As filed with the Securities and Exchange Commission on December 15, 2021

Registration No. 333-261363

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_______________________

FORM -1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

_______________________

(Exact Name of Registrant as Specified in Its Charter)

_______________________

| | 85-2515483 | |

| (State or Other Jurisdiction of | (I.R.S. Employer |

35 West 35th Street, Floor 6,

New York, NY 10001

Telephone: (844) 443-6246

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

_______________________

Stan Vashovsky

Chief Executive Officer

35 West 35th Street, Floor 6,

New York, NY 10001

Telephone: (844) 443-6246

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

_______________________

Copies to:

|

George Stamas |

_______________________

Approximate date of commencement of proposed sale to the public:

From time to time after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, please check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 under the Securities Exchange Act of 1934:

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| | ☒ | Smaller reporting company | | |||

| Emerging growth company | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

CALCULATION OF REGISTRATION FEE

|

Title of Each Class of Securities to Be Registered |

Amount to Be |

Proposed |

Proposed |

Amount of |

|||||||||

|

Common Stock, par value $0.0001 per share(2) |

34,551,232 |

$ |

8.10 |

(3) |

$ |

279,864,979.20 |

$ |

25,943.48 |

|

||||

|

Warrants to purchase Common Stock(4) |

2,533,333 |

|

— |

|

|

— |

|

— |

|

||||

|

Total |

|

|

|

$ |

25,943.48 |

(5) |

|||||||

____________

(1) Pursuant to Rule 416 under the Securities Act of 1933, as amended (the “Securities Act”), the registrant is also registering an indeterminate number of additional shares of common stock, par value $0.0001 per share (“Common Stock”), and warrants to purchase Common Stock of DocGo Inc. (formerly known as Motion Acquisition Corp.) that may become issuable as a result of any stock dividend, stock split, recapitalization or other similar transaction.

(2) Consists of the following shares of Common Stock registered for resale by the selling securityholders: (i) 28,234,175 shares of Common Stock, and (ii) 2,533,333 shares of Common Stock issuable upon the exercise of 2,533,333 Private Warrants (as defined below), and (iii) 3,783,724 shares of Common Stock issuable upon the exercise of 3,783,724 Public Warrants (as defined below).

(3) Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(c) under the Securities Act, based upon the average of the high and low selling prices of the Common Stock on November 23, 2021, as reported on the Capital Market of the Nasdaq Stock Market LLC, under the symbol “DCGO.” Prior to November 5, 2021, the trading symbol was “MOTN.”

(4) Consists of 2,533,333 Private Warrants. Pursuant to Rule 457(g) under the Securities Act, no separate registration fee is required for the warrants.

(5) Previously paid.

_______________________

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment that specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. Neither we nor the selling securityholders may sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION — DATED DECEMBER 15, 2021

PRELIMINARY PROSPECTUS

![]()

Up to 28,234,175 Shares of Common Stock

Up to 6,317,057 Shares of Common Stock Issuable Upon Exercise of the Warrants

Up to 2,533,333 Private Warrants

_______________________

This prospectus relates to the offer and sale from time to time by the selling securityholders named in this prospectus of: (i) up to 28,234,175 shares of our Common Stock and (ii) up to 2,533,333 warrants to purchase Common Stock (“Private Warrants”) originally issued in a private placement in connection with the initial public offering of Motion Acquisition Corp. (“Motion”). We will not receive any proceeds from the sale of shares of Common Stock or Warrants (as defined below) by the selling securityholder (the “Selling Securityholders”) pursuant to this prospectus.

In addition, this prospectus relates to the issuance by us of up to an aggregate of 6,317,057 shares of our Common Stock which consists of (i) 2,533,333 shares of Common Stock that are issuable upon the exercise of the 2,533,333 Private Warrants and (ii) 3,783,724 shares of Common Stock that are issuable upon the exercise of those 3,783,724 warrants (“Public Warrants,” together with the Private Warrants, the “Warrants”) to purchase Common Stock, which were issued at the initial public offering of Motion. We will receive the proceeds from any exercise of any Warrants for cash. We will bear the costs, fees and expenses incurred in effecting the registration of the securities covered by this prospectus, including all registration and filing fees, Nasdaq listing fees and fees and expenses of our counsel and our independent registered public accounting firm. The Selling Securityholders will pay any underwriting discounts and commissions and expenses incurred by the Selling Securityholders for brokerage, accounting, tax or legal services or any other expenses incurred by the Selling Securityholders in disposing of the securities.

We are registering the securities for resale pursuant to the Selling Securityholders’ registration rights under certain agreements between us and the Selling Securityholders. Our registration of the securities covered by this prospectus does not mean that either we or the selling securityholders will offer or sell any of the shares of Common Stock or Warrants. The Selling Securityholders or their permitted transferees may offer, sell or distribute all or a portion of their shares of Common Stock or Warrants publicly or through private transactions at prevailing market prices or at negotiated prices. We provide more information about how the Selling Securityholders may sell the Common Stock or Warrants in the section entitled “Plan of Distribution.”

You should read this prospectus and any prospectus supplement or amendment carefully before you invest in our securities.

Our Common Stock and our Public Warrants are listed on the Capital Market of the Nasdaq Stock Market LLC (“Nasdaq”), under the symbols “DCGO” and “DCGOW,” respectively. On December 14, 2021, the closing price of our Common Stock was $8.14 and the closing price for our Public Warrants was $1.96.

_______________________

We are an “emerging growth company” under federal securities laws and are subject to reduced public company reporting requirements.

_______________________

Investing in our securities involves a high degree of risks. See the section entitled “Risk Factors” beginning on page 17 of this prospectus to read about factors you should consider before buying our securities.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2021.

TABLE OF CONTENTS

|

Page |

||

|

i |

||

|

ii |

||

|

iv |

||

|

v |

||

|

vi |

||

|

1 |

||

|

10 |

||

|

11 |

||

|

SUMMARY HISTORICAL FINANCIAL INFORMATION OF MOTION ACQUISITION CORP. |

13 |

|

|

SUMMARY UNAUDITED CONDENSED COMBINED PRO FORMA FINANCIAL INFORMATION |

14 |

|

|

15 |

||

|

17 |

||

|

51 |

||

|

52 |

||

|

UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION |

53 |

|

|

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND |

62 |

|

|

74 |

||

|

94 |

||

|

99 |

||

|

104 |

||

|

106 |

||

|

109 |

||

|

112 |

||

|

121 |

||

|

124 |

||

|

127 |

||

|

132 |

||

|

132 |

||

|

F-1 |

||

|

II-1 |

i

INTRODUCTORY NOTE REGARDING THE BUSINESS COMBINATION

On November 5, 2021 (the “Closing” and such date, the “Closing Date”), Motion Acquisition Corp., a Delaware corporation (“Motion” and, following the Closing, the “Company”), consummated the previously announced business combination pursuant to that certain Merger Agreement, dated March 8, 2021 (the “Merger Agreement”) by and among Motion, Motion Merger Sub Corp., a Delaware corporation and wholly-owned subsidiary of Motion (“Merger Sub”), and Ambulnz, Inc., a Delaware corporation (“Ambulnz”). The Merger Agreement provided for, among other things, the merger of Merger Sub with and into Ambulnz, with Ambulnz surviving the merger as a wholly-owned subsidiary of Motion (the “Business Combination”), with the stockholders of Ambulnz became stockholders of Motion.

Pursuant to the Merger Agreement, at the effective time of the Business Combination (the “Effective Time”), the equityholders of Ambulnz, which consisted of holders of Ambulnz Class A common stock, no par value (“Ambulnz Class A Common Stock”), including the former holders of Ambulnz Series A preferred stock, no par value (“Ambulnz Preferred Stock”), which converted to Ambulnz Class A common stock prior to the Closing, and the holders of Ambulnz Class B common stock, no par value (together with Ambulnz Class A common stock, the “Ambulnz Common Stock”), received aggregate consideration of 83.6 million shares of Motion’s single class of common stock following the Business Combination, par value $0.0001 per share (“Common Stock”), at an exchange ratio equal to dividing 83.6 million by the fully-diluted number of shares of Ambulnz’s Common Stock outstanding immediately prior to the Effective Time. Additionally, the holders Ambulnz Common Stock received, immediately prior to the Closing, the contingent right to receive a pro rata portion of up to an aggregate of 5,000,000 additional shares of Common Stock (the “Contingent Shares”) upon the satisfaction of certain earnout conditions described in Note 4 in the Notes to Unaudited Pro Forma Condensed Combined Financial Information.

Concurrent with the Closing, each option to acquire securities of Ambulnz outstanding immediately prior to the Closing (“Ambulnz Option”) was assumed and converted into an equivalent option to acquire Common Stock of DocGo (“Substitute Option”). Each Substitute Option is exercisable for a number of shares of Common Stock equal to the number of whole shares of Ambulnz Common Stock subject to such Ambulnz Option that were issuable immediately prior to the effective time of the Merger multiplied by 645.1452 (the “Exchange Ratio”), rounded down to the nearest number of whole shares of Common Stock. The per share exercise price for the shares of Common Stock issuable upon exercise of such Substitute Option is equal to the quotient determined by dividing the exercise price per share of Ambulnz Common Stock at which such Ambulnz Option was exercisable immediately prior to the effective time of the Merger by the Exchange Ratio, rounded up to the nearest whole cent.

