Exhibit 99.1

Information Statement

OSPREY BITCOIN TRUST

Osprey Bitcoin Trust (the

“Trust”) issues common units of fractional undivided beneficial interest (“Units”), which represent

ownership in the Trust. The Trust’s purpose is to hold Bitcoins, which are digital assets that are created and transmitted

through the operations of the peer-to-peer Bitcoin Network, a decentralized network of computers that operates on cryptographic

protocols. The investment objective of the Trust, which is a passive investment vehicle, is for the Units to reflect the performance

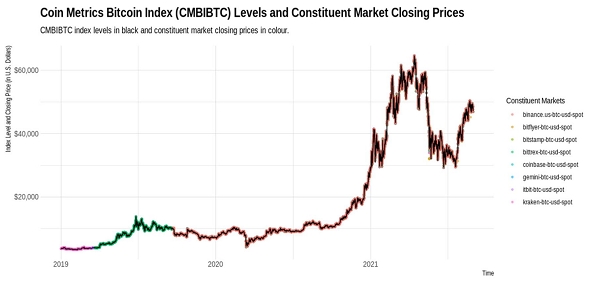

of Bitcoin as measured by reference to Coin Metrics CMBI Bitcoin Index (the “Index”) provided by Coin Metrics Inc. (the

“Index Provider”), less the Aggregate Trust Expenses (defined below) and other liabilities. The Trust determines the

current value of Bitcoin by reference to the market price of Bitcoin traded on Coinbase Pro, the Trust’s principal market, as determined at 4:00 p.m., New York time on each day the New York Stock Exchange

is open for trading (each, a “Business Day”) (the “Bitcoin Market Price”). The Bitcoin Market Price is

available at https://pro.coinbase.com/trade/BTC-USD. The Units are intended to constitute a cost-effective and convenient means of

gaining investment exposure to Bitcoin. However, an investment in the Units may operate and perform differently over time, or at any

specific point in time, than an investment directly in Bitcoin due to such factors as Trust fees and expenses, the quantity of Units

available for trading, the relative liquidity of the Units, and differences in the markets trading Bitcoin and Units (e.g., hours of

operation, marketplace rules, clearance and settlement, and market participants). Osprey Funds, LLC is the sponsor of the Trust (the

“Sponsor”), Delaware Trust Company is the trustee of the Trust (the “Trustee”), Continental Stock

Transfer & Trust Company is the transfer agent of the Trust (in such capacity, the “Transfer Agent”), Theorem

Fund Services is the administrator of the Trust (in such capacity, the “Administrator”), and Fidelity Digital Assets

Services, LLC is the custodian for the Trust (the “Custodian”), and will custody the Trust’s Bitcoin.

The Trust issues Units only

in connection with purchase orders for a minimum of $25,000.00 for initial investments and $10,000.00 for subsequent investments.

The Units represent common units of fractional undivided beneficial interest in and ownership of the Trust and have no par value.

The Units may be purchased from the Trust on an ongoing basis, but only by an accredited investor (“Accredited Investor”)

(as defined in Rule 501 under the Securities Act of 1933, as amended (the “Securities Act”). At this time, the Sponsor

is not operating a redemption program for the Units and therefore Units are not redeemable by the Trust. Due to the lack of an

ongoing redemption program as well as price volatility, low trading volume and closings of Bitcoin exchanges due to fraud, failure,

security breaches or otherwise, there can be no assurance that the market value of the Units will reflect the per Unit value of

the Trust’s Bitcoin, less the Trust’s expenses and other liabilities (“NAV per Unit”), and the Units may

trade at a substantial premium over, or a substantial discount to, the NAV per Unit.

Investments in the Units involves

significant risks. See “Risk Factors” starting on page 7.

The Units are neither interests

in nor obligations of the Sponsor or the Trustee.

Units are distributed by

the Sponsor through sales in private placement transactions exempt from the registration requirements of the Securities Act pursuant

to Rule 506(c) thereunder. The Units are quoted on OTC Markets Group Inc.’s OTCQX® Best Marketplace (“OTCQX”)

under the ticker symbol “OBTC.”

The Trust uses the Bitcoin Market Price to calculate

its “Bitcoin Holdings,” which is the aggregate value, expressed in U.S. dollars, of the Trust’s assets (other

than U.S. dollars, other fiat currency, and Additional Currency (as that term is defined herein)), less the U.S. dollar value of

the Trust’s expenses and other liabilities calculated in the manner set forth under “Valuation of Bitcoin and Determination

of the Trust’s Bitcoin Holdings.” “Bitcoin Holdings per Unit” is calculated by dividing Bitcoin Holdings

by the number of Units currently outstanding.

The date of this Information Statement is

September 10, 2021

TABLE OF CONTENTS

| STATEMENT REGARDING FORWARD-LOOKING STATEMENTS |

1 |

| KEY OPERATING METRICS |

1 |

| SUMMARY |

3 |

| RISK FACTORS |

7 |

| OVERVIEW OF THE BITCOIN INDUSTRY AND MARKET |

35 |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

44 |

| DESCRIPTION OF THE TRUST |

51 |

| ACTIVITIES OF THE TRUST |

52 |

| THE SPONSOR |

54 |

| THE TRUSTEE |

56 |

| THE TRANSFER AGENT |

56 |

| THE CUSTODIAN |

57 |

| CONFLICTS OF INTEREST |

58 |

| PRINCIPAL UNITHOLDERS |

59 |

| DESCRIPTION OF THE UNITS |

60 |

| CUSTODY OF THE TRUST’S BITCOINS |

63 |

| DESCRIPTION OF ISSUANCE OF UNITS |

64 |

| VALUATION OF BITCOIN AND DETERMINATION OF BITCOIN HOLDINGS |

66 |

| EXPENSES; SALES OF BITCOINS |

69 |

| STATEMENTS, FILINGS AND REPORTS |

69 |

| DESCRIPTION OF THE TRUST DOCUMENTS |

70 |

| CERTAIN U.S. FEDERAL INCOME TAX CONSEQUENCES |

76 |

| ERISA AND RELATED CONSIDERATIONS |

82 |

| INDEX TO FINANCIAL STATEMENTS |

F-1 |

Neither the Sponsor nor

the Trust have authorized anyone to provide you with information different from that contained in this Information Statement or

any amendment or supplement to this Information Statement prepared by us or on our behalf. Neither the Sponsor nor the Trust take

any responsibility for, or can provide any assurance as to the reliability of, any information other than the information in this

Information Statement or any amendment or supplement to this Information Statement prepared by the Sponsor, the Trust or on the

Trust’s behalf. The information in this Information Statement is accurate only as of the date of this Information Statement.

In this Information Statement,

unless otherwise stated or the context otherwise requires, “we,” “our” and “us” refers to the

Sponsor acting on behalf of the Trust.

Industry and Market Data

Although we are responsible

for all disclosure contained in this Information Statement, in some cases we have relied on certain market and industry data obtained

from third-party sources that we believe to be reliable. Market estimates are calculated by using independent industry publications

in conjunction with our assumptions regarding the Bitcoin industry and market. While we are not aware of any misstatements regarding

any market, industry or similar data presented herein, such data involves risks and uncertainties and is subject to change based

on various factors, including those discussed under the headings “Statement Regarding Forward-Looking Statements” and

“Risk Factors” in this Information Statement.

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Information Statement

contains “forward-looking statements” with respect to the Trust’s financial conditions, results of operations,

plans, objectives, future performance and business. Statements preceded by, followed by or that include words such as “may,”

“might,” “will,” “should,” “expect,” “plan,” “anticipate,”

“believe,” “estimate,” “predict,” “potential” or “continue,” the negative

of these terms and other similar expressions are intended to identify some of the forward-looking statements. All statements (other

than statements of historical fact) included in this Information Statement that address activities, events or developments that

will or may occur in the future, including such matters as changes in market prices and conditions, the Trust’s operations,

the Sponsor’s plans and references to the Trust’s future success and other similar matters are forward-looking statements.

