As filed with the Securities and Exchange Commission on March 11, 2022

Registration No. 333-257924

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

POST-EFFECTIVE AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter)

| Delaware | 6199 | 84-1770732 | ||||||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) | ||||||

767 Fifth Avenue

New York, New York 10153

(212) 287-3200

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Vladimir Shendelman, Esq.

General Counsel

Perella Weinberg Partners 767 Fifth Avenue

New York, New York 10153

(212) 287-3200

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

Joseph A. Coco, Esq.

Michael J. Schwartz, Esq.

Blair T. Thetford, Esq.

Skadden, Arps, Slate, Meagher & Flom LLP

One Manhattan West

New York, NY 10001

(212) 735-3000

Approximate date of commencement of proposed sale to the public: From time to time on or after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | ||||||||

| ☒ | Smaller reporting company | ||||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

This Post-Effective Amendment No. 1 (this “Post-Effective Amendment No. 1”) to the Registration Statement on Form S-1 (File No. 333-257924) (the “Registration Statement”), as originally declared effective by the Securities and Exchange Commission (the “SEC”) on July 26, 2021, is being filed to include information contained in the registrant’s Annual Report on Form 10-K for the fiscal year ended December 31, 2021, which was filed with the SEC on March 11, 2022, and to update certain other information in the Registration Statement.

The information included in this filing amends the Registration Statement and the prospectus contained therein. No additional securities are being registered under this Post-Effective Amendment No. 1. All applicable registration fees were paid at the time of the original filing of the Registration Statement on July 15, 2021.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the SEC, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. Neither we nor the selling security holders may sell or distribute the securities described herein until the registration statement filed with the SEC is effective. This prospectus is not an offer to sell and is not soliciting an offer to buy the securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MARCH 11, 2022

PRELIMINARY PROSPECTUS

Perella Weinberg Partners

64,738,934 Shares of Class A Common Stock

203,333 Warrants to Purchase Class A Common Stock

This prospectus relates to: (1) the issuance by us of up to 7,869,975 shares of our Class A common stock, par value $0.0001 per share (“Class A common stock”) that may be issued upon exercise of warrants to purchase Class A common stock at an exercise price of $11.50 per share of Class A common stock, including the Public Warrants and the Private Placement Warrants (each as defined below); and (2) the offer and sale, from time to time, by the selling holders identified in this prospectus (the “Selling Holders”), or their permitted transferees, of (i) up to 64,738,934 shares of Class A common stock and (ii) up to 203,333 Warrants (as defined below).

This prospectus provides you with a general description of such securities and the general manner in which we and the Selling Holders may offer or sell the securities. More specific terms of any securities that we and the Selling Holders may offer or sell may be provided in a prospectus supplement that describes, among other things, the specific amounts and prices of the securities being offered and the terms of the offering. The prospectus supplement may also add, update or change information contained in this prospectus.

We will not receive any proceeds from the sale of shares of Class A common stock or Warrants by the Selling Holders pursuant to this prospectus or of the shares of Class A common stock by us pursuant to this prospectus, except with respect to amounts received by us upon exercise of the Warrants to the extent such Warrants are exercised for cash. However, we will pay the expenses, other than underwriting discounts and commissions, associated with the sale of securities pursuant to this prospectus.

Our registration of the securities covered by this prospectus does not mean that either we or the Selling Holders will issue, offer or sell, as applicable, any of the securities. The Selling Holders may offer and sell the securities covered by this prospectus in a number of different ways and at varying prices. We provide more information in the section entitled “Plan of Distribution.”

You should read this prospectus and any prospectus supplement or amendment carefully before you invest in our securities.

Our Class A common stock and Warrants are traded on the Nasdaq Global Select Market (the “Nasdaq”) under the symbols “PWP” and “PWPPW,” respectively. On March 8, 2022, the closing price of our Class A common stock on the Nasdaq was $9.72 per share and the closing price of our Warrants on the Nasdaq was $2.28 per Warrant.

We are an “emerging growth company” as that term is defined under the federal securities laws and, as such, are subject to certain reduced public company reporting requirements.

Investing in our securities involves risks. See “Risk Factors” beginning on page 30 and in any applicable prospectus supplement.

Neither the SEC nor any state securities commission has approved or disapproved of the securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2022.

TABLE OF CONTENTS

i

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form S-1 that we filed with the SEC using a “shelf” registration process. Under this shelf registration process, we and the Selling Holders may, from time to time, issue, offer and sell, as applicable, any combination of the securities described in this prospectus in one or more offerings. We may use the shelf registration statement to issue up to an aggregate of 7,869,975 shares of Class A common stock upon exercise of the Public Warrants and Private Placement Warrants. The Selling Holders may use the shelf registration statement to sell up to an aggregate of 64,738,934 shares of Class A common stock and up to 203,333 Warrants from time to time through any means described in the section entitled “Plan of Distribution.” More specific terms of any securities that the Selling Holders offer and sell may be provided in a prospectus supplement that describes, among other things, the specific amounts and prices of the Class A common stock and/or Warrants being offered and the terms of the offering.

A prospectus supplement may also add, update or change information included in this prospectus. Any statement contained in this prospectus will be deemed to be modified or superseded for purposes of this prospectus to the extent that a statement contained in such prospectus supplement modifies or supersedes such statement. Any statement so modified will be deemed to constitute a part of this prospectus only as so modified, and any statement so superseded will be deemed not to constitute a part of this prospectus. You should rely only on the information contained in this prospectus or any applicable prospectus supplement. See “Where You Can Find More Information.”

Neither we nor the Selling Holders have authorized anyone to provide any information or to make any representations other than those contained in this prospectus or any accompanying prospectus supplement we have prepared. We and the Selling Holders take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the securities offered hereby and only under circumstances and in jurisdictions where it is lawful to do so. No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus or any applicable prospectus supplement. This prospectus is not an offer to sell securities, and it is not soliciting an offer to buy securities, in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus or any prospectus supplement is accurate only as of the date on the front of those documents, regardless of the time of delivery of this prospectus or any applicable prospectus supplement, or any sale of a security. Our business, financial condition, results of operations and prospects may have changed since those dates.

This prospectus contains summaries of certain provisions contained in some of the documents described herein, but reference is made to the actual documents for complete information. All of the summaries are qualified in their entirety by the actual documents. Copies of some of the documents referred to herein have been filed, will be filed or will be incorporated by reference as exhibits to the registration statement of which this prospectus is a part, and you may obtain copies of those documents as described below under “Where You Can Find More Information.”