Concurrent with the Closing, Motion filed its second amended and restated certificate of incorporation with the Delaware Secretary of State, which, among other things, (x) changed the name of Motion to “DocGo Inc.” and (y) redesignated each share of Class A Common Stock of Motion, par value $0.0001 (“Motion Class A Common Stock”), which included all shares of Class B Common Stock of Motion, par value $0.001 (“Motion Class B Common Stock”) which were converted to shares of Motion Class A Common Stock on August 24, 2021, as Common Stock. The transactions set forth in the Merger Agreement, including the Business Combination, constituted a “Business Combination” as contemplated by Motion’s amended and restated certificate of incorporation, dated October 16, 2020. Upon the Closing, in addition to changing its name, Motion changed the trading symbol of the Common Stock on the Capital Market of the Nasdaq Stock Market LLC (“Nasdaq”) from “MOTN” to “DCGO” and the trading symbol of the warrants to purchase Common Stock that were issued in Motion’s initial public offering (the “Initial Public Offering”) with at an exercise price of $11.50 (the “Public Warrants”) from “MOTNW” to “DCGOW”.

Concurrent with the execution of the Merger Agreement, Motion and certain accredited investors (“PIPE Investors”) entered into a series of subscription agreements, dated March 8, 2021 (“PIPE Agreements”) providing for the purchase by the PIPE Investors at the Effective Time of an aggregate of 12,500,000 shares of Common Stock at a price per share of $10.00, for an aggregate purchase price of $125,000,000, on the terms and subject to the conditions set forth therein (collectively, the “PIPE Financing”).

Concurrent with the execution of the Merger Agreement, Motion entered into lock-up agreements, with Ambulnz and certain Ambulnz equityholders (the “New Holders”), pursuant to which the New Holders agreed, subject to certain exceptions, not to transfer or dispose of their Common Stock until (x) the earlier of May 5, 2022 (six (6) months after the Closing Date) and (y) the date after the Closing on which the Company completes a liquidation, merger, capital stock exchange, reorganization or other similar transaction that results in all of its stockholders having the right to exchange their equity for cash, securities or other property. See the section entitled “Securities Eligible for Future Sale — Lock-up and Escrow Agreements.”

ii

Concurrent with the execution of the Merger Agreement, certain parties entered into agreements imposing certain transfer restrictions on their ownership of Motion Class B Common Stock or shares issuable upon the conversion of the Motion Class B Common Stock. Pursuant to the letter agreement entered at the time of the Initial Public Offering, Motion Acquisition LLC, a Delaware limited liability company (“Sponsor”), and Motion’s officers and directors agreed, subject to certain exceptions, not to transfer or dispose of their Common Stock for a specified period of time, as described in the sections entitled “Certain Relationships and Related Person Transactions — Motion — Class B Common Stock” and “Securities Available for Future Sale — Lock-up and Escrow Agreements — Letter Agreement.”

On November 4, 2021, Motion, the Sponsor and Ambulnz entered into that certain Amended and Restated Sponsor Agreement (the “A&R Sponsor Agreement”), whereby the Sponsor agreed to, among other things, forfeit and defer certain shares of Motion Class A Common Stock it held in relation to the number of shares that holders of Motion Class A Common Stock sold in the Initial Public offering sought redemption in connection with the consummation of Business Combination. See the section entitled “Certain Relationships and Related Person Transactions — Motion — A&R Sponsor Agreement.”

Immediately prior to the Closing, Sponsor entered into an escrow agreement (the “Sponsor Escrow Agreement”) with Motion and Continental Stock Transfer & Trust Company, as escrow agent, whereby, immediately following the Closing, the Sponsor deposited (i) 575,000 shares of Common Stock (the “Sponsor Earnout Shares”) into escrow pursuant to the Merger Agreement and (ii) 162,965 shares of Common Stock (the “Additional Earnout Shares”) into escrow pursuant to the A&R Sponsor Agreement. The Sponsor Escrow Agreement provides that such Sponsor Earnout Shares and Additional Earnout Shares will either be released to the Sponsor or surrendered to and canceled by the Company depending on whether certain stock price conditions are met, as described in the section entitled “Securities Available for Future Sale — Lock-up and Escrow Agreements — Sponsor Escrow Agreement.”

Immediately prior to the Closing, Sponsor, Motion and certain equityholders of Ambulnz amended and restated the existing Registration Rights Agreement, by and between Sponsor and Motion, dated October 14, 2020 (“A&R Registration Rights Agreement”). Pursuant to the A&R Registration Rights Agreement, the Company agreed to register for resale under the Securities Act of 1933, as amended (the “Securities Act”), after the lapse or expiration of any transfer restrictions, lock-up, or escrow provisions which may apply, the shares of Common Stock held by Sponsor and shares of Common Stock held by certain equityholders of Ambulnz prior to the Effective Time. Any other stockholders of the Company with piggyback registration rights may also participate in any such registrations, subject to customary cutbacks in an underwritten offering. See the section entitled “Securities Available for Future Sale — Registration Rights.”

This prospectus relates to the offer and sale from time to time by the Selling Securityholders named in this prospectus of the following:

• up to 28,234,175 shares of Common Stock, consisting of: (i) 13,160,962 shares of Common Stock issued to Stan Vashovsky, the Company’s Chief Executive Officer, in connection with the Business Combination, (ii) 2,573,213 shares of Common Stock held by Sponsor, and (iii) 12,500,000 shares of Common Stock issued pursuant to the PIPE Agreements; and

• up to 2,533,333 warrants to purchase Common Stock at a price of $11.50 per share that were issued to Sponsor in a private transaction that closed concurrent with the closing of the Initial Public Offering at (the “Private Warrants” and, together with the Public Warrants, the “Warrants”).

• Simultaneously with the closing of the Initial Public Offering, the Sponsor purchased an aggregate of 2,533,333 Private Warrants at a price of $1.50 per Private Warrant ($3.8 million in the aggregate). Each Private Warrant is exercisable for one share of Common Stock at a price of $11.50 per share, subject to adjustment

In addition, this prospectus relates to the issuance by us of up to an aggregate of 6,317,057 shares of Common Stock issuable upon the exercise of the Warrants offered hereby.

iii

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form S-1 that we filed with the Securities and Exchange Commission (the “SEC”) using a “shelf” registration process. Under this shelf registration process, we and the Selling Securityholders may, from time to time, issue, offer and sell, as applicable, any combination of the securities described in this prospectus in one or more offerings from time to time through any means described in the section entitled “Plan of Distribution.” More specific terms of any securities that the Selling Securityholders offer and sell may be provided in a prospectus supplement that describes, among other things, the specific amounts and prices of the Common Stock and/or Warrants being offered and the terms of the offering.

A prospectus supplement may also add, update or change information included in this prospectus. Any statement contained in this prospectus will be deemed to be modified or superseded for purposes of this prospectus to the extent that a statement contained in such prospectus supplement modifies or supersedes such statement. Any statement so modified will be deemed to constitute a part of this prospectus only as so modified, and any statement so superseded will be deemed not to constitute a part of this prospectus. You should rely only on the information contained in this prospectus, any applicable prospectus supplement or any related free writing prospectus. See “Where You Can Find More Information.”

Neither we nor the Selling Securityholders have authorized anyone to provide any information or to make any representations other than those contained in this prospectus, any accompanying prospectus supplement or any free writing prospectus we have prepared or authorized. We and the Selling Securityholders take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the securities offered hereby and only under circumstances and in jurisdictions where it is lawful to do so. No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus, any applicable prospectus supplement or any related free writing prospectus. This prospectus is not an offer to sell securities, and it is not soliciting an offer to buy securities, in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus or any prospectus supplement is accurate only as of the date on the front of those documents only, regardless of the time of delivery of this prospectus or any applicable prospectus supplement, or any sale of a security. Our business, financial condition, results of operations and prospects may have changed since those dates.

For investors outside the United States: neither we nor the Selling Securityholders have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of our securities and the distribution of this prospectus outside the United States.

