UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2022

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from _______________ to _______________

Commission file number 001-39189

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | ||||||||||

(Address of Principal Executive Offices) | (Zip Code) | ||||||||||

Registrant's telephone number, including area code

N/A

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports); and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ☐ | x | |||||||||

Non-accelerated filer | ☐ | Smaller reporting company | |||||||||

Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No x

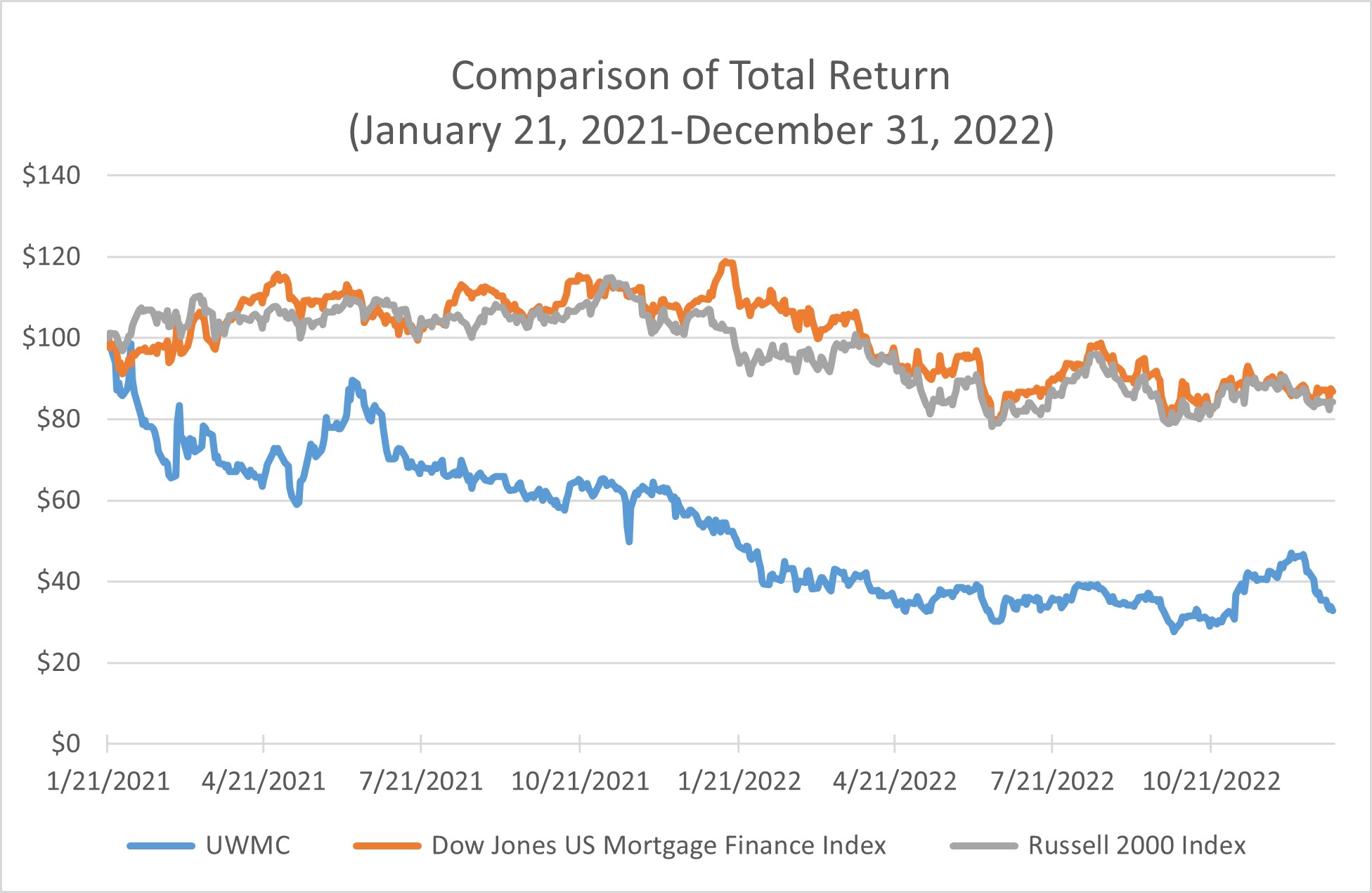

The aggregate market value of the registrant's voting stock held by non-affiliates on June 30, 2022 was $326,829,162 , based on the closing price on the New

York Stock Exchange on that date of $3.54. (Does not include shares issuable upon exercise of warrants).

As of February 24, 2023, the registrant had 93,101,971 shares of Class A common stock outstanding and 1,502,069,787 shares of Class D common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for use in connection with its 2023 Annual Meeting of Stockholders, which is to be filed no later than 120

Table of Contents

| Section Name | Page | ||||

| PART I | |||||

| PART II | |||||

Item 8. Financial Statements and Supplementary Data | |||||

| PART III | |||||

| PART IV | |||||

GLOSSARY OF TERMS

Terms | Definitions | |||||||

“Fannie Mae” | The Federal National Mortgage Association is a government-sponsored enterprise that purchases qualifying mortgage loans from mortgage lenders, packages them together, and sells them as a mortgage-backed security to investors on the secondary market. | |||||||

“FHA” | The Federal Housing Administration is a governmental agency that provides mortgage insurance on loans made by FHA-approved lenders. | |||||||

“Forward-settling Loan Sale Commitment” or “FLSC” or “TBA” | A forward-settling Loan Sale Commitment (also referred to as a FLSC or a TBA) is a forward derivative that requires a mortgage lender to commit to deliver at a specific future date a mortgage-backed security issued by Fannie Mae, Freddie Mac or guaranteed by Ginnie Mae which is collateralized by an undesignated pool of mortgage loans. | |||||||

“Freddie Mac” | The Federal Home Loan Mortgage Corporation is a government-sponsored enterprise that purchases qualifying mortgage loans from mortgage lenders, packages them together, and sells them as a mortgage-backed security to investors on the secondary market. | |||||||

“Ginnie Mae” | Government National Mortgage Association is a government-owned corporation that guarantees mortgage-backed securities that have been guaranteed by a government agency, mainly the Federal Housing Administration and the Veterans Administration. | |||||||

“GSE” | Government-sponsored enterprises, such as Fannie Mae and Freddie Mac. | |||||||

“interest rate lock commitment” or “IRLC” | An interest rate lock commitment is a binding agreement by a mortgage lender with a borrower to extend a mortgage loan at a specified interest rate and term within a specified period of time. | |||||||

“loan officers” | We use the term loan officers to refer to the individual employees of our clients. Each loan officer is licensed, or exempt from licensure, in the state or states in which he or she operates. | |||||||

“mortgage-backed security” or “MBS” | Mortgage-backed securities, or MBSs, are securities that are secured by a pool of mortgage loans, which does not include the MSRs which are separated from the mortgage loan prior to the mortgage loan being placed in the pool and are therefore not part of the collateral. | |||||||

“mortgage servicing rights” or “MSRs” | Mortgage servicing rights, or MSRs, are the right to service a mortgage loan for a fee, which rights are separated from the mortgage loan once the mortgage loan is sold in the secondary market. | |||||||

“To Be Announced market” | The To Be Announced market is a secondary market where FLSCs or TBAs are sold by lenders seeking to hedge the risk that market interest rates may change and lock in a price for the mortgages they are in the process of originating. | |||||||

1

Cautionary Note Regarding Forward-Looking Statements

This report contains “forward-looking statements” within the meaning of Section 27A of the Securities Act and Section 21E of the Exchange Act. These forward-looking statements relate to expectations for future financial performance, business strategies or expectations for our business. Specifically, forward-looking statements in this report include statements relating to:

•the future financial performance of our business;

•our future growth, including our loan originations and position in the industry compared to our peers;

•our client-based business strategies, strategic initiatives, technological developments and product pipeline;

•expectations regarding the impact and timing of discontinuation of LIBOR on our warehouse and other facilities;

•the impact of interest rate risk on our business;

•our ability to renew our sale and repurchase agreements, and the impacts of counterparty risks on our business;

•our mitigation of credit risks and the impacts of defaults on our business, as well as our risk mitigation strategies;

•our accounting policies and recent amendments to the FASB rules regulations;

•macroeconomic conditions that may affect our business and the mortgage industry in general;

•political and geopolitical conditions that may affect our business and the mortgage industry in general;

•our utilization of our warehouse facilities, MSR Facility, and Revolving Credit Facility, including outstanding borrowings through 2023;

•the impact of litigation on our financial position;

•our repurchase and indemnification obligations; and

•other statements preceded by, followed by or that include the words “may,” “can,” “should,” “will,” “estimate,” “plan,” “project,” “forecast,” “intend,” “expect,” “anticipate,” “believe,” “seek,” “target” or similar expressions.