ii

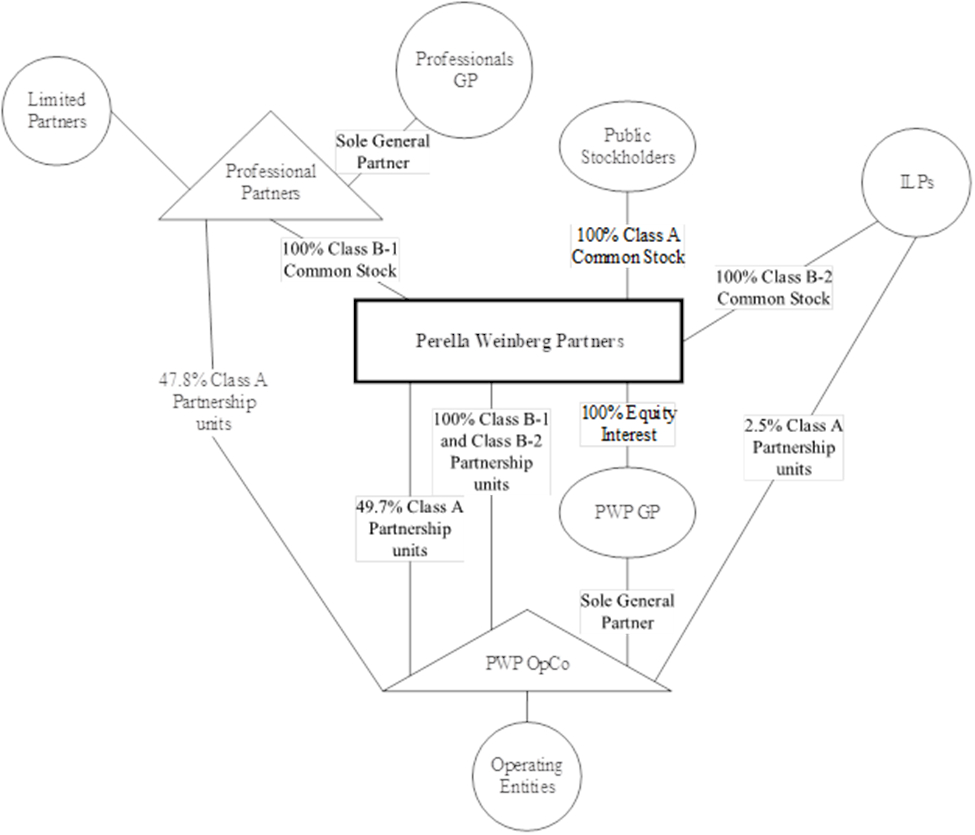

On June 24, 2021 (the “Closing Date”), Perella Weinberg Partners (formerly known as FinTech Acquisition Corp. IV (“FTIV”)), consummated its previously announced business combination pursuant to that certain Business Combination Agreement, dated as of December 29, 2020 (the “Business Combination Agreement”), by and among FTIV, FinTech Investor Holdings IV, LLC, a Delaware limited liability company, FinTech Masala Advisors, LLC, a Delaware limited liability company (together with FinTech Investor Holdings IV, LLC, “Sponsor”), PWP Holdings LP, a Delaware limited partnership (“PWP OpCo”), PWP GP LLC, a Delaware limited liability company and the general partner of PWP OpCo (“PWP GP”), PWP Professional Partners LP, a Delaware limited partnership and a limited partner of PWP OpCo (“Professional Partners”), and Perella Weinberg Partners LLC, a Delaware limited liability company and the general partner of Professional Partners (“Professionals GP”). As contemplated by the Business Combination Agreement, (i) FTIV acquired certain partnership interests in PWP OpCo, (ii) PWP OpCo became jointly-owned by the Company, Professional Partners and certain existing partners of PWP OpCo, and (iii) PWP OpCo serves as the Company’s operating partnership as part of an umbrella limited partnership C-corporation (Up-C) structure (collectively with the other transactions contemplated by the Business Combination Agreement, the “Business Combination”).

Unless the context indicates otherwise, references to the “Company,” “we,” “us” and “our” refer, prior to the Business Combination, to FTIV or PWP OpCo, as the context suggests, and, following the Business Combination, to Perella Weinberg Partners, a Delaware corporation, and its consolidated subsidiaries.

iii

MARKET, RANKING AND OTHER INDUSTRY DATA

Certain market, ranking and industry data included in this prospectus, including the size of certain markets and our size or position and the positions of our competitors within these markets, including our products and services relative to our competitors, are based on estimates by our management. These estimates have been derived from our management’s knowledge and experience in the markets in which we operate, as well as information based on research, industry and general publications, including surveys and studies conducted by third parties. Industry publications, surveys and studies generally state that they have been obtained from sources believed to be reliable.

We are responsible for all of the disclosure in this prospectus and while we believe the data from these sources to be accurate and complete, we have not independently verified all data from these sources or obtained third-party verification of market share data and this information may not be reliable. In addition, these sources may use different definitions of the relevant markets. Data regarding our industry is intended to provide general guidance, but is inherently imprecise. Market share data is subject to change and cannot always be verified with certainty due to limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in any statistical survey of market shares. In addition, customer preferences can and do change. As a result, you should be aware that market share, ranking and other similar data set forth herein, and estimates and beliefs based on such data, may not be reliable. References herein to us being a leader in a market or product category refers to our belief that we have a leading market share, expertise or thought leadership position in each specified market, unless the context otherwise requires. In addition, the discussion herein regarding our various markets is based on how we define the markets for our products or services, which products or services may be either part of larger overall markets or markets that include other types of products and services. Assumptions and estimates regarding our current and future performance are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Risk Factors—Risks Related to Our Business.” These and other factors could cause our future performance to differ materially from our assumptions and estimates. See “Cautionary Statement Regarding Forward-Looking Statements.”

In this prospectus, we use the term “independent advisory firms” to refer to independent investment banks that offer advisory services. We consider the independent advisory firms to be our publicly traded peers, Evercore Partners Inc.; Greenhill & Co., Inc.; Houlihan Lokey, Inc.; Lazard Ltd; Moelis & Company; PJT Partners, Inc., as well as our non-publicly traded peers, Centerview Partners; Guggenheim Partners; and NM Rothschild & Sons Limited. The mergers and acquisitions (“M&A”) market data for announced and completed transactions and estimated fee data referenced throughout this prospectus were obtained from Dealogic, LLC.

iv

NON-GAAP FINANCIAL MEASURES

In addition to financial measures presented in accordance with United States generally accepted accounting principles (“GAAP”), we present certain non-GAAP financial measures in this prospectus, including Adjusted total compensation and benefits, Adjusted non-compensation expense, Adjusted operating income (loss), Adjusted non-operating income (expenses), Adjusted income (loss) before income taxes, Adjusted income tax benefit (expense) and Adjusted net income (loss), which we monitor to manage our business, make planning decisions, evaluate our performance and allocate resources. We believe that these non-GAAP financial measures are key financial indicators of our business performance over the long term and provide useful information regarding whether cash provided by operating activities is sufficient to maintain and grow our business. We believe that the methodology for determining these non-GAAP financial measures can provide useful supplemental information to help investors better understand the economics of our platform. These non-GAAP financial measures have limitations as analytical tools and should not be considered in isolation from, or as a substitute for, the analysis of other GAAP financial measures, including total compensation and benefits, non-compensation expense, operating income (loss), nonoperating income (expenses), income (loss) before taxes, income tax benefit (expense) and net income (loss). These non-GAAP financial measures are not universally consistent calculations, limiting their usefulness as comparative measures. Other companies may calculate similarly titled financial measures differently. Additionally, these non-GAAP financial measures are not measurements of financial performance or liquidity under GAAP. In order to facilitate a clear understanding of our consolidated historical operating results, you should examine our non-GAAP financial measures in conjunction with our historical consolidated financial statements and notes thereto included elsewhere in this prospectus. Management compensates for the inherent limitations associated with using these non-GAAP financial measures through disclosure of such limitations, presentation of our financial statements in accordance with GAAP and reconciliation of such non-GAAP financial measures to the most directly comparable GAAP financial measure. For additional information regarding see “Summary Historical Financial and Other Information.”

