UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

For

the fiscal year ended

or

For the transition period from [____] to [____]

Commission

file number

(Exact name of registrant as specified in its charter)

State or other jurisdiction of incorporation or organization |

(I.R.S. Employer Identification No.) | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s

Telephone number, including area code:

Securities registered pursuant to Section 12(b) of the Act:

| Title of Class | Trading Symbol (s) | Name of each exchange on which registered | ||

Securities registered pursuant to Section 12(g) of the Act:

| Title of Each Class | Name of Each Exchange On Which Registered | |

| N/A | N/A |

Indicate

by check mark if the registered is a well-known seasonal issuer, as defined in Rule 405 the Securities Act Yes ☐

Indicate

by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act Yes ☐

Indicate

by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2)

has been subject to such filing requirements for the last 90 days.

Indicate

by check mark whether the registrant has submitted electronically, every Interactive Data File required to be submitted and posted pursuant

to Rule 405 of Regulation S-K (§229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant

was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definition of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If

an emerging growth company, indicate by a check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act

Indicate

by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness

of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered

public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate

by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐

The

aggregate market value of common stock held by non-affiliates of the registrant based on the closing price of the registrant’s

common stock as reported on the Nasdaq Capital Market on June 30, 2022, was $

Indicate the number of shares outstanding of each of the registrant’s classes of common stock as of the latest practicable date.

As of March 10, 2023, shares of the registrant’s common stock, par value $0.0001 per share, were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

TABLE OF CONTENTS

| 2 |

Cautionary Note Regarding Forward-Looking Statements

This annual report contains forward-looking statements and information within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, which are subject to the “safe harbor” created by those sections. These forward-looking statements include, but are not limited to, statements concerning our strategy, future operations, future financial position, future revenues, projected costs, prospects and plans and objectives of management. The words “anticipates,” “believes,” “estimates,” “expects,” “intends,” “may,” “plans,” “projects,” “will,” “would” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain these identifying words. We may not actually achieve the plans, intentions, or expectations disclosed in our forward-looking statements and you should not place undue reliance on our forward-looking statements. Actual results or events could differ materially from the plans, intentions and expectations disclosed in the forward-looking statements that we make. These forward-looking statements involve risks and uncertainties that could cause our actual results to differ materially from those in the forward-looking statements, including, without limitation, the risks set forth in our filings with the SEC. The forward-looking statements are applicable only as of the date on which they are made, and we do not assume any obligation to update any forward-looking statements.

As used in this report, the terms “EzFill” “we”, “us”, “our” and “Company” mean EzFill Holdings, Inc. and/or our subsidiaries, unless otherwise indicated.

| 3 |

PART 1

Item 1. Business

Overview

EzFill is a leading on-demand fuel delivery company in Florida and the only mobile fueling company that combines on-demand fills and subscription services which fill customer vehicles on routine intervals. The emergence of the digital technology, GPS-Based / On-Demand consumer deliveries, and the sharp increase in home delivery of products and services during the COVID-era are trends expected to continue in the post-COVID economy. The increased adoption rate of such ‘at home’ or ‘at work’ delivery of products and services has become the method both individual and commercial customers prefer.

| EzFill provides customers in Florida the ability to have fuel delivered to their vehicles (cars, trucks, and specialty vehicles) without having to leave the comfort of their home, office, and job site. EzFill’s app-based platform conveniently brings the gas station to customers with a growing fleet of EzFill-branded, Mobile Fueling Trucks. EzFill’s business verticals align to the high-use, high demand cases in vehicle operations. These are; individual CONSUMERS, COMMERCIAL entities and SPECIALTY vehicle markets. |

An EzFill Mobile Delivery Truck |

For CONSUMERS, EzFill services individual “consumer” customers directly at their residences or places of work. In the consumer vertical, EzFill customers sign-up for EzFill services individually, or as part of employer which offer discounted EzFill services to their employees as an employee benefit while at work at offices, in office parks or on-job locations. Fuel deliveries are completed at optimal times during the day for ‘at work’ customers or at night for residential deliveries. | |

| In the COMMERCIAL vertical, EzFill provides vital fuel delivery services to commercial fleets of delivery trucks, rental cars, livery operators, and job sites. Deliveries for the commercial vertical are completed during down-times, when the majority of commercial vehicles are at designated locations. This method also allows EzFill to complete multiple fills at once, while providing the commercial customers the benefit of a fleet of fueled vehicles ready for operations on any given morning. | |

| In the SPECIALTY vertical, EzFill adapts to each market based on the type of vehicles that can benefit from “at location” fuel delivery. In EzFill’s home market, Florida, their “specialty” vertical services hundreds of boat owners at the marinas at which they are docked. EzFill’s specialty market also includes equipment rental companies, construction job sites, agricultural operations, motorsports events and recreational vehicle grounds. |

EzFill Model – Resolving Pain Points in the Consumer and Commercial Fuel Customer Markets

EzFill’s experience in this market indicates that the legacy gas station model is ripe for disruption specifically by a model which works to address major issues with the status of the industry, such as:

| ● | Convenience. People find going to the gas station inconvenient. Leaving the house, a little late in the morning on an empty tank means coming late to the office or stopping for gas on your way home after a long day. This number does not include the time it takes to drive to and from the gas station. Our solution saves our customers time and shaves time off of our customers commutes to and from work. Our Mobile Fueling Truck brings a convenient fueling solution that we expect to disrupt the current industry by saving our customers time and helping them to avoid the stress of not having a full tank of gas. |

| 4 |

| ● | Fleet Driver Expense. When fleet managers send their vehicles to the gas station to fill up, they are paying for: (i) the driver to take the vehicle to the gas station; (ii) the gas the vehicle consumes on the way to and from the gas station; (iii) wear and tear on the vehicle being driven to the gas station; and (iv) indirectly the downtime for the vehicle being driven to the gas station, which usually will be during the regular working day due to the fact that an employee must take the vehicle there. When fleet managers use EzFill, they only pay for gas, and we fill up the vehicles after hours so there is no downtime during the regular working day. | |

| ● | Fleet Driver Fraud. Research conducted by Fleet News confirmed the 64% of fleets have been the victims of fuel theft or fuel fraud. According to a survey conducted by Shell, 93% of fleet managers think that some of their drivers are committing fraudulent activity and 41% of fleet managers think that more than 10% of their drivers are committing fraudulent activity. According to Shell’s research, 48% of fleet managers think that improving practices to tackle fraud could reduce a fleet’s fuel spend by more than 5% and 14% of fleet managers believe it would reduce fuel spend by more than 10%. EzFill’s solution tackles fraud head on by taking the drivers out of the equation. EzFill brings the gas directly to our customers fleets and reduces the risk of driver related fuel fraud. | |

| ● | Operating Costs. The rising cost of real estate in major metros, over the past couple of years has caused many gas stations to close their doors, leaving major cities without significant competition, which could lead to higher local gas prices. According to data provided by Fueleconomy.gov there were 168,000 gas stations in 2004, compared to just 115,000 gas stations reported by marketwatch.com in February 2020 (a 31% drop). EzFill’s App-based approach lowers our underlying costs and allows us to offer gas with competitive pricing in each zip code in which we operate. | |

