As filed with the Securities and Exchange Commission on October 15, 2021

No. 333-[

]

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter)

Delaware |

7389 |

98-1499860 | ||

(State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

101 S. Hanley Rd., Suite 300

St. Louis, MO 63105

Telephone: (314) 412-1227

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Jason Pello

Chief Financial Officer

c/o

Nerdy Inc.

101 S. Hanley Rd., Suite 300

St. Louis, MO 63105

Telephone: (314) 412-1227

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

| John M. Mutkoski Jocelyn M. Arel Evyn W. Rabinowitz Goodwin Procter LLP 100 Northern Avenue Boston, Massachusetts 02210 Tel: (617) 570-1000 |

Chris Swenson Chief Legal Officer Nerdy Inc. 101 S. Hanley Rd., Suite 300 St. Louis, MO 63105 Telephone: (314) 412-1227 |

Approximate date of commencement of proposed sale to the public:

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated

filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2

of the Exchange Act.Large accelerated filer |

☐ |

Accelerated filer |

☐ | |||

☒ |

Smaller reporting company |

|||||

Emerging growth company |

||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule

13e-4(i)

(Cross-Border Issuer Tender Offer) ☐ Exchange Act Rule

14d-l(d)

(Cross-Border Third-Party Tender Offer) ☐ CALCULATION OF REGISTRATION FEE

| | ||||||||

| Title of each class of securities to be registered |

Amount to be registered (1) |

Proposed maximum offering price per security |

Proposed maximum aggregate offering price |

Amount of registration fee | ||||

| Class A common stock (2)(3) |

55,665,294 | $9.16 (4) | $509,894,093.04 (4) | $47,267.18 | ||||

| Warrants to purchase Class A common stock (2)(5) |

8,281,469 | $2.28 (6) | $18,881,749.30 (6) | $1,750.34 | ||||

| Class A common stock (2)(7) |

87,065,506 | $9.16 (4) | $797,520,034.96 (4) | $73,930.11 | ||||

| Total |

$1,326,295,877.30 |

$122,948 | ||||||

| | ||||||||

| | ||||||||

(1) |

Immediately prior to the consummation of the Business Comnination described in the prospectus forming part of this registration statement (the “Prospectus”), TPG Pace Tech Opportunities Corp., a Cayman Islands exempted company (“TPG Pace”), effected a deregistration under the Cayman Islands Companies Law (2020 Revision) and a domestication under Section 388 of the Delaware General Corporation Law, pursuant to which TPG Pace’s jurisdiction of incorporation was changed from the Cayman Islands to the State of Delaware (the “Domestication”), and was renamed “Nerdy Inc.” (“Nerdy”), as further described in the prospectus. All securities being registered were or will be issued by Nerdy. |

(2) |

Pursuant to Rule 416(a) of the Securities Act of 1933, as amended (the “Securities Act”), an indeterminable number of additional securities that may be issued to prevent dilution resulting from stock splits, stock dividends or similar transactions are also being registered. |

(3) |

The number of shares of Class A common stock being registered represents the sum of (a) 11,549,890 shares of Class A common stock issued to legacy Nerdy LLC holders in connection with the closing of the Business Combination, (b) 7,883,250 shares of Class A common stock issued to TPG Pace Tech Opportunities Sponsor, Series LLC which were issued upon the conversion of the Founder Shares, (c) 4,000,000 Earnout Shares issued to certain affiliates of TPG Pace, (d) 642,089 Earnout Shares issued to legacy Nerdy LLC holders, (e) 15,000,000 shares of Class A common stock issued to certain qualified institutional buyers and accredited investors in private placements consummated in connection with the PIPE Investment (as defined herein), (f) 16,116,750 shares of Class A common stock issued pursuant to the Forward Purchase Agreements (as defined herein) and (g) 473,315 shares of Class A common stock reserved for issuance upon the exercise of the Stock Appreciation Rights held by former employees and consultants. |

(4) |

Estimated solely for the purpose of calculating the registration fee, based on the average of the high and low prices of the Class A ordinary shares of Nerdy on the New York Stock Exchange (the “NYSE”) on October 13, 2021 (such date being within five business days of the date that this registration statement was first filed with the SEC). This calculation is in accordance with Rule 457(c) of the Securities Act. |

(5) |

The number of warrants being registered represents the sum of (a) 3,000,000 warrants to purchase shares of Class A common stock issued to certain shareholders of TPG Pace, (b) 4,888,889 warrants to purchase Class A common stock issued to TPG Pace Tech Opportunities, Series LLC and (c) 392,580 warrants to purchase shares of Class A common stock issued to legacy Nerdy LLC holders. |

(6) |

Estimated solely for the purpose of calculating the registration fee, based on the average of the high and low prices of the warrants of Nerdy on the NYSE on October 13, 2021 (such date being within five business days of the date that this registration statement was first filed with the SEC). This calculation is in accordance with Rule 457(c) of the Securities Act. |

(7) |

The number of shares of Class A common stock being registered represents the sum of (a) 8,281,469 shares of Class A common stock to be issued to certain shareholders upon exercise of outstanding Class A warrants, with each warrant exercisable for one share of common stock, subject to adjustment, for an exercise price of $11.50 per share, (b) 2,051,864 shares of Class A common stock underlying the 2,051,864 shares of Class B common stock to be issued to certain shareholders upon exercise of the outstanding Class B warrants, with each warrant exercisable for one share of Class B common stock, subject to adjustment, for an exercise price of $11.50 per share and (c) 76,732,173 shares of Class A common stock underlying the shares of outstanding Class B common stock (including 3,357,911 Earnout Shares). |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until this registration statement shall become effective on such date as the SEC, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED OCTOBER 15, 2021

PROSPECTUS FOR

55,665,294 SHARES OF CLASS A COMMON STOCK

8,281,469 CLASS A WARRANTS TO PURCHASE SHARES OF CLASS A COMMON STOCK

8,281,469 SHARES OF CLASS A COMMON STOCK UNDERLYING WARRANTS TO PURCHASE CLASS A COMMON STOCK

2,051,864 SHARES OF CLASS A COMMON STOCK UNDERLYING THE SHARES OF CLASS B COMMON STOCK UNDERLYING THE WARRANTS TO PURCHASE CLASS B COMMON STOCK

AND

76,732,173 SHARES OF CLASS A COMMON STOCK UNDERLYING CLASS B COMMON STOCK

OF

NERDY INC.

This prospectus relates to (i) the resale of 11,549,890 shares of Class A common stock, par value $0.0001 per share (the “Class A common stock”) issued to legacy Nerdy LLC holders in connection with the closing of the Business Combination, (ii) resale of 7,883,250 shares of Class A common stock issued to TPG Pace Tech Opportunities Sponsor, Series LLC which were issued upon the conversion of the Founder Shares, (iii) resale of 4,000,000 Earnout Shares issued to certain affiliates of TPG Pace, (iv) resale of 642,089 Earnout Shares issued to legacy Nerdy LLC holders, (v) the resale of 15,000,000 shares of Class A common stock issued in the PIPE Investment (as defined below) by certain of the selling securityholders, (vi) the resale of 16,116,750 shares of Class A common stock issued in connection with the Forward Purchase Agreements and (vii) the resale of 473,315 shares of Class A common stock reserved for issuance upon the exercise of the Stock Appreciation Rights held by former employees and consultants. This prospectus also relates to (a) the resale of 3,000,000 warrants to purchase shares of Class A common stock issued to certain shareholders of TPG Pace (as defined below), (b) 4,888,889 warrants to purchase Class A common stock issued to TPG Pace Tech Opportunities, Series LLC (c) the resale of 392,580 warrants to purchase shares of Class A common stock issued in exchange for warrants of Nerdy (as defined below), (d) the issuance by us of up to 8,281,469 shares of Class A common stock upon the exercise of outstanding warrants to purchase shares of Class A common stock, (e) the issuance by us of up to 2,051,864 shares of Class A common stock underlying the 2,051,864 shares of Class B common stock to be issued upon exercise of the outstanding warrants to purchase Class B common stock and (e) the issuance by us of up to 76,732,173 shares of Class A common stock upon the exercise of the OpCo Redemption Right (as defined herein) by the holders of OpCo Units.

