As filed with U.S. Securities and Exchange Commission on September 3, 2020.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Green Grass Ecological Technology Development Co., Ltd.

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

| Cayman Islands | 700 | Not Applicable | ||

| (State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer | ||

| incorporation or organization) | Classification Code Number) | Identification number) |

9th Floor, Lvdi Zhihai Tower A3

North Kerqin Road, Nandian Street, Xincheng District

Huhe Haote City, Inner Mongolia 010000

Tel: + (86) 471-5287999

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Cogency Global Inc.

122 East 42nd Street, 18th Floor

New York, NY 10168

Phone: (800) 221-0102

Fax: (800) 944-6607

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Jeffrey

Li Foster Garvey, P.C. Flour Mill Building 1000 Potomac Street NW, Suite 200 Washington, D.C. 20007-3501 (202) 298-1735 |

Approximate date of commencement of proposed sale to the public: as soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to section 7(a)(2)(B) of the Securities Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Calculation of Registration Fee

| Title of Class of Securities to be Registered | Amount to Be Registered | Proposed Maximum Offering Price per Share | Proposed Maximum Aggregate Offering Price (1) | Amount of Registration Fee | ||||||||||||

| Ordinary shares, par value $0.0001 per share(2) | — | $ | — | $ | 23,000,000 | $ | 2,985.40 | |||||||||

| Underwriter Warrants(3) | — | $ | — | $ | — | $ | — | |||||||||

| Ordinary shares underlying Underwriter Warrants(2) (4) | — | $ | — | $ | 1,322,500 | $ | 171.66 | |||||||||

| Total | — | — | $ | 24,322,500 | $ | 3,157.06 | ||||||||||

| (1) | The registration fee for securities to be offered by the Registrant is based on an estimate of the Proposed Maximum Aggregate Offering Price of the securities, and such estimate is solely for the purpose of calculating the registration fee pursuant to Rule 457(o). |

| (2) | In accordance with Rule 416(a), the Registrant is also registering an indeterminate number of additional ordinary shares that shall be issuable pursuant to Rule 416 to prevent dilution resulting from share splits, share dividends or similar transactions. Includes ______ ordinary shares which may be issued upon exercise of the underwriters’ over-allotment option. |

| (3) | In accordance with Rule 457(g) under the Securities Act, because the registrant’s ordinary shares underlying the Underwriter’s warrants (“Underwriter Warrants”) are registered hereby, no separate registration fee is required with respect to the warrants registered hereby. |

| (4) | As estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(g) under the Securities Act. We have agreed to issue to the representative of the underwriters, upon closing of this offering, the Underwriter Warrants exercisable for a period of five years from the effective date of this registration statement entitling the representative to purchase up to 5% of the number of shares sold in this offering at a per share exercise price equal to 115% of the public offering price. The Registration Statement of which this prospectus is a part also covers ordinary shares issuable upon the exercise thereof. See “Underwriting.” As estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(g) under the Securities Act, the proposed maximum aggregate offering price of the ordinary shares underlying the Underwriter Warrants is $__________ (which is equal to 115% of $______ multiplied by ______ shares). |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS (Subject to Completion) | Dated September 3, 2020 |

__ Ordinary Shares

Green Grass Ecological Technology Development Co., Ltd.

This is the initial public offering of our ordinary shares. We are offering __ ordinary shares. We expect the initial public offering price of the shares to be between $__ and $__ per share. Currently, no public market exists for our ordinary shares. We have applied to have our ordinary shares listed on the Nasdaq Capital Market (“Nasdaq”) under the symbol “QQCY.”

We are an “emerging growth company,” as that term is used in the Jumpstart Our Business Startups Act of 2012, and will be subject to reduced public company reporting requirements.

Investing in our ordinary shares is highly speculative and involves a significant degree of risk. See “Risk Factors” beginning on page 13 of this prospectus for a discussion of information that should be considered before making a decision to purchase our ordinary shares.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

| Public offering price | $ | $ | ||||||

| Underwriting discount | $ | $ | ||||||

| Proceeds to us, before expenses | $ | $ | ||||||

| (1) | The underwriter will receive compensation in addition to such discount and commissions as set forth under “Underwriting.” |

We have granted the placement agent a 45-day option to purchase up to an additional __________ ordinary shares at the public offering price, less the placement discount, to cover any over-allotments.

The underwriter expects to deliver the ordinary shares against payment as set forth under “Underwriting”, on or about ●, 2020.

The date of this prospectus is ●, 2020

| TABLE OF CONTENTS | |

| Page | |

| PROSPECTUS SUMMARY | 1 |

| RISK FACTORS | 13 |

| SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS | 40 |

| USE OF PROCEEDS | 41 |

| CAPITALIZATION | 42 |

| DILUTION | 43 |

| EXCHANGE RATE INFORMATION | 44 |

| ENFORCEABILITY OF CIVIL LIABILITIES | 45 |

| SELECTED CONSOLIDATED FINANCIAL AND OPERATING DATA | 46 |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 47 |

| 66 | |

| BUSINESS | 68 |

| MANAGEMENT | 82 |

| PRINCIPAL SHAREHOLDERS | 86 |

| RELATED PARTY TRANSACTIONS | 87 |

| DESCRIPTION OF SHARE CAPITAL | 88 |

| SHARES ELIGIBLE FOR FUTURE SALE | 93 |

| TAXATION | 95 |

| UNDERWRITING | 101 |

| EXPENSES RELATING TO THIS OFFERING | 107 |

| LEGAL MATTERS | 107 |

| EXPERTS | 107 |

| WHERE YOU CAN FIND ADDITIONAL INFORMATION | 107 |

| INDEX TO CONSOLIDATED FINANCIAL STATEMENTS | F-1 |

|

You should rely only on the information contained in this prospectus or in any related free-writing prospectus. We have not authorized anyone to provide you with information different from that contained in this prospectus or any free-writing prospectus. We are offering to sell, and seeking offers to buy, the ordinary shares only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is current only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of the ordinary shares. | |

i

This summary highlights certain information contained elsewhere in this prospectus. You should read the entire prospectus carefully, including our financial statements and related notes and the risks described under “Risk Factors” beginning on page 13. We note that our actual results and future events may differ significantly based upon a number of factors. The reader should not put undue reliance on the forward-looking statements in this document, which speak only as of the date on the cover of this prospectus.

All references to “we,” “us,” “our,” “Company,” “Registrant” or similar terms used in this prospectus refer to Green Grass Ecological Technology Development Co., Ltd, an exempted company incorporated under the laws of the Cayman Islands (“QQCY” or “Green Grass Cayman”), including its consolidated subsidiaries and variable interest entities (“VIEs”), unless the context otherwise indicates. We currently conduct our business through Inner Mongolia Green Grass Yuan Ecological Technology Development Co., Ltd. (“IMGG”) and Beijing Rongshiyuan Ecological Technology Development Co., Ltd. (“BRE”), our operating entities in China.

“PRC” or “China” refers to the People’s Republic of China, excluding, for the purpose of this prospectus, Taiwan, Hong Kong and Macau, “RMB” or “Renminbi” refers to the legal currency of China and “$”, “US$” or “U.S. Dollars” refers to the legal currency of the United States.

Our Business

We are currently engaged in the businesses of specialty agriculture farming of alfalfa, wasteland transformation, agriculture harvesting services and biomass raw materials (straw and agriculture residue) collection and processing for power plants and paper mills.

