false2022FY0001818383P3Yhttp://fasb.org/us-gaap/2022#OtherAssetsNoncurrenthttp://fasb.org/us-gaap/2022#OtherAssetsNoncurrenthttp://fasb.org/us-gaap/2022#AccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2022#AccruedLiabilitiesCurrenthttp://fasb.org/us-gaap/2022#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2022#OtherLiabilitiesNoncurrent00018183832022-01-012022-12-3100018183832022-06-30iso4217:USD0001818383us-gaap:CommonClassAMember2023-01-31xbrli:shares0001818383us-gaap:CommonClassBMember2023-01-3100018183832022-12-3100018183832021-12-310001818383us-gaap:CommonClassAMember2022-12-31iso4217:USDxbrli:shares0001818383us-gaap:CommonClassAMember2021-12-310001818383us-gaap:CommonClassBMember2022-12-310001818383us-gaap:CommonClassBMember2021-12-3100018183832021-01-012021-12-3100018183832020-01-012020-12-310001818383max:QLHoldingsLLCMember2022-01-012022-12-310001818383max:QLHoldingsLLCMember2021-01-012021-12-310001818383max:QLHoldingsLLCMember2020-01-012020-12-310001818383us-gaap:PreferredClassAMember2019-12-310001818383us-gaap:ReceivablesFromStockholderMember2019-12-310001818383us-gaap:CommonClassAMemberus-gaap:CommonStockMember2019-12-310001818383us-gaap:CommonClassBMemberus-gaap:CommonStockMember2019-12-310001818383us-gaap:AdditionalPaidInCapitalMember2019-12-310001818383us-gaap:RetainedEarningsMember2019-12-310001818383us-gaap:NoncontrollingInterestMember2019-12-3100018183832019-12-310001818383us-gaap:PreferredClassAMember2020-01-012020-12-310001818383us-gaap:RetainedEarningsMember2020-01-012020-12-310001818383us-gaap:ReceivablesFromStockholderMember2020-01-012020-12-310001818383us-gaap:CommonClassAMemberus-gaap:CommonStockMember2020-01-012020-12-310001818383us-gaap:CommonClassBMemberus-gaap:CommonStockMember2020-01-012020-12-310001818383us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310001818383us-gaap:NoncontrollingInterestMember2020-01-012020-12-310001818383us-gaap:PreferredClassAMember2020-12-310001818383us-gaap:ReceivablesFromStockholderMember2020-12-310001818383us-gaap:CommonClassAMemberus-gaap:CommonStockMember2020-12-310001818383us-gaap:CommonClassBMemberus-gaap:CommonStockMember2020-12-310001818383us-gaap:AdditionalPaidInCapitalMember2020-12-310001818383us-gaap:RetainedEarningsMember2020-12-310001818383us-gaap:NoncontrollingInterestMember2020-12-3100018183832020-12-310001818383us-gaap:RetainedEarningsMember2021-01-012021-12-310001818383us-gaap:CommonClassAMemberus-gaap:CommonStockMember2021-01-012021-12-310001818383us-gaap:CommonClassBMemberus-gaap:CommonStockMember2021-01-012021-12-310001818383us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001818383us-gaap:NoncontrollingInterestMember2021-01-012021-12-310001818383us-gaap:PreferredClassAMember2021-12-310001818383us-gaap:ReceivablesFromStockholderMember2021-12-310001818383us-gaap:CommonClassAMemberus-gaap:CommonStockMember2021-12-310001818383us-gaap:CommonClassBMemberus-gaap:CommonStockMember2021-12-310001818383us-gaap:AdditionalPaidInCapitalMember2021-12-310001818383us-gaap:RetainedEarningsMember2021-12-310001818383us-gaap:NoncontrollingInterestMember2021-12-310001818383us-gaap:CommonClassAMemberus-gaap:CommonStockMember2022-01-012022-12-310001818383us-gaap:CommonClassBMemberus-gaap:CommonStockMember2022-01-012022-12-310001818383us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001818383us-gaap:NoncontrollingInterestMember2022-01-012022-12-310001818383us-gaap:RetainedEarningsMember2022-01-012022-12-310001818383us-gaap:PreferredClassAMember2022-12-310001818383us-gaap:ReceivablesFromStockholderMember2022-12-310001818383us-gaap:CommonClassAMemberus-gaap:CommonStockMember2022-12-310001818383us-gaap:CommonClassBMemberus-gaap:CommonStockMember2022-12-310001818383us-gaap:AdditionalPaidInCapitalMember2022-12-310001818383us-gaap:RetainedEarningsMember2022-12-310001818383us-gaap:NoncontrollingInterestMember2022-12-310001818383us-gaap:CommonClassAMemberus-gaap:IPOMember2020-10-302020-10-300001818383us-gaap:CommonClassAMemberus-gaap:IPOMember2020-10-300001818383us-gaap:CommonClassAMemberus-gaap:OverAllotmentOptionMember2020-10-302020-10-300001818383us-gaap:CommonClassAMemberus-gaap:IPOMembermax:WhiteMountainsOfIntermediateHoldcoMember2020-10-302020-10-300001818383max:InsigniaSeniorExecutivesAndLegacyProfitInterestsHoldersMemberus-gaap:CommonClassBMemberus-gaap:IPOMember2020-10-302020-10-300001818383max:LegacyProfitInterestsHoldersMemberus-gaap:CommonClassAMemberus-gaap:IPOMember2020-10-302020-10-3000018183832020-10-27xbrli:pure0001818383max:TaxReceivablesAgreementMembermax:InsigniaAndSeniorExecutivesMember2020-10-302020-10-300001818383max:TaxReceivablesAgreementMembermax:WhiteMountainsOfIntermediateHoldcoMember2020-10-302020-10-300001818383srt:MinimumMember2022-01-012022-12-310001818383srt:MaximumMember2022-01-012022-12-310001818383max:TopOneCustomerMemberus-gaap:RevenueFromContractWithCustomerMemberus-gaap:CustomerConcentrationRiskMember2022-01-012022-12-310001818383max:TopTwoCustomersMemberus-gaap:RevenueFromContractWithCustomerMemberus-gaap:CustomerConcentrationRiskMember2021-01-012021-12-310001818383us-gaap:AccountsReceivableMembermax:TopOneCustomerMemberus-gaap:CustomerConcentrationRiskMember2021-12-310001818383us-gaap:AccountsReceivableMembermax:TopOneCustomerMemberus-gaap:CustomerConcentrationRiskMember2021-01-012021-12-310001818383us-gaap:SupplierConcentrationRiskMembermax:TopOneSupplierMembermax:CostOfRevenueBenchmarkMember2022-01-012022-12-310001818383us-gaap:SupplierConcentrationRiskMembermax:TopOneSupplierMembermax:CostOfRevenueBenchmarkMember2021-01-012021-12-310001818383us-gaap:SupplierConcentrationRiskMembermax:TopTwoSuppliersMembermax:AccountsPayableBenchmarkMember2022-12-310001818383us-gaap:SupplierConcentrationRiskMembermax:TopTwoSuppliersMembermax:AccountsPayableBenchmarkMember2022-01-012022-12-310001818383us-gaap:SupplierConcentrationRiskMembermax:TopTwoSuppliersMembermax:AccountsPayableBenchmarkMember2021-12-310001818383us-gaap:SupplierConcentrationRiskMembermax:TopTwoSuppliersMembermax:AccountsPayableBenchmarkMember2021-01-012021-12-310001818383us-gaap:ComputerEquipmentMember2022-01-012022-12-310001818383us-gaap:FurnitureAndFixturesMember2022-01-012022-12-310001818383us-gaap:SoftwareAndSoftwareDevelopmentCostsMember2022-01-012022-12-31max:reportingUnitmax:segment0001818383max:TaxReceivablesAgreementMember2022-01-012022-12-310001818383max:TaxReceivablesAgreementMember2021-01-012021-12-310001818383us-gaap:RevolvingCreditFacilityMember2022-12-310001818383us-gaap:SalesChannelDirectlyToConsumerMember2022-01-012022-12-310001818383us-gaap:SalesChannelDirectlyToConsumerMember2021-01-012021-12-310001818383us-gaap:SalesChannelDirectlyToConsumerMember2020-01-012020-12-310001818383us-gaap:SalesChannelThroughIntermediaryMember2022-01-012022-12-310001818383us-gaap:SalesChannelThroughIntermediaryMember2021-01-012021-12-310001818383us-gaap:SalesChannelThroughIntermediaryMember2020-01-012020-12-310001818383max:PropertyAndCasualtyInsuranceMember2022-01-012022-12-310001818383max:PropertyAndCasualtyInsuranceMember2021-01-012021-12-310001818383max:PropertyAndCasualtyInsuranceMember2020-01-012020-12-310001818383max:HealthInsuranceMember2022-01-012022-12-310001818383max:HealthInsuranceMember2021-01-012021-12-310001818383max:HealthInsuranceMember2020-01-012020-12-310001818383max:LifeInsuranceMember2022-01-012022-12-310001818383max:LifeInsuranceMember2021-01-012021-12-310001818383max:LifeInsuranceMember2020-01-012020-12-310001818383max:OtherMember2022-01-012022-12-310001818383max:OtherMember2021-01-012021-12-310001818383max:OtherMember2020-01-012020-12-310001818383max:QuoteLabLLCMember2022-02-242022-02-240001818383us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembermax:A2021CreditFacilitiesMember2022-04-012022-04-010001818383max:CustomerHelperTeamLLCMembersrt:MinimumMember2022-02-242022-02-240001818383srt:MaximumMembermax:CustomerHelperTeamLLCMember2022-02-242