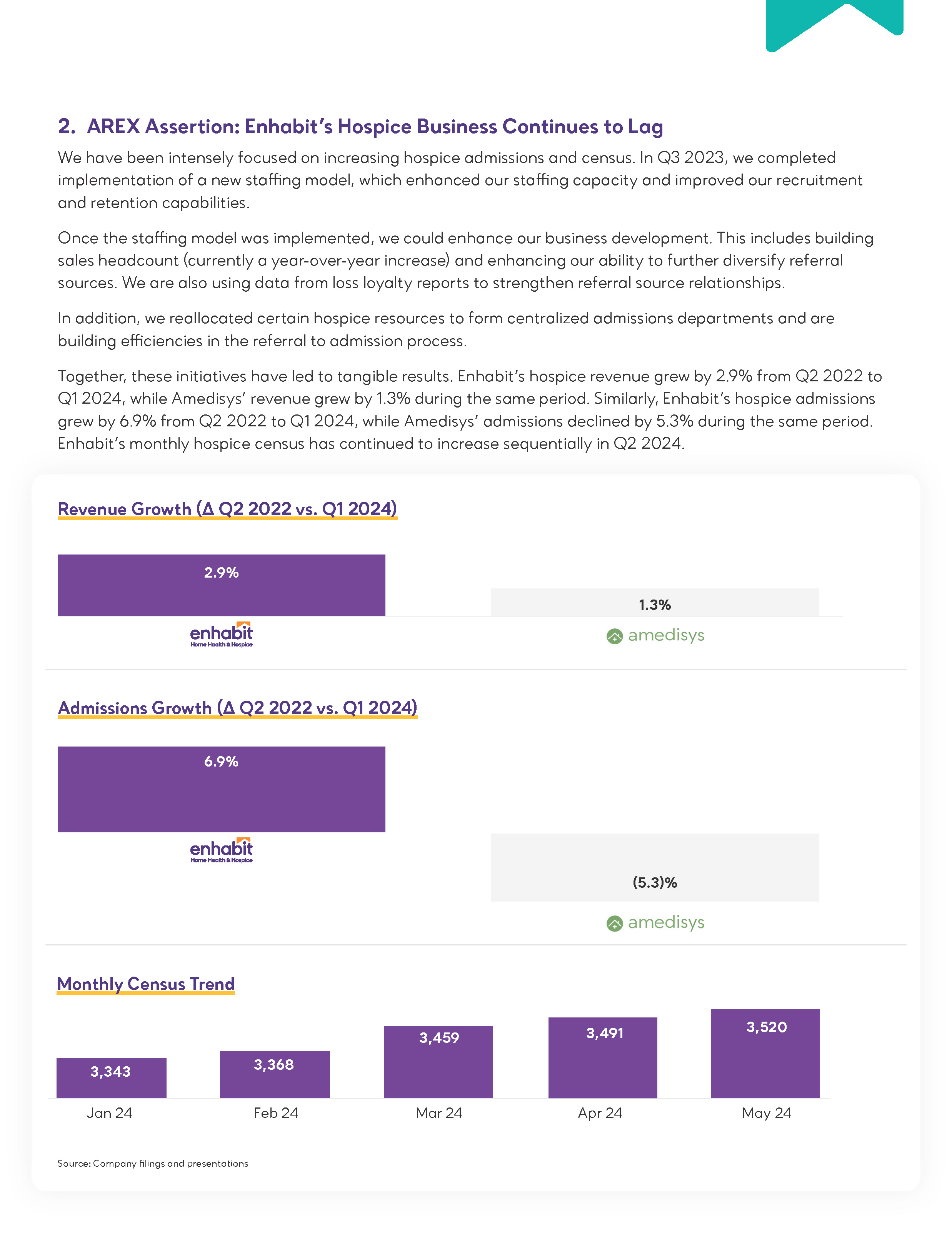

/M][I8CM=2>3?(6+"&;=@,7 #;'XW!T7YV+;PQ?>GK87'NEI+56^:_K_AC

M\SXCX*IYC>I0M3JN5Y7OR2O:]TKV?6Z6KOS)M\R^/KO]EOQ9;R.BV2R*K$!U

MN( K@' 90\BM@]1N56QU4'BO:684WU_!_P"1^45.",?%M*FFDVKJI3L_-"UEB>"?BYX@^'&T:1J5W9QK,)O*BF=86D&WYGASY4F0

MJA@ZL'4!6!7BN:KAH5?BBGI:[2O;UW1+BF?J3^SG_P %"X=>:+2_& 2"X=XX

MXM0C4) PV8+70+8B8N!F2,>3^\^9((XR[?+8W)G'WJ>JUO'K\N_H]=.K9SSI

M=C]2:^6.<* "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M"@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H

M * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "

M@ H * "@#YF_:.\37N@I9):3R0"0S%S&Q0DH$"Y9<-@;FXS@G!() Q^<<98V

MKAU35.4H\SFWRMQ;MRVU5G]IZ;=]D?H7".#IXAU'4BIS5]@?)A0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0 4 % !0 4 % !0!^'/_ 4.^-?_ FVNIX>LY-UEI6?.VME9+QQ

M\^=LC(WDKB(;E62*5KE#P:^YR;"^SASO>6W^'[NN_9JQUTHV5S\[Z^B-PH *

M "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

MH * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M"@ H * "@ H * "@ H * /W^_87^.JW^?;6RV.*I&S/MBO$,@H *

M"@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H

M * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "

M@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H ^2OVI/^

M8?\ ]O/_ +2K\JXY_P"77_<3_P!QGZ?P5_R]_P"X?_N0^2:_*S]."@ H * "

M@#VSX<_!.]\9E9[@&VL\J2S B212-V8@1@@C WGY?FR-^TK7V63\,U<=:<[P

MIW6K34FFK^ZFO3WGIK="O&'OSL]$TXIIV]YI^NBUTL[73/JJ3

MX+:)+9+9&V&$&!,.)]V"-YD !8Y).ULQYP-FU0!^GRX:PKI*ER+1?'M.]GJY

M+?>]G[NVEDD?FJXBQ*J.IS[OX=X6NM%%[;6NO>WUNVSY$^(?P>OO 69O]?9C

M;^_48P6XPZ9)7G@-RIRHW!FVC\HS?AVKEWO?'3T]]*VKZ-7;6O75:K6[L?J.

M4\04LP]WX9Z^XW?1=G9)Z=-'H]+*YY)7RI].% !0!]Q_LS_\@>;_ *^W_P#1

M<5?M7!7^[R_Z^R_](IGX[QC_ +Q'_KU'_P!+F?1%??GP@4 % !0 4 % !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 ?RE^+_$TWC74KO5+

MA46:]N)KB14!"!YG:1@H8L0H+' ))QC))YK]7ITU3BHK9)+[E8]%*QSM:#"@

M H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

MH * "@ H * "@ H * "@ H _07_@FQJ$-GXRN$ED1'FTN=(E9@#(XFMY"J G

M+,$1W(&3M1FQA21\]GB;I+RDK_AA7KQP\7.;M&*NV_P"ON6[>

MB/L'X<_L^P:6%N=6 FF(4BW_ .6<; Y^8@XD. 1_J_O#$@PP_6LGX1C2M/$

M6E*R?)]F+O?5I^]TT^'=>\K,_*\WXJE5O"A[L;M<_P!IJUM+KW>NOQ;/W=4?

M3-?HY^>A0!#<6Z7:-'(H='!5E8 A@1@@@\$$<$'@BHG!3332:::::NFGT*A-

MP::=FG=-:--=3YA^(W[/27Y:ZT?$W8@1GC.(CCY22/NL=GS<-&J@'\U

MSCA!5+SP]DVVW!NT=OLZ::]'IKHXI6/T7*.*W3M#$:I))32O+?[6NNG5:Z;2

M;N?(E_I\VER&&XC>*5<;D=2K#(R,@@$9!!'L7_ %]E_P"D

M4S\=XQ_WB/\ UZC_ .ES/HBOOSX0* "@ H * "@ H * "@ H * "@ H * "@

M H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

MH * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M"@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H

M * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "

M@ H * "@ H * "@ H * "@ H * /Y*:_6ST@H * "@ H * "@ H * "@ H *

M "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

MH * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M"@#ZU_86_P"2AZ1_V^?^D5Q7D9M_!E_V[_Z4C.IL?T0U^=G"% !0 4 % !0

M4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 9&OZ[;

M^%[.XO[Q_+MK6&2:9]K-MCB4N[;5!8X4$X4$GH 35P@YM);MI+U8TKGP-_P\

MP\(?\^6K_P#?BV_^2J]_^PJG>/WR_P#D3;V+/PTQ+N"Y

M@A\XI'%Y=/"I.5FF[:-[_-(B4'$^GZ

M\LS"@ H * "@ H * "@ H * "@ H * "@ H * /ASQ[_ ,% ?"?@#5+O298-

M1GELYFAEDAAB\OS$.V15,L\;G:P*$E0"5)4LA5C[E')ZE6*DG%75]6[V^29L

MJ38> O\ @H#X3\?ZI::3%!J,$MY,L,4DT,7E^8YVQJQBGD<;F(0$*0"P+%4#

M,"MD]2E%R;B[*^C=[?-('2:/N.O#,3Y*_:D_YA__ &\_^TJ_*N.?^77_ '$_

M]QGZ?P5_R]_[A_\ N0^2:_*S]."@#U7X=?"6]\?ONYM[4 DW#(2&.2 (QE=Y

MR"&P0% .3G:K?49/P_5S)WUA"WQN+:>ZLEIS:K76RZN]D_FLVSVGEZM\4[_

MFDUL[O>VCTTN^BM=K[I\(>!['P-"8;*/;NV^8Y.YW*C +$_B=HPH)8A1DU^V

M9=E=++X\M)6O:[>K;2M=O]%9)MV2N?C>/S*KCYR6B2;OHOU=V[*[=C

MK:]4\L\P^*WQCT7X+V+W^L7*1 ([10!E,]P5V@I!$2#(V70$C"IN#.R)EAU8

M?#2Q#M%>KZ+U?]>148\Q\??\/,/"'_/EJ_\ WXMO_DJO8_L*IWC]\O\ Y$U]

MBS[7^'GQ*TCXKV(U+1;I+JU+LF]0RE73[RNCA71N0P#JI*LK@%64GQ*U"5!\

MLE9_UV,6K'R[CQ(-NV9,"50"3@,0SEV;5K^&9S&EO)#;CP5I?DW8VS23/*R?*=F0J ;E9@V0@;(QC=C&1S^K\-9=/ 4.6II*4Y

M2:T=MHI73:>D;_.W0_+N(LPACJ_-#6,8QBGJK[RO9I-:RM\K]3UNOJCY@* "

M@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H

M* "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

M H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

MH * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M"@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * /Y*:

M_6ST@H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

M H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M "@ H * "@ H * "@ H * "@ H * "@#ZU_86_Y*'I'_ &^?^D5Q7D9M_!E_

MV[_Z4C.IL?T0U^=G"% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M4 % !0 4 % !0 4 % !0 4 >2?'[_D4->_[!&H?^DTE=>#_B0_QQ_P#2D5'=

M>I_,)7Z@>@?HA_P3/_Y&^]_[!$__ *4VM?.Y[_#7^-?^DR,*VWS/W&KX8Y H

M * "@ H * "@ H * "@ H * "@ H * "@#^83X_?\C?KW_87U#_TIDK]0P?\

M.'^"/_I*/0CLO0/@#_R-^@_]A?3_ /TICHQG\.?^"7_I+"6S]#^GNOR\\\^2

MOVI/^8?_ -O/_M*ORKCG_EU_W$_]QGZ?P5_R]_[A_P#N0^5;#3YM4D$-O&\L

MK9VHBEF.!DX !)P 2?89K\PI4I5GRP3DWLDFWM?9'Z35JQI+FDU%+=MI+MNS

MZ[^'/[/26!6ZUC$DBE62W4@QCC.)3CYB"?NJ=GR\M(K$#]7R?A!4[3Q%FTTU

M!.\=OM::Z]%IIJY)V/R[-^*W4O##Z)IIS:M+?[.NFG5ZZ[1:N?3UO;I:(L<:

MA$0!550 % & !P !P . *_2H04$DDDDDDDK))=#\ZG-S;;=VW=MZMM]2:K)

M"@#^=/\ ;2^(;?$3QOJ+9?R;!_L$*NJ*4%L2LH&S.Y3.9G1F)8JX!V@!%_1L

MKH^RI+O+WG\]OPL=U-61\JUZIH?>'?&T&GPM_HVIPSQ7$9+;3Y,

M,D\;A0P7S%:,JK,&VQR2J "^1X>+37S:7W:_@C&JKH_?.O@#C"@#

MR3XO_'#0O@;9K>:U<>5YN\00HI>:=D7<5C0?@I=RD2,Z!Y$WKGKPV$GB7:*V

MW>R7]??Y%1BY!\%OC3I?QXTO^UM)\Y8EF>&2.9 DD\6PTBTFO+EL'9$I;:I94WNWW8XPS*&D327G_6

MK\A-V/TS^'G_ 3&F9A)XCU1%0.P:"P4L639\C"XG50C;S\R^1("J\."^4^9

MK9ZOL1^:GGLT_>BFO*Z_/F$JS/@7X\_L@>(_@0LEY.J7FE*X47L!X4.[+

M&)HC\\3'"[C\\*M(D8F=V /T&$S*&)T6DNS_ $?7\^MC:-12/E6O5- H * "

M@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * /K7]A;_DH>D?