These forward-looking statements involve estimates and assumptions which may be affected by risks and uncertainties

in the Company’s business, as well as other external factors, which could cause future results to materially differ from those

expressed or implied in any forward-looking statement including those risks set forth below in Risk Factor Summary and the

other risks and uncertainties indicated in this report, including those set forth under the section entitled “Risk Factors.”

All forward-looking statements speak only as of the date of this report and should not be relied upon as representing our views as of any subsequent date. We do not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

RISK FACTOR SUMMARY

An investment in our securities involves substantial risk. Our ability to execute on our strategy also is subject to certain risks. The risks described under the heading “Risk Factors” immediately following the Summary below may cause us not to realize the full benefits of our competitive strengths or may cause us to be unable to successfully execute all or part of our strategy. Some of the more significant challenges and risks we face include the following:

•our dependence on macroeconomic and U.S. residential real estate market conditions, including changes in U.S. monetary policies that affect interest rates;

•our reliance on our warehouse facilities to fund mortgage loans and otherwise operate our business, leveraging of assets under these facilities and the risk of a decrease in the value of the collateral underlying certain of our facilities causing an unanticipated margin call;

•our ability to sell loans in the secondary market, including to government sponsored enterprises, and to securitize our loans into mortgage-backed securities through the GSEs and Ginnie Mae, and our ability to sell MSRs in the bulk MSR secondary market;

•our dependence on the GSEs and the risk of changes to these entities and their roles, including, as a result of GSE reform, termination of conservatorship or efforts to increase the capital levels of the GSEs;

•changes in the GSEs’, FHA, USDA and VA guidelines or GSE and Ginnie Mae guarantees;

•our dependence on licensed residential mortgage officers or entities, including brokers that arrange for funding of mortgage loans, or banks, credit unions or other entities that use their own funds or warehouse

2

facilities to fund mortgage loans, but in any case do not underwrite or otherwise make the credit decision with regard to such mortgage loans to originate mortgage loans;

•the unique challenges posed to our business by the COVID-19 pandemic and the impact of governmental actions taken in response to the pandemic on our ability to originate mortgages, our servicing operations, our liquidity and our team members;

•the risk that an increase in the value of the MBSs we sell in forward markets to hedge our pipeline may result in an unanticipated margin call;

•our inability to continue to grow, or to effectively manage the growth of, our loan origination volume;

•our ability to continue to attract and retain our Independent Mortgage Broker relationships;

•the occurrence of a data breach or other failure of our cybersecurity;

•loss of key management;

•reliance on third-party software and services;

•reliance on third-party sub-servicers to service our mortgage loans or our mortgage servicing rights;

•intense competition in the mortgage industry;

•our ability to implement technological innovation;

•our ability to continue to comply with the complex state and federal laws, regulations or practices applicable to mortgage loan origination and servicing in general, including maintaining the appropriate state licenses, managing the costs and operational risk associated with material changes to such laws;

•fines or other penalties associated with the conduct of Independent Mortgage Brokers;

•errors or the ineffectiveness of internal and external models or data we rely on to manage risk and make business decisions;

•loss or inability to enforce intellectual property rights or contractual rights;

•risk of counterparty terminating servicing rights and contracts;

•the possibility that we may be adversely affected by other economic, business, and/or competitive factors; and

•the requirements of being a public company may strain our resources, divert management’s attention and affect our ability to attract and retain qualified board members and team members.

PART I

Item 1. Business

Unless otherwise indicated or the context otherwise requires, when used in this Annual Report, the term “UWMC” means UWM Holdings Corporation, “UWM” means United Wholesale Mortgage, LLC and "the Company," “we,” “our” and “us” refer to UWM Holdings Corporation and our subsidiaries.

Overview

We are the publicly traded indirect parent of United Wholesale Mortgage, LLC (“UWM”). Commencing in the third quarter of 2022, UWM is the largest overall residential mortgage lender in the U.S., despite originating mortgage loans exclusively through the wholesale channel. For the last eight years, including the year ended December 31, 2022, we have been the largest Wholesale Mortgage Lender in the U.S. by closed loan volume. We originate primarily conforming and government loans across all 50 states and the District of Columbia.

We are focused on propelling the wholesale mortgage broker channel forward. During 2022, as interest rates rose and the mortgage industry experienced a slow-down of refinancings, we continued to make significant strides to provide Independent Mortgage Brokers with a variety of product offerings to address market conditions and bring more awareness to the broker channel overall and the value that this channel provides to consumers. With a culture of continuous innovation of technology, enhanced client experience, and market responsive pricing and profitability enhancements, our main goal has been to ensure the Independent Mortgage Broker community, and therefore UWM, is set up to win.

3

Founded in 1986 and headquartered in Pontiac, Michigan, we have built a client-focused, team-oriented culture that strives to bring superior customer service, efficiency and operational stability to our clients, the Independent Mortgage Brokers. UWM completed its business combination with Gores Holdings IV, Inc. (“Gores IV”) on January 21, 2021, pursuant to which UWM became an indirect subsidiary of Gores IV. Upon consummation of the business combination, Gores IV changed its name to UWM Holdings Corporation. We began trading on the New York Stock Exchange on January 22, 2021 under the ticker symbol UWMC.

Strategy

Our principal strategy that has driven our substantial growth over the past years, is our strategic decision to operate solely as a Wholesale Mortgage Lender—thereby avoiding conflict with our partners, the Independent Mortgage Brokers and their direct relationship with borrowers. We believe that by not competing for the borrower connection and relationship, we are able to generate significantly higher loyalty and satisfaction from our clients (the Independent Mortgage Brokers) who, in turn, armed with our partnership tools are positioned to direct a growing share of the residential mortgage volume nationwide.

Integral components of our strategy are (1) continuing our leadership position in the growing wholesale channel by investing in technology and partnership tools designed to meet the needs of Independent Mortgage Brokers and their customers, (2) capitalizing on our strategic advantages which include a singular focus on the wholesale channel, that can quickly adapt to market conditions and opportunities, and ample capital and liquidity, (3) employing our six pillars (see below) to drive a unique culture that we believe results in a durable competitive advantage and (4) originating high quality loans, the vast majority of which are backed directly or indirectly by the federal government, to minimize market risks and to maximize opportunity in different macroeconomic environments.

