As filed with the U.S. Securities and Exchange Commission on April [__], 2022

Registration No. 333-258109

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

POST-EFFECTIVE AMENDMENT NO. 1

TO

FORM

REGISTRATION STATEMENT

Under the Securities Act of 1933

AvePoint, Inc.

(Exact name of registrant as specified in its charter)

| | 7379 | |

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

(

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Brian Michael Brown

Chief Legal and Compliance Officer and Secretary

AvePoint, Inc.

901 East Byrd Street, Suite 900

Richmond, VA 23213

(804) 372-8080

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

John T. McKenna

Brian F. Leaf

Katie Kazem

Cooley LLP

3175 Hanover Street

Palo Alto, CA 940304

(650) 843-5000

Approximate date of commencement of proposed sale to the public:

From time to time after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| | Smaller reporting company |

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

EXPLANATORY NOTE

On March 31, 2022, AvePoint, Inc. filed its Annual Report on Form 10-K for fiscal year ended December 31, 2021 (the “Annual Report”). Interested parties should refer to such Annual Report for more information.

The form of prospectus included in this Post-Effective Amendment may be used in one or more offerings by one or more selling stockholders identified in the prospectus contained herein with one or more of the underwriters named therein and with different types and amounts of securities offered.

No additional securities are being registered under this Post-Effective Amendment. All applicable registration fees were paid at the time of the original filing of the Registration Statement or the Pre-Effective Amendment, as applicable.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, Dated . 2022

PRELIMINARY PROSPECTUS

Up to 136,029,478 Shares of Common Stock

Up to 17,905,000 Shares of Common Stock Issuable Upon Exercise of Warrants

Up to 405,000 Warrants to Purchase Common Stock

This Prospectus relates to the issuance by us of an aggregate of up to 17,905,000 shares of our Common Stock, $0.0001 par value per share (the “Common Stock”), which consists of (i) up to 405,000 shares of Common Stock that are issuable upon the exercise of 405,000 warrants (the “Private Warrants”) originally issued in a private placement to Apex Technology Sponsor LLC (the “Sponsor”) in connection with the initial public offering of Apex Technology Acquisition Corporation (“Apex”) and (ii) up to 17,500,000 shares of Common Stock that are issuable upon the exercise of 17,500,000 warrants (the “Public Warrants” and, together with the Private Warrants, the “Warrants”) originally issued in the initial public offering of Apex. We will receive the proceeds from any exercise of any Warrants for cash.

This Prospectus also relates to the offer and sale from time to time by the selling securityholders named in this Prospectus or their permitted transferees (the “selling securityholders”) of (i) up to 136,029,478 shares of Common Stock consisting of (a) up to 14,000,000 shares of Common Stock issued in a private placement pursuant to subscription agreements (the “Subscription Agreements”) entered into on November 23, 2020, as amended, (b) up to 8,750,000 shares of Common Stock (which includes 2,916,700 Sponsor Earn-Out Shares (as defined below)) issued in a private placement to the Sponsor and Cantor Fitzgerald & Co in connection with the initial public offering of Apex (the “Sponsor Shares”), (c) up to 810,000 shares of Common Stock that were issued in connection with the separation of the Private Units (as defined herein), (d) up to 405,000 shares of Common Stock issuable upon exercise of the Private Warrants and (e) up to 112,070,264 shares of Common Stock (including up to 13,329,196 shares of Common Stock issuable pursuant to outstanding options and up to 1,912,155 shares of Common Stock issuable as Earnout Shares (as defined below)) pursuant to that certain Amended and Restated Registration Rights Agreement, dated July 1, 2021, between us and the selling securityholders granting such holders registration rights with respect to such shares and (ii) up to 405,000 Private Warrants. We will not receive any proceeds from the sale of shares of Common Stock or Warrants by the selling securityholders pursuant to this Prospectus.

The selling securityholders may offer, sell or distribute all or a portion of the securities hereby registered publicly or through private transactions at prevailing market prices or at negotiated prices. We will not receive any of the proceeds from such sales of the shares of Common Stock or Warrants, except with respect to amounts received by us upon exercise of the Warrants. We will bear all costs, expenses and fees in connection with the registration of these securities, including with regard to compliance with state securities or “blue sky” laws. The selling securityholders will bear all commissions and discounts, if any, attributable to their sale of shares of Common Stock or Warrants. See the section titled “Plan of Distribution.”

Our Common Stock and Warrants are listed on the Nasdaq Global Select Market under the symbols “ AVPT” and “AVPTW,” respectively. On April 1, 2022, the last reported sales price of our Common Stock was $5.35 per share and the last reported sales price of our Warrants was $0.90 per warrant.

We are an “emerging growth company” as defined under U.S. federal securities laws and, as such, have elected to comply with reduced public company reporting requirements. This Prospectus complies with the requirements that apply to an issuer that is an emerging growth company.

Investing in our securities involves a high degree of risks. You should review carefully the risks and uncertainties described in the section titled “Risk Factors” beginning on page [10] of this Prospectus, and under similar headings in any amendments or supplements to this Prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities, or passed upon the accuracy or adequacy of this Prospectus. Any representation to the contrary is a criminal offense.

Prospectus dated , 2022

ABOUT THIS PROSPECTUS

This Prospectus is part of a Registration Statement on Form S-1 that we filed with the Securities and Exchange Commission (the “SEC”) using the “shelf” registration process. Under this shelf registration process, the selling securityholders may, from time to time, sell the securities offered by them described in this Prospectus. We will not receive any proceeds from the sale by such selling securityholders of the securities offered by them described in this Prospectus. This Prospectus also relates to the issuance by us of the shares of Common Stock issuable upon the exercise of any Warrants. We will not receive any proceeds from the sale of shares of Common Stock underlying the Warrants pursuant to this Prospectus, except with respect to amounts received by us upon the exercise of the Warrants for cash.

Neither we nor the selling securityholders have authorized anyone to provide you with any information or to make any representations other than those contained in this Prospectus or any applicable Prospectus supplement or any free writing Prospectuses prepared by or on behalf of us or to which we have referred you. Neither we nor the selling securityholders take responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. Neither we nor the selling securityholders will make an offer to sell these securities in any jurisdiction where the offer or sale is not permitted.

We may also provide a Prospectus supplement or post-effective amendment to the Registration Statement to add information to, or update or change information contained in, this Prospectus. You should read both this Prospectus and any applicable Prospectus supplement or post-effective amendment to the Registration Statement together with the additional information to which we refer you in the sections of this Prospectus titled “Where You Can Find More Information.”

On July 1, 2021, Legacy AvePoint, Apex, and the Merger Subs (as such terms are defined below), consummated the closing of the transactions contemplated by the Business Combination Agreement (as defined below). Pursuant to the terms of the Business Combination Agreement, a business combination of Legacy AvePoint and Apex was effected by the merger of Merger Sub 1 (as defined below) with and into Legacy AvePoint, with Legacy AvePoint surviving the First Merger (as defined below) as a wholly-owned subsidiary of Apex, and promptly following the First Merger, Legacy AvePoint was merged with and into Merger Sub 2 (as defined below), with Merger Sub 2 surviving the Second Merger (as defined below) as a wholly-owned subsidiary of Apex. Following the consummation of the Mergers on the Closing Date (as defined below), the Surviving Entity (as defined below) changed its name to AvePoint US, LLC and Apex changed its name from Apex Technology Acquisition Corporation to AvePoint, Inc. On July 26, 2021, AvePoint US, LLC was merged with and into AvePoint, Inc.

