UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

___________________________

FORM 10-K

___________________________

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2021

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission File Number: 001-39653

___________________________

(Exact name of registrant as specified in its charter)

___________________________

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||

| (address of principal executive offices) | |||||||||||

(212 ) 419-3000

(Registrant’s telephone number, including area code)

___________________________

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol(s) | Name of each exchange on which registered | ||||||||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer | ☐ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report Yes ☐ No ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the common shares held by non-affiliates of the registrant on June 30, 2021, was approximately $4.1 billion. As of February 16, 2022, there were 404,919,411 of the registrant’s shares of Class A common stock outstanding, 674,766,200 shares of the registrant’s Class C common stock outstanding and 319,132,127 of the registrant’s Class D common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

TABLE OF CONTENTS

| Page | ||||||||

F-1 | ||||||||

2

DEFINED TERMS

| Assets Under Management or AUM | Refers to the assets that we manage, and are generally equal to the sum of (i) net asset value (“NAV”); (ii) drawn and undrawn debt; (iii) uncalled capital commitments; and (iv) total managed assets for certain Real Estate products. | |||||||

| our BDCs | Refers to our business development companies, as regulated under the Investment Company Act of 1940, as amended: Owl Rock Capital Corporation (NYSE: ORCC) (“ORCC”), Owl Rock Capital Corporation II (“ORCC II”), Owl Rock Capital Corporation III (“ORCC III”), Owl Rock Technology Finance Corp. (“ORTF”), Owl Rock Technology Finance Corp. II (“ORTF II”), Owl Rock Core Income Corp. (“ORCIC”) and Owl Rock Technology Income Corp. (“ORTIC”). | |||||||

| Blue Owl, the Company, the firm, we, us, and our | Refers to the Registrant and its consolidated subsidiaries. | |||||||

| Blue Owl Carry | Refers to Blue Owl Capital Carry LP. | |||||||

| Blue Owl GP | Refers collectively to Blue Owl Capital Holdings GP LLC and Blue Owl Capital GP LLC, which are directly or indirectly wholly owned subsidiaries of the Registrant that hold the Registrants interests in the Blue Owl Operating Partnerships. | |||||||

| Blue Owl Holdings | Refers to Blue Owl Capital Holdings LP. | |||||||

| Blue Owl Operating Group | Refers collectively to the Blue Owl Operating Partnerships and their consolidated subsidiaries. | |||||||

| Blue Owl Operating Group Units | Refers collectively to a unit in each of the Blue Owl Operating Partnerships. | |||||||

| Blue Owl Operating Partnerships | Refers to Blue Owl Carry and Blue Owl Holdings, collectively. | |||||||

| Blue Owl Securities | Refers to Blue Owl Securities LLC (formerly, Owl Rock Capital Securities LLC). | |||||||

| Business Combination | Refers to the transactions contemplated by the Business Combination Agreement, which were completed on May 19, 2021. | |||||||

| Business Combination Agreement or BCA | Refers to the agreement dated as of December 23, 2020 (as the same has been or may be amended, modified, supplemented or waived from time to time), by and among Altimar Acquisition Corporation, Owl Rock Capital Group LLC, Owl Rock Capital Feeder LLC, Owl Rock Capital Partners LP and Neuberger Berman Group LLC. | |||||||

| Business Combination Date | Refers to May 19, 2021. | |||||||

| Class A Shares | Refers to the Class A common stock, par value $0.0001 per share, of the Registrant. | |||||||

| Class B Shares | Refers to the Class B common stock, par value $0.0001 per share, of the Registrant. | |||||||

| Class C Shares | Refers to the Class C common stock, par value $0.0001 per share, of the Registrant. | |||||||

| Class D Shares | Refers to the Class D common stock, par value $0.0001 per share, of the Registrant. | |||||||

| Class E Shares | Refers to the Class E common stock, par value $0.0001 per share, of the Registrant. | |||||||

| Direct Lending | Refers to our Direct Lending products, which offer private credit solutions to middle-market companies through four investment strategies: diversified lending, technology lending, first lien lending and opportunistic lending. Direct Lending products are managed by the Owl Rock division of Blue Owl. | |||||||

| Dyal Capital | Refers to the Dyal Capital Partners business, which was acquired from Neuberger Berman Group LLC in connection with the Business Combination, and is now a division of Blue Owl. | |||||||

| Fee-Paying AUM or FPAUM | Refers to the AUM on which management fees are earned. For our BDCs, FPAUM is generally equal to total assets (including assets acquired with debt but excluding cash). For our other Direct Lending products, FPAUM is generally equal to NAV or investment cost. FPAUM also includes uncalled committed capital for products where we earn management fees on such uncalled committed capital. For our GP Capital Solutions products, FPAUM for the GP minority equity investments strategy is generally equal to capital commitments during the investment period and the cost of unrealized investments after the investment period. For GP Capital Solutions’ other strategies, FPAUM is generally equal to investment cost. For Real Estate, FPAUM is generally based on total assets (including assets acquired with debt). | |||||||

| Financial Statements | Refers to our consolidated and combined financial statements included in this report. | |||||||

3

| GP Capital Solutions | Refers to our GP Capital Solutions products, which primarily focus on acquiring equity stakes in, or providing debt financing to, large, multi-product private equity and private credit platforms through three existing and one emerging investment strategies: GP minority equity investments, GP debt financing, professional sports minority investments and co-investments and structured equity. GP Capital Solutions products are managed by the Dyal Capital division of Blue Owl. | |||||||

| NYSE | Refers to the New York Stock Exchange. | |||||||

| Oak Street | Refers to the investment advisory business of Oak Street Real Estate Capital, LLC that was acquired on December 29, 2021, and is now a division of Blue Owl. | |||||||

| Oak Street Acquisition | Refers to the acquisition of Oak Street completed on December 29, 2021. | |||||||

| Owl Rock | Refers collectively to the combined businesses of Owl Rock Capital Group LLC (“Owl Rock Capital Group”) and Blue Owl Securities LLC (formerly, Owl Rock Capital Securities LLC), which was the predecessor of Blue Owl for accounting and financial reporting purposes. References to the Owl Rock division refer to Owl Rock Capital Group and its subsidiaries that manage our Direct Lending products. | |||||||

| Partner Manager | Refers to alternative asset management firms in which the GP Capital Solution products invest. | |||||||

| Part I Fees | Refers to quarterly performance income on the net investment income of our BDCs and similarly structured products, subject to a fixed hurdle rate. These fees are classified as management fees throughout this report, as they are predictable and recurring in nature, not subject to repayment, and cash-settled each quarter. | |||||||

| Part II Fees | Generally refers to fees from our BDCs and similarly structured products that are paid in arrears as of the end of each measurement period when the cumulative aggregate realized capital gains exceed the cumulative aggregate realized capital losses and aggregate unrealized capital depreciation, less the aggregate amount of Part II Fees paid in all prior years since inception. Part II Fees are classified as realized performance income throughout this report. | |||||||

| Principals | Refers to our founders and senior members of management who hold, or in the future may hold, Class B Shares and Class D Shares. Class B Shares and Class D Shares collectively represent 90% of the total voting power of all shares. | |||||||

| Real Estate | Refers, unless context indicates otherwise, to our Real Estate products, which primarily focus on providing investors with predictable current income, and potential for appreciation, while focusing on limiting downside risk through a unique net lease platform. Real Estate products are managed by the Oak Street division of Blue Owl. | |||||||

| Registrant | Refers to Blue Owl Capital Inc. | |||||||

| SEC | Refers to the U.S. Securities and Exchange Commission. | |||||||

| Tax Receivable Agreement or TRA | Refers to the Amended and Restated Tax Receivable Agreement, dated as of October 22, 2021, as may be amended from time to time by and among the Registrant, Blue Owl Capital GP LLC, the Blue Owl Operating Partnerships and each of the Partners (as defined therein) party thereto. | |||||||

