UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

OR

For the fiscal year ended

OR

OR

Date of event requiring this shell company report . . . . . . . . . . . . . . .

For the transition period from to

Commission file number:

Medicenna Therapeutics Corp.

(Exact name of Registrant as specified in its charter)

N/A

(Translation of Registrant’s name into English)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Telephone:

E-mail: ewilliams@medicenna.com

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| | | The |

Securities registered or to be registered pursuant to Section 12(g) of the Act

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to section 15(d) of the Act

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☐ Yes ☒

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files)

☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ Accelerated filer ☐

Emerging growth company

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.

†The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP | ☐ | | ☒ | Other | ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

(APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PAST FIVE YEARS)

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

☒ Yes ☐ No

Unless otherwise noted or the context indicates otherwise “we”, “us”, “our”, the “Company” or “Medicenna” refer to Medicenna Therapeutics Corp. and its subsidiaries.

Unless otherwise indicated, financial information in this Annual Report on Form 20-F (this “Annual Report”) has been prepared in accordance with International Financial Reporting Standards (“IFRS”), as issued by the International Accounting Standards Board (“IASB”). Unless otherwise noted herein, all references to “$,” “C$,” “Canadian dollars,” or “dollars” are to the currency of Canada and “US$,” “United States dollars,” or “U.S. dollars” are to the currency of the United States.

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”) and as such, we have elected to comply with certain reduced U.S. public company reporting requirements.

Unless otherwise indicated, the Company has obtained the market and industry data contained in this Annual Report from its internal research, management’s estimates and third-party public information and other industry publications. While the Company believes such internal research, management’s estimates and third-party public information is reliable, such internal research and management’s estimates have not been verified by any independent sources and the Company has not verified any third party public information. While the Company is not aware of any misstatements regarding the market and industry data contained in this Annual Report, such data involves risks and uncertainties and are subject to change based on various factors, including those described under “Cautionary Statement Regarding Forward-Looking Information and Statements” and “Item 3.D. Risk Factors”.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements that are subject to risks and uncertainties. These forward-looking statements include information about possible or assumed future results of our business, financial condition, results of operations, liquidity, plans and objectives. In some cases, you can identify forward-looking statements by terminology such as “will, ” “seek,” “believe,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “expect,” “predict,” “potential,” or the negative of these terms or other similar expressions. The statements we make regarding the following matters are forward-looking by their nature and are based on certain of the assumptions noted below:

| ● |

the intentions, plans and future actions of the Company; |

| ● |

statements relating to the business and future activities of the Company; |

| ● |

anticipated developments in operations of the Company; |

| ● |

market position, ability to compete and future financial or operating performance of the Company; |

| ● |

the timing and amount of funding required to execute the Company’s business plans; |

| ● |

capital expenditures; |

| ● |

the effect on the Company of any changes to existing or new legislation or policy or government regulation; |

| ● |

the availability of labor; |

| ● |

requirements for additional capital; |

| ● |

goals, strategies and future growth; |

| ● |

the adequacy of financial resources; |

| ● |

expectations regarding revenues, expenses and anticipated cash needs; and |

| ● |

general market conditions and macroeconomic trends driven by the COVID-19 pandemic and/or geopolitical conflicts, including supply chain disruptions, market volatility, inflation, and labor challenges, among other factors. |

The preceding list is not intended to be an exhaustive list of all of our forward-looking statements. The forward-looking statements are based on our beliefs, assumptions and expectations of future performance, taking into account the information currently available to us. These statements are only predictions based upon our current expectations and projections about future events. There can be no assurance that such statements will prove to be accurate and actual results and future events could differ materially from those anticipated in such statements. There are important factors that could cause our actual results, levels of activity, performance or achievements to differ materially from the results, levels of activity, performance or achievements expressed or implied by the forward-looking statements, including, but not limited to, those factors identified under the Risk Factors listed below in Item 3.D. of this Annual Report. Furthermore, unless otherwise stated, the forward-looking statements contained in this Annual Report are made as of the date hereof, and we have no intention and undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events, changes or otherwise, except as required by law.

GLOSSARY

“AACR” means the America Association for Cancer Research;

“Articles” means the articles of continuance dated November 13, 2017 which govern the Company;

“ASCO” means the American Society of Clinical Oncology;

“ATM” means at-the-market;

“Board” means the Board of Directors of the Company;

“By-law” means the Company’s by-law no. 2 dated July 31, 2020;

“CBCA” means the Canada Business Corporations Act;

“CED” means convection-enhanced delivery;

“CEO” means the Chief Executive Officer of the Company;

“CFO” means the Chief Financial Officer of the Company;

“cGMP” means Good Manufacturing Practices;

“Common Shares” means the Common Shares of the Company;

“CPRIT” means Cancer Prevention and Research Institute of Texas;

“Director” means a member of the Board of Directors of the Company;

“ECA” means External Control Arm;

“Eligible Person” means a director, officer, employee or service provider of the Company or any related entity (being a person that controls or is controlled by the Company or that is controlled by the same person that controls the Company) that options may be granted to under the Company’s Stock Option Plan;

“EMA” means European Medicines Agency;

“ENA” means EORTC (European Organisation for Research and Treatment of Cancer) – NCI (National Cancer Institute) AACR;

“Exchange Act” means the Securities Exchange Act of 1934;

“FDA” means U.S. Food and Drug Administration;

“GBM” means glioblastoma;

“IFRS” means International Accounting Standards Board;

“IL-2” means interleukin-2;

“IL-4” means interleukin-4;

“IL4R” means interleukin-4 receptor;

“IL-13” means interleukin-13;

“IMPD” means Investigational Medical Product Dossier;

“KOL” means key opinion leader;

“MBI” means Medicenna Biopharm Inc., a Delaware corporation;

“mOS” means median overall survival;

“MTD” maximum tolerated dose;

“MTI” means Medicenna Therapeutics Inc., a British Columbia corporation;

“MTI Reverse Takeover” means the reverse takeover of A2 Acquisition Corp. by the shareholders of MTI;

“Nasdaq” means the Nasdaq Capital Market;

“Nasdaq Rules” means the rules of the Nasdaq Capital Market;

“NHP” means non-human primate;

“NIH” means the National Institutes of Health;

“NK” means natural killer;

“Officer” means an executive officer of the Company;

“Options” means the stock options of the Company;

“OS-24” means overall survival at 24 months;

“Phase 1/2 ABILITY Study” means a Beta-only IL-2 Immuno Therapy Study;

“Preferred Shares” means the Preferred Shares of the Company;

“rGBM” means recurrent glioblastoma;

“RRIF” means Registered Retirement Income Fund;

“RRSP” means Registered Retirement Savings Plan;

“Shareholders” means holders of Common Shares of the Company;

“Stanford” means the Leland Stanford Junior University;

“Stock Option Plan” means the Company’s Stock Option Plan, which was approved for adoption by shareholders on September 21, 2017, which amended, restated and superseded the previous stock option plan adopted by the Company in 2015;

“TFSA” means Tax-Free Savings Account;

“TME” means tumor microenvironment;

“TMZ” means temozolomide;

“Tregs” means regulatory T cells;

“TSX” means the Toronto Stock Exchange; and

“USPTO” means the United States Patent and Trademark Office.

