As filed with the U.S. Securities and Exchange Commission on June 28, 2024.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Ostin Technology Group Co., Ltd.

(Exact name of registrant as specified in its charter)

| Cayman Islands | Not Applicable | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

Building 2, 101

1 Kechuang Road

Qixia District, Nanjing

Jiangsu Province, China 210046

Tel: +86 (25) 58595234

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Cogency Global Inc.

122 East 42nd Street, 18th Floor

New York, NY 10168

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With a Copy to:

William S. Rosenstadt, Esq.

Mengyi “Jason” Ye, Esq.

Ortoli Rosenstadt LLP

366 Madison Avenue, 3rd Floor

New York, NY 10017

+1-212-588-0022 - telephone

+1-212-826-9307 - facsimile

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement is declared effective.

| If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. | ☒ |

| If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. | ☐ |

| If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. | ☐ |

| If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. | ☐ |

| Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933. |

| Emerging growth company | ☒ |

| If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. | ☐ |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to such Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. Neither we nor the selling shareholder may sell these securities until the registration statement filed with the U.S. Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION, DATED [●], 2024 |

Up to 2,800,000 Class A Ordinary Shares

Ostin Technology Group Co., Ltd.

This prospectus relates to the offer and resale, by the selling shareholder identified in this prospectus, of up to an aggregate of 2,800,000 class A ordinary shares, par value US$0.0001 per share (the “Class A Ordinary Shares”), of Ostin Technology Group Co., Ltd. (“Ostin”). The Class A Ordinary Shares were sold by Ostin in a private placement pursuant to certain subscription agreement dated January 31, 2024.

The selling shareholder is identified in the table commencing on page 34 of this prospectus. No Class A Ordinary Shares are being registered hereunder for sale by us. We will not receive any proceeds from the sale of the Class A Ordinary Shares by the selling shareholder. All net proceeds from the sale of the Class A Ordinary Shares covered by this prospectus will go to the selling shareholder. See “Use of Proceeds.” Information regarding the selling shareholder, the amounts of Class A Ordinary Shares that may be sold by it, and the times and manner in which it may offer and sell the Class A Ordinary Shares under this prospectus is provided under the sections titled “Selling Shareholder” and “Plan of Distribution,” respectively, in this prospectus. We do not know when or in what amount the selling shareholder may offer the Class A Ordinary Shares for sale. The selling shareholder may sell any, all, or none of the Class A Ordinary Shares offered by this prospectus.

Our authorized share capital is a dual class structure consisting of Class A Ordinary Shares and class B ordinary shares of a par value of US$0.0001 each (“Class B Ordinary Shares”). Holders of Class A Ordinary Shares and Class B Ordinary Shares shall vote together as one class on all resolutions of the shareholders and have the same rights except each Class A Ordinary Share shall entitle its holder to one (1) vote and each Class B Ordinary Share shall entitle its holder to twenty (20) votes. The Class B Ordinary Shares would not be convertible into Class A Ordinary Shares or any other equity securities authorized to be issued by the Company.

Our Class A Ordinary Shares are listed on The Nasdaq Capital Market, or Nasdaq, under the symbol “OST.” On June 27, 2024, the last reported sale price of our Class A Ordinary Shares on Nasdaq was US$0.418 per share.

We received a written notification from the Nasdaq Stock Market LLC (the “Nasdaq”) on January 19, 2024, notifying us that we are not in compliance with the minimum bid price requirement set forth in the Nasdaq rules for continued listing on the Nasdaq (the “Minimum Bid Price Requirement”). To regain compliance, Ostin’s Class A Ordinary Shares must have a closing bid price of at least US$1.00 for a minimum of 10 consecutive trading days by July 17, 2024. We are currently preparing to request for an additional 180 calendar day grace period to regain compliance. For more information, see “Item 3. Key Information-D. Risk Factors- Risks Related to Ostin’s Class A Ordinary Shares – The market price of Ostin’s Class A Ordinary Shares has recently declined significantly, and Ostin’s Class A Ordinary Shares could be delisted from the Nasdaq or trading could be suspended.” in our annual report on Form 20-F for the fiscal year ended September 30, 2023 (the “2023 Annual Report”), which is incorporated herein by reference, and on page 30 of this prospectus.

The principal executive office of Ostin is located at Building 2, 101, 1 Kechuang Road, Qixia District, Nanjing, Jiangsu Province, China 210046, and its telephone number is +86 (25) 58595234. The registered address of Ostin is located at the offices of Maples Corporate Services Limited, PO Box 309, Ugland House, Grand Cayman, KY1-1104, Cayman Islands.

In this prospectus, “we,” “us,” “our,” “our company,” the “Company,” or similar terms refer to Ostin Technology Group Co., Ltd. and/or its consolidated subsidiaries. Investors are purchasing an interest in Ostin, the Cayman Islands holding company. Investing in Ostin’s securities is highly speculative and involves a significant degree of risk. The risks could result in a material change in the value of the securities we are registering for sale or could significantly limit or completely hinder our ability to offer or continue to offer securities to investors. Ostin’s Class A Ordinary Shares offered in this prospectus are shares of our Cayman Islands holding company, which has no material operations of its own, and conducts substantially all of its operations through the operating entities established in the People’s Republic of China, or the PRC, primarily Jiangsu Austin Optronics Technology Co., Ltd. (“Jiangsu Austin”), our majority owned subsidiary and its subsidiaries. For a description of our corporate structure, see “Corporate Structure” on page 2 of this prospectus. See also “Risk Factors” on page 16.

As a Cayman Islands holding company with operations primarily conducted by its subsidiaries based in China, Ostin and its subsidiaries are subject to complex and evolving PRC laws and regulations and face various legal and operational risks and uncertainties relating to doing business in China. For example, Ostin and its subsidiaries in the PRC face risks associated with regulatory approvals on offshore offerings, anti-monopoly regulatory actions, and oversight on cybersecurity and data privacy, as well as the lack of inspection on our auditors by the PCAOB, which may impact our ability to conduct certain businesses, accept foreign investments, or list and conduct offerings on a United States or other foreign exchange. These risks could result in a material adverse change in our operations and the value of Ostin’s Class A Ordinary Shares, significantly limit or completely hinder our ability to continue to offer securities to investors, or cause the value of such securities to significantly decline. For a detailed description of risks relating to doing business in China, please refer to risks disclosed under “Risk Factors-Risks Related to Doing Business in China” on page 16 of this prospectus.

PRC government’s significant authority in regulating our operations and its oversight and control over offerings conducted overseas by, and foreign investment in, China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors. Implementation of industry-wide regulations, including data security or anti-monopoly related regulations, in this nature may cause the value of such securities to significantly decline. We are not operating in an industry that prohibits or limits foreign investment. As a result, as advised by our PRC counsel, King & Wood Mallesons, other than those requisite for a domestic company in China to engage in the businesses similar to ours, we are not required to obtain any permission from Chinese authorities, including the CSRC, the Cyberspace Administration of China (the “CAC”) or any other governmental agency that is required to approve our operations. However, if we do not receive or maintain the approvals, or we inadvertently conclude that such approvals are not required, or applicable laws, regulations, or interpretations change such that we are required to obtain approval in the future, we may be subject to investigations by competent regulators, fines or penalties, ordered to suspend our relevant operations and rectify any non-compliance, prohibited from engaging in relevant business or conducting any offering, and these risks could result in a material adverse change in our operations, significantly limit or completely hinder our ability to offer or continue to offer securities to investors, or cause such securities to significantly decline in value or become worthless. For more details, see “Risk Factors-Risks Related to Doing Business in China- The PRC government exerts substantial influence over the manner in which we conduct our business activities. The PRC government may also intervene or influence our operations at any time, which could result in a material change in our operations and Ostin’s Class A Ordinary Shares could decline in value or become worthless.” on page 20.