This prospectus contains summaries of certain provisions contained in some of the documents described herein, but reference is made to the actual documents for complete information. All of the summaries are qualified in their entirety by the actual documents. Copies of some of the documents referred to herein have been filed, will be filed or will be incorporated by reference as exhibits to the registration statement of which this prospectus is a part, and you may obtain copies of those documents as described below under “Where You Can Find More Information.”

iv

TRADEMARKS, SERVICE MARKS AND TRADE NAMES

This prospectus contains references to trademarks, trade names or service marks of the Company and other entities. Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus are presented without the TM, SM and ® symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our respective rights or the rights of the applicable licensors to these trademarks, service marks and trade names.

v

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended, regarding, among other things, the plans, strategies and prospects, both business and financial of the Company. These statements are based on the beliefs and assumptions of our management. Although the Company believes that its plans, intentions and expectations reflected in or suggested by these forward-looking statements are reasonable, the Company cannot assure you that it will achieve or realize these plans, intentions or expectations. Forward-looking statements are inherently subject to risks, uncertainties and assumptions. Generally, statements that are not historical facts, including statements concerning possible or assumed future actions, business strategies, events or results of operations, are forward-looking statements. These statements may be preceded by, followed by or include the words “believes,” “estimates,” “expects,” “projects,” “forecasts,” “may,” “will,” “should,” “seeks,” “plans,” “scheduled,” “anticipates,” “intends” or similar expressions. Forward-looking statements contained in this prospectus include, but are not limited to, statements about the ability of the Company to:

• access, collect and use personal data about consumers;

• execute its business strategy, including monetization of services provided and expansions in and into existing and new lines of business;

• anticipate the impact of the coronavirus disease 2019 (“COVID-19”) pandemic and its effect on business and financial conditions;

• manage risks associated with operational changes in response to the COVID-19 pandemic;

• recognize the anticipated benefits of and successfully deploy the proceeds from the Business Combination, which may be affected by, among other things, competition, the ability to integrate the combined businesses and the ability of the combined business to grow and manage growth profitably;

• anticipate the uncertainties inherent in the development of new business lines and business strategies;

• retain and hire necessary employees;

• increase brand awareness;

• attract, train and retain effective officers, key employees or directors;

• upgrade and maintain information technology systems;

• acquire and protect intellectual property;

• meet future liquidity requirements and comply with restrictive covenants related to long-term indebtedness;

• effectively respond to general economic and business conditions;

• maintain the listing on, or the delisting of the Company’s securities from, Nasdaq or an inability to have our securities listed on Nasdaq or another national securities exchange;

• obtain additional capital, including use of the debt market;

• enhance future operating and financial results;

• anticipate rapid technological changes;

• comply with laws and regulations applicable to its business, including laws and regulations related to data privacy and insurance operations;

• stay abreast of modified or new laws and regulations applying to its business;

• anticipate the impact of, and response to, new accounting standards;

• respond to fluctuations in foreign currency exchange rates and political unrest and regulatory changes in international markets from various events;

• anticipate the rise in interest rates which would increase the cost of capital;

• anticipate the significance and timing of contractual obligations;

vi

• maintain key strategic relationships with partners and distributors;

• respond to uncertainties associated with product and service development and market acceptance;

• anticipate the ability of the renewable sector to develop to the size or at the rate it expects;

• manage to finance operations on an economically viable basis;

• anticipate the impact of new U.S. federal income tax law, including the impact on deferred tax assets;

• successfully defend litigation;

• comply with privacy and data protection laws, and respond to privacy or data breaches, or the loss of data; and

• successfully deploy the proceeds from the Merger.

Forward-looking statements are not guarantees of performance and speak only as of the date hereof. While DocGo believes that these forward-looking statements are reasonable, there can be no assurance that DocGo will achieve or realize these plans, intentions or expectations. You should understand that the following important factors, in addition to those discussed under the headings “Risk Factors” and elsewhere in this prospectus, could affect the future results of DocGo and could cause those results or other outcomes to differ materially from those expressed or implied in the forward-looking statements in this prospectus:

• litigation, complaints, product liability claims and/or adverse publicity;

• the impact of changes in consumer spending patterns, consumer preferences, local, regional and national economic conditions, crime, weather, demographic trends and employee availability;

• increases and/or decreases in utility and other energy costs, increased costs related to utility or governmental requirements;

• privacy and data protection laws, privacy or data breaches, or the loss of data; and

• the impact of the COVID-19 pandemic and its effect on business and financial conditions of DocGo.

These and other factors that could cause actual results to differ from those implied by the forward-looking statements in this prospectus are more fully described under the heading “Risk Factors” and elsewhere in this prospectus. The risks described under the heading “Risk Factors” are not exhaustive. Other sections of this prospectus describe additional factors that could adversely affect the business, financial condition or results of operations of DocGo. New risk factors emerge from time to time and it is not possible to predict all such risk factors, nor can DocGo assess the impact of all such risk factors on the business of DocGo, or the extent to which any factor or combination of factors may cause actual results to differ materially from those contained in any forward-looking statements. All forward-looking statements attributable to DocGo or persons acting on its behalf are expressly qualified in their entirety by the foregoing cautionary statements. DocGo undertakes no obligations to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

In addition, statements of belief and similar statements reflect the reasonable beliefs and opinions of DocGo. These statements are based upon information available to DocGo as of the date of this prospectus, and while DocGo believes such information forms a reasonable basis for such statements, such information may be limited or incomplete, and statements should not be read to indicate that DocGo has conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain, involve risks and are subject to change based on various factors, including those discussed under the headings “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus.

Market, ranking and industry data used throughout this prospectus, including statements regarding subscriber acquisition costs, attrition and adoption rates, is based on the good faith estimates of DocGo’s management, which in turn are based upon DocGo’s management’s review of internal surveys, independent industry surveys and publications, including reports by third-party research and publicly available information, all of which involve a number of assumptions and limitations. These estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under the headings “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus.

vii

SUMMARY

This summary highlights certain significant aspects of our business and is a summary of information contained elsewhere in this prospectus. This summary is not complete and does not contain all of the information that you should consider before making your investment decision. You should carefully read this entire prospectus, including the information presented under the sections titled “Risk Factors,” “Cautionary Note Regarding Forward-Looking Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Unaudited Pro Forma Condensed Combined Financial Information,” and the consolidated financial statements and the related notes thereto included elsewhere in this prospectus before making an investment decision.

Unless otherwise specified or where the context requires otherwise, references in this prospectus to “we,” “us,” “our” and “the Company” (i) for the periods prior to the Closing, refer to Motion, the special purpose acquisition company, and (ii) for the periods after the Closing, to DocGo Inc., the combined company, and its consolidated subsidiaries. References to and the descriptions of the business included in this prospectus refer, prior to the Closing, to the business Ambulnz, and after the Closing, to the business of DocGo Inc. See “Introductory Note and Selected Definitions.”

Business Summary

Overview

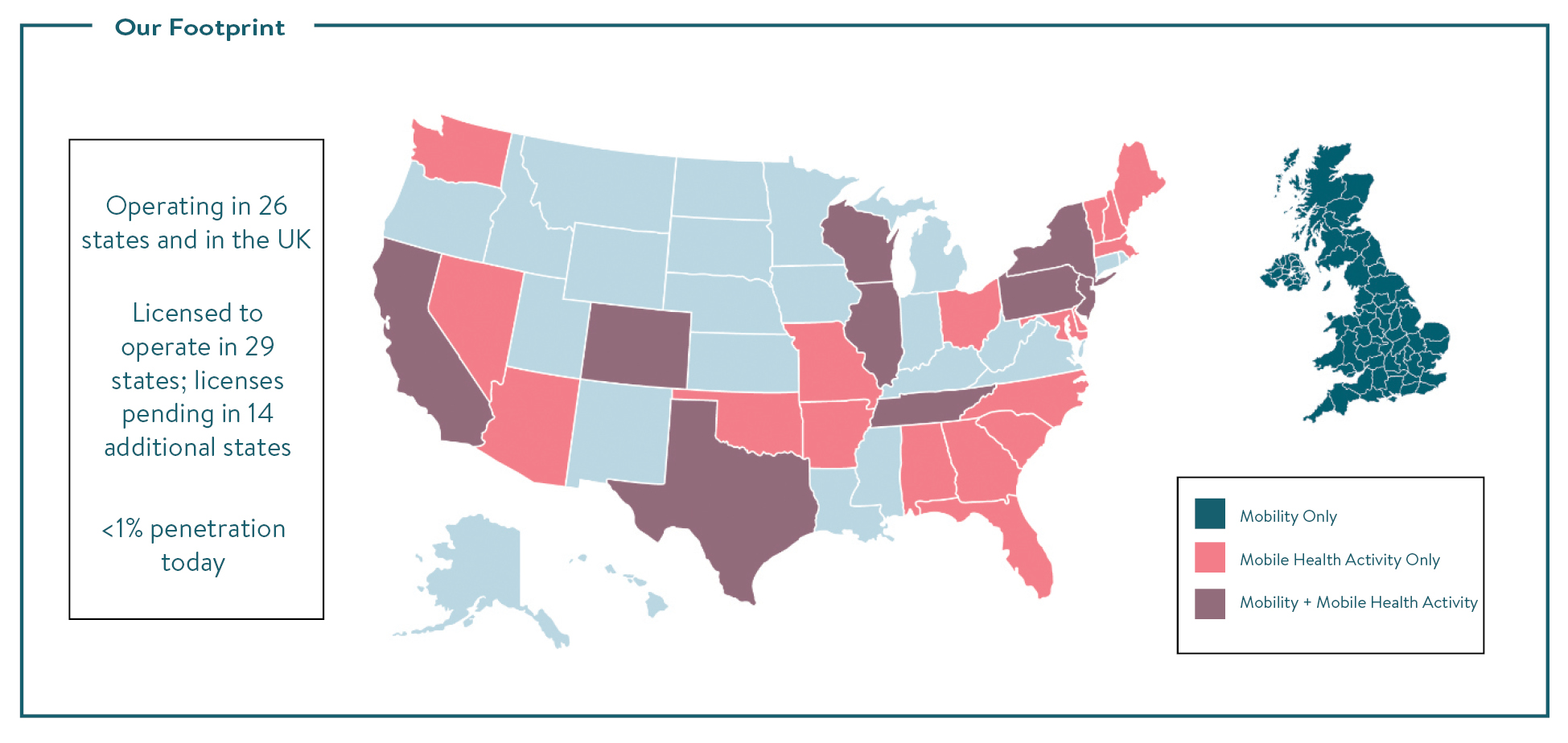

DocGo is redefining on-demand access to healthcare. We deliver high-quality, cost-effective healthcare mobility solutions and are unlocking further promise and potential of telehealth treatment through our “last-mile” care capabilities. We do so by leveraging our proprietary technology platform powered by artificial intelligence (“AI”), and our network of healthcare professionals spanning more than 25 states and the United Kingdom. We often provide our services in collaboration with leading healthcare organizations, via long-term partnerships that drive meaningful recurring revenue, ensure efficient and effective capital allocation, and create low-risk opportunities for significant growth. DocGo, our new corporate name, represents and better communicates who we are as a company and what our solutions offer our customers.