These statements are only predictions. Actual events or results may differ materially from such statements. These statements are

based upon certain assumptions and analyses the Sponsor made based on its perception of historical trends, current conditions and

expected future developments, as well as other factors appropriate in the circumstances. You should specifically consider the numerous

risks outlined under “Risk Factors.” Whether or not actual results and developments will conform to the Sponsor’s

expectations and predictions, however, is subject to a number of risks and uncertainties, including:

| ● | the risk factors discussed in this Information Statement, including the particular risks associated with new technologies such

as Bitcoin and blockchain technology; |

| ● | the inability to redeem Units; |

| ● | the economic conditions in the Bitcoin industry and market; |

| ● | general economic, market and business conditions; |

| ● | the use of technology by us and our vendors, including the Custodian, in conducting our business, including disruptions in

our computer systems and data centers and our transition to, and quality of, new technology platforms; |

| ● | changes in laws or regulations, including those concerning taxes, made by governmental authorities or regulatory bodies; |

| ● | the costs and effect of any litigation or regulatory investigations; |

| ● | our ability to maintain a positive reputation; and |

| ● | other world economic and political developments. |

Consequently, all the forward-looking

statements made in this Information Statement are qualified by these cautionary statements, and there can be no assurance that

the actual results or developments the Sponsor anticipates will be realized or, even if substantially realized, that they will

result in the expected consequences to, or have the expected effects on, the Trust’s operations or the value of the Units.

Should one or more of the risks discussed under “Risk Factors” or other uncertainties materialize, or should underlying

assumptions prove incorrect, actual outcomes may vary materially from those described in forward-looking statements. Forward-looking

statements are made based on the Sponsor’s beliefs, estimates and opinions on the date the statements are made and neither

the Trust nor the Sponsor is under a duty or undertakes an obligation to update forward-looking statements if these beliefs, estimates

and opinions or other circumstances should change, other than as required by applicable laws. Moreover, neither the Trust, the

Sponsor, nor any other person assumes responsibility for the accuracy and completeness of any of these forward-looking statements.

KEY OPERATING METRICS

The Trust’s Bitcoins

are carried, for financial statement purposes, at fair value, as required by the U.S. generally accepted accounting principles

(“GAAP”). The Trust values its Bitcoin holdings at the Bitcoin Market Price

as of 4:00 p.m., New York time on each Business

Day. The net asset value of the Trust determined on a GAAP basis is referred to in this Information Statement as “NAV.”

Prior to May 18, 2021, the Trust referenced Index as its principal market and used the Index for purposes of determining the valuation

of its Bitcoin holdings. The Trust changed its principal market to Coinbase Pro on May 18, 2021 to facilitate its compliance with

GAAP. The Trust selected Coinbase Pro, among other Bitcoin markets, because it provides the greatest liquidity, with approximately

45% of daily trading volume as of May 10, 2021. More information about the valuation of the Trust’s Bitcoin Holdings and

the use of the Bitcoin Market Price is located herein under “Valuation of Bitcoin and Determination of Bitcoin Holdings.”

To determine which Bitcoin

market will serve as the Trust’s principal market (or in the absence of a principal market, the most advantageous market)

for purposes of calculating the Trust’s NAV, the Trust follows Financial Accounting Standards Board (“FASB”)

Accounting Standards Codification (“ASC”) 820-10, which outlines the application of fair value accounting. ASC 820-10

determines fair value to be the price that would be received for Bitcoin in a current sale, which assumes an orderly transaction

between market participants on the measurement date. ASC 820-10 requires the Trust to assume that Bitcoin is sold in its principal

market to market participants or, in the absence of a principal market, the most advantageous market. Market participants are defined

as buyers and sellers in the principal or most advantageous market that are independent, knowledgeable, and willing and able to

transact.

The Trust purchases Bitcoin

directly from various counterparties, such as Galaxy Digital, Jane Street, and Cumberland DRW LLC, and does not itself transact

in any Bitcoin markets. Therefore, the Trust looks to these counterparties when assessing entity-specific and market-based volume

and the level of activity in the Bitcoin markets. The Trust utilizes the Bitcoin Market Price to determine the value of Bitcoin

at any given time. The Trust evaluates its principal market selection (or in the absence of a principal market the most advantageous

market) at least annually and conducts a quarterly analysis to determine (i) if there have been recent changes to each Bitcoin

market’s trading volume and level of activity in the trailing twelve months, (ii) if any Bitcoin markets have developed that

the Trust has access to, or (iii) if recent changes to a Bitcoin market’s price stability have occurred that would materially

impact the selection of the principal market and necessitate a change in the Trust’s determination of its principal market.

The Trust does not anticipate changing its principal market more frequently than annually, in connection with its annual evaluation

of its principal market selection and annual financial audit. Each annual evaluation will take into account the findings from the

Trust’s quarterly reviews.

The cost basis of a Trust

investment in Bitcoin recorded by the Trust for financial reporting purposes is the fair value of the Bitcoin at the time of contribution

to the Trust. The Bitcoin cost basis recorded by the Trust may differ from the value of the proceeds collected by the Sponsor from

the sale of the corresponding Units to investors.

The investment objective

of the Trust is for the Units to reflect the performance of the Bitcoin as measured by reference to the Index, less the Aggregate

Trust Expenses (as defined below) and other liabilities. See “Valuation of Bitcoin and Determination of Bitcoin Holdings.” Units may not

be redeemed from the Trust currently, and absent the granting of certain SEC relief, the Trust does not currently contemplate offering

a redemption program. In addition, the Trust may from time to time halt creations. As a result, there can be no assurance that

the market value of the Units will reflect the value of the Trust’s NAV per Unit. The Units may trade at a substantial premium

over, or a substantial discount to, the NAV per Unit for a variety of reasons, including as a result of market price volatility,

trading volume and closings of Bitcoin trading markets due to fraud, failure, security breaches or otherwise.

The Trust uses the Bitcoin

Market Price to calculate its “Bitcoin Holdings,” which is the aggregate value, expressed in U.S. dollars, of the Trust’s

assets (other than U.S. dollars, other fiat currency, and Additional Currency (as that term is defined herein)), less the U.S.

dollar value of the Trust’s expenses and other liabilities calculated in the manner set forth under “Valuation of Bitcoin

and Determination of the Trust’s Bitcoin Holdings.” “Bitcoin Holdings per Unit” is calculated by dividing

Bitcoin Holdings by the number of Units currently outstanding. Bitcoin Holdings and Bitcoin Holdings per Unit are not measures

calculated in accordance with GAAP. Bitcoin Holdings is not intended to be a substitute for the Trust’s NAV calculated in

accordance with GAAP, and Bitcoin Holdings per Unit is not intended to be a substitute for the Trust’s NAV per Unit calculated

in accordance with GAAP.

SUMMARY

The following is a summary

only and is qualified in its entirety by reference to the more detailed information set forth in the Trust Agreement and in the

other agreements described herein. To the extent of any conflict between this summary and the Trust Agreement, the terms of the

Trust Agreement will govern.

See “Glossary of

Defined Terms” for the definition of certain capitalized terms used in this Information Statement. All other capitalized

terms used, but not defined, herein have the meanings given to them in the Trust Agreement.

Overview of the Trust and the Units

The Trust is a Delaware

Statutory Trust that was formed on January 3, 2019 by the filing of the Certificate of Trust with the Delaware Secretary of State

in accordance with the provisions of the Delaware Statutory Trust Act. The Trust issues Units, which represent common units of

fractional undivided beneficial interest in, and ownership of, the Trust, on an ongoing basis to certain “accredited investors”

within the meaning of Rule 501(a) of Regulation D under the Securities Act.

