Table of Contents

(State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

Non-accelerated filer |

☒ | Smaller reporting company | ||||

| Emerging growth company | ||||||

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED APRIL 30, 2024

543,590 shares of Class A Common Stock

Issuable upon Exercise of Outstanding Warrants

This prospectus relates to the resale from time to time, by the selling shareholders identified in this prospectus under the caption “Selling Shareholders,” of up to 543,590 shares of our Class A common stock, $0.0001 par value per share (the “Class A Common Stock”), they may acquire upon the exercise of outstanding warrants, which we refer to as the “Common Warrants.” We issued the Common Warrants to the selling shareholders in a private placement which was completed on December 13, 2023. The Common Warrants have an exercise price of $11.24 per share, and are exercisable at any time beginning six months following their original issuance and will expire five and a half years from the original issuance date.

The selling shareholders may, from time to time, sell, transfer or otherwise dispose of any or all of their Class A Common Stock or interests in their Class A Common Stock on any stock exchange, market or trading facility on which the Class A Common Stock is traded or in private transactions. These dispositions may be at fixed prices, at prevailing market prices at the time of sale, at prices related to the prevailing market price, at varying prices determined at the time of sale, or at negotiated prices. See “Plan of Distribution” in this prospectus for more information. We will not receive any proceeds from the resale or other disposition of the shares of Class A Common Stock by the selling shareholders. However, we will receive the proceeds of any cash exercise of the Common Warrants. If all of the Common Warrants are exercised for cash, we will receive aggregate proceeds of approximately $6.1 million. See “Use of Proceeds” beginning on page 48 and “Plan of Distribution” beginning on page 107 of this prospectus for more information.

Our Class A Common Stock is listed on the New York Stock Exchange (the “NYSE”) under the symbol “BODI.” On April 29, 2024, the last reported sales price of our Class A Common Stock on the NYSE was $9.24 per share.

An investment in our securities involves a high degree of risk. Before deciding whether to invest in our securities, you should consider carefully the risks and uncertainties described in the section captioned “Risk Factors” beginning on page 11 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2024.

Table of Contents

TABLE OF CONTENTS

| Clause | Page | |||

| 1 | ||||

| 1 | ||||

| 4 | ||||

| 5 | ||||

| 10 | ||||

| 11 | ||||

| 48 | ||||

| 49 | ||||

| 50 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS OF BEACHBODY |

60 | |||

| 78 | ||||

| 85 | ||||

| 94 | ||||

| 96 | ||||

| 97 | ||||

| 100 | ||||

| 102 | ||||

| 104 | ||||

| 107 | ||||

| 110 | ||||

| 110 | ||||

| 110 | ||||

| 112 | ||||

| F-1 | ||||

| II-1 | ||||

| II-9 | ||||

You should rely only on the information contained in this prospectus. No one has been authorized to provide you with information that is different from that contained in this prospectus. This prospectus is dated as of the date set forth on the cover hereof. You should not assume that the information contained in this prospectus is accurate as of any date other than that date.

i

Table of Contents

TRADEMARKS

This document contains references to trademarks and service marks belonging to other entities. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of it by, any other companies.

SELECTED DEFINITIONS

Unless otherwise stated in this prospectus or the context otherwise requires, references to:

| • | “2021 Plan” are to the Beachbody Company, Inc. 2021 Incentive Award Plan; |

| • | “2023 Employment Inducement Incentive Award Plan” are to the Beachbody Company, Inc. 2023 Employment Inducement Incentive Award Plan; |

| • | “Beachbody” are to FRX after the Business Combination and its name change from Forest Road Acquisition Corp.; |

| • | “Exchange Act” are to the Securities Exchange Act of 1934, as amended; |

| • | “Business Combination” are to the transactions contemplated by that certain Agreement and Plan of Merger, dated as of February 9, 2021, by and among FRX, BB Merger Sub, LLC, a Delaware limited liability company and a direct, wholly owned subsidiary of FRX, Myx Merger Sub, LLC, a Delaware limited liability company and a direct, wholly owned subsidiary of FRX, The Beachbody Company Group, LLC, a Delaware limited liability company and Myx Fitness Holdings, LLC, a Delaware limited liability company; |

| • | “Bylaws” are to the Amended and Restated Bylaws of The Beachbody Company, Inc.; |

| • | “Certificate of Incorporation” are our second amended and restated certificate of incorporation, as amended; |

| • | “Class A Common Stock” are to shares of our Class A common stock, par value $0.0001 per share; |

| • | “Class X Common Stock” are to shares of our Class X common stock, par value $0.0001 per share; |

| • | “Company,” “we,” “us” and “our” are to FRX prior to the Business Combination and to Beachbody after the Business Combination and its change of name to The Beachbody Company, Inc.; |

| • | “common stock” are to our Class A Common Stock and Class X Common Stock, collectively; |

| • | “Common Warrants” are to the warrants to purchase up to 543,590 shares of our Class A Common Stock at an exercise price of $11.24, originally issued in connection with the offering; |

| • | “Continental” are to Continental Stock Transfer & Trust Company; |

| • | “DGCL” are to the General Corporation Law of the State of Delaware; |

| • | “ESPP” are to our 2021 Employee Stock Purchase Plan; |

| • | “Exchange Act” are to the Securities Exchange Act of 1934, as amended; |

| • | “FRX” or “Forest Road” are to Forest Road Acquisition Corp., prior to the Business Combination; |

| • | “GAAP” are to accounting principles generally accepted in the United States of America; |

| • | “JOBS Act” are to the Jumpstart Our Business Startups Act of 2012; |

1

Table of Contents

| • | “Management Awards” are to equity awards under the 2020 Plan in the form of restricted stock units expected to be granted to certain of our employees within 90 days following the Closing; |

| • | “NYSE” are to the New York Stock Exchange; |

| • | “Person” are to any individual, firm, corporation, partnership, limited liability company, incorporated or unincorporated association, joint venture, joint stock company, governmental authority or instrumentality or other entity of any kind; |

| • | “Pre-funded Warrants” are to the 122,821 warrants to purchase up to 122,821 shares of our Class A Common Stock at an exercise price of $0.0001 per share; |

| • | “Organizational Documents” are to the Certificate of Incorporation and the Bylaws; |

| • | “Private Placement” are to the issuance and sale of Common Warrants to purchase 543,590 shares of Class A Common Stock in a private placement to the selling shareholders; |

| • | “public shareholders” are to holders of public shares, whether acquired in FRX’s initial public offering or acquired in the secondary market; |

| • | “public shares” are to the FRX Class A ordinary shares, par value $0.0001 per share, (including those that underlie the units) that were offered and sold by FRX in its initial public offering and registered pursuant to the IPO registration statement or the shares of our common stock issued as a matter of law upon the conversion thereof at the time of the Business Combination, as context requires; |

| • | “public warrants” are to the redeemable warrants (including those that underlie the units) that were offered and sold by FRX in its initial public offering and registered pursuant to the IPO registration statement or the redeemable warrants of Beachbody issued as a matter of law upon the conversion thereof at the time of the Domestication, as context requires; |

