UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________________________________

FORM 10-Q

__________________________________________________

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended June 30, 2024

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from _______ to _______

Commission File Number: 001-39313

__________________________________

(Exact name of registrant as specified in its charter)

__________________________________

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

(888 ) 276-2108

(Registrant’s telephone number, including area code)

N/A

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| x | Accelerated filer | o | |||||||||

| Non-accelerated filer | o | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No x

As of August 2, 2024, there were 65,195,489 shares of the registrant’s Class A common stock, $0.0001 par value per share, outstanding, 21,733,490 shares of the registrant’s Class B common stock, $0.0001 par value per share, outstanding and 1,665,854 shares of the registrant’s Class C common stock, $0.0001 par value per share, outstanding.

SHIFT4 PAYMENTS, INC.

TABLE OF CONTENTS

2

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q (“Quarterly Report”) contains forward-looking statements. We intend such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (“the Exchange Act”). All statements other than statements of historical fact contained in this Quarterly Report, including, without limitation, statements relating to our position as a leader within our industry; our future results of operations and financial position, business strategy and plans; the anticipated benefits of and costs associated with recent acquisitions; and objectives of management for future operations and activities, including, among others, statements regarding expected growth, international expansion, future capital expenditures, debt covenant compliance, financing activities, debt service obligations, and the timing of any of the foregoing, are forward-looking statements. These statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements.

In some cases, you can identify forward-looking statements by terms such as “may,” “will,” “should,” “expect,” “plan,” “anticipate,” “could,” “intend,” “target,” “project,” “contemplate,” “believe,” “estimate,” “predict,” “potential,” or “continue” or the negative of these terms or other similar expressions, though not all forward-looking statements can be identified by such terms or expressions. The forward-looking statements in this Quarterly Report are only predictions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition and results of operations. These forward-looking statements speak only as of the date of this Quarterly Report and are subject to a number of important factors that could cause actual results to differ materially from those in the forward-looking statements, including, but not limited to, those factors described in the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our Annual Report on Form 10-K for the fiscal year ended December 31, 2023, filed on February 29, 2024 (the “2023 Form 10-K”).

Moreover, we operate in an evolving environment. New risk factors and uncertainties may emerge from time to time, and it is not possible for management to predict all risk factors and uncertainties.

You should read this Quarterly Report and the documents that we reference herein completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements. Except as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained herein, whether as a result of any new information, future events, changed circumstances or otherwise.

3

PART I: FINANCIAL INFORMATION

Item 1. Financial Statements (unaudited)

SHIFT4 PAYMENTS, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(Unaudited)(in millions, except share and per share amounts)

| June 30, 2024 | December 31, 2023 | ||||||||||

| Assets | |||||||||||

| Current assets | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash | |||||||||||

| Settlement assets | |||||||||||

| Accounts receivable, net | |||||||||||

| Inventory | |||||||||||

| Prepaid expenses and other current assets | |||||||||||

| Total current assets | |||||||||||

| Noncurrent assets | |||||||||||

| Equipment for lease, net | |||||||||||

| Property, plant and equipment, net | |||||||||||

| Right-of-use assets | |||||||||||

| Investments in securities | |||||||||||

| Collateral held by the card networks | |||||||||||

| Goodwill | |||||||||||

| Residual commission buyouts, net | |||||||||||

| Capitalized customer acquisition costs, net | |||||||||||

| Other intangible assets, net | |||||||||||

| Other noncurrent assets | |||||||||||

| Total assets | $ | $ | |||||||||

| Liabilities and Stockholders' Equity | |||||||||||

| Current liabilities | |||||||||||

| Settlement liabilities | $ | $ | |||||||||

| Accounts payable | |||||||||||

| Accrued expenses and other current liabilities | |||||||||||

| Deferred revenue | |||||||||||

| Bank deposits | |||||||||||

| Current lease liabilities | |||||||||||

| Total current liabilities | |||||||||||

| Noncurrent liabilities | |||||||||||

| Long-term debt | |||||||||||

| Deferred tax liability | |||||||||||

| Noncurrent lease liabilities | |||||||||||

| Other noncurrent liabilities | |||||||||||

| Total liabilities | |||||||||||

| Commitments and contingencies (Note 16) | |||||||||||

| Stockholders' equity | |||||||||||

Preferred stock, $ | |||||||||||

Class A common stock, $ | |||||||||||

Class B common stock, $ | |||||||||||

Class C common stock, $ | |||||||||||

| Additional paid-in capital | |||||||||||

| Accumulated other comprehensive income (loss) | ( | ||||||||||

| Retained deficit | ( | ( | |||||||||

| Total stockholders' equity attributable to Shift4 Payments, Inc. | |||||||||||

| Noncontrolling interests | |||||||||||

| Total stockholders' equity | |||||||||||

| Total liabilities and stockholders' equity | $ | $ | |||||||||

See accompanying notes to unaudited condensed consolidated financial statements. | |||||||||||

4

SHIFT4 PAYMENTS, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Unaudited) (in millions, except share and per share amounts)

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

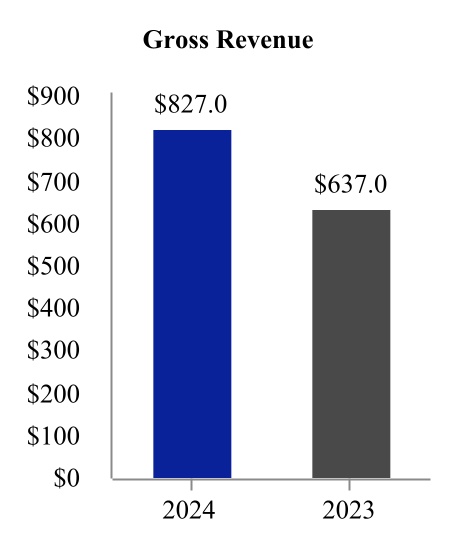

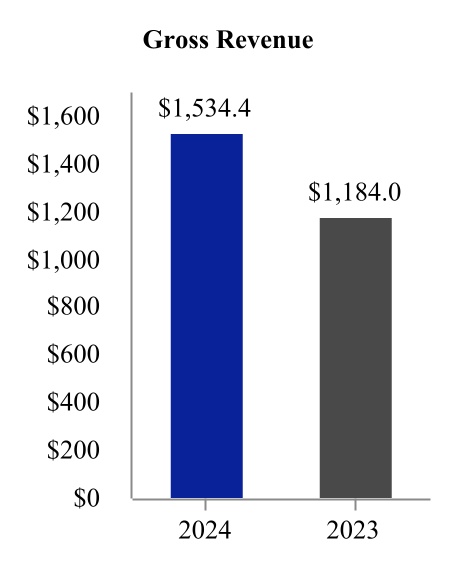

| Gross revenue | $ | $ | $ | $ | |||||||||||||||||||

| Cost of sales (exclusive of certain depreciation and amortization expense shown separately below) | ( | ( | ( | ( | |||||||||||||||||||

| General and administrative expenses | ( | ( | ( | ( | |||||||||||||||||||

| Revaluation of contingent liabilities | ( | ( | ( | ( | |||||||||||||||||||

| Depreciation and amortization expense (a) | ( | ( | ( | ( | |||||||||||||||||||

| Professional expenses | ( | ( | ( | ( | |||||||||||||||||||

| Advertising and marketing expenses | ( | ( | ( | ( | |||||||||||||||||||

| Income from operations | |||||||||||||||||||||||

| Interest income | |||||||||||||||||||||||

| Other income (expense), net | ( | ( | |||||||||||||||||||||

| Unrealized gain (loss) on investments in securities | ( | ||||||||||||||||||||||

| Change in TRA liability | ( | ( | ( | ( | |||||||||||||||||||

| Interest expense | ( | ( | ( | ( | |||||||||||||||||||

| Income before income taxes | |||||||||||||||||||||||

| Income tax benefit | |||||||||||||||||||||||

| Net income | |||||||||||||||||||||||

| Less: Net income attributable to noncontrolling interests | ( | ( | ( | ( | |||||||||||||||||||

| Net income attributable to Shift4 Payments, Inc. | $ | $ | $ | $ | |||||||||||||||||||

| Basic net income per share | |||||||||||||||||||||||

| Class A net income per share - basic | $ | $ | $ | $ | |||||||||||||||||||

| Class A weighted average common stock outstanding - basic | |||||||||||||||||||||||

| Class C net income per share - basic | $ | $ | $ | $ | |||||||||||||||||||

| Class C weighted average common stock outstanding - basic | |||||||||||||||||||||||

| Diluted net income per share | |||||||||||||||||||||||

| Class A net income per share - diluted | $ | $ | $ | $ | |||||||||||||||||||

| Class A weighted average common stock outstanding - diluted | |||||||||||||||||||||||

| Class C net income per share - diluted | $ | $ | $ | $ | |||||||||||||||||||

| Class C weighted average common stock outstanding - diluted | |||||||||||||||||||||||

| See accompanying notes to unaudited condensed consolidated financial statements. | |||||||||||||||||||||||

