UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

OR

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

Commission file number:

(Exact name of Registrant as specified in its charter) |

N/A

(Translation of the Registrant’s name into English)

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Telephone:

Email: zoe@pavs.ai

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

* Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of Each Class |

| Trading Symbol |

| Name of Each Exchange on Which Registered |

|

|

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

The number of outstanding shares of each of the issuer’s classes of capital or common stock as of March 31, 2024 were 6,724,675 Class A ordinary shares, par value $0.01 per share and 612,255 Class B ordinary shares, par value $0.01 per share.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ | Accelerated filer ☐ | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive- based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

☒ | ☐ | International Financial Reporting Standards as issued by the International Accounting Standards Board | ☐ | Other |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow: Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

TABLE OF CONTENTS

|

|

| Page |

|

|

|

| Number |

|

| ii |

| ||

|

|

|

| |

| iii |

| ||

|

|

|

|

|

| 1 |

| ||

| 1 |

| ||

| 1 |

| ||

| 24 |

| ||

| 49 |

| ||

| 50 |

| ||

| 62 |

| ||

| 68 |

| ||

| 68 |

| ||

| 69 |

| ||

| 69 |

| ||

| 81 |

| ||

| 82 |

| ||

| 82 |

| ||

MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS |

| 82 |

| |

| 82 |

| ||

| 83 |

| ||

| 83 |

| ||

| 84 |

| ||

| 84 |

| ||

| 84 |

| ||

PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS |

| 84 |

| |

| 85 |

| ||

| 85 |

| ||

| 85 |

| ||

DISCLOSURE REGARDING FOREIGN JURISDICTION THAT PREVENT INSPECTIONS |

| 85 |

| |

| 87 |

| ||

| 87 |

| ||

| 88 |

| ||

i |

| Table of Contents |

INTRODUCTORY NOTES

Unless otherwise indicated or the context otherwise requires in this annual report:

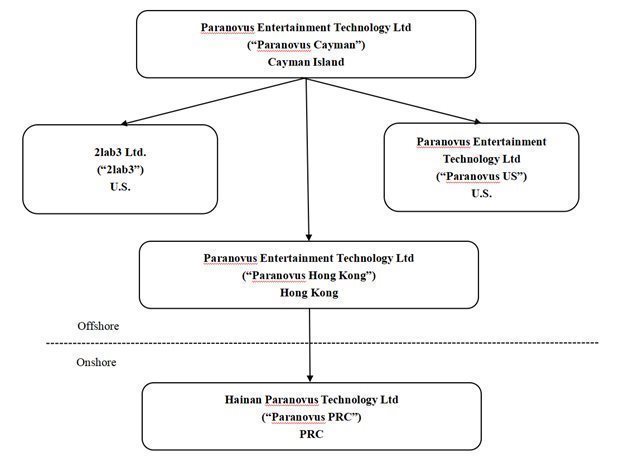

| ● | “2lab3” refer to 2lab3 Inc., a Delaware corporation which is wholly owned by the Company; |

|

|

|

| ● | “China” or the “PRC” refers to the People’s Republic of China, including Hong Kong Special Administrative Region and the Macau Special Administrative Region, unless referencing specific laws and regulations adopted by the PRC and other legal or tax matters only applicable to mainland China, and excluding, for the purposes of this annual report only, Taiwan; “PRC subsidiaries” and “PRC entities” refer to entities established in accordance with PRC laws and regulations; |

|

|

|

| ● | “Class A Ordinary Shares” refer to the Class A ordinary shares of the Company, par value $0.01 each; |

|

|

|

| ● | “Class B Ordinary Shares” refer to the Class B ordinary shares of the Company, par value $0.01 each; |

| ● | “Fujian Happiness” is to Fujian Happiness Biotech Co., Limited, a limited liability company organized under the laws of the PRC and a wholly-owned subsidiary of Happiness Fuzhou; |

| ● | “Happiness Hong Kong” refers to Happiness Holding Group Limited (formerly known as Happiness Biology Technology Group Limited), a Hong Kong limited liability company organized under the laws of Hong Kong and a wholly-owned subsidiary of Happiness Development; |

| ● | “Happiness Fuzhou” refers to Happiness (Fuzhou) E-commerce Co., Ltd,, formerly known as Happiness (Nanping) Biotech Co., Limited (“Happiness Nanping”), a limited liability company organized under the laws of the PRC and a wholly-owned subsidiary of Happiness Hong Kong; |

|

|

|

| ● | “Happy Buy” refers to Happy Buy (Fujian) Internet Technology Co., Limited, a limited liability company organized under the laws of the PRC and a wholly-owned subsidiary of Happiness Fuzhou; |

| ● | “PAVS”, “Paranovus”, or “the Company” refer to Paranovus Entertainment Technology Ltd. (formerly known as “Happiness Development Group Limited”), an exempted company registered in the Cayman Islands with limited liability; |

| ● | “Paranovus Hong Kong” refers to Paranovus Entertainment Technology Limited, a limited liability company established under the laws of Hong Kong and a wholly owned subsidiary of PAVS; |

|

|

|

| ● | “Paranovus PRC” refers to Hainan Paranovus Entertainment Technology Co., Ltd., a limited liability company organized under the laws of the PRC and a wholly-owned subsidiary of Paranovus Hong Kong; |

| ● | “RMB” and “Renminbi” refer to the legal currency of China; |

|

|

|

| ● | “Shunchang Happiness” is to Shunchang Happiness Nutraceutical Co., Ltd, a 100% subsidiary of “Fujian Happiness”; |

| ● | “Taochejun,” refers Taochejun (Fujian) Auto Sales Co., Limited., a 51% subsidiary controlled by Happiness Fuzhou; |

| ● | “US$,” “U.S. dollars,” “$” and “dollars” refer to the legal currency of the United States; and |

| ● | “we,” “us,” “our company” and “our” refer to Paranovus Entertainment Technology Ltd. and its consolidated subsidiaries. We conduct operations in China through our PRC subsidiaries. |

