UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

For the quarterly period ended

OR

For the transition period from ________ to __________

Commission file number:

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| | ||

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number,

including area code:

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Indicate by check mark whether

the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such

filing requirements for the past 90 days.

Indicate by check mark whether

the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T

(§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit

such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company,

indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial

accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether

the registrant is a shell company (as defined in Rule 12b-2 of the Act) Yes ☐

No

As

of June 14, 2024, there were

WETOUCH TECHNOLOGY INC.

QUARTERLY REPORT ON FORM 10-Q

i

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q (the “Quarterly Report”) contains “forward-looking statements” within the meaning of Section 27A of the Securities Act, Section 21E of the Exchange Act, and the Private Securities Litigation Reform Act of 1995. Forward-looking statements may be preceded by, or contain, words such as “may,” “will,” “expect,” “anticipate,” “intend,” “plan,” “believe,” “estimate,” “predict,” “potential,” “might,” “could,” “would,” “should” or other words indicating future results, though not all forward-looking statements necessarily contain these identifying words. All statements other than statements of historical fact are statements that could be deemed forward-looking statements, including, without limitation, statements about our future business operations and results, our strategy and competition. These statements represent our current expectations or beliefs concerning various future events and involve numerous risks and uncertainties that could cause actual results to differ materially from expectations, including, but not limited to:

| ● | Our reliance on our top customers is significant. Failure to attract new customers or retain existing ones cost-effectively could materially and adversely impact our business, financial condition, and results of operations. |

| ● | We hold a substantial amount of accounts receivable, which may become uncollectible. |

| ● | Dismissing BF Borgers may cause significant expenses or delays in financings or SEC filings, affecting our stock price and market access. |

| ● | You are unlikely to collect judgments or exercise remedies against BF Borgers for their work as our auditor. |

| ● | We face fines and penalties from the Chinese government for not completing required filings. |

| ● | Our capacity to uphold the quality and safety standards of our products. |

| ● | Our ability to compete effectively within the touchscreen display industry. |

| ● | Without substantial additional financing, our ability to execute our business plan will be compromised. |

| ● | Failure to secure a new parcel for constructing our new buildings and facilities, as well as acquiring and installing new production lines on the new parcel, could materially and adversely affect our business, financial condition, and results of operations. |

| ● | Revocation or unavailability of preferential tax treatments and government subsidies , or successful challenges to our tax liability calculation by PRC tax authorities, may necessitate payment of tax, interest, and penalties exceeding our tax provisions. |

| ● | Significant interruptions in the operations of our third-party suppliers could potentially disrupt our operations. |

| ● | Risks associated with fluctuations in the cost, availability, and quality of raw materials may adversely affect our results of operations. |

| ● | We are reliant on key executives and highly qualified managers, and retention cannot be assured. |

ii

| ● | Absence of long-term contracts with our suppliers allows them to reduce order quantities or terminate sales to us at any time. |

| ● | Failure to adopt new technologies to evolving customer needs or emerging industry standards may materially and adversely affect our business. |

| ● | Lack of business liability or disruption insurance exposes us to significant costs and business disruption. |

| ● | Adverse regulatory developments in Mainland China may subject us to additional regulatory review, restrictions, disclosure requirements, and regulatory scrutiny by the SEC, increasing compliance costs and hindering future securities offerings. |

| ● | Our common stock may be prohibited from trading in the U.S. under the Holding Foreign Companies Accountable Act if PCAOB inspection of our auditor is incomplete, leading to delisting or prohibition and potential decline in stock value. |

| ● | Changes in China’s economic, political, or social conditions or government policies may adversely affect our business and operations. |

| ● | Uncertainties regarding the PRC legal system, including enforcement and sudden changes in laws and regulations, could adversely affect us and limit legal protections. |

| ● | Fluctuations in exchange rates could materially and adversely affect our results of operations and your investment value. |

| ● | The other risks and uncertainties discussed under the section titled “Risk Factors” beginning on page 9 of this Quarterly Report and our other filings with the Securities and Exchange Commission. |

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance, or achievements. We undertake no obligation to update or revise any of the forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

You should read this Quarterly Report with the understanding that our actual future results may be materially different from what we expect. We qualify all of the forward-looking statements in the foregoing documents by these cautionary statements.

iii

Item 1. Financial Statements

WETOUCH TECHNOLOGY INC. AND ITS SUBSIDIARIES

INDEX TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

1

WETOUCH TECHNOLOGY INC. AND ITS SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(Unaudited)

| March 31, 2024 | December 31, 2023 | |||||||

| ASSETS | ||||||||

| CURRENT ASSETS | ||||||||

| Cash | $ | $ | ||||||

| Accounts receivable | ||||||||

| Inventories | ||||||||

| Prepaid expenses and other current assets | ||||||||

| TOTAL CURRENT ASSETS | ||||||||

| Long term prepaid expenses | ||||||||

| Property, plant and equipment, net | ||||||||

| TOTAL ASSETS | $ | $ | ||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| CURRENT LIABILITIES | ||||||||

| Accounts payable | $ | $ | ||||||

| Loan from a third party | ||||||||

| Income tax payable | ||||||||

| Accrued expenses and other current liabilities | ||||||||

| Convertible promissory notes payable | ||||||||

| TOTAL CURRENT LIABILITIES | ||||||||

| Common stock purchase warrants liability | ||||||||

| TOTAL LIABILITIES | $ | $ | ||||||

| COMMITMENTS AND CONTINGENCIES (Note 12) | ||||||||

| STOCKHOLDERS’ EQUITY | ||||||||

| Common stock, $ | $ | $ | ||||||

| Additional paid in capital* | ||||||||

| Statutory reserve | ||||||||

| Retained earnings | ||||||||

| Accumulated other comprehensive loss | ( | ) | ( | ) | ||||

| TOTAL STOCKHOLDERS’ EQUITY | ||||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY | $ | $ | ||||||

| * |

The accompanying notes are an integral part of these condensed consolidated financial statements.

F-1

WETOUCH TECHNOLOGY INC. AND ITS SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE LOSS

(Unaudited)

| For the Three Months Ended March 31, | ||||||||

| 2024 | 2023 | |||||||

| REVENUES | $ | $ | ||||||

| Cost of revenues | ( | ) | ( | ) | ||||

| GROSS PROFIT | ||||||||

| OPERATING EXPENSES | ||||||||

| Selling expenses | ( | ) | ( | ) | ||||

| General and administrative expenses | ( | ) | ( | ) | ||||

| Research and development expenses | ( | ) | ( | ) | ||||

| Total operating expenses | ( | ) | ( | ) | ||||

| INCOME FROM OPERATIONS | ||||||||

| OTHER INCOME (EXPENSES) | ||||||||

| Interest income | ||||||||

| Interest expense | ( | ) | ( | ) | ||||

| Other income | ||||||||

| Gain (loss) on changes in fair value of common stock purchase warrants liability | ( | ) | ||||||

| TOTAL OTHER EXPENSES | ( | ) | ( | ) | ||||

| INCOME BEFORE INCOME TAX EXPENSE | ||||||||

| INCOME TAX EXPENSE | ( | ) | ( | ) | ||||

| NET INCOME | $ | $ | ||||||

| OTHER COMPREHENSIVE (LOSS) INCOME | ||||||||

| Foreign currency translation adjustment | ( | ) | ( | ) | ||||

| COMPREHENSIVE (LOSS) INCOME | $ | ( | ) | $ | ||||

| EARNINGS PER COMMON SHARE | ||||||||

| Basic | $ | $ | ||||||

| Diluted | $ | $ | ||||||

| WEIGHTED AVERAGE NUMBER OF SHARES OUTSTANDING* | ||||||||

| Basic | ||||||||

| Diluted | ||||||||

| * | Retrospectively restated for effect of reverse stock split (1-for-20), see Note 9 (2) |

The accompanying notes are an integral part of these consolidated financial statements.

