As filed with the Securities and Exchange Commission on July 28, 2022

Registration No. 333-258978

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

POST-EFFECTIVE

AMENDMENT No. 1

TO

FORM S-1 ON

FORM S-3

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

(Exact name of registrant as specified in its charter)

| 83-2530757 | ||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) |

12603 Southwest Freeway, Suite 210

Stafford, Texas 77477

(281) 491-9505

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Craig Webster

Chief Financial Officer

Microvast Holdings, Inc.

12603 Southwest Freeway, Suite 210

Stafford, Texas 77477

(281) 491-9505

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| With copies to: Alain Dermarkar, Esq. Shearman & Sterling LLP 2828 North Harwood Street, 18th Floor Dallas, Texas 75201 (214) 271-5777 |

With copies to: William B. Nelson, Esq. |

Approximate date of commencement of proposed sale to the public: From time to time on or after the effective date of this registration statement.

If the only securities being registered on this Form are being offered pursuant to dividend or interest reinvestment plans, please check the following box: ☐

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: ☒

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a registration statement pursuant to General Instruction I.D. or a post-effective amendment thereto that shall become effective upon filing with the Commission pursuant to Rule 462(e) under the Securities Act, check the following box. ☐

If this Form is a post-effective amendment to a registration statement filed pursuant to General Instruction I.D. filed to register additional securities or additional classes of securities pursuant to Rule 413(b) under the Securities Act, check the following. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Smaller reporting company | ||

| Emerging growth company |

If an emerging growth company, indicate by check

mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting

standards provided to Section 7(a)(2)(B) of the Securities Act.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Explanatory Note

The information in this prospectus is not complete and may be changed. Neither we nor the selling securityholders may sell or distribute the securities described herein until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell and is not soliciting an offer to buy the securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED July 28, 2022

PRELIMINARY PROSPECTUS

Microvast Holdings, Inc.

321,460,085 Shares of Common Stock

837,000 Warrants to Purchase Common Stock

This prospectus relates to: (1) the issuance by us of up to 27,600,000 shares of our common stock, par value $0.0001 per share (“common stock”) that may be issued upon exercise of public warrants (as defined below) to purchase common stock at an exercise price of $11.50 per share of common stock and (2) the offer and sale, from time to time, by the selling holders identified in this prospectus (the “Selling Holders”), or their permitted transferees, of (i) up to 293,860,085 shares of common stock and (ii) up to 837,000 private warrants (each as defined below).

Microvast Holdings, Inc. is a Delaware corporation that is a holding company. As a holding company with no material operations of our own, our operations are conducted through our subsidiaries, including subsidiaries based in China. References to “we,” “us,” “our” and the “Company” refer to Microvast Holdings, Inc. and our subsidiaries, taken as a whole. All securities being offered pursuant to this prospectus are securities of the Delaware holding company, and accordingly no investor will acquire a direct interest in any of the equity securities of our subsidiaries.

A substantial portion of our facilities are currently located in the People’s Republic of China, which we refer to as the “PRC” or “China”.

INVESTING IN OUR COMMON STOCK INVOLVES SUBSTANTIAL RISKS, INCLUDING RISKS RELATED TO THE FACT THAT WE ARE A HOLDING COMPANY WITH NO MATERIAL OPERATIONS OF OUR OWN AND THAT WE CONDUCT A SUBSTANTIAL MAJORITY OF OUR OPERATIONS THROUGH OUR OPERATING ENTITIES ESTABLISHED IN THE PRC. RECENT REGULATORY DEVELOPMENTS IN CHINA, IN PARTICULAR WITH RESPECT TO RESTRICTIONS ON CHINA-BASED COMPANIES RAISING CAPITAL OFFSHORE, AND THE GOVERNMENT-LED CYBER SECURITY REVIEWS OF CERTAIN COMPANIES WITH VIE STRUCTURES, MAY LEAD TO ADDITIONAL REGULATORY REVIEW IN CHINA OVER THE CONDUCT OF OUR BUSINESS AND OUR FINANCING AND CAPITAL RAISING ACTIVITIES IN THE UNITED STATES.

THE CENTRAL AND LOCAL PRC GOVERNMENTS CONTINUE TO EXERCISE A SUBSTANTIAL DEGREE OF CONTROL AND INFLUENCE OVER BUSINESSES OPERATING IN CHINA. SUCH INFLUENCE AND CONTROL CAN BE EXERTED IN NUMEROUS WAYS, INCLUDING BY MEANS OF POLICIES IN RESPECT OF THE APPROVALS AND PERMITS REQUIRED TO OPERATE IN CHINA OR OWN A SUBSIDIARY IN CHINA, CONTROL OVER OFFERINGS CONDUCTED OVERSEAS AND/OR FOREIGN INVESTMENT IN CHINA-BASED ISSUERS, CONTROL OVER DATA SECURITY, PREFERENTIAL TREATMENTS SUCH AS TAX INCENTIVES, ELECTRICITY PRICING, AND SAFETY, ENVIRONMENTAL AND QUALITY CONTROL. IF THE PRC GOVERNMENT CHANGES ITS CURRENT POLICIES, OR THE INTERPRETATION OF THOSE POLICIES THAT ARE CURRENTLY BENEFICIAL TO US, WE MAY FACE PRESSURE ON OUR OPERATIONS AND OUR ABILITY TO GENERATE REVENUE OR MAXIMIZE OUR PROFITABILITY, OR WE MAY EVEN BE UNABLE TO CONTINUE TO OPERATE IN CHINA OR OFFER OR CONTINUE TO OFFER SECURITIES, ALL OF WHICH IN TURN COULD CAUSE THE VALUE OF OUR SECURITIES TO SIGNIFICANTLY DECLINE OR BE WORTHLESS.

RECENT STATEMENTS MADE AND REGULATORY ACTIONS UNDERTAKEN BY CHINA’S GOVERNMENT, INCLUDING THE RECENT ENACTMENT OF CHINA’S NEW DATA SECURITY LAW, AS WELL AS OUR OBLIGATIONS TO COMPLY WITH CHINA’S CYBERSECURITY REVIEW MEASURES (REVISED DRAFT FOR PUBLIC CONSULTATION) AND ANY OTHER FUTURE LAWS AND REGULATIONS MAY REQUIRE US TO INCUR SIGNIFICANT EXPENSES AND COULD MATERIALLY AFFECT OUR ABILITY TO CONDUCT OUR BUSINESS, ACCEPT FOREIGN INVESTMENTS OR LIST ON A U.S. OR OTHER FOREIGN EXCHANGE. ADDITIONALLY, CHINA’S ANTI-MONOPOLY LAW AND SECURITY REVIEW RULES MAY RESTRICT OUR ABILITY TO MAKE INVESTMENTS IN OUR SUBSIDIARIES OR ACQUISITIONS IN CHINA.

THE HOLDING FOREIGN COMPANIES ACCOUNTABLE ACT (THE “HFCAA”) PROVIDES FOR ENHANCED DISCLOSURE REQUIREMENTS IF THE PUBLIC COMPANY ACCOUNTING OVERSIGHT BOARD (THE “PCAOB”) IS UNABLE TO inspect or investigate completely registered public accounting firms BECAUSE THE COMPANY USES A FOREIGN AUDITOR NOT SUBJECT TO PCAOB INSPECTION. ON DECEMBER 2, 2021, THE SEC ISSUED FINAL RULES UNDER THE HFCAA, WHICH BECAME EFFECTIVE ON JANUARY 10, 2022, AMENDING THE DISCLOSURE REQUIREMENTS IN ANNUAL REPORTS FOR REGISTRANTS THAT THE SEC IDENTIFIES AS HAVING FILED AN ANNUAL REPORT CONTAINING AN AUDIT ISSUED BY A REGISTERED PUBLIC ACCOUNTING FIRM THAT IS LOCATED IN A FOREIGN JURISDICTION THAT THE PCAOB IS UNABLE TO INSPECT OR INVESTIGATE COMPLETELY BECAUSE OF A POSITION TAKEN BY AN AUTHORITY IN THAT JURISDICTION. ON DECEMBER 16, 2021, THE PCAOB ISSUED ITS DETERMINATION THAT THE PCAOB IS UNABLE TO INSPECT OR INVESTIGATE COMPLETELY PCAOB-REGISTERED PUBLIC ACCOUNTING FIRMS HEADQUARTERED IN MAINLAND CHINA AND IN HONG KONG, BECAUSE OF POSITIONS TAKEN BY PRC AUTHORITIES IN THOSE JURISDICTIONS, AND THE PCAOB INCLUDED IN THE REPORT OF ITS DETERMINATION A LIST OF THE ACCOUNTING FIRMS THAT ARE HEADQUARTERED IN THE PRC OR HONG KONG. THIS LIST INCLUDES OUR AUDITOR, DELOITTE TOUCHE TOHMATSU CERTIFIED PUBLIC ACCOUNTANTS LLP.