| • | “redemption” are to each redemption of public shares for cash pursuant to the Organizational Documents; |

| • | “Registered Direct Offering” are to the issuance and sale of 420,769 shares of Class A Common Stock and Pre-funded Warrants to purchase up to an aggregate 122,821 shares of Class A Common Stock in a registered direct offering; |

| • | “Registration Rights Agreement” are to the Amended and Restated Registration Rights Agreement entered into by and among Beachbody, Forest Road Acquisition Sponsor LLC, a Delaware limited liability company, certain equity holders of The Beachbody Company Group, LLC and Carl Daikeler, Mary Conlin, John Salter, Michael Heller, Ben Van de Bunt and Kevin Mayer (collectively with Forest Road and the Beachbody Holders, the “Holders”) pursuant to which we were required to register for resale common shares held by the Holders; |

| • | “Reverse Stock Split” are to the 1-for-50 reverse stock split of our issued and outstanding common stock, effected on November 21, 2023; |

| • | “Sarbanes Oxley Act” are to the Sarbanes-Oxley Act of 2002; |

| • | “SEC” are to the United States Securities and Exchange Commission; |

| • | “Securities Act” are to the Securities Act of 1933, as amended; |

| • | “Sponsor” are to Forest Road Acquisition Sponsor LLC, a Delaware limited liability company; |

| • | “warrants” are to the public warrants, Common Warrants, warrants to purchase our Class A Common Stock originally issued to affiliates of Blue Torch Finance, LLC, warrants to purchase our Class A Common Stock, originally issued to Akron Supplement, LLC and Schwarzenegger Blind Trust in connection with the acquisition of Ladder, LLC, Pre-funded Warrants and warrants entitling the holder to purchase one share of our Class A Common Stock, originally issued in a private placement in connection with the initial public offering of FRX. |

2

Table of Contents

Additionally, when we refer to “Beachbody,” “BODi,” “we,” “our,” “us” and the “Company” in this prospectus, we mean The Beachbody Company, Inc. and its consolidated subsidiaries, unless otherwise specified. When we refer to “you,” we mean the potential holders of the Class A Common Stock offered hereby.

3

Table of Contents

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements within the meaning of Section 27A of the Securities Act, and Section 21E of the Exchange Act, including statements about the financial condition, results of operations, earnings outlook and prospects of BODi. Forward-looking statements are typically identified by words such as “plan,” “believe,” “expect,” “anticipate,” “intend,” “outlook,” “estimate,” “forecast,” “project,” “continue,” “could,” “may,” “might,” “possible,” “potential,” “predict,” “should,” “would” and other similar words and expressions, but the absence of these words does not mean that a statement is not forward-looking.

The forward-looking statements are based on our current expectations as applicable and are inherently subject to uncertainties and changes in circumstances and their potential effects and speak only as of the date of such statement. There can be no assurance that future developments will be those that have been anticipated. These forward-looking statements involve a number of risks, uncertainties or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to the following:

| • | our future financial performance, including our expectations regarding our revenue, cost of revenue, gross profit, operating expenses including changes in selling and marketing, general and administrative, and enterprise technology and development expenses (including any components of the foregoing), Adjusted EBITDA (as defined below) and our ability to achieve and maintain future profitability; |

| • | our anticipated growth rate and market opportunity; |

| • | our liquidity and ability to raise financing; |

| • | our success in retaining or recruiting, or changes required in, officers, key employees or directors; |

| • | other than the Pre-funded Warrants, our warrants are accounted for as liabilities and changes in the value of such warrants could have a material effect on our financial results; |

| • | our ability to effectively compete in the fitness and nutrition industries; |

| • | our ability to successfully acquire and integrate new operations; |

| • | our reliance on a few key products; |

| • | market conditions and global and economic factors beyond our control; |

| • | intense competition and competitive pressures from other companies worldwide in the industries in which we will operate; |

| • | litigation and the ability to adequately protect our intellectual property rights; and |

| • | other risks and uncertainties set forth in this prospectus under the heading “Risk Factors.” |

Should one or more of these risks or uncertainties materialize or should any of the assumptions made by management prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements.

You should not place undue reliance upon our forward-looking statements.

Except to the extent required by applicable law or regulation, we undertake no obligation to update these forward-looking statements to reflect events or circumstances after the date of this prospectus or to reflect the occurrence of unanticipated events.

4

Table of Contents

SUMMARY

This summary highlights selected information from this prospectus and may not contain all of the information that is important to you in making an investment decision. Before investing in our securities, you should carefully read this entire prospectus, including our financial statements and the related notes included in this prospectus and the information set forth under the headings “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” See also the section entitled “Where You Can Find Additional Information.”

Unless context otherwise requires, references in this prospectus to “Beachbody,” “BODi,” the “Company,” “we,” “us” or “our” refer to the business of The Beachbody Company, Inc. and its consolidated subsidiaries.

The Company

BODi is a leading subscription health and fitness company. We focus primarily on digital content, supplements, connected fitness, and consumer health and wellness. Our goal is to continue to provide holistic health and wellness content and subscription-based solutions. We are the creator of some of the world’s most popular fitness programs, including P90X, Insanity, and 21 Day Fix, which transformed the at-home fitness market and disrupted the global fitness industry by making it accessible for people to get results—anytime, anywhere. Our comprehensive nutrition-first programs, Portion Fix and 2B Mindset, teach healthy eating habits and promote healthy, sustainable weight loss. These fitness and nutrition programs are available through our Beachbody On Demand (“BOD”) and Beachbody On Demand Interactive (“BODi”) streaming services.

We offer nutritional products such as Shakeology nutrition shakes, BEACHBAR snack bars, and Ladder premium supplements as well as a commercial-grade stationary cycle with or without a 360-degree touch screen tablet and connected fitness software. Leveraging our history of fitness content creation, nutrition innovation, and our network of micro-influencers, whom we call “Partners”, we plan to continue market penetration into the health and wellness markets to reach a wider health, wellness and fitness audience.

Our revenue is generated primarily through our network of Partners, social media marketing channels, and direct response advertising. Components of revenue include recurring digital subscription revenue, revenue from the sale of nutritional and other products, and connected fitness revenue. In addition to selling individual products on a one-time basis, we bundle digital and nutritional products together at discounted prices.

Corporate Information

We were incorporated under the name “Forest Road Acquisition Corp.” on September 24, 2020 as a Delaware corporation for purposes of effecting a merger, share exchange, asset acquisition, share purchase, reorganization or similar business combination with one or more businesses. On June 25, 2021, we changed our name to “The Beachbody Company, Inc.”

Our principal executive office is located at 400 Continental Blvd, Suite 400, El Segundo, California 90245. Our telephone number is (310) 883-9000. Our website address is www.beachbody.com. Information contained on our website is not a part of this prospectus, and the inclusion of our website address in this prospectus is an inactive textual reference only.