The purpose of the Trust,

which is passive investment vehicle, is to provide investors a cost-effective and convenient way to invest in Bitcoin. However, an

investment in the Units may operate and perform differently over time, or at any specific point in time, than an investment directly

in Bitcoin due to such factors as Trust fees and expenses, the quantity of Units available for trading, and the relative liquidity

of the Units, and differences in the markets trading Bitcoin and Units (e.g., hours of operation, marketplace rules, clearance and

settlement, and market participants). The investment objective of the Trust is for the Units to reflect the performance of Bitcoin as measured by reference to the Index, less the Aggregate Trust Expenses (as defined below) and other liabilities. The Trust issues Units only

in connection with purchase orders for a minimum of $25,000.00 for initial investments and $10,000.00 for subsequent investments.

The Units represent common units of fractional undivided beneficial interest in and ownership of the Trust and have no par value.

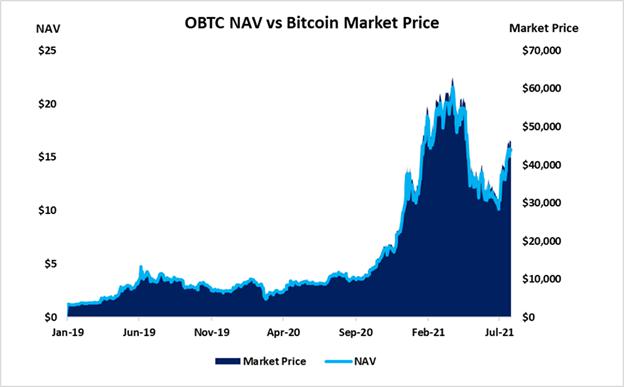

See “Description of Issuance of Units.” The Trust measure the NAV by reference to its principal market,

Coinbase Pro. An internal review during the period from May 18, 2021 through August 16, 2021 showed that the

difference between the Index values and the Trust’s NAV was immaterial. The Sponsor periodically compares the

Trust’s daily NAV over time to the performance of the Index. Although the Trust does not currently offer redemptions

of Units, the Units are quoted on the OTCQX market under the symbol “OBTC.” The market price of the Units on the

OTCQX has experienced significant premiums and discounts to NAV. Each business day, the Sponsor compares the

4:00 p.m., New York time closing price of the Units to the NAV and publishes the discount or premium on the Trust’s

website.

Most Units purchased directly

from the Trust are restricted securities that may not be resold except in transactions exempt from registration under the Securities

Act and state securities laws and any such transaction must be approved in advance by the Sponsor. In determining whether to grant

approval, the Sponsor will specifically look at whether the conditions of Rule 144 under the Securities Act and any other applicable

laws have been met. Any attempt to sell Units without the approval of the Sponsor in its sole discretion will be void ab initio.

See “Description of the Units—Transfer Restrictions” for more information. The Units are quoted on OTCQX under

the ticker symbol “OBTC.” Units quoted on the OTCQX either were sold originally to investors “unrestricted”

in a limited offering pursuant to Rule 504 under the Securities Act, or have become unrestricted in accordance with Rule 144 under

the Securities Act. See “Description of Units—Transfer Restrictions” for more detail. We intend to seek to list

the Units on a national securities exchange (the “Listing Exchange”) under the ticker symbol “OBTC” sometime

in the future. Any such listing will require the Listing Exchange to first receive approval from the SEC. To date, no Listing Exchange

has received such approval for any Bitcoin trust. As a result, there can be no guarantee that we will be successful in listing

the Units on the Listing Exchange. See “Risk Factors—Risk Factors Related to the Bitcoin Markets—Failure of funds

that hold digital assets or that have exposure to digital assets through derivatives to receive SEC approval to list their shares

on exchanges could adversely affect the value of the Units.”

At this time, the Trust

is not operating a redemption program for the Units and therefore Units are not redeemable by the Trust. Because the Trust does

not currently operate a redemption program and because the Trust may from time to time halt creations, there can be no assurance

that the market price of the Units will reflect the value of the Trust’s NAV per Unit, and the Units may trade at a substantial

premium over, or a substantial discount to, the NAV per Unit. The Units may also trade at a substantial premium over, or a substantial

discount to, NAV per Unit as a result of the volatility of the market price of Bitcoin, trading volume and closings of Bitcoin

trading markets due to fraud, failure, security breaches or otherwise. As a result of the foregoing, in the past, the price of

the Units as quoted on OTCQX has varied significantly from the Trust’s NAV per Unit.

The Trust is a passive investment vehicle and

its assets are not actively managed. As a result, the Trust will not engage in any management activities designed to obtain a profit

from, or to ameliorate losses caused by, changes in the market prices of Bitcoin.

Valuation of Bitcoin and Bitcoin Holdings

The Trust’s Bitcoin

Holdings is the aggregate U.S. dollar value of the Trust’s assets (other than U.S. dollars, other fiat currency, and Additional

Currency (as that term is defined herein)), less the U.S. dollar value of its expenses and other liabilities. The Trust’s

primary assets are Bitcoins and the Trust values its Bitcoins by reference to the Bitcoin Market Price, which is the market price

of Bitcoin traded on Coinbase Pro, the principal trading market for the Bitcoin in which the Trust invests, as determined each

Business Day at 4:00 p.m., New York time. The daily Bitcoin Market Price is available at https://pro.coinbase.com/trade/BTC-USD.

See “Valuation of Bitcoin and Determination of Bitcoin Holdings.”

If the Bitcoin Market Price

becomes unavailable, or if the Sponsor determines in good faith that the Bitcoin Market Price does not reflect an accurate Bitcoin

price, the Sponsor will, on a best-efforts basis, contact Coinbase Global Inc., the parent company of Coinbase Pro, to obtain the price of Bitcoin at 4:00 p.m., New York time directly. If the closing price remains unavailable or the Sponsor continues to

believe in good faith that such price does not reflect an accurate Bitcoin price, the Sponsor will employ a cascading set of rules

to determine the Bitcoin Market Price, as described in “Valuation of Bitcoin and Determination of Bitcoin Holdings.”

As of June 30, 2021, the

Bitcoin Holdings per Unit, was 0.00034.

Additional Currency

From time to time, the Trust

may come into possession of rights incident to its ownership of Bitcoins, which permit the Trust to acquire, or otherwise establish

dominion and control over, other virtual currencies. These rights are generally expected to arise in connection with forks in the

Blockchain, airdrops offered to holders of Bitcoins and other similar events and arise without any action of the Trust or of the

Sponsor or Trustee on behalf of the Trust. We refer to these rights as “Incidental Rights” and any such virtual currency

acquired through Incidental Rights as “Additional Currency.” The Trust does not expect to take any Additional Currency

it may hold into account for purposes of determining the Trust’s Bitcoin Holdings or the Bitcoin Holdings per Unit. See “Activities

of the Trust—Additional Currency.”

With respect to any fork,

airdrop or similar event, the Sponsor will, in its discretion, decide to cause the Trust to distribute the Additional Currency

in kind to an agent of the Unitholders for resale by such agent, or to irrevocably abandon the Additional Currency. In the case

of an in-kind distribution, the Unitholders’ agent would attempt to sell the Additional Currency, and if the agent is able

to do so, remit the cash proceeds to Unitholders. There can be no assurance as to the price or prices for any Additional Currency

that the agent may realize, and the value of the Additional Currency may increase or decrease after any sale by the agent. In the

case of abandonment, the Trust would not receive any direct or indirect consideration for the Additional Currency and thus the

value of the Units will not reflect the value of the Additional Currency.

Trust Expenses

The Trust will pay as an

ordinary recurring charge the remuneration due to the Sponsor (the “Management Fee”). The Management Fee equals an

annualized 0.49% of the average daily NAV of the Trust for each year. The Management Fee will accrue daily in Bitcoin and will

be payable, at the Sponsor’s sole discretion, in Bitcoin or in U.S. dollars and valued at the Bitcoin Market Price in effect

at the time of such payment. The Sponsor expects that the Trust will pay the Management Fee in monthly installments in arrears.