We signed contracts with the local counties of Feng Zhen City in the Inner Mongolian Autonomous Region for use rights to mostly abandoned and wastelands comprising 74,220 mu or 12,228 acres (approximately 50 square kilometers) in August 2013. We grow and farm alfalfa on these lands that lack water resources or are far from the villages and cannot be farmed without modern technologies and machinery. We obtain the contractual rights for the use of these abandoned and wastelands from the local government through a land use rights transfer process at a much lower cost than normal market prices. We then use biological and engineering measures to construct desertification protection systems for these wastelands, and use drip technologies to efficiently utilize the available water resources to grow alfalfa.

Alfalfa is a perennial herb and its strong and deep roots could bind organic substances to the soil. It absorbs calcium and breaks down phosphates and deposits them in the soil to decompose into organic colloids, which can stabilize the soil and improve its chemical and physical conditions. Alfalfa roots can retain the nitrogen from the surrounding air to increase soil fertility. Usually, Alfalfa can be harvested 3 times annually.

Alfalfa is a preferred feed for livestock and fresh alfalfa is a top choice for cattle. It can also be processed as hay, hay meal or with a mixture of other animal feeds. High-quality alfalfa is essential for the production of organic milk and for the livestock farming, including cattle, sheep and pigs. More than 50 percent of China’s supply of alfalfa comes from the United States. Inner Mongolia is the province with the highest consumption of high-quality alfalfa in China, and its milk output accounts for about one fifth of China’s total. High quality alfalfa products are in short supply in Inner Mongolia and China, and there is a large market for our alfalfa products, as a substitute for imports. Our alfalfa in Feng County have three harvests a year (early June, mid-July and early October) with hay production between 3,642 and 6,070 kg per acre. We sell our alfalfa hay in two ways: (i) on-site sales at our fields and (ii) finished products sales, shipping out of our warehouse. Customers can review the color of alfalfa hay and test the moisture content of the products to select the product they would like to buy. The quality of our alfalfa products has reached the quality level of imported products, and our sales price is 15% to 20% lower than that of comparable imported products. Currently our alfalfa products are in short supply.

We own large agricultural machinery and equipment and are well-equipped to operate on a modern agriculture production scale, compared to most farmers in China. The degree of our mechanization and automation operations has reached the level of similar farming companies in the United States. We own John Deere (USA) tractors and CLAAS (Germany) tractors, KUHN (France) precision seed drillers, KUHN field mowers, KUHN rake machines, KUHN large square balers, a KUHN wind wrap machine, KUHN fertilizer spreaders, KUHN hydraulic turnover plows, KUHN power driven harrows, KUHN subsoilers, and KUHN fertilizer application machines. We also own other ancillary machines, such as hydraulic folding press machines; graders; grass grabbers; folding joint preparation machines; loaders; holding clamp machines; spray machines; movable generators; soil preparation machines; fertilizer application machines; rotary tillers; trenching machines; and planer graders.

Our agricultural machinery and equipment cover the full range from initial land preparation and planting to harvesting and transportation, and meet the requirements of modern agricultural machinery operation and efficiency. Our agricultural machinery and equipment not only ensure the consistency of our yield and quality control for our own products, but also can be used to provide harvesting services to other famers in China. Also, we have a fleet of transportation vehicles such as large flat transport vehicles, fuel trucks, a 55-ton large oil storage tank, and a pickup truck for both passenger and cargo, which can effectively serve our logistical needs.

1

We do not lease our harvesting equipment and other agricultural machinery to other growers but use them as a part of our harvesting services, i.e. our operators will operate these equipment and agricultural machinery to harvest alfalfa, wheat or corn for other growers. Because these agricultural machinery are expensive and require trainings before operation, we only allow our own operators to operate these agricultural machinery and charge fees for such harvest services. Our services include crop harvesting, packing and baling and transporting them to designated warehouses. Our service fee varies depending on the service items, harvest areas, time schedule and travel distance.

Our service team provides inter-state services for an operating radius of more than 2,000 kilometers. We have approximately 50 experienced professional operators of our large imported machinery, who each have 5 to 10 years of machine operation experience and long distance cross-provincial operation experience. Our agriculture harvesting services have served farmers in Shandong Province, Heilongjiang Province, Xinjiang Autonomous Region, Liaoning Province, Jilin Province, Anhui Province, Henan Province, Ningxia Autonomous Region and Shanxi Province, as well as in our own home state, Inner Mongolian Autonomous Region.

As of December 31, 2019, we had accumulatively spent approximately $6.5 million of the agricultural machinery and equipment that we used in our farming business. In addition, we spent approximately $2.7 million, $3.1 million and $3.0 million for the six months ended December 31, 2019 and for the years ended June 30, 2019 and 2018, respectively, of maintaining mechanization and automation in our farming business.

We have our own mechanical staffs who maintain our equipment and machinery, replace wearing and spare parts and make oil changes as a part of daily operations. With good maintenance, we do not expect any major repair to existing machinery or costs to acquire new equipment in the near future. If we have to make any major repair or replace any of our agricultural machinery, it will have negative impact on our operation and financial result due to reduce of productivity and increase of the expenses.

The increased automation allow us to operate our alfalfa and biomass business in large scales. Without large agricultural machinery, it is costly and physically impossible to grow, manage, harvest, pack, process and transport alfalfa and straws in large farm land and provide harvest services to small growers. With these agricultural machinery, we create scale effect and meet demands of large customers for their needs of alfalfa and biomass materials at a competitive price compared to less automated competitors.

Another main business of ours is to process and sell biomass waste and residues to power generation plants and paper mills, mainly corn and wheat straws. The straws are the waste and residue from the agriculture industry after harvesting of the crops. We purchase and collect the straws from local farmers, then cut, pack and sell them to the biomass power plants or paper mills as the raw materials for their production. It is expensive and time consuming for farmers to collect and process these straws. Traditionally, Chinese farmers pile such agricultural waste up in their fields and burn it, which has been a main cause of the air pollution in China, and also increases the risk of forest fires.

With the strong air pollution control laws and regulations currently in China, burning agricultural waste and residue is strictly prohibited and there is 24/7 satellite monitoring and enforcement. Farmers are fined for violations, or criminally penalized if the violation is serious. Also, local government officials can be held accountable for any such violations in their jurisdiction by the central government.

Straw is a renewable energy source. The caloric value of every two tons of straw is equivalent to one ton of standard coal, and its average sulfur content is only 0.38%, while the average sulfur content of coal is about 1%.

We own full sets of highly efficient machinery and equipment to collect, process and dispose of agricultural waste and residue. We sell such biomass products to biomass power generation plants to generate electricity, as well as to the paper mills as alternative raw material in place of wood and wood pulp.

Currently, we conduct combined harvesting, processing, packaging, storage and transportation of straw, mainly of corn straw in three provinces in northeast China (Heilongjiang, Liaoning and Jilin provinces) and wheat straw in four provinces (Anhui, Henan, Shandong and Hebei provinces). We are in the process of assembling a straw biomass cleaning production line and we expect to add an additional value-added service to pre-clean the biomass raw materials before turning them to our customers once we completed our assembling and final testing phase of the production line.

In November 2017, we entered into a cooperative contract with one of the biomass power plants of Guoneng Biomass Power Generation Group Co. Ltd. (“Guoneng”), a subsidiary of the State Grid. In April 2019, we entered into three more cooperative contracts with three additional biomass power plants of Guoneng. Pursuant to the cooperative contracts, we will purchase and collect the straws from local farmers, process such straws including dust removal and sell them to the power plants. The four biomass power plants have agreed to purchase all the straw we can supply for its power generation plants all year long. Guoneng owns 41 biomass power plants in operation and the total demand of 41 power plants is approximately 13.5 million tons per year. We currently can only supply approximately 400,000 tons per year, leaving substantial room for growth.

