Exhibit 99.1

ASX ANNOUNCEMENT - 2022 HALF YEAR RESULTS

9 August 2022

Record half year financial results:

| ü | Revenue US$1,980m, Net Income US$562m, Adjusted EBITDA US$849m, Group Average Realised Met Coal Price US$293/tonne |

| ü | Strong Net Cash position of US$171m and Available Liquidity of US$586m |

| ü | Half year dividend declaration of US$125m (US 7.5 cents per CDI) and offer to purchase up to US$25m Senior Secured Notes |

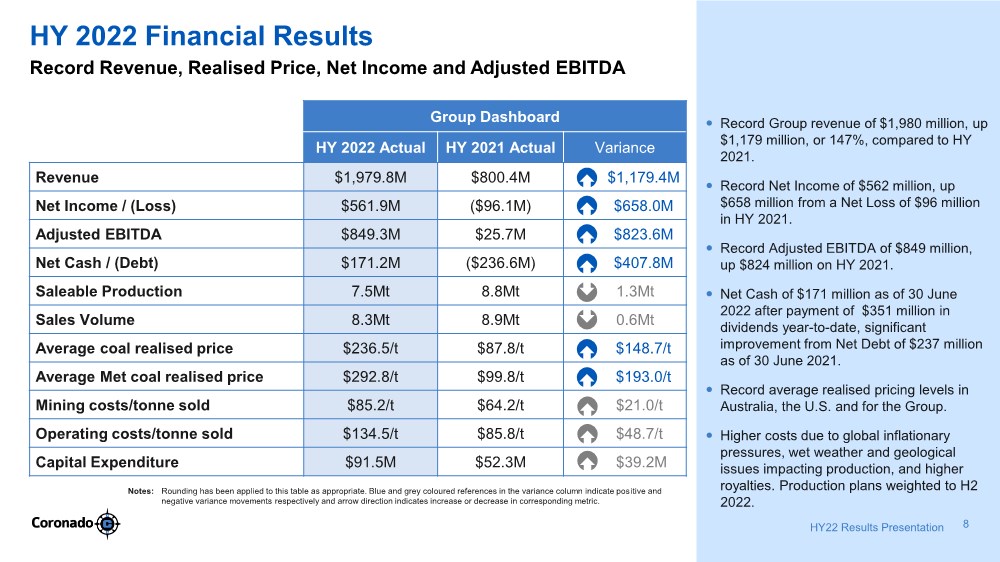

| RESULTS | HY22 | HY21 | Variance % | |||||||||

| Revenue ($m) | 1,979.8 | 800.4 | 147.4 | |||||||||

| Net Income / (Loss) ($m) | 561.9 | (96.1 | ) | 685.0 | ||||||||

| Adjusted EBITDA ($m) | 849.3 | 25.7 | 3,204.7 | |||||||||

| Net Cash / (Debt) ($m) | 171.2 | (236.6 | ) | 172.4 | ||||||||

| Saleable Production (MMt) | 7.5 | 8.8 | (14.8 | ) | ||||||||

| Sales Volume (MMt) | 8.3 | 8.9 | (7.0 | ) | ||||||||

| Group Average Realised Met Price per tonne sold ($/t) | 292.8 | 99.8 | 193.4 | |||||||||

| Mining Cost per tonne sold ($/t) | 85.2 | 64.2 | 32.7 | |||||||||

| Operating Cost per tonne sold ($/t) | 134.5 | 85.8 | 56.8 | |||||||||

| Capital Expenditure ($m) | 91.5 | 52.3 | 74.9 | |||||||||

Coronado Global Resources Inc. (Coronado, Company or the Group) (ASX: CRN) has released its half year financial results for the six months to 30 June 2022 (HY22). All amounts quoted in this release are in USD and million metric tonnes (MMt). Comparisons are to the six-month period ended 30 June 2021 (HY21) unless otherwise stated.

HY22 HIGHLIGHTS

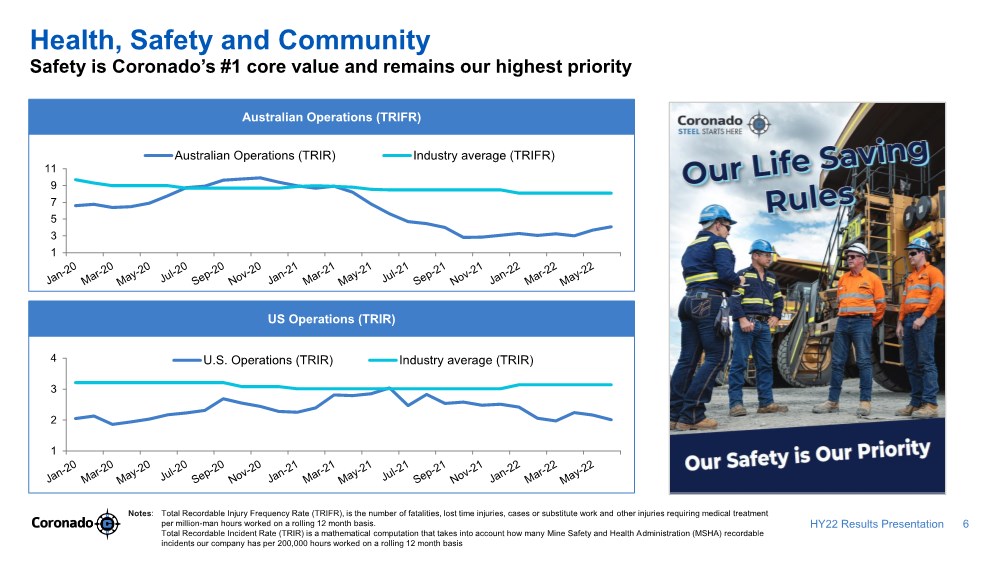

| · | Safety is Coronado’s number one core value and remains our highest priority. Australian TRIFR was 4.08 and U.S. TRIR was 2.01 at 30 June 2022, representing year-on-year improvements of 28% and 34% respectively. |

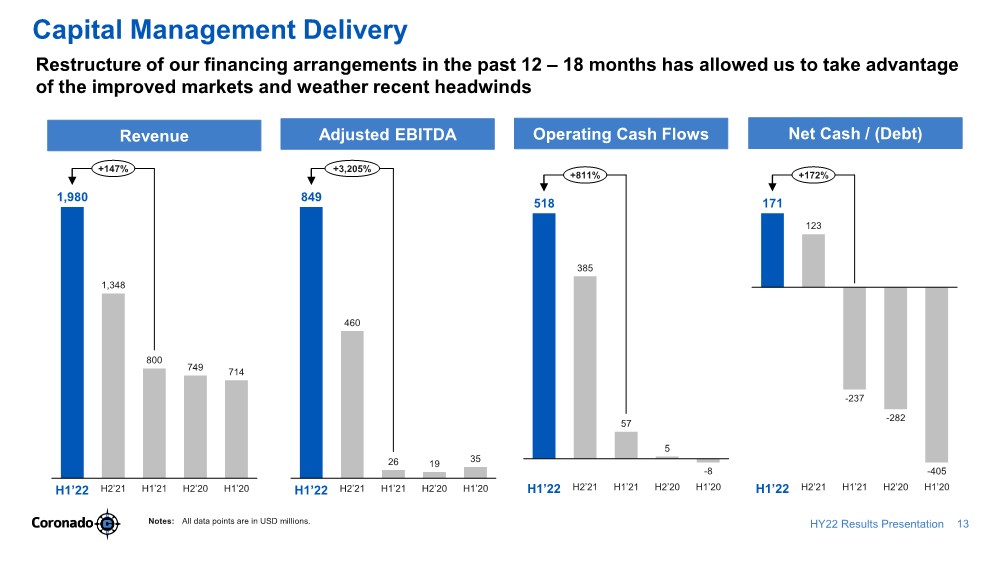

| · | Record Group Revenue of $1,979.8 million, up 147% due to the improvement in Met coal pricing, strong global demand for steel and tight Met coal supply during HY22. |

| · | Record Group Average Realised Met Coal Price of $292.8 per tonne, up 193% compared to the prior year. |

| · | Record Net Income of $561.9 million, an improvement of 685% from a Net Loss of $96.1 million in the prior year. |

| · | Record Adjusted EBITDA of $849.3 million, up more than 3,000% due to the higher Met coal price environment. |

| · | Year-to-date, Coronado has distributed $351 million in cash dividends to Shareholders. |

| · | Strong HY22 results enable Coronado to declare a further dividend of $125.7 million (US 7.5 cents per CDI) to Shareholders inclusive of the US 0.5 cents per CDI fixed dividend component; and offer to purchase up to $25.2 million of the outstanding aggregate principal amount of Senior Secured Notes at 104%, pursuant to the terms of the Indenture. |

| · | Strong closing Net Cash of $171.2 million at 30 June 2022, compared to Net Debt of $236.6 million at 30 June 2021. |