On September 20, 2021 (the “Closing Date”), Nerdy Inc., a Delaware corporation (formerly known as TPG Pace Tech Opportunities Corp.) (the “Company”), consummated the previously announced business combination (the “Closing”) pursuant to that certain Business Combination Agreement, dated as of January 28, 2021 (as amended on March 19, 2021, on July 14, 2021, on August 11, 2021 and on August 18, 2021, the “Business Combination Agreement”) by and among the Company, TPG Pace Tech Merger Sub LLC, a Delaware limited liability company (“TPG Pace Merger Sub”), TCV VIII (A) VT, Inc., a Delaware corporation (“TCV Blocker”), LCSOF XI VT, Inc., a Delaware corporation (“Learn Blocker” and, together with TCV Blocker, the “Blockers”), TPG Pace Blocker Merger Sub I Inc., a Delaware corporation (“Blocker Merger Sub I”), TPG Pace Blocker Merger Sub II Inc., a Delaware corporation (“Blocker Merger Sub II” and, together with Blocker Merger Sub I, the “Blocker Merger Subs” and, together with TPG Pace Merger Sub, the “Merger Subs”), Live Learning Technologies LLC, a Delaware limited liability company (“Nerdy LLC”), and, solely for the purposes described therein, certain entities affiliated with the Blockers (the “Blocker Holders”). The transactions contemplated by the Business Combination Agreement are collectively referred to herein as the “Business Combination.” Unless the context otherwise provides, “TPG Pace” refers to the registrant prior to the Closing, and “we,” “us,” “our,” “Nerdy Inc.,” and the “Company” refer to the registrant and, where appropriate, its subsidiaries following the Closing.

We are registering the resale of shares of common stock and warrants as required by (i) an amended and restated registration rights agreement, dated as of September 20, 2021 (the “Registration Rights Agreement”) with certain holders of Class A Common Stock and private placement warrants, (ii) the subscription agreements entered into by and between TPG Pace and certain qualified institutional buyers and accredited investors relating to the purchase of shares of common stock in private placements consummated in connection with the Business Combination, and (iii) the forward purchase agreements entered into by and between TPG Pace and (a) certain third parties and (b) certain employees, affiliates and “friends of the firm” of TPG Global (such employees, affiliates and friends of the firm, the “TPG Global Purchasers” together with the third party forward purchasers, the “forward purchasers”).

We are also registering the (i) resale of other shares of common stock held by certain of our shareholders and (ii) the issuance and resale of shares of common stock reserved for issuance upon the exercise of Stock Appreciation Rights to receive shares of common stock and the settlement of restricted stock units, in each case, held by certain of our current and former employees.

We will receive the proceeds from any exercise of the warrants for cash, but not from the resale of the shares of common stock or warrants by the selling securityholders.

We will bear all costs, expenses and fees in connection with the registration of the shares of common stock, Stock Appreciation Rights and warrants. The selling securityholders will bear all commissions and discounts, if any, attributable to their respective sales of the shares of common stock and warrants.

Trading of our common stock and warrants began on The New York Stock Exchange (the “NYSE”) on September 20, 2021, under the new ticker symbol “NRDY” for the common stock and “NRDY WS” for the warrants. Prior to the Domestication, TPG Pace’s Class A ordinary shares, par value $0.0001 per share (the “TPG Pace Class A ordinary shares”) and warrants to purchase TPG Pace Class A ordinary shares (the “TPG Pace warrants”) traded under the ticker symbols “PACE” and “PACE WS”, respectively, on the NYSE. On October 14, 2021, the closing sale price of the our common stock was $9.02 per share and the closing price of our warrants was $2.10 per warrant.

Investing in shares of our common stock or warrants involves risks that are described in the “Risk Factors” section beginning on page 12 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued under this prospectus or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2021.

TABLE OF CONTENTS

Page |

||||

i |

||||

ii |

||||

ii |

||||

viii |

||||

1 |

||||

12 |

||||

51 |

||||

52 |

||||

53 |

||||

62 |

||||

71 |

||||

96 |

||||

114 |

||||

119 |

||||

124 |

||||

126 |

||||

132 |

||||

137 |

||||

149 |

||||

150 |

||||

153 |

||||

153 |

||||

153 |

||||

F-1 |

||||

II-1 |

||||

You should rely only on the information contained in this prospectus. No one has been authorized to provide you with information that is different from that contained in this prospectus. This prospectus is dated as of the date set forth on the cover hereof. You should not assume that the information contained in this prospectus is accurate as of any date other than that date.

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form

S-1

that we filed with the Securities and Exchange Commission (the “SEC”) using the “shelf” registration process. Under this shelf registration process, the Selling Securityholders may, from time to time, sell the securities offered by them described in this prospectus. We will not receive any proceeds from the sale by such Selling Securityholders of the securities offered by them described in this prospectus. This prospectus also relates to the issuance by us of the shares of Class A and Class B Common Stock issuable upon the exercise of any Warrants. We will receive proceeds from any exercise of the Warrants for cash. Neither we nor the Selling Securityholders have authorized anyone to provide you with any information or to make any representations other than those contained in this prospectus or any applicable prospectus supplement or any free writing prospectuses prepared by or on behalf of us or to which we have referred you. Neither we nor the Selling Securityholders take responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. Neither we nor the Selling Securityholders will make an offer to sell these securities in any jurisdiction where the offer or sale is not permitted.

We may also provide a prospectus supplement or post-effective amendment to the registration statement to add information to, or update or change information contained in, this prospectus. You should read both this prospectus and any applicable prospectus supplement or post-effective amendment to the registration statement together with the additional information to which we refer you in the sections of this prospectus entitled “Where You Can Find More Information.”

Neither we nor the Selling Securityholders have authorized anyone to provide any information or to make any representations other than those contained in this prospectus, any accompanying prospectus supplement or any free writing prospectus we have prepared. We and the Selling Securityholders take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the securities offered hereby and only under circumstances and in jurisdictions where it is lawful to do so. No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus, any applicable prospectus supplement or any related free writing prospectus. This prospectus is not an offer to sell securities, and it is not soliciting an offer to buy securities, in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus or any prospectus supplement is accurate only as of the date on the front of those documents, regardless of the time of delivery of this prospectus or any applicable prospectus supplement, or any sale of a security. Our business, financial condition, results of operations and prospects may have changed since those dates.

For investors outside the United States: neither we nor the Selling Securityholders have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of our securities and the distribution of this prospectus outside the United States.