| ● | Safety Concerns. Gas stations have a reputation of being unsafe locations. This reputation developed due to the many robberies and assaults that occur at gas stations. According to FBI crime data, over the past five years 1.3% of all violent crimes occurred at gas stations. Violent crimes such as robberies and assaults are commonplace at gas stations because often, customer’s need to exit their vehicles in remote and secluded areas, at late hours, with improper lighting and security at the location. EzFill’s Mobile Fueling Trucks address these safety issues by bringing the gas to the consumer, who, from the comfort of their home or office can order a fill-up via our App without even going outdoors. The customer simply needs to place the order and leave the gas tank access open on their vehicle. | |

| ● | Fraud Concerns. Gas stations are hubs for fraud issues. These issues primarily emanate from gas stations employing mostly old-fashioned magnetic strip credit card readers. Gas stations experience hundreds of millions of dollars in credit card fraud annually. According to the Florida Department of Agriculture, more than 1500 skimmers were found at Florida gas stations in 2019. A study from FICO, found that fraud from credit card skimmers is increasing at a rate of 10% per year. The US Secret Service reports finding between 20 and 30 credit card skimmers at gas pumps, per week. EzFill’s platform does not store any customer credit card data and uses the latest in credit card processing technology to verify cards and secure customers’ payments to ensure authenticity of purchases. | |

| ● | Addressing Environmental Concerns. We can never eliminate our environmental exposure completely. However, by delivering fuel to areas with high vehicle density, we are lowering the environmental impact by reducing the number of separate trips our customers make to refuel their vehicles. Since EzFill sources direct from oil companies on a daily basis, we have a very high turnover of inventory and do not store our fuel in underground tanks. All our tanks go through a rigorous annual inspection, plus they are visually inspected before and after every shift to ensure proper fuel storage and no loss of vapors. A rapid turnover of inventory and daily tank inspections are not available for underground tanks used by retail gas stations. |

| 5 |

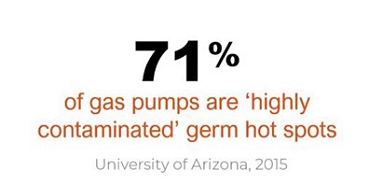

| ● | Sanitary and Touchless. According to a study conducted by the Kymberly Clark Group, the gas station pump handle is the dirtiest surface Americans touch on their way to work. Also, according to a recent study conducted by busbudy.com, gas station pumps have 11,000 times more bacteria than the common household toilet seat, while pump station buttons contain 15,000 times more. In addition to being germ and bacteria infested, a recent article by njtvonline.org highlighted the near impossibility of social distancing at self-service gas stations, further exacerbating the health risks of going to the gas station. Proper social distancing is required to help stop the spread of Covid-19. Our service is a sanitary and touch free way for our customers to get gas. We believe our service eliminates one of the dirtiest and most unhealthy places from our customers once mandatory to-do list. |  |

Our Product Offerings

We provide gas delivery via our Mobile Fueling Trucks in the greater South Florida area as well as in the West Palm Beach, Jacksonville, Tampa, and Orlando areas, and expect to soon begin fueling in other areas in Florida. Our goal is to service all our customers across all our lines of business at predictable locations during vehicle downtimes. Our fleet currently includes 24 Mobile Fueling Trucks that we utilize to deliver fuel directly to our customers. We have three major lines of business and to our knowledge we are the only company in the space which fuels all three verticals:

| 1. | SERVICING CONSUMERS AT HOME AND AT WORK |

We offer residential fueling services to customers who can request a fuel delivery through our app and have fuel delivered directly to their vehicle, from the comfort of their home or apartment building, while they go about their night. We offer convenient weekly schedules to our residential customers, so they can live with the comfort of knowing that they will never be without a full tank of gas when they need it. Additionally, because of our lower operational costs, our competitive pricing keeps our residential customers from having to travel out of their neighborhood for lower gas prices. Our residential customers currently pay a delivery fee or they have the option to pay a monthly subscription for unlimited deliveries. We currently offer delivery to residential customers in Miami-Dade, Broward, and Palm Beach counties, as well as the Tampa area. Our service is a great new amenity for condominiums, which has been widely used by residents of the buildings we service and has been enhancing residents’ experience.

Through entering agreements with local and national businesses, we work directly with businesses HR departments to offer employee perks, and fuel employees’ cars while they are working. This is a new and creative benefit for employers to offer, enabling their employees to have their cars filled, stress free. Additionally, we work directly with the landlords of corporate office parks to bring the amenity of EzFill to their tenants. Our corporate employee fueling is currently done at competitive prices with no delivery fee. Our corporate office park solution offers benefits to employers and EzFill. Benefits to employers include: (i) a new perk to offer their employees; and (ii) happier employees who do not have to waste precious time going to the gas station. Benefits to EzFill include: (i) multiple deliveries at one location creates efficiencies and cuts operating costs; (ii) the employers serve as “influencers” which reduces our marketing costs for each location; and (iii) push-marketing by the employers also results in more residential consumer fills.

| 2. | SERVICING COMMERCIAL ENTITIES |

We partner with and offer national and local businesses who operate fleets an alternative solution for fueling their fleet to reduce the businesses operational costs and improve fleet efficiency. Our solution for fleets helps businesses: (i) save money spent on expensive gas stations; (ii) save money on paying employees to go to gas stations; (iii) eliminate unnecessary wear and tear to Company fleet vehicles on trips to the gas station; (iv) better monitor their gas consumption; (v) eliminate employee mistakes (putting regular gas into a diesel engine); and (vi) prevent theft by employees (customers have reported instances where it was months before they realized their employee was making unauthorized charges on their fleet card).

We fuel fleets at night, so they are ready to go the next day. This way, drivers stay on the road when and where they are needed most, instead of spending idle time at a gas station. EzFill also reduces a driver’s Off Route Time, saving a company money as well as wear and tear on the company vehicles. The technology provided, including a customized Dashboard, monitors the fleet and simplifies invoicing for every customer.

The cost analysis makes this point even greater especially when taking in to account that EzFill’s prices are competitive with the local gas station.

| 6 |

| 3. | SERVICING SPECIALTY MARKETS |

EzFill delivers fuel directly to other, market-specific personal and commercial vehicles. In our home market, the prevalence of boats and boat owners was the first specialty market we developed, particular to the south Florida area which is the base of our services. Marina gas stations are some of the highest priced in the country. We offer low prices and pre-scheduling so our marine customers can get affordable fuel whenever they need it. The same is true for the markets which we have targeted to enter. In these markets we find similar, market-specific vehicles which our future customers use for; construction or agricultural purposes, personal or recreational vehicle use, motorsports, or other sporting events where a large concentration of vehicles can be serviced at specific locations.

Customers

In addition to our individual, residential customers, we also have structured relationships with property management companies and builders who co-market our services as a benefit to their residents and allow our trucks to enter their communities to fill vehicle owners at their single-family homes, condominiums, or apartments. Employers who have offered at-work fueling as a corporate perk have included Ryder, Norwegian Cruise Lines, Carnival Cruise Lines, Royal Caribbean, Telemundo, Loreal, Y Green, and more. Our services are very flexible, and our residential customers do not have to sign any long-term commitments with us and can decide not to use our service whenever they choose.

