As filed with the Securities and Exchange Commission on August 1

1

, 2021 No. 333-254485

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

TO FORM

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter)

Cayman Islands* |

6770 |

98-1499860 | ||

(State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

301 Commerce St., Suite 3300

Fort Worth, TX 76102

Telephone: (212) 405-8458

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Jerry Neugebauer

c/o

TPG Pace Tech Opportunities Corp.

301 Commerce St., Suite 3300

Fort Worth, TX 76102

Telephone: (212) 405-8458

Facsimile: (512) 533-6601

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies of all communications, including communications sent to agent for service, should be sent to:

| Keith Fullenweider Sarah K. Morgan Vinson & Elkins L.L.P. 1001 Fannin St. Suite 2500 Houston, Texas 77002 (713) 758-2222 |

John M. Mutkoski Jocelyn M. Arel Goodwin Procter LLP 100 Northern Avenue Boston, Massachusetts 02210 Tel: (617) 570-1000 |

Approximate date of commencement of proposed sale to the public:

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a

non-accelerated

filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2

of the Exchange Act. | Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

Non-accelerated filer |

☒ | Smaller reporting company | ||||

| Emerging growth company | ||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule

13e-4(i)

(Cross-Border Issuer Tender Offer) ☐ Exchange Act Rule

14d-l(d)

(Cross-Border Third-Party Tender Offer) ☐ The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the registration statement shall become effective on such date as the SEC, acting pursuant to Section 8(a), may determine.

The information in this preliminary proxy statement/prospectus is not complete and may be changed. The registrant may not sell the securities described in this preliminary proxy statement/prospectus until the registration statement filed with the Securities and Exchange Commission is declared effective. This preliminary proxy statement/prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY—SUBJECT TO COMPLETION, DATED AUGUST 11, 2021

PROXY STATEMENT FOR

EXTRAORDINARY GENERAL MEETING OF TPG PACE TECH OPPORTUNITIES CORP.

TPG PACE TECH OPPORTUNITIES CORP.

301 Commerce Street, Suite 3300

Fort Worth, Texas 76102

Dear TPG Pace Tech Opportunities Corp. Shareholders:

You are cordially invited to attend an extraordinary general meeting of the shareholders of TPG Pace Tech Opportunities Corp., an exempted company incorporated in the Cayman Islands (“TPG Pace”), which will be held on , 2021 at local time at the offices of Vinson & Elkins L.L.P., located at 1114 Avenue of the Americas, 32

nd

Floor, New York, NY 10036 and virtually pursuant to the procedures described in the accompanying proxy statement/prospectus (the “extraordinary general meeting”). The extraordinary general meeting has been called to approve, among other things, the Business Combination (as defined below) between TPG Pace and Live Learning Technologies LLC, a Missouri limited liability company (“Nerdy”). As used in the accompanying proxy statement/prospectus, “OpCo” refers to Nerdy following the Merger (as defined below). As further described in the accompanying proxy statement/prospectus, pursuant to the Domestication (as defined below), on the Closing Date (as defined below), prior to the Effective Time (as defined in the Business Combination Agreement), TPG Pace will become a Delaware corporation named “Nerdy Inc.” As part of the Domestication, the outstanding Class A ordinary shares of TPG Pace (the “Class A Shares”) and Class F ordinary shares of TPG Pace (the “Founder Shares” and, together with the Class A Shares, the “TPG Pace ordinary shares”) will convert into common stock of Nerdy Inc. in the manner described further below. In addition, the warrants of TPG Pace will become warrants to purchase Class A Common Stock of Nerdy Inc. In connection with the Domestication, Nerdy Inc. will be governed by materially different governance documents than TPG Pace. See “” in the accompanying proxy statement/prospectus for more information. As used in the accompanying proxy statement/prospectus, “Nerdy Inc.” refers to TPG Pace after giving effect to the Domestication and the Business Combination.

Comparison of Corporate Governance and Shareholder Rights

At the extraordinary general meeting, TPG Pace shareholders will be asked to consider and vote upon a proposal, which is referred to herein as the “Business Combination Proposal” to approve and adopt the Business Combination Agreement (and the transactions contemplated thereby, the “Business Combination”) dated as of January 28, 2021 (as amended on March 19, 2021, on July 14, 2021 and on August 11, 2021 and as may be amended, supplemented or otherwise modified from time to time, the “Business Combination Agreement”), by and among TPG Pace, TPG Pace Tech Merger Sub LLC, a Delaware limited liability company (“TPG Pace Merger Sub”), TCV VIII (A) VT, Inc., a Delaware corporation (“TCV Blocker”), LCSOF XI VT, Inc., a Delaware corporation (“Learn Blocker” and, together with TCV Blocker, the “Blockers”), TPG Pace Blocker Merger Sub I Inc., a Delaware corporation (“Blocker Merger Sub I”), TPG Pace Blocker Merger Sub II Inc., a Delaware corporation (“Blocker Merger Sub II” and, together with Blocker Merger Sub I, the “Blocker Merger Subs” and, together with TPG Pace Merger Sub, the “Merger Subs”), Nerdy, and, solely for the purposes described therein, certain entities affiliated with the Blockers, a copy of which is attached to the accompanying proxy statement/prospectus as Annex

A-I,

A-II, A-III and A-IV, including the transactions contemplated thereby. As described in further detail below, the aggregate consideration to be paid to the holders of Nerdy equity (including the owners of the Blockers with respect to their indirect interest in Nerdy equity and the holders of Nerdy unit appreciation rights and profit units, collectively, the “Existing Nerdy Holders”) will be based on an enterprise value of $1,250,000,000 (subject to certain debt related adjustments) and shall consist of (i) an amount of cash equal to the excess of the amount of Available Cash (as defined in the accompanying proxy statement/prospectus) over $250,000,000 (but not to exceed $388,200,000), (ii) equity consideration valued at $10.00 per share/unit in respect of the remaining portion of Nerdy’s enterprise value after deducting the cash consideration in clause (i), (iii) certain Nerdy warrants (iv) the Nerdy Earnout Consideration (as defined herein).

plus

plus

plus

The Business Combination is being accomplished through what is commonly referred to as an

“Up-C”

structure, which is often used by partnerships and limited liability companies undertaking an initial public offering. The ” and “”

Up-C

structure allows the Existing Nerdy Holders (other than the owners of the Blockers) to retain their equity ownership in Nerdy, an entity that is classified as a partnership for U.S. federal income tax purposes, in the form of OpCo Units (as defined below) and OpCo warrants (as defined below). Immediately following the Closing, Existing Nerdy Holders are expected to own approximately 40% of the OpCo Units. Following the completion of the Business Combination, holders of OpCo Units (other than Nerdy Inc.) will, subject to certain limitations, have the right to cause OpCo to acquire all or a portion of their OpCo Units and corresponding shares of Class B Common Stock (as defined below) for Class A Common Stock (as defined below), subject to Nerdy Inc.’s right to acquire each tendered OpCo Unit directly from such holder for Class A Common Stock or an equivalent amount of cash. These acquisitions of OpCo Units will provide potential future tax benefits for Nerdy Inc. (a substantial portion of which Existing Nerdy Holders that are parties to the Tax Receivable Agreement will benefit from pursuant to the Tax Receivable Agreement). For more information, please see “Business Combination Proposal—Related Agreements—

OpCo

LLC Agreement

Business Combination Proposal—Related Agreements—Tax Receivable

Agreement.

As further described in the accompanying proxy statement/prospectus, subject to the terms and conditions of the Business Combination Agreement, the Business Combination and related transactions will be accomplished as follows:

| (a) | On the date of the transactions contemplated by the Business Combination Agreement (the “Closing Date”), prior to the Effective Time (as defined in the Business Combination Agreement), (i) TPG Pace will become a Delaware corporation (the “Domestication”) with the name “Nerdy Inc.” (for further details, see “ Proposal No. 2—The Domestication Proposal |

| (b) | TPG Pace Merger Sub will merge with and into Nerdy (the “Merger”), with Nerdy surviving the Merger. Pursuant to the Merger, (i) each holder of Nerdy common units (other than the Blockers) will exchange its Nerdy common units for (A) certain cash consideration, (B) certain limited liability company units in Nerdy (“OpCo Units”) and an equivalent number of shares of Nerdy Inc.’s Class B common stock (“Class B Common Stock”) and (C) certain Nerdy warrants and (ii) each holder of Nerdy unit appreciation rights will exchange all such unit appreciation rights for (1) corresponding stock appreciation rights in Nerdy Inc. or (2) certain cash consideration. The holders of Nerdy common units (other than the Blockers) will also receive the rights set forth in the Tax Receivable Agreement. In lieu of receiving OpCo Units and a corresponding number of shares of Class B Common Stock, each holder of Nerdy common units (other than the Blockers) may elect to receive shares of Nerdy Inc.’s Class A common stock (“Class A Common Stock” and, together with Class B Common Stock, “Common Stock”). |

