Exhibit 99.1

Developing Cutting - Edge Treatments for Debilitating Fibrotic and Neurodegenerative Diseases Corporate Presentation March 2022

Disclaimer and Other Important Information 2 This Presentation (the “Presentation”) is for informational purposes only to assist interested parties in evaluating the busi nes s of Blade Therapeutics, Inc. (the “Target”). The Target and Biotech Acquisition Company ("BAC") have entered into a proposed initial business combination (the “Transaction” or “Business Combina tio n”), pursuant to which the Target will become a wholly - owned subsidiary of BAC. In connection with the closing of the Business Combination, BAC will re - domesticate as a Delaware corp oration and will change its name to “Blade Biotherapeutics, Inc.” The continuing combined entity is hereinafter referred to as the “Company” or the “Combined Entity”. The information contained herein does not purport to be all - inclusive and none of the Target, nor any of its subsidiaries, stock holders, affiliates, representatives, control persons, partners, members, managers, directors, officers, employees, advisers, contract counterparties or agents make any representation or war ran ty, express or implied, as to the accuracy, completeness or reliability of the information contained in this Presentation. Recipients should consult with their own counsel and tax and f ina ncial advisors as to legal and related matters concerning the matters described herein, and, by accepting this Presentation, you confirm that you are not relying upon the information cont ain ed herein to make any investment decision. To the fullest extent permitted by law, in no circumstances will the Target or any of its subsidiaries, stockholders, affiliates, representa tiv es, control persons, partners, members, managers, directors, officers, employees, advisers, contract counterparties or agents be responsible or liable for any direct, indirect or consequ ent ial loss or loss of profit arising from the use of this Presentation, its contents, its omissions, reliance on the information contained within it, or on opinions communicated in relation thereto or oth erwise arising in connection therewith. In addition, this Presentation does not purport to be all - inclusive or to contain all of the information that may be required to make a full analy sis of BAC, the Target, or the Business Combination. The general explanations included in this Presentation cannot address, and are not intended to address, your specific investment objectiv es, financial situations or financial needs. In connection with the proposed Business Combination, BAC intends to file with the Securities and Exchange Commission (the “S EC” ), a registration statement on Form S - 4, containing a preliminary proxy statement/prospectus of BAC. After the registration statement is declared effective, BAC will mail a defini tiv e proxy statement/prospectus relating to the proposed Business Combination to its shareholders. This Presentation is not intended to constitute the basis of any voting or investment decis ion in respect of the Business Combination or the securities of BAC. BAC’s and the Target’s respective shareholders and other interested persons are advised to read, when available, the prelimin ary proxy statement/prospectus and the amendments thereto and the definitive proxy statement/prospectus and other documents filed in connection with the proposed Business Combination, as these materials will contain important information about BAC, the Target and the Business Combination. Shareholders will also be able to obtain copies of the preliminary proxy statem ent /prospectus, the definitive proxy statement/ prospectus and other documents filed with the SEC, without charge, once available, at the SEC’s website at www.sec.gov, or by directing a re que st to: Biotech Acquisition Company, 545 West 25th Street, 20th Floor, New York, NY 10001. No Offer or Solicitation: This Presentation shall not constitute a “solicitation” as defined in Section 14 of the Exchange A ct. This Presentation does not constitute (i) a solicitation of a proxy, consent or authorization with respect to any securities or in respect of the Business Combination or (ii) an offer to sell, a so licitation of an offer to buy, or a recommendation to purchase any security of BAC, the Target, or any of their respective affiliates nor shall there be any sale of securities, investment or o the r specific product in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. NEITHER THE SEC NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THE SECURITIES OR DETERMINED IF THIS PRESE NTA TION IS TRUTHFUL OR COMPLETE.

Disclaimer and Other Important Information (cont’d) 3 Certain statements included in this Presentation are not historical facts but are forward - looking statements. Forward - looking st atements generally are accompanied by words such as "believe," "may," "will," "estimate," "continue," "anticipate," "intend," "expect," "should," "would," "plan," "future," "outlook," and sim ilar expressions, but the absence of these words does not mean that a statement is not forward - looking. These forward - looking statements include, but are not limited to, statements regarding estimates and forecasts of other performance metrics and projections of market opportunity. These statements are based on various assumptions, whether or not identified in this Prese nta tion, and on the current expectations of the Target’s management and are not predictions of actual performance. These forward - looking statements are provided for illustrative purpose s only and are not intended to serve as, and must not be relied on by any person as, a guarantee, an assurance, a prediction or a definitive statement of fact or probability. Actual eve nts and circumstances are difficult or impossible to predict and will differ from assumptions. Many actual events and circumstances are beyond the control of BAC and the Target. Some important f act ors that could cause actual results to differ materially from those in any forward - looking statements could include changes in domestic and foreign business, market, financial, political and legal conditions. These forward - looking statements are subject to a number of risks and uncertainties, including the ability to protect and enhanc e the Target’s respective corporate reputation and brand; the impact from future regulatory, judicial, and legislative changes in the Target’s or the Company’s industry; the timing, costs , c onduct, and outcome of clinical trials and future preclinical studies and clinical trials, including the timing of the initiation and availability of data from such trials; the timing and likelih ood of regulatory filings and approvals for product candidates; whether regulatory authorities determine that additional trials or data are necessary in order to obtain approval; the potential mark et size and the size of the patient populations for product candidates, if approved for commercial use, and the market opportunities for product candidates; the ability to locate and ac qui re complementary products or product candidates and integrate those into the Company’s business; and, the uncertain effects of the COVID - 19 pandemic; and those factors set forth in documents of BAC filed, or to be filed, with SEC. The foregoing list of risks is not exhaustive. If any of these risks materialize or our assumptions prove incorrect, actual results could differ materially from the results im plied by these forward - looking statements. There may be additional risks that are presently unknown or that the Target currently believes are immaterial that could also cause actual results to di ffer from those contained in the forward - looking statements. The data contained herein are derived from various internal and external sources. No representation is made as to the reasonablen ess of the assumptions made within or the accuracy or completeness of any projections or modeling or any other information contained herein. Any data on past performance or modeli ng contained herein are not an indication as to future performance. Recipients of this Presentation should conduct their own independent evaluation and due diligence of the Target. The Target d oes not intend to update or otherwise revise this Presentation following its distribution and the Target makes no representation or warranty, express or implied, as to the accuracy or comp let eness of any of the information contained in this Presentation after the date of the Presentation.

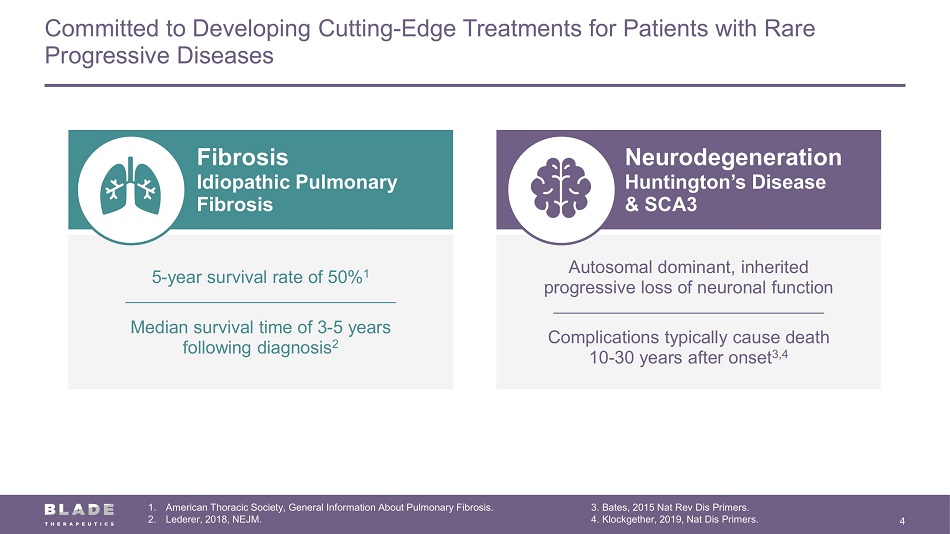

Committed to Developing Cutting - Edge Treatments for Patients with Rare Progressive Diseases 4 5 - year survival rate of 50% 1 Median survival time of 3 - 5 years following diagnosis 2 Neurodegeneration Huntington’s Disease & SCA3 Fibrosis Idiopathic Pulmonary Fibrosis Autosomal dominant, inherited progressive loss of neuronal function Complications typically cause death 10 - 30 years after onset 3,4 1. American Thoracic Society, General Information About Pulmonary Fibrosis. 2. Lederer, 2018, NEJM. 3. Bates, 2015 Nat Rev Dis Primers. 4. Klockgether, 2019, Nat Dis Primers.

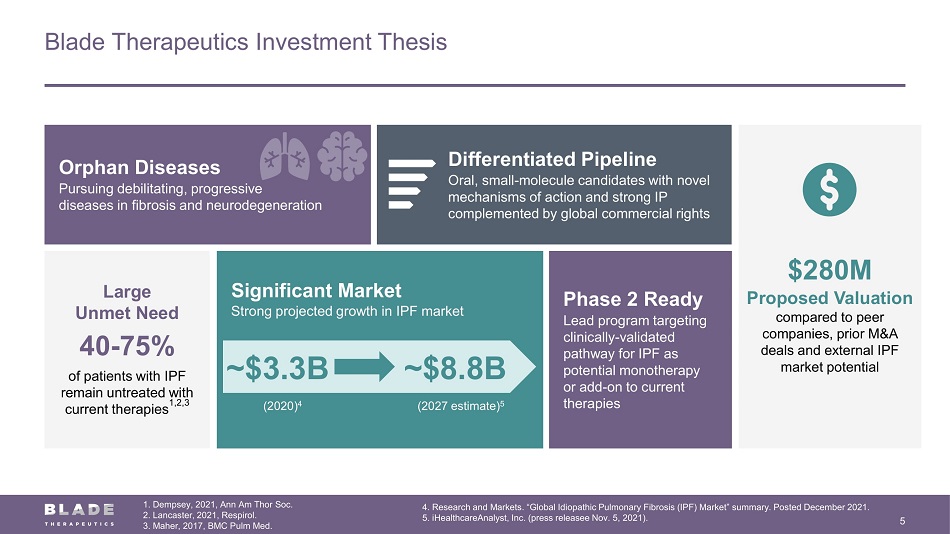

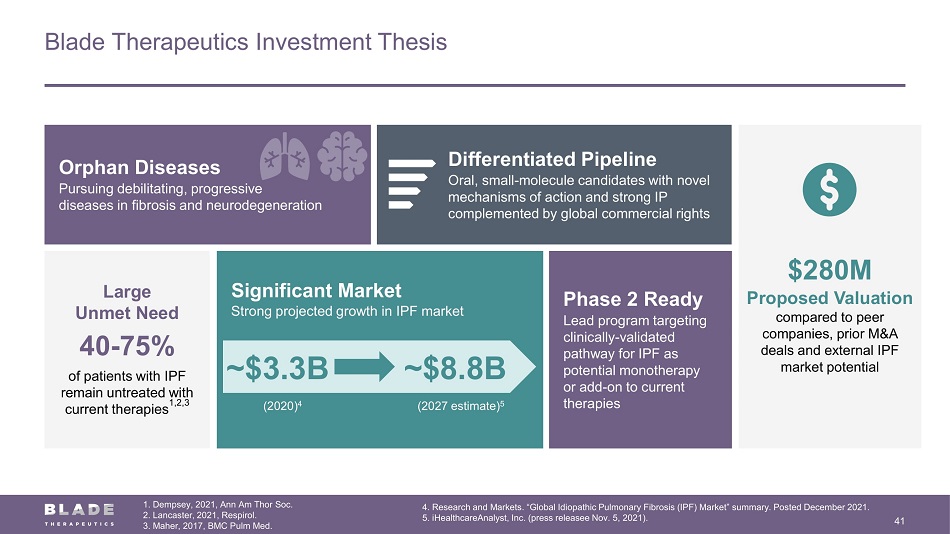

Blade Therapeutics Investment Thesis 5 4. Research and Markets. “Global Idiopathic Pulmonary Fibrosis (IPF) Market” summary. Posted December 2021. 5. iHealthcareAnalyst, Inc. (press releasee Nov. 5, 2021). Orphan Diseases Pursuing debilitating, progressive diseases in fibrosis and neurodegeneration Significant Market Strong projected growth in IPF market Large Unmet Need 40 - 75% of patients with IPF remain untreated with current therapies 1,2,3 ~$3.3B ~$8.8B (2027 estimate) 5 (2020) 4 Differentiated Pipeline Oral, small - molecule candidates with novel mechanisms of action and strong IP complemented by global commercial rights Phase 2 Ready Lead program targeting clinically - validated pathway for IPF as potential monotherapy or add - on to current therapies $280M Proposed Valuation compared to peer companies, prior M&A deals and external IPF market potential 1. Dempsey, 2021, Ann Am Thor Soc. 2. Lancaster, 2021, Respirol. 3. Maher, 2017, BMC Pulm Med.

Biotech Acquisition Company Overview 6 • Nasdaq - listed SPAC (Nasdaq: BIOT) completed $230 million IPO on January 28, 2021 • SPAC affiliated with SPRIM, a global healthcare consulting firm and clinical research organization • SPRIM Global Investments is a leading life sciences venture capital firm with in - depth understanding of clinical - stage biotech companies Competitive Differentiation Decades of diverse experience operating businesses and driving value creation across 17 countries Management team has worked together for more than 20 years and has strong record of working with clinical - stage biotech companies Deep industry and life science experience

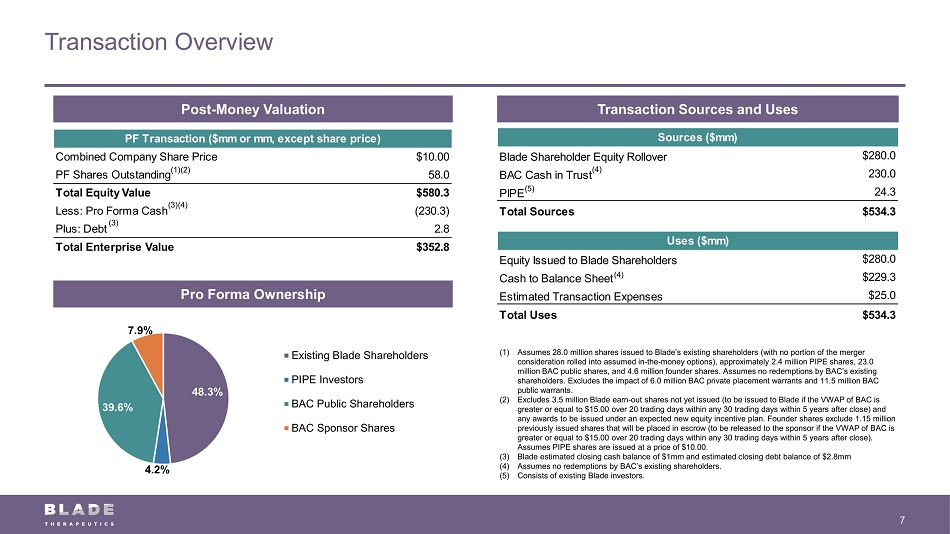

Uses ($mm) Equity Issued to Blade Shareholders $280.0 Cash to Balance Sheet $229.3 Estimated Transaction Expenses $25.0 Total Uses $534.3 Transaction Overview 7 Post - Money Valuation Transaction Sources and Uses Pro Forma Ownership (1) Assumes 28.0 million shares issued to Blade’s existing shareholders (with no portion of the merger consideration rolled into assumed in - the - money options), approximately 2.4 million PIPE shares, 23.0 million BAC public shares, and 4.6 million founder shares. Assumes no redemptions by BAC’s existing shareholders. Excludes the impact of 6.0 million BAC private placement warrants and 11.5 million BAC public warrants. (2) Excludes 3.5 million Blade earn - out shares not yet issued (to be issued to Blade if the VWAP of BAC is greater or equal to $15.00 over 20 trading days within any 30 trading days within 5 years after close) and any awards to be issued under an expected new equity incentive plan. Founder shares exclude 1.15 million previously issued shares that will be placed in escrow (to be released to the sponsor if the VWAP of BAC is greater or equal to $15.00 over 20 trading days within any 30 trading days within 5 years after close). Assumes PIPE shares are issued at a price of $10.00. (3) Blade estimated closing cash balance of $1mm and estimated closing debt balance of $2.8mm (4) Assumes no redemptions by BAC’s existing shareholders. (5) Consists of existing Blade investors. (1) (3) (3) (4) (4) (2) (4) 48.3% 4.2% 39.6% 7.9% Existing Blade Shareholders PIPE Investors BAC Public Shareholders BAC Sponsor Shares Sources ($mm) Blade Shareholder Equity Rollover $280.0 BAC Cash in Trust 230.0 PIPE 24.3 Total Sources $534.3 (5) PF Transaction ($mm or mm, except share price) Combined Company Share Price $10.00 PF Shares Outstanding 58.0 Total Equity Value $580.3 Less: Pro Forma Cash (230.3) Plus: Debt 2.8 Total Enterprise Value $352.8

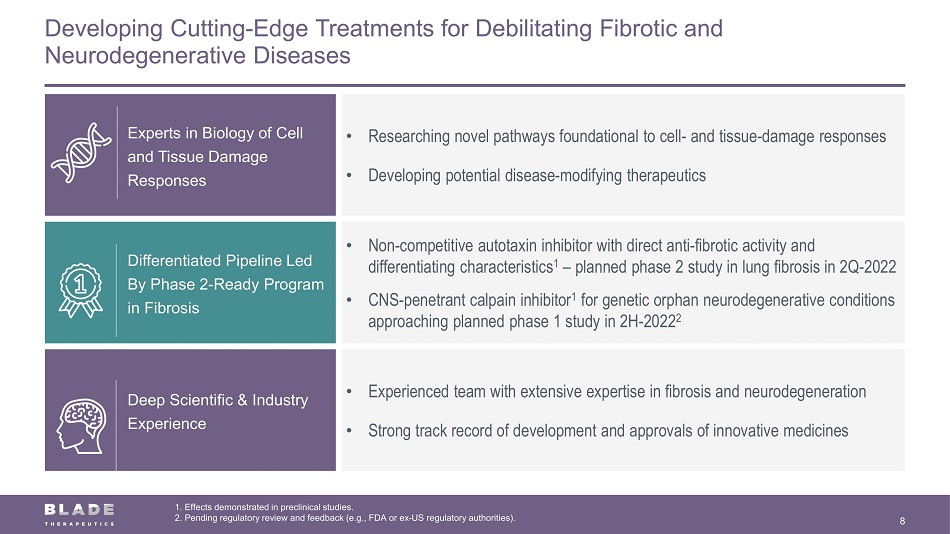

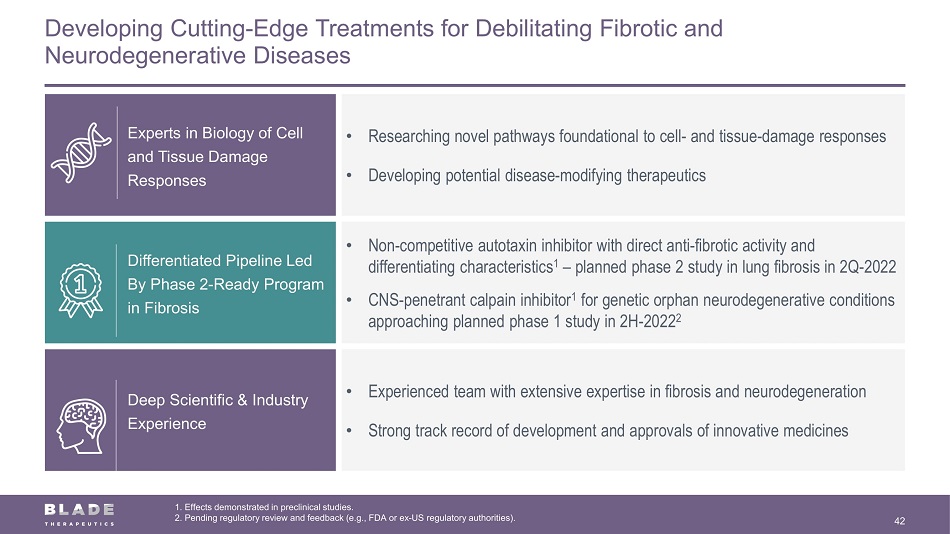

Developing Cutting - Edge Treatments for Debilitating Fibrotic and Neurodegenerative Diseases 8 1. Effects demonstrated in preclinical studies. 2. Pending regulatory review and feedback (e.g., FDA or ex - US regulatory authorities). Experts in Biology of Cell and Tissue Damage Responses • Researching novel pathways foundational to cell - and tissue - damage responses • Developing potential disease - modifying therapeutics Differentiated Pipeline Led By Phase 2 - Ready Program in Fibrosis • Non - competitive autotaxin inhibitor with direct anti - fibrotic activity and differentiating characteristics 1 – planned phase 2 study in lung fibrosis in 2Q - 2022 • CNS - penetrant calpain inhibitor 1 for genetic orphan neurodegenerative conditions approaching planned phase 1 study in 2H - 2022 2 Deep Scientific & Industry Experience • Experienced team with extensive expertise in fibrosis and neurodegeneration • Strong track record of development and approvals of innovative medicines

