Table of Contents

As filed with the Securities and Exchange Commission on July 6, 2021

Registration No. 333-253969

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

POST-EFFECTIVE

AMENDMENT NO. 1

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

E2open Parent Holdings, Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware |

7372 | 86-1874570 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

9600 Great Hills Trail, Suite 300E

Austin, Texas 78759

(866) 432-6736

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Laura Fese

Executive Vice President and General Counsel

E2open Parent Holdings, Inc.

9600 Great Hills Trail, Suite 300E

Austin, Texas 78759

(866) 432-6736

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

Copy to:

Morgan D. Elwyn

Claire E. James

Willkie Farr & Gallagher LLP

787 Seventh Avenue

New York, New York 10019

(212) 728-8000

Approximate date of commencement of proposed sale to the public: From time to time after this Registration Statement becomes effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ | |||

| Emerging growth company | ☒ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

EXPLANATORY NOTE

This Post-Effective Amendment No. 1 to the Registration Statement on Form S-1 (File No. 333-253969) (the “Registration Statement”) of E2open Parent Holdings, Inc., as originally declared effective by the Securities and Exchange Commission (the “SEC”) on March 29, 2021, is being filed pursuant to the undertakings in Item 17 of the Registration Statement to (i) include the information contained in registrant’s Annual Report on Form 10-K for the fiscal year ended February 28, 2021, that was filed with the SEC on May 20, 2021, (ii) include the audited consolidated financial statements of BluJay Topco Limited for the years ended March 31, 2021 and March 31, 2020, and (iii) update certain other information in the Registration Statement.

The information included in this filing amends the Registration Statement and the prospectus contained therein. No additional securities are being registered under this Post-Effective Amendment No. 1. All applicable registration fees were paid at the time of the original filing of the Registration Statement.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion, dated July 6, 2021

Preliminary Prospectus

205,042,231 Shares of Class A Common Stock

15,280,000 Warrants to Purchase Class A Common Stock

This prospectus relates to: (1) the issuance by us of up to 29,079,972 shares of our Class A Common Stock, par value $0.0001 per share (“Class A Common Stock”), that may be issued upon exercise of warrants to purchase Class A Common Stock at an exercise price of $11.50 per share of Class A Common Stock, including the Public Warrants, the Private Placement Warrants and the Forward Purchase Warrants (each as defined under “Frequently Used Terms”); and (2) the offer and sale, from time to time, by the selling holders identified in this prospectus (the “Selling Holders”), or their permitted transferees, of (i) up to 205,042,231 shares of Class A Common Stock and (ii) up to 15,280,000 Private Placement Warrants and Forward Purchase Warrants.

This prospectus provides you with a general description of such securities and the general manner in which we and the Selling Holders may offer or sell the securities. More specific terms of any securities that we and the Selling Holders may offer or sell may be provided in a prospectus supplement that describes, among other things, the specific amounts and prices of the securities being offered and the terms of the offering. The prospectus supplement may also add, update or change information contained in this prospectus.

We will not receive any proceeds from the sale of shares of Class A Common Stock or Warrants by the Selling Holders pursuant to this prospectus or of the shares of Class A Common Stock by us pursuant to this prospectus, except with respect to amounts received by us upon exercise of the Warrants to the extent such Warrants are exercised for cash. However, we will pay the expenses, other than underwriting discounts and commissions, associated with the sale of securities pursuant to this prospectus.

Our registration of the securities covered by this prospectus does not mean that either we or the Selling Holders will issue, offer or sell, as applicable, any of the securities. The Selling Holders may offer and sell the securities covered by this prospectus in a number of different ways and at varying prices. We provide more information about how the Selling Holders may sell the shares in the section entitled “Plan of Distribution.” In addition, certain of the securities being registered hereby are subject to vesting and/or transfer restrictions that may prevent the Selling Holders from offering or selling such securities upon the effectiveness of the registration statement of which this prospectus is a part. See “Description of Securities” for more information.

You should read this prospectus and any prospectus supplement or amendment carefully before you invest in our securities. Our Class A Common Stock is listed on The New York Stock Exchange under the symbol “ETWO.” On July 2, 2021, the last reported sale price of our Class A Common Stock on The New York Stock Exchange was $11.54 per share.

Investing in our Class A Common Stock involves a high degree of risk. See the section titled “Risk Factors” beginning on page 31.

Neither the Securities and Exchange Commission nor any other state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2021.

Table of Contents

| Page | ||||

| 1 | ||||

| 3 | ||||

| 12 | ||||

| 14 | ||||

| Selected Unaudited Pro Forma Condensed Combined Financial Information |

27 | |||

| 31 | ||||

| 60 | ||||

| Unaudited Pro Forma Condensed Combined Financial Information |

61 | |||

| Management’s Discussion and Analysis of CCNB1’s Financial Condition and Results of Operations |

78 | |||

| Management’s Discussion and Analysis of E2open’s Financial Condition and Results of Operations |

85 | |||

| 121 | ||||

| 134 | ||||

| 141 | ||||

| 147 | ||||

| 150 | ||||

| Selling Holders |

153 | |||

| 163 | ||||

| 179 | ||||

| Material United States Federal Income and Estate Tax Consequences to Non-U.S. Holders |

181 | |||

| 184 | ||||

| 189 | ||||

| 189 | ||||

| 189 | ||||

| 190 | ||||

| F-1 | ||||

Table of Contents

This prospectus is part of a registration statement on Form S-1 that we filed with the SEC using a “shelf” registration process. Under this shelf registration process, we and the Selling Holders may, from time to time, issue, offer and sell, as applicable, any combination of the securities described in this prospectus in one or more offerings. We may use the shelf registration statement to issue up to an aggregate of 29,079,972 shares of Class A Common Stock upon exercise of the Public Warrants, Private Placement Warrants and Forward Purchase Warrants. The Selling Holders may use the shelf registration statement to sell up to an aggregate of 205,042,231 shares of Class A Common Stock (which includes up to 15,280,000 shares of Class A Common Stock issuable upon the exercise of outstanding Warrants) and up to 15,280,000 warrants from time to time through any means described in the section entitled “Plan of Distribution.” More specific terms of any securities that the Selling Holders offer and sell may be provided in a prospectus supplement that describes, among other things, the specific amounts and prices of the Class A Common Stock and/or warrants being offered and the terms of the offering.

A prospectus supplement may also add, update or change information included in this prospectus. Any statement contained in this prospectus will be deemed to be modified or superseded for purposes of this prospectus to the extent that a statement contained in such prospectus supplement modifies or supersedes such statement. Any statement so modified will be deemed to constitute a part of this prospectus only as so modified, and any statement so superseded will be deemed not to constitute a part of this prospectus. You should rely only on the information contained in this prospectus, any applicable prospectus supplement or any related free writing prospectus. See “Where You Can Find More Information.”

Neither we nor the Selling Holders have authorized anyone to provide any information or to make any representations other than those contained in this prospectus, any accompanying prospectus supplement or any free writing prospectus we have prepared. We and the Selling Holders take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the securities offered hereby and only under circumstances and in jurisdictions where it is lawful to do so. No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus, any applicable prospectus supplement or any related free writing prospectus. This prospectus is not an offer to sell securities, and it is not soliciting an offer to buy securities, in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus or any prospectus supplement is accurate only as of the date on the front of those documents only, regardless of the time of delivery of this prospectus or any applicable prospectus supplement, or any sale of a security. Our business, financial condition, results of operations and prospects may have changed since those dates.

This prospectus contains summaries of certain provisions contained in some of the documents described herein, but reference is made to the actual documents for complete information. All of the summaries are qualified in their entirety by the actual documents. Copies of some of the documents referred to herein have been filed, will be filed or will be incorporated by reference as exhibits to the registration statement of which this prospectus is a part, and you may obtain copies of those documents as described below under “Where You Can Find More Information.”