Our mission is to transform medical transportation and telehealth, with more accessible, affordable, and efficient patient-centered care. Since our founding in 2015, through more than 2.2 million patient interactions, we have created an unmatched medical transportation network that can provide better care outside of the physical walls of the healthcare system. We began by developing a state-of-the-art, intuitive platform to drive greater efficiency and improved access to patient care. Our innovative technology can change the way healthcare facilities manage patient transportation, and eliminate many of the common obstacles faced when scheduling service, ultimately freeing medical professionals to focus more time and their valuable resources on what they do best — providing patient care. Additionally, in certain markets, our Mobile Health in-person care model facilitates medical treatment directly to patients in the comfort of their homes, workplaces, and other non-traditional locations. Working under the guidance of prescribing physicians, our network of over 1,900 medical professionals, including Emergency Medical Technicians (“EMTs”), paramedics, nurses and support staff, provides a wide range of tests, procedures and interventions that, until now, required a visit to a traditional healthcare setting.

Our Strengths

We believe we have a number of competitive advantages that enable us to consolidate and build on our position as a leader in medical mobility and telehealth solutions, including the following:

A robust, industry-leading AI-powered technology suite

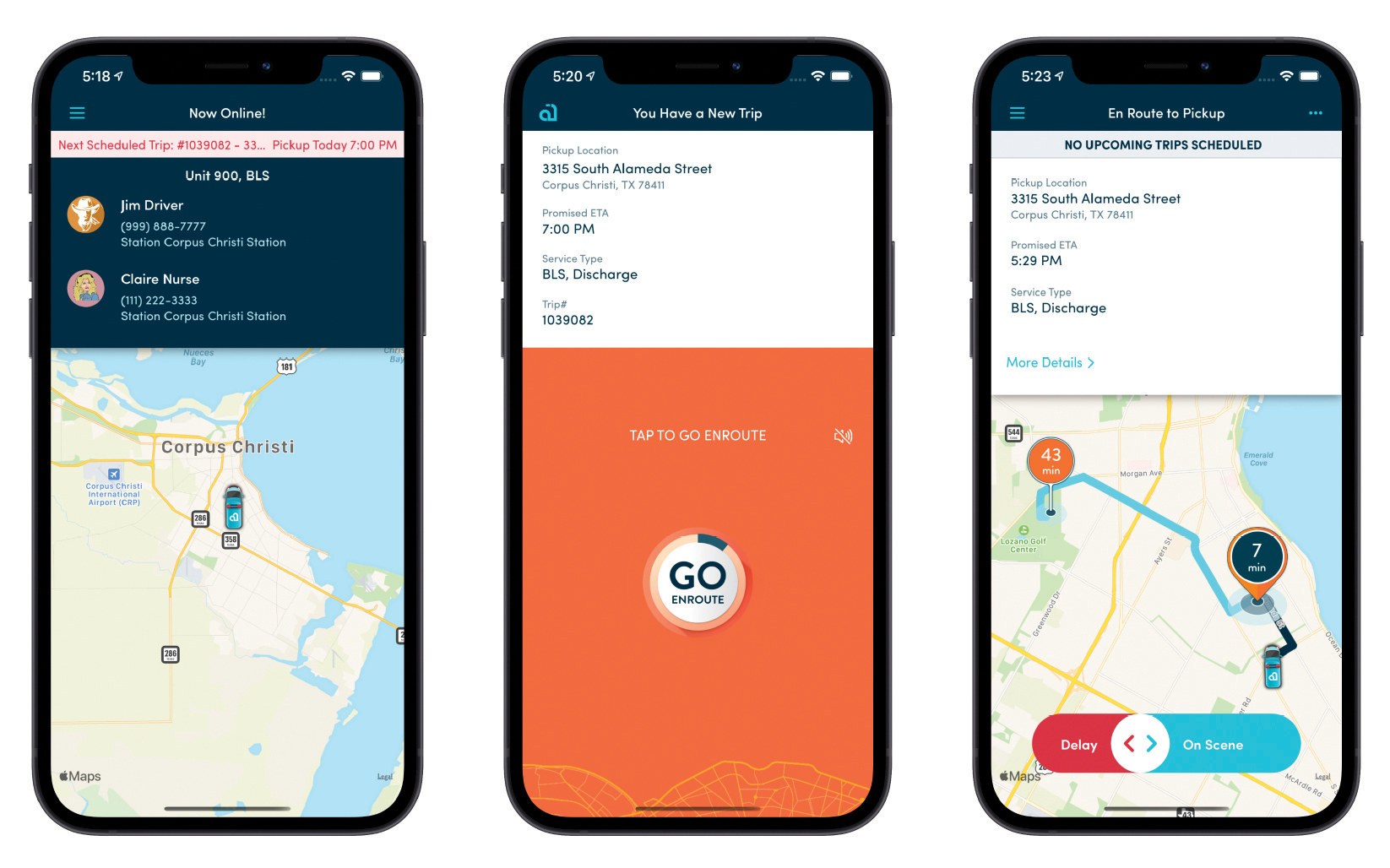

DocGo developed what we believe to be the industry’s first fully integrated medical transportation and mobile healthcare platform. Our platform is designed to track various distributed resources and intelligently predict the best means for mobile healthcare service and delivery of care.

The DocGo platform uses AI and machine learning to predict and optimize every aspect of the lifecycle of our solutions. This includes leveraging AI to dispatch the appropriate vehicles and staff based on medical necessity, routing our vehicles through dynamic traffic patterns, and even predicting the time it will take our team to reach a specific hospital facility, to timely deliver patients for time-sensitive medical appointments. Further, the system helps determine the financial feasibility of each trip, to better assist with final insurance adjudication.

1

How We Help Health Networks

To allow for fast, accurate ordering of Mobile Health and medical mobility services, DocGo’s platform integrates with major EMR systems, which allows seamless interoperability for accessing patient demographics and insurance information. Additionally, hospital systems get real-time analytics into every transport’s estimated arrival and departure times, helping them intelligently predict bed-management, measure interdepartmental performance, and ultimately provide a smoother patient experience.

How We Optimize Our Workforce

DocGo’s platform is founded on service utilization and accuracy. As part of an intelligent learning system, our platform continually verifies and monitors all modes of transport available to our customers and partners. Each level of service is distinctly identified, based on local and state regulations, to provide a specific mode of health transport. The location, status, availability, and equipment on each mode of transport are tracked in real-time. This combined intelligence is at the heart of how our platform automatically provides the best, most accurate modes of transportation and facilitation of Mobile Health medical care.

This level of control can substantially increase profitability, which results in increased earning potential for employees, a highly motivated workforce, and a better patient experience.

How We Help Patients

To better service both our patients and health network partners, DocGo creates detailed digital mapping of all facilities we service. From bedside to bedside, our platform intelligently understands and predicts the time from curbside to lobby, the time to reach a particular department within a facility, and the delays within particular hospital departments. This level of intelligence provides a much higher level of accuracy and transparency to our patients. Our customer facing ShareLinkTM notifies patients, loved ones, and hospital staff of the real-time locations of our vehicles, keeping them informed each step of the way.

To ensure that our technology stays on the cutting edge, DocGo employs a large team of highly skilled engineers and computer scientists headquartered in New York City, San Francisco, and Tallinn, Estonia. This team includes software engineers, data engineers, cybersecurity engineers, DevOps engineers and system architects.

DocGo’s Product Development utilizes in-process research & development to continually keep up with rapid business growth and adapt to service expansion. To ensure the utmost quality and reduce time to market, DocGo uses established best practices to build, test, and release software. Our development life cycle follows a proven and standard software development lifecycle (SDLC) which allows for product research, specifications, development, acceptance testing, and ultimately deployment.

With a focus on rapid iterative deployment cycles, our engineering teams leverage test-driven development (TDD) and behavior-driven development (BDD), to author unit tests and lean heavily on automated testing in integration environments. With our mature, proven deployment pipeline, releases are shipped to production several times a business day, benefiting DocGo’s employees, patients, and customers.

DocGo’s technology infrastructure is built using a distributed and scalable architecture. All production infrastructure at DocGo is deployed on Amazon Web Services (AWS). Data is transmitted in encrypted form and encrypted at rest in our system. Autoscaling is leveraged to ensure capacity on-demand, to provide a low latency and an effective user experience. Logs and metrics are streamed to CloudWatch for visibility, traceability, and alerting.