Leadership with Deep Scientific and Industry Experience 9 Wendye Robbins, M.D. Chief Executive Officer Jean - Frédéric Viret, Ph.D. Chief Financial Officer Prabha Ibrahim, Ph.D. Chief Technical Officer Felix Karim, Ph.D. EVP, Business Development Bassem Elmankabadi, M.D. SVP, Clinical Development Daven Mody, PharmD SVP, Regulatory Affairs Michael Blash SVP, Communications

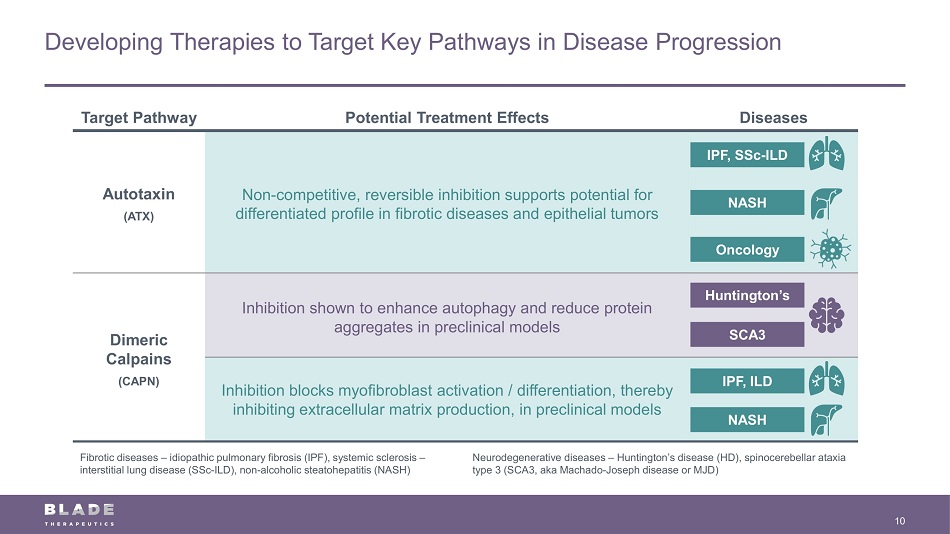

Developing Therapies to Target Key Pathways in Disease Progression 10 Target Pathway Potential Treatment Effects Diseases Autotaxin (ATX) Non - competitive, reversible inhibition supports potential for differentiated profile in fibrotic diseases and epithelial tumors Dimeric Calpains (CAPN) Inhibition shown to enhance autophagy and reduce protein aggregates in preclinical models Inhibition blocks myofibroblast activation / differentiation, thereby inhibiting extracellular matrix production, in preclinical models Huntington’s SCA3 IPF, SSc - ILD IPF, ILD NASH NASH Fibrotic diseases – idiopathic pulmonary fibrosis (IPF), systemic sclerosis – interstitial lung disease (SSc - ILD), non - alcoholic steatohepatitis (NASH) Neurodegenerative diseases – Huntington’s disease (HD), spinocerebellar ataxia type 3 (SCA3, aka Machado - Joseph disease or MJD) Oncology

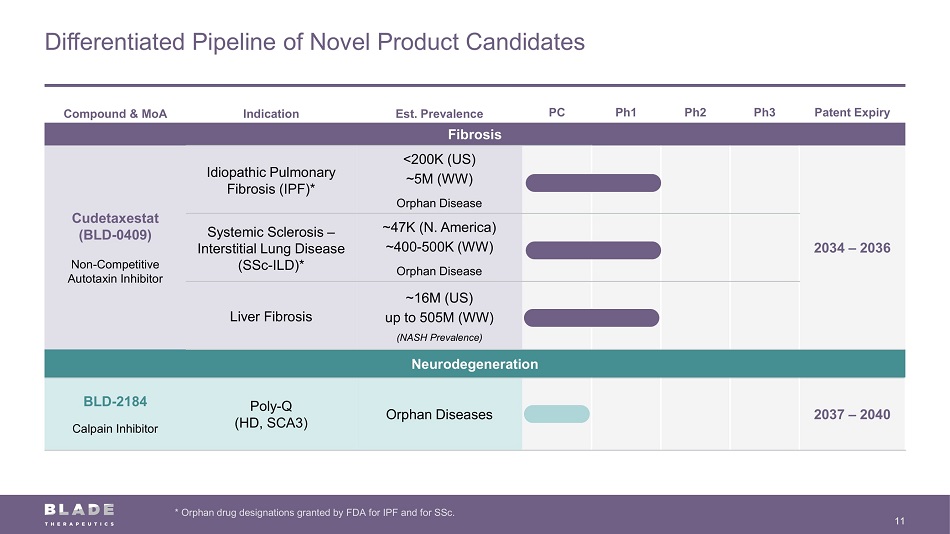

Differentiated Pipeline of Novel Product Candidates 11 * Orphan drug designations granted by FDA for IPF and for SSc. Compound & MoA Indication Est. Prevalence PC Ph1 Ph2 Ph3 Patent Expiry Fibrosis Cudetaxestat (BLD - 0409) Non - Competitive Autotaxin Inhibitor Idiopathic Pulmonary Fibrosis (IPF)* <200K (US) ~5M (WW) Orphan Disease 2034 – 2036 Systemic Sclerosis – Interstitial Lung Disease (SSc - ILD)* ~47K (N. America) ~400 - 500K (WW) Orphan Disease Liver Fibrosis ~16M (US) up to 505M (WW) (NASH Prevalence) Neurodegeneration BLD - 2184 Calpain Inhibitor Poly - Q (HD, SCA3) Orphan Diseases 2037 – 2040

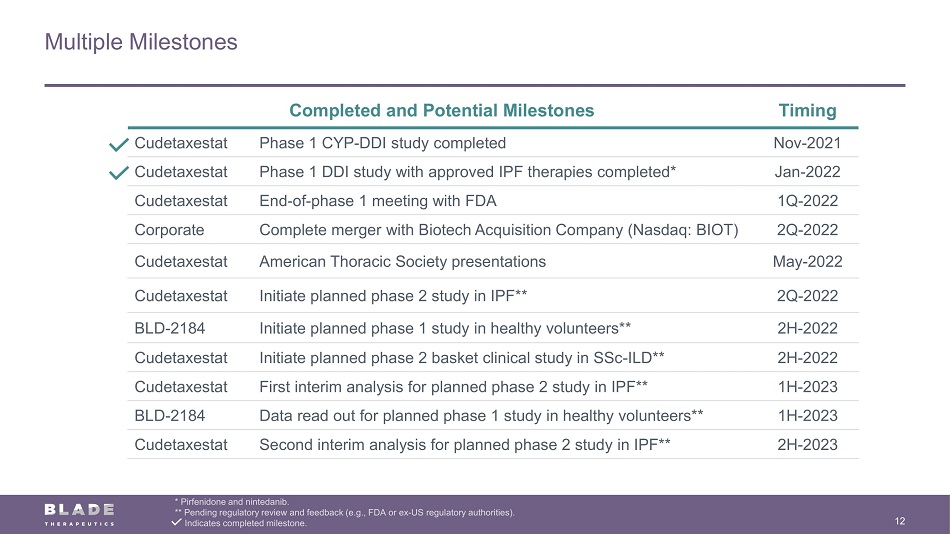

Multiple Milestones 12 * Pirfenidone and nintedanib. ** Pending regulatory review and feedback (e.g., FDA or ex - US regulatory authorities). Indicates completed milestone. Completed and Potential Milestones Timing Cudetaxestat Phase 1 CYP - DDI study completed Nov - 2021 Cudetaxestat Phase 1 DDI study with approved IPF therapies completed* Jan - 2022 Cudetaxestat End - of - phase 1 meeting with FDA 1Q - 2022 Corporate Complete merger with Biotech Acquisition Company (Nasdaq: BIOT) 2Q - 2022 Cudetaxestat American Thoracic Society presentations May - 2022 Cudetaxestat Initiate planned phase 2 study in IPF** 2Q - 2022 BLD - 2184 Initiate planned phase 1 study in healthy volunteers** 2H - 2022 Cudetaxestat Initiate planned phase 2 basket clinical study in SSc - ILD** 2H - 2022 Cudetaxestat First interim analysis for planned phase 2 study in IPF** 1H - 2023 BLD - 2184 Data read out for planned phase 1 study in healthy volunteers** 1H - 2023 Cudetaxestat Second interim analysis for planned phase 2 study in IPF** 2H - 2023

13 Fibrosis – Cudetaxestat Non - Competitive Autotaxin Inhibitor Targeting IPF

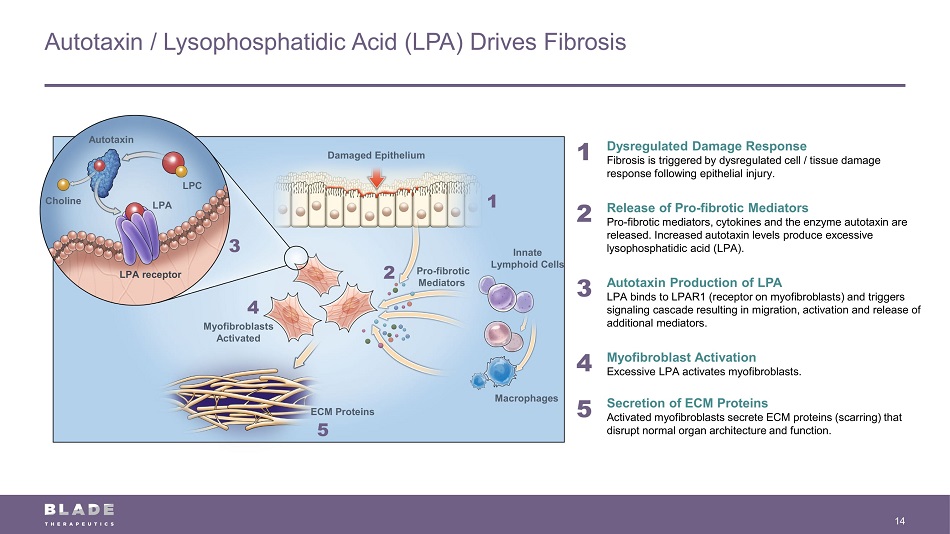

Autotaxin / Lysophosphatidic Acid (LPA) Drives Fibrosis 14 Innate Lymphoid Cells Macrophages LPA LPC LPA receptor Choline Autotaxin 1 Dysregulated Damage Response Fibrosis is triggered by dysregulated cell / tissue damage response following epithelial injury. 2 Release of Pro - fibrotic Mediators Pro - fibrotic mediators, cytokines and the enzyme autotaxin are released. Increased autotaxin levels produce excessive lysophosphatidic acid (LPA). 3 Autotaxin Production of LPA LPA binds to LPAR1 (receptor on myofibroblasts) and triggers signaling cascade resulting in migration, activation and release of additional mediators. 4 Myofibroblast Activation Excessive LPA activates myofibroblasts. 5 Secretion of ECM Proteins Activated myofibroblasts secrete ECM proteins (scarring) that disrupt normal organ architecture and function. 1 2 3 4 5 Damaged Epithelium Myofibroblasts Activated ECM Proteins Pro - fibrotic Mediators

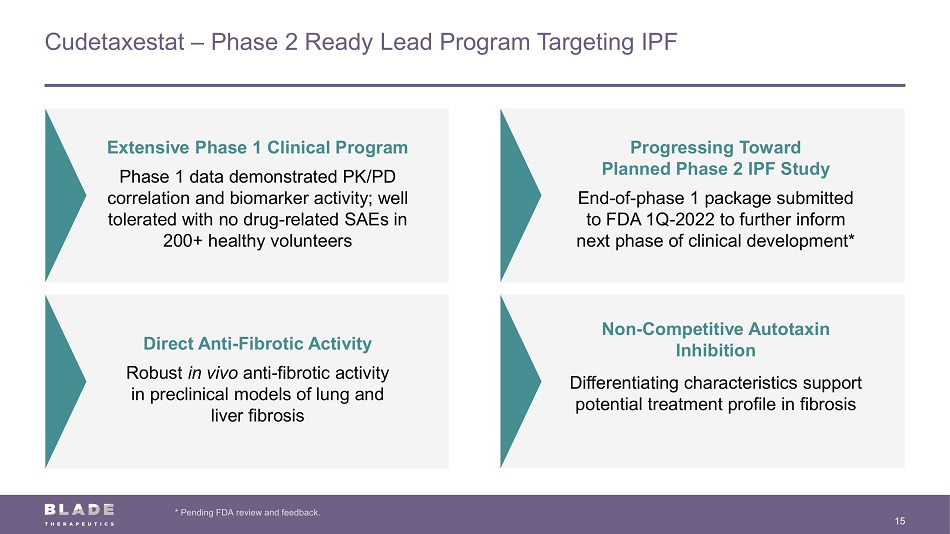

Cudetaxestat – Phase 2 Ready Lead Program Targeting IPF 15 * Pending FDA review and feedback. Direct Anti - Fibrotic Activity Robust in vivo anti - fibrotic activity in preclinical models of lung and liver fibrosis Non - Competitive Autotaxin Inhibition Differentiating characteristics support potential treatment profile in fibrosis Extensive Phase 1 Clinical Program Phase 1 data demonstrated PK/PD correlation and biomarker activity; well tolerated with no drug - related SAEs in 200+ healthy volunteers Progressing Toward Planned Phase 2 IPF Study E nd - of - phase 1 package submitted to FDA 1Q - 2022 to further inform next phase of clinical development*

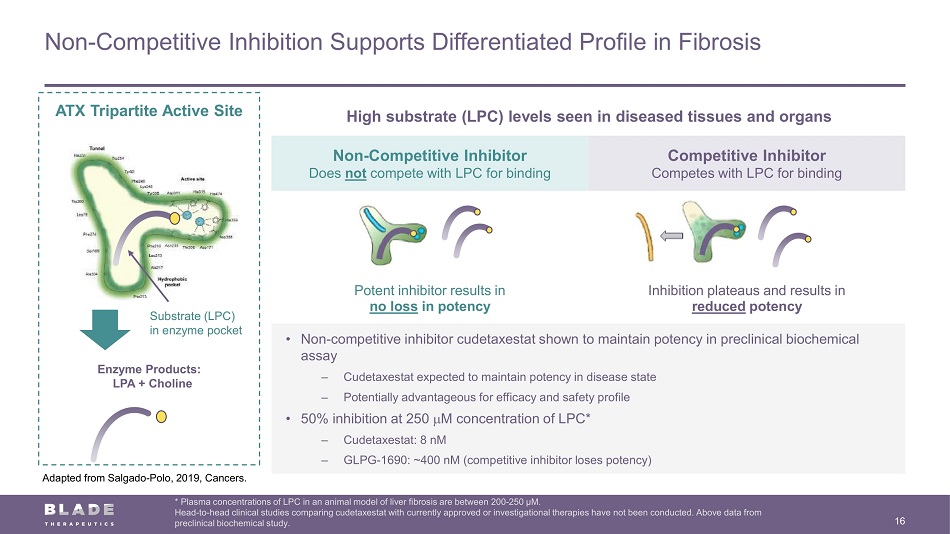

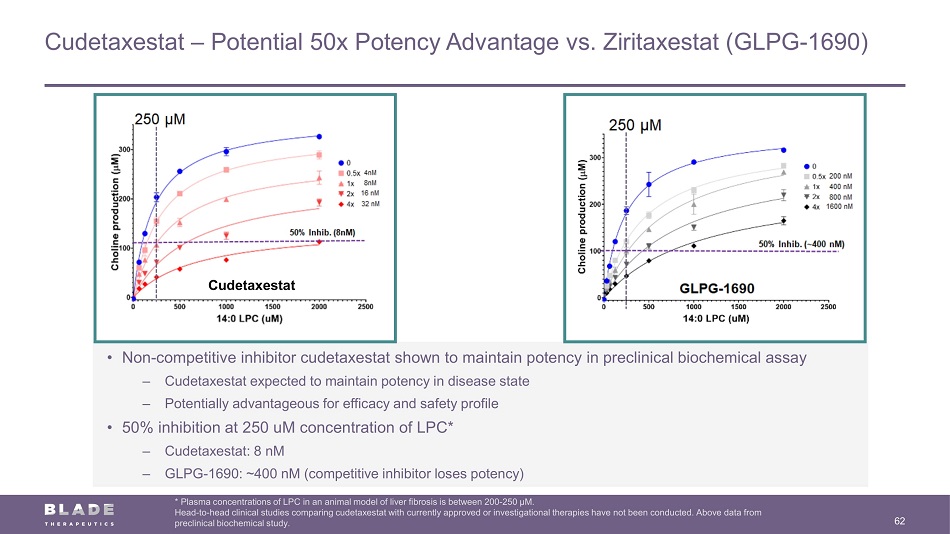

Non - Competitive Inhibitor Does not compete with LPC for binding Competitive Inhibitor Competes with LPC for binding Potent inhibitor results in no loss in potency Inhibition plateaus and results in reduced potency Non - Competitive Inhibition Supports Differentiated Profile in Fibrosis 16 * Plasma concentrations of LPC in an animal model of liver fibrosis are between 200 - 250 µM. Head - to - head clinical studies comparing cudetaxestat with currently approved or investigational therapies have not been conducte d. Above data from preclinical biochemical study. ATX Tripartite Active Site Substrate (LPC) in enzyme pocket Enzyme Products: LPA + Choline • Non - competitive inhibitor cudetaxestat shown to maintain potency in preclinical biochemical assay – Cudetaxestat expected to maintain potency in disease state – Potentially advantageous for efficacy and safety profile • 50% inhibition at 250 m M concentration of LPC* – Cudetaxestat: 8 nM – GLPG - 1690: ~400 nM (competitive inhibitor loses potency) High substrate (LPC) levels seen in diseased tissues and organs Adapted from Salgado - Polo, 2019, Cancers.