Unless the context indicates otherwise, references in this Prospectus to the “AvePoint,” “we,” “us,” “our” and similar terms refer to AvePoint, Inc. (f/k/a Apex Technology Acquisition Corporation) and its consolidated subsidiaries (including, as the context may require, Legacy AvePoint) upon and at all times after the consummation of the Business Combination. References to “Legacy AvePoint” refer to the operating company prior to the consummation of the Business Combination. References to “Apex” refer to the predecessor blank check “special purpose acquisition company” prior to the consummation of the Business Combination.

TABLE OF CONTENTS

| Page |

|

| Special Note Regarding Forward-Looking Statements |

1 |

| Prospectus Summary |

5 |

| Risk Factors |

13 |

| Market and Industry Data |

51 |

| Use of Proceeds |

51 |

| Dividend Policy |

51 |

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

52 |

| Business |

65 |

| Management |

92 |

| Executive Compensation |

100 |

| Certain Relationships and Related Party Transactions |

118 |

| Principal Stockholders |

124 |

| Selling Securityholders |

126 |

| Material U.S. Federal Income Tax Consequences |

132 |

| Description of Capital Stock |

138 |

| Plan of Distribution |

145 |

| Legal Matters |

148 |

| Experts |

148 |

| Change in Registrant's Certifying Accountant | 150 |

| Where You Can Find More Information |

152 |

| Audited Financial Information |

F-1 |

| Index to Financial Statements |

F-1 |

| Part II - Information Not Required in Prospectus | II-1 |

| Signatures | S-1 |

You should rely only on the information contained in this Prospectus, any supplement to this Prospectus or in any free writing Prospectus, filed with the SEC. Neither we nor the selling securityholders have authorized anyone to provide you with additional information or information different from that contained in this Prospectus filed with the SEC. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. The selling securityholders are offering to sell, and seeking offers to buy, our securities only in jurisdictions where offers and sales are permitted. The information contained in this Prospectus is accurate only as of the date of this Prospectus, regardless of the time of delivery of this Prospectus or any sale of our securities. Our business, financial condition, results of operations and prospects may have changed since that date.

For investors outside of the United States: Neither we nor the selling securityholders have done anything that would permit this offering or possession or distribution of this Prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this Prospectus must inform themselves about, and observe any restrictions relating to, the offering of our securities and the distribution of this Prospectus outside the United States.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Prospectus contains “forward-looking statements” that involve substantial risks and uncertainties. The forward-looking statements are contained principally in the sections titled “Prospectus Summary” “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Business” and elsewhere in this Prospectus. In some cases, you can identify forward-looking statements by terms such as “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “objective,” “ongoing,” “plan,” “potential,” “predict,” “project,” “should,” “will” and “would,” or the negative of these terms or other similar expressions intended to identify statements about the future. These statements speak only as of the date of this Prospectus and involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition and results of operations. These forward-looking statements include, without limitation, statements about:

| • |

our ability to recognize the anticipated benefits of the Business Combination, which may be affected by, among other things, competition and the ability of the combined business to grow and manage growth profitably; |

| • |

costs related to the Business Combination; |

| • |

our future operating or financial results; |

| • |

future acquisitions, business strategy and expected capital spending; |

| • |

changes in our strategy, future operations, financial position, estimated revenues and losses, projected costs, prospects and plans; |

| • |

the implementation, market acceptance and success of our business model and growth strategy; |

| • |

expectations and forecasts with respect to the size and growth of the cloud industry and digital transformation in general and Microsoft’s products and services in particular; |

| • |

the ability of our products and services to meet customers’ compliance and regulatory needs; |

| • |

our ability to compete with others in the digital transformation industry; |

| • |

our ability to grow our market share; |

| • |

our ability to attract and retain qualified employees and management; |

| • |

our ability to adapt to changes in consumer preferences, perception and spending habits and develop and expand our product offerings and gain market acceptance of our products, including in new geographies; |

| • |

developments and projections relating to our competitors and industry; |

| • |

our ability to develop and maintain our brand and reputation; |

| • |

developments and projections relating to our competitors and industry; |

| • |

the impact of health epidemics, including the COVID-19 pandemic, on our business and the actions we may take in response thereto; |

| • |

the impact of the COVID-19 pandemic on customer demands for cloud services; |

| • |

unforeseen business disruptions or other impacts due to political instability, civil disobedience, terrorism, armed hostilities (including the recent outbreak of hostilities between Russia and Ukraine), extreme weather conditions, natural disasters, other pandemics or other calamities. |

| • |

our expectations regarding our ability to obtain and maintain intellectual property protection and not infringe on the rights of others; |

| • |

expectations regarding the time during which we will be an emerging growth company under the JOBS Act; |

| • |

our future capital requirements and sources and uses of cash; |

| • |

our ability to obtain funding for our operations and future growth; and |

| • |

our business, expansion plans and opportunities. |

The foregoing list of risks is not exhaustive. Other sections of this Prospectus may include additional factors that could harm our business and financial performance. Moreover, we operate in an evolving environment. New risk factors and uncertainties may emerge from time to time, and it is not possible for management to predict all risk factors and uncertainties. As a result of these factors, we cannot assure you that the forward-looking statements in this Prospectus will prove to be accurate. Except as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained herein, whether as a result of any new information, future events, changed circumstances or otherwise, except as required by law.

Because forward-looking statements are inherently subject to risks and uncertainties, some of which cannot be predicted or quantified and some of which are beyond our control, you should not rely on these forward-looking statements as predictions of future events. Although we believe that we have a reasonable basis for each forward-looking statement contained in this Prospectus, the events and circumstances reflected in our forward-looking statements may not be achieved or occur and actual results could differ materially from those projected in the forward-looking statements. You should refer to the ‘‘Risk Factors’’ section of this Prospectus for a discussion of important factors that may cause our actual results to differ materially from those expressed or implied by our forward-looking statements.

You should read this Prospectus and the documents that we reference in this Prospectus and have filed as exhibits to the Registration Statement, of which this Prospectus is a part, completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements.

In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based upon information available to us as of the date of this Prospectus and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and such statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain, and investors are cautioned not to unduly rely upon these statements.

FREQUENTLY USED TERMS

“Apex” means Apex Technology Acquisition Corporation (which was renamed AvePoint, Inc. in connection with the Business Combination).

“Apex IPO” means Apex’s initial public offering of units, consummated on September 19, 2019.

“Apex Initial Stockholders” means the initial stockholders of Apex, including Apex’s officers and Apex’s directors, listed on Schedule C of the Business Combination Agreement.

“Business Combination” means the transactions contemplated by the Business Combination Agreement.