1

| · | Available liquidity of $585.6 million at 30 June 2022, comprising $485.6 million of cash (excluding restricted cash) and $100.0 million of undrawn funds under the Asset Based Loan (ABL) facility. |

| · | Sales and Production volumes lower than prior year due to wet weather impacts, geological issues and scheduled planned downtime for key maintenance activities. Volumes are weighted to the second half of 2022. Saleable Production market guidance anticipated to be at the low-end of 18.0 – 19.0 MMt, exceeding FY21 production levels (17.4 MMt). |

| · | Costs per tonne sold higher than prior year. Increases associated with global inflationary pressures, lower year-to-date production volumes and higher royalties (Stanwell rebate, Government royalties) due to higher realised pricing. Revised FY22 Mining Costs per tonne sold between $79 - $81 per tonne. |

| · | Capital expenditure of $91.5 million, up 74.9%. Full-year run-rate aligned with market guidance. |

| · | Coronado is pursuing optionality of switching certain U.S. high vol and Australian PCI / Semi Met coal products to the Thermal market to meet the high price and demand for energy coal. |

| · | S&P Dow Jones Indices announced the inclusion of Coronado in the S&P / ASX 200 index effective 20 June 2022. |

| · | Coronado released its 2021 Sustainability Report, revealing a heightened focus on environment and climate including emission reduction plans and targets. |

COMMENTS FROM MANAGING DIRECTOR AND CEO, GERRY SPINDLER

“In the first half of 2022, Coronado has delivered on its capital management goals. We have generated record Revenue, Net Income and Adjusted EBITDA and distributed $351 million in cash dividends to Shareholders while remaining in a Net Cash position. Coronado’s half-year Adjusted EBITDA eclipses the highest full-year Adjusted EBITDA ever reported in the history of Coronado. These strong results are due to the higher price environment, which has resulted in record price realisations for our high-quality metallurgical coal products, but also from the structural changes made to our business over the past 12 – 18 months that have allowed us to take advantage of the improved markets.

“I am proud of our financial results and am equally proud of a significant number of other achievements delivered by the Coronado team. We have improved our reportable safety rates year-on-year; released our fourth Sustainability Report in which we include emission reduction plans and targets; completed critical planned maintenance activities; improved performance at Curragh from our Draglines and newly transitioned fleets under Coronado management; entered the S&P / ASX 200 index for the first time; and continued to reinvest in our business via capital expenditure to secure future production plans and growth.

“We experienced unforeseen headwinds outside of our control during the first half of 2022 from significant wet weather in Queensland, which impacted production, and growing inflationary cost pressures for labour, transport and materials and supplies. Royalty costs also significantly increased during the period due to the substantially higher coal price. As a result, year-to-date costs per tonne are not reflective of our cost expectations for the second half of 2022, nor are they a reasonable comparison to prior year in which we operated in a very different market dynamic. Despite the headwinds, Coronado remains an effective and agile operator ready to deliver on its near, and longer term, growth plans.

“As we look to the second half of 2022, the prospect of strong financial returns remains despite recent reductions in Metallurgical coal prices. Thermal pricing remains at significantly elevated levels, and we will divert Metallurgical tonnes into Thermal markets to achieve higher realisations where we have the flexibility to do so. Coronado’s capital investment in its operations drives the second half weighted production plans, which we anticipate will see us deliver production levels exceeding 2021 levels and lower second half costs. I remain extremely confident in our ability to weather the headwinds and continue to provide enhanced value and returns to all Shareholders,” Mr Spindler said.

HEALTH AND SAFETY

The safety and well-being of our workforce continue to be Coronado’s number one priority.

In Australia, the 12-month rolling average Total Reportable Injury Frequency Rate (TRIFR) at 30 June 2022 was 4.08, compared to 5.63 at 30 June 2021, reflecting a 28% year-on-year improvement. In the U.S., the 12-month rolling average Total Reportable Incident Rate (TRIR) at 30 June 2022 was 2.01, compared to 3.04 at 30 June 2021, reflecting a 34% year-on-year improvement.

2

Safety results have improved year on year due to several factors, including hazard identification and critical control verification programs, effectiveness audits and enhanced training programs. Reportable rates in Australia and the U.S. remain below the relevant industry averages.

New and revised health and safety initiatives across all Coronado operations continue to be implemented quarterly. In Australia, Curragh continued to reinforce the importance of safety by developing and communicating to the workforce ‘Our Life-Saving Rules’. These rules apply to all employees and contractors on site and reinforce to everyone that safety is our priority and our key accountability. In the U.S., we continued to train our existing workforce and develop new miners. This has resulted in 9,500 hours of discretionary training year to date, which has helped set solid expectations for new hires and articulate Coronado’s safety culture and focus.

Coronado’s Covid-19 Steering Committee continues to monitor the status and impacts on our workforce from the Covid-19 pandemic. Throughout the first half of the year, the Committee remained vigilant in dealing with variants and their impacts on our people, operations and customers. Following the successful implementation of the Coronado Vaccine Inventive Plan at our U.S. operations, we are seeing workforce absenteeism reduce and workforce availability levels increase.

FINANCIAL PERFORMANCE

Coronado delivered record financial results and finished HY22 in a very strong financial position. While the business incurred higher costs from global inflationary pressures, lower production from wet weather and geological issues, and higher royalties, these were mitigated by peaking Met coal prices. As a result, liquidity levels are high, and our balance sheet is in a significantly stronger position than this time last year.

HY22 Revenue of $1,979.8 million was $1,179.5 million, or 147.4%, higher than HY21 and a record for the Company. Record revenues were driven by substantially higher realised Met coal pricing despite lower Sales Volumes. Coronado delivered record quarterly revenue in the recent June quarter of $1,032.7 million.

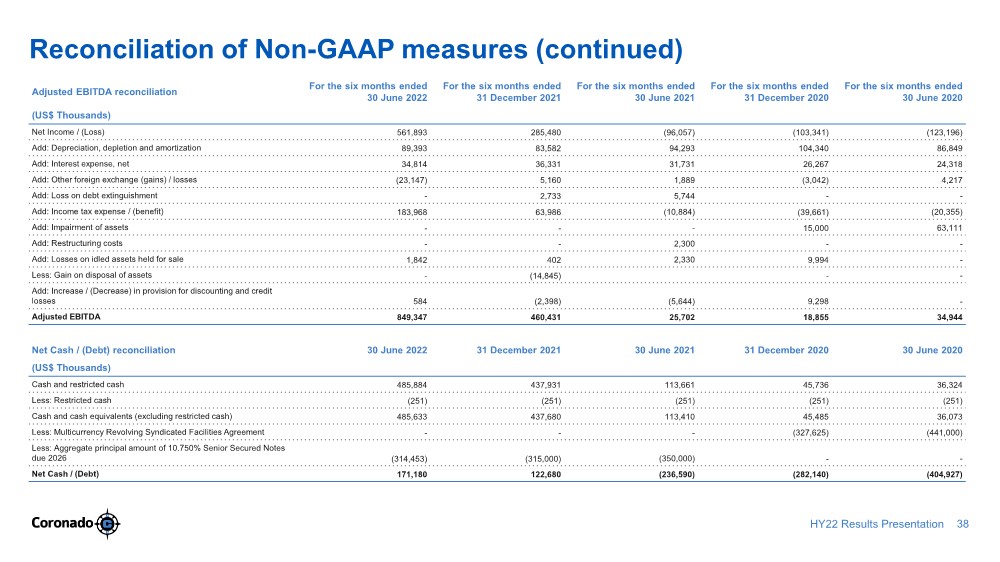

Coronado reported record Net Income of $561.9 million, an improvement of $658.0 million from the $96.1 million Net Loss reported in HY21.

Adjusted EBITDA was $849.3 million, an increase of $823.6 million compared to HY21, and a record for the Company. HY22 Adjusted EBITDA is higher than any full-year Adjusted EBITDA reported by the Company since inception.