022-02-240001818383max:CustomerHelperTeamLLCMember2022-02-242022-02-24max:period0001818383max:CustomerHelperTeamLLCMembersrt:MinimumMember2022-12-312022-12-310001818383srt:MaximumMembermax:CustomerHelperTeamLLCMember2022-12-312022-12-310001818383max:CustomerHelperTeamLLCMember2022-01-012022-12-310001818383max:QuoteLabLLCMember2022-02-240001818383max:CustomerHelperTeamLLCMember2022-04-010001818383us-gaap:CustomerRelationshipsMembermax:QuoteLabLLCMember2022-01-012022-12-310001818383us-gaap:TrademarksAndTradeNamesMembermax:QuoteLabLLCMember2022-01-012022-12-310001818383max:QuoteLabLLCMember2022-01-012022-12-310001818383max:CustomerHelperTeamLLCMember2022-04-012022-12-310001818383max:CustomerHelperTeamLLCMember2021-01-012021-12-310001818383us-gaap:CustomerRelationshipsMembersrt:MinimumMember2022-01-012022-12-310001818383us-gaap:CustomerRelationshipsMembersrt:MaximumMember2022-01-012022-12-310001818383us-gaap:CustomerRelationshipsMember2022-12-310001818383us-gaap:CustomerRelationshipsMember2021-12-310001818383us-gaap:NoncompeteAgreementsMember2022-01-012022-12-310001818383us-gaap:NoncompeteAgreementsMember2022-12-310001818383us-gaap:NoncompeteAgreementsMember2021-12-310001818383us-gaap:IntellectualPropertyMembersrt:MinimumMember2022-01-012022-12-310001818383srt:MaximumMemberus-gaap:IntellectualPropertyMember2022-01-012022-12-310001818383us-gaap:IntellectualPropertyMember2022-12-310001818383us-gaap:IntellectualPropertyMember2021-12-310001818383us-gaap:SecuredDebtMembermax:A2021CreditFacilitiesMember2021-07-290001818383us-gaap:SecuredDebtMembermax:A2020CreditFacilitiesMember2021-07-290001818383us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembermax:A2021CreditFacilitiesMember2021-07-290001818383max:A2021CreditFacilitiesMemberus-gaap:LondonInterbankOfferedRateLIBORMember2021-07-292021-07-290001818383srt:MinimumMembermax:A2021CreditFacilitiesMemberus-gaap:LondonInterbankOfferedRateLIBORMember2021-07-292021-07-290001818383srt:MaximumMembermax:A2021CreditFacilitiesMemberus-gaap:LondonInterbankOfferedRateLIBORMember2021-07-292021-07-290001818383us-gaap:BaseRateMembersrt:MinimumMembermax:A2021CreditFacilitiesMember2021-07-292021-07-290001818383srt:MaximumMemberus-gaap:BaseRateMembermax:A2021CreditFacilitiesMember2021-07-292021-07-290001818383max:A2021CreditFacilitiesMember2021-07-290001818383us-gaap:SecuredDebtMembermax:A2020CreditFacilitiesMember2020-09-230001818383us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembermax:A2020CreditFacilitiesMember2020-09-2300018183832020-09-232020-09-230001818383max:A2020CreditFacilitiesMembermax:NYFRBRateMember2020-09-232020-09-230001818383max:AdjustedLIBORateMembermax:A2020CreditFacilitiesMember2020-09-232020-09-230001818383max:AdjustedLIBORateMembermax:A2020CreditFacilitiesMember2020-09-230001818383srt:MinimumMembermax:AlternateBaseRateMembermax:A2020CreditFacilitiesMember2020-09-230001818383max:AdjustedLIBORateMembersrt:MinimumMembermax:A2020CreditFacilitiesMember2020-09-230001818383srt:MinimumMembermax:ApplicableRateMembermax:A2020CreditFacilitiesMember2020-09-232020-09-230001818383srt:MaximumMembermax:ApplicableRateMembermax:A2020CreditFacilitiesMember2020-09-232020-09-230001818383max:EurodollarBorrowingsMembersrt:MinimumMembermax:A2020CreditFacilitiesMember2020-09-232020-09-230001818383max:EurodollarBorrowingsMembersrt:MaximumMembermax:A2020CreditFacilitiesMember2020-09-232020-09-230001818383max:A2020CreditFacilitiesMember2020-09-232020-09-230001818383max:A2020CreditFacilitiesMember2020-12-012020-12-010001818383us-gaap:OtherExpenseMemberus-gaap:RevolvingCreditFacilityMembermax:A2019CreditFacilitiesMember2020-01-012020-12-310001818383us-gaap:SecuredDebtMembermax:A2021CreditFacilitiesMember2022-12-310001818383us-gaap:SecuredDebtMembermax:A2021CreditFacilitiesMember2021-12-310001818383us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembermax:A2021CreditFacilitiesMember2022-12-310001818383us-gaap:LineOfCreditMemberus-gaap:RevolvingCreditFacilityMembermax:A2021CreditFacilitiesMember2021-12-310001818383us-gaap:RevolvingCreditFacilityMember2022-01-012022-12-31max:vote0001818383us-gaap:IPOMembermax:ClassB1UnitMember2020-10-302020-10-300001818383us-gaap:CommonClassBMember2020-10-300001818383max:QLHoldingsLLCAndSubsidiariesMembermax:ClassB1UnitMember2020-10-302020-10-300001818383us-gaap:IPOMembermax:IntermediateHoldcoMembermax:ClassB1UnitMember2020-10-302020-10-300001818383max:TwoThousandTwentyTermLoanFacilityMemberus-gaap:IPOMembermax:QLHoldingsLLCAndSubsidiariesMembermax:IntermediateHoldcoMember2020-10-302020-10-300001818383us-gaap:IPOMembermax:QLHoldingsLLCAndSubsidiariesMembermax:IntermediateHoldcoMember2020-10-302020-10-300001818383max:QLHoldingsLLCAndSubsidiariesMembermax:ClassB1UnitMember2022-12-310001818383max:QLHoldingsLLCAndSubsidiariesMemberus-gaap:PreferredClassAMember2019-12-310001818383max:QLHoldingsLLCAndSubsidiariesMemberus-gaap:CapitalUnitClassAMember2019-12-310001818383max:QLHoldingsLLCMembermax:QLHoldingsLLCAndSubsidiariesMember2020-09-232020-09-2300018183832022-03-140001818383max:QLHClassBUnitsMember2022-01-012022-12-310001818383max:QLHClassBUnitsMember2021-01-012021-12-310001818383max:QLHClassBUnitsMember2020-01-012020-12-310001818383max:QLHRestrictedClassB1UnitsMember2022-01-012022-12-310001818383max:QLHRestrictedClassB1UnitsMember2021-01-012021-12-310001818383max:QLHRestrictedClassB1UnitsMember2020-01-012020-12-310001818383max:RestrictedClassASharesMember2022-01-012022-12-310001818383max:RestrictedClassASharesMember2021-01-012021-12-310001818383max:RestrictedClassASharesMember2020-01-012020-12-310001818383us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001818383us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001818383us-gaap:RestrictedStockUnitsRSUMember2020-01-012020-12-310001818383max:PerformanceRestrictedStockUnitsMember2022-01-012022-12-310001818383max:PerformanceRestrictedStockUnitsMember2021-01-012021-12-310001818383max:PerformanceRestrictedStockUnitsMember2020-01-012020-12-310001818383us-gaap:CostOfSalesMember2022-01-012022-12-310001818383us-gaap:CostOfSalesMember2021-01-012021-12-310001818383us-gaap:CostOfSalesMember2020-01-012020-12-310001818383us-gaap:SellingAndMarketingExpenseMember2022-01-012022-12-310001818383us-gaap:SellingAndMarketingExpenseMember2021-01-012021-12-310001818383us-gaap:SellingAndMarketingExpenseMember2020-01-012020-12-310001818383max:ProductDevelopmentMember2022-01-012022-12-310001818383max:ProductDevelopmentMember2021-01-012021-12-310001818383max:ProductDevelopmentMember2020-01-012020-12-310001818383us-gaap:GeneralAndAdministrativeExpenseMember2022-01-012022-12-310001818383us-gaap:GeneralAndAdministrativeExpenseMember2021-01-012021-12-310001818383us-gaap:GeneralAndAdministrativeExpenseMember2020-01-012020-12-310001818383srt:MaximumMembermax:QLHClassBRestrictedUnitPlanMembermax:ProfitsInterestsToDirectorsEmployeesManagersIndependentContractorsAndAdvisorsMembermax:ClassBUnitsMember2020-10-2900018183832020-10-292020-10-290001818383us-gaap:IPOMembermax:QLHClassBProfitsInterestsMember2020-10-302020-10-300001818383max:QLHClassBProfitsInterestsMember2020-10-302020-10-30max:employee0001818383max:QLHClassBUnitsMembermax:QLHClassBProfitsInterestsMember2019-12-310001818383max:QLHClassBUnitsMembermax:QLHClassBProfitsInterestsMember2020-01-012020-12-310001818383max:QLHClassBUnitsMembermax:QLHClassBProfitsInterestsMember2020-12-310001818383max:QLHClassBUnitsMemberus-gaap:IPOMembermax:QLHClassBProfitsInterestsMember2020-01-012020-12-310001818383max:QLHClassB1UnitsMemberus-gaap:IPOMembermax:QLHClassBProfitsInterestsMember2020-01-012020-12-310001818383max:QLHRestrictedClassB1UnitsMembermax:QLHClassB1UnitsMember2020-01-012020-12-310001818383max:QLHClassBUnitsMemberus-gaap:IPOMembermax:QLHClassBProfitsInterestsMember2020-12-310001818383srt:MinimumMembermax:QLHClassBProfitsInterestsMember2020-01-012020-12-310001818383srt:MaximumMembermax:QLHClassBProfitsInterestsMember2020-01-012020-12-310001818383max:QLHClassBProfitsInterestsMember2020-01-012020-12-310001818383srt:MinimumMember2020-01-012020-12-310001818383srt:MaximumMember2020-01-012020-12-310001818383us-gaap:IPOMembermax:QLHClassBProfitsInterestsMember2020-01-012020-12-310001818383max:CompanyRestrictedClassASharesMember2022-01-012022-12-310001818383max:QLHRestrictedClassB1UnitsMember2022-01-012022-12-310001818383max:QLHRestrictedClassB1UnitsMember2019-12-310001818383max:QLHRestrictedClassB1UnitsMember2020-01-012020-12-310001818383max:QLHRestrictedClassB1UnitsMember2020-12-310001818383max:QLHRestrictedClassB1UnitsMember2021-01-012021-12-310001818383max:QLHRestrictedClassB1UnitsMember2021-12-310001818383max:QLHRestrictedClassB1UnitsMember2022-01-012022-12-310001818383max:QLHRestrictedClassB1UnitsMember2022-12-310001818383max:QLHClassB1UnitsMember2022-01-012022-12-310001818383max:QLHClassB1UnitsMember2021-01-012021-12-310001818383max:QLHClassB1UnitsMember2020-01-012020-12-310001818383max:QLHClassBRestrictedUnitPlanMemberus-gaap:ShareBasedCompensationAwardTrancheOneMembermax:ClassBUnitsMember2022-01-012022-12-310001818383max:RestrictedClassASharesMemberus-gaap:RestrictedStockUnitsRSUMember2019-12-310001818383max:RestrictedClassASharesMemberus-gaap:RestrictedStockUnitsRSUMember2020-01-012020-12-310001818383max:RestrictedClassASharesMemberus-gaap:RestrictedStockUnitsRSUMember2020-12-310001818383max:RestrictedClassASharesMemberus-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001818383max:RestrictedClassASharesMemberus-gaap:RestrictedStockUnitsRSUMember2021-12-310001818383max:RestrictedClassASharesMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001818383max:RestrictedClassASharesMemberus-gaap:RestrictedStockUnitsRSUMember2022-12-310001818383max:UnvestedCompanyClassASharesMember2022-12-310001818383max:UnvestedCompanyClassASharesMember2022-01-012022-12-310001818383max:UnvestedCompanyClassASharesMember2021-01-012021-12-310001818383max:UnvestedCompanyClassASharesMember2020-01-012020-12-310001818383max:OmnibusIncentivePlanMembermax:RestrictedStockUnitsAndOtherEquityBasedAwardsMember2020-10-310001818383max:ClassAUnitsMembermax:OmnibusIncentivePlanMembermax:RestrictedStockUnitsAndOtherEquityBasedAwardsMember2022-01-012022-12-310001818383max:ClassAUnitsMembermax:OmnibusIncentivePlanMembermax:RestrictedStockUnitsAndOtherEquityBasedAwardsMember2022-12-310001818383srt:MinimumMemberus-gaap:RestrictedStockUnitsRSUMembermax:OmnibusIncentivePlanMember2020-10-312020-10-310001818383srt:MaximumMemberus-gaap:RestrictedStockUnitsRSUMembermax:OmnibusIncentivePlanMember2020-10-312020-10-310001818383us-gaap:RestrictedStockUnitsRSUMember2019-12-310001818383us-gaap:RestrictedStockUnitsRSUMember2020-12-310001818383us-gaap:RestrictedStockUnitsRSUMember2021-12-310001818383us-gaap:RestrictedStockUnitsRSUMember2022-12-310001818383us-gaap:PerformanceSharesMemberus-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001818383us-gaap:PerformanceSharesMemberus-gaap:RestrictedStockUnitsRSUMember2021-12-310001818383us-gaap:PerformanceSharesMemberus-gaap:RestrictedStockUnitsRSUMember2022-12-310001818383us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2022-12-310001818383us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2022-12-310001818383us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001818383us-gaap:FairValueMeasurementsRecurringMember2022-12-310001818383us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2021-12-310001818383us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2021-12-310001818383us-gaap:FairValueInputsLevel3Memberus-gaap:FairValueMeasurementsRecurringMember2021-12-310001818383us-gaap:FairValueMeasurementsRecurringMember2021-12-310001818383us-gaap:FairValueInputsLevel3Membermax:ContingentConsiderationObligationMember2021-12-310001818383us-gaap:FairValueInputsLevel3Membermax:ContingentConsiderationObligationMember2022-01-012022-12-310001818383us-gaap:FairValueInputsLevel3Membermax:ContingentConsiderationObligationMember2022-12-310001818383us-gaap:FairValueInputsLevel3Memberus-gaap:MeasurementInputDiscountRateMembersrt:MinimumMembermax:ValuationTechniqueMonteCarloMember2022-12-310001818383us-gaap:MeasurementInputPriceVolatilityMemberus-gaap:FairValueInputsLevel3Membersrt:MinimumMembermax:ValuationTechniqueMonteCarloMember2022-12-310001818383srt:MaximumMemberus-gaap:FairValueInputsLevel3Memberus-gaap:MeasurementInputDiscountRateMembermax:ValuationTechniqueMonteCarloMember2022-12-310001818383us-gaap:MeasurementInputPriceVolatilityMembersrt:MaximumMemberus-gaap:FairValueInputsLevel3Membermax:ValuationTechniqueMonteCarloMember2022-12-310001818383max:QuoteLabLLCMember2022-12-310001818383us-gaap:FairValueInputsLevel3Memberus-gaap:MeasurementInputDiscountRateMemberus-gaap:ValuationTechniqueDiscountedCashFlowMember2022-12-310001818383us-gaap:MeasurementInputPriceVolatilityMemberus-gaap:FairValueInputsLevel3Memberus-gaap:ValuationTechniqueOptionPricingModelMember2022-12-310001818383us-gaap:FairValueInputsLevel3Memberus-gaap:MeasurementInputDiscountForLackOfMarketabilityMemberus-gaap:ValuationTechniqueOptionPricingModelMember2022-12-310001818383max:TaxReceivablesAgreementMember2022-12-310001818383us-gaap:DomesticCountryMember2022-12-310001818383us-gaap:StateAndLocalJurisdictionMember2022-12-310001818383us-gaap:ForeignCountryMember2022-12-310001818383max:WhiteMountainsOfIntermediateHoldcoMember2022-12-310001818383max:WhiteMountainsOfIntermediateHoldcoMember2021-12-310001818383max:TaxReceivablesAgreementMembermax:WhiteMountainsOfIntermediateHoldcoMember2022-01-012022-12-310001818383max:TaxReceivablesAgreementMembermax:InsigniaAndSeniorExecutivesMember2022-01-012022-12-310001818383max:TaxReceivablesAgreementMember2021-12-3100018183832020-10-272020-12-310001818383us-gaap:CommonClassAMember2022-01-012022-12-310001818383us-gaap:CommonClassAMember2021-01-012021-12-310001818383us-gaap:CommonClassAMember2020-10-272020-12-310001818383max:ClassB1UnitsMember2021-01-012021-12-310001818383max:RestrictedClassASharesMember2021-01-012021-12-310001818383us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001818383max:ClassACommonStockAndPotentialClassACommonStockMember2021-01-012021-12-310001818383max:ClassBOrB1UnitsMembermax:QLHoldingsLLCMember2022-01-012022-12-310001818383max:ClassBOrB1UnitsMembermax:QLHoldingsLLCMember2021-01-012021-12-310001818383max:ClassBOrB1UnitsMembermax:QLHoldingsLLCMember2020-01-012020-12-310001818383us-gaap:RestrictedStockMember2022-01-012022-12-310001818383us-gaap:RestrictedStockMember2021-01-012021-12-310001818383us-gaap:RestrictedStockMember2020-01-012020-12-310001818383us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001818383us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001818383us-gaap:RestrictedStockUnitsRSUMember2020-01-012020-12-310001818383max:QLHMember2022-12-310001818383max:QLHMember2021-12-310001818383us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2021-12-310001818383us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2022-01-012022-12-310001818383us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2022-12-310001818383us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2020-12-310001818383us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2021-01-012021-12-310001818383us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2019-12-310001818383us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2020-01-012020-12-310001818383us-gaap:AllowanceForCreditLossMember2021-12-310001818383us-gaap:AllowanceForCreditLossMember2022-01-012022-12-310001818383us-gaap:AllowanceForCreditLossMember2022-12-310001818383us-gaap:AllowanceForCreditLossMember2020-12-310001818383us-gaap:AllowanceForCreditLossMember2021-01-012021-12-310001818383us-gaap:AllowanceForCreditLossMember2019-12-310001818383us-gaap:AllowanceForCreditLossMember2020-01-012020-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