M]OG_ *17%>1FW\&7_;O_ *4C.IL?T0U^=G"% !0 4 % !0 4 % !0 4 % !0

M 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 >2?'[_D4->_[!&H?^DT

ME=>#_B0_QQ_]*14=UZG\PE?J!Z!^B'_!,_\ Y&^]_P"P1/\ ^E-K7SN>_P -

M?XU_Z3(PK;?,_<:OACD"@ H * "@ H * "@ H * "@ H * "@ H * /YA/C]

M_P C?KW_ &%]0_\ 2F2OU#!_PX?X(_\ I*/0CLO0/@#_ ,C?H/\ V%]/_P#2

MF.C&?PY_X)?^DL);/T/Z>Z_+SSSE_%'@S3_&:(E_")1&24.64J2,'#*5;!XR

M,X) )&0,>9CLMI8Y)58J7*[K5IKYQ:?JMGIV1Z."S&K@FW2ERW5GHFG\FFO1

M[[]V1>&? FF^#MQL;=(F;.7Y9\'&1O:G!951P-_9046^NK

M?32\FW;1:7M?6Q>,S.MC?XLG)+IHEUUM%)7U>MK]#K:]4\L* "@ H _"/_@H

M%\&;CP3XEDUV&'&FZKL?S(XE2..Z"[98V*DYDDV&XWL$,IDDQO:.1J^\R?%*

MI#D;UCYZVZ/TUMY67='92E=6/@6O?-C],O\ @GA\!K[5-73Q?=1O%I]HDR6C

MD[3<3NIA8Y$TZKNWBU4J5.& C:5\(C,=HF:*2(>+CLSCAO=6LK;

M=%Z_G;\KW,IU.4_;OX4_!S1?@O8I8:/;)$ B++.54SW!7<0\\H ,C9=R <*F

MXJBHF%'Q&(Q,L0[R?HNB]%_7F6S[)8GZJ>H((R&4@AD=25=2'4E2"?L:=15$I

M1=T]F=*=SG:T&% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M4 ?6O["W_)0](_[?/_2*XKR,V_@R_P"W?_2D9U-C^B&OSLX0H * "@ H * "

M@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H

M* "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@#R3X_?\

MBAKW_8(U#_TFDKKP?\2'^./_ *4BH[KU/YA*_4#T#]$/^"9__(WWO_8(G_\

M2FUKYW/?X:_QK_TF1A6V^9^XU?#'(% !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 ?S"?'[_D;]>_["^H?^E,E?J&#_AP_P $?_24>A'9>@? '_D;]!_["^G_

M /I3'1C/X<_\$O\ TEA+9^A_3W7Y>>>% !0 4 % !0 4 5-0T^'5H9+>XC26

M&5&22-U#(Z,"K*RL"&4@D$$$$$@C%--Q=UN@/+_^% ^$/^@#I'_@OMO_ (W7

M5]MUR$A0!^2G_!4G_F7O^XC_ .VE?79!]O\ [=_]N.FC

MU/R4KZTZ3]QO^"9__(H7O_87G_\ 2:UKX;/?XB_P+_TJ1R5M_D?HA7SI@% !

M0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % '\E-

M?K9Z04 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M 4 % !0 4 % !0 4 % '1>$O"5]X[OH-,TR![F\N7V11)U8]223@*H +.[$*

MB@NQ"@D9U*BIIRD[);L3=C]@OV<_^"?5CX86+4_%H2]O&2-UL/\ EA;R!]^)

M65\7+8"JR$>0,RH1.I20?'8W.7/W:>BU][J_\OSVV.:=6^Q^F5?,G.% !0 4

M % !0!X=\:?V=O#_ ,>+?RM6@VW"[!'>PA$NHU1F(1961LQGWW=_/]"XS<3\+?VA?V7=:_9XF1KPI0AMA(+;8

MY5(S%,4&_9EU(W!))/+DV_=X/'QQ2TT:W3_3NOZ:5SKC/F/FRO2- H * "@

MH * "@ H * "@ H * "@ H * "@ H * "@ H * /K7]A;_DH>D?]OG_I%<5Y

M&;?P9?\ ;O\ Z4C.IL?T0U^=G"% !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0!\P?'S

M]K+P_P# 1#%)U

M6B_F=[;VT[O^FT:1@Y'Y;>.?^"A_C/Q+-NTY[;2X5>0JD,*3.R,1L65[@2!F

M0#&Z-(0Q+$IC:%^II9+2@O>O)Z;MK[K6_&YT*DD?-G_"_O%__0>U?_P87/\

M\-_"4S3V^N7SNR%"+B4W:8)!R([GS4#

M<##A0P&0#AF!RJ9?2FK.*^2Y?_2;"<$S[N^"G_!23_5V7B^V_NI_:%JO_7-=

MT]O_ -_))'@/HD=K7A8K).M-_P#;K^>S^Y*_S9C*EV/U)\)>+;'QW8P:GIDZ

M7-G[2ZM]R)P21Z?\ 'S_@HI;^%;@V'A.*&]EAF99[

MNX5FM655'%OY4B/)\Q(,I*IA,H)DD61>7!Y*YJ]2ZNM$M_G=.WI]]K6)C2ON

M?G)XF_:F\;^+9EGN-%=,N2R&5 5:/R,1DL)KW+Q=

MM-;J_G>[_'Y&4J2Z'[!?"SXIZ7\8]+BU?2)?,MY/E96P)(9 6BE4$[9%R,C

M)# JZLT;([?'XC#RH2Y9;_@UW7E_6YS2C8]$KF)/)/C]_P BAKW_ &"-0_\

M2:2NO!_Q(?XX_P#I2*CNO4_F$K]0/0/T%_X)OZA#I/BK4+BXD2*&+1;EY)'8

M*B(MQ:LS,S$!5 !))( ))Q7SV=IRII+=S7Y2,:NWS/1/CG_ ,%&[Z^FFL?"

M,:6]NCE5U&9/,EE"E"'BAD79$IPZXF65FC96VP2 J.?"9(DKU-7_ "K1==VM

M_E;7NB8TNY\3Z[^TSXT\17#W4VNZBLC[3^T+I?^NB[H+?_OW)&\Y]4DM:^JPN2=:C

M_P"W5\MW]Z=ODSHC2[GPCXF_:F\;^+9EGN-+_\ H/:O_P"#"Y_^.5K]3I_R

M1_\ 8_Y#Y5V/I_X<_\ !1/Q;X7N"VL>3J]LV,QND=M(N%;'ER01A1EBI?S(

MY77R6G->[>+^;7W-_DT9NDF??/C7]KRS\4> =5\2^%9=E[9^5$T

M-S&OG6S3SI"KO$&9#E6:2%LR1,R[6#%)8A\_2RUPK1A4V=W=;.R;W_!]?P9B

MH6=F?F#_ ,-T_$/_ *"__DG9?_(]?4?V31_E_P#)I?YG1[-'W?\ L,?M3:_\

M8-2O-%UYTNG2V:[BN@D<3J$>*)HF2)$1E/F!U;"LI#@EPR^7X.;9?"A%2AIK

M9K5]&[ZOR_KKC4@EL?IE7S)SG\PGQ^_Y&_7O^POJ'_I3)7ZA@_X

MA'9>@? '_D;]!_["^G_^E,=&,_AS_P $O_26$MGZ'[&_M&?MT:1\(6ETW253

M4M7C>2*5-S+!:NJ<&5PN)6#D*T,3 C;*CRPR* WQN"RF5?WI>['1KN_\O5^5

MDSEA3N?F#\0_VTO&_P 1&.[47L(=ZNL-AFV"%4V8$JDW#*+_\ H/:O_P"#"Y_^.5U?4Z?\D?\ P&/^

M17*NQZUX%_;@\<^!O)3^T/MUO#O_ '-[&LV_?N/[R;Y;EMI;\DM7:S7RN]/\ @WL<\J;1]QUX

M9B% 'PC^W1^T3J_P+L;"WT79%=:B\Q^U,JR&%+?RBRI&ZLA:3S0"SA@JA@$+

M,KQ^]E."CB6W+:-M-KWOU7H;4XU]6]K]V^YUQBH['DE=91[C\,_VD?%7P>LWL-#O_LMM),TSI]GMYYZ)_PW3\0_P#H+_\ DG9?

M_(]/HJC4E&.RM;YI/]3DFK,]]KSR H * "@ H * "@ H

M* "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

M H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

MH * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M"@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H

M * "@ H * "@ H * "@ H * "@ H * "@ H * /Y*:_6ST@H * "@ H * "@

M H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H ^

MG_@'^R;X@^/;B6W3['IHVEKZX1Q&Z^8486X _?R+M)=Y/3LKV^[OY_HXC>*:)V22-U*NCJ2K*RL 58$$$$ @@@C-?6)J2NMF

M=)4I@% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 ?6O["W_)0](_[

M?/\ TBN*\C-OX,O^W?\ TI&=38_HAK\[.$* "@ H * "@ H * "@ H * "@

MH * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M/AS]LC]J_P#X4/;KI6F#=K=Y#YD;LF8[:%F9!,=PVR2%E811\J"I>0;0L]O)=W]W=;4X4=593D, 017FO-:*=N;\)/\D1[1')>.?V7/&?PYA^T:CI%PL.R1VDAV7*

M1I$ SM*UNTHB4 YS(4! 8@D*V-:6/I57:,E?3>ZW[7M?Y#4TSP*O0+/HC]G;

M]HG5/@/JD$L4\S:6TP-[9 EXY(W*"5TB+J@N J@QR J"1XW*.A9&*DI(A

MCD4D$':Z,R..C*Q4@@D4FD]_ZMJ :?I\VK31V]O&\LTKJD<:*6=W8A5554$L

MQ) ))( &:&U%7>R ^G]/\ V)/B#J4,4

M=593D, 017EO-:*=N;\)/\D9^T1YA\3/@1XE^#VPZYI\UK')M"2Y66$LV_">

M=$SQ"3",?++;]HW;=I!/50Q<*_P-/RV?W.SMKN4I)['DE=91[[^SG\>;[X!:

MU%?02.;&5XTU"W W": -\Q"%D'G("S0ON7:Q*D^6\B-Y^-PBQ,;/=7Y7V?\

MEW_SL1./,?TG:?J$.K0QW%O(DL,J*\Z. \O^/W_(H:]_V"-0_P#2:2NK!_Q(?XX_^E(J.Z]3^82OU ] MVVH36:R

M)%(Z),@2558@2('60*X!PRAT1P#D;D5L94$)I/Y;?E^H&OX9\(:EXUF:WTNT

MN+V94+M';PO,X0$*6*QJQ"@LH)QC) SDBHJ5(TU>327FTOS$W8^D_P#AA;XA

M_P#0(_\ )RR_^2*\S^UJ/\W_ )++_(CVB/#OB-\)==^$EP+77+*:SD;.PN T

M7Y_*:)U>.1&*NCJ0RLK*058$

M @@@@@$'-=32DK/9E%2F!Z?\//@MXC^*[!=%TZXND+LGG*FV!71-[*\[[84;

M:00'=2=R@ EE!Y:V*A0^*27EU[;+4ER2/4-=_8Q\?>';=[J;1IFC3;D0RP7$

MAW,%&V*"625N2,[5.T98X4$CEAF=&;LI+YII?>TD2JB9\UZAI\VDS26]Q&\4

MT3LDD;J5='4E65E8 JP((((!!!!&:]--25ULS0J4P/V-_8-_:IF\4M_PBNO7

M%Q\:PM<:7IE]>PJY1I+>UFF0.

M&*EHT8!@&4D9S@@XP16%2O"F[2DD_-I?F)M(Z+_A0/B__H ZO_X+[G_XW6?U

MRG_/'_P*/^8N9=S]Y_V0?"5]X'\#Z58:E ]M=(D[O"_#H)KB65 PZJQ1U)1L

M,A)5@K J/@LRJ*I5DXNZTU]$E^AQU'=GTI7F&84 % !0 4 % !0 4 % !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M% !0 4 % 'B>N?'_ $31GV(\ER06#&%,A2IQ]YRBL#SM*%@0,YP1GXW%<6X6

M@[)RGJT^2-TK>-W

M_P!\1_\ QVC_ %UP_P#+4_\ 8?_ "P/]3L1_-3_ / I_P#R ?\ #3&C_P#/

M&[_[XC_^.T?ZZX?^6I_X##_Y8'^IV(_FI_\ @4__ ) /^&F-'_YXW?\ WQ'_

M /':/]=-W_P!\1_\ QVC_ %UP_P#+4_\ 8?_ "P/]3L1

M_-3_ / I_P#R ?\ #3&C_P#/&[_[XC_^.T?ZZX?^6I_X##_Y8'^IV(_FI_\

M@4__ ) /^&F-'_YXW?\ WQ'_ /':/]=-W_P!\1_\ QVC_

M %UP_P#+4_\ 8?_ "P/]3L1_-3_ / I_P#R ?\ #3&C_P#/&[_[XC_^.T?Z

MZX?^6I_X##_Y8'^IV(_FI_\ @4__ ) /^&F-'_YXW?\ WQ'_ /':/]=-W_P!\1_\ QVC_ %UP_P#+4_\ 8?_ "P/]3L1_-3_ / I_P#R

M ?\ #3&C_P#/&[_[XC_^.T?ZZX?^6I_X##_Y8'^IV(_FI_\ @4__ ) /^&F-

M'_YXW?\ WQ'_ /':/]=-W_P!\1_\ QVC_ %UP_P#+4_\

M 8?_ "P/]3L1_-3_ / I_P#R ?\ #3&C_P#/&[_[XC_^.T?ZZX?^6I_X##_Y

M8'^IV(_FI_\ @4__ ) /^&F-'_YXW?\ WQ'_ /':/]=7*^:%^LTDKW2M>,I

M6WW=DENSEQ/"F(HQYERSMTBVW:S>THQOMLKM]$>UV]PEVBR1L'1P&5E((8$9

M!!'!!'((X(K[*$U-)IIII--.Z:?4^0G!P;35FG9IZ--=":K)"@ H * "@ H

M* "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

M H * "@ H * "@ H * "@ H * /Y*:_6ST@H * "@ H * "@ H * "@ H *

M"@ H * "@ H * "@ H * "@ H * "@ H * "@ H * +>GZ?-JTT=O;QO+-*Z

MI'&BEG=V(5555!+,20 "22 !FDVHJ[V0'ZP?L\_\$[/N:AXT_Z:@:7&_P!%

M1YKB&3_>81Q'_GFS2_ZR&OD\;G7V:7E[W^2:_%^>G4YIU>Q^L&GZ?#I,,=O;

MQI%#$BI'&BA41% 5555 "J !BODFW)W>[.8MT@"@ H * "@ H * "

M@ H * "@#Y@^/G[)OA_X]H9;A/L>I#<5OK=$$CMY811< C]_&NU"%8JZA-B2

MQJS[O4P>8SPVBU7\KO;>^G9_TTS2,W$_"[XV? ;6O@%?)8ZO&A$J;X+B$LT$

MP&-X1V5#N0D*Z,JLN5;&QXW;[K"XN.)5X]-T]T=<9/Y=M:PR3

M3/M9ML<2EW;:H+'"@G"@D] ":N$'-I+=M)>K&E<_F$^+7Q&N/BWKM[KET-LE

MY,7"94^7&H"11[E5 WEQJD>_:"^W@J$%!=%^/5]>IWQ5E8J?#7X

M>7WQ7U>UT730ANKIRJ;VV(H52[NSB_ *QC@L8DEOBA%QJ#QJ)YBVTN W)CARB[(58JNT$EY-\C?G>+Q

MLL2[O;I&^B_X/G^FAPRGS'OM>>0% 'Y;?MO?L@0ZQ#=>+M!5(KF)'GU*VR%2

M9%!:2YCS@+, "TJ\"8 N/W^X3_4Y5F3BU3GL](OMY>G;MZ;=%.IT9^.5?9'4

M?KM_P32^+DUXM[X4N"[I"AO;1CDB-"Z1SQY+X52[QR1HB ;GG=FRR@_(9YAD

MK5%U]U_FGMY-/Y'-6CU/U@KY,YC^2FOUL](* /Z(/V3?V9K/X"Z6EQ-'NUN\

MA0WLS[2T6X!C:QE691&C8#LK'SG7S"=HB2/\[S''/$RLOA3T7?S]?RV[WXIS

MYCZVKR#(J:AI\.K0R6]Q&DL,J,DD;J&1T8%65E8$,I!((((()!&*:;B[K= ?