The Business Combination

On February 4, 2021 (the “Closing Date”), E2open Parent Holdings, Inc. (formerly known as CC Neuberger Principal Holdings I), consummated its previously announced business combination pursuant to that certain Business Combination Agreement, dated as of October 14, 2020 (the “Business Combination Agreement”), among CC Neuberger Principal Holdings I (“CCNB1”), Sonar Merger Sub I, LLC, a Delaware limited liability company (“Blocker Merger Sub 1”), Sonar Merger Sub II, LLC, a Delaware limited liability company (“Blocker Merger Sub 2”), Sonar Merger Sub III, LLC, a Delaware limited liability company (“Blocker Merger Sub 3”), Sonar Merger Sub IV, LLC, a Delaware limited liability company (“Blocker Merger Sub 4”), Sonar Merger Sub V, LLC, a Delaware limited liability company (“Blocker Merger Sub 5”), Sonar Merger Sub VI, LLC, a Delaware limited liability company (“Blocker Merger Sub 6,” and together with Blocker Merger Sub 1, Blocker Merger Sub 2, Blocker Merger Sub 3, Blocker Merger Sub 4 and Blocker Merger

1

Table of Contents

Sub 5, the “Blocker Merger Subs”), Insight (Cayman) IX Eagle Blocker, LLC, a Delaware limited liability company (“Insight Cayman Blocker”), Insight (Delaware) IX Eagle Blocker, LLC, a Delaware limited liability company (“Insight Delaware Blocker”), Insight GBCF (Cayman) Eagle Blocker, LLC, a Delaware limited liability company (“Insight GBCF Cayman Blocker”), Insight GBCF (Delaware) Eagle Blocker, LLC, a Delaware limited liability company (“Insight GBCF Delaware Blocker”), Elliott Eagle JV LLC, a Delaware limited liability company (“Elliott Eagle Blocker”), PDI III E2open Blocker Corp., a Delaware corporation (“PDI Blocker,” and together with Insight Cayman Blocker, Insight Delaware Blocker, Insight GBCF Cayman Blocker, Insight GBCF Delaware Blocker, and Elliott Eagle Blocker, the “Blockers”), Elliott Associates, L.P., a Delaware limited partnership, Elliott International, L.P., a Cayman Islands limited partnership, Sonar Company Merger Sub, LLC a Delaware limited liability company (“Company Merger Sub,” and together with the Buyer and the Blocker Merger Subs, the “Buyer Parties”), E2open, and Insight Venture Partners, LLC, a Delaware limited liability company, solely in its capacity as representative of the Blocker Owners and the Company Equityholders (the “Equityholder Representative”). As contemplated by the Business Combination Agreement, on the Closing Date, CCNB1 domesticated into a Delaware corporation (the “Domestication”) and consummated the acquisition of a majority of the company units of E2open Holdings, the parent of E2open, LLC, as a result of a series of mergers (the “Business Combination”).

The BluJay Acquisition

On May 27, 2021, E2open, BluJay and its shareholders (the “BluJay Sellers”) entered into a Share Purchase Deed, dated as of May 27, 2021 (as may be amended from time to time in accordance with the terms thereof, the “BluJay Purchase Agreement”), pursuant to which E2open or a direct or indirect subsidiary thereof will purchase all of the outstanding shares of capital stock of BluJay from the BluJay Sellers. As a result of the consummation of the transactions contemplated by the BluJay Purchase Agreement, BluJay and its subsidiaries will become subsidiaries of E2open (the “BluJay Acquisition”).

Upon consummation of the BluJay Acquisition (the “BluJay Closing”), in exchange for the shares of BluJay, E2open will issue to the BluJay Sellers an aggregate of 72,383,299 shares of Class A Common Stock of E2open and pay to the BluJay Sellers cash in the aggregate amount of $456.8 million, subject to increase for a ticking fee and adjustments for leakage and other enumerated items as provided in the BluJay Purchase Agreement.

The BluJay Purchase Agreement follows a typical locked-box mechanism, pursuant to which the purchase price is fixed upfront by reference to the balance sheet position of BlueJay as at December 31, 2020, without any purchase price adjustment following the BluJay Closing. E2open is also required to pay an additional consideration on a daily basis for the period between December 31, 2020, and the date of the BluJay Closing at a rate of $63,000 per day. The purchase price will be reduced on a dollar for dollar basis if any value is extracted to or for the benefit of any BluJay Sellers between December 31, 2020, and the date of the BluJay Closing, which we refer to as leakage, other than for certain narrowly defined permitted leakage items specifically agreed by the BluJay Sellers and E2open and expressly provided for in the BluJay Purchase Agreement.

In connection with the BluJay Acquisition, on May 27, 2021, E2open entered into subscription agreements (the “BluJay Subscription Agreements”) with certain investors, including certain existing stockholders of E2open (the “BluJay PIPE Investors”). Pursuant to the BluJay Subscription Agreements, substantially simultaneously with and conditioned upon the occurrence of the BluJay Closing, E2open has agreed to issue to the BluJay PIPE Investors an aggregate of 28,909,022 shares of Class A Common Stock in exchange for aggregate gross proceeds of approximately $300 million (the “BluJay Pre-Closing Financing”).

The consummation of the BluJay Acquisition and the BluJay Pre-Closing Financing are subject to the satisfaction or waiver of certain customary conditions. The shares of Class A Common Stock to be offered and sold in connection with the BluJay Pre-Closing Financing and the BluJay Purchase Agreement, as described above, have not been registered under the Securities Act in reliance upon the exemption provided in Section 4(a)(2) thereof.

Unless the context indicates otherwise, references to “E2open,” “the Company,” “we,” “us,” and “our” refer to E2open Parent Holdings, Inc., a Delaware corporation, and its consolidated subsidiaries following the Business Combination. “CCNB1” refers to CC Neuberger Principal Holdings I prior to the Business Combination.

2

Table of Contents

Unless otherwise stated in this prospectus or the context otherwise requires, references to:

“acquisition churn” means churn of an acquired company that was initiated or notified prior to E2open’s acquisition that has an impact on post-acquisition performance.

“ASC” means the Accounting Standards Codification.

“Backstop” means the NBOKS commitment, subject to the availability of capital it has committed to all special purpose acquisition companies sponsored by CC Capital and NBOKS on a first come first serve basis, to allocate up to an aggregate of $300,000,000 to subscribe for shares of Class A Common Stock at $10.00 per share in connection with the Business Combination, which subscription amount shall not exceed the number of shares of CCNB1 subject to Redemption, pursuant to the terms and subject to the conditions of the Backstop Agreement.

“Backstop Agreement” means the Backstop Facility Agreement, dated October 14, 2020, between CCNB1 and NBOKS, pursuant to which NBOKS agreed to, subject to the availability of capital it has committed to all special purpose acquisition companies sponsored by CC Capital and NBOKS on a first come first serve basis, provide the Backstop.

“Blockers” means the Insight Blockers, collectively, the PDI Blocker and the Elliott Eagle Blocker.

“Blocker Sellers” means the owners of equity interests in the Blockers.

“Blocker Merger Subs” means Sonar Merger Sub I, LLC, a Delaware limited liability company, Sonar Merger Sub II, LLC, a Delaware limited liability company, Sonar Merger Sub III, LLC, a Delaware limited liability company, Sonar Merger Sub IV, LLC, a Delaware limited liability company, Sonar Merger Sub V, LLC, a Delaware limited liability company, and Sonar Merger Sub VI, LLC, a Delaware limited liability company.

“BluJay” means BluJay Topco Limited.

