Table of Contents

As confidentially submitted to the Securities and Exchange Commission on May 10, 2021. This draft registration statement has not been filed publicly with the Securities and Exchange Commission and all information contained herein remains confidential.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

TDCX Inc.

(Exact name of Registrant as specified in its charter)

| Cayman Islands | 7373 | Not Applicable | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

750D Chai Chee Road,

#06-01/06 ESR BizPark @ Chai Chee

Singapore 469004

(65) 6309 1688

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||

| Rajeev P. Duggal, Esq. Skadden, Arps, Slate, Meagher & Flom LLP 6 Battery Road Suite 23-02 Singapore 049909 (65) 6434-2900 |

Sharon Lau, Esq. Latham & Watkins LLP 9 Raffles Place #42-02 Republic Plaza Singapore 048619 (65) 6536-1161 | |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered(1)(2) |

Proposed Maximum Aggregate Offering Price(2)(3) |

Amount of Registration Fee | ||

| Class A ordinary shares, par value US$ per share | US$ | US$ | ||

|

| ||||

|

| ||||

| (1) | American depositary shares issuable upon deposit of ordinary shares registered hereby will be registered under a separate registration statement on Form F-6 (Registration No. ). Each American depositary share represents Class A ordinary shares. |

| (2) | Includes (a) Class A ordinary shares initially offered and sold outside the United States that may be resold from time to time in the United States either as part of the distribution or within 40 days after the later of the effective date of this registration statement and the date the securities are first bona fide offered to the public, and (b) additional Class A ordinary shares that are issuable upon the exercise of the underwriters’ option to purchase additional shares to cover over-allotments, if any. |

| (3) | Estimated solely for the purposes of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission acting pursuant to said Section 8(a) may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. Neither we nor the selling shareholders may sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS (Subject to Completion)

, 2021

TDCX Inc.

American Depositary Shares

Representing Class A Ordinary Shares

This is the initial public offering of TDCX Inc. We are offering American Depositary Shares, or ADSs[, and the selling shareholders] identified in this prospectus are offering an additional ADSs. We will not receive any of the proceeds from the sale of our ADSs by the selling shareholders.

Prior to this offering, there has been no public market for our ADSs or ordinary shares. Each ADS represents of our Class A ordinary shares, par value US$ per ordinary share. It is currently estimated that the initial public offering price per ADS will be between US$ and US$ . We intend to apply for listing of our ADSs on the under the symbol “ .”

We are a “controlled company” under the corporate governance rules of the New York Stock Exchange.

We are an “emerging growth company” under the U.S. federal securities laws and have elected to comply with certain reduced public reporting requirements.

Investing in our ADSs involves risks. See “Risk Factors” beginning on page 21.

| Per ADS | Total | |||||||

| Public offering price |

US$ | US$ | ||||||

| Underwriting discount and commission(1) |

US$ | US$ | ||||||

| Proceeds, before expenses, to TDCX Inc. |

US$ | US$ | ||||||

| Proceeds, before expenses, to the selling shareholders |

US$ | US$ | ||||||

| (1) | See “Underwriting” for a description of compensation and other items of value payable to the underwriters. [We and certain selling shareholders] have granted the underwriters the right to purchase up to an additional ADSs to cover over-allotments within 30 days after the date of this prospectus. |

Neither the Securities and Exchange Commission nor any state securities commission or any other regulator has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Immediately prior to the completion of this offering, our outstanding share capital will be re-designated into Class A ordinary shares and Class B ordinary shares. Holders of Class A ordinary shares are entitled to one vote per share, while holders of Class B ordinary shares are entitled to ten votes per share. Holders of Class A ordinary shares and Class B ordinary shares will vote together as one class on all matters that require a shareholders’ vote. Each Class B ordinary share is convertible into one Class A ordinary share at any time by the holder thereof, while Class A ordinary shares are not convertible into Class B ordinary shares under any circumstance. Upon the completion of this offering, assuming the underwriters do not exercise their over-allotment option to purchase additional ADSs, Mr. Laurent Bernard Marie Junique, our Founder, Executive Chairman and Chief Executive Officer, will own an aggregate of Class B ordinary shares, which will represent % of the then total outstanding ordinary shares and % of total voting power of our outstanding shares (assuming the underwriters do not exercise their over-allotment option).

The underwriters expect to deliver the ADSs against payment to purchasers on or about , 2021.

| Goldman Sachs |

Credit Suisse |

, 2021

Table of Contents

Table of Contents

Table of Contents

Table of Contents

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with information different from that contained in this prospectus. If anyone provides you with different or inconsistent information, you should not rely on it. We are not making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. We are offering to sell ADSs and seeking offers to buy ADSs, only in jurisdictions where offers and sales are permitted. Unless otherwise noted, the information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of the ADSs.

We have not taken any action to permit a public offering of the ADSs outside the United States or to permit the possession or distribution of this prospectus outside the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about and observe any restrictions relating to the offering of the ADSs and the distribution of this prospectus outside of the United States.

Until and including , 2021 (the 25th day after the date of this prospectus), all dealers that buy, sell or trade ADSs, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

Market, Industry and Other Data

This prospectus includes estimates regarding market and industry data and forecasts, which are based on publicly available information, industry publications and surveys, reports from government agencies, reports by market research firms or other independent sources and our own estimates based on our management’s knowledge of and experience in the market sectors in which we compete. Certain information in this prospectus is based on a report on the outsourced business support services industry prepared by Frost & Sullivan Limited, or Frost & Sullivan, which was commissioned by us.

i

Table of Contents

Trademarks and Intellectual Property

We own or otherwise have rights to the service mark “TDCX” mentioned in this prospectus that we use in conjunction with the marketing and sale of our services. This service mark is the property of TDCX Holdings Pte. Ltd. and it will eventually be licensed for use by us and our subsidiaries. This prospectus also mentions and cites trademarks, service marks, copyrights and trade names of other companies, which are the property of their respective owners. We do not intend our use or display of other companies’ trademarks, copyrights or trade names to imply a relationship with, or endorsement or sponsorship of us by any other companies. Solely for convenience, our trademark and trade name referred to in this prospectus may appear without the ® roundel or TM symbol, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights to those trademarks and trade names.

Conventions that Apply to this Prospectus

Unless the context provides otherwise, for the purposes of this prospectus:

| • | “ADR” means American Depositary Receipt; |

| • | “ADS” means American Depositary Shares; |

| • | “agent” means an FTE, as classified under our employee classification system; |

| • | “AI” means artificial intelligence; |

| • | “B2B” means business-to-business; |

| • | “B2C” means business-to-consumer; |

| • | “Class A ordinary share” means our Class A ordinary shares of par value US$ per share; |

| • | “Class B ordinary share” means our Class B ordinary shares of par value US$ per share; |

| • | “clients” means our corporate clients with whom we have entered into contractual arrangements; |

| • | “CRM” means customer relationship management; |

| • | “customers” means the parties with whom we have customer interactions on behalf of our clients; |

| • | “CX” means customer experience; |

| • | “Founder” means Mr. Laurent Bernard Marie Junique, our founder, Executive Chairman and Chief Executive Officer; |

| • | “FTE” means full-time equivalent employee; |

| • | “KPI” means key performance indicator; |

| • | “MSA” means master services agreement; |

| • | “new economy” means high growth industries that are on the cutting edge of digital technology and are the driving forces of economic growth; |

| • | “NYSE” means the New York Stock Exchange; |

| • | “SOW” means statements of work; |

| • | “TDCX HPL” means TDCX Holdings Pte. Ltd. (formerly Agorae Pte Ltd); |

| • | “TDCX KY” means TDCX (KY) PTE LTD; |

| • | “TDCX SG” means TDCX (SG) Pte. Ltd. (formerly Teledirect Pte Ltd); |

| • | “U.S.” and “United States” means the United States of America; and |

| • | “We,” “us,” “our”, “our Company” and “TDCX” mean TDCX Inc. and its subsidiaries and associated companies, collectively. |

ii

Table of Contents

Certain metrics presented in this prospectus, which include the annual voluntary attrition rate of our employees and our employee satisfaction scores, are calculated using internal company data. While we believe these metrics to be reasonable estimates for the applicable period of measurement, collected through our internal employee surveys and human resources management systems, there are inherent challenges in measuring employee satisfaction and similar metrics. In addition, we are continually seeking to improve the estimation and evaluation criteria that we use to calculate our annual voluntary attrition rate and employee satisfaction, and such estimates may change due to improvements or changes in our methodology. References to the average number of agents and average number of employees are an average of headcount at end of each month over the course of the given period.

We regularly review our processes for calculating these metrics, and from time to time we may discover inaccuracies in our metrics or make adjustments to improve their accuracy, including adjustments that may result in the recalculation of our historical metrics. In addition, our estimates may not be comparable to estimates of similar metrics published by third parties, such as research analysts, due to differences in methodology.