MSI_M>?!:W^!GBB6PL>+&XACNK5"[.T<$/#,WC74K32[=D6:]N(

M;>-G)"!YG6-2Q4,0H+#) )QG )XK.I45.+D]DF_N5Q-V/Z0_@'\ ]+_9^TL6

M%@/,N)-K7=VR@27$@!Y/)VQKDB*($B,$G+2-)(_YMC,9+%2N]NBZ)?Y]W^ED

M<,I"FNJ_'JNG4[XNZN>=UTE']3OPP\33>-=!TS5+A46:]L;6

MXD5 0@>:%)&"ABQ"@L< DG&,DGFORNO35.I^+=?:G4?9G[&_P"S-_POG5&N=2CF&B67,SK\JSS J5M0^X,,J=\K

M1AF2,!WDN_P#E?\;,RJ3Y3]Z/"7A*Q\"6,&F:9 EM

M9VR;(HDZ*.I))R68DEG=B6=B78EB2?@JE1U&Y2=V]V<;=SHJS$>8?%;X.:+\

M:+%[#6+9)04=8IPJB>W+;27@E()C;*(2!E7VA75TRIZL/B98=WB_5='ZK^O(

MJ,N4_G>^//P3OO@%K4FD7SI*"@FMYTX$T#,RHY3),;91E=&SM93AG39(WZ)A

M,4L3'F7HUV9VQES'C-=I9^B'_!,__D;[W_L$3_\ I3:U\[GO\-?XU_Z3(PK;

M?,_<:OACD/YA/C]_R-^O?]A?4/\ TIDK]0P?\.'^"/\ Z2CT([+T/)*ZRC]'

M/V*OV0+3XNPOK_B!7?3%=X;>U!DB-PZC#2M(NP^2A)5?*;+S(X9E6)DE^;S3

M,G0?)#XMV]';RMW]>GKIA4J6T1^U^GZ?#I,,=O;QI%#$BI'&BA41% 5555 "

MJ !BOB6W)W>[.0MT@/ OCS^SGHOQ]L9(+Z)(KX(!;Z@D:F>$KN* M

MP9(?#C5+O2+

M]=MS9S-$^ P5MI^5TWJK&-UP\;%1OC96Q@U^BT:JJQ4ELU?^O/N=R=S)T#7;

MCPO>6]_9OY=S:S1S0OM5MLD3!T;:P*G# '# @]""*N<%--/9II^C!JY_3W\)

M?B-;_%O0K+7+4;8[R$.4RQ\N124ECW,J%O+D5X]^T!]NY?E(K\PQ%!T)N#Z/

M\.CZ]#@DK.Q^;'_!4G_F7O\ N(_^VE?2Y!]O_MW_ -N-Z/4_)2OK3I/W&_X)

MG_\ (H7O_87G_P#2:UKX;/?XB_P+_P!*D_P"X

MC_[:5]=D'V_^W?\ VXZ:/4_)2OK3I/W&_P""9_\ R*%[_P!A>?\ ])K6OAL]

M_B+_ +_ -*D,=K 9X. P^[\[,/TK@_-G"?U>5VI7<-K1:3D_D[7WT?3WFS\ZXMRM3A]8C9.

M-E+O)-J*^:O\UUT2/LROU\_)PH * "@ H * "@ H * "@ H * "@ H * "@

MH * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M"@#^2FOUL](* "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H

M* "@ H * "@ H * /RM?[NWG^I$IJ)^XWP#_9-\/_ 1!+;I]LU([2U]

M<(AD1O+*,+< ?N(VW.2JEG8/L>6153;\-C,QGB='HOY5>V]]>[_I)')*;D?3

M]>69A0 4 % !0 4 % !0 4 % !0 4 % !0!SOBWPE8^.[&?3-3@2YL[E-DL3

M]&'4$$8*L" R.I#(P#J0P!&E.HZ;4HNS6S&G8_'W]HS_ ()]7WAAI=3\)![V

MS9Y':P_Y;V\83?B)F?-RN0RJ@'GC,2 3L7D'V."SE3]VIH]/>Z/_ "_+?8Z8

M5;[GYFU],= 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 ?6O["W_)0](_

M[?/_ $BN*\C-OX,O^W?_ $I&=38_HAK\[.$* "@ H * "@ H * "@ H * "@

M H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H ^

M5?VV]0FTSX?:P\$CQN4MD+(Q4E)+J&.1200=KHS(XZ,K%2""17JY4DZT;^?X

M1;-*>Y_.G7Z,=Q[C\"OCW?\ [/MY/?Z9;6D]S/#Y)>Y69MD>X.RHL7

M_85/O+[X_P#R)G[%!_P\P\7_ //EI'_?BY_^2J/["I]Y??'_ .1#V*#_ (>8

M>+_^?+2/^_%S_P#)5']A4^\OOC_\B'L45-0_X*0>*M6ADM[C3]%EAE1DDC>V

MN&1T8%65E:Z(92"000002",4UDE.+NG.Z\U_\B/V2\S\^J^A-CZ(_9,\4_\

M"'^.=$N?+\W?=K;;=VW'VM6M=^<-]SS=^W'S;=N5SN'G9C3]I2DO*_\ X#[W

MZ$35T?TG5^:G ?R4U^MGI'OO[+/AF;Q;XWT.W@9%=+Z*X)?_TFM:^&SW^(

MO\"_]*D_P"P1J'_ *325Y&#_B0_QQ_]*1E'=>I_,)7Z

M@>@?=W_!.KPS#KWC<7$K.'L+&YN(@I #.Q2V(?()*[)W( *G<%.< JW@YU4<

M:5OYI)/\9?H8U7H?O17P1QA0 4 ?A=_P4GT^&S\96[Q1HCS:7 \K*H!D<37$

M89R!EF"(B G)VHJYPH ^ZR-MTGY2=ON3_4[*6Q^?5?0FQ_19^Q)J$VI?#[1W

MGD>1PER@9V+$)'=31QJ"23M1%5$'154* *_.S^S[2VMMV[=YFY3=;\8&W'VC9MRWW-V?FVK]5DU/EI7_F;

M?_MO_MIT4EH?#E>X;'])W[*'@FS\#>"](BLUQ]IM(;R9R%#/-=1K*Y8JJ[MN

MX1H6RPB2-"S;7;W \M_E+ -NF%L. SKU&$\PU]%DE7EJ.-_B6WFM

M?RN;TGJ?AS7W)UGZ(?\ !,__ )&^]_[!$_\ Z4VM?.Y[_#7^-?\ I,C"MM\S

M]QJ^&.0_F$^/W_(WZ]_V%]0_]*9*_4,'_#A_@C_Z2CT([+T/+]/T^;5IH[>W

MC>6:5U2.-%+.[L0JJJJ"68D@ $DD #-=3:BKO9%']3W@+P39_#C2[32+!=M

MM9PK$F0H9MH^9WV*JF1VR\C!1O=F;&37Y76JNK)R>[=_Z\NQYS=SK:Q$% !0

M!^2G_!3SP+_R"->BA_YZV5Q/O_[;6T>PM_U]-N5?9V_U8KZ[(:OQ0OV:7X/]

M/ZN=-%]#\E*^M.D_=S_@G#KMQJ_@N2&=]T=GJ-Q# -JC9&T<,Y7( +?O)I&R

MV3\V,[0H'P>=P4:MUUBF_6[7Y)''56IX=_P5)_YE[_N(_P#MI7?D'V_^W?\

MVXNCU/R4KZTZ3]QO^"9__(H7O_87G_\ 2:UKX;/?XB_P+_TJ1R5M_D?HA7SI

M@?DI_P %2?\ F7O^XC_[:5]=D'V_^W?_ &XZ:/4_)2OK3I/W&_X)G_\ (H7O

M_87G_P#2:UKX;/?XB_P+_P!*DYUF_9V+$74R@DDG"N54<]@ !T X%?S=G$W/$U6

MVW^]FM7?12:2^25EV1_0^404KE/^\4O^OM/

M_P!+1YF:?[O5_P"O53_TAGZ>U_2A_.H4 % !0 4 % !0 4 % !0 4 % !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0!_)37ZV>D% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 ?IE^SG_P3ZOO$[1:GXM#V5FKQNMA_P M[B,IOQ*R

MOFV7)560CSSB5"(&"2'YG&YRH>[3U>OO=%_G^6VYSSJVV/V"\)>$K'P)8P:9

MID"6UG;)LBB3HHZDDG)9B26=V)9V)=B6))^.J5'4;E)W;W9S-W.BK,04 % !

M0 4 % !0 4 % !0 4 % !0 4 % !0 4 ?$_[1G[$^B_&99;_ $]4T[6=DA66

M-52"XE9_,S=(JDLQ)<&9,2C?N<3!$CKV\%FDL/H_>CIZI;:?Y;>FYK"IRGXH

M?%;X.:U\%[Y[#6+9XB'=8IPK&"X"[27@E( D7#H2!ADW!75'RH^VP^)CB%>+

M]5U7JOZ\CKC+F/,*ZB@H * "@ H * "@ H * "@ H * "@ H * /K7]A;_DH

M>D?]OG_I%<5Y&;?P9?\ ;O\ Z4C.IL?T0U^=G"% !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M4 ?)/[=/_)/-7_[<_P#TMMZ]?*?XT?\ M[_TEFM/<_G?K]$.TZWPMX UCQSY

MG]E6%W?>3M\W[-;R3;-^=N_RU;;NVMMSC.TXZ&L:E:-/XFE?NTOS$W8Z[_A0

M/B__ * .K_\ @ON?_C=9?7*?\\?_ */^8N9=P_X4#XO_P"@#J__ (+[G_XW

M1]/_@4?\PYE

MW#_A0/B__H ZO_X+[G_XW1]+5DTW=JW0F4E8_HAK\[.$_DIK];

M/2/K7]A;_DH>D?\ ;Y_Z17%>1FW\&7_;O_I2,ZFQ_1#7YV<(4 % 'Y*?\%2?

M^9>_[B/_ +:5]=D'V_\ MW_VXZ:/4_)2OK3I/W&_X)G_ /(H7O\ V%Y__2:U

MKX;/?XB_P+_TJ1R5M_D?6OQ^_P"10U[_ +!&H?\ I-)7D8/^)#_''_TI&4=U

MZG\PE?J!Z!^B'_!,_P#Y&^]_[!$__I3:U\[GO\-?XU_Z3(PK;?,_<:OACD"@

M H _#G_@IA_R-]E_V"(/_2FZK[G(OX;_ ,;_ /28G71V^9^=]?1&Y_1!^PM_

MR3S2/^WS_P!+;BOSO-OXTO\ MW_TE'%4W/R4_;I_Y*'J_P#VY_\ I%;U];E/

M\&/_ &]_Z4SII['R57KFA_53X \4_P#"_PU_C7_ *3(PK;?,_<:OACD/YA/

MC]_R-^O?]A?4/_2F2OU#!_PX?X(_^DH]".R]#G?AAXFA\%:]IFJ7"NT-E?6M

MQ(J %RD,R2,%#%06(4X!(&<9('-:5Z;J0E%;N+7WJPVKH_J=K\K/."@ H *

M/S8_X*;:[;V_AO3;!GQBM3\4*^V.L_<;_@F?_R*%[_V%Y__ $FM:^&SW^(O\"_]*D?\ ])K6OAL]_B+_ +_ -*D_[B/_ +:5

M]=D'V_\ MW_VXZ:/4_)2OK3I/W&_X)G_ /(H7O\ V%Y__2:UKX;/?XB_P+_T

MJ1R5M_D?HA7SI@% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 ?F%X_P#^0Q?_

M /7WC7E0?-%V?\ 7<:=C\4/

MVC/V%]7^$*RZEI+/J6D1I)+*^U5GM45^!*@;,JA"&::)0!ME=XH8U!;[;!9M

M&O[LO=EHEV?^7H_*S9UPJ7/A&O>-@H * "@ H * "@ H * "@ H * "@ H ^

MM?V%O^2AZ1_V^?\ I%<5Y&;?P9?]N_\ I2,ZFQ_1#7YV<(4 % !0 4 % !0

M4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0!XS^T-\/&^*OA35-(B#M-/;%H$1D0O/"1- A9_E"M)&BN3CY2?F

M4_,.W!5O8U(RZ)Z^CT>WDRX.S/YCZ_3CO/M?]A?XYP_!_P 1M:ZA,D.F:HBP

MSR.0J12Q[FMY6;8Q"@L\1^:.-1,99&VQ#'B9MA'7A=:RCJO3JM_GWTLMS*I&

MZ/W_ *_/SB"@ H X;XE?$.Q^%&D76M:D7%K:H&?8N]V+,$1%7@;G=E0%BJ@L

M"S*H+#>A1=>2C'=_\.-*Y^?7@G_@IOI>KWBPZOI4UA;/@?:(K@76QBRC+Q^5

M"WEA2S,R>8_R@+$Y;CZ&KD4HJ\9)OLUR_J]?N]3=T3])]"U^S\46Z7EA<0W5

MM)NV30R++&VUBK;70E3A@5.#P01U%?-3@X.S33[-69@U8UZ@1_)37ZV>D?6O

M["W_ "4/2/\ M\_](KBO(S;^#+_MW_TI&=38_HAK\[.$* "@#\E/^"I/_,O?