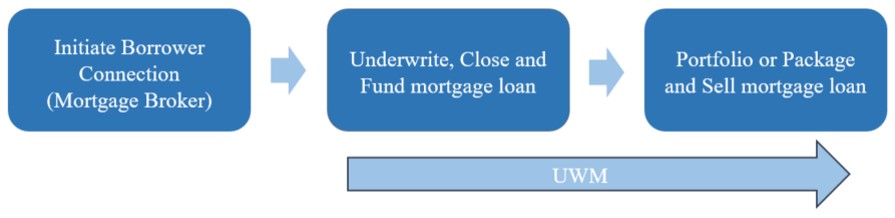

The residential mortgage loan financing process typically involves three stages:

•Initiate Borrower Connection. A broker or other party is approached by a potential borrower for a mortgage loan. This party advises the borrower on loan options, runs the initial credit check, gathers the borrower’s information for the loan application and submits the loan application.

•Underwrite, Close and Fund. The borrower’s loan application is reviewed, the mortgage loan is underwritten, the borrower is approved, the closing is arranged and the loan is funded, collectively referred to as loan origination.

•Portfolio or Package and Sell mortgage loan into Secondary Market Sales. The loan is either placed into an investment portfolio (in the case of banks and typically only for certain loans tied to shorter term interest rates) or packaged together with other loans and sold as MBS to investors in the secondary market.

We operate exclusively as a Wholesale Mortgage Lender and only originate, underwrite and close mortgage loans arranged by an Independent Mortgage Broker. We believe that by focusing only on the wholesale channel, we can be a true partner to our clients (all of which are Independent Mortgage Brokers). Unlike “Retail Mortgage Lenders” that both offer mortgage loans directly to individual borrowers and underwrite the mortgage loans, we do not work directly with the borrower during the mortgage loan financing process.

Many of our competitors are primarily Retail Mortgage Lenders that also compete in the wholesale channel as Wholesale Mortgage Lenders. We believe that by competing in both channels, these competitors have an inherent conflict that makes them a less attractive option for Independent Mortgage Brokers when deciding which lender to work with when originating a mortgage loan. We further believe that this competitive advantage is a major reason that has and will continue to drive market share growth and loan production as the wholesale channel grows.

4

Leading in the Growing Wholesale Channel

According to the Nationwide Multistate Licensing System ("NMLS"), as of September 30, 2022, there were approximately 386,000 federally registered mortgage loan officers in the U.S. Our exclusive focus on the wholesale channel has resulted in relationships with over 12,000 independent broker businesses throughout the U.S., with over 45,000 associated loan officers—of which approximately 33,000 have submitted a loan to us during the year 2022. As the wholesale channel continues to grow, especially in a rising interest rate environment, we see a significant opportunity for these mortgage loan officers to join the wholesale channel.

Benefits to Borrower

•Provides Trusted Advisor in Complex Financial Instruments. Independent Mortgage Brokers serve as advisors to borrowers, leveraging their deep knowledge base of complex financial products to help borrowers make informed decisions. Independent Mortgage Brokers assist prospective borrowers in analyzing their financial situation, assessing his or her credit history and current mortgage and making an informed decision based on their personal circumstances.

•Maximizes Optionality. Independent Mortgage Brokers are able to provide borrowers with multiple options on product structure and pricing rather than being rooted in a single platform offering, which we believe empowers borrowers and enhances their borrowing experience. We believe that Independent Mortgage Brokers are able to deliver borrowers access to better rates than their Retail Mortgage Lender counterparts. As a partner to our clients, we continually strive to provide a range of residential loan options, so that our clients can match the needs of their borrowers with our product offerings.

•Streamlines and Enhances the Experience. Independent Mortgage Brokers are best positioned to be the single personalized point-of-contact for the loan process and provide borrowers a superior customer service experience.

•Aligns Interest. In the wholesale channel, the interests of the Independent Mortgage Broker and the borrower are aligned to achieve the best outcome for the borrower—which increases borrower loyalty to the Independent Mortgage Broker and provides a greater likelihood that the borrower will retain the advisor for future transactions.

Benefits to Independent Mortgage Broker

•Drives Brand Recognition and Loyalty. We believe that allowing Independent Mortgage Brokers to “own” the relationship with the borrower drives client brand recognition and loyalty. When borrowers view their Independent Mortgage Brokers as the person who delivered the superior results, rather than just as a conduit to funding, they are more likely to return to that Independent Mortgage Broker for their next residential mortgage loan, whether it is a new purchase or a refinance. Our technology provides Independent Mortgage Brokers with advanced personalized marketing tools to establish and maintain their borrower relationships.

•Offers Flexibility. We believe that Independent Mortgage Brokers and their loan officers are better served by the wholesale channel as it provides them the flexibility of matching their borrowers’ needs with the most applicable lender and lender program. A Wholesale Mortgage Lender needs to earn business every day. If the Wholesale Mortgage Lender is not faster, easier and more affordable, it will not be successful in earning that business.

• Develops and Protects Relationship with Borrower. Utilizing the wholesale channel with a true Wholesale Mortgage Lender allows Independent Mortgage Brokers to both cultivate new borrower relationships and maintain their relationships with borrowers throughout the mortgage lending process and beyond with less risk of being replaced by the lender in the next new purchase or a refinance. Retail Mortgage Lenders that dabble in the wholesale channel do not afford this protected relationship.

•Ability to Provide Superior Sophisticated and Personalized Service. The wholesale channel allows Independent Mortgage Brokers to offer a diverse set of product options and capitalize on the benefits of scale to offer superior service, such as turn times and pull through rates, with the focus on personal service. Our suite of full-service technology platforms positions Independent Mortgage Brokers to effectively compete with banks and other non-bank loan originators by delivering a closely managed end-to-end experience for the borrower from origination through closing.

5

Benefits to UWM

•Access to Extensive Network. The wholesale channel offers us access to a broad network of Independent Mortgage Brokers, reducing reliance on any one entity or any geographic region.

•Volume Levels Supports Significant Automation. Our volume allows for significant investment in automating each step of the residential loan process, which in turn reduces error rates, improves customer service and enhances efficiency.

•Distribute Fixed Cost Across Wider Network. Our exclusive focus on the wholesale channel reduces our fixed costs by allowing us to distribute costs across a wider network of clients. We invest in the personnel and technology resources to underwrite, close, fund and sell residential mortgage loans. This results in a minimal fixed cost base for origination and high marginal profitability.

•Supports Scalability. We believe that our exclusive focus on the wholesale channel coupled with our efficient and centralized processes, cost structure and technology platform has resulted in a business that is highly scalable with minimal incremental investment.

Capitalizing on our Strategic Advantages

We believe that our exclusive focus on the wholesale channel along with our business model, team members, technologies and competitive position provide us with some significant strategic advantages.

•Strong Brand Recognition. Our leading position as a Wholesale Mortgage Lender and ability to deliver superior client service provides us strong brand recognition with Independent Mortgage Brokers. Starting in the third quarter 2022, we were the largest residential mortgage lender in the U.S. For the year ended December 31, 2022, we had approximately 38% market share in the wholesale channel (based on data released by Inside Mortgage Finance ("IMF")) and 8% share of the overall mortgage market.

•Operational Excellence. We believe our exclusive focus on the wholesale channel provides us with a differentiated, client-centric business model that enables us to invest in, and deliver to our clients, a full suite of technology and workflow solutions that allow for industry-leading closing times for our clients. For the year ended December 31, 2022, we originated approximately 348,000 loans, down from approximately 654,000 loans for the year ended December 31, 2021. For the year ended December 31, 2022, our average application to clear to close time was 18 business days, compared to management's estimate of the industry average of 50 calendar days for 2022. During 2022, we closed an average of 5.9 loans per month per production team member, well above the industry average of 1.7 during the nine months ended September 30, 2022 (based on a Mortgage Bankers Association report). Furthermore, we delivered this speed while receiving an 89% average monthly client Net Promoter Score ("NPS") for the year ended December 31, 2022, as well as an 86% average monthly client NPS for the past six years.