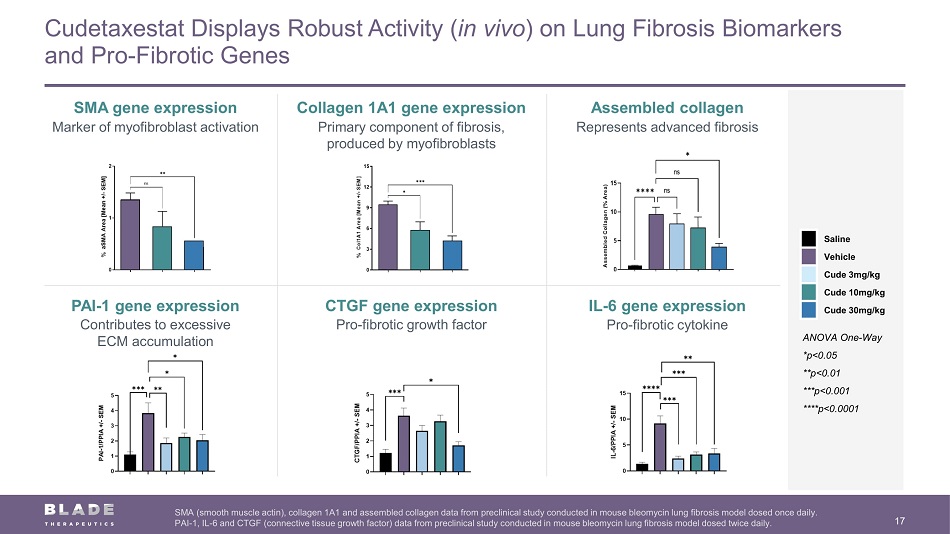

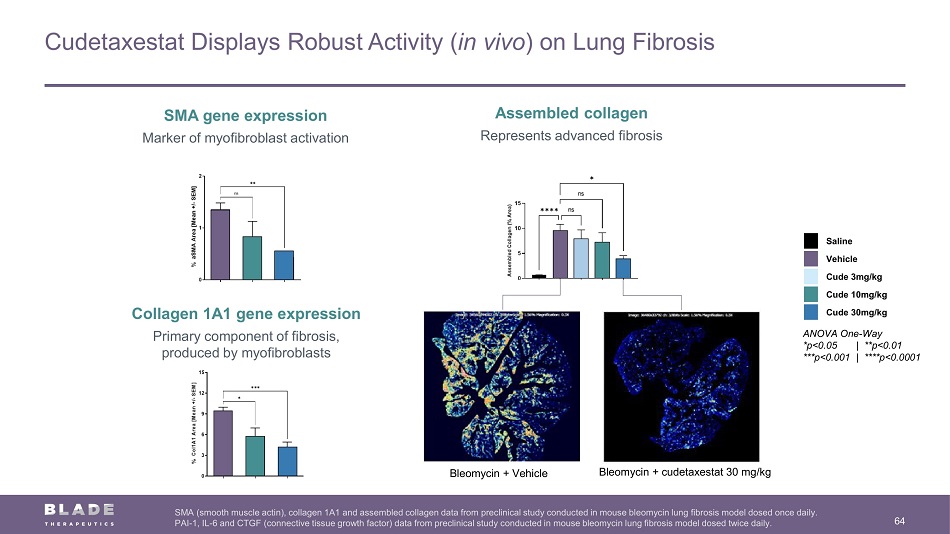

Cudetaxestat Displays Robust Activity ( in vivo ) on Lung Fibrosis Biomarkers and Pro - Fibrotic Genes 17 SMA (smooth muscle actin), collagen 1A1 and assembled collagen data from preclinical study conducted in mouse bleomycin lung fib rosis model dosed once daily. PAI - 1, IL - 6 and CTGF (connective tissue growth factor) data from preclinical study conducted in mouse bleomycin lung fibrosis mo del dosed twice daily. SMA gene expression Marker of myofibroblast activation PAI - 1 gene expression Contributes to excessive ECM accumulation Assembled collagen Represents advanced fibrosis IL - 6 gene expression Pro - fibrotic cytokine Collagen 1A1 gene expression Primary component of fibrosis, produced by myofibroblasts CTGF gene expression Pro - fibrotic growth factor ANOVA One - Way *p<0.05 **p<0.01 ***p<0.001 ****p<0.0001 Saline Vehicle Cude 3mg/kg Cude 10mg/kg Cude 30mg/kg

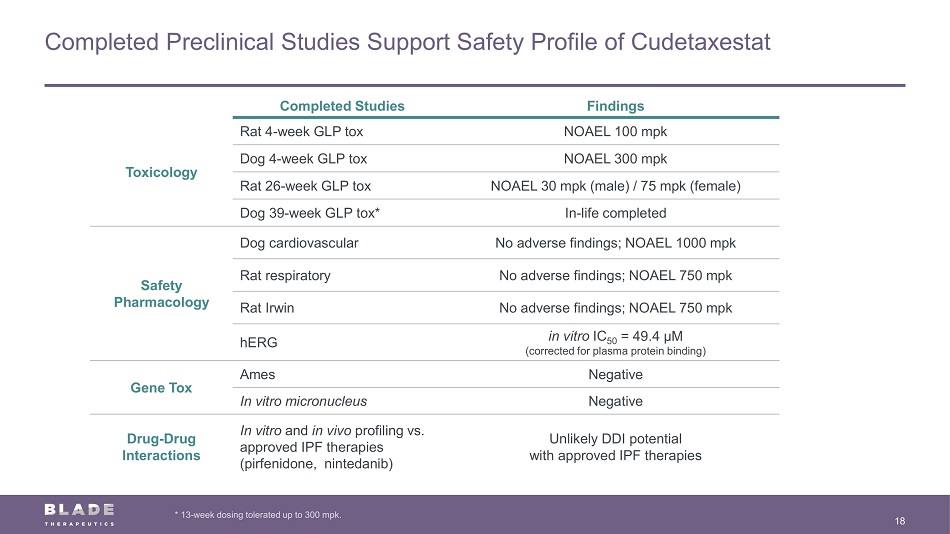

Completed Preclinical Studies Support Safety Profile of Cudetaxestat 18 * 13 - week dosing tolerated up to 300 mpk. Completed Studies Findings Toxicology Rat 4 - week GLP tox NOAEL 100 mpk Dog 4 - week GLP tox NOAEL 300 mpk Rat 26 - week GLP tox NOAEL 30 mpk (male) / 75 mpk (female) Dog 39 - week GLP tox* In - life completed Safety Pharmacology Dog cardiovascular No adverse findings; NOAEL 1000 mpk Rat respiratory No adverse findings; NOAEL 750 mpk Rat Irwin No adverse findings; NOAEL 750 mpk hERG in vitro IC 50 = 49.4 µM (corrected for plasma protein binding) Gene Tox Ames Negative In vitro micronucleus Negative Drug - Drug Interactions In vitro and in vivo profiling vs. approved IPF therapies (pirfenidone, nintedanib) Unlikely DDI potential with approved IPF therapies

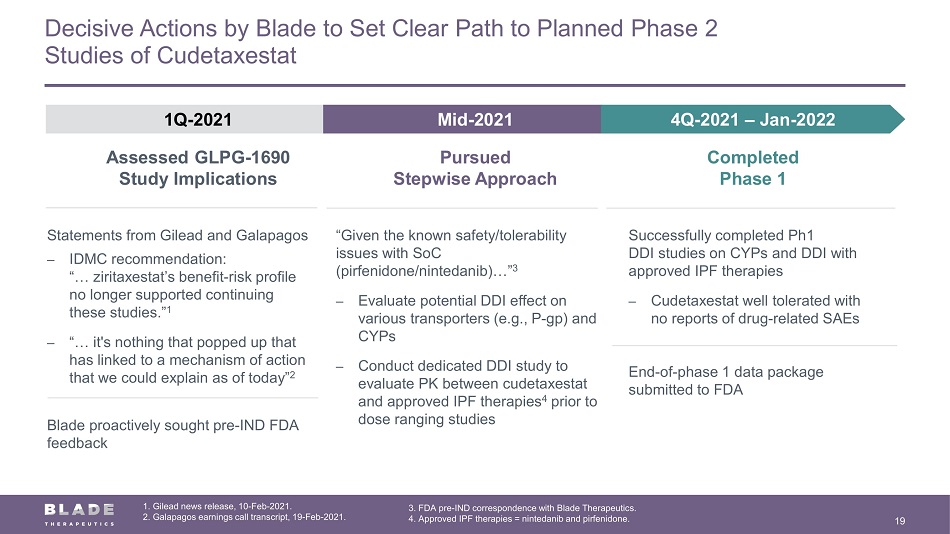

Decisive Actions by Blade to Set Clear Path to Planned Phase 2 Studies of Cudetaxestat 19 Completed Phase 1 4Q - 2021 – Jan - 2022 1Q - 2021 Assessed GLPG - 1690 Study Implications Successfully completed Ph1 DDI studies on CYPs and DDI with approved IPF therapies ‒ Cudetaxestat well tolerated with no reports of drug - related SAEs End - of - phase 1 data package submitted to FDA “Given the known safety/tolerability issues with SoC (pirfenidone/nintedanib)…” 3 ‒ Evaluate potential DDI effect on various transporters (e.g., P - gp) and CYPs ‒ Conduct dedicated DDI study to evaluate PK between cudetaxestat and approved IPF therapies 4 prior to dose ranging studies Pursued Stepwise Approach Mid - 2021 S tatements from Gilead and Galapagos ‒ IDMC recommendation: “… ziritaxestat’s benefit - risk profile no longer supported continuing these studies.” 1 ‒ “… it's nothing that popped up that has linked to a mechanism of action that we could explain as of today” 2 Blade proactively sought pre - IND FDA feedback 1. Gilead news release, 10 - Feb - 2021. 2. Galapagos earnings call transcript, 19 - Feb - 2021. 3. FDA pre - IND correspondence with Blade Therapeutics. 4. Approved IPF therapies = nintedanib and pirfenidone.

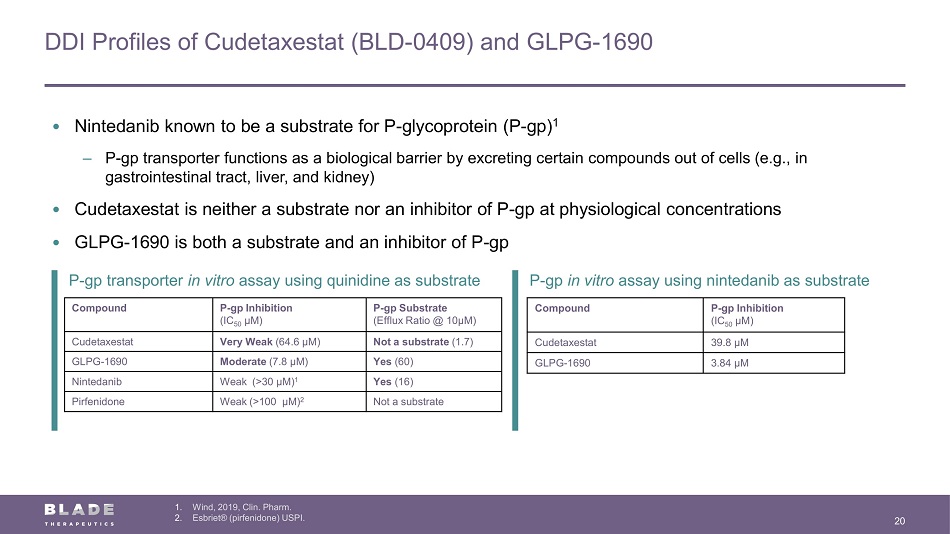

P - gp in vitro assay using nintedanib as substrate P - gp transporter in vitro assay using quinidine as substrate DDI Profiles of Cudetaxestat (BLD - 0409) and GLPG - 1690 20 1. Wind, 2019, Clin. Pharm. 2. Esbriet® (pirfenidone) USPI. Compound P - gp Inhibition (IC 50 µM) P - gp Substrate (Efflux Ratio @ 10µM) Cudetaxestat Very Weak (64.6 µM) Not a substrate (1.7) GLPG - 1690 Moderate (7.8 µM) Yes (60) Nintedanib Weak (>30 µM) 1 Yes (16) Pirfenidone Weak (>100 µM) 2 Not a substrate Compound P - gp Inhibition (IC 50 µM) Cudetaxestat 39.8 µM GLPG - 1690 3.84 µM • Nintedanib known to be a substrate for P - glycoprotein (P - gp) 1 ‒ P - gp transporter functions as a biological barrier by excreting certain compounds out of cells (e.g., in gastrointestinal tract, liver, and kidney) • Cudetaxestat is neither a substrate nor an inhibitor of P - gp at physiological concentrations • GLPG - 1690 is both a substrate and an inhibitor of P - gp

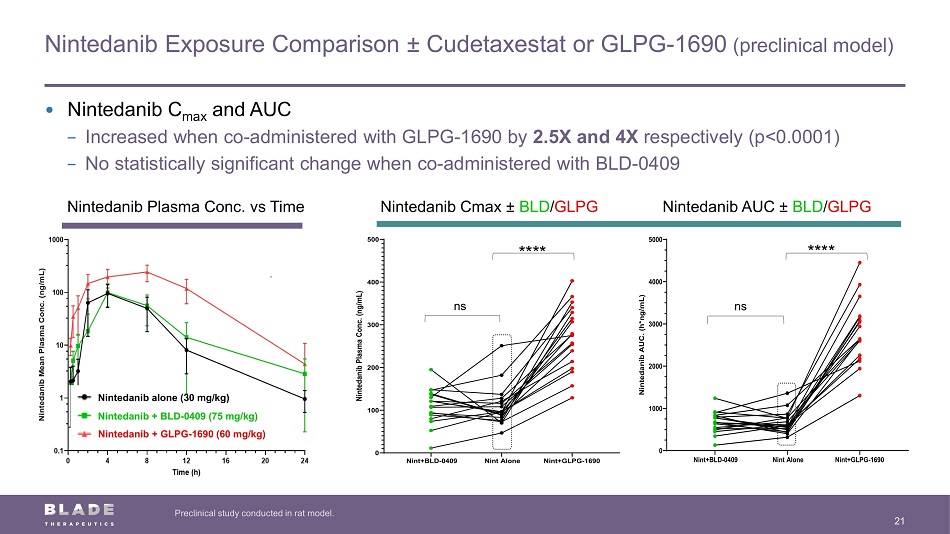

Nintedanib Exposure Comparison ± Cudetaxestat or GLPG - 1690 (preclinical model) 21 Preclinical study conducted in rat model. Nintedanib Plasma Conc. vs Time Nintedanib alone (30 mg/kg) Nintedanib + BLD - 0409 (75 mg/kg) Nintedanib + GLPG - 1690 (60 mg/kg) Nint+BLD-0409 Nint Alone Nint+GLPG-1690 0 100 200 300 400 500 N i n t e d a n i b P l a s m a C o n c . ( n g / m L ) • Nintedanib C max and AUC − Increased when co - administered with GLPG - 1690 by 2.5X and 4X respectively (p<0.0001) − No statistically significant change when co - administered with BLD - 0409 ns ns **** **** Nintedanib Cmax ± BLD / GLPG Nintedanib AUC ± BLD / GLPG

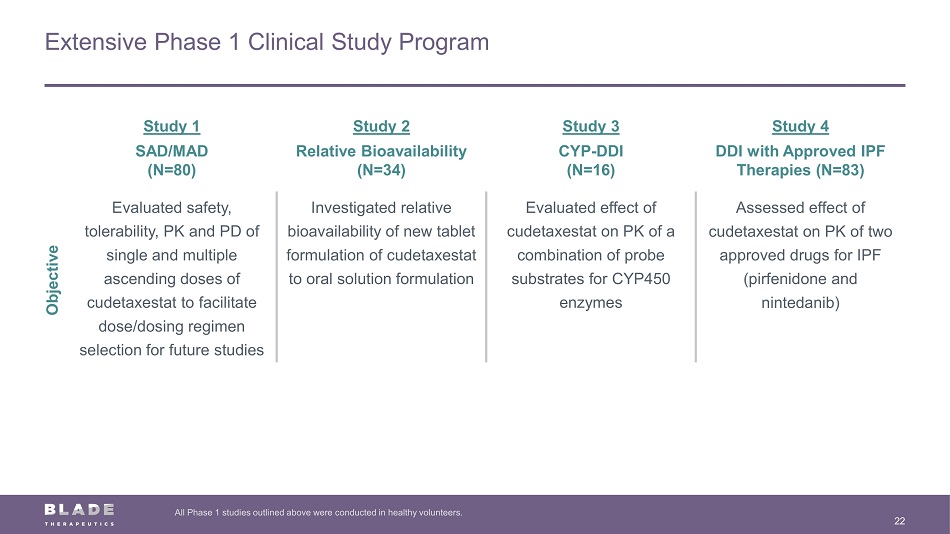

Extensive Phase 1 Clinical Study Program 22 All Phase 1 studies outlined above were conducted in healthy volunteers. Study 1 SAD/MAD (N=80) Study 2 Relative Bioavailability (N=34) Study 3 CYP - DDI (N=16) Study 4 DDI with Approved IPF Therapies (N=83) Evaluated safety, tolerability, PK and PD of single and multiple ascending doses of cudetaxestat to facilitate dose/dosing regimen selection for future studies Investigated relative bioavailability of new tablet formulation of cudetaxestat to oral solution formulation Evaluated effect of cudetaxestat on PK of a combination of probe substrates for CYP450 enzymes Assessed effect of cudetaxestat on PK of two approved drugs for IPF (pirfenidone and nintedanib) Objective

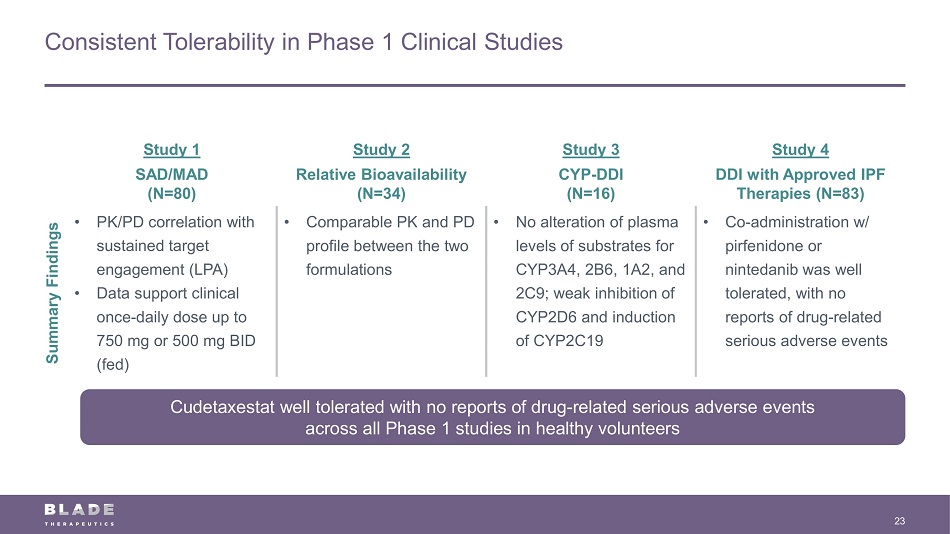

Consistent Tolerability in Phase 1 Clinical Studies 23 Study 1 SAD/MAD (N=80) Study 2 Relative Bioavailability (N=34) Study 3 CYP - DDI (N=16) Study 4 DDI with Approved IPF Therapies (N=83) • PK/PD correlation with sustained target engagement (LPA) • Data support clinical once - daily dose up to 750 mg or 500 mg BID (fed) • Comparable PK and PD profile between the two formulations • No alteration of plasma levels of substrates for CYP3A4, 2B6, 1A2, and 2C9; weak inhibition of CYP2D6 and induction of CYP2C19 • Co - administration w/ pirfenidone or nintedanib was well tolerated, with no reports of drug - related serious adverse events Summary Findings Cudetaxestat well tolerated with no reports of drug - related serious adverse events across all Phase 1 studies in healthy volunteers