Risks and uncertainties arising from the legal system in China, including risks and uncertainties regarding the enforcement of laws and quickly evolving rules and regulations in China, could result in a material adverse change in our operations and the value of Ostin’s Class A Ordinary Shares. On February 17, 2023, the China Securities Regulatory Commission (the “CSRC”) promulgated Trial Administrative Measures of the Overseas Securities Offering and Listing by Domestic Companies and relevant five guidelines (collectively, the “Overseas Listing Trial Measures”), which became effective on March 31, 2023. The Overseas Listing Trial Measures comprehensively improve and reform the existing regulatory regime for overseas offering and listing of mainland China domestic companies’ securities and regulates both direct and indirect overseas offering and listing of mainland China domestic companies’ securities by adopting a filing-based regulatory regime. According to the Overseas Listing Trial Measures, (i) mainland China domestic companies that seek to offer or list securities overseas, both directly and indirectly, should fulfill the filing procedure and report relevant information to the CSRC; if a mainland China domestic company fails to complete the filing procedure or conceals any material fact or falsifies any major content in its filing documents, such mainland China domestic company may be subject to administrative penalties, such as order to rectify, warnings, fines, and its controlling shareholders, actual controllers, the person directly in charge and other directly liable persons may also be subject to administrative penalties, such as warnings and fines; (ii) if the issuer meets both of the following conditions, the overseas offering and listing shall be determined as an indirect overseas offering and listing by a mainland China domestic company: (a) any of the total assets, net assets, revenues or profits of the domestic operating entities of the issuer in the most recent accounting year accounts for more than 50% of the corresponding figure in the issuer’s audited consolidated financial statements for the same period; (b) its major operational activities are carried out in mainland China or its main places of business are located in mainland China, or the senior managers in charge of operation and management of the issuer are mostly PRC citizens or have their usual place(s) of residence located in mainland China. The Overseas Listing Trial Measures require subsequent reports to be filed with the CSRC on material events, such as change of control or voluntary or forced delisting of the issuers who have completed overseas offerings and listings. In addition, an overseas-listed company must also submit the filing with respect to its follow-on offerings, issuance of convertible corporate bonds and exchangeable bonds, and other equivalent offering activities, within the time frame specified by the Overseas Listing Trial Measures. However, if we do not maintain the permissions and approvals of the filing procedure in a timely manner under PRC laws and regulations, we may be subject to investigations by competent regulators, fines or penalties, ordered to suspend our relevant operations and rectify any non-compliance, prohibited from engaging in relevant business or conducting any offering, and these risks could result in a material adverse change in our operations, limit our ability to offer or continue to offer securities to investors, or cause such securities to significantly decline in value or become worthless. As the Overseas Listing Trial Measures were newly published, there exists uncertainty with respect to the filing requirements and their implementation. Any failure or perceived failure of us to fully comply with such new regulatory requirements could significantly limit or completely hinder our ability to offer or continue to offer securities to investors, cause significant disruption to our business operations, and severely damage our reputation, which could materially and adversely affect our financial condition and results of operations and could cause the value of Ostin’s securities to significantly decline or be worthless. For more details, see “Risk Factors-Risks Related to Doing Business in China- There are uncertainties regarding the interpretation and enforcement of PRC laws, rules and regulations.” on page 17.

Furthermore, as more stringent criteria have been imposed by the SEC and the Public Company Accounting Oversight Board (the “PCAOB”) recently, Ostin’s securities may be prohibited from trading if our auditor cannot be fully inspected. On December 16, 2021, the PCAOB issued its determination that the PCAOB is unable to inspect or investigate completely PCAOB-registered public accounting firms headquartered in mainland China and in Hong Kong, because of positions taken by PRC authorities in those jurisdictions, and the PCAOB included in the report of its determination a list of the accounting firms that are headquartered in mainland China or Hong Kong. This list does not include our auditor, TPS Thayer, LLC. On August 26, 2022, the PCAOB announced that it had signed a Statement of Protocol (the “Statement of Protocol”) with the CSRC and the Ministry of Finance of China (“MOF”). The terms of the Statement of Protocol would grant the PCAOB complete access to audit work papers and other information so that it may inspect and investigate PCAOB-registered accounting firms headquartered in mainland China and Hong Kong. On December 15, 2022, the PCAOB announced that it has secured complete access to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong and voted to vacate the previous 2021 determination report to the contrary. On December 29, 2022, a legislation entitled “Consolidated Appropriations Act, 2023” (the “Consolidated Appropriations Act”) was signed into law by President Biden. The Consolidated Appropriations Act contained, among other things, an identical provision to the Accelerating Holding Foreign Companies Accountable Act, which reduces the number of consecutive non-inspection years required for triggering the prohibitions under the Holding Foreign Companies Accountable Act from three years to two. As a result of the Consolidated Appropriations Act, the Holding Foreign Companies Accountable Act (the “HFCA Act”) now also applies if the PCAOB’s inability to inspect or investigate the relevant accounting firm is due to a position taken by an authority in any foreign jurisdiction. The denying jurisdiction does not need to be where the accounting firm is located. Our current auditor, TPS Thayer, LLC, as an auditor of companies that are traded publicly in the United States and a firm registered with the PCAOB, is subject to laws in the United States pursuant to which the PCAOB conducts regular inspections to assess its compliance with the applicable professional standards. Notwithstanding the foregoing, in the future, if there is any regulatory change or step taken by PRC regulators that does not permit our auditor to provide audit documentations located in China to the PCAOB for inspection or investigation, investors may be deprived of the benefits of such inspection. Any audit reports not issued by auditors that are completely inspected by the PCAOB, or a lack of PCAOB inspections of audit work undertaken in China that prevents the PCAOB from regularly evaluating our auditors’ audits and their quality control procedures, could result in a lack of assurance that our financial statements and disclosures are adequate and accurate, then such lack of inspection could cause Ostin’s securities to be delisted from the stock exchange. See “Risk Factors-Risks Related to Doing Business in China - Ostin’s Class A Ordinary Shares may be delisted under the Holding Foreign Companies Accountable Act if the PCAOB is unable to inspect our auditors. The delisting of Ostin’s Class A Ordinary Shares, or the threat of their being delisted, may materially and adversely affect the value of your investment.” on page 28.

Ostin is a holding company with no operations of its own. We conduct substantially all of our operations through our subsidiaries in China. As a result, although other means are available for us to obtain financing at the holding company level, Ostin’s ability to pay dividends to its shareholders and to service any debt it may incur may depend upon dividends paid by our PRC subsidiaries. If any of our PRC subsidiaries incurs debt on its own behalf in the future, the instruments governing such debt may restrict our PRC subsidiaries’ ability to pay dividends to Ostin. In addition, our PRC subsidiaries are permitted to pay dividends to Ostin only out of their retained earnings, if any, as determined in accordance with PRC accounting standards and regulations. Further, our PRC subsidiaries are required to make appropriations to certain statutory reserve funds or may make appropriations to certain discretionary funds, which are not distributable as cash dividends except in the event of a solvent liquidation of the companies. For more details, see “Item 5. Operating and Financial Review and Prospects-B. Liquidity and Capital Resources-Holding Company Structure.” in our 2023 Annual Report, which is incorporated herein by reference.

Under PRC laws and regulations, our PRC subsidiaries are subject to certain restrictions with respect to paying dividends or otherwise transferring any of their net assets to us. Remittance of dividends by a wholly foreign-owned enterprise out of China is also subject to examination by the banks designated by the State Administration of Foreign Exchange, or SAFE. The amounts restricted include the paid-up capital and the statutory reserve funds of our PRC subsidiaries, totalled $24,753,990, $24,752,533 and $11,889,822 as of September 30, 2023, 2022 and 2021, respectively.