F-2

WETOUCH TECHNOLOGY INC. AND ITS SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

(Unaudited)

Common stock at Par value $0.001 | Additional paid-in | Statutory | Retained | Accumulated other comprehensive | Total stockholders’ | |||||||||||||||||||||||

| Shares | Amount | capital | reserve | Earnings | loss | equity | ||||||||||||||||||||||

| Balance as of December 31 2022 | $ | $ | $ | $ | $ | ( | ) | $ | ||||||||||||||||||||

| Shares issued to private placement | ||||||||||||||||||||||||||||

| Net income | - | |||||||||||||||||||||||||||

| Foreign currency translation adjustment | - | ( | ) | ( | ) | |||||||||||||||||||||||

| Balance as of March 31, 2023 | $ | $ | $ | $ | $ | ( | ) | $ | ||||||||||||||||||||

Common stock at Par value $0.001 | Additional paid-in | Statutory | Retained | Accumulated other comprehensive | Total stockholders’ | |||||||||||||||||||||||

| Shares | Amount | capital | reserve | Earnings | loss | equity | ||||||||||||||||||||||

| Balance as of December 31 2023* | $ | $ | $ | $ | $ | ( | ) | $ | ||||||||||||||||||||

| Issuance of common stock from the 2024 Public Offering, net of issuance costs | ||||||||||||||||||||||||||||

| Exercise of warrants issued in conjunction with legal/consultant services in 2020 and 2021 | ( | ) | ||||||||||||||||||||||||||

| Exercise of warrants issued to third parties in conjunction with debt issuance in 2021 | ( | ) | ||||||||||||||||||||||||||

| Net income | - | |||||||||||||||||||||||||||

| Foreign currency translation adjustment | - | ( | ) | ( | ) | |||||||||||||||||||||||

| Balance as of March 31, 2024 | $ | $ | $ | $ | $ | ( | ) | $ | ||||||||||||||||||||

| * | Retrospectively restated for effect of reverse stock split (1-for-20), see Note 9 (2) |

The accompanying notes are an integral part of these condensed consolidated financial statements.

F-3

WETOUCH TECHNOLOGY INC. AND ITS SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

For the Three Months

Ended March 31, | ||||||||

| 2024 | 2023 | |||||||

| Cash flows from operating activities | ||||||||

| Net income | $ | $ | ||||||

| Adjustments to reconcile net income to cash (used in) provided by operating activities | ||||||||

| Depreciation | ||||||||

| Amortization of discounts and issuance cost of the notes | ||||||||

| Gain (loss) on changes in fair value of common stock purchase warrants liability | ( | ) | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Accounts receivable | ( | ) | ( | ) | ||||

| Amounts due from related parties | ( | ) | ||||||

| Inventories | ||||||||

| Prepaid expenses and other current assets | ( | ) | ||||||

| Accounts payable | ( | ) | ||||||

| Amounts due to related parties | ( | ) | ||||||

| Income tax payable | ||||||||

| Accrued expenses and other current liabilities | ( | ) | ||||||

| Net cash (used in) provided by operating activities | ( | ) | ||||||

| Cash flows from investing activities | ||||||||

| Purchase of property, plant and equipment | ( | ) | ||||||

| Net cash used in investing activities | ( | ) | ||||||

| Cash flows from financing activities | ||||||||

| Proceeds from issuance of common stock, net of issue costs | ||||||||

| Proceeds from stock issuance of private placement | ||||||||

| Repayment of interest-free advances to a third party | ( | ) | ||||||

| Proceeds from interest-free advances from a third party | ||||||||

| Repayments of convertible promissory notes payable | ( | ) | ( | ) | ||||

| Net cash provided by financing activities | ||||||||

| Effect of changes of foreign exchange rates on cash | ( | ) | ( | ) | ||||

| Net (decrease) increase in cash | ( | ) | ||||||

| Cash, beginning of period | ||||||||

| Cash, end of period | $ | $ | ||||||

| Supplemental disclosures of cash flow information | ||||||||

| Income tax paid | $ | $ | ||||||

| Interest paid | $ | $ | ||||||

| Issue costs charged to additional paid-in capital | $ | $ | ||||||

| Exercise of warrant shares | $ | $ | ||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

F-4

WETOUCH TECHNOLOGY INC. AND ITS SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1 — BUSINESS DESCRIPTION

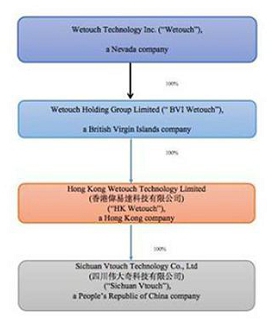

Wetouch Technology Inc. (“Wetouch”, or the “Company”), formerly known as Gulf West Investment Properties, Inc., was originally incorporated in August 1992, under the laws of the state of Nevada.

On October 9, 2020, the Company entered into a share exchange agreement

(the “Share Exchange Agreement”) with Wetouch Holding Group Limited (“BVI Wetouch”) and all the shareholders of

BVI Wetouch (each, a “BVI Shareholder” and collectively, the “BVI Shareholders”), to acquire all the issued and

outstanding capital stock of BVI Wetouch in exchange for the issuance to the BVI Shareholders an aggregate of

BVI Wetouch is a holding

company whose only asset, held through a subsidiary, is

The Reverse Merger was accounted for as a recapitalization effected by a share exchange, wherein BVI Wetouch is considered the acquirer for accounting and financial reporting purposes. The assets and liabilities of BVI Wetouch have been brought forward at their book value and no goodwill has been recognized. The number of shares, par value amount, and additional paid-in capital in the prior years are retrospectively adjusted accordingly.

Corporate History of BVI Wetouch

BVI Wetouch was incorporated under the laws of British Virgin Islands on August 14, 2020. It became the holding company of Hong Kong Wetouch Electronics Technology Limited (“Hong Kong Wetouch”) on September 11, 2020.

Hong Kong Wetouch Technology Limited (“HK Wetouch”), was incorporated as a holding company under the laws of Hong Kong Special Administrative Region (the “SAR”) on December 3, 2020. On March 2, 2021, HK Wetouch acquired all shares of Hong Kong Wetouch. Due to the fact that Hong Kong Wetouch and HK Wetouch are both under the same sole stockholder, the acquisition is accounted for under common control.

In June 2021, Hong Kong Wetouch completed its dissolution process pursuant to the minutes of its special stockholder meeting.

Sichuan Wetouch was formed

on May 6, 2011 in the PRC and became a Wholly Foreign-Owned Enterprise (“WFOE”) in PRC on February 23, 2017. On July 19, 2016,

Sichuan Wetouch was

On December 30, 2020, Sichuan Vtouch was incorporated in Chengdu, Sichuan, under the PRC laws.

F-5

In March 2021, pursuant to local PRC government guidelines on local environmental issues and the national plan, Sichuan Wetouch was under the government directed relocation order. Sichuan Vtouch took over the operating business of Sichuan Wetouch.

On March 30, 2023, an independent third party acquired all shares of Sichuan Wetouch for a nominal amount.

As a result of the above restructuring, HK Wetouch became the sole stockholder of Sichuan Vtouch.

The following diagram illustrates the Company’s current corporate structure:

NOTE 2 — SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

(a) Basis of Presentation and Principles of Consolidation

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”). Certain information and footnote disclosures normally included in financial statements prepared in accordance with U.S. GAAP have been condensed or omitted as permitted by rules and regulations of the United States Securities and Exchange Commission (the “SEC”). The condensed consolidated balance sheet as of December 31, 2023 was derived from the audited consolidated financial statements of Wetouch. The accompanying unaudited condensed consolidated financial statements should be read in conjunction with the consolidated balance sheet of the Company as of December 31, 2023, and the related consolidated statements of comprehensive income, changes in equity and cash flows for the years then ended.

In the opinion of the management, all adjustments (which include normal recurring adjustments) necessary to present a fair statement of the financial position as of March 31, 2024, the results of operations and cash flows for the three-month periods ended March 31, 2024 and 2023 have been made. However, the results of operations included in such financial statements may not necessarily be indicative of annual results.

F-6

Deconsolidation of Sichuan Wetouch

On March 30, 2023, upon transferring Sichuan Wetouch to a third-party individual for a nominal value, the Company was no longer able to operate and exert control over this subsidiary whose operation has been taken over by Sichuan Vtouch since the first quarter of 2021. As a result, Sichuan Wetouch was deconsolidated accordingly since the disposal date.

| March 30, 2023 |

||||

| Total assets as of deconsolidated date | $ | |||

| Total liabilities as of deconsolidated date | ||||

| Total gain or loss from deconsolidation | $ | |||

Upon the deconsolidation, the Company was no longer entitled to the assets and also legally released from the liabilities previously held by the deconsolidated Sichuan Wetouch, derived nil gain or loss from the deconsolidation in the condensed consolidated statements of operations and comprehensive income for the three months ended March 31, 2023. The disposal of Sichuan Wetouch did not represent a strategic shift and did not have a major effect on the Company’s operation. There was no cash outflow for the disposal for the three months ended March 31, 2023.