•Innovative Technology Platforms. Leveraging our culture of continuous technological innovation, we have built proprietary technology platforms and exclusively license technology that support our clients and borrowers to provide what we believe to be a best-in-class client experience. We believe that our technology platforms provide us with a competitive advantage, driving client retention and offering the ability to efficiently and quickly achieve closings on loan originations. We offer our clients a complete platform with a highly efficient, external-facing interface that includes required regulatory and compliance mechanisms. We seek to continuously improve and innovate our technology platforms and have a team of over 1,100 full time team members as of December 31, 2022 committed to our information systems and technologies.

6

Employing Our Six Pillars to Drive a Durable Competitive Advantage

We were founded with a simple goal in mind: attract great people, to a great workplace, and give them the tools they need to do great work. Our culture is based on six pillars:

•People—our people are the secret to our success. We invest in our team members with continuous and real-time training so they can continue to set the standard. Team members are given a path to succeed and are rewarded for that success.

•Service—We pride ourselves on creating a memorable service experience for every partner. Internal service among team members is critical.

•Relationship driven—Our long-term reputation is more important than short-term gains. We place a premium on creating lasting relationships with our clients and counterparties, such as our Independent Mortgage Brokers, warehouse banks, vendors, regulators and other agencies.

•Thumb pointers—Team members are focused on accountability and personal responsibility. Our team members concentrate on taking ownership, improving and delivering results.

•Continuous improvement—We develop and introduce cutting-edge, industry leading technology and information processes.

•Fun and friendship—We are a big believer that work can (and should) be fun. It’s about finding your passion and purpose—but always leaving time for friendship and camaraderie. UWM is consistently recognized as a great place to work, winning Top Workplaces USA in 2022 along with its 10th year in-a-row of both Best and Brightest Metro Detroit and Best and Brightest National.

These core principles influence everything we do and form the basis of our client-focused culture.

Originating High Quality Loans Backed Directly or Indirectly by the Federal Government to Minimize Risks and to Maximize Opportunity in Different Macroeconomic Environments

An integral component to our strategy is to originate high quality loans throughout the U.S. For the year ended December 31, 2022, our borrowers had a weighted average FICO score of approximately 738 as compared to a weighted average FICO score of 750 for the year ended December 31, 2021. The following charts illustrate our loan originations portfolio by type and FICO score mix for the year ended December 31, 2022:

7

Our model is focused on the origination business, with a specific focus on purchase loans. Historically, residential purchase mortgage loan origination volume has experienced less volatility in response to interest rate movements than the refinancing mortgage loan origination volume. Consequently, we believe that by focusing on the purchase business we will be better positioned to deliver more consistent volume in increasing and decreasing interest rate environments. In rising interest rate environments, we believe that our demonstrated reputation for excellent client service and short loan closing times will drive continued purchase mortgage volume, our broad client base will allow us to capitalize on lead generation and our cost structure will allow us to be more competitive on margins.

We currently retain the majority of the mortgage servicing rights ("MSRs") associated with our production, but we have, and intend to continue to opportunistically sell MSRs depending on market conditions. This nimble approach has provided us funding flexibility, and reduced legacy MSR asset exposure. In addition, our wholesale-only business is uniquely positioned to capture a greater share of purchase originations and, we believe, provides a competitive advantage relative to correspondent or various retail origination models.

Our Loan Programs

Over the past 10 years we have developed technologies and processes that allow us to quickly introduce and market new loan programs or to adjust for existing loan programs and to adapt services and offerings to ever-changing markets for home financing. These technologies allow us to quickly and efficiently build guidelines, rules, pricing, and controls into our loan origination platforms and workflows; generate new loan documents, disclosures and program descriptions from our systems; and efficiently distribute internal communications. By having nimble and flexible systems that are controlled internally, we believe we are better positioned to take advantage of market opportunities when they present themselves and change the direction of loan programs when the market dictates.

Conventional agency-conforming mortgage loans

Since 2012, we have been primarily focused on originating conventional, agency-eligible loans that can be sold to Fannie Mae, Freddie Mac or transferred to Ginnie Mae pools for sale in the secondary market. Our conventional agency-conforming loans meet the general underwriting guidelines established by Fannie Mae and Freddie Mac. Loans that are written under the FHA program, the VA program or the USDA program are guaranteed by the governmental agencies and then transferred to Ginnie Mae pools for sale in the secondary market. Substantially all of our mortgage loans are underwritten to the “Qualified Mortgage” underwriting standards established by the Consumer Financial Protection Bureau ("CFPB"). For the year ended December 31, 2022, 94% of loans originated were sold to Fannie Mae or Freddie Mac, or were transferred to Ginnie Mae pools in the secondary market, while the remainder were primarily jumbo loans that are underwritten to the same “Qualified Mortgage" underwriting standards and have a similar risk profile but are sold to third party investors purely due to loan size.

8

The following table summarizes our loan production by loan type for the periods indicated.

| ($ in thousands) Loan Type | For the year ended December 31, 2022 | For the year ended December 31, 2021 | For the year ended December 31, 2020 | ||||||||||||||

| Purchase: | |||||||||||||||||

| Conventional | $ | 62,274,030 | $ | 63,026,794 | $ | 33,717,939 | |||||||||||

| Government | 23,773,422 | 14,833,808 | 8,619,874 | ||||||||||||||

| Jumbo and other | 4,782,879 | 9,395,143 | 583,299 | ||||||||||||||

| Total purchase | $ | 90,830,331 | $ | 87,255,745 | $ | 42,921,112 | |||||||||||

| Refinance: | |||||||||||||||||

| Conventional | $ | 27,059,252 | $ | 120,152,065 | $ | 119,807,647 | |||||||||||

| Government | 7,834,636 | 12,034,583 | 18,921,473 | ||||||||||||||

| Jumbo and other | 1,561,242 | 7,061,299 | 897,409 | ||||||||||||||

| Total refinance | 36,455,130 | 139,247,947 | 139,626,529 | ||||||||||||||

| Total Loan Production | $ | 127,285,461 | $ | 226,503,692 | $ | 182,547,641 | |||||||||||

| Production volume (closest '000) | 348,000 | 654,000 | 561,000 | ||||||||||||||

| Average initial loan balance | $ | 365 | $ | 346 | $ | 325 | |||||||||||

Our Mortgage Lending Process

We believe that our highly scaled, efficient and centralized mortgage lending processes are key to our success. Utilizing our proprietary system, “Easiest Application System Ever” (EASETM), and our dedicated team members we focus on client service, and loan quality throughout the entire loan origination, underwriting and closing processes. EASETM automates the process and, based on the jurisdictional requirements of the client and borrower, automatically generates the necessary documents required by us and by the clients for applications. The entire origination, underwriting and preparation of closing documents takes place in our centralized, paperless work environment where documents and data are entered into EASETM and are reviewed, processed and analyzed based on a set of pre-determined, rules-based workflows. We focus on speed to close as it is one of the primary metrics for client satisfaction. We believe our closing process is the most efficient in the industry and results in shorter application to clear-to-close times than any of the other major Retail Mortgage Lenders or Wholesale Mortgage Lenders. For both the years ended December 31, 2022 and December 31, 2021, we delivered an average of 18 business days from loan application to clear to close, as compared to management's estimates of the industry averages of 50 and 46 calendar days, respectively.

Our rules-based mortgage loan origination system, or LOS allows multiple teams to work on the same loan at the same time, to track and be alerted to missing or incomplete items, to flag items in order to alert other team members of possible deficiencies and to have visibility into the history, status and progress of loans in process. We use advanced technologies and workflow systems to assist all underwriting and operations team members in prioritizing which loans require their immediate attention and to monitor each team’s progress so workload-balancing decisions can be made among the operation teams in real time and avoid bottlenecks.