“BluJay Acquisition” means the transactions contemplated by the BluJay Purchase Agreement.

“BluJay Closing” means the consummation of the BluJay Acquisition.

“BluJay PIPE Investors” means the investors that have signed BluJay Subscription Agreements.

“BluJay Pre-Closing Financing” means the issuance of 28,909,022 shares of Class A Common Stock to the BluJay PIPE Investors in exchange for aggregate gross proceeds of approximately $300 million.

“BluJay Purchase Agreement” means the Share Purchase Deed, entered into as of May 27, 2021 (as may be amended from time to time in accordance with the terms thereof), by and among E2open, BluJay and the BluJay Sellers.

“BluJay Sellers” means the shareholders of BluJay party to the BluJay Purchase Agreement.

“BluJay Subscription Agreements” means those certain subscription agreements entered into by and among E2open on the one hand, and the BluJay PIPE Investors, on the other hand, in connection with the BluJay Pre-Closing Financing.

“Board” means the board of directors of the Company.

“Business Combination” means the transactions contemplated by the Business Combination Agreement.

3

Table of Contents

“Business Combination Agreement” means the Business Combination Agreement, entered into as of October 14, 2020, by and among CCNB1, the Blocker Merger Subs, the Company Merger Sub, E2open, the Blockers, EALP, EILP, and Equityholder Representative, as amended on January 28, 2021.

“Business Combination PIPE Investment” means the private placement pursuant to which Business Combination PIPE Investors purchased an aggregate of 69,500,000 shares of Class A Common Stock in exchange for an aggregate amount of $695,000,000, on the terms and conditions set forth in the Business Combination Subscription Agreements.

“Business Combination PIPE Investors” means the investors that have signed Business Combination Subscription Agreements.

“Business Combination Subscription Agreements” means those certain subscription agreements entered into by and among CCNB1 on the one hand, and the Business Combination PIPE Investors, on the other hand, in connection with the Business Combination PIPE Investment.

“Bylaws” mean the bylaws of the Company in effect following the Business Combination.

“CAGR” means compound annual growth rate.

“Cayman Islands Companies Law” refers to the Companies Law (2020 Revision) of the Cayman Islands.

“CCNB1” means CC Neuberger Principal Holdings I.

“CCNB1 Board” means the board of directors of CCNB1.

“CC Capital” means CC Capital Partners, LLC, a Delaware limited liability company.

“churn” means the last transaction with an entity that ends its relationship with E2open.

“Class A Common Stock” means the Class A Common Stock of the Company, par value $0.0001 per share.

“Class A ordinary shares” means the Class A ordinary shares of CCNB1, par value $0.0001 per share.

“Class B common stock” means, collectively, the Series B-1 common stock and the Series B-2 common stock.

“Class B ordinary shares” means the Class B ordinary shares of CCNB1, par value $0.0001 per share.

“Class V Common Stock” means the Class V Common Stock of the Company, par value $0.0001 per share.

“Closing” means the closing of the Business Combination.

“Closing Date” means February 4, 2021, the closing date of the transactions contemplated by the Business Combination Agreement.

“Code” means the Internal Revenue Code of 1986, as amended.

“Common Units” means common units representing limited liability company interests of E2open Holdings, which are non-voting, economic interests in E2open Holdings.

“Company” means E2open Parent Holdings, Inc.

“Company Equityholders” has the same meaning as in the Business Combination Agreement.

4

Table of Contents

“Company Merger Sub” means Sonar Company Merger Sub, LLC, a Delaware limited liability company.

“Company Shares” means, collectively, all shares of the Class A Common Stock, Class B common stock and Class V Common Stock of the Company.

“cross-sell” means transactions with customers that already have an existing relationship and purchase a different SKU.

“customer tenure” means the average time measured in years since customers initiated their contracts or business with E2open. In cases where a company and its customer list are acquired, tenure is measured from the earliest contract date associated with the customer. Average customer tenure metrics are weighted against each customer’s respective recurring revenue for the most recent fiscal quarter available and are calculated as of fiscal year 2020.

“DGCL” means the Delaware General Corporation Law, as amended.

“Domestication” means the February 4, 2021 continuation of CCNB1 by way of domestication of CCNB1 into a Delaware corporation, with the ordinary shares of CCNB1 becoming shares of common stock of the Delaware corporation under the applicable provisions of the Cayman Islands Companies Law and the DGCL; the term includes all matters and necessary or ancillary changes in order to effect such Domestication, including the adoption of our certificate of incorporation consistent with the DGCL and changing the name and registered office of CCNB1 to our name and registered office.

“downsell” means transactions in which a customer reduces spend within a given SKU but remains a customer.

“DTC” means the Depository Trust Company.

“DWAC” means The Depository Trust Company’s deposit/withdrawal at custodian system.

“Elliott Eagle Blocker” means Elliott Eagle JV LLC, a Delaware limited liability company.

“Equity Incentive Plan” means the E2open Parent Holdings, Inc. 2021 Omnibus Incentive Plan.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“E2open Holdings” means E2open Holdings, LLC, a Delaware limited liability company.

“E2open Sellers” means, collectively, the Blocker Sellers, the Flow-Through Sellers, the Vested Optionholders and the Unvested Optionholders.

“FATCA” means the Foreign Account Tax Compliance Act.

“Flow-Through Sellers” means, prior to the Business Combination, those members of E2open Holdings that held Class A units, Class A-1 units or Class B units of E2open Holdings.

“Forward Purchase” means the purchase of the Forward Purchase Securities contemplated by the Forward Purchase Agreement.

“Forward Purchase Agreement” means the Forward Purchase Agreement, dated as of April 28, 2020, by and between among CCNB1 and Neuberger Berman Opportunistic Capital Solutions Master Fund LP.

“Forward Purchase Securities” means, collectively, the Forward Purchase Shares and Forward Purchase Warrants.

“Forward Purchase Shares” means 20,000,000 Class A ordinary shares purchased pursuant to the Forward Purchase Agreement.

5

Table of Contents

“Forward Purchase Warrants” means 5,000,000 redeemable warrants purchased pursuant to the Forward Purchase Agreement.

“Founder Holders” means CC NB Sponsor 1 Holdings LLC, a Delaware limited liability company, and Neuberger Berman Opportunistic Capital Solutions Master Fund LP.

“GAAP” means U.S. generally accepted accounting principles.

“gross retention” means the percentage of recurring revenue at the beginning of a four-quarter period retained over a subsequent four-quarter period after adjusting for churn and downsell recurring revenue recorded in those four quarters; unless otherwise stated, references to approximate gross retention figures reflect the average at fiscal year end from fiscal year 2018 to fiscal year 2020 and exclude acquisition and volumetric churn.

“Insider Letter Agreement” means the Letter Agreement, dated April 28, 2020, by and between CCNB1, the Sponsor and each of the executive officers and directors of CCNB1.

“Insight Cayman Blocker” means Insight (Cayman) IX Eagle Blocker, LLC, a Delaware limited liability company.

“Insight Delaware Blocker” means Insight (Delaware) IX Eagle Blocker, LLC, a Delaware limited liability company.

“Insight GBCF Cayman Blocker” Insight GBCF (Cayman) Eagle Blocker, LLC, a Delaware limited liability company.

“Insight GBCF Delaware Blocker” Insight GBCF (Delaware) Eagle Blocker, LLC, a Delaware limited liability company.

“Insight Member” means Insight E2open Aggregator, LLC, a Delaware limited liability company.

“Insight Partners” means, collectively, entities affiliated with Insight Venture Management, LLC, including funds under management.

“Investment Company Act” means the Investment Company Act of 1940, as amended.

