The Company’s shares of common stock began trading on the NASDAQ Global Select Market on June 30, 2016. Accordingly, no comparative stock performance information is available for periods ending prior to this date. The performance graph below compares the Company’s cumulative shareholder return on its common stock since inception of trading on June 30, 2016 to the cumulative total return of the Russell 2000 index of small capitalization companies and the SNL U.S. Thrift Composite comprising thrifts with total assets of $1.0 billion to $5.0 billion. The initial offering price of the Company’s shares was $10.00 per share; however, the graph below depicts the cumulative return on the stock since inception of trading at $7.14 per share on June 30, 2016. Total shareholder return is measured by dividing total dividends (assuming dividend reinvestment) for the measurement period plus share price change for the period from the share price at the beginning of the measurement period. The return is based on the initial investment of $100.00. The information provided under Item 12 hereto is incorporated herein by reference.

The following information in this Item 5 of this Annual Report 10-K is not deemed to be “soliciting material” or to be “filed” with the SEC or subject to Regulation 14A or 14C under the Securities Exchange Act of 1934 or to be liabilities of Section 18 of the Securities Exchange Act of 1934, and will not be deemed incorporated by reference into any filing under the Securities Act of 1933 or the Securities Exchange Act of 1934, except to the extent the Company specifically incorporates it by reference to such filing. The stock price performance shown on the stock performance graph and associated table below is not necessarily indicative of future price performance. Information used in the graph and table was obtained from a third-party provider, a source believed to be reliable, but the Company is not responsible for any errors or omissions in such information.

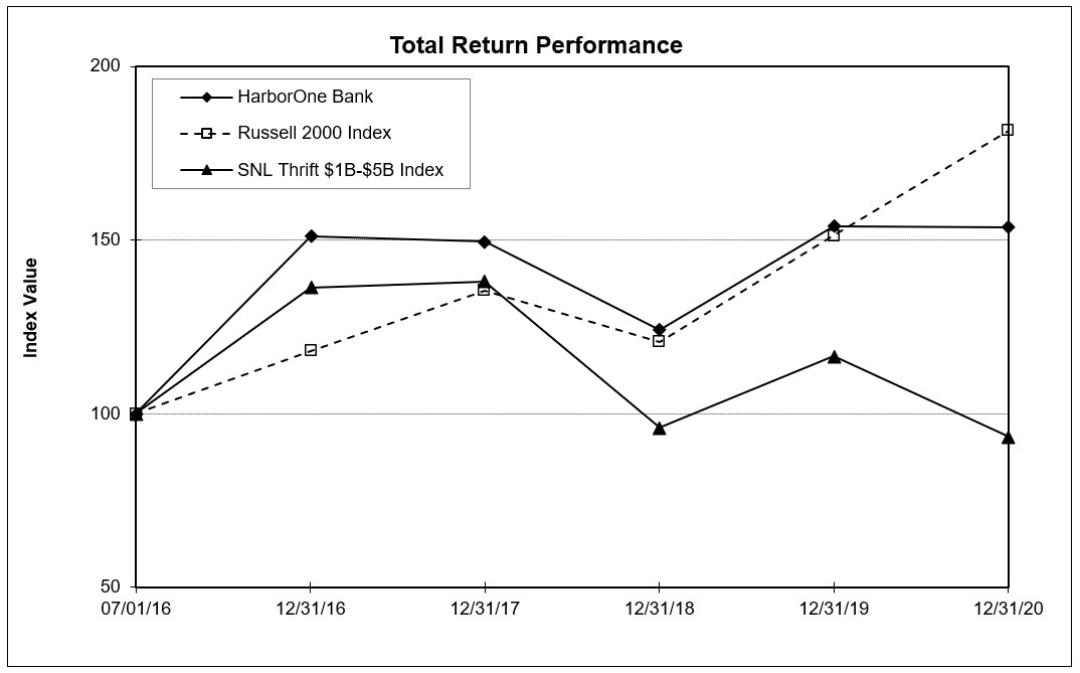

The following chart depicts the total return performance of the Company:

Period Ending | |||||||||||

Index | 07/01/16 | 12/31/16 | 12/31/17 | 12/31/18 | 12/31/19 | 12/31/20 | |||||

HarborOne Bancorp, Inc. | 100.00 | 150.98 | 149.57 | 124.04 | 154.03 | 153.72 | |||||

Russell 2000 Index | 100.00 | 118.18 | 135.49 | 120.56 | 151.34 | 181.55 | |||||

SNL Thrift $1B-$5B Index | 100.00 | 136.19 | 137.94 | 98.98 | 116.46 | 93.54 | |||||

Source : SNL Financial, an offering of S&P Global Market Intelligence | |||||||||||

32