Underwriting

Our underwriting process is one of our key strategic advantages as our extensive training program and technology platforms allow us to produce a portfolio of high-quality loans, with an industry-leading time from application to clear to close and maintain the superior level of client service that allows us to attract and retain our clients. All mortgage loans that we originate are underwritten in-house by our underwriting team. We invest significant time and resources in our underwriters through our robust training process to help them and us succeed. We believe that our intensive training program is an integral component of our scalability as we are able to materially increase our underwriting resources, at a consistent quality, with less labor constraints and complications than our competitors.

Our clients, the Independent Mortgage Brokers, have the initial communication with a potential borrower and they receive from the borrower the relevant financial and property information to run a credit check and obtain a pre-approval through one of the automated underwriting systems. Once a pre-approval has been received, an Independent Mortgage Broker is able to seamlessly import the borrower’s information and documentation into our EASETM LOS without the need for extra data entry. One of our senior underwriters then reviews the file and, based on the loan product and the financial and other information provided, makes an underwriting decision. If the mortgage loan is approved, our system generates a “conditions to

9

close” list based on the specifics of the borrower, the property and the loan product and a junior underwriter who generally takes ownership of the file ensuring that each of these conditions is met prior to granting a “clear-to-close.”

We utilize technology and automated processes throughout the underwriting process, to provide our underwriters “guard rails” and allow us to efficiently and effectively underwrite loans while mitigating risk. For example, if a loan product requires an 80% loan-to-value or a family gift is providing a portion of a deposit, our systems are programmed to automatically populate the appropriate conditions and not permit the loan to move on to the next step in the underwriting process until the appropriate documents are uploaded into the system. We also recently launched BOLT, which allows mortgage brokers to obtain initial underwriting approval for qualified borrowers in as little as 15 minutes, which we believe will enable brokers to close loans faster.

Loan closings

UWM UCloseTM, our document closing tool, allows clients to facilitate and easily control the closing process, including document generation, title company interaction and the timing of closing. In addition, we structure our closing process such that all conditions are satisfied prior to the generation of closing documents and therefore are able to provide clients and borrowers automatic funding for all closings. Once a title agent uploads the executed documents into UCloseTM, the funds are automatically wired to the appropriate parties. We believe that eliminating the hours of waiting in a title office leads to more satisfied borrowers and repeat business for us and our clients.

We believe we have achieved industry leading close times through the use of proprietary technology and process innovations such as DocHub, UClose and BOLT (described in the "Advanced technologies and systems" section below). Additionally, in 2021, we recognized that one of the pain points in timely closings were the delays in obtaining appraisals. Consequently, we launched UWM Appraisal Direct. Appraisal Direct provides mortgage brokers a streamlined, transparent process for the scheduling, execution and delivery of an appraisal that they can easily track, which we believe will deliver faster appraisals to offer a better experience and relieve a key pain point in the mortgage industry.

Loan closing speeds are also positively impacted for clients who select our innovative Title Review and Closing ("TRAC") program, which provides an alternative to utilizing a traditional lender title policy. By leveraging in-house title counsel to review title related documents and issue attorney title opinion letters ("ATOL(s)") UWM is able to streamline the title review process and facilitate a faster and easier experience for the borrower.

Capital Markets and Secondary Marketing

Our capital markets team is dedicated to maximizing loan sale profitability while at the same time minimizing operational, interest rate and market risks. This team manages the interest rate risk for the business and is responsible for interest rate lock management policies and procedures, hedging the pipeline, managing warehouse facilities and associated facility utilization and managing risk and sales of mortgage servicing rights on the balance sheet. We aggregate our loan production into pools that are (i) sold to Fannie Mae or Freddie Mac or securitized through the issuance of Fannie Mae or Freddie Mac bonds, (ii) transferred into Ginnie Mae pools and securitized by us into government-insured mortgage-backed securities, or (iii) sold outright or securitized to investors in the secondary mortgage market. Our primary access to the secondary market comes from pooling and selling eligible loans that we originate through Fannie Mae, Freddie Mac, and Ginnie Mae’s securitization programs. The goal of the capital markets team is to protect margin at origination, and to maximize execution at sale. We believe that our technologies, automated workflow and experienced capital markets team allow us to quickly aggregate and sell the pools of loans in order to make efficient use of our capital and warehouse facilities. Our focus on agency deliverable originations and speed to sale reduces our exposure to market volatility, liquidity risk and credit risk.

When we have identified a pool of mortgage loans to sell to the agencies, non-governmental entities, or through our private label securitization transactions, we repurchase such loans from our warehouse lender and sell the pool of mortgage loans into the secondary market, but generally retain the mortgage servicing rights, or MSRs, associated with those loans. To the extent we generate non-agency loans, these loans are typically sold under an incentive-based servicing structure which permits us to retain servicing and control the borrower experience. We retain MSRs for a period of time depending on business and liquidity considerations. When we sell MSRs, we typically sell them in the bulk MSR secondary market.

Repurchase and indemnification risks

Although we do not retain credit risk on the loans we sell into the secondary market, we (i) have repurchase and indemnification obligations to purchasers of mortgage loans for breaches under our loan sale agreements and (ii) are

10

contractually obligated, in certain circumstances, to refund to the purchasers certain premiums paid to us on the sale if the mortgagor prepays the loan within a specified period of time.

Loan sale agreements, including Fannie Mae and Freddie Mac master agreements, require us to make certain representations and warranties related to, among other things, the quality of the loans, underwriting of the loans in conformity with the applicable agency, FHA or VA guidelines, and origination in compliance with applicable federal, state and local laws and regulations. Generally, liability only arises if there is a breach of the representations and warranties in a material respect based on standards set forth under the terms of the related loan sale agreement. While some of the representations and warranties in our loan sale agreements may extend over the life of the loan, most of our historical repurchase activity has involved loans which defaulted within the first few years after origination. We attempt to limit the risk of repurchase and indemnification by structuring our operations to ensure that we originate high-quality mortgages that are compliant with the representations and warranties given in the loan sale agreements.

Infrastructure, Systems and Technologies

Advanced technologies and systems

We are a technology driven company that continuously seeks to innovate and provide superior systems to our clients, with over 1,100 highly trained team members dedicated to our technology and information systems located in our Pontiac, Michigan headquarters as of December 31, 2022.

We focus on automating and providing sophisticated tools for loan origination functions, but also with respect to automating the infrastructure that supports those core operations, such as training, capital markets, human resources and facilities functions. Our integrated technology platforms create an automated, scalable, standardized and controlled end-to-end loan origination process that incorporates government/agency guidelines and loan program requirements into rules-based workflows, to ensure loans progress to closing only as conditions, guidelines and requirements are met and required information is provided and verified, and accounts for variations in state laws, loan programs and property type, among other variables.

Our client facing systems are generally proprietary (other than Blink+TM), developed in-house and were built to be scalable and readily modified, which allows us to quickly introduce enhanced features and to change loan program guidelines in response to market, industry and regulatory changes without excessive complex programming or dependency on outside entities. Our client facing systems are as follows:

•Boost - Our exclusive platform which provides independent mortgage brokers with streamlined access to purchase tailored leads, stay in touch with past clients, connect with real estate agents and opt into live call transfers.

•BOLT – Allows mortgage brokers to obtain initial underwriting approval for qualified borrowers in as little as 15 minutes, which we believe will enable brokers to close loans faster. We also believe that BOLT will unlock underwriter capacity and ultimately drive down our cost-per-loan.