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISORS

Not required.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not required.

3.A.

[Reserved]

3.B. Capitalization and Indebtedness

Not required.

3.C. Reasons for the Offer and Use Of Proceeds

Not required.

3.D. Risk Factors

Following is a list of risks that the Company faces in its normal course of business. The risks and uncertainties set out below are not the only ones the Company is facing. There are additional risks and uncertainties that the Company does not currently know about or that the Company currently considers immaterial which may also impair the Company’s business operations and cause the price of the Common Shares of the Company to decline. If any of the following risks actually occur, the Company’s business may be harmed and the Company’s financial condition and results of operations may suffer significantly. Investors should carefully consider the risk factors set out below and consider all other information contained herein and in the Company's other public filings before making an investment decision. The risks set out below are not an exhaustive list and should not be taken as a complete summary or description of all the risks associated with the Company's business and the biotechnology business generally.

Risks Related to the Company’s Business, Industry, and Financial Position

The Company has no sources of product revenue and there is uncertainty regarding its ability to maintain operations and research and development without sufficient funding.

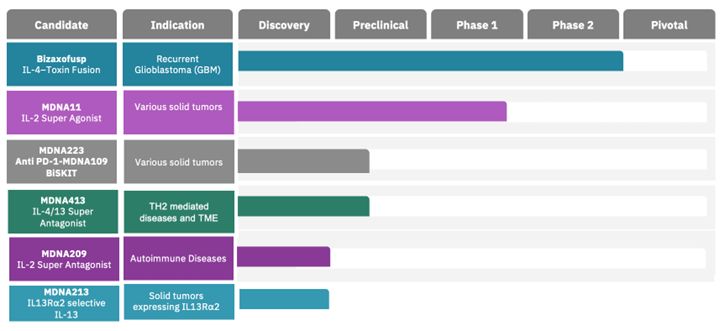

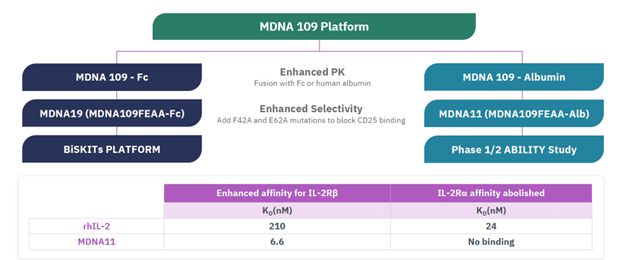

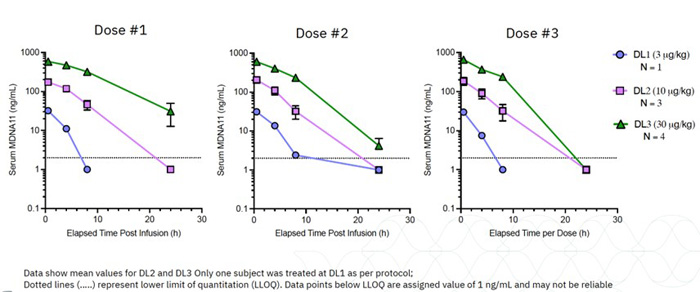

The Company has no sources of product revenue and cannot predict when or if it will generate product revenue. The Company’s ability to generate product revenue and ultimately become profitable depends upon its ability, alone or with partners, to successfully develop the product candidates, obtain regulatory approval, and commercialize products, including any of the current product candidates, or other product candidates that may be developed, in-licensed or acquired in the future. The Company does not anticipate generating revenue from the sale of products for the foreseeable future. The Company expects research and development expenses to increase in connection with ongoing activities, particularly as MDNA11 is advanced from the dose escalation portion of the Phase 1/2 ABILITY Study into the Phase 2 dose expansion cohorts as well as advancing a lead BiSKIT candidate into IND enabling studies.

The Company will require significant additional capital resources to expand its business, in particular the further development of its proposed products. Advancing its product candidates or acquisition and development of any new products or product candidates will require considerable resources and additional access to capital markets. In addition, the Company’s future cash requirements may vary materially from those now expected.

The Company can potentially seek additional funding through corporate collaborations and licensing arrangements, through public or private equity or debt financing, or through other transactions. However, if clinical trial results are neutral or unfavorable, or if capital market conditions in general, or with respect to life sciences companies such as Medicenna, are unfavorable, the Company’s ability to obtain significant additional funding on acceptable terms, if at all, will be negatively affected. Additional financing that it may pursue may involve the sale of the Common Shares or financial instruments that are exchangeable for, or convertible into, the Common Shares, which could result in significant dilution to its shareholders. If sufficient capital is not available, the Company may be required to delay the implementation of its business strategy, which could have a material adverse effect on its business, financial condition, prospects or results of operations.

The Company will need substantial additional funding which may not be available on terms acceptable to the Company or at all. If the Company is unable to raise capital when needed, the Company would be forced to delay, reduce, terminate or eliminate product development programs.

The Company expects research and development expenses to increase in connection with ongoing activities, particularly as MDNA11 is advanced into the Phase 2 portion of the Phase 1/2 ABILITY Study as well as advancing a lead BiSKIT candidate into IND enabling studies. In addition, if the Company obtains regulatory approval for any of its product candidates, the Company expects to incur significant commercialization expenses for product sales, marketing, manufacturing and distribution. Furthermore, the Company will need to obtain additional funding in connection with continuing operations. If the Company is unable to raise capital when needed or on attractive terms, the Company could be forced to delay, reduce, terminate or eliminate its product development programs, potentially including the ongoing Phase 1/2 ABILITY Study.

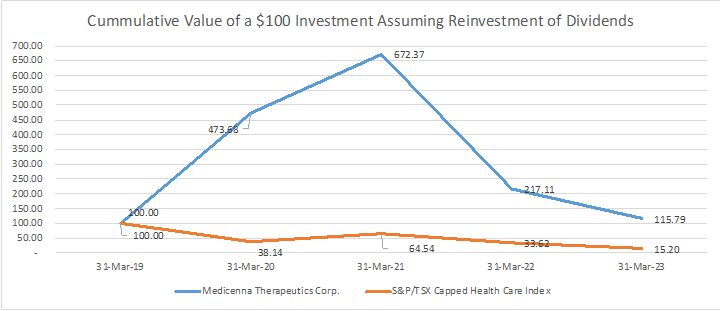

As of March 31, 2023, the Company had cash and cash equivalents of $33.6 million.