Our commercial vertical has serviced the fleets for many national and local businesses, such as a leading national delivery company, a leading national grocer, a leading OEM, Enterprise, Telemundo, Easy Scripts and Air Around the Clock

In our specialty market vertical, we service hundreds of boats at various marinas across Miami-Dade and Broward Counties, as well as boats at customers’ homes and recently began serving marine customers in the Tampa area. We are a preferred delivery partner for a mobile application with thousands of boat-owner users. We have recently begun developing this line of business and it is growing, mostly through existing customer outreach and strategic partnerships with marinas.

Software Systems, IT, User Interface and Experience

Our software systems provide us logistical and cost saving efficiencies that allow us to forecast the need for truckloads of fuel to effectively service clusters of customers in a specific area or zip code. At the front end of our system, we employ an app-based approach that provides all our customers with an easy-to-engage user interface and ordering system. Customers are able to select the times and locations of their on-demand or routinely scheduled fills and manage their account on their mobile device and in the future on a computer browser via our customer portal.

On the back end of our system, we have built a proprietary admin control dashboard where we aggregate customer orders based on their location and expected gallon demand for their vehicles. The aggregation of customer orders based on these variables triggers a truckload fill of one of our mobile tankers designated for each of the customer orders our system generates.

Our software and IT systems have been developed and customized in-house to provide cost-saving efficiencies which produce higher margins than traditional, gas station fuel margins.

We are planning to expand our software capabilities with a routing system built from the ground up specific for the on-demand business EzFill runs. This system will use AI and machine learning algorithms that will, among other things, automatically generate outbound “fill reminder” communications to customers based on their recorded usage amounts and time intervals. Collecting this data allows us to be reactive with our customers instead of proactive.

| 7 |

Our Mobile Application

The EzFill Mobile Application has been designed for iPhone and Android devices with our customers and convenience in mind. The goal when building the app was to order gas in four easy steps.

Sign Up: The EzFill App provides a quick and easy registration process.

Profile Management: The EzFill App provides easy profile management where users can seamlessly update personal information, such as: vehicle details and location, this way we are able to provide the best services to our customers.

Location Sharing: This feature enables our customers to simply drop a pin at their location on an integrated map which lets our driver know where to deliver the fuel.

Wallet: A central location for updating payment methods, redeem promo codes and earning free credits by referring friends, family, and colleagues.

Request Fuel Delivery: The EzFill App lets our customers pick the type and quantity of fuel to be delivered in addition to the time and date of availability.

Weekly Delivery Schedule: The EzFill App also enables our customers to preschedule weekly deliveries, on a specific day of the week. This feature enables our customers to request their delivery for a specific time window, this ensures they can schedule their fill up at convenient times when they would be busy attending other tasks and their car is idle.

Push Notifications: The EzFill App has a push notification feature. This allows us to keep customers informed of all the activities associated with the service they have requested. We also use it to keep our customers updated with recent offers and discounts, which helps to boost customer satisfaction and promotes our business.

Transaction History: The EzFill App offers our customers the ability to always view their transaction history. This gives our customers an option to check the previous fuel delivery requests and bills.

Loyalty: We plan on soon rolling out our new EzFill Unlimited Loyalty Program. We believe that a loyalty program will allow our customers to remain sticky while strengthening the relationship with our brand.

Our Market Opportunity

Information provided by Statista indicates that there are about 275 million registered cars in the United States as of 2018. According to the US Energy Information Administration, as of May 2022 there was an average of approximately 39 million fill-ups per day. According to Statista.com, in 2021, US gas stations produced revenues of roughly 583 billion dollars. EzFill wants to take advantage of the growing number of US drivers and the dwindling number of gas stations by bringing the gas directly to the consumers. We feel that our service is years in the making and solves many problems posed by the legacy gas station. EzFill presents a new way for Americans to get gas: at home, at the office, wherever, on demand.

The on-demand market continues to grow. According to a study conducted by rockresearch.com, in 2019 the on-demand market was $110 billion, growing by 18% from the previous year (according to PwC research that number is expected to grow to $335 billion by 2025). The same study by rockresearch.com indicates that participation in the on-demand market has tripled since 2016, with an estimated 64+ million consumers purchasing on-demand goods or services. EzFill believes that the on-demand market will continue to grow and expand into new areas, such as the gasoline market.

| 8 |

We believe our market opportunity is to expand into major MSAs across the continental U.S. with sufficient concentration of business and residential customers. We want to be in locations where people rely heavily on their personal cars to get places. Based on our research, we have identified several major MSAs across the U.S that would be attractive for expansion.

As we expand to a new market, we plan to employ a strategy that has helped us build a strong base of business in our existing market. The strategy we developed begins with sales in our fleet category, preferably a larger anchor tenant, to build a base of business in the target city, while developing and strengthening our delivery operations. Next, after launch, we build outwards from our anchor tenant and depot to secure corporate and landlord agreements which will allow us to begin marketing our services to their employees and tenants. These agreements include fueling at large office parks during daytime hours and fueling at residential buildings during nighttime hours.

We generate business through establishing corporate and landlord partnerships, we then leverage companies’ internal communication channels to market directly to their employees or residential tenants. By implementing our digital marketing campaigns as well as placement of our content throughout residential and corporate facilities, we are able to develop greater brand awareness. We coordinate with our partners to set up organic marketing efforts and on-site activations with our brand ambassadors to help increase recognition and assist users with downloading the app and setting up their accounts.

Our Growth Strategy

Our strategy is to leverage our established business relationships and generate organic methods of acquiring new markets. This has given us significant brand recognition by the consumer and has enabled us to acquire competitor territories. As we continue to develop our business relationships and expand our geographic footprint in Florida, our goal is to open in new markets along the east coast.

EzFill’s current focus is on expanding its geographic footprint. We aim to open in new markets along the east coast in the future both organically and through acquisitions of existing companies in the space. We make our expansion decisions based off research into optimal target markets where public transportation is less prevalent, leading to more residents owning cars and the areas where a demand for lifestyle improving technology is present. We also consider State/City/County regulations when assessing new areas to expand into. We are targeting high potential locations with the least regulations on mobile fuel delivery.

EzFill currently has strategic partnerships with businesses across industries such as property management, parking solutions services, travel industry, delivery industry, transportation and logistics, marinas, and other diversified business sectors. By establishing these strategic business-to-business relationships, we are able to offer cost effective business solutions, whether through human resource departments as employee perks, optimization of efficiency for fleet companies, or tenant satisfaction by adding amenities.