Furthermore, cash transfers from our PRC subsidiaries to entities outside of China are subject to PRC government controls on currency conversion. To the extent cash in our business is in the PRC or a PRC entity, such cash may not be available to fund operations or for other use outside of the PRC due to restrictions and limitations imposed by the governmental authorities on the ability of us or our PRC subsidiaries to transfer cash outside of the PRC. Shortages in the availability of foreign currency may temporarily delay the ability of our PRC subsidiaries to remit sufficient foreign currency to pay dividends or other payments to us, or otherwise satisfy their foreign currency denominated obligations. In view of the foregoing, to the extent cash in our business is held in China or by a PRC entity, such cash may not be available to fund operations or for other use outside of the PRC. For risks relating to the fund flows of our operations in China, see “Risk Factors-Risks Related to Doing Business in China-We rely on dividends and other distributions on equity paid by our subsidiaries to fund offshore cash and financing requirements and any limitation on the ability of our PRC subsidiaries to transfer cash out of China and/or make remittance to pay dividends to us could limit our ability to access cash generated by the operations of those entities” on page 26 and “- PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay us from using the proceeds of our initial public offering and future financings to make loans or additional capital contributions to our PRC subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand our business.” on page 25.

Under PRC law, Ostin may provide funding to our PRC subsidiaries only through capital contributions or loans, subject to satisfaction of applicable government registration and approval requirements. For the fiscal years ended September 30, 2023, 2022, and 2021, Ostin provided funding to our PRC subsidiaries of $0, $4,078,600 and $0, respectively.

In addition, funds are transferred among our PRC subsidiaries for working capital purposes, primarily between Jiangsu Austin, our main operating subsidiary and its subsidiaries. The following table provides a summary of the distributions and working capital funds transferred between Jiangsu Austin and its subsidiaries:

| Fiscal Years Ended September 30, | ||||||||||||

| 2023 | 2022 | 2021 | ||||||||||

| Cash transferred to its subsidiaries from Jiangsu Austin | $ | 8,617,106 | $ | 9,096,665 | $ | - | ||||||

| Cash transferred to Jiangsu Austin from its subsidiaries | $ | - | $ | - | $ | 7,640,965 | ||||||

The transfer of funds among companies are subject to the Provisions of the Supreme People’s Court on Several Issues Concerning the Application of Law in the Trial of Private Lending Cases (2020 Second Amendment, the “Provisions on Private Lending Cases”), which was implemented on January 1, 2021 to regulate the financing activities between natural persons, legal persons and unincorporated organizations. The Provisions on Private Lending Cases set forth that private lending contracts will be upheld as invalid under the circumstance that (i) the lender swindles loans from financial institutions for relending; (ii) the lender relends the funds obtained by means of a loan from another profit-making legal person, raising funds from its employees, illegally taking deposits from the public; (iii) the lender who has not obtained the lending qualification according to the law lends money to any unspecified object of the society for the purpose of making profits; (iv) the lender lends funds to a borrower when the lender knows or should have known that the borrower intended to use the borrowed funds for illegal or criminal purposes; (v) the lending is violations of public orders or good morals; or (vi) the lending is in violations of mandatory provisions of laws or administrative regulations. As advised by our PRC counsel, King & Wood Mallesons, the Provisions on Private Lending Cases does not prohibit using cash generated from one subsidiary to fund another subsidiary’s operations. We have not been notified of any other restriction which could limit our PRC subsidiaries’ ability to transfer cash between subsidiaries. See “Item 4. Information on the Company - B. Business Overview - Regulation - Regulations Relating to Private Lending.” in our 2023 Annual Report, which is incorporated herein by reference.

Our majority owned subsidiary, Jiangsu Austin, has maintained cash management policies which dictate the purpose, amount and procedure of cash transfers between Jiangsu Austin and its subsidiaries. Cash transferred to Jiangsu Austin’s subsidiaries of less than RMB5 million (US$0.69 million) must be reported to and reviewed by Jiangsu Austin’s financial department and the relevant PRC subsidiary’s chief executive officer, and must be approved by the Chief Financial Officer and Chairman of Jiangsu Austin. Cash transfer in excess of RMB5 million (US$0.69 million) but less than RMB20 million (US$2.74 million), and less than 50% of Jiangsu Austin’s consolidated total assets must be approved by the board of directors of Jiangsu Austin. Cash transfer in excess of RMB20 million (US$2.74 million), or more than 50% of Jiangsu Austin’s consolidated total assets must be approved by shareholders of Jiangsu Austin. Jiangsu Austin conducts regular review and management of all its subsidiaries’ cash transfers and reports to its Risk Management Department and board of directors.

We are an “emerging growth company” as that term is used in the Jumpstart Our Business Startups Act of 2012, as amended, or the “JOBS Act,” and, as such, we have elected to comply with certain reduced public company reporting requirements. See “Prospectus Summary-Implications of Being an Emerging Growth Company” on page 7 of this prospectus.

Investing in our Class A Ordinary Shares involves a high degree of risk, including the risk of losing your entire investment. See “Risk Factors” beginning on page 16 of this prospectus and in the documents incorporated by reference into this prospectus to read about factors you should consider before buying our Class A Ordinary Shares.

Neither the Securities and Exchange Commission nor any state securities commission nor any other regulatory body has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2024.

TABLE OF CONTENTS

i

This prospectus is part of a registration statement on Form F-1 that we filed with the U.S. Securities and Exchange Commission (the “SEC”). As permitted by the rules and regulations of the SEC, the registration statement filed by us includes additional information not contained in this prospectus. You may read the registration statement and the other reports we file with the SEC at the SEC’s website described below under the heading “Where You Can Find Additional Information.”

You should rely only on the information that is contained in this prospectus or that is incorporated by reference into this prospectus. We have not authorized anyone to provide you with information that is in addition to or different from what is contained in, or incorporated by reference into, this prospectus. If anyone provides you with different or inconsistent information, you should not rely on it.

We are not offering to sell or solicit any securities other than the Class A Ordinary Shares offered by this prospectus. In addition, we are not offering to sell or solicit any securities to or from any person in any jurisdiction where it is unlawful to make this offer to or solicit an offer from a person in that jurisdiction. The information contained in this prospectus is accurate as of the date on the front of this prospectus only, regardless of the time of delivery of this prospectus or of any sale of our Class A Ordinary Shares. Our business, financial condition, results of operations and prospects may have changed since that date.

This prospectus contains summaries of certain provisions contained in some of the documents described herein, but reference is made to the actual documents for complete information. All of the summaries are qualified in their entirety by the actual documents. Copies of some of the documents referred to herein have been filed, will be filed or will be incorporated herein by reference as exhibits to the registration statement, and you may obtain copies of those documents as described below under the section entitled “Where You Can Find Additional Information.”

Our financial statements are prepared and presented in accordance with U.S. GAAP. Our historical results do not necessarily indicate our expected results for any future periods.

