thousand tonnes of ore milled for the same period in the prior year at an average grade of 15.11 g/t Au resulting in gold production of 81,801 ounces.

15

For the nine months ended September 30, 2023, Fosterville milled 468 thousand tonnes of ore at an average grade of 15.48 g/t Au resulting in gold production of 228,161 ounces, compared to 385 thousand tonnes of ore milled for the same period in the prior year at an average grade of 20.46 g/t Au resulting in gold production of 249,693 ounces.

GEOs earned were 1,612 and 4,199 for the three and nine months ended September 30, 2023, respectively, compared to 2,016 and 6,599 respectively for the prior year.

Agnico Eagle now expects full year 2023 gold production at Fosterville of approximately 285,000 ounces, compared to prior guidance of 295,000 to 315,000 ounces. This is mainly driven by a focus on underground development to advance upgrades to the primary ventilation system.

Ongoing exploration work at Fosterville continued through the third quarter, including a highlight intercept of 10.8 g/t Au gold over 10.0 meters in the Cardinal splay, approximately 190 metres down-plunge of current mineral reserves. The result is the deepest visible-gold intercept in the Cardinal splay achieved to date, which is a key target of the Lower Phoenix zone.

2. | Beta Hunt (Operator: Karora Resources Inc.) |

Pursuant to the Maverix acquisition, the Company acquired 3.25% GRR and 1.5% NSR royalties on all gold production and aggregate 1.5% NSR royalties on all nickel production from the Beta Hunt mine, located in Australia.

GEOs earned were 1,207 and 3,621 for the three and nine months ended September 30, 2023, respectively.

Karora Resources continues to advance development of a second decline at Beta Hunt to increase mine capacity to 2 million tonnes per annum by the end of 2024. Exploration work throughout 2023 focused on the Fletcher and Mason zones, which indicate the potential for resource expansion outside the main Western Flanks and A Zone areas. Notably at the Mason zone, drilling in the third quarter of 2023 extended the mineralized strike by 100 meters to 800 meters, providing confidence for a potential new deposit for mining. Highlight assays include 14.7 g/t Au over 4.0 meters and 12.2g/t Au over 6.0 meters.

3. | Young-Davidson Gold Mine (Operator: Alamos Gold Inc.) |

We own a 1.5% NSR royalty interest in Alamos Gold Inc.’s (“Alamos Gold”) Young-Davidson mine in Canada. On October 25, 2023, Alamos Gold reported results for the third quarter of 2023. For the three months ended September 30, 2023, Young-Davidson processed 754,705 tonnes of ore at an average grade of 2.08 g/t Au and a recovery of 90%, resulting in gold production of 45,100 ounces, compared to 719,050 tonnes of ore processed for the same period in the prior year at an average grade of 2.31 g/t Au and a recovery of 92%, resulting in gold production of 49,300 ounces.

For the nine months ended September 30, 2023, Young-Davidson processed 2,153,377 tonnes of ore at an average grade of 2.14 g/t Au and a recovery of 90%, resulting in gold production of 135,300 ounces, compared to 2,161,792 tonnes of ore processed for the same period in the prior year at an average grade of 2.31 g/t Au and a recovery of 91%, resulting in gold production of 147,600 ounces.

GEOs earned were 684 and 2,011 for the three and nine months ended September 30, 2023, respectively, compared to 733 and 2,300 respectively for the prior year.

According to Alamos Gold, Young-Davidson had a strong third quarter with mining at forecasted rates. Higher grades are expected to drive stronger performance in the fourth quarter of 2023 and the asset is on track to achieve its full-year gold production guidance of 185,000 to 200,000 ounces.

16

The following table summarizes other financial assets as at September 30, 2023 and December 31, 2022:

|

| As at |

| As at | ||

($ thousands) | | September 30, 2023 | | December 31, 2022 | ||

Prepaid gold interests – Auramet Capital Partners1 | | $ | 40,818 | | $ | — |

Investments2 | |

| 6,165 | |

| 5,372 |

Prepaid gold interest – Steppe Gold3 | |

| — | |

| 4,534 |

Total financial assets | |

| 46,983 | |

| 9,906 |

| 1 | On January 19, 2023, as part of the Maverix acquisition, the Company acquired a prepaid gold interest with Auramet Capital Partners, L.P., a subsidiary of Auramet International LLC (“Auramet”). The contract requires Auramet to deliver 1,250 ounces of gold to Triple Flag per quarter. Triple Flag is required to make ongoing cash payments equal to 16% of the spot gold price for each gold ounce delivered. On and after ten years and 50,000 ounces of gold have been delivered (since inception), Auramet shall have the option to terminate the stream for a cash payment of $5 million less certain cash flows related to the gold deliveries. As at September 30, 2023, 38,750 ounces of gold were yet to be delivered under the contract. The Auramet Prepaid Gold Interest is accounted for as a financial asset at fair value through profit or loss. |