________________________

FORM 10-K

________________________

(Mark One)

| | | | | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2022

OR

| | | | | |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO |

Commission File Number 001-39671

________________________

MediaAlpha, Inc.

(Exact name of Registrant as specified in its Charter)

________________________

| | | | | |

| Delaware | 85-1854133 |

(State or other jurisdiction of

incorporation or organization) | (I.R.S. Employer

Identification No.) |

700 South Flower Street, Suite 640

Los Angeles, California 90017

(Address of principal executive offices, including zip code)

(213) 316-6256

(Registrant’s telephone number, including area code)

________________________

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading

Symbol(s) | | Name of each exchange on which registered |

| Class A Common Stock, $0.01 par value per share | | MAX | | NYSE |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | |

| Large accelerated filer | o | | Accelerated filer | x |

| | | | |

| Non-accelerated filer | o | | Smaller reporting company | o |

| | | | |

| Emerging growth company | o | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the Registrant’s Class A Common Stock and Class B Common Stock held by non-affiliates was $255.2 million based upon the closing market price as of the close of business June 30, 2022, the last business day of the registrant’s most recently completed second fiscal quarter.

As of January 31, 2023, there were 44,022,910 shares of MediaAlpha, Inc.’s Class A common stock, $0.01 par value per share, and 18,895,493 shares of MediaAlpha, Inc.’s Class B common stock, par value $0.01 per share, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Parts of the registrant’s Proxy Statement for the registrant’s 2023 Annual Meeting of Stockholders are incorporated by reference into Part III of this Annual Report on Form 10-K.

Table of Contents

Certain Definitions

As used in this Annual Report on Form 10-K:

•“Class A-1 units” refers to the Class A-1 units of QL Holdings LLC (“QLH”).

•“Class B-1 units” refers to the Class B-1 units of QLH.

•“CAGR” means compound annual growth rate.

•“Consumer Referral” means any consumer click, call or lead purchased by a buyer on our platform.

•“Consumers” and “customers” refer interchangeably to end consumers. Examples include individuals shopping for insurance policies.

•“Digital consumer traffic” refers to visitors to the mobile, tablet, desktop and other digital platforms of our supply partners, as well as to our proprietary websites.

•“Direct-to-consumer” or “DTC” means the sale of insurance products or services directly to end consumers, without the use of retailers, brokers, agents or other intermediaries.

•“Distributor” means any company or individual that is involved in the distribution of insurance, such as an insurance agent or broker.

•“Exchange agreement” means the exchange agreement, dated as of October 27, 2020 by and among MediaAlpha, Inc., QLH, Intermediate Holdco, Inc. and certain Class B-1 unitholders party thereto.

•“Founders” means, collectively, Steven Yi, Eugene Nonko, and Ambrose Wang.

•“High-intent” consumer or customer means an in-market consumer that is actively browsing, researching or comparing the types of products or services that our partners sell.

•“Insignia” means Insignia Capital Group, L.P. and its affiliates.

•“InsurTech” means insurance technology.

•“Intermediate Holdco” means Guilford Holdings, Inc., our wholly owned subsidiary and the owner of all Class A-1 units.

•“Inventory,” when referring to our supply partners, means the volume of Consumer Referral opportunities.

•“IPO” means our initial public offering of our Class A common stock, which closed on October 30, 2020.

•“Legacy Profits Interest Holders” means certain current or former employees of QLH or its subsidiaries (other than the Senior Executives), who indirectly held Class B units in QLH prior to our IPO and includes any estate planning vehicles or other holding companies through which such persons hold their units in QLH (which holding companies may or may not include QL Management Holdings LLC).

•“Lifetime value” or “LTV” is a type of metric that many of our business partners use to measure the estimated total worth to a business of a customer over the expected period of their relationship.

•“NAIC” means the National Association of Insurance Commissioners.

•“Open Marketplace” refers to one of our two business models. In Open Marketplace transactions, we have separate agreements with demand partners and suppliers. We earn fees from our demand partners and separately pay a revenue share to suppliers and a fee to Internet search companies to drive consumers to our proprietary websites.

•“Partner” refers to a buyer or seller on our platform, also referred to as “demand partners” and “supply partners,” respectively.

◦“Demand partner” refers to a buyer on our platform. As discussed under Part II, Item 7. Management’s Discussion & Analysis – Management Overview, our demand partners are generally insurance carriers and distributors looking to target high-intent consumers deep in their purchase journey.

◦“Supply partner” or “supplier” refers to a seller to our platform. As discussed under Part II, Item 7. Management’s Discussion & Analysis – Management Overview, our supply partners are primarily insurance carriers looking to maximize the value of non-converting or low LTV consumers, and insurance-focused research destinations or other financial websites looking to monetize high-intent consumers.

•“Private Marketplace” refers to one of our two business models. In Private Marketplace transactions, demand partners and suppliers contract with one another directly and leverage our platform to facilitate transparent, real-time transactions utilizing the reporting and analytical tools available to them from use of our platform. We charge a fee based on the Transaction Value of the Consumer Referrals sold through Private Marketplace transactions.

•“Proprietary” means, when used in reference to our properties, the websites and other digital properties that we own and operate. Our proprietary properties are a source of Consumer Referrals on our platform.

•“Secondary Offering” means the means the sale of 8,050,000 shares of Class A common stock pursuant to the registration statement on Form S-1 (File No. 333-254338), which was declared effective by the Securities Exchange Commission ("SEC") on March 18, 2021.

•“Senior Executives” means the Founders and the other current and former officers of the Company listed in Exhibit A to the Exchange Agreement. This term also includes any estate planning vehicles or other holding companies through which such persons hold their units in QLH.

•“Selling Class B-1 Unit Holders” means Insignia, the Senior Executives, and the Legacy Profits Interests Holders who sold a portion of their Class B-1 units to Intermediate Holdco in connection with the IPO.

•“Transaction Value” means the total gross dollars transacted by our partners on our platform.

•“Vertical” means a market dedicated to a specific set of products or services sold to end consumers. Examples include property & casualty insurance, life insurance, health insurance, and travel.

•“White Mountains” means White Mountains Insurance Group, Ltd. and its affiliates.

•“Yield” means the return to our sellers on their inventory of Consumer Referrals sold on our platform.

Cautionary Statement Regarding Forward-Looking Statements and Risk Factor Summary

We are including this Cautionary Statement to caution investors and qualify for the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 (the “Act”) for forward-looking statements. This Annual Report on Form 10-K contains forward-looking statements. These forward-looking statements reflect our current views with respect to, among other things, future events and our financial performance. These statements are often, but not always, made through the use of words or phrases such as “may,” “should,” “could,” “predict,” “potential,” “believe,” “will likely result,” “expect,” “continue,” “will,” “anticipate,” “seek,” “estimate,” “intend,” “plan,” “projection,” “would,” and “outlook,” or the negative version of those words or other comparable words or phrases of a future or forward-looking nature. These forward-looking statements are not historical facts, and are based on current expectations, estimates and projections about our industry, management’s beliefs and certain assumptions made by management, many of which, by their nature, are inherently uncertain and beyond our control. Accordingly, we caution you that any such forward-looking statements are not guarantees of future performance and are subject to risks, assumptions and uncertainties that are difficult to predict. Although we believe that the expectations reflected in these forward-looking statements are reasonable as of the date made, actual results may prove to be materially different from the results expressed or implied by the forward-looking statements.

There are or will be important factors that could cause our actual results to differ materially from those indicated in these forward-looking statements, including, but not limited to, the following:

•Our ability to attract and retain supply partners and demand partners to our platform and to make available quality Consumer Referrals at attractive volumes and prices to drive transactions on our platform;

•Our reliance on a limited number of supply partners and demand partners, many of which have no long-term contractual commitments with us, and any potential termination of those relationships;

•Fluctuations in customer acquisition spending by property and casualty insurance carriers due to unexpected changes in underwriting profitability as the carriers go through cycles in their business;

•Existing and future laws and regulations affecting the property & casualty insurance, health insurance and life insurance verticals;

•Changes and developments in the regulation of the underlying industries in which our partners operate;

•Competition with other technology companies engaged in digital customer acquisition, as well as buyers that attract consumers through their own customer acquisition strategies, third-party online platforms or other traditional methods of distribution;

•Our ability to attract, integrate and retain qualified employees;

•Reductions in DTC digital spend by our buyers;

•Mergers and acquisitions could result in additional dilution and otherwise disrupt our operations and harm our operating results and financial condition;

•Our dependence on internet search companies to direct a significant portion of visitors to our suppliers’ websites and our proprietary websites;

•The impact of broad-based pandemics or public health crises, such as COVID-19;

•The terms and restrictions of our existing and future indebtedness;

•Disruption to operations as a result of future acquisitions;

•Our failure to obtain, maintain, protect and enforce our intellectual property rights, proprietary systems, technology and brand;

•Our ability to develop new offerings and penetrate new vertical markets;

•Our ability to manage future growth effectively;

•Our reliance on data provided to us by our demand and supply partners and consumers;

•Natural disasters, public health crises, political crises, economic downturns, or other unexpected events;

•Significant estimates and assumptions in the preparation of our financial statements;

•Potential litigation and claims, including claims by regulatory agencies and intellectual property disputes;

•Our ability to collect our receivables from our partners;

•Fluctuations in our financial results caused by seasonality;

•The development of the DTC insurance distribution sector and evolving nature of our relatively new business model;

•Disruptions to or failures of our technological infrastructure and platform;

•Failure to manage and maintain relationships with third-party service providers;

•Cybersecurity breaches or other attacks involving our systems or those of our partners or third-party service providers;

•Our ability to protect consumer information and other data and risks of reputational harm due to an actual or perceived failure by us to protect such information and other data;

•Risks related to changes in tax laws or exposure to additional income or other tax liabilities could affect our future profitability;

•Risks related to being a public company;

•Risks related to internal control on financial reporting;

•Risks related to shares of our Class A common stock;

•Risks related to our intention to take advantage of certain exemptions as a “controlled company” under the rules of the NYSE, and the fact that the interests of our controlling stockholders (White Mountains, Insignia, and the Founders) may conflict with those of other investors;

•Risks related to our corporate structure; and

•The other risk factors described under “Risk factors.”