This prospectus contains summaries of certain provisions contained in some of the documents described herein, but reference is made to the actual documents for complete information. All of the summaries are qualified in their entirety by the actual documents. Copies of some of the documents referred to herein have been filed, will be filed or will be incorporated by reference as exhibits to the registration statement of which this prospectus is a part, and you may obtain copies of those documents as described below under “Where You Can Find More Information.”

i

TRADEMARKS

This document contains references to trademarks, trade names and service marks belonging to other entities. Solely for convenience, trademarks, trade names and service marks referred to in this prospectus may appear without the

®

or TM symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies. NON-GAAP

FINANCIAL MEASURE Adjusted EBITDA (Loss) is a

non-GAAP

financial measure and should not be considered a substitute for any other performance metric derived in accordance with GAAP. Adjusted EBITDA (loss) is defined as net income or net loss, as applicable, before net interest income (expense), taxes, depreciation and amortization expense, gain on extinguishment of debt, non-cash

compensation expense, transaction related costs, and losses on subleases. Nerdy’s management believes that Adjusted EBITDA (Loss) provides useful information to management and investors regarding certain financial and business trends relating to Nerdy’s financial condition and results of operations. The Company believes that the use of Adjusted EBITDA (Loss) provides an additional tool for investors to use in evaluating ongoing operating results and trends. Adjusted EBITDA (Loss) is not a GAAP measure of our financial performance or liquidity and management does not consider Adjusted EBITDA (Loss) in isolation or as an alternative to financial measures determined in accordance with GAAP. Other companies may calculate Adjusted EBITDA (Loss) differently, and therefore the Adjusted EBITDA (Loss) of Nerdy included in this presentation may not be directly comparable to similarly titled measures of other companies. Please refer to the consolidated financial statements and notes thereto included elsewhere in this prospectus. SELECTED DEFINITIONS

Unless otherwise stated in this prospectus or the context otherwise requires, references to:

| • | “additional forward purchasers” means third party purchasers not affiliated with TPG Global who committed to purchase securities under the Forward Purchase Agreements; |

| • | “amended and restated memorandum and articles of association” means the amended and restated memorandum and articles of association of TPG Pace, effective October 6, 2020; |

| • | “Available Cash” means as of the closing, the amount of funds contained in TPG Pace’s trust account (net of any shareholder redemption amounts) plus the net cash proceeds to TPG Pace resulting from the Subscription Agreements and the Forward Purchase Agreements; |

| • | “Blocker Merger Sub I” means TPG Pace Blocker Merger Sub I Inc., a Delaware corporation and wholly owned subsidiary of TPG Pace; |

| • | “Blocker Merger Sub II” means TPG Pace Blocker Merger Sub II Inc., a Delaware corporation and wholly owned subsidiary of TPG Pace; |

| • | “Blocker Merger Subs” means Blocker Merger Sub I and Blocker Merger Sub II; |

| • | “Blockers” means TCV Blocker and Learn Blocker; |

| • | “Business Combination Agreement” means that certain Business Combination Agreement, dated January 28, 2021, by and among TPG Pace, TPG Pace Merger Sub, TCV Blocker, Learn Blocker, Blocker Merger Sub I, Blocker Merger Sub II, Nerdy, and, solely for the purposes stated therein, certain entities affiliates with the Blockers (as amended on March 19, 2021, on July 14, 2021, on August 11, 2021 and on August 18, 2021 and as amended, supplemented or otherwise modified from time to time in accordance with its terms); |

ii

| • | “Business Combination” means the Domestication, the Merger and other transactions contemplated by the Business Combination Agreement, collectively, including the PIPE Financing; |

| • | “Call Right” means the right, pursuant to the OpCo LLC Agreement and upon the exercise of the OpCo Redemption Right by an OpCo Unitholder, for Nerdy Inc. to acquire each tendered OpCo Unit directly from such OpCo Unitholder for, at Nerdy Inc.’s election, (i) one share of Class A Common Stock, subject to conversion rate adjustments for stock splits, stock dividends and reclassification, or (ii) an equivalent amount of cash; |

| • | “Cayman Islands Companies Act” means the Companies Act (2021 Revision) of the Cayman Islands as the same may be amended from time to time; |

| • | “Class A Common Stock” means Class A common stock, $0.0001 par value of Nerdy Inc.; |

| • | “Class A Shares” means the Class A ordinary shares, $0.0001 par value in the capital of TPG Pace, which automatically converted, on a one-for-one |

| • | “Class B Common Stock” means the Class B common Stock, par value $0.0001 per share of Nerdy Inc.; |

| • | “Closing Date” means the date on which the Closing occurred; |

| • | “Closing” means the closing of the transactions contemplated by the Business Combination Agreement; |

| • | “Cohn” means, collectively, Cohn Investments, LLC and Charles K. Cohn VT Trust U/A/D May 26, 2017 |

| • | “Common Stock” means the Class A Common Stock and Class B Common Stock; |

| • | “Condition Precedent Proposals” means the Business Combination Proposal, the Domestication Proposal, the Charter Proposal, the Director Election Proposal, the Equity Incentive Plan Proposal and the NYSE Proposal, collectively; |

| • | “Continental” means Continental Stock Transfer & Trust Company; |

| • | “Domestication” means the transfer by way of continuation and deregistration of TPG Pace from the Cayman Islands and the continuation and domestication as a corporation registered in the State of Delaware, upon which TPG Pace changed its name to Nerdy Inc.; |

| • | “Earnout Equity” means the TPG Pace Sponsor Earnout Equity and the Nerdy Earnout Consideration; |

| • | “Effective Time” means the time at which the Merger became effective; |

| • | “Equity Incentive Plan” means the Nerdy Inc. 2021 Equity Incentive Plan adopted and approved by the shareholders pursuant to the Equity Incentive Plan Proposal; |

| • | “Excess Shares” means shares in excess of 15,000,000 aggregate forward purchase shares; |

| • | “Excess Share Forfeitures” means the forfeiture of Excess Shares pursuant to the Waiver Agreement; |

| • | “Existing Governing Documents” means the amended and restated memorandum and articles of association; |

| • | “Existing Nerdy Holders” means the existing holders of equity securities of Nerdy, but including with respect to the Blockers, the owners of the Blockers with respect to their indirect interest in Nerdy equity; |

| • | “Experts” means Nerdy’s tutors, instructors, subject matter experts, educators and other professionals; |

| • | “Forward Purchase Agreements” means those certain forward purchase agreements, entered into in connection with the TPG Pace IPO, by and among TPG Pace, TPG Holdings and certain third parties |

iii

| pursuant to which TPG Holdings, certain transferees of TPG Holdings and certain third parties, upon the terms and subject to the conditions set forth therein, have agreed to purchase certain Class A Shares and forward purchase warrants prior to the consummation of TPG Pace’s initial business combination; |

| • | “forward purchase shares” means the shares of Class A Common Stock issued pursuant to the Forward Purchase Agreements; |

| • | “forward purchase warrants” means the warrants issued pursuant to the Forward Purchase Agreements; |

| • | “forward purchases” means the transactions contemplated under the Forward Purchase Agreements; |

| • | “forward purchase securities” means, collectively, forward purchase shares and forward purchase warrants; |

| • | “Founder Shares” means the 11,250,000 Class F ordinary shares, par value $0.0001 per share, of TPG Pace that were initially issued to our Sponsor in a private placement prior to our initial public offering and of which 160,000 were transferred to each of Chad Leat, Kathleen Philips, Wendi Sturgis and Kneeland Youngblood (40,000 shares each) in October 2020, and, following the Domestication, the 11,250,000 Class F ordinary shares automatically converted, on a one-for-one |

| • | “Learn Blocker” means LCSOF XI VT, Inc., a Delaware corporation; |

| • | “Learn Capital” means, collectively, Learn Blocker, Learn Capital Special Opportunities Fund XIV, L.P. and Learn Capital Special Opportunities Fund XV; |

| • | “Learners” means Nerdy’s students, users, parents, guardians, and purchasers; |

| • | “Merger Subs” means the Blocker Merger Subs and TPG Pace Merger Sub; |

| • | “Merger” means the merger of TPG Pace Merger Sub with and into Nerdy pursuant to the Business Combination Agreement, with Nerdy as the surviving company in the Merger and, after giving effect to such Merger, OpCo becoming a subsidiary of TPG Pace; |

| • | “Minimum Available Cash Condition” means the condition in the Business Combination Agreement that states that Available Cash must equal no less than $250,000,000; |

| • | “Nerdy” means, prior to the Closing of the Business Combination, Live Learning Technologies LLC, a Missouri limited liability company; |