Basis of Presentation

TDCX was incorporated on April 16, 2020 and is 100% owned by our Founder in accordance with the laws of the Cayman Islands. TDCX was created to acquire our Founder’s shareholder’s interest in TDCX KY. On December 22, 2020, TDCX KY acquired our Founder’s 100% interest in TDCX HPL. Prior to September 2018, TDCX SG, was 60% owned by our Founder and 40% owned by a third party. In September 2018, the remaining 40% of TDCX SG was acquired by TDCX HPL by paying cash in an amount of S$38 million. In January 2019, our Founder reduced his 60% equity interest in TDCX SG through cancellation of his shares in TDCX SG, and TDCX SG became a wholly owned subsidiary of TDCX HPL. On March 23, 2021, TDCX acquired 100% of TDCX KY from our Founder. As TDCX, TDCX KY, TDCX HPL and TDCX SG were under common control of the Founder during all the periods presented, the acquisitions of TDCX SG and TDCX HPL by TDCX KY as well as the acquisition of TDCX KY by TDCX were accounted for in a manner similar to a pooling of interest with assets and liabilities all reflected at their historical amounts in our consolidated financial statements as if the reorganization had always been in place. As such, the consolidated financial statements were prepared as if TDCX had control over TDCX KY, TDCX HPL and TDCX SG for all periods presented. For more information, see Note 1 to our audited consolidated financial statements included elsewhere in this prospectus.

When we refer to “U.S. dollars” and “US$” in this prospectus, we are referring to United States dollars, the legal currency of the United States. When we refer to “S$”, we are referring to Singapore dollars, the legal currency of Singapore. When we refer to “IFRS”, we are referring to International Financial Reporting standards, or IFRS, as issued by the International Accounting Standards Board, or IASB.

Unless otherwise noted, all translations from Singapore dollars to U.S. dollars and from U.S. dollars to Singapore dollars in this prospectus were made at a rate of S$1.3221 to US$1.00, being the rate in effect as of December 31, 2020. We make no representation that any Singapore dollar or U.S. dollar amount could have been, or could be, converted into U.S. dollars or Singapore dollar, as the case may be, at any particular rate, the rates stated below, or at all. On May 5, 2021, the rate was S$1.3345 to US$1.00.

Certain amounts, percentages and other figures included in this prospectus have been subject to rounding adjustments. Accordingly, amounts, percentages and other figures shown as totals in certain tables or charts may not be the arithmetic aggregation of those that precede them, and amounts and figures expressed as percentages in the text may not total 100% or, when aggregated may not be the arithmetic aggregation of the percentages that precede them.

iii

Table of Contents

LETTER FROM MR. LAURENT BERNARD MARIE JUNIQUE, OUR FOUNDER, EXECUTIVE CHAIRMAN AND CHIEF EXECUTIVE OFFICER

I founded TDCX in 1995 with a vision of a better way to deliver customer experience services. The flagship office was a compact space in Singapore with a staff of 2. Those early days taught me that a tight-knit team of talented and dedicated employees that can tackle the most complex challenges, would set us apart. This formula of quality people and work culture drives everything we do.

We now operate out of nine geographies — the sun does not set on TDCX. I attribute our success to our ability to anticipate seismic shifts in the customer experience market and then to respond by positioning TDCX to meet our clients’ changing needs.

The 2008 global recession provided an object lesson. The world’s largest digital companies flocked to Asia to capitalize on the region’s dynamic recovery. These were the salad days of the smartphone and e-commerce. These established New Economy brands rapidly scooped up customers in Asia, tailoring their products and offerings . . . but they did not have the local resources and knowledge to support their growth. And there we were with the customer experience services to complete the picture.

Our lean and agile structure of customer experience knowledge, AI tools and high quality localized offerings, such as talent acquisition, were curated for the iconic businesses that became our clients in the new world of the digital economy.

TDCX and the Digital Economy – A Symbiotic Partnership

A client once told me: “In a fast-moving economy, we need a fast-moving and innovative partner.” That’s TDCX! We are widely recognized as a high-growth digital customer experience solutions provider for technology and blue-chip companies even our competitors publicly talk about.

TDCX is the preferred specialist partner to fast-growing New Economy companies that are redefining digital advertising, e-commerce, online travel and hospitality, consumer electronics, fintech and other technology-enabled sectors in Asia.

Our clients trust us with their most pressing customer interactions. We are now approximately 11,500 strong, handling complex assignments daily in more than 20 languages across digital advertising, online bookings, troubleshooting smart technology and moderating platform content to keep the Internet decent and safe for the next generation.

The Future Beckons

We are living more and more of our lives online, which has simplified daily routines, brought greater convenience and given us more time with family and friends. Concurrently, this transformational shift has overturned the horse-and-buggy interaction between vendors and their customers and elevated their transactions to a hitherto unimagined plane.

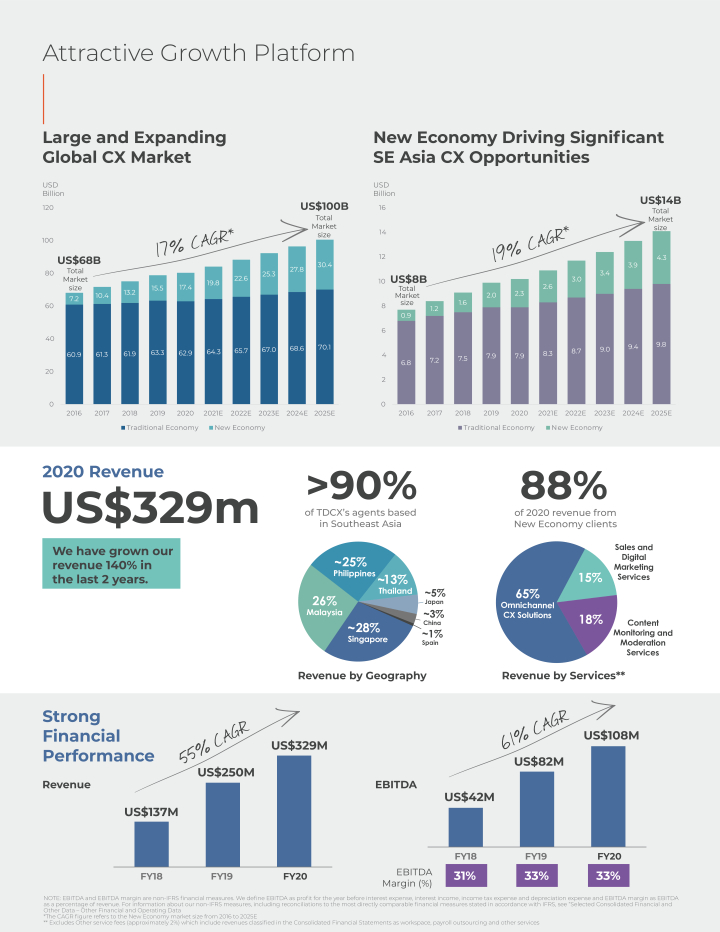

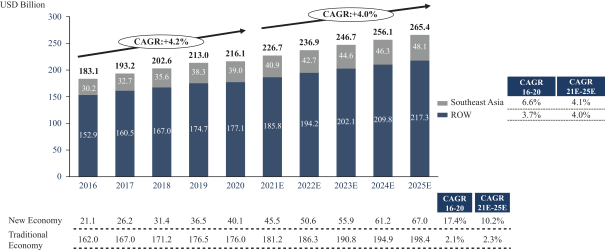

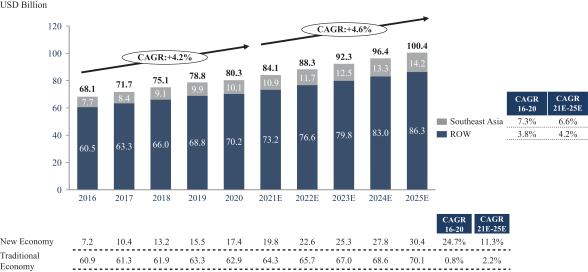

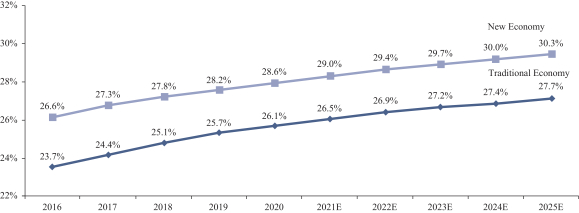

Now responses to basic enquiries are automated or demands for them eliminated, questions are complex and sophisticated, and customers’ expectations for speed of resolution and accuracy have gone through the roof. We envision a future where very capable specialists working from home or at a breathtaking work location solve increasingly complex problems for New Economy Clients overwhelmed with unprecedented growth and fierce competition that require them to stand out from the pack — agile, flexible and effective Customer Experience capabilities. According to Frost and Sullivan, the global customer experience market is expected to grow from US$80 billion in 2020 to US$100 billion in 2025. In Southeast Asia alone, the Customer Experience Market for the New Economy sector is expected to grow at a staggering 19% CAGR between 2016 and 2025.