Our National Operations Center — based on Tuscaloosa, Alabama — provides human monitoring to help ensure that we address issues as they arise and provide 24/7 service delivery.

An industry-leading technology suite with deep clinical integration

Efficient, high-quality transportation is vital to move and discharge patients within a healthcare system; even short delays or downtime can be extremely costly to providers and frustrating for patients. To create more efficient systems and improve the patient experience, our technology platform is fully integrated with some of the nation’s largest

2

EMR systems. This class-differentiating connectivity allows our healthcare provider partners to efficiently monitor and manage their operations, including patient flow, triage times, staffing and specialty services. For example, hospital staff traditionally request transportation by phone and must often place repeated follow-up calls to inquire about vehicle arrival, reducing valuable time that can be spent preparing for the patient’s arrival and focusing on patient care. Once a patient is picked up, there is typically no way to track the patient’s location until the vehicle arrives at its destination. In contrast, DocGo’s proprietary system enables transportation requests with a few simple clicks of a mouse from any Internet-enabled device. We believe that our unique algorithms ensure intelligent fleet routing and peak vehicle utilization, along with accurate estimates of arrival times and wait times, which result in our industry-leading on time compliance. Our EMR integrations further simplify the process, pulling accurate patient information directly from the hospital’s EMR system. Using our hospital partners’ EMR saves time, by avoiding needing to take a patient’s medical history, eliminating illegible handwriting and ensuring data accuracy, which is critical when dealing with health records. Our ShareLinkTM technology gives healthcare providers and patients real-time information regarding vehicle location and added peace of mind, all in a user-friendly interface similar to popular ride-sharing applications.

By dramatically increasing healthcare transportation efficiency, transparency and predictability, our technology empowers our partners to maximize patient resource utilization, improve their bottom lines, and enhance the overall experience for their staff and patients alike. Additionally, our proprietary technology enables us to better deploy and utilize our fleet and medical professionals, reducing our downtime and ultimately improving margins.

Progressive partnership model that drives significant benefits for us and our healthcare provider partners

A primary goal in our rethinking medical transportation was to fundamentally change the relationship between healthcare providers and transportation companies. Rather than being a mere vendor, we collaborate with a number of our key healthcare provider customers through a unique, long-term partnership model, whereby we share the economics of the relationship and work collaboratively to grow our enterprise to mutual benefit. This structure facilitates a more consistent level of service to the provider and its patients, improving the quality of patient care. We use this model with some of the largest U.S. healthcare providers, including Fresenius Medical Care, UCHealth, and Jefferson Health.

We gain substantial economic benefits from our innovative model. Our partnerships provide us with a recurring, predictable transportation revenue stream within the geographic markets where our partner operates. The partnership also makes us a preferred provider, so that we capture a greater share of revenue that would otherwise be contracted out to other transportation providers. This deep-rooted relationship creates cross-selling opportunities to drive additional revenues through our Mobile Health solutions as well.

The partner also acts as an “anchor” customer in its geographic market(s), meaning we can use resources deployed for this relationship to acquire new business from additional customers, at a lower incremental cost and with less risk to our investment. Our partners benefit not only from the economic efficiency of our superior technology, but also from reduced costs and new revenue sources as the partnerships grow. Our differentiated approach effectively converts medical transportation from a cost to an economic opportunity for our partners.

Our largest partner, Fresenius Medical Care, one of the world’s largest dialysis treatment providers, demonstrates how our model benefits both parties. Fresenius’ patients with end-stage renal disease undergo dialysis treatments up to three times per week and often require medical transportation to and from their appointments. In partnering with DocGo, Fresenius uses our platform to efficiently schedule and monitor patient transports, helping maximize patient flow-through and treatment compliance while minimizing the administrative burden of managing these transportation services. The partnership generates reliable, recurring revenue for us and creates pathways to larger medical transportation opportunities in the markets where Fresenius operates.

3

Well-dispersed national and international scale, poised for continued growth

Our nationwide footprint and burgeoning international presence in the United Kingdom demonstrate success in building our network, and create opportunities to use this infrastructure to support further growth in existing markets and new geographies. We currently maintain an organization of more than 1,900 medical professionals, including EMTs, paramedics, nurses and support staff, and a fleet of more than 340 technology-equipped vehicles that have provided services across more than 25 states and throughout England.

Given our innovative partnership business model, and that our solutions are easily leveraged to serve significantly higher volumes, we can rapidly scale with our existing partners, add new clients in existing markets, and grow into new ones, without the need to invest and risk significant additional capital.

Differentiated brand identity focused on enhancing the patient’s experience

The medical transportation industry is intimidating to most consumers. While it addresses a patient’s most basic and immediate healthcare needs, it was not designed with the patient’s experience in mind. DocGo created a transportation solution based on a completely different proposition — to create an improved experience for all stakeholders, including the patient. Our ShareLinkTM technology provides radical transparency, improving the patient experience and easing concerns by showing the precise ETAs and real-time locations of our vehicles. Our employees undergo customer service training to ensure that they deliver care with the customer experience in mind. Our calming light blue brand identity, and less-formal uniforms for our healthcare professionals, create a more comfortable experience for our patient customers and those of our healthcare provider partners. We believe this carefully crafted brand experience helps alleviate concern during an inherently traumatic, uncertain time for patients.

Our healthcare professionals’ utilization of state-of-the-art logistics and other technologies further reinforces our differentiated brand proposition. Our DocGo brand was built in a similar fashion, to help convey the humanity and empathy we strive to deliver with each and every patient interaction.

Founder-led, highly experienced management team

Our founder and management team members have on average over 25 years of industry and other relevant professional experience. Our management team is comprised of industry veterans who have held leadership roles at some of the largest public and private healthcare and consumer businesses, ranging from start-ups to Fortune 500 companies, with pertinent healthcare, technology and mobility expertise. We believe this collective experience and first-hand knowledge of the challenges inherent in today’s healthcare system provide our company with the foundation to pursue its mission to transform the medical mobility and telehealth industries while navigating a rapidly evolving

4

landscape. Our key executives also have extensive experience in growing businesses, both organically and through acquisitions, supporting all aspects of our growth strategy. Our leadership team’s top quality and talent will help us create and capitalize on the opportunities we see ahead.

Our Growth Strategies

Growth Strategies

Identify new partners and expand into new markets

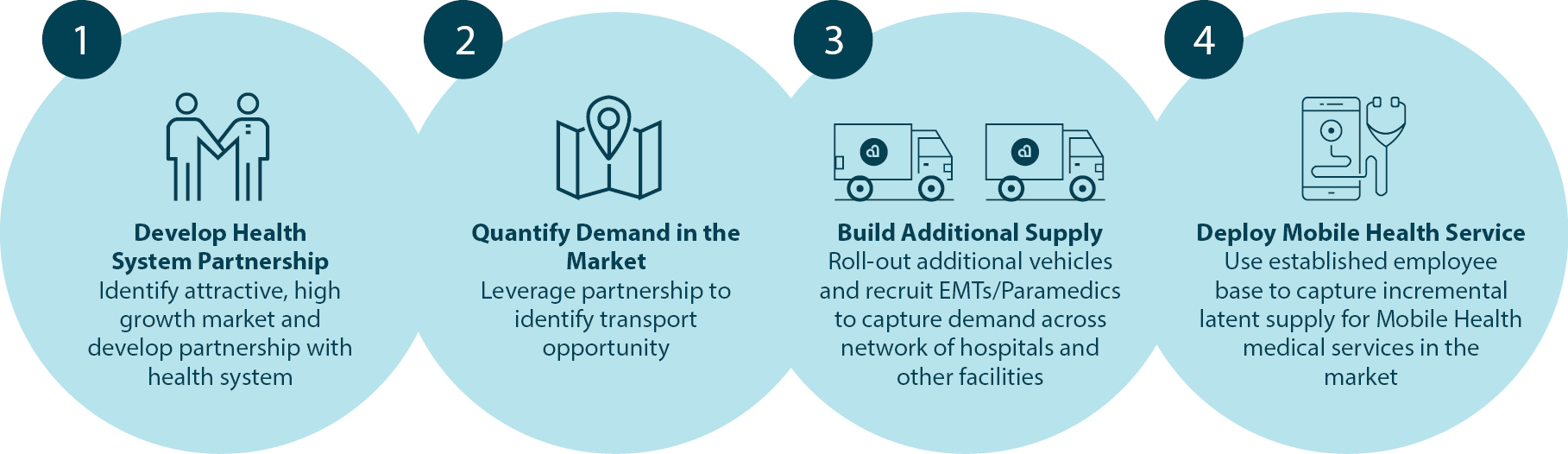

Partnerships are integral to our growth strategy, providing predictable revenue and visibility into market volume and data, and helping us rapidly scale to service demand. These relationships also allow us to grow with our partners as they expand into additional geographies. Further, our partnership model provides a foundational customer, from which we can expand our customer base within that market, and, in certain instances, growth into neighboring markets, in each case more fully utilizing our assets with increased predictability and risk management.