| • | “Nerdy Earnout Consideration” means those aggregate 4,000,000 (1) shares of Class A Common Stock or (2) OpCo Units (and a corresponding number of shares of Class B Common Stock) that were paid to certain Existing Nerdy Holders (treating for such calculation each OpCo Unit and corresponding share of Pace Class B Common Stock as one), which such shares or units, as applicable, were issued but subject to forfeiture until the achievement of Triggering Event I with respect 1,333,333 shares or units, Triggering Event II with respect to 1,333,333 shares or units, and Triggering Event III with respect to 1,333,334 shares or units; |

| • | “Nerdy Inc. Board” means the board of directors of Nerdy Inc.; |

| • | “Nerdy Inc. Founder Shares” means, after the domestication, the Class F Common Stock, par value $0.0001 of Nerdy Inc.; |

| • | “Nerdy Inc. Preferred Stock” means shares of Nerdy Inc. preferred stock, par value $0.0001; |

| • | “Nerdy Inc.” means Nerdy Inc., a Delaware corporation (f.k.a. TPG Pace Tech Opportunities Corp.), upon and after the Domestication; |

| • | “Nerdy Recapitalization” means the conversion of each outstanding class of Nerdy preferred units and the Nerdy profit units (whether vested or unvested) into Nerdy common units (subject to substantially the same terms and conditions, including applicable vesting requirements); |

iv

| • | “Nerdy Securities” means Class A Common Stock and Nerdy Inc. warrants; |

| • | “Nerdy Stockholder Group” means, collectively, Cohn, Learn Capital and TCV; |

| • | “Nerdy Inc. warrants” means the warrants issued by Nerdy Inc. to acquire shares of Class A Common Stock; |

| • | “Nerdy warrants” means the Nerdy Inc. warrants and the OpCo warrants that were issued to the equity holders of Nerdy in connection with the Business Combination. |

| • | “NYSE” means the New York Stock Exchange; |

| • | “OpCo” means, after the conversion to a Delaware limited liability company and the Merger, Nerdy, LLC, a Delaware limited liability company; |

| • | “OpCo LLC Agreement” means the Second Amended and Restated Limited Liability Company Agreement of OpCo entered into in connection with the Closing; |

| • | “OpCo Redemption Right” means the right, pursuant to the OpCo LLC Agreement, for OpCo Unitholders (other than Nerdy Inc.) to cause OpCo to acquire all or a portion of their vested OpCo Units and corresponding shares of Class B Common Stock for shares of Class A Common Stock at a redemption ratio of one share of Class A Common Stock for each OpCo Unit redeemed, subject to conversion rate adjustments for stock splits, stock dividends and reclassification; |

| • | “OpCo Units” means the units of OpCo; |

| • | “OpCo Unitholder” means a holder of OpCo Units; |

| • | “OpCo warrants” means the warrants issued by OpCo to purchase OpCo Units; |

| • | “PIPE Financing” means the transactions contemplated by the Subscription Agreements, pursuant to which the certain investors agreed to purchase, and TPG Pace agreed to issue and sell to such investors, newly issued shares of Class A Common Stock at a purchase price of $10.00 per share for gross proceeds of approximately $150 million, which purchase and sale was consummated concurrently with the Business Combination; |

| • | “PIPE Investors” means the investors who participated in the PIPE Financing. |

| • | “private placement warrants” means the 7,333,333 private placement warrants outstanding as of the date of this proxy statement/prospectus that were issued to our Sponsor (which became exercisable for Class A Shares at an exercise price of $11.50 per share), which are substantially identical to the public warrants sold as part of the units in the TPG Pace IPO, subject to certain limited exceptions, 2,444,444 were forfeited by our Sponsor pursuant to the Waiver Agreement in connection with the Business Combination and, after the Domestication, the 4,888,889 private placement warrants (after giving effect to the forfeiture described in the foregoing) that are exercisable for Class A Common Stock at $11.50 per share; |

| • | “public shareholders” means holders of public shares; |

| • | “public shares” means the currently outstanding 45,000,000 Class A Shares issued as part of the Units in the TPG Pace IPO; |

| • | “public warrants” means the currently outstanding 9,000,000 warrants to purchase Class A Shares that were issued as part of the Units in the TPG Pace IPO (which became exercisable for Class A Shares at an exercise price of $11.50 per share) and, after the Domestication, the 9,000,000 warrants to purchase Class A Common Stock that are exercisable for shares of Class A Common Stock at $11.50 per share; |

| • | “redemption” means each redemption of public shares for cash pursuant to the Existing Governing Documents; |

v

| • | “Registration Rights Agreement” means that certain agreement with certain holders of Class A Common Stock and warrants after Closing, pursuant to which registration rights with respect to such securities will be offered; |

| • | “SEC” means the Securities and Exchange Commission; |

| • | “Securities Act” means the Securities Act of 1933, as amended; |

| • | “Share Forfeitures” means, together, the Excess Share Forfeiture and the additional forfeiture of 2,000,000 shares of Class A Common Stock by holders of Founder Shares pursuant to the Waiver Agreement; |

| • | “Stockholders’ Agreement” means that certain agreement by and among TPG Pace, the Nerdy Stockholder Group and Sponsor, pursuant to which certain governing rights and obligations of the parties are given; |

| • | “Sponsor” means TPG Pace Tech Opportunities Sponsor, Series LLC, a Delaware limited liability company; |

| • | “Subscription Agreements” means the subscription agreements, entered into by TPG Pace and certain investors in connection with the PIPE Financing; |

| • | “TCV” means, collectively, TCV Blocker, TCV VIII (A) VT, L.P., TCV VIII, L.P., TCV VIII (B), L.P., TCV Member Fund, L.P and TCV VIII Master, L.P.; |

| • | “TCV Blocker” means TCV VIII (A) VT, Inc., a Delaware corporation; |

| • | “TPG” means TPG Global, LLC and its affiliates; |

| • | “TPG Capital BD” means TPG Capital BD, LLC, an affiliate of our Sponsor and TPG Pace; |

| • | “TPG Global” means TPG Global, LLC; |

| • | “TPG Global Purchasers” means affiliates and employees of TPG Global that have committed to purchase forward purchase securities pursuant to the Forward Purchase Agreements; |

| • | “TPG Pace Initial Shareholders” means our Sponsor and the TPG Pace Independent Directors; |

| • | “TPG Pace IPO” means TPG Pace’s initial public offering that was consummated on October 9, 2020; |

| • | “TPG Pace Merger Sub” means TPG Pace Tech Merger Sub LLC, a Delaware limited liability company and wholly owned subsidiary of TPG Pace; |

| • | “TPG Pace ordinary shares” means our Class A Shares and our Founder Shares; |

| • | “TPG Pace Public Securities” means Class A Shares and TPG Pace Public Warrants; |

| • | “TPG Pace Public Warrants” means the currently outstanding 9,000,000 warrants to purchase Class A Shares that were issued as part of the Units in the TPG Pace IPO (which became exercisable for Class A Shares at an exercise price of $11.50 per share); |

| • | “TPG Pace Sponsor Earnout Equity” means 4,000,000 shares of Class A Common Stock that have been made subject to potential forfeiture by Sponsor following the Closing until the achievement of Triggering Event I with respect 1,333,333 shares, Triggering Event II with respect to 1,333,333 shares, and Triggering Event III with respect to 1,333,334 shares, consistent with the forfeiture thresholds for the Nerdy Earnout Consideration; |

| • | “TPG Pace,” means TPG Pace Tech Opportunities Corp., a Cayman Islands exempted company, prior to the consummation of the Domestication; |

| • | “TRA Holders” means the OpCo Unitholders (other than Nerdy Inc.) that are a party to the Tax Receivable Agreement (and their respective successors and permitted assigns under the Tax Receivable Agreement); |

| • | “transfer agent” means Continental, TPG Pace’s transfer agent; |

vi

| • | “Triggering Event I” means the date on which the closing sale price of one share of Class A Common Stock quoted on the New York Stock Exchange (or the exchange on which the shares of Class A Common Stock are then listed) is greater than or equal to $12.00 for any 20 days within any 30 consecutive day period in which the Class A Common Stock are actually traded on the applicable exchange for the period between January 28, 2021 and the five-year anniversary of the Closing Date; |