(b) Uses of Estimates

In preparing the consolidated financial statements in conformity with US GAAP, management makes estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. These estimates are based on information as of the date of the consolidated financial statements. Significant estimates required to be made by management include, but are not limited to, the allowance for estimated uncollectible receivables, fair values of financial instruments, inventory valuations, useful lives of property, plant and equipment, the recoverability of long-lived assets, provision necessary for contingent liabilities, revenue recognition and realization of deferred tax assets. Actual results could differ from those estimates.

(c) Significant Accounting Policies

For a detailed discussion about Wetouch’s significant accounting policies, refer to Note 2 — “Summary of Significant Accounting Policies,” in Wetouch’s consolidated financial statements included in Company’s 2023 audited consolidated financial statements. Other than the revised accounting policy on property, plant and equipment, net, as below, during the three-month periods ended March 31, 2024, there were no significant changes made to Wetouch significant accounting policies.

Property, plant and equipment, net

| Useful life | ||

| Buildings | ||

| Machinery and equipment | ||

| Office and electric equipment | ||

| Vehicles |

Expenditures for maintenance and repairs, which do not materially extend the useful lives of the assets, are charged to expense as incurred. Expenditures for major renewals and betterments which substantially extend the useful life of assets are capitalized. The cost and related accumulated depreciation of assets retired or sold are removed from the respective accounts, and any gain or loss is recognized in the consolidated statements of income and other comprehensive income in other income or expenses.

Construction in progress, funded by Company’s working capital, represents manufacturing facilities and office building under construction, is stated at cost and transferred to property, plant and equipment when it is substantially ready for its intended use. No depreciation is recorded for construction in progress. The management estimate that construction in progress will be completed by the end of first quarter of 2025 and will transfer construction in progress to property, plant and equipment to start depreciation.

F-7

NOTE 3 — ACCOUNTS RECEIVABLE

| March 31, 2024 | December 31, 2023 | |||||||

| Accounts receivable | $ | $ | ||||||

The Company’s accounts receivable primarily includes balance due from customers when the Company’s products are sold and delivered to customers.

NOTE 4 — PREPAID EXPENSES AND OTHER CURRENT ASSETS

| March 31, 2024 |

December 31, 2023 |

|||||||

| Advance to suppliers | $ | $ | ||||||

| VAT input | ||||||||

| Issue cost related to convertible promissory notes | ||||||||

| Prepayment for land use right (i) | ||||||||

| Security deposit (ii) | ||||||||

| Prepaid consulting service fees (iii) | ||||||||

| Prepaid market research fees (iv) | ||||||||

| Others receivable (v) | ||||||||

| Prepaid expenses and other current assets | $ | $ | ||||||

| (i) |

| (ii) |

| (iii) | |

| (iv) |

| (v) |

F-8

NOTE 5 — PROPERTY, PLANT AND EQUIPMENT, NET

| March 31, 2024 | December 31, 2023 | |||||||

| Buildings | $ | $ | ||||||

| Machinery and equipment | ||||||||

| Vehicles | ||||||||

| Construction in progress | ||||||||

| Subtotal | ||||||||

| Less: accumulated depreciation | ( | ) | ( | ) | ||||

| Property, plant and equipment, net | $ | $ | ||||||

Depreciation expense was $

Pursuant to local PRC government guidelines on

local environment issues and the national overall plan, Sichuan Wetouch, was under the government directed relocation order to relocate

no later than December 31, 2021 and received compensation accordingly. On March 18, 2021, pursuant to the agreement with the local government

and an appraisal report issued by a mutual agreed appraiser, Sichuan Wetouch received a compensation of RMB

On March 16, 2021, in order to minimize interruption

of the Company’s business, Sichuan Vtouch entered into a leasing agreement with Sichuan Renshou Shigao Tianfu Investment Co., Ltd.

(later renamed as Meishan Huantian Industrial Co., Ltd.), a limited liability company owned by the local government, to lease the property,

and all buildings, facilities and equipment thereon (the “Demised Properties) of Sichuan Wetouch, commencing from April 1, 2021

until December 31, 2021 at a monthly rent of RMB

As of March 31, 2024, the Company had construction

commitment of RMB

F-9

NOTE 6 — INCOME TAXES

Wetouch

Wetouch is subject to a tax rate of

BVI Wetouch

Under the current laws of the British Virgin Islands, BVI Wetouch, a wholly owned subsidiary of Wetouch, is not subject to tax on its income or capital gains. In addition, no British Virgin Islands withholding tax will be imposed upon the payment of dividends by the Company to its stockholders.

Hong Kong

HK Wetouch is subject to profit taxes in Hong

Kong at a progressive rate of

PRC

Sichuan Vtouch files income tax returns in the

PRC. Effective from January 1, 2008, the PRC statutory income tax rate is

Sichuan Vtouch is subject to a

The effective income

tax rates for the three-month period ended March 31, 2024 and 2023 were

The estimated effective income tax rate for the year ending December 31, 2024 would be similar to actual effective tax rate of the three-month period ended March 31, 2024.

F-10

NOTE 7 — ACCRUED EXPENSES AND OTHER CURRENT LIABILITIES

| March 31, 2024 | December 31, 2023 | |||||||

| Advance from customers (i) | $ | $ | ||||||

| Accrued payroll and employee benefits | ||||||||

| Accrued interest expenses | ||||||||

| Accrued private placement agent fees (ii) | ||||||||

| Accrued consulting fees (iii) | ||||||||

| Accrued litigation charges (iv) | ||||||||

| Accrued professional fees | ||||||||

| Accrued director fees | ||||||||

| Other tax payables (v) | ||||||||

| Others (vi) | ||||||||

| Accrued expenses and other current liabilities | $ | $ | ||||||

| (i) | |

| (ii) |

| (iii) |

| (iv) |

| (v) | |

| (vi) |

F-11

NOTE 8 — CONVERTIBLE PROMISSORY NOTES PAYABLE

a) Convertible promissory notes

In October, November,

and December 2021, the Company, issued seven (7) convertible promissory notes (the “Notes”) of an aggregate principal amount

of US$

The details of the Notes are as follows:

Unless the Notes are

converted, the principal amounts of the Notes, and accrued interest at the rate of

The Lenders have the

right to convert any or all of the principal and accrued interest on the Notes into shares of common stock of the Company on the earlier

of (i) 180 calendar days after the issuance date of the Notes or (ii) the closing of a listing for trading of the common stock of the

Company on a national securities exchange offering resulting in gross proceeds to the Company of $

Subject to customary exceptions, if the Company issues shares or any securities convertible into shares of common stock at an effective price per share lower than the conversion price of the Notes, the conversion rate of the Notes shall be reduced to such lower price.

Until the Notes are either paid or converted in their entirety, the Company agreed with the Lenders not to sell any securities convertible into shares of common stock of the Company (i) at a conversion price that is based on the trading price of the stock or (ii) with a conversion price that is subject to being reset at a future date or upon an event directly or indirectly related to the business of the Company or the market for the common stock. The Company also agreed to not issue securities at a future determined price.

The Lenders have the

right to require the Company to repay the Notes if the Company receives cash proceeds, including proceeds from customers and the issuance

of equity (including in the Uplist Offering). If the Company prepays the Notes prior to the Maturity Date, the Company shall pay a

From December 28, 2022 to April 6, 2023, the lenders of five outstanding Notes and the Company entered into an amendment to the Notes (“Amendment to Promissory Note”) extending the term of the Notes for an additional 6 months.

During the year ended

December 31, 2023, principal and default charges totaling $

During the year ended

December 31, 2023, principal, accrued and unpaid interest and default charges totaling $

F-12

On February 23, 2024, immediately upon the closing

of the public offering (the “2024 Public Offering”), the Company made a full payment of $

During the three-month period ended March 31,

2024 and 2023, amortization of discounts and issuance cost of the notes were US$

For

the three-month period ended March 31, 2024 and 2023, the Company recognized interest expenses of the Notes in the amount of US$

b) Warrants

Accounting for Warrants

In connection with the

issuance of the Notes, the Company also issued to the lenders seven (7) three-year warrants (the “Note Warrants”) to purchase

an aggregate of

The Note Warrants

issued to the lenders granted the holders the rights to purchase up to

The lenders have the right to exercise the Note Warrants on a cashless basis if the highest traded price of a share of common stock of the Company during the 150 trading days prior to exercise of the Note Warrants exceeds the exercise price, unless there is an effective registration statement of the Company which covers the resale of the Lenders.

If the Company issues shares or any securities convertible into shares at an effective price per share lower than the exercise price of the Note Warrants, the exercise price of the Note Warrants shall be reduced to such lower price, subject to customary exceptions.