“Investor Rights Agreement” means the Investor Rights Agreement, dated as of February 4, 2021, by and among the Company, the Sponsor, certain Company Equityholders (as defined therein), equityholders of certain Blockers, and certain other parties.

“IPO” means CCNB1’s initial public offering of its Units, Public Shares and Public Warrants pursuant to the IPO registration statement and completed on April 28, 2020.

“IPO registration statement” means the registration statement filed for CCNB1’s IPO on Form S-l declared effective by the SEC on April 23, 2020 (File Nos. 333-236974 and 333-237817).

“IVP Director” means the board members of the Company nominated by the Insight Member.

“JOBS Act” means the Jumpstart Our Business Startups Act of 2012, as amended.

“Lock-Up Period” means the period commencing on February 4, 2021 and ending on August 4, 2021.

“Maximum Forward Purchase Amount” means $200,000,000.

“Merger Subs” means the Blocker Merger Subs and the Company Merger Sub.

“NBOKS” means Neuberger Berman Opportunistic Capital Solutions Master Fund LP, a Cayman Islands exempted company.

6

Table of Contents

“net retention” means the percentage of recurring revenue at the beginning of a four-quarter period retained over a subsequent four-quarter period after adjusting for churn and downsell recurring revenue and adding upsell and cross-sell recurring revenue recorded in those four quarters, which net retention figures mentioned in this prospectus have been adjusted to eliminate the impact of pre-acquisition churn from acquired companies.

“network growth” means, for any given period, the increase in the total number of users integrated into and using the platform as a percentage of the total number of users as of immediately prior to the start of such period.

“NYSE” means The New York Stock Exchange.

“organic growth” represents management estimates for historical subscription revenue growth performance, assuming all acquisitions were owned as of the beginning of the period and excluding customer churn and contract renegotiation known at the time of acquisition.

“Original Registration Rights Agreement” means the Registration Rights Agreement, dated as of April 28, 2020, by and among CCNB1, the Sponsor and the other parties thereto.

“PDI Blocker” means PDI III E2open Blocker Corp., a Delaware corporation.

“PFIC” means passive foreign investment company under the Code.

“point solutions” means software solutions or services that are typically designed to solve one single, specific business problem as compared to E2open’s end-to-end capabilities.

“Preferred Stock” means the shares of preferred stock, par value $0.0001, to be authorized for future issuance by the Company.

“Preferred Stock Designation” means the resolution or resolutions adopted by the Board providing for the issue of a series of Preferred Stock.

“Private Placement” means the private placement by CCNB1 of 10,280,000 Private Placement Warrants to the Sponsor simultaneously with the closing of the IPO.

“Private Placement Warrants” means 10,280,000 warrants to purchase Class A ordinary shares sold to the Sponsor simultaneously with the closing of the IPO in a private placement at a price of $1.00 per warrant, which automatically became redeemable warrants to acquire shares of Class A Common Stock in connection with the Business Combination.

“prospectus” means the prospectus forming a part of this registration statement.

“Public Shareholders” means the holders of the Public Shares or Public Warrants that were sold in the IPO.

“Public Shares” means CCNB1’s Class A ordinary shares sold in the IPO (whether they were purchased in the IPO or thereafter in the open market).

“Public Warrants” means the warrants to purchase Class A ordinary shares sold in the IPO, which automatically became redeemable warrants to acquire shares of Class A Common Stock in connection with the Business Combination.

“recurring revenue” means the sum of the average annual subscription revenue for all customer contracts to which E2open is a party that are at least 12 months in duration as of the time of measurement and include the full impact of acquisitions as though they were completed at the beginning of the referenced period.

7

Table of Contents

“Related Agreements” means certain additional agreements entered into in connection with the Business Combination Agreement as further described in this prospectus.

“Restricted Common Units” means the Series 2 RCUs.

“Restricted Sponsor Shares” means the 2,500,000 shares of Series B-1 common stock previously held by the Sponsor Parties, which converted into shares of Class A Common Stock on June 8, 2021, in accordance with our certificate of incorporation and the Sponsor Side Letter Agreement.

“Rule 144” means Rule 144 under the Securities Act.

“SaaS” means software-as-a-service or a software distribution model in which E2open hosts applications for customers and makes these applications available to the customers via the internet/cloud technology.

“Sarbanes-Oxley Act” means the Sarbanes-Oxley Act of 2002, as amended.

“SEC” means the U.S. Securities and Exchange Commission.

“Securities Act” means the Securities Act of 1933, as amended.

“Series B-1 common stock” means the Series B-1 common stock of the Company, par value $0.0001 per share, which vested on June 8, 2021.

“Series B-2 common stock” means the Series B-2 common stock of the Company, par value $0.0001 per share.

“Series 1 RCU” means a Restricted Common Unit that vested on June 8, 2021.

“Series 2 RCU” means a Restricted Common Unit that will vest upon the occurrence of a Series 2 Vesting Event, with the rights and privileges as set forth in the Third Amended and Restated Limited Liability Company Agreement.

“Series 2 Vesting Event” with respect to each Series 2 RCU, (a) the occurrence of a VWAP 2 Vesting Event, (b) the occurrence of a change of control of the Company or E2open Holdings in which the acquirer is not a Flow-Through Seller or an affiliate thereof, or (c) a Liquidating Event pursuant to which each Common Unit would be entitled to at least $15.00 per Common Unit (taking into account the conversion of each Restricted Common Unit to a Common Unit); provided, however, that the reference to $15.00 shall be decreased by the aggregate per share amount of dividends actually paid in respect of a share of Class A Common Stock following the Closing.

“SKU” means a functional application that may be used as a standalone or with other functional applications/SKUs, each of which belongs to only one product family, and each product family has between four and ten SKUs.

“Sponsor” means CC Neuberger Principal Holdings I Sponsor LLC, a Delaware limited liability company.

“Sponsor Directors” means the board members of the Company nominated by CC Capital, on behalf of the Sponsor.

“Sponsor Parties” means the Sponsor, Eva F. Huston, Stephen C. Daffron and Keith W. Abell, in their capacity as Sponsor Directors.

8

Table of Contents

“Sponsor Side Letter Agreement” means the agreement entered into between CCNB1 and the Sponsor Parties on October 14, 2020 pursuant to which, among other things, the Sponsor Parties automatically converted an aggregate of 2,500,000 Class B ordinary shares into the Restricted Sponsor Shares on the Closing Date.

“Tax Receivable Agreement” means the Tax Receivable Agreement entered into on February 4, 2021, between the Company, Blocker Sellers and the Flow-Through Sellers.

“Third Amended and Restated Limited Liability Company Agreement” means the Third Amended and Restated Limited Liability Company Agreement of E2open Holdings, which became effective at the Closing on February 4, 2021.

“Total Addressable Market” or “TAM” means the estimated potential market size for supply chain management software in North America and Europe, E2open’s core geographies. The TAM was estimated on a bottoms-up basis by segmenting companies into industry use intensity categories: “high” (including high-tech, aerospace, and automotive industries), “medium” (including consumer packaged goods, food & beverage, manufacturing, retail, logistics, and chemicals industries), and “low” (including oil and gas and basic materials). Companies were also categorized into size buckets based on revenue to assess the potential recurring revenue opportunity. The estimated addressable market for each group of companies reflects the product of (a) the estimated number of companies for each segment and (b) the potential recurring revenue per company. The TAM reflects the sum of all groups of companies plus an aggregate estimate for industries with lower penetration (e.g., agriculture) as well as professional services and other spend.

“Transfer Agent” means Continental Stock Transfer & Trust Company.

“Treasury Regulations” means the Code, its legislative history, and final, temporary and proposed treasury regulations promulgated thereunder as then amended.