1

Table of Contents

As TDCX’s innovative New Economy clients develop their next “game-changing” products, services or apps, we will be their public face with the emerging new range of customer interactions.

TDCX will win

Our greatest advantage is our people. We hire the right people, equip them technologically, and then unleash them to fire on all cylinders.

We quickly and efficiently expand at scale to meet the demands of our global clients, while maintaining the collaborative, people-focused culture that is the heart of TDCX.

From the collaboration of the art and science of employee recruitment and development emerges talented people who bond with TDCX. Our offices are welcoming and fun. The office environment is their home-away-from-home where our employees hike the extra mile. Our employee satisfaction scores are consistently high.

Our proprietary technology platform provides the multiplier effect to extract the best from our team. It starts with Flash Hire, our customizable, automated video-based recruitment platform that auto-learns from the success profiles of our best performers to improve our hiring process, while significantly reducing recruitment time and costs. We combine this with Flash Coach and Flash Learn, which use data and an adaptive approach to allow our leaders to develop clear and systematic developmental priorities and seamlessly roll out online learning and training programs, whether we are working in the office or remotely.

We also use advanced analytics, artificial intelligence and a real-time decision support system to help us make operational changes and improve employee performance. Our ability to accurately predict performance three months ahead of time allows us to take preemptive steps and provide the additional training and resources to better manage our teams.

Our Success

Hire the right people, keep them happy, invest in them. The result: During the past two years, revenues up by 140%, new offices in 6 geographies and more than 5,600 new employees.

Our resilience and cohesiveness took center stage during the COVID-19 pandemic. 80% of our employees safely transitioned to a remote working structure. We developed FalconEye, a full-service technology platform to make it even easier, more secure and more efficient for our experts to work from home. Falcon combines our virtual helpdesk, algorithm configuration and other customer support tools with people management and data security programs to put all the resources at our employees’ fingertips.

The Path Ahead

We now step forward as a global public company, still our focus is our people, work culture and long-term vision with disciplined decision-making for the benefit of our clients, employees and shareholders.

Our blueprint for the future:

| 1. | Grow our footprint. We have first mover advantage in Southeast Asia with a unique footprint. Our leadership positions in key markets allow us to onboard new clients that expand our fast-growing network and provide a strong platform for our geographic reach. We will continue to carefully expand our global footprint without losing sight of where our center of gravity is: ASIA! |

2

Table of Contents

| 2. | Invest in people and technology. Continuously seeking to attract the best to join us in this exciting journey will remain at the centerstage of what we do. And our new structure will be a catalyst of that. Our Digital Lab will continue to expand into creating tools and solutions to drive the insights and efficiencies that our clients are reputed for. |

| 3. | Lean and mean. Our careful approach to financial management has been carrying us through all these years and will continue to do so for the foreseeable future. |

| 4. | Strategic acquisitions. Much of our growth is driven organically on the back of a growing CX services market in the New Economy sector. At the same time, we intend to partner with or acquire companies that can accelerate the delivery of our vision. |

This moment would not be possible without our livewire talented and dedicated team. The next level as a public company will provide us greater resources to expand into new markets around the world and further invest in our people, technology and operations.

I am also extremely grateful to our clients, who put their trust in TDCX to support their customers and protect their brands. We are honored to be your partner of choice. To the world, we are you.

This is an incredible opportunity to elevate the customer experience for the digital age. I hope you will join us on this journey.

Sincerely,

Laurent Junique

3

Table of Contents

The following is a summary of material information discussed in this prospectus. This summary may not contain all the details concerning our business, our ADSs or other information that may be important to you. You should carefully review this entire prospectus, including the “Risk Factors” section and our financial statements and the related notes included elsewhere in this prospectus, before making an investment decision.

Overview

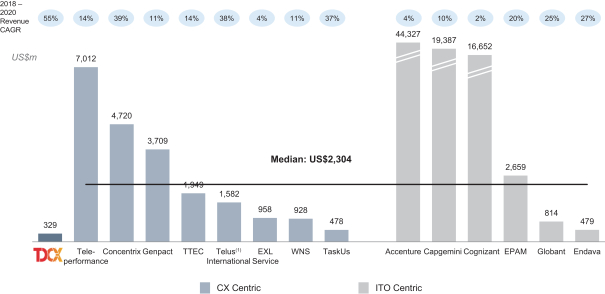

We are a high-growth digital customer experience solutions provider for innovative technology and other blue-chip companies. We have specific expertise in providing tailored digital customer experience solutions to manage complex customer interactions. We offer omnichannel CX solutions, sales and digital marketing services and content monitoring and moderation services. We have specific expertise in providing tailored digital customer experience solutions to manage complex customer interactions that go beyond providing boilerplate responses and which require a highly trained workforce capable of effectively delivering our differentiated services and solutions to our clients and their customers. Our focus on complex digital solutions enables us to provide higher value services and solutions for our clients. Our strategy has resulted in a highly attractive financial profile. We have experienced robust growth with our revenue, profit for the year and EBITDA growing at a CAGR of 54.9%, 50.3% and 60.7%, respectively, from the year ended December 31, 2018 to the year ended December 31, 2020. In the years ended December 31, 2018, 2019 and 2020, we recorded revenue of S$181.2 million, S$330.3 million and S$434.7 million (US$328.8 million), profit for the year of S$38.1 million, S$73.5 million and S$86.1 million (US$65.1 million) and EBITDA of S$55.4 million, S$108.1 million and S$142.9 million (US$108.1 million), respectively. For the same periods, we recorded net profit margins of 21.0%, 22.2% and 19.8%, respectively, and EBITDA margins of 30.6%, 32.7% and 32.9%, respectively.

We believe our employees and our distinctive corporate culture are key enablers of our success, a core strength and part of our competitive advantage. Our corporate culture is designed to foster a work environment that attracts, develops and retains a highly skilled workforce that can effectively engage in complex customer interactions. We focus on reinforcing a culture that emphasizes a sustainable and collaborative approach while being fully committed to our clients’ requirements. We strive to ensure that our distinctive culture is incorporated within all the relationships and processes of our organization and fits within our values and goals.

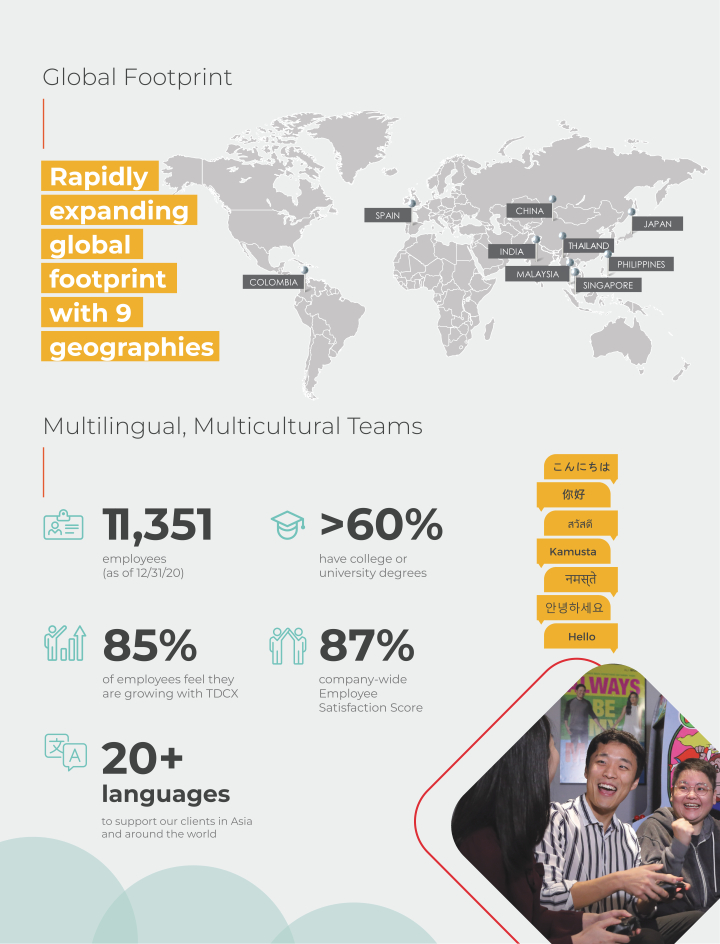

We have an international footprint. As of the date of this prospectus, we service our clients’ customers globally in more than 20 languages. This international footprint is supported by 11,351 employees as of December 31, 2020, who are located in offices in nine geographies: Singapore, the Philippines, Malaysia, Thailand, China, Japan, Spain, India and Colombia.