We also process straw and agricultural residue and sell biomass products to paper mills as raw material. According to China’s National Bureau of Statistics, from early September 2016 to mid-October 2017, pulp prices increased by 56.77% to RMB 6,550.6 ($1,008) per ton, and corrugated paper prices increased by 126.21% to RMB 5,730 ($882) per ton.

2

In 2019, the paper and cardboard production volume in China was 107.65 million tons and consumption in China was 107.04 million tons.

The paper mills have been using a new process of straw paper manufacturing, in which no chemicals are used in the production process. The biomass wastes are fermented and decomposed using bacterial liquid, such that the paper products manufactured in this way meet the safety and health requirements for food contact packing paper.

On January 8, 2020, we established a not-for- profit training school to provide trainings of agricultural skills and technologies to local farmers, such as driving and maintenance of agricultural machinery, modern agriculture technologies, cultivation and pest control of fruit trees, livestock farming, plant protection, conservation of water and soil. Through such training school, we hope to help local farmers obtain new skills for modern agriculture industry, increase income and come out of poverty. The training school could also supply us with much needed and well trained potential employees for our business development. We do not charge any tuition to the students and the local government provides certain subsidies to each farmer we successfully train.

Our Strategy

We plan to continue to expand our business in specialty alfalfa farming, wasteland transformation, agricultural harvesting services, and biomass raw materials (straw and agricultural residue) collection and processing for power plants and paper mills. We will continue to market our products and services to attract more clients through referrals from existing clients and through offline marketing methods, and we also plan to build and use an online platform for various marketing campaigns, attracting and expediting order processing, increasing our reputation and influence in the industry, and building our brand recognition in China. However, there is no guarantee that our expansion plans will be successful. We plan to implement the following strategies:

| ● | Obtain development and use rights of wasteland at a lower cost from local governments and grow more high quality alfalfa products to supply livestock and cattle farmers in Inner Mongolia and other Chinese provinces. |

| ● | Develop our biomass business by entering into long-term supply contracts with five major state owned power companies, which control a total of 499 biomass power generation plants; |

| ● | Develop our biomass business with more major paper mills in China and enter into long-term supply contracts with these paper mills; |

| ● | Expand our biomass waste and raw material collection operations into additional major agricultural provinces in China, such as Heilongjiang and Xinjiang Provinces; |

| ● | Expand our biomass raw materials of rice straw, caragana korshinskii, cotton, reed and sugarcane tops; and |

| ● | Expand our agricultural harvesting services business and expand into the southern provinces of China, which have different weather conditions and harvest seasons than our current markets in the northern provinces of China, thus reducing the idle time for our machines and operators. |

Our Strengths

We believe that the following strengths differentiate us from our competitors and provide us with advantages for realizing the full potential of our market opportunity:

| ● | We own large imported agricultural machines and equipment from the U.S., France and Germany and are well-equipped to operate on a modern agricultural production scale, compared to most farmers in China. The degree of mechanization and automation of our operations has reached the level of similar farming companies in the United States. We are more efficient in operations and cost savings than other farmers in China. |

| ● | Using large agricultural machines and equipment improves the efficiency and reduces the cost for our alfalfa farming, however, the minimum land requirements to use such large machinery is at least 5,000 mu (3.33 square kilometers). With the current land use policies, most farmers in China do not have use rights to enough land to operate large machinery, whereas we have use rights to 70,000 mu of land. The imported large agriculture machines are expensive, and cost approximately $1.5 million to $2 million, rendering them cost-prohibitive to most farmers in China. |

| ● | We use drip technology to irrigate our crops. This technology irrigates based on the actual needs of the crop, using a pipeline and tube to gradually drip water and nutrition drop by drop evenly to the root area of the crops. Such irrigation methods will not damage the soil structure, cause less evaporation and almost no surface flow or deep layer leaks, and are a water saving method which is best for areas susceptible to water shortages and helps ensure the growth of alfalfa during drought seasons. However, the dripping irrigation system is expensive to set up initially: pipes must be buried at 60 centimeter intervals and one square kilometer land requires 1,667 kilometers of irrigation pipeline, which is cost-prohibitive for small farmers; |

3

| ● | We have approximately 50 trained and experienced professional operators of our large imported machinery, each of whom has 5 to 10 years of machine operation experience and long distance cross-provincial operation experience. |

| ● | There are barriers to entry for agriculture biomass collection and process businesses, and there are almost no large professional agriculture biomass raw material supply companies, due to various factors, including that (i) a machine operation team with a daily output of 400 to 500 tons of straw requires an equipment investment of approximately RMB 8 to 10 million ($1.23-1.54 million), which is prohibitive for ordinary farmers or small companies; (ii) the equipment only operates in summer and autumn (e.g. during the harvest seasons), and is idle during most of the winter and spring, therefore, such business might not be economical for a pure agriculture biomass processing company without diversified agriculture businesses and other income resources; (iii) the operations require thorough management of production procedures, and specialized equipment operation skills, and the equipment and machines require constant maintenance and parts support; (iv) the farmers require cash payments to purchase their straw and accounts receivable take time, and the business requires large investment and cannot be done without substantial liquidity. Diversified channels to reach borrowers and investors are also required. |

| ● | We have established large, long-term clients such as biomass power plants under the State Grid and publicly traded paper companies, which expect to buy our entire supply based upon our current capacity. |

| ● | Our business is an environmentally friendly business, which aids in reducing CO2 emissions and increase income for rural low income farmers, by purchasing their agricultural waste which was formerly burned, resulting in practices which are strongly encouraged and supported by local governments. |

| ● | We have an experienced and strong management team. |

Our Challenges

We face challenges and uncertainties in realizing our business objectives and executing our strategies, including the following:

1. Fire accidents. Our products, alfalfa hay and straw, are highly flammable. Any fire accidents would materially affect our business.

2. The price of alfalfa hay in international markets, especially in the U.S. Currently, approximately 40% of high quality alfalfa consumed in China is imported, mostly from the U.S. We currently use alfalfa seeds imported from the U.S. Although the sale price of domestic alfalfa hay is 15-20% lower than similar imported products, any price and supply/demand change in international markets will impact our business.

3. Any changes in the livestock and cattle industry, such as the number of cattle, will affect our business.

4. Quantity and quality of agriculture biomass. There is a seriously insufficient supply of biomass straw for power plants and paper mills and we mainly purchase the straw from individual farmers. We supplement our supply with certain cooperative farmers associations, and the quality of biomass waste is not consistent. The impurities and dust of raw biomass waste materials might be excessive, which could be harmful to power generation systems and paper mill facilities and seriously affect the stable production of the plants/mills. We have invested in and installed the systems at the biomass power plants to filter out the impurities and remove the excessive dust to ensure the product quality, which increases our cost.

5. Obtaining more land use rights in China is a long and laborious process, which we would need to engage in if and when we expand our alfalfa farming business.

We face additional risks and uncertainties related to our corporate structure and the regulatory environment in China. Please see “Risk Factors” and other information included in this prospectus for a discussion of these and other risks and uncertainties that we face.