“Trust Account” means the trust account of CCNB1, which, prior to the Closing, held the net proceeds from the IPO and certain of the proceeds from the sale of the Private Placement Warrants, together with interest earned thereon, less amounts released to pay taxes, and which was distributed in connection with the Closing of the Business Combination.

“upsell” means transactions in which a customer purchases more of an existing SKU that is already currently utilized by that customer, which is generally from expansion of the product into different geographic regions or divisions of the customer, but may also arise from the adoption and organic growth in that account or pricing increases.

“users” means the individual participants that access E2open’s platform from its customers and their trading partners.

“VWAP” means the daily per share volume-weighted average price of the Class A Common Stock, with respect to measurement periods (or portions thereof) following the Effective Time, or the Class A ordinary shares, with respect to measurement periods (or portions thereof) prior to the Effective Time (as defined in the Business Combination Agreement), on the New York Stock Exchange or such other principal United States securities exchange on which the shares of Class A Common Stock is and/or the Class A ordinary shares, as applicable, are listed, quoted or admitted to trading, as displayed under the heading Bloomberg VWAP on the Bloomberg page designated for the Class A Common Stock (or its and/or the Class A ordinary shares, as applicable (or the equivalent successor if such page is not available)) in respect of the period from the open of trading on such trading day until the close of trading on such trading day (or if such volume-weighted average price is unavailable, (a) the per share volume-weighted average price of a share of Class A Common Stock and/or a Class A ordinary share, as applicable, on such trading day (determined without regard to afterhours trading or any other trading outside the regular trading session or trading hours), or (b) if such determination is not feasible,

9

Table of Contents

the market price per share of Class A Common Stock and/or Class A ordinary share, in either case as determined by a nationally recognized independent investment banking firm retained in good faith for this purpose by CCNB1); provided, however, that if at any time for purposes of the Class A 5-Day VWAP or Class A 20-Day VWAP (each as defined in the Third Amended and Restated Limited Liability Company Agreement), as applicable, shares of Class A Common Stock are not then listed, quoted or traded on a principal United States securities exchange or automated or electronic quotation system, then the VWAP shall mean the per share Appraiser FMV of one (1) share of Class A Common Stock (or such other equity security into which the Class A Common Stock was converted or exchanged).

“VWAP 1 Vesting Event” means the first day on which the Class A Common Stock 5-Day VWAP is equal to at least $13.50; provided, however, that the reference to $13.50 shall be decreased by the aggregate per share amount of dividends actually paid in respect of a share of Class A Common Stock following the Closing. The VWAP 1 Vesting Event occurred on June 8, 2021.

“VWAP 2 Vesting Event” means the first day on which the Class A Common Stock 20-Day VWAP is equal to at least $15.00; provided, however, that the reference to $15.00 shall be decreased by the aggregate per share amount of dividends actually paid in respect of a share of Class A Common Stock following the Closing.

“Warrants” means the Public Warrants and the Private Placement Warrants.

“Whitespace” means the portion of the TAM that does not use third-party SCM software and is estimated to be largely comprised of manual solutions completed by employees that involve little-to-no automation (e.g. spreadsheets) and home-grown solutions that are typically tailored software or add-on solutions developed in-house by IT resources and are not commercially available.

“Working Capital Loans” means certain loans that could have been made by the Sponsor or an affiliate of the Sponsor, or certain of CCNB1’s officers and directors in connection with the financing of a business combination.

10

Table of Contents

MARKET AND INDUSTRY DATA

Information contained in this prospectus concerning the market and the industry in which the Company competes, including its market position, general expectations of market opportunity and market size, is based on information from various third-party sources, on assumptions made by the Company based on such sources and the Company’s knowledge of the markets for its services and solutions. Any estimates provided herein involve numerous assumptions and limitations, and you are cautioned not to give undue weight to such information. Third-party sources generally state that the information contained in such source has been obtained from sources believed to be reliable but that there can be no assurance as to the accuracy or completeness of such information. The industry in which the Company operates is subject to a high degree of uncertainty and risk. As a result, the estimates and market and industry information provided in this prospectus are subject to change based on various factors, including those described in the section entitled “Risk Factors — Risks Related to Our Business and Operations” and elsewhere in prospectus.

TRADEMARKS AND SERVICE MARKS

The Company owns, or has rights to, trademarks, service marks, or trade names that it uses in connection with the operation of its business and that the Company considers important to its marketing endeavors, including the E2OPEN, AMBER ROAD, INTTRA marks. This prospectus also contains trademarks of other companies that, to our knowledge, are the property of their respective holders, and we do not intend our use or display of such marks to imply relationships with, or endorsements of us by, any other company.

Solely for legibility, the trademarks, service marks, and trade names referred to in this prospectus are used without the ® and ™ symbols, but such references are not intended to indicate, in any way, that the Company will not assert, to the fullest extent under applicable law, its rights or the rights of the applicable licensors to these trademarks, service marks, and trade names. All trademarks, service marks, and trade names appearing in this prospectus are the property of their respective owners.

11

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus includes statements that express our and our subsidiaries’ opinions, expectations, beliefs, plans, objectives, assumptions or projections regarding future events or future results and therefore are, or may be deemed to be, “forward-looking statements.” These forward-looking statements can generally be identified by the use of forward-looking terminology, including the terms “believes,” “estimates,” “anticipates,” “expects,” “seeks,” “projects,” “intends,” “plans,” “may,” “will” or “should” or, in each case, their negative or other variations or comparable terminology. These forward-looking statements include all matters that are not historical facts. They appear in a number of places throughout this prospectus and these forward-looking statements reflect management’s expectations regarding our future growth, results of operations, operational and financial performance and business prospects and opportunities.

As a result of a number of known and unknown risks and uncertainties, the Company’s results or performance may be materially different from those expressed or implied by these forward-looking statements. Some factors that could cause actual results to differ include:

| • | The BluJay Acquisition may not be completed or may not provide the expected benefits; |

| • | changes in anticipated timing for closing the BluJay Acquisition; |

| • | the integration of BluJay and E2open may be more difficult, time-consuming or expensive than anticipated; |

| • | changes in applicable laws or regulations; |

| • | the inability to develop and maintain effective internal controls; |

| • | the COVID-19 pandemic; |

| • | the inability to attract new customers or upsell/cross-sell existing customers; |

| • | failure to renew existing customer subscriptions on terms favorable to the Company; |

| • | risks associated with the Company’s extensive and expanding international operations; |

| • | the inability to develop and market new and enhanced solutions; |

| • | the failure of the market for cloud-based supply chain management solutions to develop as quickly as we expect; |

| • | inaccuracies in information sourced for our knowledge databases; |

| • | failure to compete successfully in a fragmented and competitive supply chain management market; |

| • | the inability to adequately protect key intellectual property rights or proprietary technology; |

| • | the diversion of management’s attention and consumption of resources as a result of potential acquisitions of other companies; |

| • | risks associates with our past and prospective acquisitions, including the failure to successfully integrate operations, personnel, systems, technologies and products of the acquired companies, adverse tax consequences of acquisitions, greater than expected liabilities of acquired companies and charges to earnings from acquisitions; |

| • | failure to maintain adequate operational and financial resources or raise additional capital or generate sufficient cash flows; |

| • | cyber-attacks and security vulnerabilities; and |

| • | other risks and uncertainties described in this prospectus in the section titled “Risk Factors.” |

The forward-looking statements contained in this prospectus are based on our current expectations and beliefs concerning future developments and their potential effects on our business. There can be no assurance that future developments affecting our business will be those that we have anticipated.

