FALSE2021FY0001788717http://fasb.org/us-gaap/2021-01-31#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2021-01-31#AccountsPayableAndAccruedLiabilitiesCurrentP1Y00017887172021-01-012021-12-3100017887172022-03-21iso4217:USD00017887172022-03-22xbrli:shares00017887172021-12-3100017887172020-12-31iso4217:USDxbrli:shares0001788717us-gaap:FranchiseMember2021-01-012021-12-310001788717us-gaap:FranchiseMember2020-01-012020-12-310001788717us-gaap:ProductMember2021-01-012021-12-310001788717us-gaap:ProductMember2020-01-012020-12-3100017887172020-01-012020-12-310001788717us-gaap:RedeemableConvertiblePreferredStockMemberus-gaap:PreferredStockMember2019-12-310001788717us-gaap:CommonStockMember2019-12-310001788717us-gaap:AdditionalPaidInCapitalMember2019-12-310001788717us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-12-310001788717us-gaap:ReceivablesFromStockholderMember2019-12-310001788717us-gaap:RetainedEarningsMember2019-12-3100017887172019-12-310001788717us-gaap:RetainedEarningsMember2020-01-012020-12-310001788717us-gaap:RedeemableConvertiblePreferredStockMemberus-gaap:PreferredStockMember2020-01-012020-12-310001788717us-gaap:CommonStockMember2020-01-012020-12-310001788717us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310001788717us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-01-012020-12-310001788717us-gaap:ReceivablesFromStockholderMember2020-01-012020-12-310001788717us-gaap:RedeemableConvertiblePreferredStockMemberus-gaap:PreferredStockMember2020-12-310001788717us-gaap:CommonStockMember2020-12-310001788717us-gaap:AdditionalPaidInCapitalMember2020-12-310001788717us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001788717us-gaap:ReceivablesFromStockholderMember2020-12-310001788717us-gaap:RetainedEarningsMember2020-12-310001788717us-gaap:RedeemableConvertiblePreferredStockMemberus-gaap:PreferredStockMember2021-01-012021-12-310001788717us-gaap:CommonStockMember2021-01-012021-12-310001788717us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001788717us-gaap:RetainedEarningsMember2021-01-012021-12-310001788717us-gaap:ReceivablesFromStockholderMember2021-01-012021-12-310001788717us-gaap:RedeemableConvertiblePreferredStockMemberus-gaap:PreferredStockMember2021-12-310001788717us-gaap:CommonStockMember2021-12-310001788717us-gaap:AdditionalPaidInCapitalMember2021-12-310001788717us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001788717us-gaap:ReceivablesFromStockholderMember2021-12-310001788717us-gaap:RetainedEarningsMember2021-12-3100017887172019-03-15xbrli:pure0001788717fxlv:MWIGLLCMember2019-03-1500017887172020-12-300001788717fxlv:FFortyFiveAusHoldCoMember2019-03-150001788717fxlv:FFortyFiveAusHoldCoMember2019-03-152019-03-150001788717fxlv:TwoThousandAndTwentyStockRepurchaseAgreementsMemberus-gaap:CommonStockMember2020-10-062020-10-060001788717fxlv:TwoThousandAndTwentyStockRepurchaseAgreementsMemberfxlv:MrDeutschMember2020-10-062020-10-060001788717us-gaap:CommonStockMemberus-gaap:IPOMember2021-07-152021-07-150001788717us-gaap:CommonStockMemberus-gaap:IPOMember2021-07-150001788717us-gaap:IPOMember2021-07-152021-07-15fxlv:shareholder00017887172021-07-150001788717us-gaap:RedeemableConvertiblePreferredStockMemberus-gaap:IPOMember2021-07-150001788717us-gaap:OverAllotmentOptionMember2021-08-132021-08-130001788717us-gaap:IPOMember2021-08-132021-08-1300017887172021-08-1300017887172021-08-172021-08-170001788717us-gaap:IPOMember2021-08-172021-08-170001788717us-gaap:CommonStockMember2021-07-012021-07-3100017887172021-07-012021-07-310001788717srt:MinimumMember2021-12-310001788717srt:MaximumMember2021-12-310001788717us-gaap:SoftwareAndSoftwareDevelopmentCostsMember2021-01-012021-12-310001788717us-gaap:RevolvingCreditFacilityMember2021-12-310001788717fxlv:TermLoanFacilitiesMember2020-12-310001788717srt:MinimumMemberus-gaap:FranchiseMember2021-01-012021-12-310001788717srt:MaximumMemberus-gaap:FranchiseMember2021-01-012021-12-310001788717fxlv:FranchiseRenewalFeeMember2021-01-012021-12-3100017887172021-01-012021-06-300001788717fxlv:DeferredStateContractsMember2021-01-012021-06-300001788717fxlv:DeferredStateFranchiseAgreementsMember2021-01-012021-12-310001788717us-gaap:InterestRateSwapMemberus-gaap:FairValueMeasurementsRecurringMember2020-12-310001788717us-gaap:FairValueMeasurementsRecurringMemberfxlv:EmbeddedDerivativeMember2020-12-310001788717us-gaap:VehiclesMember2021-01-012021-12-310001788717us-gaap:VehiclesMember2021-12-310001788717us-gaap:VehiclesMember2020-12-310001788717us-gaap:FurnitureAndFixturesMember2021-01-012021-12-310001788717us-gaap:FurnitureAndFixturesMember2021-12-310001788717us-gaap:FurnitureAndFixturesMember2020-12-310001788717fxlv:OfficeAndOtherEquipmentMember2021-01-012021-12-310001788717fxlv:OfficeAndOtherEquipmentMember2021-12-310001788717fxlv:OfficeAndOtherEquipmentMember2020-12-310001788717us-gaap:LeaseholdImprovementsMember2021-12-310001788717us-gaap:LeaseholdImprovementsMember2020-12-310001788717us-gaap:ConstructionInProgressMember2021-12-310001788717us-gaap:ConstructionInProgressMember2020-12-310001788717fxlv:ViveActiveBrookvalePtyLtdMember2021-10-290001788717fxlv:ViveActiveBrookvalePtyLtdMember2021-10-292021-10-290001788717fxlv:BrandNameMember2021-10-290001788717us-gaap:ComputerSoftwareIntangibleAssetMember2021-10-292021-10-290001788717us-gaap:ComputerSoftwareIntangibleAssetMember2021-10-290001788717us-gaap:CustomerContractsMember2021-10-292021-10-290001788717us-gaap:CustomerContractsMember2021-10-2900017887172021-10-290001788717fxlv:ViveActiveBrookvalePtyLtdMember2021-01-012021-12-310001788717us-gaap:LicensingAgreementsMember2021-04-302021-04-300001788717fxlv:FWSPVIILLCMemberus-gaap:LicensingAgreementsMember2021-04-300001788717us-gaap:LicensingAgreementsMember2021-04-300001788717fxlv:FlywheelSportsIncMember2021-07-192021-07-190001788717fxlv:FlywheelSportsIncMemberus-gaap:LicensingAgreementsMember2021-04-300001788717fxlv:FlywheelSportsIncMember2021-04-300001788717fxlv:FlywheelSportsIncMember2021-01-012021-12-310001788717us-gaap:ComputerSoftwareIntangibleAssetMember2021-01-012021-12-310001788717us-gaap:ComputerSoftwareIntangibleAssetMember2021-12-310001788717us-gaap:ComputerSoftwareIntangibleAssetMember2020-12-310001788717us-gaap:TrademarksMember2021-12-310001788717us-gaap:TrademarksMember2020-12-310001788717us-gaap:CustomerContractsMember2021-01-012021-12-310001788717us-gaap:CustomerContractsMember2021-12-310001788717us-gaap:CustomerContractsMember2020-12-310001788717srt:MinimumMemberfxlv:FlywheelCRMSoftwareMember2021-01-012021-12-310001788717srt:MaximumMemberfxlv:FlywheelCRMSoftwareMember2021-01-012021-12-310001788717fxlv:FlywheelCRMSoftwareMember2021-12-310001788717fxlv:FlywheelCRMSoftwareMember2020-12-310001788717us-gaap:ComputerSoftwareIntangibleAssetMember2020-01-012020-12-310001788717fxlv:AcquiredSoftwareMember2021-01-012021-12-310001788717fxlv:FiniteLivedIntangibleAssetsExcludingAssetsNotYetInServiceMember2021-12-3100017887172022-01-012021-12-310001788717fxlv:ConvertibleDebtAgreementMemberus-gaap:ConvertibleSubordinatedDebtMember2020-10-060001788717fxlv:ConvertibleDebtAgreementMemberus-gaap:ConvertibleSubordinatedDebtMember2020-12-310001788717fxlv:ConvertibleDebtAgreementMemberus-gaap:ConvertibleSubordinatedDebtMemberus-gaap:IPOMember2021-07-150001788717fxlv:ConvertibleDebtAgreementMemberus-gaap:ConvertibleSubordinatedDebtMemberus-gaap:IPOMember2021-07-152021-07-150001788717fxlv:ConvertibleDebtAgreementMemberus-gaap:ConvertibleSubordinatedDebtMemberus-gaap:IPOMember2021-12-310001788717fxlv:ConvertibleSubordinatedDebtSecondLienTermLoanMemberus-gaap:ConvertibleSubordinatedDebtMember2020-10-060001788717fxlv:ConvertibleSubordinatedDebtSecondLienTermLoanMemberus-gaap:ConvertibleSubordinatedDebtMember2020-12-310001788717fxlv:ConvertibleDebtAgreementMemberus-gaap:ConvertibleSubordinatedDebtMember2020-10-062020-10-060001788717fxlv:ConvertibleSubordinatedDebtSecondLienTermLoanMemberfxlv:ThirdPartyOtherThanTheLenderMemberus-gaap:ConvertibleSubordinatedDebtMember2021-01-012021-12-310001788717fxlv:ConvertibleSubordinatedDebtSecondLienTermLoanMemberus-gaap:ConvertibleSubordinatedDebtMembersrt:MaximumMember2021-10-060001788717fxlv:ConvertibleSubordinatedDebtSecondLienTermLoanMemberus-gaap:ConvertibleSubordinatedDebtMember2021-07-192021-07-190001788717fxlv:ConvertibleSubordinatedDebtSecondLienTermLoanMemberus-gaap:ConvertibleSubordinatedDebtMember2021-12-310001788717us-gaap:RevolvingCreditFacilityMemberfxlv:JpMorganChaseBankMemberfxlv:SecuredCreditAgreementFirstLienLoanMember2019-09-180001788717fxlv:TermLoanMemberfxlv:JpMorganChaseBankMemberfxlv:SecuredCreditAgreementFirstLienLoanMember2019-09-180001788717fxlv:TermLoanMemberfxlv:JpMorganChaseBankMemberfxlv:SecuredCreditAgreementFirstLienLoanMember2019-09-182019-09-180001788717fxlv:TermLoanMemberfxlv:JpMorganChaseBankMemberfxlv:SecuredCreditAgreementFirstLienLoanMemberus-gaap:LondonInterbankOfferedRateLIBORMember2019-09-182019-09-180001788717fxlv:SecondAmendmentToTheSecuredCreditAgreementMemberfxlv:TermLoanMemberfxlv:JpMorganChaseBankMemberfxlv:SecuredCreditAgreementFirstLienLoanMember2020-06-232020-06-230001788717fxlv:SecondAmendmentToTheSecuredCreditAgreementMemberfxlv:TermLoanMemberfxlv:JpMorganChaseBankMemberfxlv:SecuredCreditAgreementFirstLienLoanMember2020-06-230001788717fxlv:SecondAmendmentToTheSecuredCreditAgreementMemberfxlv:TermLoanMemberfxlv:JpMorganChaseBankMembersrt:MaximumMember2020-06-232020-06-230001788717fxlv:SecondAmendmentToTheSecuredCreditAgreementMemberfxlv:TermLoanMembersrt:MinimumMemberfxlv:JpMorganChaseBankMember2020-06-232020-06-230001788717fxlv:ConvertibleSubordinatedDebtSecondLienTermLoanMemberfxlv:TermLoanMember2021-07-192021-07-190001788717fxlv:ConvertibleSubordinatedDebtSecondLienTermLoanMemberus-gaap:RevolvingCreditFacilityMember2021-07-192021-07-190001788717fxlv:TermLoanMemberfxlv:SecuredCreditAgreementFirstLienLoanMember2021-12-310001788717fxlv:SecondAmendmentToTheSecuredCreditAgreementMemberfxlv:TermLoanMemberfxlv:JpMorganChaseBankMemberfxlv:SecuredCreditAgreementFirstLienLoanMember2020-12-310001788717fxlv:TermLoanMemberfxlv:FiveYearSeniorSecuredRevolvingFacilityMemberfxlv:SecuredCreditAgreementFirstLienLoanMember2021-08-130001788717fxlv:TermLoanMembersrt:MinimumMemberfxlv:JpMorganChaseBankMemberfxlv:SecuredCreditAgreementFirstLienLoanMemberus-gaap:InterestRateSwapMember2021-08-130001788717fxlv:TermLoanMemberfxlv:JpMorganChaseBankMembersrt:MaximumMemberfxlv:SecuredCreditAgreementFirstLienLoanMemberus-gaap:InterestRateSwapMember2021-08-130001788717fxlv:TermLoanAndRevolvingCreditFacilityMemberfxlv:JpMorganChaseBankMemberfxlv:SecuredCreditAgreementFirstLienLoanMembersrt:MaximumMember2021-08-13utr:Q0001788717fxlv:ConvertibleDebtAgreementMemberus-gaap:ConvertibleSubordinatedDebtMember2021-08-130001788717fxlv:TermLoanMemberfxlv:SecuredCreditAgreementFirstLienLoanMember2021-08-130001788717fxlv:SecondAmendmentToTheSecuredCreditAgreementMemberfxlv:TermLoanMemberfxlv:JpMorganChaseBankMemberfxlv:SecuredCreditAgreementFirstLienLoanMember2021-12-310001788717us-gaap:RevolvingCreditFacilityMemberfxlv:SecuredCreditAgreementFirstLienLoanMember2021-12-310001788717us-gaap:RevolvingCreditFacilityMemberfxlv:JpMorganChaseBankMemberfxlv:SecuredCreditAgreementFirstLienLoanMember2020-01-012020-12-310001788717us-gaap:RevolvingCreditFacilityMemberfxlv:JpMorganChaseBankMemberfxlv:SecuredCreditAgreementFirstLienLoanMember2021-12-310001788717fxlv:PaycheckProtectionProgramMember2020-04-102020-04-100001788717fxlv:PaycheckProtectionProgramMember2021-12-310001788717fxlv:PaycheckProtectionProgramMember2021-01-012021-12-310001788717us-gaap:ConvertibleSubordinatedDebtMember2021-01-012021-12-310001788717fxlv:SecondLienTermLoanMember2021-01-012021-12-310001788717fxlv:FirstLienTermLoanMember2021-01-012021-12-310001788717fxlv:TermFacilityMember2019-10-250001788717fxlv:TermFacilityMemberus-gaap:LondonInterbankOfferedRateLIBORMember2019-10-250001788717fxlv:TermFacilityMember2019-10-3000017887172021-07-212021-07-210001788717fxlv:ConvertibleNotesMember2020-10-310001788717fxlv:TermFacilityMember2021-12-310001788717us-gaap:MeasurementInputRiskFreeInterestRateMemberfxlv:LiquidityEventMembersrt:MinimumMember2020-12-310001788717us-gaap:MeasurementInputRiskFreeInterestRateMemberfxlv:LiquidityEventMembersrt:MaximumMember2020-12-310001788717fxlv:LiquidityEventMemberus-gaap:MeasurementInputPriceVolatilityMember2020-12-310001788717fxlv:LiquidityEventMemberus-gaap:MeasurementInputExpectedTermMember2020-12-31utr:Y0001788717fxlv:LiquidityEventMemberus-gaap:MeasurementInputExpectedDividendRateMember2020-12-310001788717us-gaap:MeasurementInputRiskFreeInterestRateMembersrt:MinimumMemberfxlv:QPOEventMember2020-12-310001788717us-gaap:MeasurementInputRiskFreeInterestRateMemberfxlv:QPOEventMembersrt:MaximumMember2020-12-310001788717fxlv:QPOEventMemberus-gaap:MeasurementInputPriceVolatilityMember2020-12-310001788717us-gaap:MeasurementInputExpectedTermMemberfxlv:QPOEventMember2020-12-310001788717us-gaap:MeasurementInputExpectedDividendRateMemberfxlv:QPOEventMember2020-12-310001788717us-gaap:InterestRateSwapMember2021-07-140001788717us-gaap:InterestRateSwapMember2021-07-142021-07-140001788717us-gaap:FairValueInputsLevel1Memberus-gaap:InterestRateSwapMemberus-gaap:FairValueMeasurementsRecurringMember2020-12-310001788717us-gaap:InterestRateSwapMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2020-12-310001788717us-gaap:InterestRateSwapMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2020-12-310001788717us-gaap:FairValueInputsLevel1Memberus-gaap:DerivativeMemberus-gaap:FairValueMeasurementsRecurringMember2020-12-310001788717us-gaap:DerivativeMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2020-12-310001788717us-gaap:DerivativeMemberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2020-12-310001788717us-gaap:DerivativeMemberus-gaap:FairValueMeasurementsRecurringMember2020-12-310001788717us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2020-12-310001788717us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2020-12-310001788717us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2020-12-310001788717us-gaap:FairValueMeasurementsRecurringMember2020-12-310001788717us-gaap:DomesticCountryMember2021-12-310001788717us-gaap:StateAndLocalJurisdictionMember2021-12-3100017887172020-10-06fxlv:director0001788717srt:MinimumMemberfxlv:FeesUnderManagementServiceAgreementMemberus-gaap:FranchiseMember2021-01-012021-12-310001788717fxlv:StudiosOwnedByGroupTrainingMemberus-gaap:FranchiseMember2020-01-012020-12-310001788717fxlv:DueFromRelatedPartiesCurrentMemberfxlv:FeesUnderManagementServiceAgreementMember2021-12-310001788717fxlv:DueFromRelatedPartiesCurrentMemberfxlv:FeesUnderManagementServiceAgreementMember2020-12-310001788717fxlv:ThirdPartyVendorMemberus-gaap:FranchiseMember2021-01-012021-12-310001788717fxlv:ThirdPartyVendorMemberus-gaap:FranchiseMember2020-01-012020-12-310001788717fxlv:StudiosOwnedByAnEntityMemberus-gaap:FranchiseMember2021-01-012021-12-310001788717fxlv:StudiosOwnedByAnEntityMemberus-gaap:FranchiseMember2020-01-012020-12-310001788717fxlv:FranchiseEquipmentAndMerchandiseMemberfxlv:EmployeeMember2021-01-012021-12-310001788717fxlv:FranchiseEquipmentAndMerchandiseMemberfxlv:EmployeeMember2020-01-012020-12-310001788717fxlv:StockholderThatIsAnExecutiveOfficerAndDirectorMemberfxlv:StudiosOwnedByAnEntityMember2021-12-310001788717fxlv:FranchiseEquipmentAndMerchandiseMemberfxlv:EmployeeMember2021-12-310001788717fxlv:FranchiseEquipmentAndMerchandiseMemberfxlv:EmployeeMember2020-12-310001788717fxlv:ShippingAndLogisticServicesMemberfxlv:ThirdPartyVendorMember2021-01-012021-12-310001788717fxlv:ShippingAndLogisticServicesMemberfxlv:ThirdPartyVendorMember2020-01-012020-12-310001788717fxlv:ThirdPartyVendorMember2021-12-310001788717fxlv:ThirdPartyVendorMember2020-12-310001788717fxlv:EmployeeMember2021-01-012021-12-31fxlv:studio0001788717fxlv:EmployeeMember2020-01-012020-12-310001788717fxlv:RevenueRecognizedFromFranchiseEquipmentAndMerchandiseMemberfxlv:EmployeeMember2021-12-310001788717fxlv:RevenueRecognizedFromFranchiseEquipmentAndMerchandiseMemberfxlv:EmployeeMember2020-12-310001788717us-gaap:InvestorMember2021-12-310001788717us-gaap:InvestorMember2020-12-310001788717fxlv:LiitLlcMember2020-06-230001788717fxlv:AssetTransferAndLicensingAgreementMemberfxlv:LiitLlcMember2020-06-232020-06-230001788717fxlv:AssetTransferAndLicensingAgreementMemberfxlv:LiitLlcMember2020-06-230001788717fxlv:AssetTransferAndLicensingAgreementMemberfxlv:LiitLlcMember2021-01-012021-12-310001788717fxlv:AssetTransferAndLicensingAgreementMemberfxlv:LiitLlcMember2020-01-012020-12-310001788717fxlv:AssetTransferAndLicensingAgreementMemberfxlv:LiitLlcMember2021-12-310001788717fxlv:AssetTransferAndLicensingAgreementMemberfxlv:LiitLlcMember2020-12-310001788717fxlv:AssetTransferAndLicensingAgreementMemberfxlv:LiitLlcMember2021-06-150001788717fxlv:AssetTransferAndLicensingAgreementMemberfxlv:LiitLlcMember2021-06-152021-06-150001788717fxlv:ClubFranchiseGroupLlcMember2021-12-310001788717fxlv:ClubFranchiseGroupLlcMemberfxlv:LongTermMultiUnitStudioAgreementMember2021-06-150001788717fxlv:ClubFranchiseGroupLlcMemberfxlv:LongTermMultiUnitStudioAgreementMember2021-06-152021-06-150001788717fxlv:LongTermMultiUnitStudioAgreementMemberfxlv:ClubFranchiseGroupLlcMemberfxlv:JuneTwoThousandAndTwentyTwoMember2021-06-150001788717fxlv:DecemberTwoThousandAndTwentyTwoMemberfxlv:LongTermMultiUnitStudioAgreementMemberfxlv:ClubFranchiseGroupLlcMember2021-06-150001788717fxlv:LongTermMultiUnitStudioAgreementMemberfxlv:ClubFranchiseGroupLlcMemberfxlv:DecemberTwoThousandAndTwentyThreeMember2021-06-150001788717fxlv:LongTermMultiUnitStudioAgreementMemberfxlv:ClubFranchiseGroupLlcMemberus-gaap:FranchiseMember2021-01-012021-12-310001788717fxlv:LongTermMultiUnitStudioAgreementMemberfxlv:ClubFranchiseGroupLlcMemberfxlv:FranchiseEquipmentAndMerchandiseMember2021-01-012021-12-310001788717fxlv:ClubFranchiseGroupLlcMemberfxlv:LongTermMultiUnitStudioAgreementMember2021-12-31fxlv:building00017887172020-12-012020-12-31utr:sqftfxlv:renewal_option0001788717us-gaap:PropertyLeaseGuaranteeMember2021-12-31fxlv:lease0001788717us-gaap:PropertyLeaseGuaranteeMembersrt:MinimumMember2021-12-310001788717us-gaap:PropertyLeaseGuaranteeMembersrt:MaximumMember2021-12-310001788717fxlv:TwoThousandAndTwentyPromotionalAgreementsMemberfxlv:GregnormanMember2020-10-150001788717fxlv:TwoThousandAndTwentyPromotionalAgreementsMemberfxlv:DBVenturesLimitedMemberfxlv:CompanyDeterminedAsPubliclyTradedMember2020-11-240001788717fxlv:TwoThousandAndTwentyPromotionalAgreementsMemberfxlv:DBVenturesLimitedMemberfxlv:CompanyDeterminedAsPubliclyTradedMember2021-01-012021-12-310001788717fxlv:DBVenturesLimitedMember2021-12-310001788717fxlv:DBVenturesLimitedMember2021-12-012021-12-310001788717fxlv:TwoThousandAndTwentyPromotionalAgreementsMemberfxlv:MagicJohnsonEntertainmentMemberfxlv:CompanyDeterminedAsPubliclyTradedMember2021-04-122021-04-120001788717fxlv:TwoThousandAndTwentyPromotionalAgreementsMemberfxlv:MagicJohnsonEntertainmentMemberfxlv:CompanyDeterminedAsPubliclyTradedMember2021-12-310001788717fxlv:TwoThousandAndTwentyPromotionalAgreementsMemberfxlv:MagicJohnsonEntertainmentMemberfxlv:CompanyDeterminedAsPubliclyTradedMember2021-04-120001788717fxlv:TwoThousandAndTwentyPromotionalAgreementsMemberfxlv:MagicJohnsonEntertainmentMemberfxlv:CompanyDeterminedAsPubliclyTradedMember2021-06-252021-06-2500017887172021-06-250001788717fxlv:BigSkyIncMemberfxlv:TwoThousandAndTwentyPromotionalAgreementsMemberfxlv:MalibuCrewMember2021-09-240001788717fxlv:TwoThousandAndTwentyPromotionalAgreementsMemberfxlv:LiabilityClassifiedAwardsMember2021-07-152021-07-150001788717us-gaap:AccountsPayableAndAccruedLiabilitiesMember2021-12-310001788717us-gaap:OtherNoncurrentLiabilitiesMember2021-12-310001788717fxlv:TwoThousandAndTwentyOnePromotionalAgreementsMembersrt:MinimumMemberfxlv:LiabilityClassifiedAwardsMember2021-01-012021-12-310001788717fxlv:TwoThousandAndTwentyOnePromotionalAgreementsMemberfxlv:LiabilityClassifiedAwardsMembersrt:MaximumMember2021-01-012021-12-310001788717fxlv:TwoThousandAndTwentyOnePromotionalAgreementsMemberfxlv:LiabilityClassifiedAwardsMember2021-01-012021-12-310001788717us-gaap:RestrictedStockUnitsRSUMember2021-12-302021-12-30fxlv:anniversary00017887172021-07-140001788717fxlv:F45AusHoldCoMemberus-gaap:CommonStockMemberus-gaap:SeriesOfIndividuallyImmaterialBusinessAcquisitionsMember2021-07-140001788717fxlv:F45AusHoldCoMemberfxlv:FlyhalfAcquisitionCompanyPtyLtdMember2021-07-142021-07-140001788717fxlv:F45AusHoldCoMemberfxlv:MWIGLLCMember2021-07-142021-07-140001788717us-gaap:RedeemableConvertiblePreferredStockMemberfxlv:MWIGLLCMember2021-07-140001788717fxlv:MWIGLLCMember2021-07-140001788717us-gaap:SecuredDebtMemberfxlv:FlyhalfAcquisitionCompanyPtyLtdMemberfxlv:SellersPromissoryNotesMember2021-07-140001788717us-gaap:RedeemableConvertiblePreferredStockMemberfxlv:MWIGLLCMember2021-07-142021-07-1400017887172021-07-142021-07-140001788717us-gaap:RedeemableConvertiblePreferredStockMember2020-12-302020-12-300001788717us-gaap:CommonStockMember2020-12-302020-12-300001788717us-gaap:RedeemableConvertiblePreferredStockMemberfxlv:ConversionOfRedeemableConvertiblePreferredStockToCommonStockMember2021-07-012021-07-310001788717us-gaap:RedeemableConvertiblePreferredStockMemberfxlv:ConversionOfRedeemableConvertiblePreferredStockToCommonStockMember2021-07-310001788717us-gaap:RedeemableConvertiblePreferredStockMember2021-12-310001788717fxlv:MrWahlbergMemberus-gaap:RestrictedStockUnitsRSUMember2019-03-152019-03-150001788717us-gaap:ShareBasedCompensationAwardTrancheOneMember2021-12-310001788717us-gaap:ShareBasedCompensationAwardTrancheOneMemberus-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001788717us-gaap:ShareBasedCompensationAwardTrancheTwoMember2021-12-310001788717us-gaap:ShareBasedCompensationAwardTrancheTwoMemberus-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001788717us-gaap:ShareBasedCompensationAwardTrancheThreeMember2021-12-310001788717us-gaap:RestrictedStockUnitsRSUMemberus-gaap:ShareBasedCompensationAwardTrancheThreeMember2021-01-012021-12-310001788717fxlv:MrWahlbergMemberus-gaap:RestrictedStockUnitsRSUMember2021-07-052021-07-050001788717us-gaap:IPOMember2021-07-050001788717fxlv:MrWahlbergMemberus-gaap:RestrictedStockUnitsRSUMember2021-07-152021-07-150001788717fxlv:MrWahlbergMemberus-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-31fxlv:plan0001788717fxlv:TwoThousandAndTwentyOneIncentivePlanMembersrt:ScenarioForecastMember2022-01-010001788717us-gaap:EmployeeStockOptionMembersrt:MinimumMember2021-01-012021-12-310001788717us-gaap:EmployeeStockOptionMembersrt:MaximumMember2021-01-012021-12-310001788717fxlv:TwoThousandAndTwentyOneIncentivePlanMemberfxlv:IncentiveStockOptionsMember2021-12-310001788717fxlv:IncentiveStockOptionsMember2021-01-012021-12-310001788717srt:MinimumMemberfxlv:IncentiveStockOptionsMember2021-01-012021-12-310001788717srt:MaximumMemberfxlv:IncentiveStockOptionsMember2021-01-012021-12-310001788717fxlv:IncentiveStockOptionsMember2020-12-310001788717fxlv:IncentiveStockOptionsMember2020-01-012020-12-310001788717fxlv:IncentiveStockOptionsMember2021-12-310001788717fxlv:TwoThousandAndTwentyOneIncentivePlanMemberfxlv:IncentiveStockOptionsMember2021-01-012021-12-310001788717fxlv:TwoThousandAndTwentyOneIncentivePlanMember2021-01-012021-12-310001788717fxlv:TwoThousandAndTwentyOneIncentivePlanMemberus-gaap:RestrictedStockUnitsRSUMember2021-12-310001788717us-gaap:RestrictedStockUnitsRSUMember2020-12-310001788717us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001788717us-gaap:RestrictedStockUnitsRSUMember2021-12-310001788717fxlv:TwoThousandAndTwentyOneIncentivePlanMemberus-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001788717fxlv:TwoThousandAndTwentyOneIncentivePlanMemberus-gaap:RestrictedStockMember2021-12-310001788717us-gaap:RestrictedStockMember2020-12-310001788717us-gaap:RestrictedStockMember2021-01-012021-12-310001788717us-gaap:RestrictedStockMember2021-12-310001788717fxlv:TwoThousandAndTwentyOneIncentivePlanMemberus-gaap:RestrictedStockMember2021-01-012021-12-310001788717fxlv:UnvestedRestrictedStockUnitsMember2021-01-012021-12-310001788717fxlv:UnvestedRestrictedStockUnitsMember2020-01-012020-12-310001788717us-gaap:RestrictedStockMember2021-01-012021-12-310001788717us-gaap:RestrictedStockMember2020-01-012020-12-310001788717us-gaap:EmployeeStockOptionMember2021-01-012021-12-310001788717us-gaap:EmployeeStockOptionMember2020-01-012020-12-310001788717us-gaap:ConvertiblePreferredStockMember2021-01-012021-12-310001788717us-gaap:ConvertiblePreferredStockMember2020-01-012020-12-310001788717us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001788717us-gaap:RestrictedStockUnitsRSUMember2020-01-012020-12-310001788717fxlv:ConvertibleNotesMember2021-01-012021-12-310001788717fxlv:ConvertibleNotesMember2020-01-012020-12-31fxlv:segmentfxlv:officer0001788717fxlv:UnitedStatesSegmentMemberus-gaap:FranchiseMember2021-01-012021-12-310001788717fxlv:UnitedStatesSegmentMemberus-gaap:FranchiseMember2020-01-012020-12-310001788717fxlv:UnitedStatesSegmentMemberus-gaap:ProductMember2021-01-012021-12-310001788717fxlv:UnitedStatesSegmentMemberus-gaap:ProductMember2020-01-012020-12-310001788717fxlv:UnitedStatesSegmentMember2021-01-012021-12-310001788717fxlv:UnitedStatesSegmentMember2020-01-012020-12-310001788717us-gaap:FranchiseMemberfxlv:AustraliaSegmentMember2021-01-012021-12-310001788717us-gaap:FranchiseMemberfxlv:AustraliaSegmentMember2020-01-012020-12-310001788717us-gaap:ProductMemberfxlv:AustraliaSegmentMember2021-01-012021-12-310001788717us-gaap:ProductMemberfxlv:AustraliaSegmentMember2020-01-012020-12-310001788717fxlv:AustraliaSegmentMember2021-01-012021-12-310001788717fxlv:AustraliaSegmentMember2020-01-012020-12-310001788717fxlv:RestOfWorldSegmentMemberus-gaap:FranchiseMember2021-01-012021-12-310001788717fxlv:RestOfWorldSegmentMemberus-gaap:FranchiseMember2020-01-012020-12-310001788717fxlv:RestOfWorldSegmentMemberus-gaap:ProductMember2021-01-012021-12-310001788717fxlv:RestOfWorldSegmentMemberus-gaap:ProductMember2020-01-012020-12-310001788717fxlv:RestOfWorldSegmentMember2021-01-012021-12-310001788717fxlv:RestOfWorldSegmentMember2020-01-012020-12-310001788717us-gaap:CustomerConcentrationRiskMemberus-gaap:SalesRevenueNetMemberfxlv:CustomerAMember2021-01-012021-12-310001788717us-gaap:ConstructionInProgressMember2021-01-012021-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the year ended December 31, 2021