Recent Developments

2023 Equity Offering

On December 10, 2023, the Company entered into a securities purchase agreement for the issuance and sale of 420,769 shares of Class A Common Stock at a purchase price of $9.75 per share and pre-funded warrants to

5

Table of Contents

purchase up to 122,821 shares of Class A Common Stock at a pre-funded purchase price of $9.7499 per share and an exercise price of $0.0001 per share with certain institutional investors in a registered direct offering. The Company received proceeds of $4.9 million, net of placement agent fees. The Company also issued 543,590 Common Warrants to purchase 543,590 shares of Class A Common Stock at an exercise price of $11.24 per share in a concurrent private placement (collectively, the “Registered Direct Offering”). On January 12, 2024, the investor exercised all of the pre-funded warrants and converted them into 122,821 shares of the Company’s Class A Common Stock.

Reverse Stock Split

On November 21, 2023, we effected a 1-for-50 reverse stock split of our issued and outstanding common stock. The reverse stock split did not change the authorized number of shares or the par value of our common stock or preferred stock, but did effect a proportional adjustment to the number of shares of common stock outstanding, per share exercise price and the number of shares of common stock issuable upon the exercise of outstanding stock options, the number of shares of common stock issuable upon the vesting of restricted stock awards (“RSU’s”), the number of shares of common stock under the Employee Stock Purchase Plan (the “ESPP”), the conversion rate of our outstanding warrants into common stock and the number of shares of common stock eligible for issuance under our 2021 Stock Plan (the “2021 Plan”).

Goodwill and Intangible Asset Impairment

Our annual goodwill impairment test, which was performed as of December 31, 2023, determined that our goodwill was impaired and we recorded goodwill impairment of $40.0 million in the year ended December 31, 2023. We also determined as of December 31, 2023 that our intangible assets were impaired and we recorded an intangible asset impairment of $3.1 million in the year ended December 31, 2023.

Impairment and Sale of Investment

In December 2023, the Company recorded a $4.0 million impairment on its $5.0 million investment in equity securities of a privately-held company based on an observable price change. The Company sold this investment on January 9, 2024 for $1.0 million and made a partial prepayment on the Term Loan (as defined below) of $1.0 million. On January 9, 2024 (the “Consent Effective Date”), the Company and Blue Torch entered into Consent No. 1 and Amendment No. 3 to the Financing Agreement (the “Third Amendment”), which among other things, amended the minimum liquidity financial covenant.

Sale/Leaseback of Property

On February 29, 2024, we sold our Van Nuys production facility which had a net carrying value of $4.8 million at December 31, 2023, for $6.2 million. Simultaneous with the sale we entered into a five year lease of the facility at an annual base rate of $0.3 million per year. The Company used the proceeds received from the sale to make a partial prepayment of $5.5 million on the Term Loan. On February 29, 2024, the Company and Blue Torch entered into Consent No. 2 and Amendment No. 4 to the Financing Agreement (the “Fourth Amendment”), which among other things, amended the minimum liquidity financial covenant.

2024 Restructuring

In January 2024, the Company executed cost-reduction initiatives intended to streamline the business. These actions are expected to result in approximately $1.7 million in costs consisting primarily of termination benefits during the first quarter of 2024.

6

Table of Contents

Amendment to Financing Agreement and Blue Torch Warrants

On April 5, 2024, the Company and Blue Torch entered into Amendment No. 5 to the Financing Agreement (the “Fifth Amendment”), which among other things, amended the minimum revenue financial covenant and the minimum liquidity financial covenant. In connection with the Fifth Amendment, the Company also amended and restated the warrants to purchase 97,482 shares of the Company’s Class A Common Stock, originally issued to affiliates of Blue Torch (the “Blue Torch Warrants”) (the “Warrant Second Amendment”). The Warrant Second Amendment amends the exercise price of the warrants from $20.50 per share of Class A Common Stock to $9.16 per share.

Risk Factors

Summary of Risk Factors

| • | If we are unable to anticipate and satisfy consumer preferences and shifting views of health, fitness and nutrition, our business may be adversely affected. |

| • | If we are unable to sustain pricing levels for our products and services, our business could be adversely affected. |

| • | Our success depends on our ability to maintain the value and reputation of our brands. |

| • | The perception of the effects or value of our products may change over time, which could reduce customer demand. |

| • | We may not successfully execute or achieve the expected benefits of our strategic alignment initiatives and other cost-saving measures we may take in the future, and our efforts may result in further actions and/or additional asset impairment charges and adversely affect our business. |

| • | Our marketing strategy relies on the use of social media platforms and any negative publicity on such social media platforms may adversely affect the public perception of our brand, and changing terms or conditions or ways in which advertisers use their platforms may adversely affect our ability to engage with customers. |

| • | We may be unable to attract and retain customers, which would materially and adversely affect our business, results of operations and financial condition. |

| • | Our customers use their connected fitness products and fitness accessories to track and record their workouts. If our products fail to provide accurate metrics and data to our customers, our brand and reputation could be harmed and we may be unable to retain our customers. |

| • | Our business relies on sales of a few key products. |

| • | If there are any material delays or disruptions in our supply chain, or errors in forecasting of the demand for our products and services, our business may be adversely affected. |

| • | The failure or inability of our contract manufacturers to comply with the specifications and requirements of our products could result in product recall, which could adversely affect our reputation and subject us to significant liability should the consumption of any of our products cause or be claimed to cause illness or physical harm. |

| • | If any of our products are unacceptable to us or our customers, or any other change in the competitive landscape and activities of our competitors, our business could be harmed. |

| • | Our business model relies on high quality customer service, and any negative impressions of our customer service experience may adversely affect our business and result in harm to our reputation. |

7

Table of Contents

| • | The seasonal nature of our business could cause operating results to fluctuate. |

| • | If we fail to obtain and retain high-profile strategic relationships, or if the reputation of any of these parties is impaired, our business may suffer. |

| • | Our co-founder has control over all stockholder decisions because he controls a substantial majority of our voting power through “super” voting stock. |

| • | Our financing agreement restricts our current and future operations and our ability to engage in certain business and financial transactions and may adversely affect our business. |

| • | Our ability to generate the significant amount of cash needed to pay interest and principal on our indebtedness and our ability to refinance all or a portion of our indebtedness or obtain additional financing depends on many factors beyond our control. |

| • | There can be no assurance that we can further penetrate existing markets or that we can successfully expand our business into new markets. |

| • | We may expand into international markets, which would expose us to significant risks. |

| • | The price of shares of our Class A Common Stock may experience volatility and the market price of our Class A Common Stock after this offering may drop below the price you pay. |

| • | You may experience future dilution as a result of future equity offerings or other equity issuances. |

| • | The number of shares of our Class A Common Stock available for future issuance or resale could adversely affect the market price of our Class A Common Stock. |

| • | Because we do not expect to declare cash dividends on our Class A Common Stock in the foreseeable future, shareholders must rely on appreciation of the value of our Class A Common Stock for any return on their investment. |

| • | We depend on our senior management team and other key employees, and the loss of one or more key personnel or an inability to attract, hire, integrate and retain highly skilled personnel could have an adverse effect on our business, financial condition and results of operations. |

| • | We collect, store, process, and use personal information and other customer data which subjects us to legal obligations and laws and regulations related to data security and privacy, and any actual or perceived failure to meet those obligations could harm our business. |

| • | Any major disruption or failure of our information technology systems or websites, or our failure to successfully implement upgrades and new technology effectively, could adversely affect our business and operations. |

| • | If we suffer a security breach or otherwise fail to properly maintain the confidentiality and integrity of our data, including customer credit card, debit card and bank account information, our reputation and business could be materially and adversely affected. |

| • | We face risks, such as unforeseen costs and potential liability in connection with allegations of injuries arising from equipment we supply and content we produce, license, advertise, and distribute through our various content delivery platforms. |

| • | Our nutritional products must comply with regulations of the Food and Drug Administration, (“FDA”), as well as state, local and applicable international regulations. Any non-compliance with the FDA or other applicable regulations could harm our business. |