| (c) | (i) Simultaneously with the Merger, through a series of separate merger transactions, the Blockers will merge with Nerdy Inc. (the “Blocker Mergers”), with Nerdy Inc. surviving the Blocker Mergers. In the Blocker Mergers, each holder of equity interests in the Blockers will exchange such equity interests for (A) certain cash consideration, (B) certain shares of Class A Common Stock and (C) certain Nerdy Inc. warrants. The Blocker Mergers are structured as separate mergers so as to effect such mergers in a tax-efficient manner. |

| (d) | Immediately following the Blocker Mergers and in connection with the Closing of the Business Combination (the “Closing”), Nerdy Inc. will contribute all of its assets (other than the OpCo Units it then holds and amounts necessary to fund any shareholder redemptions), which will consist of the amount of funds contained in TPG Pace’s trust account (net of any shareholder redemption amounts and including the net cash proceeds to TPG Pace resulting from the Subscription Agreements (as defined below) and the Forward Purchase Agreements (as defined below)) (collectively, “Available Cash”) less the cash consideration paid to Nerdy equity holders, to OpCo in exchange for a number of additional OpCo Units and a number of warrants to purchase OpCo Units (“OpCo warrants”), such that Nerdy Inc. will hold a number of OpCo Units equal to the total number of shares of Class A Common Stock and a number of OpCo warrants equal to the total number of Nerdy Inc. warrants, in each case, issued and outstanding immediately after giving effect to the Business Combination. The amount of |

| cash to be contributed by Nerdy Inc. to OpCo at the Closing of the Business Combination is estimated to be approximately $266 million, assuming no redemptions by TPG Pace shareholders. |

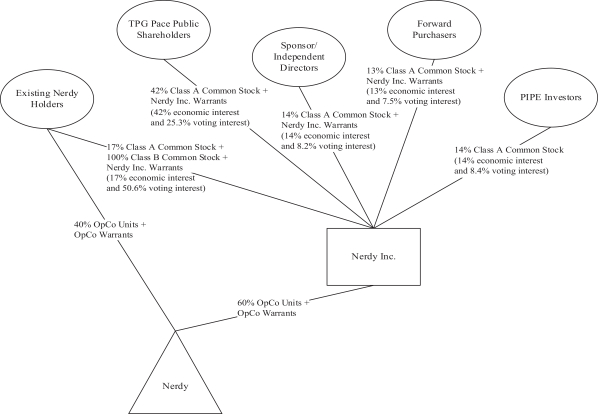

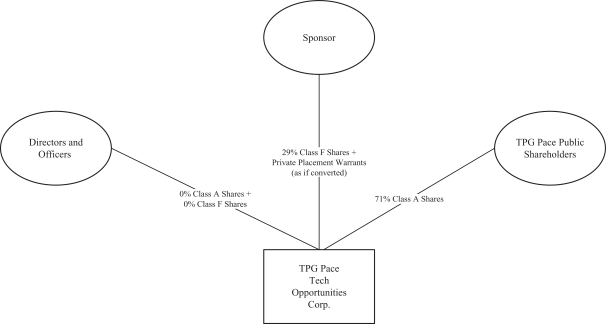

Upon the Closing, Existing Nerdy Holders are expected to hold an aggregate of 90,184,678 shares of Common Stock, including (i) 18,208,679 shares of Class A Common Stock and (ii) 71,975,999 shares of Class B Common Stock (and a number of OpCo Units corresponding to this number of shares of Class B Common Stock). In addition, the Existing Nerdy Holders will be issued (i) 417,240 Nerdy Inc. warrants and (ii) 2,027,204 OpCo warrants. As described above, the Business Combination is being accomplished through an

“Up-C”

structure and the type and mix of consideration received by the Existing Nerdy Holders reflects the implementation of such structure. Following the Closing and based on the assumptions set forth in the No Redemption Scenario, the Existing Nerdy Holders are expected (i) to own approximately 51% of the Common Stock of Nerdy Inc., comprised of approximately 17% of the outstanding Class A Common Stock and 100% of the outstanding Class B Common Stock, (ii) to own 13% of the outstanding aggregate warrants, including 100% of the OpCo warrants and 2% of the Nerdy Inc. warrants, and (iii) to receive approximately $388.2 million of cash consideration, assuming no redemptions by TPG Pace shareholders. For a summary of the assumptions surrounding the ownership percentages in the foregoing, please see “— ” As a result, the Existing Nerdy Holders will collectively have effective control over the management and decision-making of Nerdy Inc. following the Business Combination. For a diagram showing the expected post-closing corporate structure, please see the section entitled “—” on page 7 of the accompanying proxy statement.

Questions and Answers

For

Shareholders of TPG Pace

What will the Existing Nerdy Holders receive in the Business Combination with TPG Pace?

Summary of the Proxy Statement

Organizational Structure

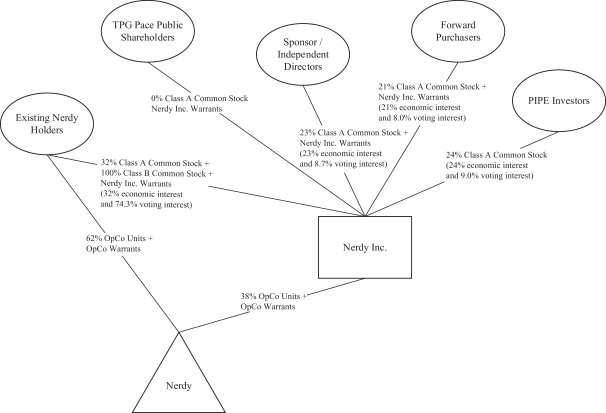

In the event that the level of redemptions by TPG Pace shareholders is at or exceeds 23,511,904 shares, or 52.2% of the public shares, Nerdy Inc. will have a minority interest in Nerdy LLC and Nerdy Inc. will not have the right to appoint a majority of the Board of Managers. If that is the case, Nerdy Inc. would account for the proposed business combination as an equity investment, which would result in Nerdy Inc. including the summarized financial information of Nerdy LLC within its periodic financial statements on Form 10-Q and include the separate financial statements of Nerdy LLC as an exhibit to Form 10-K. In such a scenario, Nerdy Inc. will not have control under US GAAP over Nerdy LLC and the operations of Nerdy LLC will not be reflected in the individual income and expense line items in Nerdy Inc.’s consolidated financial statements. For more information regarding our post-combination capital structure and pro forma financial information assuming a maximum redemption scenario, see the section entitled “”

Unaudited Pro Forma Condensed Combined Financial Information.

Concurrently with the execution of the Business Combination Agreement, TPG Pace entered into subscription agreements (the “Subscription Agreements”) with certain investors, pursuant to which such investors agreed to purchase, and TPG Pace agreed to issue and sell to such investors, newly issued shares of Class A Common Stock at a purchase price of $10.00 per share for gross proceeds of approximately $150 million, which purchase and sale will be consummated concurrently with the Business Combination (the “PIPE Financing”). In addition, pursuant to the Forward Purchase Agreements (as defined herein), TPG Pace has agreed to issue an aggregate of 16,116,750 shares of Class A Common Stock and 3,000,000 warrants to purchase Class A Common Stock to certain accredited investors, including but not limited to, affiliates of TPG Pace for an aggregate of $150 million. For more information, please see “.”

Business Combination Proposal—Related Agreements—Forward Purchase

Agreements

You will also be asked to consider and vote upon (a) a proposed certificate of incorporation of Nerdy Inc. to be effective after giving effect to the Domestication, a copy of which is attached as Annex C to this proxy statement/prospectus (such proposal the “Charter Proposal”), (b) on a

non-binding

advisory basis, six (6) separate proposals to approve material differences between TPG Pace’s existing amended and restated memorandum and articles of association and the proposed certificate of incorporation of Nerdy Inc. and the proposed bylaws of Nerdy Inc. upon the Domestication, copies of which are attached to the accompanying proxy statement/prospectus as Annexes C and D, respectively, which are referred to herein collectively as the “Governing Documents Proposals,” (c) a proposal to approve the election of two directors to serve until the 2022 annual meeting of stockholders, two directors to serve until the 2023 annual meeting of stockholders and three directors to serve until the 2024 annual meeting of stockholders, which is referred to as the “Director Election Proposal,” (d) a proposal to approve, for purpose of complying with provisions of Section 312.03 of The New York Stock Exchange’s (“NYSE”) Listed Company Manual, the issuance of Class A Common Stock in connection with the Business Combination, including, without limitation, to the investors in the PIPE Financing and the forward purchases, which is referred to herein as the “NYSE Proposal,” (e) a proposal to approve and adopt the Equity Incentive Plan, a copy of which is attached to the accompanying proxy statement/prospectus as Annex K, which is referred to herein as the “Equity Incentive Plan Proposal,” and (f) a proposal to adjourn the extraordinary general meeting to a later date or dates to the extent necessary, which is referred to herein as the “Adjournment Proposal.”

