Item 1. Reports to Stockholders.

C

OHEN

& STEERS

TAX

-A

DVANTAGED

PREFERRED

SECURITIES AND

INCOME

FUND

To Our Shareholders:

We would like to share with you our report for the six months ended April 30, 2024. The total returns for Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund (the Fund) and its comparative benchmarks were:

Six Months Ended April 30, 2024 |

||||

Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund at Net Asset Value (a ) |

15.00 |

% | ||

Cohen & Steers Tax-Advantaged Preferred Securities and Income Fund at Market Value (a) |

15.13 |

% | ||

ICE BofA 7% Constrained DRD Eligible Preferred Securities Index (b) |

13.41 |

% | ||

Blended Benchmark—50% ICE BofA 7% Constrained DRD Eligible Preferred Securities Index/35% ICE BofA U.S. IG Institutional Capital Securities Index/15% Bloomberg Developed Market USD Contingent Capital Index (b) |

12.13 |

% | ||

Bloomberg U.S. Aggregate Bond Index (b) |

4.97 |

% | ||

The performance data quoted represent past performance. Past performance is no guarantee of future results. The investment return and the principal value of an investment will fluctuate and shares, if sold, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Current total returns of the Fund can be obtained by visiting our website at cohenandsteers.com. The Fund’s returns assume the reinvestment of all dividends and distributions at prices obtained under the Fund’s dividend reinvestment plan. Index performance does not reflect the deduction of any fees, taxes or expenses. An investor cannot invest directly in an index. Performance figures for periods shorter than one year are not annualized.

The Fund expects to make regular monthly distributions at a level rate (the Policy). Distributions paid by the Fund are subject to recharacterization for tax purposes and are taxable up to the amount of the Fund’s investment company taxable income and net realized gains. As a result of the Policy, the Fund may pay distributions in excess of the Fund’s investment company taxable income and net realized gains. This excess would be a return of capital distributed from the Fund’s assets. Distributions of capital decrease the Fund’s total assets and, therefore, could have the effect of increasing the Fund’s expense ratio. In addition, in order to make these distributions, the Fund may have to sell portfolio securities at a less than opportune time.

(a ) |

As a closed-end investment company, the price of the Fund’s exchange-traded shares will be set by market forces and can deviate from the net asset value (NAV) per share of the Fund. |

(b ) |

ICE BofA 7% Constrained DRD Eligible Preferred Securities Index contains all securities in the ICE BofA Fixed Rate Preferred Securities Index that are DRD (dividends received deduction) eligible, but caps issuer exposure at 7%. The ICE BofA U.S. IG Institutional Capital Securities Index tracks the performance of U.S. dollar denominated investment grade hybrid capital corporate and preferred securities publicly issued in the U.S. domestic market. The Bloomberg Developed Market USD Contingent Capital Index includes hybrid capital securities in developed markets with explicit equity conversion or write down loss absorption mechanisms that are based on an issuer’s regulatory capital ratio or other explicit solvency-based triggers. The Bloomberg U.S. Aggregate Bond Index is a broad market measure of the U.S. dollar-denominated investment-grade fixed-rate taxable bond market. The index includes Treasuries, government-related and corporate securities, mortgage-backed securities, asset-backed securities, and commercial mortgage-backed securities. |

The comparative indexes are not adjusted to reflect expenses or other fees that the U.S. Securities and Exchange Commission (SEC) requires to be reflected in the Fund’s performance. Index performance does not reflect the deduction of any fees, taxes or expenses. An investor cannot invest directly in an index. The Fund’s performance assumes dividends and distributions are reinvested at prices obtained under the Fund’s dividend reinvestment plan. |

1

C

OHEN

& STEERS

TAX

-A

DVANTAGED

PREFERRED

SECURITIES AND

INCOME

FUND

Market Review

Preferred securities had a strong total return in the six months ended April 30, 2024. Concerns of recession receded as the world’s major economies remained healthy during this period, driven by solid consumer spending. Headline U.S. inflation, which bottomed in mid-2023, remained stubbornly above 3%—and well above the Federal Reserve’s 2% target. However, interest rates, while volatile, ended the period modestly lower as investors debated the timing and magnitude of central bank interest rate cuts.

Credit spreads narrowed markedly, given the strength of the economy and investors’ search for income. Preferreds also benefited from strong call activity and limited new supply, which bolstered demand for existing issues. Consequently, preferred securities considerably outperformed other areas of fixed income.