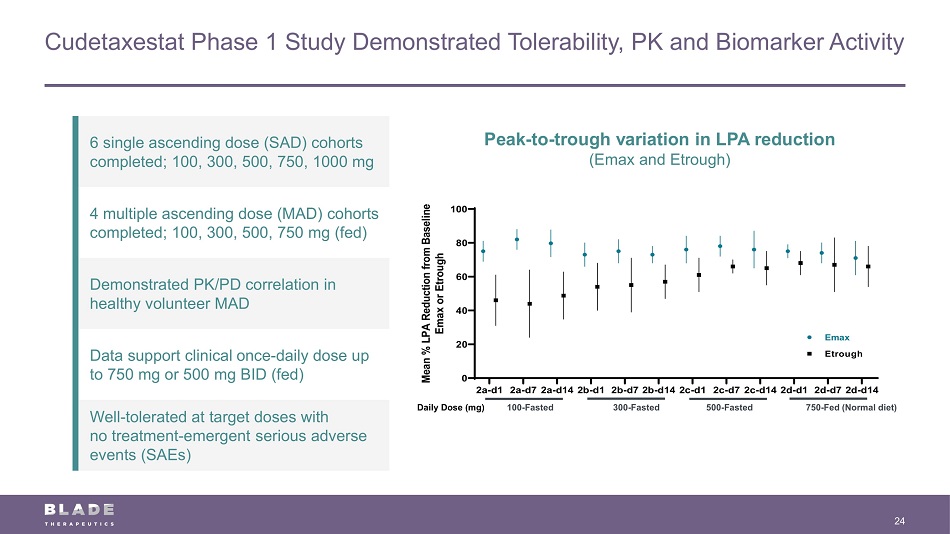

Cudetaxestat Phase 1 Study Demonstrated Tolerability, PK and Biomarker Activity 24 6 single ascending dose (SAD) cohorts completed; 100, 300, 500, 750, 1000 mg 4 multiple ascending dose (MAD) cohorts completed; 100, 300, 500, 750 mg (fed) Demonstrated PK/PD correlation in healthy volunteer MAD Data support clinical once - daily dose up to 750 mg or 500 mg BID (fed) Well - tolerated at target doses with no treatment - emergent serious adverse events (SAEs) 100 - Fasted 300 - Fasted 500 - Fasted 750 - Fed (Normal diet) Daily Dose (mg) Peak - to - trough variation in LPA reduction (Emax and Etrough) 2a-d1 2a-d72a-d142b-d1 2b-d72b-d142c-d1 2c-d72c-d142d-d1 2d-d72d-d14 0 20 40 60 80 100 M e a n % L P A R e d u c t i o n f r o m B a s e l i n e E m a x o r E t r o u g h Emax Etrough

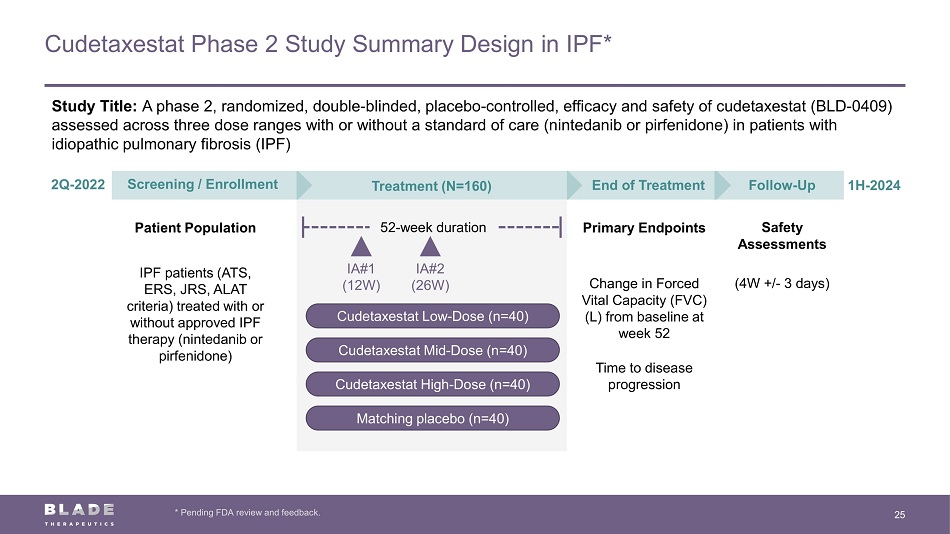

Cudetaxestat Phase 2 Study Summary Design in IPF* 25 * Pending FDA review and feedback. Study Title: A phase 2, randomized, double - blinded, placebo - controlled, efficacy and safety of cudetaxestat (BLD - 0409) assessed across three dose ranges with or without a standard of care (nintedanib or pirfenidone) in patients with idiopathic pulmonary fibrosis (IPF) Screening / Enrollment Patient Population IPF patients (ATS, ERS, JRS, ALAT criteria) treated with or without approved IPF therapy (nintedanib or pirfenidone) Follow - Up Safety Assessments (4W +/ - 3 days) End of Treatment Primary Endpoints Change in Forced Vital Capacity (FVC) (L) from baseline at week 52 Time to disease progression Treatment (N=160) 52 - week duration IA#1 (12W) IA#2 (26W) Cudetaxestat High - Dose (n=40) Matching placebo (n=40) Cudetaxestat Mid - Dose (n=40) Cudetaxestat Low - Dose (n=40) 2Q - 2022 1H - 2024

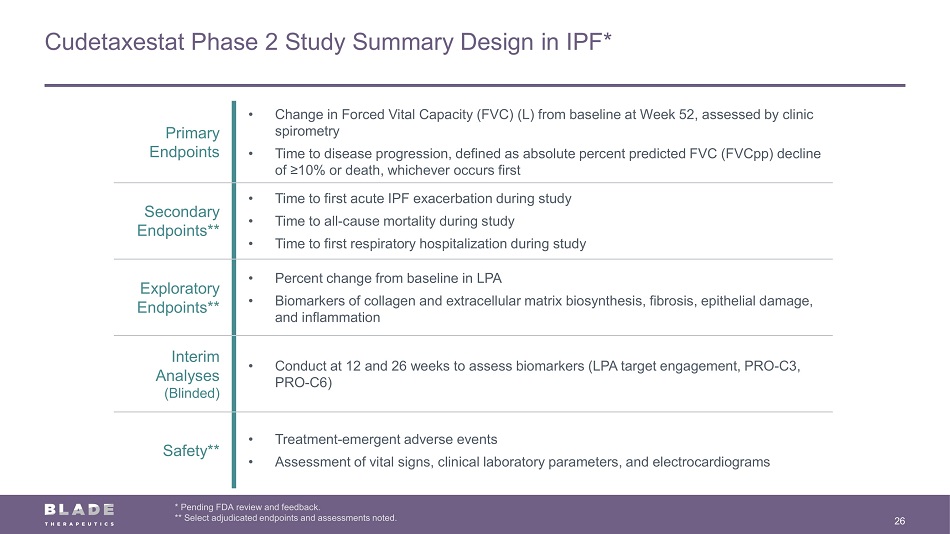

Cudetaxestat Phase 2 Study Summary Design in IPF* 26 * Pending FDA review and feedback. ** Select adjudicated endpoints and assessments noted. Primary Endpoints • Change in Forced Vital Capacity (FVC) (L) from baseline at Week 52, assessed by clinic spirometry • Time to disease progression, defined as absolute percent predicted FVC (FVCpp) decline of ≥10% or death, whichever occurs first Secondary Endpoints** • Time to first acute IPF exacerbation during study • Time to all - cause mortality during study • Time to first respiratory hospitalization during study Exploratory Endpoints** • Percent change from baseline in LPA • Biomarkers of collagen and extracellular matrix biosynthesis, fibrosis, epithelial damage, and inflammation Interim Analyses (Blinded) • Conduct at 12 and 26 weeks to assess biomarkers (LPA target engagement, PRO - C3, PRO - C6) Safety** • Treatment - emergent adverse events • Assessment of vital signs, clinical laboratory parameters, and electrocardiograms

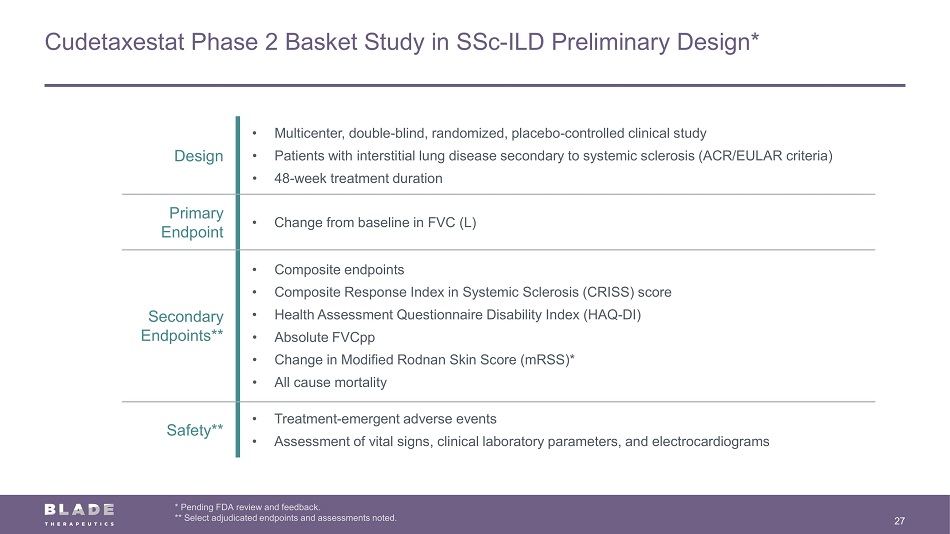

Cudetaxestat Phase 2 Basket Study in SSc - ILD Preliminary Design* 27 * Pending FDA review and feedback. ** Select adjudicated endpoints and assessments noted. Design • Multicenter, double - blind, randomized, placebo - controlled clinical study • Patients with interstitial lung disease secondary to systemic sclerosis (ACR/EULAR criteria) • 48 - week treatment duration Primary Endpoint • Change from baseline in FVC (L) Secondary Endpoints** • Composite endpoints • Composite Response Index in Systemic Sclerosis (CRISS) score • Health Assessment Questionnaire Disability Index (HAQ - DI) • Absolute FVCpp • Change in Modified Rodnan Skin Score (mRSS)* • All cause mortality Safety** • Treatment - emergent adverse events • Assessment of vital signs, clinical laboratory parameters, and electrocardiograms

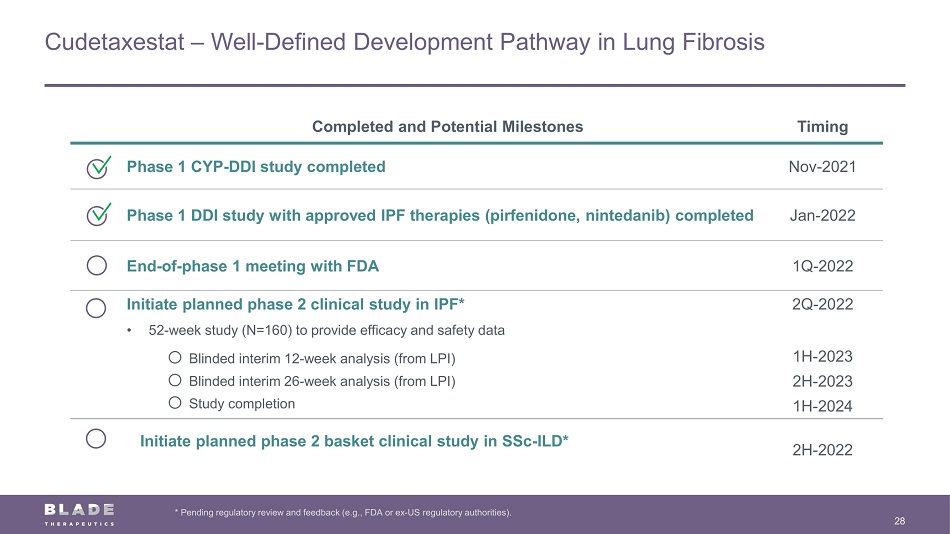

Cudetaxestat – Well - Defined Development Pathway in Lung Fibrosis 28 * Pending regulatory review and feedback (e.g., FDA or ex - US regulatory authorities). Completed and Potential Milestones Timing Phase 1 CYP - DDI study completed Nov - 2021 Phase 1 DDI study with approved IPF therapies (pirfenidone, nintedanib) completed Jan - 2022 End - of - phase 1 meeting with FDA 1Q - 2022 Initiate planned phase 2 clinical study in IPF* 2Q - 2022 • 52 - week study (N=160) to provide efficacy and safety data o Blinded interim 12 - week analysis (from LPI) o Blinded interim 26 - week analysis (from LPI) o Study completion 1H - 2023 2H - 2023 1H - 2024 Initiate planned phase 2 basket clinical study in SSc - ILD* 2H - 2022

29 Idiopathic Pulmonary Fibrosis Market Landscape and Opportunities

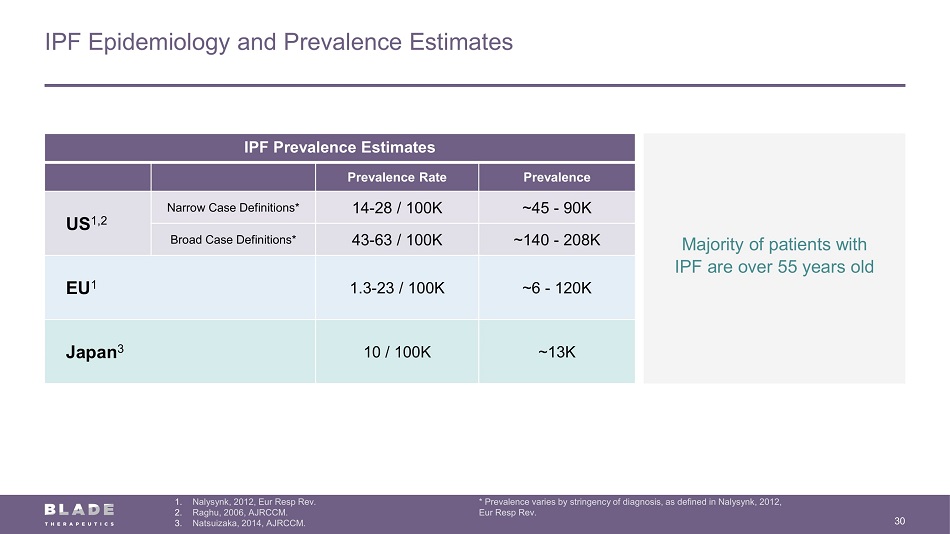

IPF Epidemiology and Prevalence Estimates 30 1. Nalysynk, 2012, Eur Resp Rev. 2. Raghu, 2006, AJRCCM. 3. Natsuizaka, 2014, AJRCCM. * Prevalence varies by stringency of diagnosis, as defined in Nalysynk, 2012, Eur Resp Rev. Majority of patients with IPF are over 55 years old IPF Prevalence Estimates Prevalence Rate Prevalence US 1,2 Narrow Case Definitions* 14 - 28 / 100K ~45 - 90K Broad Case Definitions* 43 - 63 / 100K ~140 - 208K EU 1 1.3 - 23 / 100K ~6 - 120K Japan 3 10 / 100K ~13K

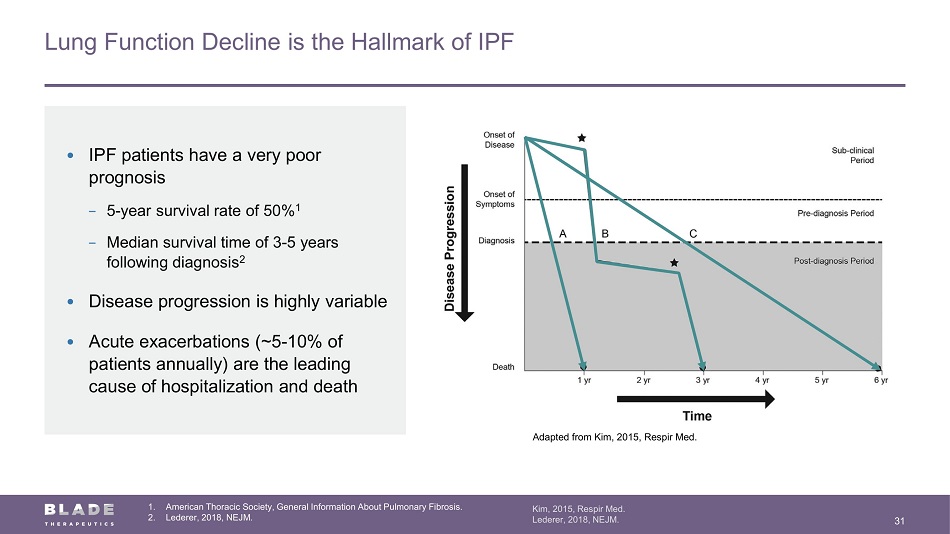

Lung Function Decline is the Hallmark of IPF 31 Kim, 2015, Respir Med. Lederer, 2018, NEJM. • IPF patients have a very poor prognosis − 5 - year survival rate of 50% 1 − Median survival time of 3 - 5 years following diagnosis 2 • Disease progression is highly variable • Acute exacerbations (~5 - 10% of patients annually) are the leading cause of hospitalization and death Adapted from Kim, 2015, Respir Med. 1. American Thoracic Society, General Information About Pulmonary Fibrosis. 2. Lederer, 2018, NEJM.