| 2 | Investments comprise equity interests and warrants in publicly traded and private companies and have been recorded at fair value. The fair value of the public equity investments is classified as level 1 of the fair value hierarchy because the main valuation inputs used are quoted prices in active markets, the fair value of the warrants is classified as level 2 because one or more of the significant inputs are based on observable market data, and the fair value of the private equity investments is classified as level 3 of the fair value hierarchy because the relevant observable inputs are not available. Refer to Note 12 of the Interim Financial Statements for additional details. |

| 3 | On September 26, 2022, the Company entered into an agreement with Steppe Gold to acquire a prepaid gold interest. The Company made a cash payment of $4.8 million to acquire the prepaid gold interest in exchange for delivery of 3,000 ounces of gold that were delivered by Steppe Gold in 8 monthly deliveries. The final delivery was made in May, 2023. |

The change in fair value of financial assets for the three months ended September 30, 2023 was $798 thousand loss (2022: $307 thousand loss), and for the nine months ended September 30, 2023 was $1,901 thousand gain (2022: $4,799 thousand loss).

Financial Condition and Shareholders’ Equity Review

Summary Balance Sheet

The following table presents summarized consolidated balance sheet information as at September 30, 2023 and December 31, 2022:

|

| As at |

| As at | ||

($ thousands) | | September 30, 2023 | | December 31, 2022 | ||

Cash and cash equivalents | | $ | 14,343 | | $ | 71,098 |

Other current assets | |

| 33,826 | |

| 19,509 |

Non-current assets | |

| 1,857,609 | |

| 1,246,424 |

Total assets | | $ | 1,905,778 | | $ | 1,337,031 |

| | | | | | |

Current liabilities | | $ | 12,534 | | $ | 12,586 |

Long-term debt | |

| 65,000 | |

| — |

Other non-current liabilities | |

| 6,544 | |

| 5,966 |

Total liabilities | |

| 84,078 | |

| 18,552 |

Total shareholders’ equity | |

| 1,821,700 | |

| 1,318,479 |

Total liabilities and shareholders’ equity | | $ | 1,905,778 | | $ | 1,337,031 |

Total assets were $1,905.8 million as at September 30, 2023, compared to $1,337.0 million as at December 31, 2022. Our asset base primarily consists of non-current assets such as mineral interests, which consist of our interests in streams and related interests and royalties. Our asset base also includes current assets, which generally include cash and cash equivalents, receivables, metal inventory

17

and financial assets. The increase in total assets from December 31, 2022 was largely driven by the mineral interests acquired pursuant to the Maverix acquisition.

Total liabilities were $84.1 million as at September 30, 2023, compared to $18.6 million as at December 31, 2022. The increase in total liabilities largely relate to the net drawdown from the Credit Facility to partially fund the Maverix acquisition, net of subsequent repayments. Total liabilities consist largely of long-term debt, amounts payable and accrued liabilities, deferred tax liabilities and lease obligations. For information about the Credit Facility, see “Liquidity and Capital Resources” below.

Total shareholders’ equity as at September 30, 2023 was $1,821.7 million, compared to $1,318.5 million as at December 31, 2022. The increase in shareholders’ equity largely reflects additional equity issued pursuant to the Maverix acquisition and income generated during the period net of dividends paid.