Mining costs per tonne sold of $85.2 per tonne were up from $64.2 per tonne in HY21 due primarily to unforeseen events outside our control including global inflationary pressures, wet weather impacts, and geological issues impacting production. Inflation levels at 30 June 2022 in the U.S. reached a 40-year high of 9.1% and in Australia reached a 20-year high of 6.1% and are expected to remain at elevated levels for the balance of 2022. Coronado anticipates that these increases will be partly mitigated by lower FX and incremental productivity improvements in the second half of 2022.

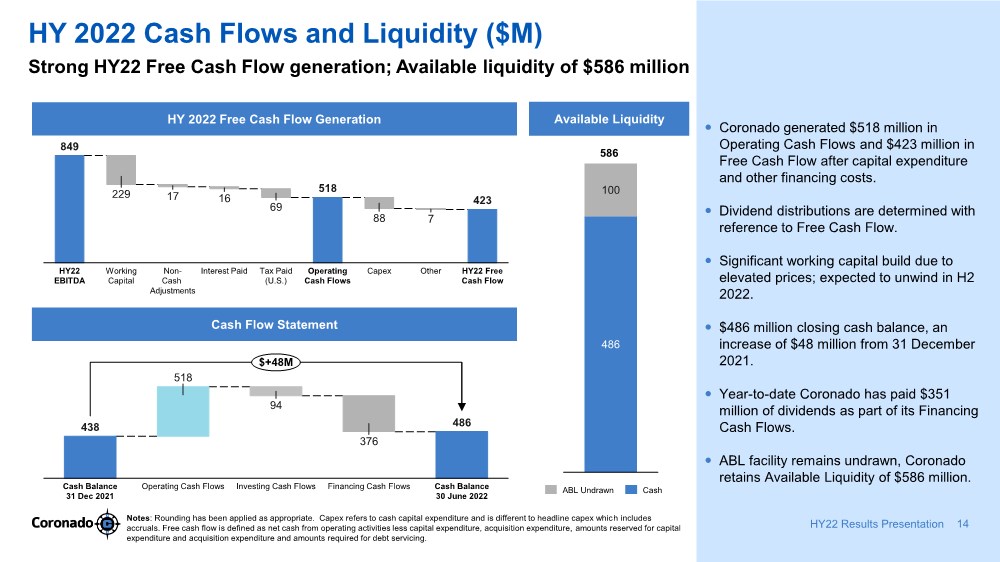

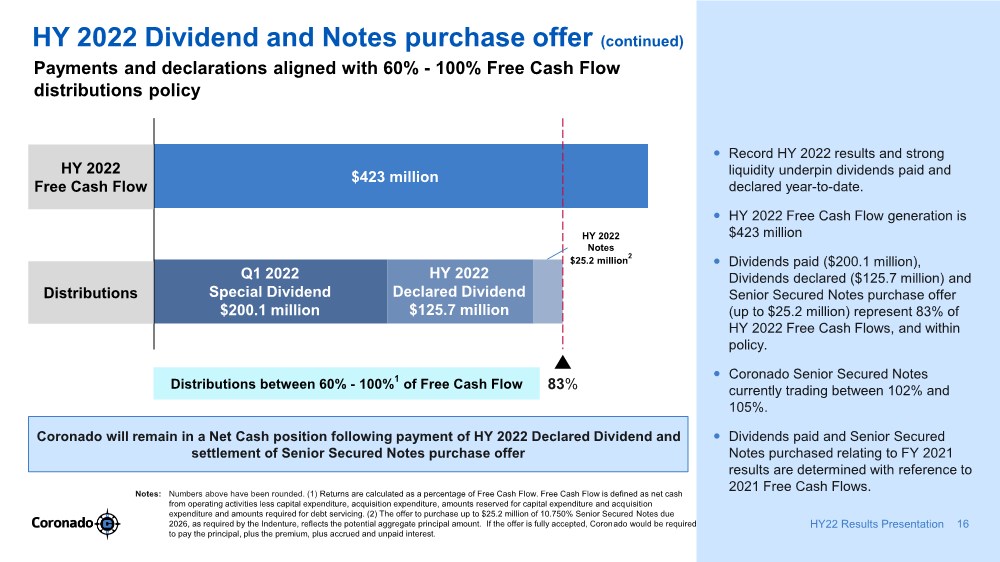

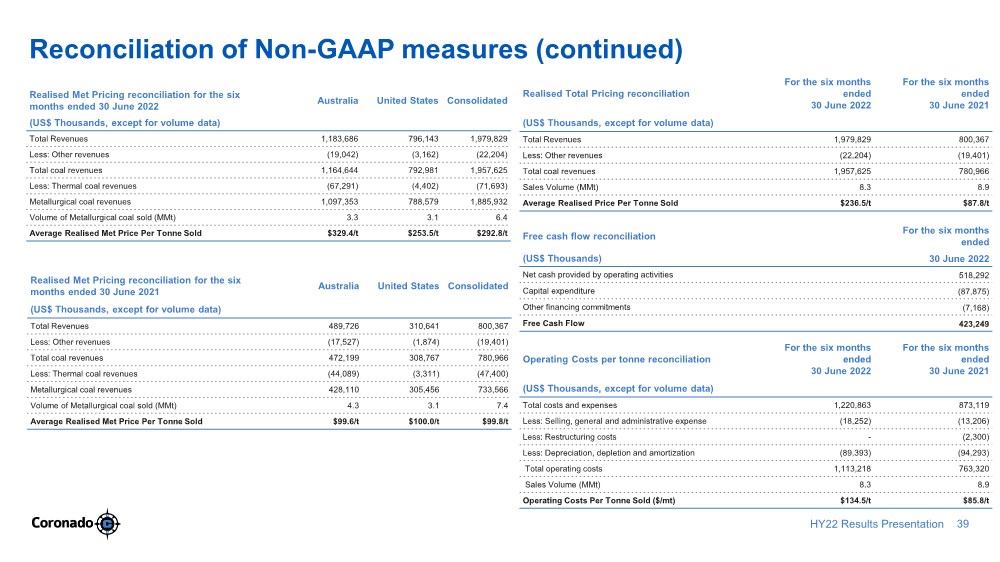

Cash generated from operating activities was $518.3 million for HY22, an increase of $461.4 million compared to cash generated of $56.9 million in HY21. Cash generated from operating activities in HY22 eclipses the cash generated for the full 2021 year.

High margins and strong cash flow generation in HY22 saw Coronado finish with Net Cash of $171.2 million at 30 June 2022, after payment of the $351 million in cash dividends distributed year-to-date. Coronado’s Net Cash position consists of a closing cash balance (excluding restricted cash) of $485.6 million and $314.5 million aggregate principal amount of outstanding 10.750% Senior Secured Notes due 2026 (“Notes”).

Coronado has Available Liquidity of $585.6 million (comprising cash and cash equivalents, excluding restricted cash, and available borrowings under our ABL facility).

DIVIDENDS AND CAPITAL MANAGEMENT

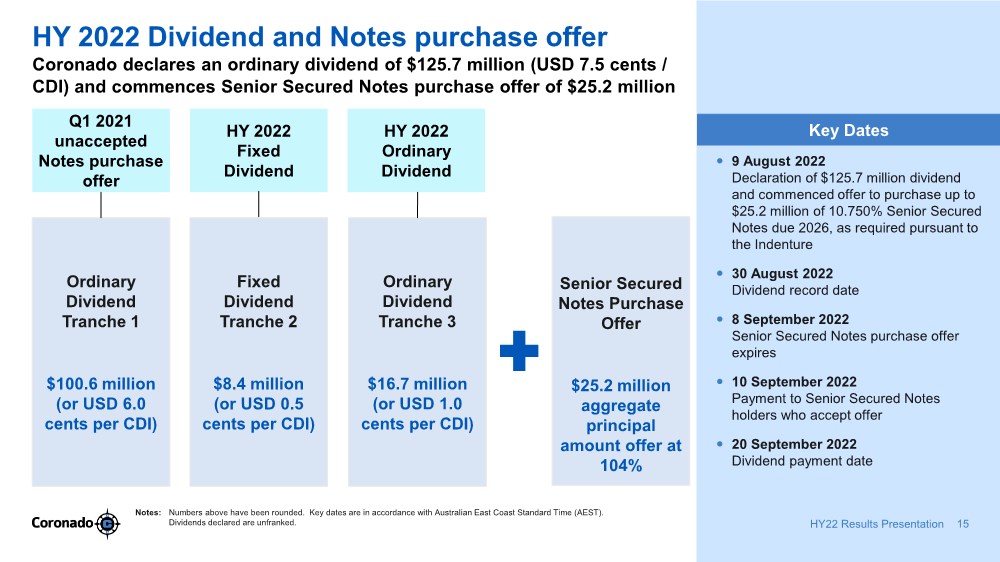

Today, Coronado’s Board of Directors declares an HY22 unfranked dividend of $125.7 million, or USD 7.5 cents per CDI (Fixed Dividend USD 0.5 cents per CDI; Ordinary Dividend USD 7.0 cents per CDI) to Shareholders.

