viewed or interpreted as giving preference to the Company’s Public Stockholders over any potential creditors with respect to access to or distributions from the Company’s assets. Furthermore, the LCAP Board may be viewed as having breached their fiduciary duties to the Company’s creditors and/or may have acted in bad faith, and thereby exposing itself and the Company to claims of punitive damages, by paying Public Stockholders from the Trust Account prior to addressing the claims of creditors. The Company cannot assure you that claims will not be brought against it for these reasons.

Risks Related to the Committed Equity Facility

It is not possible to predict the actual number of shares we will sell under the Purchase Agreement to CF Principal Investments LLC, or the actual gross proceeds resulting from those sales.

On May 17, 2022, we entered into the Purchase Agreement with CF Principal Investments LLC, pursuant to which CF Principal Investments LLC has committed to purchase up to $1 billion in Common Shares, subject to certain limitations and conditions set forth in the Purchase Agreement. Our Common Shares that may be issued under the Purchase Agreement may be sold by us to CF Principal Investments LLC at our discretion from time to time over the 36-month period commencing on the date the registration statement becomes effective.

We generally have the right to control the timing and amount of any sales of our Common Shares to CF Principal Investments LLC under the Purchase Agreement. Sales of our Common Shares, if any, to CF Principal Investments LLC under the Purchase Agreement will depend upon market conditions and other factors to be determined by us. We may ultimately decide to sell to CF Principal Investments LLC all, some or none of the Common Shares that may be available for us to sell to CF Principal Investments LLC pursuant to the Purchase Agreement.

Because the purchase price per share to be paid by CF Principal Investments LLC for the Common Shares that we may elect to sell to CF Principal Investments LLC under the Purchase Agreement, if any, will fluctuate based on the market prices of our Common Shares at the time we elect to sell shares to CF Principal Investments LLC pursuant to the Purchase Agreement, if any, it is not possible for us to predict, as of the date of this Current Report and prior to any such sales, the number of Common Shares that we will sell to CF Principal Investments LLC under the Purchase Agreement, the purchase price per share that CF Principal Investments LLC will pay for shares purchased from us under the Purchase Agreement, or the aggregate gross proceeds that we will receive from those purchases by CF Principal Investments LLC under the Purchase Agreement.

Investors who buy shares at different times will likely pay different prices.

Pursuant to the Purchase Agreement, we will have discretion, subject to market demand, to vary the timing, prices, and numbers of shares sold to CF Principal Investments LLC. If and when we do elect to sell our Common Shares to CF Principal Investments LLC pursuant to the Purchase Agreement, after CF Principal Investments LLC has acquired such shares, CF Principal Investments LLC may resell all, some or none of such shares at any time or from time to time in its discretion and at different prices. As a result, investors who purchase shares from CF Principal Investments LLC at different times will likely pay different prices for those shares, and so may experience different levels of dilution and in some cases substantial dilution and different outcomes in their investment results. Investors may experience a decline in the value of the shares they purchase from CF Principal Investments LLC as a result of future sales made by us to CF Principal Investments LLC at prices lower than the prices such investors paid for their shares. In addition, if we sell a substantial number of shares to CF Principal Investments LLC under the Purchase Agreement, or if investors expect that we will do so, the actual sales of shares or the mere existence of our arrangement with CF Principal Investors LLC may make it more difficult for us to sell equity or equity-related securities in the future at a time and at a price that we might otherwise wish to effect such sales.

Unaudited Pro Forma Condensed Combined Financial Information

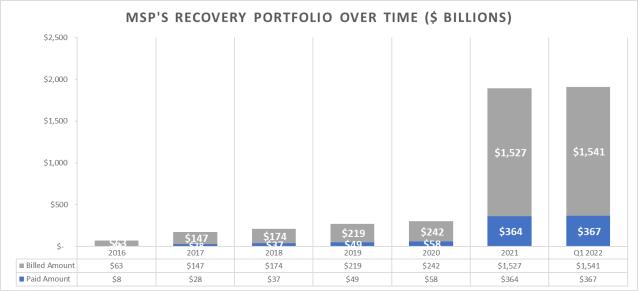

The unaudited pro forma condensed combined financial information of the Company as of and for the three months ended March 31, 2022 and for the year ended December 31, 2021 is included in as Exhibit 99.1 of this current report.

Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis provides information that MSP Recovery, Inc.’s management believes is relevant to an assessment and understanding of the Company’s combined and consolidated results of operations and financial condition. The discussion should be read together with “The Company’s Historical Financial Information” and the historical audited annual combined and consolidated financial statements as of and for the years ended December 31, 2021 and 2020 and unaudited interim condensed combined and consolidated financial statements as of March 31, 2022 and the three-month periods ended March 31, 2022 and 2021, and the related respective notes thereto, included elsewhere in this Current Report. The discussion and analysis should also be read together with the Company’s unaudited pro forma financial information for the year ended December 31, 2021 and the three months ended March 31, 2022. See “Unaudited Pro Forma Condensed Combined Financial Information.” This discussion may contain forward-looking statements based upon the Company’s current expectations, estimates and projections that involve risks and uncertainties. Actual results could differ materially from those anticipated in these forward-looking statements due to, among other considerations, the matters discussed under “Risk Factors” and “Cautionary Note Regarding Forward-Looking Statements.” Unless the context otherwise requires, all references in this subsection to “We”, “the Company” or “MSP” refers to the business of the MSP Companies prior to the consummation of the Business Combination, which is now the business of the Company and its subsidiaries following the consummation of the Business Combination.’

Our Business

We are a leading healthcare recoveries and data analytics company. We focus on the Medicare, Medicaid and commercial insurance spaces. We are disrupting the antiquated healthcare reimbursement system, using data and analytics to identify and recover improper payments made by Medicare, Medicaid, and Commercial Health Insurers.

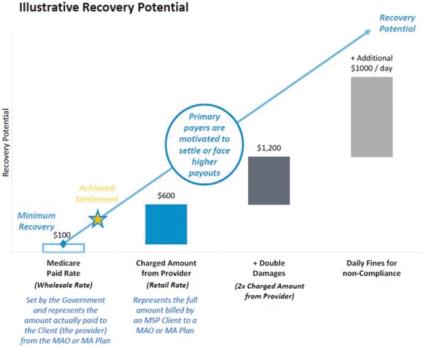

Medicare and Medicaid are payers of last resort. Too often, they end up being the first and only payer, because the responsible payer is not identified or billed. Because Medicare and Medicaid pay a far lower rate than what other insurers are often billed, this costs the healthcare system (and the supporting taxpayers) tens of billions a year in improper billing and lost recoveries. By discovering, quantifying and settling the billed-to-paid gap on a large scale basis, MSP is positioned to generate meaningful annual recovery revenue at high profit margins.

Our access to large volumes of data, sophisticated data analytics, and a leading technology platform provide a unique opportunity to discover and recover claims. We have developed over 1,400 proprietary algorithms which help identify billions in waste, fraud, and abuse in the Medicare, Medicaid, and Commercial Health Insurance segments. Our deep team of data scientists and medical professionals analyze historical medical claims data to identify recoverable opportunities. Once these potential recoveries are reviewed by our team, they are aggregated and pursued. Through federal statutory law and a series of legal cases and precedents, we believe we have an established basis for future recoveries.

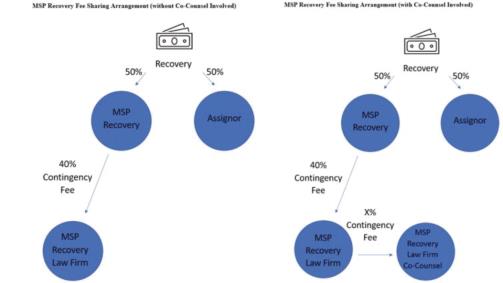

We differ from some of our competitors because we receive our recovery rights through irrevocable assignments of claims. When we are assigned these rights, we take on a risk that our competitors do not. Rather than provide services under a third-party vendor services contract, we receive the rights to certain recovery proceeds from our Assignors’ claims (and, in many cases, actually take assignment of the claims themselves, which allow us to step into the Assignor’s shoes). In the instances where we take Claims by assignment, we have total control over the direction of the litigation. We would be the plaintiff in any action filed and would have total control over the