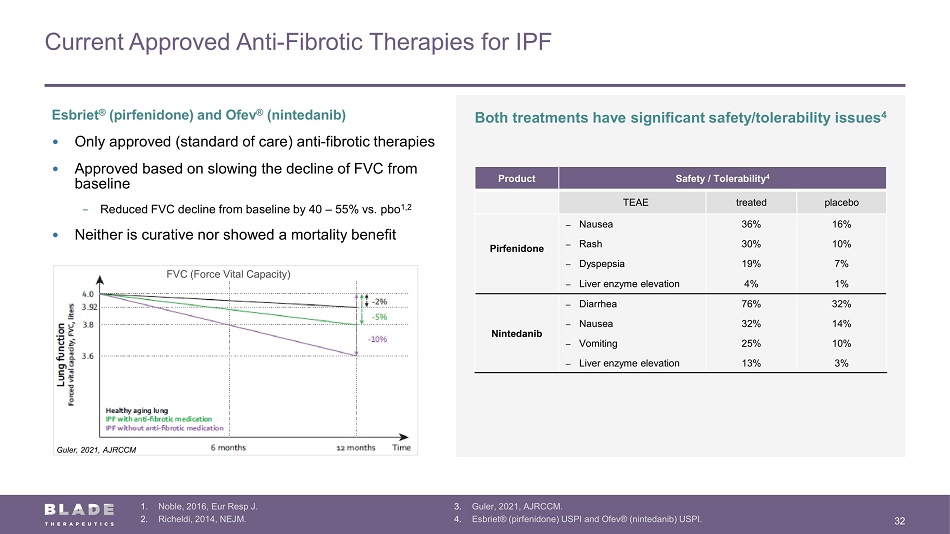

Current Approved Anti - Fibrotic Therapies for IPF 32 1. Noble, 2016, Eur Resp J. 2. Richeldi, 2014, NEJM. 3. Guler, 2021, AJRCCM. 4. Esbriet® (pirfenidone) USPI and Ofev® (nintedanib) USPI. Esbriet ® (pirfenidone) and Ofev ® (nintedanib) • Only approved (standard of care) anti - fibrotic therapies • Approved based on slowing the decline of FVC from baseline − Reduced FVC decline from baseline by 40 – 55% vs. pbo 1,2 • Neither is curative nor showed a mortality benefit Guler, 2021, AJRCCM FVC (Force Vital Capacity) Product Safety / Tolerability 4 TEAE treated placebo Pirfenidone – Nausea 36% 16% – Rash 30% 10% – Dyspepsia 19% 7% – Liver enzyme elevation 4% 1% Nintedanib – Diarrhea 76% 32% – Nausea 32% 14% – Vomiting 25% 10% – Liver enzyme elevation 13% 3% Both treatments have significant safety/tolerability issues 4

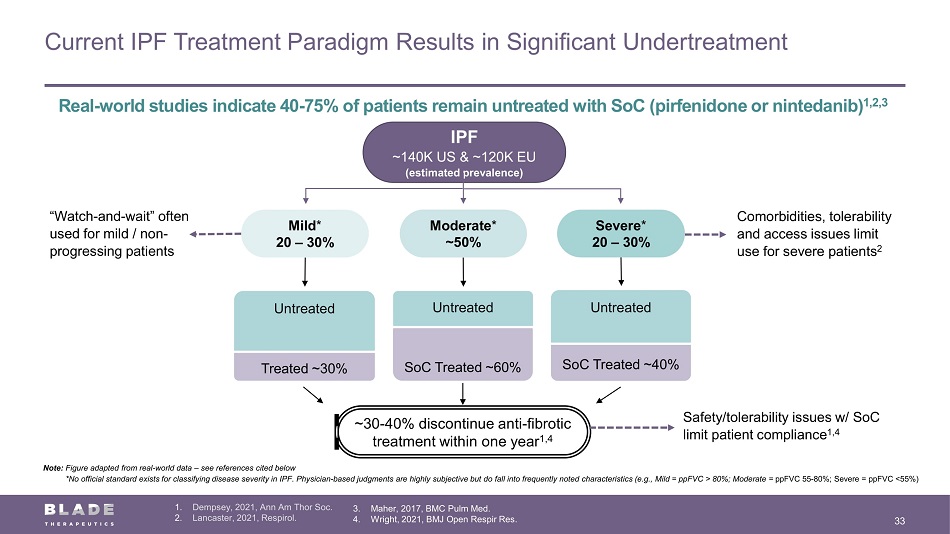

Current IPF Treatment Paradigm Results in Significant Undertreatment 33 1. Dempsey, 2021, Ann Am Thor Soc. 2. Lancaster, 2021, Respirol. 3. Maher, 2017, BMC Pulm Med. 4. Wright, 2021, BMJ Open Respir Res. Real - world studies indicate 40 - 75% of patients remain untreated with SoC (pirfenidone or nintedanib) 1,2,3 Note: Figure adapted from real - world data – see references cited below *No official standard exists for classifying disease severity in IPF. Physician - based judgments are highly subjective but do fal l into frequently noted characteristics (e.g., Mild = ppFVC > 80%; Moderate = ppFVC 55 - 80%; Severe = ppFVC <55%) IPF ~140K US & ~120K EU (estimated prevalence) ~30 - 40% discontinue anti - fibrotic treatment within one year 1,4 Safety/tolerability issues w/ SoC limit patient compliance 1,4 “Watch - and - wait” often used for mild / non - progressing patients Comorbidities, tolerability and access issues limit use for severe patients 2 Mild * 20 – 30% Moderate * ~50% Severe * 20 – 30% Treated ~30% Untreated SoC Treated ~60% Untreated SoC Treated ~40% Untreated

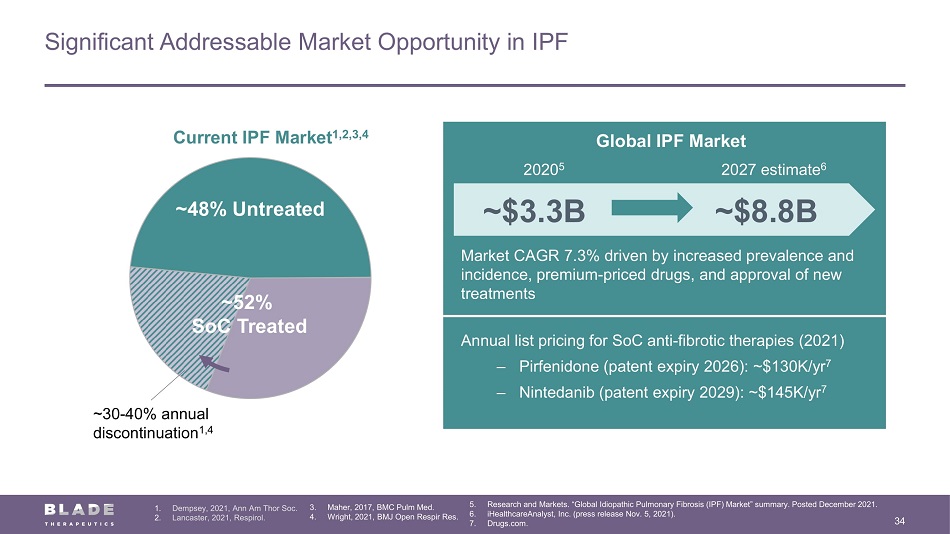

Significant Addressable Market Opportunity in IPF 34 1. Dempsey, 2021, Ann Am Thor Soc. 2. Lancaster, 2021, Respirol. 3. Maher, 2017, BMC Pulm Med. 4. Wright, 2021, BMJ Open Respir Res. 5. Research and Markets. “Global Idiopathic Pulmonary Fibrosis (IPF) Market” summary. Posted December 2021. 6. iHealthcareAnalyst, Inc. (press release Nov. 5, 2021). 7. Drugs.com. ~48% Untreated ~52% SoC Treated ~30 - 40% annual discontinuation 1,4 Current IPF Market 1,2,3,4 ~$3.3B ~$8.8B 2027 estimate 6 2020 5 Global IPF Market Market CAGR 7.3% driven by increased prevalence and incidence, premium - priced drugs, and approval of new treatments Annual list pricing for SoC anti - fibrotic therapies (2021) ‒ P irfenidone (patent expiry 2026): ~$130K/yr 7 ‒ N intedanib (patent expiry 2029): ~$145K/yr 7

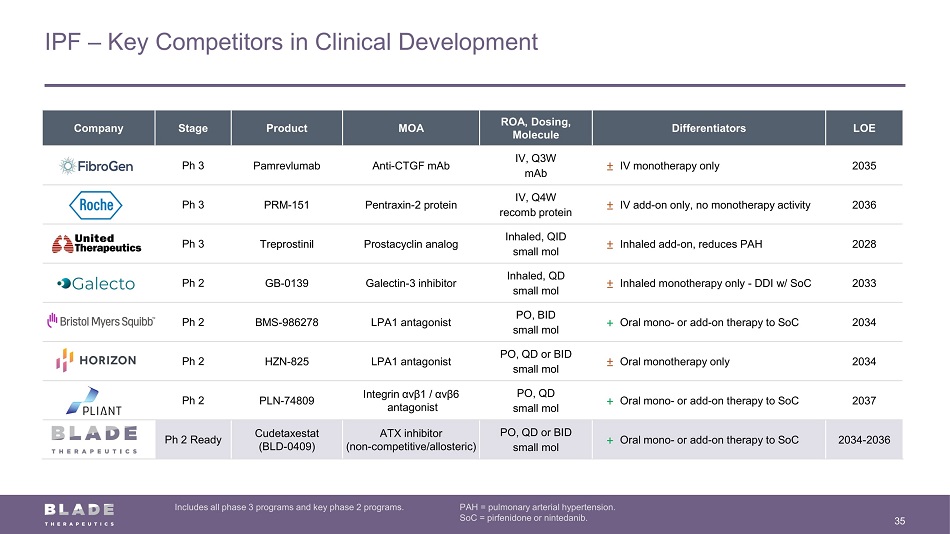

IPF – Key Competitors in Clinical Development Includes all phase 3 programs and key phase 2 programs. PAH = pulmonary arterial hypertension. SoC = pirfenidone or nintedanib. 35 Company Stage Product MOA ROA, Dosing, Molecule Differentiators LOE Ph 3 Pamrevlumab Anti - CTGF mAb IV, Q3W mAb ± IV monotherapy only 2035 Ph 3 PRM - 151 Pentraxin - 2 protein IV, Q4W recomb protein ± IV add - on only, no monotherapy activity 2036 Ph 3 Treprostinil Prostacyclin analog Inhaled, QID small mol ± Inhaled add - on, reduces PAH 2028 Ph 2 GB - 0139 Galectin - 3 inhibitor Inhaled, QD small mol ± Inhaled monotherapy only - DDI w/ SoC 2033 Ph 2 BMS - 986278 LPA1 antagonist PO, BID small mol + Oral mono - or add - on therapy to SoC 2034 Ph 2 HZN - 825 LPA1 antagonist PO, QD or BID small mol ± Oral monotherapy only 2034 Ph 2 PLN - 74809 Integrin α v β 1 / α v β 6 antagonist PO, QD small mol + Oral mono - or add - on therapy to SoC 2037 Ph 2 Ready Cudetaxestat (BLD - 0409) ATX inhibitor (non - competitive/allosteric) PO, QD or BID small mol + Oral mono - or add - on therapy to SoC 2034 - 2036

36 Neurodegeneration – BLD - 2184 CNS - Penetrant Calpain Inhibitor for Poly - Q Neurodegenerative Conditions

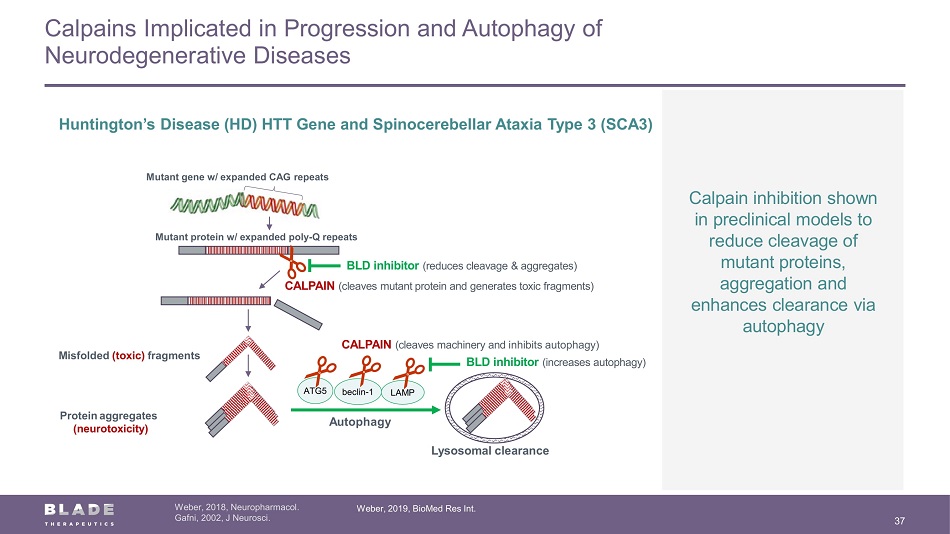

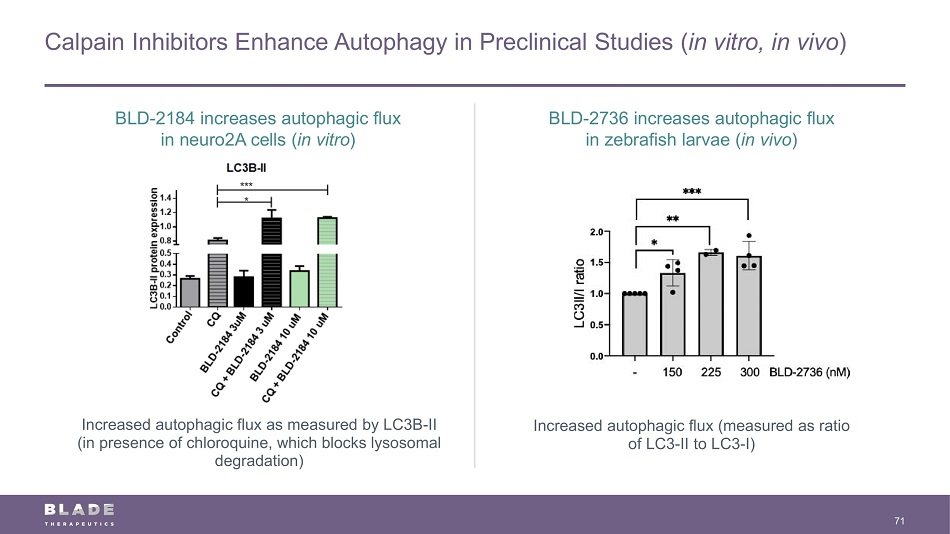

Calpains Implicated in Progression and Autophagy of Neurodegenerative Diseases 37 Weber, 2018, Neuropharmacol. Gafni, 2002, J Neurosci. Calpain inhibition shown in preclinical models to r educe cleavage of mutant proteins, aggregation and enhances clearance via autophagy Mutant gene w/ expanded CAG repeats Mutant protein w/ expanded poly - Q repeats CALPAIN (cleaves mutant protein and generates toxic fragments) BLD inhibitor (reduces cleavage & aggregates) Protein a ggregates (neurotoxicity) M isfolded (toxic) fragments CALPAIN (cleaves machinery and inhibit s autophagy) Lysosomal clearance ATG5 beclin - 1 LAMP A utophagy BLD inhibitor (increases autophagy) Huntington’s Disease (HD) HTT G ene and Spinocerebellar Ataxia Type 3 (SCA3) Weber, 2019, BioMed Res Int.

Calpain Inhibitors Demonstrate Preclinical Evidence of Neuroprotective Effects 38 1. Weber, 2018, Neuropharmacol. Gafni, 2002, J Neurosci. Weber, 2019, BioMed Res Int. 2. Robinson, 2021, Cells. Novel Target for Disease Progression 1 Calpains shown in preclinical studies to regulate formation of toxic proteins and autophagy (intracellular clearance), key components in incurable neurodegenerative Poly - Q diseases (HD, SCA3) Preclinical Evidence of Neuroprotection 2 Improvements in biomarkers, motor function and enhanced autophagy in SCA3 preclinical models (mouse, zebrafish models) Development Candidate Selection Ongoing preclinical and nonclinical activities in preparation for initiating planned phase 1 study (2H - 2022)

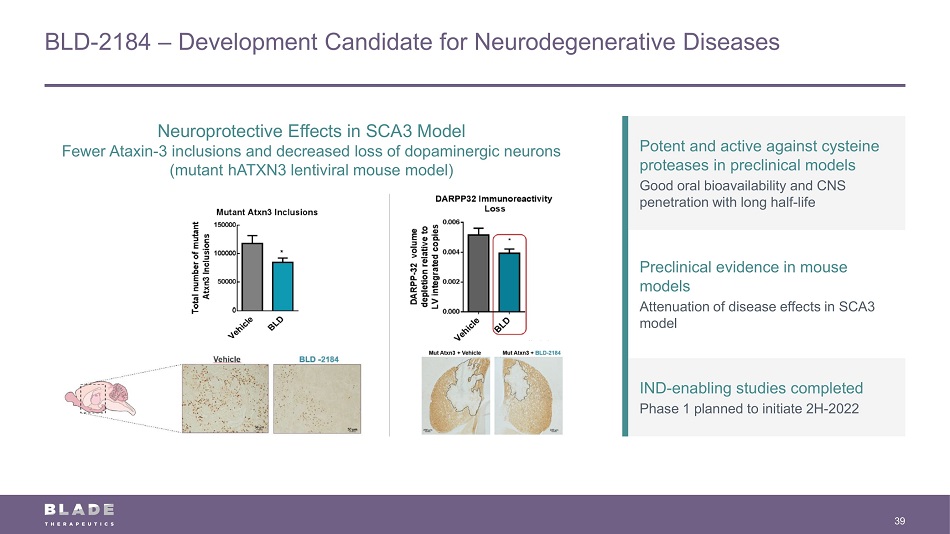

BLD - 2184 – Development Candidate for Neurodegenerative Diseases 39 Neuroprotective Effects in SCA3 Model Fewer Ataxin - 3 inclusions and decreased loss of dopaminergic neurons (mutant hATXN3 lentiviral mouse model) Potent and active against cysteine proteases in preclinical models Good oral bioavailability and CNS penetration with long half - life Preclinical evidence in mouse models Attenuation of disease effects in SCA3 model IND - enabling studies completed Phase 1 planned to initiate 2H - 2022

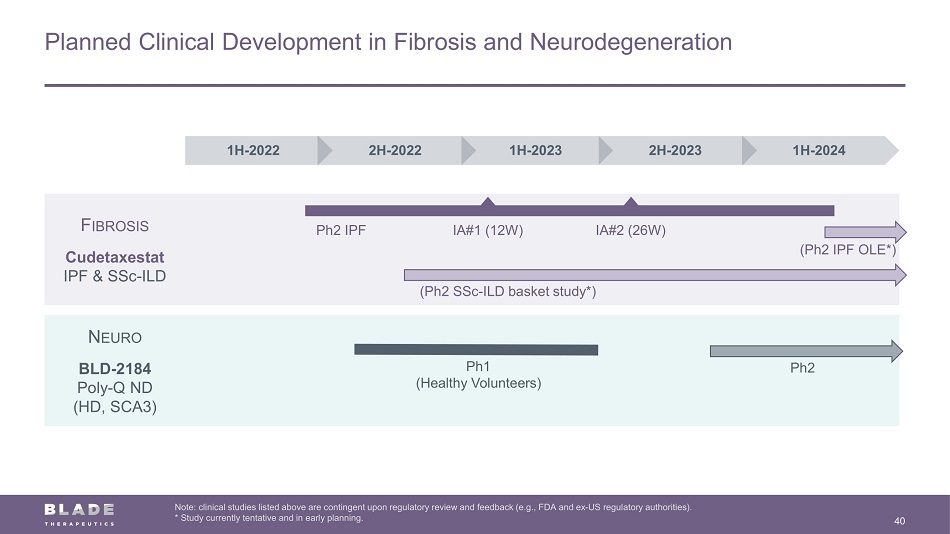

Planned Clinical Development in Fibrosis and Neurodegeneration 40 Note: clinical studies listed above are contingent upon regulatory review and feedback (e.g., FDA and ex - US regulatory authoriti es). * Study currently tentative and in early planning. Ph1 (Healthy Volunteers) Ph2 N EURO BLD - 2184 Poly - Q ND (HD, SCA3) 1H - 20 22 2H - 20 22 1H - 2023 2 H - 2023 1 H - 2024 Ph2 IPF IA#1 (12W) IA#2 (26W) F IBROSIS Cudetaxestat IPF & SSc - ILD (Ph2 IPF OLE*) (Ph2 SSc - ILD basket study*)

Blade Therapeutics Investment Thesis 41 4. Research and Markets. “Global Idiopathic Pulmonary Fibrosis (IPF) Market” summary. Posted December 2021. 5. iHealthcareAnalyst, Inc. (press releasee Nov. 5, 2021). Orphan Diseases Pursuing debilitating, progressive diseases in fibrosis and neurodegeneration Significant Market Strong projected growth in IPF market Large Unmet Need 40 - 75% of patients with IPF remain untreated with current therapies 1,2,3 ~$3.3B ~$8.8B (2027 estimate) 5 (2020) 4 Differentiated Pipeline Oral, small - molecule candidates with novel mechanisms of action and strong IP complemented by global commercial rights Phase 2 Ready Lead program targeting clinically - validated pathway for IPF as potential monotherapy or add - on to current therapies $280M Proposed Valuation compared to peer companies, prior M&A deals and external IPF market potential 1. Dempsey, 2021, Ann Am Thor Soc. 2. Lancaster, 2021, Respirol. 3. Maher, 2017, BMC Pulm Med.