In identifying new geographic market opportunities, we initially look to establish a relationship with a large player in the local healthcare system, that can serve as the “anchor” customer for our Transportation Services. Once we enter into an agreement with the healthcare provider, we deploy a fleet of vehicles equipped with our proprietary technology with the staff needed to support the customer’s transportation needs. With this core infrastructure in place, our medical professionals transport patients to and from our customer’s care facilities and additional locations, and are positioned to capture additional transportation opportunities in the region. Capitalizing on these existing resources and using our innovative technology, we use our fleet and medical professionals to provide additional “last-mile” Mobile Health services, maximizing the utilization rate and revenue potential of our assets.

We believe we have significant opportunity to expand throughout the United States, and selectively in international markets, by identifying and establishing new partnerships. While we always consider new geographies and actively engage with other prospective partners, we have prioritized key markets based on specific characteristics and have filed for licenses in certain geographic areas where we do not currently operate. We are also expanding our partnership model beyond the traditional healthcare system, partnering with companies like RXR Realty, a leading New York City real estate owner, manager and developer. Together we facilitate Mobile Health services for RXR’s employees and tenants with on-site testing, monitoring, and reporting at locations across New York and New Jersey. We consider establishing similar partnerships as a significant opportunity to grow our telehealth revenues.

Broaden our suite of “last-mile” Mobile Health offerings and expand into additional markets to grow revenues

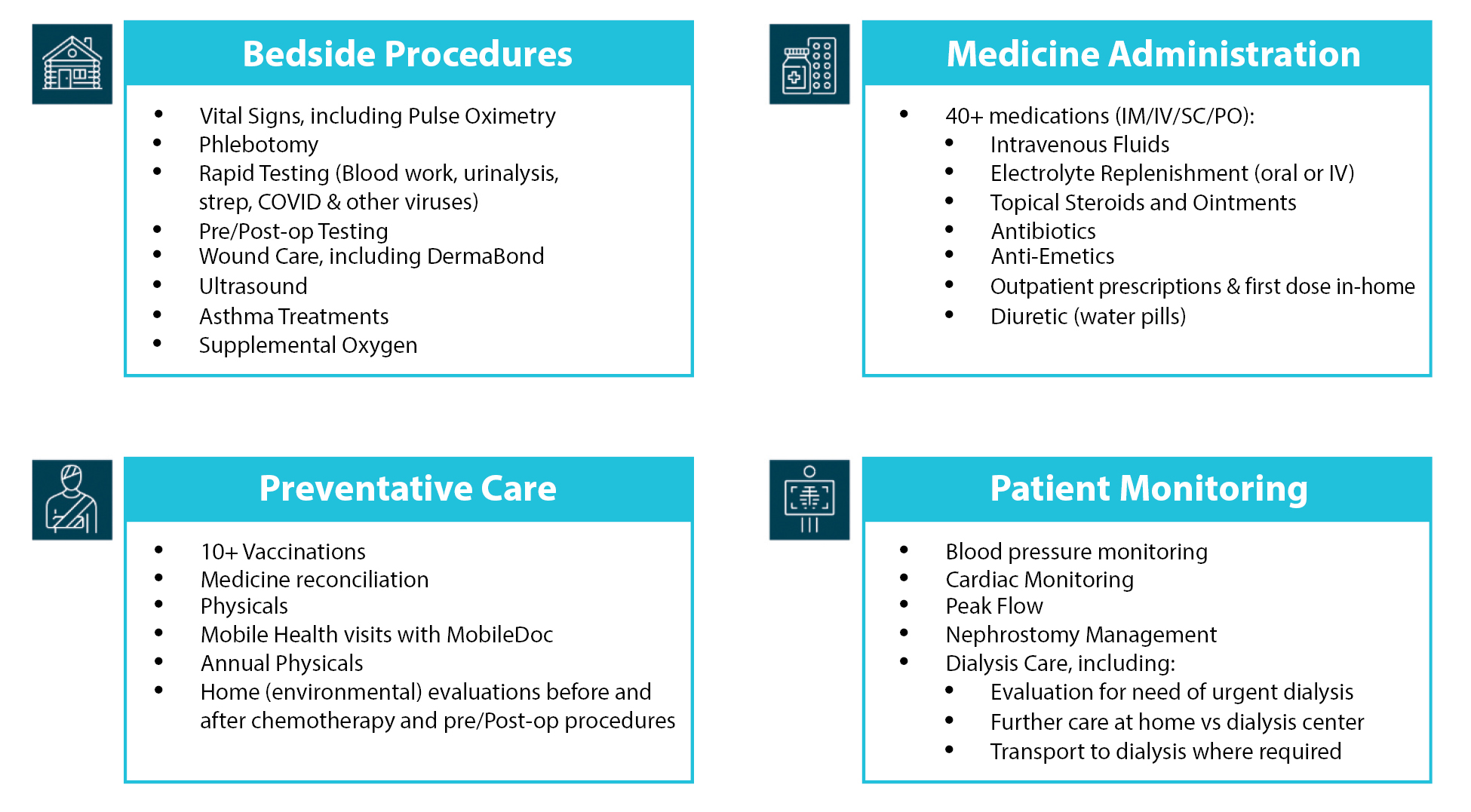

Our Mobile Health solutions offer a significant value proposition. We facilitate the “last-mile” of telehealth services to patients, supplementing virtual consultations with a suite of in-person tests, procedures and interventions that do not require the specifications of a traditional healthcare setting. This model provides greater convenience to patients, and improves our financial results, by increasing the utilization rate of our fleet and medical professionals, limiting downtime between transports, thereby increasing revenues and margins. Providing non-emergency care to patients in their homes also reduces burdens on the healthcare system, freeing up time, space and other resources in hospitals, urgent care clinics, physicians’ offices, and labs.

5

A patient symptomatic of strep throat serves as one example of how our solutions operate and benefit all stakeholders in the healthcare industry. Under the traditional telehealth model, it can take as long as two days for our suffering patient to virtually consult with a doctor, be referred to a clinic for testing, and for the physician to receive the test results; and that is all before any diagnosis or treatment can even begin. With our “last-mile” Mobile Health solution, a DocGo paramedic arrives at the patient’s home, virtually consults with a physician, tests the patient, and performs the necessary lab work on-site, resulting in the physician’s diagnosis in as little as 20 minutes. Our paramedic can even administer the first dose of antibiotics at the doctor’s instruction. Another example is at-home treatment for oncology patients. Instead of sending these immunocompromised individuals to a hospital setting, our clinicians can visit them in their homes to provide infusions. In addition to increasing patient comfort at a time of acute distress, it also greatly reduces their potential of exposure to harmful elements, and frees up resources at the healthcare facility.

We have expanded from basic testing services to include a suite of more than 25 medical tests, procedures and interventions and we intend to continue adding new services, leveraging our existing geographic footprint and extensive nationwide network of healthcare professionals. One example is Rapid Reliable Testing (“RRT”), which we launched in April 2020 in response to the COVID-19 pandemic. Established in less than two months, RRT now offers COVID-19 and IgG antibody testing to healthcare providers and other customers in New York, New Jersey, Pennsylvania, Florida, California, Texas, Tennessee, and Colorado. We partner with approximately 300 government entities, nursing homes, schools, and businesses nationwide, to provide this service onsite, at drive-thru locations, and via a fleet of mobile testing units. While some of these relationships began as testing-only contracts, we have successfully expanded to include COVID-19 vaccines and additional Mobile Health solutions, and we expect to continue expanding these relationships in the future.

At the start of 2020, we had a growing business providing telehealth services at sporting events and concerts, that was placed on pause due to COVID-19-era social distancing restrictions. With the resumption of in-person events, this burgeoning solution provides additional opportunities for expansion. We have secured contracts to provide first aid and on-site medical care at premier New York City sports venues, including Citi Field and the Barclays Center, and have since expanded those relationships to provide Mobile Health solutions as well.

We intend to expand the number of markets in which we offer our solutions. In the short time that we have offered our Mobile Health services, we have expanded our reach from select markets to offerings across 42 U.S. states.

Grow with existing customers into new geographies and further penetrate existing markets

We see significant opportunity to increase our share of our current healthcare provider customers’ business by expanding into new geographies as they grow and further penetrating markets where we currently work together. We believe that our offerings are superior to those of our competitors, and once a customer experiences the benefits of our platform and technology, our win rate with that customer will increase. Our solutions are easily scalable to serve meaningfully higher volumes, and can seamlessly accommodate the addition of Mobile Health products and services. Additionally, our partnership model is conducive to significant business growth, because these well-established relationships provide an immediate source of predictable revenue in the new market. With existing partners, we also have greater visibility into market dynamics, allowing us to better identify which markets will likely be profitable and when. Our partnership with Fresenius Medical Care, which provides kidney dialysis treatment in markets across the United States, serves as a case in point; our close working relationship allows us to map demand curves to population densities, and accordingly, make informed decisions about expansion. Finally, a partner provides us with a foundation to further expand within a given market, using existing resources to acquire new customers and to service them at a lower incremental cost, with limited capital risk.