FURTHER, ON APRIL 12, 2022, THE SEC PROVISIONALLY LISTED US AS A “COMMISSION-IDENTIFIED ISSUER” AND SUBSEQUENTLY, WE WERE CONCLUSIVELY LISTED AS A “COMMISSION-IDENTIFIED ISSUER.” ACCORDINGLY, IF WE DO NOT, IN A TIMELY MANNER, CHANGE TO AN INDEPENDENT ACCOUNTING FIRM THAT IS NOT HEADQUARTERED IN THE PRC OR HONG KONG AND IS NOT SUBJECT TO ANY OTHER RESTRICTION WHICH MAY BE IMPOSED BY THE PCAOB, TRADING IN OUR COMMON STOCK IN ANY ORGANIZED UNITED STATES MARKET will terminate, AS A RESULT OF WHICH YOU MAY LOSE THE ABILITY TO TRADE IN OUR COMMON STOCK OR MAY EVEN LOSE ALL OF THE VALUE OF YOUR SHARES.

PLEASE SEE “RISKS RELATED TO DOING BUSINESS IN THE PRC” FOR A LIST OF RISK FACTORS ASSOCIATED WITH OUR SUBSIDIARIES’ OPERATIONS IN CHINA AND OUR AUDITOR LOCATED IN CHINA AND THE FACT THAT SUCH RISKS COULD SIGNIFICANTLY AND ADVERSELY AFFECT OUR BUSINESS, OPERATIONS AND PROFITABILITY AND ACCORDINGLY THE VALUE OF OUR COMMON STOCK.

TO DATE, WE HAVE NOT PAID ANY DIVIDENDS TO OUR SHAREHOLDERS AND WE DO NOT HAVE ANY CURRENT INTENTION OF DOING SO IN THE FORESEEABLE FUTURE. SEE “DIVIDEND POLICY.”

Cash may be transferred within our organization in the following manners:

| ● | Our subsidiaries, including our PRC subsidiaries, may make dividends or other distributions to the Company. |

| ● | To date, no subsidiary has made dividends or distributions to the Company, and we do not have any present plan to make any dividends or distributions from subsidiaries to the Company in the foreseeable future. Certain of our subsidiaries, including our PRC-based subsidiaries, are subject to statutory and regulatory limitations on the payment of dividends to the Company, which could result in limitations on the availability of cash to fund dividends or distributions to investors in our securities. Please see “Risk Factors — Risks Related to Doing Business in the PRC — Laws and regulations in the jurisdictions in which our subsidiaries operate, including China, may restrict our ability to make any dividends or distributions.” |

| ● | Our subsidiaries may transfer funds to other subsidiaries in settlement of intercompany transactions for goods or services in the ordinary course of business or in the form of loans. |

| ● | From January 1, 2018 to March 31, 2022 our European and U.S. subsidiaries paid $38.0 million to our PRC subsidiaries for goods and services, and received $4.7 million from our PRC subsidiaries for services provided. During this period, the amount transferred between our PRC subsidiaries was $6.9 million for goods purchased. To date, the loans extended between our subsidiaries are not material. |

| ● | The Company may transfer funds to our subsidiaries, including our PRC subsidiaries, by way of capital contributions or loans. |

| ● | In connection with growing our business and funding operations, for the period between January 1, 2018 and July 22, 2021, the date immediately prior to the consummation of the Business Combination (as defined below), the Company (including, prior to the Business Combination, our wholly-owned subsidiary Microvast, Inc.) contributed approximately $7.7 million to our subsidiaries. Since the closing of the Business Combination on July 23, 2021 through March 31, 2022, the Company contributed or settled intercompany payables in favor of its subsidiaries in aggregate of approximately $191.5 million. |

| ● | The Company may transfer funds to subsidiaries to purchase goods or services. |

| ● | To date, the amount transferred from the Company (including, prior to the Business Combination, Microvast, Inc.) to our subsidiaries to purchase goods or services is not material. |

Our Sponsor (as defined below) paid only a nominal aggregate purchase price of $25,000 for 6,900,000 Founder Shares (as defined below), or approximately $0.004 per share, while the initial public offering price of our common stock was $10.00 per share and the trading price of our common stock was $2.06 as of July 22, 2022. Our Sponsor could earn a potential aggregate profit of $14.2 million, based on the $2.06 trading price, if the Sponsor sold all of its common stock and, even if the trading price of our common stock significantly declines, our Sponsor will stand to make significant profit on its investment in us. In addition, our Sponsor could potentially recoup its entire investment in us even if the trading price of our common stock is less than $1.00 per share. As a result, our Sponsor is likely to make a substantial profit on its investment in us even if trading price of our common stock declines, while our public shareholders could lose significant value in their common stock and experience a negative rate of return on the shares they purchased in the initial public offering (“IPO”) or in the public market.

Similarly, our Sponsor purchased 837,000 private warrants in our IPO for $1.00 per warrant. Based on the $0.2935 trading price of our warrants as of July 22, 2022, our Sponsor could have a potential loss of $0.7065 per warrant, or a potential aggregate loss of $591,341, if the Sponsor sold all of its warrants at the current trading price.

A number of outside investors agreed to purchase an aggregate of 48,250,000 shares of common stock at a price of $10.00 per share (the “PIPE investors”), the same price as the initial public offering price.

At the closing of the Business Combination (as defined below), the Company issued approximately 210,000,000 Merger Closing Shares (as defined below) to the former owners of Microvast, and 6,736,106 Bridge Notes Conversion Shares (as defined below) to the holders of the Bridge Notes (as defined below). Given that these shares were issued as consideration for the Business Combination and conversion of the Bridge Notes, respectively, the Company is unable to calculate a per share price, which could be much less than the initial public offering price. Therefore, holders of the Merger Closing Shares and the Bridge Notes Conversion Shares may experience a positive rate of return based on the current trading price, while public shareholders may experience a negative rate of return on shares they purchased at the initial public offering price.

This prospectus provides you with a general description of the securities and the general manner in which we and the Selling Holders may offer or sell the securities. More specific terms of any securities that we and the Selling Holders may offer or sell may be provided in a prospectus supplement that describes, among other things, the specific amounts and prices of the securities being offered and the terms of the offering. The prospectus supplement may also add, update or change information contained in this prospectus.

We will not receive any proceeds from the sale of shares of common stock or warrants by the Selling Holders pursuant to this prospectus, except with respect to amounts received by us upon exercise of the warrants to the extent such warrants are exercised for cash. There is no guarantee that the warrants will be exercised following the time they become exercisable and prior to their expiration, and as such, the warrants may expire worthless. Unless the stock price increases to over $11.50, it is unlikely the warrants will be exercised. Therefore, the cash proceeds associated with the exercises of the warrants is dependent on the stock price. However, we will pay the expenses, other than underwriting discounts and commissions, associated with the sale of securities pursuant to this prospectus.

The 293,860,085 shares of common stock being registered for resale under the registration statement of which this prospectus forms a part represent 98% of 302,538,640 shares of common stock currently outstanding. Resales of our common stock, including resales pursuant to this prospectus, may cause the market price of our securities to drop significantly. Additionally, outstanding warrants to purchase an aggregate of 28,437,000 shares of our common stock are exercisable in accordance with the terms of the warrant agreement governing those securities (the “Warrant Agreement”). To the extent such warrants are exercised, additional shares of our common stock will be issued, which will result in dilution to the holders of our common stock and increase the number of shares eligible for resale in the public market. Sales of substantial numbers of such shares in the public market or the fact that such warrants may be exercised could adversely affect the market price of our common stock.