As discussed in greater

detail below, if the Trust holds any Additional Currency, the Trust may pay the Management Fee, in whole or in part, with such

Additional Currency by entering into an agreement with the Sponsor and transferring such Additional Currency to the Sponsor at

a value to be determined in accordance with the terms of such agreement, but only if such agreement and transfer do not conflict

with the terms of the Trust Agreement.

The Sponsor will bear the

routine operational, administrative and other ordinary fees and expenses of the Trust (the “Assumed Expenses”) other

than audit fees, index license fees, aggregate legal fees in excess of $50,000 per annum, and the fees of the Custodian (the “Excluded

Expenses”), and certain extraordinary expenses of the Trust, including but not limited to taxes and governmental charges,

expenses and costs, expenses and indemnities related to any extraordinary services performed by the Sponsor (or any other Service

Provider, including the Trustee) on behalf of the Trust to protect the Trust or the interests of Unitholders, indemnification expenses,

fees and expenses related to public quotation on OTCQX (the “Extraordinary Expenses,” collectively with the Assumed

Expenses and Excluded Expenses, the “Aggregate Trust Expenses”).

The Trust has not incurred

or paid any Extraordinary Expenses to date. If the Trust incurs any Extraordinary Expenses, the Sponsor or its delegate (i) would

instruct the Custodian to withdraw from the Bitcoin Account, on a monthly basis as needed, Bitcoins, Additional Currency in such

quantity as necessary to permit payment of such Extraordinary Expenses, and (ii) may either (x) cause the Trust (or its delegate)

to convert such Bitcoins or Additional Currency into U.S. dollars or other fiat currencies at the exchange rate at the time of

conversion or (y) cause the Trust (or its delegate) to deliver such Bitcoins or Additional Currency in kind in satisfaction of

such Extraordinary Expenses.

The Trust may use Additional

Currency to pay the Management Fee or Extraordinary Expenses only if doing so does not conflict with the terms of the Trust Agreement.

The Trust currently expects that the value of any such Additional Currency would be determined by reference to the Trust’s

selected principal market. Pursuant to the Trust Agreement, the Trust, through the Sponsor, has general discretion to determine

the principal market for purposes of valuing any such Additional Currency. The Sponsor will identify the principal market in accordance

with GAAP. If the Trust pays the Management Fees or Extraordinary Expenses, in whole or in part, in Additional Currency, the amount

of Bitcoins that would otherwise have been used to satisfy such payment will be correspondingly reduced. The number of Bitcoins

represented by a Unit will decline each time the Trust pays the Management Fee or any Extraordinary Expenses by transferring or

selling Bitcoins. See “Expenses; Sales of Bitcoins.”

The quantity of Bitcoins

or Additional Currency to be delivered to the Sponsor or other relevant payee in payment of the Management Fee or any Extraordinary

Expenses, or sold to permit payment of the Management Fee or Extraordinary Expenses, will vary from time to time depending on the

level of the Trust’s expenses and the value of Bitcoins and Additional Currency held by the Trust. See “Activities

of the Trust—Trust Expenses.” Assuming that the Trust is a grantor trust for U.S. federal income tax purposes, each

delivery or sale of Bitcoins and Additional Currency by the Trust for the payment of expenses will be a taxable event to Unitholders.

See “Certain U.S. Federal Income Tax Consequences—Tax Consequences to U.S. Holders.”

Emerging Growth Company Status

The Trust is an “emerging

growth company” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). For as long as

the Trust is an emerging growth company, unlike other public companies, it will not be required to, among other things:

| ● | provide an auditor’s attestation report on management’s assessment of the effectiveness of our system of internal

control over financial reporting pursuant to Section 404(b) of the Sarbanes-Oxley Act of 2002; or |

| ● | comply with any new audit rules adopted by the PCAOB after April 5, 2012, unless the SEC determines otherwise. |

The Trust will cease to

be an “emerging growth company” upon the earliest of (i) it having $1.07 billion or more in annual revenues, (ii) it

becoming a “large accelerated filer,” as defined in Rule 12b-2 of the Exchange Act, (iii) it issuing more than $1.0

billion of non-convertible debt over a three-year period or (iv) the last day of the fiscal year following the fifth anniversary

of its initial public offering.

In addition, Section 107

of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period provided in

Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an emerging growth

company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies;

however, the Trust is choosing

to “opt out”

of such extended transition period, and as a result, the Trust will comply with new or revised accounting standards on the relevant

dates on which adoption of such standards is required for non-emerging growth companies.

Section 107 of the JOBS

Act provides that the Trust’s decision to opt out of the extended transition period for complying with new or revised accounting

standards is irrevocable.

Principal Offices

The Sponsor’s principal

office is located at 520 White Plains Road, Suite 500, Tarrytown, New York, New York 10591 and its telephone number is (914) 214-4174.

The Trustee’s principal office is located at 251 Little Falls Drive, Wilmington, Delaware 19808. The Custodian’s principal

office is located at 28 Liberty Street, New York, New York 10005.

RISK FACTORS

An investment in the Units

involves certain risks as described below. These risks should also be read in conjunction with the other information included in

this Information Statement, including the Trust’s financial statements and related notes thereto. See “Glossary of

Defined Terms” for the definition of certain capitalized terms used in this Information Statement.

Summary Risk Factors

The following is a summary

of some of the risks and uncertainties that could materially adversely affect our business, financial condition and results of

operations. You should read this summary together with the more detailed description of each risk factor contained below.

Risk Factors Related to Digital Assets

| ● | Digital assets such as Bitcoin were only introduced within the past decade, and the medium-to-long

term value of the Units is subject to a number of factors relating to the capabilities and development of blockchain technologies

and to the fundamental investment characteristics of digital assets. |

| ● | The Bitcoin Network is part of a new and rapidly evolving industry, and the value of the Units

depends on the development and acceptance of the Bitcoin Network. |

| ● | A determination that Bitcoin or any other digital asset is a “security” may adversely

affect the value of Bitcoin and the value of the Units, and result in potentially extraordinary, nonrecurring expenses to, or termination

of the Trust. |

| ● | Changes in the governance of a digital asset network may not receive sufficient support from users

and miners, which may negatively affect that digital asset network’s ability to grow and respond to challenges. |

| ● | Digital asset networks face significant scaling challenges and efforts to increase the volume of

transactions may not be successful. |

| ● | A temporary or permanent “fork” could adversely affect the value of the Units. |

| ● | Unitholders may not receive the benefits of any forks or “airdrops.” |

| ● | In the event of a hard fork of the Bitcoin Network, the Sponsor will, if permitted by the terms

of the Trust Agreement, use its discretion to determine which network should be considered the appropriate network for the Trust’s

purposes, and in doing so may adversely affect the value of the Units. |

| ● | If the digital asset award for solving blocks and transaction fees for recording transactions on

the Bitcoin Network are not sufficiently high to incentivize miners, miners may cease expanding processing power or demand high

transaction fees, which could negatively impact the value of Bitcoin and the value of the Units. |