Fund Performance

The Fund had a positive total return in the period and outperformed its blended benchmark on both a market price and net asset value basis.

The banking sector continued to rebound from the well-publicized bank failures that occurred in the first quarter of 2023, with concerns of contagion receding as fundamentals in the broader banking system remained healthy and resilient. Security selection in the banking sector, which accounted for roughly half of the portfolio’s assets, detracted from relative returns. This was partly due to underweight investments in certain well-performing floating-rate securities.

Insurance underperformed other preferred sectors despite solid underlying industry fundamentals. Property & casualty insurance companies continued to enjoy premium growth given the health of the economy, and life insurers benefited from rising interest rates. The sector’s underperformance stemmed partly from modest returns generated by very high-quality Japan-based insurers. The Fund’s security selection and underweight allocation to insurance aided relative performance. Contributors included out-of-index investments in a pair of well-performing, deeply discounted issues from an annuity provider and having no investment in certain low-coupon securities from Japanese companies.

Security selection in the energy and pipeline sectors further contributed to relative returns. The Fund held overweight or out-of-benchmark investments in certain securities from companies that, in addition to rising energy prices, benefited from business transactions that were viewed positively from a credit perspective.

The capital-intensive utilities sector benefited from healthy financials and a positive growth outlook partly supported by expected long-term demand for power for artificial intelligence applications. The Fund’s security selection in utilities preferreds detracted from relative performance due to out-of-index positions in several relatively defensive securities that lagged in the rally.

The portfolio’s security selection in the brokerage sector also detracted from relative performance, partly due to underweight or non-investments in well-performing issues from Morgan Stanley that we viewed as being richly valued.

Impact of Leverage on Fund Performance

The Fund employs leverage as part of an effort to enhance yield. Leverage can increase total return in rising markets, just as it can have the opposite effect in declining markets. The leverage significantly contributed to the Fund’s performance for the six months ended April 30, 2024.

2

C

OHEN

& STEERS

TAX

-ADVANTAGED

PREFERRED

SECURITIES

AND

INCOME

FUND

Impact of Derivatives on Fund Performance

The Fund used derivatives in the form of forward foreign currency exchange contracts to passively manage currency risk on certain Fund positions denominated in foreign currencies. The currency exchange contracts did not have a material impact on the Fund’s total return for the six months ended April 30, 2024.

In connection with its use of leverage, the Fund pays interest on a portion of its borrowings based on a floating rate under the terms of its credit agreement. To reduce the impact that an increase in interest rates could have on the performance of the Fund with respect to these borrowings, the Fund used interest rate swaps to exchange a significant portion of the floating rate for a fixed rate. In addition, the Fund used total return swap contracts to manage credit risk. The Fund’s use of interest rate swaps and total return swaps did not have a material impact on the Fund’s total return for the six months ended April 30, 2024.

Sincerely,

|

| |

W ILLIAM F. SCAPELL Portfolio Manager |

E LAINE ZAHARIS -NIKAS Portfolio Manager |

|

| |

J ERRY DOROST Portfolio Manager |

R OBERT KASTOFF Portfolio Manager |

The views and opinions in the preceding commentary are subject to change without notice and are as of the date of the report. There is no guarantee that any market forecast set forth in the commentary will be realized. This material represents an assessment of the market environment at a specific point in time, should not be relied upon as investment advice and is not intended to predict or depict performance of any investment.

Visit Cohen & Steers online at cohenandsteers.com

For more information about the Cohen & Steers family of mutual funds, visit cohenandsteers.com. Here you will find fund net asset values, fund fact sheets and portfolio highlights, as well as educational resources and timely market updates.

Our website also provides comprehensive information about Cohen & Steers, including our most recent press releases, profiles of our senior investment professionals and their investment approach to each asset class. The Cohen & Steers family of mutual funds specializes in liquid real assets, including real estate securities, listed infrastructure and natural resource equities, as well as preferred securities and other income solutions.

3

C

OHEN

& STEERS

TAX-

ADVANTAGED

PREFERRED

SECURITIES AND

INCOME

FUND

Performance Review (Unaudited)

Average Annual Total Returns—For Periods Ended April 30, 2024

1 Year |

5 Years |

10 Years |

Since Inception (a) |

|||||||||||||

Fund at NAV |

16.37 |

% |

— |

— |

1.69 |

% | ||||||||||

Fund at Market Value |

18.32 |

% |

— |

— |

-0.85 |

% | ||||||||||

The performance data quoted represent past performance. Past performance is no guarantee of future results. The investment return will vary and the principal value of an investment will fluctuate and shares, if sold, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Performance results reflect the effect of leverage from utilization of borrowings under a credit agreement. Current total returns of the Fund can be obtained by visiting our website at cohenandsteers.com. The Fund’s returns assume the reinvestment of all dividends and distributions at prices obtained under the Fund’s dividend reinvestment plan. The performance table does not reflect the deduction of brokerage commissions or taxes that a shareholder would pay on Fund distributions or the sale of Fund shares.