•DocHubTM – Our custom-built document management system that allows team members to control the way they view, interact with, and deliver the documents required to close and fund loans. The program allows us to scale business without increasing costs associated with document storage, and processes can be designed in conjunction with the document management system for maximum efficiency.

•Blink+TM – A client facing point of sale (POS) system white-labeled for our clients. Blink+TM allows clients to access our products and pricing, automated underwriting system and fee templates. This solution syncs loan application data, including fees, with our EASETM program, and replaces a client’s costly existing system free of charge while encouraging lead conversion. Blink+TM integrates with Brand 360TM to convert leads into applications.

•InTouch Mobile App – A mobile app that allows our clients to handle virtually every aspect of the lending process, from underwriting through clear-to-close, without need for a desktop computer.

•Brand 360TM – Our all-encompassing marketing platform supports our clients’ growth and brand building capabilities. It provides useful communications tools to help our clients stay connected to borrowers and monitors home equity, new home listings, and rates to provide relevant market updates to ensure clients stay connected with potential new or repeat borrowers.

11

•UCloseTM – Our tool that allows clients to facilitate and easily control the closing process, notably timing, document generation, and title company interaction and the autonomous nature of the tool promotes more timely and efficient closings.

•EASETM – Our “Easiest Application System Ever” is our primary LOS that allows clients to interact with us and to select products, lock rates and run the Automated Underwriting System (AUS).

Our Blink+TM (POS) system was developed by a third party and has been white-labeled for our clients and integrated into our technology suite to provide Independent Mortgage Brokers a direct online method for communicating with us the information required for residential loan applications. We pay the Blink+TM developer per unit transaction fees, subject to a minimum monthly fee. Pursuant to our agreement with the Blink+TM developer, the developer has agreed to not make its online platform available to other wholesale lenders for a term that extends until November 2023 (or November 2024 to the extent that we have closed at least 25,000 loans using the platform during 2023), subject to a de minimis exception that includes our prior written consent for new participants.

In addition, we have internally developed enterprise level systems that:

•provide automated work queue prioritization, operational visibility and relevant metrics which allow us to readily detect and address bottlenecks and inefficiencies in the loan origination process,

•use custom electronic interfaces with vendors and transaction partners, which allow us to quickly obtain and import data into our systems in a form which does not require re-keying of information; and

•deliver desktop computer based training to efficiently and effectively train clients and internal operations teams on new programs and changes in guidelines.

We also maintain an enterprise data/metrics warehouse which provides our team with the ability to interface with statistical, analytical and reporting tools that provides senior management with visibility into key performance indicators in real time.

Data security & safeguards

The Gramm-Leach-Bliley Act (“GLBA”) and other state and federal laws require that financial institutions take measures to safeguard the security and confidentiality of the personal financial information of their clients. Some states have passed laws to further protect client information, including laws that regulate the use of Social Security numbers as identifiers, require notifications to clients if the security of their personal information has been breached and/or require us to encrypt personal information when it is transmitted electronically. We employ various in-house and third-party technologies, and network administration policies, that are designed to:

•protect our computer network and network-accessible resources from unauthorized access;

•protect information stored on our computer network from losses, viruses, external threats and data corruption;

•protect the privacy of information on our computer network and with respect to transfers of information to and from our computer network; and

•protect our computer network and system availability from malicious attacks.

In light of constantly changing threats and vulnerabilities, no computer network can be said to be impervious from attack. However, we believe that the technologies and the information security program that we have adopted are appropriate to the size, complexity and scope of services we provide, as well as the nature of the information that we handle. Our network and information security team members are dedicated to monitoring security systems, evaluating the effectiveness of technologies against known risks and adjusting systems accordingly. In addition, we have outside firms specializing in network security perform periodic penetration testing and periodic internal audits of various information security functions. We also perform periodic audits of our systems for identity and access management.

Loan Servicing

In addition to loan origination, we derive revenue from MSRs related to our loan originations. After a loan is originated, loan servicers manage payments, delinquencies, and other administrative functions of mortgages for third party investors. Servicers derive contractual revenue from servicing fees on the UPB of the loans in their servicing portfolio as well as other ancillary income. The net present value of these expected future cash flows is represented on the balance sheet as

12

MSRs. MSR valuations have traditionally increased with increased interest rates because higher rates lead to decreased prepayments, thereby extending the average life of the asset and increasing related expected cash flows. Conversely, decreases in long term interest rates generally result in a decrease in the value of the MSR portfolio due to the expectation of higher prepayments. As such, MSR cash flows provide a natural hedge to originations, as volumes tend to decline in rising interest rate environments and increase in declining interest rate environments.

We retain MSRs for a period of time depending on business and liquidity considerations. When we sell MSRs, we typically sell them in the bulk MSR secondary market. We utilize two sub-servicers to service the loans for which we have retained servicing rights, one of which is a bank and one is a non-bank lender. By diversifying the type of sub-servicer, as well as splitting the MSR portfolio between two well recognized and capitalized sub-servicers, we believe it mitigates against certain risks inherent in the servicing business (whether done internally or outsourced to a sub-servicer). Our team of approximately 40 servicing oversight professionals is responsible for monitoring our sub-servicers. We have a robust sub-servicer oversight program to ensure a high level of borrower satisfaction and to support the relationships between those borrowers and our clients. Our in-house servicing team performs daily, monthly and quarterly testing to determine performance metrics and ensure agency and regulatory compliance and provides regular updates to our executive leadership team. We contractually obligate our sub-servicers to maintain appropriate licenses where required, maintain their approved servicer status with the applicable agencies and adhere to the applicable agency, investor or credit owner servicing guidelines and requirements in their servicing of mortgage loans for us.

Our servicing, quality control, internal audit, vendor relations, and legal and compliance teams perform various reviews of our servicing oversight program and operations. Our servicing team addresses any deficiencies with sub-servicers to ensure corrective action and controls are implemented.

As of December 31, 2022, our servicing portfolio consisted of 967,050 loans with an aggregate UPB of approximately $312.5 billion, a weighted average service fee of 0.2862% and weighted average note rate of 3.64%. As of December 31, 2021, our servicing portfolio consisted of 1,017,027 loans with an aggregate UPB of approximately $319.8 billion, a weighted average service fee of 0.2624% and a weighted average note rate of 2.94%.

We have experienced delinquency rates in our servicing portfolio that are lower than the industry average, with the percentage of UPB of mortgage loans that are 60 or more days delinquent in payments (referred to as the “60+ delinquency rate”) of approximately 0.85% and 0.81% as of December 31, 2022 and 2021, respectively, compared to the industry average of 2.04% and 3.38%, based on data released by the Mortgage Bankers Association. We attribute this to both our commitment to high quality originations and our focus on client service within the servicing portfolio.

Advance obligations

As a servicer, we are obligated to service the loans according to the applicable agency, investor or credit owner guidelines and law. These obligations may require that we advance certain funds to securitization trusts and to others in the event that the borrowers are delinquent on their monthly mortgage payments. When a borrower remains delinquent, we may be required to advance principal and interest payments to the securitization trusts on the scheduled remittance date. We may also be required to advance taxes, insurance payments, legal fees, and maintenance and preservation costs with respect to property that is subject to foreclosure proceedings. These advances create a receivable due to us from the securitization trusts and/or borrower, and we recover these funds from the securitization trusts, from the borrower or from the proceeds of the sale of property in foreclosure. We had receivables of $135.4 million and $135.1 million as of December 31, 2022 and December 31, 2021, respectively, which are due to us from the securitization trusts and/or borrowers.

Competition

Competition in the residential mortgage loan origination market is intense. Institutions offering to make residential mortgage loans, regardless of the channel, include regional and community banks, thrifts, credit unions, mortgage banks, mortgage brokers, brokerage firms, insurance companies, and other financial institutions.