4

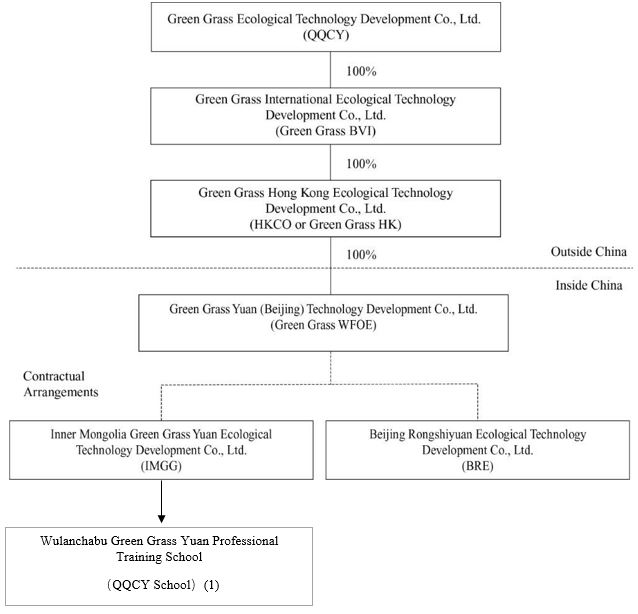

Corporate History and Structure

We began our operations in China through the Inner Mongolia Green Grass Yuan Ecological Technology Development Co., Ltd. (“IMGG”), which was incorporated in the Inner Mongolia Autonomous Region of China in May 2013. On April 28, 2019, Beijing Rongshiyuan Ecological Technology Development Co., Ltd. (“BRE”) was incorporated. On May 10, 2019, we incorporated the Green Grass Ecological Technology Development Co., Ltd. under the laws of the Cayman Islands as our offshore holding company. On May 15, 2019, we incorporated Green Grass International Ecological Technology Development Co., Ltd., our wholly owned British Virgin Islands subsidiary (“Green Grass BVI”), which established a wholly owned subsidiary in Hong Kong (“HK Co” or “Green Grass HK”) on May 30, 2019. Green Grass HK incorporated a wholly foreign owned enterprise, Green Grass Yuan (Beijing) Technology Development Co., Ltd. in PRC (“Green Grass WFOE”) on August 15, 2019. On September 6, 2019, Green Grass WFOE entered into a series of contractual arrangements, or VIE agreements with IMGG, 98% equity shareholders of IMGG (“IMGG Shareholders”), BRE and all equity shareholders of BRE (“BRE Shareholders”), through which we have obtained control and become the primary beneficiary of IMGG and BRE. These contractual arrangements allow us to effectively control and derive 100% of the economic interest from IMGG and BRE. On January 8, 2020, IMGG established Wulanchabu Green Grass Yuan Professional Training School (“QQCY School”) as a private non-enterprise entity for the training of driving and maintenance of agricultural machinery, modern agriculture technologies, cultivation and pest control of fruit trees, livestock farming, plant protection, conservation of water and soil. The QQCY School is a not-for-profit entity. The incorporation of Green Grass HK, Green Grass WFOE and execution of VIE agreements mentioned above are collectively referred as “Restructuring.”

The following diagram illustrates our corporate structure, including our principal subsidiaries and consolidated variable interest as of the date of this prospectus upon the completion of our Restructuring as mentioned above, which will be completed prior to the closing of this offering. For more information, see “Business—Our Corporate History and Structure”.

|

Equity Control |

|

Contractual Arrangements |

|

Sponsorship Control |

| (1) | Mr. Jian Sun is the principal of Wulanchabu Green Grass Yuan Professional Training School, the sponsorship interests of which is 100% held by IMGG. |

5

Foreign Private Issuer Status

We are a foreign private issuer within the meaning of the rules under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). As such, we are exempt from certain provisions applicable to United States domestic public companies. For example:

| ● | we are not required to provide as many Exchange Act reports, or as frequently, as a domestic public company; |

| ● | for interim reporting, we are permitted to comply solely with our home country requirements, which are less rigorous than the rules that apply to domestic public companies; |

| ● | we are not required to provide the same level of disclosure on certain issues, such as executive compensation; |

| ● | we are exempt from provisions of Regulation FD aimed at preventing issuers from making selective disclosures of material information; |

| ● | we are not required to comply with the sections of the Exchange Act regulating the solicitation of proxies, consents or authorizations in respect of a security registered under the Exchange Act; and |

| ● | our insiders are not required to comply with Section 16 of the Exchange Act requiring such individuals and entities to file public reports of their share ownership and trading activities and establishing insider liability for profits realized from any “short-swing” trading transaction. |

Variable Interest Entity Arrangements

In establishing our business, we have used a variable interest entity, or VIE, structure. In the PRC, investment activities by foreign investors are principally governed by the Guidance Catalog of Industries for Foreign Investment, which was promulgated and is amended from time to time by the PRC Ministry of Commerce, or MOFCOM, and the PRC National Development and Reform Commission, or NDRC. In June 2018, the Guidance Catalog of Industries for Foreign Investment was replaced by the Special Administrative Measures (Negative List) for Foreign Investment Access (2018 Version) which was amended by the Special Administrative Measures (Negative List) for Foreign Investment Access (2019 Version) in June 2019. In June, 2020, the MOFCOM and the NDRC promulgated the Special Administrative Measures (Negative List) for Foreign Investment Access (2020 Version), or the Negative List, which became effective on July 23, 2020. The Negative List divides industries into two categories: restricted and prohibited. Industries not listed in the Negative List are generally open to foreign investment unless specifically restricted by other PRC regulations. Our Company and the WFOE are considered as foreign investors or foreign invested enterprises under PRC law.

The business we conduct through our each variable interest entity may be within the category which foreign investment is currently restricted under the Negative List or other PRC Laws. In addition, we are centralizing our management and operation in the PRC without being restricted to conducting certain business activities which are important for our current or future business but are restricted or might be restricted in the future. As such, we believe the agreements between the WFOE and each variable interest entity are necessary and essential to our business operations. These contractual arrangements with each variable interest entity and its shareholders enable us to exercise effective control over the variable interest entities and hence consolidate their financial results as our VIE.

In our case, the WFOE effectively assumed management of the business activities of each our variable interest entity through a series of agreements which are referred to as the VIE Agreements. The VIE Agreements are comprised of a series of agreements, including Technical Consultation and Service Agreements, Equity Pledge Agreements, Equity Option Agreements, and Voting Rights Proxy and Finance Supporting Agreements. Through the VIE Agreements, the WFOE have the right to advise, consult, manage and operate the variable interest entities for an annual consulting service fee in the amount of 98% of IMGG’s net income and in the amount of 100% of BRE’s net income. 98% shareholders of IMGG and 100% shareholders of BRE (the “VIE Shareholders”) have pledged their right, title and equity interests in the variable interest entities as security for the WFOE to collect consulting services fees provided to the variable interest entities. In order to further reinforce the WFOE’s rights to control and operate the variable interest entities, the VIE Shareholders have granted the WFOE an exclusive right and option to acquire all of their equity interests in the variable interest entities through the Equity Option Agreement.

6

Variable Interest Entity Arrangements with IMGG

We entered into the contractual arrangements with IMGG upon consummation of the Restructuring on September 6, 2019 and have effectively control of IMGG through a series of contractual arrangements as follows:

Technical Consultation and Service Agreement. Pursuant to the Technical Consultation and Service Agreement between Green Grass WFOE and IMGG, Green Grass WFOE has the exclusive right to provide consultation and services to IMGG in the area of human resources, technology and intellectual properties. For such services, IMGG will agree to pay service fees in the amount of 98% of its net income and also has the obligation to absorb 98% of IMGG’s losses. Green Grass WFOE exclusively owns any intellectual property rights arising from the performance of this Technical Consultation and Service Agreement. The amount of service fees and payment term may be amended by Green Grass WFOE and IMGG upon consultation. The term of the Technical Consultation and Service Agreement is 20 years, which could be extended if Green Grass WFOE gives its written consent to the extension of the agreement before its expiration and IMGG shall agree with such extension without any reservation. Green Grass WFOE has the right to terminate this agreement at any time by giving 30 days’ written notice to IMGG.