8

Table of Contents

| • | Our network of micro-influencers, whom we call “Partners”, could be found not to be in compliance with current or newly adopted laws or regulations in one or more markets, which could have a material adverse effect on our business. |

| • | Our products or services offered as part of automatically renewing subscriptions or memberships could be found not to be in compliance with laws or regulations in one or more markets, which could have a material adverse effect on our business. |

| • | Our BODi Bikes and other products may be subject to warranty claims, recalls or intellectual property disputes that could result in significant direct or indirect costs, each of which could have an adverse effect on our business, financial condition, and results of operations. |

9

Table of Contents

THE OFFERING

This prospectus relates to the resale or other disposition from time to time by the selling shareholders identified in this prospectus of up to 543,590 shares of Class A Common Stock issuable upon exercise of the Common Warrants. None of the shares registered hereby are being offered for sale by us.

| Class A Common Stock offered by the selling shareholders |

Up to 543,590 shares of Class A Common Stock issuable upon exercise of the Common Warrants. |

| Common stock to be outstanding after the offering |

7,411,854 shares, assuming the exercise in full of the Common Warrants. |

| Use of Proceeds |

We will receive the proceeds of any cash exercise of the Common Warrants. We intend to use the net proceeds from any cash exercise of the Common Warrants for working capital and general corporate purposes. We will not receive any proceeds from the resale or other disposition of the shares of Class A Common Stock offered by the selling shareholders under this prospectus. See “Use of Proceeds.” |

| Risk Factors |

Investing in our securities involves a high degree of risk. You should carefully read and consider the information set forth under the heading “Risk Factors” beginning on page 11 of this prospectus and the information disclosed in “Risk Factors” in the Company’s most recent Annual Report on Form 10-K and our subsequent Quarterly Reports on Form 10-Q, as well as the other information set forth in our other filings under the Exchange Act that are incorporated herein by reference, before making a decision to invest in our securities. |

| Listing |

Our Class A Common Stock is traded on the NYSE under the trading symbol “BODI.” |

The number of shares of our common stock to be outstanding immediately after this offering and, unless otherwise indicated, the information in this prospectus supplement, is based on 4,139,261 shares of Class A Common Stock and 2,729,003 shares of Class X Common Stock issued and outstanding as of April 15, 2024, and excludes as of that date:

| • | 452,004 shares of Class A Common Stock reserved for future issuance under the Company’s benefit plans, including the Company’s Amended and Restated 2020 Equity Compensation Plan, the Company’s 2021 Incentive Award Plan, the Company’s 2021 Employee Stock Purchase Plan and the Company’s 2023 Employment Inducement Incentive Award Plan; |

| • | 1,547,826 shares of Class A Common Stock issuable upon the exercise of outstanding options, settlement of outstanding restricted stock units and exercise or settlement of any other rights to purchase or otherwise acquire shares of Class A Common Stock (other than options or rights reserved for issuance under the Company’s benefit plans, which are included above); and |

| • | 483,761 shares of Class A Common Stock issuable pursuant to the Company’s outstanding warrants other than the Common Warrants. |

Except as otherwise indicated, all information in this prospectus supplement assumes (i) no exercise or conversion of the outstanding options or warrants described above; (ii) all of the Pre-funded Warrants previously issued are exercised; and (iii) all of the Common Warrants are exercised.

10

Table of Contents

RISK FACTORS

An investment in our securities involves a high degree of risk. You should carefully consider the risks described below before making an investment decision. Our business, prospects, financial condition, or operating results could be harmed by any of these risks, as well as other risks not currently known to us or that we currently consider immaterial. The trading price of our securities could decline due to any of these risks, and, as a result, you may lose all or part of your investment.

In the course of conducting our business operations, we are exposed to a variety of risks. These risks are generally inherent to the fitness industry or otherwise generally impact companies like us. Any of the risk factors we describe below have affected or could materially adversely affect our business, financial condition and results of operations. The market price of shares of our common stock could decline, possibly significantly or permanently, if one or more of these risks and uncertainties occurs. Certain statements in “Risk Factors” are forward-looking statements. See “Cautionary Note Regarding Forward-Looking Statements.”

Risks Related to Our Business and Industry

If we are unable to anticipate and satisfy consumer preferences and shifting views of health, fitness and nutrition, our business may be adversely affected.

The fitness industry is highly susceptible to changes in consumer preferences. Our success depends on our ability to anticipate and satisfy consumer preferences relating to health, fitness and nutrition. Our business is, and all of our workouts and products are, subject to changing consumer preferences that cannot be predicted with certainty. Consumers’ preferences for health and fitness services and products, including the technology through which they consume these services and products, could shift rapidly to offerings different from what we offer, and we may be unable to anticipate and respond to such shifts in consumer preferences. It is also possible that competitors could introduce new products, services and/or technologies that negatively impact consumer preference for our workouts and products. In addition, developments or shifts in research or public opinion on the types of workouts and products we provide could negatively impact our business. Even if we are successful in anticipating consumer preferences, our ability to adequately react to and address those preferences will in part depend upon our continued ability to develop and introduce innovative, high-quality health and fitness services. Our failure to effectively introduce new health and fitness services that are accepted by consumers could result in a decrease in revenue, which could have a material adverse effect on our financial condition and adversely impact our business.

The perception of the effects of our nutritional products may change over time, which could reduce customer demand.

A substantial portion of our revenues is derived from our Shakeology line of products. We believe that these nutritional products have, or are perceived to have, positive effects on health, and compete in a market that relies on innovation and evolving consumer preferences. However, the nutritional industry is subject to changing consumer trends, demands and preferences. Additionally, the science underlying nutritious foods and dietary supplements is constantly evolving. Therefore, products once considered healthy may over time become disfavored by consumers or no longer be perceived as healthy. Trends within the food industry change often and our failure to anticipate, identify or react to changes in these trends could, among other things, lead to reduced consumer demand and spending reductions, and could adversely impact our business, financial condition and results of operations. Additionally, ingredients used in our products may become negatively perceived by consumers, resulting in reformulation of existing products to remove such ingredients, which may negatively affect taste or other qualities. Factors that may affect consumer perception of nutritional products include dietary trends and attention to different nutritional aspects of foods, concerns regarding the health effects of specific ingredients and nutrients, trends away from specific ingredients in products and increasing awareness of the environmental and social effects of product production. For example, conflicting scientific information on what

11

Table of Contents

constitutes good nutrition, diet trends and other weight loss trends may also adversely affect our business from time to time. Our success depends, in part, on our ability to anticipate the tastes and dietary habits of consumers and other consumer trends and to offer nutritional products that appeal to their needs and preferences on a timely and affordable basis. Failure to do so could have a material adverse effect on our financial condition and adversely impact our business.