M]Q'_ -M*^NR#[?\ V[_[<=-'J?DI7UITG[C?\$S_ /D4+W_L+S_^DUK7PV>_

MQ%_@7_I4CDK;_(^M?C]_R*&O?]@C4/\ TFDKR,'_ !(?XX_^E(RCNO4_F$K]

M0/0/T0_X)G_\C?>_]@B?_P!*;6OG<]_AK_&O_29&%;;YG[C5\,<@4 % 'X<_

M\%,/^1OLO^P1!_Z4W5?;?QI?]N_^DHXJFY\4?\ !3GP--!J6EZ\N]H9K9K)\1G9&\+M,FZ3

M)&Z43/M0@'$+L"PSL]O(JJ<90ZIWW[JVWE;\36B^A^6U?4G0?M)_P3P^/-CJ

MFD)X0NI$BU"T>9[1"-HN('8S.%8L0\R.TA9 $_<[&4/LF9?BLZPC4O:+5.U_

M)[?=M\_D5K::I:_GOZ69UTHVU/SCKZ0W/

MT0_X)G_\C?>_]@B?_P!*;6OG<]_AK_&O_29&%;;YG[C5\,

M_P"POJ'_ *4R5^H8/^'#_!'_ -)1Z$=EZ'DE=91_05^QA^T3;_&30H;"ZGW:

MWI\(2Z1RV^6-#LCN0SN[2[EV"=\Y$Y8LJ+)%O_/LSP3P\VTO=D]/)]NEO+R]

M&<52%F?9E>*9!0 4 ?SI_M?_ !Y7X[^(VGLY';2K-!!9!@Z!AUEF,;,0&D?H

MVV-FA2$.BNA _1LMPGU:%G\3U?Z+Y?G>QW4X\J/E6O5-#^C?]C;P3_P@W@;2

M8F6$2W,)O)'B&-_VIC+&7.U2TBPM%&Q.<; @9D537YQF=7VE66^CMKY:/Y7N

MSAJ.[/C/_@J3_P R]_W$?_;2O:R#[?\ V[_[<:T>I^2E?6G2?N-_P3/_ .10

MO?\ L+S_ /I-:U\-GO\ $7^!?^E2.2MO\C]$*^=,#\E/^"I/_,O?]Q'_ -M*

M^NR#[?\ V[_[<=-'J?DI7UITG[7_ /!,G7;>X\-ZE8*^;F#43-(FUOECG@B2

M-MV-IW-!*, DC;D@!ES\3GL&IQ?1QM\TW?\ -')66I^D]?-& 4 % !0 4 %

M!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 % !0!^87C_ /Y#%_\ ]?=Q_P"C&K^:\V_WBK_U]J?^

MEL_HK*_]WI?]>J?_ *0CD:\H],* "@ H * "@ H * "@ H * "@ H * "@ H

M * "@ H * "@ H * "@#V'X=?!J]\?I]HW"WM^RTO9Z-W2[7::/E^2W/.U^5-)+;=

MZVTU2LWWLFF?07_#,^C_ //:[_[[C_\ C5?>_P"I6'_FJ?\ @4/_ )6?#_ZX

MXC^6G_X#/_Y,\?\ 'G[/][X<#3V!-W!D?(%/GJ"3CY5!#@#:"RX)))\M5!(^

M2S7A*KA;SI7J1OLD^=7;Z*_-;2[6O7E25SZK*^*J>)M&K^[E;=MU];

M)Z=.9MV/GRO@C[@* "@ H * "@ H * "@ H * "@ H * "@ H Z[P!_R&+#_

M *^[?_T8M>KE/^\4O^OM/_TM'F9I_N]7_KU4_P#2&?I[7]*'\ZA0 4 % !0

M4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0 4 % !0 4 % !0 4 % '\E-?K9Z04 % !0 4 % !0 4 % !0 4

M% !0 4 % !0 4 % !0 4 % !0 4 % !0!]W?LY_L+ZO\7EBU+5F?3=(D2.6)

M]JM/=(S\B)"V8E* LLTJD'=$Z131L2O@XW-HT/=C[TM4^R_S]%YW:,9U+'[7

M_#SX:Z1\*+$:;HMJEK:AV?8I9BSO]YG=RSNW 4%V8A55 0JJ!\36KRKOFD[O

M^NQR-W.YK 04 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M4 ?G?^T-^P#I?Q"WW_AKR=,U$^4#;X$=BZKE6.R.-FAD*[3NC!1BF#$'D>8?

M18+.)4M)WDM==Y?B]5Z_?I8WA5MN?C-XV\!:I\.+QK#5[2:SN5R=DJE=RAF3

M>C?=DC+*P61"R/@E6(K[.E6C55XM->7]:/R.I.YR5;#"@ H * "@ H * "@

MH * "@ H ^M?V%O^2AZ1_P!OG_I%<5Y&;?P9?]N_^E(SJ;']$-?G9PA0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M4 % !0 4 % !0 4 % !0!^ '[;'[.;?!G6FU"PB?^QM1=I(F$:+%;SNS,]J/

M+P%4 ;X053,1,:[S#(]?H&5XWZQ&S^*/GJUWU_'S]4=M.?,?%%>V:GWU^SM^

MWCJGPCMX-(U:'^T=+APD;!BMU!'N0!49B4ECC4/Y<3A#DJ@GCB14'@8W*(UV

MY1?+)_M%V23\U)6_%I_@8.DSAOB'_P %&_"GAE2ND1W&K3;%9"J&

MV@R7PR/),HE5@H+@K"ZME5W EBF]')*D_BM%?>_PT_$:I-GY;?'S]IG7?V@+

M@_;I/)TZ.9I+6PCQY<65"@LP56FD"Y_>29P7D\M8D"/#DVI7LSB'5GCFMK-@ZB)(]Z><0V!N

MN!M8%%PT,<+^8X8+'\+G5>-2:BEK&Z;TUVT^7YW..J[L_06OGC$_DIK];/2/

MK7]A;_DH>D?]OG_I%<5Y&;?P9?\ ;O\ Z4C.IL?T0U^=G"% !0!^2G_!4G_F

M7O\ N(_^VE?79!]O_MW_ -N.FCU/R4KZTZ3]QO\ @F?_ ,BA>_\ 87G_ /2:

MUKX;/?XB_P "_P#2I')6W^1]:_'[_D4->_[!&H?^DTE>1@_XD/\ ''_TI&4=

MUZG\PE?J!Z!^B'_!,_\ Y&^]_P"P1/\ ^E-K7SN>_P -?XU_Z3(PK;?,_<:O

MACD"@ H _#G_ (*8?\C?9?\ 8(@_]*;JON&FI+;9^E]?GV_P B

M82Y6?S8Z_H5QX7O+BPO$\NYM9I(9DW*VV2)BCKN4E3A@1E20>H)%?I4)J:36

MS2:]&=R=RGI^H3:3-'<6\CQ31.KQR(Q5T=2&5E92"K @$$$$$ @YJFE)6>S&

M?JK\(_\ @I:UG"+?Q79/,Z)A;NR"!Y" @'F02.B!F_>.\D;HN2J+ HRP^4Q.

M1W=Z;MY2^?57^YKYG-*CV/I/5O\ @H9X&TZSBN8I;NYEDV;[6*V831;E+'>9

M3'"=I&QO+EDRQ!7;>C^Z[^]$>R9\4?&_P#X*(ZOXWA:R\.0

MOI,)>57N3(LES+$P*H%^3%LV"78QM)(K[/+F4(3)[>%R6--WF^9Z:6LD_OU^

M>G=&L:5MS\XZ^D-PH _1#_@F?_R-][_V")__ $IM:^=SW^&O\:_])D85MOF?

MN-7PQR'\PGQ^_P"1OU[_ +"^H?\ I3)7ZA@_X25UE'1>

M$O%M]X$OH-3TR=[:\MGWQ2IU4]""#D,I!*NC JZDHP*D@YU*:J)QDKI[H35S

M]8/AS_P4VLWMROB739DN5QB33PKQR99LYCGE1HMJ[!_K)MYW-^[&%/R=?(G?

MW)*W][?[TG?[E\SF='L>X^*?^"AG@;P_Y?V:6[U#?NW?9K9E\O;C&_[4;?.[

M)V[-_P!T[MOR[N"GDU66]H^K_P#D>8E4F?FQ\?/VV_$'QK0V5N/[*TT[@T%O

M*YDF5XPC)<3#9YD?+XC5(T(?#K(R(X^EP>50P^K]Y]VE9:WT6MGY_=8WC343

MXSKVC4^G_P!DWX!O\>_$"6\HQIMGLN+YBLFUXPX MPR%=LDW*J2Z%8UED7QO+S'&?5H76[T6V]M]>B_R74SG+E1_1O7YP<)^2G_!4G_F7O^XC_P"VE?79

M!]O_ +=_]N.FCU/R4KZTZ3]QO^"9_P#R*%[_ -A>?_TFM:^&SW^(O\"_]*D<

ME;?Y'Z(5\Z8'QG^WE\.;CXA>"YWM3^\TR9=0*87YXX8Y$E&YF4+LCD>7^(MY

M?EJI9QCVLHKJE55_M+E^;:M^*M\S6F[,_GUK]!.T[GX>?$K5_A1?#4M%NGM;

MH(R;U"L&1_O*Z.&1UX# .K ,JN &52,*U"-=67HFOU37Y'.Z)^K

M^@:[;^*+.WO[-_,MKJ&.:%]K+NCE4.C;6 894@X8 CH0#7RZ;3]4<[

M5C7J!!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M4 % !0 4 % !0 4 % !0 4 % !0 4 % !0!^87C_ /Y#%_\ ]?=Q_P"C&K^:

M\V_WBK_U]J?^EL_HK*_]WI?]>J?_ *0CD:\H],* "@ H * "@ H * "@ H *

M "@ H * "@ H * "@ H * "@ H T=)TF?79TMK9#)-(<(@ZD_P @ .23@ D

MD $UT8?#RQ$E"";E)V27]?>]DM7H85Z\B/L'X<_L^P:

M6%N=6 FF(4BW_P"6<; Y^8@XD. 1_J_O#$@PP_6LGX1C2M/$6E*R?)]F+O?

M5I^]TT^'=>\K,_*\WXJE5O"A[L;M<_VFK6TNO=ZZ_%L_=U1],U^CGYZ% !0!

MX=\2O@E:^-/](M=EM=C<68)\DI.3^\ QABQYD +8)RK_ "[?BLZX9IX_WZ=H

M3UN[:2O=ZVZW^UJ[7NGI;[')^))X'W9WG#2ROK&UEI?I;[.BVLUK?XB\1>&K

MOPI.;:]B,4H ;!(((/0AE)5AU&02 01U! _&,9@JF#ER58N,K)VT>CZIJZ?R

M>]UNC]@PF,IXN//3?,KM7U6JZ-.S7SZ6>S,*N([ H * "@ H * "@ H * "@

M H * "@ H Z[P!_R&+#_ *^[?_T8M>KE/^\4O^OM/_TM'F9I_N]7_KU4_P#2

M&?I[7]*'\ZA0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % '\E-?K9Z04 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 =;X)\!:I\1[Q

M;#2+2:\N6P=D2EMJEE3>[?=CC#,H:1RJ)D%F K&K6C25Y-)>?]:OR$W8_9G]

MGG]@'2_A[LO_ !+Y.IZB/- M\"2Q16PJG9)&K32!=QW2 (I? B+QI,?C,;G$

MJND+Q6FNTOP>B]/OULM6_F^5O,$R,4F@9U

MVEHW'X,4-]BXZ\-BYX9WB]]UNG_7WE1DXGX<_M#?L>Z[\!-]Y_P ?

M^CKY0^W1J$V-)D;9H=[O'\PVA\M$VZ,>8)'\M?N<%F4,3IM+7W?\G97_ #WT

MMJ=D*BD?)5>N:!0 4 % !0 4 % !0 4 % !0!]:_L+?\E#TC_M\_](KBO(S;

M^#+_ +=_]*1G4V/Z(:_.SA"@ H * "@ H * "@ H * "@ H * "@ H * "@

MH * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@#G?%OA*Q\=V,

M^F:G ES9W*;)8GZ,.H((P58$!D=2&1@'4A@"-*=1TVI1=FMF-.Q^"_[1/[&&

MN_!NXGNK"&;4-$7+I=( \D2;7=AX+,X8A)-I

M2[='Z>M]M_7<[(5$SXSKVC4* "@"WI^GS:M-';V\;RS2NJ1QHI9W=B%55502

MS$D DD@ 9I-J*N]D!^JO[*W[!4QFM]=\7Q((0BRP:6P)?_TFM:^&SW^(

MO\"_]*D_P"P1J'_ *325Y&#_B0_QQ_]*1E'=>I_,)7Z

M@>@?HA_P3/\ ^1OO?^P1/_Z4VM?.Y[_#7^-?^DR,*VWS/W&KX8Y H * /PY_

MX*8?\C?9?]@B#_TINJ^YR+^&_P#&_P#TF)UT=OF?G?7T1N?T0?L+?\D\TC_M

M\_\ 2VXK\[S;^-+_ +=_])1Q5-SZVKR#(^'/VK_V-[?X\8U/2FAL];78KR2;

MEAN8QA<3%%9A(B_ZN4*Q*@1."OEM#[F7YF\-[LKN/XI^5^G=?/O?:%3E/PY\

M;> M4^'%XUAJ]I-9W*Y.R52NY0S)O1ONR1EE8+(A9'P2K$5]S2K1JJ\6FO+^

MM'Y'6G-Y9I75(XT4L[NQ"JJJH)9B2 220 ,TFU

M%7>R ^P=5_8WU3P1X-OO%>NM]FDCAMFM;$9\X--8

M8FC:)_&CF<:E54X:ZN[Z:1;T[Z]?NO>YE[2[LCXSKVC4_1#_ ()G_P#(WWO_

M &")_P#TIM:^=SW^&O\ &O\ TF1A6V^9^XU?#'(?S"?'[_D;]>_["^H?^E,E

M?J&#_AP_P1_])1Z$=EZ&1\(="M_%'B32+"\3S+:ZU&SAF3:0]_I116%_%"RHA)5"D

MZ@N(6WL A9BLH9=K%]\FC:6OKA'$;KYA1A;@#]_(NUR54JBE-CRQLR;O+QF8PPVCU

M?\JM?:^O9?TDS.4U$_?/X6?"S2_@YI<6D:1%Y=O'\S,V#)-(0 TLK #=(V!D

MX 4!455C5$7X'$8B5>7-+?\ !+LO+^MSCE*YZ)7,2?DI_P %2?\ F7O^XC_[

M:5]=D'V_^W?_ &XZ:/4_)2OK3I/W&_X)G_\ (H7O_87G_P#2:UKX;/?XB_P+

M_P!*D"9IM4\+Q/>Z8SH19('ENX"Y(*JH4F

M:%3MPP)F57&]&6-YV^WP.;QJ)1J:2[Z*+_R?X??8ZX5;[GYQU](;A0!_3W\

M?^10T'_L$:?_ .DT=?E^,_B3_P ?+=^IZW7(2% !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M 4 % !0 4 % 'YA>/_\ D,7_ /U]W'_HQJ_FO-O]XJ_]?:G_ *6S^BLK_P!W