Our registration of the securities covered by this prospectus does not mean that either we or the Selling Holders will issue, offer or sell, as applicable, any of the securities. The Selling Holders may offer and sell the securities covered by this prospectus in a number of different ways and at varying prices. We provide more information in the section entitled “Plan of Distribution.”

You should read this prospectus and any prospectus supplement or amendment carefully before you invest in our securities.

Our common stock and warrants are traded on the Nasdaq Global Select Market (“NASDAQ”) under the symbols “MVST,” and “MVSTW”, respectively. On July 22, 2022, the closing price of our common stock was $2.06 per share, and the closing price of our warrants was $0.2935 per warrant.

We are an “emerging growth company,” as that term is defined under the federal securities laws and, as such, are subject to certain reduced public company reporting requirements.

Investing in our securities involves risks. See “Risk Factors” beginning on page 19 and in any applicable prospectus supplement.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is .

TABLE OF CONTENTS

i

ABOUT THIS PROSPECTUS

This prospectus is part of a registration statement on Form S-3 that we filed with the Securities and Exchange Commission (the “SEC”) using a “shelf” registration process. Under this shelf registration process, we and the Selling Holders may, from time-to-time, issue, offer and sell, as applicable, any combination of the securities described in this prospectus in one or more offerings. We may use the shelf registration statement to issue up to an aggregate of 27,600,000 shares of common stock upon exercise of the public warrants. The Selling Holders may use the shelf registration statement to sell up to an aggregate of 293,860,085 shares of common stock and up to 837,000 warrants from time-to-time through any means described in the section entitled “Plan of Distribution.” More specific terms of any securities that the Selling Holders offer and sell may be provided in a prospectus supplement that describes, among other things, the specific amounts and prices of the common stock or warrants being offered and the terms of the offering.

A prospectus supplement may also add, update or change information included in this prospectus. Any statement contained in this prospectus will be deemed to be modified or superseded for purposes of this prospectus to the extent that a statement contained in such prospectus supplement modifies or supersedes such statement. Any statement so modified will be deemed to constitute a part of this prospectus only as so modified, and any statement so superseded will be deemed not to constitute a part of this prospectus. You should rely only on the information contained in this prospectus, any applicable prospectus supplement or any related free writing prospectus. See “Where You Can Find More Information.”

Neither we nor the Selling Holders have authorized anyone to provide any information or to make any representations other than those contained in this prospectus, any accompanying prospectus supplement or any free writing prospectus we have prepared. We and the Selling Holders take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the securities offered hereby and only under circumstances and in jurisdictions where it is lawful to do so. No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus, any applicable prospectus supplement or any related free writing prospectus. This prospectus is not an offer to sell securities, and it is not soliciting an offer to buy securities, in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus or any prospectus supplement is accurate only as of the date on the front of those documents only, regardless of the time of delivery of this prospectus or any applicable prospectus supplement, or any sale of a security. Our business, financial condition, results of operations and prospects may have changed since those dates.

This prospectus contains summaries of certain provisions contained in some of the documents described herein, but reference is made to the actual documents for complete information. All of the summaries are qualified in their entirety by the actual documents. Copies of some of the documents referred to herein have been filed, will be filed or will be incorporated by reference as exhibits to the registration statement of which this prospectus is a part, and you may obtain copies of those documents as described below under “Where You Can Find More Information.”

On July 23, 2021 (the “Closing Date”), the registrant, Microvast Holdings, Inc. (formerly known as Tuscan Holdings Corp.) consummated the previously announced acquisition of Microvast, Inc., a Delaware corporation (“Microvast”), pursuant to the Agreement and Plan of Merger (the “Merger Agreement”) dated February 1, 2021, between the Tuscan Holdings Corp., Microvast and TSCN Merger Sub Inc., a Delaware corporation (“Merger Sub”), pursuant to which Merger Sub merged with and into Microvast, with Microvast surviving the merger (the “Merger”). Unless the context otherwise requires, “Tuscan” refers to the registrant prior to the Closing, and “we,” “us,” “our” and the “Company” refer to the registrant and its subsidiaries, including Microvast, following the Closing.

In connection with the Merger Agreement, Tuscan, MVST SPV Inc., a wholly owned subsidiary of Tuscan (“MVST SPV”), Microvast, Microvast Power System (Huzhou) Co., Ltd., our majority owned subsidiary (“MPS”), certain MPS convertible loan investors (the “CL Investors”) and certain minority equity investors in MPS (the “Minority Investors” and, together with the CL Investors, the “MPS Investors”) and certain other parties entered into a framework agreement (the “Framework Agreement”), pursuant to which, among other things, (1) the CL Investors waived certain rights with respect to the convertible loans (the “Convertible Loans”) held by such CL Investors that were issued under that certain Convertible Loan Agreement, dated November 2, 2018, among Microvast, MPS, such CL Investors and the MPS Investors (the “Convertible Loan Agreement”) and, in connection therewith, certain affiliates of the CL Investors (“CL Affiliates”) subscribed for 6,719,845 shares of common stock, $0.0001 par value per share (“common stock”), of Tuscan in a private placement in exchange for MPS convertible loans (the “CL Private Placement”).

In connection with the Merger Agreement, Tuscan entered into subscription agreements with (a) the holders of an aggregate of $57,500,000 outstanding promissory notes issued by Microvast (the “Bridge Notes”) pursuant to which Tuscan agreed to issue an aggregate of 6,736,106 shares of common stock upon conversion (the “Bridge Notes Conversion”) of the Bridge Notes, and (b) a number of outside investors who agreed to purchase an aggregate of 48,250,000 shares of common stock at a price of $10.00 per share, for an aggregate purchase price of $482,500,000 (the “PIPE Financing”).

The CL Private Placement, the Bridge Notes Conversion and the PIPE Financing closed contemporaneously with the closing under the Merger Agreement (collectively, the “Closing”). Upon the Closing Date (as defined below), the CL Private Placement, the Bridge Notes Conversion, the PIPE Financing and related transactions (collectively, the “Business Combination”), Microvast became a wholly-owned subsidiary of the Company, with the stockholders of Microvast becoming stockholders of the Company, and the Company changed its name to “Microvast Holdings, Inc.”

ii

MARKET, RANKING AND OTHER INDUSTRY DATA

Certain market, ranking and industry data included in this prospectus, including the size of certain markets, are based on estimates of our management. These estimates have been derived from our management’s knowledge and experience in the markets in which we operate, as well as information obtained from surveys, reports by market research firms, our customers, distributors, suppliers, trade and business organizations and other contacts in the markets in which we operate, which, in each case, we believe are reliable.

We are responsible for all of the disclosure in this prospectus and while we believe the data from these sources to be accurate and complete, we have not independently verified data from these sources or obtained third-party verification of market share data and this information may not be reliable. In addition, these sources may use different definitions of the relevant markets. Data regarding our industry is intended to provide general guidance, but is inherently imprecise. Market share data is subject to change and cannot always be verified with certainty due to limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in any statistical survey of market shares.

Assumptions and estimates of our future performance are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Risk Factors — Risks Related to Our Business.” These and other factors could cause our future performance to differ materially from our assumptions and estimates. See “Cautionary Statement Regarding Forward-Looking Statements.”

iii

TRADEMARKS, SERVICE MARKS AND TRADE NAMES

This prospectus contains some of our trademarks, service marks and trade names. Each one of these trademarks, service marks or trade names is either (1) our registered trademark, (2) a trademark for which we have a pending application, or (3) a trade name or service mark for which we claim common law rights. All other trademarks, trade names or service marks of any other company appearing in this prospectus belong to their respective owners. Solely for convenience, the trademarks, service marks and trade names referred to in this prospectus are presented without the TM, SM and ® symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our respective rights or the rights of the applicable licensors to these trademarks, service marks and trade names.

iv

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements include, but are not limited to, statements about future financial and operating results, our objectives, expectations and intentions with respect to future operations, products and services; and other statements identified by words such as “will likely result,” “are expected to,” “will continue,” “is anticipated,” “estimated,” “believe,” “intend,” “plan,” “projection,” “outlook” or words of similar meaning. These forward-looking statements include, but are not limited to, statements regarding our industry and market sizes, and future opportunities for us. Such forward-looking statements are based upon the current beliefs and expectations of management and are inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are difficult to predict and generally beyond our control. Actual results and the timing of events may differ materially from the results anticipated in these forward-looking statements.