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For transition period from to

Commission File Number 001-36773

F45 Training Holdings Inc.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

Delaware (State or other jurisdiction of incorporation or organization) | | 84-2529722 (I.R.S. Employer Identification Number) |

3601 South Congress Avenue, Building E Austin, Texas 78704 (Address of principal executive offices and zip code) (737) 787-1955 (Registrant's telephone number, including area code) |

| | | | | | | | |

Securities registered pursuant to Section 12(b) of the Act: |

Title of each class Common stock, par value $0.00005 | Trading Symbol FXLV | Name of each exchange on which registered New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ◻ No ⌧

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ◻ No ⌧

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes No

Indicate by check mark whether the Registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). Yes No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | |

Large accelerated filer |

| | Accelerated filer |

|

Non-accelerated filer | ý | | Smaller reporting company | ý |

| | | Emerging growth company | ý |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act): Yes No

The aggregate market value of the common stock held by non-affiliates of the registrant as of March 21, 2022 was approximately $270 million (based on the closing sales price of the registrant’s common stock on that date). The registrant’s common stock was not publicly traded on June 30, 2021, the last day of the registrant’s second fiscal quarter in 2021.

As of March 22, 2022, there were approximately 94,760,402 shares of the registrant's common stock outstanding.

Portions of the registrant’s Proxy Statement for the 2022 Annual Meeting of Stockholders are incorporated herein by reference in Part III of this Annual Report on Form 10-K to the extent stated herein. Such proxy statement will be filed with the Securities and Exchange Commission within 120 days of the registrant’s fiscal year ended December 31, 2021.

F45 Training Holdings Inc.