MI?\ 7JG_ .D(Y&O*/3"@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M"@ H ]0\ _";4/'K!XU\FVX)GD!"D;MI$?'[QAAN 0H(PS*2,_2Y3D%;,7=+

MEA_/).V]GR_S/1^6EFU='SN:9[2R]6?O3_DBU?:ZO_*M5YZW2>I]Q>"_AWI_

M@./9:1YD.[=,^#*P)!P6 &%X&% "\9P6))_:LMR>CERM36NMYNSF[M:726FB

MT5EI>U[L_'FEHJZBK=;7>NKU=WK;;0[FO:/&"@ H * "@#G?%/

MA:U\96KVEVFZ-N01PR,.CH><,,^X()4@J2#Y^.P-/'4W3J*Z?WI]>:_P"

M[IM'?@L;/!352F[-?^#"T]N#6(903)&H&[,H

M P !D;Q\ORY.S<%K\8SCAFK@;SA>=.[U2;DDE?WDEZ^\M-+OEND?L&4<1T\;

M:,_)U\:?7!0 4 % !0 4 % !0 4 % !0 4 %

M'7> /^0Q8?\ 7W;_ /HQ:]7*?]XI?]?:?_I:/,S3_=ZO_7JI_P"D,_3VOZ4/

MYU"@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

M H * "@ H * "@ H * "@ H * "@ H * "@ H * /Y*:_6ST@H * "@ H *

M"@ H * "@ H * "@ H * "@ H * "@ H * "@#ZU_9Y_8]UWX][+S_CPT=O-

M'VZ10^]H\#;##O1Y/F.TOE8EVR#S#(GEMY&-S*&&TWEI[O\ F[.WY[:6U,YU

M%$_<;X0? _0O@;9M9Z+;^5YNPSS.Q>:=D7:&D<_BP1 D2,[E(TWMGX;$XN>)

M=Y/;9;)?U]YQRDY'K=X>SO[>:UN

M8]N^&:-HI%W*&7AKZ^$U-7337=.Z.E.YD58PH * "@ H *

M"@ H * /K7]A;_DH>D?]OG_I%<5Y&;?P9?\ ;O\ Z4C.IL?T0U^=G"% !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 % !0 4 >!>.?V7/!GQ&F^T:CI%LTV^1VDAWVSR/*0S

MM*UNT1E8D9S(7()8@@LV?0I8^K25HR=M-[/;M>]OD6IM'SOJ'_!-CP;>322I

M<:I"CNS+$D\)2,$DA%,EN[E5Z NSM@##;) ^X8( +%<,?!;PY\*%"Z+IUM:N$9/.5-T[([[V5YWW3.NX @.[ ;5 "J!Y=;%3

MK_%)ORZ=MEH9N39Z?7*2% !0!\U^+?V0? _CB^GU*_TI'NKE]\SI/<0AW/5B

MD4J(&;[SD*"[$NQ+,Q/IT\RJTTHJ6BVT3_-,T51HU_AY^R]X/^%5\-3TC34@

MO%1D25IIYB@?AB@FDD",1E2Z@-M+)G:S Q6Q]2LN64KKM9+\DA.;9[[7GD!0

M 4 <-\0_AKI'Q7L3INM6J75J75]C%E*NGW61T*NC!?\,+?#S_H$?\ DY>__)%>A_:U;^;_ ,EC_D:>T9]*>$O"5CX$

ML8-,TR!+:SMDV11)T4=223DLQ)+.[$L[$NQ+$D^94J.HW*3NWNS-NYKZAI\.

MK0R6]Q&DL,J,DD;J&1T8%65E8$,I!((((()!&*A-Q=UNA'RI_P ,+?#S_H$?

M^3E[_P#)%>M_:U;^;_R6/^1K[1GJ'PP_9[\,?!J::XT*P2UFG0))(9)97* [

MMJM,\A12<%@A4.50L"47'+7QE3$)*;NEY)?DD2Y.6Y[-7$0% !0!YA\3_@QH

M'QFAA@UZR2[2W#;.:.5[C5)D1U9HGGA"2 $$HQCMT<*W0E&1L$[64X(U>>

M56MHKSL_U;#VK/JKX9_ CPU\'MYT/3X;623<'ERTLQ5MF4\Z5GE$>44^6&V;

MANV[B2?)KXN=?XVWY;+[E97UW,W)O<]0U#3X=6ADM[B-)8949)(W4,CHP*LK

M*P(92"000002",5RIN+NMT2?*G_#"WP\_P"@1_Y.7O\ \D5ZW]K5OYO_ "6/

M^1K[1GL_PP^#&@?!F&:#0;)+1+AP\I#R2.Y484-)*SN57G:F[:I9R "[$\5?

M%3Q#3F[VVV7Y6(X^"

M?V-O W@;:T6DPW,HA$3R7A:ZWXVY69A0 4 <-\0_AKI'Q7L3INM6J75J75]C%E*NGW61T*N

MC[,V[G15F(* "@#AO$WPPT'QK,MQJFF6-[,J!%DN+6&9P@)8

M*&D1B%!9B!G&23C)-;TZ\Z:M&32\FU^0TVCP[3_V)/A]ILT-U=0]S=

M2(2I! :.29D=>.4=65AD,""17<\UK-6YOPBOR1?M&?55>49A0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0 4 % !0 4 ?F%X__P"0Q?\ _7WE_P!>J?\ Z0CD:\H],* "@ H * "@ H * "@ H * "@ H * "@ H

M* "@ H FM[=[MUCC4N[D*JJ"2Q)P .22> !R35P@YM))MMI))7;;Z$SFH)M

MNR2NV]$DNI]8?#S]G;I<:U_M#[*K?@K/(C?4A4/]TE_O)7ZCE'!_V\3Y_NT_

MDFY1?J[+RN]XGYGFW%OV,/Y?O&OFTHR7HKOSLMF?5]O;I:(L<:A$0!550 %

M& !P !P . *_4H04$DDDDDDDK))=#\RG-S;;=VW=MZMM]2:K)"@ H * "@

MH * "@#YL^)GP#AUO==Z4$@F"U]$?'&

MK:3/H4[VURACFC.'0]0?Y$$<@C(((()!!K\CQ&'EAY.$TU*+LT_Z^Y[-:K0_

M5J%>.(BIP=XR5TU_7WK=/1F=7.;A0 4 % !0 4 % !0 4 % !0!UW@#_ )#%

MA_U]V_\ Z,6O5RG_ 'BE_P!?:?\ Z6CS,T_W>K_UZJ?^D,_3VOZ4/YU"@ H

M* "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

M H * "@ H * "@ H * "@ H * "@ H * /Y*:_6ST@H * "@ H * "@ H *

M"@ H * "@ H * "@ H * "@ H U]"T"\\47"6=A;S75S)NV0PQM+(VU2S;40

M%CA06.!P 3T%1.:@KMI+NW9";L?KM^SG_P $](=!:+5/&!2>X1XY(M/C8/ H

MV9*W1*XE8.1F.,^3^[^9YXY"B_(8W.7+W:>BUO+K\NWJ]=>C1S3J]C]2:^6.

M<* "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "

M@ H * "@ H * /G?X^?LS:%^T!;G[='Y.HQPM':W\>?,BRP8!E#*LT8;/[N3

M. \GEM$[EZ]'!XZ>%>FJOK'H_P#)_P# O/+EPH8!E#,T,A7/[N3&2DGEM*B%Z^YP>.ABEIH[:QZK_-?\"]CLC-

M2/G>O1+"@ H * "@ H * "@#ZU_86_Y*'I'_ &^?^D5Q7D9M_!E_V[_Z4C.I

ML?T0U^=G"% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 ?F%X_\ ^0Q?_P#7WUEN3ULQ=J:TUO-W4%9+2Z3

MUU6BN];VM=GCYCFU++U>H]=+15G)WZVNM-'J[+2V^A]Q^ ?A-I_@)0\:^=<\

M$SR %@=NTB/C]VIRW )8@X9F &/VK*<@HY6X.UT+#!*D?@=IRI(4E3@5Y68Y72S"/+55[7LUHTVK

M73_1W3:5T['J8#,JN ES4W:]KIZII.^J_56:N[-7/A'Q]\)M0\!,7D7SK;DB

M>,$J!NV@26MDW9G[/E

M>>TLP5E[L_Y)-7VN[?S+1^>EVEH>7U\T?1!0 4 % !0 4 % !0 4 % '7> /

M^0Q8?]?=O_Z,6O5RG_>*7_7VG_Z6CS,T_P!WJ_\ 7JI_Z0S]/:_I0_G4* "@

M H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M "@ H * "@ H * "@ H * "@ H * "@ H _DIK];/2"@ H * "@ H * "@ H

M * "@ H * "@ H * "@ H * /HCX!_LS:[^T!<#[#'Y.G1S+'=7\F/+BRI8A

M5+*TT@7'[N/."\?F-$CAZ\[&8Z&%6NKMI'J_\E_P;7(E-1/W&^ ?[,VA?L_V

MX^PQ^=J,D*QW5_)GS)<,6(52S+#&6Q^[CQD)'YC2N@>OAL9CIXIZZ*^D>B_S

M?_!M8XY37GMT22273Y&+SJ=^0M

MJ0N95"$XCD/G?N_E>>20(OV."SE2]VIH]+2Z?/MZK37HD=4*O<_,'4-/FTF:

M2WN(WBFB=DDC=2KHZDJRLK %6!!!! ((((S7U":DKK9G05*8!0 4 % !0 4

M?9G[ NA7&K^/K&:!-T=G#=S3GMT_R3,JKT/Z"J_/CB"@ H * "@ H * "@ H * "@ H * "@ H * "@ H

M * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@#QF]_:$\,:9KX

M\+SWZ1ZN71!;O'*H+R1B2-1*4$.YU9=@WY9F$8!D(6NU8.HX>T2]WO==';:]

M_P "^5VN>S5Q$'C/Q/\ VA/#'P:FAM]=OTM9IT+QQB.65R@.W:7YM%J+EL>MZ?J$.K0QW%O(DL,J*\Z(+=( H * "@ H * "@ H * "@ H \9\!_M">&/

MB?J4^DZ-?I=WELDCR*D3MDV^=C/E>=L\GS,_)

MLW[O-_WRVUV+Y':Y[C7"0% !0 4 % !0!XS

MX\_:$\,?##4H-)UF_2TO+E(WC5XY=FR1VC5FE5#%&NY&!,CJ% +,0O-=M'!U

M*T7**NE?JNBOM>Y:BV>S5Q$!0!XS>_M">&-,U\>%Y[](]7+H@MWCE4%Y(Q)&

MHE*"'[WNNCMM>_X%\KM<]FKB("@ H * "@

MH * /&?B?^T)X8^#4T-OKM^EK-.A>.,1RRN4!V[F6%)"BDY"EPH&(SAC

M^CY/PC*K:>(O&-T^3[4E:^K3]WII\6Z]UV9^>YOQ5&E>%#WI6:Y_LIWMI=>]

MUU^'9^]JC[!TG28-"@2VMD$<,8PB#H!_,DGDDY))))))-?K6'P\""."#P143@IIII-----733Z%0FX--

M.S3NFM&FNI\J_$O]GTW+O>:. "Q!-IPHR2=QC8D*HZ'RS@ ;MK ;8Z_,,ZX1

MYVZF&MJU^[T2UW<6VDN_*]%K9[1/TK)^*N5*GB.B?[S5OR323;_Q+7:ZWD?)

M5Q;O:.T0:_*YP<&TTTTVFFK--=#]/A-32:=TU=

M-:II]2&H*"@ H * "@ H * "@#KO '_(8L/^ONW_ /1BUZN4_P"\4O\ K[3_

M /2T>9FG^[U?^O53_P!(9^GM?TH?SJ% !0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M % !0 4 ?R4U^MGI!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0!;T_3YM

M6FCM[>-Y9I75(XT4L[NQ"JJJH)9B2 220 ,TFU%7>R _3[]G/_ ()Z3:\L

M6J>,"\%NZ1R1:?&Q2=COR5NB5S$I0#,<9\[]Y\SP21E&^7QN73Y

M=_5Z:=4SGG5['[!:?I\.DPQV]O&D4,2*D<:*%1$4!5554 *H &*^.