The lenders may not convert

the Notes or exercise the Note Warrants if such conversion or exercise will result in each of the lenders, together with any affiliates,

beneficially owning in excess of

During the year ended

December 31, 2022, three lenders exercised the Note Warrants cashlessly for

During the year ended

December 31, 2023, two lenders exercised the Note Warrants cashlessly for

During the three months

ended March 31, 2024, one lender exercised the Note Warrants cashlessly for

F-13

| March 31, 2024 | ||||||||||||||||||||||||||||

| Volatility (%) | Expected dividends yield (%) | Weighted average expected life (year) | Risk-free interest rate (%) (per annum) | Common stock purchase warrants liability as of December 31, 2023 (US$) | Changes of fair value of common stock purchase warrants liability (+ (loss)/(- (gain) (US$) | Common stock purchase warrants liability as of March 31, 2024 (US$) | ||||||||||||||||||||||

| Convertible Note - Talos Victory (Note 9 (a)) | % | % | % | ( | ) | |||||||||||||||||||||||

| Convertible Note - First Fire (Note 9 (a)) | % | % | % | ( | ) | |||||||||||||||||||||||

| Convertible Note - LGH Note 9 (a)) | % | % | % | ( | ) | |||||||||||||||||||||||

| Convertible Note - Fourth Man (Note 9 (ab)) | % | % | % | ( | ) | |||||||||||||||||||||||

| Convertible Note - Jeffery Street Note 9 (a)) | % | % | % | ( | ) | |||||||||||||||||||||||

| Convertible Note - Blue Lake Note 9 (a)) | % | % | % | ( | ) | |||||||||||||||||||||||

| Total | ( | ) | ||||||||||||||||||||||||||

(c) Registration Rights Agreements

Pursuant to the terms of the Registration Rights Agreements between the Company and lenders of the Notes, the Company agreed to file a registration statement with the Securities and Exchange Commission to register the shares of common stock underlying the Notes and the shares issuable upon exercise of the Note Warrants within sixty days from the date of each Registration Rights Agreement. The Company also granted the lenders piggyback registration rights on such securities pursuant to the Purchase Agreements.

NOTE 9 — STOCKHOLDERS’ EQUITY

1) Common Stock

The Company’s authorized shares of common

stock was

On December 22, 2020, the Company issued

On January 1, 2021, the Company issued an aggregate

of

On April 14, April 27 and September 1, 2022, the

Company issued

During the year ended

December 31, 2022, the Company issued

During the year ended

December 31, 2022, the Company issued

On January 19, 2023,

the Company sold an aggregate of

F-14

During the year ended December 31, 2023, the Company

issued

During the year ended December 31, 2023, the Company

issued

On February 20, 2024, the Company

issued

As of March 31, 2024, there were

2) Reverse Stock Split

On February 17, 2023, the Company’s board of directors authorized a reverse stock split of common stock with a ratio of not less than one to five (1:5) and not more than one to eighty (1:80), with the exact amount and the timing of the reverse stock split to be determined by the Chairman of the Board. Upon effectiveness of such reverse stock split, the number of authorized shares of the common stock of the Company will also be decreased in the same ratio. Pursuant to Section 78.209 of the Nevada Revised Statutes, the reverse stock split does not have to be approved by the stockholders of the Company.

On July 16, 2023, the Company’s board of directors approved the reverse stock split of the Company’s common stock at a ratio of 1-for-20. On July 16, 2023, the Company filed a certificate of change (with an effective date of July 16, 2023) with the Nevada Secretary of State pursuant to Section 78.209 of the Nevada Revised Statutes to effectuate a 1-for-20 reverse stock split of its common stock. On September 11, 2023, the reverse stock split was approved by the Financial Industry Regulatory Authority and took effect on September 12, 2023. All share information included in this report has been adjusted as if the reverse stock split occurred as of the earliest period presented.

3) Closing of the 2024 Public Offering

On February

23, 2024, the Company closed its offering of

The Company complies with the requirements of

FASB ASC Topic 340-10-S99-1, “Other Assets and Deferred Costs – SEC Materials” (“ASC 340-10-S99”) and SEC

Staff Accounting Bulletin Topic 5A, “Expenses of Offering”, and charged issuance costs of $

F-15

NOTE 10 — SHARE BASED COMPENSATION

The Company applied ASC 718 and related interpretations in accounting for measuring the cost of share-based compensation over the period during which the consultants are required to provide services in exchange for the issued shares. The fair value of above award was estimated at the grant date using the Black-Scholes model for pricing the share compensation expenses.

On December 22, 2020,

the Board of Directors of the Company authorized the issuance of an aggregate of

On January 1, 2021, the Board of Directors of

the Company authorized the issuance of an aggregate of

The

The fair value of the above warrants was estimated

at the grant date using Black-Scholes model for pricing the share compensation expenses. The fair value of the Black-Scholes model includes

the following assumptions: expected life of

During the three months ended March 31, 2024, warrants for

As of March 31, 2024 and 2023, the Company recognized relevant share-based compensation expense of and for the vested shares, and and for the warrants, respectively.

F-16

NOTE 11 — RISKS AND UNCERTAINTIES

Credit Risk – The carrying amount of accounts receivable included in the balance sheet represents the Company’s exposure to credit risk in relation to its financial assets. No other financial asset carries a significant exposure to credit risk. The Company performs ongoing credit evaluations of each customer’s financial condition. The Company maintains allowances for doubtful accounts and such allowances in the aggregate have not exceeded management’s estimates.

The Company has its cash in bank deposits primarily

at state owned banks located in the PRC. Historically, deposits in PRC banks have been secured due to the state policy of protecting depositors’

interests. The PRC promulgated a Bankruptcy Law in August 2006, effective June 1, 2007, which contains provisions for the implementation

of measures for the bankruptcy of PRC banks. The bank deposits with financial institutions in the PRC are insured by the government authority

for up to RMB

Interest Rate Risk – The Company is exposed to the risk arising from changing interest rates, which may affect the ability of repayment of existing debts and viability of securing future debt instruments within the PRC.

Currency Risk - A majority of the Company’s revenue and expense transactions are denominated in RMB and a significant portion of the Company’s assets and liabilities are denominated in RMB. RMB is not freely convertible into foreign currencies. In the PRC, certain foreign exchange transactions are required by law to be transacted only by authorized financial institutions at exchange rates set by the People’s Bank of China (“PBOC”). Remittances in currencies other than RMB by the Company in China must be processed through the PBOC or other China foreign exchange regulatory bodies which require certain supporting documentation in order to affect the remittance.

Concentrations - The Company sells

its products primarily to customers in the PRC and to some extent, the overseas customers in European countries and East Asia such as

South Korea and Taiwan. For the three-month period ended March 31, 2024 and 2023, five customers accounted for

The Company’s top

ten customers aggregately accounted for an aggregate of

As of March 31, 2024, three customers accounted

for

The Company purchases its raw materials through various suppliers.

Raw material purchases from these suppliers which individually exceeded

F-17

NOTE 12 — COMMITMENTS AND CONTINGENCIES

Contingencies

The Company’s common stock began trading on the Nasdaq Capital Market under the ticker symbol “WETH” on February 21, 2024. The Company failed to timely complete the filing procedures with China Securities Regulatory Commission (“CSRC”) on overseas offering and transfer of listing pursuant to the regulations below:

1) Pursuant to Article 13 and Article 8 and Article 25 of CSRC Announcement (2023) No. 43 -Trial Measures for the Administration of Overseas Issuance and Listing of Securities for Domestic Enterprises” (the “Trial Measures”), which was effective on March 31, 2023 ( http://www.csrc.gov.cn/csrc/c101954/c7124478/content.shtml), when an issuer conducts an overseas offering or listing, it shall submit overseas issuance and listing application documents to CSRC within three working days of submitting its application documents for transfer and listing overseas; when a domestic enterprise transfers its listing overseas, it shall comply with the requirements of the overseas first public listing requirements for issuance and listing, and shall file with the CSRC within 3 working days, after its submitting application documents for transfer and listing overseas.

2) Article 27 of Trial Measures stipulates that if a domestic enterprise

violates the provisions of Article 13 of these Measures and fails to perform the filing procedures, or violates the provisions of Articles

8 and 25 of these Measures for overseas issuance and listing, CSRC shall order it to make corrections and give a warning, and impose a

fine of not less than RMB

As of the date of this Quarterly Report, the Company has not received any notice of penalty from the CSRC. Management will closely monitor any notice or action from the CSRC.

