As filed with the Securities and Exchange Commission on June 4, 2024

Registration No. 333-277066

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 2 to

FORM

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

(Exact Name of Registrant as Specified in its Charter)

| 2834 | 83-2262816 | |||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

201 E. Fifth Street, Suite 1900

Cincinnati, Ohio 45202

Telephone: (513) 620-4101

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Bruce Harmon

Chief Financial Officer

201 E. Fifth Street, Suite 1900

Cincinnati, Ohio 45202

Telephone: (513) 620-4101

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

with copies to:

Barry I. Grossman, Esq.

Jessica Yuan, Esq.

Ellenoff Grossman & Schole LLP

1345 Avenue of the Americas

New York, NY 10105

Phone: (212) 370-1300

Fax: (212) 370-7889

Approximate date of commencement of proposed sale to the public: From time to time after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||

| ☒ | Smaller reporting company | |||||

| Emerging growth company |

If an emerging growth company,

indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial

accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission acting pursuant to said Section 8(a), may determine.

EXPLANATORY NOTE

Pursuant to Rule 429 under the Securities Act of 1933, as amended (the “Securities Act”), the prospectus included in this Registration Statement on Form S-1 (this “Registration Statement”) is a combined prospectus relating to the following shares of common stock of Onconetix, Inc. (the “Registrant”) being registered on this Registration Statement and previously registered on the Registrant’s Registration Statement on Form S-3 (File No. 333-267142), as amended (the “Prior Registration Statement”):

| ● | The offer and resale of 4,972,428 shares of Common Stock (the “Inducement PIO Shares”) issuable upon exercise of common stock preferred investment options (the “Inducement PIOs”) issued to Armistice Capital Master Fund Ltd. (“Armistice”) in a warrant inducement transaction (the “Warrant Inducement”), which closed on August 2, 2023. |

| ● | The offer and resale of 149,173 Inducement PIO Shares issuable upon exercise of Inducement PIOs issued to H.C. Wainwright & Co., LLC, the Company’s placement agent for the Warrant Inducement, or its designees on August 2, 2023 in the Warrant Inducement (the “Placement Agent Inducement PIOs”). |

| ● | The offer and resale of 2,486,214 shares of Common Stock issuable upon exercise of common stock preferred investment options (the “Sabby PIOs”, and together with the Inducement PIOs and the Placement Agent Inducement PIOs, the “PIOs”) issued to Sabby in a private placement, which were registered on a registration statement on Form S-1 (File No. 333-267142) on September 19, 2022 that was declared effective by the SEC, as amended by the Prior Registration Statement (the “Initial Registration Statement”) |

| ● | The offer and resale of 220,997 shares of Common Stock (“August 2022 Wainwright Warrant Shares”) issuable upon exercise of the warrants (the “August 2022 Wainwright Warrants”) issued to H.C. Wainwright & Co., LLC, or its designees, in a private placement, which were registered on the Initial Registration Statement. |

This Registration Statement also constitutes Post-Effective Amendment No. 2 to the Prior Registration Statement, and such Post-Effective Amendment No. 1 to the Initial Registration Statement shall hereafter become effective concurrently with the effectiveness of this Registration Statement in accordance with Section 8(c) of the Securities Act.

The information in this prospectus is not complete and may be changed. The Selling Stockholders named in this prospectus may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

| PROSPECTUS | SUBJECT TO COMPLETION | DATED JUNE 4, 2024 |

7,828,812 Shares of Common Stock

This prospectus relates to the resale by Selling Stockholders of 7,828,812 shares of common stock of Onconetix, Inc. (“we,” “us,” “our,” the “Company,” or “Onconetix”), par value $0.00001 per share (the “Common Stock”), by the Selling Stockholders listed in this prospectus or their permitted transferees (the “Selling Stockholders”). The shares of Common Stock registered for resale pursuant to this prospectus include:

| ● | 4,972,428 shares of Common Stock (the “Inducement PIO Shares”) issuable upon exercise of common stock preferred investment options (the “Inducement PIOs”) issued to Armistice Capital Master Fund Ltd. (“Armistice”) in a warrant inducement transaction (the “Warrant Inducement”), which closed on August 2, 2023; |

| ● | 149,173 Inducement PIO Shares issuable upon exercise of Inducement PIOs issued to H.C. Wainwright & Co., LLC, the Company’s placement agent for the Warrant Inducement, or its designees on August 2, 2023 in the Warrant Inducement (the “Placement Agent Inducement PIOs”); |

| ● | 2,486,214 shares of Common Stock issuable upon exercise of common stock preferred investment options (the “Sabby PIOs”, and together with the Inducement PIOs and the Placement Agent Inducement PIOs, the “PIOs”) issued to Sabby in the August 2022 Private Placement; and |

| ● | 220,997 shares of Common Stock (“August 2022 Wainwright Warrant Shares”) issuable upon exercise of the warrants (the “August 2022 Wainwright Warrants”) issued to H.C. Wainwright & Co., LLC, or its designees, in the August 2022 Private Placement. |

For additional information about the Warrant Inducement and the Private Placement, see “Warrant Inducement and Private Placement.”

The Inducement PIOs have an exercise price of $1.09 per share and will expire five years from the issuance date. The Placement Agent Inducement PIOs have an exercise price of $1.3625 per share and will expire five years from the issuance date. The Sabby PIOs have an exercise price of $2.546 per share and will expire five years from the issuance date.

We are registering the shares on behalf of the Selling Stockholders, to be offered and sold by them from time to time. We are not selling any securities under this prospectus and will not receive any of the proceeds from the sale of shares by the Selling Stockholders.

Our common stock is listed on The Nasdaq Capital Market under the symbol “ONCO.” The last reported sale price of our common stock on The Nasdaq Capital Market on May 30, 2024 was $0.238 per share. We recommend that you obtain current market quotations for our common stock prior to making an investment decision.

The Selling Stockholders may offer all or part of the shares for resale from time to time through public or private transactions, at either prevailing market prices or at privately negotiated prices. Our registration of the shares of common stock covered by this prospectus does not mean that the Selling Stockholders will offer or sell any of the shares. With regard only to the shares the Selling Stockholders sell for their own behalf, the Selling Stockholders may be deemed an “underwriter” within the meaning of the Securities Act of 1933, as amended (the “Securities Act”). The Company has paid all of the registration expenses incurred in connection with the registration of the shares. We will not pay any of the selling commissions, brokerage fees and related expenses.

We will pay the expenses incurred in registering the shares, including legal and accounting fees. See “Plan of Distribution” on page 155 of this prospectus.

Investing in our Common Stock involves certain risks. See “Risk Factors” on page 5 of this prospectus, included in any accompanying prospectus supplement and in the documents incorporated by reference in this prospectus for a discussion of the factors you should carefully consider before deciding to purchase these securities.

We may amend or supplement this prospectus from time to time by filing amendments or supplements as required. We urge you to read the entire prospectus, any amendments or supplements, any free writing prospectuses, and any documents incorporated by reference carefully before you make your investment decision.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2024

TABLE OF CONTENTS

i

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form S-1 that we filed with the Securities and Exchange Commission (the “SEC”) using a “shelf” registration process for the delayed or continuous offering and sale of securities pursuant to Rule 415 under the Securities Act of 1933, as amended (the “Securities Act”). This prospectus generally describes Onconetix, Inc. and our Common Stock. The Selling Stockholders may use the shelf registration statement to sell up to an aggregate of up to 7,828,812 shares of our Common Stock from time to time through any means described in the section entitled “Plan of Distribution.”