(a)Depreciation and amortization expense includes depreciation of equipment under lease of $13.0 million and $24.9 million for the three and six months ended June 30, 2024, respectively, and $8.2 million and $15.4 million for the three and six months ended June 30, 2023, respectively.

5

SHIFT4 PAYMENTS, INC.

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited) (in millions)

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

| Net income | $ | $ | $ | $ | |||||||||||||||||||

| Other comprehensive income (loss) | |||||||||||||||||||||||

| Unrealized gain (loss) on foreign currency translation adjustment | ( | ( | ( | ||||||||||||||||||||

| Comprehensive income | |||||||||||||||||||||||

| Less: Comprehensive income attributable to noncontrolling interests | ( | ( | ( | ( | |||||||||||||||||||

| Comprehensive income attributable to Shift4 Payments, Inc. | $ | $ | $ | $ | |||||||||||||||||||

| See accompanying notes to unaudited condensed consolidated financial statements. | |||||||||||||||||||||||

6

SHIFT4 PAYMENTS, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY

(Unaudited) (in millions, except share amounts)

Class A Common Stock | Class B Common Stock | Class C Common Stock | Additional Paid-In Capital | Treasury Stock | Retained Deficit | Accumulated Other Comprehensive Income | Noncontrolling Interests | Total Equity | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Shares | Amount | Shares | Amount | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balances at December 31, 2023 | $ | $ | $ | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Distributions to noncontrolling interests | — | — | — | — | — | — | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Equity-based compensation | — | — | — | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Vesting of restricted stock units, net of tax withholding | — | — | — | — | — | ( | — | — | — | — | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss | — | — | — | — | — | — | — | — | — | — | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balances at March 31, 2024 | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Recognition of Vectron noncontrolling interest | — | — | — | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Repurchases of Class A common stock to treasury stock | — | — | — | — | — | — | ( | ( | ( | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of Class A common stock, net of tax withholding | — | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Retirement of treasury stock | ( | — | — | — | — | — | ( | ( | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Exchange of shares held by Rook | — | ( | — | ( | — | — | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Distributions to noncontrolling interests | — | — | — | — | — | — | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Equity-based compensation | — | — | — | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Vesting of restricted stock units, net of tax withholding | — | — | — | — | — | ( | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss | — | — | — | — | — | — | — | — | — | — | ( | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balances at June 30, 2024 | $ | $ | $ | $ | $ | $ | ( | $ | ( | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

7

Class A Common Stock | Class B Common Stock | Class C Common Stock | Additional Paid-In Capital | Treasury Stock | Retained Deficit | Accumulated Other Comprehensive Income | Noncontrolling Interests | Total Equity | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Shares | Amount | Shares | Amount | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balances at December 31, 2022 | $ | $ | $ | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of Class A common stock and contingent share earnout in connection with an acquisition | — | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Exchange of shares held by Rook | — | ( | — | ( | — | — | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Distributions to noncontrolling interests | — | — | — | — | — | — | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Equity-based compensation | — | — | — | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Vesting of restricted stock units, net of tax withholding | — | — | — | — | — | ( | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive income | — | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balances at March 31, 2023 | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Issuance of Class A common stock | — | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Repurchases of Class A common stock to treasury stock | — | — | — | — | — | — | ( | ( | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Retirement of treasury stock | ( | — | — | — | — | — | ( | ( | — | — | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Exchange of shares held by Rook | — | ( | — | ( | — | — | — | — | — | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Distributions to noncontrolling interests | — | — | — | — | — | — | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Equity-based compensation | — | — | — | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Vesting of restricted stock units, net of tax withholding | — | — | — | — | — | ( | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Other comprehensive loss | — | — | — | — | — | — | — | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Balances at June 30, 2023 | $ | $ | $ | $ | $ | $ | ( | $ | $ | $ | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| See accompanying notes to unaudited condensed consolidated financial statements. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

8

SHIFT4 PAYMENTS, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited) (in millions)

| Six Months Ended June 30, | |||||||||||

| 2024 | 2023 | ||||||||||

| Operating activities | |||||||||||

| Net income | $ | $ | |||||||||

| Adjustments to reconcile net income to net cash provided by operating activities | |||||||||||

| Depreciation and amortization | |||||||||||

| Equity-based compensation expense | |||||||||||

| Revaluation of contingent liabilities | |||||||||||

| Unrealized gain on investments in securities | ( | ( | |||||||||

| Change in TRA liability | |||||||||||

| Amortization of capitalized financing costs | |||||||||||

| Provision for bad debts | |||||||||||

| Deferred income taxes | ( | ( | |||||||||

| Unrealized foreign exchange gains | ( | ||||||||||

| Other noncash items | ( | ||||||||||

| Change in operating assets and liabilities | |||||||||||

| Settlement activity, net | ( | ||||||||||

| Accounts receivable | ( | ( | |||||||||

| Prepaid expenses and other assets | ( | ( | |||||||||

| Inventory | |||||||||||

| Capitalized customer acquisition costs | ( | ( | |||||||||

| Accounts payable | |||||||||||

| Accrued expenses and other liabilities | |||||||||||

| Payments on contingent liabilities in excess of initial fair value | ( | ||||||||||

| Right-of-use assets and lease liabilities, net | ( | ||||||||||

| Deferred revenue | ( | ( | |||||||||

| Net cash provided by operating activities | |||||||||||

| Investing activities | |||||||||||

| Acquisitions, net of cash acquired | ( | ( | |||||||||

| Acquisition of equipment to be leased | ( | ( | |||||||||

| Capitalized software development costs | ( | ( | |||||||||

| Acquisition of property, plant and equipment | ( | ( | |||||||||

| Residual commission buyouts | ( | ( | |||||||||

| Purchase of intangible assets | ( | ||||||||||

| Proceeds from sale of investments in securities | |||||||||||

| Net cash used in investing activities | ( | ( | |||||||||

| Financing activities | |||||||||||

| Repurchases of Class A common stock | ( | ( | |||||||||

| Payments for withholding tax related to vesting of restricted stock units | ( | ( | |||||||||

| Payments on contingent liabilities | ( | ( | |||||||||

| Distributions to noncontrolling interests | ( | ( | |||||||||

| Net change in bank deposits | ( | ||||||||||

| Net cash used in financing activities | ( | ( | |||||||||

| Effect of exchange rate changes on cash and cash equivalents and restricted cash | ( | ||||||||||

| Change in cash and cash equivalents and restricted cash | ( | ( | |||||||||

| Cash and cash equivalents and restricted cash, beginning of period | |||||||||||

| Cash and cash equivalents and restricted cash, end of period | $ | $ | |||||||||

| See accompanying notes to unaudited condensed consolidated financial statements. | |||||||||||

9

SHIFT4 PAYMENTS, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Unaudited) (in millions, except share and per share amounts)

1.Organization, Basis of Presentation and Significant Accounting Policies

Organization

Shift4 Payments, Inc. (“Shift4 Payments” or “the Company”) was incorporated in Delaware in order to carry on the business of Shift4 Payments, LLC and its consolidated subsidiaries. The Company is a leading independent provider of software and payment processing solutions in the United States (“U.S.”) based on total volume of payments processed.