Legal Proceedings

From time to time, the Company and its subsidiaries are parties to various legal actions arising in the ordinary course of business. Although Hong Kong Wetouch, Sichuan Wetouch, the deconsolidated subsidiary of the Company (see Note 2-(a) - Deconsolidation of Sichuan Wetouch), Sichuan Vtouch and Mr. Guangde Cai, the former Chairman and director of the Company, were named as defendants in several litigation matters, as of the date of this report, all such matters have been settled and Sichuan Wetouch, Hong Kong Wetouch and Mr. Guangde Cai were unconditionally and fully discharged and released therefrom Accordingly, there are no pending material legal proceedings against the Company as of the date of this report.

| i) | An equity dispute case with Yunqing Su with a disputed amount of RMB |

On June 22, 2017, Yunqing Su, a former stockholder,

entered an Equity Investment Agreement with Sichuan Wetouch and Guangde Cai, agreed that Yunqing Su would invest RMB

On May 9, 2022, pursuant to a civil mediation

statement issued by the Renshou County People’s Court of Sichuan Province, Sichuan Wetouch and Guangde Cai agreed to repay Yunqing

Su the principal and interest in the total amount of RMB

| ii) | Legal case with Chengdu SME Credit Guarantee Co., Ltd. on a court acceptance fee of RMB |

On July 5, 2013, Sichuan Wetouch obtained a one-year

loan of RMB

On July 31, 2014, Sichuan Wetouch repaid RMB

F-18

Chengdu SME applied to the Chengdu High-tech Court

for enforcement of the above-mentioned loan default penalties of RMB

On September 16, 2020, Sichuan Wetouch made a

full repayment of RMB

On March 16, 2023, pursuant to an Enforcement

Settlement Agreement entered among Chengdu SME, Sichuan Wetouch and Chengdu Wetouch, Chengdu Wetouch agreed to pay the court acceptance

fee of RMB

| iii) | Legal case with Lifan Financial Leasing (Shanghai) Co., Ltd. and Sichuan Wetouch, Chengdu Wetouch, Meishan Wetouch and Xinjiang Wetouch Electronic Technology Co., Ltd. on a court acceptance fee of RMB |

On November 20, 2014, Lifan Financial Lease (Shanghai)

Co., Ltd. (“Lifan Financial”) and Chengdu Wetouch entered into a Financial Lease Contract (Sale and Leaseback), which stipulated

that Lifan Financial shall lease the equipment to Chengdu Wetouch after the purchase of the production equipment owned by Chengdu Wetouch

at a purchase price, the purchase price/lease principal shall be RMB

On August 9, 2021, Lifan Financial filed a lawsuit

against Chengdu Wetouch, Guangde Cai, Sichuan Wetouch, Meishan Wetouch and Xinjiang Wetouch in the Chengdu Intermediate People’s

Court. The court ruled that: 1) the Financial Lease Contract (Sale and Leaseback) was terminated; 2) the leased property was owned by

Lifan Financial; 3) Chengdu Wetouch shall pay Lifan Financial all outstanding rent and interest thereon in the total amount of RMB

The parties executed a settlement agreement on

March 7, 2023, in which the parties confirmed that the outstanding payment of RMB

| iv) | Legal case with Sichuan Renshou Shigao Tianfu Investment Co., Ltd and Renshou Tengyi Landscaping Co., Ltd. on a court acceptance fee of RMB |

On March 19, 2014, Chengdu Wetouch, a related party, obtained a two-

and half-year loan of RMB

Upon the loan due in January 2017, Chengdu Wetouch defaulted the loan, thus, CDHT Investment filed a lawsuit against Chengdu Wetouch, Sichuan Wetouch, and Hong Kong Wetouch demanding a full repayment of such debts.

Upon the expiration of the guarantee, Chengdu

Wetouch still defaulted on repayment of the above pledge. As a result, CDHT Investment levied this collateral of RMB

F-19

On December 2, 2019, pursuant to the reconciling agreement issued by Chengdu Intermediate People’s Court, the parties agreed to cancel the demand to seize property of Sichuan Wetouch rather than the property of Chengdu Wetouch, and to waive freezing Guangde Cai’s 60% shareholding equity in Xinjiang Wetouch Electronic Technology Co., Ltd.

On October 9, 2020, pursuant to a settlement and release agreement, Sichuan Wetouch, Hong Kong Wetouch and Guangde Cai are fully discharged and released from any and all obligations under the outstanding debts, and from all liabilities under guarantee with Chengdu Wetouch being responsible for the outstanding debts by December 31, 2020.

On October 27, 2020, Chengdu Wetouch made a full payment of the above debts.

The settlement and release agreement did not specify

which party shall pay the court acceptance fee. On March 10, 2023, pursuant to an enforcement settlement agreement entered among Sichuan

Renshou, Renshou Tengyi, Sichuan Wetouch, Chengdu Wetouch, and other relevant parties, Sichuan Wetouch agreed to pay the court acceptance

fee of RMB

| v) | Legal case with Chengdu High Investment Financing Guarantee Co. on a court acceptance fee of RMB |

On March 22, 2019, Chengdu High Investment Financing

Guarantee Co., Ltd, (“Chengdu High Investment”) filed a lawsuit against Hong Kong Wetouch in the Chengdu Intermediate People’s

Court, claiming that Hong Kong Wetouch should assume the guarantee liability for the debt payable by Chengdu Wetouch. On May 21, 2020,

the court rendered a judgment ordering Hong Kong Wetouch to pay compensation of RMB

On March 16, 2023, Chengdu Wetouch, Sichuan Wetouch

and Chengdu High Investment entered into a settlement enforcement agreement, confirming that Chengdu High Investment had received RMB

| vi) | Legal case with Hubei Lai’en Optoelectronics Technology Co., Ltd. on a product payment of RMB |

Sichuan Wetouch purchased products from Hubei

Lai’en Optoelectronics Technology Co., Ltd. (“Hubei Lai’en) multiple times from March to June 2019, but failed to pay

the corresponding amount of RMB

| vi) | Legal case with Chengdu Hongxin Shunda Trading Co., Ltd.

on settlement of accounts payable and related fund interests totalling RMB |

In March 2022, Sichuan Vtouch purchase steel products

from Chengdu Hongxin Shunda Trading Co., Ltd. (“Chengdu Hongxin”) for facility construction, but failed to settle the accounts

payable on time. In July 2023, Chengdu Hongxin filed a lawsuit to a local district court against the Company and its new facility constructors

(“the three defendants”) requesting the settlement of the remaining accounts payable and the corresponding fund interests,

penalties and legal fees, totalling of RMB

| vii) | Legal case with Mr. Guangchuang Liu on a refund of equity

transfer price and related interests totalling RMB |

In July 2022 Mr. Liu entered into an equity transfer

agreement with Mr. Guangde Cai and Sichuan Vtouch with the intention to subscribe the Company’s shares of

F-20

| viii) | Legal case with Sichuan Yali Cement Manufacturing Co., Ltd.

and Sichuan Chunqiu Development & Construction Group Co. Ltd. on a debt payable of RMB RMB |

On August 10, 2022, Sichuan Yali Cement Manufacturing Co., Ltd. (“Yali Co.”) and Sichuan Chunqiu Development & Construction Group Co. Ltd. (“Chunqiu Co.”) entered into construction materials contract for Sichuan Vtouch’s new facility. Under this contract, Sichuan Vtouch was listed as the joint responsibility party for the payment settlement between Yali Company and Chunqiu Company.

On February 15, 2023, Yali Co. filed a lawsuit

against Chunqiu Co. to the Chengdu Wenjiang District People’s Court, claiming that Chunqiu Co. should pay the remaining debt of

RMB RMB

On August 22, 2023, Chunqiu Co. appealed to Chengdu

Municipal Intermediate People’s Court against Yali Co. and Sichuan Vtouch requesting Sichuan Vtouch to be responsible for this debt

payable. On October 30, 2023, the court ordered Chunqiu Co. to pay pack all the debts, and Sichuan Vtouch to bear the joint and several

liability for the above debts of Chunqiu Co. including a court fee of RMB

Capital Expenditure Commitment

As of March 31, 2024, the Company had construction

commitment of RMB

NOTE 13 — REVENUES

| For the Three Months Ended March 31, | ||||||||

| 2024 | 2023 | |||||||

| Sales in PRC | $ | $ | ||||||

| Sales in Overseas | ||||||||

| -Republic of China (ROC, or Taiwan) | ||||||||

| -South Korea | ||||||||

| -Others | ||||||||

| Sub-total | ||||||||

| Total revenues | $ | $ | ||||||

NOTE 14 — SUBSEQUENT EVENT

The Company’s common stock began trading on the Nasdaq Capital Market under the ticker symbol “WETH” on February 21, 2024. The Company failed to timely complete the filing procedures with China Securities Regulatory Commission (“CSRC”) on overseas offering and transfer of listing. As of the date of this Quarterly Report, the Company has not received any notice of penalty from the CSRC. Management will closely monitor any notice or action from CSRC. For details, please refer to NOTE 12 — COMMITMENTS AND CONTINGENCIES-Contingencies

F-21

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The discussion should be read in conjunction with the Company’s consolidated financial statements and the notes presented herein. In addition to historical information, the following Management’s Discussion and Analysis of Financial Condition and Results of Operations contains forward-looking statements that involve risks and uncertainties. Actual results could differ significantly from those expressed, implied or anticipated in these forward-looking statements as a result of certain factors discussed herein and any other periodic reports filed and to be filed with the Securities and Exchange Commission. See “Cautionary Note Regarding Forward Looking Statement.”