Shareholders’ Equity

As at September 30, 2023 |

| Number of shares |

Common shares |

| 201,693,662 |

As at December 31, 2022 |

| Number of shares |

Common shares |

| 155,685,593 |

In November 2022, Triple Flag received approval from the TSX to renew its normal course issuer bid (“NCIB”). Under the NCIB, the Company may acquire up to 2,000,000 of its common shares from time to time in accordance with the NCIB procedures of the TSX. Repurchases under the NCIB are authorized until November 14, 2023. Daily purchases on the TSX will be limited to 9,186 common shares, representing 25% of the average daily trading volume of the common shares on the TSX for the period from May 1, 2022 to October 31, 2022 (being 36,744 common shares), except where purchases are made in accordance with the “block purchase exemption” of the TSX rules. All common shares that are repurchased by the Company under the NCIB will be cancelled. For the three and nine months ended September 30, 2023, the Company purchased 234,474 and 1,146,120, respectively of its common shares under the normal course issuer bid (“NCIB”) for $3.2 million and $16.3 million respectively. Triple Flag may purchase a remaining 684,858 common shares out of the authorized total of 2,000,000.

On September 30, 2023, in connection with the NCIB, the Company entered into an Automatic Share Purchase Plan (“ASPP”) with the designated broker responsible for the NCIB. The ASPP is intended to allow for the purchase of its common shares under the NCIB at times when the Company would ordinarily not be permitted to purchase its common shares due to regulatory restrictions and customary self-imposed blackout periods. On September 29, 2023, the Company instructed the designated broker to make purchases under the ASPP during the period between October 2, 2023 to November 9, 2023. The Company has recorded a liability of $1.5 million reflecting the obligation to purchase shares under ASPP as at September 30, 2023.

As at November 7, 2023, 201,569,762 common shares are issued and outstanding and stock options are outstanding to purchase a total of 5,015,773 common shares.

For the three and nine months ended September 30, 2023, we declared and paid dividends in United States dollars totaling $10.6 million and $30.7 million, respectively (2022: $7.8 million and $22.6 million, respectively). For the three and nine months ended September 30, 2023, no shares were issued from treasury for participation in the Dividend Reinvestment Plan.

18

Condensed Consolidated Statements of Income (loss)

Three and nine months ended September 30, 2023 compared to three and nine months ended September 30, 2022

The following table presents summarized consolidated statements of income (loss) information for the three and nine months ended September 30, 2023 and 2022:

| | Three months ended | | Nine months ended | ||||||||

| | September 30 | | September 30 | ||||||||

($ thousands except share and per share information) |

| 2023 |

| 2022 |

| 2023 |

| 2022 | ||||

Revenue | | $ | 49,425 | | $ | 33,754 | | $ | 152,285 | | $ | 107,999 |

Cost of sales |

| | 23,616 | | | 14,034 | | | 76,656 | | | 45,453 |

Gross profit |

| | 25,809 | | | 19,720 | | | 75,629 |

| | 62,546 |

| | | | | | | | | | | | |

General administration costs |

| | 4,440 | | | 3,627 | | | 15,296 |

| | 11,084 |

Business development costs |

| | 991 | | | 694 | | | 3,346 |

| | 1,932 |

Impairment charges | | | 27,107 | | | — | | | 27,107 | | | — |

Expected credit losses | | | 974 | | | — | | | 974 | | | — |

Sustainability initiatives |

| | 206 | | | 255 | | | 428 |

| | 638 |

Operating income (loss) |

| | (7,909) | | | 15,144 | | | 28,478 |

| | 48,892 |

| | | | | | | | | | | | |

(Loss) gain on disposition of mineral interest |

| | — | | | — | | | (1,000) |

| | 2,099 |

(Decrease) increase in fair value of financial assets |

| | (798) | | | (307) | | | 1,901 |

| | (4,799) |

Finance costs, net |

| | (539) | | | (262) | | | (3,117) |

| | (1,241) |

Foreign currency translation loss |

| | (327) | | | (136) | | | (275) |

| | (289) |

Other expenses |

| | (1,664) | | | (705) | | | (2,491) |

| | (4,230) |

Earnings (loss) before income taxes |

| | (9,573) | | | 14,439 | | | 25,987 |

| | 44,662 |

Income tax recovery (expense) |

| | 3,532 | | | (1,624) | | | 540 |

| | (5,036) |

Net (loss) earnings | | $ | (6,041) | | $ | 12,815 | | $ | 26,527 | | $ | 39,626 |

Weighted average shares outstanding – basic | |

| 201,839,092 | | | 155,970,318 | | | 198,589,730 | |

| 156,003,665 |

Weighted average shares outstanding – diluted | |

| 201,839,092 | | | 155,970,318 | | | 198,814,120 | |

| 156,003,665 |

Earnings (loss) per share – basic and diluted | | $ | (0.03) | | $ | 0.08 | | $ | 0.13 | | $ | 0.25 |