Developing pharmaceutical products, which includes manufacturing, quality control, conducting preclinical studies and clinical trials, is expensive. Our operations have consumed significant amounts of cash since inception. As we continue to advance MDNA11 or future product candidates into clinical trials and launch and commercialize any product candidates for which we receive regulatory approval, we expect research and clinical development expenses, as well as selling, general and administrative expenses to increase substantially. In connection with our ongoing activities, we believe that our existing cash and cash equivalents will be sufficient to fund our operating requirements through calendar Q3 2024. However, circumstances may cause us to consume capital more rapidly than we anticipate. We will require additional capital for the further development and potential commercialization of future product candidates.

We have incurred significant losses in every quarter since our inception and anticipate that we will continue to incur significant losses in the future.

Investment in a biotechnology company is highly speculative because it entails substantial upfront capital expenditures and significant risk that any potential product candidate will fail to demonstrate adequate effect or an acceptable safety profile, gain regulatory approval or become commercially viable. We have not generated any revenue from product sales to date, and all of our product candidates are in early clinical or preclinical development. We continue to incur significant expenses related to our ongoing operations. As a result, we are not profitable and have incurred losses in every reporting period since our inception. We expect to continue to incur significant expenses and operating losses for the foreseeable future as we seek to identify, acquire and conduct research and development of future product candidates, and potentially begin to commercialize any future products that may achieve regulatory approval. We may encounter unforeseen expenses, difficulties, complications, delays and other unknown factors that may adversely affect our financial condition. The size of our future net losses will depend, in part, on the rate of future growth of our expenses and our ability to generate revenues. Our prior losses and expected future losses have had, and will continue to have, an adverse effect on our financial condition. If any of our future product candidates fail in clinical trials or do not gain regulatory approval, or if approved, fail to achieve market acceptance, we may never become profitable. Even if we achieve profitability in the future, we may not be able to sustain profitability in subsequent periods.

Risks Related to the Discovery, Development and Commercialization of our Product Candidates

Our product candidates are in early stages of development and may fail in development or suffer delays that materially and adversely affect their commercial viability. If we are unable to complete development of, or commercialize our product candidates, if approved, or experience significant delays in doing so, our business will be materially harmed.

We are in the early stages of development efforts for MDNA11 and our BiSKIT platform. We have no products on the market and all of our product candidates, with the exception of bizaxofusp which is not in active development by the Company, are still in early clinical, preclinical or drug discovery stages, and we may not ever obtain regulatory approval for any of our product candidates. We have limited experience in conducting and managing the clinical trials necessary to obtain regulatory approvals, including approval by the FDA. Before obtaining regulatory approval for the commercial distribution of our product candidates, we or an existing or future collaborator must conduct extensive preclinical tests and clinical trials to demonstrate the safety and efficacy in humans of our product candidates. Additionally, our BiSKIT platform is in earlier stages of discovery and preclinical development and may never advance to clinical-stage development. If we do not receive marketing approvals and successfully commercialize our product candidates, if approved, we may not be able to continue our operations.

The success of the Company’s product candidates will depend on several factors, including the following:

| ● |

securing additional funding to continue development; |

| ● |

successful completion of preclinical studies and clinical trials; |

| ● |

demonstrating a superior product profile compared with competitors; |

| ● |

receipt of marketing approvals from the FDA, Health Canada and similar regulatory authorities outside the United States and Canada; |

| ● |

establishing commercial manufacturing capabilities by identifying and securing arrangements with third party manufacturers for the product candidates; |

| ● |

maintaining patent and trade secret protection and regulatory exclusivity for the product candidates; |

| ● |

launching commercial sales of the product candidates, if and when approved, whether alone or in collaboration with others; |

| ● |

acceptance of the products, if and when approved, by patients, the medical community and third party payers; |

| ● |

effectively competing with other therapies; and |

| ● |

a continued acceptable safety profile of the products following approval. |

If the Company does not achieve one or more of these factors in a timely manner or at all, the Company could experience significant delays or an inability to successfully commercialize its product candidates, if approved, which would materially harm its business.

Clinical drug development involves a lengthy and expensive process with an uncertain outcome, results of earlier studies and trials may not be predictive of future trial results, and the Company’s product candidates may not have favorable results in later trials or in the commercial setting.

Clinical testing is expensive and can take many years to complete, and its outcome is inherently uncertain. Failure can occur at any time during the clinical trial process. The results of preclinical studies and early clinical trials may not be predictive of the results of later-stage clinical trials. In the case of bizaxofusp, the promising results seen in the Phase 2b clinical study may not be replicated in a randomized, controlled Phase 3 clinical study. Success in preclinical or animal studies and early clinical trials does not ensure that later large-scale efficacy trials will be successful nor does it predict final results. This is applicable to MDNA11 as the promising preclinical data may not be replicated in the Phase 1/2 ABILITY Study. Favorable results in early trials may not be repeated in later trials. There is no assurance the FDA, the EMA or other similar government bodies will view the results as the Company does or that any future trials of its product candidates for other indications will achieve positive results. Product candidates in later stages of clinical trials may fail to show the desired safety and efficacy traits despite having progressed through preclinical studies and initial clinical trials.

The Company will be required to demonstrate through larger-scale clinical trials that any product candidate is safe and effective before it can seek regulatory approvals for commercial sale of its product. There is typically an extremely high rate of attrition from the failure of product candidates proceeding through clinical and post-approval trials. If bizaxofusp, MDNA11 and other product candidates fail to demonstrate sufficient safety and efficacy in future clinical trials, the Company’s operations and financial condition will be adversely impacted.

The Company may not achieve its publicly announced milestones according to schedule, or at all.

From time to time, the Company may announce the timing of certain events expected to occur, such as the anticipated timing of results from clinical trials. These statements are forward-looking and are based on the best estimates of management at the time relating to the occurrence of such events. However, the actual timing of such events may differ from what has been publicly disclosed. The timing of events such as initiation or completion of a clinical trial, filing of an application to obtain regulatory approval or announcement of additional clinical trials for a product candidate may ultimately vary from what is publicly disclosed. These variations in timing may occur as a result of different events, including the ability to recruit patients in a clinical trial in a timely manner, the nature of results obtained during a clinical trial or during a research phase, problems with a contract development and manufacturing organizations (“CDMO”) or a contract research organization (“CRO”), or any other event having the effect of delaying the publicly announced timeline. The Company undertakes no obligation to update or revise any forward-looking information, whether as a result of new information, future events or otherwise, except as otherwise required by law. Any variation in the timing of previously announced milestones could have a material adverse effect on the business plan, financial condition or operating results and the trading price of the Common Shares.

If the Company’s competitors develop and market products that are more effective than the Company’s existing product candidates or any future product candidates it may develop, or if they obtain marketing approval before it does, the Company’s products may be rendered obsolete or uncompetitive.