M;^\_X\-8;RA]N

MC4OO6/(VS0[T23Y3M#Y65=L8\PQIY;>O@LRGAM-XZ^[_ ).SM^6^E]36%1Q/

MPZ^+_P #]=^!MXMGK5OY7F[S!,C!X9U1MI:-Q^#%'"2HKH7C3>N?N<-BX8E7

MB]MULU_7W'7&2D>25UE!0 4 % !0!^GW_!,GP3>3:QJ6N;<645H;/>0PWS2R

M12X0[=C;%BS(-P9?,B^4A\CY?/:JY8PZMW^237ZZ>C.>L^A^S%?&'*% !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 % 'X<_&O\ Y+G!_P!A?0__ $79U]SA?]T?^"I^W?#->0

M12+N4,NY'<,,J0PR.00>AJ88:\-^%[A[._U?3K

M6YCV[X9KR"*1=RAEW([AAE2&&1R"#T-:PPTYJZC)KNHMK\AJ+9W.GZA#JT,=

MQ;R)+#*BO'(C!D=& 965E)#*00002"""#BN=IQ=GNB3SO3_C=X5U::.WM];T

MN6:5U2.-+ZW9W=B%5559"68D@ $DD #-=+PM2*NXRLO[K_R*Y6>GURDG.^)

MO%^F^"H5N-4N[:RA9PBR7$R0H7(+!0TC*"Q"L0,YP"<8!K2G3E4=HIM^2;_(

M:5RIX6\?Z/XY\S^RK^TOO)V^;]FN(YMF_.W?Y;-MW;6VYQG:<=#55*,J?Q)J

M_=-?F#5CK:Q$% 'X<_\ !,__ )&^]_[!$_\ Z4VM?1!N)9(BV]E&

MQ\D CY&Y^4XQ5.37-9V6[L[??\Q6/Q;_ ."F'_(WV7_8(@_]*;JOM)=6\07/AOPL9K.*":;3V\J-7NKJXW^2QC(5WC^8%;?R2

MLQ)\PL'9(XOL\!ED(P4ZEG=*6KLDK7\K^=].GKU0IJUV>7ZG\1?BY^S#,DVK

MS7WDS/"3]M=;^VD*ER(?/+3")G"OOCBDBF* ,< (PZHT,-C%:*5U?X?=?36V

ME_FFBK1D?L;\#_B_9_'+0K?6K-?*\WUU_7XG+*/*SUNN0D_#G_ (*8?\C?9?\ 8(@_]*;JON=3HRJ?"F[=DW^1FE0K&,(6 8H&+!'(VG;!UUAZBFU=*_P"*:_4J+Y7<^5?V%?V??^%7_;]5

M_MJTU+S\6WE:;<^?9C9MDWRMM7=<+NPBX'E1NYR_GX3U46EYIK\P::.YK 1R7BGQ_H_@;R_[5O[2Q\[=Y7VFXCAW[,;MG

MF,N[;N7=C.-PSU%;4Z,JGPINW9-_D-*Y;\,^+]-\:PM<:7=VU["KE&DMYDF0

M. &*EHV8!@&4D9S@@XP14U*

M=CLPIX*/-4=M'9:# L]P!\]=+KENT?D6;\1U,;

M>,/V5]D?(!0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0!YWX^^&=C\0(SYZ[+A4*Q3K]Y.[E> /\ D,6'_7W;_P#HQ:]7*?\ >*7_ %]I_P#I:/,S3_=ZO_7JI_Z0S]/:

M_I0_G4* "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

MH * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H _DIK];/2"@ H * "

M@ H * "@ H * "@ H * "@ H * /6_A!\#]=^.5XUGHMOYOE;#/,[!(8%=MH

M:1S^+!$#RNJ.4C?8V.3$XN&&5Y/?9;M_U]Q,I*)^XO[//['NA? 39>?\?^L+

MYH^W2*4V+)@;88=[I'\HVE\M*VZ0>8(W\M?AL;F4\3IM'3W?\W97_+;2^IR3

MJ.1];5Y!D% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 <[XM\)6/CNQGTS4X$N;.

MY39+$_1AU!!&"K @,CJ0R, ZD, 1I3J.FU*+LULQIV/Q;_:&_8!U3X>[[_PU

MYVIZNNT?Q>C]?

MOUL=4*M]S\[Z^B-PH * /1/A9\+-4^,>J1:1I$7F7$GS,S9$<,8(#2RL =L:

MY&3@EB515:1D1N;$8B-"/-+;\6^R\_ZV)E*Q_1O\#_A!9_ W0K?1;-O-\K<\

MTY14:>9SEY&"_@B!B[)$D<9=]FX_G&+Q+Q,W)]=EO9?U^)PRES,];KD)"@ H

M * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "

M@ H * "@ H * "@ H * "@#\ /VN?$TW@KXJWFJ6ZHTUE<:;<1JX)0O#;6TB

MA@I4E25&0"#C."#S7Z!EU-5,.HO9J:^^4D=L%>/WG<_\/,/%_P#SY:1_WXN?

M_DJL/["I]Y??'_Y$GV*/E7XY?'+4OC_J46J:I%;1316RVZK;JZH45Y) 2)))

M#NS(V3D# '&?";P/X:T'1I/

M)U&_T.QDFN%W"2WMS!&BF([=HDE99%$@8O"(V(57>*1/G\)@57JSG+51J2LN

MC=V]?):>M_5&,87;?F>,_ S_ ()_ZE\6M(AUF]U!--AND#VT?V9YI63^M\G9)&^/]XPS!=\3[XW3_7P-U5*=/,:=U\GU3[?YKK]S

M*:4T>H?\%(-0AU;Q5I]Q;R)+#+HML\,;

M@^ K"6:!;Z[!N+*9S#&LULK%VF5AN7RU0M*@!9S#'^[DEBA"^Q7E3IKVSL^5

M:-:NS[>M]/5]&S5V6I[[^T3^PO?? O2/[:M[]-1M8G5;K,/V=X1(RI&ZJ991

M(I=@C $,I9"%92[1^?@LV6)ERMVM[]7T5B(5.8^G_ -D?]J)?#_@#4WU0

M/*_AM$$18OB:*X+"T@,F96#>:&@!V+%##Y/!"N1Y>8X#FK1Y?^7GX-;OITUW

MNW\^7 P481E+?2*;;=MV_Z\E9&WP+0I_&7X/VWP2FM+[0O$5CJZ;P1

M-97$27-O.A+H?*BGE<+P&29&^5P581GRS)6%Q+Q":G!Q\I)V:]6E]W_!L1ES

M;H_:3]D/XTW'QS\+Q7]]S?6\TEK=.$5%DDC"N)%56(^:.2,O@(/-\P*BH%KX

MK,L*L-4LMFKKKH_^"G\CEG'E9]/UY9F?S'_ WXY:E\ -2EU32XK:6:6V:W9;

MA79 C/'(2!')&=V8UP$CBH\LKV3OI;LUU3[G?*/,?57_ \P

M\7_\^6D?]^+G_P"2J\K^PJ?>7WQ_^1,_8H^;/AAXFF\:_$'3-4N%19KW7[6X

MD5 0@>:\21@H8L0H+' ))QC))YKTJ]-4Z,HK94VONC8T:LOD?8/_ 4"_:)U

M0ZS)X4TZ>:ULK6%!>B,F-KB2XBW%&=7)>W$,BKY9"!G:3>L@6(KX^3X*/+[2

M23;>G6R3_.ZW]+=3*E#J>2:%^R-HFH:6ES=>,]#MM2>%G-F;BWDC20@E(WN%

MN?\ =$CI&X0[MGFJH9^R>8S4K*E-J^]FG;O;E^[7[BG-]F=%^Q'\=;[X9^)H

MO#>HW3R:9=NUG'$)_/@@NC(3$\!C$JE9)"T9,++%)YPG=V6-366:X15J?/%>

M\M;VLVK:WO;9:ZZZ6ZA4C=7-?]MS]HG4OB=K4O@[2-YT^VN%MWCA5S+>W:L%

M*,NT,5CES''$H97E3SMTF8?+C*L%&C'VLMVKZVLH_P#!6K?;336ZIPMJ=%_P

M[#UC^SO-_M>T_M+_ )]_*D^S_?Q_Q\_ZS[GS?\>_W_D^[^\K/^WH\WPNW>ZO

MMV_X/^0O;'Q]\+K*^TGQ]H]GJ9?[9::U86LJN_F%#;7$4 C#@L"L801IM)4*

MH"_*!7L8AJ5&3CLX2:Z;IN_SO_][M;^]W%2ET#]DS]C'_A,+71/&G]J^5LNUN?

MLGV3=G[)=LNSSO/7[_E9W;/EW=&QR9CF?LW*ER]+7YOYH]K>?<)U+:'AO[9.

MA7'BCXGZA86:>9<;*.T?$CHNZ2**42,[MPPA_EU]UOZL*M'J?KM7R!

MS'X&?'ZUU']F/XBS:[IUY:7%Q+=SWL:AD=HOM.7DM[J#<9(\I,55_E\V)Q+$

MZ2!EB^_P;CC**A)-))+JMMFGUV^3T>F_9'WE8_3WP3\0O!W[:>A+:7L4,LAQ

M+<:;++BXMY(BH,B,A24QY<*MQ'M#I(8VVLTD(^7JT:N7SNK]E)+1I^MU?39^

MO9F#3@RY\(?B/\/O!5]_PA'AN5(+R.XN4:T6"ZR9XMYG+SRH0[*(V =I&^5%

M1"5"+4XFA6J+VL]59:WCL]M$_/L*2;U9]55Y1F?AS_P4P_Y&^R_[!$'_ *4W

M5?-GAN"Y2%%C4L

M5N5!8A1D@ 9S@ <5I4R:G4DY-RNVWNNKO_*-TDSSOXY?M?:]\?\ 38M+U2WL

M8H8KA;A6MXYE+ZXFN;6U:1\D_ K]F/Q!^UE+/K-WJ&RV6;R9[ZY=[FXD

MD2($*B%@S[%,*L9)(P$<;"Y1D'K8O'PP5HI:VNDK)6O_ ,/LGYFLIJ!D?%+X

M4^*/V+-8M[FVO_+^T>8;6[M7*^:D,B,8YX6_[8O)"XE@;<%WR[6Q>'Q%/,(M

M-;6NGTNGJG]]GH_0<9*9]$_M@?M!7GQ+\#>&I8AY$6L_:);U%W)NFL62)D4"

M1@;

M]?37_MUVUT_X:)VC,0B22[M,Q(AE

ME 7>'D." 6D8[_NRUV7I\C*,N:1^9GP#^ >J?M Z

MH+"P'EV\>UKN[928[>,D\GD;I&P1%$"#(03E8UDD3Z?&8R.%C=[]%U;_ ,N[

M_6R-Y2Y3WWX[?L5:U^SM:#Q#8:@EW:VCP,\Z!K6Y@E:3:DBIO<%5?R@'23S0

M[@^6%0R5Y^$S2.*?(U9N^GQ)JWHO/I;S(C4YM#Z?^!/QYOOC!\-?$]CJLCSW

MVE:7=H;AAS+!+:3>29'W$O,ICD5W*KN41LQDD,CGR\7A%0KP<=%*2T\U)7^6

MJ_'I8SE&S1YW_P $Y?$T/@K3?%FJ7"NT-E;6EQ(J %RD*7DC!0Q4%B%. 2!G

M&2!S73G5-U)4XK=N2^]Q1557L?._AG1O%W[='B-A70T6O3^:3\W\]]ETZ(MV@CT_XN?L$>(/

M@];P:OX?NYM5EAF5F6VMWANH6#*8I85265Y,-]XH5>,[7"LF]X^7#9O"NW&:

M4;KJTT^Z=TO^#^)M.TK=-('-Y.KWDTQV.9#'++#NC?S&S,9&8R*R[#RP]

M_$XIX>T80E+1;+W4M5;1/73:VQM*7+L@O/[1_9)\00:AH.LZ=J2GS-DUE_: ^W:;31]L>'?#5IX4@%M91"*($M@$DDGJ2S$LQZ#))( Z ?LN#P5/!QY

M*45&-V[:O5]6W=OYO:RV1^0XO&5,7+GJ/F=DKZ+1=$E9+Y=;O=FY7:<84 %

M!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0!4O]/AU2,PW$:2Q-C\[L_5LHXJC5M"O[LK)<_V6[VULO=Z:_#N_=T1\S5^<'Z$% !0 4 %

M !0!UW@#_D,6'_7W;_\ HQ:]7*?]XI?]?:?_ *6CS,T_W>K_ ->JG_I#/T]K

M^E#^=0H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "

M@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@#^2FOUL](* "@ H *

M "@ H * "@ H * "@ H * "@#]$/V>?V =4^(6R_\2^=IFG'S0+?!COG9<*I

MV21LL,9;<=T@+L$P(@DB3#YW&YQ&EI"TGIKO'\'J_3[]+&$ZMMC]I/"7A*Q\

M"6,&F:9 EM9VR;(HDZ*.I))R68DEG=B6=B78EB2?BJE1U&Y2=V]VU?\ O^?;V47^\$\NYF_X S;K?^\@

M[25A5S[?DCZ.3_1?Y_Y"=;L?HA\(/@?H7P-LVL]%M_*\W89YG8O-.R+M#2.?

MQ8(@2)&=RD:;VS\YB<7/$N\GMLMDOZ^\PE)R/6ZY"0H * "@ H * "@ H *

M"@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H

M * "@ H * /PY^-?_)[=W^??S]4<3

M2MBWVY,JDRJBL!^\8$IN0H[?6Y51>'I>_I=N6O166_;;Y=3IIKE6H?MP^&9O

M!6I>']+N&1IK+PUI]O(R$E"\+SQL5+!25)4X) .,9 /%&55%4C.2V=63^])A

M3=[^I^_]?GYQ'X<_!3_DN<__ &%]<_\ 1=Y7W.*_W1?X*?YQ.N7P_)'Z(?MT

M_P#)/-7_ .W/_P!+;>OG_P#268T]S\J_@)H5QXB\ ^.H;5-\BPZ3

M,1N5<1V\\T\K98@?+'&[8ZMC"@L0#]5C)J%:DWWFOFTDOQ9T2=FOF>=_L[_!

M?2_C=>36%]K<.D7(\H6J2PB3[4TC%"B,TT*^8&,86,%GDWDJI"-CIQN*EATF

MHN2UO9VM^#TWUZ%3ERGK?QU_95\/_L^>1'JOB.::YN/F2UMM,1YA&,CS7#WT

M:K'N&Q26!=LA%8)(4Y,)F$\5?E@DEU68M\I\Q9&E61Q(R-A=GRC?)\YFV)E

M5GRR27)?9WWL[WLM+6Z>IC4E=^A]QUX9B?AS_P $S_\ D;[W_L$3_P#I3:U]

MSGO\-?XU_P"DR.NMM\S]QJ^&.0_G>_YJ_P#]S;_[DJ_1/^8;_N#_ .V'=]GY

M?H9/[5G@/_A!_'NIP7KS+;7=V;P3K!\QANV\YS$C.JR^6S21 ^8BR/$P+1G(

M6\OK>THQ:M=*UK]5IKII??;KU"#NCZ3T_P#8"T74](CUY/%]L-*D176[>R6.