Three months ended September 30, 2023 compared to three months ended September 30, 2022

Revenue was $49.4 million, an increase of 46% from $33.8 million for the same period in the prior year largely due to $12.1 million revenue from streams, royalties and related interests acquired pursuant to the Maverix acquisition, $2.8 million higher revenue due to higher silver prices, $2.2 million higher revenue due to higher gold prices, and $1.0 million higher revenue due to higher volume from streams and related interests, partially offset by $1.8 million lower revenue due to lower revenue from royalties, and $0.6 million lower revenue due to lower diamond prices. Higher revenue from streams and related interests was largely driven by higher deliveries from Northparkes, Buriticá, and Cerro Lindo.

Market gold price and gold sales volume for our streams were $1,928 per ounce and 7,475 ounces, respectively, compared to $1,729 per ounce and 7,199 ounces, respectively, in the prior year. Market silver price and silver sales volume were $23.57 per ounce and 790 thousand ounces, respectively, compared to $19.23 per ounce and 558 thousand ounces, respectively, in the prior year.

Cost of sales primarily represented the price of metals acquired under the stream agreement, non-cash cost of sales related to prepaid gold interests, as well as the depletion expense for streams and royalties, all of which are calculated based on units of metal sold or attributable royalty ounces. Cost of sales was $23.6 million (including depletion) from streams and related interests and royalties, compared to $14.0 million (including depletion) from streams and royalties for the same period in the prior year. The increase in cost of sales for the three months ended September 30, 2023 was largely due to cost of sales associated with streams, royalties and related

19

interests acquired pursuant to the Maverix acquisition and cost of sales associated with higher metal deliveries from streams and related interests.

Gross profit was $25.8 million, an increase of 31% from $19.7 million for the same period in the prior year. The increase was largely driven by gross profit from newly acquired assets pursuant to the Maverix acquisition, higher gross profit from the Cerro Lindo, Northparkes and Buriticá streams due to higher deliveries at higher metal prices, partially offset by lower gross profit from the ATO stream due to lower deliveries.

General administration costs were $4.4 million, compared to $3.6 million for the same period in the prior year. Higher costs for the three months ended September 30, 2023 were largely due to higher employee costs and higher office, insurance and other expenses driven by various public company costs, including directors’ and officers’ liability insurance costs relating to an increase in the number of directors and the US listing, and higher professional services as we continued to grow the business.

Business development costs were $1.0 million, compared to $0.7 million for the same period in the prior year. Business development costs represent ongoing business development costs incurred throughout the year including use of third-party service providers, net of costs capitalized, and costs reimbursed from our counterparties.

Impairment charges relate to the impairment of the Renard stream and receivables and the Beaufor royalty.

Expected credit loss provision was $974 thousand, compared to nil for the same period in the prior year. The expected credit loss represents the difference between the contractual cash flows that are due to the Company and the cash flows that management expects to receive discounted at the original effective interest rate.

For the three months ended September 30, 2023, expenditures on various sustainability initiatives were $206 thousand, compared to $255 thousand for the same period in the prior year.

Decrease in fair value of financial assets for the three months ended September 30, 2023 represents decrease in the fair value of our equity investments, partially offset by increase of fair value of the prepaid gold interests.

Finance costs, net were $0.5 million, compared to $0.3 million for the same period in the prior year. The finance costs largely reflect interest charges and standby fees on the Credit Facility, net of interest earned on bank deposits and loan receivables. Higher finance costs were driven by interest charges on a higher drawn balance of the Credit Facility.

Income tax recovery was $3.5 million, compared to income tax expense of $1.6 million for the same period in the prior year. The income tax recovery was driven by tax recovery associated with the impairment charges, increased general administration costs and business development costs, partially offset by sales mix.

Net loss was $6.0 million, compared to net income of $12.8 million for the same period in the prior year. Net loss was driven by impairment charges of $27.1 million, higher general administration costs, and expected credit loss provision related to our loan receivables, partially offset by higher gross profit.