We rely on consumer discretionary spending, which may be adversely affected by economic downturns and other macroeconomic conditions or trends.

Our business and operating results are subject to global economic conditions and their impact on consumer discretionary spending. Some of the factors that may negatively influence consumer spending include high levels of unemployment, higher consumer debt levels, reductions in net worth, declines in asset values and related market uncertainty, home foreclosures and reductions in home values, fluctuating interest rates and credit availability, fluctuating fuel and other energy costs, fluctuating commodity prices and general uncertainty regarding the overall future of the political and economic environment. Consumer purchases of discretionary items generally decline during periods of economic uncertainty, when disposable income is reduced or when there is a reduction in consumer confidence. If consumer purchases of subscriptions and products decline, our revenue may be adversely affected.

For example, the outbreak of COVID-19 has led to an increase in at-home gyms and workouts which has in turn led to an increase in our consumers, a trend which may be negatively impacted as commercial and office gyms continue to reopen. The ultimate severity of the coronavirus outbreak and distribution and vaccine inoculation results are uncertain at this time and therefore we cannot predict the full impact it may have on our end markets or operations; however, the effect on our results could be material and adverse. Any significant or prolonged decrease in consumer spending on fitness or nutritional products could adversely affect the demand for our offerings, reducing our cash flows and revenues, and thereby materially harming our business, financial condition, results of operations and prospects.

Further, COVID-19 has had an adverse impact on global supply chains, resulting in an increased uncertainty in shipping lead times as well as increased import and logistics costs. However, if a significant percentage of consumers return to the gym and do not continue at-home fitness, or consumer sentiment shifts from prioritizing health and fitness, or import and logistics costs continue to increase, our business, financial condition, results of operations and prospects may be adversely affected.

If we are unable to sustain pricing levels for our products and services, our business could be adversely affected.

If we are unable to sustain pricing levels for our products and services, including our nutritional products, digital services and connected fitness products, whether due to competitive pressure or otherwise, our revenue and gross margins could be significantly reduced. In particular, we may not be able to increase prices to offset the impact of inflation on our costs. Further, our decisions around the development of new ancillary products and services are grounded in assumptions about eventual pricing levels. If there is price compression in the market after these decisions are made, it could have a negative effect on our business.

Our success depends on our ability to maintain the value and reputation of our brands.

We believe that our brands are important to attracting and retaining customers. Maintaining, protecting, and enhancing our brands depends largely on the success of our marketing efforts, ability to provide consistent, high-quality products, services, features, content, and support, and our ability to successfully secure, maintain, and defend our rights to use our trademarks, logos and other intellectual property important to our brands. We believe that the importance of our brands will increase as competition further intensifies and brand promotion activities may require substantial expenditures. Our brands could be harmed if we fail to achieve these objectives

12

Table of Contents

or if our public image were to be tarnished by negative publicity. Unfavorable publicity about us, including our products, services, technology, subscriber service, content, personnel, industry, distribution and/or marketing channel, and suppliers could diminish confidence in, and the use of, our products and services. Such negative publicity also could have an adverse effect on the size, engagement and loyalty of our customer base and result in decreased revenue, which could have an adverse effect on our business, financial condition, and operating results.

Adverse publicity associated with our products, ingredients or network marketing program, or those of similar companies, could adversely affect our business.

The size of our distributor base and the results of our operations may be significantly affected by the perception of our company and similar companies. This perception is dependent upon opinions concerning:

| • | the safety and quality of our products and nutritional supplement ingredients; |

| • | the safety and quality of similar products and ingredients distributed by other companies; |

| • | our distributors; |

| • | publicity concerning network marketing; and |

| • | the direct selling business generally. |

Adverse publicity concerning any actual or purported failure of our Company or our distributors to comply with applicable laws and regulations regarding product claims and advertising, good manufacturing practices, the regulation of our network marketing business, the licensing of our products for sale in our target markets, or other aspects of our business, whether or not resulting in enforcement actions or the imposition of penalties, could have an adverse effect on the goodwill of our Company and could negatively affect our ability to attract, motivate and retain distributors, which would have a material adverse effect on our ability to generate revenue. We cannot ensure that all distributors will comply with applicable legal requirements relating to the advertising, sale, labeling, licensing or distribution of our products or promotion of the income opportunity.

In addition, our distributors’ and consumers’ perception of the safety and quality of our products and ingredients as well as similar products and ingredients distributed by other companies can be significantly influenced by national media attention, publicized scientific research or findings, widespread product liability claims and other publicity concerning our products or ingredients or similar products and ingredients distributed by other companies. Adverse publicity, whether or not accurate or resulting from consumers’ use or misuse of our products, that associates consumption of our products or ingredients or any similar products or ingredients with illness or other adverse effects, questions the benefits of our or similar products or claims that any such products are ineffective, inappropriately labeled or have inaccurate instructions as to their use, could have a material adverse effect on our reputation or the market demand for our products.

We may not successfully execute or achieve the expected benefits of our strategic alignment initiatives and other cost-saving measures we may take in the future, and our efforts may result in further actions and/or additional asset impairment charges and adversely affect our business.

Beginning in early 2022 and continuing in 2023, we executed cost reduction activities intended to streamline the business and strategically align operations, including multiple reductions in headcount. Our strategic alignment initiatives were intended to address the short-term health of our business as well as our long-term objectives based on our current estimates, assumptions and forecasts, which are subject to known and unknown risks and uncertainties, including whether we have targeted the appropriate areas for our cost-saving efforts and at the appropriate scale, and whether, if required in the future, we will be able to appropriately target any additional areas for our cost-saving efforts. As such, the actions we intended to take under the strategic alignment initiatives and that we may decide to take in the future may not be successful in yielding our intended results and may not appropriately address either or both of the short-term and long-term strategy for our business.

13

Table of Contents

Additionally, implementation of the strategic alignment initiatives and any other cost-saving initiatives may be costly and disruptive to our business, the expected costs and charges may be greater than we have forecasted, and the estimated cost savings may be lower than we have forecasted. In addition, our initiatives could result in personnel attrition beyond our planned reductions in headcount or reduce employee morale, which could in turn adversely impact productivity, including through a loss of continuity, loss of accumulated knowledge and/or inefficiency during transitional periods, or our ability to attract highly skilled employees. Unfavorable publicity about us or any of our strategic initiatives, including our strategic alignment initiatives, could result in reputation harm and could diminish confidence in, and the use of, our products and services. The strategic alignment initiatives have required, and may continue to require, a significant amount of management’s and other employees’ time and focus, which may divert attention from effectively operating and growing our business. We also cannot assure you that it will impact our ability to achieve or maintain profitability.

Our marketing strategy relies on the use of social media platforms and any negative publicity on such social media platforms may adversely affect the public perception of our brand, and changing terms or conditions or ways in which advertisers use their platforms may adversely affect our ability to engage with customers, both of which in turn could have a material and adverse effect on our business, results of operations and financial condition. In addition, our use of social media could subject us to fines or other penalties.