Form 10-K

Table of Contents

| | | | | | | | |

| Part I. | | Page |

| | |

| Item 1. | Business | |

| Item 1A. | Risk Factors | |

| Item 1B. | Unresolved Staff Comments | |

| Item 2. | Properties | |

| Item 3. | Legal Proceedings | |

| Item 4. | Mine Safety Disclosures | |

| | |

| Part II. | | |

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |

| Item 6. | Selected Consolidated Financial Data | |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | |

| Item 8. | Financial Statements and Supplementary Data | |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |

| Item 9A. | Controls and Procedures | |

| Item 9B. | Other Information | |

| | |

| Part III. | | |

| Item 10. | Directors, Executive Officers, and Corporate Governance | |

| Item 11. | Executive Compensation | |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters | |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | |

| Item 14. | Principal Accountant Fees and Services | |

| | |

| Part IV. | | |

| Item 15. | Exhibits, Financial Statement Schedules | |

| Item 16. | Form 10-K Summary | |

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act. Forward-looking statements generally relate to future events or our future financial or operating performance. In some cases, you can identify forward-looking statements because they contain words such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “could,” “intends,” “target,” “projects,” “contemplates,” “believes,” “estimates,” “predicts,” “potential,” or “continue” or the negative of these words, variations of these words or other similar terms or expressions that concern our expectations, strategy, plans, or intentions. Such forward-looking statements are subject to certain risks, uncertainties and assumptions relating to factors that could cause actual results to differ materially from those anticipated in such statements, including, without limitation, the following:

•our dependence on the operational and financial results of, and our relationships with, our franchisees and the success of their new and existing studios;

•our ability to protect our brand and reputation;

•our ability to identify, recruit and contract with a sufficient number of qualified franchisees;

•our ability to execute our growth strategy, including through development of new studios by new and existing franchisees;

•our ability to manage our growth and the associated strain on our resources;

•our ability to identify, source and procure components of our inventories on a timely basis and at attractive economics terms;

•our ability to successfully integrate any acquisitions, or realize their anticipated benefits;

•the high level of competition in the health and fitness industry;

•economic, political and other risks associated with our international operations, including due to the Russia-Ukraine conflict;

•changes to the industry in which we operate;

•our reliance on information systems and our and our franchisees’ ability to properly maintain the confidentiality and integrity of our data;

•the occurrence of cyber incidents or a deficiency in our cybersecurity protocols;

•our and our franchisees’ ability to attract and retain members;

•our and our franchisees’ ability to identify and secure suitable sites for new franchise studios;

•risks related to franchisees generally;

•our ability to obtain third-party licenses for the use of music to supplement our workouts;

•certain health and safety risks to members that arise while at our studios;

•our ability to adequately protect our intellectual property;

•risks associated with the use of social media platforms in our marketing;

•our ability to obtain and retain high-profile strategic partnership arrangements;

•our ability to comply with existing or future franchise laws and regulations;

•our ability to anticipate and satisfy consumer preferences and shifting views of health and fitness;

•our business model being susceptible to litigation; and

•additional factors discussed in our SEC filings, including those identified under the header “Risk Factors” beginning on Page 17 of this Annual Report on Form 10-K.

You should not rely upon forward-looking statements as predictions of future events. We have based the forward-looking statements contained in this Annual Report on Form 10-K on historical performance, management’s current expectations and projections about future events and trends that management believes may affect our business, results of operations, financial condition and prospects in light of information currently available to us.

The outcome of the events described in these forward-looking statements is subject to risks, uncertainties and other factors described in the section titled “Risk Factors” and elsewhere in this Annual Report on Form 10-K. Moreover, we operate in a very competitive and rapidly changing environment. New risks and uncertainties emerge from time to time, and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward- looking statements contained in this Annual Report on Form 10-K. We cannot assure you that the results, events, and circumstances reflected in the forward-looking

statements will be achieved or occur, and actual results, events or circumstances could differ materially from those described in the forward-looking statements.

The forward-looking statements made in this Annual Report on Form 10-K relate only to events as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements made in this Annual Report on Form 10-K to reflect events or circumstances after the date of this report or to reflect new information or the occurrence of unanticipated events, except as required by law. We may not actually achieve the plans, intentions, or expectations disclosed in our forward-looking statements, and you should not place undue reliance on our forward-looking statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures, or investments we may make.

In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based upon information available to us as of the date of this Annual Report on Form 10-K, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain, and investors are cautioned not to unduly rely upon these statements.

Part I.

Item 1. Business

In this Annual Report on Form 10-K, unless otherwise indicated or the context otherwise requires, all references to “we,” “our,” “us,” “F45,” “the Company,” and “our Company” refer to F45 Training Holdings Inc. and its subsidiaries.

In assessing the performance of our business, we use certain key measures for determining how our business is performing. The below metrics are used throughout this Form 10-K and, unless otherwise indicated, all references to such metrics shall have the meanings ascribed to such metrics below:

In assessing the performance of our business, we use certain key measures for determining how our business is performing. The below metrics are used throughout this Form 10-K and, unless otherwise indicated, all references to such metrics shall have the meanings ascribed to such metrics below:

•“Average Unit Volume” or “AUV” means average studio-level revenue generated by a group of studios during a particular period of time. Due to the relatively young age of our studio base, we believe it is appropriate to assess AUV for studios that have been open for the full period for which AUV is calculated. We define a cohort as a group of studios that opened during the same full year and are also open and operational during the twelve months ended December 31, 2021.

◦“Cash-on-cash returns” means studio-level EBITDA over initial investment.

◦“Initial Studio Openings” means the number of studios that were determined to be first opened during such period. We classify an Initial Studio Opening to occur in the first month in which the studio first generates monthly revenue of at least $4,500. Initial Studio Openings are not adjusted downward for studios that were temporarily closed due to the COVID-19 pandemic or otherwise.

◦“Members” refers to the number of paying members who were billed $20 or more in membership fees in a given month.

◦“New Franchises Sold” means, for any specific period, the number of franchises sold during such period using the methodology set forth below for “Total Franchises Sold.”

◦“Open Studios” means the number of studios that were open for business as of a certain date. A studio may be classified as an Open Studio regardless of whether or not it generated minimum monthly revenue of $4,500. During the COVID-19 pandemic, a significant portion of our network was forced to temporarily close, which reduced the number of Open Studios. As studios re-open in accordance with state and local regulations, they are reflected in the Open Studios figures.

◦“Same store sales” means, for any reporting period, studio-level revenue generated by a comparable base of franchise studios, which we define as open studios that have been operating for more than 16 months.

◦System-wide Sales” are defined as all payments made to our studios and includes payment for classes, apparel and other sales for a given period. We track System-wide Sales as an indication of the strength of our franchisee network.

◦“Total Franchises Sold” represents, as of any specified date, (i) the total number of signed franchise agreements in place as of such date for which an establishment fee has been paid and (ii) the total number of franchises committed in a multi-studio agreement in place as of such date for which an upfront payment has been made, in each case that have not been terminated. Each new franchise is included in the number of Total Franchises Sold from the date on which such franchise first satisfies the condition in clause (i) or (ii) above, as applicable. Total Franchises Sold includes franchise arrangements in all stages of development after signing a franchise agreement, and includes franchises with open studios. Franchises are removed from Total Franchises Sold upon termination of the franchise agreement.

◦“Total Studios” as of any specified date, means the total cumulative Initial Studio Openings as of that date less cumulative permanent studio closures as of that date. Total Studios are not adjusted downward for studios that were temporarily closed due to the COVID-19 pandemic or otherwise.

◦“Visits” means the number of registered individual workouts for any specified period. A workout is registered when the consumer checks into a class.

Additionally, This annual report contains estimates, projections and other information concerning our industry, our business, our franchises and the markets for our products and services. Some data and statistical information are based on independent reports from third parties, including the International Health, Racquet & Sports Club Association, or IHRSA, and a member survey with 4,184 respondents that we conducted in October 2017.

Some data and other information related to our franchisees, including estimated initial investment, EBITDA margins and average unit volumes, are based on internal estimates and calculations that are derived from research we conducted. In order to determine certain franchise and studio-level information, we conducted a survey of our franchisees, or the Franchise Survey, in July 2019, which only reflects data from prior to the outbreak of COVID-19. This survey was provided to the franchisees of all studios at the time that the survey was conducted and generated responses from franchisees representing approximately 57% of studios across our global network of studios. In generating the data, estimates and calculations derived from the information provided by these respondents, we excluded certain responses that were incomplete or that we determined to be significant outliers. As a result, while we believe that the data and other information related to our franchisees presented in this annual report are accurate and reliable, such data and other information are based on responses provided by a limited respondent pool, which may not represent the broader network of franchisees, and that have not been independently verified by us or any independent sources. Such data also does not reflect any impacts on our business or franchisees from COVID-19 or otherwise after July 2019.