Basis of Presentation

The accompanying interim condensed consolidated financial statements of the Company are unaudited. These interim condensed consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the U.S. (“U.S. GAAP”) and the applicable rules and regulations of the U.S. Securities and Exchange Commission (“SEC”) for interim financial information. These financial statements do not include all information and footnotes required by U.S. GAAP for complete financial statements. The December 31, 2023 Condensed Consolidated Balance Sheet was derived from audited financial statements as of that date, but does not include all of the information and footnotes required by U.S. GAAP for complete financial statements.

In the opinion of management, the unaudited condensed consolidated financial statements reflect all adjustments consisting only of normal recurring adjustments necessary to state fairly the financial position, results of operations and cash flows for the periods presented in conformity with U.S. GAAP applicable to interim periods. The results of operations for the interim periods presented are not necessarily indicative of results for the full year or future periods. These unaudited condensed consolidated financial statements should be read in conjunction with the audited consolidated financial statements and the related notes thereto as of and for the fiscal year ended December 31, 2023, as disclosed in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2023 (the “2023 Form 10-K”).

The assets and liabilities of Shift4 Payments, LLC represent substantially all of the consolidated assets and liabilities of Shift4 Payments, Inc. with the exception of certain cash balances, amounts payable under the Tax Receivable Agreement (“TRA”), and the aggregate principal amount of $690.0 million of 2025 Convertible Notes and $632.5 million of 2027 Convertible Notes (together, the “Convertible Notes”) that are held by Shift4 Payments, Inc. directly. As of June 30, 2024 and December 31, 2023, $5.5 million and $3.6 million of cash, respectively, was directly held by Shift4 Payments, Inc. As of June 30, 2024 and December 31, 2023, the TRA liability was $8.2 million and $5.1 million, respectively. In connection with the issuance of the Convertible Notes, Shift4 Payments, Inc. entered into Intercompany Convertible Notes with Shift4 Payments, LLC, whereby Shift4 Payments, Inc. provided the net proceeds from the issuance of the Convertible Notes to Shift4 Payments, LLC in the amount of $1,322.5 million. Shift4 Payments, Inc., which was incorporated on November 5, 2019, has not had any material operations on a standalone basis since its inception, and all of the operations of the Company are carried out by Shift4 Payments, LLC and its subsidiaries.

Use of Estimates

10

Significant Accounting Policies

The Company’s significant accounting policies are discussed in Note 1 to Shift4 Payments, Inc.’s consolidated financial statements as of and for the year ended December 31, 2023 in the 2023 Form 10-K. There have been no significant changes to these policies which have had a material impact on the Company’s unaudited condensed consolidated financial statements and related notes during the six months ended June 30, 2024.

Cash and Cash Equivalents and Restricted Cash

Highly liquid investments with maturities of three months or less at the date of purchase are considered to be cash equivalents and are stated at cost, which approximates fair value. The Company’s cash equivalents consist of highly liquid investments in money market funds.

The Company classifies certain cash that is not available for use in its operations as restricted. Substantially all of the Company’s Restricted cash balance is related to a deposit in its U.S. sponsor bank merchant settlement account.

| June 30, 2024 | December 31, 2023 | ||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash | |||||||||||

| Cash and cash equivalents included in Settlement assets | |||||||||||

| Total cash and cash equivalents and restricted cash on the unaudited Condensed Consolidated Statements of Cash Flows | $ | $ | |||||||||

The Company maintains its cash with what are widely considered to be high credit quality financial institutions. U.S. cash balances are insured by the Federal Deposit Insurance Corporation (“FDIC”) up to $250 thousand per bank. The Company maintains cash and cash equivalent balances in excess of FDIC limits. The Company does not believe that it is subject to unusual credit risk beyond the normal credit risk associated with commercial banking relationships.

Settlement Assets and Liabilities

Settlement assets and liabilities are balances related to the settlement process which involves the transferring of funds between card issuers, merchants and other third parties. The Company currently operates under two different models: (1) a sponsorship model and (2) a direct member model. In the U.S., the Company operates under the sponsorship model and outside the U.S. the Company primarily operates under the direct member model. The Company’s operations outside the U.S. are primarily related to the business of Finaro, which was acquired in the fourth quarter of 2023.

Sponsorship Model

In the U.S., the Company operates under the sponsorship model. In order for the Company to provide payment processing services, Visa, MasterCard and other payment networks require sponsorship by a member clearing bank. The Company has an agreement with banks and financial institutions (the “Sponsoring Member”), to provide sponsorship services to the Company. The sponsorship services allow the Company to route transactions under the Sponsoring Members’ membership to clear card transactions through card networks. Under this model, the standards of the payment networks restrict the Company from performing funds settlement and require that these funds be in the possession of the Sponsoring Member until the merchant is funded. Accordingly, settlement assets and obligations resulting from the submission of settlement files to the network or cash received from the network in advance of funding the network are the responsibility of the Sponsoring Member and are not recorded on the Company’s unaudited Condensed Consolidated Balance Sheets.

11

Direct Member Model

The Company’s European and U.K. business (previously known as Finaro) operates as a full acquirer and without a sponsor bank. Under the direct member model, the Company’s Consolidated Balance Sheets include settlement assets and liabilities that represent balances arising from the settlement process which involves the transferring of funds between card issuers, payment networks, processors, and merchants, as well as collateral held to manage merchant credit risk. As a processor, the Company facilitates the clearing and settlement activity for the merchant and records settlement assets and liabilities on the Consolidated Balance Sheets upon processing a payment transaction. Settlement assets represent cash received or amounts receivable primarily from payment networks or bank partners. Settlement liabilities primarily represent amounts payable to merchants. Settlement assets are in excess of Settlement liabilities due to prefunding provided to certain merchants.

Amounts included on the unaudited Condensed Consolidated Balance Sheets as Collateral held by card networks relate to collateral required by the card networks to operate as a direct member.

Recent Accounting Pronouncements

Accounting Pronouncements Adopted

In June 2022, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2022-03, Fair Value Measurement of Equity Securities Subject to Contractual Sale Restrictions, to clarify that a contractual restriction on the sale of an equity security is not considered part of the unit of account of the equity security and, therefore, is not considered in measuring the fair value of the equity security. ASU 2022-03 also clarifies that an entity cannot recognize and measure a contractual sale restriction as a separate unit of account. The amendments in ASU 2022-03 became effective for the Company on January 1, 2024 on a prospective basis. The adoption did not have a significant impact on the Company’s unaudited condensed consolidated financial statements.

Accounting Pronouncements Not Yet Adopted

In December 2023, the FASB issued ASU 2023-09, Income Taxes: Improvements to Income Tax Disclosures, which provides qualitative and quantitative updates to the rate reconciliation and income taxes paid disclosures, among others, in order to enhance the transparency of income tax disclosures, including consistent categories and greater disaggregation of information in the rate reconciliation and disaggregation by jurisdiction of income taxes paid. The amendments in ASU 2023-09 are effective for fiscal 2025, with early adoption permitted. The amendments should be applied prospectively, however, retrospective application is also permitted. The Company does not plan to early adopt ASU 2023-09 and is evaluating the impact of the amendments on the Company’s unaudited condensed consolidated financial statements.

2.Acquisitions

Each of the following acquisitions was accounted for as a business combination using the acquisition method of accounting. The respective purchase prices were allocated to the assets acquired and liabilities assumed based on the estimated fair values at the date of acquisition. The excess of the purchase price over the fair value of the net assets acquired was allocated to goodwill and represents the future economic benefits arising from other assets acquired, which cannot be individually identified or separately recognized.