In addition to factors identified elsewhere in this prospectus, the following factors, among others, could cause actual results and the timing of events to differ materially from the anticipated results or other expectations expressed in the forward-looking statements:

| ● | risks of operations in the People’s Republic of China (the “PRC” or “China”); |

| ● | the impact of the ongoing COVID-19 pandemic; |

| ● | the conflict between Russia and Ukraine and any restrictive actions that have been or may be taken by the U.S. and/or other countries in response thereto, such as sanctions or export controls; |

| ● | risks related to cybersecurity and data privacy; |

| ● | the impact of inflation; |

| ● | changes in availability and price of raw materials; |

| ● | changes in the highly competitive market in which we compete, including with respect to our competitive landscape, technology evolution or regulatory changes; |

| ● | changes in the markets that we target; |

| ● | heightened awareness of environmental issues and concern about global warming and climate change; |

| ● | risk that we may not be able to execute our growth strategies or achieve profitability; |

| ● | risk that we are unable to secure or protect our intellectual property; |

| ● | the risk that we may experience effects from global supply chain challenges, including delays in delivering our products to our customers; |

| ● | risk that our customers or third-party suppliers are unable to meet their obligations fully or in a timely manner; |

| ● | risk that our customers will adjust, cancel or suspend their orders for our products; |

| ● | risk that we will need to raise additional capital to execute our business plan, which may not be available on acceptable terms or at all; |

| ● | risk of product liability or regulatory lawsuits or proceedings relating to our products or services; |

| ● | risk that we may not be able to develop and maintain effective internal controls; and |

| ● | outcome of any legal proceedings that may be instituted against us or any of our directors or officers. |

Actual results, performance or achievements may differ materially, and potentially adversely, from any projections and forward-looking statements and the assumptions on which those forward-looking statements are based. There can be no assurance that the data contained herein is reflective of future performance to any degree. You are cautioned not to place undue reliance on forward-looking statements as a predictor of future performance as projected financial information and other information are based on estimates and assumptions that are inherently subject to various significant risks, uncertainties and other factors, many of which are beyond our control.

All information set forth herein speaks only as of the date hereof, and we disclaim any intention or obligation to update any forward-looking statements as a result of developments occurring after the date hereof except as may be required under applicable securities laws. Forecasts and estimates regarding our industry and end markets are based on sources we believe to be reliable, however there can be no assurance these forecasts and estimates will prove accurate in whole or in part.

v

PROSPECTUS SUMMARY

This summary highlights certain significant aspects of our business and is a summary of information contained elsewhere in this prospectus. This summary is not complete and does not contain all of the information that you should consider before making your investment decision. You should carefully read this entire prospectus, including the information presented under the sections titled “Risk Factors,” “Cautionary Statement Regarding Forward Looking Statements,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and the consolidated financial statements and the related notes thereto included elsewhere in this prospectus before making an investment decision.

Microvast Holdings, Inc.

Microvast Holdings, Inc. is a Delaware corporation that is a holding company. As a holding company with no material operations of our own, our operations are conducted through our subsidiaries, including subsidiaries based in China. Although we are in the process of diversifying the geographic concentration of our operations, including by developing and expanding manufacturing facilities in Europe and the United States (“U.S.”), a substantial portion of our facilities are currently located in the PRC. Our auditor is located in China.

Effect of Holding Foreign Companies Accountable Act and Recent PCAOB Developments

The HFCAA requires a foreign company to certify that it is not owned or manipulated by a foreign government if the PCAOB is unable to inspect or investigate completely registered public accounting firms because the company uses a foreign auditor not subject to PCAOB inspection. If the PCAOB is unable to inspect the company’s auditors for three consecutive years, the issuer’s securities are prohibited from trading on a national exchange. The United States Senate passed the Accelerating Holding Foreign Companies Accountable Act, which was introduced in the United States House of Representatives. This Act, if enacted, would decrease the number of non-inspection years from three years to two, thus reducing the time period before our common stock may be prohibited from trading or delisted. The lack of access to the PCAOB inspection in China prevents the PCAOB from fully evaluating audits and quality control procedures of the auditors based in China. As a result, the investors may be deprived of the benefits of such PCAOB inspections. The inability of the PCAOB to conduct inspections of auditors in China makes it more difficult to evaluate the effectiveness of these accounting firms’ audit procedures or quality control procedures as compared to auditors outside of China that are subject to the PCAOB inspections, which could cause existing and potential investors in our stock to lose confidence in our audit procedures and reported financial information and the quality of our financial statements.

On December 2, 2021, the SEC issued final rules under the HFCAA, which became effective on January 10, 2022, amending the disclosure requirements in annual reports. These amendments apply to registrants that the SEC identifies as having filed an annual report containing an audit issued by a registered public accounting firm that is located in a foreign jurisdiction that the PCAOB is unable to inspect or investigate completely because of a position taken by an authority in that jurisdiction. The amendments require the submission of documentation to the SEC establishing that such a registrant is not owned or controlled by a governmental entity in that foreign jurisdiction and also require disclosure in an issuer’s annual report regarding the audit arrangements of, and governmental influence on, such registrants. The SEC is to identify a reporting company that has retained a registered public accounting firm to issue an audit report where that registered public accounting firm has a branch or office that:

| ● | is located in a foreign jurisdiction; and |

| ● | the PCAOB has determined that it is unable to inspect or investigate completely because of a position taken by an authority in the foreign jurisdiction. |

Once identified, Section 104(i)(2)(B) of the Sarbanes-Oxley Act requires these issuers, which the SEC refers to as “Commission-Identified Issuers,” to submit, in connection with their annual report, documentation to the SEC establishing that they are not owned or controlled by a governmental entity in that foreign jurisdiction and to name any director who is affiliated with the Chinese Communist Party or whether the company’s articles include any charter of the Chinese Communist Party.

1

On December 16, 2021, the PCAOB determined that the PCAOB is unable to inspect or investigate completely PCAOB-registered public accounting firms headquartered in mainland China and in Hong Kong, because of positions taken by PRC authorities in those jurisdictions, and the PCAOB included in the report of its determination a list of the accounting firms that are headquartered in the PRC or Hong Kong. This list includes our auditor, Deloitte Touche Tohmatsu Certified Public Accountants LLP.

Pursuant to the HFCAA, if an issuer is a Commission-Identified Issuer for three consecutive years (two consecutive years if the amendment to the HFCAA approved by the United States Senate and introduced in the United States House of Representatives is enacted), the SEC must prohibit the securities of the issuer from being traded on a national securities exchange or through any other method that is within the jurisdiction of the SEC to regulate, including through “over-the-counter” trading. On March 29, 2022, we filed our annual report for the year ended December 31, 2021, and on April 12, 2022, the SEC provisionally listed Microvast as a “Commission-Identified Issuer” and subsequently, we were conclusively listed as a “Commission-Identified Issuer.”

If we do not change to an independent accounting firm that is not headquartered in the PRC or Hong Kong in a timely manner, then trading in our common stock in any organized United States market will terminate, as a result of which you will lose the ability to trade our common stock or you may even lose all of the value of your shares of our common stock.

It will be necessary for us to change our independent auditors in sufficient time that we can satisfy the SEC that our new auditors are not headquartered in the PRC or Hong Kong or subject to any new disqualifying factor that the PCAOB may have adopted. In the event the PCAOB expands the category of firms which it cannot inspect, any new firm we engage would need to be a firm which is subject to regular inspection by the PCAOB. We cannot assure you that in the future we will be able to become an issuer that is not a Commission-Identified Issuer, in which event our common stock will not be tradable in any United States stock exchange or market and it may be necessary for us to list on a foreign exchange if shares of our common stock are to be traded. It is possible that, in the event trading in our stock in the United States is no longer possible, you may lose the entire value of your shares of our common stock.