Nine months ended September 30, 2023 compared to nine months ended September 30, 2022

Revenue was $152.3 million, an increase of 41% from $108.0 million for the same period in the prior year largely due to $39.3 million revenue from streams, royalties and related interests acquired pursuant to the Maverix acquisition, $6.9 million higher revenue due to higher volume from streams and related interests and $3.3 million higher revenue due to higher gold prices, $2.4 million higher revenue due to higher silver prices partially offset by $6.2 million lower revenue from royalties, and $1.5 million lower revenue due to lower diamond prices. Higher revenue from streams and related interests was largely driven by higher deliveries from ATO, Buriticá, and Northparkes, partially offset by lower deliveries from RBPlat. Lower revenue from royalties was driven by lower attributable ounces from Fosterville.

Market gold price and gold sales volume for our streams were $1,930 per ounce and 21,292 ounces, respectively, compared to $1,824 per ounce and 20,447 ounces, respectively, in the prior year. Market silver price and silver sales volume were $23.40 per ounce and 2.4 million ounces, respectively, compared to $21.92 per ounce and 1.8 million ounces, respectively, in the prior year.

20

Cost of sales primarily represented the price of metals acquired under the stream agreements, non-cash cost of sales related to prepaid gold interests, as well as the depletion expense for streams and royalties, all of which are calculated based on units of metal sold or attributable royalty ounces. Cost of sales was $76.7 million (including depletion) from streams and related interests and royalties, compared to $45.5 million (including depletion) from streams and royalties for the same period in the prior year. The increase in cost of sales for the nine months ended September 30, 2023 was largely due to cost of sales associated with streams, royalties and related interests acquired pursuant to the Maverix acquisition and cost of sales associated with higher metal deliveries from streams and related interests.

Gross profit was $75.6 million, an increase of 21% from $62.5 million for the same period in the prior year. The increase was largely driven by gross profit from newly acquired assets pursuant to the Maverix acquisition, higher gross profit from the Buriticá, Northparkes and Cerro Lindo streams due to higher deliveries at higher metal prices, partially offset by lower gross profit from Fosterville due to lower attributable ounces.

General administration costs were $15.3 million, compared to $11.1 million for the same period in the prior year. Higher costs for the nine months ended September 30, 2023 were largely due to higher employee costs and higher office, insurance and other expenses driven by various public company costs, including directors’ and officers’ liability insurance costs relating to an increase in the number of directors and the US listing, and higher professional services as we continued to grow the business.

Business development costs were $3.3 million, compared to $1.9 million for the same period in the prior year. Business development costs represent ongoing business development costs incurred throughout the year including use of third-party service providers, net of costs capitalized, and costs reimbursed from our counterparties.

Impairment charges relate to the impairment of the Renard stream and receivables and the Beaufor royalty.

Expected credit loss provision was $974 thousand, compared to nil for the same period in the prior year. The expected credit loss represents the difference between the contractual cash flows that are due to the Company and the cash flows that management expects to receive discounted at the original effective interest rate.

Sustainability initiatives represent costs incurred to acquire carbon offsets to counter our carbon footprint, which consists of not only the greenhouse gas emissions associated with our direct business activities, but also includes our share of emissions associated with production of our attributable metals by our counterparties, to the point of saleable metals. Sustainability initiatives also include funding of a bursary program in South Africa, community investments around Northparkes, and various social initiatives including donations and administration costs relating to the ESG program. For the nine months ended September 30, 2023, expenditures on various sustainability initiatives were $428 thousand, compared to $638 thousand for the same period in the prior year.

Loss on disposition of mineral interests of $1.0 million represents the loss on the Eastern Borosi NSR due to a buyback (“Eastern Borosi Buyback”) exercised by Calibre Mining Corp (“Calibre”). On April 18, 2023, Calibre announced that it had commenced mining at the Eastern Borosi open pit. 2022 included a gain of $2.1 million on the Talon royalty buydown.

Increase in fair value of financial assets for the nine months ended September 30, 2023 represents increase in the fair value of prepaid gold interests, partially offset by decrease in the fair value of our equity investments.

Finance costs, net were $3.1 million, compared to $1.2 million for the same period in the prior year. The finance costs largely reflect interest charges and standby fees on the Credit Facility, net of interest earned on bank deposits and loan receivables. Higher finance costs were driven by interest charges on a higher drawn balance of the Credit Facility.

Income tax recovery was $0.5 million, compared to expense of $5.0 million for the same period in the prior year. Income tax recovery was driven by tax recovery associated with the impairment charges, increased general administration costs and business development costs, partially offset by sales mix.