We will not receive any proceeds from the sale of shares of Common Stock to be offered by the Selling Stockholders pursuant to this prospectus. However, we will pay the expenses, other than underwriting discounts and commissions, associated with the sale of shares pursuant to this prospectus.

We and the Selling Stockholders, as applicable, may deliver a prospectus supplement with this prospectus, to the extent appropriate, to update the information contained in this prospectus. The prospectus supplement may also add, update or change information included in this prospectus. You should read both this prospectus and any applicable prospectus supplement, together with additional information described below under the captions “Where You Can Find More Information” and “Incorporation of Certain Information by Reference.”

No offer of these securities will be made in any jurisdiction where the offer is not permitted.

You should rely only on the information contained in or incorporated by reference in this prospectus, any accompanying prospectus supplement or in any related free writing prospectus filed by us with the SEC. We have not authorized anyone to provide you with different information. This prospectus and any accompanying prospectus supplement do not constitute an offer to sell or the solicitation of an offer to buy any securities other than the securities described in this prospectus or such accompanying prospectus supplement or an offer to sell or the solicitation of an offer to buy such securities in any circumstances in which such offer or solicitation is unlawful. You should assume that the information appearing in this prospectus, any prospectus supplement, the documents incorporated by reference and any related free writing prospectus is accurate only as of their respective dates. Our business, financial condition, results of operations and prospects may have changed materially since those dates.

Unless the context otherwise indicates, references in this prospectus to “we,” “our” and “us” refer, collectively, to Onconetix, Inc., a Delaware corporation.

ii

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains “forward-looking statements” within the meaning of the federal securities laws, and that involve significant risks and uncertainties. Words such as “may,” “should,” “could,” “would,” “predicts,” “potential,” “continue,” “expects,” “anticipates,” “future,” “intends,” “plans,” “believes,” “estimates,” and similar expressions, as well as statements in future tense, identify forward-looking statements. Forward-looking statements should not be read as a guarantee of future performance or results and may not be accurate indications of when such performance or results will be achieved. Forward-looking statements are based on information we have when those statements are made or management’s good faith belief as of that time with respect to future events and are subject to significant risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking statements. Forward-looking statements are subject to a number of risks, uncertainties and assumptions in other documents we file from time to time with the SEC, specifically our most recent Annual Report on Form 10-K, our Quarterly Reports on Form 10-Q and our Current Reports on Form 8-K.

Important factors that could cause such differences include, but are not limited to:

| ● | our projected financial position and estimated cash burn rate; |

| ● | our estimates regarding expenses, future revenues and capital requirements; |

| ● | our ability to continue as a going concern; |

| ● | our need to raise substantial additional capital to fund our operations; |

| ● | our ability to commercialize or monetize ENTADFI and Proclarix and integrate the assets and commercial operations acquired in the share exchange with Proteomedix AG (“Proteomedix”); |

| ● | the successful development of our commercialization capabilities, including sales and marketing capabilities. |

| ● | our ability to obtain and maintain the necessary regulatory approvals to market and commercialize our products; |

| ● | the results of market research conducted by us or others; |

| ● | our ability to obtain and maintain intellectual property protection for our current products; |

| ● | our ability to protect our intellectual property rights and the potential for us to incur substantial costs from lawsuits to enforce or protect our intellectual property rights; |

| ● | the possibility that a third party may claim we or our third-party licensors have infringed, misappropriated, or otherwise violated their intellectual property rights and that we may incur substantial costs and be required to devote substantial time defending against claims against us; |

iii

| ● | our reliance on third parties, including manufacturers and logistics companies; |

| ● | the success of competing therapies or diagnostics and products that are or become available; |

| ● | our ability to successfully compete against current and future competitors; |

| ● | our ability to expand our organization to accommodate potential growth and our ability to attract, motivate and retain key personnel; |

| ● | the potential for us to incur substantial costs resulting from product liability lawsuits against us and the potential for these product liability lawsuits to cause us to limit our commercialization of our products; |

| ● | market acceptance of our products, the size and growth of the potential markets for our current products, and our ability to serve those markets; and |

| ● | disruptions in the business of the Company or Proteomedix, which could have an adverse effect on their respective businesses and financial results. |

These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including those described in “Risk Factors.” Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In light of these risks, uncertainties and assumptions, the forward-looking events and circumstances discussed in this prospectus may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements.

You should not rely upon forward-looking statements as predictions of future events. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee that the future results, levels of activity, performance or events and circumstances reflected in the forward-looking statements will be achieved or occur. Moreover, except as required by law, neither we nor any other person assumes responsibility for the accuracy and completeness of the forward-looking statements. We undertake no obligation to update publicly any forward-looking statements for any reason after the date of this prospectus to conform these statements to actual results or to changes in our expectations.

You should read this prospectus and the documents that we reference in this prospectus and have filed with the SEC as exhibits to the registration statement of which this prospectus forms a part with the understanding that our actual future results, levels of activity, performance and events and circumstances may be materially different from what we expect.

iv

SUMMARY OF MATERIAL RISKS ASSOCIATED WITH OUR BUSINESS

The following is a summary of certain risks, uncertainties and other factors related to our company. These do not represent all of the risks we face. You should carefully consider all of the risk factors presented in “Risk Factors” and all other information contained in this prospectus, including the financial statements in order to provide a more complete picture of the risk factors we face.

Our business is subject to a number of risks, including risks that may prevent us from achieving our business objectives or may adversely affect our business, financial condition, results of operations, cash flows and prospects that you should consider before making a decision to invest in our common stock. These risks are discussed more fully in “Risk Factors” beginning on page 5 of this prospectus. These risks include, but are not limited to, the following:

| ● | Sales of a substantial number of our securities in the public market by the selling securityholders and/or by our existing securityholders could cause the price of our shares of Common Stock to fall. |

| ● | We have a very limited operating history, which may make it difficult for you to evaluate the success of our business to date and to assess our future viability. |

| ● | We have incurred significant net losses since inception, have only generated minimal revenue, and anticipate that we will continue to incur substantial net losses for the foreseeable future and may never achieve profitability. Our stock is a highly speculative investment. |

| ● | There is substantial doubt about our ability to continue as a “going concern,” and we will require substantial additional funding to finance our long-term operations. If we are unable to raise additional capital when needed, we could be forced to delay, reduce or terminate certain of our products or other operations. |

| ● | We owe a significant amount of money to Veru, which funds we do not have. Veru may take action against us to enforce its rights to payment in the future, which could have a material adverse effect on us and our operations. |

| ● | Our current liabilities are significant, and if those to whom we owe accounts payable, such as Veru, IQVIA or other creditors or vendors, were to demand payment, we would be unable to pay. |

| ● | We may consider strategic alternatives in order to maximize stockholder value, including financing, strategic alliances, licensing arrangements, acquisitions or the possible sale of our business. We may not be able to identify or consummate any suitable strategic alternatives and any consummated strategic alternatives may not be successful. |

| ● | Raising additional capital may cause dilution to our existing stockholders and investors, restrict our operations, or require us to relinquish rights to our products on unfavorable terms to us. |

| ● | Due to the significant resources required for the commercialization of our products, and depending on our ability to access capital, we must prioritize commercialization of certain products. Moreover, we may expend our limited resources on products that do not yield a successful product and fail to capitalize on products that may be more profitable or for which there is a greater likelihood of success. |

| ● | As a result of our failure to timely file our Quarterly Report on Form 10-Q for the quarter ended June 30, 2023, we are currently ineligible to file new short form registration statements on Form S-3, which may impair our ability to raise capital on terms favorable to us, in a timely manner or at all. |