Equity Pledge Agreement. Pursuant to an Equity Pledge Agreement among Green Grass WFOE, IMGG and IMGG VIE Shareholders, IMGG VIE Shareholders pledged their equity interests in IMGG to Green Grass WFOE to guarantee IMGG’s performance of relevant obligations and indebtedness under the Technical Consultation and Service Agreement. In addition, IMGG VIE Shareholders have completed the registration of the equity pledge under the Equity Pledge Agreement with the competent local authority. If IMGG breaches its obligation, Green Grass WFOE, as pledgee, is entitled to certain rights, including the right to dispose the pledged 98% equity interests in order to recover these breached amounts. The Equity Pledge Agreement is continuously valid until all of the IMGG VIE Shareholders are no longer shareholders of IMGG.

Equity Option Agreement. Pursuant to an Equity Option Agreement among Green Grass WFOE, IMGG and IMGG VIE Shareholders, Green Grass WFOE has the exclusive right to require the IMGG VIE Shareholders to fulfill and complete all approval and registration procedures required under PRC laws for Green Grass WFOE to purchase, or designate one or more persons to purchase, IMGG VIE Shareholders’ equity interests in IMGG, once or at multiple times at any time in part or in whole at Green Grass WFOE’s sole and absolute discretion. The purchase price is the lowest price allowed by PRC laws (currently estimated to be RMB 1.00). If the purchase price is higher than RMB 1.00 to comply with applicable PRC laws, IMGG shall exempt Green Grass WFOE from the obligation of payment and agree that Green Grass WFOE will not be required to fulfill the payment obligation. The Equity Option Agreement remain effective until all the equity interest owned by each of the IMGG VIE Shareholders has been legally transferred to Green Grass WFOE or its designee(s).

Voting Rights Proxy and Finance Supporting Agreement. Pursuant to the Voting Rights Proxy and Finance Supporting Agreements among Green Grass WFOE, IMGG and IMGG VIE Shareholders, each of IMGG VIE Shareholders has irrevocably appointed Green Grass WFOE or Green Grass WFOE’s designee to exercise all his or her rights as an IMGG VIE Shareholder under the Articles of Association of IMGG, including but not limited to (1) proposing to hold a shareholders’ meeting, (2) the power to exercise all shareholder’s voting rights with respect to all matters to be discussed and voted in the shareholder’s meeting of IMGG, (3) exercising other voting rights the shareholders are entitled to under the laws of PRC promulgated from time to time, and (4) exercising other voting rights the shareholder is entitled to under the Articles of Association of IMGG, as may be amended from time to time. In addition, Green Grass WFOE agreed to arrange for funds to be provided as necessary to IMGG in connection with IMGG’s business (the “Financial Support”) and agreed that, should the business fails in the ordinary course of business, and as a result IMGG is unable to repay the Financial Support, IMGG shall have no repayment obligation. The term of the Voting Rights Proxy and Finance Supporting Agreements is 20 years, which may be extended by Green Grass WFOE through its written consent to the extension of the agreement before its expiration, and IMGG and IMGG VIE Shareholders also agree to the extension without reservation.

7

Variable Interest Entity Arrangements with BRE

We have entered into the contractual arrangements with BRE upon consummation of the Restructuring on September 6, 2019 and have effectively control of BRE through a series of contractual arrangements as follows:

Technical Consultation and Service Agreement. Pursuant to the Technical Consultation and Service Agreement between Green Grass WFOE and BRE, Green Grass WFOE has the exclusive right to provide consultation and services to BRE in the area of human resources, technology and intellectual properties. For such services, BRE agreed to pay service fees in the amount of 100% of its net income and also has the obligation to absorb 100% of BRE’s losses. Green Grass WFOE exclusively owns any intellectual property rights arising from the performance of this Technical Consultation and Service Agreement. The amount of service fees and payment term may be amended by Green Grass WFOE and BRE upon consultation. The term of the Technical Consultation and Service Agreement is 20 years, which may be extended if Green Grass WFOE gives its written consent to the extension of the agreement before its expiration and BRE shall also agree such extension without reservation. Green Grass WFOE has the right to terminate this agreement at any time by giving 30 days’ written notice to BRE.

Equity Pledge Agreement. Pursuant to an Equity Pledge Agreement among Green Grass WFOE, BRE and BRE Shareholders, BRE Shareholders pledged all of their equity interests in BRE to Green Grass WFOE to guarantee BRE’s performance of the relevant obligations and indebtedness under the Technical Consultation and Service Agreement. In addition, BRE Shareholders has completed the registration of the equity pledge under the Equity Pledge Agreement with the competent local authority. If BRE breaches its obligation, Green Grass WFOE, as pledgee, is entitled to certain rights, including the right to dispose the pledged equity interests in order to recover these breached amounts. The Equity Pledge Agreement is continuously valid until all of the BRE Shareholders are no longer shareholders of BRE.

Equity Option Agreement. Pursuant to an Equity Option Agreement among Green Grass WFOE, BRE and BRE Shareholders, Green Grass WFOE has the exclusive right to require the BRE Shareholders to fulfill and complete all approval and registration procedures required under PRC laws for Green Grass WFOE to purchase, or designate one or more persons to purchase, BRE Shareholders’ equity interests in BRE, once or at multiple times at any time in part or in whole at Green Grass WFOE’s sole and absolute discretion. The purchase price is the lowest price allowed by PRC laws (currently estimated to be RMB 1.00). If the purchase price is higher than RMB 1.00 to comply with applicable PRC laws, BRE shall exempt Green Grass WFOE from the obligation of payment and agree that Green Grass WFOE shall not be required to fulfill the payment obligation. The Equity Option Agreement remains effective until all the equity interest owned by each of the BRE Shareholders has been legally transferred to WFOE or its designee(s).

Voting Rights Proxy and Finance Supporting Agreement. Pursuant to the Voting Rights Proxy and Finance Supporting Agreements among Green Grass WFOE, BRE and BRE Shareholders, each of BRE Shareholders irrevocably appointed Green Grass WFOE or Green Grass WFOE’s designee to exercise all his or her rights as a BRE Shareholder under the Articles of Association of BRE, including but not limited to (1) proposing to hold a shareholders’ meeting, (2) the power to exercise all shareholder’s voting rights with respect to all matters to be discussed and voted in the shareholders’ meeting of BRE, (3) exercising other voting rights the shareholder is entitled to under the laws of PRC promulgated from time to time, and (4) exercising other voting rights the shareholder is entitled to under the Articles of Association of BRE amended from time to time. In addition, Green Grass WFOE agreed to arrange for funds to be provided as necessary to BRE in connection with BRE’s business (the “Financial Support”) and also agreed that should the business fails in the ordinary course of business, and as a result BRE is unable to repay the Financial Support, BRE shall have no repayment obligation. The term of the Voting Rights Proxy and Finance Supporting Agreements is 20 years, which can be extended by Green Grass WFOE through its written consent of the extension of the agreement before its expiration and BRE and BRE Shareholders agree such extension without reservation.

Emerging Growth Company Status

As a company with less than $1.07 billion in revenue during our last fiscal year, we qualify as an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act (the “JOBS Act”), and we are eligible to take advantage of certain exemptions from various reporting and financial disclosure requirements that are applicable to other public companies that are not emerging growth companies, including but not limited to (1) presenting only two years of audited financial statements and only two years of related management’s discussion and analysis of financial condition and results of operations in this prospectus, (2) not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”), (3) reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and (4) exemptions from the requirements of holding a non-binding advisory vote on executive compensation and shareholder approval of any golden parachute payments not previously approved. We intend to take advantage of these exemptions. As a result, investors may find investing in our ordinary shares less attractive.