Some of our competitors may have more name recognition and greater financial and other resources than we have (including access to capital). Other competitors, such as lenders who originate mortgage loans using their own funds, or direct retail lenders who market directly to homeowners, may have more operational flexibility in approving loans, may have advantages in soliciting home loans from their clients or have access to capital through deposits at lower costs than our warehouse facilities. Additionally, we operate at a competitive disadvantage in some respects to U.S. federal banks and thrifts and their subsidiaries because they enjoy federal preemption and, as a result, conduct their business under relatively uniform U.S. federal rules and standards and are generally not subject to the laws of the states in which they do business (including state

13

“predatory lending” laws). Unlike our federally chartered competitors, we are generally subject to all state and local laws applicable to lenders in each jurisdiction in which we originate and service loans. To compete effectively, we must have a very high level of operational, technological and managerial expertise, as well as access to capital at a competitive cost.

Competition for mortgage loan originations takes place on various levels, including brand awareness, marketing, convenience, pricing, and range of products offered. We have increased our share of the residential mortgage market over time due to a client-centric, disciplined, centralized approach to origination. In the face of significant changes in the mortgage market, we have maintained our commitment to high credit quality loans. Our focus on technology and process improvements creates a more efficient origination system for both us and our clients. This has been rewarded with strong client service scores, via our net promoter scores, which we believe is a significant competitive advantage.

Government Regulations Affecting Loan Originations and Servicing

We operate in a heavily regulated industry that is highly focused on consumer protection. Our business is subject to extensive oversight and regulation by federal, state and local governmental authorities. Both the scope of the laws and regulations and the intensity of the supervision to which we are subject have increased in recent years, initially in response to the financial crisis, and more recently in light of other factors such as technological and market changes. We expect to continue to face regulatory scrutiny as a participant in the mortgage sector.

Our loan origination and loan servicing operations are primarily regulated at the state level by state financial services authorities and administrative agencies, and at the federal level by the CFPB. The CFPB has federal regulatory, supervisory and enforcement authority over the residential mortgage loan origination and servicing industry, including residential mortgage lenders and servicers, such as UWM. Specifically, the CFPB has rulemaking authority with respect to the federal consumer financial services laws applicable to mortgage lenders and servicers. These laws include (i) the Truth-In-Lending Act (TILA), (ii) the Homeowners Protection Act (HPA), (iii) the Real Estate Settlement Procedures Act (RESPA), (iv) the Home Mortgage Disclosure Act (HMDA) and Regulation C, and (v) the Fair Debt Collections Practices Act (FDCPA). The CFPB’s enforcement jurisdiction is broad, and it has the ability to initiate investigations and enforcement actions against mortgage lenders and servicers for violations of applicable consumer financial services laws, including, but not limited to, the Dodd-Frank Act’s prohibitions on unfair, deceptive or abusive acts and practices. In addition, the CFPB shares jurisdiction with the FTC with respect to (i) the Equal Credit Opportunity Act (ECOA) and Regulation B issued by the CFPB pursuant to ECOA, (ii) the Fair Housing Act (FHA) and (iii) the GLBA.

As part of its enforcement authority, the CFPB can order, among other things, rescission or reformation of contracts, the refund of moneys or the return of real property, restitution, disgorgement or compensation for unjust enrichment, the payment of damages or other monetary relief, public notifications regarding violations, remediation of practices, external compliance monitoring and civil money penalties. Since its inception in 2011, the CFPB has exercised its enforcement jurisdiction aggressively with respect to mortgage industry participants, initiating investigations, entering into consent orders with significant monetary and injunctive relief, and initiating litigation. Often these matters have involved differing theories and interpretations of long-existing laws without first issuing industry guidance or rules.

In addition to the CFPB, we are subject to a variety of regulatory and contractual obligations imposed by credit owners, insurers and guarantors of the mortgages we originate and service including, but not limited to, Fannie Mae, Freddie Mac, Ginnie Mae, FHFA, FHA, VA and USDA. We periodically receive requests from federal, state and local agencies for records, documents and information relating to the policies, procedures and practices of our loan servicing, origination and collection activities. The agencies as well as GSEs and Ginnie Mae, and various investors and lenders also subject us to periodic reviews and audits and examinations. We are also subject to the Bank Secrecy Act (BSA) and related regulations including the Office of Foreign Assets Control (OFAC) and the Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act.

As noted above, we are also subject to the laws, regulations and rules of the fifty states in which we operate. These laws, regulations and rules may differ by state and sometimes differ from federal standards, are sometimes vague and subject to differing interpretations – all of which exposes us to legal and compliance risks. For example, many states have adopted regulations that prohibit various forms of “predatory” lending and place obligations on lenders to substantiate that a borrower will derive a tangible benefit from the proposed home financing transaction and/or have the ability to repay the loan. These laws have required most lenders to devote considerable resources to building and maintaining automated systems to perform loan-by-loan analysis of points, fees and other factors set forth in the laws, which often vary depending on the location of the mortgaged property.

14

Our clients, the Independent Mortgage Brokers, are also subject to extensive regulation at the state level by state licensing authorities and administrative agencies. In certain circumstances, we can be held potentially liable for the acts and practices of our clients for violations of various federal and state consumer protection and other laws and regulations, including but not limited to (i) RESPA and Regulation X, (ii) the Federal Trade Commission Act (FTC Act), the FTC Credit Practices Rules and the FTC Telemarketing Sales Rule, each of which prohibit unfair or deceptive acts or practices and certain related practices; and (iii) the Telephone Consumer Protection Act (TCPA), which restricts telephone solicitations and the use of certain automatic telephone equipment. As a part of our enterprise risk management approach, we monitor our clients’ compliance with applicable laws and regulations.

The federal and state laws, rules and regulations to which we or our clients are subject affect nearly all aspects of our lending and servicing operations as well as those of our clients and partners. Given the extensive, complex and sometimes vague nature and scope of the laws, rules and regulations applicable to us, our clients and our partners and the judicial and administrative decisions and other actions interpreting them, we are subject to significant legal and compliance risks that could arise merely from inadvertent errors and omissions that we may not be able to eliminate entirely from our operations and activities or from the inadvertent errors of clients or partners that we may not be able to control for or address proactively. Consequently, we devote substantial resources to regulatory compliance and collaborate across our legal, operations, underwriting and IT teams to maintain our compliance management systems. However, we believe that the complexity of governmental regulations and the cost of compliance is a competitive advantage insofar as it imposes barriers to entry, limiting market participants to those whose volume supports such costs. Laws, rules and regulations that affect participants in the residential mortgage lending process, such as Independent Mortgage Brokers, also afford us an opportunity to leverage our technology platform to develop processes that are faster, easier and more affordable for such participants and ultimately for consumers.

Cyclicality and Seasonality

The demand for loan originations is affected by consumer demand for home loans and the market for buying, selling, financing or re-financing residential real estate, which is primarily driven by interest rates and employment levels. Interest rates and employment levels are, in turn, affected by the national economy, regional trends, property valuations, and socio-economic trends, and by state and federal regulations and programs which may encourage or discourage certain real estate trends.

Human Capital Management

We are more than just a mortgage company, we are a team of focused professionals making dreams come true for hopeful homebuyers across the country. We have created a culture that celebrates team spirit and an environment where work-life balance is more than lip-service.

Team Members

Our team members are the secret to our success, and we believe our team is only as strong as we make it. As of December 31, 2022, we had approximately 6,000 team members, substantially all of whom are based in our corporate campus in Pontiac, Michigan. We celebrate our team members and all of their accomplishments through various events throughout the year. From our annual company-wide family fair with thousands of smiling faces to afternoon dance parties, we believe that it is important to focus on the health and happiness of our team members and their families.