12

Table of Contents

These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the heading “Risk Factors.” Should one or more of these risks or uncertainties materialize, or should any of the assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. We do not undertake any obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

13

Table of Contents

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information that you should consider before investing in our Class A Common Stock or Warrants. You should read this entire prospectus carefully, including the matters discussed under the sections titled “Risk Factors,” “Management’s Discussion and Analysis of E2open’s Financial Condition and Results of Operations,” “Unaudited Pro Forma Condensed Combined Financial Information,” “Business” and the consolidated financial statements and related notes included elsewhere in this prospectus before making an investment decision.

Our Mission

Our mission is to build the most comprehensive and capable end-to-end global supply chain software ecosystem by combining networks, data, and applications in a single platform to deliver enduring customer value.

Overview

We are a leading provider of 100% cloud-based, end-to-end supply chain management software. We generate revenue from the sale of software subscriptions and professional services. Our software combines networks, data, and applications to provide a deeply embedded, mission-critical platform that allows customers to optimize their supply chain by accelerating growth, reducing costs, increasing visibility, and driving improved resiliency. Given the mission-critical nature of our solutions, we maintain long-term relationships with our customers, which is reflected by our high gross retention and average customer tenure. In aggregate, we serve more than 1,200 customers in over 180 countries across a wide range of end-markets, including technology, consumer, industrial and transportation, among others.

We operate in what we believe is an attractive industry with strong secular tailwinds and a large Total Addressable Market, or TAM, of more than $45 billion. This TAM is comprised of significant whitespace, which we estimate is more than $1 billion. This opportunity within our existing customer base is largely driven by their current technology solution, which is often a combination of legacy point solutions and home-grown applications, many of which are tied together with manual processes and spreadsheets. As manufacturing has evolved from brands owning the full production lifecycle to orchestrating disparate manufacturing, distribution and selling processes, supply chains have grown more complex, increasing demand for software solutions like ours and the need to modernize the existing technology landscape with cloud-based modern solutions. We believe our fully cloud-based, end-to-end software platform offers a differentiated solution for customers that gives them better value as compared to solutions offered by some of our competitors.

We believe the Business Combination and our enhanced access to capital as a public company will best position us to realize our objective of building the most comprehensive and capable end-to-end global supply chain software ecosystem, delivering enduring customer value. Going forward, we plan to accelerate revenue growth and value creation through continued enhancement of our existing product portfolio, deepening of existing customer relationships and onboarding of new customers. Additionally, we anticipate expanding product offerings through data and analytics opportunities and pursuing strategic and financially accretive acquisitions.

Our Platform

Our harmonized SaaS platform brings together networks, data, and applications to facilitate end-to-end supply chain visibility across planning, execution and procurement and delivers a strong value proposition.

14

Table of Contents

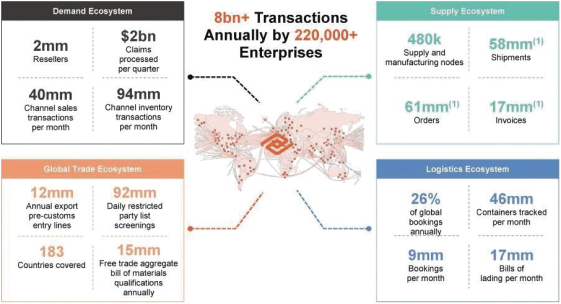

Network

Our network combines four distinct, but connected, ecosystems: Demand, Supply, Logistics and Global Trade, which we estimate supports more than 220,000 trading partners and captures more than eight billion transaction data points each year.

Our Demand ecosystem represents the global footprint established by retailers, distributors, re-sellers, and those who sell goods primarily through online channels. We estimate that we process over $2 billion in claims every quarter, more than 40 million channel sales transactions every month, and over 94 million channel inventory transactions every month.

Our Supply ecosystem is comprised of companies and other participants for which we source components and materials and/or provide manufacturing capacity for the production of goods. We estimate that, at any moment in time, we oversee an average of more than 58 million shipments as well as process an average of over 61 million orders and 17 million invoices for our customers and supply and manufacturing network participants based on samples taken over a 12-month period.

Our Logistics ecosystem includes global logistics services that transport components, raw materials, and finished goods across all modes. We estimate that we facilitate over 26% of global ocean container bookings within this ecosystem in addition to tracking the movement of over 46 million containers every month.

Our Global Trade ecosystem allows participants to automate the global movement of goods and to facilitate cross-border transactions for businesses, which we believe is increasingly important given the velocity with which import and export laws change on a global scale. This ecosystem provides our network with data on trade regulations across more than 180 countries that we estimate supports annual processing of over 12 million export pre-customs entry lines, 15 million free trade agreement bill of materials qualifications, and 92 million restricted party-list screenings, annually.

Our network connects participants across all of these ecosystems, enabling customers to analyze data, identify problems proactively and optimize asset efficiency. We are a leading provider with a unique network of ecosystems, and do not rely on third party providers for network information.

15

Table of Contents

Source: Management estimates as of August 2020.

| (1) | Estimated number of shipments, orders, and invoices overseen at any moment in time based on samples taken over a 12 month period. |

Data

Our proprietary algorithms capture the data within our network ecosystems that feed our solutions to deliver compelling value to our customers. Additionally, our customers can combine internal and external vendor data with our network to drive informed decision-making based on real-time information. We believe our ability to capture and harmonize data from our customers and their trading partners in any native format demonstrates the strong capabilities of our software architecture and integrated data model. We believe that our combination of network ecosystems, data and applications providing end-to-end supply chain visibility and connecting more than 220,000 trading partners is unique.

Applications

Our end-to-end applications provide artificial intelligence- and machine learning-based advanced analytics to help customers gain insights for enhanced decision-making across supply chain planning, execution and procurement functions. Our applications are organized into seven product families: Channel Shaping, Demand Sensing, Business Planning, Global Trade Management, Transportation and Logistics, Collaborative Manufacturing and Supply Management.

Channel Shaping allows customers to optimize activity across retail, distributor and online channels, which includes capabilities for partner selection, aligning market incentives, managing on-shelf availability, tracking sell-through and inventory management and performance incentives.

Demand Sensing utilizes artificial intelligence and machine learning to forecast demand based on historical trends, current sell-through dynamics, weather, and other relevant factors.

16

Table of Contents

Business Planning helps ensure optimized global performance through scenario-based planning and execution algorithms balancing supply, demand, inventory and financial targets.

Global Trade Management automates import and export processes to enable efficient and compliant cross- border trade while optimizing customs duties and reducing broker fees.

Transportation and Logistics orchestrates the movement of goods by allowing customers to connect with key stakeholders to optimize carriers, simplify tendering, track shipments and streamline payments.

Collaborative Manufacturing provides comprehensive visibility into internal and external manufacturing activities by monitoring yields, quality, cycle-times/utilization and other key indicators to track performance, identify deficiencies, and facilitate corrective actions.

Supply Management ensures the continuity of supply by orchestrating procurement, capacity, inventory management and drop-ship fulfilment across multiple-tiers of the manufacturing process.