8

In addition, Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended (the “Securities Act”), for complying with new or revised accounting standards. As a result, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. We intend to take advantage of such extended transition period.

We could remain an emerging growth company for up to five years, or until the earliest of (1) the last day of the first fiscal year in which our annual gross revenues exceed $1.07 billion, (2) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Exchange Act, which would occur if the market value of our ordinary shares that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter and we have been publicly reporting for at least 12 months, or (3) the date on which we have issued more than $1 billion in non-convertible debt during the preceding three-year period.

Corporate Information

Our principal executive offices are located at 9th Floor, Lvdi Zhihai Tower A3, North Kerqin Road, Nandian Street, Xincheng District, Huhe Haote City, Inner Mongolia 010000. Our telephone number at this address is + (86) 471-5287999. Our registered office in the Cayman Islands is located at Sertus Incorporations (Cayman) Limited, Sertus Chambers, Governors Square, Suite # 5-204, 23 Lime Tree Bay Avenue, P.O. Box 2547, Grand Cayman, KY1104, Cayman Islands. Investors should contact us for any inquiries through the address and telephone number of our principal executive offices.

Our website is http://www.nmgqqcy.net/. The information contained on our website is not a part of this prospectus.

Recent Developments Related to the COVID-19 Outbreak

Beginning in late 2019, there were reports of the COVID-19 (coronavirus) outbreak originating in Wuhan, China, the epidemic quickly spread to many provinces, autonomous regions, and cities all over the China. On March 11, 2020, the World Health Organization characterized the outbreak as a “pandemic.” To the prevention and control of the spread of the epidemic, the Chinese governments have issued administrative orders to impose travel and public gathering restrictions as well as to work from home and self-quarantine.

At the same time, COVID-19 has caused a decrease in the consumer demand for goods and services in the market. In addition, the circulation of production factors such as raw materials and labor has been hindered. Normal business activities such as logistics, production, sales, travels and business meetings have been severely disrupted. Enterprises have stopped production or reduced production, and social and economic activities have been adversely affected to certain extent during the outbreak.

The Company primarily conducts its business operations in the PRC. In response to the evolving dynamics related to the COVID-19 outbreak, the Company is following the guidelines of local government authorities as it prioritizes the health and safety of its employees, contractors, suppliers and retail partners. Our offices and facilities located in China were closed for the Lunar New Year Holiday Break at the end of January 2020, and remained closed as a result of the outbreak until early March. All of our offices are now open and resume ordinary operations.

Given the rapidly expanding nature of the COVID-19 pandemic, and because substantially all of our business operations and our workforce are concentrated in China, we believe there is a substantial risk that our business, results of operations, and financial condition will be adversely affected by the outbreak of COVID-19.

Potential impact to our results of operations will also depend on future developments and new information that may emerge regarding the duration and severity of the COVID-19 and the actions taken by government authorities and other entities to contain the COVID-19 or mitigate its impact, almost all of which are beyond our control.

9

The impacts of COVID-19 on our business, financial condition, and results of operations include, but are not limited to, the following:

| ● | We closed our offices and facilities for the Lunar New Year Holiday Break, and implemented work from-home policy until early March, 2020. During that period of time, our farming related work has been suspended because our employees cannot inspect and maintain the field and repair the fence, and some field surface erosion cannot be timely fixed which caused damage and loss production of alfalfa. |

| ● | Affected by traffic control and logistics restrictions in China, the transportation of supplies and delivery of products are materially negatively impacted. We could not ship our alfalfa hays during the lock down period as villages and counties have blocked roads and entrances. Currently, there are still certain restriction and quarantine requirement for inter-provincial transportation which severely limit our harvest service business and product shipment outside of Inner Mongolian Autonomous Region. |

| ● | Affected by traffic control and quarantine requirements, many of our employees could not come back to work as required and some employees have chosen to work close to home due to Covid-19 and have resigned, which cause our shortage of labor. | |

| ● | Affected by the self-quarantine requirement and travel restrictions in China, the Company’s sales staffs were unable to travel and carry out in-person business activities and face-to-face communication with customers, which greatly affected the development and introduction of potential customers. Although many businesses have reopened and more people travel and take on in-person meetings, the Company cannot reasonably predict when the business activities can fully be back to normal as to the level before the outbreak of COVID-19. |

| ● | Affected by traffic control and logistics restrictions in China, our inventory of alfalfa has increased which increases our storage costs and fire risk and related fire prevention expenses. Although our offices and facilities are reopened, our management has to spend additional time and take extra care to monitor the Covid-19 prevention measures, such as constant disinfecting the working places, wearing masks and taking temperatures for employees. If any of our employees are suspected to or actually infected by Covid-19, we will have to close the entire office or facility and quarantine other employees at this location and disinfect the office/facility, which will severely impact our business operation. |

| ● | The epidemic severely interrupted our customers’ normal work, businesses and lives, for example, our main customers, cattle famers, cannot normally and timely receive animal feeds from suppliers like us or ship their cattle to their customers due to traffic control during lock-down period and had to reduce the number of cattle. If our customers cannot weather COVID-19 and the resulting economic impact, or cannot resume business as usual after a prolonged outbreak, our revenues and business operations may be materially and adversely impacted. Although none of our customers has terminated contracts with us to date, we cannot assure you if any customer will terminate its contract with us due to the epidemic. |

| ● | In March 2020, the World Health Organization declared the COVID-19 as a pandemic. To date, confirmed cases and number of deaths are still climbing every day. To prevent and control the spread of the pandemic, many countries have canceled flights, closed borders, banned non-essential economic activities, and issued stay at home or even city lockdown orders. As a result, the global economy has also been materially negatively affected. This crisis is like no other, the impact is large and there is continued severe uncertainty about the duration and intensity of its impacts. It is extremely uncertain about the China and global growth forecast, which would seriously affect people’s investment desires in China and internationally. The shipment, delivery and customs clearance for alfalfa seeds that we purchased from United States have also been delayed due to Covid-19. |

The situation remains highly uncertain. It is therefore difficult for the Company to estimate the negative impact on our business or operating results. However, it is clear that the first and second quarter operating results will be adversely impacted in any event.

10

The Offering

Securities being offered: |

__ ordinary shares1. |

| Initial offering price: | The purchase price for the shares will be between $__ and $__ per ordinary share. |

| Number of ordinary shares outstanding before the offering: | 30,000,000 of our ordinary shares are outstanding as of the date of this prospectus. |

| Number of ordinary shares Outstanding After the Offering2: | __ ordinary shares |

Proceeds to us, net of underwriting discount but before expenses: |

Between $__ and $__, based on an offering price between $__ and $__. |

| Use of proceeds: | We intend to use the net proceeds of this offering to increase our production and storage capacity of biomass straw business and management and for other general corporate purposes. For more information on the use of proceeds, see “Use of Proceeds” on page 41. |

| Lock-up | All of our directors and officers and certain shareholders have agreed with the underwriters, subject to certain exceptions, not to sell, transfer or dispose of, directly or indirectly, any of our ordinary shares or securities convertible into or exercisable or exchangeable for our ordinary shares for a period of twelve (12) months after the date of this prospectus. See “Shares Eligible for Future Sale” and “Underwriting” for more information. |

| Proposed Nasdaq Symbol: | QQCY |

| Risk factors: | Investing in our ordinary shares involves a high degree of risk. As an investor you should be able to bear a complete loss of your investment. You should carefully consider the information set forth in the “Risk Factors” section beginning on page 13. |

| 1 | In addition, we may issue up to __ ordinary shares pursuant to the underwriters’ over-allotment option. |

| 2 | Excludes ordinary shares underlying underwriters’ warrants and ordinary shares and warrants pursuant to the underwriters’ over-allotment option. |

11

SUMMARY CONSOLIDATED FINANCIAL AND OPERATING DATA

The following summary consolidated financial data for the years ended June 30, 2019 and 2018 are derived from our audited consolidated financial statements included elsewhere in this prospectus. The following summary consolidated financial data for the six months ended December 31, 2019 and 2018 are derived from our unaudited consolidated financial statements included elsewhere in this prospectus. Our consolidated financial statements are prepared and presented in accordance with generally accepted accounting principles in the United States, or U.S. GAAP.