Names of certain companies provided in this annual report are translated or transliterated from their original Chinese legal names.

ii |

| Table of Contents |

FORWARD-LOOKING STATEMENTS

This annual report on Form 20-F contains forward-looking statements that reflect our current expectations and views of future events. These statements are made under the “safe harbor” provisions of the U.S. Private Securities Litigation Reform Act of 1995. You can identify these forward-looking statements by terminology such as “may,” “will,” “expect,” “anticipate,” “aim,” “estimate,” “intend,” “plan,” “believe,” “is/are likely to,” “potential,” “continue” or other similar expressions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our financial condition, results of operations, business strategy and financial needs. These forward-looking statements include, but are not limited to:

| · | the adverse effects of the COVID-19 outbreak on our business or the market price of our ordinary shares; |

|

|

|

| · | our goals and strategies; |

|

|

|

| · | our future business development, financial condition and results of operations; |

|

|

|

| · | our expectations regarding the market for our concrete products; |

|

|

|

| · | our expectations regarding demand for and market acceptance of our nutraceutical and dietary supplements products; |

|

|

|

| · | our plans to establish partnerships and develop new businesses; |

|

|

|

| · | our plans to invest in our business; |

|

|

|

| · | our relationships with our partners; |

|

|

|

| · | our future business development, results of operations and financial condition; |

|

|

|

| · | market conditions affecting our equity capital; |

|

|

|

| · | change in macroeconomic conditions; |

|

|

|

| · | competition in our industry; and |

|

|

|

| · | relevant government policies and regulations relating to our industry. |

We would like to caution you not to place undue reliance on these forward-looking statements and you should read these statements in conjunction with the risk factors disclosed in “Item 3. Key Information—D. Key Information—Risk Factors.” Those risks are not exhaustive. We operate in an evolving environment. New risks emerge from time to time and it is impossible for our management to predict all risk factors, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ from those contained in any forward-looking statement. We do not undertake any obligation to update or revise the forward-looking statements except as required under applicable law. You should read this annual report and the documents that we reference in this annual report completely and with the understanding that our actual future results may be materially different from what we expect.

iii |

| Table of Contents |

PART I

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

Not applicable.

ITEM 3. KEY INFORMATION

A. [Reserved]

B. Capitalization and indebtedness.

Not applicable.

C. Reasons for the offer and use of proceeds.

Not applicable.

D. Risk factors.

An investment in our ordinary shares involves a high degree of risk. You should carefully consider the risks and uncertainties described below together with all other information contained in this annual report, including the matters discussed under the headings “Forward-Looking Statements” and “Operating and Financial Review and Prospects” before you decide to invest in our ordinary shares. We are a holding company with substantial operations in China and are subject to a legal and regulatory environment that in many respects differs from the United States. If any of the following risks, or any other risks and uncertainties that are not presently foreseeable to us, actually occur, our business, financial condition, results of operations, liquidity and our future growth prospects could be materially and adversely affected.

| 1 |

| Table of Contents |

Summary of Risk Factors

Investing in our company involves significant risks. You should carefully consider all of the information in this annual report before making an investment in our company. These risks include but not limited to the following:

Risk factors relating to our business include but not limited to the following:

| ● | We face risks related to nature disasters (whether or not caused by climate change), unusually adverse weather conditions, pandemic outbreaks, in particular, the current coronavirus pandemic, terrorist acts and global political events. See a more detailed discussion of this risk factor on page 5 of this annual report. |

| ● | Our failure to compete effectively could adversely affect our market share, revenues and growth prospects. See a more detailed discussion of this risk factor on page 6 of this annual report. |

| ● | We are dependent on certain key personnel and loss of these key personnel could have a material adverse effect on our business, financial condition and results of operations. See a more detailed discussion of this risk factor on page 7 of this annual report. |

| ● | If we fail to increase our brands’ recognition, we may face difficulty in obtaining new customers. See a more detailed discussion of this risk factor on page 7 of this annual report. |

| ● | If we are unable to provide superior user experience, we may not be able to maintain or grow our user base or keep our users highly engaged. See a more detailed discussion of this risk factor on page 7 of this annual report. |

| ● | Developments in China’s automotive industry will impact our automobile sales business’s net revenues and future growth, including government regulations and policies. See a more detailed discussion of this risk factor on page 9 of this annual report. |

|

|

|

| ● | The AI industry faces its own risks and changing and extensive regulations. See a more detailed discussion of this risk factor on page 9 of this annual report. |