4

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Exchange Act, which reflect our current views with respect to, among other things, future events, operations and financial performance. You can identify these forward-looking statements by the use of forward-looking words such as “outlook,” “believes,” “expects,” “potential,” “continues,” “may,” “will,” “should,” “seeks,” “approximately,” “predicts,” “projects,” “intends,” “plans,” “estimates,” “anticipates” or the negative version of those words, other comparable words or other statements that do not relate to historical or factual matters. The forward-looking statements are based on our beliefs, assumptions and expectations of our future performance, taking into account all information currently available to us. Such forward-looking statements are subject to various risks, uncertainties (some of which are beyond our control) or other assumptions relating to our operations, financial results, financial condition, business prospects, growth strategy and liquidity that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. Some of these factors are described under the headings “Item 1A. Risk Factors” and “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.” These factors should not be construed as exhaustive and should be read in conjunction with the risk factors and other cautionary statements that are included in this report and in our other periodic filings. If one or more of these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, our actual results may vary materially from those indicated in these forward-looking statements. New risks and uncertainties arise over time, and it is not possible for us to predict those events or how they may affect us. Therefore, you should not place undue reliance on these forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made. We do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law.

AVAILABLE INFORMATION

We file annual, quarterly and current reports, proxy statements and other information required by the Securities Exchange Act of 1934, as amended (the “Exchange Act”) with the SEC. We make available free of charge on our website (www.blueowl.com) our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and other filing as soon as reasonably practicable after such material is electronically filed with or furnished to the SEC. We also use our website to distribute company information, including assets under management and performance information, and such information may be deemed material. Accordingly, investors should monitor our website, in addition to our press releases, SEC filings and public conference calls and webcasts.

Also posted on our website in the “Investor Relations—Governance” section is the charter for our Audit Committee, as well as our Corporate Governance Guidelines and Code of Business Conduct governing our directors, officers and employees. Information on or accessible through our website is not a part of or incorporated into this report or any other SEC filing. Copies of our SEC filings or corporate governance materials are available without charge upon written request to Blue Owl Capital Inc., 399 Park Avenue, 38th Floor, New York, New York 10022, Attention: Office of the Secretary. Any materials we file with the SEC are also publicly available through the SEC’s website (www.sec.gov).

No statements herein, available on our website or in any of the materials we file with the SEC constitute, or should be viewed as constituting, an offer of any fund.

5

RISK FACTOR SUMMARY

The following is a summary of the risks and uncertainties that could adversely affect our business and financial condition and should be read in conjunction with the complete discussion of risk factors set forth in “Item 1A. Risk Factors.” Some of the factors that could materially and adversely affect our business, financial condition, results of operations and cash flows include, but are not limited to, the following:

•The COVID-19 pandemic has caused severe disruptions in the US and global economy, has disrupted, and may continue to disrupt, industries in which we, our products and our products’ portfolio companies and investments operate and could potentially negatively impact our business, financial condition and results of operations.

•Intense competition among alternative asset managers may make fundraising and the deployment of capital more difficult, thereby limiting our ability to grow or maintain our FPAUM. Such competition may be amplified by changes in fund investor allocations away from alternative asset managers.

•We recently ceased to be an emerging growth company, and now are being required to comply with certain heightened reporting requirements. Fulfilling our obligations incident to being a public company, including compliance with the Exchange Act and the requirements of the Sarbanes-Oxley Act and the Dodd-Frank Act, are expensive and time-consuming, and any delays or difficulties in satisfying these obligations could have a material adverse effect on our future results of operations and our stock price.

•Difficult market and political conditions, including tensions between Russia and Ukraine, may reduce the value or hamper the performance of the investments made by our products or impair the ability of our products to raise or deploy capital, each of which could materially reduce our revenue, earnings and cash flow and adversely affect our financial prospects and condition.

•Management fees comprise the majority of our revenues and a reduction in fees could have an adverse effect on our results of operations and the level of cash available for distributions to our shareholders.

•Our growth depends in large part on our ability to raise new and successor funds. If we were unable to raise such funds, the growth of our FPAUM and management fees, and ability to deploy capital into investments, earning the potential for performance income, would slow or decrease, all of which would materially reduce our revenues and cash flows and adversely affect our financial condition.

•Our GP Capital Solutions products may suffer losses if our Partner Managers are unable to raise new funds or grow their AUM.

•Conflicts of interest may arise in our allocation of capital and co-investment opportunities or in circumstances where we hold investments at different levels of the capital structure.

•Our business is currently focused on multiple investment strategies.

•Our entitlement and that of certain of our shareholders, Principals and employees to receive realized performance income from certain of our funds may create an incentive for us to make more speculative investments and determinations on behalf of our funds than would be the case in the absence of such performance income.

•Our use of leverage to finance our businesses exposes us to substantial risks. Any security interests or negative covenants required by a credit facility we enter into may limit our ability to create liens on assets to secure additional debt.

•Employee misconduct could harm us by impairing our ability to attract and retain fund investors and subjecting us to significant legal liability, regulatory scrutiny and reputational harm.

•Cybersecurity risks and cyber incidents could adversely affect our business by causing a disruption to our operations, a compromise or corruption of our confidential information and confidential information in our possession and damage to our business relationships, any of which could negatively impact our business, financial condition and operating results.

•The use of leverage by our products may materially increase the returns of such funds but may also result in significant losses or a total loss of capital.

•The multi-class structure of our common stock has the effect of concentrating voting power with the Principals, which will limit an investor’s ability to influence the outcome of important transactions, including a change in control.

6

•The Registrant is a holding company and its only material source of cash is its indirect interest (held through Blue Owl GP) in the Blue Owl Operating Partnerships, and it is accordingly dependent upon distributions made by its subsidiaries to pay taxes, cause Blue Owl GP to make payments under the Tax Receivable Agreement, and pay dividends.

7

PART I

Item 1. Business.

Blue Owl is a global alternative asset manager with $94.5 billion in AUM as of December 31, 2021. Anchored by a strong permanent capital base, the firm deploys private capital across Direct Lending, GP Capital Solutions and Real Estate strategies on behalf of institutional and private wealth clients. Blue Owl’s flexible, consultative approach helps position the firm as a partner of choice for businesses seeking capital solutions to support their sustained growth. The firm’s management team is comprised of seasoned investment professionals with more than 25 years of experience building alternative investment businesses. Blue Owl employs over 350 people across 9 offices globally.