We rely on social media marketing through various social media platforms, such as Instagram, YouTube and Facebook, as a means to engage with our existing customers as well as attract new customers. Existing and new customers alike interact with the brand both organically, through posts by the BODi community, as well as through distributors via their own social media accounts. While the use of social media platforms allows us access to a broad audience of consumers and other interested persons, our use of, and reliance on, social media as a key marketing tool exposes us to significant risk of widespread negative publicity. Social media users generally have the ability to post information to social media platforms without filters or checks on accuracy of the content posted. Information concerning the Company or its many brands may be posted on such platforms at any time. Such information may be adverse to our interests or may be inaccurate, each of which can harm our reputation and value of our brands. The harm may be immediate without affording us an opportunity for redress or correction. In addition, social media platforms provide users with access to such a broad audience that collective action against our products and offerings, such as boycotts, can be more easily organized. If such actions were organized, we could suffer reputational damage. Social media platforms may be used to attack us, our information security systems, including through use of spam, spyware, ransomware, phishing and social engineering, viruses, worms, malware, distributed denial of service attacks, password attacks, “Man in the Middle” attacks, cybersquatting, impersonation of employees or officers, abuse of comments and message boards, fake reviews, doxing and swatting. As such, the dissemination of information on social media platforms and other online platforms could materially and adversely affect our business, results of operations and financial condition, regardless of the information’s accuracy.

Our reliance on social media platforms for advertising also subjects us to the risk that any change to the platforms’ algorithms, terms and conditions and/or ways in which advertisers may advertise on their platforms may adversely affect our ability to effectively engage with customers and sell our products, which in turn could have a material and adverse effect on our business, results of operations and financial condition.

In addition, our use of social media platforms as a marketing tool could also subject us to fines or other penalties. As laws and regulations, including those from the Federal Trade Commission, State Attorneys General, and other enforcement agencies rapidly evolve to govern the use of these platforms, the failure by us, our distributors, influencers, or other third parties acting at our direction to abide by applicable laws and regulations in the use of these platforms could materially and adversely impact our business, results of operations and financial condition or subject us to fines or other penalties.

14

Table of Contents

We may be unable to attract and retain customers, which would materially and adversely affect our business, results of operations and financial condition.

The success of our business depends on our ability to attract and retain customers. Our marketing efforts may not be successful in attracting customers, and membership levels may materially decline over time. Customers may cancel their membership at any time. In addition, we experience attrition, and we must continually engage existing customers and attract new customers in order to maintain membership levels. Some of the factors that could lead to a decline in membership levels include, among other factors:

| • | changing desires and behaviors of consumers or their perception of our brand; |

| • | changes in discretionary spending trends; |

| • | market maturity or saturation; |

| • | a decline in our ability to deliver quality service at a competitive price; |

| • | a failure to introduce new features, products or services that customers find engaging; |

| • | the introduction of new products or services, or changes to existing products and services, that are not favorably received; |

| • | technical or other problems that affect the customer experience; |

| • | an increase in membership fees due to inflation; |

| • | direct and indirect competition in our industry; |

| • | a decline in the public’s interest in health and fitness; and |

| • | a general deterioration of economic conditions or a change in consumer spending preferences or buying trends. |

Any decrease in our average fees or higher membership costs may materially and adversely impact our results of operations and financial condition. Additionally, further expansion into international markets may create new challenges in attracting and retaining customers that we may not successfully address, as these markets carry unique risks as discussed below. As a result of these factors, we cannot be certain that our membership levels will be adequate to maintain or permit the expansion of our operations. A decline in membership levels would have an adverse effect on our business, results of operations and financial condition.

Our customers use their connected fitness products and fitness accessories to track and record their workouts. If our products fail to provide accurate metrics and data to our customers, our brand and reputation could be harmed, and we may be unable to retain our customers.

Our customers use their connected fitness products and fitness accessories to track and record certain metrics related to their workouts. Examples of metrics tracked on our platform currently include heartrate and calories burned. These metrics assist our customers in tracking their fitness journeys and understanding the effectiveness of their workouts. We anticipate introducing new metrics and features in the future. If the software used in our connected fitness products or on our platform malfunctions and fails to accurately track, display, or record customers workouts and metrics, we could face claims alleging that our products and services do not operate as advertised. Such reports and claims could result in negative publicity, product liability claims, and, in some cases, may require us to expend time and resources to refute such claims and defend against potential litigation. If our products and services fail to provide accurate metrics and data to our customers, or if there are reports or claims of inaccurate metrics and data or claims of inaccuracy regarding the overall health benefits of our products and services in the future, we may become the subject of negative publicity, litigation, regulatory proceedings, and warranty claims, and our brand, operating results, and business could be harmed.

15

Table of Contents

Our business relies on sales of a few key products.

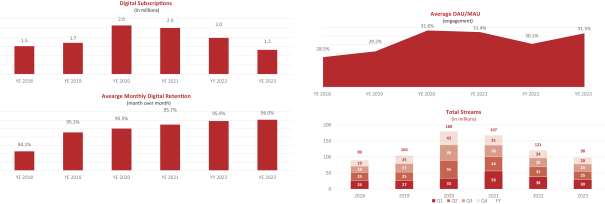

Our digital platforms which provide recurring subscription revenue also provide a significant portion of our revenue, accounting for approximately 49% of revenue for the year ended December 31, 2023. Our nutrition products also constitute a significant portion of our revenue, accounting for approximately 47% of revenue for the year ended December 31, 2023, and Shakeology, our premium nutrition shake, specifically constitutes a significant portion of our revenue, accounting for approximately 20% of revenue for the year ended December 31, 2023. If consumer demand for these products decreases significantly or we cease offering these products without a suitable replacement, our operations could be materially adversely affected. Despite these efforts, our financial performance currently remains dependent on a few products. Any significant diminished consumer interest in these products would adversely affect our business. We could also experience adverse financial consequences if we fail to sustain market interest in our BODi Bike business, which accounted for approximately 4% of revenue for the year ended December 31, 2023. We may not be able to develop successful new products or implement successful enhancements to existing products. Any products that we do develop or enhance may not generate sufficient revenue to justify the cost of developing and marketing these products.

We operate in highly competitive markets and we may be unable to compete successfully against existing and future competitors.

Our products and services are offered in a highly competitive market. We face significant competition in every aspect of our business, including at-home fitness equipment and content, fitness clubs, nutritional products, dietary supplements, and health and wellness apps. Moreover, we expect the competition in our market to intensify in the future as new and existing competitors introduce new or enhanced products and services that compete with ours.