EzFill believes a strategic partnership with a major oil company will help with our expansion by enabling us to lower cost and attract a larger customer base by selling branded gasoline. However, there cannot be any assurance that EzFill will be able to obtain such a strategic partnership. The oil companies Exxon and Shell are both in the mobile fuel delivery space though investments in mobile fueling companies.

| 9 |

Technology License Agreement

On April 7, 2021, the Company entered into a Technology License Agreement with Fuel Butler LLC (“Fuel Butler” or “Licensor”), under which the Company licensed certain proprietary technology. Under the terms of the license, the Company issued 265,728 shares of its common stock to the Licensor upon signing. The Company also issued 332,160 shares to the Licensor in May 2021 upon the filing of a patent application related to the licensed technology. Upon completion of the Company’s IPO, 186,010 shares were issued to the Licensor. The Company will issue up to 730,752 additional shares to the Licensor upon the achievement of certain milestones. In addition, the Company has granted stock options for 531,456 shares at an exercise price of $3.76 per share that will become exercisable for three years after the end of the fiscal year in which certain sales levels are achieved using the licensed technology. The Company has the option for four years after the achievement of certain milestones to either acquire the technology or acquire the Licensor for the purchase price of 1,062,913 of its common shares. Until the Company exercise one of these options, it will share with the Licensor 50% of pre-revenue costs and 50% of the net revenue, as defined, from the use of the technology.

Under the Technology Agreement, the Company licenses proprietary technology that it believes will enable the Company to expand its services into certain highdensity areas like New York City. The Company does not expect any significant revenue from this agreement in 2023. Fuel Butler has delivered a purported notice of termination of the Technology Agreement based on certain alleged breaches arising from our failure to issue equity securities to Fuel Butler. We have been in communications with Fuel Butler regarding the termination of the Technology Agreement and continue to believe that the Company is in compliance with the Technology Agreement and that the Technology Agreement continues to be in force. While we contest Fuel Butler’s claims of breach and contend that in fact Fuel Butler is in breach, we have communicated to Fuel Butler that we wish to terminate the Technology Agreement. We have sent a proposal to Fuel Butler whereby we will cease utilizing the Technology and Fuel Butler will return any shares it received under the Technology Agreement. However, to date, the Company has not had further communications with Fuel Butler regarding this matter. Currently, the Company does not expect to expand into the state of New York for the foreseeable future.

Competition

EzFill is a mobile fuel delivery service and competes with other local fuel delivery companies and gas stations. We differentiate ourselves by allowing our customers to request our service via a mobile app and delivering the fuel directly to the end user. We use our innovative technology and excellent concierge service to offer convenient fueling solutions to all our vertical markets at different times of the day to maximize the efficiency of each mobile fueling truck.

We distinguish ourselves from our competitors by:

| ● | Prioritizing our customer’s experience and satisfaction; | |

| ● | Streamlining our customers ordering experience; | |

| ● | Rigorously vetting and training our drivers; | |

| ● | Providing the latest in scheduling, GPS technology, and payment systems; | |

| ● | Offering competitive pricing in the zip codes which we service; | |

| ● | Providing all our customers with certified, accurate reports and detailed invoices. |

Though the electric vehicle industry is growing, we do not consider this relatively new subsegment of the vehicle market a threat to our business model or growth trajectory. The vast majority of vehicles are gas or diesel powered and the entire fuel industry is a major component of the economy. According to Inside Climate News, less than 5% of the vehicles sold in the U.S. in 2020 were electric vehicles.

Additionally, the continued growth of the electric vehicle industry means more and more traditional gas stations are closing because of: (i) high overhead because of rising real-estate prices; (ii) lack of demand due to electric vehicle adoption; and (iii) their inability to fuel vehicles outside of their station. Our mobile fueling solution allows us to service many zip codes with one truck, so if sales slowdown in one area we are able to transition seamlessly to areas with higher demand.

Government Regulation

Our industry has certain government regulations, EzFill is dedicated to ensuring that we are always operating in a way that is in compliance with all applicable regulations.

| 1. | DOT/Hazmat Registration: Our company is required to be registered with the Department of Transportation to transport and dispense hazardous materials. EzFill as a company is registered to transport and dispense hazardous material. |

| 10 |

| 2. | Weights and Measures: In order to ensure the accuracy of our fuel sales to customers, our fuel meters and registers have to be calibrated and certified by the Florida Department of Agriculture. EzFill’s fuel meters and registers have been calibrated and certified by the Department of Agriculture to be a fuel retailer. | |

| 3. | CDL Licensing with Hazmat Endorsement: Drivers are required to have a Commercial Driver’s License with a Hazmat endorsement in order to operate the Mobile Fueling Trucks. All of our drivers have their Commercial Driver’s License with the Hazmat endorsement. |

Our operations may also be subject to local fire marshal regulations, which varies in the different cities and counties. EzFill keeps up to date on the local regulations in each of the locations it operates and does ample research into local regulations before opening in any new location.

The costs of compliance includes general liability insurance, workman’s comp. insurance, vehicle insurance, meters and registers maintenance for yearly inspection, vehicle maintenance for yearly inspection, hazmat permits and licensing, safety procedures and equipment, emergency response team, and live safety monitoring system.

Our safety protocol includes:

Training

Management oversight

Live tracking 24-7

Safety spill kits

Automatic pump shut off system

24-7 800# support line

We have implemented a safety protocol and monitoring system that allows us to operate at maximum efficiency in optimal safety conditions. Our drivers carry the proper commercial driver’s licenses and endorsements and are fully trained and certified to transport and dispense fuel. We have been licensed by the U.S. Department of Transportation and our fueling trucks have been fitted with safety equipment and emergency tools such as spill kits, fire extinguishers, emergency response handbook and a dedicated 24/7 emergency responder support team in the event of emergency situations. We have management oversight around the clock to ensure safe operations. We have an emergency response team on call, in the unlikely situation where there is a spill, the emergency response team will come to the scene to control and properly handle the clean-up of any hazardous materials. We also have state of the art technology that enables us, in real-time, to track the location of our Mobile Fueling Trucks and the inventory levels of each Mobile Fueling Truck.

Corporate Information

EzFill FL, LLC was established on July 27, 2016, in the state of Florida. The assets of EzFill, LLC were acquired as of April 9, 2019, by EzFill, Holdings Inc. (formed in March of 2019) which purchased certain assets of EzFill FL LLC’s mobile fueling business. The business is located and operates in South Florida.

Our principal executive offices are located at 2999 NE 191st Street, Suite 500, Aventura, FL 33180, and our telephone number is 305-791-1169. Our website address is ezfl.com. Information contained on, or accessible through, our website is not a part of this 10K or the registration statement of which it forms a part.

Ezfl.com, EZFL, EzFill, and other trade names, trademarks, or service marks of EzFill appearing in this 10K are the property of EzFill. Trade names, trademarks, and service marks of other companies appearing in this 10K are the property of their respective holders.

Human Capital Resources

As of March 10, 2023, we had a total of approximately 53 employees, all of whom were full-time. None of our employees are covered by a collective bargaining agreement, and we consider our relations with our employees to be good.

Properties

We lease office space at 2999 NE 191st Street, Aventura, FL 33180 and pay approximately $22,000 per month, including operating expenses and taxes. Additionally, we have office space and parking for our trucks at our fuel supplier located at 2965 E. 11th Ave., Hialeah, FL 33013. We also have access to parking for our trucks at various locations of Palmdale Oil Company in Florida. We believe our current office space is sufficient to meet our needs.