The Business Combination will be consummated only if the Business Combination Proposal, the Domestication Proposal, the Charter Proposal, the Director Election Proposal, the Equity Incentive Plan Proposal and the NYSE Proposal (collectively, the “Condition Precedent Proposals”) are approved at the extraordinary general meeting. The Adjournment Proposal is not conditioned upon the approval of any other proposal, and the Governing Documents Proposals are being submitted for approval on a

non-binding

advisory basis. Each of these proposals is more fully described in the accompanying proxy statement/prospectus, which each shareholder is encouraged to read carefully and in its entirety. The Adjournment Proposal provides for a vote to adjourn the extraordinary general meeting to a later date or dates (A) to the extent necessary to ensure that any required supplement or amendment to the accompanying proxy statement/prospectus is provided to TPG Pace shareholders or, if as of the time for which the extraordinary general meeting is scheduled, there are insufficient TPG Pace ordinary shares represented (either in person, virtually, or by proxy) to constitute a quorum necessary to conduct business at the extraordinary general meeting, (B) in order to solicit additional proxies from TPG Pace shareholders in favor of one or more of the proposals at the extraordinary general meeting or (C) if TPG Pace shareholders have elected to redeem an amount of the Class A Shares issued as part of the units (“public shares”) in the initial public offering of TPG Pace (the “TPG Pace IPO”) such that the condition to consummation of the Business Combination that the aggregate cash proceeds to be received by TPG Pace from the trust account established at the consummation of the TPG Pace IPO (the “Trust Account”) in connection with the Business Combination, together with the aggregate gross proceeds from the PIPE Financing and the forward purchases, equal no less than $250,000,000 after deducting any amounts paid to TPG Pace shareholders that exercise their redemption rights in connection with the Business Combination would not be satisfied (such condition to the consummation of the Business Combination, the “Minimum Available Cash Condition”).

In connection with the Business Combination, certain related agreements have been, or will be entered into on or prior to the closing of the Business Combination, including the Subscription Agreements, the Transaction Support Agreement, the OpCo LLC Agreement, the Tax Receivable Agreement, the Stockholders’ Agreement, the Waiver Agreement and the Registration Rights Agreement (each as defined in the accompanying proxy statement/prospectus). See “” in the accompanying proxy statement/prospectus for more information.

Business Combination Proposal—Related Agreements

Pursuant to its amended and restated memorandum and articles of association, TPG Pace is providing its public shareholders with the opportunity to redeem all or a portion of their Class A Shares in connection with the Business Combination at .

a per-share price,

payable in cash, equal to the aggregate amount then on deposit in the Trust Account as of two business days prior to the consummation of the Business Combination, including interest earned on the funds held in the Trust Account and not previously released to TPG Pace to pay its taxes, divided by the number of then outstanding Class A Shares. The per-share

amount TPG Pace will pay to investors who properly redeem their shares will not be reduced by the deferred underwriting commission totaling $15,750,000 that TPG Pace will pay to the underwriters of the TPG Pace IPO or transaction expenses incurred in connection with the Business Combination. For illustrative purposes, based on the fair value of marketable securities held in the Trust Account of approximately $450 million as of December 31, 2020, the estimated per share redemption price would have been approximately $10.00. Public shareholders may elect to redeem their shares even if they vote for the Business Combination

A public shareholder, together with any of his, her or its affiliates or any other person with whom it is acting in concert or as a “group” (as defined under Section 13 of the Securities Exchange Act of 1934, as amended), will be restricted from redeeming in the aggregate his, her or its shares or, if part of such a group, the group’s

shares, in excess of 15% of the Class A Shares included in the units sold in the TPG Pace IPO without the prior consent of TPG Pace. Any beneficial holder of Class A Shares on whose behalf a redemption right is being exercised must identify itself to TPG Pace in connection with any redemption election in order to validly elect to redeem such Class A Shares. TPG Pace has no specified maximum redemption threshold under its amended and restated memorandum and articles of association, other than the aforementioned 15% threshold. Each redemption of Class A Shares by TPG Pace’s public shareholders will reduce the amount in the Trust Account.

The Business Combination Agreement provides that Nerdy’s obligation to consummate the Business Combination is conditioned on the amount in the Trust Account (net of the amount of any TPG Pace public shareholder redemptions) plus the net proceeds from the PIPE Financing and the forward purchases equaling or exceeding $250,000,000 as of the closing of the Business Combination. The conditions to closing in the Business Combination Agreement are for the sole benefit of the parties thereto and may be waived by such parties. If, as a result of redemptions of Class A Shares by holders of public shares and a failure to consummate the PIPE Financing and forward purchases, this condition is not met or is not waived, then Nerdy may elect not to consummate the Business Combination. In addition, in no event will TPG Pace redeem its Class A Shares in an amount that would cause its net tangible assets to be less than $5,000,001, as provided in TPG Pace’s amended and restated memorandum and articles of association and as required as a closing condition to each party’s obligation to consummate the Business Combination under the terms of the Business Combination Agreement. Holders of outstanding public warrants do not have redemption rights in connection with the Business Combination. Unless otherwise specified, the information in the accompanying proxy statement/prospectus assumes that no holders of public shares exercise their redemption rights with respect to their Class A Shares.

Chad Leat, Kathleen Philips, Wendi Sturgis and Kneeland Youngblood (the “TPG Pace Independent Directors,” and together with our Sponsor, the “TPG Pace Initial Shareholders”) as well as TPG Pace’s officers and other current directors, have agreed to waive their redemption rights with respect to any TPG Pace ordinary shares they may hold in connection with the consummation of the Business Combination, and the Founder Shares will be excluded from the pro rata calculation used to determine the

per-share

redemption price. Currently, the TPG Pace Initial Shareholders own 20% of the issued and outstanding TPG Pace ordinary shares. The TPG Pace Initial Shareholders and the other directors and officers of TPG Pace have agreed to vote any TPG Pace ordinary shares owned by them in favor of the Business Combination. The Founder Shares are subject to transfer restrictions. The amended and restated memorandum and articles of association of TPG Pace includes a conversion adjustment and such mechanic shall be applied so that following the automatic conversion of the Founder Shares at the time of the Domestication into an equivalent number of Nerdy Inc. Class F Common Stock (“Nerdy Inc. Founder Shares”), and upon the completion of the Business Combination, such Nerdy Inc. Founder Shares will convert into Class A Common Stock at a conversion rate that entitles the holders of such Founder Shares to continue to own, in the aggregate, 20% of the Class A Common Stock after giving effect to the PIPE Financing and the forward purchases, subject to the waivers of certain conversion rights pursuant to the Waiver Agreement. Such adjustment will apply in connection with the Business Combination with respect to shares of Class A Common Stock received following the Domestication. Pursuant to the Waiver Agreement, Sponsor and each holder of Founder Shares has agreed to waive this adjustment with respect to (i) the Class A Common Stock issued in the PIPE Financing and (ii) any shares in excess of an aggregate of 15,000,000 shares of Class A Common Stock issued pursuant to the Forward Purchase Agreements. As a result of such waiver, immediately following the closing of the Business Combination the TPG Pace Initial Shareholders will hold approximately 11% of the total number of Class A Common Stock outstanding. TPG Pace is providing the accompanying proxy statement/prospectus and accompanying proxy card to TPG Pace’s shareholders in connection with the solicitation of proxies to be voted at the extraordinary general meeting and at any adjournments of the extraordinary general meeting. Information about the extraordinary general meeting, the Business Combination and other related business to be considered by TPG Pace’s shareholders at the extraordinary general meeting is included in the accompanying proxy statement/prospectus.

Whether or not you plan to attend the extraordinary general meeting, all of TPG Pace’s shareholders are urged to read the accompanying proxy statement/prospectus, including the annexes and other documents referred to therein, carefully and in their entirety. You should also carefully consider the risk factors described in “

” beginning on page 59 of the accompanying proxy statement/prospectus.

After careful consideration, the board of directors of TPG Pace has unanimously approved the Business Combination Agreement and the transactions contemplated thereby, including the Merger, and unanimously recommends that shareholders vote “FOR” the adoption of the Business Combination Agreement and approval of the transactions contemplated thereby, including the Merger, and “FOR” all other proposals presented to TPG Pace’s shareholders in the accompanying proxy statement/prospectus. When you consider the recommendation of these proposals by the board of directors of TPG Pace, you should keep in mind that TPG Pace’s directors and officers have interests in the Business Combination that may conflict with your interests as a shareholder. See the section entitled “

Business Combination

Proposal—Interests of TPG Pace’s Directors and Executive Officers in the Business Combination

” in the accompanying proxy statement/prospectus for a further discussion of these considerations.