TRADEMARKS, SERVICE MARKS AND TRADE NAMES

This prospectus may contain some trademarks, service marks and trade names of the Company or of third parties. Each one of these trademarks, service marks or trade names is either (1) our registered trademark, (2) a trademark for which we have a pending application, or (3) a trade name or service mark for which we claim common law rights. All other trademarks, trade names or service marks of any other company appearing in this prospectus belong to their respective owners. Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus are presented without the TM, SM and ® symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our respective rights or the rights of the applicable licensors to these trademarks, service marks and trade names.

SELECTED DEFINITIONS

Unless stated in this prospectus or the context otherwise requires, references to:

•“Class A common stock” are to Class A common stock, par value $0.0001 per share, of FTIV prior to the Business Combination, and of the Company immediately following the consummation of the Business Combination;

•“Class B common stock” are to Class B common stock, par value $0.0001 per share, of FTIV prior to the Business Combination and, collectively to Class B-1 common stock, par value $0.0001 per share, and Class B-2 common stock, par value $0.0001 per share, of the Company immediately following the consummation of the Business Combination;

•“Class B Condition” are to the condition that Professional Partners or its limited partners as of the date of the Closing or its or their respective successors or assigns maintain, directly or indirectly, ownership of PWP OpCo Class A partnership units that represent at least ten percent (10%) of our issued and outstanding Class A common stock (calculated, without duplication, on the basis that all issued and outstanding PWP OpCo Class A partnership units not held by us or our subsidiaries had been exchanged for our Class A common stock).

v

•“Closing” are to the consummation of the transactions contemplated by the Business Combination;

•“Common Stock” are to the Class A common stock and the Class B common stock, together;

•“Convertible Notes” are to PWP’s 7.0% subordinated unsecured convertible notes due 2026, which were redeemed in connection with the Closing.

•“Exchange Act” are to the Securities Exchange Act of 1934, as amended;

•“Exchange Shares” are to shares of Class A common stock issued or issuable in exchange for PWP OpCo Class A partnership units and Class B common stock pursuant to the PWP OpCo LPA (as defined below);

•“Founder Shares” are to the 7,870,000 shares of Class B common stock held by the Sponsor prior to the Business Combination, 1,023,333 of which were forfeited and 6,846,667 of which were converted into shares of our Class A common stock at the closing of the Business Combination. All but 1,000,000 of the Founder Shares held by the Sponsor were distributed to the Sponsor’s members pursuant to the Sponsor Distribution (as defined below);

•“Group LP” are to Perella Weinberg Partners Group LP, a Delaware limited partnership and a wholly owned subsidiary of PWP OpCo;

•“ILPs” are to certain existing investor limited partners of PWP OpCo who hold interests in PWP OpCo, alongside Professional Partners;

•“Incentive Plan” are to the Perella Weinberg Partners 2021 Omnibus Incentive Plan approved in connection with the Business Combination;

•“Initial Stockholders” are to the Sponsor and any other holders of Class B common stock prior to FTIV’s initial public offering;

•“IPO” are to FTIV’s initial public offering on September 29, 2020 in which it sold 23,000,000 units;

•“JOBS Act” are to the Jumpstart Our Business Startups Act of 2012;

•“Legacy Partners” are to former working Limited Partners whose tenure was terminated prior to November 1, 2020;

•“Limited Partners” are to limited partners of Professional Partners;

•“PIPE Shares” are to the 12,500,000 shares of Class A common stock issued to the PIPE Investors pursuant to the Subscription Agreements;

•“Placement Shares” are to the 610,000 shares of Class A common stock underlying the 610,000 units that were initially issued to the Sponsor in a private placement simultaneously with the closing of the IPO and which were distributed to the Sponsor’s members pursuant to the Sponsor Distribution;

•“Private Placement Warrants” are to the 203,333 warrants underlying the 610,000 units that were initially issued to Sponsor in a private placement simultaneously with the closing of the IPO and which were distributed to the Sponsor’s members pursuant to the Sponsor Distribution;

•“Public Warrants” are to the redeemable warrants underlying the units that were initially offered and sold by FTIV in its IPO;

•“PWP” (i) prior to the Business Combination are to PWP OpCo and its consolidated subsidiaries and (ii) following the consummation of the Business Combination are to Perella Weinberg Partners and its consolidated subsidiaries;

vi

•“PWP OpCo” (i) prior to the PWP Separation, are to PWP Holdings LP as the holding company for both the advisory business and asset management business of PWP and (ii) following the PWP Separation, are to PWP Holdings LP as the holding company solely for the advisory business of PWP;

•“PWP OpCo Class A partnership unit” are to a Class A common unit of PWP Holdings LP, a Delaware limited partnership, that is issued by PWP Holdings LP pursuant to the PWP OpCo LPA;

•“PWP Separation” are to the separation of the advisory business from the asset management business of PWP OpCo pursuant to a master separation agreement, dated as of February 28, 2019;

•“Redeeming Holders” are to all of the holders who agreed to collectively tender for redemption $150 million aggregate principal amount of the Convertible Notes (such convertible notes, the “Redeemed Notes”) for cash, pursuant to the terms of the letter agreements at a redemption price equal to 100% of the principal amount (plus, with respect to any Redeeming Holder owning at least $5.0 million principal amount of convertible notes, an applicable premium based on a discounted U.S. treasury rate), and accrued and unpaid interest to, but excluding, the closing date of the Business Combination;

•“RRA Parties” are to the Sponsor, Professional Partners, the ILPs and others party to the Amended and Restated Registration Rights Agreement (as defined below), including certain parties affiliated with the Sponsor who became a party to the Amended and Restated Registration Rights Agreement in connection with the Sponsor Distribution;

•“Sarbanes-Oxley Act” are to the Sarbanes-Oxley Act of 2002;

•“Secondary Class B Condition” are to the condition that Professional Partners or its limited partners as of the date of Closing or its or their respective successors or assigns maintain, directly or indirectly, ownership of PWP OpCo Class A partnership units that represent at least five percent (5%) of our issued and outstanding Class A common stock (calculated, without duplication, on the basis that all issued and outstanding PWP OpCo Class A partnership units not held by us or our subsidiaries had been exchanged for our Class A common stock).

•“Securities Act” are to the Securities Act of 1933, as amended;

•“Selling Holders” are to the selling holders identified in this prospectus and the pledgees, donees, transferees, assignees, successors and others who later come to hold any of the Selling Holders’ interest in the shares of Class A common stock or Warrants, as applicable, after the date of this prospectus such that registration rights shall apply to those securities;

•“Sponsor Distribution” are to the distribution by the Sponsor of 5,456,667 shares of Class A common stock (Founder Shares and Placement Shares) and 203,333 Private Placement Warrants to its members on January 7, 2022 pursuant to its contractual obligation under the limited liability company agreement, after which the Sponsor owned 1,000,000 shares of Class A common stock and no Private Placement Warrants.