Our competitors may develop, or have already developed, products, features, content, services, or technologies that are similar to ours or that achieve greater acceptance, may undertake more successful product development efforts, create more compelling employment opportunities, or marketing campaigns, or may adopt more aggressive pricing policies. Our competitors may develop or acquire, or have already developed or acquired, intellectual property rights that significantly limit or prevent our ability to compete effectively in the public marketplace. In addition, our competitors may have significantly greater resources than us, allowing them to identify and capitalize more efficiently upon opportunities in new markets and consumer preferences and trends, quickly transition and adapt their products and services, devote greater resources to marketing, advertising and research and development, or be better positioned to withstand substantial price competition. If we are not able to compete effectively against our competitors, they may acquire and engage customers or generate revenue at the expense of our efforts, which could have an adverse effect on our business, financial condition, and operating results. The business of marketing nutritional products is highly competitive and sensitive to the introduction of new products, including various prescription drugs, which may rapidly capture a significant share of the market. These market segments include numerous manufacturers, distributors, marketers, retailers and physicians that actively compete for the business of consumers both in the United States and abroad. In addition, we anticipate that we will be subject to increasing competition in the future from large electronic commerce sellers. Some of these competitors have significantly greater financial, technical, product development, marketing and sales resources, greater name recognition, larger established subscriber bases, and better-developed distribution channels than we do. Our present or future competitors may be able to develop products that are comparable or superior to those we offer, adapt more quickly than we do to new technologies, evolving industry trends and standards or subscriber requirements, or devote greater resources to the development, promotion and sale of their products than we do. Accordingly, we may not be able to compete effectively in our markets and competition may intensify.

We are also subject to competition for the recruitment of distributors from other organizations, including those that market nutritional products, dietary and nutritional supplements, and personal care products as well as other types of products. Our ability to remain competitive depends, in part, on our success in recruiting and retaining Partners through an attractive compensation plan, the maintenance of an attractive product portfolio,

16

Table of Contents

and other incentives. We cannot ensure that our programs for recruitment and retention efforts will be successful, or that we will be able to continue to offer the same compensation plans to our Partners. We have recently changed the compensation plan for our Partners and such changes, and any future changes, may have an adverse effect on our relationships with our current Partners and our ability to recruit new Partners.

We compete with other direct selling organizations, some of which have longer operating histories and higher visibility, name recognition and financial resources. The Company competes for new Partners on the basis of the culture, premium quality products and compensation plan. We envision the entry of many more direct selling organizations into the marketplace as this channel of distribution expands. There can be no assurance that the Company will be able to successfully meet the challenges posed by increased competition.

We also compete for the time, attention and commitment of our independent distributor force. Given that the pool of individuals interested in the business opportunities presented by direct selling tends to be limited in each market, the potential pool of distributors for our products is reduced to the extent other companies successfully recruit these individuals into their businesses. Although we believe that we offer an attractive business opportunity, there can be no assurance that other companies will not be able to recruit our existing distributors or deplete the pool of potential distributors in a given market.

We have limited control over our suppliers, manufacturers, and logistics providers, which may subject us to significant risks, including the potential inability to produce or obtain quality products on a timely basis or in sufficient quantity in order to meet demand.

We have limited control over our suppliers, manufacturers, and logistics providers, which subjects us to risks, such as the following:

| • | inability to satisfy demand for our products or other products or services that we currently offer or may offer in the future; |

| • | reduced control over delivery timing and product reliability; |

| • | reduced ability to monitor the manufacturing process and components used in our products; |

| • | limited ability to develop comprehensive manufacturing specifications that take into account any materials shortages or substitutions; |

| • | variance in the manufacturing capability of our third-party manufacturers; |

| • | price increases; |

| • | failure of a significant supplier, manufacturer, or logistics provider to perform its obligations to us for technical, market or other reasons; |

| • | difficulties in establishing additional supplier, manufacturer or logistics provider relationships if we experience difficulties with our existing suppliers, manufacturers, or logistics providers; |

| • | shortages of materials or components; |

| • | misappropriation of our intellectual property; |

| • | exposure to natural catastrophes, pandemics, political unrest, terrorism, labor disputes, and economic instability resulting in the disruption of trade from foreign countries in which our products are manufactured or the components thereof are sourced; |

| • | changes in local economic conditions in the jurisdictions where our suppliers, manufacturers, and logistics providers are located; |

| • | the imposition of new laws and regulations, including those relating to labor conditions, quality and safety standards, imports, duties, tariffs, taxes, and other charges on imports, as well as trade restrictions and restrictions on currency exchange or the transfer of funds; and |

| • | insufficient warranties and indemnities on ingredients or components supplied to our manufacturers or performance by these parties. |

17

Table of Contents

We also rely on our logistics providers, including last mile warehouse and delivery providers, to complete deliveries to customers. If any of these independent contractors do not perform their obligations or meet the expectations of us or our customers, our reputation and business could suffer.

The occurrence of any of these risks, especially during seasons of peak demand, could cause us to experience a significant disruption in our ability to produce and deliver our products to our customers.

The failure or inability of our contract manufacturers to comply with the specifications and requirements of our products could result in a product recall, which could adversely affect our reputation and subject us to significant liability should the consumption of any of our products cause or be claimed to cause illness or physical harm.

We sell nutritional products for human consumption, which involves risks such as product contamination or spoilage, product tampering, other adulteration, mislabeling and misbranding. We also sell stationary bikes. All of our products are manufactured by independent third-party contract manufacturers. In addition, we do not own a warehouse facility, instead it is managed for us by a third party. Under certain circumstances, we may be required to, or may voluntarily, recall or withdraw products.

A widespread recall or withdrawal of any of our products may negatively and significantly impact our sales and profitability for a period of time and could result in significant losses depending on the costs of the recall, destruction of product inventory, reduction in product availability, and reaction of competitors and consumers. We may also be subject to claims or lawsuits, including class actions lawsuits (which could significantly increase any adverse settlements or rulings), resulting in liability for actual or claimed injuries, illness or death. Any of these events could adversely affect our business, financial condition and results of operations. Even if a product liability claim or lawsuit is unsuccessful or is not fully pursued, the negative publicity surrounding any assertion that our products caused illness or physical harm could adversely affect our reputation with existing and potential consumers and its corporate and brand image. Moreover, claims or liabilities of this sort might not be covered by insurance or by any rights of indemnity or contribution that we may have against others. We maintain product liability and product recall insurance in an amount that we believe to be adequate. However, we may incur claims or liabilities for which it is not insured or that exceed the amount of its insurance coverage. A product liability judgment against us or a product recall could adversely affect our business, financial condition and results of operations.

If any of our products are unacceptable to us or our customers, our business could be harmed.

We have occasionally received, and may in the future continue to receive, shipments of products that fail to comply with our technical specifications or that fail to conform to our quality control standards. We have also received, and may in the future continue to receive, products that either meet our technical specifications but that are nonetheless unacceptable to us, or products that are otherwise unacceptable to us or our customers. Under these circumstances, unless we are able to obtain replacement products in a timely manner, we risk the loss of net revenue resulting from the inability to sell those products and related increased administrative and shipping costs. Additionally, if the unacceptability of our products is not discovered until after such products are purchased by our customers or riders, they could lose confidence in the quality of our products and our results of operations could suffer and our business could be harmed.

Our products and services may be affected from time to time by design and manufacturing defects that could adversely affect our business and result in harm to our reputation.