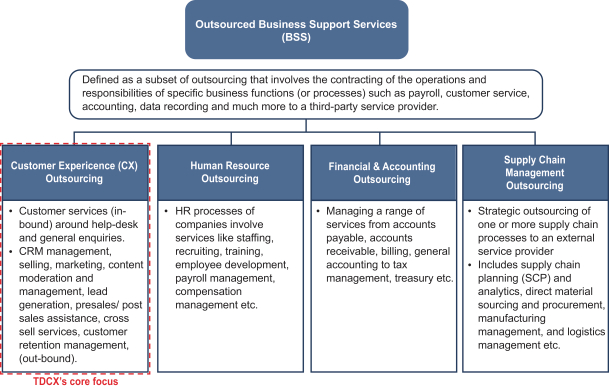

Our business comprises three key service offerings: (1) omnichannel CX solutions; (2) sales and digital marketing services; and (3) content monitoring and moderation services. We also offer services consisting of miscellaneous activities, such as providing workspaces to existing clients and providing human resource and administration services to clients. We help our clients manage relationships with their customers by providing digital customer experience solutions, such as after-sales service and customer support across ten industry verticals, including travel and hospitality, digital advertising and media and fast-moving consumer goods. Our sales and digital marketing services offering helps our clients market their products and services to potential customers in both the business-to-consumer, or B2C, and the business-to-business, or B2B, markets. Our content monitoring and moderation services offering helps our clients create a safe and secure online environment for social media platforms by providing a human touch to content monitoring and moderation services.

4

Table of Contents

Our competitive strengths

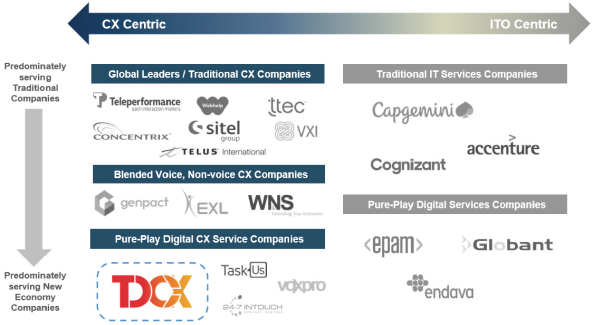

Digital customer experience solutions provider for high-growth technology disruptors

We provide a high value-added service platform to market-leading clients in the new economy sectors and traditional blue-chip clients who are undergoing digital transformation across their organizations. Frost & Sullivan defines the “new economy” as the high growth industries that are on the cutting edge of digital technology and are the driving forces of economic growth. These industries are seen as an evolution of the existing traditional economy aided by technological advancements and innovation. Our services provide synergies with our clients’ digital economy value chains and enable our clients to grow and transform their businesses’ consumer experience. We offer customized and differentiated customer contact solutions and possess the ability to handle complex and mission-critical digital customer experience interactions. These offerings are enhanced by our ability to solve problems for our clients by leveraging customer interaction data analytics to allow our clients to access real-time data which gives them valuable insights on their end-customers, allows them to improve business processes and make more prompt business decisions to resolve problems in a more timely manner.

We have leveraged our integrated omnichannel and multimodal solutions to shape user experiences in a world of evolving and proliferating digital communication and technology platforms from traditional channels, such as voice and email, to advanced technology driven channels, ranging from messaging and social media to AI-powered chat bots and in-app interactions. We are also able to synergize our in-house developed technology with third-party technology and platforms to solve operational issues which our clients are facing.

We have an international footprint with offices in nine geographies across Asia and in Spain and Latin America, which provides us with access to a broad talent pool and equips us with multilingual capabilities to serve a global customer base, including English and key Asian languages, such as Mandarin, Thai, Korean, Malay (Malaysia and Indonesia), Vietnamese and Japanese.

Strong focus on human capital development to deliver superior customer experiences

We believe the quality of our employees is a key differentiator in winning and retaining business, as well as in delivering a superior customer experience. Through our structured recruitment process and strong emphasis on career development, we strive to attract, develop and retain the industry’s high caliber talent who possess deep knowledge of local customs and cultural sensitivities. As of December 31, 2020, we had 11,351 employees of which more than 60% are college or university graduates, including employees with master’s degrees and/or doctorates, which helps us handle complex campaigns. Our employees have access to ongoing internally and externally developed supplementary training and certifications in a number of areas, such as COPC, a standard certification, which is a widely recognized standard across the customer experience industry.

In the years ended December 31, 2018, 2019 and 2020, our annual voluntary attrition rate, measured by the number of employees that voluntarily left us in a period divided by the average number of employees in such period, was 21.5%, 23.1% and 24.8%, respectively, compared to the industry average of 30% to 34% in the Asia Pacific region, according to Frost & Sullivan. Consistent with our improving attrition rates, employee satisfaction surveys have demonstrated a high degree of satisfaction. Our company-wide employee satisfaction scores were at 87%, 91% and 87% in the years ended December 31, 2018, 2019 and 2020, respectively. We conducted our survey for 2020 in July during the COVID-19 pandemic, which we believe reflects our continued commitment to our employees through this challenging period. We believe that our strong focus on human capital has been critical to our ability to minimize business disruptions and rehiring and training costs, resulting in high service quality for our clients. Our commitment to the development of our people is reflected in the multiple awards we have received, including the Best Companies to Work for In Asia 2020 (both our Thai and Philippines office), the Top 100 Asia’s Best Employer Brands 2019 from Employer Branding Awards (our Malaysian office) from

5

Table of Contents

the HR Asia Awards, the Great Place to Learn Certification from the Great Place to Work Institute & SkillsFuture Singapore in 2019 and 2020 (our Singapore office), and Asia’s Best Employer Brand Award from the World HRD Congress in 2018 (our Singapore office).

Well-positioned to capitalize on positive “digital economy” trends and increasing demand for our services