| ● | We depend entirely on the success of a limited number of products. If we do not successfully commercialize our products or we experience significant delays in doing so, these products may not be profitable. |

| ● | Obtaining and maintaining regulatory approval of our products in one jurisdiction does not mean that we will be successful in obtaining regulatory approval in other jurisdictions. |

| ● | Proclarix is subject to competition from other prostate cancer diagnostics and larger, well-established companies with substantially greater resources than us. |

| ● | ENTADFI is subject to competition from other BPH drugs and larger, well-established companies with substantially greater resources than us. |

| ● | We may not be able to successfully grow sales of ENTADFI in the U.S. market and Proclarix in the European markets or, if authorized, grow sales of either in any other market. |

| ● | There can be no assurance that we will be able to comply with the continued listing standards of Nasdaq. |

v

PROSPECTUS SUMMARY

The SEC allows us to “incorporate by reference” certain information that we file with the SEC, which means that we can disclose important information to you by referring you to those documents. The information incorporated by reference is considered to be part of this prospectus, and information that we file later with the SEC will update automatically, supplement and/or supersede the information disclosed in this prospectus. Any statement contained in a document incorporated or deemed to be incorporated by reference in this prospectus shall be deemed to be modified or superseded for purposes of this prospectus to the extent that a statement contained in this prospectus or in any other document that also is or is deemed to be incorporated by reference in this prospectus modifies or supersedes such statement. Any such statement so modified or superseded shall not be deemed, except as so modified or superseded, to constitute a part of this prospectus. You should read the following summary together with the more detailed information regarding our company, our Common Stock and our financial statements and notes to those statements included in this prospectus.

Our Company

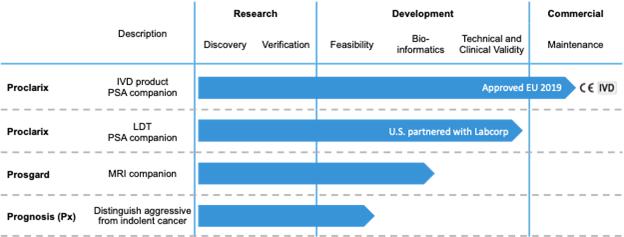

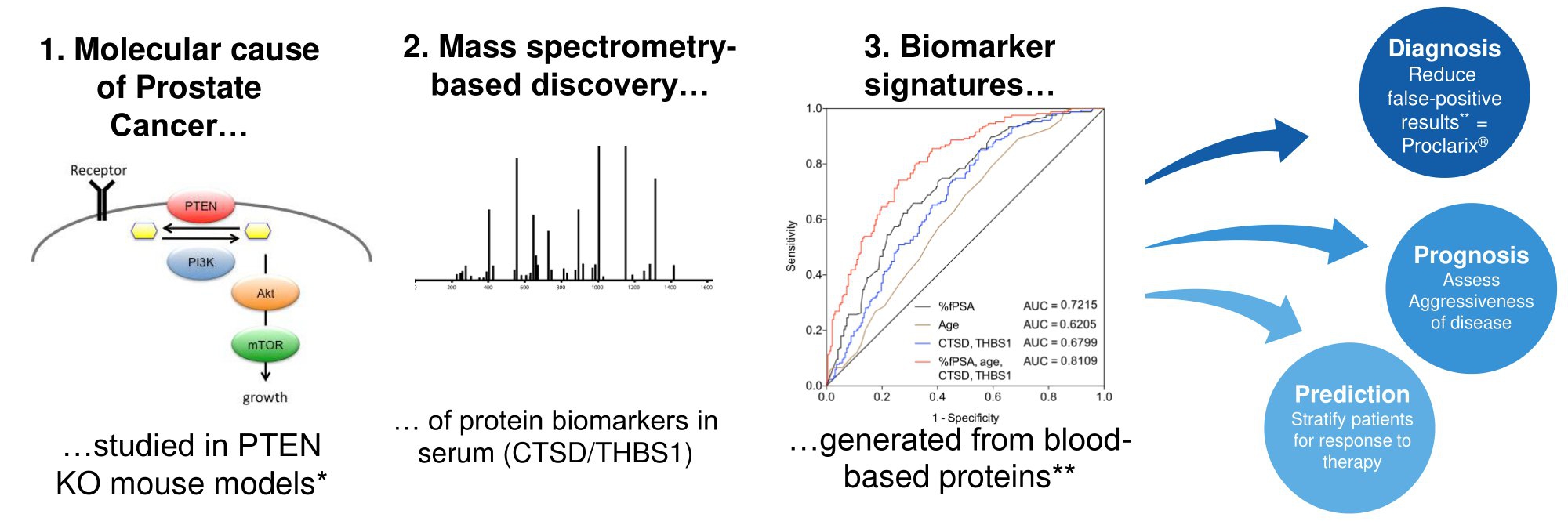

We are a commercial stage biotechnology company focused on the research, development, and commercialization of innovative solutions for men’s health and oncology. Through our recent acquisition of Proteomedix, we own Proclarix, an in vitro diagnostic test for prostate cancer originally developed by Proteomedix and approved for sale in the European Union under the In Vitro Diagnostic Regulation (“IVDR”), which we anticipate will be marketed in the U.S. as a lab developed test (“LDT”) through our license agreement with Labcorp. We also own ENTADFI, an FDA-approved, once daily pill that combines finasteride and tadalafil for the treatment of BPH, a disorder of the prostate.

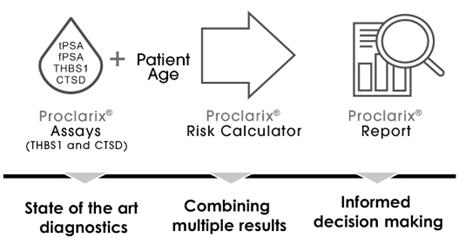

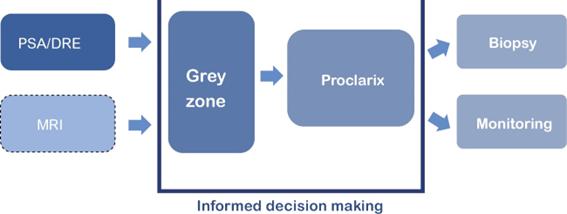

Proclarix is an easy-to-use next generation protein-based blood test that can be done with the same sample as a patient’s regular Prostate-Specific Antigen (“PSA”) test. The PSA test is a well-established prostate specific marker that measures the concentration of PSA molecules in a blood sample. A high level of PSA can be a sign of prostate cancer. However, PSA levels can also be elevated for many other reasons including infections, prostate stimulation, vigorous exercise, or even certain medications. PSA results can be confusing for many patients and even physicians. It is estimated over 50% of biopsies with elevated PSA are negative or clinically insignificant resulting in an overdiagnosis and overtreatment that impacts the physician’s routine, our healthcare system, and the quality of patients’ lives. Approximately 10% of all men have elevated PSA levels, commonly referred to as the diagnostic “grey zone”, of which only 20 – 40% present clinically with cancer. Proclarix is intended for use in diagnosing these patients where it is difficult to decide if a biopsy is necessary to verify a potential clinically significant cancer diagnosis.

Proclarix helps doctors and patients with unclear PSA test results through the use of our proprietary Proclarix Risk Score which delivers clear and immediate diagnostic support for further treatment decisions. No additional intervention is required, and results are available quickly. Local diagnostic laboratories can integrate this multiparametric test into their current workflow because Proclarix assays use the enzyme-linked immunosorbent assay (“ELISA”) standard, which most diagnostic laboratories are already equipped to process.