•“Sponsor Related PIPE Investors” are to the certain PIPE Investors that subscribed to $1.5 million in the PIPE Investment (as defined below);

•“Subscription Agreements” are to the subscription agreements with the PIPE Investors, pursuant to, and on the terms and subject to the conditions of, which the PIPE Investors collectively subscribed for 12,500,000 shares of the Company’s Class A common stock for an aggregate purchase price equal to $125 million (the “PIPE Investment”);

•“Warrants” are to Public Warrants and Private Placement Warrants; and

•“Working Partners” are to working Limited Partners whose tenure was not terminated prior to November 1, 2020.

vii

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Certain statements made in this prospectus are “forward looking statements” within the meaning of the federal securities laws, including the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Exchange Act. Statements regarding the expectations regarding the combined business are “forward looking statements.” In addition, words such as “estimates,” “projected,” “expects,” “estimated,” “anticipates,” “forecasts,” “plans,” “intends,” “believes,” “seeks,” “may,” “will,” “would,” “future,” “propose,” “target,” “goal,” “objective,” “outlook” and variations of these words or similar expressions (or the negative versions of such words or expressions) are intended to identify forward-looking statements. These forward-looking statements are not guarantees of future performance, conditions or results, and involve a number of known and unknown risks, uncertainties, assumptions and other important factors, many of which are outside the control of the parties, that could cause actual results or outcomes to differ materially from those discussed in the forward-looking statements. Important factors, among others, that may affect actual results or outcomes include:

•any projected financial information, anticipated growth rate, and market opportunity of the Company;

•the ability to maintain the listing of the Company’s Class A common stock and Warrants on Nasdaq following the Business Combination;

•our public securities’ potential liquidity and trading;

•our success in retaining or recruiting partners and other employees, or changes related to, our officers, key employees or directors following the completion of the Business Combination;

•members of our management team allocating their time to other businesses and potentially having conflicts of interest with our business;

•factors relating to the business, operations and financial performance of the Company, including:

◦whether the Company realizes all or any of the anticipated benefits from the Business Combination;

◦whether the Business Combination results in any increased or unforeseen costs or has an impact on the Company’s ability to retain or compete for professional talent or investor capital;

◦global economic, business, market and geopolitical conditions, including the impact of public health crises, such as the ongoing rapid, worldwide spread of a novel strain of coronavirus and the pandemic caused thereby (collectively, “COVID-19”), as well as the impact of recent hostilities between Russia and Ukraine;

◦the Company’s dependence on and ability to retain working partners and other key employees;

◦the Company’s ability to successfully identify, recruit and develop talent;

◦risks associated with strategic transactions, such as joint ventures, strategic investments, acquisitions and dispositions;

◦conditions impacting the corporate advisory industry;

◦the Company’s dependence on its fee-paying clients and fluctuating revenues from its non-exclusive, engagement-by-engagement business model;

◦the high volatility of the Company’s revenue as a result of its reliance on advisory fees that are largely contingent on the completion of events which may be out of its control;

◦the ability of the Company’s clients to pay for its services, including its restructuring clients;

viii

◦the Company’s ability to appropriately manage conflicts of interest and tax and other regulatory factors relevant to the Company’s business, including actual, potential or perceived conflicts of interest and other factors that may damage its business and reputation;

◦strong competition from other financial advisory and investment banking firms;

◦potential impairment of goodwill and other intangible assets, which represent a significant portion of the Company’s assets;

◦the Company’s successful formulation and execution of its business and growth strategies;

◦the outcome of third-party litigation involving the Company;

◦substantial litigation risks in the financial services industry;

◦cybersecurity and other operational risks;

◦the Company’s ability to expand into new markets and lines of businesses for the advisory business;

◦exposure to fluctuations in foreign currency exchange rates;

◦assumptions relating to the Company’s operations, financial results, financial condition, business prospects, growth strategy and liquidity;

◦extensive regulation of the corporate advisory industry and U.S. and foreign regulatory developments relating to, among other things, financial institutions and markets, government oversight, fiscal and tax policy and laws (including the treatment of carried interest);

◦the impact of the global COVID-19 pandemic on any of the foregoing risks; and

◦other risks and uncertainties described under the section entitled “Risk Factors.”

The forward-looking statements contained in this prospectus are based on current expectations and beliefs concerning future developments and their potential effects on the Company. There can be no assurance that future developments affecting the Company will be those that the Company has anticipated. The Company undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

ix

PROSPECTUS SUMMARY

This summary highlights certain significant aspects of our business and is a summary of information contained elsewhere in this prospectus. This summary is not complete and does not contain all of the information that you should consider before making your investment decision. You should carefully read this entire prospectus, including the information presented under the sections titled “Risk Factors,” “Cautionary Statement Regarding Forward Looking Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Unaudited Pro Forma Condensed Combined Financial Information,” and the consolidated financial statements and the related notes thereto included elsewhere in this prospectus before making an investment decision. The definition of some of the other terms used in this prospectus are set forth under the section “Selected Definitions.”

Business Summary

We are a leading global independent advisory firm that provides strategic and financial advice to clients across a range of the most active industry sectors and international markets. We provide advisory services to a wide range of clients globally, including large public multinational corporations, mid-sized public and private companies, individual entrepreneurs, private and institutional investors, creditor committees and government institutions.

We were founded in June 2006 with the opening of offices in New York and London, led by a team of ten seasoned advisory partners who previously held senior management positions at large global investment banks. The foundation of our Company was rooted in a belief, among other considerations, that clients would increasingly seek out deeply experienced advisors who offer independent strategic thinking and who are not burdened by the complicated conflicts that large investment banking institutions may face due to their various businesses. The 2008 global financial crisis reinforced this hypothesis and contributed to the early growth of our Company. Today, we believe that our independence is even more important. For clients and for us, independence means freedom from the distractions that dilute strategic thinking and a willingness and candor to share an honest opinion, even if at times it is contrary to our clients’ point of view. We believe that our clients choose to engage us because they value our unbiased perspective and expert advice regarding complex financial and strategic matters.

Our business provides services to multiple industry sectors, geographic markets and advisory service offerings. We believe that our collaborative partnership and integrated approach combining deep industry insights, significant technical, product and transactional expertise, and rigorous work ethic create a significant opportunity for our Company to realize sustainable growth. We seek to advise clients throughout their evolution, with the full range of our advisory capabilities including, among other things, advice related to mission-critical strategic and financial decisions, M&A execution, shareholder and defense advisory, capital raising, capital structure and restructuring, capital markets advisory, specialized underwriting and research services for the energy and related industries.

Since our inception, we have experienced significant growth in our business, driven by hiring professionals who are highly regarded in their fields of expertise, expanding the scope and geographic reach of our advisory services, deepening and expanding our client relationships and maintaining a firm culture that attracts, develops and retains talented people. In addition to our hiring and internal development of individual professionals, in November 2016, we completed a business combination with Tudor, Pickering, Holt & Co., LLC (“TPH”), an independent advisory firm, focused on the energy industry, that shares our culture and strategic vision, which increased our footprint in this sector. As of December 31, 2021, we serve our clients with 422 advisory professionals, including 60 advisory partners (which numbers include two advisory partners who retired from the Company in January 2022), based in ten offices, located in five countries around the world.

1

We have demonstrated robust financial performance, achieving revenues of $801.7 million and operating income of $66.6 million for the year ended December 31, 2021, revenues of $519.0 million and operating loss of $14.6 million for the year ended December 31, 2020 and revenues of $533.3 million and operating loss of $155.1 million for the year ended December 31, 2019. The operating losses in 2019 and 2020 were largely due to amortization of the equity-based compensation awards granted by Professional Partners, which have no economic impact on PWP or PWP OpCo. The vesting of equity awards granted in connection with the Transaction have been and will be recorded as an equity-based compensation expense at PWP OpCo for GAAP accounting purposes. As a result (or due to other factors), we may continue to experience operating losses in future periods. We believe we have established leading franchises in each of our areas of focus, as evidenced by the lead role we often command among advisors, the complexity of the situations in which we advise clients and our clients’ reputation as leaders in their respective industries.