PLEASE SEE “— RISKS RELATED TO DOING BUSINESS IN THE PRC” FOR A LIST OF RISK FACTORS ASSOCIATED WITH OUR SUBSIDIARIES’ OPERATIONS IN CHINA AND OUR AUDITOR LOCATED IN CHINA.

All securities being offered pursuant to this prospectus are securities of the Delaware holding company, and accordingly no investor will acquire a direct interest in any of the equity securities of our subsidiaries.

Business Summary

We are a technology innovator for lithium-ion (“Li-ion”) batteries. We design, develop and manufacture battery systems for electric vehicles and energy storage systems that feature ultra-fast charging capabilities, long life and superior safety. Our vision is to solve the key constraints in electric vehicle development and in high-performance energy storage applications. We believe the ultra-fast charging capabilities of our battery systems make charging electric vehicles as convenient as fueling conventional vehicles. We believe that the long battery life of our battery systems also reduces the total cost of ownership of electric vehicles and energy storage applications.

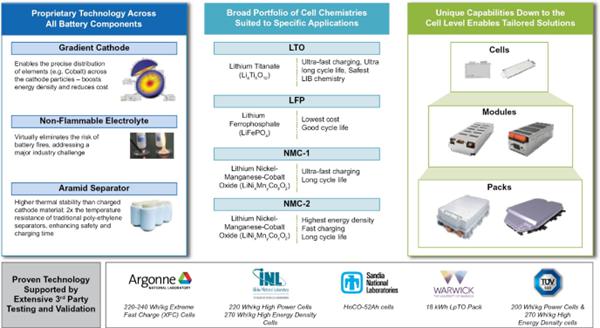

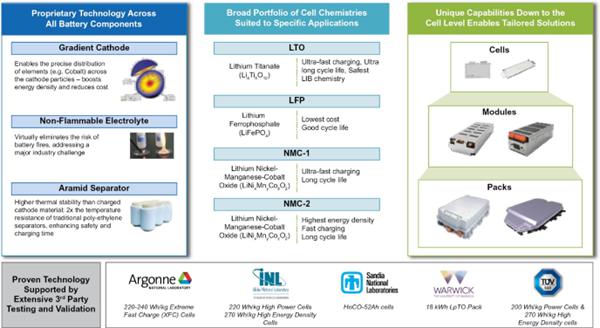

We offer our customers a broad range of cell chemistries, including lithium titanate oxide (“LTO”), lithium iron phosphate (“LFP”), nickel manganese cobalt version 1 (“NMC-1”) and nickel manganese cobalt version 2 (“NMC-2”). Based on our customer’s application, we design, develop and integrate the preferred chemistry into our cell, module and pack manufacturing capabilities. Our strategic priority is to offer these battery solutions for commercial vehicles and energy storage systems. We define commercial vehicles as light, medium, heavy-duty (“HD”) trucks, buses, trains, mining trucks, marine and port applications, automated guided and specialty vehicles. For energy storage applications, we focus on high-performance applications such as grid management and frequency regulation.

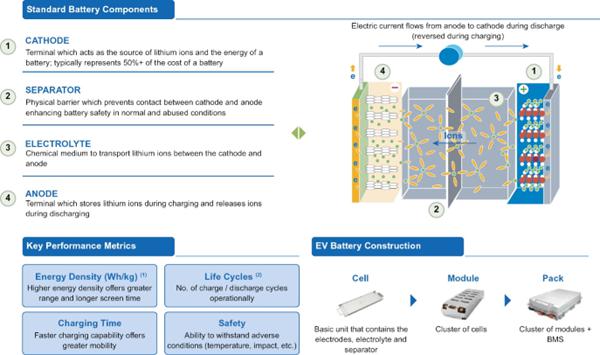

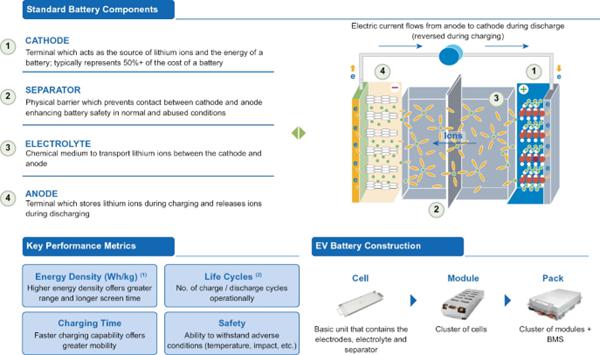

Additionally, as a vertically integrated battery company, we design, develop and manufacture the following battery components: cathode, anode, electrolyte and separator. We also intend to market our full concentration gradient (“FCG”) cathode and polyaramid separator to passenger car original equipment manufacturers (“OEMs”) and consumer electronics manufacturers. Please see the illustration below for an explanation of the functions of different battery parts.

2

Since we launched our first ultra-fast battery system in 2009, we have sold and delivered approximately 2,767.6 megawatt hours (“MWh”) of battery systems. As of March 31, 2022, we had an order backlog of approximately $120.8 million for our battery systems equivalent to approximately 327.6 MWh. Our revenue for the three months ended March 31, 2022, increased $21.7 million, or 145.5%, to $36.7 million, compared to the same period in 2021.

After initially focusing on the PRC and the Asia & Pacific regions, we have expanded and intend to continue expanding our presence and product promotion in Europe and the U.S. to capitalize on the rapidly growing electrification markets. A number of prototype projects are ongoing with regard to sports cars, commercial vehicles, trucks, port equipment and marine applications in the U.S. and Europe.

Set forth below is a diagram explaining the basic workings of batteries.

Industry and Market Opportunity

We believe global economic growth, greater awareness of environmental issues, government regulations and incentives and improved electric powertrain technologies are increasing the demand for environmentally friendly energy solutions, including electric vehicles. With the growing focus on, and the broad scientific acceptance of, the link between greenhouse gas emissions and climate change, many countries are adopting increasingly stringent environmental standards, especially as regards the emissions of CO2 from many forms of transport. It will be increasingly difficult for the conventional combustion engine to meet the emission targets being proposed, creating a huge opportunity for battery technologies.

Advances in chemistry and materials, of which we have been a leading innovator, have significantly improved electric powertrains. This, combined with the growing investment in charging station infrastructure and clear air initiatives, is leading to higher penetration rates for electric vehicles globally. Many consumers and businesses are increasingly willing to consider buying electric vehicles with new features and capabilities as their preferred clean-energy solution. We believe the following factors will result in significant growth in the market for electric vehicles:

| ● | Emission regulations: The introduction of public policies related to the reduction of greenhouse gas emissions, enhanced energy efficiency and increasing restrictions on the use of diesel engines, especially in the European Union (“EU”), represent one of the key market drivers for Li-ion e-mobility solutions. In 2020, the EU member states agreed to the 2030 European Green Deal, which includes targets and policy objectives to achieve a more competitive, secure and sustainable energy system within the EU. The 2030 European Green Deal seeks to reduce energy consumption by 27% by the end of 2030 compared to a “business as usual” scenario (base year 2014). The 2030 European Green Deal also seeks to reduce greenhouse gas emissions by 55% when compared to 1990 levels by 2030. In addition, the EU adopted the 2030 European Green Deal with the goal of net zero emissions of greenhouse gases by 2050. We believe that electrifying the many types of commercial vehicles, which is one of our focus areas, is an important step for countries to meet the current CO2 and NOx targets, which make cities and, in particular, city centers cleaner. |