We have not taken any action to permit a public offering of the securities outside the United States or to permit the possession or distribution of this prospectus outside the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about and observe any restrictions relating to the offering of the securities and the distribution of this prospectus outside of the United States.

ii

COMMONLY USED DEFINED TERMS

Unless otherwise indicated or the context requires otherwise, references in this prospectus to:

| ● | “AMOLED” refers to active-matrix organic light emitting diode, which is an organic light emitting diode display technology; |

| ● | “CAC” refers to the Cyberspace Administration of China; |

| ● | “China” or the “PRC”, in each case, refers to the People’s Republic of China, including Hong Kong and Macau. The term “Chinese” has a correlative meaning for the purpose of this prospectus; |

| ● | “Class A Ordinary Shares” refers to Ostin’s class A ordinary shares, par value US$0.0001 per share, each with one vote per share; |

| ● | “Class B Ordinary Shares” refers to Ostin’s class B ordinary shares, par value US$0.0001 per share, each with 20 vote per share; |

| ● | “CSRC” refers to the China Securities Regulatory Commission; |

| ● | “Exchange Act” refers to the Securities Exchange Act of 1934, as amended; |

| ● | “FINRA” refers to the Financial Industry Regulatory Authority, Inc.; |

| ● | “HK$,” “HKD,” or “Hong Kong dollars” refers to the legal currency of the Hong Kong Special Administrative Region; |

| ● | “Hong Kong” refers to the Hong Kong Special Administrative Region; |

| ● | “IoT” refers to Internet of Things; | |

| ● | “Jiangsu Austin” refers to Jiangsu Austin Optronics Technology Co., Ltd., our majority owned subsidiary, which is a company limited by shares incorporated in China; |

iii

| ● | “JOBS Act” refers to the Jumpstart Our Business Startups Act, enacted in April 2012; | |

| ● | “MOFCOM” refers to China’s Ministry of Commerce; | |

| ● | “Nasdaq” refers to Nasdaq Stock Market LLC; | |

| ● | “OLED” refers to organic light emitting diode, a light emitting display technology; |

| ● | “Ostin” refers to Ostin Technology Group Co., Ltd., a Cayman Islands exempted company, and “we,” “us,” “our company,” the “Company,” “our,” or similar terms used in this prospectus refer to Ostin Technology Group Co., Ltd. and/or its consolidated subsidiaries, unless the context otherwise indicates; |

| ● | “PCAOB” refers to the Public Company Accounting Oversight Board of the United States; | |

| ● | “polarizer” refers to polarizing film, a composite optical film used in LCD/OLED/AMOLED displays |

| ● | “RMB” or “Renminbi” refer to the legal currency of the People’s Republic of China; |

| ● | “SAFE” refers to China’s State Administration of Foreign Exchange; |

| ● | “SAT” refers to China’s State Administration of Taxation; |

| ● | “SEC” refers to the United States Securities and Exchange Commission; |

| ● | “Securities Act” refers to the Securities Act of 1933, as amended; |

| ● | “share capital” or similar expressions include a reference to shares in a company that does not have a share capital under its governing law, but which is authorized to issue a maximum or unlimited number of shares; |

| ● | “TFT-LCD” refers to Thin-film transistor liquid crystal display, a display technology; |

| ● | “US$,” “$,” “dollars,” “USD” or “U.S. dollars” refer to the legal currency of the United States; and |

| ● | “U.S. GAAP” refers to the generally accepted accounting principles in the United States. |

This prospectus contains information and statistics relating to China’s economy and the industries in which Ostin operates through its operating entities in China derived from various publications issued by market research companies and PRC governmental entities, which have not been independently verified by us. The information in such sources may not be consistent with other information compiled in or outside of China.

Unless otherwise noted, all other financial and other data related to the Company in this prospectus is presented in U.S. dollars. We present our financial results in RMB. We make no representation that any RMB or U.S. dollar amounts could have been, or could be, converted into U.S. dollars or RMB, as the case may be, at any particular rate, or at all. The PRC government imposes control over its foreign currency reserves in part through direct regulation of the conversion of RMB into foreign exchange and through restrictions on foreign trade. This prospectus contains translations of certain foreign currency amounts into U.S. dollars for the convenience of the reader. Unless otherwise stated, all translations of Renminbi into U.S. dollars in this prospectus were made at the rate at RMB7.2960 to US $1.00, the rate published by the Federal Reserve Board on September 29, 2023.

Our fiscal year end is September 30. References to a particular “fiscal year” are to our fiscal year ended September 30 of that calendar year. Our audited consolidated financial statements have been prepared in accordance with the U.S. GAAP.

iv

Investors in Ostin’s securities are not purchasing an equity interest in our operating entities in China but instead are purchasing an equity interest in a Cayman Islands holding company.

This summary highlights selected information that is presented in greater detail elsewhere, or incorporated by reference, in this prospectus. It does not contain all of the information that may be important to you and your investment decision. Before investing in the securities that we are offering, you should carefully read this entire prospectus, including the matters set forth under the section of this prospectus captioned “Risk Factors,” “Special Note Regarding Forward-Looking Statements” and the financial statements and related notes and other information that we incorporate by reference herein, including, but not limited to, our 2023 Annual Report and other SEC reports.

Overview

Ostin is an exempted company incorporated in the Cayman Islands. As a holding company with no material operations of its own, Ostin conducts substantially all of its operations through its operating entities established in the PRC, primarily Jiangsu Austin and its subsidiaries. Ostin and its subsidiaries are subject to complex and evolving PRC laws and regulations and face various legal and operational risks and uncertainties relating to doing business in China. For example, Ostin and its subsidiaries in the PRC face risks associated with regulatory approvals on offshore offerings, anti-monopoly regulatory actions, and oversight on cybersecurity and data privacy, as well as the lack of inspection on our auditors by the PCAOB, which may impact our ability to conduct certain businesses, accept foreign investments, or list and conduct offerings on a United States or other foreign exchange. These risks could result in a material adverse change in our operations and the value of Ostin’s Class A Ordinary Shares, significantly limit or completely hinder our ability to continue to offer securities to investors, or cause the value of such securities to significantly decline. For a detailed description of risks relating to doing business in China, please refer to risks disclosed under “Item 3. Key Information-D. Risk Factors-Risks Relating to Doing Business in China.” in our 2023 Annual Report, which is incorporated herein by reference.

PRC government’s significant authority in regulating our operations and its oversight and control over offerings conducted overseas by, and foreign investment in, China-based issuers could significantly limit or completely hinder our ability to offer or continue to offer securities to investors. Implementation of industry-wide regulations, including data security or anti-monopoly related regulations, in this nature may cause the value of such securities to significantly decline. For more details, see “Item 3. Key Information-D. Risk Factors-Risks Relating to Doing Business in China- The PRC government exerts substantial influence over the manner in which we conduct our business activities. The PRC government may also intervene or influence our operations at any time, which could result in a material change in our operations and Ostin’s Class A Ordinary Shares could decline in value or become worthless.” in our 2023 Annual Report, which is incorporated herein by reference.

Risks and uncertainties arising from the legal system in China, including risks and uncertainties regarding the enforcement of laws and quickly evolving rules and regulations in China, could result in a material adverse change in our operations and the value of Ostin’s Class A Ordinary Shares. For more details, see “Item 3. Key Information-D. Risk Factors-Risks Relating to Doing Business in China- There are uncertainties regarding the interpretation and enforcement of PRC laws, rules and regulations.” in our 2023 Annual Report, which is incorporated herein by reference.

1

We are a supplier of display modules and polarizers in China. We design, develop and manufacture TFT-LCD modules in a wide range of sizes and customized sizes according to the specifications of our customers. Our display modules are mainly used in consumer electronics, commercial LCD displays and automotive displays. We also manufacture polarizers used in the TFT-LCD display modules and are in the process of developing protective films for the OLED display panel. Furthermore, we are currently in the process of developing our new IoT display products, including our all-in-one intelligent conference system and Pintura wireless photo transmission system which was launched in China since September 2022.

We were formed in 2010 by a group of individuals with industry expertise and have been operating our business, primarily through Jiangsu Austin and its subsidiaries. We currently operate one headquarter and three manufacturing facilities in China with an aggregate of 50,335 square meters - the headquarter is located in Jiangsu Province, one factory is located in Jiangsu Province for the manufacture of display modules, one in Chengdu, Sichuan Province for the manufacture of TFT-LCD polarizers and one in Luzhou, Sichuan Province, for manufacture of display modules which are primarily used in display devices for education, healthcare, transportation, businesses and offices.