We are F45 Training, the fastest growing fitness franchisor in the world according to Entrepreneur in 2021, focused on creating a leading global fitness training and lifestyle brand. We primarily offer consumers functional 45-minute workouts that are effective, fun and community-driven. Our workouts combine elements of high-intensity interval, circuit and functional training to offer consumers what we believe is the world’s best functional training workout. We deliver our workouts primarily through our digitally-connected global network of studios, and we have built a differentiated, technology-enabled platform that allows us to create and distribute workouts to our global franchisee base. Our platform enables the rapid scalability of our model and helps to promote the success of our franchisees. We offer consumers a continuously evolving fitness program in which virtually no two workouts are ever the same. Our vast and growing library of functional training movements allows us to vary workout programs to keep consumers engaged with fresh content, stay at the forefront of consumer trends and drive maximum individual results, while helping our members achieve their fitness goals.

We were founded in 2013 in Sydney, Australia. Our CEO and co-founder Adam Gilchrist recognized an opportunity to leverage technology to offer consumers an effective, multi-disciplinary and

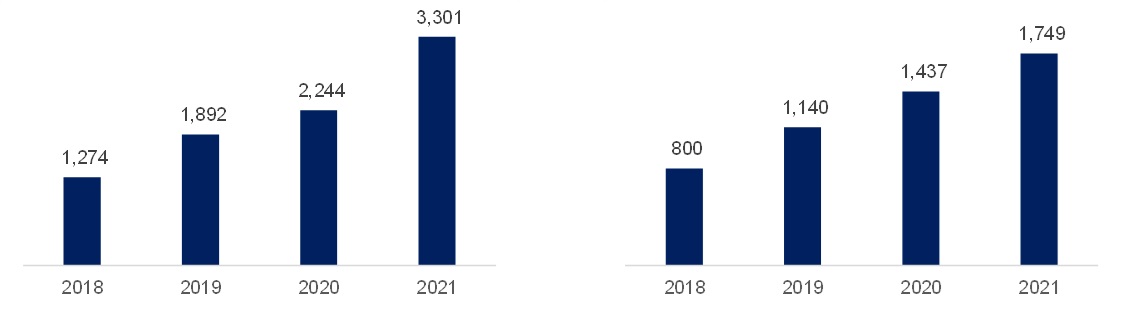

community-driven workout that serves as an affordable alternative to one-on-one personal training and repetitive, single-discipline studio classes. Soon after the first F45 Training studio opened in Paddington, Australia, our founders focused on using technology to streamline and standardize the F45 Training experience in order to franchise the business. We quickly expanded, initially selling franchises to members of the original studio, after which viral word-of-mouth marketing led to rapid growth, and we opened nearly 200 studios over the following 30 months. In less than nine years, we have scaled our global footprint to 3,301 Total Franchises Sold in 67 countries, including 1,749 Total Studios.

Our in-studio experience utilizes our proprietary technologies: our fitness programming algorithm and our patented technology-enabled delivery platform. Our fitness programming algorithm leverages a rich, growing content database of over 8,000 unique functional training movements across modalities to offer new workouts each day. Our content delivery platform allows us to standardize the F45 Training experience across our global footprint and broadcast content, including workout instructions and timing, directly to our in-studio technologically-enabled content delivery platform, or F45TV, and speaker systems. Our in-studio experience is further enhanced by trainers who provide guidance on proper form and movement, as well as motivate our members and foster a positive sense of community. We believe our approach helps to provide a consistent and high-quality fitness experience across our network of studios, keeping members highly engaged and helping them to achieve and sustain their fitness goals.

We operate a nearly 100% franchise model that offers compelling economics to us and our franchisees. We believe our franchisees generally benefit from a relatively low initial investment and low four-wall operating expenses, which allows them to generate strong profitability and returns on investment. The optimized box layout of our studios, which requires as little as approximately 1,600 square feet of training area, contributes to the relatively low initial investment and operating costs of our franchise model, and allows our studios to be located in a wide array of attractive prospective retail locations. We believe this flexibility will help enable us to capitalize on our estimated long-term global opportunity of over 23,000 studios. Based on the Franchise Survey conducted prior to the COVID-19 pandemic, we estimate that a typical F45 Training franchise in a normalized operating environment requires an aggregate initial investment of approximately $315,000 and, in its third year of operation can produce average EBITDA margins in excess of 30% and average cash-on-cash returns in excess of 33%.

We believe our franchise model is attractive due to its potential for asset-light growth, strong profitability and robust cash flow generation, and has helped to facilitate our rapid growth and strong financial performance prior to, and resilience during, the COVID-19 pandemic. Despite challenges posed by the pandemic, we grew our footprint and experienced minimal permanent closures, which we believe underscores the durability of our business model. Between 2019 and 2021 we grew our Total Franchises Sold at the compound annual rate of 32% and our Total Studios at the rate of 24%. Between 2020 and 2021, our Total Franchises Sold increased by 47% and our Total Studios increased by 22%.

Total Franchises Sold (as of period end) Total Studios (as of period end)1

1 Due to the lead time associated with opening a new studio after a franchise is sold, Total Franchises Sold is always greater than Total Studios as of a certain date. Of our 3,301 Total Studios as of December 31, 2021, we had 1,749 Total Studios, which are studios that were open for business

Impact of the COVID-19 Pandemic

The COVID-19 pandemic has had and may continue to have a significant impact on the gym and fitness industry generally, as well as our business, financial condition and results of our operations. Following the outbreak of the pandemic in early 2020 and at its initial peak, nearly all of our studios temporarily closed pursuant to local, state and federal mandates and guidelines. As businesses have been allowed to re-open, we have worked closely with our franchisees in helping to re-open their studios. As of December 31, 2021, we had approximately 1,580 Open Studios, which represented 90% of our Total Studios. The remaining 10% of our Total Studios are generally located in regions that continue to face restrictions, which we expect to be lifted in due course.

We believe our performance over the course of the pandemic has underscored the resilience of our business model. While our revenues decreased to $82.3 million for the year ended December 31, 2020 compared to $92.7 million for the year ended December 31, 2019 due to the pandemic, between February 1, 2020 and December 31, 2021, only 20 studios permanently closed due to financial hardship or otherwise, which represents approximately 1% of our Total Studios as of December 31, 2021. Additionally, less than approximately 1% of our Total Backlog Studios, which is the difference between the Total Franchises Sold and Total Studios, terminated franchise agreements during that same period. These metrics compare favorably to the estimated 25% of all U.S. fitness facilities that had permanently closed as of January 1, 2022, according to IHRSA.

Despite challenges posed by the COVID-19 pandemic, we successfully continued to sell new franchises and open new studios during the years ended December 31, 2020 and 2021.

For additional information on the impact of COVID-19 on our business, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—COVID-19 Impact.”

The Three Pillars of F45 Training

Our differentiated approach to fitness is firmly rooted in the three pillars of our DNA: Innovation, Motivation and Results.

Innovation: at the core of everything we do. We are dedicated to driving new innovations that will continue to elevate the F45 Training experience and further our position as a global fitness training and lifestyle brand. We are able to distinguish ourselves from competitors through such innovations as:

•Technology-Enabled Centralized Delivery Platform: Our technology-enabled centralized delivery platform distributes daily workout content via in-studio F45TVs that display proper exercise form, timing and sequencing, driving consistency and efficiency across our global network of studios. In-studio trainers coach members throughout their workout and adjust movements to suit individual levels of experience, strength and flexibility;

•Proprietary Fitness Programming Algorithm: Our fitness programming algorithm configures movements from our vast content library into new workout plans based on various criteria, including duration, target muscle group, equipment type and aerobic versus anaerobic focus, among others, ensuring that virtually no two workouts are ever the same; and

•Curated High-Quality Workout Plans: Our curated workout plans are subject to a rigorous in-house quality control process and are designed to sequence movements in what we believe to be a safe, effective manner. This quality control process is led by our centralized F45 Athletics Department, which consists of training professionals, athletes and sports scientists

Motivation: the key to creating a community and sanctuary. We believe the foundation for any effective fitness program is motivation. We motivate our members through a combination of positivity,

inclusivity and teamwork, which encourages our members to view each studio as a sanctuary and is driven by:

•Positive Trainers: Our in-studio trainers are responsible for fostering a positive environment for all members before, during and after workouts, and we specifically instruct them to drive positivity, inclusivity and teamwork;

•“No Mirrors, No Microphones, No Egos”: Our studios are deliberately free of mirrors and microphones, which mitigates the appearance-related pressures and trainer intimidation that are associated with many fitness alternatives. Our goal is to emphasize our members’ achievements in completing our workouts; and

•Community: Our positive, inclusive philosophy permeates the studio and creates a genuine sense of camaraderie, team-building and community amongst our members

Results: supported by the sustainability of our workouts over time. We strive to help our members achieve and maintain results by focusing on creating a sustainable fitness program. Our fitness programming algorithm offers new workouts each day and is specifically designed to encourage members to visit studios multiple times per week over the course of their long-term fitness journey. We believe we offer members a winning formula to achieve long-term results, driven by:

•Total Body Workout: Our fitness programming algorithm offers a total body workout that combines cardiovascular and strength modalities to deliver comprehensive results;

•Safety: We believe our emphasis on functional training movements and relatively low weight resistance helps to mitigate the risk of injury, thereby enabling our members to push themselves and maximize individual performance without compromising their safety; and

•Frequency: The curation, style and cadence of workouts, combined with the use of low weight resistance, allows for members to visit as frequently as their schedules permit. Workouts alternate between cardiovascular and strength modalities from day to day, which alternates the impact on the body.