“Business Combination Agreement” means the Business Combination Agreement and Plan of Reorganization, dated as of November 23, 2020, as amended on December 30, 2020, March 8, 2021 and May 18, 2021, and as may be further amended from time to time, by and among Apex, AvePoint and Merger Subs.

“Closing” means the consummation of the Business Combination.

“Closing Date” means July 1, 2021, the date on which the Closing occurred.

“Closing Price” means, for each day that the common stock is trading on the Nasdaq Global Select Market, the closing price (based on such trading day) of shares of common stock on the Nasdaq Global Select Market, as reported on Nasdaq.com.

“Cantor” means Cantor Fitzgerald & Co, representative of the underwriters of the Apex IPO.

“Cantor Shares” means the 152,500 units initially purchased by Cantor and certain of its designees in a private placement in connection with the Apex IPO.

“First Merger” means the merger of Merger Sub I with and into Legacy AvePoint, with Legacy AvePoint surviving the First Merger as a wholly-owned subsidiary of Apex.

“Initial Stockholder Shares” means the 657,500 units initially purchased by the Apex Initial Stockholders in a private placement in connection with the Apex IPO.

“Legacy AvePoint” means AvePoint, Inc. a Delaware corporation, doing business as AvePoint, Inc., and, unless the context requires otherwise, its consolidated subsidiaries.

“Mergers” means the First Merger and Second Merger, together.

“Merger Sub 1” means Athena Technology Merger Sub, Inc., a Delaware corporation and wholly-owned subsidiary of Apex.

“Merger Sub 2” means Athena Technology Merger Sub 2, LLC, a Delaware limited liability company and a wholly-owned subsidiary of Apex.

“Merger Subs” means Merger Sub I and Merger Sub 2, together.

“Merger Sub Common Stock” means Merger Sub 1’s common stock, par value $0.00001 per share.

“PIPE” means that certain private placement in the aggregate amount of $140 million, consummated immediately prior to the consummation of the Business Combination, pursuant to those certain Subscription Agreements with Apex, and subject to the conditions set forth therein, pursuant to which the subscribers purchased 14,000,000 shares of our common stock at a purchase price of $10.00 per share.

“PIPE Shares” means an aggregate of 14,000,000 shares of common stock issued to the subscribers in the PIPE.

“Private Warrants” means the 405,000 warrants to purchase shares of common stock purchased in a private placement in connection with the Apex IPO.

“Public Warrants” means the 17,500,000 warrants included as a component of the Apex units sold in the Apex IPO, each of which is exercisable for one share of common stock, in accordance with its terms.

“Private Units” means the 810,000 private units purchased in a private placement in connection with the Apex IPO.

“Registration Rights Agreement” means that certain Amended and Restated Registration Rights Agreement, dated July 1, 2021, between and among AvePoint and certain securityholders who are parties thereto.

“Second Merger” means the merger of Legacy AvePoint with and into Merger Sub 2, with Merger Sub 2 surviving as a wholly-owned subsidiary of Apex.

“Sponsor” means the Apex Technology Sponsor LLC.

“Sponsor Earn-Out Shares” means up to 2,916,700 shares of Apex Common Stock that the Sponsor deposited into escrow subject to the following vesting provisions: a) 100% of the Sponsor Earn-Out Shares shall vest and be released to the Sponsor if at any time from and after the Closing through the seventh anniversary thereof, the Closing Price is greater than or equal to $15.00 (as adjusted for share splits, share capitalization, reorganizations, recapitalizations, and the like) over any 20 trading days within any 30 trading day period; and 100% of the remaining Sponsor Earn-Out Shares that have not previously vested under the Sponsor Support Agreement (as defined herein) shall vest and be released to the Sponsor if at any time from and after the Closing through the seventh anniversary thereof, Apex consummates a Subsequent Transaction.

“Sponsor Shares” means the Initial Stockholder Shares and Cantor Shares.

“Subsequent Transaction” means any transaction or series of related transactions, including any sale, merger, liquidation, exchange offer or other similar transaction, that is consummated after the effective time of the First Merger that results (a) in any person or “group” (within the meaning of Section 13(d)(3) of the Exchange Act) acquiring beneficial ownership of 50% or more of the outstanding voting securities of AvePoint (as successor to Apex), directly or indirectly, immediately following such transaction, provided that any transaction or series of related transactions which results in at least 50% of the combined voting power of the then outstanding shares of common stock (or at least 50% of the combined voting power of the then outstanding shares of AvePoint (as successor to Apex) or any parent company of AvePoint issued in exchange for common stock) immediately following the closing of such transaction (or series of related transactions) being beneficially owned, directly or indirectly, by individuals and entities who were the beneficial owners of at least 50% of the shares of common stock outstanding immediately prior to such transaction (or series of related transactions), shall not be deemed a “Subsequent Transaction” or (b) a sale or disposition of all or substantially all of the assets of AvePoint (as successor to Apex) and its subsidiaries on a consolidated basis.

“Surviving Corporation” means Legacy AvePoint following the consummation of the Mergers.

“Warrants” means the Private Warrants and the Public Warrants, together.

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this Prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our securities, you should carefully read this entire Prospectus, including our consolidated financial statements and the related notes thereto and the information set forth in the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Unless the context otherwise requires, we use the terms “AvePoint,” “we,” “us” and “our” in this Prospectus to refer to AvePoint, Inc. and our wholly owned subsidiaries after the consummation of the Business Combination.

Overview of Our Business

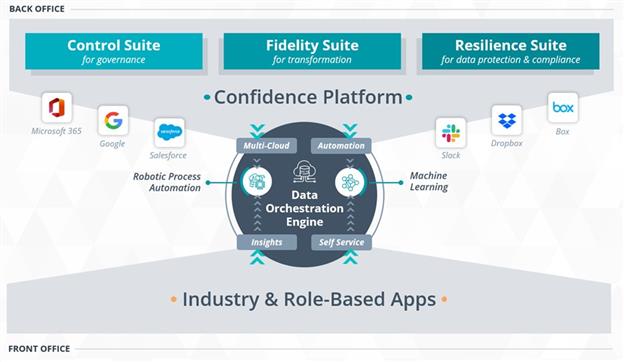

Our mission at AvePoint, Inc. (“AvePoint,” “we,” “us,” or “our”) is to help organizations collaborate with confidence across the cloud. Our goal is to be the catalyst of business transformation by empowering organizations with relevant technologies that are efficient, secure, and well governed. We help transform data and collaboration so users can be more productive with the latest cloud services (like Microsoft 365 ("M365")), and drive efficiency in delivery and management of those services for service providers.

We do this through our Confidence Platform, a software-as-a-service (“SaaS”) platform that assists organizations who use M365 and more than a half dozen cloud collaboration platforms. The Confidence Platform (built on “AvePoint Online Services” or "AOS") supports the collaboration of 8 million users across 7 continents with a scalable, secure, and intelligent architecture. This scalable architecture manages more than 125 PB of content, spread across 14 global data centers, with a 99.9% uptime. Our privacy and security policies are backed by industry certifications including ISO, SOC2 Type II, and FedRAMP moderate authorization. The intelligence engine driving the Confidence Platform ensures continuing value for customers by using AI to maximize relevant data, providing insights, automating operations, and enabling our Control, Fidelity, and Resilience software suites.