The foregoing factors should not be construed as exhaustive and should be read together with the other cautionary statements included in this Annual Report on Form 10-K. If one or more events related to these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, actual results may differ materially from what we anticipate. Many of the important factors that will determine these results are beyond our ability to control or predict. Accordingly, you should not place undue reliance on any such forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made, and, except as otherwise required by law, we do not undertake any obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise. New factors emerge from time to time, and it is not possible for us to predict which will arise. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

PART I

Except as otherwise indicated or required by the context, all references in this Annual Report to the “Company,” “MediaAlpha,” “we,” “us” and “our” refer to (i) QL Holdings, LLC and its consolidated subsidiaries prior to the completion of our initial public offering and (ii) MediaAlpha, Inc. and its consolidated subsidiaries following the completion of our initial public offering on October 30, 2020.

Item 1. Business.

Our Company

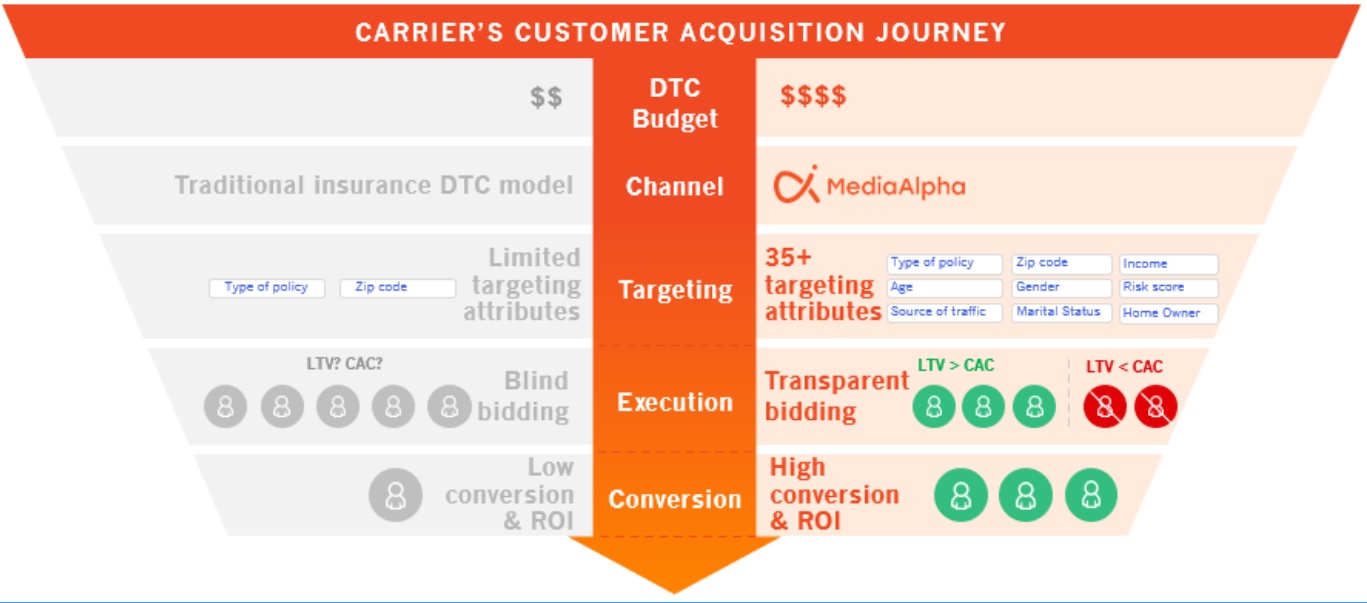

Our mission is to help insurance carriers and distributors target and acquire customers more efficiently and at greater scale through technology and data science. Our technology platform brings leading insurance carriers and high-intent consumers together through a real-time, programmatic, transparent, and results-driven ecosystem. We believe we are the largest online customer acquisition platform in our core verticals of property & casualty (“P&C”) insurance, health insurance, and life insurance, supporting $696 million in Transaction Value(1) across our platform from these verticals during the year ended December 31, 2022.

We believe in the disruptive power of transparency. Traditionally, insurance customer acquisition platforms operated in a black box. We recognized that consumers may be valued differently by one insurer versus another; therefore, insurers should be able to determine pricing granularly based on the value that a particular customer segment is expected to bring to their business. As a result, we developed a technology platform that powers an ecosystem where buyers and sellers can transact with full transparency, control, and confidence.

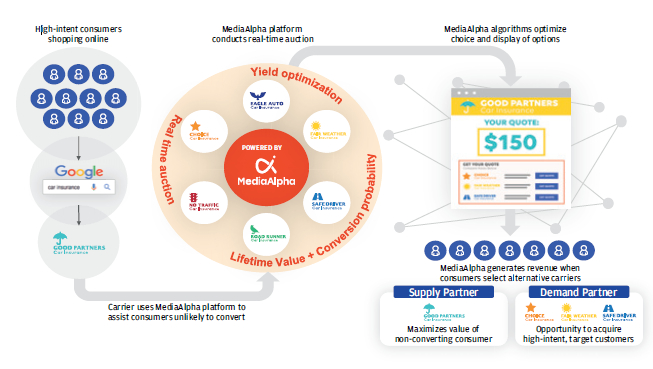

We have multi-faceted relationships with top-tier insurance carriers and distributors. A buyer or a demand partner within our ecosystem is generally an insurance carrier or distributor seeking to reach high-intent insurance consumers. A seller or a supply partner is typically an insurance carrier looking to maximize the value of non-converting or low LTV consumers, or an insurance-focused research or other financial destination looking to monetize the high-intent shoppers on their websites. Our model’s versatility allows for the same insurance carrier or distributor to be both a demand and supply partner, which deepens the partner’s relationship with us. In fact, it is this supply partnership that presents insurance carriers with a highly differentiated monetization opportunity, enabling them to capture revenue from website visitors who either do not qualify for a policy or otherwise may be more valuable as a potential referral to another carrier.

For the year ended December 31, 2022, we had 15 of the top 20 largest auto insurance carriers by customer acquisition spend as demand partners on our platform, accounting for 25% of our revenue. Of these demand partners, 60% were also supply partners in our ecosystem. During 2022, an average of 26.0 million consumers shopped for insurance products through the websites of our diversified group of supply partners and our proprietary websites each month, producing an average of over 7.5 million Consumer Referrals on our platform each month.

We believe our technology is a key differentiator and a powerful driver of our performance. We maintain deep, custom integrations with partners representing the majority of our Transaction Value, which enable automated, data-driven processes that optimize these partners’ customer acquisition spend and revenue. Through our platform, our insurance carrier partners can target and price across over 35 separate consumer attributes to manage customized acquisition strategies. Our platform’s granular price management tools and robust data science capabilities enable our insurance partners to target consumers based on a precise calculation of the expected lifetime value of the consumer to that partner and to make real-time, automated customer acquisition decisions.

We built our business model to align the interests of all parties participating on our platform. We generate revenue by earning a fee for each Consumer Referral sold on our platform. Our revenue is generally not contingent on the sale of an insurance product to the consumer.

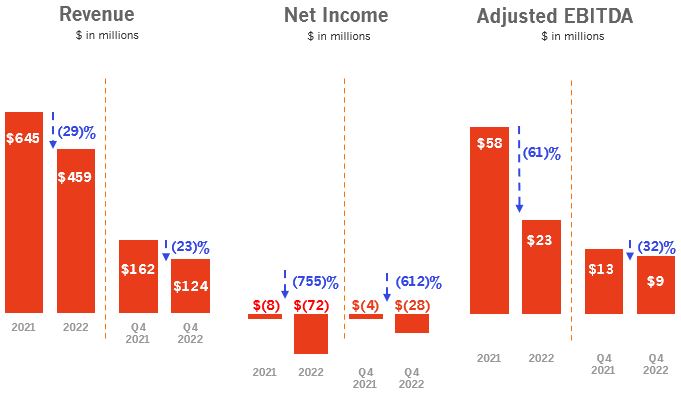

We have historically delivered strong growth in our Transaction Value and revenue, enabled by our unique business model and technology platform. However, for the year ended December 31, 2022, we generated $737.5 million of Transaction Value and $459.1 million of revenue, representing decreases of 27.6% and 28.9%, respectively, compared with the year ended December 31, 2021 as challenging conditions in the personal auto insurance industry continued to pressure P&C carrier underwriting profitability and in turn customer acquisition investments on our platform. Beginning in the second half of 2021 and continuing into 2022, many of our demand partners in our P&C vertical experienced higher-than-expected underwriting losses driven by inflation in automobile replacement and repair costs as well as by elevated claims costs from Hurricane Ian, leading them to reduce their customer acquisition spend until they obtain approval of premium increases from state regulators. We believe we are poised to capitalize on the continued shift among P&C carriers to direct, digital distribution when their underwriting profitability recovers.