Blue Owl was formed through the combination of Owl Rock and Dyal Capital in May 2021, at which time these businesses merged with and into Altimar Acquisition Corporation (“Altimar”), a blank check, special purpose acquisition company.

The combination of Owl Rock and Dyal Capital creates a platform primed to continue servicing these markets. In December 2021, we acquired Oak Street, which expanded our firm’s offerings to include real estate-focused products.

Our breadth of offerings and permanent capital base enable us to offer a differentiated, holistic platform of capital solutions to middle market companies, large alternative asset managers and corporate real estate owners and tenants. We provide these solutions through our permanent capital vehicles, as well as long-dated private funds, that we believe provide our business with a high degree of earnings stability and predictability. Our permanent capital vehicles are products that do not have ordinary redemption provisions or a requirement to exit investments after a prescribed period of time to return invested capital to investors, except as required by applicable law or pursuant to redemption requests that can only be made after significant lock-up periods. For the quarter ended December 31, 2021, approximately 98% of our management fees were earned from permanent capital vehicles.

Our global, high-caliber, investor base includes a diversified mix of institutional investors, including prominent public and private pension funds, endowments, foundations, family offices, private banks, high net worth individuals, asset managers and insurance companies, as well as retail clients, accessed through many well-known wealth management firms. We have continued to grow our investor base and presence in the growing private markets and alternative asset management sector by emphasizing our disciplined investment approach, client service, and portfolio performance.

While we currently offer Direct Lending, GP Capital Solutions and Real Estate products across three divisions (Owl Rock, Dyal Capital and Oak Street), our management takes a one-firm approach when making operating decisions and determining how to allocate resources. As a result, we currently operate as a single reportable segment. Management regularly reviews our revenues by product line and our expenses by type at the total firm level (e.g., compensation and benefits; general, administrative and other expenses), and therefore we have presented details of our operating results throughout this report consistent with how management reviews our results.

Our revenues are generated primarily from the investment advisory and administrative services agreements we have with our products. See Note 2 to our Financial Statements for a detailed description of how we earn our revenues and the significant impact that our FPAUM has on the amount of revenues we earn each period. Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) presents additional information on our revenues and operating results, as well as historical AUM and performance information for certain of our products; such information should be read in conjunction with this description of our business.

Our Products

We have three major product lines: Direct Lending, GP Capital Solutions and Real Estate. We believe our products, while distinct, are complementary to each other and together enable us to provide a differentiated platform of varied capital solutions. All of our products employ a disciplined investment philosophy with a focus on long-term investment horizons and are managed by tenured leadership and investment professionals with significant experience in their respective strategies.

Our products are generally structured as BDCs, REITs and private investments funds that aggregate capital from investors. As the investment manager of our products, we invest that capital with the goal of generating attractive, risk-based returns for the investors in our products. In many of our products, we may use leverage to increase the size of the investments our products are able to make. As further explained in Note 2 to our Financial Statements, we generally earn management fees on the amount of FPAUM that we manage; therefore, the growth and success of our product offerings is paramount to our success as an alternative asset manager.

8

Our products create a robust foundation for our holistic platform. We believe the success and growth in our businesses since inception has been driven by a singular, dedicated focus on providing capital solutions and the differentiating competitive features of our platform.

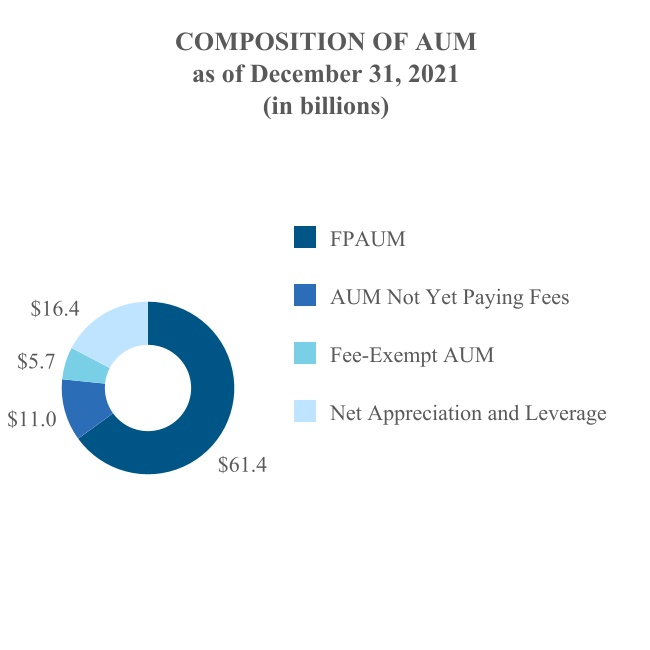

Blue Owl AUM: $94.5 billion FPAUM: $61.4 billion | ||||||||||||||

Direct Lending Products AUM: $39.2 billion FPAUM: $32.0 billion | GP Capital Solutions Products AUM: $39.9 billion FPAUM: $21.2 billion | Real Estate Products AUM: $15.4 billion FPAUM: $8.2 billion | ||||||||||||

Diversified Lending Commenced 2016 AUM: $25.8 billion FPAUM: $21.6 billion | GP Minority Equity Commenced 2010 AUM: $38.7 billion FPAUM: $20.4 billion | Net Lease Commenced 2009 AUM: $15.4 billion FPAUM: $8.2 billion | ||||||||||||

Technology Lending Commenced 2018 AUM: $7.9 billion FPAUM: $6.9 billion | GP Debt Financing Commenced 2019 AUM: $1.0 billion FPAUM: $0.7 billion | |||||||||||||

First Lien Lending Commenced 2018 AUM: $3.5 billion FPAUM: $2.3 billion | Professional Sports Minority Investments Commenced 2021 AUM: $0.2 billion FPAUM: $0.2 billion | |||||||||||||

Opportunistic Lending Commenced 2020 AUM: $2.0 billion FPAUM: $1.2 billion | ||||||||||||||

Direct Lending

Our Direct Lending products offer private credit products to middle-market companies seeking capital solutions. We believe our breadth of offerings establishes us as the lending partner of choice for private-equity sponsored companies, as well as other predominately non-cyclical, recession-resistant businesses. Since the launch of our flagship institutional product, ORCC, we have continued to prudently expand our offerings, focusing on adjacent strategies that are both additive and complementary to our existing product base. Our Direct Lending products are offered through a mix of BDCs, long-dated private funds and other vehicles across the following investment strategies:

•Diversified Lending: Our Diversified Lending strategy seeks to generate current income and, to a lesser extent, capital appreciation by targeting investment opportunities with favorable risk-adjusted returns across credit cycles with an emphasis on preserving capital primarily through originating and making loans to, and making debt and equity investments in, U.S. middle market companies. We provide a wide range of financing solutions with strong focus on the top of the capital structure and operate this strategy through diversification by borrower, sector, sponsor, and position size. Our Diversified Lending strategy is primarily offered to investors through our BDCs.