The approval of the Domestication Proposal and the Charter Proposal require a special resolution, being the affirmative vote of at least a

two-thirds

(2/3) majority of the votes cast by the holders of the issued TPG Pace ordinary shares present in person (including virtually) or represented by proxy at the extraordinary general meeting and entitled to vote on such matter. The approval of each of the Business Combination Proposal, the Director Election Proposal, the NYSE Proposal, the Equity Incentive Plan Proposal and the Adjournment Proposal requires an ordinary resolution, being the affirmative vote of at least a majority of the votes cast by the holders of the issued TPG Pace ordinary shares present in person (including virtually) or represented by proxy at the extraordinary general meeting and entitled to vote on such matter. Your vote is very important

. Whether or not you plan to attend the extraordinary general meeting, please vote as soon as possible by following the instructions in the accompanying proxy statement/prospectus to make sure that your shares are represented at the extraordinary general meeting. If you hold your shares in “street name” through a bank, broker or other nominee, you will need to follow the instructions provided to you by your bank, broker or other nominee to ensure that your shares are represented and voted at the extraordinary general meeting. The Business Combination will be consummated only if the Condition Precedent Proposals are approved at the extraordinary general meeting. Each of the Condition Precedent Proposals is cross-conditioned on the approval of each other. The Adjournment Proposal is not conditioned upon the approval of any other proposal set forth in this proxy statement/prospectus, and the Governing Documents Proposals are being submitted for approval on a

non-binding

advisory basis. We intend to offer an for updated information and information regarding the protocols for attending the meeting in person, if applicable. If you are to attend the extraordinary general meeting, please check our website ten days prior to the meeting date. If the extraordinary general meeting is postponed or adjourned, your proxy will still be valid and may be voted at the rescheduled meeting. You may change or revoke your proxy until it is voted. As always, we encourage you to vote your shares prior to the extraordinary general meeting.

in-person

attendance option for shareholders to attend the extraordinary general meeting in person. However, we are continuing to monitor the impacts of COVID-19.

In the event we believe it is not possible or advisable to hold the extraordinary general meeting in person, we will announce alternative arrangements for the meeting as promptly as practicable, which may include holding the meeting partially or solely by means of remote communication. Please monitor our website at https://www.tpg.com/pace-tech-opportunitiesIf you sign, date and return your proxy card without indicating how you wish to vote, your proxy will be voted FOR each of the proposals presented at the extraordinary general meeting. If you fail to return your proxy card or fail to instruct your bank, broker or other nominee how to vote, and do not attend the extraordinary general meeting in person, the effect will be that your shares will not be counted for purposes of determining whether a quorum is present at the extraordinary general meeting. If you are a shareholder of record and you attend the extraordinary general meeting and wish to vote in person, you may withdraw your proxy and vote in person.

TO EXERCISE YOUR REDEMPTION RIGHTS, YOU MUST DEMAND IN WRITING THAT YOUR PUBLIC SHARES ARE REDEEMED FOR A PRO RATA PORTION OF THE FUNDS HELD IN THE TRUST ACCOUNT AND TENDER YOUR SHARES TO TPG PACE’S TRANSFER AGENT AT LEAST TWO

BUSINESS DAYS PRIOR TO THE VOTE AT THE EXTRAORDINARY GENERAL MEETING. IN ORDER TO EXERCISE YOUR REDEMPTION RIGHT, YOU NEED TO IDENTIFY YOURSELF AS A BENEFICIAL HOLDER AND PROVIDE YOUR LEGAL NAME, PHONE NUMBER AND ADDRESS IN YOUR WRITTEN DEMAND. YOU MAY TENDER YOUR SHARES BY EITHER DELIVERING YOUR SHARE CERTIFICATE TO THE TRANSFER AGENT OR BY DELIVERING YOUR SHARES ELECTRONICALLY USING THE DEPOSITORY TRUST COMPANY’S DWAC (DEPOSIT WITHDRAWAL AT CUSTODIAN) SYSTEM. IF THE BUSINESS COMBINATION IS NOT COMPLETED, THEN THESE SHARES WILL BE RETURNED TO YOU OR YOUR ACCOUNT. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BANK OR BROKER TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR REDEMPTION RIGHTS.

On behalf of TPG Pace’s board of directors, I would like to thank you for your support and look forward to the successful completion of the Business Combination.

Sincerely,

Karl Peterson

Chairman of the Board of Directors

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES REGULATORY AGENCY HAS APPROVED OR DISAPPROVED THE TRANSACTIONS DESCRIBED IN THE ACCOMPANYING PROXY STATEMENT/PROSPECTUS, PASSED UPON THE MERITS OR FAIRNESS OF THE BUSINESS COMBINATION OR RELATED TRANSACTIONS OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE DISCLOSURE IN THE ACCOMPANYING PROXY STATEMENT/PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY CONSTITUTES A CRIMINAL OFFENSE.

The accompanying proxy statement/prospectus is dated , 2021 and is first being mailed to shareholders on or about , 2021.

TPG PACE TECH OPPORTUNITIES

301 Commerce Street, Suite 3300

Fort Worth, Texas 76102

NOTICE OF EXTRAORDINARY GENERAL MEETING

TO BE HELD ON , 2021

Dear TPG Pace Tech Opportunities Corp. Shareholders:

NOTICE IS HEREBY GIVEN that an extraordinary general meeting of the shareholders (the “extraordinary general meeting”) of TPG Pace Tech Opportunities Corp., a Cayman Islands exempted company (“TPG Pace”), will be held on , 2021 at local time at the offices of Vinson & Elkins L.L.P., located at 1114 Avenue of the Americas, 32

nd

Floor, New York, NY 10036. You are cordially invited to attend the extraordinary general meeting, which will be held for the following purposes: | • | Proposal No. 1—The Business Combination Proposal—RESOLVED plus plus plus |

| • | Proposal No. 2—The Domestication Proposal—RESOLVED de-registered in the Cayman Islands pursuant to article 47 of its articles of association and registered by way of continuation as a corporation under the laws of the state of Delaware (the “Domestication”) pursuant to Part XII of the Companies Law (Revised) of the Cayman Islands and Section 388 of the General Corporation Law of the State of Delaware and, immediately upon being de-registered in the Cayman Islands, TPG Pace be continued and domesticated as a corporation and, conditional upon, and with effect from, the registration of TPG Pace as a corporation in the State of Delaware, the name of TPG Pace be changed from “TPG Pace Tech Opportunities Corp.” to “Nerdy Inc.” (the “Domestication Proposal”). |

| • | Proposal No. 3—The Charter Proposal—RESOLVED |

| • | Governing Documents Proposals non-binding advisory basis, certain governance provisions in the Existing Governing Documents, and to approve the following material differences between the Existing Governing Documents and the Proposed Certificate of Incorporation and the proposed new bylaws, copies of which are attached to the proxy statement/prospectus as Annex C and Annex D, respectively (the “Proposed Bylaws” and, together with the Proposed Certificate of Incorporation, the “Proposed Governing Documents”), of Nerdy Inc. (such proposals, collectively, the “Governing Documents Proposals”): |

| • | Proposal No. 4—Governing Documents Proposal A—RESOLVED “Up-C” structure and (d) shares of preferred stock, par value $0.0001 per share, of Nerdy Inc., be approved. |

| • | Proposal No. 5—Governing Documents Proposal B—RESOLVED |

| • | Proposal No. 6—Governing Documents Proposal C—RESOLVED |

| • | Proposal No. 7—Governing Documents Proposal D—RESOLVED |

| • | Proposal No. 8—Governing Documents Proposal E—RESOLVED |

| • | Proposal No. 9—Governing Documents Proposal F—RESOLVED |

| (iii) adopting Delaware as the exclusive forum for certain stockholder litigation and the United States District Courts as the exclusive forum for litigation arising out of the federal securities laws, and (iv) removing certain provisions related to our status as a blank check company that will no longer be applicable upon consummation of the Business Combination, be approved. |

| • | Proposal No. 10—The Director Election Proposal—RESOLVED |

| • | Proposal No. 11—The NYSE Proposal—RESOLVED, |

| • | Proposal No. 12—The Equity Incentive Plan Proposal—RESOLVED |

| • | Proposal No. 13—The Adjournment Proposal—RESOLVED |

Each of the Business Combination Proposal, the Domestication Proposal, the Charter Proposal, the Director Election Proposal, NYSE Proposal and the Equity Incentive Plan Proposal is conditioned on the approval and adoption of each of the other Condition Precedent Proposals. The Adjournment Proposal is not conditioned upon the approval of any other proposal, and the Governing Documents Proposals are being submitted for approval on a

non-binding

advisory basis. These items of business are described in this proxy statement/prospectus, which we encourage you to read carefully and in its entirety before voting.

Only holders of record of ordinary shares at the close of business on , 2021 are entitled to notice of and to vote and have their votes counted at the extraordinary general meeting and any adjournment of the extraordinary general meeting.