In our health and life insurance verticals, we continue to capitalize on the shift to direct, digital distribution. We aim to drive deeper adoption and integration of our platform within the insurance ecosystem to continue delivering strong results to our partners. While our focus remains on insurance, we plan to continue to grow opportunistically in sectors with similar market dynamics. During the year ended December 31, 2022, we closed the acquisition of substantially all of the assets of Customer Helper Team, LLC ("CHT"), a provider of customer generation and acquisition services for Medicare insurance, automobile insurance, health insurance, and life insurance. We believe the acquisition is a good strategic fit with our long-term

We designed our business model to be capital efficient, with high operating leverage and cash flow conversion. We have funded our growth primarily through internally generated cash flow with no outside primary capital. Our strong cash flow generation is driven by (i) the nature of our revenue model, which is fee based and generated at the time a Consumer Referral is sold, and (ii) our proprietary technology platform, which is highly scalable and requires minimal capital expenditures ($0.1 million and $0.7 million for the years ended December 31, 2022 and 2021, respectively).

The foundation of our success is our company culture. Personal development is critical to our team’s engagement and retention, and we continually invest to support our core values of open-mindedness, intellectual curiosity, candor, and humility. This has resulted in a growth-minded team, with low turnover, committed to building great products and the long-term success of our partners.

Our market opportunity

Insurance is one of the largest industries in the United States, with attractive growth characteristics and market fundamentals. Insurance companies wrote over $2 trillion in premiums in 2021, growing at a 9% CAGR from 2018, according to S&P Global Market Intelligence. Demand for insurance products is stable, due to, in many instances, coverage being mandated by law (for example, auto insurance) or federally subsidized (for example, senior health insurance). The insurance industry as a whole is highly competitive and invests heavily in customer acquisition. Total customer acquisition spend in the insurance industry was estimated to be $146 billion in 2021 and is expected to grow to approximately $176 billion by 2025, according to William Blair.

Our technology platform was created to serve and grow with our insurance end markets. As such, we believe secular trends in the insurance industry will continue to provide strong tailwinds for our business.

•Direct-to-consumer is the fastest growing insurance distribution channel. In the auto insurance industry, there are carriers focused on DTC distribution (such as Progressive and GEICO) and carriers focused more on traditional, agent-based distribution (such as State Farm, Liberty Mutual and Allstate). DTC carriers accounted for approximately 31% of industry premiums in 2019, up from approximately 23% in 2013, according to S&P Global Market Intelligence. This industry shift to more direct distribution is accelerating. A major driver of this growth has been the DTC carriers’ outsized investments, relative to peers, in direct customer acquisition channels. According to S&P Global Market Intelligence, GEICO’s customer acquisition spend increased from $1.7 billion in 2018 to $2.1 billion in 2021, representing 20% growth, and Progressive’s customer acquisition spend increased from $1.3 billion in 2018 to $1.9 billion in 2021, representing 45% growth. Traditional, agent-based carriers have responded by investing more heavily in direct customer acquisition efforts themselves, as well as launching digital brands (such as Nationwide and Spire), acquiring

digital agencies (such as Prudential and AssuranceIQ), or acquiring digital insurers (such as Allstate and Squaretrade).

Similarly, tech-enabled distribution businesses focused on health and life insurance, such as eHealth, GoHealth and SelectQuote, have also emerged in recent years. These companies advertise to and acquire customers primarily through digital means and rank among the largest distribution platforms for health and life insurance products.

•More insurance consumers are shopping online. Consumers are increasingly using the internet not just for research and price discovery, but to purchase insurance as well. The J.D. Power 2021 U.S. Insurance Shopping Study suggests that 88% of consumers are open to purchasing their auto insurance online. By comparison, a decade ago, only 35% of consumers who had not made an online auto insurance policy purchase in the past said they would consider doing so in the future, according to the Comscore 2010 Online Auto Insurance Shopping Report. This shift is not only prevalent among younger insurance shoppers. According to LexisNexis Insurance Demand Meter, consumers 56 and older were the fastest growing group of online auto insurance shoppers in 2020.

•Insurance customer acquisition spending is growing. Total insurance customer acquisition spending was estimated to be $146 billion in 2021 and is expected to grow to $176 billion by 2025, according to William Blair. In fact, two of the top five most-advertised brands in the U.S. across traditional and online channels are insurance companies—Progressive and GEICO. According to S&P Global Market Intelligence, Progressive’s customer acquisition spend was $1.9 billion in 2021, while GEICO’s customer acquisition spend was nearly $2.1 billion in the same period. In the face of such aggressive spending and customer acquisition by DTC carriers such as Progressive and GEICO, agent-based carriers are compelled to spend heavily to remain competitive.

•Digital customer acquisition spending by insurers has plenty of headroom. According to William Blair, insurance carriers allocate a lower percentage of their advertising budgets to digital channels than other industries. While the advertising industry as a whole allocates approximately 65% of their budgets to digital, insurers allocated less than 20% of their budgets to digital channels in 2020. Industry analysts expect digital marketing spend by the insurance industry to narrow this gap significantly over time as carriers increase their adoption of digital channels.

•Carriers and distributors are increasingly focused on optimizing customer acquisition budgets. Mass-market customer acquisition spend is becoming more costly, leading carriers and distributors to increasingly focus on optimizing customer acquisition spend. They are able to do so by adopting more sophisticated customer acquisition strategies enabled by data science. A significant percentage of marketers believe the inability to measure customer acquisition impact across channels and campaigns is one of their biggest challenges in demonstrating customer acquisition performance. We believe there is growing demand for improved transparency of Consumer Referral quality, for carriers to secure higher quality Consumer Referrals online, and for the ability to manage consumer acquisition spend across multiple vendors.

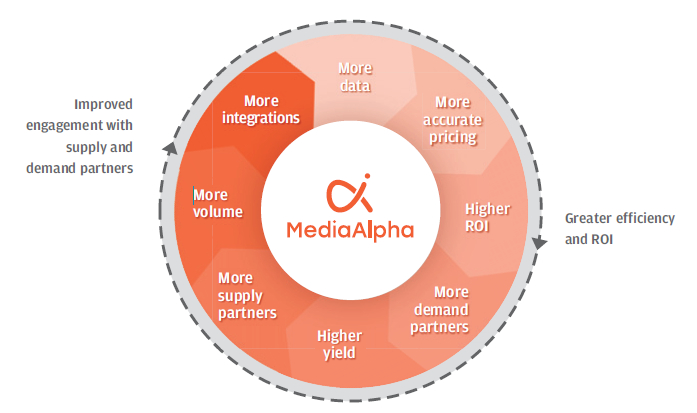

MediaAlpha is poised to capitalize on these trends. We believe that we provide the leading technology platform enabling insurance carriers and distributors to efficiently acquire customers online at scale. Our platform allows buyers to target consumers granularly and to determine their pricing based on how they value various consumer segments. Buyers leveraging our data science capabilities make value-maximizing decisions on how to acquire customers. This results in greater customer acquisition efficiency and better return on investment, allowing us to attract more buyers into the ecosystem. Simultaneously, we provide our supply partners the insights and tools they need to drive competition for their high-intent consumers and maximize yield, which draws more supply partners into the ecosystem, providing our buyers with even more high-quality demand sources. As both demand and supply partners begin to see the benefits of the platform, we deepen our relationships with them through additional integrations that drive more data into the platform. All of this creates the powerful “flywheel” effect that has propelled our business forward as a result of the value created within our ecosystem.

Our platform

We have created one of the largest global insurance customer acquisition technology platforms. For the year ended December 31, 2022, we had $737.5 million in Transaction Value and served over 950 total insurance partners, excluding our partners within our agent business. For the year ended December 31, 2021, we had $1.0 billion in Transaction Value and served over 900 total insurance partners, excluding our partners within our agent business.

During 2022, over 312 million high-intent consumers shopped for insurance products on the websites of sellers on our platform and our proprietary websites, resulting in over 90 million Consumer Referrals acquired by buyers on our platform. We serve over 600 buyer partners, excluding our buyer partners within our agent business. Our platform was designed for multiple Consumer Referral products and flexible deployment models to best serve the varying needs of our partners.

Insurance carriers access our platform through a self-service web interface that enables them to manage customer acquisition strategies across all sources of Consumer Referrals, efficiently and with full transparency. Our platform provides insurance companies sophisticated targeting capabilities for efficient customer acquisition. Further, it offers our carrier partners the ability to offset their customer acquisition costs by using predictive analytics to identify and refer non-converting consumers to other carriers, delivering better returns on investment relative to traditional channels.

We connect insurance companies with websites where consumers shop for insurance. Insurance carriers and distributors are able to target high-intent consumers when they are actively shopping for insurance. Our end consumers typically access our partners’ websites or our proprietary websites looking for an insurance quote, where they volunteer relevant data in connection with their quote request. Our platform then controls the matching of these consumers with insurance companies, presenting them with multiple brands to choose from. We believe the rich data available with every consumer quote request gives our platform the unparalleled ability to direct each Consumer Referral to the right set of carriers. We maximize value to both demand and supply partners by allowing insurance companies to reach consumers when they are actively shopping at the point of purchase and precisely target granular consumer segments using rich data.

We enable insurance companies to reach and acquire new customers in multiple ways. In our platform, end consumers can engage with insurance companies through multiple touchpoints based on their preferences. Our platform enables consumers to (i) proceed to an insurance carrier’s website on a self-directed basis to purchase a policy (click), (ii) engage with an insurance carrier or agent via phone (call), or (iii) submit their data to insurance companies to receive inbound inquiries (lead). Our platform’s flexibility in turn enables insurance carriers to acquire and convert consumers through one or more touchpoints, depending on their strengths and preferences.