•Technology Lending: Our Technology Lending strategy seeks to maximize total return by generating current income from our debt investments and other income producing securities, and capital appreciation from our equity and equity-linked investments primarily through originating and making loans to, and making debt and equity investments in, technology related companies based primarily in the United States. We originate and invest in senior secured or unsecured loans, subordinated loans or mezzanine loans, and equity and equity-related securities including common equity, warrants, preferred stock and similar forms of senior equity, which may be convertible into a portfolio company’s common equity. Our Technology Lending strategy invests in a broad range of established and high growth technology companies that are capitalizing on the large and growing demand for technology products and services. This strategy focuses on companies that operate in technology-related industries or sectors which include, but are not limited to, information technology, application or infrastructure software, financial services, data and analytics, security, cloud computing, communications, life sciences, healthcare, media, consumer electronics, semi-conductor, internet commerce and advertising, environmental, aerospace and defense industries and sectors. Our Technology Lending strategy is primarily offered to investors through our technology-focused BDCs.

9

•First Lien Lending: Our First Lien Lending strategy seeks to realize current income with an emphasis on preservation of capital primarily through originating primary transactions in and, to a lesser extent, secondary transactions of first lien senior secured loans in or related to private-equity sponsored, middle market businesses based primarily in the United States. Our First Lien strategy is offered to investors through our long-dated private funds and managed accounts.

•Opportunistic Lending: Our Opportunistic Lending strategy seeks to generate attractive risk-adjusted returns by taking advantage of credit opportunities in U.S. middle market companies with liquidity needs and market leaders seeking to improve their balance sheets. We focus on high-quality companies that could be experiencing disruption, dislocation, distress or transformational change. We aim to be the partner of choice for companies by being well-equipped to provide a variety of financing solutions to meet a broad range of situations, including the following: (i) rescue financing, (ii) new issuance and recapitalizations, (iii) wedge capital, (iv) debtor-in-possession loans, (v) financing for additional liquidity and covenant relief and (vi) broken syndications. Our Opportunistic Lending strategy is offered to investors through our long-dated private funds and managed accounts.

GP Capital Solutions

Our GP Capital Solutions products position us as a leading capital solutions provider to large private capital managers. We primarily focus on acquiring equity stakes in, or providing debt financing to large, multi-product private equity and private credit firms, which we may refer to as “GPs.” Our GP Capital Solutions division also houses our Business Services Platform, which provides strategic support to our Partner Managers. Our GP Capital Solutions products are offered primarily through permanent capital vehicles across the following investment strategies:

•GP Minority Equity Investments: We build diversified portfolios of minority equity investments in institutionalized alternative asset management firms across multiple strategies, geographies, and asset classes. Our investment objective is to generate compelling cash yield by collecting a set percentage of contractually fixed management fees, a set percentage of carried interest and return on balance sheet investments made by underlying managers. We primarily focus on acquiring minority positions in large, multi-product alternative asset managers who continue to gain a disproportionate proportion of the assets flowing into private investment strategies and exhibit high levels of stability. Our inaugural funds followed a hedge fund manager-focused investment program that has since evolved into a private capital manager-focused investment program in our more recent funds. Our GP Minority Equity Investments strategy is offered to investors through our closed-end, permanent capital funds. A fundamental component of the fundraising efforts for our investment programs is the ability to identify and execute co-investment opportunities for our investors. We may offer, from time-to-time and in our sole discretion, co-investment opportunities in certain fund investments, generally with no management or incentive-based fee.

•GP Debt Financing: The GP Debt Financing strategy focuses on originating and making collateralized, long-term debt investments, preferred equity investments and structured investments in private capital managers. We originate and invest in secured term loans that are collateralized by substantially all of the assets of a manager and subject to repayment on an accelerated basis pursuant to cash flow sweeps of set percentages of management fees, GP realization, carried interest and other fee streams of the management company in the event that certain minimum coverage ratios are not maintained. Our investment objective is to generate current income by targeting investment opportunities with attractive risk-adjusted returns. We expect that the loans will be made to allow borrowers to support business growth, fund GP commitments, and launch new strategies. The GP Debt Financing strategy allows us to offer a comprehensive suite of solutions to private capital managers.

•Professional Sports Minority Investments: Our Professional Sports Minority Investments strategy focuses on building diversified portfolios of minority equity investments in professional sport teams. Our first fund in this strategy is NBA-focused.

10

Real Estate

Our real estate products primarily focus on structuring sale-leaseback transactions, which includes triple net leases.

•Net Lease: Our Net Lease real estate strategy is focused on acquiring properties net-leased, long-term to investment grade and creditworthy tenants. Oak Street’s Net Lease real estate strategies focus on acquiring single tenant properties, across industrial, essential retail and mission critical office sectors. By combining our proprietary origination platform, enhanced lease structures and a disciplined investment criteria, we seek to provide investors with predictable current income, and potential for appreciation, while focusing on limiting downside risk.

Our History

Blue Owl’s history is predicated on the key milestones of both Owl Rock and Dyal Capital. Owl Rock was founded in 2016 by Doug Ostrover, Marc Lipschultz and Craig Packer to address the evolving need for direct lending solutions by middle-market companies. Dyal Capital was founded in 2010 by Michael Rees to fill the need for flexible capital solutions for private capital managers. In December 2021, we acquired the Oak Street business, which allowed us to further diversify the products we offer our investors. Since its founding in 2009 by Marc Zahr, Oak Street has established itself as a leader in private equity real estate, offering flexible and unique capital solutions to a variety of corporations and other organizations.

The combination of these businesses creates a platform primed to continue servicing these markets. Blue Owl’s robust and diversified platform offerings will continue to serve as a response to the following sector dynamics:

•shifting allocations by retail institutional investors.

•rotation onto alternatives given the search for yield and reliability of returns.

•rising need for private debt driven by sponsor demand.

•evolving landscape of the private debt market.

•de-leveraging of the global banking system.

•increasing need for flexible capital solutions by private capital managers.

Across our businesses, our presence in the market combined with our constant dialogue with financial sponsors, companies and our investors, has allowed us to identify attractive opportunities in adjacent subsectors over time.

Since inception, Owl Rock, Dyal Capital and Oak Street have launched multiple new strategies and products, exclusively in areas where we believed we could leverage our competitive advantage and expertise, and where we believe we had identified critical mass of lending, capital and real estate solutions opportunities as well as heightened investor interest. We have focused on executing on key adjacencies that are natural extensions of existing core strategies in order to capitalize on the growing dislocations in the market and rising investor demand.

Our Competitive Strengths

•High proportion of permanent capital. We have a high-quality capital base heavily weighted toward permanent capital. For the quarter ended December 31, 2021, approximately 98% of our management fees were earned on AUM that we refer to as permanent capital. Our BDCs, by nature, are closed-end, permanent (or potentially permanent) funds with no mandatory redemption and potentially unlimited duration once listed. Substantially all of the AUM in our GP Capital Solutions and Real Estate products are also structured as permanent capital vehicles. The high proportion of permanent capital in our AUM provides a stable base and allows for our AUM to grow more predictably without having reductions in our asset levels due to ordinary redemptions. Our permanent capital base also lends stability and flexibility to our portfolio companies and Partner Managers, providing us the opportunity to grow alongside these companies and positioning us to be a preferred source of capital and the incumbent lender for follow-ons and other capital solutions to high-performing companies. As such, we are able to be a compelling partner for these firms as they seek capital to support their long-term vision and business development goals. The stability of our AUM base enables us to focus on generating attractive returns by investing in assets with a long-term focus across different periods in the market cycle.