The HY22 unfranked dividend record date is 30 August 2022, and payment date is 20 September 2022. It is anticipated that the Company will be able to pay franked dividends from early 2023.

3

Following the payment of the HY22 dividend, Coronado will have distributed $477 million in cash dividends to Shareholders in the calendar year, and $1.2 billion in cumulative dividends since listing on the ASX in October 2018.

The Company also announces an offer to purchase up to $25.2 million of the outstanding aggregate principal amount of the Notes, at a price of 104% of their principal amount, pursuant to the terms of the Indenture governing such Notes. The payment of the $125.7 million dividend to shareholders is not contingent on acceptance of the offer to purchase the Notes. All distributions will be made from available cash, and the Company expects to remain in a Net Cash position post distribution.

The Company’s primary focus is to maintain a strong balance sheet, sustainable profits and investment flexibility through volatile price cycles. A strong balance sheet allows further investment in existing operations and positions the Company well to take advantage of acquisition opportunities as they arise. Coronado expects consolidation in the Met coal industry over time. The Company is uniquely positioned to pursue acquisitions of Met coal assets as the larger diversified miners look to exit. Maintaining prudent cash and debt levels will ensure the Company has sufficient liquidity and the necessary flexibility to pursue acquisition opportunities.

Coronado’s year-to-date paid and declared distributions are made with the confidence that a strong balance sheet is retained. The Company is cognisant of ongoing geopolitical uncertainty, global inflationary pressures, capital expenditure plans underpinning future growth, and other unforeseen events. The Board of Directors will consider these factors, among others, before assessing the likelihood of further distributions as the year progresses.

OPERATIONS

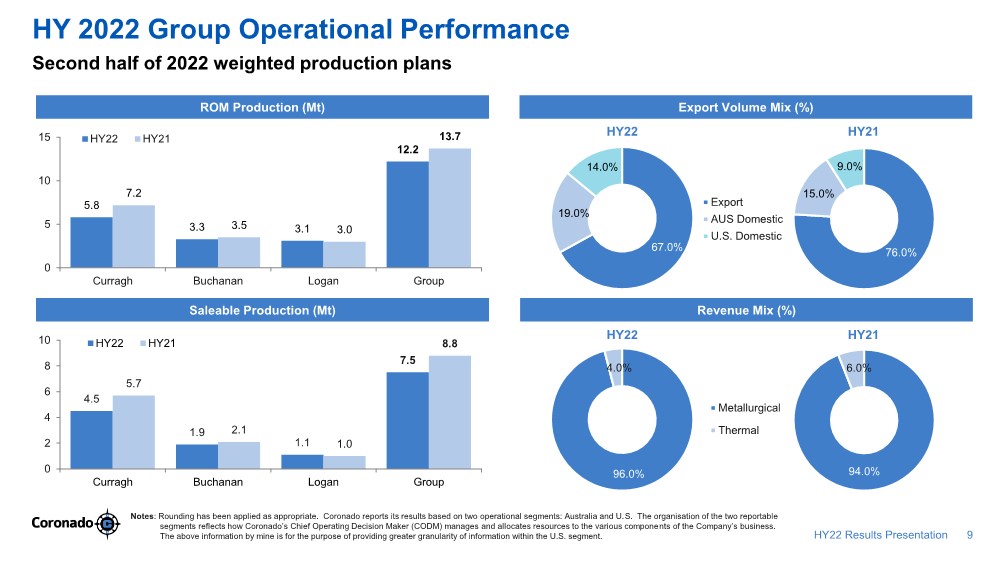

ROM production for HY22 was 12.2 MMt (11.0% lower), saleable production was 7.5 MMt (14.8% lower), and sales volume was 8.3 MMt (7.0% lower) compared to HY21.

The Curragh mine and most of the Bowen Basin were significantly impacted by wet weather during the June quarter. Blackwater, the nearest town to Curragh, received 213mm of rain in the quarter, representing nearly a 300% increase on the 10-year rainfall average for the area. At the height of the rain event, the mine was evacuated due to road closures and flooding in the surrounding regions to ensure the safety of our people travelling to and from the site. The consistent rain from late April through May was a key contributor to the lower production volumes in Australia. Production levels at our U.S. operations were broadly aligned with the first half of 2021 despite the impacts from a rock intrusion at the Buchanan mine in April.

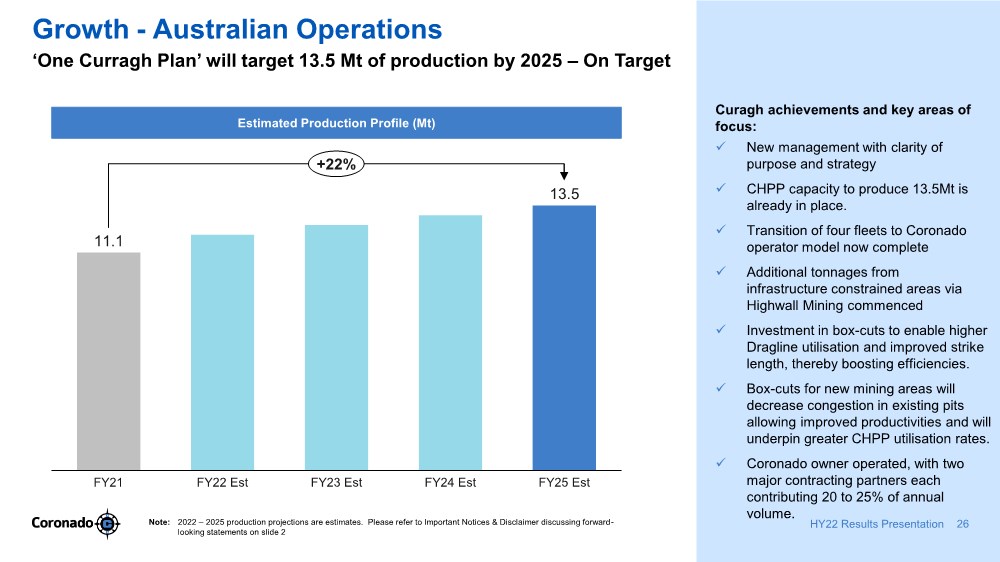

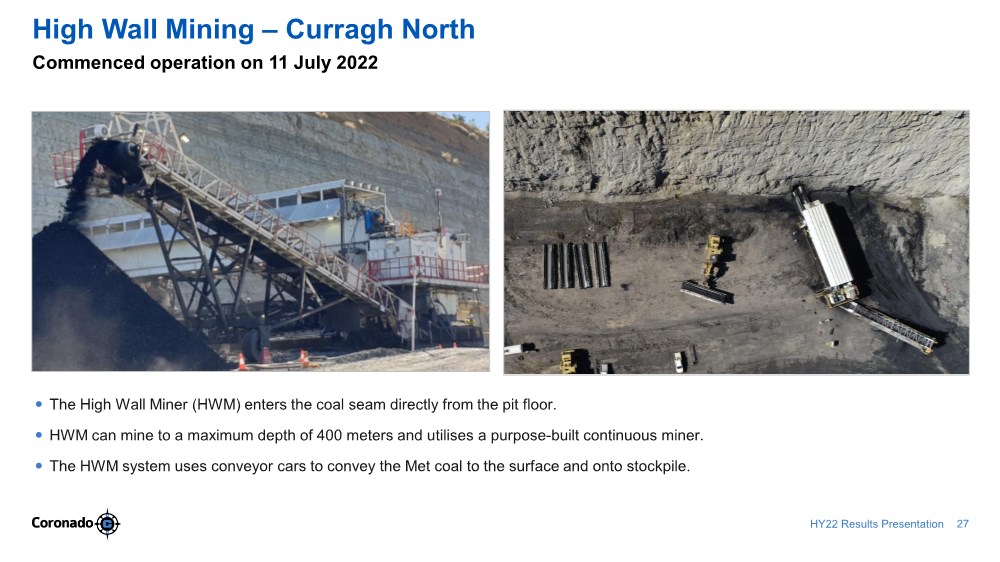

Despite the impacts of the Bowen Basin rain events, Curragh successfully completed major planned maintenance activities on the CHPP and two Draglines. Completion of this maintenance was essential to the mine’s second-half 2022 weighted production plans. During HY22, Curragh also significantly progressed the conversion of four fleets to a Coronado operator model, which is now complete, and has also now commenced high-wall mining operations in Curragh North. The mine’s focus on waste movement in the first half of the year is also evident, with waste movement YTD broadly aligned with the same period in the prior year despite heavy rain (June 2022 YTD: 88.0 Mbcms vs June 2021 YTD: 90.9 Mbcms).