| • | “Triggering Event II” means the date on which the closing sale price of one share of Class A Common Stock quoted on the New York Stock Exchange (or the exchange on which the shares of Class A Common Stock are then listed) is greater than or equal to $14.00 for any 20 days within any 30 consecutive day period in which the Class A Common Stock are actually traded on the applicable exchange for the period between January 28, 2021 and the five-year anniversary of the Closing Date; |

| • | “Triggering Event III” means the date on which the closing sale price of one share of Class A Common Stock quoted on the New York Stock Exchange (or the exchange on which the shares of Class A Common Stock are then listed) is greater than or equal to $16.00 for any 20 days within any 30 consecutive day period in which the Class A Common Stock are actually traded on the applicable exchange for the period between January 28, 2021 and the five-year anniversary of the Closing Date; |

| • | “Trust Account” means the trust account established at the consummation of the TPG Pace’s IPO that holds the proceeds of the initial public offering and is maintained by Continental, acting as trustee; |

| • | “Units” means the units of TPG Pace, each unit representing one Class A Share and one-fifth of one warrant to acquire one Class A Share, that were offered and sold by TPG Pace in its initial public offering and in its concurrent private placement; |

| • | “Waiver Agreement” means that certain waiver agreement, dated January 29, 2021, by and among TPG Pace, our Sponsor and each holder of issued and outstanding Founder Shares which provides, among other things, that (i) holders of Founder Shares agreed to forfeit for no consideration a number of shares of Class A Common Stock equal to the number of shares of Class A Common Stock issued pursuant to certain Forward Purchase Agreements over an aggregate of 15,000,000 shares of Class A Common Stock, (ii) such holders of Founder Shares agreed to forfeit for no consideration 2,000,000 shares of Class A Common Stock, which shares of Class A Common Stock were immediately cancelled upon the Closing, (iii) Sponsor agreed to forfeit for no consideration 2,444,444 private placement warrants that were immediately cancelled upon the Closing and (iv) Sponsor further agreed to subject 4,000,000 shares of Class A Common Stock following the closing to potential forfeiture if certain stock price thresholds are not achieved within a period of five years from the Closing Date, consistent with the forfeiture thresholds for the Nerdy Earnout Consideration; |

| • | “warrants” means, collectively, the FPA Warrants, public warrants, private placement warrants and certain Nerdy warrants. |

Unless otherwise specified, the share counts and other data set forth in this prospectus

| • | includes (a) the 8,000,000 aggregate shares of Class A Common Stock or OpCo Units (with equivalent number of shares of Class B Common Stock) that comprise the Earnout Equity, which are issued and outstanding as of Closing, but subject to forfeiture and (b) an expected 18,075,207 shares (of which 5,976,406 will be shares of Class A Common Stock of Nerdy, Inc. and 12,098,801 shares of Class B Common Stock of Nerdy Inc.) underlying (i) 9,036,422 vested (of which 1,233,379 are vested unit appreciation rights and 7,803,043 are vested profit interest units) and (ii) 9,038,785 unvested (of which 4,743,027 are unvested stock appreciation rights and 4,295,758 are unvested profit interest units), which unvested stock appreciation rights and profit interest units will be subject to certain vesting conditions and a risk of forfeiture, that are held by the former Nerdy unit appreciation rights and profit interest units holders immediately following the Closing; |

| • | does not take into account the issuance of any shares under the Equity Incentive Plan; and |

| • | otherwise assumes that none of TPG Pace’s existing shareholders or Nerdy equity holders purchase Class A Shares in the open market. |

vii

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements in this prospectus may constitute “forward-looking statements” for purposes of the federal securities laws. Our forward-looking statements include, but are not limited to, statements regarding our or our management team’s expectations, hopes, beliefs, intentions or strategies regarding the future, including those relating to the Business Combination. The information included in this prospectus in relation to Nerdy has been provided by Nerdy and its respective management, and forward-looking statements include statements relating to our and its respective management team’s expectations, hopes, beliefs, intentions or strategies regarding the future, including those relating to the Business Combination. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “believe,” “contemplate,” “continue,” “could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “will,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this prospectus may include, for example, statements about:

| • | the market opportunity of Nerdy Inc.; |

| • | the ability to obtain and/or maintain the listing of the Class A and Class B Common Stock and the Company warrants on the NYSE, and the potential liquidity and trading of such securities; |

| • | the risk that the Business Combination disrupts current plans and operations of the Company as a result of the announcement and consummation of the Business Combination; |

| • | the ability to recognize the anticipated benefits of the Business Combination, which may be affected by, among other things, competition, the ability of the combined company to grow and retain its key employees; |

| • | costs related to the Business Combination; |

| • | changes in applicable laws or regulations; |

| • | our ability to raise financing in the future; |

| • | our ability to effectively and strategically use the cash received in connection with the Business Combination; |

| • | our success in retaining or recruiting, or changes required in, our officers, key employees or directors following the completion of the Business Combination; |

| • | the period over which the Company anticipates its existing cash and cash equivalents will be sufficient to fund its operating expenses and capital expenditure requirements; |

| • | regulatory developments in the United States and foreign countries; |

| • | the impact of laws and regulations; |

| • | our ability to attract and retain key management personnel; |

| • | our estimates regarding expenses, future revenue, capital requirements and needs for additional financing; |

| • | our financial performance; |

| • | the effect of COVID-19 on the foregoing; and |

| • | other factors detailed in the Prospectus in the section entitled “Risk Factors” beginning on page 12. |

The forward-looking statements contained in this prospectus are based on information available as of the date of this Prospectus and current expectations and beliefs concerning future developments and their potential

viii

effects on us. There can be no assurance that future developments affecting us will be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the heading “.” Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. Some of these risks and uncertainties may in the future be amplified by the

Risk Factors

COVID-19

outbreak and there may be additional risks that we consider immaterial or which are unknown. It is not possible to predict or identify all such risks. We do not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws. As a result of a number of known and unknown risks and uncertainties, our actual results or performance may be materially different from those expressed or implied by these forward-looking statements. You should not place undue reliance on these forward-looking statements.

ix

SUMMARY OF THIS PROSPECTUS

This summary highlights selected information from this prospectus and does not contain all of the information that is important to making an investment descision. Before investing in our securities, you should carefully read this entire prospectus, including our financial statements and the related notes included in this prospectus and the information set forth under the headings “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” See also the section entitled “Where You Can Find Additional Information.”

Unless otherwise indicated or the context otherwise requires, references in this Business Summary to “we,” “us,” “our” and other similar terms refer to Nerdy and its subsidiaries prior to the Business Combination and to Nerdy Inc. and its consolidated subsidiaries after giving effect to the Business Combination.

Mission

Our mission is to transform how people learn through technology. We are enabling access to high quality, personalized, live learning in any subject, anywhere, at any time.