Developing Cutting - Edge Treatments for Debilitating Fibrotic and Neurodegenerative Diseases 42 1. Effects demonstrated in preclinical studies. 2. Pending regulatory review and feedback (e.g., FDA or ex - US regulatory authorities). Experts in Biology of Cell and Tissue Damage Responses • Researching novel pathways foundational to cell - and tissue - damage responses • Developing potential disease - modifying therapeutics Differentiated Pipeline Led By Phase 2 - Ready Program in Fibrosis • Non - competitive autotaxin inhibitor with direct anti - fibrotic activity and differentiating characteristics 1 – planned phase 2 study in lung fibrosis in 2Q - 2022 • CNS - penetrant calpain inhibitor 1 for genetic orphan neurodegenerative conditions approaching planned phase 1 study in 2H - 2022 2 Deep Scientific & Industry Experience • Experienced team with extensive expertise in fibrosis and neurodegeneration • Strong track record of development and approvals of innovative medicines

Risks Related to the Business Combination 43 BAC’s shareholders will experience dilution due to the issuance of shares of common stock of BAC (after its re - domestication fro m the Cayman Islands to Delaware), and securities that are exchangeable for shares of common stock of BAC, to: (i) the Target’s security holders as consideration in the merger and (ii) ce rtain PIPE investors in the PIPE financing. The consummation of the Business Combination is subject to a number of conditions, including those set forth in the definitiv e A greement and Plan of Merger (the “Merger Agreement”), and if those conditions are not satisfied or waived, the Merger Agreement may be terminated in accordance with its terms and the Bus iness Combination may not be completed. If the Business Combination benefits do not meet the expectation of investors or securities analysts, the market price of BAC ’s securities, or following the consummation of the Business Combination, the securities of the combined company (the “Combined Entity”), may decline. Potential legal proceedings in connection with the Business Combination, the outcome of which may be uncertain, could delay o r p revent the completion of the Business Combination. Following the consummation of the Business Combination, the Combined Entity will be an “emerging growth company” and it canno t b e certain if the disclosure requirements applicable to emerging growth companies will make the Combined Entity’s common stock less attractive to investors and may make it more diff icu lt to compare performance with other public companies. The Combined Entity will incur significantly increased expenses and administrative burdens as a public company, which could h ave an adverse effect. The ability of BAC’s shareholders to exercise redemption rights with respect to a large number of BAC’s shares may not allow BAC to complete the Business Combination or for the Combined Entity to have the full cash available to execute its development and capital expenditure plans. There is no assurance that BAC’s diligence will reveal all material risks that may present with regard to the Target. BAC may issue additional shares of common or preferred stock to complete the Business Combination or under an equity incentiv e p lan after completion of the Business Combination, any one of which would dilute the interest of BAC’s shareholders and likely present other risks. BAC’s key personnel may negotiate employment or consulting agreements with the Combined Entity in connection with the Busines s C ombination. These agreements may provide for them to receive compensation following the Business Combination and as a result, may cause them to have conflicts of interest in d ete rmining whether the Business Combination is advantageous. Because BAC’s initial shareholders, executive officers and directors will lose their entire investment in BAC if the Business Co mbination or an alternative business combination is not completed, and because BAC’s Sponsor, executive officers and directors will not be eligible to be reimbursed for their out - of - po cket expenses if the Business Combination is not completed, a conflict of interest may have arisen in determining whether the Target is appropriate for BAC’s initial business combinatio n. Some of the officers and directors of BAC, on the one hand, and the Target, on the other hand, may be argued to have conflict s o f interest that may influence them to support or approve the Business Combination without regard to your interests. The value of the Sponsor’s founder shares following completion of the Business Combination is likely to be substantially high er than the nominal price paid for them, even if the trading price of BAC’s common stock at such time is substantially less than $10.00 per share.

Risks Related to the Business Combination (cont’d) 44 BAC’s shareholders and the Target’s stockholders may not realize a benefit from the Business Combination commensurate with th e o wnership dilution they will experience in connection with the Business Combination. During the pendency of the Business Combination, BAC and the Target may not be able to enter into a business combination with an other party because of restrictions in the Merger Agreement, which could adversely affect their respective businesses. Furthermore, certain provisions of the Merger Agreement may discourage third parties from submitting alternative takeover proposals, including proposals that may be superior to the arrangements contemplated by the Merger Agreement. If the conditions to the Merger are not met, including the approval by each party’s respective shareholders, the Business Com bin ation may not occur. Each of BAC and the Target may waive one or more of the conditions to the Business Combination, subject to certain limitation s a s set out in the Merger Agreement. U.S. federal income tax reform could adversely affect the Combined Entity and holders of the Combined Entity’s securities. The Combined Entity will be affected by extensive laws, governmental regulations, administrative determinations, court decisi ons and similar constraints both domestically and abroad. Delaware law and the Combined Entity’s proposed charter and bylaws may contain certain provisions, including anti - takeover provi sions that limit the ability of stockholders to take certain actions and could delay or discourage takeover attempts that stockholders may consider favorable, as well as certain provisio ns limiting the ability of the Combined Entity’s stockholders to choose the judicial forum for disputes with the Combined Entity or its directors, officers, or employees. The proposed charter will not limit the ability of the Sponsor or its affiliates to compete with the Combined Entity. The Combined Entity’s business and operations could be negatively affected if it becomes subject to any securities litigation or stockholder activism, which could cause the Combined Entity to incur significant expense, hinder execution of business and growth strategy and impact its stock price. Upon effectiveness of the proposed domestication of BAC from the Cayman Islands to Delaware in connection with the Business C omb ination, the rights of holders of the Combined Entity’s common stock arising under the Delaware General Corporate Law will differ from and may be less favorable to the rights of hol der s of BAC’s shares arising under the Cayman Islands Companies Act. There is a risk that a U.S. Holder may recognize taxable gain with respect to its BAC shares at the effective time of the pro pos ed domestication. BAC identified material weaknesses in its internal controls over financial reporting with respect to the accounting treatment of certain of its warrants. Failure to maintain effective internal controls over financial reporting could cause BAC to inaccurately report its financial results or fail to prevent fraud.

Risks Related to Combined Entity’s Business 45 The Target is very early in its development efforts, has completed few clinical trials, has no products approved for commerci al sale, and has no historical product revenues, which makes it difficult to assess the Target’s future prospects and financial results. The Target’s ability to generate revenue and achieve profitability depends significantly on its ability to achieve its object ive s relating to the discovery, development and commercialization of its product candidates. The Target has limited sales and distribution experience and needs to build a marketing and sales organization. We expect to inv est significant financial and management resources to build these capabilities. To the extent any of the Target’s product candidates for which it maintains commercial rights is approved for marketing, if w e a re unable to establish marketing and sales capabilities or enter into agreements with third parties to market and sell such product candidates, we may not be able to market and sell any product candidates e ffe ctively or generate product revenues. The marketing and sale of cudetaxestat or future approved products may be unsuccessful or less successful than anticipated. T he Target is heavily dependent on the success of cudetaxestat, which has not been approved for the treatment of idiopathic pulmonary fibrosis or nonalcoholic steatohepatitis. If the Target is unable to ad vance cudetaxestat or our other product candidates through clinical development, obtain regulatory approval and ultimately commercialize our product candidates, or experience significant delays in doing so, th e Target’s business will be materially harmed. The Target is also dependent on the success of its other preclinical product candidates (BLD - 2184 and other candidates). We cann ot give any assurance that any product candidate will successfully complete clinical trials or receive regulatory approval, which is necessary before it can be commercialized. The clinical and commercial success of the Target’s product candidates will depend on a number of factors, many of which are bey ond the Target’s control. The Target’s future commercial success depends upon attaining significant market acceptance of its product candidates, if approved, among physicians, patients, third - party pay ors, and others in the health care community. Clinical development is a lengthy and expensive process with an uncertain outcome, and results of earlier studies and trials as well as data from any interim analysis of ongoing clinical trials may not be predictive of future trial results or approved label for clinical use. Clinical failure can occur at any stage of clinical de vel opment. Due to the Target’s limited resources and access to capital in the past, the Target has decided to prioritize development of cer tain product candidates and may have forgone the opportunity to capitalize on product candidates or indications that may ultimately have been more profitable or for which there was a greater likelihood o f s uccess. If the Target is unable to raise substantial additional capital to finance its operations when needed, or on acceptable terms, the Target may be forced to delay, reduce or eliminate one or more of its res ear ch and drug development programs, future commercialization efforts, product development or other operations. The approach the Target is taking to discover and develop drugs is novel and may never lead to approved or marketable product s. The Target may not be successful in its efforts to use and expand its novel, proprietary target discovery platform to build a pi peline of product candidates. The Target’s product candidates may fail in development or suffer delays that adversely affect their commercial viability. The regulatory approval processes of the FDA and other comparable regulatory authorities are lengthy, time consuming and inhe ren tly unpredictable, which may affect the commercial viability of the Target’s products in development. If the Target is unable ultimately to obtain regulatory approval for its product candidates, its bus ine ss will be substantially harmed. In connection with the Target’s global clinical trials, local regulatory authorities may have differing perspectives on clini cal protocols and safety parameters, which impacts the manner in which the Target conducts these global clinical trials and could negatively impact the Target’s chances for obtaining regulatory approvals or mar keting authorization in different jurisdictions, or for obtaining the requested label or dosage for the Target’s product candidates, if regulatory approvals or marketing authorizations are obtained. The results of th e Target’s clinical trials may not satisfy the requirements of different regulatory authorities.

Risks Related to Combined Entity’s Business (cont’d) 46 Even if the Target receives regulatory approval for any of its product candidates, the Target will be subject to ongoing obli gat ions and continued regulatory review, which may result in significant additional expense. Additionally, the Target’s product candidates, if approved, could be subject to labeling and other restrictions and mar ket withdrawal and the Target may be subject to penalties if it fails to comply with regulatory requirements or experience unanticipated problems with its products. The Target’s preclinical studies and its future clinical trials or those of any of its collaborators may fail to adequately d emo nstrate the safety and efficacy of any of its product candidates or reveal significant adverse events not seen in its preclinical studies or earlier clinical trials which would prevent or delay the development, r egu latory approval, and commercialization of any of the Target’s product candidates. The Target has limited experience as a company in conducting clinical trials. If the Target experiences delays or difficulties in the enrollment or maintenance of subjects in clinical trials, its regulat ory submissions or the receipt of necessary marketing approvals could be delayed or prevented. Legislative and regulatory activity may exert downward pressure on potential pricing and reimbursement for any of the Target’ s p roduct candidates, if approved, that could materially affect the opportunity to commercialize. The Target faces significant competition for its drug discovery and development efforts, and if the Target does not compete effectively, i ts commercial opportunities will be reduced or eliminated. The Target relies on adequate protection of its proprietary rights to compete effectively in its market. The Target’s ability to compete may decline if it does not adequately protect its proprietary rights. The cost of maintaining the Target’s patent protection is high and requires continuous review and compliance. The Target may not be able to effectively maintain i ts intellectual property position throughout our market. The Target may be involved in intellectual property disputes with third parties and competitors that could be costly and time co nsuming and negatively affect its competitive position. The Target relies on third parties for the conduct of most of its preclinical studies and clinical trials for its product can did ates, and if its third - party contractors do not properly and successfully perform their obligations under the Target’s agreements with them, the Target may not be able to obtain or may be delayed in receiving regu lat ory approvals for its product candidates. The Target current relies, and expects to continue to rely, on third parties to conduct many aspects of its product candidate ma nufacturing activities and the Target intends to rely on third parties for potential commercial product manufacturing. The Target’s business could be harmed if those third parties fail to provide us with suffic ien t quantities of product or fail to do so at acceptable quality levels or prices. The Target’s business, results of operations and future growth prospects could be materially and adversely affected by the CO VID - 19 pandemic. If the Target is unable to obtain, maintain and enforce patent protection for its technology and product candidates, or if th e s cope of patent protection obtained is not sufficiently broad, the Target’s competitors could develop and commercialize technology and products similar or identical to thos e of the Target and the Target’s ability to successfully develop and commercialize its technology and product candidates may be adversely affected.

Appendix

Strategic and Smart Capital to Advance Novel Therapies in Unmet Needs in Orphan Diseases 48 * Pending regulatory review and feedback (e.g., FDA or ex - US regulatory authorities). Backed by experienced life - science and strategic investors with deep experience investing in fibrosis therapeutic area • Expected differentiated competitive support post de - SPAC Minimum cash condition of $75 million • Allows sufficient runway through at least 1Q - 2024 Multiple anticipated near - and long - term clinical milestones* • Phase 2 trial in IPF for cudetaxestat with anticipated interim analyses in 1H - 2023 and 2H - 2023 • Phase 1 trial for BLD - 2184 in healthy volunteers with anticipated data readout in 1H - 2023

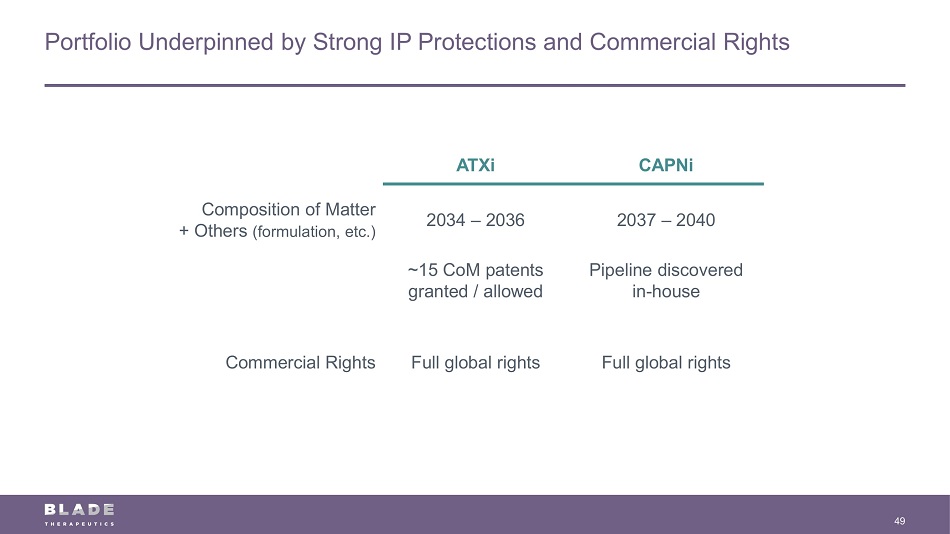

Portfolio Underpinned by Strong IP Protections and Commercial Rights 49 ATXi CAPNi Composition of Matter + Others (formulation, etc.) 2034 – 2036 2037 – 2040 ~15 CoM patents granted / allowed Pipeline discovered in - house Commercial Rights Full global rights Full global rights

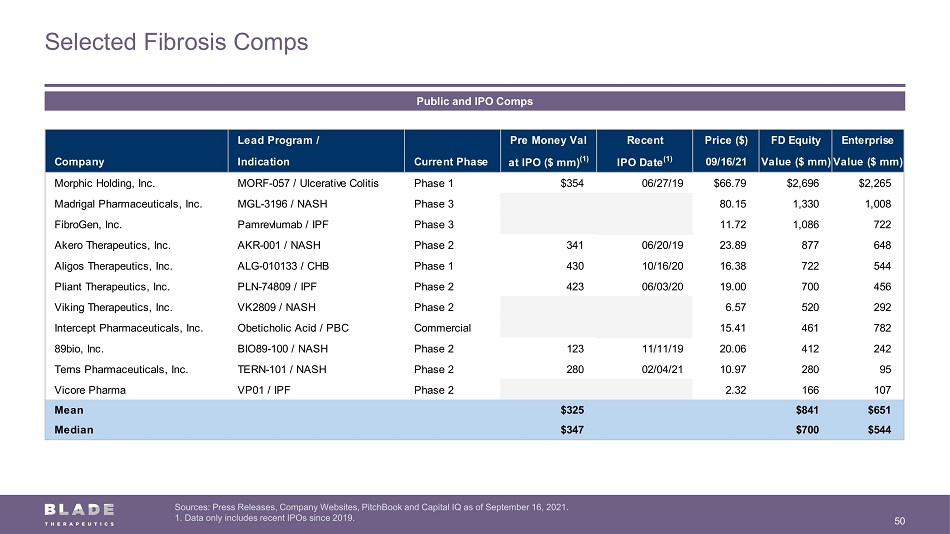

Selected Fibrosis Comps 50 Sources: Press Releases, Company Websites, PitchBook and Capital IQ as of September 16, 2021. 1. Data only includes recent IPOs since 2019. Public and IPO Comps Lead Program / Pre Money Val Recent Price ($) FD Equity Enterprise Company Indication Current Phase at IPO ($ mm) (1) IPO Date (1) 09/16/21 Value ($ mm)Value ($ mm) Morphic Holding, Inc. MORF-057 / Ulcerative Colitis Phase 1 $354 06/27/19 $66.79 $2,696 $2,265 Madrigal Pharmaceuticals, Inc. MGL-3196 / NASH Phase 3 80.15 1,330 1,008 FibroGen, Inc. Pamrevlumab / IPF Phase 3 11.72 1,086 722 Akero Therapeutics, Inc. AKR-001 / NASH Phase 2 341 06/20/19 23.89 877 648 Aligos Therapeutics, Inc. ALG-010133 / CHB Phase 1 430 10/16/20 16.38 722 544 Pliant Therapeutics, Inc. PLN-74809 / IPF Phase 2 423 06/03/20 19.00 700 456 Viking Therapeutics, Inc. VK2809 / NASH Phase 2 6.57 520 292 Intercept Pharmaceuticals, Inc. Obeticholic Acid / PBC Commercial 15.41 461 782 89bio, Inc. BIO89-100 / NASH Phase 2 123 11/11/19 20.06 412 242 Terns Pharmaceuticals, Inc. TERN-101 / NASH Phase 2 280 02/04/21 10.97 280 95 Vicore Pharma VP01 / IPF Phase 2 2.32 166 107 Mean $325 $841 $651 Median $347 $700 $544