Competition from pharmaceutical companies, biotechnology companies and universities is intense and is expected to increase. Many of the Company’s competitors and potential competitors have substantially greater product development capabilities and financial, scientific, marketing and human resources than the Company does. Our future success depends in part on our ability to maintain a competitive position, including our ability or the ability of our partners to further progress bizaxofusp, MDNA11 and our BiSKIT platform through the necessary preclinical and clinical trials towards regulatory approval for sale and commercialization. MDNA11 is in a particularly competitive space and the need to differentiate the program clinically is important to its future success. Other companies may succeed in commercializing their products earlier than we are able to commercialize our product candidates, if approved, or they may succeed in developing products that are more effective than our product candidates, if approved. While the Company will seek to expand its technological capabilities in order to remain competitive, there can be no assurance that developments by others will not render its product candidates, if approved, non-competitive or that the Company or its licensors will be able to keep pace with technological developments. Competitors have developed technologies that could be the basis for competitive products. Some of those products may have an entirely different approach or means of accomplishing the desired therapeutic effect than the Company’s product candidates and may be more effective or less costly than its product candidates. In addition, other forms of medical treatment may offer competition to the product candidates, if approved. The success of the Company’s competitors and their products and technologies relative to its technological capabilities and competitiveness could have a material adverse effect on the future preclinical and clinical trials of its product candidates, including its ability to obtain the necessary regulatory approvals for the conduct of such trials.

The Company may not be able to secure a partnership for bizaxofusp which would halt future development.

The Company is seeking a partner to continue the clinical development and commercialization of bizaxofusp. The Company does not have the financial resources to complete the necessary development work internally and should it not be able to secure a partnership, further development of bizaxofusp may not continue.

The Company is subject to extensive government regulation that will increase the cost and uncertainty associated with gaining regulatory approval of its product candidates.

Securing regulatory approval for the manufacture and sale of human therapeutic products in the United States, Canada and other markets is a long and costly process that is controlled by that particular country’s national regulatory agency. Approval in the United States, Canada or Europe does not assure approval by other national regulatory agencies, although often test results from one country may be used in applications for regulatory approval in another country. Other national regulatory agencies may have similar regulatory approval processes, but each is different.

Prior to obtaining regulatory approval to market a drug product, every national regulatory agency has a variety of statutes and regulations which govern the principal development activities. These laws require controlled research and testing of product candidates, government review and approval of a submission containing preclinical and clinical data establishing the safety and efficacy of the product candidate for each use sought, approval of manufacturing facilities including adherence to cGMP during production and storage and control of marketing activities, including advertising and labelling. There can be no assurance that MDNA11 or bizaxofusp will be approved or successfully commercialized, if approved, in any given country. There can be no assurance that the Company’s product candidates will prove to be safe and effective in clinical trials under the standards of the regulations in the various jurisdictions or receive applicable regulatory approvals from applicable regulatory bodies.

Negative results from clinical trials or studies of third parties and adverse safety events involving the targets of the Company’s product candidates may have an adverse impact on future commercialization efforts.

From time to time, studies or clinical trials on various aspects of biopharmaceutical products are conducted by academic researchers, competitors or others. The results of these studies or trials, when published, may have a significant effect on the market for the biopharmaceutical product that is the subject of the study. The publication of negative results of studies or clinical trials or adverse safety events related to the Company’s product candidates, or the therapeutic areas in which the Company’s product candidates compete, could adversely affect the share price and ability to finance future development of the Company’s product candidates, and the business and financial results could be materially and adversely affected.

The Company faces the risk of product liability claims, which could exceed its insurance coverage and cause product recalls, each of which could deplete cash resources.

The Company is exposed to the risk of product liability claims alleging that use of its product candidates MDNA11, bizaxofusp, and in the future, the BiSKIT platform, caused an injury or harm. These claims may arise at any point in the development, testing, manufacture, marketing or sale of product candidates and may be made directly by patients involved in clinical trials of product candidates, by consumers or healthcare providers or by individuals, organizations or companies selling the product candidates, if approved. Product liability claims can be expensive to defend, even if the product or product candidate did not actually cause the alleged injury or harm.

Insurance covering product liability claims becomes increasingly expensive as a product candidate moves through the development pipeline to commercialization. Currently the Company maintains clinical trial liability insurance coverage of US$5 million. However, there can be no assurance that such insurance coverage is or will continue to be adequate or available at a cost acceptable to the Company or at all. The Company may choose or find it necessary under its collaborative agreements to increase the insurance coverage in the future, but may not be able to secure greater or broader product liability insurance coverage on acceptable terms or at reasonable costs when needed. Any liability for damages resulting from a product liability claim could exceed the amount of the coverage, require payment of a substantial monetary award from the Company’s cash resources and have a material adverse effect on the business, financial condition and results of operations. Moreover, a product recall, if required, could generate substantial negative publicity about the products and business, inhibit or prevent commercialization of other products and product candidates, if approved, or negatively impact existing or future collaborations.

If the Company is unable to enroll subjects in clinical trials, it will be unable to complete its clinical trials on a timely basis.

Patient enrollment, a significant factor in the timing of clinical trials, is affected by many factors including the size and nature of the patient population, the proximity of subjects to clinical sites, the eligibility criteria for the trial, the design of the clinical trial, the ability to obtain and maintain patient consents, the risk that enrolled subjects will drop out before completion, competing clinical trials, and clinicians’ and patients’ perceptions as to the potential advantages of the drug being studied in relation to other available therapies, including any new drugs that may be approved for the indications the Company is investigating. Furthermore, the Company relies on CROs and clinical trial sites to ensure the proper and timely conduct of its clinical trials, and while it has agreements governing their committed activities, the Company has limited influence over their actual performance.

If the Company experiences delays in the completion or termination of any clinical trial of its product candidates or any future product candidates, the commercial prospects of its product candidates will be harmed and its ability to generate product revenues from any of these product candidates, if approved, will be delayed. In addition, any delays in completing clinical trials will increase costs, slow down product candidate development and approval processes and may shorten any periods during which the Company may have the exclusive right to commercialize its product candidates, if approved, all of which may allow the Company’s competitors to bring products to market before it does. Delays may further jeopardize the Company’s ability to commence product sales, which will impair its ability to generate revenues and may harm the business, results of operations, financial condition and cash flows and future prospects. In addition, many of the factors that may cause a delay in the commencement or completion of clinical trials may also ultimately lead to the denial of regulatory approval of its product candidates or its future product candidates.

Even if any product candidates we develop receive marketing approval, they may fail to achieve the degree of market acceptance by physicians, patients, healthcare payers, and others in the medical community necessary for commercial success.