ENTADFI allows men to receive treatment for their symptoms of BPH without the negative sexual side effects typically seen in patients on finasteride alone. Following a recent business strategy shift towards the field of men’s health and oncology and deprioritizing of preclinical vaccine programs, we are building additional assets in therapeutics, diagnostics, and clinician services for men’s health and oncology.

Since our inception in October 2018 until April 2023, when we acquired ENTADFI, we devoted substantially all of our resources to performing research and development, undertaking preclinical studies and enabling manufacturing activities in support of our product development efforts, hiring personnel, acquiring and developing our technology and now deprioritized vaccine candidates, organizing and staffing our company, performing business planning, establishing our intellectual property portfolio and raising capital to support and expand such activities.

1

Prior to the acquisition of ENTADFI, we managed one distinct business segment, which was research and development. Beginning in the second quarter of 2023, as a result of the acquisition of ENTADFI, we operated in two business segments: research and development and commercial. During the third quarter of 2023, we deprioritized our vaccine discovery and development programs, and accordingly, we now operate in one segment: commercial. Our recent acquisition of Proteomedix during the fourth quarter of 2023 and its related diagnostic product Proclarix was determined to be within our commercial segment. The research and development segment was our historical business, and was dedicated to the research and development of various vaccines to prevent infectious diseases. The commercial segment was new in the second quarter of 2023 and is dedicated to the commercialization of our products approved for sale, namely ENTADFI in the U.S. and Proclarix in Europe.

ENTADFI has not generated any revenue from product sales, and Proclarix has generated only minimal amounts of development revenue since its acquisition.

On December 15, 2023, the Company closed its acquisition of Proteomedix and introduced Onconetix, Inc. as the new name for the combined company. The closing of the acquisition of Proteomedix for all stock consideration provides Proteomedix shareholders with an initial 16.4% ownership stake of Onconetix, and Series B Preferred Stock convertible into 269,672,900 shares of Onconetix Common Stock, subject to Onconetix stockholder approval of the same (“Stockholder Approval”).

It is anticipated that, following the conversion of Series B Preferred Stock upon stockholder approval and the closing of an investment by Altos Ventures, a former shareholder of Proteomedix (the “PMX Investor”), the former holders of capital stock of Proteomedix will own approximately 87.2% of the outstanding equity interests of Onconetix, the PMX Investor will own approximately 7.5% of the outstanding equity interests of Onconetix, and the stockholders of Onconetix immediately prior to the acquisition of Proteomedix will own approximately 5.3% of the outstanding equity interests of Onconetix.

In light of (i) the time and resources needed to continue pursuing commercialization of ENTADFI, and (ii) the Company’s cash runway and indebtedness, the Company has determined to pause its commercialization of ENTADFI, as it considers strategic alternatives. As part of a cost reduction plan approved by the Board and in connection with our pause in commercializing ENTADFI, we terminated three employees involved with the ENTADFI program, effective April 30, 2024, with such individuals to continue assisting the Company on an as-needed, consulting basis. The Company continues to consider various measures, including strategic alternatives, to rationalize its operations and optimize its existing Proclarix diagnostic program.

We are currently focusing our efforts on commercializing Proclarix.

Proclarix was first CE marked under the IVD Directive in Europe in January 31, 2019. On October 7, 2022, Proclarix gained CE marking under the IVDR and was registered in the United Kingdom and Switzerland under applicable regulations. Given Proclarix is CE-marked for sale in the European Union, we expect to generate revenue from sales of Proclarix by 2025. Although we anticipate these sales to offset some expenses relating to commercial scale up and development, we expect our expenses will increase substantially in connection with our ongoing activities, as we:

| ● | commercialize Proclarix; |

| ● | hire additional personnel; |

| ● | operate as a public company; and |

| ● | obtain, maintain, expand and protect our intellectual property portfolio. |

2

To the extent that we resume the commercialization of ENTADFI, we also expect to incur significant commercialization expenses related to marketing, manufacturing, and distribution for ENTADFI. We rely and will continue to rely on third parties for the manufacturing of ENTADFI and Proclarix. We have no internal manufacturing capabilities, and we will continue to rely on third parties, of which the main suppliers are single-source suppliers, for commercial products.

We do not have any products approved for sale, aside from Proclarix in the EU, from which we have generated only minimal amounts of development revenue since its acquisition, and ENTADFI, from which we have not generated any revenue from product sales, and for which we have determined to pause commercialization activities. To date, we have financed our operations primarily with proceeds from our sale of preferred securities to seed investors, the initial public offering (“IPO”), the April 2022 Private Placement (as defined below), the August 2022 Private Placement (as defined below), the proceeds received from a warrant exercise in August 2023, and the proceeds received from the issuance of debt in January 2024. We will continue to require significant additional capital to commercialize Proclarix and ENTADFI (if we decide to resume its commercialization), and to fund operations for the foreseeable future. Accordingly, until such time as we can generate significant revenue, if ever, we expect to finance our cash needs through public or private equity or debt financings, third-party (including government) funding and to rely on third-party resources for marketing and distribution arrangements, as well as other collaborations, strategic alliances and licensing arrangements, or any combination of these approaches, to support our operations.

We have incurred net losses since inception and expect to continue to incur net losses in the foreseeable future. Our net losses may fluctuate significantly from quarter-to-quarter and year-to-year, depending in large part on the timing of our preclinical studies, clinical trials and manufacturing activities, our expenditures on other research and development activities and commercialization activities. As of December 31, 2023, the Company had a working capital deficit of approximately $11.4 million and an accumulated deficit of approximately $56.8 million. We will need to raise additional capital within the next 12 months to sustain operations. In addition, if Stockholder Approval is not obtained by January 1, 2025, the Company may be obligated to cash settle the Series B Preferred Stock. Based on the closing price of $0.238 for the Company’s stock as of May 30, 2024, the Series B Preferred Stock would be redeemable for approximately $64.2 million.

Until we generate revenue sufficient to support self-sustaining cash flows, if ever, we will need to raise additional capital to fund our continued operations, including our product development and commercialization activities related to our current and future products. There can be no assurance that additional capital will be available to us on acceptable terms, or at all, or that we will ever generate revenue sufficient to provide self-sustaining cash flows. These circumstances raise substantial doubt about our ability to continue as a going concern. The accompanying consolidated financial statements of Onconetix included elsewhere in this prospectus do not include any adjustment that might be necessary if the Company is unable to continue as a going concern.

Because of the numerous risks and uncertainties associated with our business, we are unable to predict the timing or amount of increased expenses or when or if we will be able to achieve or maintain profitability. Additionally, even if we are able to generate revenue from Proclarix or ENTADFI, we may not become profitable. If we fail to become profitable or are unable to sustain profitability on a continuing basis, then we may be unable to continue our operations at planned levels and may be forced to reduce our operations.