Our Competitive Strengths

We believe there are several competitive strengths that form the foundation of our strategy and are key differentiating factors of our business.

The Next Generation Global Fitness Training and Lifestyle Brand Striving to Deliver the World’s Best Workout

Over the last nine years, we have focused on leveraging our differentiated approach to fitness to develop a global brand that is viewed as the gold standard in industry. We strive to offer our members the best functional training workout in each F45, FS8, Malibu Crew, Avalon House and Vive Active studio on a daily basis. Our differentiated, technology-driven approach, including our proprietary fitness programming algorithm’s database of over 8,000 unique functional training movements across modalities, helps us to design workouts that are fun, challenging, safe, dynamic and sustainable for members to attend day after day and week after week. The versatility of our workouts resonates with both women and men, and across a broad range of fitness levels.

Innovative and Differentiated Technology-Enabled Delivery Platform Driving Quality and Consistency within Each Studio

A critical component to the success of our business is our patented technology that provides us with the ability to remotely manage each in-studio experience across our global network of 1,749 Total Studios as of December 31, 2021 from our centralized technology systems at F45 Training headquarters. We have built an automated, centralized delivery platform that gives us the ability to control the delivery and timing of our workout content through our F45TVs in each of our studios. Our centralized delivery platform enables a seamless F45 Training experience on a consistent basis at scale across a broad geographic footprint. In response to temporary studio closures due to the COVID-19 pandemic, we were able to leverage our technology platform and create a home digital product called F45 AtHome Workouts. This offering provides users with the ability to access part of our library of fitness and wellness offerings from remote or outdoor locations, and allows users to maintain their engagement with F45 during temporary studio closures. In addition, as our studios have re-opened, our adaptable workout model has enabled us to modify workouts so they can be completed in socially distanced setting and with minimal equipment requirements.

Highly Scalable Commercial Delivery and Franchise Development Model

Our differentiated approach, including our fitness programming algorithm and our proprietary technology-enabled delivery platform, plays an integral role in the scalability of our business. By integrating technology into the workout experience, we have been able to develop a franchise model that is highly replicable for both new and existing franchisees across multiple geographies. In addition, our purpose-built studio design, which utilizes an open floor plan and modest physical footprint (as little as 1,600 square feet of training area), can be built within a wide array of attractive prospective retail locations. We have also substantially simplified the pre-opening process by providing franchisees with a comprehensive studio opening pack, which we call a World Pack, that includes the key items needed to operate the studio, including fitness equipment, technology, AV equipment and more. Our World Pack has resulted in a streamlined pre-opening process for our franchisees.

Compelling Franchisee Studio Economics

We believe we offer a compelling business opportunity for franchisees to generate strong returns driven by a relatively low initial investment combined with attractive AUVs and low four-wall operating expenses. Prior to the COVID-19 pandemic and based on data collected through our booking systems and the Franchise Survey, we estimate that in a normalized operating environment, a typical F45 Training franchise requires an aggregate initial investment of approximately $315,000 and, in its third year of operation can produce an AUV of approximately $354,000, average EBITDA margins in excess of 30% and average cash-on-cash returns in excess of 33%.

Across the F45 network, we believe that many studios that have re-opened following the onset of the COVID-19 pandemic have demonstrated the ability to quickly ramp up AUV levels. Further, we believe that many studios that have re-opened following the onset of COVID-19 have been able to return to or lower their pre COVID-19 operating costs.

Predictable, Asset-Light Model Driving Rapid Growth

As a franchisor, we have employed an economic model that, other than due to the unprecedented global shutdown of our network due to the COVID-19 pandemic, has been predictable, asset light and cash flow generative and has enabled us to open new studios at an accelerated pace compared to an owner-operator model. For the majority of franchises that we sell, we receive an upfront payment from the franchisee, which varies by geography. Once a new studio has opened, we receive contractual, recurring monthly franchise fees that provide us with a high degree of revenue visibility. During the certain periods of the COVID-19 pandemic, we offered franchisees temporary relief from contractual monthly franchise

fees. As our network of total studios grows, we expect recurring revenue as a percentage of total revenue to increase.

Given our model is nearly 100% franchised, we have also been able to maintain a strong margin profile. For the year ended December 31, 2021, we reported operating margin and Adjusted EBITDA margin of (61.6)% and 38.8%, respectively.

Proven Management Team with Value-Added Investors and Ambassadors

F45 Training is led by an experienced and passionate team dedicated to driving the continued growth of the business. Our CEO and co-founder, Adam Gilchrist, has developed and fostered our strategic vision and culture of excellence from the very beginning. Our broader management team consists of a deep bench of experienced professionals with expertise in finance, operations, marketing and other critical areas, which we believe helps to position us to execute on our long-term strategy.

In March 2019, Mark Wahlberg made a strategic minority investment in F45 Training, providing critical branding and marketing capabilities to supplement the strengths of our management team.

In addition to Mr. Wahlberg, we have established relationships with several internationally recognized ambassadors, including Earvin “Magic” Johnson, Jr., David Beckham, Greg Norman, Cindy Crawford, and other celebrities and professional athletes.

Our Growth Strategies

We believe there are several attractive opportunities to continue to drive the long-term growth of our business.

Expand Studio Footprint in the United States

We believe there is a significant opportunity to meaningfully expand our franchise studio footprint in the United States. As of December 31, 2021, we had 1,710 Franchises Sold and 654 Total Studios in the United States. Prior to the COVID-19 pandemic, we had seen the pace of our U.S. growth accelerate with average net Franchises Sold per month increasing from 12 in 2017 to 19 in 2018 to 32 in 2019. Due to COVID-19, the average net Franchises Sold per month decreased in 2020 to 10. In 2021, the average net Franchises Sold per month increased to 65 and 88 in the US and globally respectively, the most in our operating history. We believe there is long-term studio potential for over 7,000 F45 Training studios in the United States.

Expand Studio Footprint Throughout the Rest of the World

We believe in the proven portability of our brand and franchise model, as evidenced by our strong growth outside of our core U.S. and Australian markets. We have designed our studios to be deployed successfully in both developed and emerging markets, and to drive continued growth in both under penetrated and new markets. As of December 31, 2021, we had 788 Franchises Sold outside of our core markets of the United States and Australia. Based on an extrapolation of current Franchises Sold in Australia per capita as of December 31, 2021, we believe there is a long-term global opportunity for over 23,000 studios, with a potential for approximately 16,000 studios outside of the U.S. market. We believe we can continue to grow our international presence through our existing franchising strategy and by opportunistically pursuing master franchising agreements to sell select territories to experienced, local partners.

Generate Incremental Franchise Fee Revenue by Driving Growth in Same Store Sales and AUVs

Our franchise agreements generally provide us with contractual monthly franchise fees equal to the greater of a fixed monthly fee or a percentage of gross monthly studio revenue, generally 7%. We

believe this model helps to align our interests with those of our franchisees while also providing us with the opportunity to participate in revenue upside as our franchisees grow studio AUVs.

Pursue Franchise Agreements with Multi-Unit Franchise Systems

The majority of our studios are owned by franchisees who are either owner-operators or investors that have more than one studio. Going forward, we intend to seek opportunities to develop multi-unit franchise systems with select financial partners. As of December 31, 2021, approximately 65% of our Franchises Sold were owned by multi-unit franchisees, up from approximately 50% as of December 31, 2020, which highlights the strong market demand for multi-unit franchise opportunities.

Expand Into New Channels

We believe there is a significant opportunity to expand into new channels, and we are actively pursuing potential opportunities to partner with major universities, hospitality operators, corporations and military facilities. In 2016, we believe we became the first external studio fitness provider to open a studio on a major U.S. university campus through our collaboration with the University of Southern California. As of December 31, 2021, we had 34 studios located on major university campuses in the United States, including Purdue University, Stanford University and the University of Texas at Austin. In 2021, we expanded our presence in the hospitality channel through our partnerships with Hilton Resorts and OneSpaWorld.

Develop Workout Programs to Access New Target Demographics

We believe there is a significant opportunity to create workout programs that enable us to target a broader range of consumer demographic groups.

We recently developed a new fitness concept called FS8, which we began marketing in Australia in March 2021. FS8 integrates three popular methods in the health and fitness industry, the remixing of Pilates, yoga and tone, to create a new workout style. This workout style is an effective method of building lean muscle and definition. FS8 offers members a premium fitness experience through F45’s platform of training systems, the FS8TV and FS8 App, and also offers franchisees a proprietary business model and large community via the franchise network. We also have a dedicated support team to assist across all business functions. As of December 31, 2021, we had sold 123 total FS8 studios in Australia.