Risk factors relating to doing business in China include but not limited to the following:

| ● | Our business is subject to certain PRC laws and regulations. There are uncertainties regarding the interpretation and enforcement of PRC laws, rules and regulations. The uncertainty in the PRC legal system may make it difficult for us to predict the outcome of any disputes that we may be involved in. See a more detailed discussion of this risk factor on page 16 of this annual report. |

| 2 |

| Table of Contents |

| ● | In light of the greater oversight by the Cyberspace Administration of China, or CAC, over data security, we are subject to a variety of laws and other obligations regarding cybersecurity and data protection, and any failure to comply with applicable laws and obligations could have a material and adverse effect on our business, our listing on Nasdaq, financial condition and results of operations. See a more detailed discussion of this risk factor on page 17 of this annual report. |

|

|

|

| ● | The approval of the China Securities Regulatory Commission, or the CSRC, may be required in connection with an offering under PRC rules, regulations, or policies, and, if required, we cannot predict whether or how soon we will be able to obtain such approval. As a result, we fact uncertainty about future actions by the PRC government that could significantly affect our business, our listing on Nasdaq, financial condition and results of operations. See a more detailed discussion of this risk factor on page 18 of this annual report. |

|

|

|

| ● | The PRC government has significant authority to intervene or influence the China operations of an offshore holding company, such as ours, at any time. The PRC government may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers. If the PRC government exerts more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers and we were to be subject to such oversight and control, it may result in a material adverse change to our business operations, significantly limit or completely hinder our ability to offer or continue to offer securities to investors, and cause the ordinary shares to significantly decline in value or become worthless. See a more detailed discussion of this risk factor on page 19 of this annual report. |

| ● | As of March 31, 2024, our main operations and assets are located in the PRC. Shareholders may not be accorded the same rights and protection that would be accorded under the US law. In addition, it would be difficult to enforce a U.S. judgment against our PRC subsidiaries and our officers and directors. See a more detailed discussion of this risk factor on page 16 of this annual report. |

| ● | It may be difficult for overseas shareholders and/or regulators to conduct investigation or collect evidence within China. See a more detailed discussion of this risk factor on page 20 of this annual report. |

| ● | Our results and financial conditions are highly susceptible to changes in the PRC’s political, economic and social conditions as our revenue is currently wholly derived from our operations in the PRC. See a more detailed discussion of this risk factor on page 21 of this annual report. |

| ● | PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our PRC resident beneficial owners or our PRC subsidiary to liability or penalties, limit our ability to inject capital into our PRC subsidiary, limit our PRC subsidiary’s ability to increase their registered capital or distribute profits to us, or may otherwise adversely affect us. See more detailed discussion of this risk factor on page 20 of this annual report. |

| ● | PRC regulation of loans and direct investment by offshore holding companies to PRC entities may delay or prevent us from using the proceeds from the offerings of any securities to make loans or additional capital contributions to our PRC operating subsidiaries. See more detailed discussion of this risk factor on page 23 of this annual report. |

| 3 |

| Table of Contents |

| ● | Uncertainty in the interpretation of PRC tax regulations may have a negative impact on our business operations, our acquisition or restructuring strategy or the value of our investment in it. See more detailed discussion of this risk factor on page 22 of this annual report. |

| ● | Currency fluctuations and restrictions on currency exchange may adversely affect our business, including limiting our ability to convert RMB into foreign currencies and, if RMB were to decline in value, reducing our revenues and profits in U.S. dollar terms. See more detailed discussion of this risk factor on page 23 of this annual report. |

| ● | We are subject to the risks relating to the restrictions on paying dividends or making other payments to us by our subsidiaries in China. See more detailed discussion of this risk factor on page 24 of this annual report. |

Risk factors relating to our Class A Ordinary Shares include but not limited to the following:

| ● | Our Memorandum and Articles of Association afford less protection to our shareholders and may discourage claims and limit shareholders’ ability to bring claims. See more detailed discussion of this risk factor on page 25 of this annual report. |

| ● | Certain judgments obtained against us by our shareholders may not be enforceable. See more detailed discussion of this risk factor on page 25 of this annual report. |

| ● | We are an emerging growth company within the meaning of the Securities Act and may take advantage of certain reduced reporting requirements. See more detailed discussion of this risk factor on page 26 of this annual report. |

| ● | We qualify as a foreign private issuer and, as a result, we are not subject to U.S. proxy rules and are subject to Exchange Act reporting obligations that permit less detailed and less frequent reporting than that of a U.S. domestic public company. See more detailed discussion of this risk factor on page 26 of this annual report. |

| ● | As a foreign private issuer, we are permitted to adopt certain home country practices in relation to corporate governance matters that differ significantly from Nasdaq corporate governance listing standards. See more detailed discussion of this risk factor on page 27 of this annual report. |

| ● | There can be no assurance that we will not be a passive foreign investment company, or PFIC, for U.S. federal income tax purposes for any taxable year, which could result in adverse U.S. federal income tax consequences to U.S. holders of our ordinary shares. See more detailed discussion of this risk factor on page 27 of this annual report. |

| ● | We may be exposed to potential risks relating to our internal controls over financial reporting. See more detailed discussion of this risk factor on page 29 of this annual report. |

| ● | The relative lack of public company experience of our management team may put us at a competitive disadvantage. See more detailed discussion of this risk factor on page 29 of this annual report. |

| ● | Our Class A Ordinary Shares are very thinly traded, and there can be no assurance that there will be an active market for our Class A Ordinary Shares in the future. See more detailed discussion of this risk factor on page 29 of this annual report. |

| 4 |

| Table of Contents |

Risks related to Our Business

We have an evolving business model with still untested growth initiatives.