11

•Significant embedded growth in current AUM with built-in mechanisms for fee revenue increases. While we expect to continue our successful fundraising track record to supplement our existing capital base, our current AUM, predominately permanent capital in nature, already provides for significant embedded growth. Of our $94.5 billion AUM base, $61.4 billion represents our current FPAUM. As of December 31, 2021, we have approximately $11.0 billion in AUM not yet paying fees, providing approximately $140.0 million of annualized management fees once deployed. In addition, to the extent any of our BDCs become publicly listed, under the advisory agreements the advisory fees from the applicable BDC could potentially increase, subject to any fee waivers or deferral arrangements agreed to by us and the applicable BDC.

•Stable earnings model with attractive margin profile. The majority of our revenues is generated from our stable management fees. Our predictable revenue base translates to a stable earnings model through a disciplined, efficient cost structure, producing strong profit margins and mitigating the risk of volatility in the profit margins. This allows our business model to maintain a disciplined cost structure and stable operating margins.

•Extensive, long-term relationships with a robust and vast network of alternative asset managers. We have extensive alternative asset manager relationships, which allow us to quickly and efficiently source potential investment opportunities for our products. We believe our deep relationships position us to receive “early looks” and “last looks” from alternative asset managers, which in turn, allow us to be highly selective in deciding which investments to pursue. We believe the depth and breadth of our relationships are predicated on several, differentiating features of our platform and that alternative asset managers value our team’s experience and deep focus both within products and across a broad spectrum of capital solutions. Our expansive set of product offerings allows us to provide flexible and creative solutions, and in tandem with our sizeable permanent capital base, enables us to provide access to scaled, sizeable commitments. Partner Managers in our GP Capital Solutions products also value our Business Services Platform, which provides strategic value-added services to our Partner Managers in five key areas: client development and marketing support, business strategy, product development, talent management, and operational advice. We expect our differentiated approach and broad spectrum of capital solution products will continue to strengthen our relationships, and we intend to further expand our network to fortify our position as a preferred partner for alternative asset managers and their portfolio companies.

•Increasing benefits of scale. We believe our robust, scaled platform presents us with a competitive advantage which enables us to provide attractive solutions as a trusted partner and therefore continue to capture market share. Many institutional investors are concentrating their relationships in an effort to partner with dependable, scaled firms with proven track records that they have a high level of comfort with. Our scaled platform enables us to remain a partner of choice not only for borrowers, GPs and tenants, but also for investors. We believe we will not only maintain, but continue to expand our share of the market as a result of the high level of confidence investors have in our scaled capital solutions platform. Our ability to provide diversification and niche access points will continue to attract investor interest as they seek diversification and continue to value lower-correlation portfolio allocations.

Within Direct Lending, there is significant competition for loans below $50 million, but there are much fewer lenders capable of providing solutions over $100 million. Our differentiated approach and scaled direct lending platform allow us to capitalize on opportunities across the sizing spectrum—from loans below $50 million to loans over $1.0 billion. Our platform’s scale has demonstrated the ability to originate larger deals, while also providing diversification in our portfolios. We believe our scale enables us to broaden our deal funnel and provides us access to more investment opportunities than many other direct lenders. We have significant available capital that allows us to provide scaled financing solutions, commit to full capital structures and support capital needs of borrowers. We believe being a total solutions provider also grants us a broader view of market opportunities, which allows us to continue operating as a market leader.

Within GP Capital Solutions, we have also established ourselves as a market leader, with a long track record, greatest amount of aggregate capital raised and largest number of publicly-announced deals. The target size of our current fund being raised, Fund V, is materially larger than the approximately $5 billion fund sizes of our main competitors. Our large base of stable capital not only enables participation in investments across the sizing spectrum, but also creates a competitive advantage by positioning us as a highly qualified buyer for minority stakes in large, established GPs. We believe that we also gain access to proprietary deal flow as a result of the market’s confidence in our ability to execute on large investments expeditiously. We believe our strong reputation in the market combined with our scale will continue to provide us with unique access to the most attractive sectors of the alternative asset management universe.

12

Within Real Estate, we have a targeted origination strategy that benefits from Oak Street’s strong network and allows us to be competitive with other net lease peers. Oak Street proactively builds and maintains strong relationships with large investment grade-rated and creditworthy companies whose businesses offer essential goods or services and which we believe are generally resistant to e-commerce and economic downside risks, and structures mutually beneficial transactions with long lease durations, and in many cases, favorable pricing. We intend to leverage Oak Street’s corporate partnerships to both source unique investment opportunities unavailable to other market participants and negotiate attractive lease terms. We believe our strong origination capabilities, conservative underwriting criteria and strong existing tenant relationships will allow our Real Estate products to purchase properties in the future at attractive terms and pricing, providing significant long-term opportunities for growth and scale.

Diverse, global and growing high-quality investor base. Our global investor base is composed of long-standing institutional relationships, as well as a quickly growing retail investor base. Our institutional clients include large domestic and international public and private pension funds, endowments, foundations, family offices, sovereign wealth funds, asset managers and insurance companies. Our retail clients include prominent wealth management firms, private banks, and high-net worth investors. As we continue to grow, we expect to retain our existing clients through our breadth of offerings. As of December 31, 2021, approximately 36% of our institutional investors are invested in more than one product, with many increasing their commitment to their initial strategy and additionally committing additional capital across our other strategies. We believe our diligent management of investors’ capital, combined with our strong performance and increasingly diversified product offerings has helped retain and attract investors which has furthered our growth in FPAUM and facilitated further expansion of our strategies. We also believe the global nature of our investor base enables significant cross-selling opportunities between our products and strategies. We are committed to providing our clients with a superior level of service. We believe our client-focused nature, rooted in our culture of transparency will help us continue to retain and attract high quality investors to our platform.

Industry-leading management team with proven track record. We are led by a team of seasoned executives with significant and diverse experience at the world’s leading financial institutions. Our best-in-class management team has considerable expertise across their respective product strategies, with a long track record of successful investing experience across multiple businesses and credit cycles. Members of our senior management have an average of over 25 years of experience and a strong track record in building successful businesses from the ground up and generating superior returns across market cycles. Additionally, our senior management team has experienced no turnover since the inception of our predecessor businesses which we believe has enabled us to build meaningful long-term relationships and partnerships with alternative asset managers as well as with our investors.

Alignment of interests with stakeholders. We consider the alignment of interests of our executive management team and other professionals with those of the investors in our products to be core to our business. AUM (inclusive of accrued carried interest) related to our executives and other employees totaled approximately $1.9 billion, which aligns their interests with our clients’ interests by motivating the continued high-performance and retention of our dedicated team of professionals.