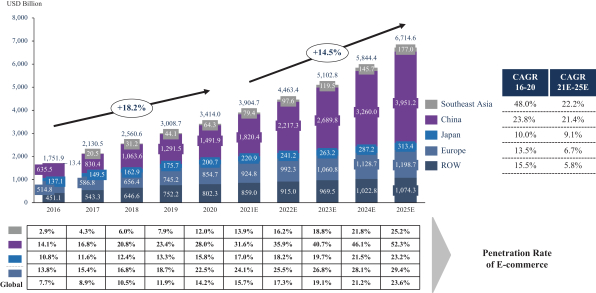

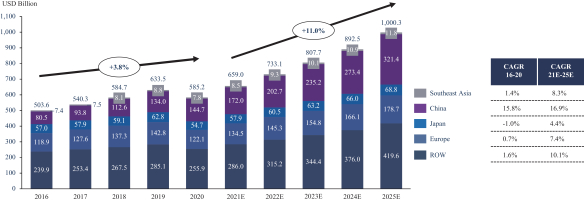

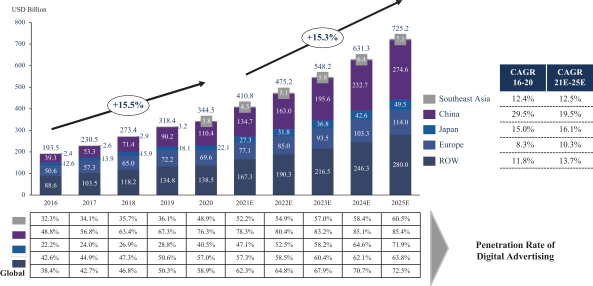

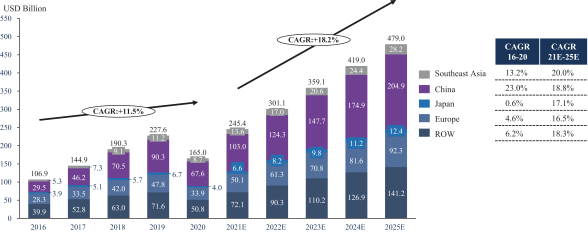

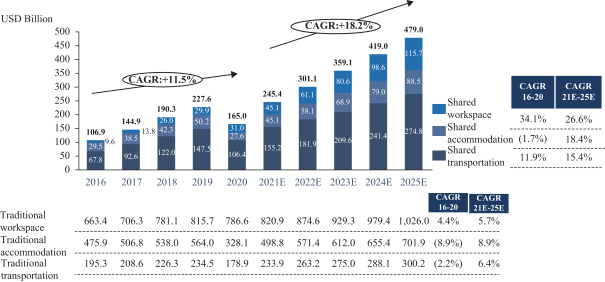

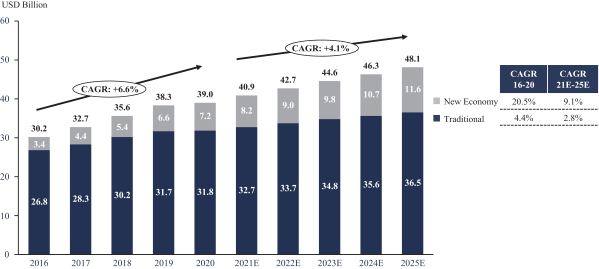

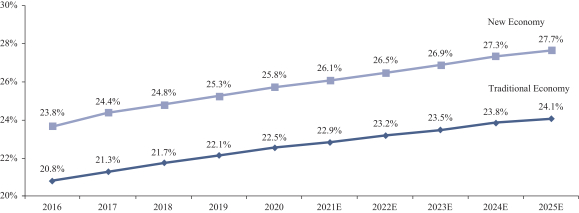

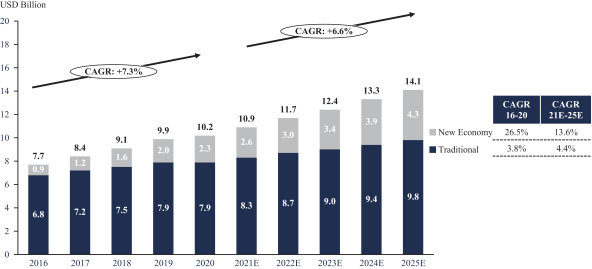

We believe favorable underlying industry trends continue to fuel the growth of our clients. According to Frost & Sullivan, there are a plethora of internet-based technology offshoots driving the new economy growth, including companies in the e-commerce, digital advertising, fintech, online gaming and sharing economy industries. Driven by fundamental shifts in consumer behavior and increased adoption of internet and mobile usage, the global market sizes of retail e-commerce sales, digital advertising spend and sharing economy (by transaction value) are estimated to grow at CAGRs of 14.5%, 15.3% and 18.2% from 2021 through 2025, respectively, as reported by Frost & Sullivan.

We believe our clients view their relationship with us as strategically important. New economy clients increasingly seek customized solutions in an evolving digital business services market that is increasingly becoming more complex. We believe the trend will continue as new economy clients rely on us to perform omnichannel CX solutions so that they can maintain their employee-lite, nimble business models, while we provide a service framework that can scale along with their growth. Furthermore, given their relative lack of physical touchpoints with their end-users, new economy clients tend to place a greater emphasis on the quality of customer experience service providers, where we believe we are strongly positioned. Our digital hiring platform, Flash Hire, enables us to remain agile and keep up with the growth of our high-growth clients by allowing us to rapidly identify, evaluate and hire candidates as needed.

Attractive client base of some of the largest and most disruptive companies in fast-growing industries and markets along with traditional blue-chip companies which are undergoing digital transformations

Our client base consists of some of the leading names in their respective industries, such as Facebook and Airbnb, other fast-growing, new economy companies for which we can scale up projects as they grow, as well as traditional blue-chip companies that rely on us to partner in their digital transformation journey. In the past few years, we have proactively increased our new economy client base, which provides strong growth opportunities for us. As of December 31, 2020, 90% of our agents, which are the customer facing employees that work on our campaigns, were staffed on campaigns for new economy clients.

We seek to forge partnerships and create long-term relationships with our clients, where they view us as an integral part of their organization through the solutions we offer. By growing and partnering with them over the long term, we have expanded the scope of our services and solutions and have become seamlessly integrated into our clients’ operations, while helping them deliver on their brand promise. On a combined basis, Facebook and Airbnb accounted for a total of 52.0%, 65.9% and 60.4% of our revenue for the years ended December 31, 2018, 2019 and 2020, respectively.

Track record of high-growth financial performance

We focus on providing our clients with a differentiated level of service, which we believe enables us to grow our business together with the growth of our clients’ businesses as well as grow our share of our client’s budget. Due to a combination of an increase in the amount of work for existing clients as well as attracting work from new clients, we increased the average number of our agents 118% from 3,701 for 2018 to 8,070 for 2020. During this period, we generated strong revenue, net profit and EBITDA growth at a CAGR of 54.9%, 50.3% and 60.7%, respectively from the year ended December 31, 2018 to the year ended December 31, 2020.

6

Table of Contents

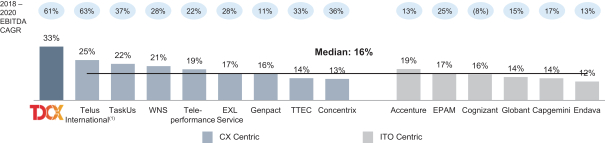

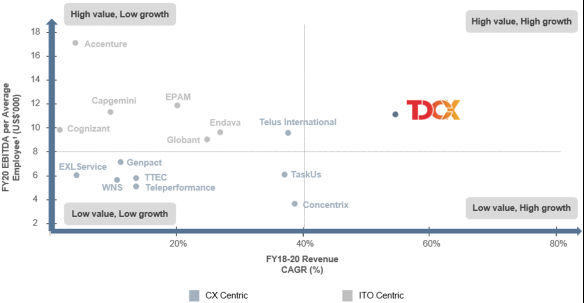

Our ability to provide a differentiated level of service and higher valued and more sophisticated services, while efficiently increasing the scale of our business has resulted in our net profit margin of 21.0%, 22.2% and 19.8% and EBITDA margin of 30.6%, 32.7% and 32.9% for the years ended December 31, 2018, 2019 and 2020, respectively. Our EBITDA margin for 2020 is the highest among CX-centric outsourced service providers, according to Frost & Sullivan.

We have also managed our growth while maintaining a low debt profile. As of December 31, 2018, 2019 and 2020, we had a total debt to EBITDA ratio of 0.6, 0.3 and 0.3, respectively. Our strong balance sheet, combined with our ability to grow our business and generate cash flows, gives us a strong foundation for focused investments and further business expansion.

Dynamic and highly experienced management team

We have an experienced, hands-on and savvy management team who combine global expertise with local insights. Our Founder, Executive Chairman and Chief Executive Officer, Mr. Laurent Bernard Marie Junique, has over 25 years of industry experience and has won numerous awards, including the “Ernst & Young Entrepreneur of the Year in the Outsourced Solutions category” for Singapore in 2018. Our management team has an average of over 15 years of relevant industry experience and most of our senior management have worked with us for over five years, which has allowed us to accumulate valuable operational experience and deep vertical expertise, while building and maintaining close relationships with our key clients. Our management team has been a champion in promoting a vibrant and distinctive culture that emphasizes teamwork, a high degree of flexibility, dedication to the client and alignment with client goals. Under the leadership of our management, we have been able to grow our Company from 1,400 employees as of December 31, 2012, the year we commenced servicing new economy clients, to 11,351 employees as of December 31, 2020.

Our growth strategy

Leverage network effects to expand client coverage and service offerings globally

Our growth strategy is to create a significant network in each of our markets so that we can gain local insights, on-the-ground capabilities and operational experience to expand our client coverage and digital offerings. We intend to achieve this through (i) deepening our relationships with our existing clients, (ii) growing our client base and (iii) extending and “future-proofing” our omnichannel capabilities. We expect the learning and insights from each client will enable us to deepen our expertise in key verticals and further expand our capabilities across service offerings, industries and regions, thereby creating network effects. As we scale and grow our expertise, we expect to penetrate more markets as the impact from our network effects increase.

Deepening our relationships with our existing clients

Our relationships with our new economy clients offer significant opportunities for growth. As we demonstrate the value that we provide, we are frequently able to expand the scale and scope of our services in a variety of ways and grow our wallet share. With our new economy clients’ strong business model scalability, we are well-positioned to ride their growth. We also find opportunities to cross-sell different types of digital offerings and use data analytics to provide integrated insight-driven strategies to help clients improve their business outcomes. In the past, clients who have engaged us for our services have been willing to turn over additional and more critical processes to us as we demonstrate our capabilities over time. As we become more intricately knowledgeable of our clients’ businesses and processes, we find opportunities to expand across the value chain and provide new and increasingly complex digital offerings to them via multiple channels to improve their processes. This in turn encourages client “stickiness” and is a factor that discourages our clients from turning to other providers.

7

Table of Contents

Growing our client base

We seek to develop long-term client relationships with new clients, especially with clients who (i) require similarly complex services as our existing clients, (ii) provide opportunities for us to deliver a wider range of capabilities and meaningful impact to their businesses, and (iii) facilitate robust pipeline development and a strong win-rate of new top-tier clients. We use a multifaceted, technology driven strategy to attract new economy clients.

Extending and “future-proofing” our omnichannel capabilities

We seek to improve our capabilities through continued investments in digital technology and use of third-party technology. We strive to grow our capabilities in future technologies and channels and to continuously evolve with new technology offerings, such as Internet of Things, or IoT, products, wearables and apps, among other areas.

Enhance our human capital and reinforce our distinct corporate culture

Our people are critical to our success. Our ability to grow will depend on our ability to continue to attract, train, and retain large numbers of talented individuals. We continue to focus on maintaining a work environment that would make TDCX an “employer of choice.” We intend to achieve this through various initiatives, including:

| • | working with new economy digital disruptor clients that are the companies of the future; |

| • | utilizing innovative recruiting techniques that will appeal to potential employees including young talent; |

| • | providing training and development throughout the tenure of an employee’s career, such that our employees remain educated and agile to meet our clients’ evolving requirements; |

| • | providing compensation with appropriate incentives that rewards employee commitment, resulting in high standards of customer experience and support for our clients; |

| • | supporting our employees in work from home situations with the technology ecosystem that enables them to remain productive and connected to training opportunities; |

| • | fostering a healthy work environment where employees work hard but have fun; and |

| • | having office locations in areas that are accessible and appealing, with office interior designs that are contemporary, collaborative and inspiring. |

We believe that maintaining a vibrant and distinctive culture is critical to growing our business.