Our Market Opportunity

We founded our Company with the objective of providing strategic and financial advice to business leaders that is critical to the success of their businesses throughout their corporate evolution. The decisions that business leaders confront often transcend traditional transaction-related questions, focusing instead on the core risks and opportunities facing their businesses. We believe that clients are increasingly looking for an independent advisor who can serve as an unbiased sounding board, work with them in genuine partnership and be by their side as they navigate mission-critical and complex issues.

We believe many factors drive the demand for such advice, including, but not limited to:

Sector-Specific Transformation and Disruption: The sectors on which we focus are all experiencing change at an accelerating pace. Such change within a sector may be driven by new regulation, new competition, business model innovation and transformation and the increasing impact of technology, among other factors. Business leaders are highly focused on the effect of such change on their marketplace and the implications for their businesses.

Business Growth: Business leaders all share a desire to grow their business and improve their position relative to their peers and the market overall. This focus on growth often can lead to organic and inorganic initiatives such as business or business model transformation, expansion through acquisitions, rationalization of certain low-growth, non-core elements of their businesses or the selection of technologies that can alter the trajectory of their businesses.

Challenges for Leadership: Business leaders have to be vigilant in how they confront specific immediate and potential future challenges. These challenges can range from traditional business execution risk, to increased competitive risks, to funding and balance sheet constraints to shareholder initiatives or governance-related matters. These challenges are often highly complex and can be mission-critical to the success or survival of a company.

Rapidly Changing Political and Regulatory Landscape: Changes in political regimes, regulation, monetary policies, tariff policies, tax policies, environmental laws, regulations and policies, migration policies and economic stability, among others, can have a significant impact on the decisions that business leaders make to drive the success of their businesses.

The above issues are among the most important topics faced by business leaders every day, regardless of the size or the global nature of their business. In a business environment that is increasingly competitive, global, and undergoing significant transformation, we believe that business leaders will increasingly seek to partner with advisors who provide independent thought and advice to holistically navigate these opportunities and challenges and drive the long-term success of their businesses.

We believe that our collaborative partnership and integrated approach positions us well to stand by our clients and support them with independent thinking, expertise and knowledge, and that this can lead to an expanded demand for our advisory services. The principal drivers of this opportunity include:

2

Growing Demand for Independent Advice: We believe the momentum driving demand for independent advice remains strong. When we founded our Company in 2006, this dynamic was driven largely by growing client concern about conflicts at the large financial conglomerates and a growing desire by bankers to join a pure play advisory platform, all of which became increasingly apparent during the 2008 global financial crisis. In our experience, our clients value a broad approach to independence—advisors who deliver deep industry, product and technical expertise rather than offer a wide array of financial products while also acting as transaction counterparty. Since 2005, the year before our founding, the demand for independent advice has increased significantly. On average, our peer independent advisory firms advised on 66% of volume from the top 25 announced M&A transactions in the five-year period ended December 31, 2021, up from 47% on average during the five-year period ended December 31, 2005, according to Dealogic. Similarly, according to Dealogic, the estimated M&A fee pool of our peer independent advisory firms averaged $5.4 billion in the five-year period ended December 31, 2021, up from an average of $1.2 billion in the five-year period ended December 31, 2005. We expect the trend toward independent advice to continue as business leaders become increasingly experienced with the independent advisory model and believe our Company is well positioned to continue to capitalize on this trend.

Dynamic Mergers & Acquisitions Activity: We believe the M&A environment will remain active based on a variety of economic, regulatory and strategic factors, strong corporate balance sheets, significant undeployed venture and private equity capital, attractive financing markets, a rapidly accelerating trend toward global consolidation and business model transformation. However, we also see various factors which we believe could make our markets more volatile and 2022 a less active year in M&A than 2021, including rising interest rates and inflation, shifting U.S. anti-trust policy, potential tax law changes, geopolitical developments, international hostilities and other factors. In 2021 and 2020, globally announced M&A volume reached $5.8 trillion and $3.7 trillion, respectively, with approximately 71% occurring in North America and in Europe, the markets in which we are primarily focused. Dealogic estimates that the global M&A fee pool averaged approximately $30 billion annually in the five-year period ended December 31, 2021, which illustrates the large market opportunity that exists today. We believe that our Company is well positioned to further capitalize on these robust fundamentals and M&A trends, which we expect will continue to drive global growth of the financial advisory market.

Growing Demand in Liability Management (Restructuring and Capital Markets) Advisory Services: We believe that, due to large debt issuances by companies in recent years, a steady liability management (including restructuring and capital markets) advisory market will continue to exist as interest rates rise and/or credit markets become more difficult to access, even with a stable macroeconomic environment and robust M&A activity. According to Dealogic, the past nine years represented record years in volume of corporate bond issuance in the United States, as companies took advantage of historically low borrowing costs to add leverage to their capital structures. Additionally, beyond typical capital structure-related issues, we believe that the pace of business model transformation driven by a changing regulatory backdrop, and technology innovation and unanticipated shock resulting from the COVID-19 pandemic, among other factors, will lead to an entirely different wave of restructuring activity as companies consider their readiness for such change and the requirements to fund their growth and success in such an environment. We believe our integrated industry and geographic approach positions us to provide solutions to clients in both robust and challenging economic environments. We also believe that our broad industry coverage is an attractive complement to our restructuring and capital markets advisory practices due to the often uncorrelated industry-specific challenges that can lead to disruption for companies in distressed situations. Our strong positioning in each of our primary areas of industry focus and our restructuring and capital markets advisory practices diversifies our revenues and differentiates us from our peers.

Our Principles Define Our Strategy

Since our founding in 2006, we have focused on building a trust-based, focused, and high-intensity advisory business that we believe is well positioned to deliver significant value to our clients, our shareholders, and our employees.

3

Five key principles drive our approach:

Relationships are Everything to Us: We cultivate deep, long-term relationships, which transcend traditional transactional dialogue. Our clients often rely on us to assist them in assessing opportunities and challenges throughout their corporate evolution.

Partnership is at Our Core: We operate as a highly collaborative and integrated partnership defined by a culture of integrity, humility, rigor, and intensity. Working together is a critical ingredient of our success.

Focused Internationally: Since its founding, our organization has been integrated globally and is deliberately focused on the most active advisory markets worldwide. Our closely integrated partnership approach enables us to efficiently leverage our deep industry expertise with clients across geographies.

We Thrive in Complexity: We excel in complex, mission-critical situations where we can utilize our insights, experience, deep strategic thinking and personalized approach to partner with our clients to achieve their objectives.

Independence is Core to Our Character: We strive to be viewed as independent thinkers and our goal is to attract people to the Company with innovative, independent views and a willingness to speak with candor. We are not afraid to voice our perspective and are not afraid for “no” to be the right answer.

We believe these principles capture the essence of who we are and how we seek to be thought of in our markets. If we remain focused on these principles, we believe clients will continue to have the confidence to put their trust in us.

Our Key Competitive Strengths

When we founded the Company, we saw a compelling market opportunity to create a platform with deeply experienced, senior advisory professionals from the most reputable institutions around the world to focus solely on advising clients without the distractions and conflicts that may often plague senior bankers at large investment banking institutions. Over fifteen years later, we have built a leading global independent advisory platform offering a range of advisory services. Our success has been driven by the trust bestowed upon us by our clients, the high-caliber professionals who have joined the Company, and the continued growth in demand for independent advice.