3

ABOUT THIS OFFERING

| Common Stock outstanding prior to this offering | 22,327,701 shares | |

| Shares of Common Stock offered by the Selling Stockholders | 7,828,812 shares of Common Stock | |

| Common Stock to be outstanding after this offering | 30,156,513 shares (assuming the exercise of the PIOs) | |

| Use of proceeds | We are not selling any securities under this prospectus and will not receive any of the proceeds from the sale of the shares of Common Stock covered hereby by the Selling Stockholders. | |

| Terms of this offering | The Selling Stockholders, including their transferees, donees, pledgees, assignees, and successors-in-interest, may sell, transfer, or otherwise dispose of any or all of the shares of Common Stock offered by this prospectus from time to time on The Nasdaq Capital Market or any other stock exchange, market or trading facility on which the shares are traded or in private transactions. The shares of Common Stock may be sold at fixed prices, at market prices prevailing at the time of sale, at prices related to prevailing market price or at negotiated prices. | |

| Nasdaq symbol | Our Common Stock is listed on The Nasdaq Capital Market under the symbol “ONCO.” | |

| Risk Factors | Investing in our securities involves significant risks. Before making a decision whether to invest in our securities, please read the information contained in or incorporated by reference under the heading “Risk Factors” in this prospectus, the documents we have incorporated by reference herein and under similar headings in other documents filed after the date hereof and incorporated by reference into this prospectus. See “Incorporation of Certain Information by Reference” and “Where You Can Find More Information.” |

4

RISK FACTORS

Investing in our securities involves a high degree of risk. You should carefully consider the risks and uncertainties described in this prospectus, in our most recent Annual Report on Form 10-K, as supplemented and updated by subsequent Quarterly Reports on Form 10-Q and Current Reports on Form 8-K that we have filed or will file with the SEC, and in other documents which are incorporated by reference into this prospectus, before making an investment decision pursuant to this.

Our business, financial condition and results of operations could be materially and adversely affected by any or all of these risks or by additional risks and uncertainties not presently known to us or that we currently deem immaterial that may adversely affect us in the future.

Risks Related to This Offering

Sales of a substantial number of our securities in the public market by the selling securityholders and/or by our existing securityholders could cause the price of our shares of Common Stock to fall.

The selling securityholders can sell, under this prospectus, up to 7,828,812 shares of Common Stock. The sale of all or a portion of the securities being offered in this prospectus, or the perception that those sales might occur, could depress the market price of our Common Stock, and could impair our ability to raise capital through the sale of additional equity securities. We are unable to predict the effect that such sales may have on the prevailing market price of our Common Stock.

Risks Related to our Financial Position and Need for Capital

We have a very limited operating history, which may make it difficult for you to evaluate the success of our business to date and to assess our future viability.

To date, we have devoted substantially all of our resources to performing research and development, hiring personnel, licensing and developing our technology, organizing and staffing our company, performing business planning, establishing our intellectual property portfolio, potential asset and business acquisitions, expenditures associated with the now paused commercial launch of ENTADFI, and raising capital to support and expand such activities. As an organization, we have not yet demonstrated an ability to successfully manufacture a commercial-scale product or conduct sales and marketing activities necessary for successful commercialization or arrange for a third party to conduct these activities on our behalf. Consequently, any predictions about our future success or viability may not be as accurate as they could be if we had a longer operating history.

We may encounter unforeseen expenses, difficulties, complications, delays and other known or unknown factors in achieving our business objectives, including with respect to our products. We are in the process of transitioning from a company with a research and development focus to a company capable of supporting commercial activities and may not be successful in such a transition.

We have incurred significant net losses since inception, have only generated minimal revenue, and anticipate that we will continue to incur substantial net losses for the foreseeable future and may never achieve profitability. Our stock is a highly speculative investment.

We are a commercial-stage biotechnology company that was incorporated in October 2018. Our net loss was $11.1 million for the three months ended March 31, 2024, and $37.4 million and $13.4 million for the years ended December 31, 2023, and 2022, respectively. As of March 31, 2024, we had an accumulated deficit of $67.9 million, and as of December 31, 2023, we had an accumulated deficit of $56.8 million. We also generated negative operating cash flows of $5.2 million for the three months ended March 31, 2024, and negative operating cash flows of $13.6 million for the year ended December 31, 2023.

We expect to continue to spend significant resources to commercialize our product. We expect to incur substantial and increasing operating losses over the next several years. As a result, our accumulated deficit will also increase significantly. Additionally, there can be no assurance that our current products or those that may be under development by us in the future will be commercially viable. If we are unable to achieve profitability or raise sufficient working capital, we may be unable to continue our operations.

5

There is substantial doubt about our ability to continue as a “going concern,” and we will require substantial additional funding to finance our long-term operations. If we are unable to raise additional capital when needed, we could be forced to delay, reduce or terminate certain of our products or other operations.

The Company has incurred substantial operating losses since inception and expects to continue to incur significant operating losses for the foreseeable future. As of March 31, 2024, the Company had cash of approximately $4.5 million, a working capital deficit of approximately $15.1 million and an accumulated deficit of approximately $67.9 million. In addition, as of May 15, 2024, the Company’s cash balance was approximately $1.9 million. As of December 31, 2023, the Company had cash of approximately $4.6 million, a working capital deficit of approximately $11.4 million and an accumulated deficit of approximately $56.8 million.

On January 23, 2024, the Company issued the Altos Debenture in exchange for $4.6 million in net cash proceeds. The Altos Debenture, as amended on April 24, 2024, is repayable in full upon the earlier of (i) the closing under the Subscription Agreement and (ii) October 31, 2024.

Additionally, pursuant to our Forbearance Agreement with Veru (see About the Company - Recent Acquisitions – ENTADFI), until March 31, 2025, we are obligated to pay Veru 15% of (i) the monthly cash receipts of Proteomedix for the licensing or sale of any products or services, (ii) monthly cash receipts of the Company or any of its subsidiaries for the sales of Proclarix anywhere in the world, and (iii) monthly cash receipts of the Company or any of its subsidiaries for milestone payments or royalties from Labcorp. Any payments that we are required to make to Veru will detract from our ability to support our operations.

We estimate, as of the date of the financial statements included in this prospectus, that our current cash balance is only sufficient to fund our operations into the third quarter of 2024. We believe that we will need to raise substantial additional capital to fund our continuing operations, satisfy existing and future obligations and liabilities, and otherwise support the Company’s working capital needs and business activities, including making the remaining payments to Veru and the commercialization of Proclarix. In addition, if Stockholder Approval is not obtained by January 1, 2025, the Company may be obligated to cash settle the Series B Preferred Stock. The Company does not currently have sufficient cash to redeem the shares of Series B Preferred Stock. Based on the closing price of $0.238 for the Company’s stock as of May 30, 2024, the Series B Preferred Stock would be redeemable for approximately $64.2 million. We also do not currently have sufficient cash to make the remaining payments to Veru. Management’s plans include generating product revenue from sales of Proclarix, which may still be subject to further successful commercialization activities within certain jurisdictions. In addition, the Company has paused commercialization activities for ENTADFI and it is exploring strategic alternatives for its monetization, such as a potential sale of the ENTADFI assets. Management’s plans also include attempting to secure additional required funding through equity or debt financings if available. However, there are currently no commitments in place for further financing nor is there any assurance that such financing will be available to the Company on favorable terms, if at all. If the Company is unable to secure additional capital, it may be required to delay or curtail any future commercialization of products, and it may take additional measures to reduce expenses in order to conserve its cash in amounts sufficient to sustain operations and meet its obligations. These conditions raise substantial doubt about the Company’s ability to continue as a going concern for a period of time within one year from the issuance of the condensed consolidated financial statements included in this prospectus. Our future capital requirements will depend on many factors, including:

| ● | the costs of future commercialization activities, including product manufacturing, marketing, sales, royalties and distribution, for Proclarix, and ENTADFI (if we decide to resume its commercialization), and other products for which we have received or will receive marketing approval; |

| ● | the cost of redeeming our Series B Preferred Stock, if stockholder approval is not obtained by January 1, 2025; |

| ● | our ability to maintain existing, and establish new, strategic collaborations, licensing or other arrangements and the financial terms of any such agreements, including the timing and amount of any future milestone, royalty, or other payments due under any such agreement; |

| ● | any product liability or other lawsuits related to our products; |

| ● | the expenses needed to attract, hire, and retain skilled personnel; |

| ● | the revenue, if any, received from commercial sales of Proclarix and ENTADFI (if we decide to resume its commercialization), or other products for which we may receive marketing approval; |

| ● | the costs to establish, maintain, expand, enforce, and defend the scope of our intellectual property portfolio, including the amount and timing of any payments we may be required to make, or that we may receive, in connection with licensing, preparing, filing, prosecuting, defending, and enforcing our patents or other intellectual property rights; and |

| ● | the costs of operating as a public company. |

Our ability to raise additional funds will depend on financial, economic, and other factors, many of which are beyond our control. We cannot be certain that additional funding will be available on acceptable terms, or at all. We have no committed source of additional capital and if we are unable to raise additional capital in sufficient amounts or on terms acceptable to us, we may be forced to delay, reduce or terminate our business activities.