The commercial success of any of our product candidates, if approved, will depend upon its degree of market acceptance by physicians, patients, third party payers, and others in the medical community. Even if any product candidates we may develop receive marketing approval, they may nonetheless fail to gain sufficient market acceptance by physicians, patients, healthcare payers, and others in the medical community. The degree of market acceptance of any product candidates we may develop, if approved for commercial sale, will depend on a number of factors, including:

| ● |

the efficacy and safety of such product candidates as demonstrated in pivotal clinical trials and published in peer-reviewed journals; |

| ● |

the potential and perceived advantages compared to alternative treatments; |

| ● |

the ability to offer our products for sale at competitive prices; |

| ● |

the ability to offer appropriate patient access programs, such as co-pay assistance; |

| ● |

the extent to which physicians recommend our products to their patients; |

| ● |

convenience and ease of dosing and administration compared to alternative treatments; |

| ● |

the clinical indications for which the product candidate is approved by the FDA, EMA or other comparable foreign regulatory agencies; |

| ● |

product labeling or product insert requirements of the FDA, EMA or other comparable foreign regulatory authorities, including any limitations, contraindications or warnings contained in a product’s approved labeling; |

| ● |

restrictions on how the product is distributed; |

| ● |

the timing of market introduction of competitive products; |

| ● |

publicity concerning our products or competing products and treatments; |

| ● |

the effectiveness of marketing and distribution efforts by us and other licenses and distributors; |

| ● |

sufficient governmental and third-party coverage or reimbursement; and |

| ● |

the prevalence and severity of any side effects. |

If any product candidates we develop and for which we receive marketing approval do not achieve an adequate level of acceptance by physicians, healthcare payers, patients and the medical community, we will not be able to generate significant revenue, and we may not become or remain profitable. The failure of any of our product candidates, if approved, to find market acceptance would harm our business prospects.

The Company’s discovery, testing, development and manufacturing processes involve the use of hazardous and radioactive materials which may result in potential environmental exposure.

Although our current laboratory and manufacturing activities are handled by third parties, the Company’s discovery, testing and development processes may, in the future, involve the direct controlled use of hazardous and radioactive materials. Accordingly, the Company may become subject to federal, provincial, state and local laws and regulations governing the use, manufacture, storage, handling and disposal of such materials and certain waste products. The risk of accidental contamination or injury from these materials cannot be completely eliminated. In the event of such an accident, the Company could be held liable for any damages that result and any such liability could exceed the Company’s resources. The Company is not specifically insured with respect to this liability. There can be no assurance that the Company will not be required to incur significant costs to comply with environmental laws and regulations in the future, or that the operations, business or assets will not be materially adversely affected by current or future environmental laws or regulations.

Significant disruption in availability of key components for ongoing clinical studies could considerably delay completion of potential clinical trials, product testing and regulatory approval of potential product candidates.

The Company relies on third parties to supply ingredients and excipients for the manufacture and formulation of its product candidates, compatible syringes or infusion systems for drug administration, catheters required to deliver the product candidate to the brain as well as imaging software to accurately place catheters in the tumor (“Components”). Each of the suppliers of these Components in turn need to comply with applicable regulatory requirements. Any significant disruption in supplier relationships could harm the Company’s business. Any significant delay in the supply of a Component for an ongoing or future clinical study could considerably delay initiation or completion of a clinical trial, drug manufacturing, drug testing and regulatory approval of a product candidate or future product candidate. If the Company or its suppliers are unable to purchase these Components after regulatory approval has been obtained for the product candidates, or the suppliers decide not to manufacture these Components or provide support for any of the Components, clinical trials or the commercial launch of that product candidate, if approved, would be delayed or there would be a shortage in supply, which would impair the ability to generate revenues from the sale of the product candidates, if approved. It may take several years to establish an alternative source of supply for such Components and to have any such new source approved by the FDA and other regulatory agencies.

Preliminary and interim data from our clinical trials that we may announce or publish from time to time may change as patient data are further examined, audited or verified and more patient data become available.

From time to time, we may announce or publish preliminary or interim data from our clinical trials. Preliminary and interim data remain subject to audit and verification procedures that may result in the final data being materially different from the preliminary or interim data. Preliminary and interim results of a clinical trial are not necessarily predictive of final results. There can be no assurance that favorable interim or preliminary data will result in favorable final data. Preliminary and interim data are subject to the risk that one or more of the clinical outcomes may materially change as patient enrollment continues, patient data are further examined and reviewed, more patient data become available, and we prepare and issue our final clinical study report. As a result, preliminary and interim data should be viewed with caution until the final, complete data are available. Material adverse changes in the final data compared to the preliminary or interim data could significantly harm our business, prospects, financial condition and results of operations.

Biologics carry unique risks and uncertainties, which could have a negative impact on future results of operations.

The successful discovery, development, manufacturing and sale of biologics is a long, expensive and uncertain process. There are unique risks and uncertainties with biologics. For example, access to and supply of necessary biological materials, such as cell lines, may be limited and governmental regulations restrict access to and regulate the transport and use of such materials. In addition, the development, manufacturing and sale of biologics is subject to regulations that are often more complex and extensive than the regulations applicable to other pharmaceutical products. Manufacturing biologics, especially in large quantities, is often complex and may require the use of innovative technologies. Such manufacturing also requires facilities specifically designed and validated for this purpose and sophisticated quality assurance and quality control procedures. Biologics are also frequently costly to manufacture because production inputs are derived from living animal or plant material, and some biologics cannot be made synthetically. Failure to successfully discover, develop, manufacture and sell our biological candidates would adversely impact our business and future results of operations.

Bizaxofusp has been granted Fast Track designation by the FDA and we may seek Fast Track designation for one or more of our other drug or biologic candidates in the future. Even if we apply for Fast Track designation in the future, we might not receive such designation, and even if we do, such designation may not actually lead to a faster development or regulatory review or approval process, and further, such designation could be withdrawn by the FDA.

If a drug or biologic candidate is intended for the treatment of a serious condition and nonclinical or clinical data demonstrate the potential to address an unmet medical need for this condition, a product sponsor may request an FDA Fast Track designation from the FDA. If we seek Fast Track designation for a drug or biologic candidate, we may not receive it from the FDA. However, even if we receive Fast Track designation, Fast Track designation does not ensure that we will receive marketing approval or that approval will be granted within any particular time frame. We may not experience a faster development or regulatory review or approval process with Fast Track designation compared to conventional FDA procedures. In addition, the FDA may withdraw Fast Track designation if the designation is no longer supported by data from our clinical development program. Fast Track designation alone does not guarantee qualification for the FDA’s priority review procedures.

Even if we obtain regulatory approval for a product, we will remain subject to ongoing regulatory requirements. Maintaining compliance with ongoing regulatory requirements may result in significant additional expense to us, and any failure to maintain such compliance could subject us to penalties and cause our business to suffer.

If any of our drug or biologic candidates are approved, we will be subject to ongoing regulatory requirements with respect to manufacturing, labeling, packaging, storage, advertising, promotion, sampling, record-keeping, conduct of post-marketing clinical trials and submission of safety, efficacy and other post-approval information, including both federal and state requirements in the United States and requirements of comparable foreign regulatory authorities.

Manufacturers and manufacturers’ facilities are required to continuously comply with FDA and comparable foreign regulatory authority requirements, including ensuring that quality control and manufacturing procedures conform to cGMP regulations and corresponding foreign regulatory manufacturing requirements. As such, we and our CDMOs will be subject to continual review and inspections to assess compliance with cGMP and adherence to commitments made in any BLA, NDA or other marketing authorization application.