3

| ● | Strong pull from transportation authorities and car manufacturers: Transportation authorities across Europe (for example, in London, Copenhagen, Barcelona, Paris and Milan) have communicated their mid-to-long term plans to replace existing internal combustion engine (“ICE”)-based bus fleets with new electrified buses. Moreover, regional and city governments across many countries in Europe have been active in general promotion of e-mobility penetration through, for example, introduction of bans on diesel cars in city centers and plans for free public transportation in certain towns and cities. More than 200 cities have already introduced emission and access regulation zones and a number of large cities, such as Paris and Madrid, have pledged to ban diesel vehicles from city centers by 2025. On December 15, 2020, the European Automobile Manufacturers’ Association (“ACEA”) announced that Europe’s truck manufacturers have concluded that by 2040 all new trucks sold need to be fossil free in order to reach carbon-neutrality by 2050. ACEA represents 16 major Europe-based car, van, truck and bus makers. |

| ● | Push for expanded electric vehicle market from major fleet companies: In January 2020, Amazon.com, AT&T Inc., DHL Express USA Inc. and other select companies with major delivery fleets came together and joined the Corporate Electric Vehicle Alliance (“CEVA”). CEVA will help member companies make and achieve bold commitments to fleet electrification, and is expected to boost the electric vehicle market by signaling the breadth and scale of corporate demand for electric vehicles — expanding the business case for the production of a more diverse array of electric vehicle models: |

| ● | Amazon: As part of The Climate Pledge, which includes a commitment to deliver 50% of shipments with net zero carbon by 2030, it is pursuing the highest standards in transportation sustainability. |

| ● | DHL: As part of its commitment to achieve net zero emissions from transport activities by 2050 globally, it has set the ambitious interim target of performing 70% of first- and last-mile operations with green vehicles by 2025. Electric vehicles will play an important role in reaching that target. |

| ● | IKEA: It has a commitment to use electric vehicles for all of its in-home furniture deliveries by 2025. |

Globally, the total addressable market for commercial vehicles is large and rapidly growing. According to Bloomberg New Energy Finance (“BNEF”), electric vehicle penetration in the key markets for commercial vehicle sales (i.e., U.S., Europe, the PRC, Japan and South Korea) is expected to grow from approximately 1.5% of the total units sold in 2020 to approximately 8.5% by 2025. Based on this estimate, the growth in commercial vehicles will increase the demand for battery capacity from 17.5 gigawatt hours (“GWh”) in 2019 to 98.6 GWh in 2025. In terms of drivetrain adoption in commercial vehicle sales, BNEF predicts that approximately one-third of the global light commercial vehicle (“LCV”) market will be electrified by 2030 and the adoption rate will reach almost 60% by 2040. According to BNEF, in some markets, such as in Europe and in South Korea, electric LCVs will take up 50% of the local LCV market by 2030, but in many other countries, such as the U.S. and Japan, sales will exceed 40%. Similarly, according to BNEF, in HD segments, sales of electric trucks are projected to reach 30% by 2040.

We believe that the adoption of electric vehicles has been handicapped by many challenges imposed by conventional battery systems, including:

| ● | Range anxiety and reduced mobility. Electric vehicles powered by conventional battery systems need significantly more time to be fully charged and many models (usually with battery capacity of no more than 40 kilowatts per hour (“kw/h”) only provide up to 100 miles of range. This has compared unfavorably to internal combustion engine vehicles which can travel more than 300 miles between fuel stops and can refuel within 10 minutes. |

4

| ● | High replacement costs. Most conventional battery systems have a shorter life span than the useful life of the vehicles that they are installed in. As a result of this mismatch, the battery typically needs to be replaced during the life of the vehicle, leading to significant replacement costs. |

| ● | Safety. Li-ion batteries are known to be a factor in consumer electronic and passenger vehicle fires. |

| ● | Design and performance not optimized for commercial vehicles. Conventional battery systems designed for passenger cars offer longer charge times and limited cycle life, thus reducing operational efficiency and battery life. |

Our Solution

Our approach is offering a tailored battery solution based on the operating requirements of our customers. With a broad range of battery chemistries to select from, we can offer several different battery solutions to our customers, including LTO, LFP, NMC-1 and NMC-2. We believe our technologies and battery systems offer the following advantages over commonly used battery systems:

| ● | Ultra-Fast Charging Capability. Depending on the selected battery chemistry, we can offer battery solutions that can be fully charged within 10-30 minutes, significantly faster than commonly used battery systems. The ultra-fast charging capabilities of our battery systems significantly enhance electric vehicle mobility and have the potential to accelerate consumer adoption of electric vehicles. Our latest-generation LTO cells can be fully charged within 10 minutes while providing an energy density of up to 180 watt-hours per liter (“Wh/l”) and 95 watt-hours per kilogram (“Wh/kg”). These ultra-fast charging capabilities and long battery life can meet the diverse vehicle design requirements of our OEM customers. Our NMC-2 products can be fully charged within 30 minutes, providing higher energy density of more than 220Wh/kg. |

| ● | Long Battery Life. Depending on the selected battery chemistry, we can offer battery solutions with a life of between 2,500 and 20,000 full charge/discharge cycles. The longer battery life enables our battery systems’ useful life to match the life of the vehicles in which our systems are installed, avoiding the need to replace the battery and thereby lowering our customers’ total cost of ownership. For example, our LTO batteries retain 90% of their initial capacity after approximately 10,300 full charge/discharge cycles, according to a test report produced by Warwick Manufacturing Group (“WMG”), an academic department at the University of Warwick in the United Kingdom (the “U.K.”). |

| ● | Enhanced Margin of Safety. Drawing from an intellectual property library that took over a decade to develop, we work to increase the margin of safety of our products, beginning with the initial design and through the use of carefully selected battery components. Our LTO battery is inherently safer than other battery chemistries, with very good thermal stability, the ability to operate in a broad range of temperatures, and a lower risk of internal short circuits and fire-related hazards. For products demanding higher energy densities, our in-house manufactured battery components, the aramid separator, non-flammable electrolyte and full-concentration gradient cathode individually or collectively are being implemented in certain current and future products to improve product safety. Our in-depth knowledge of how these battery components interact with each other in the battery cell is utilized in the design and build of our products, helping ensure our products have better safety margins. |

Our Competitive Strengths

We believe the following strengths position us well to capitalize on and lead the global vehicle electrification trend:

Breakthrough battery solutions

Our vision is to solve the key constraints in electric vehicle batteries and to design electric vehicle power systems that facilitate the mass adoption of electric vehicles. Our battery solutions have a proven track record enabled by our transformational technologies that make electric vehicles more convenient, affordable and safe.

| ● | We believe our ultra-fast charging battery technology makes charging electric vehicles as convenient as fueling conventional vehicles and has the potential to accelerate consumer adoption of electric vehicles. In addition, our ultra-fast charging battery technology significantly increases the utilization and efficiency of charging stations with its short charging time requirements. |

| ● | Our battery solutions significantly reduce the total cost of ownership of an electric vehicle. Our ultra-fast charging battery technology enables our customers to install fewer battery packs per vehicle, while the longer battery life matches with the life of the vehicle, eliminating the need to replace the battery during the life of the vehicle. |

5

Since the first electric buses powered with our battery system were put into commercial operation in 2009, we have sold and delivered over 28,000 battery systems for commercial vehicles. Our systems are in use in 220 cities from 28 countries under diverse weather conditions, accumulating billions of miles of operational distance.

We believe our battery solutions best position us to be a key player in the vehicle electrification revolution and to pave the way for mass adoption of electric vehicles.

Market leader in providing ultra-fast charging battery solutions

We are a provider of ultra-fast charging battery solutions to electric vehicles globally. We believe our ultra-fast charging battery technology best positions us to continue penetrating the fast-growing global electric vehicle market. Since we first launched our LTO ultra-fast charging battery technology in 2009, we have successfully deployed our product portfolio in large scale commercial operations in the PRC, the Asia & Pacific region and in Europe and we are in the process of expanding our customer base in the U.S. With our expanding customer base in the Western Hemisphere, we believe we are well on our way of establishing ourselves as a leading supplier of Li-ion battery solutions for commercial vehicles globally.

Vertical integration from initial concept development to final system manufacturing

We have adopted a customer-oriented product development approach to provide highly customized solutions. This is facilitated by our vertical integration which extends from core battery chemistry to application technologies such as battery management systems and other power control electronics. Our vertical integration capability is supported by our unique research and development (“R&D”) and design capabilities across the complete battery system and our established in-house manufacturing capability. This vertical integration gives us the flexibility to produce key materials in-house to manage supply and cost of materials. We believe we are one of the very few leading battery solution providers that can provide highly customized battery systems with the ability to address a range of battery materials, manufacturing, application engineering and design issues. The ability to work with partners and customers across the design process enables us to better understand customers’ needs and allows us to customize our products to their specific requirements.