6

We owe a significant amount of money to Veru, which funds we do not have. Veru may take action against us to enforce its rights to payment in the future, which could have a material adverse effect on us and our operations.

Due to recent financial constraints, the Company may be unable to timely pay amounts due to Veru, from whom we purchased ENTADFI in April 2023. We may not have sufficient funds to pay amounts due to Veru in the near term, if at all, including but not limited to $10 million, $5 million of which was due on April 19, 2024 and is subject to certain forbearance terms (see About the Company- Recent Acquisitions – ENTADFI), and $5 million is due on September 30, 2024. On April 24, 2024, Veru agreed to forbear its rights and remedies until March 31, 2025 with respect to, among other things, our inability to pay amounts due as of April 19, 2024. However, Veru may take future action against us, including filing legal proceedings against us seeking amounts due and interest accrued or attempting to terminate its relationship with us. If Veru were to take legal action against us, we may be forced to scale back our business plan and/or seek bankruptcy protection. We may be subject to litigation and damages for our failure to pay amounts due to Veru, and may be forced to pay interest and penalties, which funds we do not currently have. We are currently considering strategic options for ENTADFI, including a potential sale, and plan to seek funding to support our operations, and to pay amounts due to Veru, through a combination of equity offerings, debt financing or other capital sources, including potential collaborations, licenses, sales, and other similar arrangements, which may not be available on favorable terms, if at all. The sale of additional equity or debt securities, if accomplished, may result in dilution to our stockholders. Furthermore, any revenue or financing proceeds that we are required to pay to Veru will detract from our ability to use such funds to support our operations.

Our current liabilities are significant, and if those to whom we owe accounts payable, such as Veru, IQVIA or other creditors or vendors, were to demand payment, we would be unable to pay.

As of March 31, 2024, we had total current liabilities of approximately $21.4 million, including accounts payable of approximately $4.3 million, accrued expenses of approximately $1.9 million, and approximately $15.2 million (net of discounts) related to notes payable, primarily due to Veru and the debenture due to the PMX Investor. As of the same date, we had cash of only $4.5 million. As of December 31, 2023, we had total current liabilities of approximately $17.2 million, including accounts payable of approximately $5.3 million, accrued expenses of approximately $2.2 million, and approximately $9.6 million (net of discount) related to the notes payable due to Veru. As of the same date, we had cash of only $4.6 million. As our agreements with IQVIA have been terminated and IQVIA is not currently providing any services to the Company, the accounts payable to IQVIA relate to potential termination payments that are currently under negotiation.

We are currently considering strategic options for ENTADFI, including a potential sale, and plan to seek funding to support our operations. However, the level of our current liabilities may make it more difficult for us to obtain adequate financing on favorable terms, if at all. If those to whom these payments are due were to demand immediate payment, as they are entitled to do, and we are not able to make the required payments, we would be subject to liability if our creditors chose to enforce their rights, which could result in our bankruptcy and insolvency. Under such a scenario, our assets would be distributed to our creditors, leaving nothing to be distributed to our stockholders.

We may consider strategic alternatives in order to maximize stockholder value, including financing, strategic alliances, licensing arrangements, acquisitions or the possible sale of our business. We may not be able to identify or consummate any suitable strategic alternatives and any consummated strategic alternatives may not be successful.

We may consider all strategic alternatives that may be available to us to maximize stockholder value, including financing, strategic alliances, licensing arrangements, acquisitions, or the possible sale of our business. Our exploration of various strategic alternatives may not result in any specific action or transaction. To the extent that this engagement results in a transaction, our business objectives may change depending upon the nature of the transaction. There can be no assurance that we will enter into any transaction as a result of the engagement. Furthermore, if we determine to engage in a strategic transaction, we cannot predict the impact that such strategic transaction might have on our operations or stock price. We also cannot predict the impact on our stock price if we fail to enter into a transaction.

In addition, we face significant competition in seeking appropriate strategic partners, and the negotiation process is time-consuming and complex. Moreover, we may not be successful in our efforts to establish a strategic partnership or other alternative arrangements for our business activities because they may be deemed to be at too early of a stage of development for collaborative effort. Any delays in entering into new strategic partnership agreements harm our business prospects, financial condition, and results of operations.

If we license or acquire products or businesses, we may not be able to realize the benefit of such transactions if we are unable to successfully integrate them with our existing operations and company culture. We cannot be certain that, following a strategic transaction, license, or acquisition, we will achieve the results, revenue or specific net income that justifies such transaction.

7

Raising additional capital may cause dilution to our existing stockholders and investors, restrict our operations, or require us to relinquish rights to our products on unfavorable terms to us.

We may seek additional capital through a variety of means, including through private and public equity offerings and debt financings, collaborations, strategic alliances and marketing, distribution, or licensing arrangements. To the extent that we raise additional capital through the sale of equity or convertible debt securities, or through the issuance of shares under other types of contracts, or upon the exercise or conversion of outstanding options, warrants, convertible debt or other similar securities, the ownership interests of our stockholders will be diluted, and the terms of such financings may include liquidation or other preferences, anti-dilution rights, conversion and exercise price adjustments and other provisions that adversely affect the rights of our stockholders, including rights, preferences and privileges that are senior to those of our holders of common stock in terms of the payment of dividends or in the event of a liquidation. In addition, debt financing, if available, could include covenants limiting or restricting our ability to take certain actions, such as incurring additional debt, making capital expenditures, entering into licensing arrangements, or declaring dividends and may require us to grant security interests in our assets. If we raise additional funds through collaborations, strategic alliances, or marketing, distribution, or licensing arrangements with third parties, we may have to relinquish valuable rights to our technologies, future revenue streams or products or grant licenses on terms that may not be favorable to us. If we are unable to raise additional funds through equity or debt financing when needed, we may need to curtail or cease our operations.

Due to the significant resources required for the commercialization of our products, and depending on our ability to access capital, we must prioritize commercialization of certain products. Moreover, we may expend our limited resources on products that do not yield a successful product and fail to capitalize on products that may be more profitable or for which there is a greater likelihood of success.

Due to the significant resources required for the development of our products, we must decide which products to pursue and advance and the number of resources to allocate to each. Our decisions concerning the allocation of management and financial resources toward particular products may not lead to the development of any viable commercial products and may divert resources away from better opportunities. Similarly, our potential decisions to delay, terminate, license, or collaborate with third parties in respect of certain products may subsequently also prove to be less than optimal and could cause us to miss valuable opportunities. If we make incorrect determinations regarding the viability or market potential of any of our products or misread trends in the pharmaceutical or diagnostic industry, our business could be seriously harmed. As a result, we may fail to capitalize on viable commercial products or profitable market opportunities, be required to forego or delay pursuit of opportunities with other products and/or product candidates that may later prove to have greater commercial potential than those we choose to pursue or relinquish valuable rights to such products and/or product candidates through collaboration, licensing or other royalty arrangements in cases in which it would have been advantageous for us to invest additional resources to retain sole development and commercialization rights.