We seek to improve our market position through our close collaborative customer relationships and a focus on the development of high-end display products and new display materials. Our customers include many of the leading manufacturers of computers, automotive electronics and LCD displays primarily in China. We have also successfully introduced our polarizers to many companies in China and have witnessed a significant revenue since we commenced the production and sales of polarizers in 2019, and expanded our product lines to include polarizers used for both vertical alignment (VA) panels and in-plane switching (IPS) panels in 2020.

Our dedication to technology and innovation has helped us win the high new-tech enterprise designation in Jiangsu Province, China, which entitles Jiangsu Austin, our main operating entity in China, to a preferential tax rate of 15% and numerous other recognitions, including but not limited to, Jiangsu Provincial Credit Enterprise and Key Optoelectronic Product Laboratory, which are endorsements to our credit and research and development capabilities. During the fiscal years ended September 30, 2023, 2022 and 2021, our revenues were $57,525,700, $105,416,746, and $167,744,801, respectively, and net income/(loss) were $(10,787,269), $112,227 and $3,295,507, respectively.

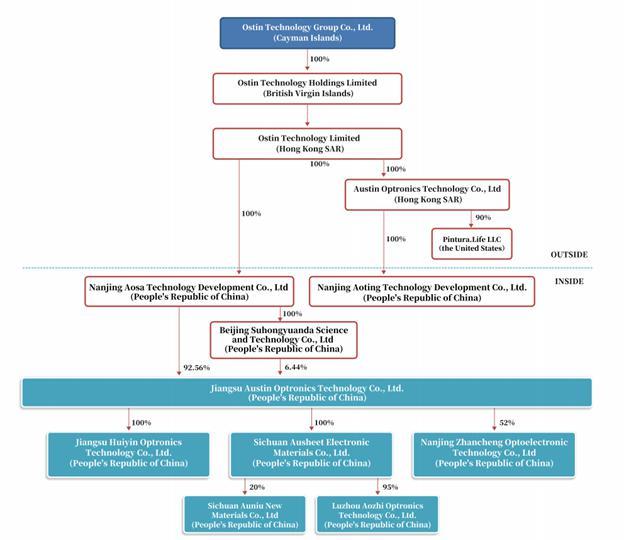

Corporate Structure

Ostin is a Cayman Islands exempted company structured as a holding company and conducts its operations in China through Jiangsu Austin and its subsidiaries. We first started our business through Jiangsu Austin, which was formed in December 2010. With the growth of our business and in order to facilitate international capital investment in us, we started a reorganization as described below involving new offshore and onshore entities in the fourth quarter of 2019 and completed it in the first half of 2020.

On September 26, 2019, Ostin was incorporated under the laws of the Cayman Islands as an exempted company. Further, Ostin Technology Holdings Limited and Ostin Technology Limited, were established in the British Virgin Islands in October 2019 and in Hong Kong in October 2019, respectively, as intermediate holding companies.

In March 2020, Nanjing Aosa Technology Development Co., Ltd., our wholly owned subsidiary (“Nanjing Aosa”) was formed as a limited liability company in China and became a wholly owned subsidiary of Ostin Technology Limited in June 2020. Beijing Suhongyuanda Science and Technology Co., Ltd. (“Suhong Yuanda”) was formed as a limited liability company in September 2019 in China and became a wholly owned subsidiary of Nanjing Aosa in May 2020, holding 9.97% of the shares of Jiangsu Austin.

2

In June 2020, Nanjing Aosa entered into the variable interest entity arrangements (the “VIE Arrangements”) with shareholders of Jiangsu Austin who were directors, supervisors or senior management members of Jiangsu Austin, and other shareholders (excluding Suhong Yuanda and collectively, the “VIE Shareholders”) holding an aggregate of 87.88% of the shares of Jiangsu Austin, which, along with our company’s direct ownership of 9.97% of Jiangsu Austin, enables us to obtain control over Jiangsu Austin through Nanjing Aosa. As a result of the VIE Arrangements, before Jiangsu Austin became our majority owned subsidiary as described below, we were regarded as the primary beneficiary of Jiangsu Austin for accounting purposes, and we consolidated the financial results of Jiangsu Austin and its subsidiaries in our financial statements in accordance with U.S. GAAP.

In April 2021, Nanjing Aosa and Jiangsu Austin unwound part of the VIE Arrangements with the minority shareholders of Jiangsu Austin who were not directors, supervisors or senior management members of Austin (the “non-management VIE Shareholders”) and whose shares of Jiangsu Austin were no longer subject to the limitations as a result of Jiangsu Austin’s voluntary delisting from the NEEQ, through exercise of an exclusive option to purchase an aggregate of 17,869,615 shares of Jiangsu Austin from the non-management VIE Shareholders as well as certain VIE Shareholders who were directors, supervisors or senior management members of Jiangsu Austin. As a result, our company, through Nanjing Aosa, held an aggregate of 57.88% of the shares of Jiangsu Austin directly with the remaining 39.97% controlled through the VIE Arrangements. The remaining 2.15% of the shares of Jiangsu Austin were owned by two individual shareholders including Tao Ling, our Chief Executive Officer and Chairman who holds 1.54% of the shares.

In August 2021, certain directors, supervisors and members of senior management team of Jiangsu Austin, who were also shareholders of Jiangsu Austin holding an aggregate of 39.97% of its outstanding shares, resigned all their positions with Jiangsu Austin and entered into shares transfer agreements, pursuant to which, they agreed to transfer an aggregate of 39.97% of shares of Jiangsu Austin after six months following the registration of their resignation with relevant government authorities, which resulted in Nanjing Aosa, our WFOE, holding an aggregate of 97.85% of the shares of Jiangsu Austin following the completion of the share transfers.

In February 2022, we fully terminated the VIE Arrangements and completed the reorganization of our corporate structure, as a result of which we held 97.85% of the issued and outstanding shares of Jiangsu Austin.

On April 29, 2022, we consummated our initial public offering of 3,881,250 ordinary shares at a price of $4.00 per share, generating gross proceeds of $15,525,000 before deducting underwriting discounts and commissions and offering expenses.

In June 2022, through Nanjing Aosa and its subsidiary Suhong Yuanda, we purchased the remaining shares of Jiangsu Austin from two individual shareholders, including Tao Ling, our Chief Executive Officer and Chairman, and Qingning Cao. As a result, Jiangsu Austin became our wholly owned subsidiary.

In January 2023, Nanjing Aosa increased its investment in Jiangsu Austin through capital contribution. As the result, Nanjing Aosa directly holds 92.56% of the issued and outstanding shares of Jiangsu Austin, and indirectly holds 7.44% of the issued and outstanding shares of Jiangsu Austin through Suhong Yuanda.

On March 8, 2023, Pintura.Life LLC, a limited liability company, was established in California, the United States. Austin Optronics Technology Co., Ltd. acquired a majority ownership of Pintura.Life LLC on June 18, 2023. We primarily promote and sell our independently developed Pintura products in the U.S. market through Pintura.

On July 24, 2023, to align with our strategic adjustments within our corporate structure and our future development strategy, Jiangsu Austin transferred its entire share ownership in Austin Optronics Technology Co., Ltd. to Ostin Technology Limited.

On November 20, 2023, Suhong Yuanda transferred 500,000 shares of Jiangsu Austin to Shenzhen Ouxun Electronic Co., Ltd., a PRC limited liability company. As a result, we currently hold 99% of the issued and outstanding shares of Jiangsu Austin.

On January 3, 2024, Sichuan Ausheet Electronic Materials Co., Ltd. (“Sichuan Ausheet”) transferred 71.43% of equity interest in Sichuan Auniu New Materials Co., Ltd. to Nanjing Oni Investment Management Partnership Enterprise (Limited Partnership) (“Nanjing Oni”). As a result, Sichuan Ausheet and Nanjing Oni held 28.57% and 71.43% of shares of Sichuan Auniu, respectively.