Competitive Strengths

We believe the following competitive strengths will contribute to our ongoing success:

Attractive Industry Tailwinds and Large TAM

We participate in the growing supply chain management (“SCM”) software industry. We estimate that the TAM is more than $45 billion across North America and Europe, and we anticipate this market will continue to grow. Several secular trends are increasing the demand for SCM software, including:

| • | Complexity of Global Supply Chains: |

| • | Brand owners have transitioned from being manufacturers to orchestrators that produce little but manage a vast network of outsourced of trading partners and support their minute-by-minute operations across channel, manufacturing, supply, global trade and logistics. |

| • | As supply chains become increasingly global and complex, SCM software is essential to run supply chains efficiently at scale. |

| • | Need for Integrating Siloed Data to Drive Decision Making: |

| • | Manufacturers are increasingly focused on utilizing disparate data to drive more efficient decision making. |

| • | Historically, data to help manufacturers bring their products to market has existed in silos within various departments of the manufacturers, as well as across their extended partner ecosystems. |

| • | Access to timely and comprehensive data is valuable not just to each department within a manufacturer, but is also critical for partners of the manufacturer to run efficient operations on its behalf. |

| • | Brand owners are increasingly focused on applying data from different parts of the supply chain to make more informed manufacturing decisions, such as using retail demand sensing to forecast required manufacturing output. |

| • | Brand owners are increasingly focused on a flexible, multi-modal value proposition spanning carriers, shippers, and third-party logistics providers. |

17

Table of Contents

| • | Regulatory Environment Complexity: |

| • | Manufacturers increasingly need to navigate complex frameworks of regional and local taxes, tariffs and regulatory compliance protocols. |

| • | SCM software solutions help automate these tasks and reduce the regulatory burden for companies, which will continue to be a strategic priority. |

| • | Geographic Consolidation: |

| • | Shippers and third-party logistics providers operate in a global environment and want to execute within a single technology platform. |

| • | Many SCM technology solutions have historically had stronger capabilities within the region in which they were initially developed. North America is the most developed, with Europe served by a smaller number of SCM software solutions while Latin America and APAC are comparatively underpenetrated. |

| • | Supply Chain Disruption: |

| • | As a result of disruptions related to COVID-19 and recent events like the Suez Canal blockage, it has become increasingly important to diversify supply chains to mitigate disruption risk resulting from concentration within a supply chain. The complexity that arises from diversifying a supply chain and increasing the number of trading partners across more geographies and production facilities drives further demand for SCM software. |

We believe that the TAM has approximately 85% whitespace for modern SCM solutions. Many companies currently rely on legacy, on-premise applications or homegrown and/or spreadsheet-based solutions created over time, each of which requires significant manual effort to achieve end-to-end supply chain visibility. Moreover, these SCM solutions often rely on latent and one-off, point-to-point connections with partners for collecting data. These alternatives provide less value and are significantly more error prone, creating an attractive competitive dynamic within the industry for modern SCM software providers where there is significant opportunity to grow without the need to replace an incumbent competitor. We believe there is more than $1 billion of whitespace for the solutions we already offer, which we believe provides very actionable growth opportunities through expanding our existing customer relationships.

Category-Defining End-to-End Provider of Mission-Critical Software

As businesses have transitioned from being owners of the production lifecycle to orchestrators of discrete manufacturing, distribution and selling processes, they have increasingly looked to software solutions to manage this growing complexity. However, most SCM software has not been designed to address these challenges comprehensively, and manufacturers often employ multiple point solutions with siloed data and processes that inhibit visibility, resulting in sub-optimal decision-making based on inaccurate or outdated information. Our approach, which is built around a cloud-based SaaS platform with end-to-end visibility and real-time, network-powered data, provides best-of-breed functionality across the supply chain and facilitates optimal supply chain performance.

As described above, we operate a software platform that integrates network ecosystems, data and applications across a harmonized and simplified user interface, driving compelling value proposition and return on investment for our customers. This has created a mission-critical software solution and long-term relationships with customers as evidenced by our high gross retention rate. Additionally, we have been widely recognized as a differentiated leader by Gartner, International Data Corporation, Nucleus, and others in the realm of multi-enterprise solutions, which we believe will be the future of SCM software. In May 2021, the Company was placed by Gartner in the Leaders quadrant with the highest ability to execute and completeness of vision in its 2021 Magic Quadrant for Multienterprise Supply Chain Business Networks for the second year in a row.

18

Table of Contents

Strong Network Effects Enhanced by a Flexible and Integrated Data Model

Our core offerings are underpinned by an integrated data model that facilitates the flow and processing of data for participants across several ecosystems and applications. This model facilitates low-latency, “many- to-one-to-many” data exchange across trading partner ecosystems. The combination of our integrated and flexible data model along with the four network ecosystems powers our customers’ solutions allowing them to efficiently orchestrate their end-to-end supply chains. This architecture is designed to ensure that each participant and data source within these ecosystems enhances our applications, which in turn improves the network and the value we deliver to our customers and participants alike.

Our software architecture and ability to harmonize disparate forms of data create a scalable software platform that can efficiently integrate acquisitions and new product applications seamlessly into a consolidated and holistic SaaS solution. Our software architecture and this ability has been a driving force behind our robust track-record of successful acquisition integrations, and we believe our scalable platform will allow us to generate substantial value through tuck-in and transformative acquisitions in the future.

Importantly, we believe there is incremental value we can create by utilizing the data flowing through our network to develop insights that can further help our customers as well as other target markets. We plan to work to develop a comprehensive strategy to capture this market opportunity and deepen our relationships with customers, which has the potential to meaningfully accelerate revenue growth.

Long-Term Relationships with Diversified and Blue-Chip Customer Base with Proven Wallet Share Expansion

We deliver solutions for some of the largest brand owners and manufacturers globally, and we estimate more than 125 of our customers have annual revenues of over $10 billion. We believe we are mission-critical to our customers’ operations, as evidenced by our 95% gross retention. We possess a diverse customer base consisting of more than 1,200 clients that spans a broad spectrum of industries, including the technology, industrial, consumer and transportation sectors, among others.

Our customers utilize our solutions to orchestrate their supply chains, which we believe enables them to realize significant value and return on investment. For example, a leading consumer packaged goods company

19

Table of Contents

was able to cut forecast errors by 40% and reduce inventory by 35% using our product suite. They are now able to leverage our platform to forecast every product using artificial-intelligence and machine-learning technology. Moreover, a leading high-tech company has utilized our software to realize $300 million in savings over three years. An additional example includes a high-growth, large-scale consumer technology platform, which utilized our software to reduce its execution time from eight weeks to seven days, creating substantial opportunity to accelerate their revenue growth in addition to reducing costs.

In March 2021, the Suez Canal was blocked for six days after the grounding of Ever Given, a container ship. During this crisis, our customers utilized our tools to monitor and respond to the situation, making real-time adjustments to their supply chains.

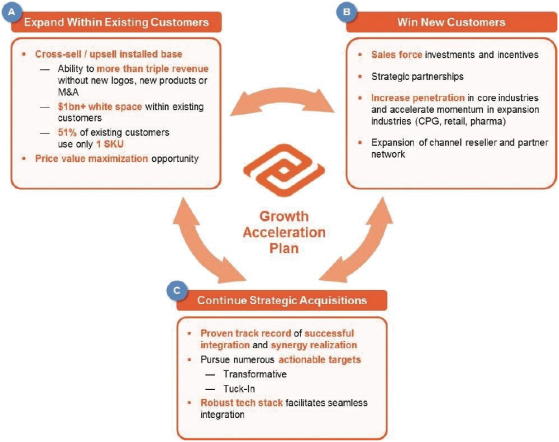

Growth Strategies

We intend to profitably grow our business and create shareholder value through the following strategic initiatives:

Expand Within Existing Customers

As described above, we believe there is significant opportunity to drive growth through expansion of our existing customer relationships. We have an opportunity to more than triple our revenue over time without any new logos, new products or acquisitions given that we believe there is more than $1 billion of whitespace. Our

20

Table of Contents

acquisition strategy is focused on acquiring complimentary best-of-breed point solutions to incorporate into our integrated end-to-end platform. As a result, we currently sell just one SKU to many of our customers, as most acquired companies had only one product to offer their customers. We believe this represents a significant opportunity to cross-sell additional products to these customers, accelerating growth and strengthening relationships with our installed base, especially as it grows over time with new customer wins. Importantly, we have a strong track record of achieving growth within our existing customer base. From fiscal 2018 to fiscal 2020, we increased the recurring revenue with a leading consumer packaged goods company, a leading industrial manufacturer, a blue-chip technology firm and a global hardware and software technology provider by 2.7x, 2.0x, 1.9x and 1.6x, respectively.