(a) |

Commencement of investment operations was October 28, 2020. |

4

C

OHEN

& STEERS

TAX

-ADVANTAGED

PREFERRED

SECURITIES

AND

INCOME

FUND

Our Leverage Strategy

(Unaudited)

Our current leverage strategy utilizes borrowings up to the maximum permitted by the Investment Company Act of 1940 to provide additional capital for the Fund, with an objective of increasing net income available for shareholders. As of April 30, 2024 leverage represented 35% of the Fund’s managed assets.

Through a combination of variable rate financing and interest rate swaps, the Fund has locked in interest rates on a significant portion of this additional capital through 2027 (where we effectively reduce our variable rate obligation and lock in our fixed rate obligation over various terms). Locking in a significant portion of our leveraging costs is designed to protect the dividend-paying ability of the Fund. The use of leverage increases the volatility of the Fund’s NAV in both up and down markets. However, we believe that locking in portions of the Fund’s leveraging costs for the various terms partially protects the Fund’s expenses from an increase in short-term interest rates.

Leverage Facts

(a)(b

)

Leverage (as a % of managed assets) |

35% | |

% Variable Rate Financing |

3% | |

Variable Rate |

6.0% | |

% Fixed Rate Financing (c ) |

97% | |

Weighted Average Rate on Fixed Financing |

1.2% | |

Weighted Average Term on Fixed Financing |

1.9 years |

The Fund seeks to enhance its dividend yield through leverage. The use of leverage is a speculative technique and there are special risks and costs associated with leverage. The NAV of the Fund’s shares may be reduced by the issuance and ongoing costs of leverage. So long as the Fund is able to invest in securities that produce an investment yield that is greater than the total cost of leverage, the leverage strategy will produce higher current net investment income for shareholders. On the other hand, to the extent that the total cost of leverage exceeds the incremental income gained from employing such leverage, shareholders would realize lower net investment income. In addition to the impact on net income, the use of leverage will have an effect of magnifying capital appreciation or depreciation for shareholders. Specifically, in an up market, leverage will typically generate greater capital appreciation than if the Fund were not employing leverage. Conversely, in down markets, the use of leverage will generally result in greater capital depreciation than if the Fund had been unlevered. To the extent that the Fund is required or elects to reduce its leverage, the Fund may need to liquidate investments, including under adverse economic conditions which may result in capital losses potentially reducing returns to shareholders. There can be no assurance that a leveraging strategy will be successful during any period in which it is employed.

(a) |

Data as of April 30, 2024. Information is subject to change. |

(b) |

See Note 7 in Notes to Financial Statements. |

(c) |

Represents fixed payer interest rate swap contracts on variable rate borrowing. |

5

C

OHEN

& STEERS

TAX-

ADVANTAGED

PREFERRED

SECURITIES AND

INCOME

FUND

April 30, 2024

Top Ten Holdings

(a)

(Unaudited)

Security |

Value |

% of Managed Assets |

||||||

Wells Fargo & Co., 7.625% |

$ |

38,525,140 |

2.2 |

|||||

Stichting AK Rabobank Certificaten, 6.50% (Netherlands) |

34,604,344 |

2.0 |

||||||

JPMorgan Chase & Co., 6.875%, Series NN |

34,229,794 |

2.0 |

||||||

Charles Schwab Corp., 5.375%, Series G |

31,520,816 |

1.8 |

||||||

Wells Fargo & Co., 3.90%, Series BB |

27,367,675 |

1.6 |

||||||

Citigroup, Inc., 7.625%, Series AA |

26,891,672 |

1.6 |

||||||

Goldman Sachs Group, Inc., 7.50%, Series X |

26,356,056 |

1.5 |

||||||

Charles Schwab Corp., 4.00%, Series I |

24,632,982 |

1.4 |

||||||

Bank of America Corp., 6.10%, Series AA |

23,131,964 |

1.4 |

||||||

BNP Paribas SA, 7.75% (France) |

20,824,808 |

1.2 |

||||||

(a) |

Top ten holdings (excluding short-term investments and derivative instruments) are determined on the basis of the value of individual securities held. The Fund may also hold positions in other securities issued by the companies listed above. See the Schedule of Investments for additional details on such other positions. |