Our ability to use our net operating loss carryforwards and certain other tax attributes may be limited, each of which could harm our business.

As of December 31, 2023, we had U.S. federal, foreign, and state net operating loss carryforwards of approximately $27.9 million, $18.0 million, and $23.8 million, respectively. Under Sections 382 and 383 of the Internal Revenue Code, or the Code, if a corporation undergoes an “ownership change,” the corporation’s ability to use its pre-ownership change net operating loss carryforwards and other pre-ownership change tax attributes, such as research tax credits, to offset its post-ownership change income and taxes may be limited. In general, an ownership change will occur when the percentage of the Corporation’s ownership (by value) of one or more “5-percent stockholders” (as defined in the Code) has increased by more than 50 percent over the lowest percentage owned by such stockholders at any time during the prior three years (calculated on a rolling basis). Similar rules may apply under state tax laws. An entity that experiences an ownership change generally will be subject to an annual limitation on its pre-ownership change tax loss and credit carryforwards equal to the equity value of the corporation immediately before the ownership change, multiplied by the long-term, tax-exempt rate posted monthly by the U.S. Internal Revenue Service (subject to certain adjustments). The annual limitation would be increased each year to the extent that there is an unused limitation in a prior year. In the event that it is determined that we have in the past experienced an ownership change as a result of transactions in our stock, or if we experience one or more ownership changes as a result of future transactions in our stock, then we may be limited in our ability to use our net operating loss carryforwards and other tax assets to reduce taxes owed on the net taxable income that we earn. Any limitations on the ability to use our net operating loss carryforwards and other tax assets could harm our business.

8

Our insurance coverage may be inadequate or expensive.

We are subject to claims in the ordinary course of business. These claims may involve substantial amounts of money and involve significant defense costs. It is not possible to prevent or detect all activities giving rise to claims and the precautions we take may not be effective in all cases. We maintain voluntary and required insurance coverage, including, among others, general liability, property, director and officer, business interruption, cyber and data breach. Our insurance coverage is expensive and maintaining or expanding our insurance coverage may have an adverse effect on our results of operations and financial condition.

Our insurance coverage may be insufficient to protect us against all losses and costs stemming from operational and technological failures and we cannot be certain that such insurance will continue to be available to us on economically reasonable terms, or at all, or that any insurer will not deny coverage as to any future claim. The successful assertion of one or more large claims against us that exceed available insurance coverage, or the occurrence of changes in our insurance policies, including premium increases or the imposition of large retention, or deductible, or co-insurance requirements, could have an adverse effect on our business, financial condition, and results of operations.

We entered into an asset purchase agreement and management services agreement with WraSer, which have been terminated because we believe that a material adverse event has occurred with respect to the WraSer Assets. However, the termination is subject to WraSer’s right to challenge the termination and assert claims against us, and WraSer is likely to commence litigation seeking damages for the termination of the asset purchase agreement.

On June 13, 2023, we entered into the WraSer APA and the WraSer MSA with WraSer in connection with the purchase of the WraSer Assets. Under the WraSer APA, we paid $3.5 million in cash to WraSer at signing. In October 2023, WraSer alerted us that its sole manufacturer for the API for Zontivity, the key driver for the WraSer acquisition, would no longer manufacture the API for Zontivity. We believed that this development constituted a Material Adverse Effect under the WraSer APA enabling us to terminate the WraSer APA and the WraSer MSA. On October 20, 2023, we filed a motion for relief from the automatic stay in the Bankruptcy Court to exercise our termination rights under the WraSer APA, as amended. On December 18, 2023, the Bankruptcy Court entered an Agreed Order lifting the automatic stay to enable us to exercise our rights to terminate the WraSer APA and the WraSer MSA without prejudice to the parties’ respective rights, remedies, claims, and defenses they had against one another under the WraSer APA and the WraSer MSA. On December 21, 2023, we filed a Notice with the Bankruptcy Court terminating the WraSer APA and the WraSer MSA. WraSer has advised us that it does not believe that a Material Adverse Event occurred. WraSer has recently filed a plan of reorganization that indicates it may seek damages from us due to the termination of the APA and MSA. Due to the WraSer bankruptcy filing and our status as an unsecured creditor of WraSer, it is also unlikely that we will recover the $3.5 million Signing Cash or any other advances, costs and resources in connection with services provided by the Company under the WraSer MSA.

As a result of our failure to timely file our Quarterly Report on Form 10-Q for the quarter ended June 30, 2023, we are currently ineligible to file new short form registration statements on Form S-3, which may impair our ability to raise capital on terms favorable to us, in a timely manner or at all.

Form S-3 permits eligible issuers to conduct registered offerings using a short form registration statement that allows the issuer to incorporate by reference its past and future filings and reports made under the Securities Exchange Act of 1934, as amended, or the Exchange Act. In addition, Form S-3 enables eligible issuers to conduct primary offerings “off the shelf” under Rule 415 of the Securities Act of 1933, as amended, or the Securities Act. The shelf registration process, combined with the ability to forward incorporate information, allows issuers to avoid delays and interruptions in the offering process and to access the capital markets in a more expeditious and efficient manner than raising capital in a standard registered offering pursuant to a Registration Statement on Form S-1.

9

As a result of our failure to timely file our Quarterly Report on Form 10-Q for quarter ended June 30, 2023, we are currently ineligible to file new short form registration statements on Form S-3 and are unable to conduct “off the shelf” offerings under Rule 415 of the Securities Act using our currently effective Registration Statement on Form S-3 (File No. 333-270383). As a result, we may be unable to conduct an “at the market” offering pursuant to our At The Market Offering Agreement with Wainwright after such date. In addition, if we seek to access the capital markets through a registered offering during the period of time that we are unable to use Form S-3, we may be required to publicly disclose the proposed offering and the material terms thereof before the offering commences, we may experience delays in the offering process due to SEC review of a Form S-1 registration statement and we may incur increased offering and transaction costs and other considerations. Disclosing a public offering prior to the formal commencement of an offering may result in downward pressure on our stock price. In addition, our inability to conduct an offering “off the shelf” may require us to offer terms that may not be advantageous (or may be less advantageous) to us or may generally reduce our ability to raise capital in a registered offering. If we are unable to raise capital through a registered offering, we would be required to conduct our financing transactions on a private placement basis, which may be subject to pricing, size and other limitations imposed under Nasdaq rules.

Our operating results may fluctuate significantly, which makes our future operating results difficult to predict and could cause our operating results to fall below expectations or any guidance we may provide.

Our quarterly and annual revenue and operating results may fluctuate significantly, which makes it difficult for us to predict our future operating results. Our quarterly and annual operating results may fluctuate as a result of a variety of factors, many of which are outside our control and, as a result, may not fully reflect the underlying performance of our business. These fluctuations may occur due to a variety of factors, including, but not limited to:

| ● | the level of demand for our diagnostic tests, which may vary significantly; |

| ● | the timing and cost of manufacturing our diagnostic tests, which may vary depending on the quantity of production and the terms of our agreements with third-party suppliers and manufacturers; |

| ● | expenditures that we may incur to acquire, develop, or commercialize additional tests and technologies; |

| ● | unanticipated pricing pressures; |

| ● | the rate at which we grow our sales force and the speed at which newly hired salespeople become effective, and the cost and level of investment therein; |

| ● | currency fluctuations due to our expectation of generating future revenue from international sales, subjecting us to risks such as currency exchange rate volatility; |

| ● | geopolitical instability, economics problems, and other uncertainties in certain foreign countries in which we operate; |

| ● | the degree of competition in our industry and any change in the competitive landscape of our industry, including consolidation among our competitors or future partners; and |

| ● | coverage and reimbursement policies with respect to cancer treatment equipment, and potential future diagnostic tests that compete with our diagnostic tests. |

The cumulative effects of these factors could result in large fluctuations and unpredictability in our future financial results. As a result, comparing our operating results on a period-to-period basis may not be meaningful. Further, our historical results are not necessarily indicative of results expected for any future period, and quarterly results are not necessarily indicative of the results to be expected for the full year or any other period, and accordingly should not be relied upon as indicative of future performance.