Our vertical integration also enables a quicker and more coordinated development process for new technologies and products. It also ensures better quality and cost control during the manufacturing process. Furthermore, by managing each design step, from battery chemistry to power system, we can better protect our intellectual property and know-how.

Proven track record of innovation

We have adopted a customer focused approach in directing our R&D efforts to develop battery technologies that are bespoke to the requirements of commercial vehicle owners. We focus on building our battery systems from the ground up, not relying on any third-party technologies or approaches. The combination of our vertically integrated manufacturing system and cutting-edge lab research has helped us to innovate, develop and quickly commercialize new technologies and products.

We have a strong track record of product innovation, successful commercialization of such innovations, and those products being proven over many years and across many different types of commercial vehicles. For example, we first launched LTO ultra-fast charging battery technology in 2009 and put it into commercial operation in the same year.

6

In 2013, we launched the second generation LTO battery system, which offers higher-energy density while retaining fast-charging and long-cycle life capabilities. In 2017, we launched the NMC-1 battery system, which offers much higher-energy density while and long cycle life attributes. In 2019, we launched the NMC-2 battery system which can be fully charged in 30 minutes.

We have an expansive R&D team of scientists and engineers, including leading electric vehicle battery industry veterans as well as experts in the research and science community, who are focused on developing cutting edge technologies. As of March 31, 2022, we have been granted 400 patents and have 149 patent applications pending.

Large and growing customer base and applications

We have strategically prioritized the development of battery systems for commercial vehicles and energy storage applications. We believe that our battery systems have a unique combination of features: ultra-fast charging capabilities, long battery life and enhanced safety. These features are highly valued by commercial vehicles and high-performance energy storage customers who are sensitive to the total cost of ownership.

We can count some of the leading global commercial vehicle OEMs as our customers, including Iveco, Yutong, Higer, Foton, King Long, JBM and Wright Bus. With our batteries being deployed across a broad range of commercial vehicles, including automated guided vehicles, port equipment, mining trucks and fork-lift trucks, we have customer relationships with the likes of eVersum, Kion, Kalmar, Linde, PSA Singapore and Gaussin. All of these names are recognized as leading OEMs in their particular area of focus.

Experienced and visionary senior management team with highly motivated employees

Mr. Yang Wu, our Founder, Chief Executive Officer and Chairman, and Dr. Wenjuan Mattis, our Chief Technology Officer, have led us in successfully innovating and commercializing new technologies. Mr. Wu is a visionary leader and entrepreneur with over 25 years of experience in technology development. While most of our competitors were still focusing on developing lithium iron phosphate-based battery technologies, he focused on developing a new battery technology to create an ultra-fast charging battery to address the key constraints for electric vehicle development. Dr. Mattis has over 16 years of experience in the Li-ion battery industry and has authored 22 papers and holds 93 patent applications and patents.

Our senior management team also includes Mr. Craig Webster, our Chief Financial Officer. Mr. Webster has over 20 years of experience in accounting, finance, legal and capital markets, as well as public company board service. Our expansion to regions beyond the Asia & Pacific region is led, for the U.S., Canada and South America markets, by Mr. Shane Smith, and for Europe, Middle East and North Africa markets, by Mr. Sascha Kelterborn. Mr. Smith and Mr. Kelterborn are both experienced senior managers with more than 20 years international business experience, and Mr. Kelterborn was recently promoted to President of the Company on April 14, 2022.

As we grow, we remain focused on hiring employees who share the same ethos. We have built a team focused on developing innovative solutions to the problems faced by electric vehicle batteries, and we believe our employees’ shared passion, experience and vision represent an increasingly important competitive advantage.

Our Strategies

Our strategy is to globally market our competitive product portfolio. Initially, we intend to focus our sales and marketing efforts on our battery solutions in commercial vehicles and energy storage customers, where our vertical integration and high-performance technology can address the challenging and diverse set of requirements desired by these customers. For passenger electric vehicles and consumer electronics applications, we are marketing our FCG cathode and polyaramid separator components to manufacturers that need better materials to meet demands for higher energy densities and greater intrinsic safety.

Global market presence

After initially being focused on the PRC and the Asia & Pacific regions, we have expanded and intend to continue expanding our presence and product promotion to Europe and the U.S. to capitalize on the rapidly growing electrification markets. In 2021, we increased our marketing efforts directed at potential customers in regions outside the Asia & Pacific region and added more employees to support business development efforts in the Western Hemisphere.

7

The Western Hemisphere presents enormous growth opportunities for electric vehicles, driven by higher emission standards, reduced total cost of ownership compared to gas-based combustion engines, and growing environmental awareness. In the U.S., we believe the current political administration is likely to push the electrification revolution through regulation. In pursuing contract opportunities with industry-leading companies in the Western Hemisphere, we have seen how our potential customers recognize the lower total cost of ownership for commercial electric vehicles and are seeking alternative forms of energy for energy storage applications.

Our growing operations in Europe and the U.S. are conducted through our subsidiaries in Germany and the U.S. Revenues generated in Europe and the U.S. are expected to be used to continue to fund operations and growth in those particular geographies.

As we expand our presence globally, we will continue to invest in our existing operations in the PRC and the Asia & Pacific region and continue our efforts to grow our business in that region as well. Revenues generated in the PRC and the Asia & Pacific region are expected to be used to continue to fund operations and growth in those particular geographies.

Improve performance and reduce total cost of ownership of our battery systems

The total cost of ownership is an important criterion for commercial electric vehicle and energy storage system customers. In order to maintain our leading position in the market, we will continue investing in R&D for our high-performing battery technology and seek new innovations to further lower costs.

For battery system solutions, this means continuing to develop new battery cells and modules and improving the energy densities of our existing batteries. Our R&D team is constantly working to integrate new designs, technologies and materials into our cells to enhance performance and lower cost. We have used this approach to develop cells with various chemistries (LTO, LFP, NMC-1, NMC-2), and to provide a variety of products (LpTO, LpCO, MpCO, HnCO) with different energy densities, fast charge times and cycle life.

One important strategy we have employed historically and will continue to focus on going forward is the research emphasis on advanced materials to enhance our products. For example, in 2019, we received the R&D 100 Award for a battery incorporating our unique FCG and polyaramid components, which showcases how new materials enable higher energy density and longer cycle life products as well as improving performance and lowering total costs of ownership. Improving performance at the base components has the added advantage of making both our battery solutions and our component products more attractive.

Expand manufacturing capacity to meet growing demand

We plan to prudently expand our manufacturing capacity to capture the large and growing market opportunity for electric vehicles. Our capacity expansion will be phased in based on our ongoing assessment of medium- and long-term demand for our products. We reached an aggregate manufacturing capacity of approximately 4 GWh per year as of March 31, 2022. We plan to achieve a total manufacturing capacity of 11 GWh per year by 2025 to support growing demand for our existing products. As for battery components, we plan to expand our manufacturing capacity for the polyaramid separator and FCG cathode.

In 2021, we completed a 170,000 square foot facility near Berlin, Germany, which included the installation of a fully automated battery module line and started the ramp-up phase of serial production. We are also in the process of fully equipping the facility by installing a semi-automated pack equipment line to support anticipated demand. The Berlin facility, once fully equipped, will be able to support up to 6 GWh of battery module and battery pack capacity. In light of anticipated EU regulations designed to require battery cell production to be located in Europe and “green” energy usage for battery production and the introduction of a “battery passport,” we anticipate that in the near future we will need to build additional cell manufacturing capacity in Europe to meet local demand.

In February 2021, we began converting an existing building we purchased in Clarksville, Tennessee to support up to 2 GWh of cell, module and pack capacity. The existing facility, once fully equipped, will be able to support up to 4 GWh of cell, module and pack capacity. Once completed, it is anticipated that this facility will primarily serve our customers in the U.S. In addition, we believe there is sufficient acreage at the existing Clarksville site to construct another building and further increase capacity by an additional 4 GWh, for a total of 8 GWh of future manufacturing capacity in Clarksville.