M(!F" ,TEVH1MY\LH^UEDS&P#@K7FO.)*7)[-\W;FN^_2/](S]KTL>8?LX?#'

MPOXC\::?;:=KEW)<6EVMS 9=*$4-U]CD$Q1'%[))'O2-G5I8DPH(($FV-NK&

MUZD*3ZM_PH/XLW>H7\4-U';ZNUX\8

M3S1Y-V?/4HKF,?:(XY@T9)"I<(K;F5Q^"^E>/(?B?\ %*RUFW@2VAN]?LGCC6,1G9]IB56D

M56<>S?\%,/^1OLO\

ML$0?^E-U7%D7\-_XW_Z3$BCM\SZV_P""F'_(H67_ &%X/_2:ZKR,B_B/_ __

M $J)G1W^1T7[!WQ,T6Z\'Z9HJWUL-3B>[1K-I%6WA?\

M='_@J?G(UC\/R9^XU?#'(?AS_P $S_\ D;[W_L$3_P#I3:U]SGO\-?XU_P"D

MR.NMM\S]QJ^&.0_G(^&.GZ7\3O'LA\;O_9T5S=W=Q>1L1;1K<;GE>WE>:17M

MXRP:,G+S9VQ#:[^='^CUY2HT?W7O644NKMHKJRU?X=?([GHM#T3]HOX)R_L@

M:[9:EX=U3^[) 'FB^W0-AE)DB 7S;>3;(HD$?E,-]O*OW3-SX+%?7H.,X^NC

MY7\^C7K?JO*82YUJ:_\ P3KGTO3_ !9+<:C<6D,HM&BLDN"%D>XFEC0?9V9=

MGF;=T94.LSB7:B.GF[(SI2=.T4WK=VVLD]_+KVTUZ!5V/WOD7\1_X'_P"E1-:._P C

MY5\?:?->? K0'BC=TAU25Y6521&AFU",,Y PJEW1 3@;G5M_(JE'J>M_!WP9X?USX2:5IOC)H;*TN//:*6ZD2V:.22XN)8)8

M))L 2&,F2,C(DB)RKPNZMQXFK..)E*E=M6NDF]$HIIVZ7T?9^9,F^;0^,_VF

M?V(?^%%:=)K5KJL,]D)M@@N%\JX_>.HBCB*EDN) I=Y3B#"1-(J$95/:P.:_

M69&OC-JGQ+^%'BC3]6FFNY=.FTUX[J:4R2-'<

MWD9$;%AO;8T3L'=W)$@C&U(U!B>%C1Q%.44ES*6B5E=1>OX_AYB<;21<_P""

M=WQCT7X:WVIV&KW*69U!+=H)YF5(,VWG%T>5B C,) 4+85MK+N#F-7G.L-*L

MHN*ORWNEJ];=/D%6-S]!/VQ?C-I?PX\+ZE8SS0OJ-_:/;06?F@3,MT'A,VP!

MF$:+YC[V"H[1^5O5W6OG\LPLJM2+2=HN[=M--;>NWWW,:<;L_/O]C?3YH_!7

MCVX:-Q#)I;(DA4[&>.UO&=5;&"RB1"P!RH="0 PS]!F;7M:2Z\W_ +='_(VJ

M;HYW]DSP3_PL+P=XYT\+,\C6EC+%'"-TCS6_VJ>%%7:Q;?)&BE0-S E5(8@C

M7,:OLJM*6F\D[[6?*G^#'-V:.M_X)O\ Q3TOP7JE_I%_+Y-QJOV5;1FP(WDA

M,P\HMGY9'\T>4",.5*;O,:-'QSO#RJ14EJHWOWL[:^FFO^5Q58W/T^^-/[1/

MA_X#V_FZM/NN&V&.RA*/=2*[, ZQ,ZXC&UR9'*IE2@8R%4;Y?"X*>)=HK3N[

MV^_OY?H<\8.1^;'[9WC.W_:/\+Z5XMT-9C8Z==W=I>1RQLLT$DX@9&<)OB$>

M$7+B0C=-"G+LRI]+EE)X2I*G.UY*+5GHTK^COKVZ,WIKE=F>&_LV_LMZ7^T7

M;R"+7OL>I09::Q>R#L(]V%EC?[2GF1\@.0JF-SM90K1/)W8['RPKUA=/9\UM

M>WPNS_/[[7.?+T*GQ/\ @%X1^%.I0Z7=^*GN)G+DJ=ETO.U]+Z>Y^.B\P4F^GX_\ /W&^#'PPA^#

M.@66@P3/<):(X,K@*7>21I9&"CA5+NVQ;?[Q5_Z^U/\ TMG]%97_ +O2_P"O5/\ ](1R->4>F% !0 4 % !0 4 %

M !0 4 % !0!KZ)H-UXDF%O9Q/-*:I)17=OR;LN[TV6KZ'VE\-/@1!X3=+R^83WB

M$E57F%#D;6 *AF<8R&. I/"[E5Z_8J3;6]WHKZ*Z

M3/R7..)Y8M.G27+!I7;^-]UHVDO):NVKLVCZ"K[T^&"@ H * "@ H * "@ H

M * "@ H * "@ H * "@ H * "@ H * "@#Q_XE_""T\=H\\8$-_@;9N<-M!P

ML@'!!'&\#>H"\LJ[#\EG7#U/,4Y*T:ME:6MG;I)?A>UUINE9_59/G]3 -1?O

M4[N\=+J_5/\ &U[/79NY\.>*_!U[X+G,%Y&4.2$?!\N0#'*-@!A@@GNN<,%;

M('XKC\NJX&7)436KL]>5VMJGUW7FMFD]#]BP.84\;'FIN^BNM.97OHUTV?D]

MTVM3EZ\T]$* "@ H Z[P!_R&+#_K[M__ $8M>KE/^\4O^OM/_P!+1YF:?[O5

M_P"O53_TAGZ>U_2A_.H4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0!_)3

M7ZV>D% !0 4 % !0 4 % !0 4 % !0 4 =S\//AKJ_Q7OAINBVKW5T49]BE5

M"HGWF=W*HB\A0790694!+,H.%:O&@N:3LOZ[";L?MU^S5^Q)I?P6_P!/U4PZ

MGJQ\MD=H@8;5EVO^X5\DR"09%R0C[54(D.9-_P /CLUEB-(WC'7KJ_6W2W3\

M]#DG4YC[CKPS$* "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

MH * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M"@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H

M * "@ H * "@ H * "@ H * "@ H * "@ H ^'/&O[&/_"8>.8_&G]J^5LN[

M&Y^R?9-V?LBPKL\[SU^_Y6=VSY=W1L<^Y2S/V=+V7+TDK\W\U^EO/N;*I96/

MN.O#,3X<_:8_8Q_X:*UB'5?[5^P^3:);>5]D\[.R263?N\^+&?-QMP<;[O?FMT2[/L;0JKC[5;VMI;VZSJHCD6

M2WB$2W$62_ER<$@9<89HV\R-G5N&.,E"HZD=&VW;=6;O9[77_#[D>P:]Z+3\

MK/\ /E-U61]5?L[?L':7\([B#5]6F_M'5(5=.,5RQ?WM?HGU7XV,YU+FO^TQ^QC_ ,-%:Q#JO]J_8?)M

M$MO*^R>=G9)+)OW>?%C/FXVX.-N<\X$8',_JL7'EO=WOS6Z)=GV"%3E/N.O#

M,3X<\%?L8_\ "'^.9/&G]J^;ON[ZY^R?9-N/M:S+L\[SV^YYN=VSYMO1<\>Y

M5S/VE+V7+TBK\W\MNEO+N;.I=6/HCXZ?"W_A=/AV\T'[1]D^U^3^_P#+\W9Y

M4T&,YYQ@^=A,1]7FIVO:^E[;IKL^YG&7*[GDG[+?[+?\ PS5_

M:'_$P^W_ &_[-_R[>1Y?D>;_ --9=V[S?]G&WOGCLQ^/^MVTMRWZWWMY+L7.

M?,?._P XU;;GG?PY_X)DWCW!;Q+J4*6RXQ'IY9

MY),JVY%W_O;?$K

M'P)8P:9ID"6UG;)LBB3HHZDDG)9B26=V)9V)=B6))^3J5'4;E)W;W9S-W.BK

M,1\.?LS_ +&/_#.NL3:K_:OV[SK1[;ROLGDXWR12;]WGRYQY6-N!G=G/&#[F

M.S/ZU%1Y;6=[\U^C79=S:=3F/N.O#,3\[_\ A@C_ (J__A*_[9_YB_\ :7V;

M[%_T\_:/*\W[1_P#?L_VMG:OHO[7_=^SY?L0A=X!#;8Y5(Q+"'._9E&!W!)(_,DW<&#Q\L*]-4]T_T

M[/\ IIV(C/E/SD_X=D^)/MFS^TM.^Q>=CSLS^=Y.[&_R?*V>9M^;R_-V[OE\

MW'SU]'_;L+?#*]MM+7];[>=OD;^V1^B'[-O[+6E_LZ6\AB?[9J4^5FOGC",8

M]V5BC3<_EQ\ N S&1QN9BJQ)'\[CLPEBGKHELKWU[]+O\OOOA.?,'[27[+6E

M_M%V\9E?['J4&%AODC#L(]V6BD3

M_6S_ #^ZQ"?*?G?H7_!,GQ)<7"+?ZEIT%L=V^2$SSR+\IV[8WB@5LM@',BX!

M+?,1M/T4\]@EI&3?G9+[[O\ (W=9'OO@W_@G%#X*UK3]6@UIW2QN+2X,+V8S

M(\#1O(!()P$5W5B@V,8U8*3*5+MY]7.W4BXN/Q*2OS=[KM_P_D0ZMST_]IC]

MC'_AHK6(=5_M7[#Y-HEMY7V3SL[))9-^[SXL9\W&W!QMSGG Y<#F?U6+CRWN

M[WYK=$NS[$PJ-UDCV>;$\;!@T32)($8C=&QV

MY,;NN0&->;AL3+#RYH[Z[WM^#7_#F<9>OW_*SNV?+NZ-CGEI9G[.E[

M+EZ25^;^:_2WGW)52RL?<=>&8GPY^S/^QC_PSKK$VJ_VK]N\ZT>V\K[)Y.-\

MD4F_=Y\N<>5C;@9W9SQ@^YCLS^M14>6UG>_-?HUV7#<6H'V@,@V#;!)(V^)CAR6E-P-S@A J[&X*6>3BK22D^CV[[I;_

M "L0JK/T2?M,? 3_AHK1X=

M*^V?8?)NTN?-\GSL[(Y8]FWS(L9\W.[)QMQCG(Z\#C/JLG*U[JUKVZI]GV*A

M+E-?X5?!"W^'WA*/PC>2_;[80W4,S[&@\V.ZDE=UVK(S)\LI3*OGC<"IX$8C

M%.K4]HM'=-==4EY>78)2N[GYW?$;_@F3>)H%DDCPJXQ)!$Z

MR[FWG_5P[!M7]XJWOQ=_[NWW-JWWOY&ZK=SHOA'_P326SF%QXKO4F

M1'RMI9%PD@!0CS)Y$1PK?O$>.-$;!5UG4Y49XG/+JU-6\Y?/HK_>W\A2K=CZ

M?_:T_9>F_:1ALFM[Y+2;3TNS&CPETF><1;59U<&)08@"P24X8D(2N&\O+L>L

M(W=74K=;6M?RUW\C.$^4^$="_P""9/B2XN$6_P!2TZ"V.[?)"9YY%^4[=L;Q

M0*V6P#F1< EOF(VGWIY[!+2,F_.R7WW?Y&SK(^D_CA\$['X!?"+5-(L7>4E[

M2:XG?@S3M=VJNX3)$:X151%SM51EG??(WFX3%/$XF,G_ 'DEV7+(SC+FD?GU

M^S/^S#_PTA9ZOY%W]DO;#[*8-Z;X9/.6YRDF,.F6CCQ(N_8N_P#=2$KM^@QV

M/^J.-U=2O?OIR_YO3\4;SGRGT3X)_P""9.L37B_VYJ5I%9#!?[&9)9GPRY0>

M;%$D>5W8D/F;6"_NG!./.JY[&WN1=_.R7X-_=IZF;K=C],K3X)V.@^$9O!^F

MN\%J]C5AE S%Y&D*J47)*J$7 7YEXIRJ>TEJ^9.VVUM/PL8

M;_LXV]\\=6/Q_

MUNVEN6_6^]O)=BISYCP/XY_\$Z+'Q;--J'A>X2PN)7+M9S#_ $3+%,B)HU+P

M*/WC[-LREF6-!#&!COPF=."M45TNJ^+KO??IV^;+C5MN>2>!O^"8VI3S;M>U

M2VAA5XSLLE>9Y$R?,7?,L(B; 1MDPR22F%P_95SV*7N1;>OQ67IM>_X%.MV

M/U)_X5+H7]A?\(U]BA_L?R?)^RX.W;G=G.=_F;OWGF[O-\W][O\ ,^:OEOK$

M^?GN^:][_P!=.EMK:;'/S.]S\MO'/_!,;4H)MV@ZI;30L\AV7JO"\:9'EKOA

M682M@D.VR$9 (3#83ZFEGL6O?BT]/AL_7>UOQ.A5NYZ?\#_^"J?_I".1KRCTPH * "

M@ H * "@ H * "@ H ];^'GP>OO'N)O]19G=^_89R5XPB9!;G@MPHPPW%EVG

MZK*.':N8^]\%/7WVKZKHE=-Z]=%H];JQ\QFW$%++_=^*>GN)VT?=V:6G35ZK

M2SN?@VOB2$V]

MY$DT1S\K#."01E3U5L$X92&&>"*Y,3A*>*CR5(J2[->35UV>NC6JZ'5AL5/#

M2YJ$5\0?9A0 4 >H?!WPY)XDUJV"'"P.MQ(W!PL3 C@D9W-M3C)&

M[=@@&OI>'<&\5B86V@U-O3:+3[K=V7E>]M#YWB#%K#8>=]YIP2\Y)KL]E=^=

MK7U/T;K^A#\$"@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * /Y*:_6ST@H

M * "@ H * "@ H * "@ H * /M?]G/\ 8GUKXS-%?Z@KZ=HV^,M+(K)/<1,G

MF9M492&4@H!,^(AOW()BCQUXF-S2.'T7O2U]$]M?\M_3B5S$A0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 >!?M0_#R^^*O@_4M(TP(UY.D+1([; YAGCF*!CP&81

ME4+87<1N95RP]# 5E1J1E+97O\TU^I<'9GSO^P7\ M?^"<.K2Z] EL]Z]JL4

M0ECE?$ F+.QB9T"GS@%&XME7RJC:6]'-\9#$./([VO=V:WMWMV+JR4MC]!:^

M>,0H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H

M * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "

M@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H _,+Q_\

M\AB__P"ONX_]&-7\UYM_O%7_ *^U/_2V?T5E?^[TO^O5/_TA'(UY1Z84 % !