Risk Factors Related to the Bitcoin Markets

| ● | The value of the Units relates directly to the value of Bitcoins, the value of which may be highly

volatile and subject to fluctuations due to a number of factors. |

| ● | Due to the unregulated nature and lack of transparency surrounding the operations of Bitcoin exchanges,

they may experience fraud, security failures or operational problems, which may adversely affect the value of Bitcoin and, consequently,

the value of the Units. |

| ● | Competition from the emergence or growth of other digital assets or methods of investing in Bitcoin

could have a negative impact on the price of Bitcoin and adversely affect the value of the Units. |

| ● | Failure of funds that hold digital assets or that have exposure to digital assets through derivatives

to receive SEC approval to list their shares on exchanges could adversely affect the value of the Units. ● NAV may not always

correspond to the weighted-average market price of Bitcoin and, as a result, Units may be purchased (or redeemed, if ever permitted)

at a value that differs from the secondary market price of the Units. ● Suspension or disruptions of market trading may adversely

affect the value of units. |

| ● | The lack of active trading markets for the Units may result in losses on an investment in the Trust

at the time of disposition of Units. |

| ● | A possible “short squeeze” due to a sudden increase in demand for the Units that largely

exceeds supply may lead to price volatility in the Units. |

| ● | Difficulties or limitations in the processes of issuance and redemption (if any) of Units may interfere

with opportunities for arbitrage transactions intended to keep the price of the Units closely linked to the price of Bitcoin, which

may adversely affect an investment in the Units. |

| ● | Disruptions at OTC trading desks and potential consequences of an OTC trading desk’s failure

could adversely affect an investment in the Units. |

| ● | Disruptions at Bitcoin exchanges and potential consequences of a Bitcoin exchange’s failure

could adversely affect an investment in the Units. |

| ● | Momentum pricing of Bitcoin may subject the Bitcoin price to greater volatility and adversely affect

an investment in the Units. |

Risk Factors Related to the Trust and the

Units

| ● | The Trust has only a limited performance history. |

| ● | The Units are new securities and their value could decrease if unanticipated operational or trading

problems arise. |

| ● | Fees and expenses are charged regardless of profitability and may result in depletion of assets. |

| ● | The security of our Bitcoin Holdings cannot be assured, by the Trust, the Custodian or any other

person. |

| ● | Possibility of termination of the Trust may adversely affect a Unitholder’s portfolio. |

| ● | Any errors, discontinuance or changes in determining the value of the Bitcoin held by the Trust

may have an adverse effect on the value of the Units. |

| ● | The value of the Units will be adversely affected if the Trust is required to indemnify the Sponsor

or the Custodian as contemplated in the Trust Agreement or the Custodial Services Agreement. |

| ● | The Trust’s Bitcoin trading may subject the Trust to the risk of counterparty non-performance,

potentially negatively affecting the market price of the Units. |

| ● | The Trust’s Bitcoin Holdings could become illiquid, which could cause large losses to Unitholders

at any time or from time to time. |

| ● | Transactions in Bitcoin are irreversible, and the Trust may be unable to recover improperly transferred

Bitcoin. |

| ● | The Trust’s Bitcoin may be lost, stolen, or subject to other inaccessibility. |

| ● | Any disruptions to the computer technology used by the Trust or its service providers could adversely

affect the Trust’s ability to function and an investment in the Units. |

| ● | The Sponsor’s computer infrastructure may be vulnerable to security breaches. Any such problems

could cause interruptions in the Trust’s operations and adversely affect an investment in the Units. |

| ● | Technology system failures could cause interruptions in the Trust’s ability to operate. |

| ● | The lack of full insurance and Unitholders’ limited rights of legal recourse against the

Trust, Trustee, Sponsor, Transfer Agent and Custodian expose the Trust and its Unitholders to the risk of loss of the Trust’s

Bitcoins for which no person or entity is liable. |

| ● | Because the Units reflect the estimated accrued but unpaid expenses of the Trust, the number of

Bitcoins represented by a Unit will gradually decrease over time as the Trust’s Bitcoins are used to pay the Trust’s

expenses. |

Risk Factors Related to the Regulation of

the Trust and the Units

| ● | Regulation of the Bitcoin industry continues to evolve and is subject to change; future regulatory

developments are impossible to predict but may significantly and adversely affect the Trust. |

| ● | The sale of the Units could be subject to SEC or state securities registration. |

| ● | The Trust is not a registered investment company. |

| ● | The Trust could be, or could become, subject to the Commodity Exchange Act. |

| ● | Future U.S. and foreign regulation of the Bitcoin market may impose other regulatory burdens, which

could harm the Trust or even cause the Trust to liquidate. |

| ● | Banks may not provide banking services, or may cut off banking services, to businesses that provide

Bitcoin-related services or that accept Bitcoin as payment, which could directly impact the Trust’s operations, damage the

public perception of Bitcoin and the utility of Bitcoin as a payment system and could decrease the price of Bitcoin and adversely

affect an investment in the Units. |

| ● | It may be illegal now, or in the future, to acquire, own, hold, sell or use Bitcoin in one or more

countries, and ownership of, holding or trading in Units may also be considered illegal and subject to sanctions. |

| ● | If regulatory changes or interpretations of the Trust’s or Sponsor’s activities require

registration as money service businesses under the regulations promulgated by FinCEN under the authority of the U.S. Bank Secrecy

Act or as money transmitters or digital currency businesses under state regimes for the licensing of such businesses, the Trust

and/or Sponsor could suffer reputational harm and also extraordinary, recurring and/or nonrecurring expenses, which would adversely

impact an investment in the Units. |

| ● | The treatment of the Trust for U.S. federal income tax purposes is uncertain. |

| ● | Unitholders could incur a tax liability without an associated distribution. |

| ● | The treatment of Bitcoin for U.S. federal income tax purposes is uncertain. |

| ● | Future developments regarding the treatment of digital currency for U.S. federal income tax purposes

could adversely affect the value of the Units. |

| ● | Future developments in the treatment of digital currency for tax purposes other than U.S. federal income tax purposes could

adversely affect the value of the Units. |

| ● | A U.S. tax-exempt Unitholder may recognize “unrelated business taxable income” a consequence of an investment in

Units. |

| ● | Non-U.S. Holders may be subject to U.S. federal withholding tax on income derived from forks, airdrops and similar occurrences. |

Risk Factors Related to Potential Conflicts of Interest

| ● | Potential conflicts of interest may arise among the Sponsor or its affiliates and the Trust. The

Sponsor and its affiliates have no fiduciary duties to the Trust and its Unitholders other than as provided in the Trust Agreement,

which may permit them to favor their own interests to the detriment of the Trust and its Unitholders. |

| ● | Unitholders cannot be assured of the Sponsor’s continued services, the discontinuance of

which may be detrimental to the Trust. |

| ● | The Custodian could resign or be removed by the Sponsor, which would trigger early termination

of the Trust. |

| ● | Unitholders may be adversely affected by the lack of independent advisers representing investors

in the Trust. |

Risk Factors Related to Digital Assets

Digital assets such as Bitcoin were only

introduced within the past decade, and the medium-to-long term value of the Units is subject to a number of factors relating to

the capabilities and development of blockchain technologies and to the fundamental investment characteristics of digital assets.

Digital assets such as Bitcoin

were only introduced within the past decade, and the medium-to-long term value of the Units is subject to a number of factors relating

to the capabilities and development of blockchain technologies, such as the infancy of their development, their dependence on the

internet and other technologies, their dependence on the role played by miners and developers and the potential for malicious activity.

For example, the realization of one or more of the following risks could materially adversely affect the value of the Units:

| ● | The trading prices of many digital assets, including Bitcoin, have experienced extreme volatility

in recent periods and may continue to do so. For instance, there were steep increases in the value of certain digital assets, including

Bitcoin, over the course of 2017, and multiple market observers asserted that digital assets were experiencing a “bubble.”

These increases were followed by steep drawdowns throughout 2018 in digital asset trading prices, including for Bitcoin. These

drawdowns notwithstanding, Bitcoin prices have increased significantly again during 2019 and the Bitcoin markets may still be experiencing

a bubble or may experience a bubble again in the future. Extreme volatility in the future, including further declines in the trading

prices of Bitcoin, could have a material adverse effect on the value of the Units and the Units could lose all or substantially

all of their value. |

| ● | Digital asset networks and the software used to operate them are in the early stages of development.