Prudent expansion into new geographic markets

We have a wide footprint of delivery centers in a number of locations across Asia and in Colombia and Spain to serve domestic, regional and global markets and we plan to expand our coverage. As of the date of this prospectus, we had offices in a total of nine geographies, including newly opened offices in Beijing in 2017; Barcelona in 2018; Cebu and Yokohama in 2019; and Bogota, Hyderabad and Shanghai in 2020. The expansion into new locations was driven by our strategy of growing to meet the needs of our existing clients, such as our clients expanding into new markets or seeking to replace their existing service providers. Since adding offices in these locations, we have also added new clients based in these countries, as well as internationally who have been attracted by our increased geographical capacities. We intend to continue to expand our footprint prudently, but rapidly, to ensure we can meet the evolving needs of our clients, including processes requiring multi-jurisdictional and multi-lingual capabilities, and better position ourselves to win new engagements from our existing clients and attract new clients.

8

Table of Contents

In addition to expansion in recently entered markets, we have identified Eastern Europe, Korea and other Chinese regional markets where we do not currently operate as potential new markets for entry. In 2020, we established a new office in Hyderabad, India as an entry point to the Indian market and to serve as our hub for digital innovation, established an office in Bogota, Colombia in 2020 as an initial office marking our entrance into the Latin America market, and grew our China presence by establishing an office in Shanghai. We also intend to open an office in the Republic of Korea by 2022 and are exploring a potential opportunity to open an additional office in Europe as well. While there are no current operations in our offices in India and Colombia, we expect to begin operations in each in 2021. Key location criteria for setting up new offices include (i) the ability to tap a wide talent pool that has the desired skills to better cater to client requirements, (ii) minimal time zone difference with, and proximity to, existing and potential clients, and (iii) cost competitiveness.

Maintain operational efficiencies through streamlined operations

We strive to be a productive and efficient operator. For example, we utilize digital recruiting techniques, such as our Flash Hire platform, to minimize recruiting costs and improve candidate selection accuracy. We are also adept at educating and developing our employees, through our TDU online learning platform of online courses and learning opportunities, which is a fast and flexible way to train our workforce across multiple geographies. Our innovative digital operating platform, Flash, which we had implemented prior to the COVID-19 pandemic, has enabled us to continue to implement our growth strategy in new markets despite social distancing restrictions on in-person meetings and training sessions. We have business excellence teams that review our standard operating procedures, design customer interaction playbooks and gather and implement best practices across the organization. Larger campaigns also have campaign-specific materials developed to meet specific client needs. In addition, insights gained through our data analytics capabilities also help us optimize staffing levels, track key performance indicators and employee engagement, and enhance workforce management to realize operational efficiencies. As we grow in scale, we intend to further centralize our procurement processes for our infrastructure, technology, telecommunication equipment and professional services in order to lower costs and streamline supplier relationships.

Prudent strategic acquisitions and opportunistic partnerships

We plan to continue to expand our capabilities globally as well as across industry verticals and service offerings. While we expect this will primarily occur through organic growth, from time to time, we expect to selectively evaluate strategic partnerships, alliances and acquisitions to develop or acquire:

| • | new clients within our existing client verticals, with minimal overlap with existing clients; |

| • | new client verticals with high growth potential, such as industries where demand exceeds our ability to scale our business organically and other industries such as in financial technology, digital marketing and gaming; |

| • | new language capabilities to enter into new, large and diverse markets such as Europe and Latin America; and |

| • | new operational capabilities which can improve our efficiencies and complement our existing offerings, including the ability to introduce new offerings. |

We believe that our strong balance sheet combined with our ability to grow our business and generate cash flows gives us a strong foundation for focused investments and further business expansion.

9

Table of Contents

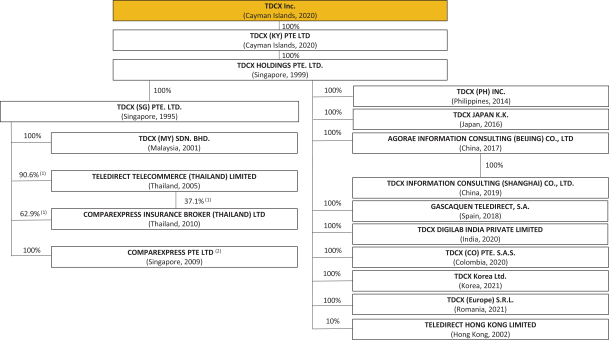

The chart below sets out our corporate structure as of the date of this prospectus.

| (1) | Effective ownership (voting powers). |

| (2) | Dormant entity |

Risks Related to Our Business and Industry

Below are certain risks associated with our business and industry. These risks are described in the section titled “Risk Factors”. These risks include the following:

| • | Our largest clients account for a significant portion of our total revenue and any loss of a large portion of business from any of those large clients could have a material adverse effect on our business, financial condition and results of operations; |

| • | Our failure to successfully implement our business strategy and global, growth-oriented business model and sustain our growth rate and financial performance could harm our business; |

| • | We operate in a highly competitive environment, and any failure to compete effectively against current and future competitors could adversely affect our revenue and profitability; |

| • | Our profitability will suffer if we are not able to maintain our pricing, control costs or continue to grow our business through higher value campaigns; |

| • | Effects of the novel coronavirus (COVID-19) as well as any other health pandemics on our and our clients’ business and operations could adversely affect our financial results; |

| • | Our success depends on the continued service of our Founder and certain of our key employees and management; |

| • | We may fail to attract and retain enough highly trained employees to support our operations; |

10

Table of Contents

| • | A substantial portion of our operations and investments are located in Southeast Asia and we are therefore exposed to various risks inherent in operating and investing in the region; |

| • | Our key clients have significant leverage over our contractual terms and may terminate such contracts on short notice or require us to accept contractual terms that are more favorable to them; |

| • | Spending on omnichannel CX solutions by our clients and prospective clients is subject to fluctuations depending on many factors, including both the economic and regulatory environments in the markets in which they operate; |

| • | Increases in employee salaries and benefits expenses as well as changes to labor laws could affect our business; |

| • | We may be involved in disputes, legal, regulatory, and other proceedings arising out of our business operations, and may incur costs arising therefrom and may be affected by negative publicity which may have an adverse impact on our reputation and goodwill; |

| • | We may enter into contracts with significant fixed price elements or solely fixed price contracts with our clients and any failure to accurately price these arrangements may affect our profitability; |

| • | If our services do not comply with the service level and performance requirements required by our clients or we are in breach of our obligations under our contracts with our clients, it may result in reduced payments or the termination of our client agreements; |

| • | We are subject to risks associated with operating in the rapidly evolving new economy sectors; |

| • | We and our clients are subject to privacy, data protection and information security laws in the jurisdictions in which we and our clients operate; and |

| • | Our inability to protect our systems and data from continually evolving cybersecurity risks or other technological risks could affect our reputation among our clients and their customers and may expose us to liability. |

Corporate Information

We were incorporated in the Cayman Islands on April 16, 2020 as TDCX Capital Pte Ltd and subsequently changed our name to TDCX Inc. on January 29, 2021. Our registered office in the Cayman Islands is at the offices of Maples Corporate Services Limited, PO Box 309, Ugland House, Grand Cayman, KY1-1104, Cayman Islands. Our principal executive offices is at 750D Chai Chee Road, #06-01/06 ESR BizPark @ Chai Chee, Singapore, Singapore 469004. Our telephone number at this location is +65 6309 1688. Our principal website address is www.tdcx.com. The information contained on our website does not form part of this prospectus. Our agent for service of process in the United States is , located at .

Because we are incorporated under the laws of the Cayman Islands, you may encounter difficulty protecting your interests as shareholder, and your ability to protect your rights through the U.S. federal court system may be limited. Please refer to the sections entitled “Risk Factors” and “Enforceability of Civil Liabilities” for more information.

Implications of Being a “Controlled Company”

Upon the completion of this offering, Mr. Laurent Bernard Marie Junique, our Founder, Executive Chairman and Chief Executive Officer, will be the beneficial owner of an aggregate of ordinary shares, which will represent % of the then total outstanding ordinary shares and % of the total voting power of our outstanding ordinary shares % of the then total outstanding ordinary shares and % of the total voting

11

Table of Contents

power of our outstanding ordinary shares if the underwriters exercise their option to purchase additional ADSs in full. As a result, we will remain a “controlled company” within the meaning of the NYSE listing rules and therefore we are eligible for, and, in the event we no longer qualify as a foreign private issuer, we intend to rely on, certain exemptions from the corporate governance listing requirements of the NYSE.