This proxy statement/prospectus and accompanying proxy card is being provided to TPG Pace’s shareholders in connection with the solicitation of proxies to be voted at the extraordinary general meeting and at

any adjournment of the extraordinary general meeting.

Whether or not you plan to attend the extraordinary general meeting, all of TPG Pace’s shareholders are urged to read this proxy statement/prospectus, including the annexes and the documents referred to herein carefully and in their entirety. You should also carefully consider the risk factors described in “

Risk Factors

” beginning on page

59 of this proxy statement/prospectus.

After careful consideration, the board of directors of TPG Pace has unanimously approved the Business Combination Agreement and the transactions contemplated thereby, including the Merger, and unanimously recommends that shareholders vote “FOR” the adoption of the Business Combination Agreement and approval of the transactions contemplated thereby, including the Merger, and “FOR” all other proposals presented to TPG Pace’s shareholders in the accompanying proxy statement/prospectus. When you consider the recommendation of these proposals by the board of directors of TPG Pace, you should keep in mind that TPG Pace’s directors and officers have interests in the Business Combination that may conflict with your interests as a shareholder. See the section entitled “

Business Combination Proposal—Interests of TPG Pace’s Directors and Executive Officers in the Business Combination

” in the accompanying proxy statement/prospectus for a further discussion of these considerations.

Pursuant to its amended and restated memorandum and articles of association, TPG Pace is providing its public shareholders with the opportunity to redeem all or a portion of their Class A Shares in connection with the Business Combination at .

a per-share price,

payable in cash, equal to the aggregate amount then on deposit in the Trust Account as of two business days prior to the consummation of the Business Combination, including interest earned on the funds held in the Trust Account and not previously released to TPG Pace to pay its taxes, divided by the number of then outstanding Class A Shares. The per-share

amount TPG Pace will pay to investors who properly redeem their shares will not be reduced by the deferred underwriting commission totaling $15,750,000 that TPG Pace will pay to the underwriters of the TPG Pace IPO or transaction expenses incurred in connection with the Business Combination. For illustrative purposes, based on the fair value of marketable securities held in the Trust Account of approximately $450 million as of December 31, 2020, the estimated per share redemption price would have been approximately $10.00. Public shareholders may elect to redeem their shares even if they vote for the Business Combination

A public shareholder, together with any of his, her or its affiliates or any other person with whom it is acting in concert or as a “group” (as defined under Section 13 of the Securities Exchange Act of 1934, as amended), will be restricted from redeeming in the aggregate his, her or its shares or, if part of such a group, the group’s shares, in excess of 15% of the Class A Shares included in the units sold in the TPG Pace IPO without the prior consent of TPG Pace. Any beneficial holder of Class A Shares on whose behalf a redemption right is being exercised must identify itself to TPG Pace in connection with any redemption election in order to validly elect to redeem such Class A Shares. TPG Pace has no specified maximum redemption threshold under its amended and restated memorandum and articles of association, other than the aforementioned 15% threshold. Each redemption of Class A Shares by TPG Pace’s public shareholders will reduce the amount in the Trust Account.

The Business Combination Agreement provides that Nerdy’s obligation to consummate the Business Combination is conditioned on the amount in the Trust Account (net of the amount of any TPG Pace public shareholder redemptions) plus the net proceeds from the PIPE Financing and the forward purchases equaling or exceeding $250,000,000 as of the closing of the Business Combination. The conditions to closing in the Business Combination Agreement are for the sole benefit of the parties thereto and may be waived by such parties. If, as a result of redemptions of Class A Shares by holders of public shares and a failure to consummate the PIPE Financing and forward purchases, this condition is not met or is not waived, then Nerdy may elect not to consummate the Business Combination. In addition, in no event will TPG Pace redeem its Class A Shares in an amount that would cause its net tangible assets to be less than $5,000,001, as provided in TPG Pace’s amended and restated memorandum and articles of association and as required as a closing condition to each party’s obligation to consummate the Business Combination under the terms of the Business Combination Agreement. Holders of outstanding public warrants do not have redemption rights in connection with the Business Combination. Unless otherwise specified, the information in the accompanying proxy statement/prospectus assumes that no holders of public shares exercise their redemption rights with respect to their Class A Shares.

TPG Pace Tech Opportunities Sponsor, Series LLC, a Delaware limited liability company (our “Sponsor”), and Chad Leat, Kathleen Philips, Wendi Sturgis and Kneeland Youngblood (the “TPG Pace Independent Directors,” and together with our Sponsor, the “TPG Pace Initial Shareholders”), as well as TPG Pace’s officers and other current directors, have agreed to waive their redemption rights with respect to any TPG Pace ordinary shares they may hold in connection with the consummation of the Business Combination, and the Founder Shares (as defined below) will be excluded from the pro rata calculation used to determine the

per-share

redemption price. Concurrently with the execution of the Business Combination Agreement, TPG Pace entered into subscription agreements (the “Subscription Agreements”) with certain investors, pursuant to which such investors agreed to purchase, and TPG Pace agreed to issue and sell to such investors, newly issued shares of Class A Common Stock at a purchase price of $10.00 per share for gross proceeds of approximately $150 million, which purchase and sale will be consummated concurrently with the Business Combination (the “PIPE Financing”). In addition, pursuant to the Forward Purchase Agreements (as defined herein), TPG Pace has agreed to issue an aggregate of 16,116,750 shares of Class A Common Stock and 3,000,000 warrants to purchase Class A Common Stock to certain accredited investors, including but not limited to, affiliates of TPG Pace for an aggregate of $150 million. For more information, please see “.”

Business Combination Proposal—Related Agreements—Forward Purchase Agreements

In connection with the Closing, each share of Class A Common Stock purchased in the PIPE Financing and each share of Class A Common Stock and forward purchase warrants purchased pursuant to the Forward Purchase Agreements will be exchanged for an equivalent number of securities of Nerdy Inc. The securities to be issued pursuant to the Subscription Agreements and Forward Purchase Agreements have not been registered under the Securities Act of 1933, as amended (the “Securities Act”), in reliance upon the exemption provided in Section 4(a)(2) of the Securities Act and/or Regulation D promulgated thereunder.

Holders must complete the procedures for electing to redeem their public shares in the manner described above prior to 5:00 p.m., Eastern Time, on , 2021 (two business days before the extraordinary general meeting) in order for their shares to be redeemed.

Holders of units must elect to separate the units into the underlying public shares and warrants prior to exercising redemption rights with respect to the public shares. If holders hold their units in an account at a brokerage firm or bank, holders must notify their broker or bank that they elect to separate the units into the underlying public shares and warrants, or if a holder holds units registered in its own name, the holder must contact Continental Stock Transfer & Trust Company (“Continental”), TPG Pace’s transfer agent, directly and instruct them to do so. The redemption rights include the requirement that a holder must identify itself in writing as a beneficial holder and provide its legal name, phone number and address to Continental in order to validly redeem its shares. Public shareholders may elect to redeem public shares regardless of if or how they vote in respect of the Business Combination Proposal. If the Business Combination is not consummated, the public shares will be returned to the respective holder, broker or bank. If the Business Combination is consummated, and if a public shareholder properly exercises its right to redeem all or a portion of the public shares that it holds and timely delivers its shares to Continental, TPG Pace’s transfer agent, TPG Pace will redeem such public shares for a ” in this proxy statement/prospectus for a detailed description of the procedures to be followed if you wish to redeem your public shares for cash.

per-share

price, payable in cash, equal to the pro rata portion of Trust Account, calculated as of two business days prior to the consummation of the Business Combination. For illustrative purposes, as of December 31, 2020, this would have amounted to approximately $10.00 per issued and outstanding public share. If a public shareholder exercises its redemption rights in full, then it will be electing to exchange its public shares for cash and will no longer own public shares. The redemption will take place following the Domestication and, accordingly, it is shares of Class A Common Stock that will be redeemed immediately after consummation of the Business Combination. See “Extraordinary General Meeting of TPG Pace —Redemption Rights

The Business Combination Agreement is subject to the satisfaction or waiver of certain other closing conditions as described in the accompanying proxy statement/prospectus. There can be no assurance that the parties to the Business Combination Agreement would waive any such provision of the Business Combination Agreement.

The approval of each of the Domestication Proposal and Charter Proposal requires a special resolution, being the affirmative vote of at least a

two-thirds

(2/3) majority of the votes cast by the holders of the issued ordinary shares present in person (or virtually) or represented by proxy at the extraordinary general meeting and entitled to vote on such matter. The approval of each of the Business Combination Proposal, the Director Election Proposal, the NYSE Proposal, the Equity Incentive Plan Proposal and the Adjournment Proposal requires an ordinary resolution, being the affirmative vote of at least a majority of the votes cast by the holders of the issued ordinary shares present in person (or virtually) or represented by proxy at the extraordinary general meeting and entitled to vote on such matter. Your vote is very important

non-binding

advisory basis. If you sign, date and return your proxy card without indicating how you wish to vote, your proxy will be voted FOR each of the proposals presented at the extraordinary general meeting. If you fail to return your proxy card or fail to instruct your bank, broker or other nominee how to vote, and do not attend the extraordinary general meeting in person, the effect will be that your shares will not be counted for purposes of determining whether a quorum is present at the extraordinary general meeting. If you are a shareholder of record and you attend the extraordinary general meeting and wish to vote in person, you may withdraw your proxy and vote in person.