The “One Curragh Plan” utilizing our new management structure is producing positive results. The continued focus on improving Dragline productivity has resulted in an approximately 10% productivity improvement in two of Curragh’s draglines, with focus swinging to the remaining two draglines in the second half of the year. The newly transitioned excavator fleets, which replaced contractor units, operated with approximately 20% lower costs and 30% more operating time compared with previous contractor rates in Curragh North. We expect to see these changes deliver continually improved results in the remainder of the year.

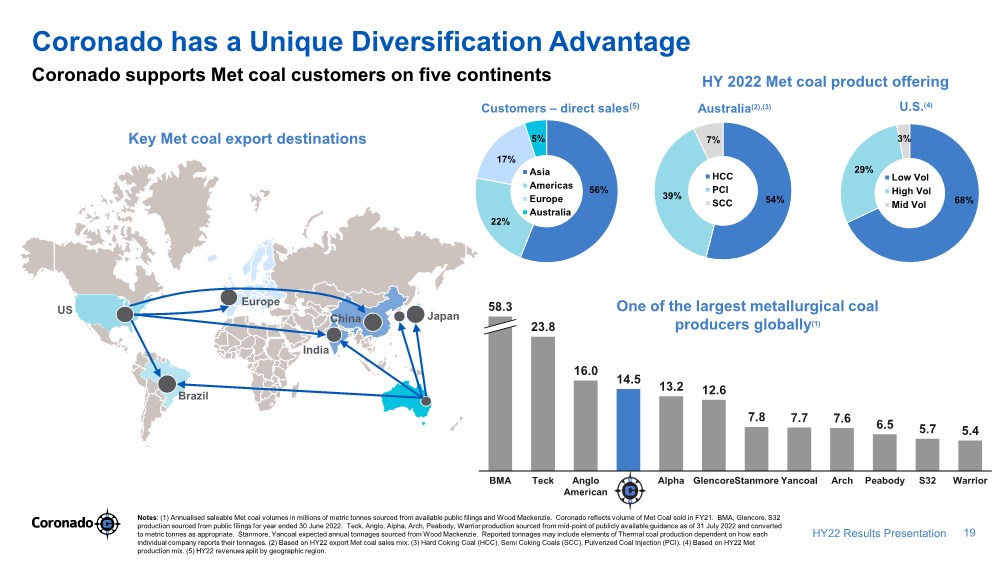

Met and thermal coal sales represented 96% and 4%, respectively, of total coal revenues for HY22. Export, Australian domestic and U.S. domestic sales represented 67%, 19% and 14%, respectively, of total coal volumes sold.

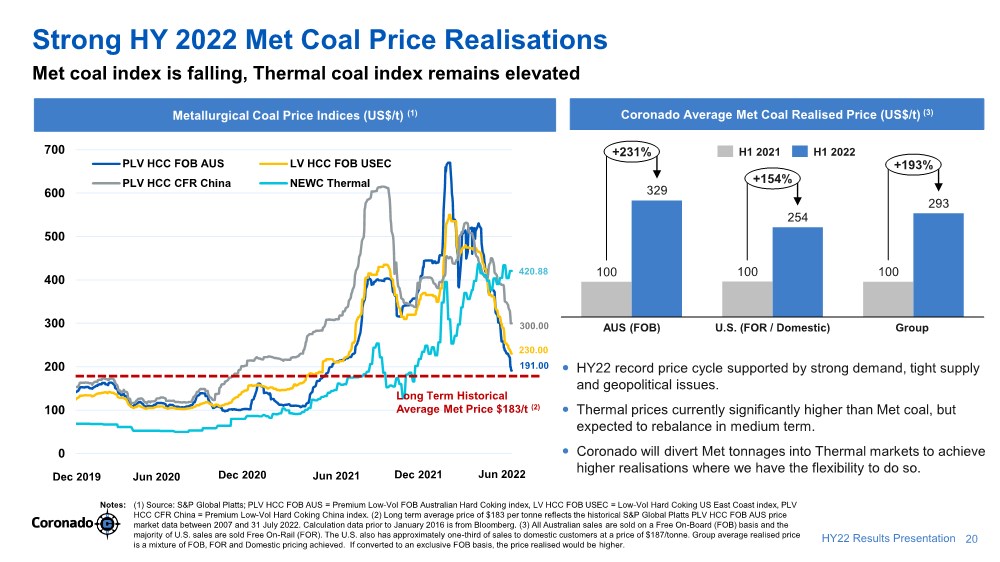

Met coal prices for shipments from both our U.S. and Australian operations reached record levels in the second quarter of FY22. The increase in benchmark prices since mid-2021 resulted in an HY22 Group average realised Met coal price of $292.8 per metric tonne sold (mixture of FOR, FOB and domestic terms), 193.4% higher compared to HY21.

On a segmental basis, the U.S. average realised Met coal price of $253.5 per metric tonne sold (primarily FOR basis), up 153.5% from HY21, reflecting a combination of contracted domestic and export prices. This realised price includes the $187 per metric tonne (FOR) price on domestic contracts received for FY22 U.S. volumes. The Australia average realised Met coal price per metric tonne sold, across all grades of Met coal produced from the Curragh operation, was $329.4 per metric tonne (FOB basis), up 230.7% from HY21.

4

SUSTAINABILITY

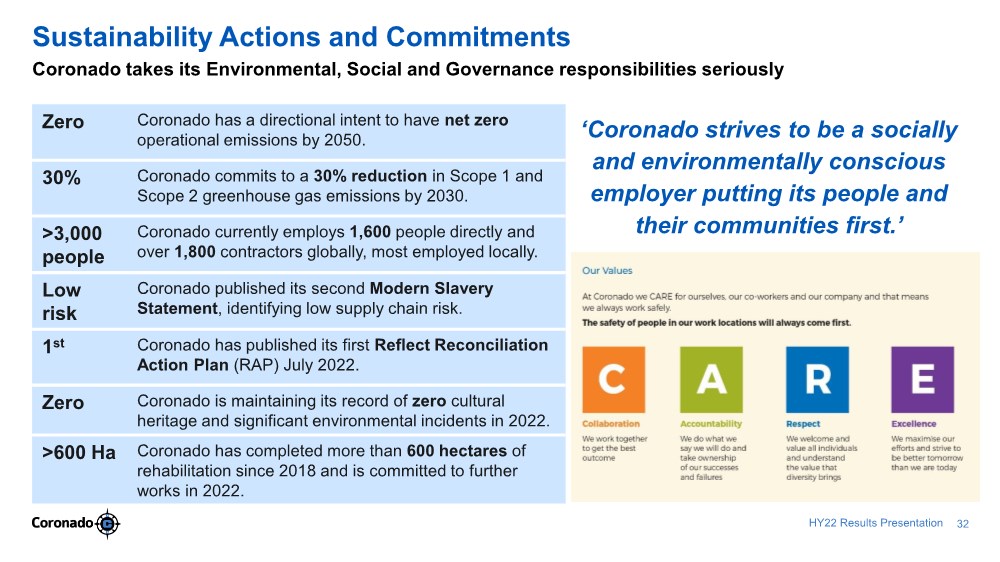

On 19 May 2022, Coronado released its fourth Sustainability Report, revealing a heightened focus on the environment and climate and a significant ongoing commitment to its people and communities.

The report, which summarises Coronado’s performance for the financial year ended 31 December 2021, highlights our commitment to sustainability through new targets, including a 30% reduction in greenhouse gas emissions by 2030, as part of Coronado’s directional intent to be net zero by 2050.

Underpinning our 30% reduction targets is the commencement on 27 July 2022 of our Ventilation Air Methane (VAM) project at our Buchanan Mine. Utilising the latest technology, the VAM project converts fugitive methane gas emissions to carbon dioxide, reducing the mine’s carbon footprint by 22.25 times. Overall projections show a reduction in Buchanan emissions by approximately 61% by 2030. While Coronado is also investigating other projects to reduce our carbon footprint, if the VAM projections are achieved, this project alone will meet our 30% reduction target.