Digital assets have experienced, and we expect will experience in the future, sharp fluctuations in value. Given the infancy of

the development of digital asset networks, parties may be unwilling to transact in digital assets, which would dampen the growth,

if any, of digital asset networks. |

| ● | Digital asset networks are dependent upon the internet. A disruption of the internet or a digital

asset network, such as the Bitcoin Network, would affect the ability to transfer digital assets, including Bitcoin, and, consequently,

their value. |

| ● | The acceptance of software patches or upgrades by a significant, but not overwhelming, percentage

of the users and miners in a digital asset network, such as the Bitcoin Network, could result in a “fork” in such network’s

blockchain, resulting in the operation of multiple separate networks. |

| ● | Governance of the Bitcoin Network is by voluntary consensus and open competition. As a result,

there may be a lack of consensus or clarity on the governance of the Bitcoin Network, which may stymie the |

| |

|

Bitcoin Network’s utility and ability to grow and face challenges. In particular, it may be difficult to find solutions or martial sufficient effort to overcome any future problems on the Bitcoin Network, especially long-term problems. |

| ● | The foregoing notwithstanding, the Bitcoin Network’s protocol is informally managed by a

group of core developers that propose amendments to the Bitcoin Network’s source code. The core developers evolve over time,

largely based on self-determined participation. To the extent that a significant majority of users and miners adopt amendments

to the Bitcoin Network, the Bitcoin Network will be subject to new protocols that may adversely affect the value of Bitcoin. |

| ● | The loss or destruction of a private key required to access a digital asset such as Bitcoin may

be irreversible. If a private key is lost, destroyed or otherwise compromised and no backup of the private key is accessible, the

Trust will be unable to access the Bitcoin held in the Bitcoin Account corresponding to that private key and the private key will

not be capable of being restored by the Bitcoin Network. |

| ● | Bitcoins have only recently become selectively accepted as a means of payment by retail and commercial

outlets, and use of Bitcoins by consumers to pay such retail and commercial outlets remains limited. Banks and other established

financial institutions may refuse to process funds for Bitcoin transactions; process wire transfers to or from Bitcoin exchanges,

Bitcoin-related companies or service providers; or maintain accounts for persons or entities transacting in Bitcoin. As a result,

the prices of Bitcoins are largely determined by speculators and miners, thus contributing to price volatility that makes retailers

less likely to accept it as a form of payment in the future. |

| ● | Miners, developers and users may switch to or adopt certain digital assets at the expense of their

engagement with other digital asset networks, which may negatively impact those networks, including the Bitcoin Network. |

| ● | Over the past several years, digital asset mining operations have evolved from individual users

mining with computer processors, graphics processing units and first generation application specific integrated circuit machines

to “professionalized” mining operations using proprietary hardware or sophisticated machines. If the profit margins

of digital asset mining operations are not sufficiently high, digital asset miners are more likely to immediately sell tokens earned

by mining, resulting in an increase in liquid supply of that digital asset, which would generally tend to reduce that digital asset’s

market price. |

| ● | To the extent that any miners cease to record transactions that do not include the payment of a

transaction fee in solved blocks or do not record a transaction because the transaction fee is too low, such transactions will

not be recorded on the Blockchain until a block is solved by a miner who does not require the payment of transaction fees or is

willing to accept a lower fee. Any widespread delays in the recording of transactions could result in a loss of confidence in the

digital asset network. |

| ● | Many digital asset networks face significant scaling challenges and are being upgraded with various

features to increase the speed and throughput of digital asset transactions. These attempts to increase the volume of transactions

may not be effective. |

| ● | The open-source structure of many digital asset network protocols, such as the protocol for the

Bitcoin Network, means that developers and other contributors are generally not directly compensated for their contributions in

maintaining and developing such protocols. As a result, the developers and other contributors of a particular digital asset may

lack a financial incentive to maintain or develop the network, or may lack the resources to adequately address emerging issues.

Alternatively, some developers may be funded by companies whose interests are at odds with other participants in a particular digital

asset network. A failure to properly monitor and upgrade the protocol of the Bitcoin Network could damage that network. |

| ● | Banks may not provide banking services, or may cut off banking services, to businesses that provide

digital asset-related services or that accept digital assets as payment, which could dampen liquidity in the market and damage

the public perception of digital assets generally or any one digital asset in |

| |

|

particular, such as Bitcoin, and their or its utility as a payment system, which could decrease the price of digital assets generally or individually. |

Moreover, because digital

assets, including Bitcoin, have been in existence for a short period of time and are continuing to develop, there may be additional

risks in the future that are impossible to predict as of the date of this Information Statement.

The Bitcoin Network is part of a new

and rapidly evolving industry, and the value of the Units depends on the development and acceptance of the Bitcoin Network.

The Bitcoin Network was

first launched in 2009 and Bitcoins were the first cryptographic digital assets created to gain global adoption and critical mass.

Although the Bitcoin Network is the most established digital asset network, the Bitcoin Network and other cryptographic and algorithmic

protocols governing the issuance of digital assets represent a new and rapidly evolving industry that is subject to a variety of

factors that are difficult to evaluate. For example, the realization of one or more of the following risks could materially adversely

affect the value of the Units:

| ● | As the Bitcoin Network continues to develop and grow, certain technical issues might be uncovered,

and the troubleshooting and resolution of such issues requires the attention and efforts of Bitcoin’s global development

community. |

| ● | In August 2017, the Bitcoin Network underwent a hard fork that resulted in the creation of a new

digital asset network called Bitcoin Cash. This hard fork was contentious, and as a result some users of the Bitcoin Cash network

may harbor ill will toward the Bitcoin Network. These users may attempt to negatively impact the use or adoption of the Bitcoin

Network. |

| ● | Also in August 2017, the Bitcoin Network was upgraded with a technical feature known as “Segregated

Witness” that, among other things, potentially doubles the transactions per second that can be handled on-chain and enables

so-called second layer solutions, such as the Lightning Network or payment channels, that have the potential to substantially increase

transaction throughput (i.e., millions of transactions per second). As of the date of this Information Statement, wallets and intermediaries

that support Segregated Witness or Lightning Network-like technologies do not yet have material adoption. This upgrade may fail

to work as expected leading to a decline in support and price of Bitcoin. |

| ● | As of June 27, 2021, the largest 100 Bitcoin wallets held approximately 15.59% of the Bitcoins

in circulation and it is possible that some of these wallets are controlled by the same person or entity. Moreover, it is possible

that other persons or entities control multiple wallets that collectively hold a significant number of Bitcoin, even if they individually

only hold a small amount. As a result of this concentration of ownership, large sales by such holders could have an adverse effect

on the market price of Bitcoin. |

Moreover, in the past, flaws

in the source code for digital assets have been exposed and exploited, including flaws that disabled some functionality for users,

exposed users’ personal information and/or resulted in the theft of users’ digital assets. The cryptography underlying

Bitcoin could prove to be flawed or ineffective, or developments in mathematics and/or technology, including advances in digital

computing, algebraic geometry and quantum computing, could result in such cryptography becoming ineffective. In any of these circumstances,

a malicious actor may be able to take the Trust’s Bitcoin, which would adversely affect the value of the Units. Moreover,

functionality of the Bitcoin Network may be negatively affected such that it is no longer attractive to users, thereby dampening

demand for Bitcoin. Even if another digital asset other than Bitcoin were affected by similar circumstances, any reduction in confidence

in the source code or cryptography underlying digital assets generally could negatively affect the demand for digital assets and

therefore adversely affect the value of the Units.

The Trust is not actively

managed and will not have any formal strategy relating to the development of the Bitcoin Network.

A determination that Bitcoin or any other

digital asset is a “security” may adversely affect the value of Bitcoin and the value of the Units, and result in potentially

extraordinary, nonrecurring expenses to, or termination of the Trust

The SEC has stated that

certain digital assets may be considered “securities” under the federal securities laws. The test for determining whether

a particular digital asset is a “security” is complex and the outcome is difficult to predict. Further, if any other

digital asset is determined to be a “security” under federal or state securities laws by the SEC or any other agency,

or in a proceeding in a court of law or otherwise, it may have material adverse consequences for Bitcoin as a digital asset due

to negative publicity or a decline in the general acceptance of digital assets. As such, any determination that Bitcoin or any

other digital asset is a security under federal or state securities laws may adversely affect the value of Bitcoin and, as a result,

the value of the Units.