Any regulatory approvals that we receive for our drug or biologic candidates may be subject to limitations on the approved indicated uses for which the drug or biologic candidate may be marketed or to the conditions of approval, or contain requirements for potentially costly post-marketing testing, including Phase IV clinical trials, and surveillance to monitor the safety and efficacy of the drug or biologic candidate. In addition, if the FDA or a comparable foreign regulatory authority approves any of our drug or biologic candidates, the manufacturing processes, labeling, packaging, distribution, adverse event reporting, storage, advertising, promotion and record keeping for the products will be subject to extensive and ongoing regulatory requirements. Any new legislation addressing drug safety issues could result in delays in product development or commercialization, or increased costs to assure compliance.

We must also comply with requirements concerning advertising and promotion for any of our drug or biologic candidates for which we hope to obtain marketing approval. Promotional communications with respect to prescription drugs and biologics are subject to a variety of legal and regulatory restrictions and must be consistent with the information in the product’s approved labeling. If we are not able to comply with post-approval regulatory requirements, we could have marketing approval for any of our products withdrawn by regulatory authorities and our ability to market any future products could be limited, which could adversely affect our ability to achieve or sustain profitability. Thus, the cost of compliance with post-approval regulations may have a negative effect on our operating results and financial condition.

In addition, later discovery of previously unknown problems with a product, such as adverse events of unanticipated severity or frequency, or problems with the facility where the product is manufactured, or failure to comply with applicable regulatory requirements may result in a variety of risks. For example, a regulatory agency or enforcement authority may, among other things:

| ● |

impose restrictions on the marketing or manufacturing of the product, complete withdrawal of the product from the market or product recalls; |

| ● |

impose requirements to conduct post-marketing studies or clinical trials; |

| ● |

issue warning or untitled letters if the regulator is the FDA, or comparable notice of violations from foreign regulatory authorities; |

| ● |

issue consent decrees, injunctions or impose civil or criminal penalties; |

| ● |

require the payment of fines, restitution or disgorgement of profits or revenues; |

| ● |

suspend or withdraw regulatory approval; |

| ● |

suspend any of our ongoing clinical trials; |

| ● |

refuse to approve pending applications or supplements to approved applications submitted by us; |

| ● |

impose restrictions on our operations, including closing our or our CDMOs’ manufacturing or analytical testing facilities; or |

| ● |

require product seizure or detention, recalls or refuse to permit the import or export of products. |

Any government investigation of alleged violations of law would require us to expend significant time and resources in response and could generate adverse publicity. Any failure to comply with ongoing regulatory requirements may significantly and adversely affect our ability to develop and commercialize our products and our value and our operating results would be adversely affected. In addition, regulatory authorities’ policies (such as those of the FDA or EMA) may change and additional government regulations may be enacted that could prevent, limit or delay regulatory approval of our drug or biologic candidates. If we are slow or unable to adapt to changes in existing requirements or the adoption of new requirements or policies, or if we are otherwise not able to maintain regulatory compliance, we may lose any marketing approval that we may have obtained, which would adversely affect our business, prospects and ability to achieve or sustain profitability.

We currently have limited marketing and sales experience. If we are unable to establish sales and marketing capabilities or enter into agreements with third parties to market and sell our drug or biologic candidates, we may be unable to generate any revenue.

Although some of our employees may have marketed, launched and sold other pharmaceutical products in the past while employed at other companies, we have no experience selling and marketing our drug or biologic candidates, and we currently have no marketing or sales organization. To successfully commercialize any products that may result from our development programs, we will need to find one or more collaboration partners to commercialize our products or invest in and develop these capabilities, either on our own or with others, which would be expensive, difficult and time consuming. Any failure or delay in the timely development of our internal commercialization capabilities could adversely impact the potential for success of our products.

If commercialization collaboration partners do not commit sufficient resources to commercialize our future drugs or biologics, and if we are unable to develop the necessary marketing and sales capabilities on our own, we will be unable to generate sufficient product revenue to sustain or grow our business. We may be competing with companies that currently have extensive and well-funded marketing and sales operations, particularly in the markets our drug or biologic candidates are intended to address. Without appropriate capabilities, whether directly or through third-party collaboration partners, we may be unable to compete successfully against these more established companies.

Failure to obtain or maintain adequate reimbursement or insurance coverage for approved products, if any, could limit our ability to market those products and decrease our ability to generate revenue.

The pricing, coverage, and reimbursement of our approved drugs, if any, must be sufficient to support our commercial efforts and other development programs, and the availability and adequacy of coverage and reimbursement by third-party payors, including governmental and private insurers, are essential for most patients to be able to afford medical treatments. Sales of our approved drugs, if any, will depend substantially, both domestically and abroad, on the extent to which the costs of our approved drugs, if any, will be paid for or reimbursed by health maintenance, managed care, pharmacy benefit and similar healthcare management organizations, or government payors and private payors. If coverage and reimbursement are not available, or are available only in limited amounts, we may have to subsidize or provide drugs for free or we may not be able to successfully commercialize our drugs.

In addition, there is significant uncertainty related to the insurance coverage and reimbursement for newly approved drugs. In the United States, the principal decisions about coverage and reimbursement for new drugs are typically made by the Centers for Medicare and Medicaid Services (“CMS”) an agency within the United States Department of Health and Human Services, as CMS decides whether and to what extent a new drug will be covered and reimbursed under Medicare. Private payors tend to follow the coverage reimbursement policies established by CMS to a substantial degree. It is difficult to predict what CMS will decide with respect to reimbursement for novel drug or biologic candidates such as ours and what reimbursement codes our drug or biologic candidates may receive if approved. Moreover, Congress recently enacted and President Biden signed into law new authorities for CMS to negotiate drug prices annually for certain prescription drugs and biological products, subject to statutory criteria and a future selection process that is in the process of being developed by CMS. It is unclear how these forthcoming changes in the way that CMS does business with certain members of the biopharmaceutical industry may impact coverage or reimbursement decisions across the industry as a whole.

Outside the United States, international operations are generally subject to extensive governmental price controls and other price-restrictive regulations, and we believe the increasing emphasis on cost-containment initiatives in Europe, Canada and other countries has and will continue to put pressure on the pricing and usage of drugs. In many countries, the prices of drugs are subject to varying price control mechanisms as part of national health systems. Price controls or other changes in pricing regulation could restrict the amount that we are able to charge for our drugs, if any. Accordingly, in markets outside the United States, the potential revenue may be insufficient to generate commercially reasonable revenue and profits.

Moreover, increasing efforts by governmental and private payors in the United States and abroad to limit or reduce healthcare costs may result in restrictions on coverage and the level of reimbursement for new drugs and, as a result, they may not cover or provide adequate payment for our drugs, if any. We expect to experience pricing pressures in connection with drugs due to the increasing trend toward managed healthcare, including the increasing influence of health maintenance organizations and additional legislative changes. The downward pressure on healthcare costs in general, and prescription drugs or biologics in particular, has and is expected to continue to increase in the future. As a result, profitability of our drugs, if any, may be more difficult to achieve even if any of them receive regulatory approval.