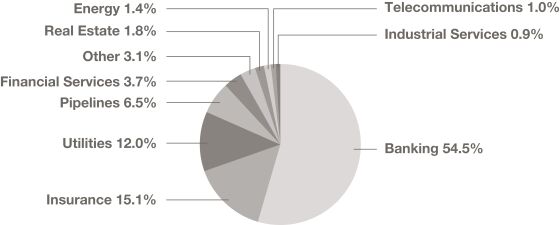

Sector Breakdown

(b)

(Based on Managed Assets)

(Unaudited)

(b) |

Excludes derivative instruments. |

6

C

OHEN

& STEERS

TAX-

ADVANTAGED

PREFERRED

SECURITIES AND

INCOME

FUND

SCHEDULE OF INVESTMENTS

April 30, 2024 (Unaudited)

Shares |

Value |

|||||||||||

P REFERRED SECURITIES —EXCHANGE -TRADED |

27.1% |

|||||||||||

B ANKING |

6.6% |

|||||||||||

Federal Agricultural Mortgage Corp., 4.875%, Series G (a) |

410,836 |

$ |

7,949,677 |

|||||||||

First Horizon Corp., 6.50% (a)(b) |

226,999 |

5,379,876 |

||||||||||

Morgan Stanley, 4.25%, Series O (a)(b) |

74,599 |

1,385,303 |

||||||||||

Morgan Stanley, 5.85% to 4/15/27, Series K (a)(b) |

294,081 |

7,046,181 |

||||||||||

Morgan Stanley, 6.375% to 10/15/24, Series I (a)(b) |

289,449 |

7,213,069 |

||||||||||

Morgan Stanley, 6.875% to 7/15/24, Series F (a)(b) |

680,397 |

17,118,789 |

||||||||||

Morgan Stanley, 7.125% to 7/15/24, Series E (a)(b) |

350,000 |

8,830,500 |

||||||||||

Regions Financial Corp., 5.70% to 5/15/29, Series C (a)(b)(c) |

164,750 |

3,601,435 |

||||||||||

Texas Capital Bancshares, Inc., 5.75%, Series B (a)(b) |

103,308 |

1,970,084 |

||||||||||

Wells Fargo & Co., 4.375%, Series CC (a)(b) |

117,864 |

2,245,309 |

||||||||||

Wells Fargo & Co., 4.70%, Series AA (a)(b) |

288,351 |

5,813,156 |

||||||||||

Wells Fargo & Co., 4.75%, Series Z (a)(b) |

268,039 |

5,459,954 |

||||||||||

74,013,333 |

||||||||||||

C ONSUMER STAPLE PRODUCTS |

0.7% |

|||||||||||

CHS, Inc., 7.50%, Series 4 (a) |

299,435 |

7,680,508 |

||||||||||

F INANCIAL SERVICES |

3.0% |

|||||||||||

Affiliated Managers Group, Inc., 6.75%, due 3/30/64 (b)(d) |

176,252 |

4,512,051 |

||||||||||

Apollo Global Management, Inc., 7.625% to 9/15/28, due 9/15/53 (b)(c) |

147,108 |

3,886,593 |

||||||||||

Brookfield Oaktree Holdings LLC, 6.55%, Series B (a)(b) |

633,858 |

13,627,947 |

||||||||||

Brookfield Oaktree Holdings LLC, 6.625%, Series A (a)(b) |

214,812 |

4,682,902 |

||||||||||

TPG Operating Group II LP, 6.95%, due 3/15/64 (b)(d) |

266,478 |

6,872,468 |

||||||||||

33,581,961 |

||||||||||||

I NDUSTRIAL SERVICES |

1.4% |

|||||||||||

WESCO International, Inc., 10.625% to 6/22/25, Series A (a)(c) |

600,807 |

15,855,297 |

||||||||||

I NSURANCE |

8.7% |

|||||||||||

Allstate Corp., 7.375%, Series J (a)(b) |

174,600 |

4,658,328 |

||||||||||

Arch Capital Group Ltd., 4.55%, Series G (a)(b) |

172,499 |

3,329,231 |

||||||||||

Arch Capital Group Ltd., 5.45%, Series F (a)(b) |

351,086 |

7,871,348 |

||||||||||