Business Overview

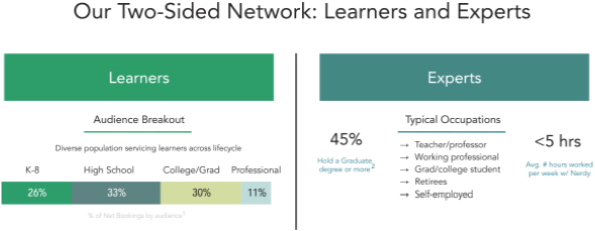

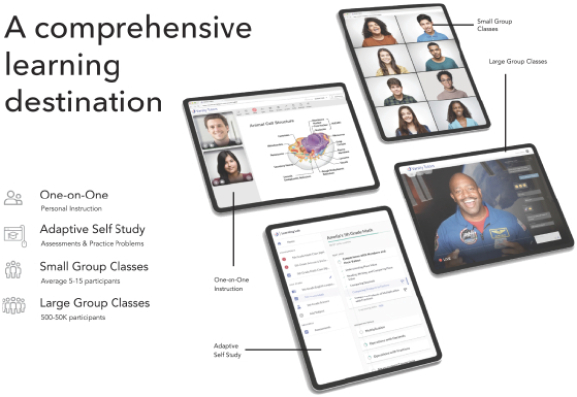

Nerdy is a leading platform for live online learning. We have built a comprehensive online learning destination that enables the delivery of scaled, high-quality, live instruction for Learners of all ages across more than 3,000 subjects. Through our flagship business, Varsity Tutors, we delivered over 4.7 million hours of live learning in 2020, including 1.6 million paid hours of live learning and 3.1 million hours of free live learning, across multiple learning formats including instruction, small group classes, large format group classes, and adaptive self-study. Our purpose-built proprietary platform leverages technology, including artificial intelligence, or AI, to source, evaluate, and match tutors, instructors, subject matter experts, educators and other professionals (“Experts”) directly with students, users, parents, guardians, and purchasers (“Learners”).

direct-to-consumer

one-on-one

Every day millions of student and professional learners in our country struggle to get the help they need to master the subjects they are attempting to learn. Whether it is seeking help understanding algebra or chemistry, learning to code, studying for a nursing exam or attempting to comprehend thousands of other topics, Learners are increasingly looking for help to supplement their training. We created Nerdy to help these Learners get the help they need from the Experts who are most qualified to provide the assistance.

in-classroom

education or on-the-job

We attract Learners across a variety of audiences and subjects including

K-8,

High School, College, Graduate, Professional, and other Adult Learners to get the knowledge that they need. The breadth of our platform offering in terms of both subject and learning format, combined with our ability to build trust, own the customer relationship, and make good on our customer promises has allowed us to generate high customer satisfaction as evidenced by our Net Promoter Score of 68 for customers surveyed in 2020. This relationship with our customers and a relentless focus on delivering an exceptional customer experience enables longer-term and higher lifetime value relationships with Learners. We attract Experts to our platform who are highly qualified to instruct across a variety of audiences and subjects. We offer Experts the opportunity to generate income from the convenience of home with less hassle, deliver a superior online instruction experience, and empower them to help people learn. Our technology platform matches Learners to the Experts who are qualified to provide the unique assistance our Learners need, which results in long-term highly-satisfied customer relationships that generate sustained income for our Experts.

1

Finding the exact right Expert to meet the specific and unique needs of a Learner is a critical driver of having a successful learning experience and has a profound impact on Learner satisfaction. Our technology platform identifies and curates the top Experts in every subject, which enables us to match Learners to the Experts who are ideally qualified to help them learn. The result is an exceptional experience for Learners. We use AI to select the ideal Expert for a given Learner’s needs, taking into account more than 100 variables, including Learner and Expert attributes, diagnostic assessments, and data from past learning experiences. We believe quality matching is a key differentiator for Nerdy, something that legacy offline models and online directories struggle to do well.

| Nerdy’s Model |

Online Directories / Online Open Marketplace Models |

Offline / Legacy Models | ||||

| Expert Quality | Technology driven-process for identifying and curating top Experts |

Limited qualifying and vetting of Experts | Limited ability to find top Experts due to constraint of local geography | |||

| Matching Students to Experts | Technology-driven process helps Nerdy identify the right Expert for each Learner’s particular needs | Limited effort to match the Experts best suited to help a specific Learner and limited data captured programmatically to inform personalization | Limited ability to optimize matching due to geographic constraints and limited data captured programmatically to inform personalization | |||

| Availability of Formats | Multiple learning formats woven together into one comprehensive online experience | Limited formats typically involving one online format or only facilitating off- platform learning | Multiple offline formats requiring in-person attendance | |||

| Session Convenience | Efficient, convenient, and high customer satisfaction | Inefficient, inconsistent customer experience and satisfaction | Inefficient, inconsistent and costly | |||

A recent industry report estimates that the global market for supplemental education in 2020 is $1.3 trillion, excluding government-funded education. The vast majority, approximately 98%, of this market remains offline. We believe that inefficiencies in traditional learning total addressable market was approximately $47 billion in 2019 and will grow to approximately $62 billion by 2024.

direct-to-consumer

in-person

learning models have created a significant opportunity for online learning. COVID-19

has further highlighted the inadequacies of traditional in-person

models as well as the benefits of online supplemental learning. We believe these trends will persist past COVID-19,

as a November 2020 survey of 1,000 parents of K-12

students indicated that those consumers are 70% more likely to use online learning than they were a year ago, and 83% of consumers report that they plan to continue using online learning going forward. We estimate our U.S. direct-to-consumer

Nerdy’s multi-format online learning destination improves access and lowers cost barriers to high-quality, live learning and other additive learning resources. In addition to our paid instruction and small group class products, we offer free live large-format online classes that are interactive and can accommodate 500 to over 50,000 Learners. In 2020, over 500,000 Learners experienced over 3 million hours of free live online instruction, including classes taught by celebrity scientists, astronauts, and wildlife experts completely free of charge to Learners. In addition, Nerdy’s library of hundreds of thousands of resources, including online adaptive diagnostic tests and practice problems, are offered completely free for Learners. Our free content helps attract new users to our platform and complements our paid product offerings by increasing retention of our existing users.

one-on-one

2

Our platform and multiple learning formats allow us to deliver value in more ways and establish lasting relationships between Learners and Experts. This generates powerful network effects in our business: high customer satisfaction attracts more Learners to our platform which in turn attracts more Experts as well. Our business has delivered growth and healthy unit economics.

Active Learner growth is up 80% for the three months ended June 30, 2021 compared to the same period in 2020, while paid online sessions have grown 109% in the same time frame. Active Learner growth is up 67% for the six months ended June 30, 2021, while paid online sessions have grown 142% in the same time frame. For the year ended December 31, 2020, Active Learners increased by 37% from approximately 63 thousand in 2019 to approximately 87 thousand in 2020, while paid online sessions increased by 103% in the same time frame from 549 thousand to 1.1 million sessions.

Revenue during the three months ended June 30, 2021 increased $11.2 million from $21.6 million to $32.8 million, or 52%, compared to the prior year period. Revenue during the six months ended June 30, 2021 increased $22.8 million from $44.6 million to $67.4 million, or 51%, compared to the prior period, due to increased online revenue, which was partially offset by a decline in instruction and small group classes, as well as free services including large format group classes, and adaptive self-study together into a single comprehensive learning destination. These initiatives resulted in revenue growth throughout the second half of 2020 which continued through the three and six months ended June 30, 2021. Revenue for the year ended December 31, 2020 increased $13.5 million from $90.5 million to $104.0 million, or 15% compared to the same period in 2019. Online revenue increased by $33.1 million from approximately $64.4 million in the year ended December 31, 2019 to approximately $97.4 million in the year ended December 31, 2020, an increase of 51% year-over-year.

in-person

revenues. In the first half of 2020, the COVID-19

pandemic and the resulting closure of schools and testing centers significantly negatively impacted revenue. We completed the transition to delivering live instruction 100% online in April 2020. The Company scaled and integrated several new services, including one-on-one

Gross margins of 65% in the three months ended June 30, 2021, remained flat at 65% compared to the same period in 2020. Gross margins of 66% in the six months ended June 30, 2021, increased by 2% compared to the same period in 2020. Gross margin increases as the result of increased adoption of our online products were partially offset by lower than expected expirations of hours purchased by Learners and increased capitalized software amortization costs. For the year ended December 31, 2020, gross margins increased to 66.5% from 65.9% in the year ended December 31, 2019. Margin expansion for the year ended December 31, 2020 was primarily driven by increased adoption of our online services.