Overview

We were originally incorporated under the laws of the state of Nevada in August 1992. On October 9, 2020, we entered into a share exchange agreement (the “Share Exchange Agreement”) with BVI Wetouch and all the shareholders of BVI Wetouch, to acquire all the issued and outstanding capital stock of BVI Wetouch in exchange for the issuance to such shareholders an aggregate of 28 million shares of our common stock (the “Reverse Merger”). The Reverse Merger closed on October 9, 2020. As a result of the Reverse Merger, BVI Wetouch is now our wholly-owned subsidiary.

Through our wholly-owned subsidiaries, BVI Wetouch, HK Wetouch, Sichuan Wetouch, and Sichuan Vtouch, we are engaged in the research, development, manufacturing, sales and servicing of medium to large sized projected capacitive touchscreens, which constitutes our source of revenues. We are specialized in large-format touchscreens, which are developed and designed for a wide variety of markets and used in by the financial terminals, automotive, POS, gaming, lottery, medical, HMI, and other specialized industries. Our product portfolio comprises medium to large sized projected capacitive touchscreens ranging from 7.0 inch to 42 inch screens. In terms of the structures of touch panels, we offer (i) Glass-Glass (“GG”), primarily used in GPS/car entertainment panels in mid-size and luxury cars, industrial HMI, financial and banking terminals, POS and lottery machines; (ii) Glass-Film-Film (“GFF”), mostly used in high-end GPS and entertainment panels, industrial HMI, financial and banking terminals, lottery and gaming industry; (iii) Plastic-Glass (“PG”), typically adopted by touchscreens in GPS/entertainment panels motor vehicle GPS, smart home, robots and charging stations; and (iv) Glass-Film (“GF”), mostly used in industrial HMI.

On July 16, 2023, the Company’s board of directors approved a reverse stock split of the Company’s common stock at a ratio of 1-for-20. On July 16, 2023, the Company filed a certificate of change (with an effective date of July 16, 2023) with the Nevada Secretary of State pursuant to Nevada Revised Statutes 78.209 to effectuate a 1-for-20 reverse stock split of its outstanding common stock. On September 11, 2023, the Company received a notice from FINRA/OTC Corporate Actions the reverse split would take effect at the open of business on September 12, 2023, and the reverse stock that split took effect on that date. All share information included in this Quarterly Report has been reflected as if the reverse stock splits occurred as of the earliest period presented.

Construction of our new facility

We have been actively engaged in the construction of our new production facilities and office buildings in Chengdu Medicine City (Technology Park), Wenjiang District, Chengdu, Sichuan Province, Peoples’s Republic of China since the summer of 2023.

As of the date of this Quarterly Report, we estimate to finish the building construction by the end of 2024 and commence production in the third quarter of 2025,

During the three months ended March 31, 2024, the Company has planned to increase the scope of facility construction by adding a touch machine construction area, to be completed by the end of 2024.

Highlights for the three-month period ended March 31, 2024 include:

| ● | Revenues were $14.9 million, an increase of 11.2% from $13.4 million in the first quarter of 2023 | |

| ● | Gross profit was $3.3 million, a decrease of 45.0% from $6.0 million in the first quarter of 2023 | |

| ● | Gross profit margin was 22.4% as compared to 45.0% in the first quarter of 2023 | |

| ● | Net income was $0.6 million, a decrease of 78.6% from $2.8 million in the first quarter of 2023 | |

| ● | Total volume shipped was 681,370 units, an increase of 7.3% from 635,276 units in the first quarter of 2023 |

2

Results of Operations

The following table sets forth, for the periods indicated, statements of income data:

| (in US Dollar millions, except percentage) | Three-Month Period Ended March 31, | Change | ||||||||||

| 2024 | 2023 | % | ||||||||||

| Revenues | $ | 14.9 | $ | 13.4 | 11.2 | % | ||||||

| Cost of revenues | (11.6 | ) | (7.4 | ) | (56.7 | )% | ||||||

| Gross profit | 3.3 | 6.0 | (45.0 | )% | ||||||||

| Total operating expenses | (1.0 | ) | (1.7 | ) | (41.1 | )% | ||||||

| Operating income | 2.3 | 4.3 | (46.5 | )% | ||||||||

| Total other expenses | (1.1 | ) | (0.1 | ) | (1,000.0 | )% | ||||||

| Interest expense | (1.2 | ) | (0.0 | ) | N/A | |||||||

| Income before income taxes | 1.2 | 4.2 | (71.4 | )% | ||||||||

| Income tax expense | (0.6 | ) | (1.4 | ) | (57.1 | )% | ||||||

| Net income | $ | 0.6 | $ | 2.8 | (78.6 | )% | ||||||

Three Months Ended March 31, 2024 Compared to Three Months Ended March 31, 2023

Revenues

We generated revenue of $14.9 million for the three months ended March 31, 2024, an increase of $1.5 million, or 11.2%, compared to $13.4 million in the same period of last year. This was due to an increase of 7.3% in sales volume, an increase of 8.5% in the average selling price of our products, and partially offset by 5.1% negative impact from exchange rate due to depreciation of RMB against US dollars, compared with that of the same period of last year.

| For the Three-Month Ended March 31, | ||||||||||||||||||||||||

| 2024 | 2023 | Change | Change | |||||||||||||||||||||

| Amount | % | Amount | % | Amount | % | |||||||||||||||||||

| (in US Dollar millions except percentage) | ||||||||||||||||||||||||

| Revenue from sales to customers in Mainland China | $ | 9.4 | 63.1 | % | $ | 9.3 | 69.4 | % | $ | 0.1 | 1.1 | % | ||||||||||||

| Revenue from sales to customers overseas | 5.5 | 36.9 | % | 4.1 | 30.6 | % | 1.4 | 34.1 | % | |||||||||||||||

| Total Revenues | $ | 14.9 | 100 | % | $ | 13.4 | 100 | % | $ | 1.5 | 11.2 | % | ||||||||||||

| For the Three-Month Ended March 31, | ||||||||||||||||||||||||

| 2024 | 2023 | Change | Change | |||||||||||||||||||||

| Unit | % | Unit | % | Unit | % | |||||||||||||||||||

| (in UNIT, except percentage) | ||||||||||||||||||||||||

| Units sold to customers in Mainland China | 432,050 | 63.4 | % | 414.518 | 65.3 | % | 17,532 | 4.2 | % | |||||||||||||||

| Units sold to customers overseas | 249,320 | 36.6 | % | 220,758 | 34.7 | % | 28,562 | 12.9 | % | |||||||||||||||

| Total Units Sold | 681,370 | 100 | % | 635,276 | 100 | % | 46,094 | 7.3 | % | |||||||||||||||

(i) PRC Domestic Market

For the three months ended March 31, 2024, revenue from the PRC domestic market increased by $0.1 million, or 1.1%, as a combined result of: (i) an increase of 4.2% in sales volume and (ii) an increase of 4.1% in the average RMB selling price of our products, and partially offset by 5.1% negative impact from exchange rate due to depreciation of RMB against US dollars, compared with that of the same period of last year.

As for the RMB selling price, the increase of 4.2% was mainly due to the increased sales of new models of higher-end products such as medical touchscreens and industrial control computer touchscreens with higher selling prices in the PRC domestic market during the three-month period ended March 31, 2024.

Due to our proactive efforts to market new models and efforts to obtain new customers and penetrate into new regions, our sales increased by 16.9% in Southwest China, and 11.0% in South China, partially offset by a decrease of 1.2% in East China during the three months ended March 31, 2024.

(ii) Overseas Market

For the three-month period ended March 31, 2024, revenues from the overseas market were $5.5 million as compared to $4.1 million of the same period of 2023, representing an increase by $1.4 million, or 34.1%, mainly due to an increase of 12.9% in sales volume due to increased sales in industrial control computer touchscreens, automotive touchscreens and gaming touchscreens, and an increase of 18.1% in average selling price in RMB in these touchscreen products.