Legal Proceedings

From

time to time, we may become involved in various lawsuits and legal proceedings that arise in the ordinary course of business. Litigation

is subject to inherent uncertainties, and an adverse result in matters may arise from time to time that may harm our business. As of

the date of this 10K, management believes that there are no claims against us, which it believes will result in a material adverse

effect on our business or financial condition.

| 11 |

RISK FACTORS

Any investment in our securities involves a high degree of risk. You should carefully consider the risks described below as well as other information provided to you in this document, including information in the section of this document entitled “Information Regarding Forward Looking Statements.” If any of the following risks actually occur, the Company’s business, financial condition or results of operations could be materially adversely affected, the value of the Company’s Common Stock could decline, and you may lose all or part of your investment.

Our business, financial condition or operating results could be materially adversely affected by any of these risks. In such case, the trading price of our common stock could decline, and our stockholders may lose all or part of their investment in our securities.

Risks Related to Our Business

Our business and results of operations have been, and may continue to be, impacted by the global COVID-19 pandemic.

The coronavirus pandemic and the resulting macroeconomic trends have had, and may continue to have, an adverse impact on our operations, our customers’ demand for our products and services, our ability to find new clients, and our revenue. This is due in part to restrictions such as social distancing requirements, stay at home orders, the shutdown of non-essential businesses and the impact these restrictions have had on peoples’ and companies’ driving habits and their need for gasoline for their personal cars, fleets, and boats. For example, we have noted that we have not had the number of car fills at office parks compared to prior periods, even as pandemic-related restrictions have been lifted. The reduced number of office park fills has been largely offset by increased sales to delivery service fleets. Therefore, our current customers may not need our services as often and we may have trouble attracting new customers. If our customers need less gas and we have trouble finding new customers, this may negatively impact our operations and revenues.

Uncertain geopolitical conditions could adversely affect our results of operations.

Uncertain geopolitical conditions, including the invasion of Ukraine, sanctions, and other potential impacts on this region’s economic environment and currencies, may cause demand for our products and services to be volatile, cause abrupt changes in our customers’ buying patterns, and interrupt our ability to supply products or limit customers’ access to financial resources and ability to satisfy obligations to us. Specifically, terrorist attacks, the outbreak of war, or the existence of international hostilities could damage the world economy, adversely affect the availability of and demand for crude oil and petroleum products and adversely affect both the price of our fuel and our ability to obtain fuel.

Operating and litigation risks may not be covered by insurance.

Our operations are subject to all of the operating hazards and risks normally incidental to handling, storing, transporting and otherwise providing combustible liquids such as gasoline for use by consumers. These risks could result in substantial losses due to personal injury and/or loss of life, and severe damage to and destruction of property and equipment arising from explosions and other catastrophic events, including acts of terrorism. Additionally, environmental contamination could result in future legal proceedings. There can be no assurance that our insurance coverage will be adequate to protect us from all material expenses related to pending and future claims or that such levels of insurance would be available in the future at economical prices. Moreover, defense and settlement costs may be substantial, even with respect to claims and investigations that have no merit. If we cannot resolve these matters favorably, our business, financial condition, results of operations and future prospects may be materially adversely affected.

Future climate change laws and regulations and the market response to these changes may negatively impact our operations.

Increased regulation of greenhouse (GHG) emissions, from products such as petroleum and diesel, could impose significant additional costs on us, our suppliers, and our customers. Some states have adopted laws and regulations regulating the emission of GHGs for some industry sectors. Mandatory reporting by our customers and suppliers could have an effect on our operations or financial condition.

| 12 |

The adoption of additional federal or state climate change legislation or regulatory programs to reduce emissions of GHGs could also require us or our suppliers to incur increased capital and operating costs, with resulting impact on product price and demand. The impact of new legislation and regulations will depend on a number of factors, including (i) which industry sectors would be impacted, (ii) the timing of required compliance, (iii) the overall GHG emissions cap level, (iv)the allocation of emission allowances to specific sources, and (v) the costs and opportunities associated with compliance. At this time, we cannot predict the effect that climate change regulation may have on our business, financial condition or operations in the future.

Our auditors have included an explanatory paragraph in their opinion regarding our ability to continue as a going concern. If we are unable to continue as a going concern, our securities will have little or no value.

M&K CPA’s, PLLC, our independent registered public accounting firm for the fiscal year ended December 31, 2022, has included an explanatory paragraph in their opinion that accompanies our audited consolidated financial statements as of and for the year ended December 31, 2022, indicating that our current liquidity position raises substantial doubt about our ability to continue as a going concern. If we are unable to improve our liquidity position, we may not be able to continue as a going concern.

We anticipate that we will continue to generate operating losses and use cash in operations through the foreseeable future. As further set forth below, we anticipate that we will need significant additional capital by March 31, 2023, or we may be required to curtail or cease operations.

In order to continue as a going concern, we will need significant additional capital by March 31, which we may be unable to obtain.

Revenues generated from our operations are not presently sufficient to sustain our operations. Therefore, we will need to raise additional capital in the future to continue our operations. We anticipate that our principal sources of liquidity will only be sufficient to fund our activities through March 31, 2023. In order to have sufficient cash to fund our operations beyond March 31, 2023, we will need to raise additional equity or debt capital. There can be no assurance that additional funds will be available when needed from any source or, if available, will be available on terms that are acceptable to us. We will be required to pursue sources of additional capital through various means, including debt or equity financings. Future financings through equity investments are likely to be dilutive to existing stockholders. Also, the terms of securities we may issue in future capital transactions may be more favorable for new investors. Newly issued securities may include preferences, superior voting rights, the issuance of warrants or other derivative securities, and the issuances of incentive awards under equity employee incentive plans, which may have additional dilutive effects. Further, we may incur substantial costs in pursuing future capital and/or financing, including investment banking fees, legal fees, accounting fees, printing and distribution expenses and other costs. We may also be required to recognize non-cash expenses in connection with certain securities we may issue, such as convertible notes and warrants, which will adversely impact our financial condition. Our ability to obtain needed financing may be impaired by such factors as the capital markets and our history of losses, which could impact the availability or cost of future financings. If the amount of capital we are able to raise from financing activities, together with our revenues from operations, is not sufficient to satisfy our capital needs, even to the extent that we reduce our operations accordingly, we may be required to curtail or cease operations.

If we are unable to protect our information technology systems against service interruption, misappropriation of data, or breaches of security resulting from cyber security attacks or other events, or we encounter other unforeseen difficulties in the operation of our information technology systems, our operations could be disrupted, our business and reputation may suffer, and our internal controls could be adversely affected.

In the ordinary course of business, we rely on information technology systems, including the Internet and third-party hosted services, to support a variety of business processes and activities and to store sensitive data, including (i) intellectual property, (ii) our proprietary business information and that of our suppliers and business partners, (iii) personally identifiable information of our customers and employees, and (iv) data with respect to invoicing and the collection of payments, accounting, procurement, and supply chain activities. In addition, we rely on our information technology systems to process financial information and results of operations for internal reporting purposes and to comply with financial reporting, legal, and tax requirements. Despite our security measures, our information technology systems may be vulnerable to attacks by hackers or breached due to employee error, malfeasance, sabotage, or other disruptions. A loss of our information technology systems, or temporary interruptions in the operation of our information technology systems, misappropriation of data, or breaches of security could have a material adverse effect on our business, financial condition, results of operations, and reputation.