We experienced net loss of $0.3 million in the three months ended June 30, 2021 as compared to a net loss of $4.1 million in the same period in 2020. Net loss for the six months ended June 30, 2021 was $6.1 million compared to the $12.1 million in the same period in 2020. Net loss in the year ended December 31, 2020 was $24.7 million, compared to a net loss of $22.4 million in the same period in 2019.

Our Market Opportunity

A recent industry report estimates that the global market for supplemental education in 2020 is estimated to be $1.3 trillion, excluding government-funded education. GSV Ventures estimates that online penetration of this market is expected to grow 5 fold over the next seven years, which represents a CAGR of 30%, providing significant macroeconomic tailwinds for our business.

COVID-19

has further highlighted the need for consumers to take ownership of their own education. We believe these trends will persist past COVID-19,

as a November 2020 survey of 1,000 parents of K-12

students conducted by a third-party indicated that those consumers are 70% more likely to use online learning than they were a year ago, and 83% of consumers report that they plan to continue using online learning going forward. 3

The market for learning is large, fragmented, and ripe for disruption. We believe that inefficiencies in traditional learning total addressable market was approximately $47 billion in 2019 and will grow to approximately $62 billion by 2024. We believe that a significant portion of our market opportunity is currently being served by traditional

direct-to-consumer

in-person

learning models have created a significant opportunity for online learning platforms. We estimate our U.S. direct-to-consumer

in-person

learning models but is rapidly transitioning online. We view our market opportunity across a handful of major categories: | • | Academic Tutoring: Academic Tutoring Academic Tutoring |

| • | Test Preparation: Test Preparation Test Preparation |

| • | Professional Certifications, Training, & Skills: Professional Certifications, Training, & Skills |

| • | Other Education: Other Education non-academic segments such as enrichment, visual arts, and technology. The size of this market in the US is estimated to be $5.8 billion in 2019 and is projected to grow to $6.9 billion by 2024, according to IBISWorld research from June 2020. |

Our Competitive Strengths

Innovative highly scalable technology platform purpose-built for online learning.

We have built our proprietary technology platform from the ground up with the purpose of transforming how people learn. We leverage AI and process automation to scale high quality, live instruction, and our platform is designed to optimize online Learner-Expert interactions through tech-enabled features. Our platform is built to scale quickly to accommodate high volumes, and the rapid introduction of new learning formats and subjects. In the second quarter of 2021, our platform hosted 468 thousand online sessions, serving 54 thousand Active Learners, representing 109% and 80% year-over-year growth, respectively. For the six months ended June 30, 2021, our platform hosted 945 thousand online sessions, serving 73 thousand Active Learners, representing 142% and 67% year-over-year growth, respectively. Our recently introduced large classes format served over 500,000 Active Learners in 2020. We believe our highly scalable platform provides us with opportunities to continue to grow with relatively low capital expenditure requirements.

Trusted online learning destination with a leading consumer brand

We provide an engaging and enjoyable learning experience for both our Learners and the Experts, as reflected in our Net Promoter Score of 68 and average

all-time

session rating of 4.9 out of 5.0 for each quarter in 2020. The engagement of Experts on the platform is growing, demonstrated by the increase in paid sessions per Active Expert in the three and six months ended June 30, 2021 of 31% and 59%, respectively, compared to the same period in 2020. Our high-quality free large class format drives incremental traffic, brand awareness, and engagement on our platform. Our aided brand awareness is rapidly increasing, growing from 31% in 2019 to 64% in 2020 based on a survey of 1,000 parents of K-12

learners conducted by a third party. As a result of our 4

commitment to quality, we have become a trusted online learning destination with 90% of Learners believing Varsity Tutors offers high quality instruction and 87% believing Varsity Tutors is a brand they can trust based on a November 2020 survey of current and past Nerdy Learners.

Strong unit economics

We generate revenue from our Learner’s consumption of paid online sessions across both instruction and group classes. In 2020, we generated approximately $1,100 per Active Learner. As a result, our customers are profitable on their first package purchase, unlike many other

one-on-one

gig-economy

business models that depend on substantial retention before an individual customer is profitable. Additional formats and our adaptive self-study capability provide the opportunity to consume more free and paid resources through our platform, which has proven to even further extend the lifetime value of our Learners. Superior learning experience powered by a rich dataset

As a result of our online model, we are able to instrument and capture a rich dataset that we utilize to enhance the learning experience throughout the customer journey, which also creates a data driven competitive advantage that would be hard for competitors to replicate. We leverage AI and process automation to rigorously identify and vet highly qualified Experts to ensure high quality instruction at scale is consistently delivered to Learners. Our AI powered proprietary matching algorithm analyzes over 100 attributes per Learner and Expert to identify the matches with the highest projected probability of a successful interaction. Our data asset grows more valuable as the platform scales, allowing us to better leverage the growing dataset of learning interactions to better personalize the Learner experience. We are leveraging software and AI to scale personalized learning in a way that we believe is unparalleled and nearly impossible to replicate via an antiquated

direct-to-consumer

Learner-to-Expert

in-person

model. Founder-led,

seasoned management team We are a company of thinkers, builders, and innovators with a passion for learning. Our management team brings extensive technology, consumer brand, and

e-commerce

experience and, together with our founder, are deeply passionate about transforming how people learn through technology. We embrace diversity of experience, thought, and skill sets to ensure our team has complementary strengths to succeed in a rapidly evolving industry. Our Growth Strategy

We have multiple growth vectors that will enable us to further scale our platform by attracting and retaining more Learners and Experts through more deep and meaningful relationships.

Audience and subject expansion

As a leading provider of live, online learning and one of the largest platforms for live, online learning in the United States, we attract and help Learners across multiple audience segments and subjects.

direct-to-consumer,

We are continually investing in broadening our existing catalogue of over 3,000 subjects for audiences across the learning lifecycle, including live instruction solutions, as well as proprietary content used for adaptive self-study. Most recently, we have made investments to enter the learning market for professionals by expanding our subject coverage to include and group instruction for professional certifications. There is also considerable and relatively untapped opportunity to extend our platform to reach audiences beyond the United States. We believe that as our range of subjects offered and audiences served grows across learning categories, our market presence and brand recognition will expand, driving more Learners and Experts to our platform.

one-on-one

5

Learning formats expansion and class penetration

We’ve added several learning formats beyond instruction and are constantly exploring new methods of learning that will allow us to broaden our appeal to more Learners. As we continue to improve the breadth of our class products, including small group classes, make the class experience more immersive and interactive; add selection; and optimize pricing, we aim to grow the live class business in the coming years as we seek to penetrate this large and growing market. We have seen strong initial demand for live online classes and believe there is an opportunity to further monetize this learning format and expand gross margins.

one-on-one

Cross-sell existing Learners to new offerings and new learning formats

Our comprehensive learning platform provides an opportunity to engage Learners across multiple formats as we continue to expand beyond instruction to large group classes, small group classes, and self-study formats. Our platform has evolved from an episodic, needs-based solution to a continuous, multi-format, learning experience. As Learners diversify their experiences to meet more learning needs, multi-format engagement is driving recurring relationships and expanding revenue per Learner. Average revenue per Learner is more than 60% higher in the first year from Learners who use just one additional learning format beyond instruction, including free products. We believe our revenues will continue to increase as we further capitalize with our Learners by delivering great experiences through our free large classes and adaptive self-study tool, expanding subject coverage, increasing the number of learning formats, and improving the personalized learning experience on our platform.

one-on-one

one-on-one

Product innovation and expansion

We make continuous innovations to our technology that power meaningful improvements to the experiences for Learners and Experts. As we gain further scale, our ability to leverage data to infuse more personalization throughout the experience compounds. This leads to improved retention, monetization, and organically driven growth of new Learners and Experts using the platform. We continue to evolve and enhance our product experience to build relevance and find solutions to unmet needs across all of our audiences, which opens up new avenues for new growth and lifetime value expansion.