3

The following table summarizes the breakdown of revenues by categories in US dollars:

|

Revenues For the Three-Month Ended March 31, |

||||||||||||||||||||||||

| 2024 | 2023 | Change | Change | |||||||||||||||||||||

| Amount | % | Amount | % | Amount | Margin% | |||||||||||||||||||

| (in US Dollars, except percentage) | ||||||||||||||||||||||||

| Product categories by end applications | ||||||||||||||||||||||||

| Automotive Touchscreens | $ | 4,185,270 | 28.1 | % | $ | 3,234,836 | 24.1 | % | $ | 950,434 | 29.4 | % | ||||||||||||

| Industrial Control Computer Touchscreens | 2,847,660 | 19.2 | % | 2,672,250 | 19.9 | % | 175,410 | 6.6 | % | |||||||||||||||

| POS Touchscreens | 2,114,099 | 14.2 | % | 2,066,774 | 15.4 | % | 47,325 | 2.3 | % | |||||||||||||||

| Gaming Touchscreens | 2,172,475 | 14.6 | % | 1,911,297 | 14.2 | % | 261,178 | 13.7 | % | |||||||||||||||

| Medical Touchscreens | 2,414,961 | 16.2 | % | 2,094,242 | 15.6 | % | 320,719 | 15.3 | % | |||||||||||||||

| Multi-Functional Printer Touchscreens | 1,142,794 | 7.7 | % | 1,454,062 | 10.8 | % | (311,268 | ) | (21.4 | )% | ||||||||||||||

| Total Revenues | $ | 14,877,259 | 100.0 | % | $ | 13,433,461 | 100.0 | % | $ | 1,443,798 | 11.2 | % | ||||||||||||

| * | Others include applications in self-service kiosks, ticket vending machines and financial terminals. |

The Company continued to shift production mix from traditional lower-end products to high-end products such as automotive touchscreens, medical touchscreens, gaming touchscreens, and industrial control computer touchscreens, primarily due to (i) greater growth potential of computer screen models in China and overseas market, and (ii) the stronger demand on higher-end touch screens made with better materials and better quality.

Gross Profit and Gross Profit Margin

| Three-Month Period Ended March 31, | Change | |||||||||||||||

| (in millions, except percentage) | 2024 | 2023 | Amount | % | ||||||||||||

| Gross Profit | $ | 3.3 | $ | 6.0 | $ | (2.7 | ) | (45.0 | )% | |||||||

| Gross Profit Margin | 22.4 | % | 45.0 | % | (22.6 | )% | ||||||||||

Gross profit was $3.3 million in the first quarter ended March 31, 2024, compared to $6.0 million in the same period of 2023. Our gross profit margin decreased to 22.4% for the first quarter ended March 31, 2024, as compared to 45.0% for the same period of 2023, primarily due to the increase of cost of goods sold by 56.7% resulting from the increase of costs of raw materials. Our cost of raw materials was increased by 66.9% due to (i) export controls imposed by U.S. Department of Commerce on advanced computing and semiconductor manufacturing to the People’s Republic of China, and (ii) production under capacity of other raw materials during the first quarter of 2024 because of holiday season of Chinese Spring Festival.

The management has forecasted the procurement costs of the chip and other categories of raw material will come to stabilize due to supplier production becoming normalized after the second quarter of 2024.

Selling Expenses

| Three-Month Period Ended March 31, |

Change | |||||||||||||||

| (in US dollars, except percentage) | 2024 | 2023 | Amount | % | ||||||||||||

| Selling Expenses | $ | 459,792 | $ | 50,705 | $ | 409,087 | 806.8 | % | ||||||||

| as a percentage of revenues | 3.4 | % | 0.0 | % | 3.4 | % | ||||||||||

Selling expenses were $459,792 million for the three-month period ended March 31, 2024, compared to $50,705 in the same period in 2023, representing an increase of $0.5 million. The increase was primarily due to the increase of $0.3 million traveling expenses, $0.1 million logistic expenses to market our products and other miscellaneous selling expenses during the three months ended March 31,2024.

General and Administrative Expenses

| Three-Month Period Ended March 31, | Change | |||||||||||||||

| (in millions, except percentage) | 2024 | 2023 | Amount | % | ||||||||||||

| General and Administrative Expenses | $ | 0.5 | $ | 1.7 | $ | (1.2 | ) | (70.6 | )% | |||||||

| as a percentage of revenues | 3.4 | % | 12.7 | % | (9.3 | )% | ||||||||||

General and administrative expenses were $0.5 million for the three-month period ended March 31, 2024, compared to $1.7 million in the same period in 2023, representing a decrease of $1.2 million, or 70.6%. The decrease was primarily due to full payment of an accrued $1.2 million private placement agent fees in connection with a private placement during the three months ended March 31, 2023. The Company made the full payment in February, 2024. (see Note 8 of the accompanying financial statements).

4

Research and Development Expenses

| Three-Month Period Ended March 31, | Change | |||||||||||||||

| (in US dollars, except percentage) | 2024 | 2023 | Amount | % | ||||||||||||

| Research and Development Expenses | $ | 42,738 | $ | 20,885 | $ | 21,853 | 104.6 | % | ||||||||

| as a percentage of revenues | 0.0 | % | 0.0 | % | 0.0 | % | ||||||||||

Research and development expenses were $42,738 for three-month period ended March 31, 2024 compared to $20,885 in the same period in 2023, representing an increase of $21,853, which was due to an increase in material consumption.

Operating Income

Total operating income was $2.3 million for the three-month period ended March 31, 2024 as compared to $4.3 million of the same period of last year, primarily due to lower gross margin and higher selling expenses, partially offset by lower general and administrative expenses for the three-month period ended March 31, 2024.

Gain (loss) on Changes in Fair Value of Common Stock Purchase Warrants

| Three-Month Period Ended March 31, | Change | |||||||||||||||

| (in millions, except percentage) | 2024 | 2023 | Amount | % | ||||||||||||

| Gain (loss) on changes in fair value of common stock purchase warrants | $ | 0.0 | $ | (0.1 | ) | $ | 0.1 | (100,0 | )% | |||||||

| as a percentage of revenues | 0.0 | % | 0.7 | % | (0.7 | )% | ||||||||||

Gain on changes in fair value of common stock purchase warrants for the three-month period ended March 31, 2024 was $7,821, compared to $97,602 of loss on changes in fair value of common stock purchase warrants in 2023.

(See Note 9 (b) of the accompanying financial statements).

Interest Expenses

| Three-Month Period Ended March 31, | Change | |||||||||||||||

| (in millions, except percentage) | 2024 | 2023 | Amount | % | ||||||||||||

| Interest Expenses | $ | 1.2 | $ | 0.0 | $ | 1.2 | N/A | |||||||||

| as a percentage of revenues | 8.1 | % | 0.0 | % | 8.1 | % | ||||||||||

For the three-month period ended March 31, 2024 and 2023, the Company recognized interest expenses of convertible promissory notes in the amount of $1,169,974 (mainly the default interest charges of $1,145,995 upon the repayment of the notes payable) and $33,399, respectively. (See Note 9 (a) of the accompanying financial statements).

Income Taxes

| Three-Month Period Ended March 31, | Change | |||||||||||||||

| (in millions, except percentage) | 2024 | 2023 | Amount | % | ||||||||||||

| Income before Income Taxes | $ | 1.2 | $ | 4.2 | $ | (3.0 | ) | (71.4 | )% | |||||||

| Income Tax (Expense) | (0.6 | ) | (1.4 | ) | 0.8 | (57.1 | )% | |||||||||

| Effective income tax rate | 25.4 | % | 33.5 | % | 5.4 | % | ||||||||||

The effective income tax rates for the three-month period ended March 31, 2024 and 2023 were 25.4% and 33.5%, respectively.

Net Income

As a result of the above factors, we had a net income of $0.6 million in the first quarter of 2024 compared to a net income of $2.8 million in the same quarter of 2023.

Liquidity and Capital Resources

Historically, our primary uses of cash have been to finance working capital needs. We expect that we will be able to meet our needs to fund operations, capital expenditures and other commitments in the next 12 months primarily with our cash and cash equivalents, operating cash flows and bank borrowings.

We may, however, require additional cash resources due to changes in business conditions or other future developments. If these sources are insufficient to satisfy our cash requirements, we may seek to sell additional equity or debt securities or obtain a credit facility. The sale of additional equity or equity-linked securities could result in additional dilution to stockholders. The incurrence of indebtedness would result in increased debt service obligations and could result in operating and financial covenants that would restrict operations. Financing may not be available in amounts or on terms acceptable to us, or at all.