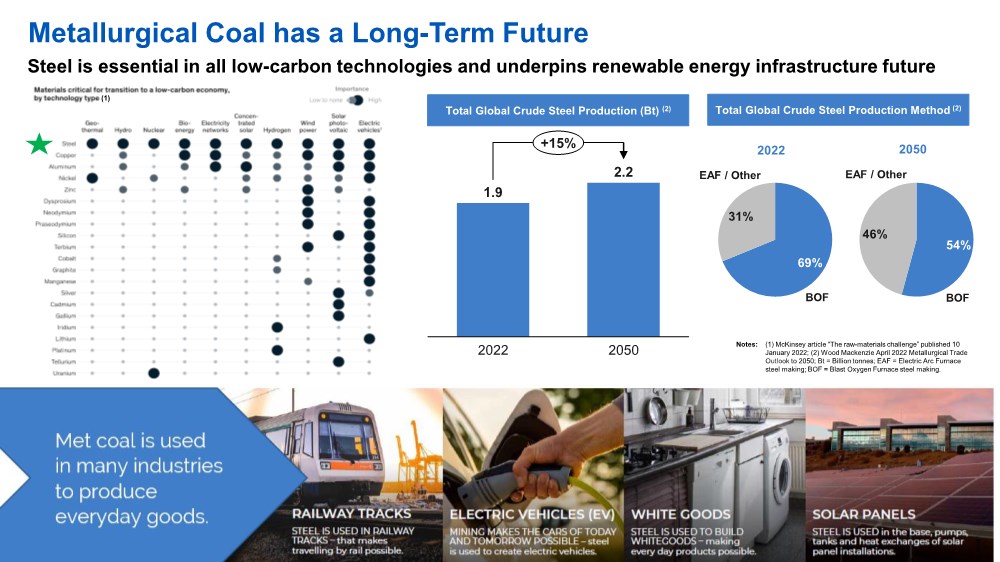

Coronado recognises its pivotal role in meeting the growing demand for steel globally. Steel is an essential material in creating future green technologies, including electric vehicles, solar panels and wind turbines. As technologies evolve and new solutions are found, we expect to leverage these, in addition to our identified projects, to achieve our emissions reduction goals.

The 2021 Sustainability Report can be accessed at https://coronadoglobal.com/environment-social-governance/.

5

METALLURGICAL COAL MARKET OUTLOOK 1

Interest in spot cargoes of Met Coal reduced significantly late in HY22 as steel production decreased globally and Australian coal supply improved. Covid-19 lockdowns in China have also led to disruptions to logistics along the steel value chain, including the supply of steel to end-users and raw materials to steel mills, lowering domestic steel and Met Coal demand in the short term.

Traditional market fundamentals continue to be challenged by the pandemic and the war in Ukraine. With European gas supplies under threat and Russian coal sales restricted, global demand for thermal coal has led to high energy prices and a market where thermal coal prices are currently above metallurgical coal prices. We expect these markets to revert to historical norms over the medium term.

Coronado Met Coal remains in high demand. Our high-quality products and unique geographical diversification allow us to switch products into different geographical markets or market segments that provide the highest return, for example, moving U.S. exports from China to Europe, or blending high-volatile coking coals for thermal applications, to take advantage of current unique market fundamentals created by trade restrictions.

Metallurgical coals can be utilized as thermal coal in thermal boilers if blended correctly. Depending on the technical design of the power station, there are some limitations concerning volatile matter content and free-swelling index, which must meet certain thresholds, making it harder to switch some Met coals than others. For example, specific PCI or Semi-Soft Coking Coals (SSCC) and other High Volatile Met coals, including Coronado US High Vol coals, have a greater ability to switch to the thermal coal market than the premium low volatile coals, which require a specifically designed power station (a smaller market segment).

In recent times, Coronado has seen the emergence of demand for our US high-volatile coking coals marketed as thermal coals into the European thermal market and similar demand for Australian PCI-type coals for Asian thermal markets and will switch to these markets where it makes sense to do so.

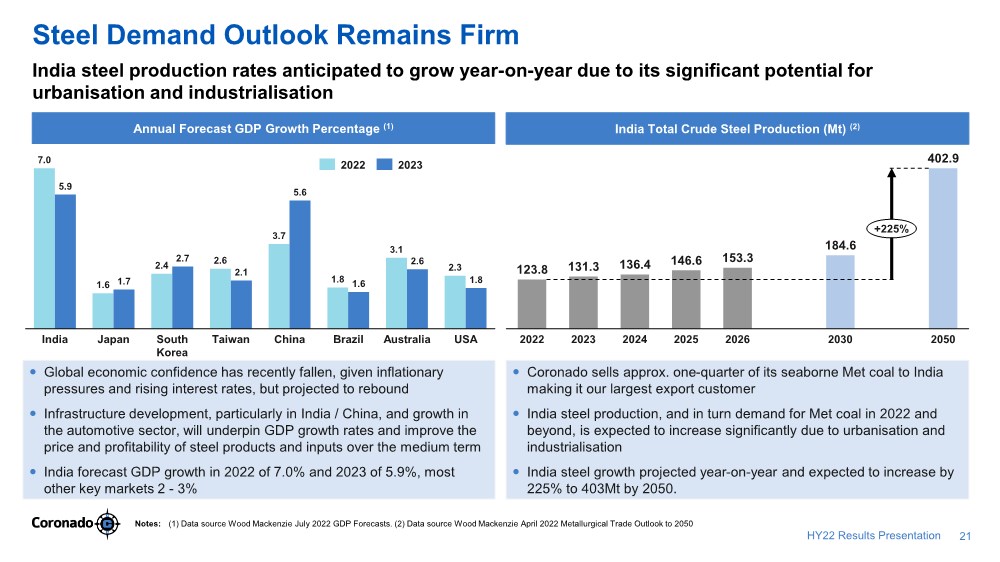

Global economic confidence has recently fallen, given global inflationary pressures and rising interest rates. However, confidence is projected to return in the longer term, which will underpin infrastructure projects requiring steel. India, Coronado’s largest single market, is forecasting GDP growth rates in 2022 and 2023 of 7.0% and 5.9%, respectively, with most other key markets forecasting modest growth rates of approximately 2% or higher.

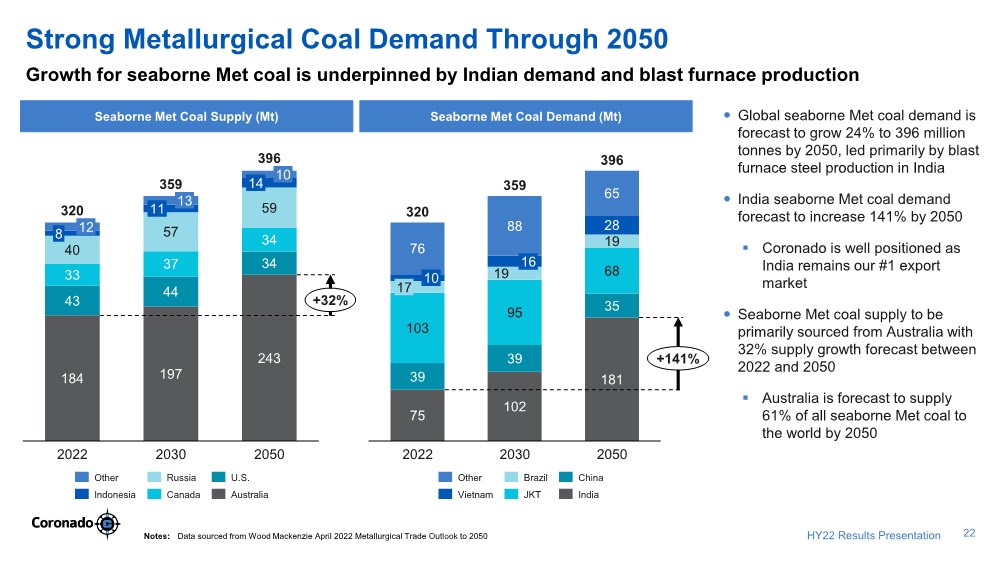

Long-term growth in global Met coal demand is anticipated to push seaborne trade up from an estimated 320 MMt in 2022 to 396 MMt in 2050. India is expected to lead all countries in import demand growth due to its significant potential for urbanisation and industrialisation. Imports are expected to increase to 181 MMt by 2050, up 141% from expected 2022 levels. Indian crude steel production is expected to grow from 124 MMt to 403 MMt by 2050, an increase underpinned by Blast Furnace steel generation methods. Coronado traditionally sells approximately one-quarter of its seaborne Met coal to India making it Coronado’s largest market.