51 Idiopathic Pulmonary Fibrosis Market Landscape and Opportunities

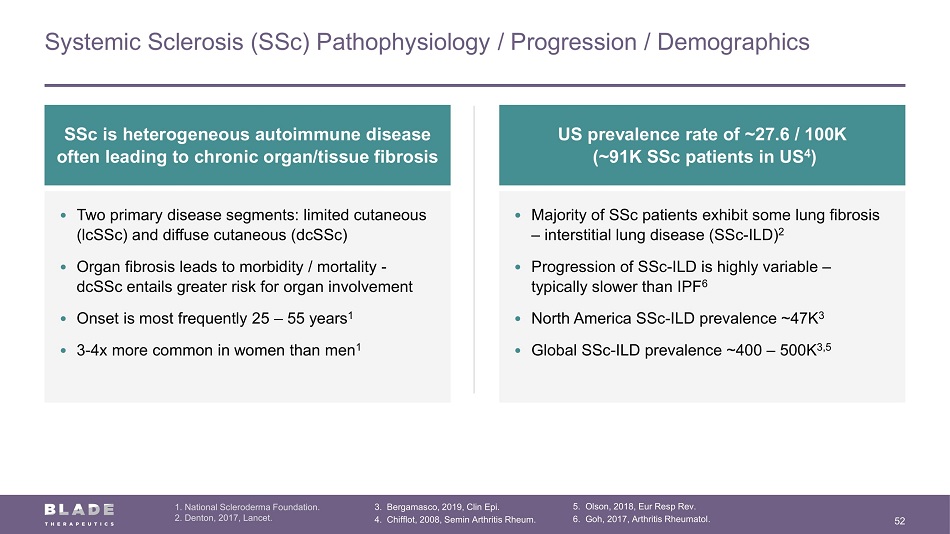

Systemic Sclerosis (SSc) Pathophysiology / Progression / Demographics 52 1. National Scleroderma Foundation. 2. Denton, 2017, Lancet. 3. Bergamasco, 2019, Clin Epi. 4. Chifflot, 2008, Semin Arthritis Rheum. 5. Olson, 2018, Eur Resp Rev. 6. Goh, 2017, Arthritis Rheumatol. SSc is heterogeneous autoimmune disease often leading to chronic organ/tissue fibrosis • Majority of SSc patients exhibit some lung fibrosis – interstitial lung disease (SSc - ILD) 2 • Progression of SSc - ILD is highly variable – typically slower than IPF 6 • North America SSc - ILD prevalence ~47K 3 • Global SSc - ILD prevalence ~400 – 500K 3,5 • Two primary disease segments: limited cutaneous (lcSSc) and diffuse cutaneous (dcSSc) • Organ fibrosis leads to morbidity / mortality - dcSSc entails greater risk for organ involvement • Onset is most frequently 25 – 55 years 1 • 3 - 4x more common in women than men 1 US prevalence rate of ~27.6 / 100K (~91K SSc patients in US 4 )

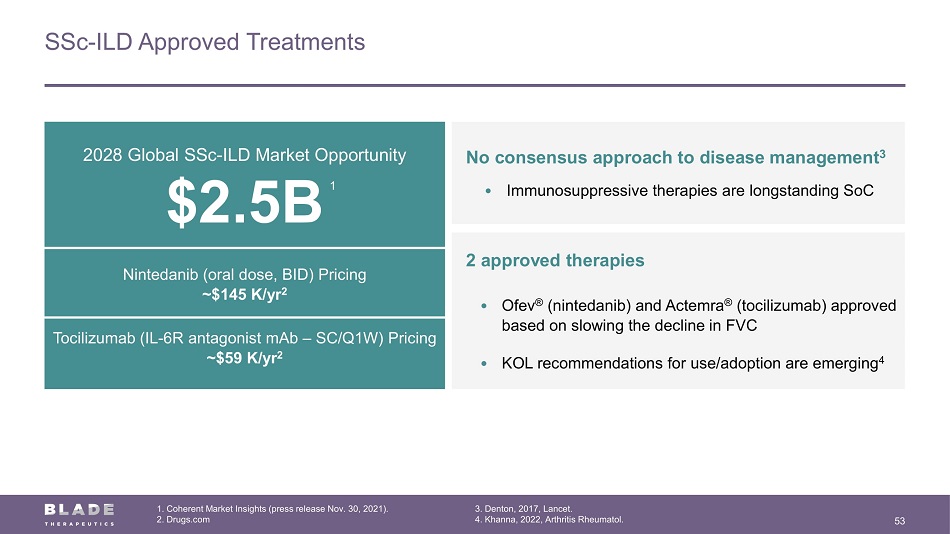

SSc - ILD Approved Treatments 53 1. Coherent Market Insights (press release Nov. 30, 2021). 2. Drugs.com No consensus approach to disease management 3 • Immunosuppressive therapies are longstanding SoC 2 approved therapies • Ofev ® (nintedanib) and Actemra ® (tocilizumab) approved based on slowing the decline in FVC • KOL recommendations for use/adoption are emerging 4 2028 Global SSc - ILD Market Opportunity $2.5B Nintedanib (oral dose, BID) Pricing ~$145 K/yr 2 Tocilizumab (IL - 6R antagonist mAb – SC/Q1W) Pricing ~$59 K/yr 2 1 3. Denton, 2017, Lancet. 4. Khanna, 2022, Arthritis Rheumatol.

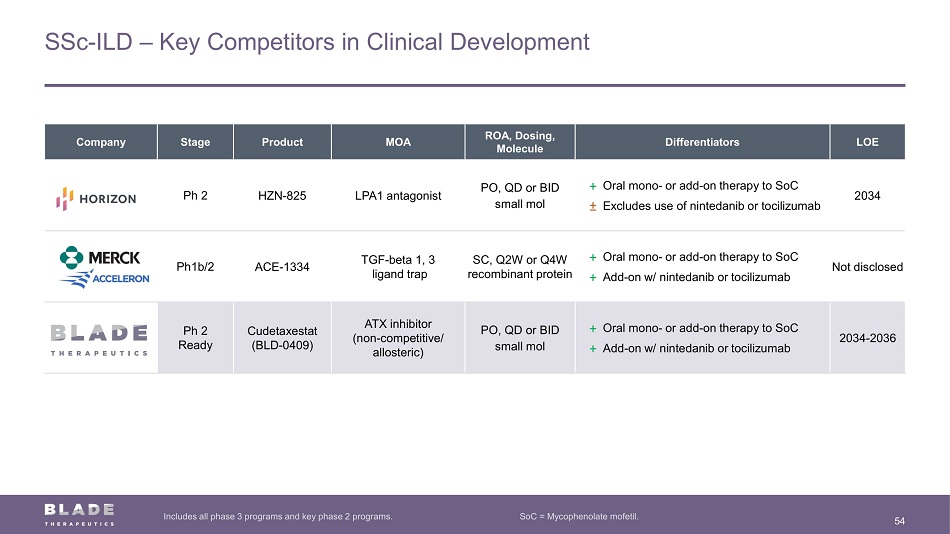

SSc - ILD – Key Competitors in Clinical Development 54 Includes all phase 3 programs and key phase 2 programs. SoC = Mycophenolate mofetil. Company Stage Product MOA ROA, Dosing, Molecule Differentiators LOE Ph 2 HZN - 825 LPA1 antagonist PO, QD or BID small mol + Oral mono - or add - on therapy to SoC ± Excludes use of nintedanib or tocilizumab 2034 Ph1b/2 ACE - 1334 TGF - beta 1, 3 ligand trap SC, Q2W or Q4W recombinant protein + Oral mono - or add - on therapy to SoC + Add - on w/ nintedanib or tocilizumab Not disclosed Ph 2 Ready Cudetaxestat (BLD - 0409) ATX inhibitor (non - competitive/ allosteric) PO, QD or BID small mol + Oral mono - or add - on therapy to SoC + Add - on w/ nintedanib or tocilizumab 2034 - 2036

55 Neurodegeneration Market Landscape and Opportunities

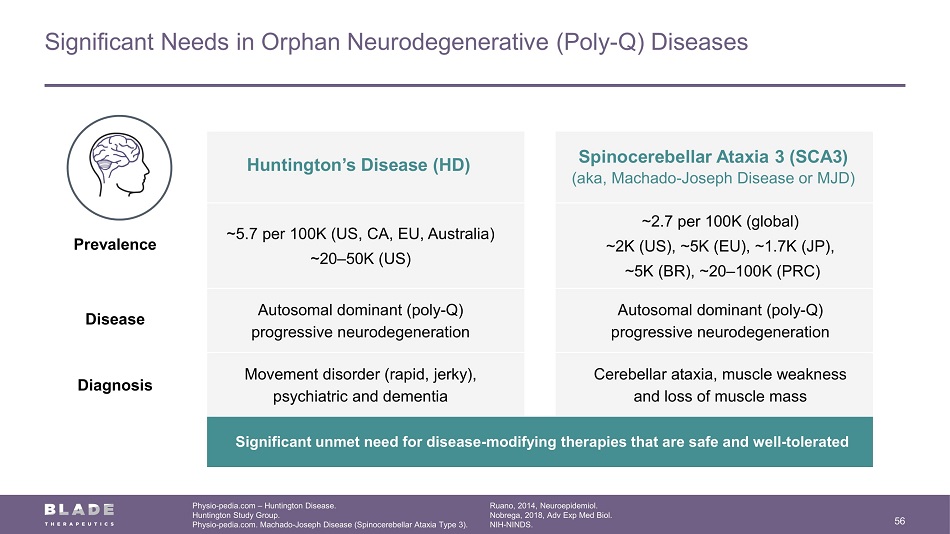

Significant Needs in Orphan Neurodegenerative (Poly - Q) Diseases 56 Physio - pedia.com – Huntington Disease. Huntington Study Group. Physio - pedia.com. Machado - Joseph Disease (Spinocerebellar Ataxia Type 3). Ruano, 2014, Neuroepidemiol. Nobrega, 2018, Adv Exp Med Biol. NIH - NINDS. Huntington’s Disease (HD) Spinocerebellar Ataxia 3 (SCA3) (aka, Machado - Joseph Disease or MJD) Prevalence ~5.7 per 100K (US, CA, EU, Australia) ~20 – 50K (US) ~2.7 per 100K (global) ~2K (US), ~5K (EU), ~1.7K (JP), ~5K (BR), ~20 – 100K (PRC) Disease Autosomal dominant (poly - Q) progressive neurodegeneration Autosomal dominant (poly - Q) progressive neurodegeneration Diagnosis Movement disorder (rapid, jerky), psychiatric and dementia Cerebellar ataxia, muscle weakness and loss of muscle mass Significant unmet need for disease - modifying therapies that are safe and well - tolerated

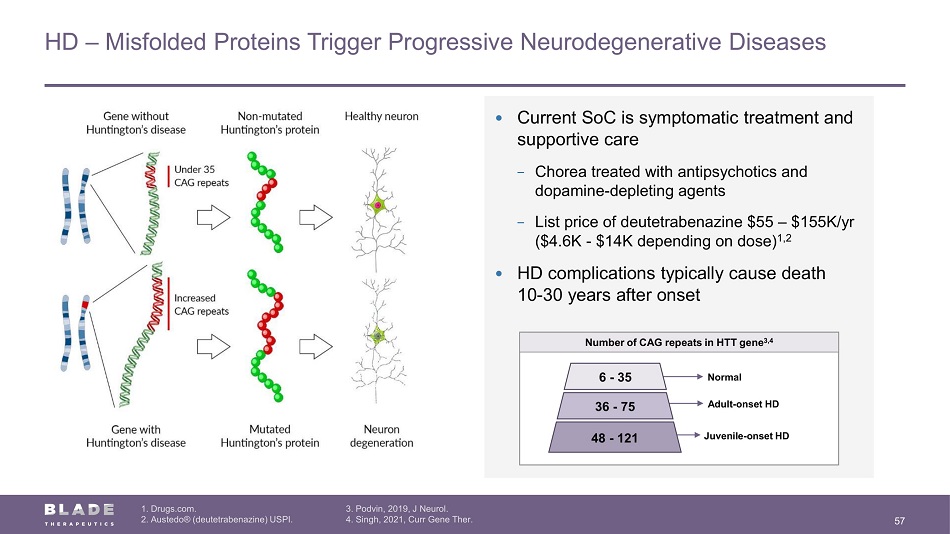

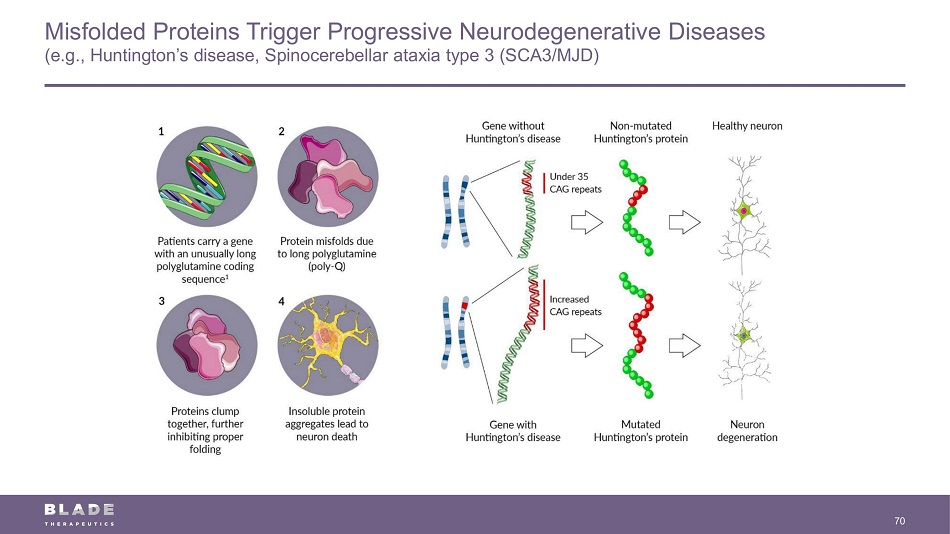

HD – Misfolded Proteins Trigger Progressive Neurodegenerative Diseases 57 1. Drugs.com. 2. Austedo® ( deutetrabenazine) USPI. 3. Podvin, 2019, J Neurol. 4. Singh, 2021, Curr Gene Ther. • Current SoC is symptomatic treatment and supportive care − Chorea treated with antipsychotics and dopamine - depleting agents − List price of deutetrabenazine $55 – $155K/yr ($4.6K - $14K depending on dose) 1,2 • HD complications typically cause death 10 - 30 years after onset Number of CAG repeats in HTT gene 3,4 Juvenile - onset HD Adult - onset HD Normal 48 - 121 36 - 75 6 - 35

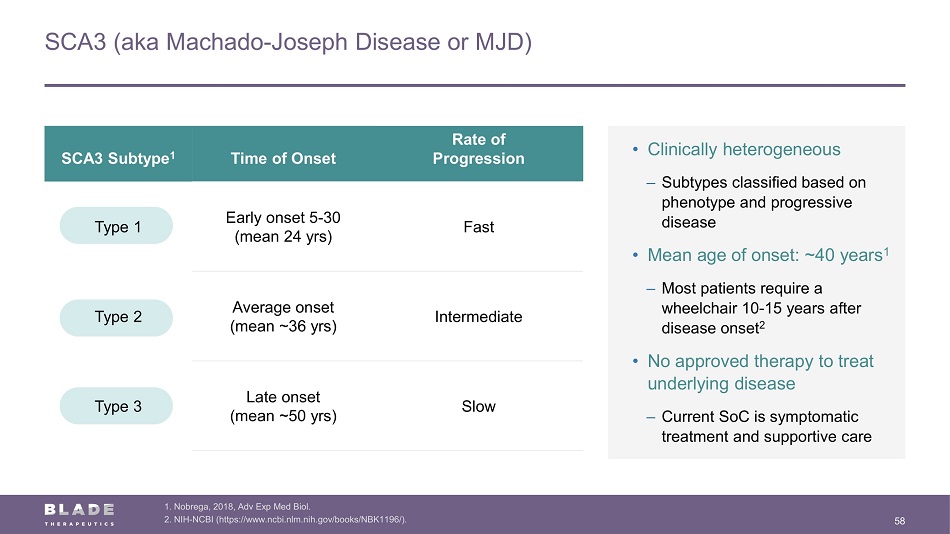

SCA3 (aka Machado - Joseph Disease or MJD) 58 1. Nobrega, 2018, Adv Exp Med Biol. 2. NIH - NCBI (https://www.ncbi.nlm.nih.gov/books/NBK1196/). SCA3 Subtype 1 Time of Onset Rate of Progression Type 1 Early onset 5 - 30 (mean 24 yrs) Fast Type 2 Average onset (mean ~36 yrs) Intermediate Type 3 Late onset (mean ~50 yrs) Slow • Clinically heterogeneous ‒ Subtypes classified based on phenotype and progressive disease • Mean age of onset: ~40 years 1 ‒ Most patients require a wheelchair 10 - 15 years after disease onset 2 • No approved therapy to treat underlying disease ‒ Current SoC is symptomatic treatment and supportive care

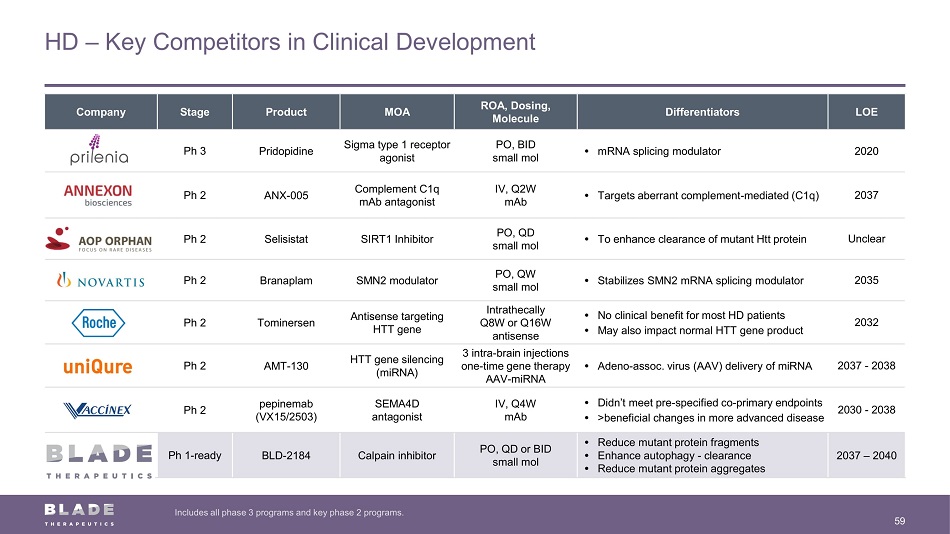

HD – Key Competitors in Clinical Development Includes all phase 3 programs and key phase 2 programs. 59 Company Stage Product MOA ROA, Dosing, Molecule Differentiators LOE Prilenia Ph 3 Pridopidine Sigma type 1 receptor agonist PO, BID small mol • mRNA splicing modulator 2020 Annexon Ph 2 ANX - 005 Complement C1q mAb antagonist IV, Q2W mAb • Targets aberrant complement - mediated (C1q) 2037 AOP Orphan Pharma Ph 2 Selisistat SIRT1 Inhibitor PO, QD small mol • To enhance clearance of mutant Htt protein Unclear Novartis Ph 2 Branaplam SMN2 modulator PO, QW small mol • Stabilizes SMN2 mRNA splicing modulator 2035 Roche Ph 2 Tominersen Antisense targeting HTT gene Intrathecally Q8W or Q16W antisense • No clinical benefit for most HD patients • May also impact normal HTT gene product 2032 UniQure Ph 2 AMT - 130 HTT gene silencing (miRNA) 3 intra - brain injections one - time gene therapy AAV - miRNA • Adeno - assoc. virus (AAV) delivery of miRNA 2037 - 2038 Ph 2 pepinemab (VX15/2503) SEMA4D antagonist IV, Q4W mAb • Didn’t meet pre - specified co - primary endpoints • >beneficial changes in more advanced disease 2030 - 2038 Ph 1 - ready BLD - 2184 Calpain inhibitor PO, QD or BID small mol • Reduce mutant protein fragments • Enhance autophagy - clearance • Reduce mutant protein aggregates 2037 – 2040