5

As of March 31, 2024, we had current assets of $110.0 million, consisting of $94.8 million in cash, $10.9 million in accounts receivable, $0.2 million in inventories, and $4.1 million in prepaid expenses and other current assets Our current liabilities as of March 31, 2024 were $2.2 million, which is comprised of $0.6 million in accounts payable, $0.4 million in loan from a third party, $0.6 million in income tax payable, $0.6 million in accrued expenses and other current liabilities.

The following is a summary of our cash flows provided by (used in) operating, investing, and financing activities for the three-month periods ended March 31, 2024 and 2023:

| Three-Month Period Ended March 31, |

||||||||

| (in US Dollar millions) | 2024 | 2023 | ||||||

| Net cash (used in) provided by operating activities | $ | (9.2 | ) | $ | 2.7 | |||

| Net cash used in investing activities | (0.1 | ) | - | |||||

| Net cash provided by financing activities | 7.5 | 40.0 | ||||||

| Effect of foreign currency exchange rate changes on cash and cash equivalents | (1.4 | ) | (0,7 | ) | ||||

| Net (decrease) increase in cash and cash equivalents | (3.2 | ) | 42.0 | |||||

| Cash and cash equivalents at the beginning of period | 98.0 | 51.3 | ||||||

| Cash and cash equivalents at the end of period | $ | 94.8 | $ | 93.3 | ||||

Operating Activities

Net cash used in operating activities was $9.2 million for the three months ended March 31, 2024 as compared to $2.7 million provided by operating activities for the same period of the last year, primarily due to (i) the decrease of $2.2 million net income for the three months ended March 31, 2024 as compared to the same period of 2023, (ii) the decrease of $0.1 million gain on changes of fair value of common stock purchase warrants for the three months ended March 31, 2024, (iii) the increase of $0.2 million in inventories, and $3.4 million in prepaid and other current assets, (iv) the decrease of $0.8 million in accounts payable, $0.7 million in income tax payable, and $4.5 million in accrued expenses and other current liabilities, partially offset by (v) the decrease of $0.4 million in accounts receivable for the three months ended March 31, 2024.

Investing Activities

Net cash used in investing activities for the three-month period ended March 31, 2024 was $0.1 million for the purchase of property, plant and equipment.

There was no cash flow in investing activities for the three-month period ended March 31, 2023.

Financing Activities

Net cash provided by financing activities for the three months ended March 21, 2024 was $7.5 million, including $9.0 million in net proceeds from the 2024 Public Offering, partially offset by $1.4 million repayment of convertible promissory notes, and $82,864 repayment of interest-free advances to a third party.

Net cash provided by financing activities for the three months ended March 31, 2023 was $40.0 million, including $40.0 million in proceeds from stock issuance in a private placement, and $86,735 in proceeds from interest-free advances from a third party, partially offset by the repayment of $35,000 convertible promissory note payable.

As of March 31, 2024, our cash and cash equivalents were $94.8 million, as compared to $98.0 million at December 31, 2023.

Days Sales Outstanding (“DSO”) has decreased to 56 days for the three-month period ended March 31, 2024 from 77 days for the year ended December 31, 2023.

The following table provides an analysis of the aging of accounts receivable as of March 31, 2024 and December 31, 2023:

| March 31, 2024 | December 31 2023 | |||||||

| -Current | $ | 4,561,092 | $ | 3,740,488 | ||||

| -1-3 months past due | 5,925,002 | 2,635,045 | ||||||

| -4-6 months past due | 451,746 | 1,079,719 | ||||||

| Total accounts receivable | $ | 10,937,840 | $ | 7,455,252 | ||||

The majority of the Company’s revenues and expenses were denominated in Renminbi (“RMB”), the currency of the People’s Republic of China. There is no assurance that exchange rates between the RMB and the U.S. Dollar will remain stable. Inflation has not had a material impact on the Company’s business.

Based on past performance and current expectations, we believe our cash and cash equivalents provided by operating activities and financing activities will satisfy our working capital needs, capital expenditures and other liquidity requirements associated with our operations for at least the next 12 months.

6

Holding Company Structure

There have been no changes to the Company’s holding company structure during the three months ended March 31, 2024. For more details, refer to the Company’s holding company structure disclosures set forth in Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations- Holding Company Structure” of the 2023 Form 10-K.

Cash and Other Assets Transfers between the Holding Company and Its Subsidiaries

Please see “ITEM 7- Management’s Discussion and Analysis of Financial Condition and Results of Operations- Cash and Other Assets Transfers between the Holding Company and Its Subsidiaries” of the 2023 Form 10-K for more details.

Commitments and Contingencies

Contingencies

The Company’s common stock began trading on the Nasdaq Capital Market under the ticker symbol “WETH” on February 21, 2024. The Company failed to timely complete the filing procedures with China Securities Regulatory Commission (“CSRC”) on overseas initial public offering and transfer of listing as regulated below:

1) Per Article 13 and Article 8 and Article 25 of CSRC Announcement (2023) No. 43 -Trial Measures for the Administration of Overseas Issuance and Listing of Securities for Domestic Enterprises” (“Trial Measures” Announcement No. 43), which was implemented on March 31, 2023 ( http://www.csrc.gov.cn/csrc/c101954/c7124478/content.shtml), when an issuer conducts an overseas initial public offering or listing, it shall submit overseas issuance and listing application documents to CSRC within three working days; When a domestic enterprise transfers its listing overseas, it shall comply with the requirements of the overseas first public listing requirements for issuance and listing, and shall file with the CSRC within 3 working days, after its submitting application documents for transfer and listing overseas.

2) Article 27 of Trial Measures Announcement No. 43 stipulates that if a domestic enterprise violates the provisions of Article 13 of these Measures and fails to perform the filing procedures, or violates the provisions of Articles 8 and 25 of these Measures for overseas issuance and listing, CSRC shall order it to make corrections and give a warning, and impose a fine of not less than RMB 1 million but not more than RMB 10 million.

As of the date of this Quarterly Report, the Company has not received any notice of penalty from the CSRC. Management will closely monitor any notice or action from CSRC.

Capital Expenditure Commitment

As of March 31, 2024, the Company had construction commitment of RMB5.0 million (equivalent to $0.7 million).

Off Balance Sheet Arrangements

We have no off balance sheet arrangements.

Critical Accounting Policies

The preparation of financial statements and related disclosures in conformity with GAAP and the Company’s discussion and analysis of its financial condition and operating results require the Company’s management to make judgments, assumptions and estimates that affect the amounts reported. Note 2, “SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES” of the Notes to Condensed Consolidated Financial Statements in Part I, Item 1 of this Form 10-Q and in the Notes to Consolidated Financial Statements in Part II, Item 8 of the 2023 Form 10-K describe the significant accounting policies and methods used in the preparation of the Company’s condensed consolidated financial statements. There have been no material changes to the Company’s critical accounting estimates since the 2023 Form 10-K.

Item 3. Quantitative and Qualitative Disclosures About Market Risk.

Not applicable for smaller reporting companies.

Item 4. Controls and Procedures.

Evaluation of Disclosure Controls and Procedures

Under supervision and with the participation of our management, including our Chief Executive Officer and Chief Financial Officer (our “Certifying Officers”), we evaluated the effectiveness of our disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) under the Exchange Act) as of March 31, 2024. Based upon that evaluation, our Chief Executive Officer and Chief Financial Officer concluded that our disclosure controls and procedures were not effective as of March 31, 2024, as a result of the material weakness identified below.

In light of this material weakness, we performed additional analysis as deemed necessary to ensure that our financial statements were prepared in accordance with U.S. GAAP. Based on such analysis and notwithstanding the identified material weakness, management, including our Chief Executive Officer and Chief Financial Officer, believe the unaudited condensed consolidated financial statements included in this Quarterly Report fairly represent in all material respects our financial condition, results of operations and cash flows at and for the periods presented in accordance with U.S. GAAP.

7

Material Weakness

In connection with the audit of the financial year ended December 31, 2023, we identified certain control deficiencies in the design and operation of our internal controls over our financial reporting that constituted a material weakness in aggregation. A “material weakness” is a deficiency, or a combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of our company’s annual or interim financial statements will not be prevented or detected on a timely basis.

The material weaknesses related to internal control over financial reporting that was identified during the annual report of 2023 and still applied as of March 31, 2024 were:

| ● | Inadequate segregation of duties consistent with control objectives; |