For the remainder of 2022, Coronado expects Met Coal demand to be balanced between downward pressure on steel demand due to the current short-term global growth outlook and upward pressure from the seaborne coal trade restrictions on Russian coal taking effect from August 2022 and expectations of India restocking following the monsoon season. Despite the uncertainties, Met Coal prices are expected to remain above historical averages supported by the global automotive sector improving as the supply crunch eases and high energy costs benefit thermal coal prices, providing support to Met Coal prices.

1 Source: Wood Mackenzie April 2022 Metallurgical Trade Outlook to 2050; Wood Mackenzie July 2022 GDP forecasts.

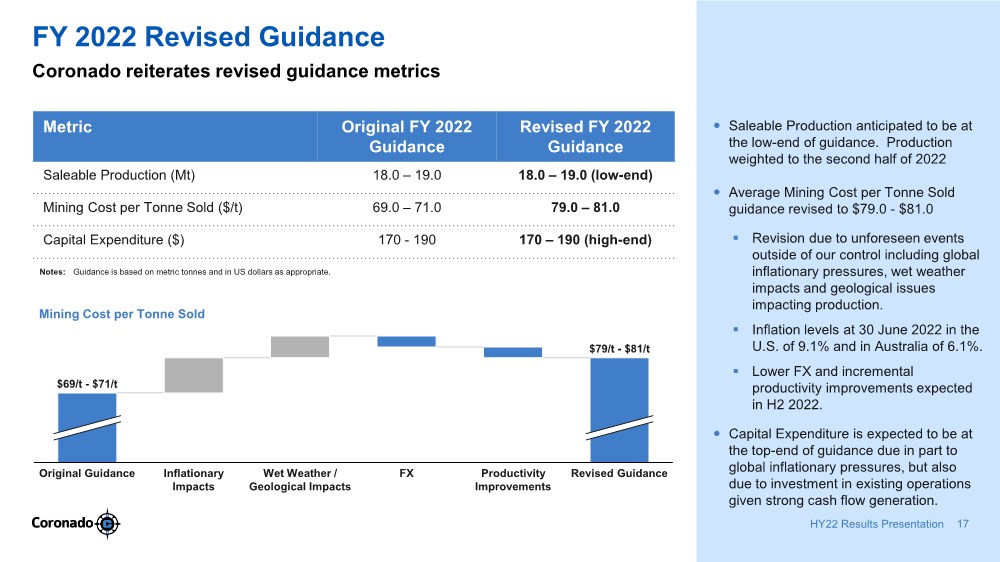

FY22 GUIDANCE

Original FY 2022 Guidance | Revised FY 2022 Guidance | |||

| Saleable Production (MMt) | 18.0 – 19.0 | 18.0 – 19.0 (low-end) | ||

| Mining Cost per Tonne Sold ($) * | 69.0 – 71.0 | 79.0 – 81.0 | ||

| Capex ($m) | 170 - 190 | 170 – 190 (high-end) |

* Mining Cost per Tonne Sold revised guidance assumes an average AUD : USD foreign exchange rate assumption of 0.71 for FY22.

6

Mining Cost per Tonne Sold guidance for FY2022 is revised to $79.0 - $81.0 due to unforeseen events outside of our control including global inflationary pressures exceeding original budget estimates and year-to-date wet weather impacts and geological issues impacting production. Inflation levels at 30 June 2022 in the U.S. reached a 40-year high of 9.1% and in Australia reached a 20-year high of 6.1%, and are expected to remain at elevated levels for the balance of 2022. Coronado anticipates that these increases will be partly mitigated by lower FX and incremental productivity improvements in H2 2022.

For a detailed review of Coronado’s operating and financial performance, investors should refer to the Company’s Quarterly Report on Form 10-Q, Appendix 4D, and the Investor Presentation released to the Australian Securities Exchange and the Securities and Exchange Commission on 9 August 2022 (AEST).

Approved for release by the Board of Directors of Coronado Global Resources Inc.

For further information, please contact:

Investors Andrew Mooney Vice President Investor Relations & Communications P: +61 458 666 639 E: amooney@coronadoglobal.com E: investors@coronadoglobal.com |

Media Helen McCombie Citadel Magnus P: +61 411 756 248 E: hmccombie@citadelmagnus.com

|

7

Cautionary Notice Regarding Forward–Looking Statements

This report contains forward-looking statements concerning our business, operations, financial performance and condition, the coal, steel and other industries, as well as our plans, objectives and expectations for our business, operations, financial performance and condition. Forward-looking statements may be identified by words such as "may," "could," "believes," "estimates," "expects," "intends," “plans”, "considers", “forecasts”, “targets” and other similar words that involve risk and uncertainties. Forward-looking statements provide management's current expectations or predictions of future conditions, events or results. All statements that address operating performance, events or developments that we expect or anticipate will occur in the future are forward-looking statements. They may include estimates of revenues, income, earnings per share, cost savings, capital expenditures, dividends, share repurchases, liquidity, capital structure, market share, industry volume, or other financial items, descriptions of management’s plans or objectives for future operations, or descriptions of assumptions underlying any of the above. All forward-looking statements speak only as of the date they are made and reflect the company's good faith beliefs, assumptions and expectations, but they are not guarantees of future performance or events. Furthermore, the company disclaims any obligation to publicly update or revise any forward-looking statement, except as required by law. By their nature, forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those suggested by the forward-looking statements. Factors that might cause such differences include, but are not limited to, a variety of economic, competitive and regulatory factors, many of which are beyond the Company's control, that are described in our Annual Report on Form 10-K filed with the ASX and SEC on 23 February 2022 (AEST), our Quarterly Report on Form 10-Q filed with the ASX and SEC on 10 May 2022 (AEST) and our Quarterly Report on Form 10-Q filed with the ASX and SEC on 9 August 2022 (AEST), as well as additional factors we may describe from time to time in other filings with the ASX and SEC. You may get such filings for free at our website at www.coronadoglobal.com. You should understand that it is not possible to predict or identify all such factors and, consequently, you should not consider any such list to be a complete set of all potential risks or uncertainties.

Reconciliation of Non-GAAP Measures

This report which includes a discussion of results of operations includes references to and analysis of certain non-GAAP measures (as described below), which are financial measures not recognized in accordance with U.S. GAAP. Non-GAAP financial measures are used by the Company and investors to measure operating performance.

Management uses a variety of financial and operating metrics to analyze performance. These metrics are significant factors in assessing operating results and profitability. These financial and operating metrics include: (i) safety and environmental metrics; (ii) Adjusted EBITDA, (iii) total sales volumes and average realised price per Mt sold, which we define as total coal revenues divided by total sales volume; (iv) Metallurgical coal sales volumes and average realized metallurgical price per tonne sold, which we define as metallurgical coal revenues divided by metallurgical sales volume; (v) Mining costs per Mt sold, which we define as mining cost of coal revenues divided by sales volumes (excluding non-produced coal) for the respective segment; (vi) Operating costs per Mt sold, which we define as operating costs divided by sales volumes for the respective segment. Investors should be aware that the Company’s presentation of Adjusted EBITDA and other non-GAAP measures may not be comparable to similarly titled financial measures used by other companies. We define Net Cash / (Debt) as cash and cash equivalents (excluding restricted cash) less the outstanding aggregate principal amount of 10.750% senior secured notes due 2026.

Reconciliations of certain forward-looking non-GAAP financial measures, including our 2022 Mining Cost per Tonne Sold guidance, to the most directly comparable GAAP financial measures are not provided because the Company is unable to provide such reconciliations without unreasonable effort, due to the uncertainty and inherent difficulty of predicting the occurrence and the financial impact of items impacting comparability and the periods in which such items may be recognised. For the same reasons, the Company is unable to address the probable significance of the unavailable information, which could be material to future results.