During 2021, we also continued the development of additional concepts, including Malibu Crew, a functional fitness studio clubhouse targeting men over the age of 50, as well as Avalon House, a studio sanctuary for women of a similar age. As of December 31, 2021, we had one Malibu Crew and one Avalon House company-owned locations in operation, respectively. We believe there is a significant long-term opportunity to grow the footprints of these concepts through our innovative go-to-market franchise model.

Strategically Utilize M&A to Further Grow Footprint and Attract New Members

The boutique fitness industry remains highly fragmented, which offers attractive opportunities to utilize strategic and bolt-on M&A to drive consolidation.

In the fourth quarter of 2021, we announced the acquisition of Vive Active, a high-growth, profitable Australian fitness company that offers reformer and mat Pilates workouts through in-studio, at-home streaming and on-demand classes. We completed this acquisition in the fourth quarter of 2021. We plan to continue to grow Vive Active’s footprint through a mix of company-owned studios and franchised studios in select international markets.

Our Workouts

Functional Training Experience

We believe we offer the world’s best functional training workout. We combine elements of high intensity interval, circuit and functional training to offer our members an intense 45-minute workout consisting of natural real-world movements, such as lifting, squatting, jumping, twisting, kicking, rowing, cycling and other high intensity exercises. Our workouts utilize our proprietary, in-studio technology to allow members to walk through a series of exercise stations. In-studio F45TVs provide video instructions for each exercise, and our in-studio trainers help guide members on proper form and movement. We believe that by designing highly innovative and effective total body workouts that minimize injury risk and allow for increased visit frequency, we provide our members with a fitness program that is well positioned to serve as the basis for achieving their long-term fitness goals.

Dynamic Fitness Programming

Our fitness program consists of strength, cardio and hybrid branded workouts. Our branded workouts are mapped on thirteen four-week cycles, with each cycle focusing on specific disciplines, such as boxing, American football training, partner workouts and more. This structure helps to ensure that each member experiences a differentiated and engaging workout. As new fitness trends arise, we are able to adapt our programming and cater to changing consumer preferences through the continuous evolution of our workouts, utilizing both new and existing content in our branded workout and functional training movement library. Once the branded workout cycle is set, we employ an automated workout programming algorithm that scans our database of over 8,000 unique functional training movements across modalities to select exercises based on each of the branded workout’s defined key characteristics and configure a series of exercises within each workout. Our workout programming algorithm accounts for the following criteria, ensuring every routine is dynamic, sustainable and new:

•movement and exercise types;

•muscle groups;

•type of equipment;

•exercise frequency (avoiding repetition); and

•number of stations and sequencing.

After the algorithm builds a workout cycle, these workouts are then vetted by head trainers in the F45 Athletics Department to confirm quality, avoid duplication of targeted muscle groups or movements and provide for efficient transitions between stations. The new cycle is finalized approximately three weeks ahead of its system-wide release after testing the new program across several test studios for quality and ease of use by trainers and members.

Our Studios

Studio Layout and Design

We have designed our studios around the principles of functionality, simplicity and purpose. Each studio has an optimized footprint, with a minimum training area of as little as approximately 1,600 square feet, which enables our studios to be located in a wide array of attractive prospective retail locations. We believe the flexible design and open floor plan layout of our studios positions us to be responsive to potential shifts in consumer preferences as new fitness trends emerge with different setup requirements. The flexible design of our studios has proven to be particularly helpful in allowing us to effectively modify studio layout to accommodate proper social distancing during the pandemic, as well as enter new channels.

Each studio has standardized F45 Training-branded fitness equipment and related technology, which includes F45TVs, spin bikes, dumbbells, kettlebells, sleds and more, all of which are included in our World Pack. The wall-mounted F45TVs are positioned throughout the studio to provide an illustrative, station-by-station guide for each workout and to serve as a reference point for members to visualize proper form and progress through each workout station. In-studio trainers provide additional support by helping members execute exercises with appropriate form and resistance level, while offering encouragement and motivation. To drive a welcoming, intimidation-free environment, we purposely

exclude mirrors on the walls of our studios. Our standardized studio design helps ensure the consistency of the F45 Training experience across our global network of studios.

Studio Membership and Member Pricing

We provide franchisees with suggested pricing for workouts and membership options based on relevant market dynamics, but pricing is ultimately managed at the discretion of our franchisees. Franchisees typically offer multiple membership options, such as weekly memberships with unlimited workouts, monthly memberships with a limited number of workouts, workout packs that include a fixed number of workouts that can be used at any time, as well as single workout options. Franchisees may also offer other membership options, including longer-term memberships for a discounted rate and specific promotional membership plans. Many franchisees offer a limited free trial period to attract prospective new members. We do not offer multi-studio membership plans and memberships are not transferable across our studios.

Franchise Model

Franchising Strategy

We utilize an attractive franchise model that has allowed us to scale our business rapidly. As of December 31, 2021, we had a global network of 3,301 Total Franchises Sold, including 1,749 Total Studios, of which 1,580 had re-opened following one or more temporary COVID-related closures. Approximately 35% of Total Franchises Sold are owned by single-unit franchisee owners, with the other 65% owned by multi-unit franchisees. As of December 31, 2021, our largest franchisee owns 362 franchises, representing approximately 11% of our Total Franchises Sold. As we pursue opportunities to develop multi-unit franchise systems with financial partners, we expect the percentage of multi-unit franchisees to increase over time.

Franchise Agreement

For each franchise license, we enter into an agreement with the franchisee covering standard terms and conditions. We grant our franchisees an exclusive area or territory under the franchise agreement, and territories are determined as agreed with us using our internal analysis, after taking into account population density and demographics. The proposed location must be approved by us, and each franchisee is responsible for the acquisition or lease of the premises from which to operate the business within their respective territory. The franchise agreement requires that the franchisee operate the studio at a specific location.

The typical franchise agreement has an initial five-year term. We may refuse to extend the term of the agreement if the franchisee is in default under the franchise agreement or has failed to achieve minimum performance targets. More specifically, within 12 months of opening, each franchisee must achieve an annual gross revenue of at least 70% of the average gross revenue of all franchisees who have been operating for at least 12 months. Within six months of the expiration of the initial five-year term, franchisees have the opportunity to renew for an additional five-year term, subject to the terms and conditions prevailing at the time of renewal.

The franchise agreement requires franchisees to comply with our standard methods of operation, which govern the provision of services, use of vendors and sale of merchandise. These provisions require that franchisees must generally purchase equipment from us and may only buy products, goods and materials approved by us. We may terminate the franchise agreement upon an event of default by the franchisee, and the franchisee may terminate only with our mutual consent.

Historically, franchisees have paid a fixed monthly franchise fee. Since July 2019, we transitioned our model in the United States for new franchisees to a franchise fee based on the greater of a fixed monthly franchise fee or a percentage of gross monthly studio revenue. In select markets outside of the

United States, and for renewals of existing franchisees in the United States, we are in the process of transitioning to a similar model.

Attractive Franchisee Return Profile

Our franchise model has the potential to generate strong returns for franchisees as a result of a relatively low initial investment and favorable operating cost structure driven by our purpose-built studio design and proprietary technology-enabled ecosystem. We believe that our scale provides us with cost advantages that allow us to offer our equipment to our franchisees for a significantly lower cost than if they were to acquire it on their own. We recommend that our franchisees typically staff one lead trainer and at least one assistant trainer during business hours. We also provide ongoing back-office support through our customer relationship management capabilities to assist with day-to-day booking and operation of the business. We believe the modest initial investment, combined with limited staffing needs, creates the potential for strong financial performance and expands the universe of potential franchisees.

Industry Dynamics

Favorable Industry Fundamentals

The fitness industry represents a large market that has historically exhibited attractive growth characteristics due to various secular consumer trends. According to IHRSA, the global health club market size was estimated to be $97 billion in 2019, with the U.S. segment of this market representing $35 billion. From 2014 to 2019, the global health club industry grew at a CAGR of 2.8%, with the U.S. health club industry growing at a CAGR of 7.7%. We believe that the following have been, and will continue to be, key drivers of industry growth:

•increased consumer focus on health and wellness, driven by education on the health benefits of exercise;

•changes in consumer spending in favor of experiences, including group fitness; and

•cultural shifts promoting fitness as an aspirational lifestyle and form of community, supporting the studio fitness model.

With only 64.2 million Americans ages six and older having health club memberships according to IHRSA, we believe there is significant opportunity for further growth in fitness engagement and membership in the United States.

COVID Impact on Fitness Industry

The COVID-19 pandemic has negatively impacted the fitness industry. At the peak of the pandemic, nearly all health and fitness centers in the United States were closed. Many other developed markets around the world in which we operate experienced similar closures. Multiple health club operators have entered bankruptcy and many gyms and health clubs will never reopen. According to IHRSA, as of January 1, 2022, 25% of fitness facilities in the United States had permanently closed. Our studio network has proven to be resilient in the face of the pandemic, with approximately 1% of the number of total studios permanently closed in the year ended December 31, 2021.