To the extent that Bitcoin

is determined to be a security, the Trust and the Sponsor may also be subject to additional regulatory requirements, including

under the Investment Company Act, and the Sponsor may be required to register as an investment adviser under the Investment Advisers

Act of 1940, as amended (the “Advisers Act”).. See “—Risks Relating to the Regulation of the Trust and the Units—Regulatory changes or interpretations

could cause the Trust and the Sponsor to register and comply with new regulations, resulting in potentially extraordinary, nonrecurring

expenses to the Trust.” If the Sponsor determines not to comply with such additional regulatory and registration requirements,

the Sponsor will terminate the Trust. Any such termination could result in the liquidation of the Trust’s Bitcoin at a time

that is disadvantageous to Unitholders.

Changes in the governance of a digital

asset network may not receive sufficient support from users and miners, which may negatively affect that digital asset network’s

ability to grow and respond to challenges.

The governance of decentralized

networks, such as the Bitcoin and Ethereum networks, is by voluntary consensus and open competition. As a result, there may be

a lack of consensus or clarity on the governance of any particular decentralized digital asset network, which may stymie such network’s

utility and ability to grow and face challenges. The foregoing notwithstanding, the protocols for some decentralized networks,

such as the Bitcoin network, are informally managed by a group of core developers that propose amendments to the relevant network’s

source code. Core developers’ roles evolve over time, largely based on self-determined participation. If a significant majority

of users and miners adopt amendments to a decentralized network based on the proposals of such core developers, such network will

be subject to new protocols that may adversely affect the value of the relevant digital asset.

As a result of the foregoing,

it may be difficult to find solutions or marshal sufficient effort to overcome any future problems, especially long-term problems,

on digital asset networks.

Digital asset networks face significant

scaling challenges and efforts to increase the volume of transactions may not be successful.

Many digital asset networks

face significant scaling challenges due to the fact that public blockchains generally face a trade-off regarding security and scalability.

One means through which public blockchains achieve security is decentralization, meaning that no intermediary is responsible for

securing and maintaining these systems. For example, a greater degree of decentralization generally means a given digital asset

network is less susceptible to manipulation or capture. In practice, this typically means that every single node on a given digital

asset network is responsible for securing the system by processing every transaction and maintaining a copy of the entire state

of the network. As a result, a digital asset network may be limited in the number of transactions it can process by the capabilities

of each single fully participating node.

As corresponding increases

in throughput lag behind growth in the use of digital asset networks, average fees and settlement times may increase considerably.

For example, the Bitcoin Network has been, at times, at capacity, which has led to increased transaction fees. Since January 1,

2017, Bitcoin transaction fees have increased from $0.35 per Bitcoin transaction, on average, to a high of $55.16 per transaction,

on average, on December 22, 2017. As of June 2021, Bitcoin transaction fees stood around $6 per transaction, on average. Increased

fees and decreased settlement speeds could preclude certain uses for Bitcoin (e.g., micropayments), and could reduce demand for,

and the price of, Bitcoin, which could adversely impact the value of the Units.

Many developers are actively

researching and testing scalability solutions for public blockchains that do not necessarily result in lower levels of security

or decentralization (e.g., off-chain payment channels like the Lightning Network, sharding, or off-chain computations). However,

there is no guarantee that any of the mechanisms in place or being explored for increasing the scale of settlement of the Bitcoin

Network transactions will be effective, or how long these mechanisms will take to become effective, which could adversely impact

the value of the Units.

If a malicious actor or botnet obtains

control of more than 50% of the processing power on the Bitcoin Network, or otherwise obtains control over the Bitcoin Network

through its influence over core developers or otherwise, such actor or botnet could manipulate the Blockchain to adversely affect

the value of the Units or the ability of the Trust to operate.

If a malicious actor or

botnet (a volunteer or hacked collection of computers controlled by networked software coordinating the actions of the computers)

obtains a majority of the processing power dedicated to mining on the Bitcoin Network, it may be able to alter the Blockchain on

which transactions in Bitcoin rely by constructing fraudulent blocks or preventing certain transactions from completing in a timely

manner, or at all. The malicious actor or botnet could also control, exclude or modify the ordering of transactions. Although the

malicious actor or botnet would not be able to generate new tokens or transactions using such control, it could “double-spend”

its own tokens (i.e., spend the same tokens in more than one transaction) and prevent the confirmation of other users’ transactions

for so long as it maintained control. To the extent that such malicious actor or botnet did not yield its control of the processing

power on the Bitcoin Network or the Bitcoin community did not reject the fraudulent blocks as malicious, reversing any changes

made to the Blockchain may not be possible. Further, a malicious actor or botnet could create a flood of transactions in order

to slow down the Bitcoin Network.

Although there are no known

reports of malicious activity on, or control of, the Bitcoin Network, it is believed that certain mining pools may have exceeded

the 50% threshold on the Bitcoin Network. The possible crossing of the 50% threshold indicates a greater risk that a single mining

pool could exert authority over the validation of Bitcoin transactions, and this risk is heightened if over 50% of the processing

power on the network falls within the jurisdiction of a single governmental authority. For example, it is believed that more than

50% of the processing power on the Bitcoin Network is located in China. Because the Chinese government has subjected digital assets

to heightened levels of scrutiny recently, reportedly forcing several digital asset exchanges to shut down, there is a risk that

the Chinese government could also achieve control over more than 50% of the processing power on the Bitcoin Network. If network

participants, including the core developers and the administrators of mining pools, do not act to ensure greater decentralization

of Bitcoin mining processing power, the feasibility of a malicious actor obtaining control of the processing power on the Bitcoin

Network will increase, which may adversely affect the value of the Units.

A malicious actor may also

obtain control over the Bitcoin Network through its influence over core developers by gaining direct control over a core developer

or an otherwise influential programmer. To the extent that the Bitcoin ecosystem does not grow, the possibility that a malicious

actor may be able obtain control of the processing power on the Bitcoin Network in this manner will remain heightened.

A temporary or permanent “fork”

could adversely affect the value of the Units.

The Bitcoin Network operates

using open-source protocols, meaning that any user can download the software, modify it and then propose that the users and miners

of Bitcoin adopt the modification. When a modification is introduced and a substantial majority of users and miners consent to

the modification, the change is implemented and the network remains uninterrupted. However, if less than a substantial majority

of users and miners consent to the proposed modification, and the modification is not compatible with the software prior to its

modification, the consequence would be what is known as a “hard fork” of the Bitcoin Network, with one group running

the pre-modified software and the other running the modified software. The effect of such a fork would be the existence of two

versions of Bitcoin running in parallel, yet lacking interchangeability. For example, in August 2017, Bitcoin “forked”

into Bitcoin and a new digital asset, Bitcoin Cash, as a result of a several-year dispute over how to increase the rate of transactions

that the Bitcoin Network can process.

Forks may also occur as

a network community’s response to a significant security breach. For example, in June 2016, an anonymous hacker exploited

a smart contract running on the Ethereum network to syphon approximately $60 million of ETH held by The DAO, a distributed autonomous

organization, into a segregated

account. In response to the hack, most participants

in the Ethereum community elected to adopt a “fork” that effectively reversed the hack. However, a minority of users

continued to develop the original blockchain, now referred to as “Ethereum Classic” with the digital asset on that

blockchain now referred to as Ether Classic, or ETC. ETC now trades on several digital asset exchanges. A fork may also occur as

a result of an unintentional or unanticipated software flaw in the various versions of otherwise compatible software that users

run. Such a fork could lead to users and miners abandoning the digital asset with the flawed software. It is possible, however,

that a substantial number of users and miners could adopt an incompatible version of the digital asset while resisting community-led

efforts to merge the two chains. This could result in a permanent fork, as in the case of Ether and Ether Classic.

In addition, many developers

have previously initiated hard forks in the Blockchain to launch new digital assets, such as Bitcoin Gold and Bitcoin Diamond.

To the extent such digital assets compete with Bitcoin, such competition could impact demand for Bitcoin and could adversely impact

the value of the Units.