Vectron

On June 14, 2024, the Company acquired a majority stake in Vectron Systems AG (“Vectron”). Based in Germany, Vectron is a supplier of POS systems to the restaurant and hospitality verticals that management believes will provide the Company with local product expertise and a European distribution network of POS resellers. Throughout the remainder of June 2024, the Company purchased additional shares of Vectron’s common stock through a public tender offer and open market purchases. As of June 30, 2024, the Company owned approximately 74 % of Vectron’s common stock, for which it paid $59.0 million of total purchase consideration, net of cash acquired. Subsequent to June 30, 2024, the Company will attempt to acquire additional ownership through the public tender offer and implement a process to gain operational control of Vectron. The Company consolidates 100 % of Vectron’s assets, liabilities, revenues and expenses and records a noncontrolling interest balance for the 26 % economic interest in Vectron not held by the Company. Total purchase consideration was as follows:

12

| Cash | $ | ||||

| Contingent consideration (a) | |||||

| Total purchase consideration | |||||

| Less: cash acquired | ( | ||||

| Total purchase consideration, net of cash acquired | |||||

| Noncontrolling interest as of June 30, 2024 | |||||

| Fair value of net assets acquired | $ | ||||

(a) The Company agreed to a cash earnout due to certain former shareholders of Vectron based on the achievement against certain operational metrics over the next | |||||

The following table summarizes the fair value assigned to the assets acquired and liabilities assumed at the acquisition date. These amounts reflect various preliminary fair value estimates and assumptions, and are subject to change within the measurement period as valuations are finalized. The primary area of preliminary purchase price allocation subject to change relates to the valuation of accounts receivable, prepaid expenses and other current assets, other intangible assets, accounts payable, accrued expenses and other current liabilities, and residual goodwill.

| Accounts receivable | $ | ||||

| Inventory | |||||

| Prepaid expenses and other current assets | |||||

| Goodwill (a) | |||||

| Other intangible assets | |||||

| Property, plant and equipment, net | |||||

| Right-of-use assets | |||||

| Other noncurrent assets | |||||

| Accounts payable | ( | ||||

| Accrued expenses and other current liabilities | ( | ||||

| Deferred revenue | ( | ||||

| Current lease liabilities | ( | ||||

| Deferred tax liability | ( | ||||

| Noncurrent lease liabilities | ( | ||||

| Other noncurrent liabilities (b) | ( | ||||

| Net assets acquired | $ | ||||

| (a) Goodwill is not deductible for tax purposes. | |||||

(b) In connection with the Company’s majority stake in Vectron and due to Vectron’s acquisition of acardo group AG (“Acardo”) in December 2022, the Company became party to an earnout agreement with certain former shareholders of Acardo. The earnout is payable in multiple tranches, with up to € | |||||

The fair values of other intangible assets were estimated using inputs classified as Level 3 under the income approach using the relief-from-royalty method for acquired technology and the trade name, and the multi-period excess earnings method for merchant relationships. This transaction was not taxable for income tax purposes. The estimated life of acquired technology, merchant relationships and trade name are , and seven years , respectively.

The acquisition of Vectron did not have a material impact on the Company’s unaudited condensed consolidated financial statements.

13

Revel

On June 13, 2024, the Company completed the acquisition of Revel Systems, Inc. (“Revel”) by acquiring 100 % of its common stock for $245.3 million of total purchase consideration, net of cash acquired. Revel offers a cloud-based POS system primarily for multi-location merchants, focusing on restaurants, as well as back office and marketing tools that management believes will strengthen the Company’s presence within the restaurant and retail markets. Total purchase consideration was as follows:

| Cash (a) | $ | ||||

| Total purchase consideration | |||||

| Less: cash acquired | ( | ||||

| Total purchase consideration, net of cash acquired | $ | ||||

| (a) Subject to customary post-closing adjustments. | |||||

The following table summarizes the fair value assigned to the assets acquired and liabilities assumed at the acquisition date. These amounts reflect various preliminary fair value estimates and assumptions, and are subject to change within the measurement period as valuations are finalized. The primary area of preliminary purchase price allocation subject to change relates to the valuation of accounts receivable, prepaid expenses and other current assets, other intangible assets, accounts payable, accrued expenses and other current liabilities, and residual goodwill.

| Accounts receivable | $ | ||||

| Inventory | |||||

| Prepaid expenses and other current assets | |||||

| Right-of-use assets | |||||

| Goodwill (a) | |||||

| Other intangible assets | |||||

| Other noncurrent assets | |||||

| Accounts payable | ( | ||||

| Accrued expenses and other current liabilities | ( | ||||

| Deferred revenue | ( | ||||

| Current lease liabilities | ( | ||||

| Noncurrent lease liabilities | ( | ||||

| Net assets acquired | $ | ||||

| (a) Goodwill is not deductible for tax purposes. | |||||

The fair values of other intangible assets were estimated using inputs classified as Level 3 under the income approach using the relief-from-royalty method for acquired technology and the trade name, and the multi-period excess earnings method for merchant relationships. This transaction was not taxable for income tax purposes. The estimated life of acquired technology, merchant relationships and trade name are , and three years , respectively.

The acquisition of Revel did not have a material impact on the Company’s unaudited condensed consolidated financial statements.

14

Finaro

On October 26, 2023, the Company completed the acquisition of Finaro by acquiring 100 % of its common stock for $330.8 million of total purchase consideration, net of cash acquired. Finaro is a cross-border eCommerce platform and bank specializing in solving complex payment problems for multi-national merchants that we believe will help drive our expansion into international markets. Total purchase consideration was as follows:

| Cash | $ | ||||

| Shares of Class A common stock (a) | |||||

| Contingent consideration (b) | |||||

| Settlement of preexisting relationship | |||||

| Total purchase consideration | |||||

| Less: cash acquired | ( | ||||

| Total purchase consideration, net of cash acquired | $ | ||||

(a) Approximately | |||||

(b) The Company agreed to pay additional cash consideration to the sellers equal to the proceeds realized from the sale of an investment in certain securities held by Finaro, when and if realized, after the deduction of tax payments, if any. The fair value of the contingent consideration was included in the initial purchase consideration and will be revalued quarterly until settlement. As of June 30, 2024, the fair value of the contingent consideration was $ | |||||

The following table summarizes the fair value assigned to the assets acquired and liabilities assumed at the acquisition date. These amounts reflect various preliminary fair value estimates and assumptions, and are subject to change within the measurement period as valuations are finalized. The primary area of preliminary purchase price allocation subject to change relates to the valuation of accounts receivable, prepaid expenses and other current assets, accounts payable, accrued expenses and other current liabilities, and residual goodwill.

| Settlement assets, excluding cash (a) | $ | ||||

| Accounts receivable | |||||

| Investments in securities | |||||

| Prepaid expenses and other current assets | |||||

| Goodwill (b) | |||||

| Acquired technology | |||||

| Merchant relationships | |||||

| Banking license | |||||

| Property, plant and equipment | |||||

| Collateral held by the card networks | |||||

| Right-of-use assets | |||||

| Other noncurrent assets | |||||

| Settlement liabilities | ( | ||||

| Accounts payable | ( | ||||

| Accrued expenses and other current liabilities | ( | ||||

| Bank deposits | ( | ||||

| Current lease liabilities | ( | ||||

| Noncurrent lease liabilities | ( | ||||

| Deferred tax liability | ( | ||||

| Other noncurrent liabilities | ( | ||||

| Net assets acquired | $ | ||||

(a) Excludes settlement-related cash of $ | |||||

| (b) Goodwill is not deductible for tax purposes. | |||||

15

The fair values of other intangible assets were estimated using inputs classified as Level 3 under the income approach using the multi-period excess earnings method for acquired technology, the with and without method for merchant relationships, and the replacement cost method for the banking license. This transaction was not taxable for income tax purposes. Management’s estimates of fair value are based upon assumptions related to projected revenues, earnings before interest income, interest expense, income taxes, and depreciation and amortization (“EBITDA”) margins, research and development addback, obsolescence rates, and discount rates. The estimated life of acquired technology, merchant relationships and the banking license are , and two years respectively. The goodwill arising from the acquisition largely consisted of revenue synergies associated with a larger total addressable market.

In connection with the transaction, the Company also entered into compensation arrangements with employees of Finaro. In aggregate, these agreements included approximately $25.0 million of restricted stock units that were issued in the first quarter of 2024 and vest over three years . These awards are accounted for as compensation expense.