The following table presents the percentages of total Transaction Value generated from clicks, calls and leads for the year ended December 31, 2022 and 2021:

| | | | | | | | | | | | | | |

| | Year ended

December 31, |

| | 2022 | | 2021 |

| Clicks | | 75.3 | % | | 79.3 | % |

| Calls | | 15.3 | % | | 9.5 | % |

| Leads | | 9.4 | % | | 11.3 | % |

Our platform leverages precise data and data science for maximum efficiency. Insurance carriers use precise data to target and price consumer segments across demographic and geographic attributes on a source transparent basis. This allows insurance carriers to pay the right price for each Consumer Referral based on their business objectives. Insurance carriers integrate with our platform to provide real-time conversion feedback, allowing them to measure returns on their spending granularly and execute algorithmic optimization of customer acquisition cost based on the expected LTV of the customer. Increasing the number and depth of our conversion data integrations with our partners remains a key part of our strategy.

Insurance carriers are able to extract the maximum value from each consumer opportunity. We have extensive data integrations with our partners to support efficient customer acquisition. These data integrations allow us to more seamlessly transact a Consumer Referral by taking information an end consumer has already provided and pre-populating it into an insurance carrier’s purchase process, potentially increasing policy conversion rates. This enhances the value of the Consumer Referral to our insurance carriers, adding significant value to all parties in our platform. As of December 31, 2022, we had 90 buyers with this type of integration in place for active and future campaigns, representing 64% of the total Transaction Value from our insurance verticals for the year then ended. Increasing the number and depth of our data integrations with our partners remains a key part of our strategy, and we believe this number will increase as our platform grows.

Our transaction models. We transact with our demand partners and supply partners through two operating models, Open Marketplace and Private Marketplace. In our Open Marketplace transactions, we have separate agreements with demand partners and suppliers and have control over the Consumer Referrals that are sold to our demand partners. In our Private Marketplace transactions, demand partners and suppliers contract with one another directly, and we earn fees from our supply partners based on the value of the Consumer Referrals transacted on our platform. For more information regarding these arrangements, see “Management’s discussion and analysis-Key components of our results of operations-Revenue.” Our technology

Our product is a technology platform that allows insurance carriers and distributors to acquire customers and optimize customer acquisition costs to align with expected customer LTV, in a single data-rich but user-friendly environment. Our technology is what enables our growth, scale, and operating leverage, and is a key part of what differentiates us from our competitors. It is also what enables our partners to scale their customer acquisition and monetization efficiently and with minimal operating overhead. With over 90 million paid transactions on our platform in 2022, we believe we offer the largest source of Consumer Referrals in the insurance sector.

Our product is a robust, real-time customer acquisition and data analytics platform. It is fueled by rich, anonymized consumer data provided by our extensive data integrations with our partners. At the heart of our platform is a set of proprietary predictive analytics algorithms that incorporate hundreds of variables to generate conversion probabilities for each unique consumer, enabling our partners to align customer acquisition costs with expected customer LTV across the platform.

Our platform architecture is elegant, scalable, and vertical agnostic, which has enabled us to innovate rapidly in our core insurance verticals and grow opportunistically across sectors with similarly attractive attributes. We continuously invest in our technology and believe that our focus on innovation enhances our competitive position.

We believe the following attributes collectively differentiate the MediaAlpha technology platform:

Multiple high-quality Consumer Referrals accessible through a single platform with transparent pricing and control. Most insurance carriers and distributors today have multiple sources for customer acquisition. These sources offer a wide range of Consumer Referral quality and, in most cases, must be managed manually and separately by insurance carriers. Our platform allows users to access multiple sources of Consumer Referrals transparently through a unified platform with a single sign-on, creating scale and operational efficiencies.

Proprietary user data integrated in a secure environment. Our platform allows buyers to fully integrate first-party consumer data to enhance targeting parameters, bidding granularity, and conversion tracking, resulting in more accurate customer acquisition and LTV predictions. We maintain robust data security protections and preserve the confidentiality of each insurance carrier’s customer acquisition strategy. We are able to seamlessly aggregate this data across all of our users to enhance our data analytics models while maintaining end-consumer confidentiality. We believe this has allowed us to continue strengthening our rich consumer database and analytics platform and to maintain strong relationships with our partners.

Robust data science tools to optimize customer acquisition. Our unique search and conversion datasets enable automated, algorithmic customer acquisition optimizations. As our platform grows and processes more customer acquisition transactions, we gather more conversion data to further refine our predictive analytics algorithms. This further enhances our platform’s capability to predict our partners’ expected return per consumer and support more efficient customer acquisition strategies. We believe this creates a flywheel effect by which the attractiveness and value of our platform will continue to grow as we scale our marketplaces.

Self-service model. We offer a self-service model that empowers our partners to directly manage the buying and selling process independently. Supply partners can easily manage their digital consumer traffic on our platform, while demand partners can direct their consumer acquisition spend in real time with minimal involvement from our team. We believe this enables us to scale efficiently without requiring significant investments in sales and support functions.

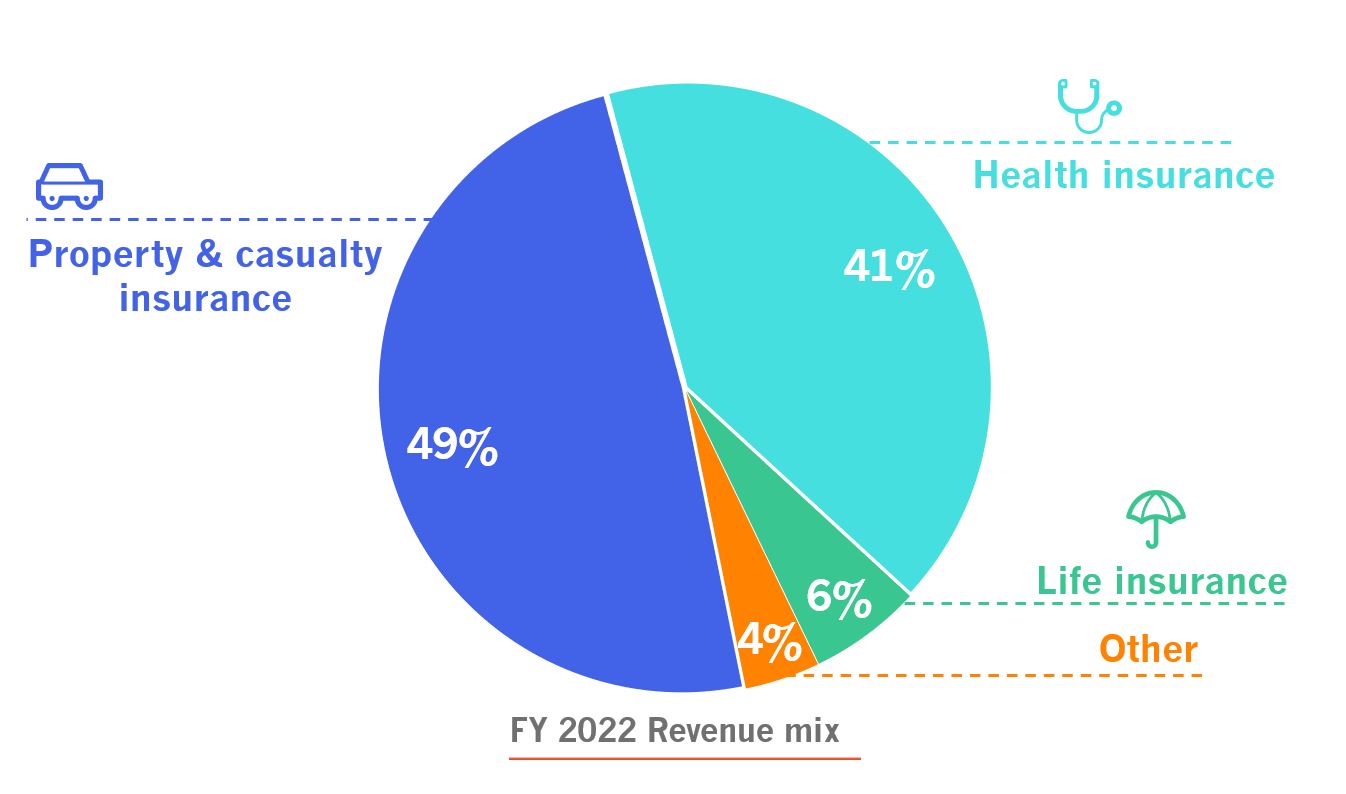

Highly extensible and scalable platform. Our platform and industry-agnostic technology enables us to quickly expand our operations into existing and adjacent verticals with minimal investments. We have organically scaled the P&C insurance vertical and the health and life insurance verticals to $399.9 million and $296.0 million in Transaction Value, respectively, for the year ended December 31, 2022. While our primary focus remains on insurance, we intend to continue to grow opportunistically in sectors with similar, attractive market fundamentals. We believe our proprietary technology will allow us to react nimbly to growing demands and opportunities in emerging verticals.

Our target audience

Our buyers: Our demand partners are insurance carriers and distributors looking to target high-intent consumers deep in their purchase journey. Repeat buyers continue to be a strong driver of our business, with 92% of our Transaction Value for 2022 driven by repeat buyers from 2021 (with total Transaction Value from such repeat buyers decreasing 37% in 2022) and 97% of our Transaction Value for 2021 driven by repeat buyers from 2020. Annual spend per demand partner on our platform with over $1 million in Transaction Value was $9.0 million in 2020 and $9.1 million in 2021, but declined to $6.3 million in 2022, driven by a reduction in marketing spend by our top insurance partners due to significant declines in their underwriting profitability.