Furthermore, a hard fork

can lead to new security concerns. For example, when the Ethereum and Ethereum Classic networks split in July 2016, replay attacks,

in which transactions from one network were rebroadcast to nefarious effect on the other network, plagued Ethereum exchanges through

at least October 2016. An Ethereum exchange announced in July 2016 that it had lost 40,000 Ether Classic, worth about $100,000

at that time, as a result of replay attacks. Another possible result of a hard fork is an inherent decrease in the level of security

due to significant amounts of mining power remaining on one network or migrating instead to the new forked network. After a hard

fork, it may become easier for an individual miner or mining pool’s hashing power to exceed 50% of the processing power of

the digital asset network that retained or attracted less mining power, thereby making digital assets that rely on proof-of-work

more susceptible to attack.

A future fork in the Bitcoin

Network could adversely affect the value of the Units or the ability of the Trust to operate.

Unitholders may not receive the benefits

of any forks or “airdrops.”

In addition to forks, a

digital asset may become subject to a similar occurrence known as an “airdrop.” In an airdrop, the promotors of a new

digital asset announce to holders of another digital asset that such holders will be entitled to claim a certain amount of the

new digital asset for free, based on the fact that they hold such other digital asset.

Unitholders may not receive

the benefits of any forks, the Trust may not choose, or be able, to participate in an airdrop, and the timing of receiving any

benefits from a fork, airdrop or similar event is uncertain. We refer to the right to receive any such benefit as an “Incidental

Right” and any such virtual currency acquired through an Incidental Right as “Additional Currency.” There are

likely to be operational, tax, securities law, regulatory, legal and practical issues that significantly limit, or prevent entirely,

Unitholders’ ability to realize a benefit, through their interests in the Trust, from any such Additional Currency. For instance,

the Custodian may not agree to provide access to the Additional Currency. In addition, the Sponsor may determine that there is

no safe or practical way to custody the Additional Currency, or that trying to do so may pose an unacceptable risk to the Trust’s

holdings in Bitcoin, or that the costs of taking possession and/or maintaining ownership of the Additional Currency exceed the

benefits of owning the Additional Currency. Additionally, laws, regulation or other factors may prevent Unitholders from benefiting

from the Additional Currency even if there is a safe and practical way to custody and secure the Additional Currency. For example,

it may be illegal to sell or otherwise dispose of the Additional Currency, or there may not be a suitable market into which the

Additional Currency can be sold (immediately after the fork or airdrop, or ever). The Sponsor may also determine, in consultation

with its legal advisors and tax consultants, that the Additional Currency is, or is likely to be deemed, a security under federal

or state securities laws. In such a case, the Sponsor would irrevocably abandon, as of any date on which the Trust creates Units,

such Additional Currency if holding it would have an adverse effect on the Trust and it would not be practicable to avoid such

effect by disposing of the Additional Currency in a manner that would result in Unitholders receiving more than insignificant value

thereof. In making such a determination, the Sponsor expects to take into account a number of factors, including the definition

of a “security” under Section 2(a)(1) of the Securities Act and Section 3(a)(10) of the Exchange Act, SEC v. W.J. Howey

Co., 328 U.S. 293 (1946) and the case law interpreting it, as well as reports, orders, press releases, public statements and speeches

by the SEC providing guidance on when a digital asset is a “security” for purposes of the federal securities laws.

In the event of a hard fork of the Bitcoin

Network, the Sponsor will, if permitted by the terms of the Trust Agreement, use its discretion to determine which network should

be considered the appropriate network for the Trust’s purposes, and in doing so may adversely affect the value of the Units.

In the event of a hard fork

of the Bitcoin Network, the Sponsor will, if permitted by the terms of the Trust Agreement, use its discretion to determine, in

good faith, which peer-to-peer network, among a group of incompatible forks of the Bitcoin Network, is generally accepted as the

Bitcoin Network and should therefore be considered the appropriate network for the Trust’s purposes. The Sponsor will base

its determination on a variety of then relevant factors, including, but not limited to, the Sponsor’s beliefs regarding expectations

of the core developers of Bitcoin, users, services, businesses, miners and other constituencies, as well as the actual continued

acceptance of, mining power on, and community engagement with, the Bitcoin Network. There is no guarantee that the Sponsor will

choose the digital asset that is ultimately the most valuable fork, and the Sponsor’s decision may adversely affect the value

of the Units as a result. The Sponsor may also disagree with Unitholders, security vendors and the Index Provider on what is generally

accepted as Bitcoin and should therefore be considered “Bitcoin” for the Trust’s purposes, which may also adversely

affect the value of the Units as a result.

If the digital asset award for solving

blocks and transaction fees for recording transactions on the Bitcoin Network are not sufficiently high to incentivize miners,

miners may cease expanding processing power or demand high transaction fees, which could negatively impact the value of Bitcoin

and the value of the Units.

If the digital asset awards

for solving blocks and the transaction fees for recording transactions on the Bitcoin Network are not sufficiently high to incentivize

miners, miners may cease expending processing power to solve blocks and confirmations of transactions on the Blockchain could be

slowed. A reduction in the processing power expended by miners on the Bitcoin Network could increase the likelihood of a malicious

actor or botnet obtaining control.

Miners have historically

accepted relatively low transaction confirmation fees on most digital asset networks. If miners demand higher transaction fees

for recording transactions in the Blockchain or a software upgrade automatically charges fees for all transactions on the Bitcoin

Network, the cost of using Bitcoin may increase and the marketplace may be reluctant to accept Bitcoin as a means of payment. Alternatively,

miners could collude in an anti-competitive manner to reject low transaction fees on the Bitcoin Network and force users to pay

higher fees, thus reducing the attractiveness of the Bitcoin Network. Higher transaction confirmation fees resulting through collusion

or otherwise may adversely affect the attractiveness of the Bitcoin Network, the value of Bitcoin and the value of the Units.

Risk Factors Related to the Bitcoin Markets

The value of the Units relates directly

to the value of Bitcoins, the value of which may be highly volatile and subject to fluctuations due to a number of factors.

The value of the Units relates

directly to the value of the Bitcoins held by the Trust and fluctuations in the price of Bitcoin could adversely affect the value

of the Units. The market price of Bitcoin may be highly volatile, and subject to a number of factors, including:

| ● | An increase in the global Bitcoin supply; |

| ● | Manipulative trading activity on Bitcoin exchanges, which are largely unregulated; |

| ● | The adoption of Bitcoin as a medium of exchange, store-of-value or other consumptive asset and

the maintenance and development of the open-source software protocol of the Bitcoin Network; |

| ● | Forks in the Bitcoin Network; |

| ● | Investors’ expectations with respect to interest rates, the rates of inflation of fiat currencies

or Bitcoin, and digital asset exchange rates; |

| ● | Consumer preferences and perceptions of Bitcoin specifically and digital assets generally; |

| ● | Fiat currency withdrawal and deposit policies on Bitcoin exchanges; |

| ● | The liquidity of Bitcoin markets; |

| ● | Investment and trading activities of large investors that invest directly or indirectly in Bitcoin; |

| ● | A “short squeeze” resulting from speculation on the price of Bitcoin, if aggregate

short exposure exceeds the number of Units available for purchase; |

| ● | An active derivatives market for Bitcoin or for digital assets generally; |

| ● | Monetary policies of governments, trade restrictions, currency devaluations and revaluations and

regulatory measures or enforcement actions, if any, that restrict the use of Bitcoin as a form of payment or the purchase of Bitcoin

on the Bitcoin markets; |

| ● | Global or regional political, economic or financial conditions, events and situations; |

| ● | Fees associated with processing a Bitcoin transaction and the speed at which Bitcoin transactions

are settled; |

| ● | Interruptions in service from or failures of major Bitcoin exchanges; |

| ● | Decreased confidence in Bitcoin exchanges due to the unregulated nature and lack of transparency

surrounding the operations of Bitcoin exchanges; |

| ● | Increased competition from other forms of digital assets or payment services; and |

| ● | The Trust’s own acquisitions or dispositions of Bitcoin, since there is no limit on the number

of Bitcoin that the Trust may acquire. |

In addition, there is no