Appetize

On October 2, 2023, the Company completed the acquisition of SpotOn Technologies, Inc.’s sports and entertainment division, formerly known as Appetize, by acquiring 100 % of its membership interests for $108.7 million of total purchase consideration, net of cash acquired. Appetize is a payments and software company that has served clients that management believes will strengthen the Company’s presence within the sports and entertainment market. Total purchase consideration was as follows:

| Cash | $ | ||||

| Total purchase consideration | |||||

| Less: cash acquired | ( | ||||

| Total purchase consideration, net of cash acquired | $ | ||||

The following table summarizes the fair value assigned to the assets acquired and liabilities assumed at the acquisition date. These amounts reflect various preliminary fair value estimates and assumptions, and are subject to change within the measurement period as valuations are finalized. The primary area of preliminary purchase price allocation subject to change relates to the valuation of accounts receivable, accounts payable, accrued expenses and other current liabilities, and residual goodwill.

| Accounts receivable | $ | ||||

| Inventory | |||||

| Prepaid expenses and other current assets | |||||

| Goodwill (a) | |||||

| Other intangible assets | |||||

| Other noncurrent assets | |||||

| Accounts payable | ( | ||||

| Accrued expenses and other current liabilities | ( | ||||

| Deferred revenue | ( | ||||

| Other noncurrent liabilities | ( | ||||

| Net assets acquired | $ | ||||

| (a) Goodwill is deductible for tax purposes. | |||||

The fair value of other intangible assets was estimated using inputs classified as Level 3 under the income approach using the multi-period excess earnings method for merchant relationships. This transaction was taxable for income tax purposes. The estimated life of merchant relationships is ten years . The goodwill arising from the acquisition largely consisted of revenue synergies associated with the ability to cross-sell newly acquired customers and technology capabilities.

16

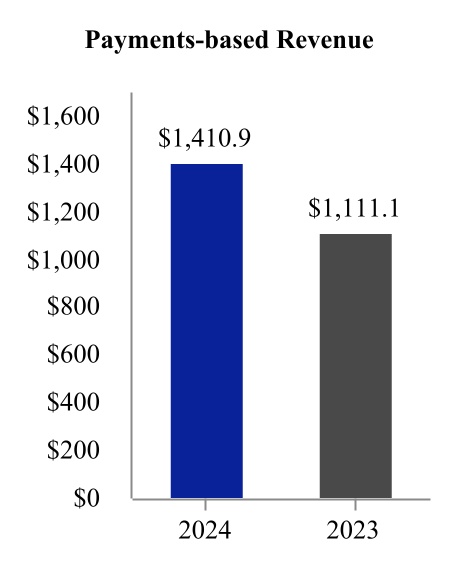

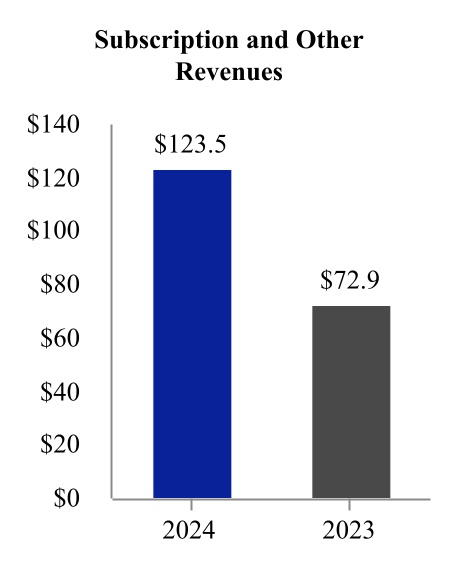

3.Revenue

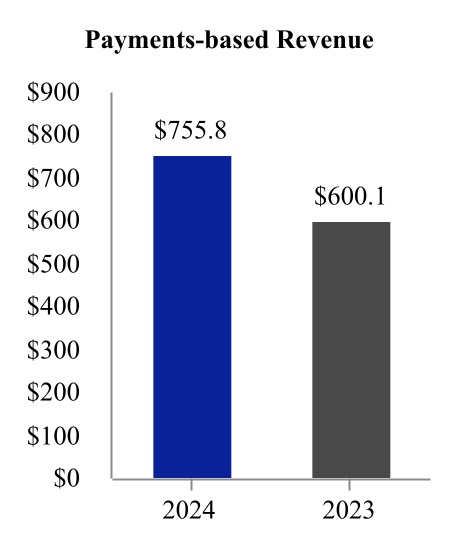

The Company’s revenue is comprised primarily of payments-based revenue which includes fees for payment processing and gateway services. Payment processing fees are primarily driven as a percentage of payment volume.

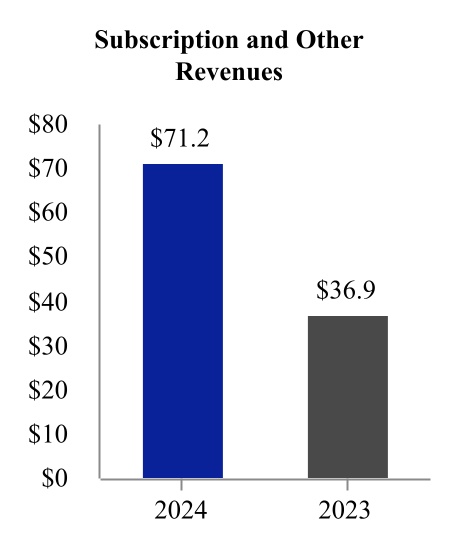

The Company also generates revenues from recurring fees which are based on the technology deployed to the merchant. Under ASC 606, the Company typically has three separate performance obligations under its recurring software as a service (“SaaS”) agreements for point-of-sale systems provided to merchants: (1) point-of-sale software, (2) lease of hardware and (3) other support services.

Disaggregated Revenue

The following table presents a disaggregation of the Company’s revenue from contracts with customers based on similar operational characteristics:

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||

| Payments-based revenue | $ | $ | $ | $ | |||||||||||||||||||

| Subscription and other revenues | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

Substantially all of the Company’s revenue is recognized over time.

Contract Liabilities

The Company charges merchants for various post-contract license support and service fees. These fees typically relate to a period of one year . The Company recognizes the revenue on a straight-line basis over its respective period. As of June 30, 2024 and December 31, 2023, the Company had deferred revenue of $19.9 million and $22.5 million, respectively. The change in the contract liabilities was primarily the result of a timing difference between payment from the customer and the Company’s satisfaction of each performance obligation.

The amount of gross revenue recognized that was included in the December 31, 2023 balance of deferred revenue was $7.0 million and $17.2 million for the three and six months ended June 30, 2024, respectively.

Allowance for Doubtful Accounts

The change in the Company’s allowance for doubtful accounts was as follows:

| Six Months Ended June 30, | |||||||||||

| 2024 | 2023 | ||||||||||

| Beginning balance | $ | $ | |||||||||

| Additions to expense | |||||||||||

| Write-offs, net of recoveries and other adjustments | ( | ( | |||||||||

| Ending balance | $ | $ | |||||||||

4.Goodwill

The changes in the carrying amount of goodwill were as follows:

| Balance at December 31, 2023 | $ | ||||

| Vectron acquisition (Note 2) | |||||

| Revel acquisition (Note 2) | |||||

| Purchase price adjustments related to prior period acquisitions | |||||

| Effect of foreign currency translation | ( | ||||

| Balance at June 30, 2024 | $ | ||||

17

5.Depreciation and Amortization

Amounts charged to expense in the Company’s unaudited Condensed Consolidated Statements of Operations for depreciation and amortization were as follows:

| Amortization | Depreciation | |||||||||||||||||||||||||||||||||||||

| Residual Commission Buyouts | Other Intangible Assets | Capitalized Customer Acquisition Costs | Equipment Under Lease | Property, Plant and Equipment | Total | |||||||||||||||||||||||||||||||||

| Three Months Ended June 30, 2024 | ||||||||||||||||||||||||||||||||||||||

| Depreciation and amortization expense | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Cost of sales | ||||||||||||||||||||||||||||||||||||||

| Total depreciation and amortization (a) | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Three Months Ended June 30, 2023 | ||||||||||||||||||||||||||||||||||||||

| Depreciation and amortization expense | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Cost of sales | ||||||||||||||||||||||||||||||||||||||

| Total depreciation and amortization (b) | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Six Months Ended June 30, 2024 | ||||||||||||||||||||||||||||||||||||||

| Depreciation and amortization expense | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Cost of sales | ||||||||||||||||||||||||||||||||||||||

| Total depreciation and amortization (c) | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Six Months Ended June 30, 2023 | ||||||||||||||||||||||||||||||||||||||

| Depreciation and amortization expense | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Cost of sales | ||||||||||||||||||||||||||||||||||||||

| Total depreciation and amortization (d) | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||

(a) Total amortization of $53.9 million consisted of amortization of acquired intangibles of $38.8 million and amortization of non-acquired intangibles of $15.1 million.