Net earnings were $26.5 million, compared to $39.6 million for the same period in the prior year. Lower net earnings in 2023 were driven by impairment charges of $27.1 million, higher general administration costs, higher business development costs, expected credit loss provision related to our loan receivables and higher finance costs, partially offset by higher gross profit. Net earnings in 2023 were

21

also impacted by a $1.0 million loss on disposition of mineral interests and an increase in fair value of financial assets of $1.9 million. Net earnings for the same period in the prior year included a gain of $2.1 million on disposition of mineral interests and a decrease in fair value of financial assets of $4.8 million.

Condensed Statements of Cash Flows

Three and nine months ended September 30, 2023 compared to three and nine months ended September 30, 2022

The following table presents summarized consolidated statements of cash flow information for the three and nine months ended September 30, 2023 and September 30, 2022:

| | Three months ended | | | Nine months ended | |||||||

| | September 30 | | | September 30 | |||||||

($ thousands) |

| 2023 | | 2022 | | 2023 |

| 2022 | ||||

Operating cash flow before working capital and taxes | | $ | 38,380 | | $ | 27,438 | | $ | 120,202 | | $ | 88,398 |

Income taxes paid | |

| (2,531) | | | (1,568) | | | (5,614) | |

| (5,053) |

Change in working capital | |

| 901 | | | (514) | | | 1,906 | |

| (1,690) |

Operating cash flow | |

| 36,750 | | | 25,356 | | | 116,494 | |

| 81,655 |

Net Cash used in investing activities | |

| (23,329) | | | (4,800) | | | (203,300) | |

| (10,961) |

Net Cash (used in) from financing activities | |

| (15,450) | | | (12,033) | | | 30,096 | |

| (28,334) |

Effect of exchange rate changes on cash and cash equivalents | |

| (66) | | | (251) | | | (45) | |

| (329) |

(Decrease) Increase in cash during the period | |

| (2,095) | | | 8,272 | | | (56,755) | |

| 42,031 |

Cash and cash equivalents at beginning of period | |

| 16,438 | | | 74,431 | | | 71,098 | |

| 40,672 |

Cash and cash equivalents at end of period | | $ | 14,343 | | $ | 82,703 | | $ | 14,343 | | $ | 82,703 |

Three months ended September 30, 2023 compared to three months ended September 30, 2022

Operating cash flow was $36.8 million, an increase of 45% from $25.4 million for the same period in the prior year. The increase was due to higher operating cash flow before working capital and taxes. Operating cash flow before working capital and taxes was $38.4 million, an increase of 40% from $27.4 million for the same period in the prior year. The increase was driven by higher cash flows from streams, royalties and related interests acquired pursuant to the Maverix acquisition, higher cash flows from streams, partially offset by higher general administration costs.

Net cash used in investing activities was $23.3 million for the three months ended September 30, 2023, compared to $4.8 million for the same period in the prior year. Net cash used in investing activities in the three months ended September 30, 2023 included $16.6 million for the acquisition of an additional royalty interest in Stawell, $3.4 million of funding for the Prieska royalty, and $3.3 million of long-term loans. Net cash used in investing activities for the same period in the prior year included $4.8 million of funding for the Steppe Gold Prepaid Gold Interest.

Net cash used in financing activities was $15.5 million for the three months ended September 30, 2023, compared to $12.0 million for the same period in the prior year. Net cash used in financing activities for the three months ended September 30, 2023, largely consisted of Credit Facility repayments of $15 million, dividend payments of $10.6 million, $3.2 million paid to purchase shares under the NCIB, as well as interest payments of $1.5 million, partially offset by $15 million of drawdown from the Credit Facility. Net cash used in financing activities for the same period in the prior year largely consisted of dividend payments of $7.8 million, $1.8 million paid to purchase shares under the NCIB, $1.8 million of costs relating to the extension of the Credit Facility, as well as interest payments of $0.5 million.

Nine months ended September 30, 2023 compared to nine months ended September 30, 2022

Operating cash flow was $116.5 million, an increase of 43% from $81.7 million for the same period in the prior year. The increase was due to higher operating cash flow before working capital and taxes. Operating cash flow before working capital and taxes was $120.2 million, an increase of 36% from $88.4 million for the same period in the prior year. The increase was driven by higher cash flows from interests acquired pursuant to the Maverix acquisition, higher cash flows from streams, partially offset by higher general administration and business development costs.

22