This variability and unpredictability could also result in our failing to meet the expectations of industry or financial analysts or investors for any period. If our revenue or operating results fall below the expectations of analysts or investors or below any guidance we may provide, or if the guidance we provide is below the expectations of analysts or investors, the price of our common stock and warrants could decline substantially. Such a stock price decline could occur even when we have met any publicly stated guidance we may provide, and could in turn negatively impact our business, financial condition and results of operations.

10

Risks Related to the Commercialization of our Products

The marketing approval processes in the United States are lengthy, time-consuming and inherently unpredictable, and if we are ultimately unable to obtain marketing approval for Proclarix, our business may be harmed.

Although the FDA regulates in vitro diagnostic devices, some laboratory companies like Labcorp have successfully commercialized diagnostic tests for various conditions and disease states without seeking clearance or approval for such tests through a 510(k) or PMA approval process. These tests are known as LDTs and are designed, manufactured, and used within a single laboratory that is certified under the CLIA. CLIA is a federal law that regulates clinical laboratories that perform testing on specimens derived from humans for the purpose of providing information for diagnostic, preventative or treatment purpose. Such LDT testing is currently under the purview of CMS and state agencies that provide oversight of the safe and effective use of LDTs. A large number of laboratory testing in the United States consists of LDTs.

Proclarix has not yet quite advanced to the point when Labcorp could seek marketing approval for commercialization by CMS and state agencies in the United States. Labcorp cannot commercialize Proclarix in the United States without first obtaining approval from the CMS and state agencies, and Proclarix marketing approval could be delayed.

On May 6, 2024, the FDA issued a final rule to amend its regulations to make explicit that IVDs are devices under the Federal Food, Drug, and Cosmetic Act (FD&C Act) including when the manufacturer of the IVD is a laboratory. In conjunction with this amendment, the Food and Drug Administration is phasing out its general enforcement discretion approach for LDTs so that IVDs manufactured by a laboratory will generally fall under the same enforcement approach as other IVDs. If the new requirements are phased in, future offerings may require a 510(k) submission or a PMA application to the FDA.

This regulatory review and approval process for medical devices can be costly, timely, and uncertain. This process may involve, among other things, successfully completing additional clinical trials and submitting a premarket clearance notice or filing a premarket approval application with the FDA. If premarket review is required by the FDA, there can be no assurance that Proclarix will be cleared or approved on a timely basis, if at all. In addition, there can be no assurance that the labeling claims cleared or approved by the FDA will be consistent with our current claims or adequate to support continued adoption of and reimbursement for our products. Ongoing compliance with FDA regulations could increase the cost of conducting business, subject us to FDA inspections and other regulatory actions, and potentially subject us to penalties in the event we fail to comply with such requirements.

We depend entirely on the success of a limited number of products. If we do not successfully commercialize our products or we experience significant delays in doing so, these products may not be profitable.

Our business currently depends heavily on the successful commercialization of our products. We cannot be certain that our products will be successfully commercialized. The manufacturing, safety, efficacy, labeling, sale, marketing, and distribution of our products are, and will remain, subject to comprehensive regulation by the FDA and similar foreign regulatory authorities. The success of our products will depend on several additional factors, including:

| ● | establishing commercial manufacturing capabilities; |

| ● | launching commercial sales, marketing and distribution operations; |

| ● | establishing relationships with partners having established distribution, marketing and sales capabilities; |

| ● | the prevalence and severity of adverse events experienced with our products; |

| ● | acceptance of our products by patients, the medical community, and third-party payors; |

| ● | a continued acceptable safety profile following approval; |

| ● | obtaining and maintaining healthcare coverage and adequate reimbursement for our products; |

| ● | competing effectively with other therapies and diagnostics, including with respect to the sales and marketing of our products; and |

| ● | qualifying for, maintaining, enforcing, and defending our intellectual property rights and claims. |

Many of these factors are beyond our control, including potential threats to our intellectual property rights and changes in the competitive landscape. If we do not achieve one or more of these factors in a timely manner or at all, we could experience significant delays or an inability to successfully commercialize our products, which would materially harm our business, financial condition, and results of operations.

Obtaining and maintaining regulatory approval of our products in one jurisdiction does not mean that we will be successful in obtaining regulatory approval in other jurisdictions.

Obtaining and maintaining regulatory approval of our products in one jurisdiction does not guarantee that we will be able to obtain or maintain regulatory approval in any other jurisdiction, while a failure or delay in obtaining regulatory approval in one jurisdiction may have a negative effect on the regulatory approval process in others. For example, even if the FDA grants marketing approval of a pharmaceutical product, comparable regulatory authorities in foreign jurisdictions must also approve the manufacturing, marketing, and promotion of the product in those countries. Approval procedures vary among jurisdictions and can involve requirements and administrative review periods different from, and greater than, those in the United States, including additional preclinical studies or clinical trials as clinical studies conducted in one jurisdiction may not be accepted by regulatory authorities in other jurisdictions. In many jurisdictions outside the United States, a product must be approved for reimbursement before it can be approved for sale in that jurisdiction. In some cases, the price that we intend to charge for our products is also subject to approval.

11

We may also submit marketing applications in other countries. Regulatory authorities in jurisdictions outside of the United States have requirements for approval of pharmaceutical or diagnostic products with which we must comply prior to marketing in those jurisdictions. Obtaining foreign regulatory approvals and compliance with foreign regulatory requirements could result in significant delays, difficulties, and costs for us and could delay or prevent the introduction of our products in certain countries. If we fail to comply with the regulatory requirements in international markets and/or receive applicable marketing approvals, our target market will be reduced and our ability to realize the full market potential of our vaccine candidates will be harmed.

Modifications to our product, ENTADFI, may require new FDA approvals.

Once a particular product receives FDA approval, expanded uses or uses in new indications may require additional human clinical trials and new regulatory approvals, including additional IND and/or NDA, and premarket approvals before we can begin clinical development, and/or prior to marketing and sales. If the FDA requires new approvals for a particular use or indication, we may be required to conduct additional clinical studies, which would require additional expenditures and harm our operating results. If the products are already being used for these new indications, we may also be subject to significant enforcement actions. Conducting clinical trials and obtaining approvals can be a time-consuming process, and delays in obtaining required future approvals could adversely affect our ability to introduce new or enhanced products in a timely manner, which in turn would harm our future growth.

Adverse events involving ENTADFI may result in product recalls that could harm our reputation, business, and financial results.

If we or others identify undesirable side effects caused by ENTADFI, several potentially significant negative consequences could result, including:

| ● | regulatory authorities may suspend or withdraw approvals of such a product; |

| ● | regulatory authorities may require additional warnings or limitations of use in product labeling; |

| ● | we may be required to change the way a product is distributed, dispensed, or administered or conduct additional clinical trials; |

| ● | we could be sued and held liable for harm caused to patients; and |

| ● | our reputation may suffer. |

Any of these events could prevent us from achieving or maintaining market acceptance of ENTADFI and could significantly harm our business, prospects, financial condition, and results of operations.