Products in our Control Suite enable IT to deliver collaboration services at scale, with automation and repeatable business templates. Business users are empowered with control over licenses, workspaces, and data owned by their departments. Our Fidelity Suite preserves data integrity as organizations undergo digital transformation projects to streamline the way they work from one collaboration system to the next. The Resilience Suite helps organizations comply with data governance regulations, preserve business records for compliance, and ensure business continuity.

Building on this Confidence Platform, we will be pursuing additional industry and role-based applications in 2022 and beyond, including an application that support secure collaboration for companies undergoing mergers and acquisition activities. We will enable our Control, Fidelity, and Resilience Suites to target highly sensitive data-room projects, enabling companies to work with third parties throughout the transitions in their business. The framework established by the Confidence Platform will empower project owners with additional self-service controls, insights, and automation, while preserving compliance records.

With our solutions, organizations have the tools to enable rapid and sustainable adoption of critical applications like Microsoft Teams, which have recently been experiencing record growth in organizations large and small. Systems like M365 can now pass security audits and give teams the control they need to have confidence in their cloud investment. Security teams no longer block progress and pursuit of “work from anywhere” initiatives. With our solutions, they can have confidence in their ability to monitor, manage and govern the rapid adoption of new cloud services. Finally, organizations can use solutions to save time and money, and can decommission home-grown or point solutions that fail to provide key insights and flexible automation that drive business outcomes. The flexibility, automation, and insights of our solutions enable IT to meet business needs and deliver value.

Agility |

We value quick, informed decision-making to meet and exceed customer expectations. We subscribe to a growth mindset, which contributes to our entrepreneurial and learning spirit. |

Passion |

Drive and energy are contagious here; we are not just going through the motions. We do things that are impactful and as a result, amplify our customers’ success. |

Teamwork |

We are invested in the success of our colleagues, partners, customers, and community. We do this by promoting global collaboration and taking pride in helping, sharing, mentoring, and coaching each other. |

Background

We were originally known as Apex Technology Acquisition Corporation. On November 23, 2020, Legacy AvePoint, Apex, and the Merger Subs consummated the transactions contemplated under the Business Combination Agreement. Pursuant to the terms of the Business Combination Agreement, a business combination of Legacy AvePoint and Apex was effected by the merger of Merger Sub 1 with and into Legacy AvePoint, with Legacy AvePoint surviving the First Merger as a wholly-owned subsidiary of Apex, and promptly following the First Merger, Legacy AvePoint was merged with and into Merger Sub 2, with Merger Sub 2 surviving the Second Merger as a wholly-owned subsidiary of Apex. Following the consummation of the Mergers on the Closing Date, the Surviving Entity changed its name to AvePoint US, LLC and Apex changed its name from Apex Technology Acquisition Corporation to AvePoint, Inc. In July 2021, AvePoint US, LLC was merged with and into AvePoint, Inc.

At the effective time of the First Merger (the “Effective Time”), as a result of the First Merger, each share of Legacy AvePoint preferred stock, par value $0.001 per share (“Legacy AvePoint Preferred Stock”) that was then issued and outstanding was cancelled and converted into the right to receive the following: (x) the number of shares of common stock equal to (1) (A) (i) the aggregate amount of shares of common stock distributable to the holders of the Legacy AvePoint Preferred Stock in the First Merger multiplied by the Per Share Amount (as defined below), minus (ii) $135 million, divided by (B) $10.00, divided by (2) the aggregate number of shares Legacy AvePoint common stock, par value $0.001 per share (“Legacy AvePoint Common Stock”) issuable upon the conversion of the Legacy AvePoint Preferred Stock immediately prior to the Effective Time; (y) an amount in cash equal to (i) $135 million in cash (subject to deduction for the aggregate amount of the PIPE financing fees payable by the holders of the Legacy AvePoint Preferred Stock in the First Merger), divided by the aggregate number of shares Legacy AvePoint Common Stock issuable upon the conversion of the Legacy AvePoint Preferred Stock immediately prior to the Effective Time; and (z) the number of shares of Common Stock equal to the aggregate amount of the contingent consideration, if any, that is distributed to the holders Legacy AvePoint securities, divided by the fully diluted number of Legacy AvePoint securities.

At the Effective Time, as a result of the First Merger, each share of Legacy AvePoint Common Stock issued and outstanding immediately prior to the Effective Time (excluding any dissenting shares and shares held by certain executives of Legacy AvePoint) (such shares, the “Named Executive Shares”) was cancelled and converted into the right to receive the following: (x) an amount in cash equal to (1) the gross merger consideration divided by the number of fully diluted number of Legacy AvePoint securities (the “Per Share Amount”), multiplied by (2) the applicable percentage of cash elected to be received by the applicable holder of such shares (subject to withholding such holder’s pro rata share of the PIPE financing fees payable by such holder); (y) the number of shares of Common Stock equal to (1) (A) the Per Share Amount, multiplied by (B) the difference obtained by subtracting applicable percentage of cash elected to be received by the applicable holder of such shares from one, divided by (2) $10.00; provided that if the aggregate amount of cash elected by all such holders of Legacy AvePoint Common Stock prior to any adjustment pursuant to this proviso exceeded the aggregate amount of cash available for distribution to such holders of Legacy AvePoint Common Stock, then the cash election percentage was cut back on a proportionate basis until the amount of cash available for distribution to such holders of Legacy AvePoint Common Stock pursuant to such adjusted elections equaled the maximum amount of cash available for distribution to such holders of Legacy AvePoint Common Stock.

Immediately prior to the Effective Time, certain executives of Legacy AvePoint (the “Named Executives”) contributed the Named Executive Shares to Apex in exchange for (x) with respect to certain of the Named Executive Shares, an amount in cash equal to the Per Share Amount (subject to withholding such Named Executive’s pro rata share of the PIPE financing fees payable by such holder) and (y) with respect to remaining Named Executive Shares, a number of shares of Common Stock equal to (1) the Per Share Amount, divided by (2) $10.00; provided that if the aggregate amount of cash elected by all holders of Legacy AvePoint Common Stock other than the Named Executives prior to any adjustment pursuant to this proviso exceeded the aggregate amount of cash available for distribution to such holders of Legacy AvePoint Common Stock, then the number of Named Executive Shares contributed to Apex in exchange for cash was decreased on a proportionate basis (and the number of Named Executive Shares contributed to Apex in exchange for shares of Common Stock was increased by an equivalent amount) until the amount of cash available for distribution to such holders of Legacy AvePoint Common Stock pursuant to the adjusted elections equaled the maximum amount of cash available for distribution to such holders of Legacy AvePoint Common Stock.

At the Effective Time, as a result of the First Merger, each share of common stock, par value $0.001 per share, of Merger Sub 1 issued and outstanding immediately prior to the Effective Time was cancelled and converted into and exchanged for one validly issued, fully paid and nonassessable share of common stock of Legacy AvePoint, the surviving corporation in the First Merger.