Implications of Being an Emerging Growth Company

As a company with less than US$1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company” as defined in the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. An emerging growth company may take advantage of specified reduced reporting and other requirements that are otherwise applicable generally to public companies. These provisions include:

| • | being permitted to provide only two years of selected financial information (rather than five years) and only two years of audited financial statements (rather than three years), in addition to any required unaudited interim financial statements, with correspondingly reduced “Management’s Discussion and Analysis of Financial Condition and Results of Operations” disclosure; and |

| • | an exemption from compliance with the auditor attestation requirement of the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act, on the effectiveness of our internal control over financial reporting. |

We may take advantage of these reporting exemptions until we are no longer an emerging growth company. We will remain an emerging growth company until the earliest of (1) the last day of the fiscal year in which the fifth anniversary of the completion of this offering occurs, (2) the last day of the fiscal year in which we have total annual gross revenue of at least US$1.07 billion, (3) the date on which we are deemed to be a “large accelerated filer” under the Securities Exchange Act of 1934, as amended, or the Exchange Act, which means the market value of our ordinary shares that is held by non-affiliates exceeds US$700.0 million as of the prior June 30, and (4) the date on which we have issued more than US$1.0 billion in non-convertible debt during the prior three-year period. We may choose to take advantage of some, but not all, of the available exemptions. We have included three years of selected financial data in this prospectus in reliance on the first exemption described above. Accordingly, the information contained herein may be different than the information you receive from other public companies in which you hold stock.

Implications of Being a Foreign Private Issuer

Upon completion of this offering, we will report under the Exchange Act as a non-U.S. company with foreign private issuer status. Even after we no longer qualify as an emerging growth company, as long as we qualify as a foreign private issuer under the Exchange Act, we will be exempt from certain provisions of the Exchange Act that are applicable to U.S. domestic public companies, including:

| • | the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations in respect of a security registered under the Exchange Act; |

| • | the sections of the Exchange Act requiring insiders to file public reports of their stock ownership and trading activities and liability for insiders who profit from trades made in a short period of time; and |

| • | the rules under the Exchange Act requiring the filing with the Securities and Exchange Commission, or the SEC, of quarterly reports on Form 10-Q containing unaudited financial and other specified information, or current reports on Form 8-K, upon the occurrence of specified significant events. |

Both foreign private issuers and emerging growth companies are also exempt from certain more stringent executive compensation disclosure rules. Thus, even if we no longer qualify as an emerging growth company but remain a foreign private issuer, we will continue to be exempt from the more stringent compensation disclosures required of companies that are neither emerging growth companies nor foreign private issuers.

12

Table of Contents

The Offering

| Offering price |

We currently estimate that the initial public offering price will be between US$ and US$ per ADS. |

| ADSs offered by us |

ADSs (or ADSs if the underwriters exercise the over-allotment option in full). |

| ADSs offered by our selling shareholders |

ADSs. |

| ADSs outstanding immediately after this offering |

ADSs (or ADSs if the underwriters exercise the over-allotment option in full). |

| Ordinary shares outstanding immediately after this offering (includes ordinary shares represented by ADSs) |

ordinary shares (or ordinary shares if the underwriters exercise the over-allotment option in full), comprising Class A ordinary shares (or Class A ordinary shares if the underwriters exercise the over-allotment option in full) and Class B ordinary shares. |

| Class B ordinary shares issued and outstanding immediately after the completion of the offering will represent % of our total issued and outstanding ordinary shares and % of the then total voting power (or % of our total issued and outstanding ordinary shares and % of the then total voting power if the underwriters exercise the over-allotment option in full). |

| The ADSs |

Each ADS represents Class A ordinary shares. |

| The depositary or its nominee will hold Class A ordinary shares underlying your ADSs. You will have rights as provided in the deposit agreement among us, the depositary and holders and beneficial owners of ADSs from time to time. |

| We do not expect to pay dividends in the foreseeable future. If, however, we declare dividends on our Class A ordinary shares, the depositary will pay you the cash dividends and other distributions it receives on our Class A ordinary shares after deducting its fees and expenses in accordance with the terms set forth in the deposit agreement. |

| You may surrender your ADSs to the depositary in exchange for Class A ordinary shares in accordance with the terms of the deposit agreement. The depositary will charge you fees for any exchange. |

| We may amend or terminate the deposit agreement without your consent. If you continue to hold your ADSs after an amendment to the deposit agreement, you agree to be bound by the deposit agreement as amended. |

13

Table of Contents

| To better understand the terms of the ADSs, you should carefully read the “Description of American Depositary Shares” section of this prospectus. You should also read the deposit agreement, which is filed as an exhibit to the registration statement that includes this prospectus. |

| Ordinary shares |

Our ordinary shares will consist of Class A ordinary shares and Class B ordinary shares immediately prior to the completion of this offering. Holders of Class A ordinary shares and Class B ordinary shares have the same rights except for voting and conversion rights. Each Class A ordinary share is entitled to one vote; each Class B ordinary share is entitled to ten votes and is convertible into one Class A ordinary share at any time by the holder thereof. Class A ordinary shares are not convertible into Class B ordinary shares under any circumstances. Upon any transfer of beneficial ownership of Class B ordinary shares by a holder thereof to any person or entity which is not an affiliate of such holder, such Class B ordinary shares shall be automatically and immediately converted into the same number of Class A ordinary shares. For a description of Class A ordinary shares and Class B ordinary shares, see “Description of Share Capital.” |

| Over-allotment option |

We [and the Selling Shareholder] have granted to the underwriters an option, exercisable for 30 days from the date of this prospectus, to purchase up to an aggregate of additional ADSs at the initial public offering price, less underwriting discounts and commissions, solely for the purpose of covering over-allotments. |

| Use of proceeds |

We expect that we will receive net proceeds from this offering of approximately US$ million, or approximately US$ million if the underwriters exercise their option to purchase additional ADSs from us in full, assuming an initial public offering price of US$ per ADS, the mid-point of the estimated range of the initial public offering price set forth on the cover of this prospectus, after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

| We plan to use the net proceeds of this offering as follows: US$[188.0] million to repay amounts outstanding under the Credit Suisse Facility, and the remainder to enable us to expand our business into new markets, which would include costs for premises, technology and systems and other infrastructure as well as for hiring of personnel and other expansion related expenses, and for general corporate purposes, including working capital needs and potential acquisitions. |

| We will not receive any of the proceeds from the sale of the ADSs by the selling shareholders. |

| Conflicts of Interest |

Because an affiliate of Credit Suisse Securities (USA) LLC, which is an underwriter in this offering, is the lender under the Credit Suisse Facility and will receive 5% or more of the net proceeds from this |

14

Table of Contents

| offering due to the repayment of the Credit Suisse Facility, Credit Suisse Securities (USA) LLC is deemed to have a conflict of interest within the meaning of Rule 5121 of the Financial Industry Regulatory Authority, Inc., or FINRA. Therefore, this offering will be conducted in accordance with FINRA Rule 5121, which requires, among other things, that a qualified independent underwriter has participated in the preparation of, and has exercised the usual standards of ‘‘due diligence’’ with respect to, this prospectus and the registration statement of which this prospectus forms a part. Goldman Sachs & Co. LLC has agreed to act as qualified independent underwriter for the offering and to undertake the legal responsibilities and liabilities of an underwriter under the Securities Act, specifically including those inherent in Section 11 of the Securities Act. We will agree to indemnify Goldman Sachs & Co. LLC against liabilities incurred in connection with acting as qualified independent underwriter, including liabilities under the Securities Act. See “Use of Proceeds” and “Underwriting.” |

| Dividend policy |

We do not intend to pay any dividends on our ordinary shares or ADSs for the foreseeable future. Instead, we anticipate that all of our earnings, if any, will be used for the operation and growth of our business. See “Dividends and Dividend Policy” for more information. |

| Lock-up |

We and each of our directors, executive officers and existing shareholders have agreed, subject to certain exceptions, for a period of [180] days after the date of this prospectus, not to, except in connection with this offering, offer, pledge, sell, contract to sell, sell any option or contract to purchase, purchase any option or contract to sell, grant any option, right or warrant to purchase, lend, or otherwise transfer or dispose of, directly or indirectly, any ADSs or ordinary shares or any other securities so owned convertible into or exercisable or exchangeable for ADSs or ordinary shares, or enter into any swap or other arrangement that transfers to another, in whole or in part, any of the economic consequences of ownership of the ADSs or ordinary shares. See “Shares Eligible for Future Sale” and “Underwriting.” |

| Risk factors |

See “Risk Factors” and other information included in this prospectus for a discussion of factors you should carefully consider before deciding to invest in our ADSs. |

| Payment and settlement |

The ADSs are expected to be delivered against payment on , 2021. The ADSs will be deposited with a custodian for, and registered in the name of a nominee of, , or , in New York, New York. In general, beneficial interests in the ADSs will be shown on, and transfers of those beneficial interests will be effected only through, records maintained by and its direct and indirect participants. |

| Listing |

We will apply to list our ADSs on the NYSE. |

| Proposed trading symbol |

15

Table of Contents

| Depositary |

| (1) | As of , 2021, there were Class A ordinary shares outstanding. |

| (2) | Except as otherwise indicated, all information in this prospectus assumes: |

| • | the adoption and effectiveness of our amended and restated memorandum and articles of association, which will occur immediately prior to the completion of this offering; and |

| • | no exercise by the underwriters of the over-allotment option to purchase up to an additional ADSs representing Class A ordinary shares from us [and certain selling shareholders.] |