Your attention is directed to the remainder of the proxy statement/prospectus following this notice (including the Annexes and other documents referred to herein) for a more complete description of the proposed Business Combination and related transactions and each of the proposals. You are encouraged to read this proxy statement/prospectus carefully and in its entirety, including the Annexes and other documents referred to herein. If you have any questions or need assistance voting your ordinary shares, please contact Morrow Sodali LLC, our proxy solicitor, by calling (800)

662-5200,

or banks and brokers can call collect at (203) 658-9400,

or by emailing pace.info@investor.morrowsodali.com. Thank you for your participation. We look forward to your continued support.

By Order of the Board of Directors of TPG Pace Tech Opportunities Corp.,

Karl Peterson

Chairman of the Board of Directors

TO EXERCISE YOUR REDEMPTION RIGHTS, YOU MUST DEMAND IN WRITING THAT YOUR PUBLIC SHARES ARE REDEEMED FOR A PRO RATA PORTION OF THE FUNDS HELD IN THE TRUST ACCOUNT AND TENDER YOUR SHARES TO TPG PACE’S TRANSFER AGENT AT LEAST TWO BUSINESS DAYS PRIOR TO THE VOTE AT THE EXTRAORDINARY GENERAL MEETING. IN ORDER TO EXERCISE YOUR REDEMPTION RIGHT, YOU NEED TO IDENTIFY YOURSELF AS A BENEFICIAL HOLDER AND PROVIDE YOUR LEGAL NAME, PHONE NUMBER AND ADDRESS IN YOUR WRITTEN DEMAND. YOU MAY TENDER YOUR SHARES BY EITHER DELIVERING YOUR SHARE CERTIFICATE TO THE TRANSFER AGENT OR BY DELIVERING YOUR SHARES ELECTRONICALLY USING THE DEPOSITORY TRUST COMPANY’S DWAC (DEPOSIT WITHDRAWAL AT CUSTODIAN) SYSTEM. IF THE BUSINESS COMBINATION IS NOT COMPLETED, THEN THESE SHARES WILL BE RETURNED TO YOU OR YOUR ACCOUNT. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BANK OR BROKER TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR REDEMPTION RIGHTS.

TABLE OF CONTENTS

Page |

||||

| iii | ||||

| iii | ||||

| iii | ||||

| x | ||||

| xii | ||||

| 1 | ||||

| 58 | ||||

| 59 | ||||

| 115 | ||||

| 124 | ||||

| 169 | ||||

| 173 | ||||

| 174 | ||||

| 177 | ||||

| 179 | ||||

| 181 | ||||

| 183 | ||||

| 185 | ||||

| 187 | ||||

| 192 | ||||

| 194 | ||||

| 200 | ||||

| 202 | ||||

| 218 | ||||

| 253 | ||||

| 274 | ||||

| 282 | ||||

| 307 | ||||

| 326 | ||||

| 331 | ||||

| 336 | ||||

| 338 | ||||

| 342 | ||||

| 345 | ||||

| 357 | ||||

| 358 | ||||

i

| 359 | ||||

| 360 | ||||

| 360 | ||||

| 360 | ||||

| 360 | ||||

| 360 | ||||

| 361 | ||||

| F-1 | ||||

| A-I-1 | ||||

| A-II-1 | ||||

| A-III-1 | ||||

| ANNEX A-IV: THIRD AMENDMENT TO BUSINESS COMBINATION AGREEMENT | A-IV-1 | |||

| B-1 | ||||

| C-1 | ||||

| D-1 | ||||

| E-1 | ||||

| F-1 | ||||

| G-1 | ||||

| H-1 | ||||

| I-1 | ||||

| J-1 | ||||

| K-1 | ||||

| L-1 | ||||

| M-I-1 | ||||

| M-II-1 |

ii

ADDITIONAL INFORMATION

You may request copies of this proxy statement/prospectus and any other publicly available information concerning TPG Pace, without charge, by written request to TPG Pace Tech Opportunities Corp., 301 Commerce Street, Suite 3300, Fort Worth, Texas 76102, or by telephone request at (212) .

405-8458;

or Morrow Sodali LLC, our proxy solicitor, by calling (800) 662-5200,

or banks and brokers can call collect at (203) 658-9400,

or by emailing pace.info@investor.morrowsodali.com or from the SEC through the SEC website at http://www.sec.gov

In order for TPG Pace’s shareholders to receive timely delivery of the documents in advance of the extraordinary general meeting of TPG Pace to be held on , 2021, you must request the information no later than five business days prior to the date of the extraordinary general meeting, by , 2021.

TRADEMARKS

This document contains references to trademarks, trade names and service marks belonging to other entities. Solely for convenience, trademarks, trade names and service marks referred to in this proxy statement/prospectus may appear without the

®

or TM symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies. SELECTED DEFINITIONS

Unless otherwise stated in this proxy statement/prospectus or the context otherwise requires, references to:

| • | “additional forward purchasers” means third party purchasers not affiliated with TPG Global who commit to purchase securities under the Forward Purchase Agreements; |

| • | “amended and restated memorandum and articles of association” means the amended and restated memorandum and articles of association of TPG Pace, effective October 6, 2020; |

| • | “Available Cash” means as of the closing, the amount of funds contained in TPG Pace’s trust account (net of any shareholder redemption amounts) plus the net cash proceeds to TPG Pace resulting from the Subscription Agreements and the Forward Purchase Agreements; |

| • | “Blocker Merger Sub I” means TPG Pace Blocker Merger Sub I Inc., a Delaware corporation and wholly owned subsidiary of TPG Pace; |

| • | “Blocker Merger Sub II” means TPG Pace Blocker Merger Sub II Inc., a Delaware corporation and wholly owned subsidiary of TPG Pace; |

| • | “Blocker Merger Subs” means Blocker Merger Sub I and Blocker Merger Sub II; |

| • | “Blockers” means TCV Blocker and Learn Blocker; |

| • | “Business Combination Agreement” means that certain Business Combination Agreement, dated January 28, 2021, by and among TPG Pace, TPG Pace Merger Sub, TCV Blocker, Learn Blocker, Blocker Merger Sub I, Blocker Merger Sub II, Nerdy, and, solely for the purposes stated therein, certain entities affiliates with the Blockers (as amended on March 19, 2021, on July 14, 2021 and on August 11, 2021 and as amended, supplemented or otherwise modified from time to time in accordance with its terms); |

| • | “Business Combination” means the Domestication, the Merger and other transactions contemplated by the Business Combination Agreement, collectively, including the PIPE Financing; |

iii

| • | “Call Right” means the right, pursuant to the OpCo LLC Agreement and upon the exercise of the OpCo Redemption Right by an OpCo Unitholder, for Nerdy Inc. to acquire each tendered OpCo Unit directly from such OpCo Unitholder for, at Nerdy Inc.’s election, (i) one share of Class A Common Stock, subject to conversion rate adjustments for stock splits, stock dividends and reclassification, or (ii) an equivalent amount of cash; |

| • | “Cayman Islands Companies Act” means the Companies Act (2021 Revision) of the Cayman Islands as the same may be amended from time to time; |

| • | “Charter Proposal” means Proposal No. 3 to approve the Proposed Certificate of Incorporation of Nerdy Inc.; |

| • | “Class A Common Stock” means Class A common stock, $0.0001 par value of Nerdy Inc.; |

| • | “Class A Shares” means the Class A ordinary shares, $0.0001 par value in the capital of TPG Pace, which will automatically convert, on a one-for-one |

| • | “Class B Common Stock” means the Class B common Stock, par value $0.0001 per share of Nerdy Inc.; |

| • | “Closing Date” means the date on which the Closing occurs; |

| • | “Closing” means the closing of the transactions contemplated by the Business Combination Agreement; |