Win New Customers

As part of our growth strategy, the second growth lever is winning new customers, which we anticipate accelerating by optimizing our sales force through several measures. First, we plan to invest in our salesforce by hiring account acquisition experts, funded by identified savings projects across various areas. Additionally, we plan to pursue strategic partnerships and leverage the networks of our new board of directors to elevate conversations with C-level executives at key targets in our pipeline. We also intend to utilize these relationships and networks as well as our own channel reseller and partner network to accelerate growth through the onboarding of new customers.

Continue Strategic Acquisitions

A third lever of our growth strategy is to continue strategic acquisitions. We plan to utilize a disciplined approach to acquisitions, focusing on opportunities that will create value by strategically broadening our product offering as well as financially through the realization of integration-related synergies. Our key strategic acquisition criteria include: mission-critical solutions in core markets; complementary cloud applications with minimal product overlap; new customer relationships in vertical or geographic markets; and TAM, proprietary data, and/or network expansion.

We have a demonstrated track record of success in expanding our product offering and accelerating growth through acquisitions. Through our acquisitions of INTTRA Inc. (“INTTRA”) and Amber Road, we were able to enhance our value proposition to customers through the addition of ocean shipping logistics solutions as well as global trade management offerings, both of which contributed to our ability to provide end-to-end supply chain visibility. The acquisition of INTTRA increased the power of our network ecosystems through the integration of 26% of global ocean freight data, which further strengthened the network effects of our software platform and business model. Our acquisition of Amber Road enhanced our platform by providing customers with global trade management solutions to automate their import and export processes and help improve sourcing decisions across more than 180 countries. Importantly, we also have a track record of efficiently integrating acquired solutions operationally and financially. Across each of our acquisitions since 2015, we have met or exceeded our integration-related cost savings targets, in each case and with 20% cumulative outperformance as a whole.

Additional Organic Growth Building Blocks

We also believe there are several additional building blocks of organic growth acceleration that provide a margin of safety for achieving our annual steady-state subscription revenue growth target, including price/value maximization, data and analytics, sales force optimization and partnerships/new sales channels.

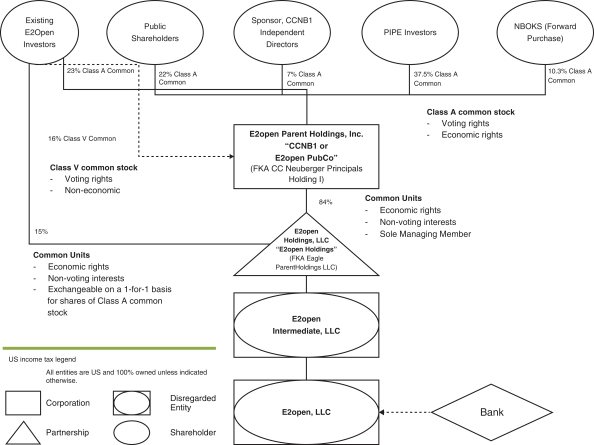

Organizational Structure

Following the completion of the Business Combination, our organizational structure is what is commonly referred to as an umbrella partnership C corporation (or Up-C) structure. This organizational structure allows

21

Table of Contents

certain owners of E2open Holdings to retain their equity ownership in E2open Holdings, an entity that is classified as a partnership for U.S. federal income tax purposes, in the form of Common Units, Series 1 RCUs (which converted into Common Units on June 8, 2021) and Series 2 RCUs. Each continuing owner of E2open Holdings also holds a number of shares of Class V Common Stock equal to the number of Common Units held by such owner, which has no economic value, but which entitles the holder thereof to one vote per share at any meeting of our shareholders. Those investors who, prior to the Business Combination, held Class A ordinary shares or Class B ordinary shares of CCNB1 and certain other investors and vested option holders now hold their equity ownership in the Company, a Delaware corporation that is a domestic corporation for U.S. federal income tax purposes.

Recent Acquisitions

On May 27, 2021, we entered into a definitive agreement to acquire BluJay, a leading SaaS-native logistics execution platform. Built on Data, Network, and Applications, BluJay offers solutions to an expansive ecosystem of suppliers, carriers, and network partners that includes over 50,000 participants and over 5,700 global customers. We believe these solutions are leaders across several areas, including Global Trade and Transportation Management, which includes last-mile logistics. E2open believes that BluJay plays a mission critical role in logistics and distribution supply chains and that BluJay is capable of driving significant efficiencies/cost savings and productivity for its customers. The BluJay Acquisition will materially enhance the Company’s supply chain execution capabilities, especially in transportation management with the expansion of the global transportation network, adding 50,000 network participants, $40 billion in annual commerce spend and 1.9 billion annual transactions. Additionally, BluJay brings a highly complementary global trade management platform that encompasses customs declaration and filing to the Company’s strong capabilities in compliance and tariffs. The BluJay Acquisition further adds key direct-to-consumer offerings including last mile, parcel and dropship commerce. Finally, the BluJay Acquisition will enhance E2open’s current value proposition to customers by broadening access to proprietary data and analytics for greater visibility, collaboration and execution across E2open’s platform.

Corporate Information

E2open Parent Holdings, Inc. is a Delaware corporation. Our principal executive offices are located at 9600 Great Hills Trail, Suite 300E, Austin, Texas 78759, and our telephone number at that address is (866) 432-6736. Our website is located at www.e2open.com. Our website and the information contained on, or accessed through, our website are not part of this prospectus, and you should rely only on the information contained in this prospectus when making an investment decision.

22

Table of Contents

THE OFFERING

We are registering the issuance by us of up to 29,079,972 shares of our Class A Common Stock that may be issued upon exercise of the Warrants to purchase Class A Common Stock, including the Public Warrants, the Private Placement Warrants and the Forward Purchase Warrants. We are also registering the resale by the Selling Holders or their permitted transferees of (i) up to 205,042,231 shares of Class A Common Stock and (ii) up to 15,280,000 Warrants.

Any investment in the securities offered hereby is speculative and involves a high degree of risk. You should carefully consider the information set forth under “Risk Factors” on page 31 of this prospectus.

Issuance of Class A Common Stock

The following information is as of June 25, 2021 and does not give effect to issuances of our Class A Common Stock, warrants or options to purchase shares of our Class A Common Stock after such date, or the exercise of warrants or options after such date.

| Shares of our Class A Common Stock to be issued upon exercise of all Public Warrants, Private Placement Warrants and Forward Purchase Warrants |

29,079,972 shares |

| Shares of our Class A Common Stock outstanding prior to (i) the exercise of all Public Warrants, Private Placement Warrants and Forward Purchase Warrants, (ii) the conversion of 3,372,184 shares of B-2 Common Stock into 3,372,184 shares of Class A Common Stock, and (iii) the conversion of 42,643,961 Common Units (including Common Units issuable upon conversion of the Restricted Common Units) into an aggregate of 42,643,961 shares of Class A Common Stock and the surrender and cancellation of a corresponding number of shares of Class V Common Stock |

195,171,415 shares |

| Use of Proceeds |

We will receive up to an aggregate of approximately $334.4 million from the exercise of all Public Warrants, Private Placement Warrants and Forward Purchase Warrants assuming the exercise in full of all such Warrants for cash. Unless we inform you otherwise in a prospectus supplement or free writing prospectus, we intend to use the net proceeds from the exercise of such Warrants for general corporate purposes, which may include acquisitions, strategic investments, or repayment of outstanding indebtedness. |

23

Table of Contents

Resale of Class A Common Stock and Warrants