Through our BODi Bike platform, we offer complex hardware and software products and services that can be affected by design and manufacturing defects. Sophisticated operating system software and applications, such as those which will be offered by us, often have issues that can unexpectedly interfere with the intended operation of hardware or software products. Defects may also exist in components and products that we source

18

Table of Contents

from third parties. Any such defects could make our products and services unsafe, create a risk of environmental or property damage and personal injury, and subject us to the hazards and uncertainties of product liability claims and related litigation. In addition, from time to time we may experience outages, service slowdowns, or errors that affect our fitness and wellness programming. As a result, our services may not perform as anticipated and may not meet customer expectations. There can be no assurance that we will be able to detect and fix all issues and defects in the hardware, software, and services we offer. Failure to do so could result in widespread technical and performance issues affecting our products and services and could lead to claims against us. We maintain general liability insurance; however, design and manufacturing defects, and claims related thereto, may subject us to judgments or settlements that result in damages materially in excess of the limits of our insurance coverage. In addition, we may be exposed to recalls, product replacements or modifications, write-downs or write-offs of inventory, property, plant and equipment, or intangible assets, and significant warranty and other expenses such as litigation costs and regulatory fines. If we cannot successfully defend any large claim, maintain our general liability insurance on acceptable terms, or maintain adequate coverage against potential claims, our financial results could be adversely impacted. Further, quality problems could adversely affect the experience for users of our products and services, and result in harm to our reputation, loss of competitive advantage, poor market acceptance, reduced demand for our products and services, delay in new product and service introductions, and lost revenue.

We may incur material product liability claims, which could increase our costs and adversely affect our revenues and operating income.

Additionally, our nutritional and dietary supplement products consist of herbs, vitamins and minerals and other ingredients that are classified as foods or dietary supplements and are not subject to pre-market regulatory approval in the United States. Our products could contain contaminated substances, and some of our products contain innovative ingredients that do not have long histories of human consumption. We do not always conduct or sponsor clinical studies for our products and previously unknown adverse reactions resulting from human consumption of these ingredients could occur. As a marketer of dietary and nutritional supplements and other products that are ingested by consumers, we have been, and may again be, subjected to various product liability claims, including that the products contain contaminants, the products include inadequate instructions as to their uses, or the products include inadequate warnings concerning side effects and interactions with other substances. It is possible that widespread product liability claims could increase our costs, and adversely affect our revenues and operating income. Moreover, liability claims arising from a serious adverse event may increase our costs through higher insurance premiums and deductibles and may make it more difficult to secure adequate insurance coverage in the future. In addition, our product liability insurance may fail to cover future product liability claims thereby requiring us to pay substantial monetary damages and adversely affecting our business.

Our business model relies on high quality customer service, and any negative impressions of our customer service experience may adversely affect our business and result in harm to our reputation.

We rely on high quality overall customer service across all of our products and services. Positive customer service experiences help drive a positive reputation, increased sales and minimization of litigation. For example, once our streaming services and integrated connected-bike products are purchased, our customers rely on our high-touch delivery and set up service to deliver and install their equipment in a professional and efficient manner. Our customers also rely on our support services to resolve any issues related to the use of such services and content. Providing a high-quality customer experience is vital to our success in generating word-of-mouth referrals to drive sales and for retaining existing customers. The importance of high-quality support will increase as we expand our business and introduce new products and services. If we do not help our customers quickly resolve issues and provide effective ongoing support, our reputation may suffer and our ability to retain and attract customers, or to sell additional products and services to existing customers, could be harmed. In addition, these levels of customer service are expensive to maintain and may provide a drain on our resources and adversely affect our revenues and operating income.

19

Table of Contents

The seasonal nature of our business could cause operating results to fluctuate.

We have experienced and continue to expect fluctuations in quarterly results of operations due to the seasonal nature of our business. The months of January to May result in the greatest retail sales due to renewed consumer focus on healthy living following New Year’s Day, as well as significant subscriber enrollment around that time. This seasonality could cause our share price to fluctuate as the results of an interim financial period may not be indicative of our full year results. Seasonality also impacts relative revenue and profitability of each quarter of the year, both on a quarter-to-quarter and year-over-year basis.

If we fail to obtain and retain high-profile strategic relationships, or if the reputation of any of these parties is impaired, our business may suffer.

A principal component of our marketing program has been to develop relationships with high-profile persons to help us extend the reach of our brand. Although we have relationships with several well-known individuals in this manner, we may not be able to attract and build relationships with new persons in the future. In addition, if the actions of these parties were to damage their or our reputation, our relationships may be less attractive to our current or prospective customers. Any of these failures by us or these parties could materially and adversely affect our business and revenues.

Our operating results could be adversely affected if we are unable to accurately forecast consumer demand for our products and services and adequately manage our inventory.

To ensure adequate inventory supply, we must forecast inventory needs and expenses and place orders sufficiently in advance with our suppliers and manufacturers, based on our estimates of future demand for particular products and services. Failure to accurately forecast our needs may result in manufacturing delays or increased costs. Our ability to accurately forecast demand could be affected by many factors, including changes in consumer demand for our products and services, changes in demand for the products and services of our competitors, unanticipated changes in general market conditions, and the weakening of economic conditions or consumer confidence in future economic conditions. We face further risk from the fact that we may not carry a significant amount of inventory and may not be able to satisfy short-term demand increases. If we fail to accurately forecast consumer demand, we may experience excess inventory levels or a shortage of products available for sale.

Inventory levels in excess of consumer demand may result in inventory write-downs or write-offs and the sale of excess inventory at discounted prices, which would cause our gross margins to suffer and could impair the strength and premium nature of our brand. Further, lower than forecasted demand could also result in excess manufacturing capacity or reduced manufacturing efficiencies, which could result in lower margins. Conversely, if we underestimate consumer demand, our suppliers and manufacturers may not be able to deliver products to meet our requirements or we may be subject to higher costs in order to secure the necessary production capacity. An inability to meet consumer demand and delays in the delivery of our products to our customers could result in reputational harm and damaged customer relationships and have an adverse effect on our business, financial condition, and operating results.

Our co-founder has control over all stockholder decisions because he controls a substantial majority of our voting power through our Class X Common Stock, or “super” voting stock.

Our co-founder, Carl Daikeler, owns or controls “super” voting shares of the Company that represent over 80% of the voting power of the Company, as of December 31, 2023. Mr. Daikeler and certain of his affiliated entities own a majority of the Company’s outstanding Class X Common Stock, which stock carries 10 votes per share, and, therefore, controls a majority of the voting power of the Company’s outstanding common stock. The Class X Common Stock carries substantially similar rights as the Class A Common Stock, except that each share of Class X Common Stock carries 10 votes. Therefore, Mr. Daikeler alone can exercise

20

Table of Contents

voting control over a majority of our voting power. As a result, Mr. Daikeler has the ability to control the outcome of all matters submitted to our stockholders for approval, including the election, removal, and replacement of our directors, amendments to the Company’s organizational documents and approval of major corporate transactions. This concentrated control could give our founder the ability to delay, defer or prevent a change of control, merger, consolidation, or sale of all or substantially all of our assets that other stockholders support. Conversely, this concentrated control could allow our founder to consummate such a transaction that our other stockholders do not support. In addition, our founder may make long-term strategic investment decisions and take risks that may not be successful and may seriously harm our business.