3

On January 23, 2024, Sichuan Auniu New Materials Co., Ltd., together with Nanjing Oni entered into a capital injection agreement with certain new investors. As a result, Sichuan Ausheet and Nanjing Oni hold 20% and 52% of shares of Sichuan Auniu, respectively.

On March 28, 2024, the Company convened its extraordinary general meeting of shareholders, during which the shareholders of the Company adopted resolutions approving all of the proposals considered at the meeting. As a result, the Company’s authorized share capital was increased from US$50,000 divided into 499,000,000 ordinary shares of a par value of US$0.0001 each and 1,000,000 preference shares of a par value of US$0.0001 each, to US$500,000 divided into 4,999,000,000 Class A Ordinary Shares of a par value of US$0.0001 each, 8,000,000 Class B Ordinary Shares of a par value of US$0.0001 each and 1,000,000 preference shares of a par value of US$0.0001 each by (i) re-designation of all ordinary shares issued and outstanding as a consequence of the resolutions above, into Class A Ordinary Shares with a par value of US$0.0001 each with one (1) vote per share and with other rights attached to it in the Second Amended and Restated Memorandum and Articles of Association; (ii) re-designation of 4,974,193,750 unissued ordinary shares of a par value of US$0.0001 each into 4,974,193,750 Class A Ordinary Shares of a par value of US$0.0001; and (iii) re-designation of 8,000,000 unissued ordinary shares into 8,000,000 Class B Ordinary Shares with a par value of US$0.0001 each with 20 votes per share and with other rights attached to it in the Second Amended and Restated Memorandum and Articles of Association. The Company shall, at the time of the above resolutions, have not less than 8,000,000 authorized but unissued ordinary shares.

On the same date, the shareholders approved for the Company to repurchase 2,000,000 Class A Ordinary Shares registered in the name of SHYD Investment Management Limited at an amount equal to the aggregate par value of US$200 (the “Repurchase Price”) and the Repurchase Price out of the proceeds from a fresh issue of 2,000,000 Class B Ordinary Shares to SHYD Investment Management Limited. Following the repurchase and issue of Class B Ordinary Shares, the Company’s issued share capital remained unchanged, and SHYD Investment Management Limited owns 1,908,612 Class A Ordinary Shares and 2,000,000 Class B Ordinary Shares of the Company, respectively, representing approximately 76.5% of our outstanding voting power. Tao Ling, Ostin’s Chief Executive Officer and Chairman is the sole shareholder and director of SHYD Investment Management Limited. Consequently, he may be deemed the beneficial owner of the securities held by SHYD Investment Management Limited and exercises voting and dispositive power over such securities.

The chart below summarizes our corporate structure as of the date of this prospectus:

4

Cash and Asset Flows through our Organization

Ostin is a holding company with no operations of its own. We conduct substantially all of our operations through our subsidiaries in China. As a result, although other means are available for us to obtain financing at the holding company level, Ostin’s ability to pay dividends to its shareholders and to service any debt it may incur may depend upon dividends paid by our PRC subsidiaries. If any of our PRC subsidiaries incurs debt on its own behalf in the future, the instruments governing such debt may restrict our PRC subsidiaries’ ability to pay dividends to Ostin. In addition, our PRC subsidiaries are permitted to pay dividends to Ostin only out of their retained earnings, if any, as determined in accordance with PRC accounting standards and regulations. Further, our PRC subsidiaries are required to make appropriations to certain statutory reserve funds or may make appropriations to certain discretionary funds, which are not distributable as cash dividends except in the event of a solvent liquidation of the companies. For more details, see “Item 5. Operating and Financial Review and Prospects-B. Liquidity and Capital Resources-Holding Company Structure.” in our 2023 Annual Report, which is incorporated herein by reference.

Under PRC laws and regulations, our PRC subsidiaries are subject to certain restrictions with respect to paying dividends or otherwise transferring any of their net assets to us. Remittance of dividends by a wholly foreign-owned enterprise out of China is also subject to examination by the banks designated by the SAFE. The amounts restricted include the paid-up capital and the statutory reserve funds of our PRC subsidiaries, totalled $24,753,990, $24,752,533 and $11,889,822 as of September 30, 2023, 2022 and 2021, respectively.

Furthermore, cash transfers from our PRC subsidiaries to entities outside of China are subject to PRC government controls on currency conversion. To the extent cash in our business is in the PRC or a PRC entity, such cash may not be available to fund operations or for other use outside of the PRC due to restrictions and limitations imposed by the governmental authorities on the ability of us or our PRC subsidiaries to transfer cash outside of the PRC. Shortages in the availability of foreign currency may temporarily delay the ability of our PRC subsidiaries to remit sufficient foreign currency to pay dividends or other payments to us, or otherwise satisfy their foreign currency denominated obligations. In view of the foregoing, to the extent cash in our business is held in China or by a PRC entity, such cash may not be available to fund operations or for other use outside of the PRC. For risks relating to the fund flows of our operations in China, see “Risk Factors-Risks Related to Doing Business in China-We rely on dividends and other distributions on equity paid by our subsidiaries to fund offshore cash and financing requirements and any limitation on the ability of our PRC subsidiaries to transfer cash out of China and/or make remittance to pay dividends to us could limit our ability to access cash generated by the operations of those entities” on page 26 and “- PRC regulation of loans to and direct investment in PRC entities by offshore holding companies and governmental control of currency conversion may delay us from using the proceeds of our initial public offering and future financings to make loans or additional capital contributions to our PRC subsidiaries, which could materially and adversely affect our liquidity and our ability to fund and expand our business.” on page 25.

Under PRC law, Ostin may provide funding to our PRC subsidiaries only through capital contributions or loans, subject to satisfaction of applicable government registration and approval requirements. For the fiscal years ended September 30, 2023, 2022, and 2021, Ostin provided funding to our PRC subsidiaries of $0, $4,078,600 and $0, respectively.

In addition, funds are transferred among our PRC subsidiaries for working capital purposes, primarily between Jiangsu Austin, our main operating subsidiary and its subsidiaries. The following table provides a summary of the distributions and working capital funds transferred between Jiangsu Austin and its subsidiaries:

| Fiscal Years Ended September 30, | ||||||||||||

| 2023 | 2022 | 2021 | ||||||||||

| Cash transferred to its subsidiaries from Jiangsu Austin | $ | 8,617,106 | $ | 9,096,665 | $ | - | ||||||

| Cash transferred to Jiangsu Austin from its subsidiaries | $ | - | $ | - | $ | 7,640,965 | ||||||

5

The transfer of funds among companies are subject to the Provisions of the Supreme People’s Court on Several Issues Concerning the Application of Law in the Trial of Private Lending Cases (2020 Second Amendment, the “Provisions on Private Lending Cases”), which was implemented on January 1, 2021 to regulate the financing activities between natural persons, legal persons and unincorporated organizations. The Provisions on Private Lending Cases set forth that private lending contracts will be upheld as invalid under the circumstance that (i) the lender swindles loans from financial institutions for relending; (ii) the lender relends the funds obtained by means of a loan from another profit-making legal person, raising funds from its employees, illegally taking deposits from the public; (iii) the lender who has not obtained the lending qualification according to the law lends money to any unspecified object of the society for the purpose of making profits; (iv) the lender lends funds to a borrower when the lender knows or should have known that the borrower intended to use the borrowed funds for illegal or criminal purposes; (v) the lending is violations of public orders or good morals; or (vi) the lending is in violations of mandatory provisions of laws or administrative regulations. As advised by our PRC counsel, King & Wood Mallesons, the Provisions on Private Lending Cases does not prohibit using cash generated from one subsidiary to fund another subsidiary’s operations. We have not been notified of any other restriction which could limit our PRC subsidiaries’ ability to transfer cash between subsidiaries. See “Item 4. Information on the Company - B. Business Overview - Regulation - Regulations Relating to Private Lending.” in our 2023 Annual Report, which is incorporated herein by reference.