16

Table of Contents

Summary Consolidated Financial and Other Data

The following summary consolidated financial data as of December 31, 2019 and 2020 and for the years ended December 31, 2018, 2019 and 2020 have been derived from our audited consolidated financial statements included elsewhere in this prospectus. The summary financial data as of December 31, 2018 is derived from audited financial statements not included herein. The summary financial data set forth below should be read in conjunction with, and are qualified by reference to, “Selected Consolidated Financial and Other Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and notes thereto included elsewhere in this prospectus. Our consolidated financial statements are prepared and presented in accordance with IFRS as issued by the IASB. Our historical results do not necessarily indicate results expected for any future period.

Summary Consolidated Statement of Profit or Loss and Other Comprehensive Income

| For the Year Ended December 31, | ||||||||||||||||

| 2020 | 2019 | 2018 | ||||||||||||||

| S$ | US$ | S$ | S$ | |||||||||||||

| (in thousands) | ||||||||||||||||

| Revenue |

434,723 | 328,812 | 330,265 | 181,233 | ||||||||||||

| Employee benefits expense |

(257,985 | ) | (195,133 | ) | (189,912 | ) | (109,373 | ) | ||||||||

| Depreciation expense |

(33,065 | ) | (25,009 | ) | (24,599 | ) | (12,908 | ) | ||||||||

| Rental and maintenance expense |

(10,603 | ) | (8,020 | ) | (9,220 | ) | (2,623 | ) | ||||||||

| Recruitment expense |

(8,005 | ) | (6,055 | ) | (6,680 | ) | (3,792 | ) | ||||||||

| Transport and travelling expense |

(1,504 | ) | (1,138 | ) | (2,083 | ) | (1,358 | ) | ||||||||

| Telecommunication and technology expense |

(6,305 | ) | (4,769 | ) | (4,522 | ) | (2,385 | ) | ||||||||

| Interest expense |

(3,058 | ) | (2,313 | ) | (2,893 | ) | (1,128 | ) | ||||||||

| Other operating expense |

(15,836 | ) | (11,978 | ) | (10,478 | ) | (6,872 | ) | ||||||||

| Gain on disposal of a subsidiary |

731 | 553 | — | — | ||||||||||||

| Share of profit from an associate |

196 | 148 | — | — | ||||||||||||

| Interest income |

594 | 449 | 465 | 268 | ||||||||||||

| Other operating income |

7,514 | 5,683 | 717 | 546 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Profit before income tax |

107,397 | 81,230 | 81,060 | 41,608 | ||||||||||||

| Income tax expenses |

(21,303 | ) | (16,113 | ) | (7,524 | ) | (3,520 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Profit for the year |

86,094 | 65,117 | 73,536 | 38,088 | ||||||||||||

| Other comprehensive income (loss)(1) |

536 | 405 | 840 | (71 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total comprehensive income for the year |

86,630 | 65,522 | 74,376 | 38,017 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Basic and diluted earnings per share |

86,093 | 65,116 | 73,535 | 35,271 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Pro forma basic and diluted earnings per share(2) |

||||||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

Note:

| (1) | Other comprehensive income (loss) includes remeasurement of retirement benefit obligation and exchange differences on translation of foreign operations. |

| (2) | Unaudited basic and diluted pro forma net income (loss) per share data assumes that an additional of our shares of common stock were outstanding for the [three months period ended March 31, 2021], which represents the number of shares of common stock that we expect to be issued to fund the debt repayment with the net proceeds of this offering as described in “Use of Proceeds.” The number of shares of common stock that we expect to be issued to fund the debt repayment was calculated in accordance with Staff Accounting Bulletin Topic 3.A. by dividing $ million, which is the estimated cost to repay indebtedness with the proceeds of this offering as described in “Use of Proceeds,” by $ per share, the low end of the initial public offering price range included on the cover of this prospectus less underwriting discounts and commissions. |

17

Table of Contents

Summary Consolidated Statement of Financial Position

| As of December 31, | ||||||||||||||||

| 2020 | 2019 | 2018 | ||||||||||||||

| S$ | US$ | S$ | S$ | |||||||||||||

| (in thousands) | ||||||||||||||||

| ASSETS |

||||||||||||||||

| Current assets |

||||||||||||||||

| Cash and cash equivalents |

59,807 | 45,237 | 35,920 | 23,973 | ||||||||||||

| Fixed deposits |

7,727 | 5,844 | 837 | — | ||||||||||||

| Trade receivables |

36,919 | 27,925 | 55,278 | 27,605 | ||||||||||||

| Contract assets |

46,842 | 35,430 | 26,523 | 18,605 | ||||||||||||

| Other receivables |

12,257 | 9,271 | 9,210 | 5,392 | ||||||||||||

| Tax recoverable |

— | — | — | 350 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total current assets |

163,552 | 123,707 | 127,768 | 75,925 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Non-current assets |

||||||||||||||||

| Pledged deposits |

2,377 | 1,798 | 2,110 | 2,096 | ||||||||||||

| Other receivables |

5,874 | 4,443 | 3,708 | 2,931 | ||||||||||||

| Plant and equipment |

40,581 | 30,694 | 40,730 | 24,911 | ||||||||||||

| Right-of-use assets |

29,221 | 22,102 | 22,840 | 18,586 | ||||||||||||

| Loan to an associate |

— | — | 784 | — | ||||||||||||

| Deferred tax assets |

1,580 | 1,195 | 1,197 | 329 | ||||||||||||

| Investment in an associate |

229 | 173 | 33 | 33 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total non-current assets |

79,862 | 60,405 | 71,402 | 48,886 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total assets |

243,414 | 184,112 | 199,170 | 124,811 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| LIABILITIES AND EQUITY |

||||||||||||||||

| Current liabilities |

||||||||||||||||

| Other payables |

37,200 | 28,137 | 26,926 | 15,870 | ||||||||||||

| Amount due to a director |

— | — | — | 10,469 | ||||||||||||

| Bank loans |

24,170 | 18,282 | 34,421 | 6,374 | ||||||||||||

| Lease liabilities |

14,664 | 11,091 | 10,963 | 7,634 | ||||||||||||

| Provision for reinstatement cost |

452 | 342 | — | — | ||||||||||||

| Income tax payable |

13,257 | 10,027 | 6,956 | 3,229 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total current liabilities |

89,743 | 67,879 | 79,266 | 43,575 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Non-current liabilities |

||||||||||||||||

| Bank loans |

16,136 | 12,205 | — | 24,174 | ||||||||||||

| Lease liabilities |

17,823 | 13,481 | 14,498 | 12,495 | ||||||||||||

| Provision for reinstatement cost |

5,617 | 4,249 | 4,955 | 1,817 | ||||||||||||

| Defined benefit obligation |

1,435 | 1,085 | 769 | 315 | ||||||||||||

| Deferred tax liabilities |

129 | 98 | 236 | 365 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total non-current liabilities |

41,140 | 31,118 | 20,458 | 39,167 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Capital, reserves and non-controlling interest |

||||||||||||||||

| Share capital |

* | * | * | * | ||||||||||||

| Reserves |

(19,843 | ) | (15,009 | ) | (20,650 | ) | (21,604 | ) | ||||||||

| Retained earnings |

132,371 | 100,122 | 120,094 | 63,673 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Equity attributable to owners of the Group |

112,528 | 85,113 | 99,444 | 42,069 | ||||||||||||

| Non-controlling interests |

3 | 2 | 2 | 1 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total equity |

112,531 | 85,115 | 99,446 | 42,070 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total liabilities and equity |

243,414 | 184,112 | 199,170 | 124,811 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| * | Amount is less than $1,000 |

18

Table of Contents

Summary Consolidated Statement of Cash Flows

| For the Year

Ended December 31, |

||||||||||||||||

| 2020 | 2019 | 2018 | ||||||||||||||

| S$ | US$ | S$ | S$ | |||||||||||||

| (Restated) | ||||||||||||||||

| (in thousands) | ||||||||||||||||

| Net cash from operating activities |

130,484 | 98,695 | 76,044 | 37,320 | ||||||||||||

| Net cash used in investing activities |