We provide a combination of health and retirement benefits to our eligible team members, including but not limited to coverage for medical care, vision, dental, life insurance, disability, 401(k) and paid time off. Our campus also offers team members easy ways to manage their health and welfare with a full-size indoor basketball court, an outdoor sand volleyball court, a large, state-of-the-art fitness center with a variety of fitness classes, a game room, featuring arcade games and table tennis, a primary care doctor's office, physical therapy studio, chiropractor and a full-time massage therapist.

We believe this commitment to our team members is why we have been recognized again in 2022 by numerous organizations for being a top employer and a great place to work. In a 2022 employee engagement survey, 95.28% of team members responded that they felt they belonged at UWM from a diversity and inclusion standpoint.

Diversity and Inclusion

15

We strive to foster a culture of diversity and inclusion so all team members feel respected and no team member feels discriminated against. Our diverse, inclusive culture was built to promote positive attitudes, strong work ethics and individual authenticity. We believe a diverse workforce fosters innovation and cultivates an environment of unique perspectives. As of December 31, 2022, approximately 42% of our team members were female and 31% of our team members that choose to identify their ethnicity identified as ethnically diverse.

Engagement and Opportunities

Continuous improvement is a primary focus of our strategic plan and one of our core pillars. We believe personal and professional growth accelerates careers while promoting productivity and innovation. We heavily invest in the development of each team member. We have approximately 200 training team members dedicated to providing our new hires and existing team members with the trainings and resources necessary to pursue their career paths and ensure compliance with our policies. In 2022, approximately 1.6 million total training hours were delivered to team members. We are dedicated to increasing team member engagement by strategically aligning talent within UWM. As a result, we promoted approximately 1,300 team members during 2022.

Community Outreach

We recognize that our team members are part of the greater community in which they live and work and we are committed to giving back and making a positive impact on these communities around us and supporting our team members in their efforts to do the same. We believe in providing our team members the opportunity to do a lot of good and support the causes they care about. Team members receive paid-time off that they can use to volunteer. We and our team members partner with charities such as Adopt-A-Family, Breast Cancer Awareness and the American Red Cross, and sponsor local backpack, bike and coat drives to provide opportunities to give back. Our unique Pay It Forward program allows everyone the chance to earn points that direct where our Company charity dollars are spent — ensuring that even small gestures can be turned into generous contributions, and the opportunity to choose where our charitable dollars go.

Available Information

Our annual reports on Form 10-K, quarterly reports on From 10-Q, current reports on Form 8-K, proxy statements and amendments to those reports filed with or furnished to the SEC pursuant to Section 13(a) or 15(d) of the Exchange Act are available free of charge through the investor relations section of our website at www.uwm.com as soon as reasonably practicable after electronically filing such material with the SEC. The SEC maintains an internet site that contains reports, proxy and information statements and other information regarding our filings at www.sec.gov. The above references to our website and the SEC’s website do not constitute incorporation by reference of the information contained on those websites and should not be considered part of this Annual Report.

Item 1A. Risk Factors

You should carefully review and consider the following risk factors and the other information contained in this Annual Report, including the financial statements and notes to the financial statements included herein. The following risk factors apply to our business and operations. The occurrence of one or more of the events or circumstances described in these risk factors, alone or in combination with other events or circumstances, may have an adverse effect on our business, cash flows, financial condition and results of operations. You should also carefully consider the following risk factors in addition to the other information included in this Annual Report, including matters addressed in the section entitled “Cautionary Note Regarding Forward-Looking Statements; Risk Factor Summary.” We may face additional risks and uncertainties that are not presently known to us, or that we currently deem immaterial, which may also impair our business or financial condition.

Risks Related to Our Business

Our loan origination and servicing revenues are highly dependent on macroeconomic and U.S. residential real estate market conditions.

Our success depends largely on the health of the U.S. residential real estate industry, which is seasonal, cyclical, and affected by changes in general economic conditions beyond our control. Economic factors such as increased interest rates, slow economic growth or inflationary conditions, the pace of home price appreciation or the lack of it, changes in household debt levels, and increased unemployment, stagnant or declining wages or decreased purchasing power due to inflation affect our borrowers’ income and thus their ability and willingness to make loan payments.

16

National or global events affect all such macroeconomic conditions. Weak or a significant deterioration in economic conditions reduce the amount of disposable income consumers have, which in turn reduces consumer spending and the willingness of qualified potential borrowers to take out loans. It is uncertain what impact the recent American Rescue Plan, other actions that the new Biden administration may adopt or steps that may be implemented by the Treasury Department may have on the macroeconomic conditions of the U.S. Furthermore, several state and local governments in the U.S. are experiencing, and may continue to experience, budgetary strain. One or more states or significant local governments could default on their debt or seek relief from their debt under the U.S. bankruptcy code or by agreement with their creditors. Any or all of the circumstances described above may lead to further volatility in or disruption of the credit markets at any time and could adversely affect our financial condition. Such economic factors typically affect buyers’ demand for new homes or their willingness or ability to refinance their current mortgages which could adversely affect the wholesale loan origination market and our financial condition or results of operations.

Any uncertainty or deterioration in market conditions that leads to a decrease in loan originations will likely result in lower revenue on loans sold into the secondary market. Lower loan origination volumes generally place downward pressure on margins, thus compounding the effect of the deteriorating market conditions. Moreover, any deterioration in market conditions that leads to an increase in loan delinquencies will result in higher expenses for loans we service for the GSEs and Ginnie Mae. The increased cost to service loans could decrease the estimated value of our MSRs. In addition, an increase in delinquencies lowers the interest income we receive on cash held in collection and other accounts and may increase our obligation to advance certain principal, interest, tax and insurance obligations owed by the delinquent mortgage loan borrower. While increased delinquencies generate higher ancillary revenues, including late fees, these fees are likely not sufficient to offset the increased cost of servicing the loans. An increase in delinquencies could therefore be detrimental to our business. Recently, financial markets have experienced significant volatility. There may be a significant increase in the rate and number of mortgage payment delinquencies, and house sales, home prices and multifamily fundamentals may be adversely affected, which could lead to a material adverse decrease of our mortgage origination activities.

Any of the circumstances described above, alone or in combination, could lead to volatility in or disruption of the credit markets at any time and have a detrimental effect on our business. For additional information on macroeconomic and U.S. residential real estate market conditions, please consider the matters addressed in the section below entitled “—The COVID-19 pandemic and the actions taken by local, state and federal governments have and are expected to continue to adversely affect the national economy and the macroeconomic environment which could adversely affect our current operations and our ability to continue to grow.”

Our financial performance is directly affected by, and subject to substantial volatility from changes in prevailing interest rates.

Our financial performance is directly affected by, and subject to substantial volatility from changes in prevailing interest rates. During 2022, in order to address rising inflation, the Federal Reserve began to aggressively raise interest rates. As a result, mortgage interests have significantly increased which has significantly adversely affected the volume of refinancings and new mortgage originations. Rising interest rates and inflation will likely decrease the demand for new mortgage originations and refinancings and increase competition for borrowers. This has and is expected to continue to adversely pressure our margins origination volumes, especially our refinance volume.

With regard to the portion of our business that is centered on refinancing existing mortgages, generally, the refinance market experiences more significant fluctuations than the purchase market as a result of interest rate changes. As interest rates rise, refinancing, has and is expected to continue to generally become a smaller portion of the market as fewer consumers are interested in refinancing their mortgages. With regard to our purchase mortgage loan business, higher interest rates may also reduce demand for purchase mortgages as home ownership becomes more expensive. This has and is expected to continue to adversely affect our revenues or require us to increase marketing expenditures in an attempt to increase or maintain our volume of mortgages.