Moreover, the efficient execution of our business is dependent upon the proper functioning of our internal systems. Any significant failure or malfunction of this information technology system may result in disruptions of our operations. Our results of operations could be adversely affected if we encounter unforeseen problems with respect to the operation of this system.

| 13 |

High fuel prices can lead to customer conservation and attrition, resulting in reduced demand for our product.

Prices for fuel are subject to volatile fluctuations in response to changes in supply and other market conditions. During periods of high fuel costs our prices generally increase. High prices can lead to customer conservation and attrition, resulting in reduced demand for our product.

Low fuel prices may also result in less demand for our product.

Low fuel prices may lead to us being unable to attract customers due to the fact that we charge a delivery price that may make our pricing less competitive.

Changes in commodity market prices may have a negative effect on our gross margin.

Our current fuel supplier agreements set terms and establishes formulas based on Oil Price Information Service (OPIS) pricing as of the time of wholesale acquisition, and we do not store inventory. OPIS is a leading source for worldwide petroleum pricing. There is a mark-up for retail fuel prices above wholesale cost, per standard practice in the retail fuel distribution model. Cost of goods sold includes direct labor, including drivers. Our gross margin as a percentage of revenue decreases as a result of increase in fuel costs.

The decline of the retail fuel market may impact our potential to get new customers.

The retail gasoline industry has been declining over the past several years, with no or modest growth or decline in total demand foreseen in the next several years. Accordingly, we expect that year-to-year industry volumes will be principally affected by weather patterns. Therefore, our ability to grow within the industry is dependent on our ability to acquire other retail distributors and to achieve internal growth, which includes the success of our sales and marketing programs designed to attract and retain customers. Any failure to retain and grow our customer base would have an adverse effect on our results.

Competition in the fuel delivery industry may negatively impact our operations.

We compete with other mobile fuel delivery companies nationwide. There is little to no barrier to entry and therefore, our competition in the industry may grow. Our ability to compete in our current markets and expand to new markets may be negatively impacted by our competitors’ successes. Additionally, fuel competes with other sources of energy, some of which are less costly on an equivalent energy basis. In addition, we cannot predict the effect that the development of alternative energy sources might have on our operations. We compete for customers against suppliers of electricity. Electricity is becoming a competitor of fuel. The convenience and efficiency of electricity make it an attractive energy source for vehicle drivers. The expansion of the electric vehicle industry may have a negative impact on our customer base.

Our trucks transport hazardous flammable fuel, which may cause environmental damage and liability to us.

Due to the hazardous nature and flammability of our product, we face the risk of a simple accident causing serious damage to life and property. Additionally, a spill of our product may result in environmental damage, the liability for which our Company may not be able to overcome. If we are involved in a spill, leak, fire, explosion or other accident involving hazardous substances or if there are releases of fuel or fuel products we own or are transporting, our operations could be disrupted and we could be subject to material liabilities, such as the cost of investigating and remediating contaminated properties or claims by customers, employees or others who may have been injured, or whose property may have been damaged. These liabilities, to the extent not covered by insurance, could have a material adverse effect on our business, financial condition and results of operations. Some environmental laws impose strict liability, which means we could have liability without regard to whether we were negligent or at fault.

In addition, compliance with existing and future environmental laws regulating fuel storage terminals, fuel delivery vessels and/or storage tanks that we own or operate may require significant capital expenditures and increased operating and maintenance costs. The remediation and other costs required to clean up or treat contaminated sites could be substantial and may not be covered by insurance.

Our cash flow and net income may decrease if we are forced to comply with new governmental regulation surrounding the transportation of fuel.

We are subject to various federal, state, and local safety, health, transportation, and environmental laws and regulations governing the storage, distribution, and transportation of fuel. It is possible we will incur increased costs as a result of complying with new safety, health, transportation and environmental regulations and such costs will reduce our net income. It is also possible that material environmental liabilities will be incurred, including those relating to claims for damages to property and persons.

| 14 |

Our current dependence on a single fuel supplier increases our risk of an interruption in fuel supply, impacting our operations.

Although we are in the process of establishing other sources, we currently purchase almost all of our fuel needs from two principal suppliers in Florida. We do not have a written agreement with the largest supplier, and as such, if fuel from this source was interrupted, the cost of procuring replacement fuel and transporting that fuel from alternative locations might be materially higher and, at least on a short-term basis, our earnings could be negatively affected. This supplier is also a shareholder in the Company.

Our profitability is subject to fuel pricing and inventory risk.

The retail fuel business is a “margin-based” business in which gross profits are dependent upon the excess of the sales price over the fuel supply costs. Fuel is a commodity, and, as such, its unit price is subject to volatile fluctuations in response to changes in supply or other market conditions. We have no control over supplies, commodity prices or market conditions. Consequently, the unit price of the fuel that we and other marketers purchase can change rapidly over a short period of time, including daily.

Loss of a major customer could result in a decrease in our future sales and earnings.

In any given quarter or year, sales of our products may be concentrated in a few major customers. We anticipate that a limited number of customers in any given period may account for a substantial portion of our total net revenue for the foreseeable future. The business risks associated with this concentration, including increased credit risks for these and other customers and the possibility of related bad debt write-offs, could negatively affect our margins and profits. Additionally, the Company does not have any long-term agreements with its customers. All customer agreements are cancelable at any time by either party and as such there cannot be any assurance that any customer will continue to use the Company’s services. The loss of a major customer, whether through competition or consolidation, or a termination in sales to any major customer, could result in a decrease of our future sales and earnings.

We operate in a new industry segment and may be subject to new and existing laws, regulations and oversight

The Company operates in a new industry segment, on-demand mobile fuel delivery, in which new state and local law adoptions are occurring. Effective December 31, 2020, Florida adopted Florida Fire Prevention Code (“Code”) Section 42.12 recognizing and setting various requirements for the consumer on-demand mobile fuel delivery business. Permitting authority is contemplated under an “Authority Having Jurisdiction” (“AHJ”). Other pre-existing Code provisions similarly contemplate AHJ permitting for commercial mobile fueling. Miami-Dade County, where most of our business is conducted adopted the Code by reference. Unlike some other states and counties, neither Florida nor Miami-Dade County have designated an AHJ for mobile fueling. Miami-Dade’s extensive permitting and fee schedule does not contemplate or assert permitting authority over mobile fueling, consumer or commercial. We may be subject to oversight, including audits, in existing or future areas of operation. If we cannot comply with the Code, or County, State or Federal rules and regulations or the laws, rules and regulations or oversight in areas in which we currently operate or may seek to operate, we could lose the ability to service those areas and our earnings could be affected.