Our majority owned subsidiary, Jiangsu Austin, has maintained cash management policies which dictate the purpose, amount and procedure of cash transfers between Jiangsu Austin and its subsidiaries. Cash transferred to Jiangsu Austin’s subsidiaries of less than RMB5 million (US$0.69 million) must be reported to and reviewed by Jiangsu Austin’s financial department and the relevant PRC subsidiary’s chief executive officer, and must be approved by the Chief Financial Officer and Chairman of Jiangsu Austin. Cash transfer in excess of RMB5 million (US$0.69 million) but less than RMB20 million (US$2.74 million), and less than 50% of Jiangsu Austin’s consolidated total assets must be approved by the board of directors of Jiangsu Austin. Cash transfer in excess of RMB20 million (US$2.74 million), or more than 50% of Jiangsu Austin’s consolidated total assets must be approved by shareholders of Jiangsu Austin. Jiangsu Austin conducts regular review and management of all its subsidiaries’ cash transfers and reports to its Risk Management Department and board of directors.

Dividends and Other Distributions

Ostin is a holding company with no material operations of its own and does not generate any revenue. We currently conduct substantially all of our operations in the PRC, primarily through Jiangsu Austin, our majority owned subsidiary and its subsidiaries. As a result, our ability to pay dividends and to finance any debt we may incur depends upon dividends paid by our subsidiaries. Our PRC subsidiaries may purchase foreign exchange from relevant banks and make distributions to offshore companies after completing relevant foreign exchange registration with the SAFE. Our offshore companies may inject capital into or provide loans to our PRC subsidiaries through capital contributions or foreign debts, subject to applicable PRC regulations. If our subsidiaries or any newly formed subsidiaries incur debt on their own behalf in the future, the instruments governing their debt may restrict their ability to pay dividends to us. In addition, our PRC subsidiaries are permitted to pay dividends to us only out of their retained earnings, if any, as determined in accordance with PRC accounting standards and regulations.

Our PRC subsidiaries are permitted to pay dividends only out of their retained earnings. However, each of our PRC subsidiaries is required to set aside at least 10% of its after-tax profits each year, after making up for previous year’s accumulated losses, if any, to fund certain statutory reserves, until the aggregate amount of such funds reaches 50% of its registered capital. This portion of our PRC subsidiaries’ respective net assets are prohibited from being distributed to their shareholders as dividends. Although the statutory reserves can be used, among other ways, to increase the registered capital and eliminate future losses in excess of retained earnings of the respective companies, the reserve funds are not distributable as cash dividends except in the event of liquidation of the companies. The reserved amounts as determined pursuant to PRC statutory laws totalled $1,497,771, $1,496,314 and $1,033,653 as of and September 30, 2023, 2022 and 2021, respectively. See “Item 4. Information on the Company-4B. Business Overview-Regulation - Regulations on Dividend Distributions”. in our 2023 Annual Report, which is incorporated herein by reference and “Risk Factors- Risks Related to Doing Business in China - We rely to a significant extent on dividends and other distributions on equity paid by our subsidiaries to fund offshore cash and financing requirements and any limitation on the ability of our PRC subsidiaries to make remittance to pay dividends to us could limit our ability to access cash generated by the operations of those entities” on page 26.

6

We intend to retain all of our available funds and any future earnings and cash proceeds from overseas financing activities to fund the development and growth of our business. As a result, we do not expect to pay any cash dividends in the foreseeable future.

In addition, the PRC government imposes controls on the convertibility of the Renminbi into foreign currencies and, in certain cases, the remittance of currency out of China. If the foreign exchange control system prevents us from obtaining sufficient foreign currencies to satisfy our foreign currency demands, we may not be able to transfer cash out of China, and pay dividends in foreign currencies to our shareholders. There can be no assurance that the PRC government will not intervene or impose restrictions on our ability to transfer or distribute cash within our organization or to foreign investors, which could result in an inability or prohibition on making transfers or distributions outside of China and may adversely affect our business, financial condition and results of operations. See “Risks Related to Doing Business in China - Restrictions on currency exchange may limit our ability to utilize our revenues effectively” on page 27.

A 10% PRC withholding tax is applicable to dividends payable to investors that are non-resident enterprises. Any gain realized on the transfer of ordinary shares by such investors is also subject to PRC tax at a current rate of 10% which in the case of dividends will be withheld at source if such gain is regarded as income derived from sources within the PRC. See also “Risks Related to Doing Business in China - Dividends payable to our foreign investors and gains on the sale of Ostin’s Class A Ordinary Shares by our foreign investors may be subject to PRC tax” on page 26.

Foreign Private Issuer Status

We are a foreign private issuer within the meaning of the rules under the Exchange Act. As such, we are exempt from certain provisions applicable to United States domestic public companies. For example:

| ● | we are not required to provide as many Exchange Act reports, or as frequently, as a domestic public company; | |

| ● | for interim reporting, we are permitted to comply solely with our home country requirements, which are less rigorous than the rules that apply to domestic public companies; | |

| ● | we are not required to provide the same level of disclosure on certain issues, such as executive compensation; | |

| ● | we are exempt from provisions of Regulation FD aimed at preventing issuers from making selective disclosures of material information; | |

| ● | we are not required to comply with the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations in respect of a security registered under the Exchange Act; and | |

| ● | we are not required to comply with Section 16 of the Exchange Act requiring insiders to file public reports of their share ownership and trading activities and establishing insider liability for profits realized from any “short-swing” trading transaction. |

Implications of Being an Emerging Growth Company

As a company with less than US$1.235 billion in revenue for the last fiscal year, we qualify as an “emerging growth company” pursuant to the JOBS Act. An emerging growth company may take advantage of specified reduced reporting and other requirements that are otherwise applicable generally to public companies. These provisions include exemption from the auditor attestation requirement under Section 404 of the Sarbanes-Oxley Act of 2002, or Section 404, in the assessment of the emerging growth company’s internal control over financial reporting. The JOBS Act also provides that an emerging growth company does not need to comply with any new or revised financial accounting standards until such date that a private company is otherwise required to comply with such new or revised accounting standards.

7

We will remain an emerging growth company until the earliest of (i) the last day of our fiscal year during which we have total annual gross revenues of at least US$1.235 billion; (ii) the last day of our fiscal year following the fifth anniversary of the completion of our initial public offering; (iii) the date on which we have, during the previous three year period, issued more than US$1.0 billion in non-convertible debt; or (iv) the date on which we are deemed to be a “large accelerated filer” under the Exchange Act, which would occur if the market value of Ostin’s Class A Ordinary Shares that are held by non-affiliates exceeds US$700 million as of the last business day of our most recently completed second fiscal quarter and we have been publicly reporting for at least 12 months. Once we cease to be an emerging growth company, we will not be entitled to the exemptions provided in the JOBS Act discussed above.

Implications of Being a Controlled Company

Mr. Tao Ling, Ostin’s Chief Executive Officer and Chairman, currently controls a majority of the voting power of our outstanding share capital. As a result, we are a “controlled company” within the meaning of applicable Nasdaq listing rules. Under these rules, a company of which more than 50% of the voting power for the election of directors is held by an individual, group or another company is a “controlled company.” For so long as we remain a “controlled company,” we may elect not to comply with certain corporate governance requirements, including the requirements:

| ● | that a majority of the board of directors consists of independent directors; |

| ● | for an annual performance evaluation of the nominating and corporate governance and compensation committees; |

| ● | that we have a nominating and corporate governance committee that is composed entirely of independent directors with a written charter addressing the committee’s purpose and responsibilities; and |

| ● | that we have a compensation committee that is composed entirely of independent directors with a written charter addressing the committee’s purpose and responsibility. |

We currently do not intend to use these exemptions but may use some or all of these exemptions in the future. As a result, you may not have the same protections afforded to shareholders of companies that are subject to all of the Nasdaq corporate governance requirements.