Currently, we engage in the AI-powered entertainment industry, specializing in the development of AI-driven games and applications to deliver immersive and engaging entertainment experiences. We have executed a strategic transition to streamline our operations and concentrate on our core competencies in providing AI-powered solutions. In connection with our transition, we consummated an acquisition of 100% of 2lab3, through which, we expanded our business into the AI and entertainment industries. Then, we suspended our e-commerce and internet information and advertising businesses in September 2023. In addition, in July 2024, we ceased our automobile sales business.

We have an evolving business model and intend to implement new strategies to grow our business in the future. There can be no assurance that we will be successful in developing new product categories or in entering new specialty markets or in implementing any other growth strategies. Similarly, there can be no assurance that we already have or will be able to obtain or retain any employees, consultants or other resources with any specialized skills or relationships to successfully implement our strategies for our business in the future.

2lab3 is a recently formed entity with little track record and limited historical financial information available.

Because 2lab3 is in the early stages of executing the business strategy, we cannot provide assurance that, or when, our AI entertainment business will be profitable. We will need to make significant investments to develop and operate 2lab3 and expect to incur significant expenses in connection with operating components, including costs for developing technology, talent fees, marketing, and salaries. We expect to incur significant capital, operational and marketing expenses for a few years in connection with our strategy and growth plan. Any failure to achieve or sustain profitability may have a material adverse impact on the value of our Class A Ordinary Shares.

The AI industry faces its own risks and changing and extensive regulations.

We are incorporating AI technology into our product. 2lab3 is planning to launch SimTwin, a platform where users can create an interactive “digital twin” of their beloved ones. SimTim will use generative AI tools to improve its content creation and production efficiency.

As with most emerging technologies, AI comes with its own set of risks and challenges that could affect its adoption and our business. AI algorithms may be flawed, and the data used could be incomplete or biased. Inappropriate or controversial data practices, by us or by others, could limit the acceptance of our AI-enhanced products and content. Certain AI applications could trigger ethical issues. Should our AI-powered product become controversial due to their effects on human rights, privacy, employment, or other social matters, we risk reputational harm or legal repercussions. In addition, uncertainties regarding the development and application of AI technology present a potential risk. There remains the possibility that AI technology may not progress as anticipated or deliver expected benefits, which could limit the acceptance and popularity of our AI-powered product.

The development and adoption of generative AI technologies are still in their early stages, and their commercial viability is uncertain. There is a risk that the demand for connectivity solutions for such technologies may not meet our expectations or that market acceptance may be slower than anticipated. Failure to achieve widespread acceptance and generate significant revenues from generative AI technologies could negatively impact our financial condition and results of operations.

Furthermore, there are uncertainties around the ownership and intellectual property protection of AI generated content (“AIGC”) products. Using AIGC tools could also lead to potential copyright infringement and other legal challenges. If we are unable to secure the needed permissions or licenses for using AI tools—whether because we cannot identify the rights holder or for any other reason—we might infringe on others’ rights which could lead to monetary claims, fines, penalties, or less content for our users.

The regulatory landscape surrounding generative AI technologies is evolving, and there is currently significant uncertainty as to whether governmental authorities, self-regulatory institutions or other regulatory authorities will take additional action to curtail the development or use of generative AI technologies. Moreover, laws, regulations or industry standards that develop in response to generative AI technologies may be burdensome or may prohibit the deployment of generative AI technologies for one or more uses, any of which could result in lower than anticipated demand for our product.

Our efforts and investments in technology development may not always produce the expected results.

We are continually developing and seeking to develop technologies that are closely related to AI that will be used in our services. As of the date of this annual report, our core research and development team consisted of a total of three employees. We cannot assure you that our future efforts to develop related technologies will be successful, in which case our products may lose their competitive edge.

In addition, we cannot assure you that the technologies we develop will be well accepted by customers, in which case our business, financial condition, results of operations and prospects may be materially and adversely affected.

We may be unable to continue as a going concern.

Our audited financial statements have been prepared on a going concern basis under which an entity is considered to be able to realize its assets and satisfy its liabilities in the ordinary course of business. The assessment of our ability to continue as a going concern and to raise sufficient funds to pay for our ongoing operating expenditures and meet our liabilities for the ensuing year involves significant judgment based on historical experience and other factors, including expectation of future events that are believed to be reasonable under the circumstances. Our future operations are dependent upon the identification and successful completion of equity or debt financings and the achievement of profitable operations at an indeterminate time in the future. There can be no assurances that we will be successful in completing equity or debt financings or in achieving profitability.

We face risks related to nature disasters (whether or not caused by climate change), unusually adverse weather conditions, pandemic outbreaks, in particular, the current coronavirus pandemic, terrorist acts and global political events, all of which could result in adverse effects to our business and financial performance.

The occurrence of one or more natural disasters, such as hurricanes, fires, floods and earthquakes (whether or not caused by climate change), unusually adverse weather conditions, pandemic outbreaks, terrorist acts or disruptive global political events, could adversely affect our operations and financial performance.

On March 11, 2020, the World Health Organization declared the outbreak of COVID-19 a global pandemic. The COVID-19 pandemic had severely impacted China and the rest of the world, and resulted in quarantines, travel restrictions, the temporary closure of offices and facilities and cancelation of public activities, among others. In the year ended March 31, 2022, more than 80% of the company’s suppliers and customers experienced lockdowns in different levels. At least 30% of the Company’s revenue was affected due to the constant spread of COVID-19 which increased costs and expenses. The Company had to close seven experience stores in 2022 due to the travel restrictions and lockdowns. The Company’s e-commerce sales were also negatively impacted as the logistics and delivery services were impaired.

| 5 |

| Table of Contents |

Many of the restrictive measures previously adopted by the PRC governments at various levels to control the spread of the COVID-19 virus have been revoked or replaced with more flexible measures since December 2022. COVID-19 did not have material impact on our results of operation and financial conditions for the years ended March 31, 2024 and 2023.