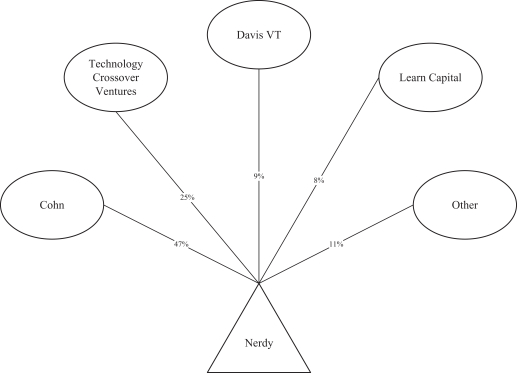

| • | “Cohn” means, collectively, Cohn Investments, LLC and Charles K. Cohn VT Trust U/A/D May 26, 2017 |

| • | “Common Stock” means the Class A Common Stock and Class B Common Stock; |

| • | “Condition Precedent Proposals” means the Business Combination Proposal, the Domestication Proposal, the Charter Proposal, the Director Election Proposal, the Equity Incentive Plan Proposal and the NYSE Proposal, collectively; |

| • | “Continental” means Continental Stock Transfer & Trust Company; |

| • | “Domestication” means the transfer by way of continuation and deregistration of TPG Pace from the Cayman Islands and the continuation and domestication as a corporation registered in the State of Delaware, upon which TPG Pace will change its name to Nerdy Inc.; |

| • | “Earnout Equity” means the TPG Pace Sponsor Earnout Equity and the Nerdy Earnout Consideration; |

| • | “Effective Time” means the time at which the Merger becomes effective; |

| • | “Equity Incentive Plan” means the Nerdy Inc. 2021 Equity Incentive Plan to be considered for adoption and approval by the shareholders pursuant to the Equity Incentive Plan Proposal; |

| • | “Excess Shares” means shares in excess of 15,000,000 aggregate forward purchase shares; |

| • | “Excess Share Forfeitures” means the forfeiture of Excess Shares pursuant to the Waiver Agreement; |

| • | “Existing Governing Documents” means the amended and restated memorandum and articles of association; |

| • | “Existing Nerdy Holders” means the existing holders of equity securities of Nerdy, but including with respect to the Blockers, the owners of the Blockers with respect to their indirect interest in Nerdy equity; |

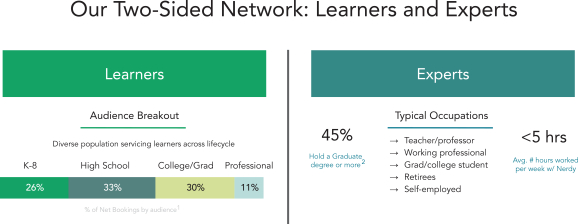

| • | “Experts” means Nerdy’s tutors, instructors, subject matter experts, educators and other professionals; |

iv

| • | “extraordinary general meeting” means the extraordinary general meeting of TPG Pace to be held on , 2021 at local time at the offices of Vinson & Elkins L.L.P., located at 1114 Avenue of the Americas, 32nd Floor, New York, NY 10036, or such other date, time and place to which such meeting may be adjourned or postponed, to consider and vote upon the proposals; |

| • | “Forward Purchase Agreements” means those certain forward purchase agreements, entered into in connection with the TPG Pace IPO, by and among TPG Pace, TPG Holdings and certain third parties pursuant to which TPG Holdings, certain transferees of TPG Holdings and certain third parties, upon the terms and subject to the conditions set forth therein, have agreed to purchase certain Class A Shares and forward purchase warrants prior to the consummation of TPG Pace’s initial business combination; |

| • | “forward purchase shares” means the shares of Class A Common Stock issuable pursuant to the Forward Purchase Agreements; |

| • | “forward purchase warrants” means the warrants issuable pursuant to the Forward Purchase Agreements; |

| • | “forward purchases” means the transactions contemplated under the Forward Purchase Agreements; |

| • | “forward purchase securities” means, collectively, forward purchase shares and forward purchase warrants; |

| • | “Founder Shares” means the 11,250,000 Class F ordinary shares, par value $0.0001 per share, of TPG Pace outstanding as of the date of this proxy statement/prospectus that were initially issued to our Sponsor in a private placement prior to our initial public offering and of which 160,000 were transferred to each of Chad Leat, Kathleen Philips, Wendi Sturgis and Kneeland Youngblood (40,000 shares each) in October 2020, and, following the Domestication, the 11,250,000 Class F ordinary shares that will automatically convert, on a one-for-one |

| • | “Learn Blocker” means LCSOF XI VT, Inc., a Delaware corporation; |

| • | “Learn Capital” means, collectively, Learn Blocker, Learn Capital Special Opportunities Fund XIV, L.P. and Learn Capital Special Opportunities Fund XV; |

| • | “Learners” means Nerdy’s students, users, parents, guardians, and purchasers; |

| • | “Merger Subs” means the Blocker Merger Subs and TPG Pace Merger Sub; |

| • | “Merger” means the merger of TPG Pace Merger Sub with and into Nerdy pursuant to the Business Combination Agreement, with Nerdy as the surviving company in the Merger and, after giving effect to such Merger, OpCo becoming a subsidiary of TPG Pace; |

| • | “Minimum Available Cash Condition” means the condition in the Business Combination Agreement that states that Available Cash must equal no less than $250,000,000; |

| • | “Nerdy” means, prior to the Closing of the Business Combination, Live Learning Technologies LLC, a Missouri limited liability company; |

| • | “Nerdy Earnout Consideration” means those aggregate 4,000,000 (1) shares of Class A Common Stock or (2) OpCo Units (and a corresponding number of shares of Class B Common Stock) that may be paid to certain Existing Nerdy Holders (treating for such calculation each OpCo Unit and corresponding share of Pace Class B Common Stock as one), which such shares or units, as applicable, shall be issued but subject to forfeiture until the achievement of Triggering Event I with respect 1,333,333 shares or units, Triggering Event II with respect to 1,333,333 shares or units, and Triggering Event III with respect to 1,333,334 shares or units; |

| • | “Nerdy Inc. Board” means the board of directors of Nerdy Inc.; |

| • | “Nerdy Inc. Founder Shares” means, after the domestication, the Class F Common Stock, par value $0.0001 of Nerdy Inc.; |

v

| • | “Nerdy Inc. Preferred Stock” means shares of Nerdy Inc. preferred stock, par value $0.0001; |

| • | “Nerdy Inc.” means Nerdy Inc., a Delaware corporation (f.k.a. TPG Pace Tech Opportunities Corp.), upon and after the Domestication; |

| • | “Nerdy Recapitalization” means the conversion of each outstanding class of Nerdy preferred units and the Nerdy profit units (whether vested or unvested) into Nerdy common units (subject to substantially the same terms and conditions, including applicable vesting requirements); |

| • | “Nerdy Securities” means Class A Common Stock and Nerdy Inc. warrants; |

| • | “Nerdy Stockholder Group” means, collectively, Cohn, Learn Capital and TCV; |

| • | “Nerdy Inc. warrants” means the warrants issued by Nerdy Inc. to acquire shares of Class A Common Stock; |

| • | “Nerdy warrants” means the Nerdy Inc. warrants and the OpCo warrants that will be issued to the equity holders of Nerdy in connection with the Business Combination. |

| • | “NYSE” means the New York Stock Exchange; |

| • | “OpCo” means, after the conversion to a Delaware limited liability company and the Merger, Nerdy, LLC, a Delaware limited liability company; |

| • | “OpCo LLC Agreement” means the Second Amended and Restated Limited Liability Company Agreement of OpCo to be entered into in connection with the Closing; |

| • | “OpCo Redemption Right” means the right, pursuant to the OpCo LLC Agreement, for OpCo Unitholders (other than Nerdy Inc.) to cause OpCo to acquire all or a portion of their vested OpCo Units and corresponding shares of Class B Common Stock for shares of Class A Common Stock at a redemption ratio of one share of Class A Common Stock for each OpCo Unit redeemed, subject to conversion rate adjustments for stock splits, stock dividends and reclassification; |

| • | “OpCo Units” means the units of OpCo; |

| • | “OpCo Unitholder” means a holder of OpCo Units; |

| • | “OpCo warrants” means the warrants issued by OpCo to purchase OpCo Units; |

| • | “PIPE Financing” means the transactions contemplated by the Subscription Agreements, pursuant to which the certain investors agreed to purchase, and TPG Pace agreed to issue and sell to such investors, newly issued shares of Class A Common Stock at a purchase price of $10.00 per share for gross proceeds of approximately $150 million, which purchase and sale will be consummated concurrently with the Business Combination; |

| • | “PIPE Investors” means the investors who participated in the PIPE Financing. |

| • | “private placement warrants” means the 7,333,333 private placement warrants outstanding as of the date of this proxy statement/prospectus that were issued to our Sponsor (which may become exercisable for Class A Shares at an exercise price of $11.50 per share), which are substantially identical to the public warrants sold as part of the units in the TPG Pace IPO, subject to certain limited exceptions, 2,444,444 of which will be forfeited by our Sponsor pursuant to the Waiver Agreement in connection with the Business Combination and, after the Domestication, the 4,888,889 private placement warrants (after giving effect to the forfeiture described in the foregoing) that will be exercisable for Class A Common Stock at $11.50 per share; |

| • | “Proposed Bylaws” means the proposed bylaws of Nerdy Inc. to be effective upon the Domestication attached to this proxy statement/prospectus as Annex D; |