We believe the primary qualities that drive our success include:

Deep Industry Insights: We believe our clients increasingly value advisors with deep industry insights when making strategic decisions that impact their businesses. These insights develop from extensive transaction experience and deep technical knowledge, and they serve as a platform for thought partnership with clients. Our primary areas of industry focus include: Consumer & Retail; Energy; Financial Institutions; Healthcare; Industrials; and Technology, Media & Telecommunications. We strive to attract and elevate individuals who are, or will be, considered thought leaders in their fields of focus. We believe our focused teams in the industries, geographies and product areas in which they specialize are leaders in their fields. We plan to continue investing in and developing professionals who will enhance our reputation as thought partners of choice to the leaders in the sectors, geographies and products on which we focus.

Independent Thought: Our foundation is rooted in a conviction, among other considerations, that clients would increasingly seek out advisors who offer independent thinking and who are not burdened by the complicated conflicts that large investment banking institutions may face due to their various businesses. We believe that our independence remains critically important and is increasingly valued by clients. We believe that our clients choose to partner with us because they value our unbiased perspectives and expert advice regarding complex financial and strategic matters, and appreciate the combination of candor and alignment of interests with their objectives that is at our core.

4

Innovation, Creativity and Ingenuity: From the very beginning, we have strived for differentiation. We seek original and exceptional ways to deliver value to our clients and to improve the way we operate. Our firm culture is an environment where colleagues are empowered to think expansively, question assumptions and pursue their ideas in an open and collaborative atmosphere. Our unique blend of innovation, creativity and ingenuity positions us well to advise on transformative and mission-critical situations for our clients.

High Standards of Integrity: We earn trust—our most important currency with clients and each other—first and foremost through integrity. We demand integrity from all of our employees in the way that they tackle their day-to-day duties, the way in which they treat clients and the way we treat each other. Integrity applies to everything we do as advisors, including the quality of the industry insights we share and our willingness to advise against transacting when an opportunity is not beneficial to our client. We demand the highest standards of integrity from all of our team members, from those hired directly out of college or business school to those with decades of experience.

Rigorous Work Ethic: As an advisory firm, the primary assets we bring to bear on any engagement are deep insights and creative ideas. However, great insights and ideas alone are not sufficient. In order for us to earn the role as a client’s advisor of choice, we must complement such insights and ideas with tireless work ethic, rigor, and intensity in everything we do in partnership with our clients. Our intensity extends throughout our business, from our junior personnel to our most experienced advisory professionals. We believe that if we can continue to maintain these standards, we will retain our reputation as a partner of choice.

We believe the attributes above are all critical components of our success. We endeavor to embody all of these attributes to maximize the value that we can create for our clients, our shareholders, and our people. We believe that our integrated approach and our partnership culture in how we work with each other and our clients provides an ideal platform to deliver the strategic and financial advice sought by our clients. We believe that if we continue to remain focused on these attributes, we will create a truly unique firm where the very best professionals prefer to work, and one that clients consistently recognize as the advisor they want by their side when it matters most.

Our Growth Strategy

Our growth strategy centers on the expansion of the depth and breadth of our advisory business in the markets we serve today and the additional markets that we may expand into in the future. This expansion will be driven by our ability to attract and develop outstanding professionals who complement or expand our market presence or broaden our advisory product offerings. Based on our partners’ expertise and client relationships, we believe our coverage presence in each of our industry sectors reaches between one-quarter and three-quarters of the relevant subsectors in the U.S. and between one-quarter and one-half of the relevant subsectors in Europe. As we execute on our growth strategy, we expect to expand our relationships with clients and the capabilities we can offer them, which will enhance our position as a leading independent advisory firm.

We plan to accomplish these goals by executing on the following strategies:

Leveraging our Existing Client Relationships: As we grow our business, we seek to deepen and expand our client relationships, which are the foundation of our Company’s success. We believe that we can accomplish this by applying a combination of our deep sector expertise, our propensity for independent thought and our tireless and intense work ethic to confront the most complex challenges that our clients face. As our relationships with clients grow, we strive to be a more integrated partner in their strategic dialogue in a manner that goes beyond traditional transactional work. We believe that this consistent, long-term approach to developing client relationships will drive superior growth potential for our Company.

5

Broadening Client Coverage in Our Markets of Focus: We have established a strong global presence in six industry sectors across which we apply our recognized M&A, capital markets and restructuring expertise to assist clients as they tackle critical decisions for their businesses. While we believe we have successfully established well-regarded practices in these core industry areas, we believe that we have substantial head room to further expand our coverage in these sectors. We intend to continue to invest in our areas of strength, and remain focused on the most relevant sectors and geographies for our business. In addition, we expect to cautiously expand our industry coverage footprint and our geographic presence in markets we believe represent a substantial commercial opportunity for the Company.

Expanding Our Advisory Capabilities to Better Serve Our Clients: We provide a range of advisory services to our clients, including strategic advisory, M&A, restructuring and capital structure advisory, capital markets advisory and energy underwriting and research. We believe we have established a reputation for the quality of our advice across these products and will continue to deepen our capabilities in the core product areas we compete in today. As we expand our client base and deepen our relationships with those clients, their need for a broader and more developed array of advisory services may grow. We plan to also invest in expanding our capabilities to provide additional advisory services where we believe such expansions can represent a compelling value proposition to our clients and an attractive commercial opportunity for us.

Investing to Drive Innovation and Insights: We believe that the market for advisory services is undergoing a period of transition away from solely transactional advice. Independent thought leadership and critical and innovative thinking are increasingly valued and expected from a trusted advisor on a continuous basis. To succeed in this new paradigm, we plan to invest rigorously in driving innovation in the way we work with clients, in the ideas that we generate for clients and in insights into the specific challenges our clients face in their target markets, taking into account, among other things, the technological disruption currently facing all industries.

Attracting, Developing and Retaining World-Class Talent to the Company: Attracting and retaining world-class talent at the Company is a critical component to our growth and to our success. We will continue to attract, develop and retain advisory professionals who seek an environment where they can collaborate to deliver excellent advice to their clients. The profiles of the people we aim to recruit are consistent in that (i) they have a strong desire to devote their full time to advising clients, (ii) they are highly committed individuals, often with a long track-record at their prior firm, (iii) they are not afraid to be honest with their clients when “no” might be the right answer, (iv) they are willing to make a long-term commitment to our Company and (v) they are committed to mentorship and investing in expanding our commitment to diversity and inclusion.

We have also put significant emphasis on the training and development of all of our professionals, and plan to continue investing meaningful resources in our human capital with commitment to investing in diversity and inclusion. As a result, we have a deep bench of internally developed talent at all levels, as evidenced by an increasing number of internal senior promotions. We believe that the combination of our efforts to internally develop professionals and to continue growing through lateral hires provides for a vibrant environment that fosters adoption of best practices and diversity.

Maintaining Discipline in How We Manage Our Business: We manage our business in an effort to deliver value creation to our shareholders. To accomplish this, we demand accountability at all levels, including our sector, product and corporate teams. This culture of accountability helps ensure that appropriate balance is in place to drive responsible profit margin expansion over time while at the same time continuing to invest in growth. We also apply opportunities for investment to drive innovation, investments in external hires and the establishment of new offices. We believe that this discipline will enable us to maintain our competitive edge while also delivering appropriate returns and long-term value creation to our shareholders.