Our Growth Strategy

We aim to continue applying our core principles and values that have guided us since inception in order to expand our business through the following strategies:

•Organically grow our core business. We expect to continue to grow AUM in our existing strategies, and intend to launch additional, successor permanent capital vehicles and similar long-dated products in the future. We will benefit from significant embedded growth in our current AUM that is not yet paying fees that can be realized as we continue to deploy and lever our existing capital base and as fee holidays in certain funds expire. We believe these key attributes, in conjunction with our ability to raise successor products in existing strategies, will continue to play a key role in our growth profile. We also expect to enhance our AUM growth by expanding our current investor relationships and also continuing to attract new investors.

13

•Expand our product offering. We plan to grow our platform by expanding our product offerings. We intend to take a diligent and deliberate approach to expansion, by adding products that are complementary, adjacent or additive to our current strategies. To date, our measured approach to growth through the addition of adjacent strategies has allowed us to continue delivering high performance to our dedicated investor base. We expect that as we continue to grow our existing strategies, there will be additional adjacencies that provide natural expansion opportunities. We believe through the disciplined expansion of our platform, we can continue to develop our breadth of offerings and further our position as a leading solutions provider. As we grow, we expect to attract new investors as well as leverage our existing investor base, as we have done with previous product launches.

•Leverage complementary global distribution networks. We are well positioned to continue to penetrate the growing global market. The success of our Direct Lending and Real Estate products to date has been primarily focused within the United States, while our GP Capital Solutions products have a more global investor base. We intend to continue fundraising both domestically and internationally. The favorable industry tailwinds are global in nature and we believe that there is additional market opportunity across the global landscape. As of December 31, 2021, 77% of capital raised was done so in the United States and Canada. We believe our strong network and track record of global fundraising has primed us to further extend our fundraising efforts across products and into additional international markets, as institutional investors across the globe are facing the same pressures and seeking the same positive attributes of the sector that have attracted domestic investors thus far. We also believe we have a significant opportunity to leverage Dyal Capital’s global fundraising capabilities and investor relationships to cross-sell our Direct Lending and Real Estate products, as well as utilize Owl Rock’s existing domestic retail channel to cross-sell our GP Capital Solutions products while increasing our global capabilities. The global market represents a large, and relatively untapped opportunity for many of our products that we believe will facilitate our pursuit of international expansion in the coming years, and position us to enter into less-developed markets where we can be a significant first-mover and play a key role in defining the markets.

•Enhance our distribution channels. As investors continue to increase their alternatives allocation in the search for yield, we believe we have the opportunity to continue diversifying our client base by attracting new investors across different channels. We intend to leverage our strong growth within and across our strategies as a means to add new investors to our growing family of funds. We have already begun executing on this strategy, with a notable influx of wealth management platforms and public and private pension fund investors in recent years. These additions helped further diversify our investor base which also includes, but is not limited to, insurance, family offices, endowments and foundations. In addition, we have continued to grow our relationships in the consultant community. We intend to be the premier direct lending and GP minority investing platform for investors across the institutional and retail distribution channels.

•Deepen and expand strong strategic relationships with key institutional investors. We have established invaluable relationships with strategic partners, consultants and large institutional investors who provide us with key market insights, operational advice and facilitate relationship introductions. We pride ourselves on continuing to foster these relationships as they are fundamental to our business and reflect the strong alignment of interests that are highly valued by our partners. As of December 31, 2021, eight institutional investors have committed at least $1.0 billion across our strategies, 25 have committed at least $500 million, and 48 have committed at least $250 million. Our strategic partnerships allow us to craft customized solutions tailored to the objectives of our clients, while reflecting the breadth of our capabilities across our strategies. We also have important relationships with sponsors, wealth management firms, banks, corporate advisory firms, industry consultants and other market participants that we believe are of significant value. As we continue to grow, both organically and through product and geographic expansion, we will continue to pursue the addition of incremental key strategic partners.

•Opportunistically pursue accretive acquisitions. In addition to our various avenues of organic growth, we intend to diligently evaluate acquisition opportunities that we believe would be value-enhancing to our current platform. These could include acquisitions that would expand the breadth of our product offerings, further develop our investor base, or facilitate our plans for global expansion. We believe that as the market continues to evolve, there will be numerous opportunities for us to consider, of which we intend to only pursue the most accretive acquisitions.

14

Competition

The investment management industry is intensely competitive, and we expect it to remain so. We compete globally and on a regional, industry and asset basis. We face competition both in the pursuit of investors for our products and investment opportunities. Generally, our competition varies across product lines, geographies and financial markets. We compete for investors based on a variety of factors, including investment performance, investor perception of investment managers’ drive, focus and alignment of interest, quality of service provided to and duration of relationship with investors, breath of our product offering, business reputation and the level of fees and expenses charged for services. We compete for investment opportunities at our funds based on a variety of factors, including breadth of market coverage and relationships, access to capital, transaction execution skills, the range of products and services offered, innovation and price, and we expect that competition will continue to increase.

Competition is also intense for the attraction and retention of qualified employees. Our ability to continue to compete effectively in our businesses will depend upon our ability to attract new employees and retain and motivate our existing employees. See “Risk Factors—Risks Related to Our Business and Operations—Our future growth depends on our ability to attract, retain and develop human capital in a highly competitive talent market.”

Direct Lending

Our competition as an asset manager and financing source to middle market companies consists primarily of other asset managers who focus principally on credit funds, including BDCs, and other credit products. We also compete with public and private funds, BDCs, commercial and investment banks, commercial finance companies and, to the extent they provide an alternative form of financing, private equity and hedge funds. Many of our competitors are substantially larger and may have more financial, technical, and marketing resources than we do. Many of these competitors have similar investment objectives to us, which may create additional competition for investment opportunities. Some of these competitors may also have a lower cost of capital and access to funding sources that are not available to us, which may create competitive disadvantages for us with respect to investment opportunities. In addition, some of our competitors may have higher risk tolerances or different risk assessments, which could allow them to consider a wider variety of investments and establish more relationships than us. Further, many of our competitors are not subject to the regulatory restrictions that the Investment Company Act imposes on us as a business development company, or to the distribution and other requirements we must satisfy to qualify for RIC tax treatment. Lastly, institutional and individual investors are allocating increasing amounts of capital to alternative investment strategies. Several large institutional investors have announced a desire to consolidate their investments in a more limited number of managers. We expect that this will cause competition in our industry to intensify and could lead to a reduction in the size and duration of pricing inefficiencies that many of our products seek to exploit. See “Risk Factors—Risks Relating to Our Businesses and Operations—The investment management business is intensely competitive.”

GP Capital Solutions

Our GP Capital Solutions products currently have limited direct competition from organizations dedicated to acquiring stakes in large institutionalized private capital managers. More recently, a limited number of asset managers have begun acquired minority stakes in certain private capital managers. Such institutions may compete with us for similar investments in the future. We believe, however, that this limited number of competitors is likely to persist, as conflicts of interest and regulatory restrictions make purchasing minority stakes in private capital managers challenging for financial institutions and private equity firms.