At the Effective Time, as a result of the First Merger, each option to purchase Legacy AvePoint Common Stock that was outstanding immediately prior to the Effective Time, whether vested or unvested (other than certain options held by the Named Executives (such options, the “Named Executive Cash-Settled Options”) and options granted pursuant to a PRC stock option award to employees and other service providers in the People’s Republic of China (such options, the “Legacy International Options”), was cancelled and converted into an option to purchase a number of shares of Common Stock (such option, an “Exchanged Option”) equal to the product (rounded down to the nearest whole number) of (x) the number of shares of Legacy AvePoint Common Stock subject to such Legacy AvePoint option immediately prior to the Effective Time and (y) the Per Share Amount divided by $10.00 (the “Exchange Ratio”), at an exercise price per share (rounded up to the nearest whole cent) equal to (1) the exercise price per share of such Legacy AvePoint option immediately prior to the Effective Time, divided by (2) the Exchange Ratio. Except as specifically provided in the Business Combination Agreement, following the Effective Time, each Exchanged Option will continue to be governed by the same terms and conditions (including vesting and exercisability terms) as were applicable to the corresponding former Legacy AvePoint option immediately prior to the Effective Time. At the Effective Time, as a result of the First Merger, each Legacy International Option was cancelled. Each cancelled Legacy International Option will be replaced and substituted with the award of a new stock option to purchase a number of shares of Common Stock pursuant to the Equity Incentive Plan equal to the product of (rounded down to the nearest whole number) of (A) the number of shares of Legacy AvePoint common Stock subject to such Legacy International Option immediately prior to the Effective Time and (B) the Exchange Ratio, at an exercise price (rounded up to the nearest whole cent) equal to (i) the exercise price per share of such Legacy International Option immediately prior to the Effective Time, divided by (ii) the Exchange Ratio. The replacement stock options will be credited with vesting to the same extent as the Legacy International Options being replaced, and the new replacement awards will be subject to the same vesting schedule and exercisability provisions. In other respects, the such new stock options will be governed by the terms and conditions of the 2021 Equity Incentive Plan (the “2021 Plan”).

At the Effective Time, as a result of the First Merger, each Named-Executive Cash Settled-Option that was outstanding as of immediately prior to the Effective Time was cancelled and converted into the right to receive an amount of cash equal to (x) the number of shares of Legacy AvePoint Common Stock subject to such Named-Executive Cash Settled Option as of immediately prior to the Effective Time multiplied by (y) (1) the Per Share Amount, minus (2) the exercise price attributable to such Named-Executive Cash Settled Option.

Promptly following the Effective Time, upon the effective time of the Second Merger, as a result of the Second Merger, each share of common stock of Legacy AvePoint, the surviving corporation in the First Merger issued and outstanding immediately prior to the effective time of such Second Merger was cancelled and converted into one newly issued, fully paid and non-assessable common membership unit of the Surviving Entity.

As additional consideration for the Mergers, we will issue to the holders of our common stock up to 3,000,000 earnout shares (the “Earnout Shares”) as follows:

| • |

1,000,000 shares of common stock, in the aggregate, if at any time from and after the Closing through the seventh anniversary thereof (x) the Closing Price is greater than or equal to $12.50 over any 20 Trading Days within any 30 Trading Day period or (y) we consummate a Subsequent Transaction, which results in our stockholders having the right to exchange their shares for cash, securities or other property having a value equaling or exceeding $12.50 per share. |

| • |

1,000,000 shares of common stock, in the aggregate, if at any time from and after the Closing through the seventh anniversary thereof (x) the Closing Price is greater than or equal to $15.00 over any 20 Trading Days within any 30 Trading Day period or (y) we consummate a Subsequent Transaction, which results in our stockholders having the right to exchange their shares for cash, securities or other property having a value equaling or exceeding $15.00 per share. |

| • |

1,000,000 shares of common stock, in the aggregate, if at any time from and after the Closing through the seventh anniversary thereof (x) the Closing Price is greater than or equal to $17.50 over any 20 Trading Days within any 30 Trading Day period or (y) we consummate a Subsequent Transaction, which results in our stockholders having the right to exchange their shares for cash, securities or other property having a value equaling or exceeding $17.50 per share. |

An aggregate of 1,912,155 of such Earnout Shares are held by our affiliates and are being registered for resale pursuant to this prospectus.

On the Closing Date, a number of purchasers (each, a “Subscriber”) purchased from AvePoint an aggregate of 14,000,000 shares of Apex Common Stock, for a purchase price of $10.00 per share and an aggregate purchase price of $140.0 million, pursuant to separate subscription agreements (each, a “Subscription Agreement”) entered into effective as of November 23, 2020. Pursuant to the Subscription Agreements, we gave certain registration rights to the Subscribers with respect to the PIPE Shares. The sale of the PIPE Shares was consummated concurrently with the Closing of the Business Combination.

Emerging Growth Company Status

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act of 2012 (“JOBS Act”). As an emerging growth company, we are exempt from certain requirements related to executive compensation, including the requirements to hold a nonbinding advisory vote on executive compensation and to provide information relating to the ratio of total compensation of our Executive Chairman and Chief Executive Officer to the median of the annual total compensation of all of our employees, each as required by the Investor Protection and Securities Reform Act of 2010, which is part of the Dodd-Frank Act.

Section 102(b)(1) of the JOBS Act exempts emerging growth companies from being required to comply with new or revised financial accounting standards until private companies are required to comply with the new or revised financial accounting standards. The JOBS Act provides that a company can choose not to take advantage of the extended transition period and comply with the requirements that apply to non-emerging growth companies, and any such election to not take advantage of the extended transition period is irrevocable. We will take advantage of the benefits of the extended transition period emerging growth company status permits.

During the extended transition period, it may be difficult or impossible to compare our financial results with the financial results of another public company that complies with public company effective dates for accounting standard updates because of the potential differences in accounting standards used.

We will remain an emerging growth company under the JOBS Act until the earliest of (a) December 31, 2024, (b) the last date of our fiscal year in which we have a total annual gross revenue of at least $1.07 billion, (c) the date on which we are deemed to be a “large accelerated filer” under the rules of the SEC with at least $700.0 million of outstanding securities held by non-affiliates or (d) the date on which we have issued more than $1.0 billion in non-convertible debt securities during the previous three years.

