Information contained herein is subject to completion or amendment. A registration statement relating to these securities has been filed with the U.S. Securities and Exchange Commission. These securities may not be sold nor may offers to buy be accepted prior to the time the registration statement becomes effective. This document shall not constitute an offer to sell or the solicitation of any offer to buy nor shall there be any sale of these securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction.

PRELIMINARY — SUBJECT TO COMPLETION — DATED FEBRUARY 23, 2021

PRELIMINARY PROXY STATEMENT OF IAC/INTERACTIVECORP, PROSPECTUS OF IAC/ INTERACTIVECORP AND OF VIMEO HOLDINGS, INC. AND CONSENT SOLICITATION STATEMENT OF VIMEO, INC.

Dear IAC/InterActiveCorp Stockholders:

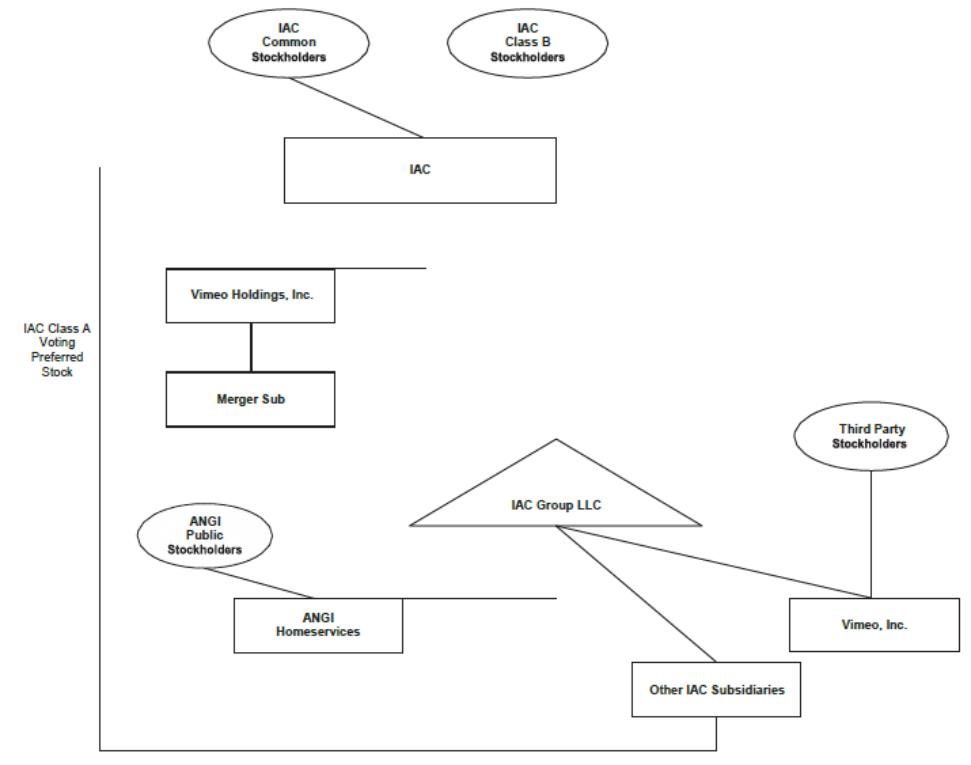

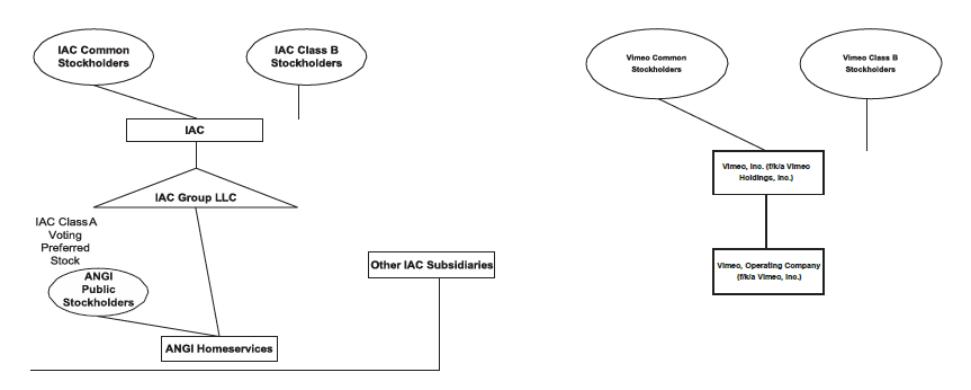

On behalf of the board of directors of IAC/InterActiveCorp (“IAC”), we are pleased to enclose the accompanying proxy statement/consent solicitation statement/prospectus relating to a series of transactions that, if completed in their entirety, will result in the transfer of IAC’s Vimeo business to Vimeo Holdings, Inc. (“SpinCo”), a Delaware corporation and a wholly owned subsidiary of IAC, that will become an independent, separately traded public company through a spin-off from IAC, and will cause Vimeo, Inc. (“Vimeo”), the IAC subsidiary that currently holds the Vimeo business, to become a wholly-owned subsidiary of SpinCo.

The spin-off would result in the current holders of IAC common stock receiving a proportionate amount of SpinCo common stock and the current holders of IAC Class B common stock receiving a proportionate amount of SpinCo Class B common stock. IAC’s common stock currently trades on The Nasdaq Global Select Market under the ticker symbol “IAC” and the reclassified shares of IAC common stock are expected to continue to trade under such symbol on The Nasdaq Global Select Market after the spin- off.

Prior to the spin-off, SpinCo will have been a wholly owned subsidiary of IAC, and its common stock has not been publicly listed. In connection with the spin-off, SpinCo will apply to list SpinCo common stock on [·] and has accordingly reserved the ticker symbol “[·].” While trading in SpinCo common stock under this symbol is expected to begin on the first business day following the completion of the spin-off, there can be no assurance that a viable and active trading market will develop.

In connection with the spin-off, SpinCo is also, via this proxy statement/consent solicitation statement/ prospectus, registering shares of SpinCo common stock that would be issued to Vimeo’s existing third-party stockholders in a merger of Vimeo with a wholly-owned subsidiary of SpinCo that would follow the spin-off, and Vimeo is soliciting consents from Vimeo’s existing stockholders in favor of such merger.

The IAC board of directors unanimously recommends that IAC stockholders vote “FOR” each of the proposals to be considered by IAC stockholders at the special meeting. Your vote is very important, regardless of the number of shares you own. Whether or not you expect to virtually attend the special meeting, please submit a proxy to vote your shares as promptly as possible so that your shares may be represented and voted at the meeting.

The completion of the spin-off is subject to the satisfaction or waiver of a number of conditions, including the receipt of IAC stockholder approval of the proposals to be presented at the special meeting. More information about IAC, SpinCo, Vimeo, the special meeting, the spin-off, the merger agreement for the Vimeo merger, and the Vimeo merger is contained in this proxy statement/consent solicitation statement/prospectus. Before voting, we urge you to read carefully and in its entirety this proxy statement/consent solicitation statement/ prospectus, including the Annexes and the documents incorporated by reference herein. In particular, we urge you to read carefully the section entitled “Risk Factors” beginning on page 14 of this proxy statement/consent solicitation statement/prospectus.

Barry Diller | |

Chairman and Senior Executive | |

IAC/InterActiveCorp |