Fully utilize lower-cost, high-value professionals to drive additional revenues and increase margins

There is a significant cost disparity among healthcare professionals. We specifically utilize paramedics and EMTs as they are generally billed at lower rates than physicians and nurses. This cost difference allows us to deliver our “last-mile” Mobile Health solutions at a lower cost than the same care via a traditional healthcare system visit. Further, unlike many healthcare professionals, paramedics and EMTs are specifically trained to work outside of clinic and hospital settings, making them a perfect fit for administering tests, procedures and interventions in a patient’s home or workplace. Furthermore, traditional medical transportation companies can fill several orders throughout the day, but the wait in between transports is lost as downtime. While our proprietary technology enables us to

6

minimize this downtime, we took remaining downtime as an opportunity for our EMTs and paramedics to provide our “last-mile” Mobile Health services, maximizing utilization rates and the revenue potential of our vehicles and professional workforce.

Opportunistically acquire businesses that fit our existing business model

In recent years, we expanded our geographic presence by strategically acquiring local provider licenses in markets that we intended to enter. Such acquisitions provided us with the requisite licenses, as well as additional infrastructure — including vehicle fleet and employee base — to operate in a local market. We occasionally acquire a business to have the necessary infrastructure to support a partnership, but acquisitions can also contribute to existing customer relationships and revenue streams. Following an acquisition, we add value to that business by integrating it with our proprietary technology platform, rebranding the fleet and retraining the staff to deliver our customer-centered, cost-effective mobility and Mobile Health services. We constantly evaluate additional acquisition opportunities and anticipate that we will continue to make acquisitions in select markets, to support our growth plans. We expect acquisitions to be the primary means of acquiring the licenses or other resources necessary to enter new markets in the future. Additionally, we may acquire new technological capabilities or telehealth solutions to supplement our existing offerings.

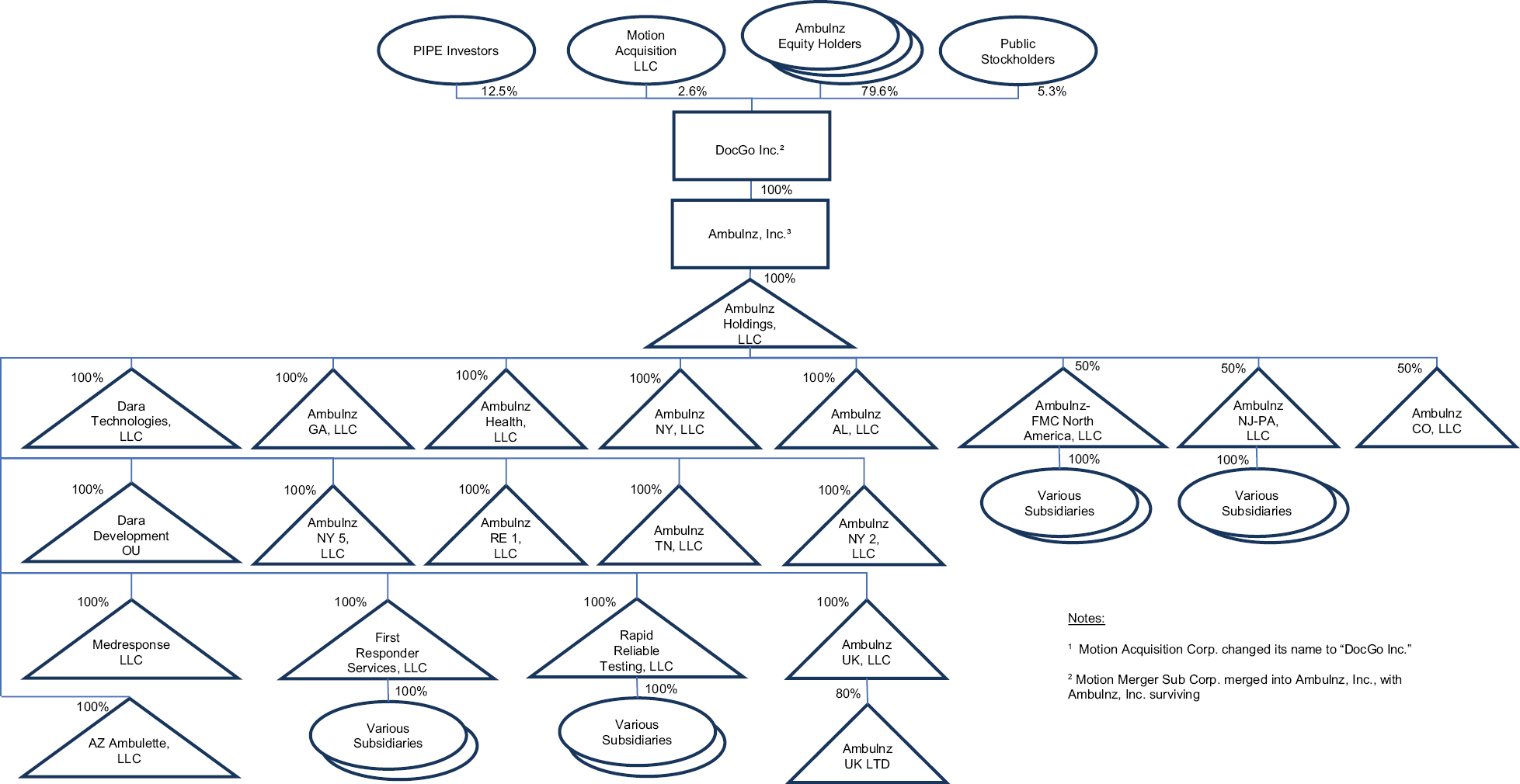

Organizational Structure

The diagram below depicts a simplified version of our equity ownership (excluding ownership interests upon the exercise of Warrants and Substitute Options) and organizational structure immediately following the Business Combination.

Implications of Being an Emerging Growth Company and a Smaller Reporting Company

We are an “emerging growth company,” as defined in Section 2(a) of the Securities Act of 1933, as amended (the “Securities Act”), as modified by the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). As such, we are eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”), reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a non-binding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. If some investors find our securities less attractive as a result, there may be a less active trading market for our securities and the prices of our securities may be more volatile.

7

In addition, Section 107 of the JOBS Act also provides that an “emerging growth company” can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an “emerging growth company” can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We have elected to take advantage of the benefits of this extended transition period.

We will remain an emerging growth company until the earlier of (1) the last day of the fiscal year (a) following the fifth anniversary of the completion of our Initial Public Offering, (b) in which we have total annual gross revenue of at least $1.07 billion, or (c) in which we are deemed to be a large accelerated filer, which means the market value of our Common Stock that are held by non-affiliates exceeds $700 million as of the prior June 30, and (2) the date on which we have issued more than $1.0 billion in non-convertible debt securities during the prior three-year period. References herein to “emerging growth company” have the meaning associated with it in the JOBS Act.

Additionally, we are a “smaller reporting company” as defined in Item 10(f)(1) of Regulation S-K. Smaller reporting companies may take advantage of certain reduced disclosure obligations, including, among other things, providing only two years of audited financial statements. We will remain a smaller reporting company until the last day of the fiscal year in which (1) the market value of our Common Stock held by non-affiliates exceeds $250 million as of the prior June 30, or (2) our annual revenues exceeded $100 million during such completed fiscal year and the market value of our Common Stock held by non-affiliates exceeds $700 million as of the prior June 30.

Summary of Risk Factors

Investing in our securities involves risks. Before you make a decision to buy our securities, in addition to the risks and uncertainties discussed below you should carefully consider the specific risks and other information set forth in this prospectus, including “Cautionary Note Regarding Forward-Looking Statements,” “Unaudited Pro Forma Condensed Combined Financial Information,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and the related notes thereto included elsewhere in this prospectus. This summary of material risks should be read in conjunction with the “Risk Factors” section below and should not be relied upon as an exhaustive summary of the material risks facing our business. The occurrence of one or more of the events or circumstances described in the section titled “Risk Factors,” alone or in combination with other events or circumstances, may materially adversely affect our business, financial condition and operating results. Such material risks include, but are not limited to:

Risk Relating to the Ownership of DocGo Securities

• Future sales, or the perception of future sales, by DocGo or its stockholders in the public market could cause the market price for Common Stock to decline.

• Nasdaq may delist DocGo’s securities from trading on its exchange, which could limit investors’ ability to make transactions in its securities and subject DocGo to additional trading restrictions.

• Warrants will become exercisable for Common Stock, which would increase the number of shares eligible for future resale in the public market and result in dilution to our stockholders.

• The Warrants may never be in the money, and they may expire worthless and the terms of the Warrants may be amended in a manner adverse to a holder if holders of at least 50% of the then-outstanding Warrants approve of such amendment.

• The market price and trading volume of Common Stock and Warrants may be volatile.

• If securities or industry analysts do not publish research, publish inaccurate or unfavorable research or cease publishing research about DocGo, its share and Warrant price and trading volume could decline significantly.

Risks Related to DocGo’s Business and Industry

• The COVID-19 pandemic has materially impacted DocGo’s business.

• DocGo’s limited operating history may make it difficult to evaluate its business, which may be unsuccessful.

8

• DocGo has a history of losses, expects its operating expenses to increase significantly in the foreseeable future and may not achieve or sustain profitability.

• If DocGo is unable to effectively manage its growth, its financial performance and future prospects will be adversely affected.

• DocGo incurs significant up-front costs in its client relationships and any inability to maintain and grow these client relationships over time or to recover these costs could adversely affect its business.

• DocGo’s labor costs are significant and any inability to control those costs could adversely affect its business.