Below is a summary of material factors that make an investment in our securities speculative or risky. Importantly, this summary does not address all of the risks and uncertainties that we face. Additional discussion of the risks and uncertainties summarized in this risk factor summary, as well as other risks and uncertainties that we face, can be found under the section titled “Risk Factors” in this Prospectus. The below summary is qualified in its entirety by that more complete discussion of such risks and uncertainties. Importantly, this summary does not address all of the risks and uncertainties that we face. You should consider carefully the risks and uncertainties described under the section titled “Risk Factors” as part of your evaluation of an investment in our securities:

Risks Related to Our Business

| • | Our success depends on our technology partners. In particular, our technical advantages are highly dependent on our partnership with Microsoft and other major software providers. Should Microsoft or these other providers acquire competitors that heavily overlap with our capabilities, or develop competing features, we may lose customer acquisition momentum and fail to secure renewals or growth targets. |

| • | We have experienced strong growth in recent periods, and our recent growth rates may not be indicative of our future growth. |

| • | We face competition from established as well as emerging companies offering solutions and related applications. We may lack sufficient financial or other resources to maintain or improve our competitive position, which may harm our ability to add new customers, retain existing customers, and grow our business. |

| • | If we fail to adapt and respond effectively to rapidly changing technology, evolving industry standards, and changing customer needs or preferences, our products and services may become less competitive. |

| • | Our success with SMB customers depends in part on our resale and distribution partnerships. Our business would be harmed if we fail to maintain or expand partner relationships. |

Risks Related to Our Operations and Financial Condition

| • | We anticipate that our operations will continue to increase in complexity as we grow, which will create management challenges. |

| • | If we fail to maintain or grow our brand recognition, our ability to expand our customer base will be impaired and our financial condition may suffer. |

| • | We intend to invest significantly in research and development, and to the extent such research and development investments do not translate into new products or material enhancements to our products, or if we do not use those investments efficiently, our business and results of operations would be harmed. |

Risks Related to Data Privacy and Cybersecurity

| • | To the extent our security measures are compromised, our products and services may be perceived as not being secure. This may result in customers curtailing or ceasing their use of our products and services, our reputation being harmed, the incurrence of significant liabilities, and harm to our results of operations and growth prospects. |

| • | We store confidential company information and sensitive data, including personal information of our customers and employees, which may in turn contain third-party personal or other confidential information. If the security of this information is compromised or is otherwise accessed without authorization, our reputation may be harmed, and we may be exposed to liability and loss of business. |

|

| • | Successful cyberattacks or data breaches at other technology companies, service providers, retailers, and other participants within our industry, whether or not we are impacted, could lead to a general loss of customer confidence that could negatively affect us, including harming the market perception of the effectiveness of our security measures, which could result in reduced use of our products and services. |

| • | If we are not able to provide successful updates, enhancements and features to our technology to, among other things, keep up with emerging cyber threats and customer needs, our business could be adversely affected. |

Legal and Regulatory Risks

| • | We may become subject to legal proceedings and litigation, including intellectual property disputes, which are costly and may subject us to significant liability and increased costs of doing business. Our business may suffer if it is alleged or determined that our technology infringes the intellectual property rights of others. |

| • | We could incur substantial costs in protecting or defending our proprietary rights. Failure to adequately protect our rights could impair our competitive position, or cause us to lose valuable assets, experience reduced revenue, or incur costly litigation. |

| • | We will provide our products and services to businesses in highly regulated industries and to customers with elevated confidentiality, privacy or security requirements, including public sector customers, which will subject us to a number of challenges and risks. |

Tax Risks

| • | Our ability to use our net operating losses to offset future taxable income may be subject to certain limitations. |

| • | Changes in tax laws or regulations that are applied adversely to us or our customers could increase the cost of our products and services and adversely impact our business. |

| • | Changes in our provision for income taxes or adverse outcomes resulting from examination of our income tax returns could affect our results. |

Risks Related to Intellectual Property

| • | We will rely on third-party proprietary and open source software for our products and services. The inability to obtain third-party licenses for such software, obtain them on favorable terms, or adhere to the license terms for such software or any errors or failures caused by such software could harm our business, results of operations and financial condition. |

| • | If we are unable to protect our intellectual property, the value of our brands and other intangible assets may be diminished, and our business may be adversely affected. |

Human Capital Risks

| • | We will depend on the continued services of our founders, senior management team and skilled individual contributors, and the loss of one or more key employees or an inability to attract and retain highly skilled employees could harm our business. |

| • | If we are unable to maintain our corporate culture as it grows, it could lose the agility, innovation, teamwork, passion and focus on execution that we believe has contributed to our success, and our business may be harmed. |

Public Sector Risks

| • | Significant changes in the contracting or fiscal policies of the public sector, or our failure to comply with certain laws or regulations, could harm the business we do with the public sector. |

Risks Related to Our Common Stock and Investment in Our Securities

| • | The market price of shares of our Common Stock may be volatile, which could cause the value of your investment to decline. |

| • | A small number of stockholders continue to have substantial control over us which may limit other stockholders’ ability to influence corporate matters and delay or prevent a third party from acquiring control over us. |

| • | If our operating and financial performance in any given period does not meet the guidance provided to the public or the expectations of investment analysts, the market price of our Common Stock may decline. |

| • | Our management has identified material weaknesses in our internal control over financial reporting and we may identify additional material weaknesses in the future or otherwise fail to maintain an effective system of internal controls, which may result in material misstatements of our financial statements or cause us to fail to meet our periodic reporting obligations |

General Risk Factors

| • | The COVID-19 pandemic could continue to disrupt the availability or performance of our products and services, require unfavorable changes to our existing products, negatively impact our global technical, sales, and distribution infrastructure, delay the introduction of future products, and adversely impact the global economy on a macro level, any one of which has the potential to harm our business, financial condition, and results of operations. |

| • | Natural catastrophic events and man-made problems such as power disruptions, global pandemics, computer viruses, data security breaches, and terrorism, including as a result of or in connection with the current conflict between Russia and the Ukraine) may disrupt our business. |

Corporate Information

Our principal executive offices are located at 525 Washington Blvd, Suite 1400, Jersey City, NJ 07310, and our telephone number is (201) 793-1111. Our principal operating offices are located at Riverfront Plaza, West Tower, 901 E Byrd St, Suite 900, Richmond, VA 23219 and our telephone number for that office is (804) 372-8080. All correspondence should be directed to our principal operating offices in Richmond, Virginia.

“AvePoint,” "AvePoint, Inc.©," and all other names, logos, and icons identifying AvePoint and/or AvePoint's products and services and our other registered and common law trade names, trademarks, and service marks are property of AvePoint, Inc. This Prospectus contains additional trade names, trademarks, and service marks of others, which are the property of their respective owners. Solely for convenience, trademarks and trade names referred to in this Prospectus may appear without the ® or ™ symbols.

Available Information

Our Internet address is https://www.avepoint.com/. At our Investor Relations website, https://ir.avepoint.com/, we make available free of charge a variety of information for investors. Our goal is to maintain the Investor Relations website as a portal through which investors can easily find or navigate to pertinent information about us, including:

| • | Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports, as soon as reasonably practicable after we electronically file that material with or furnish it to the SEC at www.sec.gov. |

|

| • | Announcements of investor conferences, speeches, presentations, and events at which our executives talk about our product, service, and competitive strategies. |

|

| • | Press releases on quarterly earnings, product and service announcements, legal developments, and national and international news. |

|

| • | Corporate governance information including our articles of incorporation, bylaws, governance guidelines, committee charters, code of ethics and business conduct, whistleblower “open door” policy for reporting accounting and legal allegations, global corporate social responsibility initiatives, and other governance-related policies. |

|

| • | Other news and announcements that we may post from time to time that investors might find useful or interesting, including with respect to our business strategies, financial results, and metrics for investors. |

In addition to these channels, we use social media to communicate to the public. It is possible that the information we post on social media could be deemed to be material to investors. We encourage investors, the media, and others interested in AvePoint to review the information we post on the social media channels listed on our Investor Relations website.