Our License Agreement with Fuel Butler may be terminated and as such our expansion plans into the state of New York may be delayed

On April 7, 2021, the Company entered into a Technology License Agreement with Fuel Butler LLC (“Technology Agreement”). Under the Technology Agreement, the Company licensed proprietary technology that the Company believes will allow the Company to provide its fuel service in high density areas like New York City. Fuel Butler has delivered a purported notice of termination of the Technology Agreement based on certain alleged breaches arising from our failure to issue equity securities to Fuel Butler. We have been in communications with Fuel Butler regarding the termination of the Technology Agreement and continue to believe that the Company is in compliance with the Technology Agreement and that the Technology Agreement continues to be in force. While we contest Fuel Butler’s claims of breach and contend that in fact Fuel Butler is in breach, we have communicated to Fuel Butler that we wish to terminate the Technology Agreement. We have sent a proposal to Fuel Butler whereby we will cease utilizing the Technology and Fuel Butler will return any shares it received under the Technology Agreement. However, to date, the Company has not had further communications with Fuel Butler regarding this matter. Currently, the Company does not expect to expand into the state of New York for the foreseeable future.

| 15 |

Risks Related to Ownership of Our Common Stock

Our stock price is expected to fluctuate significantly.

Our common stock was approved for listing on The Nasdaq Capital Market under the symbol “EZFL” and began trading on September 15, 2021. There can be no assurance that an active trading market for our shares will be sustained. The market price of shares of our common stock could be subject to wide fluctuations in response to many risk factors listed in this section, and others beyond our control, including:

| ● | actual or anticipated fluctuations in our financial condition and operating results; | |

| ● | geopolitical developments affecting supply and demand for oil and gas and an increase or decrease in the price of fuel; | |

| ● | actual or anticipated changes in our growth rate relative to our competitors; | |

| ● | competition from existing companies in the space or new competitors that may emerge; | |

| ● | issuance of new or updated research or reports by securities analysts; | |

| ● | fluctuations in the valuation of companies perceived by investors to be comparable to us; | |

| ● | share price and volume fluctuations attributable to inconsistent trading volume levels of our shares; | |

| ● | additions or departures of key management or technology personnel; | |

| ● | disputes or other developments related to proprietary rights, including intellectual property, litigation matters, and our ability to obtain patent protection for our technologies; | |

| ● | announcement or expectation of additional debt or equity financing efforts; | |

| ● | sales of our common stock by us, our insiders or our other stockholders; and | |

| ● | general economic and market conditions. |

These and other market and industry factors may cause the market price and demand for our common stock to fluctuate substantially, regardless of our actual operating performance, which may limit or prevent investors from readily selling their shares of common stock and may otherwise negatively affect the liquidity of our common stock. In addition, the stock market in general has experienced extreme price and volume fluctuations that have often been unrelated or disproportionate to the operating performance of the Company.

The majority of the Company’s common stock is held by a small number of shareholders.

Two beneficial owners control approximately 49.7% of our outstanding common stock as of March 10, 2023. As a result, these shareholders are able to influence the outcome of shareholder votes on various matters, including the election of directors and extraordinary corporate transactions, including business combinations. In addition, the occurrence of sales of a large number of shares of our common stock, or the perception that these sales could occur, may affect our stock price and could impair our ability to obtain capital through an offering of equity securities. Furthermore, the current ratios of ownership of our common stock reduce the public float and liquidity of our common stock, which can in turn affect the market price of our common stock.

| 16 |

Our Amended and Restated Certificate of Incorporation includes an exclusive forum provision that identifies the Court of Chancery of the State of Delaware as the exclusive forum for certain litigation, including any derivative actions, which could limit our stockholders’ ability to obtain a favorable judicial forum for disputes with us, our directors, officers or employees.

Our Amended and Restated Certificate of Incorporation provides that unless we consent in writing to the selection of an alternative forum, the Court of Chancery of the State of Delaware shall be the sole and exclusive forum for (i) any derivative action or proceeding brought on behalf of the Company; (ii) any action asserting a claim of breach of a fiduciary duty owed by any director, officer or other employee of the Company to the Company or the Company’s stockholders; (iii) any action asserting a claim against the Company arising pursuant to any provision of the General Corporation Law of Delaware, the Amended and Restated Certificate of Incorporation or the Bylaws of the Company; or (iv) any action asserting a claim against the Company governed by the internal affairs doctrine. To the extent that any such claims may be based upon federal law claims, Section 27 of the Securities Exchange Act of 1934, as amended, creates exclusive federal jurisdiction over all suits brought to enforce any duty or liability created by the Exchange Act or the rules and regulations thereunder. Furthermore, Section 22 of the Securities Act of 1933, as amended, provides for concurrent jurisdiction for federal and state courts over all suits brought to enforce any duty or liability created by the Securities Act or the rules and regulations thereunder, and as such, the exclusive jurisdiction clauses of our Amended and Restated Certificate of Incorporation would not apply to such suits. The choice of forum provisions in our Amended and Restated Certificate of Incorporation may limit a stockholder’s ability to bring a claim in a judicial forum that it finds favorable for disputes with us or our directors, officers or other employees, which may discourage such lawsuits against us and our directors, officers and other employees. By agreeing to these provisions, however, stockholders will not be deemed to have waived our compliance with the federal securities laws and the rules and regulations thereunder. Furthermore, the enforceability of similar choice of forum provisions in other companies’ certificates of incorporation and bylaws has been challenged in legal proceedings, and it is possible that a court could find these types of provisions to be inapplicable or unenforceable. If a court were to find the choice of forum provisions in our Amended and Restated Certificate of Incorporation” to be inapplicable or unenforceable in an action, we may incur additional costs associated with resolving such action in other jurisdictions, which could adversely affect our business and financial condition.

We have never paid dividends on our capital stock, and we do not anticipate paying any dividends in the foreseeable future. Consequently, any gains from an investment in our common stock will likely depend on whether the price of our common stock increases.

We have not paid dividends on any of our classes of capital stock to date and we currently intend to retain our future earnings, if any, to fund the development and growth of our business. In addition, the terms of any future indebtedness we may incur could preclude us from paying dividends. As a result, capital appreciation, if any, of our common stock will be your sole source of gain from an investment in our common stock for the foreseeable future. Consequently, in the foreseeable future, you will likely only experience a gain from your investment in our common stock if the price of our common stock increases.

Failure to maintain effective internal control over our financial reporting in accordance with Section 404 of the Sarbanes-Oxley Act of 2002 (“Sarbanes-Oxley Act”) could cause our financial reports to be inaccurate.

We are required pursuant to Section 404 of the Sarbanes-Oxley Act to maintain internal control over financial reporting and to assess and report on the effectiveness of those controls. This assessment includes disclosure of any material weaknesses identified by our management in our internal control over financial reporting. Although we prepare our financial statements in accordance with accounting principles generally accepted in the United States, our internal accounting controls may not meet all standards applicable to companies with publicly traded securities. If we fail to implement any required improvements to our disclosure controls and procedures, we may be obligated to report control deficiencies and our independent registered public accounting firm may not be able to certify the effectiveness of our internal controls over financial reporting. In either case, we could become subject to regulatory sanction or investigation. Further, these outcomes could damage investor confidence in the accuracy and reliability of our financial statements.

Our management has concluded that our internal controls over financial reporting were, and continue to be, effective, as of December 31, 2022. If we are not able to maintain effective internal control over financial reporting, our financial statements, including related disclosures, may be inaccurate, which could have a material adverse effect on our business.

If we fail to comply with the continued listing requirements of NASDAQ, we would face possible delisting, which would result in a limited public market for our shares and make obtaining future debt or equity financing more difficult for us.