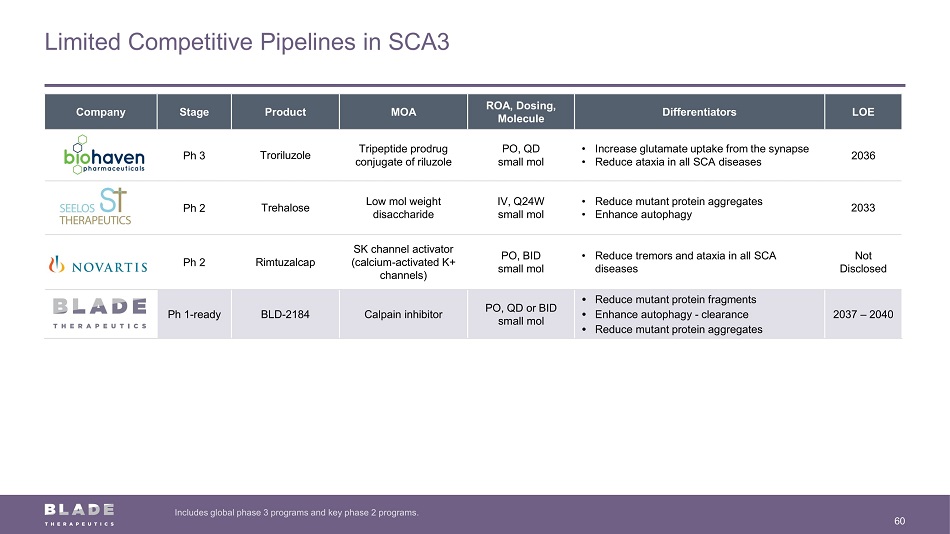

Limited Competitive Pipelines in SCA3 Includes global phase 3 programs and key phase 2 programs. 60 Company Stage Product MOA ROA, Dosing, Molecule Differentiators LOE Ph 3 Troriluzole Tripeptide prodrug conjugate of riluzole PO, QD small mol • Increase glutamate uptake from the synapse • Reduce ataxia in all SCA diseases 2036 Ph 2 Trehalose Low mol weight disaccharide IV, Q24W small mol • Reduce mutant protein aggregates • Enhance autophagy 2033 Novartis Ph 2 Rimtuzalcap SK channel activator (calcium - activated K+ channels) PO, BID small mol • Reduce tremors and ataxia in all SCA diseases Not Disclosed Ph 1 - ready BLD - 2184 Calpain inhibitor PO, QD or BID small mol • Reduce mutant protein fragments • Enhance autophagy - clearance • Reduce mutant protein aggregates 2037 – 2040

61 Fibrosis – Cudetaxestat Non - Competitive Autotaxin Inhibitor Targeting IPF

Cudetaxestat – Potential 50x Potency Advantage vs. Ziritaxestat (GLPG - 1690) 62 * Plasma concentrations of LPC in an animal model of liver fibrosis is between 200 - 250 µM. Head - to - head clinical studies comparing cudetaxestat with currently approved or investigational therapies have not been conducte d. Above data from preclinical biochemical study. • Non - competitive inhibitor cudetaxestat shown to maintain potency in preclinical biochemical assay – Cudetaxestat expected to maintain potency in disease state – Potentially advantageous for efficacy and safety profile • 50% inhibition at 250 uM concentration of LPC* – Cudetaxestat: 8 nM – GLPG - 1690: ~400 nM (competitive inhibitor loses potency) Cudetaxestat

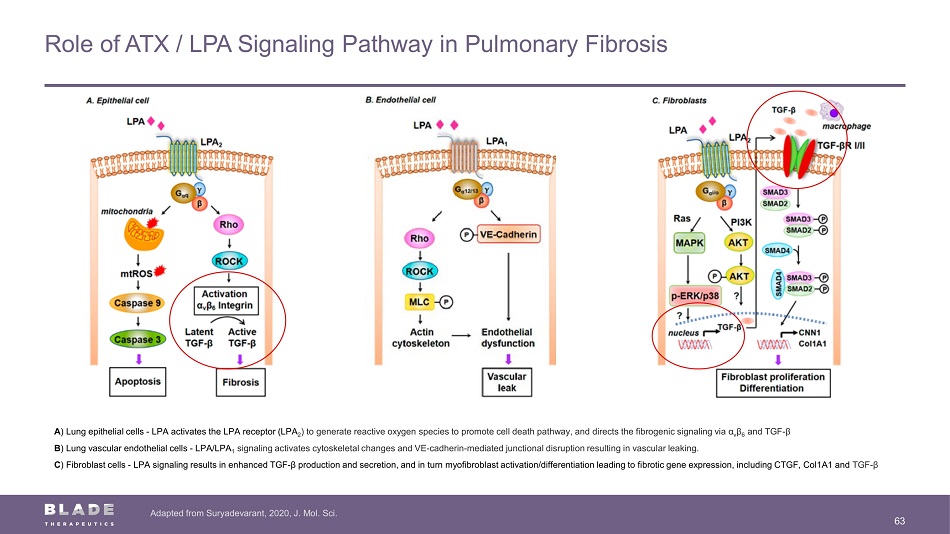

Role of ATX / LPA Signaling Pathway in Pulmonary Fibrosis 63 Adapted from Suryadevarant, 2020, J. Mol. Sci. A ) Lung epithelial cells - LPA activates the LPA receptor (LPA 2 ) to generate reactive oxygen species to promote cell death pathway, and directs the fibrogenic signaling via α v β 6 and TGF - β B ) Lung vascular endothelial cells - LPA/LPA 1 signaling activates cytoskeletal changes and VE - cadherin - mediated junctional disruption resulting in vascular leaking. C ) Fibroblast cells - LPA signaling results in enhanced TGF - β production and secretion, and in turn myofibroblast activation/diff erentiation leading to fibrotic gene expression, including CTGF, Col1A1 and TGF - β

Cudetaxestat Displays Robust Activity ( in vivo ) on Lung Fibrosis 64 SMA (smooth muscle actin), collagen 1A1 and assembled collagen data from preclinical study conducted in mouse bleomycin lung fib rosis model dosed once daily. PAI - 1, IL - 6 and CTGF (connective tissue growth factor) data from preclinical study conducted in mouse bleomycin lung fibrosis mo del dosed twice daily. SMA gene expression Marker of myofibroblast activation Collagen 1A1 gene expression Primary component of fibrosis, produced by myofibroblasts Assembled collagen Represents advanced fibrosis ANOVA One - Way *p<0.05 | **p<0.01 ***p<0.001 | ****p<0.0001 Saline Vehicle Cude 3mg/kg Cude 10mg/kg Cude 30mg/kg Bleomycin + Vehicle Bleomycin + cudetaxestat 30 mg/kg

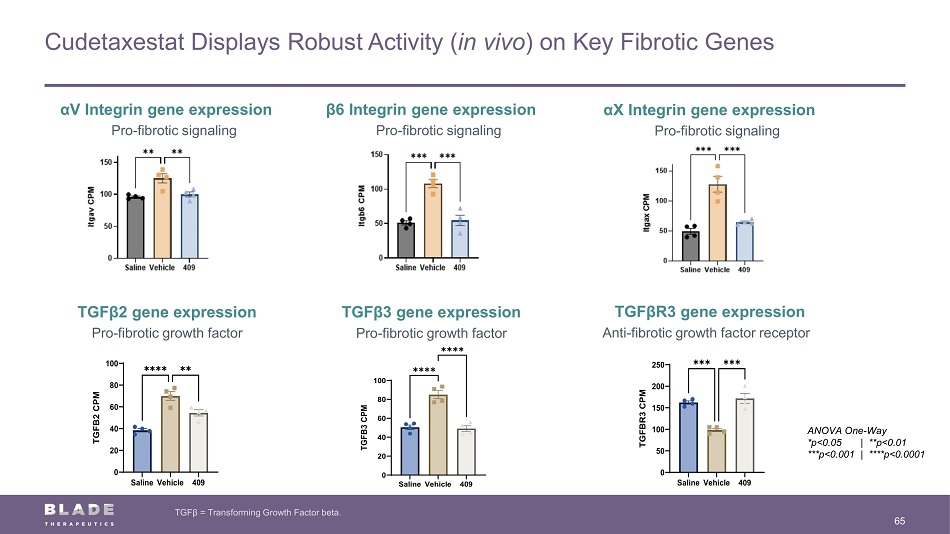

Cudetaxestat Displays Robust Activity ( in vivo ) on Key Fibrotic Genes 65 TGF β = Transforming Growth Factor beta. α V Integrin gene expression Pro - fibrotic signaling TGF β 2 gene expression Pro - fibrotic growth factor β 6 Integrin gene expression Pro - fibrotic signaling ANOVA One - Way *p<0.05 | **p<0.01 ***p<0.001 | ****p<0.0001 SalineVehicle 409 0 20 40 60 80 100 TGFB2 Gene Counts T G F B 2 C P M ✱✱✱✱ ✱✱ SalineVehicle 409 0 20 40 60 80 100 TGFB3 Gene Counts T G F B 3 C P M ✱✱✱✱ ✱✱✱✱ α X Integrin gene expression Pro - fibrotic signaling TGF β 3 gene expression Pro - fibrotic growth factor TGF β R3 gene expression Anti - fibrotic growth factor receptor

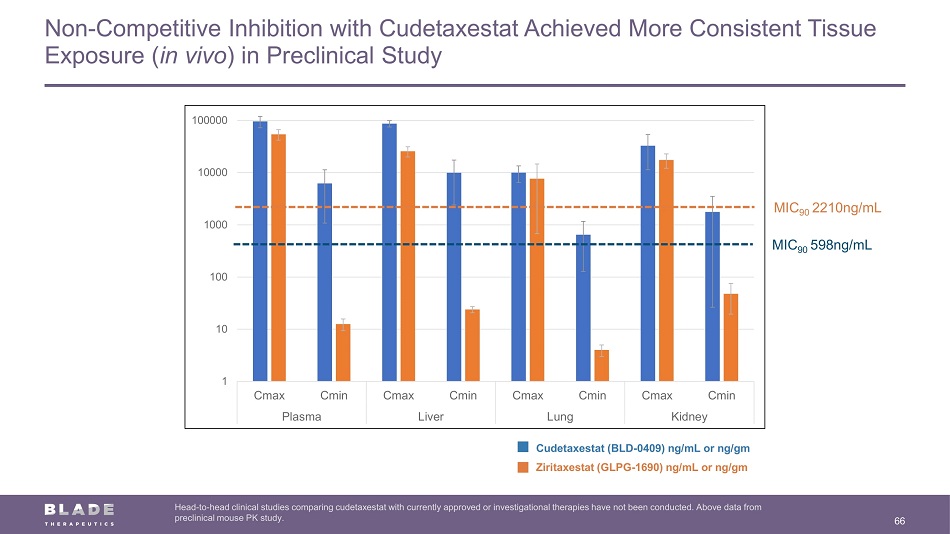

Non - Competitive Inhibition with Cudetaxestat Achieved More Consistent Tissue Exposure ( in vivo ) in Preclinical Study 66 Head - to - head clinical studies comparing cudetaxestat with currently approved or investigational therapies have not been conducte d. Above data from preclinical mouse PK study. 1 10 100 1000 10000 100000 Cmax Cmin Cmax Cmin Cmax Cmin Cmax Cmin Plasma Liver Lung Kidney MIC 90 598ng/mL MIC 90 2210ng/mL Cudetaxestat (BLD - 0409) ng/mL or ng/gm Ziritaxestat (GLPG - 1690) ng/mL or ng/gm

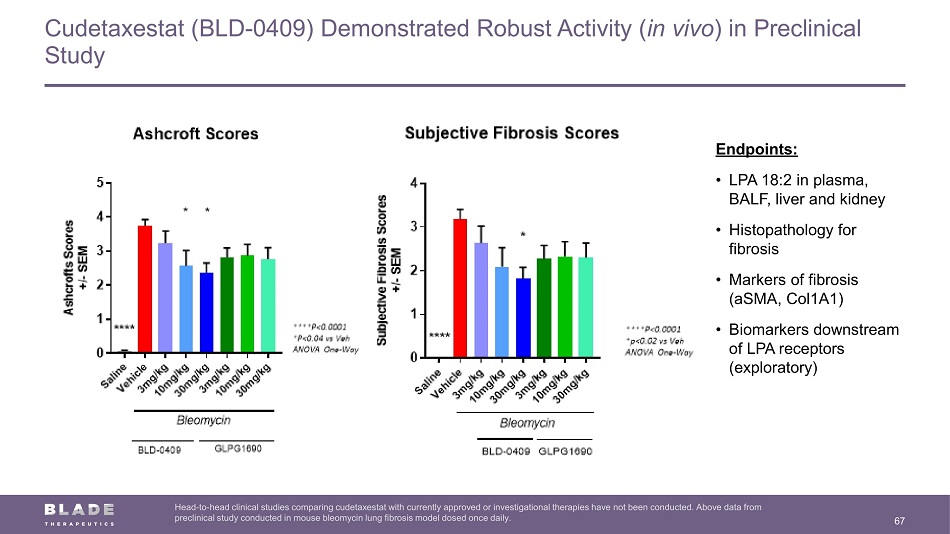

Cudetaxestat (BLD - 0409) Demonstrated Robust Activity ( in vivo ) in Preclinical Study 67 Head - to - head clinical studies comparing cudetaxestat with currently approved or investigational therapies have not been conducte d. Above data from preclinical study conducted in mouse bleomycin lung fibrosis model dosed once daily. Endpoints: • LPA 18:2 in plasma, BALF, liver and kidney • Histopathology for fibrosis • Markers of fibrosis (aSMA, Col1A1) • Biomarkers downstream of LPA receptors (exploratory)

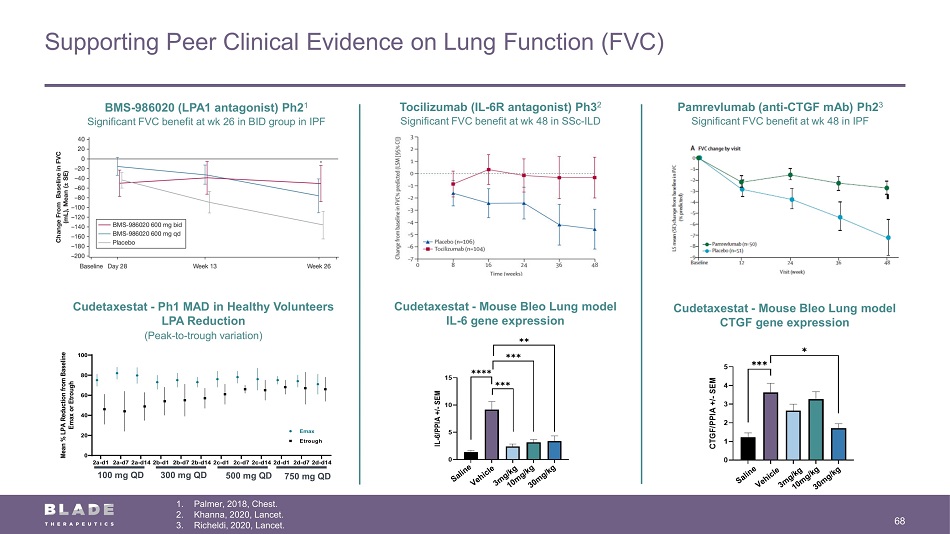

Supporting Peer Clinical Evidence on Lung Function (FVC) 68 BMS - 986020 (LPA1 antagonist) Ph2 1 Significant FVC benefit at wk 26 in BID group in IPF Tocilizumab (IL - 6R antagonist) Ph3 2 Significant FVC benefit at wk 48 in SSc - ILD Pamrevlumab (anti - CTGF mAb) Ph2 3 Significant FVC benefit at wk 48 in IPF Cudetaxestat - Ph1 MAD in Healthy Volunteers LPA Reduction (P eak - to - trough variation) 100 mg QD 300 mg QD 2a-d1 2a-d72a-d142b-d1 2b-d72b-d142c-d1 2c-d72c-d142d-d1 2d-d72d-d14 0 20 40 60 80 100 M e a n % L P A R e d u c t i o n f r o m B a s e l i n e E m a x o r E t r o u g h Emax Etrough 5 00 mg QD 750 mg QD Cudetaxestat - Mouse Bleo Lung model IL - 6 gene expression Cudetaxestat - Mouse Bleo Lung model CTGF gene expression 1. Palmer, 2018, Chest. 2. Khanna, 2020, Lancet. 3. Richeldi, 2020, Lancet.

69 Neurodegeneration – BLD - 2184 CNS - Penetrant Calpain Inhibitor for Poly - Q Neurodegenerative Conditions

Misfolded Proteins Trigger Progressive Neurodegenerative Diseases (e.g., Huntington’s disease, Spinocerebellar ataxia type 3 (SCA3/MJD) 70

Calpain Inhibitors Enhance Autophagy in Preclinical Studies ( in vitro, in vivo ) 71 BLD - 2736 increases autophagic flux in zebrafish larvae ( in vivo ) Increased autophagic flux (measured as ratio of LC3 - II to LC3 - I) Increased autophagic flux as measured by LC3B - II (in presence of chloroquine, which blocks lysosomal degradation) BLD - 2184 increases autophagic flux in neuro2A cells ( in vitro )

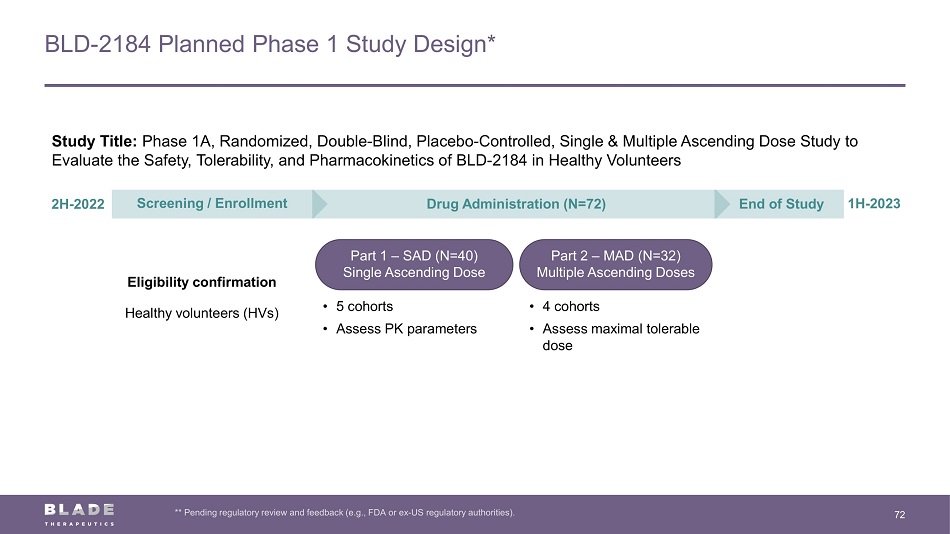

BLD - 2184 Planned Phase 1 Study Design* 72 ** Pending regulatory review and feedback (e.g., FDA or ex - US regulatory authorities). Study Title: Phase 1A, Randomized, Double - Blind, Placebo - Controlled, Single & Multiple Ascending Dose Study to Evaluate the Safety, Tolerability, and Pharmacokinetics of BLD - 2184 in Healthy Volunteers Eligibility confirmation Healthy volunteers (HVs) Part 2 – MAD (N=32) Multiple Ascending Doses Part 1 – SAD (N=40) Single Ascending Dose • 5 cohorts • Assess PK parameters • 4 cohorts • Assess maximal tolerable dose 2H - 2022 1H - 2023 Screening / Enrollment End of Study Drug Administration (N=72)