Additionally, we are in the process of adding 2 additional GWh battery cell and module capacity and 10 million square meters of separator capacity to our facility in Huzhou, China. We believe the new facility in Huzhou will support total future manufacturing capacity up to 12 GWh.

8

With facilities and resources in the PRC, Europe and the U.S., our manufacturing facilities are located in close proximity to our customers in each major region. Our manufacturing facilities are strategically located around the world to better address customer demand, reduce local content requirements, limit tariffs and reduce logistical expenses.

Our Solutions, Technologies and Applications

Our Solutions

We are in the business of developing and selling innovative, and industry-leading, energy storage solutions to OEM customers. In addition to designing and manufacturing the physical battery system, we offer services such as engineering and design, maintenance and support services.

The battery system is based on our proprietary LTO, LFP, NMC-1 or NCM-2 cell products. The cells are then made into battery modules, which are then assembled into a battery pack. We handle the manufacturing of the cell, module and pack and work with the OEM to customize the battery system, so it can be integrated into their vehicles. The battery pack may be air-cooled or liquid-cooled and is designed with a flexible layout to accommodate different cell numbers and multi-layering with frames. In some cases, battery management software and installation may be provided to the customer. The battery management software monitors the battery, improving the safety and thermal control, which enhances the battery system lifetime and cost-efficiency. We assemble the battery packs using standard components, making them easier to install and maintain.

As part of the customization process, we conduct feasibility testing using a prototype of a customer’s vehicle and obtain feedback from the customer to customize the battery system for the customer’s specific use. We may also install the battery systems for our customers after we deliver the battery systems to them. We may also provide maintenance services and train our customers’ staff on the use and maintenance of our products.

We currently sell our battery systems primarily to OEMs for use in commercial electric and other specialty vehicles. Our battery systems have a number of other applications, including (a) as energy storage for renewable energy generators and utility grids, (b) for frequency regulation, (c) as an uninterrupted power supply in other high-power electrical equipment and devices and (d) in passenger electric vehicles. In addition, we can sell components of our battery system, such as the FCG cathode or polyaramid separator, to other manufacturers focused on passenger electric vehicles.

Our Technologies

9

We have been developing battery technologies for fast charging, long life, and high safety since our founder outlined a set of research objectives in 2008. Since then, we have developed technologies spanning the battery system production through our vertically integrated approach: from basic cell materials like cathode, anode and separator, to cooling systems and software controls for the battery pack. Some of the key highlights from our technology portfolio are:

Battery Cell Materials

| ● | Polyaramid Separator — Our polyaramid separator, conceived and developed entirely by us, is significantly more stable under heat than traditional poly-ethylene separators. Polyaramid is similar to Kevlar, the material that is used in bullet-proof vests, and its excellent thermal properties (stable to nearly 300°C in the air) are well known, but we have developed the techniques necessary to form this material into ~10um thick, meters wide and hundreds of meters long porous separator material that is suited for Li-ion batteries. The material is currently being evaluated through the U.S. Advanced Battery Consortium grant, and the project manager from one of the big three OEMs has described this technology as “the greatest breakthrough in Li-ion battery separator technology in 20 years.” |

| ● | LTO — Our LTO powder is specifically manufactured to promote high power operation, making it ideal for ultra-fast-charging applications. LTO is a safer Li-ion battery anode material because it is one of the only anode materials inherently stable against traditional Li-ion electrolytes. |

| ● | FCG Cathode — Our gradient cathode was licensed from Argonne National Labs in 2017. Since then, we have developed significant, flexible manufacturing know-how to produce the material with minimal cost increases compared to normal NMC materials. By controlling the concentration of metals within a particle, the material’s safety can be enhanced. This is because the gradient is a designer cathode, meaning the material design can be tailored for specific end uses and cells/customers can receive a unique material product explicitly for their needs. This customization makes the technology well suited for ultra-fast charging and low-cost advanced Li-ion cells. We believe this technology is especially well suited going forward for the development of materials that greatly reduce or eliminate cobalt from the cathode. |

| ● | Non-Flammable Electrolyte — Since Li-ion batteries typically use flammable organic solvents, they have the potential, under certain conditions, to catch fire. Our technology, protected through patents and trade secrets, will not catch fire even if a flame is directly brought in contact with a cup of the electrolyte formulation. Using our electrolyte greatly retards, and in some cases can stop entirely, a Li-ion cell from catching fire. Reducing the flammability of Li-ion cells is an important safety feature that we believe will become even more sought after as the market pushes towards ever higher, and hence less stable, energy density cells. |

Cell Chemistry

| ● | LTO — LTO is used in place of the typical graphite on the anode. LTO greatly enhances the Li-ion cell’s safety and fast charge ability, at the cost of some energy density. Our cells using LTO have exceptional lifetimes. Our cells using LTO have successfully addressed a key problem for the technology, cell gassing. By eliminating the gas generation during cycling, our cells can have exceptionally long performance lifetimes. |

| ● | LFP — One of the safest cathode options, LFP is manufactured from low-cost materials, making it highly affordable. Our LFP cells were developed at the behest of a Chinese OEM, and our technology was selected over one of the biggest battery companies in the world because our performance and price were superior to the competitors. |

| ● | NMC — Applications requiring higher energy cell density today must be built using the layered metal oxide crystal structure (which includes NMC, NCA, NMCA and FCG). Our cells based on this chemistry have excellent cycle performance, which we attribute to our better understanding of the various cell materials from our vertical integration structure. By controlling the cathode and separator technologies going forward, our NMC cells will have lower prices and enhanced safety compared to many of our competitors’ products. Cells using NMC technology have been third-party evaluated by TUV and various U.S. National Labs, confirming our claims to performance. |

10

Our Applications

Electric Buses and Other Commercial Vehicles

The ultra-fast charging capabilities of our battery systems mean that electric buses equipped with our batteries only need to charge for 10 to 30 minutes, depending on the battery chemistry. In buses, this allows a single charge for each loop or multiple loops they travel. In contrast, electric buses equipped with certain of our competitors’ technology need to charge overnight to store sufficient energy to run an entire day. Furthermore, our battery system’s life span matches the useful life of a typical bus, which avoids the need to replace the battery during the useful life of the vehicle.

The high energy density of our battery systems makes our battery systems an ideal choice for delivery vans and trucks. It reduces the charging interval and thus ensures a smooth daily operation of the commercial vehicle by equipping sufficient energy onboard. Ultra-fast charging capability enables the use of automated guided vehicles in harbors and airports and other applications where 24-hour operations are required.

Materials

All Li-ion batteries are composed of an anode, cathode, electrolyte and separator.

| ● | Anode — Our anode is selected historically from LTO or graphite in our product cells. In the coming years, we anticipate that we will develop and market a new product that contains silicon or silicon oxide. |

| ● | Cathode — Our LFP is sourced from a commercial supplier. For NMC, our existing products are made using commercially supplied material, and our future cell products will utilize FCG when possible. For NMC based cathodes, the sourcing and availability of cobalt is a key issue for many OEM buyers. As such, we are actively engaged in research to greatly reduce or eliminate the use of cobalt from our material stream. |

| ● | Electrolyte — Our present Li-ion cells use liquid-based electrolyte formulations. For carbonate-based electrolytes we typically elect to buy the base solvents from commercial suppliers due to lower costs from their economies of scale, and then blend solutions in-house to ensure our proprietary mixtures are not shared outside the company. |

| ● | Separator — The separator is another key material in our Li-ion cells. While we have in the past used the industry norm polyethylene/polypropylene materials, we are now working to integrate as many cells as possible with our proprietary polyaramid technology. In addition, we are actively working to build on our polyaramid knowledge to develop a solid electrolyte battery system that incorporates the polyaramid material as a component of the solid electrolytes. If the solid electrolyte approach is successful, not only will it eliminate the use of liquid electrolytes, but it will also potentially enable new anode chemistries such as lithium metal, which is needed to reach cells with over 1,000 Wh/L energy densities. |

Quality and Safety Control

Our batteries have passed quality and safety control testing under the QC/T 743-2006 standard by the National Coach Quality Supervision and Test Center, a non-government entity accredited to verify certain PRC government quality and safety control standards.