However, with the uncertainties surrounding the COVID-19 outbreak, the threat to our business disruption and the related financial impact remains. Our business, results of operations, financial condition and prospects could be materially adversely affected to the extent that COVID-19 persists in China or harms the Chinese and global economy in general.

We may not effectively manage our growth, which could materially harm our business.

We expect that our business will continue to grow, which may place a significant strain on our management, personnel, systems and resources. We must continue to improve our operational and financial systems and managerial controls and procedures, and we will need to continue to expand, train and manage our technology and workforce. We must also maintain close coordination among our compliance, accounting, finance, marketing and sales organizations. We cannot assure you that we will manage our growth effectively. If we fail to do so, our business could be materially harmed.

Our continued growth will require an increased investment by us in technology, facilities, personnel and financial and management systems and controls. It also will require expansion of our procedures for monitoring and assuring our compliance with applicable regulations, and we will need to integrate, train and manage a growing employee base. The expansion of our existing businesses, any expansion into new businesses and the resulting growth of our employee base will increase our need for internal audit and monitoring processes that are more extensive and broader in scope than those we have historically required. Further, unless our growth results in an increase in our revenues that is proportionate to the increase in our costs associated with this growth, our operating margins and profitability will be adversely affected.

We are dependent on certain key personnel and loss of these key personnel could have a material adverse effect on our business, financial condition and results of operations.

Our success is, to a certain extent, attributable to the management, sales and marketing, and research and development expertise of key personnel. We are dependent upon the services of experienced personal and technicians, there can be no assurance that we will be able to recruit and retain qualified management team and skillful labor, due to labor market competition. The loss of these officers could have a material adverse effect upon our business, financial condition, and results of operations.

We may not be able to hire and retain qualified personnel to support our growth and if we are unable to retain or hire these personnel in the future, our ability to improve our products and implement our business objectives could be adversely affected.

We must attract, recruit and retain a sizeable workforce of technically competent employees. Competition for senior management and personnel in the PRC is intense and the pool of qualified candidates in the PRC is very limited. We may not be able to retain the services of our senior executives or personnel, or attract and retain high-quality senior executives or personnel in the future. This failure could materially and adversely affect our future growth and financial condition.

If we fail to increase our brands’ recognition, we may face difficulty in obtaining new customers.

We believe that maintaining and enhancing our brand recognition in a cost-effective manner outside of that market is critical to achieving widespread acceptance of our current and future products and services and is an important element in our effort to increase our customer base. Successful promotion of our brand will depend largely on our ability to maintain a sizeable and active customer base, our marketing efforts and ability to provide reliable and useful products and services at competitive prices. Brand promotion activities may not yield increased revenue, and even if they do, any increased revenue may not offset the expenses we will incur in building our brand. If we fail to successfully promote and maintain our brands, or if we incur substantial expenses in an unsuccessful attempt to promote and maintain our brand, we may fail to attract enough new customers or retain our existing customers to the extent necessary to realize a sufficient return on our brand-building efforts, in which case our business, operating results and financial condition, would be materially adversely affected.

If we are unable to provide superior user experience, we may not be able to maintain or grow our customer base or keep our customers highly engaged. As a result, our revenues, profitability and business prospects may be materially and adversely affected.

The success of our business largely depends on our ability to provide superior user experience in order to maintain and grow our user base and keep our customers highly engaged on our online platform, which in turn depends on a variety of factors. These factors include our ability to continue to offer attractive and relevant content in engaging formats, source quality merchants to respond to user demands and preferences, maintain the quality of our products and services, provide reliable and user-friendly features for our users to browse for content and products, and provide high-quality customer service. If our users are not satisfied with our content, products or services, or our platform is severely interrupted or otherwise fail to meet our users’ requests, our reputation and user loyalty could be adversely affected.

In addition, if users cannot obtain satisfactory customer services after they purchase products with us, our brand and user loyalty may be adversely affected. Any negative publicity or poor feedback regarding our customer service may harm our brand and reputation and in turn cause us to lose users and market share.

As a result, if we are unable to continue to maintain our user experience and provide high-quality customer service, we may not be able to retain or attract users or keep them highly engaged with the content and products we offer on our platform, which may have a material adverse effect on our business, financial condition and results of operations.

| 6 |

| Table of Contents |

We rely extensively on information technology systems, and cybersecurity incidents could adversely affect us.

We rely on information technology systems and infrastructure to connect with clients, people and others, and to store and process business and financial data. Increased cybersecurity threats and attacks, including computer viruses, hacking and ransomware attacks, are constantly evolving and pose a risk to our systems and networks. Security breaches, improper use of our systems and unauthorized access to our data and information by employees and others may pose a risk that sensitive data may be exposed to unauthorized persons or to the public. We also have access to sensitive or personal data or information that is subject to privacy laws and regulations. Our systems and processes may be unable to prevent material security breaches, and such breaches could adversely affect our business, results of operations, financial position and reputation.