• DocGo’s reliance on its contractual relationships with its healthcare provider partners and other strategic alliances could adversely affect its business.

• DocGo’s reliance on government contracts could adversely affect its business.

• A significant portion of our recent revenue growth is derived from a small number of large customers.

• DocGo’s business depends on numerous complex information systems and any failure to successfully maintain these systems could adversely affect its business.

• DocGo’s platform is highly technical and its failure to operate effectively could adversely affect DocGo’s business.

• DocGo is required to comply with laws governing the transmission, security and privacy of health information.

• Security breaches, loss of data and other disruptions could compromise sensitive business, customer or patient information or prevent DocGo from accessing critical information and expose it to liability, which could adversely affect DocGo’s business.

• If DocGo is unable to successfully develop new offerings and technologies or adapt to rapidly changing technology and industry standards or changes to regulatory requirements, DocGo’s business could be adversely affected.

• DocGo is subject to a variety of federal, state and local laws and regulatory regimes, including a variety of labor laws and regulations, and changes to or the failure to comply with these laws and regulations could adversely affect DocGo’s business.

• There is a potential for litigation or other disputes may arise from the restatement of Motion’s previously issued financial statements and material weakness in its internal controls over financial reporting and the preparation of its financial statements.

Corporate Information

We were incorporated on August 11, 2020 as a Delaware corporation. Upon the Closing, we changed our name to DocGo Inc. Our principal executive office is located at 35 West 35th Street, Floor 6, New York, NY 10001, and our telephone number is (844) 443-6246. Our website address is www.docgo.com. The information contained in or accessible from our website is not incorporated into this prospectus, and you should not consider it part of this prospectus. We have included our website address in this prospectus solely as an inactive textual reference.

9

THE OFFERING

|

Issuer |

DocGo Inc. |

|

|

Shares of Common Stock offered by us |

Up to 6,317,057 shares of Common Stock issuable upon exercise of the Warrants. |

|

|

Shares of Common Stock offered by the Selling Securityholders |

Up to 28,234,175 shares of Common Stock. |

|

|

Warrants Offered by the Selling Securityholders |

Up to 2,533,333 Private Warrants. |

|

|

Exercise Price of Warrants |

$11.50 per share, subject to adjustment as described herein. |

|

|

Shares of Common Stock outstanding assuming no exercise of any Warrants |

100,069,438 shares of Common Stock (as of November 23, 2021). |

|

|

Shares of Common Stock outstanding assuming exercise of all Warrants |

106,386,495 (based on total shares outstanding as of November 23, 2021). |

|

|

Use of Proceeds |

We will not receive any proceeds from the sale of shares of Common Stock or Warrants by the Selling Securityholders. We will receive up to an aggregate of approximately $72.65 million from the exercise of the Warrants, assuming the exercise in full of all of the Warrants for cash. We expect to use the net proceeds from the exercise of the Warrants for general corporate purposes. See “Use of Proceeds.” |

|

|

Redemption |

The Warrants are redeemable in certain circumstances. See “Description of Securities — Warrants” for further discussion. |

|

|

Business Combination — Related Lock-Up Agreements |

Certain of our securityholders, including certain of the Selling Securityholders, are subject to certain restrictions on transfer until the termination of applicable lock-up periods. See “Securities Eligible for Future Sale — Lock-up and Escrow Agreements.” for further discussion. |

|

|

Market for Common Stock and Warrants |

Our Common Stock and Public Warrants are currently traded on the Nasdaq under the symbols “DCGO” and “DCGOW,” respectively. |

|

|

Risk Factors |

See “Risk Factors” beginning on page 17 and other information included in this prospectus for a discussion of factors you should consider before investing in our securities. |

10

SUMMARY HISTORICAL FINANCIAL INFORMATION OF AMBULNZ, INC.

The following table sets forth selected historical financial information derived from Ambulnz’s (i) audited consolidated statements of operations and comprehensive loss for the years ended December 31, 2020 and 2019, (ii) audited consolidated balance sheets data as of December 31, 2020 and 2019, (iii) unaudited condensed consolidated statements of operations and comprehensive income (loss) for the three months and nine months ended September 30, 2021, and (iv) condensed consolidated balance sheets data as of September 30, 2021 (unaudited) and December 31, 2020, each of which is included elsewhere in this prospectus.

The summary historical information of Ambulnz included below and elsewhere in this prospectus is not necessarily indicative of the future performance of DocGo. Results from interim periods are not necessarily indicative of results that may be expected for the entire year. You should read the following summary financial information in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the financial statements and the related notes appearing elsewhere in this prospectus.

Consolidated Statement of Operations Data:

|

(Unaudited) |

(Unaudited) |

For the Year Ended |

|||||||||||||||||||

|

$ in Millions, except per share data |

2021 |

2020 |

2021 |

2020 |

2020 |

2019 |

|||||||||||||||

|

Revenues, net |

$ |

85.8 |

|

26.9 |

|

197.4 |

|

62.9 |

|

$ |

94.10 |

|

$ |

48.30 |

|

||||||

|

Cost of revenue |

|

60.0 |

|

18.3 |

|

137.1 |

|

42.0 |

|

|

62.7 |

|

|

35.1 |

|

||||||

|

Total expenses |

|

84.3 |

|

29.5 |

|

197.5 |

|

73.2 |

|

|

108.8 |

|

|

69.1 |

|

||||||

|

Income (loss) from operations |

|

1.5 |

|

(2.6 |

) |

(0.1 |

) |

(10.3 |

) |

|

(14.7 |

) |

|

(20.8 |

) |

||||||

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

Other expenses |

|

|

|

|

|

|

|

|

|

||||||||||||

|

Interest income |

|

(0.3 |

) |

(0.1 |

) |

(0.5 |

) |

(0.1 |

) |

|

(0.2 |

) |

|

(0.5 |

) |

||||||

|

Other income |

|

— |

|

— |

|

— |

|

— |

|

|

0.4 |

|

|

0.1 |

|

||||||

|

Total other income (expense) |

|

(0.1 |

) |

(0.1 |

) |

(0.4 |

) |

(0.1 |

) |

|

0.2 |

|

|

(0.4 |

) |

||||||

|

Net income (loss) before income tax benefit (expense) |

|

1.4 |

|

(2.7 |

) |

(0.5 |

) |

(10.4 |

) |

|

(14.6 |

) |

|

(21.2 |

) |

||||||

|

Income tax (expense) benefit |

|

(0.6 |

) |

— |

|

(0.6 |

) |

— |

|

|

(0.2 |

) |

|

|

|

||||||

|

Net income (loss) |

|

0.8 |

|

(2.7 |

) |

(1.1 |

) |

(10.4 |

) |

|

(14.8 |

) |

|

(21.2 |

) |

||||||

|

Net loss attributable to noncontrolling interest |

|

(2.7 |

) |

(0.3 |

) |

(1.3 |

) |

(0.5 |

) |

|

(0.4 |

) |

|

(1.0 |

) |

||||||

|

Net loss attributable to the shareholders of Ambulnz |

$ |

3.5 |

|

(2.4 |

) |

0.2 |

|

(9.9 |

) |

$ |

(14.30 |

) |

$ |

(20.20 |

) |

||||||

|

Net income (loss) per share – Basic |

$ |

38.75 |

|

(26.50 |

) |

2.02 |

|

(109.03 |

) |

$ |

(159.00 |

) |

$ |

(216.00 |

) |

||||||

11

Consolidated Balance Sheet Data:

|

As of September 30, |

As of December 31, |

|||||||||||||||

|

$ in Millions |

2021 |

2020 (unaudited) |

2020 |

2019 |

||||||||||||

|

Cash and cash equivalents |

$ |

39.6 |

|

$ |

36.6 |

|

$ |

32.4 |

|

$ |

47.7 |

|

||||

|

Working capital |

|

29.8 |

|

|

40.6 |

|

|

34.9 |

|

|

49.4 |

|

||||

|

Total assets |

|

144.1 |

|

|

96.3 |

|

|

100.2 |

|

|

101.0 |

|

||||

|

Notes payable, current portion |

|

0.9 |

|

|

0.5 |

|

|

0.7 |

|

|

0.6 |

|

||||

|

Operating and finance lease liabilities, current portion |

|

4.4 |

|

|

3.1 |

|

|

3.5 |

|

|

3.1 |

|

||||

|

Notes payable, noncurrent |

|

0.6 |

|

|

0.7 |

|

|

0.6 |

|

|

0.8 |

|

||||

|

Operating and finance lease liabilities, noncurrent |

|

9.5 |

|

|

9.1 |

|

|

9.1 |

|

|

11.1 |

|

||||

|

Accumulated deficit |

|

(87.1 |

) |

|

(82.8 |

) |

|

(87.3 |

) |

|

(72.9 |

) |

||||

12

SUMMARY HISTORICAL FINANCIAL INFORMATION OF MOTION ACQUISITION CORP.

The following table sets forth selected historical financial information derived from Motion’s (i) unaudited financial statements included elsewhere in this prospectus as of September 30, 2021 and for the three- and nine- month periods then ended and (ii) audited financial statements included elsewhere in this prospectus as of December 31, 2020 and for the period from August 11, 2020 (inception) through December 31, 2020.