We believe all of these factors are important to our continued success. Additionally, we believe we will benefit from growing comfort in the independent advisory model from business leaders across the sectors of the economy which we believe will expand our overall market opportunity.

6

Our Advisory Offerings

We are a leading independent provider of strategic and financial advice to clients across a range of the most active sectors and international markets. We believe that the demand for independent strategic and financial advice is growing, and that our integrated approach combining deep industry insights, significant technical, product and transactional expertise, and rigorous work ethic creates a significant opportunity for our Company. Since our founding, we have rapidly scaled our global platform. We believe clients value our ability to put their interests ahead of our own and, accordingly, will increasingly want us by their side.

Our Clients

We provide advisory services to a wide range of clients globally, including large public multinational corporations, mid-sized public and private companies, individual entrepreneurs, private and institutional investors, creditor committees and government institutions. We deliver the full resources of our Company and high level senior banker attention to every client, regardless of size or situation.

Our business provides services to multiple industry sectors and geographic markets through a broad range of advisory service offerings, which we believe offer us an opportunity to realize sustainable growth. Our primary areas of industry focus include: Consumer & Retail; Energy; Financial Institutions; Healthcare; Industrials; and Technology, Media & Telecommunications.

We complement our industry focus with extensive advisory expertise in the largest international advisory markets. We operate primarily out of ten offices in the United States, Canada, the United Kingdom (“U.K.”), France and Germany, and we have deep international experience that has enabled us to work extensively with clients worldwide. Since our inception, we have advised over 1,000 clients on transactions in over 40 countries.

We seek to generate repeat business from our clients by becoming long-term partners to them, rather than being viewed as solely transaction focused. In an effort to develop new client relationships, we maintain an active dialogue with a large number of potential clients, as well as with their financial and legal advisors, on an ongoing basis. We continue to build new relationships through our business development initiatives, proprietary client engagement (including sector or product focused conferences), growing our senior team with professionals who bring additional client relationships, and through introductions from our strong network of relationships with senior executives, board members, attorneys and other third parties. We have also grown our business through client referrals, which we proudly believe validates such clients’ satisfaction with our services.

Our Advisory Services

We seek to advise our clients throughout their corporate evolution, with the full range of our advisory capabilities. Those services include advice related to mission-critical strategic and financial decisions, M&A execution, shareholder and defense advisory, capital raising, structure and restructuring, capital markets advisory, energy underwriting and equity research.

M&A and Strategic Advisory: We have established a leading M&A and strategic advisory practice, advising clients on a range of strategic issues, risks and opportunities impacting their businesses. In these advisory relationships, we work closely with our clients through all stages of their assessment and evaluation of a range of strategic opportunities. Often, such situations can be complex and are mission-critical to the success of our client’s businesses. In these situations, we believe we have built a reputation for providing valuable insights, experience, deep strategic thinking, rigor, technical expertise and a personalized approach in our partnerships with our clients to thoughtfully achieve their objectives.

7

Liability Management and Capital Structure Advisory: We have built a leading franchise to serve the liability management market (including restructuring). Our liability management professionals partner with our industry professionals to provide holistic advice related to capital structure and potential solutions in anticipated or actual financial distress situations, including corporate workouts, Chapter 11 proceedings, and prepackaged bankruptcies. We advise both companies and creditors, utilizing our strong relationship network to access capital, identify potential partners and drive support for our transactions. We understand that during times of financial distress, having a true and trusted partner as an advisor is of critical importance, and our partnership and collaboration with our clients during these times have helped us develop long-lasting relationships.

Capital Markets Advisory: We also advise clients on capital markets matters, both in transaction-related and ordinary course financing execution. We provide comprehensive capital structure advice and help our clients develop financing solutions tailored to their specific needs. We partner with our clients to advise on all aspects of public and private debt and equity transactions. For example, we have an active private capital raising business focused on providing privately marketed and negotiated financing solutions to clients requiring substantial amounts of capital to fund growth initiatives or other specific financing needs. We believe our independence and objectivity, coupled with our deep experience in such matters, inform our market views and enhance the likelihood of a successful transaction for our clients.

Company Investments Including Special Purpose Acquisition Companies: We have a relationship with the sponsor of PWP Forward Acquisition Corp. I (“PFAC”), a special purpose acquisition company (“SPAC”) that was formed to effect a business combination with a company that is founded by, led by or enriches the lives of women. We may in the future have relationships with or invest in subsequent SPACs and similar entities. SPACs provide us with opportunities to use our expertise to assist private companies in accessing growth capital and becoming publicly-traded companies. In addition, we may in the future invest in companies, including our clients, or enter into new business lines, including alongside our clients, employees, officers and directors. We believe working with growth companies enhances our network and facilitates dialogues with other participants in those industries, and subsequently may lead to business opportunities.

Collaborations with Other Firms: The Company has entered into collaborative relationships with certain other firms, including Mizuho Securities Co., Ltd., Banco Itau BBA S.A., and CICC US Securities, Inc. Under these collaborative relationships, the Company and such other firms have expressed their non-binding intention to provide strategic advice to certain companies within applicable regions. We believe that the collaborations, while generally not exclusive, will create new opportunities for the clients of both the Company and its collaborators as they benefit from the firms’ combined experience, deep industry insights and market and regional intelligence. As part of the collaborations, the firms may second personnel to each other. The Company and its collaborators may approach applicable companies jointly and will seek to equitably share the fees earned from such clients. We are constantly evaluating the opportunity to collaborate with other organizations across disciplines to enhance our advisory service offerings to our clients.

Our Results

Since our inception, we have advised on over $1 trillion of M&A transactions with over 1,000 clients in over 40 countries across a broad range of transaction types. Our clients include large public multinational corporations, mid-sized public and private companies, individual entrepreneurs, private and institutional investors, creditor committees and government institutions. We strive to maintain long-term relationships with these clients and in many cases work with them across multiple transactions.

Some illustrations of the noteworthy transactions in which we have advised clients in recent years include:

| Large-Cap Advisory | Mid-Cap Advisory | Restructuring / Capital Markets | |||||||||||||||

| Client | Transaction | Client | Transaction | Client | Transaction | ||||||||||||

| Financial advisor to Royal Dutch Shell in connection with the $9.5B sale of Shell's Permian business to ConocoPhillips |  | Financial advisor to Quidel in connection with Quidel's $6.0B acquisition of Ortho Clinical Diagnostics |  | Financial advisor to Lufthansa in connection with its €2.1B capital increase | ||||||||||||