Our value proposition for buyers

•Efficiency at scale. We believe we operate the insurance industry’s largest customer acquisition platform, delivering the volume insurance companies need to drive profitable growth, while also providing precise targeting capabilities to ensure they connect with the right prospects. We believe this gives our demand partners the ability to realize greater efficiencies relative to other customer acquisition channels.

•Granular and transparent control. Our platform allows for real-time, granular control and full source transparency with every buying and pricing decision. We believe this gives our buyers the flexibility they need to realize favorable LTV relative to customer acquisition costs to maximize their revenue opportunities and the effectiveness of their marketing investments.

•Unparalleled partnership. With a fully managed service option, custom integrations, and industry-leading technology, we are dedicated to providing long-term value to our demand partners’ businesses. We have designed our platform to put the best interests of our partners first, fostering a healthy ecosystem within which buyers can transact with confidence.

Our Sellers: Our supply partners use our platform to monetize their digital consumer traffic. Our supply partners are primarily insurance carriers looking to maximize the value of non-converting or low LTV consumers, and insurance-focused research destinations and financial websites looking to monetize high-intent customers. Repeat sellers continue to be a strong driver of our business, with 98% of our Transaction Value for 2022 driven by repeat sellers from 2021 (with Transaction Value from such repeat sellers declining 27% in 2022) and 99% of our Transaction Value for 2021 driven by repeat sellers from 2020. Annual spend per supply partner on our platform representing over $1 million in Transaction Value annually has declined, from $11.9 million in 2020 and $13.9 million in 2021 to $9.5 million in 2022, due to a reduction in demand driven by reduced marketing spend from insurance advertisers on our platform.

Our value proposition for sellers

•Yield maximization. Our proprietary technology platform provides sellers with a suite of optimization tools, as well as inventory and buyer management features, that maximize competition for, and yield from, their high-intent consumers.

•Predictive analysis. Through our platform’s advanced predictive analysis and data science capabilities, sellers can assess conversion probabilities and expected customer LTV for every consumer in real time. We believe the integration of these data science models with our sellers’ user experience decision engines is a unique differentiator of our business.

•Real-time insights. We provide our sellers with unique data as to the type of consumer segments each buyer values. By providing in-depth reporting and real-time, granular insights, our sellers have the ability to continuously optimize their own customer acquisition and monetization decisions.

Our End Consumers: Our end consumers are primarily high-intent, online insurance shoppers. Due to the broad participation of top-tier insurance carriers within our ecosystem, consumers are able to more efficiently navigate a range of options and offers relevant to their policy searches. During the year ended December 31, 2022, over 312 million high-intent consumers shopped for insurance products through the websites of sellers on our platform and our proprietary websites.

Our value proposition for end consumers

•Search relevancy. By enabling insurance carriers and distributors to apply sophisticated targeting, we facilitate the delivery of hyper-relevant product options to our end consumers based on consumer-provided demographics and other relevant characteristics. We believe this improves the overall research and purchase experience and helps enable our end consumers to make better decisions.

•Shopping efficiency. We facilitate access to the most relevant products for each respective end consumer, allowing for minimal research and maximum efficiency, through an omni-channel, seamless consumer platform experience. We enable consumers to comparison shop and interact with insurance carriers and distributors through multiple mediums, including directly online or offline.

Our strengths

We believe that our competitive advantages are based on the following key strengths:

•Highly scalable, innovative technology platform with rich data. Our proprietary platform is built to be highly extensible and flexible, enabling us to quickly and efficiently develop custom solutions and tools to address the varying and evolving needs of our partners. Supported by our proprietary algorithms, our platform is able to provide continuous, real-time feedback and insights that buyers can use to maximize the value of every consumer opportunity. Our deep data integrations allow our buyers to utilize millions of anonymized data points to target and acquire their desired customers with a unique level of precision and control. As of December 31, 2022, there were over 400 insurance supply partners on our platform. We also provide our supply partners with sophisticated, data-driven yield management and monetization capabilities. We believe these capabilities are critical to our partners’ monetization strategies, as they enable optimization of business performance and revenue. Our platform is vertical agnostic, allowing us to quickly and easily expand into new markets with attractive attributes.

The increased participation in our technology-driven platform will continue to generate valuable data, enhance feedback loops, and drive stronger results for all participants in the ecosystem. We believe this creates a flywheel effect as our platform continues to grow.

•Superior operating leverage. We designed our business to be highly scalable, driving sustainable long-term growth that delivers superior value to both demand and supply partners. Our technology enables us to grow in a highly capital efficient manner, with minimal need for working capital or capital expenditure investment. In 2022, we employed an average of 164 individuals, who produced $737.5 million of Transaction Value ($4.5 million per employee), $72.4 million of net loss ($0.4 million per employee), and $22.9 million of Adjusted EBITDA ($0.1 million per employee) and in 2021, we employed 138 individuals on average who drove $1.0 billion of Transaction Value ($7.4 million per employee), $8.5 million of net loss ($0.1 million per employee), and $58.2 million of Adjusted EBITDA ($0.4 million per employee) for the year.

•Sticky, tenured relationships with insurance carriers and distributors. We have developed multi-faceted, deeply-integrated partnerships with insurance carriers and distributors, who can be both buyers and sellers on our platform. We enable insurance carriers and distributors as buyers to optimize their customer acquisition spend by offering source-level transparency, granular controls, and predictive tools to drive measurably superior performance. When we work with carriers and distributors as sellers, we enable them to use data science to turn high-intent policy shoppers unlikely to purchase a policy from that specific carrier or distributor into highly valuable Consumer Referrals for other carriers or distributors, thereby offsetting a portion of their total customer acquisition costs.

We believe the versatility and breadth of our offerings, coupled with our focus on high-quality products, provide significant value to insurance carriers and distributors, resulting in strong retention rates. As a result, many insurance carriers and distributors use our platform as their central hub for broadly managing digital customer acquisition and monetization.

Our relationships with our partners are deep, long standing, and involve top-tier insurance carriers in the industry. 15 of the top 20 largest auto insurance carriers by customer acquisition spend are demand partners on our platform. In 2022, 92% of total Transaction Value executed on our platform came from demand partner relationships in existence during 2021. In 2021, 97% of total Transaction Value executed on our platform came from demand partner relationships in existence during 2020.

•Culture of transparency, innovation, and execution. Since inception, our co-founders have led with the vision of bringing unparalleled transparency and efficiency to the online customer acquisition ecosystem, executed through a powerful technology-enabled platform. Transparency is built into our platform and is at the heart of our culture, enabling us to focus on sustainable long-term success over near-term wins. We are relentless about continuous innovation and aim to use our platform to solve big industry-wide problems. We are data-driven and focused on delivering measurable results for our partners. We believe that our long-term vision, dedication to solving systemic problems in the industry, and our relentless drive to improve, will continue to empower us to be the platform of choice for our partners.

Our growth opportunities

We intend to grow our business through the following key areas:

•Increase Transaction Value from our partners. We aim to increase overall Transaction Value from our partners across our insurance verticals by continuously improving the volume and accuracy of customer conversion data analyzed in our platform, eliminating friction between consumer handoffs, and developing additional tools and features to increase engagement. We believe that providing our platform participants with better value and a larger selection of high-quality Consumer Referrals over time will lead to increased spending on our platform.

•Improve ecosystem efficiency. We believe that traditional customer acquisition models are highly inefficient, charging platform users inflated prices while lacking the transparency and granularity to allow participants to reach end consumers effectively. Our platform is designed to disrupt and address these systemic inefficiencies by enhancing automated buying strategies and granular price discovery processes. We will continue to expand our platform and drive value for all participants within the ecosystem by increasing the number and depth of data integrations with our partners.

•Bring new partners to our platform. There are potential buyers and sellers who are not yet using our platform, and new companies are being formed every year. We intend to gain adoption of our platform with new insurance partners through business development, word-of-mouth referrals, and inbound inquiries.

•Grow our product offerings. We are constantly exploring new ways to deliver value to our partners through development of new tools and services and improvement of our conversion analytics model. We believe that providing further customized solutions and higher touch services for our partners will enhance the stickiness of our offerings and drive more customer acquisition spend and users to our platform.

•Deepen our relationships with agents. We intend to strategically expand our insurance agency relationships to capture additional customer acquisition spend within our core insurance verticals. We have a dedicated team working to incorporate agents into our digital platform and help them expand their customer acquisition capabilities. We generated over 90 million Consumer Referrals in the year ended December 31, 2022, equipping us with valuable conversion insights to help us optimize consumer routing to agents based on their desired goals. This dedicated team will continue to enhance our agency capabilities.

•Expand into and scale new verticals. While we are currently focused on growing our core insurance verticals, we continue to seek expansion opportunities in markets that share similar characteristics. We believe our vertical-agnostic platform and established playbook for entering new markets will allow us to capture attractive market opportunities effectively if we decide to pursue such opportunities.

Our competition

We operate in the broadly defined tech-enabled insurance distribution sector. We are part of a sector that is disrupting the conventional agent-based insurance distribution channels. This sector is comprised of companies engaged in varied aspects of customer acquisition. On one end of the spectrum, there are companies that are engaged in simple Consumer Referrals acquisition, which they sell to insurance carriers or distributors. On the other end of the spectrum, there are companies that acquire the customer through digital channels and take them through the entire needs-based assessment and policy application and submission process.