Our success depends on our ability to protect our intellectual property. However, we may not be able to adequately protect our intellectual property rights, and any failure to protect our intellectual property rights could adversely affect our revenues and competitive position.

We rely on copyright and trade secret laws, confidentiality procedures, controls and contractual commitments to protect our intellectual property. Despite our efforts, these protections may be limited. Unauthorized third parties may try to copy or reverse engineer our products or otherwise use our intellectual property. Our patents may be invalidated or circumvented. Any of our pending or future patent applications may not be issued with the claim scope we seek, if at all. In addition, the laws of some countries do not provide the same level of intellectual property protection as U.S. laws and courts. If we cannot protect our intellectual property against unauthorized copying or use, or other misappropriation, we may not remain competitive.

It is possible that third parties, including our competitors, may develop similar technology to ours that overlap or compete with our technology. If we are unable to adequately protect our intellectual property and other proprietary rights, our competitive position and our business could be harmed. Furthermore, changes to intellectual property laws may jeopardize the enforceability and validity of our existing intellectual property portfolio and harm our ability to obtain protection for future intellectual property rights.

In addition, we cannot assure you that we will be able to maintain consumer value in our copyrights or other intellectual property rights in our technologies, designs, software and innovations. The measures we take to protect our intellectual property rights may not provide us with a competitive advantage and our competitive position and our business could be harmed. Any of our owned or licensed intellectual property rights could be challenged, invalidated, circumvented, infringed, misappropriated or otherwise violated, our confidential information could be disclosed in an unauthorized manner to third parties, or our intellectual property rights may not be sufficient to permit us to take advantage of current market trends, which could result in competitive harm.

| 7 |

| Table of Contents |

Risks Related to Doing Business in China

Joint statement by the SEC and the PCAOB, rule changes by Nasdaq, and the HFCA Act all call for additional and more stringent criteria to be applied to emerging market companies upon assessing the qualification of their auditors, especially the non-U.S. auditors who are not inspected by the PCAOB.

On May 20, 2020, the U.S. Senate passed the HFCA Act requiring a foreign company to certify it is not owned or controlled by a foreign government if the PCAOB is unable to audit specified reports because the company uses a foreign auditor not subject to PCAOB inspection. If the PCAOB is unable to inspect the company’s auditors for three consecutive years, the issuer’s securities are prohibited to trade on a national exchange. On December 2, 2020, the U.S. House of Representatives approved the HFCA Act. On December 18, 2020, the HFCA Act was signed into law.

On September 22, 2021, the PCAOB adopted a final rule implementing the HFCA Act, which provides a framework for the PCAOB to use when determining, as contemplated under the HFCA Act, whether the board of directors of a company is unable to inspect or investigate completely registered public accounting firms located in a foreign jurisdiction because of a position taken by one or more authorities in that jurisdiction.

On December 16, 2021, the PCAOB issued a report on its determinations that it is unable to inspect or investigate completely PCAOB-registered public accounting firms headquartered in mainland China and in Hong Kong because of positions taken by PRC and Hong Kong authorities in those jurisdictions.

On August 26, 2022, the CSRC, China’s Ministry of Finance, and the PCAOB signed the SOP Agreements governing inspections and investigations of audit firms based in mainland China and Hong Kong, taking the first step toward opening access for the PCAOB to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong. Pursuant to the fact sheet with respect to the SOP Agreements disclosed by the SEC, the PCAOB shall have independent discretion to select any issuer audits for inspection or investigation and has the unfettered ability to transfer information to the SEC. On December 15, 2022, the PCAOB determined that the PCAOB was able to secure complete access to inspect and investigate registered public accounting firms headquartered in mainland China and Hong Kong and voted to vacate its previous determinations to the contrary. However, should PRC authorities obstruct or otherwise fail to facilitate the PCAOB’s access in the future, the PCAOB will consider the need to issue a new determination.

As an auditor of companies that are registered with the SEC and publicly traded in the United States and a firm registered with the PCAOB, our auditor is required under the laws of the United States to undergo regular inspections by the PCAOB to assess their compliance with the laws of the United States and professional standards.

Historically, we operated substantially in mainland China, a jurisdiction where the PCAOB is currently unable to conduct inspections without the approval of the Chinese government authorities, our current and previous auditors, Enrome LLP and TPS Thayer LLC, two independent registered public accounting firms that issues the audit report included elsewhere in this annual report, are both subject to laws in the United States pursuant to which the PCAOB conducts regular inspections to assess our auditors’ compliance with the applicable professional standards. Enrome LLP is headquartered in Singapore and can be inspected by the PCAOB on a regular basis. TPS Thayer LLC is headquartered in Sugar Land, Texas and has also been inspected by the PCAOB on a regular basis. Neither Enrome LLP or TPS Thayer LLC had been subject to the determinations announced by the PCAOB on December 16, 2021. However, in the event it is later determined that the PCAOB is unable to inspect or investigate completely our auditor because of a position taken by an authority in a foreign jurisdiction, then such lack of inspection could cause trading in our securities to be prohibited under the HFCA Act, and ultimately result in a determination by the Nasdaq to delist our securities. Delisting of our Class A Ordinary Shares would force holders of our Class A Ordinary Shares to sell their Class A Ordinary Shares. The market price of our Class A Ordinary Shares could be adversely affected as a result of anticipated negative impacts of these executive or legislative actions upon, as well as negative investor sentiment towards, companies with significant operations in China that are listed in the United States, regardless of whether these executive or legislative actions are implemented and regardless of our actual operating performance.

| 8 |

| Table of Contents |

Our business is subject to certain PRC laws and regulations. There are uncertainties regarding the interpretation and enforcement of PRC laws, rules and regulations. The uncertainty in the PRC legal system may make it difficult for us to predict the outcome of any disputes that we may be involved in.