Our historical results for any period are not necessarily indicative of results to be expected for any future period. You should read the following summary financial information in conjunction with the consolidated financial statements and related notes and the information under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this prospectus.

The following table presents our summary consolidated statement of comprehensive income for the periods as indicated below:

| For

the Six Months Ended December 31, | For

the Years Ended June 30, | |||||||||||||||

| 2019 | 2018 | 2019 | 2018 | |||||||||||||

| (Unaudited) | (Unaudited) | |||||||||||||||

| US$ | US$ | US$ | US$ | |||||||||||||

| Summary Statement of Operations data: | ||||||||||||||||

| Revenues | $ | 20,457,909 | $ | 20,857,957 | $ | 24,131,248 | $ | 22,080,450 | ||||||||

| Cost of revenues | (14,539,941 | ) | (12,761,125 | ) | (15,569,652 | ) | (16,067,375 | ) | ||||||||

| Gross profit | 5,917,968 | 8,096,832 | 8,561,596 | 6,013,075 | ||||||||||||

| (Provision for) recovery of doubtful accounts | (1,227,390 | ) | 23,238 | (1,489,570 | ) | (434,512 | ) | |||||||||

| Operating expenses | (425,795 | ) | (459,390 | ) | (941,617 | ) | (712,490 | ) | ||||||||

| Gain on sales of property, plant and equipment | 238,376 | - | - | - | ||||||||||||

| Income from operations | 4,503,159 | 7,660,680 | 6,130,409 | 4,866,073 | ||||||||||||

| Other non-operating income (expenses), net | 12,562 | 12,430 | (261,847 | ) | 241,036 | |||||||||||

| Provision for income taxes | - | - | - | - | ||||||||||||

| Net income | 4,515,721 | 7,673,110 | 5,868,562 | 5,107,109 | ||||||||||||

| Less: net income attributable to noncontrolling interest | 89,923 | 153,462 | 117,370 | 102,142 | ||||||||||||

| Net income attributable to Green Grass Ecological Technology Development Co. Ltd. | $ | 4,425,798 | $ | 7,519,648 | $ | 5,751,192 | $ | 5,004,967 | ||||||||

| Earnings per share, basic and diluted | $ | 0.15 | $ | 0.25 | $ | 0.19 | $ | 0.17 | ||||||||

| Weighted average Ordinary Shares outstanding | 30,000,000 | 30,000,000 | 30,000,000 | 30,000,000 | ||||||||||||

| December 31, 2019 | June

30, 2019 | June

30, 2018 | ||||||||||

| (Unaudited) | ||||||||||||

| US$ | US$ | US$ | ||||||||||

| Summary Consolidated Balance Sheets Data: | ||||||||||||

| Current assets | $ | 18,542,952 | $ | 16,173,902 | $ | 9,468,437 | ||||||

| Total assets | $ | 31,018,890 | $ | 26,389,967 | $ | 22,597,351 | ||||||

| Current liabilities | $ | 1,684,375 | $ | 1,267,397 | $ | 2,597,157 | ||||||

| Total liabilities | $ | 1,684,375 | $ | 1,267,397 | $ | 2,597,157 | ||||||

| Total equity | $ | 29,334,515 | $ | 25,122,570 | $ | 20,000,194 | ||||||

| For

the Six Months Ended December 31, | For

the Years Ended June 30, | |||||||||||||||

| 2019 | 2018 | 2019 | 2018 | |||||||||||||

| Summary Consolidated Statements of Cash Flows Data | (Unaudited) | (Unaudited) | ||||||||||||||

| Net cash provided by (used in) operating activities | $ | 1,006,989 | $ | (67,919 | ) | $ | 1,853,364 | $ | 4,297,041 | |||||||

| Net cash used in investing activities | (2,357,430 | ) | (902,356 | ) | (230,560 | ) | (3,231,312 | ) | ||||||||

| Net cash provided by (used in) financing activities | 1,327,485 | 858,354 | (1,845,088 | ) | (1,360,609 | ) | ||||||||||

| Effect of foreign currency translation on cash and cash equivalents | (794 | ) | (9,899 | ) | (8,366 | ) | 18,210 | |||||||||

| Net decrease in cash and cash equivalents | $ | (23,750 | ) | $ | (121,820 | ) | $ | (230,650 | ) | $ | (276,670 | ) | ||||

12

An investment in our ordinary shares involves significant risks. You should carefully consider all of the information in this prospectus, including the risks and uncertainties described below, before making an investment in our ordinary shares. Any of the following risks could have a material adverse effect on our business, financial condition and results of operations. In any such case, the market price of our ordinary shares could decline, and you may lose all or part of your investment.

Risks Related to Our Business

The loss of any of our key customers could reduce our revenues and our profitability.

Five customers accounted for 47.7% of our net revenue in the six months ended December 31, 2019. Five customers accounted for 24.6% of our net revenue in the year ended June 30, 2019, and five customers accounted for 20.3% in the year ended June 30, 2018. There can be no assurance that we will maintain or improve the relationships with these customers, or that we will be able to continue to supply these customers at current levels or at all. Any failure to pay by these customers could have a material negative effect on our company’s business. In addition, having a relatively small number of customers may cause our quarterly results to be inconsistent, depending upon when these customers pay for outstanding invoices. If we cannot maintain long-term relationships with these major customers, the loss of our sales to them could have an adverse effect on our business, financial condition and results of operations.

We rely on a limited number of vendors, and the loss of any significant vendor could harm our business, and the loss of any one of such vendors could have a material adverse effect on our business.

We consider our major vendors to be those vendors that accounted for more than 10% of overall purchases in any given fiscal period. For the six months ended December 31, 2019, the Company purchased approximately 87.6% of its raw materials from four major suppliers. For the years ended June 30, 2019 and 2018, the Company purchased approximately 67.1% and 91.0%, of its raw materials from three and five major suppliers, respectively. We have not entered into long-term contracts with our significant vendors and instead rely on individual contracts with such vendors. Although we believe that we can locate replacement vendors readily on the market for prevailing prices, any difficulty in replacing a vendor on terms acceptable to us could negatively affect our company’s performance to the extent it results in higher prices or a slower supply chain.

We lack product and business diversification. Accordingly, our future revenues and earnings are more susceptible to fluctuations than a more diversified company.

Our current primary business activities focus on agricultural products and biomass recycling. Because our focus is limited in this way, any risk affecting the agricultural or biomass recycling industries could disproportionately affect our business. Our lack of product and business diversification could inhibit the opportunities for growth of our business, revenues and profits.

Governmental support to the agriculture industry and/or our business may decrease or disappear.

Currently the Chinese government is supporting agriculture businesses with tax exemptions and our alfalfa farming is exempted from valued tax and enterprise income tax. In addition, our local government has been supporting our company by providing subsidies from time to time. These beneficial policies may change, so the support we receive from the government may decrease or disappear, which may impact our development.