(b) Total amortization of $40.1 million consisted of amortization of acquired intangibles of $29.8 million and amortization of non-acquired intangibles of $10.3 million.

(c) Total amortization of $105.6 million consisted of amortization of acquired intangibles of $76.8 million and amortization of non-acquired intangibles of $28.8 million.

(d) Total amortization of $79.0 million consisted of amortization of acquired intangibles of $59.7 million and amortization of non-acquired intangibles of $19.3 million.

As of June 30, 2024, the estimated amortization expense for each of the five succeeding years and thereafter is as follows:

| Residual Commission Buyouts | Other Intangible Assets | Capitalized Customer Acquisition Costs | Total Amortization | ||||||||||||||||||||

| 2024 (remaining six months) | $ | $ | $ | $ | |||||||||||||||||||

| 2025 | |||||||||||||||||||||||

| 2026 | |||||||||||||||||||||||

| 2027 | |||||||||||||||||||||||

| 2028 | |||||||||||||||||||||||

| Thereafter | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

18

6.Residual Commission Buyouts

Residual commission buyouts represent transactions with certain third-party distribution partners, pursuant to which the Company acquires their ongoing merchant relationships that subscribe to the Company’s end-to-end payments platform.

Residual commission buyouts, net consisted of the following:

Weighted Average Amortization Period (in years) | June 30, 2024 | |||||||||||||||||||||||||

| Carrying Value | Accumulated Amortization | Net Carrying Value | ||||||||||||||||||||||||

| Residual commission buyouts from asset acquisitions | $ | $ | ( | $ | ||||||||||||||||||||||

| Residual commission buyouts from business combinations | ( | |||||||||||||||||||||||||

| Total residual commission buyouts | $ | $ | ( | $ | ||||||||||||||||||||||

Weighted Average Amortization Period (in years) | December 31, 2023 | |||||||||||||||||||||||||

| Carrying Value | Accumulated Amortization | Net Carrying Value | ||||||||||||||||||||||||

| Residual commission buyouts from asset acquisitions | $ | $ | ( | $ | ||||||||||||||||||||||

| Residual commission buyouts from business combinations | ( | |||||||||||||||||||||||||

| Total residual commission buyouts | $ | $ | ( | $ | ||||||||||||||||||||||

7.Other Intangible Assets, Net

Other intangible assets, net consisted of the following:

Weighted Average Amortization Period (in years) | June 30, 2024 | ||||||||||||||||||||||

| Carrying Value | Accumulated Amortization | Net Carrying Value | |||||||||||||||||||||

| Merchant relationships | $ | $ | ( | $ | |||||||||||||||||||

| Acquired technology | ( | ||||||||||||||||||||||

| Trademarks and trade names | ( | ||||||||||||||||||||||

| Capitalized software development costs | ( | ||||||||||||||||||||||

| Finaro banking license | ( | ||||||||||||||||||||||

| Total other intangible assets, net | $ | $ | ( | $ | |||||||||||||||||||

Weighted Average Amortization Period (in years) | December 31, 2023 | ||||||||||||||||||||||

| Carrying Value | Accumulated Amortization | Net Carrying Value | |||||||||||||||||||||

| Merchant relationships | $ | $ | ( | $ | |||||||||||||||||||

| Acquired technology | ( | ||||||||||||||||||||||

| Trademarks and trade names | ( | ||||||||||||||||||||||

| Capitalized software development costs | ( | ||||||||||||||||||||||

| Finaro banking license | ( | ||||||||||||||||||||||

| Total other intangible assets, net | $ | $ | ( | $ | |||||||||||||||||||

8.Capitalized Customer Acquisition Costs, Net

Capitalized customer acquisition costs, net consisted of the following:

Weighted Average Amortization Period (in years) | ||||||||||||||||||||||||||

| Carrying Value | Accumulated Amortization | Net Carrying Value | ||||||||||||||||||||||||

| Total costs as of June 30, 2024 | $ | $ | ( | $ | ||||||||||||||||||||||

| Total costs as of December 31, 2023 | $ | $ | ( | $ | ||||||||||||||||||||||

19

9.Equipment for Lease, Net

Equipment for lease, net consisted of the following:

Weighted Average Depreciation Period (in years) | June 30, 2024 | ||||||||||||||||||||||

| Carrying Value | Accumulated Depreciation | Net Carrying Value | |||||||||||||||||||||

| Equipment under lease | $ | $ | ( | $ | |||||||||||||||||||

| Equipment held for lease (a) | N/A | ||||||||||||||||||||||

| Total equipment for lease, net | $ | $ | ( | $ | |||||||||||||||||||

Weighted Average Depreciation Period (in years) | December 31, 2023 | ||||||||||||||||||||||

| Carrying Value | Accumulated Depreciation | Net Carrying Value | |||||||||||||||||||||

| Equipment under lease | $ | $ | ( | $ | |||||||||||||||||||

| Equipment held for lease (a) | N/A | ||||||||||||||||||||||

| Total equipment for lease, net | $ | $ | ( | $ | |||||||||||||||||||

| (a) Represents equipment that was not yet initially deployed to a merchant and, accordingly, is not being depreciated. | |||||||||||||||||||||||

10.Property, Plant and Equipment, Net

Property, plant and equipment, net consisted of the following:

| June 30, 2024 | December 31, 2023 | ||||||||||

| Equipment | $ | $ | |||||||||

| Capitalized software | |||||||||||

| Leasehold improvements | |||||||||||

| Furniture and fixtures | |||||||||||

| Vehicles | |||||||||||

| Total property, plant and equipment, gross | |||||||||||

| Less: Accumulated depreciation | ( | ( | |||||||||

| Total property, plant and equipment, net | $ | $ | |||||||||

11.Debt

The Company’s outstanding debt consisted of the following:

| Maturity | Effective Interest Rate | June 30, 2024 | December 31, 2023 | |||||||||||||||||||||||

| Convertible Senior Notes due 2025 ("2025 Convertible Notes") | December 15, 2025 | $ | $ | |||||||||||||||||||||||

| Convertible Senior Notes due 2027 ("2027 Convertible Notes") | August 1, 2027 | |||||||||||||||||||||||||

| November 1, 2026 | ||||||||||||||||||||||||||

| Total borrowings | ||||||||||||||||||||||||||

| Less: Unamortized capitalized financing fees | ( | ( | ||||||||||||||||||||||||

| Total long-term debt | $ | $ | ||||||||||||||||||||||||

Amortization of capitalized financing fees is included within “Interest expense” in the Company’s unaudited Condensed Consolidated Statements of Operations. Amortization expense for capitalized financing fees was $2.0 million and $4.1 million for the three and six months ended June 30, 2024, respectively, and $2.0 million and $4.1 million for the three and six months ended June 30, 2023, respectively.

20

Future principal payments

As of June 30, 2024, future principal payments associated with the Company’s long-term debt were as follows:

| 2024 | $ | |||||||

| 2025 | ||||||||

| 2026 | ||||||||

| 2027 | ||||||||

| Total | $ | |||||||

Revolving Credit Facility

As of June 30, 2024, there were no borrowings on the Revolving Credit Facility and borrowing capacity was $100.0 million.