As previously reported, on May 20, 2022, the “Company received a letter from the Listing Qualifications Staff (the “Staff”) of The Nasdaq Stock Market LLC (“Nasdaq”) notifying the Company that, based upon the closing bid price of the Company’s common stock, par value $0.0001 per share (the “Common Stock”), for the prior 30 consecutive business days, the Company no longer met the requirement to maintain a minimum bid price of $1 per share (the “Minimum Bid Price Requirement”), as set forth in Nasdaq Listing Rule 5450(a)(1).

| 17 |

On November 17, 2022, the Company received a letter from Nasdaq informing it that although the Company’s common stock has not regained compliance with the minimum $1.00 bid price per share requirement, the Staff has determined that the Company is eligible for an additional 180 calendar day period, or until May 15, 2023, to regain compliance. The Staff’s determination was based on the Company meeting the continued listing requirement for market value of publicly held shares and all other applicable requirements for initial listing on the Capital Market with the exception of the bid price requirement, and the Company’s written notice of its intention to cure the deficiency during the second compliance period by effecting a reverse stock split ( the “Reverse Stock Split), if necessary.

If at any time before May 15, 2023, the bid price of the Company’s common stock closes at or above $1.00 per share for a minimum of, subject to the Staff’s discretion, 10 consecutive business days, Nasdaq will provide written notification that the Company has achieved compliance with the Minimum Bid Price Requirement.

The Company will continue to monitor the closing bid price of its Common Stock and will consider its available options to resolve the deficiency and regain compliance with the Minimum Bid Price Requirement within the allotted compliance period. If the Company does not regain compliance within the allotted compliance period, Nasdaq will provide notice that the Company’s Common Stock will be subject to delisting. The Company would then be entitled to appeal that determination to a Nasdaq hearings panel. There can be no assurance that the Company will regain compliance with the Minimum Bid Price Requirement.

If the Company fails to regain compliance with Nasdaq’s Listing Rules, we could be subject to suspension and delisting proceedings. If our securities lose their status on The NASDAQ Capital Market, our securities will likely trade in the over-the-counter market. If our securities were to trade on the over-the-counter market, selling our securities could be more difficult because smaller quantities of securities would likely be bought and sold, transactions could be delayed, and security analysts’ coverage of us may be reduced. In addition, in the event our securities are delisted, broker-dealers have certain regulatory burdens imposed upon them, which may discourage broker-dealers from effecting transactions in our securities, further limiting the liquidity of our securities. These factors could result in lower prices and larger spreads in the bid and ask prices for our securities. Such delisting from The NASDAQ Capital Market and continued or further declines in our share price could also greatly impair our ability to raise additional necessary capital through equity or debt financing and could significantly increase the ownership dilution to shareholders caused by our issuing equity in financing or other transactions.

A Reverse Stock Split could result in a significant devaluation of the Company’s market capitalization and trading price of the Common Stock, and we cannot assure you that a Reverse Stock Split will increase our stock price and have the desired effect of increasing the market price of the Common Stock such that the market price of our Common Stock meets Nasdaq’s Minimum Bid Price Requirement.

The Company may effect a reverse stock split (the “Reverse Stock Split”) to regain compliance with the Minimum Bid Price Requirement. The Company’s Board expects that a Reverse Stock Split of the outstanding Common Stock will increase the market price of the Common Stock. However, the Company cannot be certain whether the Reverse Stock Split would lead to a sustained increase in the trading price or the trading market for the Common Stock. The history of similar stock split combinations for companies in like circumstances is varied. There is no assurance that:

| ● | the market price per share of the Common Stock after the Reverse Stock Split will rise in proportion to the reduction in the number of pre-split shares of Common Stock outstanding before the Reverse Stock Split; |

| ● | the Reverse Stock Split will result in a per share price that will attract brokers and investors, including institutional investors, who do not trade in lower priced securities; |

| ● | the Reverse Stock Split will result in a per share price that will increase the Company’s ability to attract and retain employees and other service providers; |

| ● | the market price per post-split share will be sufficient to satisfy the Minimum Bid Price Requirement and |

| ● | the Reverse Stock Split will increase the trading market for the common Stock, particularly if the stock price does not increase as a result of the reduction in the number of shares of Common Stock available in the public market. |

The market price of the Common Stock will also be based on the Company’s performance and other factors, some of which are unrelated to the number of shares outstanding. If the Reverse Stock Split is consummated and the trading price of the Common Stock declines, the percentage decline as an absolute number and as a percentage of the Company’s overall market capitalization may be greater than what would occur in the absence of the Reverse Stock Split. Furthermore, the liquidity of the Common Stock could be adversely affected by the reduced number of shares that would be outstanding after the Reverse Stock Split and this could have an adverse effect on the price of the Common Stock. If the market price of the shares of Common Stock declines subsequent to the effectiveness of the Reverse Stock Split, this will detrimentally impact the Company’s market capitalization and the market value of the Company’s public float.

| 18 |

The Reverse Stock Split may result in some stockholders owning “odd lots” that may be more difficult to sell or require greater transaction costs per share to sell.

The Reverse Stock Split may result in some stockholders owning “odd lots” of less than 100 shares of Common Stock on a post-split basis. These odd lots may be more difficult to sell, or require greater transaction costs per share to sell, than shares in “round lots” of even multiples of 100 shares.

The Reverse Stock Split may not help generate additional investor interest.

There can be no assurance that the Reverse Stock Split will result in a per share price that will attract institutional investors or investment funds or that such share price will satisfy the investing guidelines of institutional investors or investment funds. As a result, the trading liquidity of our Common Stock may not necessarily improve.

If equity research analysts issue unfavorable commentary or downgrade our common stock, the price of our common stock could decline.

The trading market for our common stock may be affected by the research and reports that equity research analysts publish about us and our business. We do not control these analysts. The price of our common stock could decline if one or more equity analysts downgrade our common stock or if analysts issue other unfavorable commentary or cease publishing reports about us or our business.

We have elected to take advantage of specified reduced disclosure requirements applicable to an “emerging growth company” under the JOBS Act, the information that we provide to stockholders may be different than they might receive from other public companies.

As a company with less than $1 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” under the JOBS Act. As an emerging growth company, we may take advantage of specified reduced disclosure and other requirements that are otherwise applicable generally to public companies. These provisions include:

| ● | only two years of audited financial statements in addition to any required unaudited interim financial statements with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure; | |

| ● | reduced disclosure about our executive compensation arrangements; | |

| ● | no non-binding advisory votes on executive compensation or golden parachute arrangements; | |

| ● | exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting and delaying the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies. |

We have elected to take advantage of the above-referenced exemptions and we may take advantage of these exemptions for up to five years or such earlier time that we are no longer an emerging growth company. We would cease to be an emerging growth company if we have more than $1 billion in annual revenues, we have more than $700 million in market value of our stock held by non-affiliates, or we issue more than $1 billion of non-convertible debt over a three-year period. We may choose to take advantage of some but not all of these reduced burdens. We have not taken advantage of any of these reduced reporting burdens in this 10K, although we may choose to do so in future filings. If we do, the information that we provide stockholders may be different than you might get from other public companies that comply with public company effective dates.