M0 4 % !0 4 % %RPT^;5)!#;QO+*V=J(I9C@9. 2< $GV&:UI4I5GRP3DWL

MDFWM?9&56K&DN:344MVVDNV[/KOX<_L])8%;K6,22*59+=2#&.,XE./F()^Z

MIV?+RTBL0/U?)^$%3M/$6;334$[QV^UIKKT6FFKDG8_+LWXK=2\,/HFFG-JT

MM_LZZ:=7KKM%JY]25^FGYP% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 % !0 4 % '@7Q,^!MOXMW7-ALM[UGW.26$&-O.E:%1N[O?EE>U[VO9];I:N]TV[K[;)N)9X.T*

MMY4TK*UN:-MK7M==+-Z*UK)6?RAJ?PLUO27"26,[$C.8T\T8R1RT6Y0>.A.<

M8.,$9_+:^18JB[.E-Z7]U?(_NGROY[&MX=^

M"VM^(B,6Q@3)!>?]V 0,_=(\P@\ %5(SQG@XZ\'PUBL3]AP5VKS]SI?9^]Y7

M2:OZ,Y<7Q%AL-]OF=D[0][K;=>[YV;3M\C[8^'OP]MOAW;-! QD>0AI96"@L

M0H&!@9" Y*J2Q4LWS'-?LF491#+(.,6VY-.4FE=NR71;;M)MVN]3\BS;-IYE

M-2DK))J,4W9*[?5[[)M)7LM#OJ]T\0* "@ H * "@ H * "@ H * "@ H *

M"@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H

M * "@ H _DIK];/2"@ H * "@ H * "@ H * .B\)>$K[QW?0:9ID#W-Y8262XD"E0.!%&^\KYI$4R_&X[-W4]VG=*_Q7LW_ )+\

M7Y:HY9U;['Z3U\T8!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M 4 % !0 4 % !0 4 % !0 4 ?F%X_P#^0Q?_ /7W=Y-7C!;OIYV7F^SM=JQ]Q^ ?AG8_#^,>0N^X9 LL[?>?G)P,D(N?X

M5Z@+N+%=U?M.4Y)2RU>ZKS:M*;W>M^[LO)=E=MJY^.9IG-7,7[SM%.\8+9=/

M*[\WW=K)V/1*^@/""@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

M H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

MH * "@ H * "@#^2FOUL](* "@ H * "@ H * "@#Z?^ ?[)OB#X]N);=/L>

MFC:6OKA'$;KYA1A;@#]_(NUR54JBE-CRQLR;O+QF8PPVCU?\JM?:^O9?TDS.

M4U$_='X)_ ;1?@%8O8Z1&Y,K[Y[B8JT\Q&=@=U5!M0$JB*JJN6;&]Y';X7%8

MN6)=Y=-DMDJ?_I".1KRCTPH * "@ H * )K>W>[=8XU+NY"

MJJ@DL2< #DDG@ GO

MPMUK&8XV"LENI(D/.<2G'R@@?=4[_FY:-E(/Z5D_"#J6GB+I-)J"=I;_ &M-

M-.BUUU<6K'YUF_%:IWAA]6FTYM7CM]G777J]--I)W/L"WMTM$6.-0B( JJH

M"@# X X ' %?K,(*"22222225DDNA^5SFYMMN[;NV]6V^I-5DA0 4 % !

M0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 ?R4U^MGI

M!0 4 % !0 4 % %O3]/FU::.WMXWEFE=4CC12SN[$*JJJ@EF)( !)) S2;

M45=[(#]:_P!FG_@GTVFS0ZOXQ"%XW=DTKY)$)4@1O<2H[(Z\,WD)N5AY>^0@

MRP5\CCLYNG&E_P"!;?-(H8D5(XT4*B(H"J

MJJH 50 ,5\HVY.[W9S%ND 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 ?F%X_\ ^0Q?_P#7W![[

MQS,8;*/=MV^8Y.U$#' +$_B=HRQ 8A3@UZN7975S"7+25[6NWHDF[7;_ $5V

MTG9.QYF/S*E@(\U1VO>R6K;2OHOU=DKJ[5S[H^'7PELO ";N+BZ))-PR %1@

M@",9;8,$AL$EB3DXVJO[9D_#]++5?2<[_&XI-;JR6O+H]=;OJ[62_&LVSVIF

M#M\,+? FVGL[O:^JTTLNBO=OU6OJ#YH* "@ H * "@ H * "@ H * "@ H *

M "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@

MH * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M"@ H * "@ H * "@ H * "@ H * "@ H * /Y;?BYX)_X5QX@U+2 LRQV=W-

M%%YPQ(T*N?)=OE4'?'L<,%"N&#*-I%?J6&J^UA&6FJ3=MKVU_$]"+NCSNNDH

M* "@ H * /RM?[NWG^I$IJ)^[OP#_9FT+]G^W'V&/SM1DA6.ZOY,^9+

MABQ"J6988RV/W<>,A(_,:5T#U\'C,=/%/717TCT7^;_X-K''*;D?1%><0% !

M0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M% !0 4 % !0 4 ?F%X__ .0Q?_\ 7WJ?_I".1KRCTPH * "@#Z(^'GP NO$.+C4M]K;_,/+QMG8C@':RD(N

M<\L"QV\+A@]??Y1PG4Q/OUKPAK[NU1]-FG9>NKMM9IGPF;<4PPWNT;3EIKO!

M==TU=^FFN]TT?:6DZ3!H4"6UL@CAC&$0= /YDD\DG)))))))K]BP^'CAXJ$$

ME&*LDOZ^][MZO4_)*]>6(DYS=Y2=VW_7W+9+1&C708!0 4 % !0 4 % !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 ?E7_P %#OV=

MKC7=GB[2H/,:"$IJ:QA=WEQ\QW.U4#/L4LD[EF*1+"0HBCD=?J\FQJC^[D]W

M[OKU7^7G?JT=%*?0_'VOL#J"@ H * /TR_9S_P""?5]XG:+4_%H>RLU>-UL/

M^6]Q&4WXE97S;+DJK(1YYQ*A$#!)#\SC=6VQ^QN

MA:!9^%[=+.PMX;6VCW;(88UBC7+QE/"1YZCY5=*^KU?

M1)7;^72[V1]N_#7X)6O@O_2+K9&:> ]^I:<]+.VD;6>E^M_M:.UK):W_'\XXDGCO=A>$-;J^LKW6MNEOLZK>[

M>EO<:^U/C@H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H

M * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "

M@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H

M* "@ H * "@ H * "@ H * /SO\ C7_P3QT+QMYEYX>?^RKUMS>3@O9R,?,;

M&S[\&YF1"2IW(O(.,KAC[\,XHR5VVO)Q=_P37XFRJH

MZ+P-_P $\/&?B6;;J*6VEPJ\89YIDF=D8G>T26YD#,@&=LCPAB5 ?&XKG5SJ

ME!>[>3UV37WWM^%Q.JD?IE^SS^Q[H7P$V7G_ !_ZPOFC[=(I38LF!MAAWND?

MRC:7RTK;I!Y@C?RU^9QN93Q.FT=/=_S=E?\ +;2^IA.HY'UM7D&04 % !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M% !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0

M4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !

M0 4 % !0 4 % !0!#<6Z7:-'(H='!5E8 A@1@@@\$$<$'@BHG!3332:::::N

MFGT*A-P::=FG=-:--=3YR\1_LU6.HR![&=[53]Z,KYR] !M)96'0D[F?)/&T

M#%?GN,X+I57>E)TUU37.MEM>2:ZWNWOI8^^PG&-6FK58J;Z-/D?7>T6GTM9+

M;6YD6'[+T,<@-Q?.\7.Y4A",>.,,7<#G!/RG(XXSD*?OU6UU2@HO;NY

M2_)G55XTDU[M-)]&YN2^Y1C^:/H[P[X:M/"D MK*(11 EL DDD]268EF/09)

M) '0 #]"P>"IX./)2BHQNW;5ZOJV[M_-[66R/@<7C*F+ESU'S.R5]%HNB2L

ME\NMWNS90 _>* %WT *'S0,-U !NH$&Z@ !S

M0 $XH 6@ H * "@ H * "@ H * %S0,,T % !2 * %S3 ,T +F@0M !0 [=0

M H.: %H .E #MU #J "@!8?*;$'Q TZXSMF)Q_L/_

M /$T7"Q=?Q5;1]9#_P!\M_A1S(.5CF\56JC/F'_OEO\ "CF$4Y/&]E%UE/\

MWR_^%.XAK^-[)5W>:* %S0 ;J #=0 Z@84 %(!;U&7_6WL7M^Z3_ .)I.Q5D3:C^TYJ*(-E[

M'U_YY)Z?[M0I(R<3@]6_:7ULJ3'=HQAEQC]VAZX'=:!=0BW?\

M7&/_ .(I"Y3?T7]J_4 H=]0BX;.?)3H,?[% 2?_$47

M%8[2V_;$2;._5(/;]VH_]DIDV/:-$_:GLKDMYFI0<8Q\@]_]FF%CWZU^.6CN

MH*W\)) )_P XIA8OQ_&;39C@7L1_#_ZU K&K:_%[2Y"%-Y%GT_R*0['46WCJ

MQN4#I<(0>A_R*!&K:>(X+O!212">W_ZJ8C)_B-IWAI)/-

MO+2*1(RX629%/0X)!8'%)E6/BWXI_M>?V*[1V5WIDBFW+?ZQ7^;YACB7V'%3

M9LVA"ZN? 'C3]K+6=:9.;,X4CY4/?_MH:M)%*9\ZW?CF[O,;PG&O8<<4N:^X!

MP-PS^59MV>A3BEM^9B?:9,<#]*N4[D+S(!J,MMT ]>17,F^HI0708_B><]-I

M_#_Z]-1)V''QE>C[RJ/^ G_&AEIFTWBVXF4 [/R_^O67*,?_ ,)/,X ^7\O_

M *]:J0-=CM=.\0!XD$CH..>0/ZU7,3J2:H8+^W;#J6;' 8=B.U.X79YO+X?\

MR3(5R/4#_P"M1<+L=-I\EH"BHVPCDX/?KS3"YFIIKM]Q&([D F@+$[:>T7\+

M?E_]:@FQT4/BF:PSC9SZCT_&F.QV6F_&[5X3@+#@# _=G_XJG<+&_#^T-K-J

M:]:6R(/L>0#P

M8SGK_P!=*8N4]D\"_M?ZW*(O.:R5=QW$H1@9/QQ(OM_P!-*+BY3TS3_CG83@[[ZQ_[

M_1__ !=%Q6/2++X@6%UG%Y;'&.DJ?_%4"L=A#JD,WW9$/T8'^M,196<-W% $

MX;- QU(!>,I)7DA@4O#LPA;I@^

MK'GFJ9=CY,O[IM7^=Q@@;<#\^_UHN-.QB):#^(D5FHBY;EB=NF.:&A&>X-QP

M1C%:*5B5&P2VJVZA@>36:=BFKF?RY('/THYAG6Z)HRS,K.64$'/;^=/VA2AU

M-?4+C[ &A3#*,8/UY[5BU=E2>ECCW'VF4,W'2JV,DK.Y=G;R.$^88K/E-G[P

M6UF;X$N"O;I_C3F[BL5KK0HK+&')SZX[4*1-C#OB& P:5A,E=EC4

MYMVFM#44(8J,G;P?_KT7!(V[&.*U1@K@Y]QZ4[E6*11;CJW3WI7#E.#@@_M#

M._*XZ?C]:HFQWMCX=@/_ "T/3U% [%VY\'VTJC$ISGU6JL.4KHHQ^$(F.W>^

M/7C_ IV.=D,?A>)9O++L%]>/3/I3L:1=C5F@72D,41W@=#USGGM3L3*5S/3

MQ#+9C;L'KSFI:'$W-)^(D^G(55(SDYYSZ?6E8LTX/BY=Q?\ +&+_ ,>_QHL'

M*>C:=^U7J>F[MMK;'=CKYG;_ (%2#D/KCX;_ +8VH:P[I/;V<06-2#N<9.<=

MWID.F?9GACX[1:H%\R2T7,88XE'7CCEO>GX(H$6PX;O0,=2 7-,!U A0<4 .!S0 O2@!P:@!U "@XH =

M0 M !0 4 % "@XH >.: "@ H * "@!RF@!U !0 4 % !0 4 % !0 4 % !0

M4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 %

M!0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4 % !0 4

M % !0 4 % !0 4 % !0 4 % !0 4 -W4 )NH 2@ H * "@ H * "@ H * "@

M S0 F: #- ";J #=0 FZ@ W4 &Z@ W4 &Z@!=U !NH 7=0 9H ,T +0 4 %

M!0 4 % !0 4 % !0 N: %#4 .H * "@ H * "@ H * "@ H * "@ H * "@

MH * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H *

M"@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H

M * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "

M@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@ H * "@!A- "4 % !

M0 4 -)H ;0 4 % !0 4 ,)H 2@!I- #: &DT -H 8W- "8Q0,3.:!#6XH \;

M\<_$T^&$D(@$FQPOW\9]_NFM%&YT0I?TI6%8M7T/V( YSF@#B[Z\]N]2!V?AS01&5N-

M_P!],[<=,X/7- TCH+J?SLP8Q[_3GI4FAR]]+]B+#KC'ZT$LT=/T,:U;FX+[

M3R,8ST]\B@2)K'11:+NW9P<]/3\:3-$3W.J%!]WMZU V>=7UU]IQQC&:=C$J

M?V?Y7?\ 2J"QD2VN>](FQ$UGQUIH317^R9.,TQN<JFV&-N?QI#N:6FZR9MWR],=Z3*4KFQ?ZF

M1CY?7O30VS-L=5+L?E[>M41M*Y;-NW\7F$C]V#C_:_^M5)F

M9G:GXL-V&3RP,XYW?0^E5<95L-?,&/D!P?7_ .M5$LV=W]O,"?DW$+Z_CV]:

M>XKFQ%X&!Y\T\?[/_P!>CE&.NO#HM\?.3GV_^O18M,RKC3/LF/FSGVI-%7.=

MN;WS.,=*EH:9*MQ]C ?&<\8J1L^F?@[\36TZXB00 [82,[\=A_LTC-H_6;X2

M_$!M2L[7,(7 |