Recent Developments

On January 19, 2024, the Company entered into certain securities purchase agreement with an accredited investor pursuant to which the Company sold a senior unsecured convertible note in the original principal amount of $550,000, at a purchase price of $500,000. Subject to certain sales limitation, the note is convertible into Class A Ordinary Shares of the Company beginning on the date that is six months from the closing date. On January 22, 2024, the Company completed its issuance and sale of the note pursuant to the securities purchase agreement. The issuance of the note was made pursuant to the exemption from registration contained in Section 4(a)(2) of the Securities Act and Regulation D promulgated thereunder. The gross proceeds from the sale of the note were $500,000, prior to deducting transaction fees and estimated expenses. The Company intended to use the proceeds for working capital and general corporate purposes. On June 24, 2024, the Company repaid the convertible promissory note dated January 19, 2024 in full, and the investor released the Company from any and all obligations and liabilities under the note. As a result, the note was deemed paid in full, canceled and of no further force or effect.

On January 31, 2024, the Company entered into certain subscription agreement and registration rights agreement with the selling shareholder identified in this prospectus, which is a “non-U.S. Person” as defined in Regulation S of the Securities Act for a private placement. Pursuant to the subscription agreement, the Company issued and sold to the selling shareholder 2,800,000 ordinary shares of the Company at a purchase price equivalent to US$0.35 per share. The Company received US$980,000 in gross proceeds. The private placement was closed on February 7, 2024. The issuance of ordinary shares in the private placement was exempt from the registration requirements of the Securities Act, pursuant to Regulation S promulgated thereunder.

The foregoing descriptions of the subscription agreement and registration rights agreement are subject to, and qualified in their entirety by, such documents, which are incorporated herein by reference from our current report on Form 6-K filed with the SEC on February 7, 2024.

On June 21, 2024, the Company entered into certain securities purchase agreement with an accredited investor pursuant to which the Company sold a senior unsecured convertible note in the original principal amount of $1,360,000, at a purchase price of $1,250,000. Subject to certain sales limitation, the note is convertible into Class A Ordinary Shares of the Company beginning on the closing date and continuing thereafter until the note is repaid in full. On June 24, 2024, the Company completed its issuance and sale of the note pursuant to the securities purchase agreement. The investor has previously invested in securities of the Company or otherwise had pre-existing relationships with the Company; however, the Company did not engage in general solicitation or advertising with regard to the issuance and sale of the note. The Class A Ordinary Shares, as converted, were registered with the SEC pursuant to a prospectus supplement to the Company’s currently effective registration statement on Form F-3 (File No. 333-279177), which was initially filed with the SEC on May 7, 2024, and was declared effective on May 28, 2024 (the “Shelf Registration Statement”). The Company filed the prospectus supplement to the Shelf Registration Statement with the SEC on June 21, 2024. The gross proceeds from the sale of the note were $1,2500,000, prior to deducting transaction fees and estimated expenses. The Company intends to use the proceeds for repayment of the prior convertible promissory note dated January 19, 2024, and working capital for general corporate and administrative purposes.

8

Recent Regulatory Developments in China

Recently, the PRC government initiated a series of regulatory actions and made a number of public statements on the regulation of business operations in China with little advance notice, including cracking down on illegal activities in the securities market, enhancing supervision over China-based companies listed overseas, adopting new measures to extend the scope of cybersecurity reviews, and expanding efforts in anti-monopoly enforcement.

On February 17, 2023, the CSRC promulgated the Overseas Listing Trial Measures, which became effective on March 31, 2023. The Overseas Listing Trial Measures comprehensively improve and reform the existing regulatory regime for overseas offering and listing of mainland China domestic companies’ securities and regulates both direct and indirect overseas offering and listing of mainland China domestic companies’ securities by adopting a filing-based regulatory regime.

According to the Overseas Listing Trial Measures, (i) mainland China domestic companies that seek to offer or list securities overseas, both directly and indirectly, should fulfill the filing procedure and report relevant information to the CSRC; if a mainland China domestic company fails to complete the filing procedure or conceals any material fact or falsifies any major content in its filing documents, such mainland China domestic company may be subject to administrative penalties, such as order to rectify, warnings, fines, and its controlling shareholders, actual controllers, the person directly in charge and other directly liable persons may also be subject to administrative penalties, such as warnings and fines; (ii) if the issuer meets both of the following conditions, the overseas offering and listing shall be determined as an indirect overseas offering and listing by a mainland China domestic company: (a) any of the total assets, net assets, revenues or profits of the domestic operating entities of the issuer in the most recent accounting year accounts for more than 50% of the corresponding figure in the issuer’s audited consolidated financial statements for the same period; (b) its major operational activities are carried out in mainland China or its main places of business are located in mainland China, or the senior managers in charge of operation and management of the issuer are mostly PRC citizens or have their usual place(s) of residence located in mainland China. The Overseas Listing Trial Measures require subsequent reports to be filed with the CSRC on material events, such as change of control or voluntary or forced delisting of the issuers who have completed overseas offerings and listings.

On the same day, the CSRC also held a press conference for the release of the Overseas Listing Trial Measures and issued the Notice on Administration for the Filing of Overseas Offering and Listing by Domestic Companies, which, among others, clarifies that (i) prior to the effective date of the Overseas Listing Trial Measures, mainland China domestic companies that have already completed overseas listing shall be regarded as “existing companies”, which are not required to fulfill filing procedure immediately but shall be required to complete the filing if such existing companies conduct refinancing in the future; and (ii) the CSRC will solicit opinions from relevant regulatory authorities and complete the filing of the overseas listing of companies with contractual arrangements which duly meet the compliance requirements, and support the development and growth of these companies by enabling them to utilize two markets and two kinds of resources. However, since the Overseas Listing Trial Measures was newly promulgated, the interpretation, application and enforcement of Overseas Listing Trial Measures remain unclear.

9

On February 24, 2023, the CSRC released the Provisions on Strengthening the Confidentiality and Archives Administration Related to the Overseas Securities Offering and Listing by Domestic Enterprises, or the Confidentiality and Archives Administration Provisions, which took effect on March 31, 2023. The Confidentiality and Archives Administration Provisions require, among others, that PRC domestic enterprises that seek to offer and list securities in overseas markets, either directly or indirectly, complete approval and filing procedures to competent authorities, if such PRC domestic enterprises or its overseas listing entities provide or publicly disclose documents or materials involving state secrets and work secrets of PRC government agencies to relevant securities companies, securities service institutions, overseas regulatory agencies and other entities and individuals. It further stipulates that providing or publicly disclosing documents and materials which may adversely affect national security or public interests, and accounting files or copies shall be subject to corresponding procedures in accordance with relevant laws and regulations.

In addition, an overseas-listed company must also submit the filing with respect to its follow-on offerings, issuance of convertible corporate bonds and exchangeable bonds, and other equivalent offering activities, within the time frame specified by the Overseas Listing Trial Measures. However, if we do not maintain the permissions and approvals of the filing procedure in a timely manner under PRC laws and regulations, we may be subject to investigations by competent regulators, fines or penalties, ordered to suspend our relevant operations and rectify any non-compliance, prohibited from engaging in relevant business or conducting any offering, and these risks could result in a material adverse change in our operations, limit our ability to offer or continue to offer securities to investors, or cause such securities to significantly decline in value or become worthless. As the Overseas Listing Trial Measures were newly published, there exists uncertainty with respect to the filing requirements and their implementation.