8

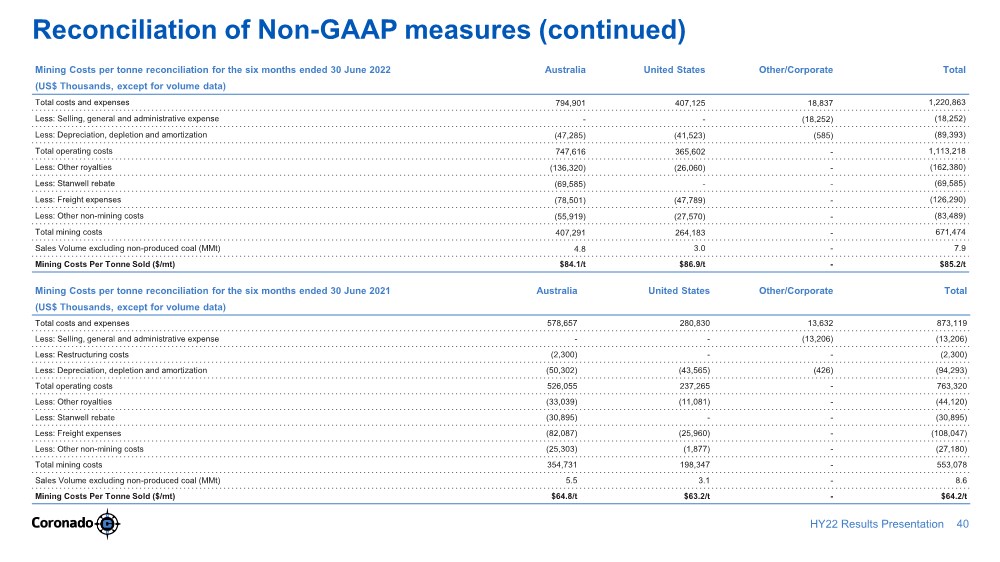

MINING AND OPERATING COSTS PER TONNE RECONCILIATION

| For the six months ended 30 June 2022 | |||||||||||||||

| (In US$’000, except for volume data) | Australia | United States |

Other / Corporate | Total Consolidated |

|||||||||||

| Total costs and expenses | 794,901 | 407,125 | 18,837 | 1,220,863 | |||||||||||

| Less: Selling, general and administrative expense | - | - | (18,252 | ) | (18,252) | ||||||||||

| Less: Depreciation, depletion and amortization | (47,285 | ) | (41,523 | ) | (585 | ) | (89,393) | ||||||||

| Total operating costs | 747,616 | 365,602 | - | 1,113,218 | |||||||||||

| Less: Other royalties | (136,320 | ) | (26,060 | ) | - | (162,380) | |||||||||

| Less: Stanwell rebate | (69,585 | ) | - | - | (69,585) | ||||||||||

| Less: Freight expenses | (78,501 | ) | (47,789 | ) | - | (126,290) | |||||||||

| Less: Other non-mining costs | (55,919 | ) | (27,570 | ) | - | (83,489) | |||||||||

| Total mining costs | 407,291 | 264,183 | - | 671,474 | |||||||||||

| Sales Volume excluding non-produced coal (MMt) | 4.8 | 3.0 | - | 7.9 | |||||||||||

| Mining Costs Per Tonne Sold | $ | 84.1 | /t | $ | 86.9 | /t | - | $ | 85.2 | /t | |||||

| For the six months ended 30 June 2021 | ||||||||||||||||

(In US$’000, except for volume data) | Australia | United States | Other / Corporate | Total Consolidated | ||||||||||||

| Total costs and expenses | 578,657 | 280,830 | 13,632 | 873,119 | ||||||||||||

| Less: Selling, general and administrative expense | - | - | (13,206 | ) | (13,206 | ) | ||||||||||

| Less: Restructuring costs | (2,300 | ) | - | - | (2,300 | ) | ||||||||||

| Less: Depreciation, depletion and amortization | (50,302 | ) | (43,565 | ) | (426 | ) | (94,293 | ) | ||||||||

| Total operating costs | 526,055 | 237,265 | - | 763,320 | ||||||||||||

| Less: Other royalties | (33,039 | ) | (11,081 | ) | - | (44,120 | ) | |||||||||

| Less: Stanwell rebate | (30,895 | ) | - | - | (30,895 | ) | ||||||||||

| Less: Freight expenses | (82,087 | ) | (25,960 | ) | - | (108,047 | ) | |||||||||

| Less: Other non-mining costs | (25,303 | ) | (1,877 | ) | - | (27,180 | ) | |||||||||

| Total mining costs | 354,731 | 198,347 | - | 553,078 | ||||||||||||

| Sales Volume excluding non-produced coal (MMt) | 5.5 | 3.1 | - | 8.6 | ||||||||||||

| Mining Costs Per Tonne Sold | $ | 64.8 | /t | $ | 63.2 | /t | - | $ | 64.2 | /t | ||||||

(In US$’000, except for volume data) | For the six months ended 30 June 2022 | For the six months ended 30 June 2021 | ||||||

| Total costs and expenses | 1,220,863 | 873,119 | ||||||

| Less: Selling, general and administrative expense | (18,252 | ) | (13,206 | ) | ||||

| Less: Restructuring costs | - | (2,300 | ) | |||||

| Less: Depreciation, depletion and amortization | (89,393 | ) | (94,293 | ) | ||||

| Total operating costs | 1,113,218 | 763,320 | ||||||

| Sales Volume (MMt) | 8.3 | 8.9 | ||||||

| Operating Costs Per Tonne Sold | $ | 134.5 | /t | $ | 85.8 | /t | ||

9

REALISED PRICING RECONCILIATION

| For the six months ended 30 June 2022 | ||||||||||||

| (In US$’000, except for volume data) | Australia | United States | Consolidated | |||||||||

| Total Revenues | 1,183,686 | 796,143 | 1,979,829 | |||||||||

| Less: Other revenues | (19,042 | ) | (3,162 | ) | (22,204 | ) | ||||||

| Total coal revenues | 1,164,644 | 792,981 | 1,957,625 | |||||||||

| Less: Thermal coal revenues | (67,291 | ) | (4,402 | ) | (71,693 | ) | ||||||

| Metallurgical coal revenues | 1,097,353 | 788,579 | 1,885,932 | |||||||||

| Volume of Metallurgical coal sold (MMt) | 3.3 | 3.1 | 6.4 | |||||||||

| Average Realised Met Price Per Tonne Sold | $ | 329.4 | /t | $ | 253.5 | /t | $ | 292.8 | /t | |||

| For the six months ended 30 June 2021 | ||||||||||||

| (In US$’000, except for volume data) | Australia | United States | Consolidated | |||||||||

| Total Revenues | 489,726 | 310,641 | 800,367 | |||||||||

| Less: Other revenues | (17,527 | ) | (1,874 | ) | (19,401 | ) | ||||||

| Total coal revenues | 472,199 | 308,767 | 780,966 | |||||||||

| Less: Thermal coal revenues | (44,089 | ) | (3,311 | ) | (47,400 | ) | ||||||

| Metallurgical coal revenues | 428,110 | 305,456 | 733,566 | |||||||||

| Volume of Metallurgical coal sold (MMt) | 4.3 | 3.1 | 7.4 | |||||||||

| Average Realised Met Price Per Tonne Sold | $ | 99.6 | /t | $ | 100.0 | /t | $ | 99.8 | /t | |||

ADJUSTED EBITDA RECONCILIATION

| (In US$’000) | For the six months 30 June 2022 | For the six months 30 June 2021 | ||||||

| Reconciliation to Adjusted EBITDA: | ||||||||

| Net Income / (Loss) | 561,893 | (96,057 | ) | |||||

| Add: Depreciation, depletion and amortization | 89,393 | 94,293 | ||||||

| Add: Interest expense, net | 34,814 | 31,731 | ||||||

| Add: Other foreign exchange (gains) / losses | (23,147 | ) | 1,889 | |||||

| Add: Loss on debt extinguishment | - | 5,744 | ||||||

| Add: Income tax expense / (benefit) | 183,968 | (10,884 | ) | |||||

| Add: Restructuring costs | - | 2,300 | ||||||

| Add: Losses on idled assets held for sale | 1,842 | 2,330 | ||||||

| Add: Increase / (Decrease) in provision for discounting and credit losses | 584 | (5,644 | ) | |||||

| Adjusted EBITDA | 849,347 | 25,702 | ||||||

NET CASH / (DEBT) RECONCILIATION

| (In US$’000) | 30 June 2022 | 30 June 2021 | ||||||

| Reconciliation to Net Cash / (Debt): | ||||||||

| Cash and restricted cash | 485,884 | 113,661 | ||||||

| Less: Restricted cash | (251 | ) | (251 | ) | ||||

| Cash and cash equivalents (excluding restricted cash) | 485,633 | 113,410 | ||||||

| Less: Aggregate principal amount of 10.750% Senior Secured Notes due 2026 | (314,453 | ) | (350,000 | ) | ||||

| Net Cash / (Debt) | 171,180 | (236,590 | ) | |||||

10