Risks Related to the Company’s Reliance on Third Parties

The Company relies and will continue to rely on third parties to plan, conduct and monitor preclinical studies and clinical trials, and their failure to perform as required could cause substantial harm to the Company’s business.

The Company relies and will continue to rely on third parties to conduct a significant portion of clinical development and planned preclinical activities. Preclinical activities include in vivo studies providing access to specific disease models in different species, pharmacology and toxicology studies, and assay development. Clinical development activities include trial design, regulatory submissions, clinical patient recruitment, clinical trial monitoring, clinical data management and analysis, safety monitoring and project management. If there is any dispute or disruption in the Company’s relationship with third parties, or if the third party is unable to provide quality services in a timely manner and at a reasonable cost, or is unable to secure access to specific disease models or is unable to acquire and maintain inventory of different species required for pre-clinical testing, any active development programs could face delays. Further, if any of these third parties fails to perform as expected or if their work fails to meet regulatory requirements, testing could be delayed, cancelled or rendered ineffective.

The Company relies on contract manufacturers over whom the Company has limited control. If the Company is subject to quality, cost or delivery issues with the preclinical and clinical grade materials supplied by contract manufacturers, business operations could suffer significant harm.

The Company has limited manufacturing experience and relies on CDMOs to manufacture MDNA11 and bizaxofusp for clinical trials and the BiSKIT Platform for preclinical development as well as for manufacturing, testing, filling, packaging, storing and shipping of its product candidates in compliance with cGMP, regulations applicable to its products. The FDA ensures the quality of drug products by carefully monitoring drug manufacturers’ compliance with cGMP regulations. The cGMP regulations for drugs contain minimum requirements for the methods, facilities and controls used in manufacturing, processing and packing of a drug product.

There can be no assurances that the CDMOs selected will be able to meet future timetables and requirements. If the Company is unable to arrange for alternative third-party manufacturing sources on commercially reasonable terms or in a timely manner, it may delay the development of the product candidates. Further, contract manufacturers must operate in compliance with cGMP and failure to do so could result in, among other things, the disruption of product supplies. The Company’s dependence upon third parties for the manufacture of its product candidates may adversely affect profit margins and ability to develop and deliver product candidates, if approved, on a timely and competitive basis.

Our reliance on third-party manufacturers also exposes us to the following additional risks:

| ● |

we may be unable to identify manufacturers to manufacture our drug or biologic candidates on acceptable terms or at all, because the number of qualified potential manufacturers is limited. Following NDA or BLA approval, a change in the manufacturing site could require additional approval from the FDA. This approval would require new testing and compliance inspections; |

| ● |

our third-party manufacturers might be unable to timely formulate and manufacture our product or produce the quantity and quality required to meet our clinical and commercial needs, if any; |

| ● |

our future third-party manufacturers may not perform as agreed or may not remain in the contract manufacturing business for the time required to supply our clinical trials or to successfully produce, store and distribute our drug or biologic candidates; |

| ● |

if any third-party manufacturer makes improvements in the manufacturing process for our products, we may not own or be able to license, or we may have to share, the intellectual property rights to any improvements made by our third-party manufacturers in the manufacturing process for our drug or biologic candidates; |

| ● |

while we currently carry insurance in an amount and on terms and conditions that are customary for similarly situated companies and that are satisfactory to our board of directors, we and/or our third-party manufacturers may not have sufficient insurance coverage in the event of any inadvertent destruction of or loss of any drug substance by them, which could result in delays in production and/or our clinical trials and/or result in additional costs to us; and |

| ● |

our third-party manufacturers could breach or terminate their agreements with us. |

Our employees, independent contractors, principal investigators, CROs, consultants or vendors may engage in misconduct or other improper activities, including noncompliance with regulatory standards and requirements.

We are exposed to the risk that our employees, independent contractors, principal investigators, CROs, consultants or vendors may engage in fraudulent or other illegal activity. Misconduct by these parties could include intentional, reckless and/or negligent conduct or disclosure of unauthorized activities to us that violates: FDA regulations, including those laws requiring the reporting of true, complete and accurate information to the FDA; manufacturing standards; federal and state health care fraud and abuse laws and regulations; or laws that require the true, complete and accurate reporting of financial information or data. In addition, sales, marketing and business arrangements in the health care industry are subject to extensive laws and regulations intended to prevent fraud, kickbacks, self-dealing and other abusive practices. These laws and regulations may restrict or prohibit a wide range of pricing, discounting, marketing and promotion, sales commission, customer incentive programs and other business arrangements. Activities subject to these laws also involve the improper use or misrepresentation of information obtained in the course of clinical trials or creating fraudulent data in our preclinical studies or clinical trials, which could result in regulatory sanctions and serious harm to our reputation.

It is not always possible to identify and deter misconduct by our employees and other third parties, and the precautions we take to detect and prevent this activity may not be effective in controlling unknown or unmanaged risks or losses or in protecting us from governmental investigations or other actions or lawsuits stemming from a failure to be in compliance with such laws or regulations. Additionally, we are subject to the risk that a person could allege such fraud or other misconduct, even if none occurred. If any such actions are instituted against us, and we are not successful in defending ourselves or asserting our rights, those actions could have a significant impact on our business, including the imposition of civil, criminal and administrative penalties, damages, monetary fines, possible exclusion from participation in Medicare, Medicaid and other federal health care programs, contractual damages, reputational harm, diminished potential profits and future earnings, and curtailment of our operations, any of which could adversely affect our business, financial condition, results of operations or prospects.

If the Company breaches any of the agreements under which it licenses rights to product candidates or technology from third parties, it can lose license rights that are important to its business. The Company’s current license agreements may not provide an adequate remedy for breach by the licensor.

The Company is seeking a partnership for bizaxofusp, developing MDNA11 and other earlier stage preclinical and discovery drug candidates pursuant to license agreements with NIH and Stanford (collectively, the “Licensors”). The Company is subject to a number of risks associated with its collaboration with the Licensors, including the risk that the Licensors may terminate a license agreement upon the occurrence of certain specified events. Each license agreement requires, among other things, that the Company makes certain payments and use reasonable commercial efforts to meet certain clinical and regulatory milestones. If the Company fails to comply with any of these obligations or otherwise breaches this or similar agreements, the Licensors or any future licensors may have the right to terminate the license in whole. The Company may also suffer the consequences of non-compliance or breaches by Licensors in connection with the license agreements. Such non-compliance or breaches by such third parties may in turn result in breaches or defaults under the Company’s agreements with other collaboration partners, and the Company may be found liable for damages or lose certain rights, including rights to develop and/or commercialize a product or product candidate, if approved. Loss of the Company’s rights to the licensed intellectual property or any similar license granted to it in the future, or the exclusivity rights provided therein, may harm the Company’s financial condition and operating results.