Beneficial tax incentives may disappear.

We operate our business through our Chinese subsidiaries and VIEs. Currently the agriculture industry is highly supported by the Chinese government. For example, to further strengthen and standardize the support of comprehensive agricultural development to the characteristic industries with agricultural advantages, the Chinese National Office of Comprehensive Agricultural Development has decided to carry out the compilation of The Plan for Comprehensive Agricultural Development to Support the Agricultural Advantage and Characteristic Industries (2019-2021) (the “New Plan”). However, the New Plan was adopted in 2018 and the final result remains to be further observed.

As an agricultural production enterprise, we are enjoying certain tax benefits, including income tax exemption. If the tax policies change in a way that some or all of the tax benefits we presently receive are cancelled, we may need to pay much higher taxes which will reduce or eliminate our profit margin.

13

The alfalfa cultivated by us may be subject to risks related to diseases, pests, abnormal temperature change and extreme weather events.

Agricultural products are exposed to diseases and pests. Pests and plant diseases during the cultivation process may significantly decrease the quantity of the qualified agricultural products provided to us, which may force us to breach our contracts with our clients by not being able to supply enough products to them timely, and further impact our revenues.

The extreme weather and other natural disasters such as drought, flood, snowstorm and earthquake may damage our production. The quality, cost and volume of our products could be materially adversely affected by extreme weather conditions or natural disasters; similarly, the end users of our products could also be adversely affected and as a result harming our sales and profitability. Man-made disasters, such as arson or other acts that may adversely affect our inventory in the winter storage season, may also damage our products or our facilities. Although we are using more and more carefully managed environments for cultivation, extreme weather events may still impact our cultivation process. We do not have insurance to protect against such risks. Also, extreme weather conditions and other natural disasters may affect our customers’ demand for our products, which would adversely affect our business prospects and results of operations.

The quality of the straw and biomass waste purchased from third party farmers may not be consistent and might be harmful to the systems of the biomass power plant and paper mills which we supply.

The quality of the straw and biomass waste purchased from third party farmers may not be consistent. The impurities and dust of certain biomass waste raw materials might be excessive, which could be harmful to power generation systems and paper mill facilities and seriously affect the stable production of the plants/mills. If we are unable to inspect and rule out any affected agricultural raw materials and sell them to our clients, our reputation will be harmed, our clients may cease purchasing products from us and ask for damages. Even if we are able to inspect the affected products, we will need to spend extra time and costs.

Our plans to increase production capacity and expand into new markets may not be successful, which will adversely affect our operating results.

Our plan to further develop our biomass business and its production capacity has placed and will continue to place, substantial demands on our managerial, operational, technological and other resources. As we plan to supply our biomass products to biomass power generation plants of all major electricity companies in China, these represent great opportunities for the company, but also represent a potential risk in losing focus and diluting management attention. If we fail to establish and manage the growth of our product offerings, operations and distribution channels effectively and efficiently in such business, we could suffer a material and adverse effect on our operations and our ability to capitalize on new business opportunities, either of which could materially and adversely affect our operating results.

Business expansion may present operating and marketing challenges. If we are unable to anticipate the changing demand that expanding operations will impose on our production systems and distribution channels, or if we fail to develop our production systems and distribution channels to meet the demand, we could experience an increase in expenses and our results of operations could be adversely affected.

Failure to accurately forecast customer demand could lead to excess supplies or supply shortages, which could result in decreased operating margins, reduced cash flows and harm to our business.

We may fail to correctly anticipate product supply requirements or suffer delays in production resulting from issues with our suppliers. Our suppliers may not supply us with a sufficient amount of materials of adequate quality, or they may provide them at significantly increased prices. We may in the future, experience delays or reductions in supply shipments, which could reduce our revenue and profitability. We may experience delays in production if we fail to identify alternative suppliers, or if supply is interrupted, each of which could materially adversely affect our business and operations.

If we fail to anticipate customer demand properly, an oversupply could result in excess or obsolete inventories, which could adversely affect our business. Additionally, if we fail to correctly anticipate our internal supply requirements, an undersupply could limit our production capacity. The difficulty in forecasting demand also makes it difficult to estimate our future results of operations, financial condition and cash flows from period to period. A failure to accurately predict the level of demand for our products could adversely affect our net revenues and net income, and we are unlikely to forecast such effects with any certainty in advance.

14

The alfalfa farming, biomass recycling and agricultural harvesting businesses are relatively new and changing rapidly in China which can result in unexpected developments and increase of competition that could negatively impact our operations.

The alfalfa farming, biomass recycling and agricultural harvesting businesses are relatively new and changing rapidly in China which can result in unexpected developments and increase of competition. Other companies may enter into these business areas or form strategic alliances to compete with us. These potential competitors may have more financial resources, offer more attractive services, respond faster to market opportunities or undertake more extensive and effective marketing campaigns. If we are unable to compete with these companies and meet the need for development in these industries, the demand for our products and service could stagnate or substantially decline, we could experience reduced revenues and our operation results could be negatively impacted. We cannot assure you that we will be able to effectively and successfully compete against new or existing competitors. Any inability to successfully compete with new or existing competitors may prevent us from increasing or sustaining our revenue and profitability level and result in a loss of market share.

Our growth prospects may be materially and adversely affected if we are unable to produce our products in sufficient quantities for our customer or if our competitors develop products that are favored by our customers.

We believe our future growth will depend on the value of our grass business for biofuel, power plant, or animal feed purposes. The ability to develop orders from customers, if at all, is uncertain due to several factors, many of which are beyond our control. If we are unable to produce sufficient alfalfa or collect sufficient straws to meet the initial demands of our customers, or if our competitors develop products that are favored by our customers, our growth will be adversely affected. If we are unable to generate our existing products in sufficient quantities - our growth prospects may be materially and adversely affected and our revenues and profitability may decline.

In addition, our customers may be subject to special requirements imposed by PRC laws and regulation. For example, certain of our customers which breed and farm livestock are required to only use animal feeds that meet certain PRC national standard. If we are unable to meet such standards, produce sufficient products and deliver them timely, our customers will suffer losses and in turn our growth prospects may be materially and adversely affected and our revenues and profitability may decline.

Our products are not nationally well known.

Our product visibility in general is not high in China. Although we plan to participate in more industry events to improve recognition and drive revenues, we have no guarantee that we will be able to materially increase the market recognition of all our edible fungi products. To the extent we are unable to increase our product visibility, we may face challenges in increasing revenues or increasing the profit margin for such products.

We may need additional capital, and financing may not be available on terms acceptable to us, or at all.

Although we believe that our current cash and cash equivalents, anticipated cash flows from operating activities and the proceeds from this offering will be sufficient to meet our anticipated working capital requirements and capital expenditures in the ordinary course of business for at least 12 months following this offering, we may need additional cash resources in the future if we experience changes in business conditions or other developments. We may also need additional cash resources in the future if we find and wish to pursue opportunities for investment, acquisition, capital expenditure or similar actions. If we determine that our cash requirements exceed the amount of cash and cash equivalents we have on hand at the time, we may seek to issue equity or debt securities or obtain credit facilities. The issuance and sale of additional equity would result in further dilution to our shareholders. The incurrence of indebtedness would result in increased fixed obligations and could result in operating covenants that would restrict our operations. We cannot assure you that financing will be available in amounts or on terms acceptable to us, if at all.

We may incur substantial debt in the future, which may adversely affect our financial condition and negatively impact our operations.

We may decide in the future to finance our company through incurring debt. The incurrence of debt could have a variety of negative effects, including:

| ● | default and foreclosure on our assets if our operating revenue is insufficient to repay debt obligations; |