The information found on our main website or our Investor Relations website is not part of this Prospectus or any report we file with, or furnish to, the SEC, for the purposes of Section 18 of the Exchange Act or otherwise subject to the liabilities of that section, nor shall it be deemed incorporated by reference in any filing under the Securities Act except as shall be expressly set forth by specific reference in such filing, and you should not consider any information contained on, or that can be accessed through, our website as part of this Prospectus or in deciding whether to purchase our securities.

The Offering

| Issuance of Common Stock |

||

| Shares of Common Stock offered by us |

17,905,000 shares of Common Stock, consisting of (i) 405,000 shares of Common Stock that are issuable upon exercise of the Private Warrants and (ii) 17,500,000 shares of Common Stock that are issuable upon exercise upon the exercise of the Public Warrants. |

|

| Shares of Common Stock outstanding prior to the exercise of all Warrants |

181,801,404 (as of December 31, 2021) |

|

| Shares of Common Stock outstanding assuming exercise of all Warrants |

199,706,404 (based on the total shares outstanding as of December 31, 2021) |

|

| Exercise price of warrants |

$11.50 per share, subject to adjustment as described herein |

|

| Use of proceeds |

We will receive up to an aggregate of approximately $205.9 million from the exercise of the Warrants. We expect to use the net proceeds from the exercise of the Warrants for general corporate purposes. See “Use of Proceeds” in this Prospectus for more information. |

|

| Resale of Common Stock and Warrants |

||

| Shares of Common Stock offered by the selling securityholders |

We are registering the resale by the selling securityholders named in this Prospectus, or their permitted transferees, an aggregate of 136,029,478 shares of Common Stock, consisting of:

• up to 14,000,000 PIPE Shares;

• up to 8,750,000 Sponsor Shares;

• up to 810,000 shares issued upon separation of the Private Units;

• up to 405,000 shares of Common Stock issuable upon the exercise of the Private Warrants; and

• up to 112,064,478 shares of Common Stock pursuant to the Registration Rights Agreement (including up to 13,329,196 shares of Common Stock issuable pursuant to outstanding options and up to 1,912,155 shares of Common Stock issuable as Earnout Shares). |

|

| Warrants offered by selling securityholders |

Up to 405,000 Private Warrants |

|

| Redemption |

The Public Warrants are redeemable in certain circumstances. See “Description of Our Securities – Warrants.” |

|

| Lock-Up Agreements |

Certain of our securityholders are subject to certain restrictions on transfer until the termination of applicable lock-up periods. See the section titled “Certain Relationships and Related Party Transactions—AvePoint Related Agreements — Lock-Up Agreements.” |

|

| Terms of the offering |

The selling securityholders will determine when and how they will dispose of the securities registered for resale under this Prospectus. |

|

| Use of proceeds |

|

We will not receive any proceeds from the sale of shares of Common Stock or Warrants by the selling securityholders. |

| Risk factors |

|

Before investing in our securities, you should carefully read and consider the information set forth in “Risk Factors”. |

| Nasdaq ticker symbols |

|

“AVPT” and “AVPTW” |

For additional information concerning the offering, see the section titled “Plan of Distribution” beginning on page 147.

RISK FACTORS

Certain factors may have a material adverse effect on our business, financial condition, and results of operations. You should consider carefully the risks and uncertainties described below, in addition to other information contained in this Prospectus, including our consolidated financial statements and related notes. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that adversely affect our business. If any of the following risks actually occurs, our business, financial condition, results of operations, and future prospects could be materially and adversely affected. In that event, the trading price of our Common Stock could decline, and you could lose part or all of your investment.

Explanatory Note

Since the filing of our Annual Report on Form 10-K for the year ended December 31, 2020, filed with the SEC on May 13, 2021 (the “Apex 10-K”), we consummated the Business Combination on July 1, 2021. As a result, because we are no longer a blank check company and there have been material changes to our business, operations, legal structure, and financial condition because of the consummation of the Business Combination, there are corresponding material changes to the risk factors affecting us as compared with those previously disclosed in Part I, Item 1A of the Apex 10-K.

Risks Related to Our Business

Our success depends on our technology partners. In particular, our technical advantages are highly dependent on our partnership with Microsoft and other major software providers. Should Microsoft or these other providers acquire competitors that heavily overlap with our capabilities, or develop competing features, we may lose customer acquisition momentum and fail to secure renewals or growth targets.

The significant majority of our customers choose to integrate their products and services with, or as an enhancement of, third-party solutions such as infrastructure, platforms or applications, in particular from Microsoft, Inc. (“Microsoft”). The functionality and popularity of our products and services depend largely on our ability to integrate our platform with third-party solutions, in particular Microsoft’s Azure, SharePoint and Office 365. We are dependent on technology partner solutions for several major categories of our offerings, including data management, migration, governance, protection and backup. As a result, our customers’ satisfaction with our products are highly dependent on their perception of, and satisfaction with, our third-party providers and their respective offerings. We will continue to depend on various third-party relationships to sustain and grow our business. Third-party providers may change the features of their solutions, alter their governing terms, or end the solutions’ availability altogether. They may restrict our ability to add, customize or integrate systems, functionality and customer experiences. Any such changes could limit or terminate our ability to use these third-party solutions and provide our customers with the full range of our products and services. Our business would be negatively impacted if we fail to retain these relationships for any reason, including due to third parties’ failure to support or secure their technology or integrations; errors, bugs, or defects in their technology; or changes in our products and services. Any such failure, as well as a prolonged disruption, a cybersecurity event or any other negative event affecting our third-party providers and leading to customer dissatisfaction, could harm our relationship with our customers, our reputation and brand, our revenue, our business, and our results of operations.

Strategic technology partners and third parties may not be successful in building integrations, co-marketing our products and services to provide significant volume and quality of lead referrals, or continue to work with us as their respective products evolve. Identifying, negotiating and documenting relationships with additional strategic technology partners require significant resources. Integrating third-party technology can be complex, costly and time-consuming. Third parties may be unwilling to build integrations. We may be required to devote additional resources to develop integrations for our own products. Strategic technology partners or providers of solutions with which we have integrations may decide to compete with us or enter into arrangements with our competitors, resulting in such partners or providers withdrawing support for our integrations. Our agreements with our partners are generally non-exclusive, meaning our partners may offer products from several different companies to their customers. Specifically, Microsoft and other major platform providers could end partnerships, cease marketing our offerings, with limited or no notice and with little or no penalty, or decide to purchase strong competition, or incorporate our capabilities into native solutions. Any of these developments would negatively impact our business.

Microsoft, as well as other cloud platform providers like Salesforce, may furthermore introduce functionality that competes with our products and services, as a result of an acquisition, or their own development. Additionally, we rely heavily on our early access to preview Microsoft technology, which enables our product strategy and development teams to anticipate future opportunities as well as validate our current direction. While Microsoft introduces competitive features as a premium option, some customers will choose a simpler first-party solution to their problem, even at a greater cost to them. Microsoft and other cloud providers may also choose to make it difficult for third party providers like us to continue making the necessary application programming interface (“API”) calls to provide their solutions, as illustrated by an increase in API “throttling” in recent years or API quotas provided by Salesforce.