Restrictions and Covenants

The 2025 Convertible Notes, 2026 Senior Notes, 2027 Convertible Notes (collectively, the “Notes”) and Revolving Credit Facility include certain restrictions on the ability of Shift4 Payments, LLC to make loans, advances, or pay dividends to Shift4 Payments, Inc.

As of June 30, 2024 and December 31, 2023, the Company was in compliance with all financial covenants under its debt agreements. The Company expects to be in compliance with such financial covenants for at least 12 months following the issuance of these unaudited condensed consolidated financial statements.

12.Fair Value Measurement

U.S. GAAP defines a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements).

The Company determines the fair values of its assets and liabilities that are recognized or disclosed at fair value in accordance with the hierarchy described below. The following three levels of inputs may be used to measure fair value:

•Level 1—Quoted prices in active markets for identical assets or liabilities;

•Level 2—Observable inputs other than Level 1 prices such as quoted prices for similar assets or liabilities, quoted prices in markets that are not active, or other inputs that are observable or can be corroborated by observable market data for substantially the full term of the assets or liabilities; and

•Level 3—Unobservable inputs that are supported by little or no market activity and that are significant to the fair value of the assets or liabilities. Level 3 assets and liabilities include items where the determination of fair value requires significant management judgment or estimation.

The Company makes recurring fair value measurements of contingent liabilities arising from certain acquisitions and residual commission buyouts using Level 3 unobservable inputs. Contingent liabilities for residual commission buyouts are expected earnout payments related to the number of existing point-of-sale merchants that convert to full acquiring merchants. Contingent liabilities included in the purchase price of an acquisition are based on achievement of specified performance metrics as defined in the purchase agreement.

Acquisition-Related Contingent Consideration

The Company’s acquisitions often include contingent consideration, or earnout, provisions. The total fair value of contingent consideration related to the acquisitions of Vectron, Finaro, Online Payments Group, and Restaurant Technology Partners as of June 30, 2024 was $49.7 million, of which $30.6 million is included in “Accrued expenses and other current liabilities” and $19.1 million is included within “Other noncurrent liabilities” on the Company’s unaudited Condensed Consolidated Balance Sheets. The change in fair value of these liabilities is included in “Revaluation of contingent liabilities” on the Company’s unaudited Condensed Consolidated Statements of Operations. Each of these fair value measurements utilize Level 3 inputs, such as projected revenues, discount rates and other subjective inputs. See Note 2 for further information on the contingent consideration for Vectron and Finaro.

21

Online Payments Group

The Company entered into an earnout agreement with the former shareholders of Online Payments Group, not to exceed $60.0 million, with $30.0 million of the earnout payable as of September 2023 (“Tranche 1”) if key customers of Online Payments Group contribute a specified amount of revenue from September 29, 2022 to September 28, 2023 and the remaining $30.0 million payable as of September 2024 (“Tranche 2”) if key customers contribute a specified amount of revenue from September 29, 2022 to September 28, 2024. Each portion of the earnout will be paid 50 % in shares of the Company’s Class A common stock and 50 % in cash. The fair value of the earnout was included in the initial purchase consideration and is revalued quarterly until the end of the earnout period as a fair value adjustment within “Revaluation of contingent liabilities” in the Company’s unaudited Condensed Consolidated Statements of Operations. Tranche 1 was fully earned and paid in 2023. The fair value of Tranche 2 as of June 30, 2024 was estimated to be $28.3 million and is included in “Accrued expenses and other current liabilities” on the Company’s unaudited Condensed Consolidated Balance Sheets as of June 30, 2024.

Restaurant Technology Partners

The Company entered into an earnout agreement with certain former shareholders of the restaurant technology partner acquired in 2023, calculated as a multiple of the number of the restaurant technology partner’s merchants that are converted to the Company’s end-to-end payments platform during the 24 months following September 1, 2022, not to exceed $2.5 million in total. The earnout is expected to be paid in cash. The fair value of the earnout was included in the initial purchase consideration and will be revalued quarterly until the end of the earnout period as a fair value adjustment within “Revaluation of contingent liabilities” in the Company’s unaudited Condensed Consolidated Statements of Operations. As of June 30, 2024, the fair value of the earnout was $0.4 million, which is recognized in “Accrued expenses and other current liabilities” on the Company’s unaudited Condensed Consolidated Balance Sheets.

Asset-Related Contingent Consideration

As of June 30, 2024, the estimated fair value of the Company’s contingent consideration agreements entered into in conjunction with residual commission buyouts and the acquisition of other intangible assets was $0.6 million, which is included in “Accrued expenses and other current liabilities” on the Company’s unaudited Condensed Consolidated Balance Sheets. The fair values of the contingent consideration were estimated based on the projected attrition rates and other financial metrics within the respective merchant portfolios over the earnout periods.

The table below provides a reconciliation of the beginning and ending balances for the Level 3 contingent liabilities:

| Six Months Ended June 30, 2024 | |||||||||||||||||

| Contingent Liabilities for Acquisitions | Contingent Liabilities for Assets Acquired | Total Contingent Liabilities | |||||||||||||||

| Balance at beginning of period | $ | $ | $ | ||||||||||||||

| Contingent consideration | |||||||||||||||||

| Fair value adjustments | |||||||||||||||||

| Impact of foreign exchange | ( | ( | |||||||||||||||

Contingent liabilities that achieved earnout | ( | ( | ( | ||||||||||||||

| Balance at end of period | $ | $ | $ | ||||||||||||||

Fair value adjustments for contingent liabilities for acquisitions are recorded within “Revaluation of contingent liabilities” in the Company’s unaudited Condensed Consolidated Statements of Operations. There were no transfers into or out of Level 3 during the six months ended June 30, 2024.

22

The estimated fair value of the Company’s outstanding debt using quoted prices from over-the-counter markets, considered Level 2 inputs, was as follows:

| June 30, 2024 | December 31, 2023 | ||||||||||||||||||||||

| Carrying Value (a) | Fair Value | Carrying Value (a) | Fair Value | ||||||||||||||||||||

| 2025 Convertible Notes | $ | $ | $ | $ | |||||||||||||||||||

| 2027 Convertible Notes | |||||||||||||||||||||||

| 2026 Senior Notes | |||||||||||||||||||||||

| Total | $ | $ | $ | $ | |||||||||||||||||||

(a) Carrying value excludes unamortized debt issuance costs related to the Revolving Credit Facility of $ | |||||||||||||||||||||||

The estimated fair value of the Company’s investments in non-marketable equity securities was $72.9 million and $62.2 million as of June 30, 2024 and December 31, 2023, respectively. These non-marketable equity investments have no readily determinable fair values and are measured using the measurement alternative, which is defined as cost, less impairment, adjusted for observable price changes from orderly transactions for identical or similar investments of the same issuer. Adjustments for these investments, if any, are recorded in “Unrealized gain on investments in securities” on the Company’s unaudited Condensed Consolidated Statements of Operations. The Company recognized fair value adjustments to its non-marketable equity investments of $(0.2 ) million and $10.8 million for the three and six months ended June 30, 2024, respectively, the entire amount of which related to securities still held as of June 30, 2024, based primarily on secondary offerings of identical securities by the respective companies in 2024. The Company has recognized cumulative fair value adjustments to its non-marketable equity investments of $38.1 million.

The estimated fair value of the Company’s crypto settlement assets and crypto settlement liabilities was $7.5 million and $3.5 million as of June 30, 2024 and December 31, 2023, respectively. The Company has valued the assets and liabilities using quoted prices from active cryptocurrency exchanges for the underlying crypto assets, considered Level 2 inputs.

13.Income Taxes

The Company holds an economic interest in Shift4 Payments, LLC and consolidates its financial position and results. The remaining ownership of Shift4 Payments, LLC not held by the Company is considered a noncontrolling interest. Shift4 Payments, LLC is treated as a partnership for income tax reporting and its members, including the Company, are liable for federal, state, and local income taxes based on their share of the LLC’s taxable income. In addition, Shift4 Payments, LLC wholly owns various U.S. and foreign subsidiaries which are taxed as corporations for tax reporting. Taxable income or loss from these subsidiaries is not passed through to Shift4 Payments, LLC. Instead, such taxable income or loss is taxed at the corporate level subject to the prevailing corporate tax rates.