| • | “Proposed Certificate of Incorporation” means the proposed certificate of incorporation of Nerdy Inc. to be effective upon the Domestication attached to this proxy statement/prospectus as Annex C; |

vi

| • | “Proposed Governing Documents” means the Proposed Certificate of Incorporation and the Proposed Bylaws; |

| • | “public shareholders” means holders of public shares; |

| • | “public shares” means the currently outstanding 45,000,000 Class A Shares issued as part of the Units in the TPG Pace IPO; |

| • | “public warrants” means the currently outstanding 9,000,000 warrants to purchase Class A Shares that were issued as part of the Units in the TPG Pace IPO (which may become exercisable for Class A Shares at an exercise price of $11.50 per share) and, after the Domestication, the 9,000,000 warrants to purchase Class A Common Stock that will be exercisable for shares of Class A Common Stock at $11.50 per share; |

| • | “redemption” means each redemption of public shares for cash pursuant to the Existing Governing Documents; |

| • | “Registration Rights Agreement” means that certain agreement with certain holders of Class A Common Stock and warrants after Closing, pursuant to which registration rights with respect to such securities will be offered; |

| • | “SEC” means the Securities and Exchange Commission; |

| • | “Securities Act” means the Securities Act of 1933, as amended; |

| • | “Share Forfeitures” means, together, the Excess Share Forfeiture and the additional forfeiture of 2,000,000 shares of Class A Common Stock by holders of Founder Shares pursuant to the Waiver Agreement; |

| • | “Stockholders’ Agreement” means that certain agreement by and among TPG Pace, the Nerdy Stockholder Group and Sponsor, pursuant to which certain governing rights and obligations of the parties are given; |

| • | “Sponsor” means TPG Pace Tech Opportunities Sponsor, Series LLC, a Delaware limited liability company; |

| • | “Subscription Agreements” means the subscription agreements, entered into by TPG Pace and certain investors in connection with the PIPE Financing; |

| • | “TCV” means, collectively, TCV Blocker, TCV VIII (A) VT, L.P., TCV VIII, L.P., TCV VIII (B), L.P., TCV Member Fund, L.P and TCV VIII Master, L.P.; |

| • | “TCV Blocker” means TCV VIII (A) VT, Inc., a Delaware corporation; |

| • | “TPG” means TPG Global, LLC and its affiliates; |

| • | “TPG Capital BD” means TPG Capital BD, LLC, an affiliate of our Sponsor and TPG Pace; |

| • | “TPG Global” means TPG Global, LLC; |

| • | “TPG Global Purchasers” means affiliates and employees of TPG Global that have committed to purchase forward purchase securities pursuant to the Forward Purchase Agreements; |

| • | “TPG Pace Board” means TPG Pace’s board of directors; |

| • | “TPG Pace Independent Directors” means each of Chad Leat, Kathleen Philips, Wendi Sturgis and Kneeland Youngblood; |

| • | “TPG Pace Initial Shareholders” means our Sponsor and the TPG Pace Independent Directors; |

| • | “TPG Pace IPO” means TPG Pace’s initial public offering that was consummated on October 9, 2020; |

| • | “TPG Pace Merger Sub” means TPG Pace Tech Merger Sub LLC, a Delaware limited liability company and wholly owned subsidiary of TPG Pace; |

vii

| • | “TPG Pace ordinary shares” means our Class A Shares and our Founder Shares; |

| • | “TPG Pace Public Securities” means Class A Shares and TPG Pace Public Warrants; |

| • | “TPG Pace Public Warrants” means the currently outstanding 9,000,000 warrants to purchase Class A Shares that were issued as part of the Units in the TPG Pace IPO (which may become exercisable for Class A Shares at an exercise price of $11.50 per share); |

| • | “TPG Pace Sponsor Earnout Equity” means 4,000,000 shares of Class A Common Stock that have been made subject to potential forfeiture by Sponsor following the Closing until the achievement of Triggering Event I with respect 1,333,333 shares, Triggering Event II with respect to 1,333,333 shares, and Triggering Event III with respect to 1,333,334 shares, consistent with the forfeiture thresholds for the Nerdy Earnout Consideration; |

| • | “TPG Pace,” means TPG Pace Tech Opportunities Corp., a Cayman Islands exempted company, prior to the consummation of the Domestication; |

| • | “TRA Holders” means the OpCo Unitholders (other than Nerdy Inc.) that are a party to the Tax Receivable Agreement (and their respective successors and permitted assigns under the Tax Receivable Agreement); |

| • | “transfer agent” means Continental, TPG Pace’s transfer agent; |

| • | “Triggering Event I” means the date on which the closing sale price of one share of Class A Common Stock quoted on the New York Stock Exchange (or the exchange on which the shares of Class A Common Stock are then listed) is greater than or equal to $12.00 for any 20 days within any 30 consecutive day period in which the Class A Common Stock are actually traded on the applicable exchange for the period between January 28, 2021 and the five-year anniversary of the Closing Date; |

| • | “Triggering Event II” means the date on which the closing sale price of one share of Class A Common Stock quoted on the New York Stock Exchange (or the exchange on which the shares of Class A Common Stock are then listed) is greater than or equal to $14.00 for any 20 days within any 30 consecutive day period in which the Class A Common Stock are actually traded on the applicable exchange for the period between January 28, 2021 and the five-year anniversary of the Closing Date; |

| • | “Triggering Event III” means the date on which the closing sale price of one share of Class A Common Stock quoted on the New York Stock Exchange (or the exchange on which the shares of Class A Common Stock are then listed) is greater than or equal to $16.00 for any 20 days within any 30 consecutive day period in which the Class A Common Stock are actually traded on the applicable exchange for the period between January 28, 2021 and the five-year anniversary of the Closing Date; |

| • | “Trust Account” means the trust account established at the consummation of the TPG Pace’s IPO that holds the proceeds of the initial public offering and is maintained by Continental, acting as trustee; |

| • | “Units” means the units of TPG Pace, each unit representing one Class A Share and one-fifth of one warrant to acquire one Class A Share, that were offered and sold by TPG Pace in its initial public offering and in its concurrent private placement; |

| • | “Waiver Agreement” means that certain waiver agreement, dated January 29, 2021, by and among TPG Pace, our Sponsor and each holder of issued and outstanding Founder Shares which provides, among other things, that (i) holders of Founder Shares agreed to forfeit for no consideration a number of shares of Class A Common Stock equal to the number of shares of Class A Common Stock issued pursuant to certain Forward Purchase Agreements over an aggregate of 15,000,000 shares of Class A Common Stock, (ii) such holders of Founder Shares agreed to forfeit for no consideration 2,000,000 shares of Class A Common Stock, which shares of Class A Common Stock will be immediately cancelled upon the Closing, (iii) Sponsor agreed to forfeit for no consideration 2,444,444 private placement warrants that will be immediately cancelled upon the Closing and (iv) Sponsor further |

viii

| agreed to subject 4,000,000 shares of Class A Common Stock following the closing to potential forfeiture if certain stock price thresholds are not achieved within a period of five years from the Closing Date, consistent with the forfeiture thresholds for the Nerdy Earnout Consideration; |

| • | “warrants” means, collectively, the FPA Warrants, public warrants, private placement warrants and certain Nerdy warrants. |

Unless otherwise specified, the share counts and other data set forth in this proxy statement/prospectus

| • | includes (a) the 8,000,000 aggregate shares of Class A Common Stock or OpCo Units (with equivalent number of shares of Class B Common Stock) that comprise the Earnout Equity, which will be issued and outstanding as of Closing, but subject to forfeiture and (b) an expected 18,075,207 shares (of which 5,976,406 will be shares of Class A Common Stock of Nerdy, Inc. and 12,098,801 will be shares of Class B Common Stock of Nerdy Inc.) underlying (i) an expected 9,036,422 vested (of which 1,233,379 are vested unit appreciation rights and 7,803,043 are vested profit interest units) and (ii) 9,038,785 unvested (of which 4,743,027 are unvested stock appreciation rights and 4,295,758 are unvested profit interest units), which unvested stock appreciation rights and profit interest units will be subject to certain vesting conditions and a risk of forfeiture, that will be held by the former Nerdy unit appreciation rights and profit interest units holders immediately following the Closing; |

| • | does not take into account (a), the issuance of any shares upon completion of the Business Combination under the Equity Incentive Plan, which is expected to include shares available for issuance for 15% of shares outstanding at Closing after giving effect to the shares of Class A Common Stock/OpCo Units issuable upon exercise of the warrants using treasury stock method assuming an $18.00 stock/unit price and assuming that the Nerdy Earnout Consideration is issued in full, plus additional shares relating to the forfeiture provisions set forth in the proposed Equity Incentive Plan and (b) 19,333,333 warrants that will remain outstanding immediately following the Business Combination and may be exercised thereafter; and |

| • | otherwise assumes that: |

| • | no public shareholders elect to have their public shares redeemed; |