With respect to our GP Debt Financing strategy, many banks provide revolving lines of credit to private equity managers, but these credit lines are typically short duration, amortize and require blanket personal guarantees. A small number of firms, provide structured or preferred equity to private capital managers, but these investments are also structurally very different from our products’ long-term loans. We believe that this limited amount of competition is likely to persist, as conflicts of interest, regulatory restrictions, capital constraints and other considerations make lending to private capital managers challenging for financial institutions, insurance companies and other private market firms.

Our current GP Capital Solutions strategies compete with among others, a number of private equity funds, specialized funds, hedge funds, corporate buyers, traditional asset managers, real estate companies, commercial banks, investment banks, other investment managers and other financial institutions, including the owners of certain of our shareholders, as well as domestic and international pension funds and sovereign wealth funds, and we expect that competition will continue to increase. See “Risk Factors—Risks Related to Our Business and Operations—The investment management business is intensely competitive.” We compete globally and on a regional, industry and asset basis.

15

Real Estate

Oak Street has remained the only net let lease private equity manager dedicated exclusively to transacting with investment grade rated and other creditworthy counterparties. The more stable and predictable nature of the net lease sector has brought additional competition into the space in recent years. Historically, such competition has primarily come from net lease REIT’s (publicly traded and non-traded), other private equity real estate funds, and high net worth buyers.

Competitors in the publicly traded net lease sector generally exhibit less stringent criteria than us with respect to pricing and lease durations, and their portfolios are comprised substantially with non-investment grade credits, shorter average lease terms, and meaningful near-term lease rollover. Additionally, many net lease peers focus on acquiring retail properties with an average deal size of less $10 million, whereas our Real Estate products’ transactions are typically $100 million and greater in size.

Competition from other private equity funds has grown, as many have either shifted their current real estate focus to building net lease teams or acquired existing net lease strategies. Despite this increased activity, competition with our Real Estate products on the deal level has remained relatively low, as those strategies concentrate their efforts in the non-investment grade space, prefer to develop properties themselves, and to deploy capital in sectors that are outside of our traditional focus of: industrial assets, mission critical office properties and essential retail. High net worth buyers have been formidable competitors and active acquirers of retail assets under $8 million; they tend to be less price sensitive and there are usually wide pools of potential buyers for these assets. As the monetization of real estate through sale-leasebacks continues to gain traction as a capital allocation tool for companies, we expect the net lease sector to grow even larger, and that will continue to attract more competition into the space.

Human Capital

As of December 31, 2021, we had approximately 350 full-time employees, including over 100 investment professionals across nine offices globally.

As an alternative asset manager, our people are the key to the success of our business. We rely significantly on our talented team, leveraging a wide variety of investment, management, business and other skills and expertise, to create value for shareholders and investors in our products. We aim to build a team that is driven and embraces an inclusive culture where our team members are engaged and work collaboratively across the organization.

Compensation and Benefits

We design our compensation programs to motivate and retain employees and align their interests with those of our shareholders. In particular, annual bonuses for our executives and other senior employees involves a combination of cash and deferred equity awards in the form of Incentive Units and RSUs (as defined in Note 1 to the Financial Statements). The proportion of compensation that is deferred and at risk of forfeiture generally increases as an employee’s level of compensation rises. Employees at higher total compensation levels are generally targeted to receive a greater percentage of their total compensation payable in Incentive Units and RSUs. To further align their interests with those of investors in our products, our employees have the opportunity to make investments in or alongside our products. We also provide our employees robust health and other wellness offerings, as well as a variety of quality of life benefits, including time-off and family planning resources. We believe our approach to compensation and benefits are consistent with companies in the alternative asset management industry and enables us to attract and retain best-in-class talent in our industry. Our senior management periodically reviews the effectiveness and competitiveness of our compensation program.

Diversity, Equity and Inclusion

Blue Owl is committed to fostering, cultivating, and preserving a culture of diversity, equity and inclusion. We prize diversity in our team and seek to create an inclusive, merit-based environment that is supportive of people from all backgrounds.

•Embracing our differences. We embrace and encourage our differences that make us unique. We believe that a team comprised of individuals with diverse backgrounds, experiences, perspectives and insights is critical to the long-term success of our firm.

•Strategic priorities. Continuing to develop as a more diverse, equitable and inclusive firm is a strategic priority for Blue Owl that we believe will further enhance our work environment and overall business. Our commitment to diversity and inclusion is relevant to all areas of the firm’s business.

16

•Corporate practices. We focus on diversity, equity and inclusion in our corporate practices and policies, including: recruitment and hiring; compensation and benefits; professional development and training; promotions; transfers; and social and recreational programs. We also believe diversity, equity, and inclusion is an important component of any environmental, social, and governance program, and are committed to actively engaging with our investment teams on integrating our corporate philosophy into our investment culture.

•Leadership. While our ongoing efforts are championed at the Blue Owl founder-level and executed upon by senior leaders across all business areas of the firm, we strongly believe that these efforts should be employee led. Our aim is to have diversity, equity and inclusion be part of the very fiber of our entire employee population.

| MUTUAL RESPECT | EXCELLENCE | CONSTRUCTIVE DIALOGUE | ONE TEAM | |||||||||||||||||

| BLUE OWL’S CORE VALUES | ||||||||||||||||||||

17

Organizational Structure

The Registrant is a publicly traded holding company, and its primary assets are ownership interests in the Blue Owl Operating Partnerships, which are held indirectly through Blue Owl GP. We conduct our business through the Blue Owl Operating Group. See Note 1 to our Financial Statements for a description of the various share and unit classes outstanding at the Registrant and Blue Owl Operating Partnership levels.

The diagram below depicts a simplified version of our organizational structure as of December 31, 2021. Ownership percentages are based on shares and units that are fully participating in dividends and distributions as of December 31, 2021.

Economic and voting percentages above do not include the potential dilutive impact of the exercise of warrants to purchase Class A Shares, as well as RSUs, unvested Incentive Units and Oak Street Earnout Units, as these interests do not participate in dividends and distributions (other than to the extent of certain tax distributions on unvested Incentive Units). See Note 1 to our consolidated and combined financial statements for additional information on these interests.

18

Regulatory and Compliance Matters

Our business, as well as the financial services industry, generally are subject to extensive regulation, including periodic examinations, by governmental agencies and self-regulatory organizations or exchanges in the U.S. and foreign jurisdictions in which we operate relating to, among other things, antitrust laws, anti-money laundering laws, anti-bribery laws relating to foreign officials, tax laws and privacy laws with respect to client and other information, and some of our funds invest in businesses that operate in highly regulated industries.

Each of the regulatory bodies with jurisdiction over us has regulatory powers dealing with many aspects of financial services, including the authority to grant, and in specific circumstances to cancel, permissions to carry on particular activities. Any failure to comply with these rules and regulations could limit our ability to carry on particular activities or expose us to liability and/or reputational damage. Additional legislation, increasing global regulatory oversight of fundraising activities, changes in rules promulgated by self-regulatory organizations or exchanges or changes in the interpretation or enforcement of existing laws and rules, either in the United States or elsewhere, may directly affect our mode of operation and profitability. See “Risk Factors—Risks Related to Our Business and Operations—Difficult market and political conditions may reduce the value or hamper the performance of the investments made by our products or impair the ability of our products to raise or deploy capital, each of which could materially reduce our revenue, earnings and cash flow and adversely affect our financial prospects and condition.”