Targeted acquisitions

We intend to leverage our leadership position, deep experience in the sector, and the scale of our platform to opportunistically acquire businesses that unlock additional technology capabilities, and provide our Learners with transformative learning technologies that drive continuous improvements across our platform and the user experience.

6

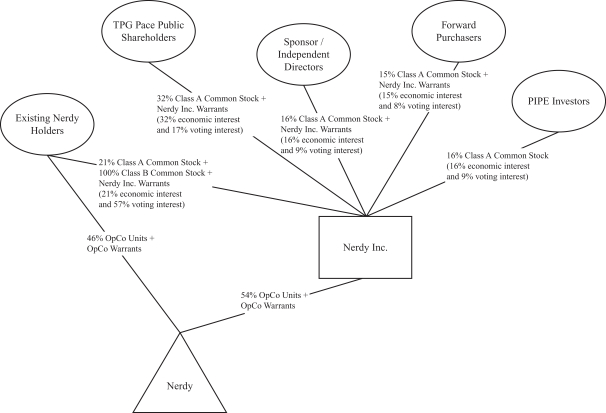

Organizational Structure

The following diagram illustrates the ownership structure of Nerdy Inc. immediately following the Closing. The equity interests shown in the diagram include (a) the 8,000,000 aggregate shares of Class A Common Stock or OpCo Units (with equivalent number of shares of Class B Common Stock) that comprise the Earnout Equity, which were issued and outstanding as of Closing, but subject to forfeiture and (b) any shares of Common Stock of Nerdy Inc. underlying vested and unvested stock appreciation rights and profit interest units held by the former Nerdy unit appreciation rights and profit interest units holders immediately following the Closing, which total 18,490,087 shares, consisting of 6,391,286 shares of Class A Common Stock for the stock appreciation rights of Nerdy Inc. and 12,098,801 shares of Class B Common Stock for the profit interest units of Nerdy Inc.

U.S. Federal Income Tax Considerations

For a discussion summarizing the U.S. federal income tax considerations of an investment in shares of Class A common stock, please see “.”

U.S. Federal Income Tax Considerations

Accounting Treatment

The Business Combination will be accounted for as a reverse recapitalization in conformity with accounting principles generally accepted in the United States of America (“GAAP”). Under this method of accounting, TPG Pace will be treated as the “acquired” company for financial reporting purposes. This determination was primarily based on Existing Nerdy Holders comprising a majority of the voting power of the combined company, Nerdy’s operations prior to the acquisition comprising the only ongoing operations of Nerdy Inc., and Nerdy’s senior management comprising a majority of the senior management of Nerdy Inc. Following the Transaction,

7

Nerdy LLC will be governed by a Board of Managers consisting of five Managers with three Managers designated by Nerdy Inc. and two Managers that were designated by the members holding a majority of the then outstanding vested units held by members other than Nerdy Inc. Under this method of accounting, the ongoing financial statements of the registrant will reflect the net assets of Nerdy and TPG Pace at historical cost, with no goodwill or other intangible assets recognized.

The Company is currently evaluating the appropriate accounting treatment related to the noncontrolling interest (“NCI”) associated with the outstanding Nerdy LLC units held by certain Existing Nerdy Holders. For purposes of the unaudited pro forma condensed combined financial information, the NCI has been classified as a component within temporary “mezzanine” equity. However, it is possible upon completion of the evaluation the NCI could be considered a component of permanent equity.

The Company is currently evaluating the accounting treatment related to certain warrants upon the close of the Transaction. For purposes of the unaudited pro forma condensed combined financial information, all warrants are classified as derivative liability instruments. However, the evaluation and finalization of accounting conclusions regarding the classification are ongoing and subject to change.

For purposes of the unaudited pro forma condensed combined financial information, all earnouts are classified as derivative liability instruments. Upon the close of the Transaction, certain earnouts were provided to employees of the Company. The Company is currently evaluating whether any of these earnouts represents compensation expense pursuant to Accounting Standards Codification (ASC) Topic 718, Compensation — Stock Compensation (“ASC 718”).

Sources of Industry and Market Data

Where information has been sourced from a third-party, the source of such information has been identified.

Unless otherwise indicated, the information contained in this Prospectus on the market environment, market developments, growth rates, market trends and competition in the markets in which we operate is taken from publicly available sources, including third-party sources, or reflects our estimates that are principally based on information from publicly available sources.

Risk Factor Summary

Our business is subject to numerous risks and uncertainties, including those highlighted in the section entitled “” immediately following this prospectus summary, that represent challenges that we face in connection with the successful implementation of our strategy and the growth of our business. In particular, the following considerations, among others, may offset our competitive strengths or have a negative effect on our business strategy, which could cause a decline in the price of shares of our common stock or warrants and result in a loss of all or a portion of your investment.

Risk Factors

Risks Related to Nerdy’s Business Model, Operations and Growth Strategy

| • | Nerdy has a limited operating history, which makes it difficult to predict future financial and operating results, and Nerdy may not achieve expected financial and operating results in the future. |

| • | Nerdy has incurred significant net losses since its formation, and its operating expenses are expected to increase significantly in the foreseeable future, which may make it more difficult to achieve and maintain profitability. |

| • | COVID-19 may materially and adversely affect Nerdy’s business and its financial results. |

8

| • | Nerdy contracts with some individuals and entities classified as independent contractors, not employees, and is subject to the federal laws and regulations, including but not limited to Internal Revenue Service regulations, and applicable state laws and regulations. |

| • | Nerdy’s business depends heavily on the adoption by new and existing customers of one-on-one |

| • | Nerdy did not design or maintain an effective control environment that meets its accounting and reporting requirements. |

| • | Nerdy faces various litigation risks which may be heightened by the fact that many users on its platform are minor children. |

| • | Attracting new Learners and Experts for existing offerings and the launch of new offerings is complex and time-consuming. |

| • | Nerdy faces competition from established as well as other emerging companies, which could result in pricing pressure or otherwise significantly reduce its revenue. |

| • | Nerdy could lose Learners, Experts, and employees, suffer economic and reputational harm, and/or be exposed to protracted and costly litigation if its security measures are breached or fail and result in unauthorized disclosure of data. |

| • | Nerdy relies on third party vendors, tools, and platforms including for services including and not limited to hosting, discovery, advertising, delivering content, and more. |

| • | Errors, defects, or disruptions in Nerdy’s platform could diminish its brand, subject it to liability, and materially and adversely affect its business, prospects, financial condition, and results of operations. |

| • | Computer malware, viruses, hacking, phishing attacks, and spamming could harm Nerdy’s business and results of operations. |

| • | Nerdy’s future products may not gain market acceptance. |

| • | The seasonality of Nerdy’s business. |

Risks Related to Regulations

| • | Any changes in laws or regulations relating to consumer data privacy or data protection or other laws applicable to Nerdy, or any actual or perceived failure by Nerdy to comply with such laws and regulations or its privacy policies. |

Risks Related to Intellectual Property

| • | Nerdy operates in an industry with extensive intellectual property litigation, and has been, and may be in the future, subject to claims related to a violation of third party’s intellectual property rights. Such claims against Nerdy or its important vendors and suppliers, even where meritless, can be costly to defend and may hurt Nerdy’s business, results of operations, and financial condition. |

| • | Failure to adequately protect Nerdy’s intellectual property and other proprietary rights could adversely affect its business, results of operations, and financial conditions. |

9

Risks Related to this Offering, Ownership of Class A Common Stock, and Nerdy Inc.’s Status as a Public Company

| • | Nerdy is an “emerging growth company” and as a result of the reduced disclosure and governance requirements applicable to emerging growth companies, Nerdy Inc.’s Class A Common Stock may be less attractive to investors. |

Risks Related to the Business Combination with TPG Pace