Although we typically receive significant advance notice of new product releases from Microsoft, Microsoft does not always preview our technology with us or other partners and, as a result, it is possible that we may not receive advance notice of changes in features and functionality of new technologies with which our products will need to interoperate. If this was to happen, there could be an increased risk of product incompatibility. Any failure of our products and services to operate effectively with solutions could reduce the demand for our products and services, resulting in customer dissatisfaction and harm to our business. If we are unable to respond to these changes or failures in a cost-effective manner, our products and services may become less marketable, less competitive, or obsolete, and the results of our operations may be negatively impacted.

We have a strategic technology partnership with Microsoft for the collaboration to co-sell and co-market our products and services to new customers. If our relationships with our strategic technology partners, such as Microsoft, are disrupted or if the co-sell and co-market program was ended for any reason, we may receive less revenue and incur costs to form other revenue-generating strategic technology partnerships. If Microsoft were to acquire a competitor of ours, it could harm our relationship with our customers, our reputation and brand, and our business and results of operations.

We have a history of operating losses and may not be able to generate sufficient revenue to achieve and sustain profitability.

We have a history of incurring operating losses. While we have experienced significant revenue growth over recent years, we may not be able to sustain or increase our growth or achieve profitability in the future. We intend to continue to invest in sales and marketing efforts, research and development, and expansion into new geographies. While our revenue has grown in recent years, if our revenue declines or fails to grow at a rate faster than these increases in its operating expenses, it will not be able to achieve and maintain profitability in future periods. As a result, we may generate losses in future periods. We cannot assure investors that we will achieve profitability in the future or that, if it does become profitable, we will be able to sustain profitability. Additionally, we may encounter unforeseen operating expenses, difficulties, complications, delays, and other unknown factors that may result in losses in future periods. If these losses exceed our expectations or our revenue growth expectations are not met in future periods, our financial performance will be harmed.

We have experienced strong growth in recent periods, and our recent growth rates may not be indicative of our future growth.

We have experienced strong growth in recent periods. In future periods, we may not be able to sustain revenue growth consistent with recent history, or at all. we believe our revenue growth and our ability to manage such growth depend on several factors, including, but not limited to, our ability to do the following:

| • | Effectively recruit, integrate, train and motivate a large number of new employees, including our sales force, technical solutions professionals, customer success managers and engineers, while retaining existing employees, maintaining the beneficial aspects of our corporate culture and effectively executing our business plan; |

| • | Attract new customers and retain and increase sales to existing customers; |

| • | Maintain and expand our relationships with our partners, including effectively managing existing channel partnerships and expand to new ones; |

| • | Successfully implement our products and services, increase our existing customers’ use of our products and services, and provide our customers with excellent customer support and the ability of our partners to do the same; |

| • | Increase the number of our partners; |

| • | Develop our existing products and services and introduce new products or new functionality to our products and services; |

| • | Expand into new market segments and internationally; |

| • | Earn revenue share and customer referrals from our partner ecosystem; |

| • | Improve our key business applications and processes to support our business needs; |

| • | Enhance information and communication systems to ensure that our employees and offices around the world are well-coordinated and can effectively communicate with each other and our growing customer base, particularly in light of the COVID-19 pandemic or the military conflict between Russia and Ukraine and the long-term effects thereof; |

| • | Enhance our internal controls to ensure timely and accurate reporting of all of our operations and financial results; |

| • | Protect and further develop our strategic assets, including our intellectual property rights; and |

| • | Make sound business decisions considering the scrutiny associated with operating as a public company. |

We may not accomplish any of these objectives and, as a result, it is difficult for us to forecast our future revenue or revenue growth. If our assumptions are incorrect or change in reaction to changes in our market, or if we are unable to maintain consistent revenue or revenue growth, our stock price could be volatile, and it may be difficult to achieve and maintain profitability. You should not rely on our revenue for any prior periods as any indication of our future revenue or revenue growth. We may not be able to sustain such revenue growth rates in the future.

Furthermore, these activities will require significant investments and allocation of valuable management and employee resources, and our growth will continue to place significant demands on our management and our operational and financial infrastructure. There are no guarantees we will be able to grow our business in an efficient or timely manner, or at all. Moreover, if we do not effectively manage the growth of our business and operations, the quality of our software could suffer, which could negatively affect the AvePoint brand, results of operations and overall business.

Our quarterly and annual operating results may be harmed due to seasonality and a variety of other factors, which could make our future results difficult to predict.

Our revenue and other results of operations have fluctuated from quarter to quarter in the past and can continue to fluctuate in the future. Our revenue depends in part on the conversion of enterprises that have installed an evaluation license for our software into paying customers. In this regard, most of our sales are typically made during the last three weeks of every quarter. We may fail to meet market expectations for that quarter if we are unable to close the number of transactions that we expect during this short period and closings are deferred to a subsequent quarter.

In addition, our sales cycle from initial contact to delivery of and payment for the software license generally becomes longer and less predictable with respect to large transactions and often involves multiple meetings or consultations at a substantial cost and time commitment to us. Although we try to minimize the potential impact of large transactions on our quarterly results of operations, the closing of a large transaction in a particular quarter may make it more difficult for us to meet market expectations in subsequent quarters and our failure to close a large transaction may adversely impact our revenue in a particular quarter.

Furthermore, we base our current and future expense levels on our revenue forecasts and operating plans, and our expenses are relatively fixed in the short term. Accordingly, we will likely not be able to reduce our costs sufficiently to compensate for an unexpected shortfall in revenue and even a relatively small decrease in revenue could disproportionately impact our financial results for such quarter.

The variability and unpredictability of these and other factors could result in us failing to meet or exceed financial expectations for a given period and could adversely impact our share price.

There are also significant seasonal factors that may cause financial statement fluctuations in some quarters compared with others. We believe this variability is largely due to our customers’ budgetary and spending patterns, as many customers spend the unused portions of their discretionary budgets prior to fiscal year ends. Historically, the fourth quarter has been typically the quarter with the largest bookings, which impacts revenue, unbilled revenue, deferred revenue, accounts receivable and amortized commissions in future periods.

Our future revenue and operating results will be harmed if we are unable to acquire new customers, expand sales to our existing customers, or develop new functionality for our products and services that achieves market acceptance.

To continue to grow our business, it is important that we continue to acquire new customers to purchase and use our products and services. Our success in adding new customers depends on numerous factors, including our ability to: (1) offer compelling products and services, (2) execute our sales and marketing strategy, (3) attract, effectively train and retain new sales, marketing, professional services, and support personnel in the markets we pursue, (4) develop or expand relationships with partners, IT consultants, systems integrators resellers and other third parties, strengthening our network, (5) expand into new geographies, including internationally, and market segments, (6) efficiently onboard new customers on to our product offerings, and (7) provide additional paid services that fulfill the needs and complement the capabilities of our customers and their partners.