8

| Lead financial advisor to Baxter in connection with Baxter's $12.4B acquisition of Hillrom |  | Financial advisor to HELLA in connection with HELLA's €6.8B business combination with Faurecia |  | Financial advisor to Invitae Corporation in connection with its $1.15B Convertible Notes Offering to SB Management | ||||||||||||

| Financial advisor to Vonovia in connection with Vonovia's €29B business combination with Deutsche Wohnen |  | Financial advisor to MKS Instruments in connection with MKS's $6.5B acquisition of Atotech |  | Financial advisor to Garrett Motion in connection with its Chapter 11 process | ||||||||||||

| Advisor to the Independent Transaction Committee of Discovery, Inc. in connection with Discovery’s $22.2B business combination with AT&T’s WarnerMedia |  | Financial advisor to Luminex in connection with its $1.8B sale to DiaSorin |  | Capital markets advisor to Maravai LifeSciences on pricing of upsized Initial Public Offering | ||||||||||||

| Financial advisor to Veolia in connection with Veolia's €25.9B merger with Suez |  | Exclusive financial advisor to Kraft Heinz in connection with the $3.35B sale of its Planters brand to Hormel Foods Corporation | Independent capital markets advisor to Maravai LifeSciences on its follow-on offering of common stock | |||||||||||||

| Advisor to Owl Rock Capital Partners LP in executing a definitive business combination agreement with Dyal Capital Partners to form Blue Owl Capital Inc. and list on NYSE via a $12.5B business combination with Altimar Acquisition Corporation |  | Financial advisor to PureCycle Technologies in its merger with Roth CH Acquisition I Co. and $1.2B listing on the Nasdaq |  | Financial advisor to Royal Caribbean Cruises Ltd. in connection with multiple financing transactions across both the debt and equity capital markets | ||||||||||||

| Exclusive financial advisor to Northrop Grumman Corp. on the sale of its Federal IT and Mission Support Services Business to Veritas Capital Fund Management, LLC for $3.4B |  | Financial advisor to Precision Medicine Group, LLC in majority investment and recapitalization transaction led by The Blackstone Group Inc. |  | Advisor to the Ad Hoc Committee in Pacific Gas and Electric Company’s debt restructuring | ||||||||||||

| Exclusive advisor to Northrop Grumman Corp. in its $9.2B acquisition of Orbital ATK, Inc. |  | Financial advisor to KKR in connection with KKR's $5.3B acquisition of Cloudera |  | Financial advisor to Alta Mesa Resources, Inc. in connection with its Chapter 11 process | |||||||||||||

| Advisor to the Supervisory Board of Peugeot S.A. on its $26B merger with Fiat Chrysler Automobiles N.V. | Financial advisor to KKR & Co. Inc. on its $4.3B acquisition of a majority stake in Coty Inc.’s Professional Beauty and Retail Hair businesses and $1.0B investment in Coty Inc. in the form of convertible preferred shares |  | Financial advisor to Del Monte Foods, Inc. and Del Monte Pacific Limited on capital structure refinancing | |||||||||||||

| Sole financial advisor to Oaktree Capital Group, LLC in 62% sale to Brookfield Asset Management Inc. |  | Lead financial advisor to Invitae Corp. in connection with $1.4B business combination with ArcherDX, Inc. |  | Financial advisor to Sabre Corp. on its $1.1 billion secured and exchangeable note offerings | ||||||||||||

9

| Advisor to Altria Group, Inc. in connection with its stake in SABMiller plc’s $107B sale to Anheuser-Busch InBev SA/NV |  | Sole financial advisor to PayPal Holdings, Inc. on its $4B acquisition of Honey Science Corporation |  | Financial advisor to the Ad Hoc Group of Constitutional Debtholders on settlement with Puerto Rico Oversight and Management Board | ||||||||||||

| Advisor to Altria Group, Inc. in its $12.8B investment in JUUL Labs, Inc. |  | Advisor to Occidental Petroleum Corp. on formation of Midland Basin JV with EcoPetrol for $1.5B |  | Advisor to Legacy Reserves Inc. in its joint Chapter 11 plan of reorganization | |||||||||||||

| Financial advisor to Altria Group, Inc. on its $1.8B acquisition of Cronos Group Inc. |  | Exclusive financial advisor to Cantel Medical Corp. on its $775M acquisition of Hu-Friedy Mfg. Co. |  | Exclusive financial advisor to the Special Committee of the WeWork Board of Directors | |||||||||||||

| Advisor to E.ON SE in its $54B acquisition of innogy SE and exchange of assets with RWE AG |  | Exclusive advisor to SodaStream International, Ltd. in its $3.2B sale to PepsiCo Inc. |  | Advisor to one of the largest creditors in Sears, Roebuck and Co.’s debt restructuring | ||||||||||||

| Lead advisor to Becton, Dickinson and Co. in its $24B acquisition of C.R. Bard, Inc. |  | Advisor to Apache Corporation in the $3.5B formation of Altus Midstream LP |  | Advisor to iHeartMedia, Inc. independent directors | ||||||||||||

Our Commitment to Environmental, Social and Governance Leadership

We believe that leadership in the Environmental, Social and Governance (“ESG”) issues is a central element of our Company’s mission because our success is tied to how responsibly and sustainably we run our business. Over the past few years, we have taken steps to oversee and manage business-relevant ESG factors that impact the long-term interests of our stakeholders, such as engaging our employees and promoting a diverse and inclusive workplace, safeguarding our data through a cybersecurity program, and adhering to what we consider to be best practices in corporate governance and risk assessment and mitigation. Our board of directors, as well as our management team, provide direction and oversight with respect to the evolving priorities of our Company’s ESG initiatives, organized into three pillars, which, in turn, contain focus areas for our attention and action:

•Environmental. The Environmental pillar is focused on assessing and monitoring our environmental footprint, and proactively raising our firm-wide awareness of environmental risk and opportunity by committing to sustainable practices to oversee environmental aspects in our business activities.

•Social. The Social pillar is focused on promoting diversity and inclusion, reinforcing our commitment to engage, develop and motivate our employees, and maintaining a rigorous cybersecurity program to protect our valuable data.

•Governance. The Governance pillar is focused on upholding our commitment to ethical business conduct, professional integrity and corporate responsibility by integrating strong governance and enterprise risk management oversight across all aspects of our business.

Our People and Inclusive Culture

We believe that our people are our most valuable asset. Our goal is to attract, develop and retain the best and brightest talent in our industry across all levels. We strive to foster a collaborative environment, and we seek individuals who are deeply committed to their clients, passionate about our business and additive to our culture.

Since our founding we have experienced significant growth of our team. At founding in 2006, we began the Company with 16 advisory professionals, including ten advisory partners. By 2010, we had grown our Company to 137 advisory professionals, including 24 advisory partners. By 2014, we had grown our Company to 183 advisory professionals, including 32 advisory partners. As of December 31, 2021, we serve our clients with 422 advisory professionals, including 60 advisory partners (which numbers include two advisory partners who retired from the Company in January 2022), based in ten offices, located in five countries around the world.

10

The drivers of the growth of the Company include a combination of internal promotions, lateral recruiting in our areas of focus and, in the case of the TPH Business Combination (as defined below), the addition of a substantial number of new partners and advisory professionals through a business combination. In addition to this promotion and addition of external hires, we have also maintained significant discipline in how we assess our advisory professionals within our culture and our strategic and financial objectives. Accordingly, we have developed a comprehensive internal review process and significantly evolved the partnership over our history. Today, we believe we have established a rigorous recruiting and review process that ensures that we maintain consistently high levels of performance and of quality among our advisors, which best positions us to serve our clients and their growing advisory needs.

Our partners are compensated based on their overall contribution to value creation for our Company. Contribution includes, among other things, the quality of advice and execution provided to clients, intellectual content and thought leadership, the financial contribution to the Company, the commitment made to recruiting new talent, the creation of an inclusive work environment and the overall spirit of partnership they demonstrate in working with their colleagues and their clients. We do not compensate on a commission-based pay model, whereby bankers are rewarded solely based upon financial contribution. We believe that our compensation model encourages a collaborative environment and attracts talented advisory professionals to join our Company.