Rigorous legal and compliance analysis of our businesses and investments made by our products is important to our culture. We strive to maintain a culture of compliance through the use of policies and procedures such as oversight compliance, codes of ethics, compliance systems, communication of compliance guidance and employee education and training. All employees must annually certify their understanding of and compliance with key global policies, procedures and code of ethics. We have a compliance group that monitors our compliance with the regulatory requirements to which we are subject and manages our compliance policies and procedures. Our Chief Compliance Officer supervises our compliance group, which is responsible for monitoring all regulatory and compliance matters that affect our activities. Our compliance policies and procedures address a variety of regulatory and compliance risks such as the handling of material non-public information, personal securities trading, valuation of investments, document retention, potential conflicts of interest and the allocation of investment opportunities.

Many jurisdictions in which we operate have laws and regulations relating to data privacy, cybersecurity and protection of personal information, including the General Data Protection Regulation, which expands data protection rules for individuals within the European Union (the “EU”) and for personal data exported outside the EU, and the California Consumer Privacy Act, which creates new rights and obligations related to personal data of residents (and households) in California. Any determination of a failure to comply with any such laws or regulations could result in fines or sanctions or both, as well as reputational harm. As these laws and regulations or the enforcement of the same become more stringent, or if new laws or regulations or enacted, our financial performance or plans for growth may be adversely impacted.

SEC Regulations

We provide investment advisory services through several entities that are registered as investment advisers with the SEC pursuant to the Advisers Act. Our BDCs elect to be regulated under the Investment Company Act and the Exchange Act and, in certain cases, the Securities Act. As compared to other, more disclosure-oriented U.S. federal securities laws, the Advisers Act and the Investment Company Act, together with the SEC’s regulations and interpretations thereunder, are highly restrictive regulatory statutes. The SEC is authorized to institute proceedings and impose sanctions for violations of the Advisers Act and the Investment Company Act, ranging from fines and censures to termination of an adviser’s registration.

Under the Advisers Act, an investment adviser (whether or not registered under the Advisers Act) has fiduciary duties to its clients. The SEC has interpreted these duties to impose standards, requirements and limitations on, among other things, trading for proprietary, personal and client accounts; allocations of investment opportunities among clients; and conflicts of interest.

The Advisers Act also imposes specific restrictions on an investment adviser’s ability to engage in principal and agency cross transactions. Our registered investment advisers are subject to many additional requirements that cover, among other things, disclosure of information about our business to clients; maintenance of written policies and procedures; maintenance of extensive books and records; restrictions on the types of fees we may charge, including realized performance income or carried interest; solicitation arrangements; maintaining effective compliance program; custody of client assets; client privacy; advertising; and proxy voting. The SEC has authority to inspect any registered investment adviser and typically inspects a registered investment adviser periodically to determine whether the adviser is conducting its activities in compliance with (i) applicable laws, (ii) disclosures made to clients and (iii) adequate systems, policies and procedures to ensure compliance.

19

A significant portion of our revenues are derived from our advisory services to our BDCs. The Investment Company Act imposes significant requirements and limitations on BDCs, including with respect to their capital structure, investments and transactions. While we exercise broad discretion over the day-to-day management of our BDCs, each of our BDCs is also subject to oversight and management by a board of directors, a majority of whom are not “interested persons” as defined under the Investment Company Act. The responsibilities of each board include, among other things, approving our advisory contract with our BDC; approving certain service providers; determining the valuation and the method for valuing assets; and monitoring transactions involving affiliates and; approving certain co-investment transactions. The advisory contracts with each of our BDCs may be terminated by the shareholders or directors of such BDC on not more than 60 days’ notice, and are subject to annual renewal by each respective BDC’s board of directors after an initial two-year term.

Generally, affiliates of our BDCs are prohibited under the Investment Company Act from knowingly participating in certain transactions with their affiliated BDCs without prior approval of the BDC’s board of directors who are not interested persons and, in some cases, prior approval by the SEC. The SEC has interpreted the prohibition on transactions with affiliates to prohibit “joint transactions” among entities that share a common investment adviser.

Certain of our products are permitted to co-invest with other products managed by us as a result of exemptive relief granted by the SEC, so long as such transactions are negotiated in a manner consistent with our BDCs’ investment objectives, positions, policies, strategies and restrictions as well as regulatory requirements and other pertinent factors, provided that certain directors of any of our participating BDCs make certain determinations. Our investment allocation policy incorporates the conditions of the exemptive relief. As a result of the exemptive relief, there could be significant overlap in the investment portfolios of our BDCs and other of our products that could avail themselves of the exemptive relief. Additionally, we have been granted exemptive relief to permit certain of our BDCs to offer multiple classes of shares of common stock and to impose asset-based distribution fees and early withdrawal fees.

Other Regulators; Self-Regulatory Organizations

In addition to the SEC regulatory oversight we are subject to under the Investment Company Act and the Advisers Act, there are a number of other regulatory bodies that have or could potentially have jurisdiction to regulate our business activities.

Blue Owl Securities is registered as a broker-dealer with the SEC, which maintains registrations in many states, and is a member of FINRA. As a broker-dealer, Blue Owl Securities is subject to regulation and oversight by the SEC and state securities regulators. In addition, FINRA, a self-regulatory organization that is subject to oversight by the SEC, promulgates and enforces rules governing the conduct of, and examines the activities of, its member firms. Due to the limited authority granted to Blue Owl Securities in its capacity as a broker-dealer, it is not required to comply with certain regulations covering trade practices among broker-dealers and the use and safekeeping of customers’ funds and securities. As a registered broker-dealer and member of a self-regulatory organization, Blue Owl Securities is, however, subject to the SEC’s uniform net capital rule. Rule 15c3-1 of the Exchange Act, which specifies the minimum level of net capital a broker-dealer must maintain and also requires that a significant part of a broker-dealer’s assets be kept in relatively liquid form.

Blue Owl Capital UK Limited (“Blue Owl UK”) is an entity organized and operating in the United Kingdom whose employees assist in the marketing and distribution of Blue Owl funds in Europe, the Middle East, and Africa. Blue Owl Capital HK Limited (“Blue Owl HK”) is an entity organized and operating in Hong Kong whose employees together with the employees of Blue Owl Capital Singapore Pte. Ltd. (“Blue Owl Singapore”), an entity organized and operating in Singapore assist in the marketing and distribution of Blue Owl funds in the Asia-Pacific region. Blue Owl HK is registered with the Hong Kong Securities & Futures Commission. Blue Owl Capital Canada ULC (“Blue Owl Canada”) is an entity organized and operating in Canada whose employees assist in the marketing and distribution of Blue Owl funds in Canada.

20

Item 1A. Risk Factors.

Risks Related to Our Business and Operations

The COVID-19 pandemic has caused severe disruptions in the U.S. and global economy, has disrupted, and may continue to disrupt, industries in which we, our products and our products’ investments operate and could potentially negatively impact us, our products or our products’ investments.