The Company is subject to the restrictions and conditions of the CPRIT agreement. Failure to comply with the CPRIT agreement may adversely affect the Company’s financial condition and results of operations.

The Company obtained a grant from CPRIT to fund a portion of its historical operations. If the Company is found to have used any grant proceeds for purposes other than intended, is in violation of the terms of the grant, or relocates its bizaxofusp related operations outside of the State of Texas, then the Company may be required to repay the grant proceeds received. A failure to maintain compliance with the grant, including maintaining a presence in the state of Texas for three years after the grant is complete, may require the Company to reimburse all or a portion of the CPRIT grant which may cause a halt or delay in ongoing operations, which may adversely affect the Company’s financial condition and operating results.

Risks Related to Intellectual Property and Litigation

The Company’s success depends upon its ability to protect its intellectual property and its proprietary technology.

The Company’s success depends, in part, on its ability and its licensors’ ability to obtain patents, maintain trade secrets protection and operate without infringing on the proprietary rights of third parties or having third parties circumvent its rights. Certain licensors and the institutions that they represent have filed and are actively pursuing certain applications for certain Canadian and foreign patents. The patent position of pharmaceutical and biotechnology firms is uncertain and involves complex legal and financial questions for which, in some cases, certain important legal principles remain unresolved. There can be no assurance that the patent applications made in respect of the owned or licensed products will result in the issuance of patents, that the term of a patent will be extendable after it expires in due course, that the licensors or the institutions that they represent will develop additional proprietary products that are patentable, that any patent issued to the licensors or the Company will provide it with any competitive advantages, that patents of others will not impede its ability to do business or that third parties will not be able to circumvent or successfully challenge the patents obtained in respect of the licensed products. The cost of obtaining and maintaining patents is high and may affect the Company’s financial condition. Furthermore, there can be no assurance that others will not independently develop competitor products which duplicate any of the owned/licensed products under pending patent protection or, if patents are issued to such owned/licensed products, will not design around such patents. There can be no assurance that the Company’s processes or products or those of its licensors do not or will not infringe upon the patents of third parties or that the scope of its patents or those of its licensors will successfully prevent third parties from developing similar and competitive products.

Much of the Company’s know-how and technology may not be patentable, though it may constitute trade secrets. There can be no assurance, however, that the Company will be able to meaningfully protect its trade secrets. To help protect its intellectual property rights and proprietary technology, the Company requires employees, consultants, advisors and collaborators to enter into confidentiality agreements. There can be no assurance that these agreements will provide meaningful protection for its intellectual property rights or other proprietary information in the event of any unauthorized use or disclosure.

The Company’s potential involvement in intellectual property litigation could negatively affect its business.

The Company’s future success and competitive position depends in part upon its ability to maintain its intellectual property portfolio. There can be no assurance that any patents will be issued on any existing or future patent applications. Even if such patents are issued, there can be no assurance that any patents issued or licensed to the Company will not be successfully challenged. The Company’s ability to establish and maintain a competitive position may require that it successfully prosecute claims against others who it believes are infringing its rights and successfully defend claims brought by others who believe that the Company is infringing their rights. In addition, enforcement of its patents in foreign jurisdictions will depend on the legal procedures in those jurisdictions. Even if the Company is successful in intellectual property litigation, the Company’s involvement in such litigation could have a material adverse effect on its ability to out-license any products that are the subject of such litigation and could result in significant expense, which could materially adversely affect the use or licensing of related intellectual property and divert the efforts of its valuable technical and management personnel from their principal responsibilities, whether or not such litigation is resolved in its favor.

The Company’s reliance on third parties requires it to share its trade secrets, which increases the possibility that a competitor will discover them.

Because the Company relies on third parties to develop its products, it must share trade secrets with them. The Company seeks to protect its proprietary technology in part by entering into confidentiality agreements and, if applicable, material transfer agreements, collaborative research agreements, consulting agreements or other similar agreements with its collaborators, advisors, employees and consultants prior to beginning research or disclosing proprietary information. These agreements typically restrict the ability of the Company’s collaborators, advisors, employees and consultants to publish data potentially relating to the Company’s trade secrets. The Company’s academic collaborators typically have rights to publish data, provided that the Company is notified in advance and may delay publication for a specified time in order to secure its intellectual property rights arising from the collaboration. In other cases, publication rights are controlled exclusively by the Company, although in some cases it may share these rights with other parties. The Company also conducts joint research and development programs which may require it to share trade secrets under the terms of research and development collaboration or similar agreements. Despite the Company’s efforts to protect its trade secrets, its competitors may discover its trade secrets, either through breach of these agreements, independent development or publication of information including its trade secrets in cases where the Company does not have proprietary or otherwise protected rights at the time of publication. A competitor’s discovery of the Company’s trade secrets may impair its competitive position and could have a material adverse effect on its business and financial condition.

Product liability claims are an inherent risk of the Company’s business, and if the Company’s clinical trial and product liability insurance prove inadequate, product liability claims may harm its business.

Human therapeutic products involve an inherent risk of product liability claims and associated adverse publicity. There can be no assurance that the Company will be able to obtain or maintain product liability insurance on acceptable terms or with adequate coverage against potential liabilities. Such insurance is expensive, difficult to obtain and may not be available in the future on acceptable terms, or at all. An inability to obtain sufficient insurance coverage on reasonable terms or to otherwise protect against potential product liability claims could have a material adverse effect on the Company’s business by preventing or inhibiting the commercialization of its products, licensed and owned, if a product is withdrawn or a product liability claim is brought against the Company.

Intellectual property rights do not necessarily address all potential threats to our business.

The degree of future protection afforded by our intellectual property rights is uncertain because intellectual property rights have limitations and may not adequately protect our business. The following examples are illustrative:

| ● |

others may be able to make compounds or formulations that are similar to our product candidates but that are not covered by the claims of any patents, should they issue, that we own or control; |

| ● |

we might not have been the first to make the inventions covered by the issued patents or pending patent applications that we own or control; |

| ● |

we might not have been the first to file patent applications covering certain of our inventions; |

| ● |

others may independently develop similar or alternative technologies or duplicate any of our technologies without infringing our intellectual property rights; |

| ● |

it is possible that our pending patent applications will not lead to issued patents; |

| ● |

issued patents that we own or control may not provide us with any competitive advantages, or may be held invalid or unenforceable as a result of legal challenges; |

| ● |

our competitors might conduct research and development activities in the United States and other countries that provide a safe harbor from patent infringement claims for certain research and development activities, as well as in countries where we do not have patent rights and then use the information learned from such activities to develop competitive drugs for sale in our major commercial markets; |

| ● |

we may not develop additional proprietary technologies that are patentable; and |

| ● |

the patents of others may have an adverse effect on our business. |

Should any of these events occur, they could have a material adverse effect on our business, financial condition, results of operations and prospects.

Risks Related to our Common Shares

Our Common Share price has been volatile in recent years and may continue to be volatile.