The PRC legal system is based on the PRC Constitution and is made up of written laws, regulations, circulars and directives. The PRC government is still in the process of developing its legal system, so as to meet the needs of investors and to encourage foreign investment. As the PRC economy is generally developing at a relative faster pace than its legal system, some degree of uncertainty exists in connection with whether and how existing laws and regulations will apply to certain events or circumstances.

Some of the laws and regulations, and the interpretation, implementation and enforcement thereof, are still subject to policy changes. There is no assurance that the introduction of new laws, changes to existing laws and the interpretation or application thereof or the delays in obtaining approvals from the relevant authorities will not have an adverse impact on our PRC subsidiaries’ business, financial performance and prospects.

Further, precedents on the interpretation, implementation and enforcement of the PRC laws and regulations are limited, and unlike other common law countries such as the United States, decisions on precedent cases are not binding on lower courts. As such, the outcome of dispute resolutions may not be consistent or predictable as in the other more developed jurisdictions and it may be difficult to obtain swift or equitable enforcement of the laws in the PRC, or obtain enforcement of judgment by a court of another jurisdiction.

In addition, the PRC government has recently announced its plans to enhance its regulatory oversight of Chinese companies listing overseas. The “Opinions on Intensifying Crack Down on Illegal Securities Activities” issued on July 6, 2021 called for:

| ● | tightening oversight of data security, cross-border data flow and administration of classified information, as well as amendments to relevant regulation to specify responsibilities of overseas listed Chinese companies with respect to data security and information security; |

| ● | enhanced oversight of overseas listed companies as well as overseas equity fundraising and listing by Chinese companies; and |

| ● | extraterritorial application of China’s securities laws. |

| 9 |

| Table of Contents |

As the Opinions on Intensifying Crack Down on Illegal Securities Activities were recently issued, there are great uncertainties with respect to the interpretation and implementation thereof. The Chinese government may promulgate relevant laws, rules and regulations that may impose additional and significant obligations and liabilities on overseas listed Chinese companies regarding data security, cross-border data flow, and compliance with China’s securities laws. It is uncertain whether or how these new laws, rules and regulations and the interpretation and implementation thereof may affect us, but among other things, our ability and the ability of our subsidiaries to obtain external financing through the issuance of equity securities overseas could be negatively affected.

In light of the greater oversight by the Cyberspace Administration of China, or CAC, over data security, we are subject to a variety of laws and other obligations regarding cybersecurity and data protection, and any failure to comply with applicable laws and obligations could have a material and adverse effect on our business, our listing on Nasdaq, financial condition and results of operations.

We are subject to PRC laws relating to the collection, use, sharing, retention, security, and transfer of confidential and private information, such as personal information and other data. Our compliance obligations include those relating to the Data Protection Act (As revised) of the Cayman Islands and the relevant PRC laws in this regard. These PRC laws apply not only to third-party transactions, but also to transfers of information between us and our subsidiaries, and among us, our subsidiaries, and other parties with which we have commercial relations. These laws continue to develop, and the PRC government may adopt other rules and restrictions in the future. Non-compliance could result in penalties or other significant legal liabilities.

Pursuant to the PRC Cybersecurity Law, which was promulgated by the Standing Committee of the National People’s Congress on November 7, 2016 and took effect on June 1, 2017, personal information and important data collected and generated by a critical information infrastructure operator in the course of its operations in China must be stored in China, and if a critical information infrastructure operator purchases internet products and services that affects or may affect national security, it should be subject to cybersecurity review by the CAC. Due to the lack of further interpretations, the exact scope of “critical information infrastructure operator” remains unclear. On December 28, 2021, the CAC and other relevant PRC governmental authorities jointly promulgated the Cybersecurity Review Measures (the “new Cybersecurity Review Measures”) to replace the original Cybersecurity Review Measures. The new Cybersecurity Review Measures took effect on February 15, 2022. Pursuant to the new Cybersecurity Review Measures, if critical information infrastructure operators purchase network products and services, or network platform operators conduct data processing activities that affect or may affect national security, they will be subject to cybersecurity review. A network platform operator holding more than one million users/users’ individual information also shall be subject to cybersecurity review before listing abroad. The cybersecurity review will evaluate, among others, the risk of critical information infrastructure, core data, important data, or a large amount of personal information being influenced, controlled or maliciously used by foreign governments and network information security risk in connection with the overseas listing. As of today, we have not received any inquiry, notice, warning, or sanctions regarding our corporate structure from the CSRC, CAC or any other PRC governmental agency. As of today, we have not received any inquiry, notice, warning, or sanctions regarding our corporate structure from the CSRC, CAC or any other PRC governmental agency. As advised by our PRC counsel, Jingtian & Gongcheng LLP, we are unlikely to be subject to cybersecurity review, because: (i) we have not received any notice from governmental agency to treat us as an operator of critical information infrastructure, and (ii) we have not received any notice from governmental agency to treat us as an online platform operator who possesses personal information of more than one million users. In addition, we currently do not have over one million users’ personal information. If we ever became subject to the cybersecurity review of CAC in the future as the applicable rules, regulations, policies or the interpretation thereof change, during such review, we may be required to suspend our operation or experience other disruptions to our operations. Cybersecurity review could also result in negative publicity with respect to our company and diversion of our managerial and financial resources.