The Company’s effective tax rate was (3 )% and (0.5 )% for the three and six months ended June 30, 2024, respectively. The Company’s effective tax rate was (10 )% and (14 )% for the three and six months ended June 30, 2023, respectively. The effective tax rate for the three and six months ended June 30, 2024 was different than the U.S. federal statutory income tax rate of 21% primarily due to the income allocated to the noncontrolling interest, the full valuation allowance on Shift4 Payments, Inc., a $5.2 1.5 4.8 million tax benefit related to the valuation allowance release due to a legal entity restructuring.

23

The Company has assessed the realizability of the net deferred tax assets and in that analysis has considered the relevant positive and negative evidence available to determine whether it is more likely than not that some portion or all of the deferred tax assets will be realized. The Company has recorded a valuation allowance against the majority of Shift4 Payments, Inc.’s deferred tax assets as of June 30, 2024, and December 31, 2023. The Company intends to continue maintaining a valuation allowance on the deferred tax assets until there is sufficient evidence to support the reversal of all or some portion of these allowances. However, given the current earnings and anticipated future earnings, the Company believes there is a reasonable possibility that within the next 12 months, sufficient positive evidence may become available to allow the Company to reach a conclusion that a significant portion of the valuation allowance will no longer be needed. Release of the valuation allowance would result in the recognition of certain deferred tax assets and an increase to income tax benefit for the period the release is recorded. The exact timing and amount of the valuation allowance release are subject to change on the basis of the level of profitability that is able to be achieved.

Uncertain Tax Positions

The effects of uncertain tax positions are recognized in the Company’s unaudited condensed consolidated financial statements if these positions meet a “more-likely-than-not” threshold. For those uncertain tax positions that are recognized in the condensed consolidated financial statements, liabilities are established to reflect the portion of those positions it cannot conclude “more-likely-than-not” to be realized upon ultimate settlement. The Company’s policy is to recognize interest and penalties related to unrecognized tax benefits within “Income tax benefit (expense)” in the Company’s unaudited Condensed Consolidated Statements of Operations. Accrued interest and penalties, if any, are included within “Deferred tax liability” in the Company’s unaudited Condensed Consolidated Balance Sheets. As of June 30, 2024 and December 31, 2023, $6.9 million and $4.7 million, respectively, of uncertain tax positions were recognized within “Other noncurrent liabilities” in the Company’s unaudited Condensed Consolidated Balance Sheets, which were primarily recognized in conjunction with acquisitions.

Tax Receivable Agreement

The Company expects to obtain an increase in its share of the tax basis in the net assets of Shift4 Payments, LLC as LLC Interests are redeemed from or exchanged by the Continuing Equity Owners, at the option of the Company, determined solely by the Company’s independent directors. The Company intends to treat any redemptions and exchanges of LLC Interests as direct purchases of LLC Interests for U.S. federal income tax purposes. These increases in tax basis may reduce the amounts that it would otherwise pay in the future to various tax authorities. In connection with the Company’s initial public offering in June 2020 and certain organizational transactions that the Company effected in connection with it, the Company entered into the TRA with the Continuing Equity Owners.

The TRA provides for the payment by Shift4 Payments, Inc. of 85% of the amount of any tax benefits the Company actually realizes, or in some cases is deemed to realize, as a result of (i) increases in the Company’s share of the tax basis in the net assets of Shift4 Payments, LLC resulting from any redemptions or exchanges of LLC Interests, (ii) tax basis increases attributable to payments made under the TRA, and (iii) deductions attributable to imputed interest pursuant to the TRA. The Company expects to benefit from the remaining 15% of any of cash savings that it realizes.

As of June 30, 2024 and December 31, 2023, the Company recognized a TRA liability of $8.2 million and $5.1 million, respectively, after concluding it was probable that, based on estimates of future taxable income, the Company will realize tax benefits associated with the TRA. As of June 30, 2024, $4.1 million of the liability is recognized in “Accrued expenses and other current liabilities” on the Company’s unaudited Condensed Consolidated Balance Sheets and $4.1 million of the liability is recognized in “Other noncurrent liabilities” on the Company’s unaudited Condensed Consolidated Balance Sheets. As of June 30, 2024, the Company has not recognized the remaining $284.8 million liability under the TRA after concluding it was not probable that the Company will be able to realize the remaining tax benefits based on estimates of future taxable income. A payment of $1.7

If Rook were to exchange any of its LLC Interests subsequent to June 30, 2024, such exchanges could generate additional deferred tax assets and TRA liability. As of December 31, 2023, the estimated impact of the exchange of all of Rook’s LLC Interests was an additional deferred tax asset of approximately $545 million and a TRA liability of approximately $463 million. The actual amounts as of June 30, 2024 could differ materially from those disclosed as of December 31, 2023 as they are impacted by the timing of the exchanges, the valuation of corporate subsidiaries, the price of the Company’s shares of Class A common stock at the time of the exchange, and the tax rates then in effect.

24

Organisation for Economic Co-operation and Development (“OECD”) - Pillar Two

In December 2021, the Organisation for Economic Co-operation and Development issued model rules for a new global minimum tax framework (“Pillar Two”), and various governments around the world have passed, or are in the process of passing, legislation on this. Certain Pillar Two rules take effect in 2024 and 2025, depending on whether a particular jurisdiction has integrated the legislation into local law. The Company is continuing to monitor these impacts on its operating footprint and anticipates an increase in income tax expense associated with jurisdictions that have implemented an income inclusion rule or a Qualifying Minimum Top-up Tax (“QDMTT”). The Company is continuing to monitor and assess the impacts of rules set to take effect in 2025, such as the under-taxed profits rule. The impacts of Pillar Two to the Company are subject to change based on expansion and future acquisitions within jurisdictions that the Company does not currently operate.

14.Lease Agreements

The Company provides hardware, including terminals and point-of-sale equipment, to its merchants under operating leases as the lessor. The Company’s operating leases generally include options to extend the contract for successive one-year periods. Extension options are not included in the determination of lease income unless, at lease inception, it is reasonably certain that the option will be exercised. The Company’s operating leases do not include purchase options.

Lease payments received are recognized as income on a straight-line basis over the term of the agreement in accordance with ASC 606 and classified as gross revenue on the Company’s unaudited Condensed Consolidated Statements of Operations.

Total lease income for the three and six months ended June 30, 2024 was $6.6 million and $12.0 million, respectively, and $5.2 million and $10.5 million for the three and six months ended June 30, 2023, respectively.

The Company expects to receive future minimum lease payments for hardware provided under the Company’s SaaS agreements of $16.0 million from July 1, 2024 through June 30, 2025.

15.Related Party Transactions

The Company has a service agreement with Jared Isaacman, the Company’s Chief Executive Officer and founder (“Founder”), including access to aircrafts and a property. Total expense for this service, which is included in “General and administrative expenses” in the Company’s unaudited Condensed Consolidated Statements of Operations, was $0.3 0.5 no 2.0 million of distributions related to income taxes paid on behalf of Rook, which are included in “Distributions to noncontrolling interests” in the Company’s unaudited Condensed Consolidated Statements of Cash Flows.

In November 2021, the Company implemented a one-time discretionary equity award program for non-management employees. The Founder agreed to fund 50 % of this program through a contribution of shares of his Class C common stock. As of June 30, 2024, the expected contribution from the Founder totaled 592,219 shares of his Class C common stock. The one-time discretionary equity award program will vest in equal installments annually beginning in 2024. Vesting of the awards is subject to the continued employment of non-management employees.

Rook has entered into margin loan agreements, pursuant to which, in addition to other collateral, it has pledged LLC Interests and shares of the Company’s Class A and Class B common stock (collectively, “Rook Units”) to secure a margin loan. If Rook were to default on its obligations under the margin loan and fail to cure such default, the lender would have the right to exchange and sell up to 15,000,000 Rook units to satisfy Rook’s obligation.