Furthermore, if we were found to be in violation of applicable laws and regulations in China during such review, we could be subject to administrative penalties, such as warnings, fines, or service suspension. Therefore, cybersecurity review could materially and adversely affect our business, financial condition, and results of operations.

In addition, the PRC Data Security Law, which was promulgated by the Standing Committee of the National People’s Congress on June 10, 2021 and took effect on September 1, 2021, requires data collection to be conducted in a legitimate and proper manner, and stipulates that, for the purpose of data protection, data processing activities must be conducted based on data classification and hierarchical protection system for data security. As the Data Security Law was recently promulgated, we may be required to make further adjustments to our business practices to comply with this law. If our data processing activities were found to be not in compliance with this law, we could be ordered to make corrections, and under certain serious circumstances, such as severe data divulgence, we could be subject to penalties, including the revocation of our business licenses or other permits. Furthermore, the recently issued Opinions on Strictly Cracking Down Illegal Securities Activities in Accordance with the Law require (i) speeding up the revision of the provisions on strengthening the confidentiality and archives management relating to overseas issuance and listing of securities and (ii) improving the laws and regulations relating to data security, cross-border data flow, and management of confidential information. As there remain uncertainties regarding the further interpretation and implementation of those laws and regulations, we cannot assure you that we will be compliant such new regulations in all respects, and we may be ordered to rectify and terminate any actions that are deemed illegal by the regulatory authorities and become subject to fines and other sanctions. As a result, we may be required to suspend our relevant e-commerce businesses, including our internet information and advertising services, and automobile sale business, shut down our website and online platform, take down our operating application, or face other penalties, which may materially and adversely affect our business, financial condition, and results of operations.

| 10 |

| Table of Contents |

On August 20, 2021, the Standing Committee of the National People’s Congress of China promulgated the Personal Information Protection Law of the PRC, or the PIPL, which took effect in November 2021. As the first systematic and comprehensive law specifically for the protection of personal information in the PRC, the PIPL provides, among others, that (i) an individual’s consent shall be obtained to use sensitive personal information, such as biometric characteristics and individual location tracking, (ii) personal information operators using sensitive personal information shall notify individuals of the necessity of such use and impact on the individual’s rights, and (iii) where personal information operators reject an individual’s request to exercise his or her rights, the individual may file a lawsuit with a People’s Court. As uncertainties remain regarding the interpretation and implementation of the PIPL, we cannot assure you that we will comply with the PIPL in all respects, we may become subject to fines and/or other penalties which may have material adverse effect on our business, operations and financial condition.

While we take measures to comply with all applicable data privacy and protection laws and regulations, we cannot guarantee the effectiveness of the measures undertaken by us and our business partners. However, compliance with any additional laws could be expensive, and may place restrictions on our business operations and the manner in which we interact with our users. In addition, any failure to comply with applicable cybersecurity, privacy, and data protection laws and regulations could result in proceedings against us by government authorities or others, including notification for rectification, confiscation of illegal earnings, fines, or other penalties and legal liabilities against us, which could materially and adversely affect our business, financial condition, and results of operations, and the value of our Class A Ordinary Shares. In addition, any negative publicity on our website or platform’s safety or privacy protection mechanism and policy could harm our public image and reputation and materially and adversely affect our business, financial condition, and results of operations.

The approval of the China Securities Regulatory Commission, or the CSRC, may be required in connection with an offering under PRC rules, regulations, or policies, and, if required, we cannot predict whether or how soon we will be able to obtain such approval. As a result, both you and us fact uncertainty about future actions by the PRC government that could significantly affect our business, our listing on Nasdaq, financial condition and results of operations.

On August 8, 2006, six PRC regulatory agencies, including the MOFCOM, the State-Owned Assets Supervision and Administration Commission, or the SASAC, the SAT, the State Administration for Industry and Commerce, or the SAIC, the CSRC, and the State Administration of Foreign Exchange, or the SAFE, jointly adopted the Regulations on Mergers and Acquisitions of Domestic Enterprises by Foreign Investors, or the M&A Rules, which came into effect on September 8, 2006 and were amended on June 22, 2009. The M&A Rules include, among other things, provisions that purport to require that an offshore special purpose vehicle that is controlled by PRC domestic companies or individuals and that has been formed for the purpose of an overseas listing of securities through acquisitions of PRC domestic companies or assets to obtain the approval of the CSRC prior to the listing and trading of such special purpose vehicle’s securities on an overseas stock exchange. On September 21, 2006, the CSRC published on its official website procedures regarding its approval of overseas listings by special purpose vehicles. However, substantial uncertainty remains regarding the scope and applicability of the M&A Rules to offshore special purpose vehicles.

While the application of the M&A Rules remains unclear, we believe, based on the advice of our PRC legal counsel, Jingtian & Gongcheng LLP, that the CSRC approval is not required for the listing and trading our Class A Ordinary Shares on the Nasdaq Capital Market because our WFOE was incorporated as a foreign-invested enterprise by means of foreign direct investments rather than by merger with or acquisition of any PRC domestic companies as defined under the M&A Rules. There can be no assurance that the relevant PRC government agencies, including the CSRC, would reach the same conclusion as our PRC legal counsel. If the CSRC or other PRC regulatory body subsequently determines that we need to obtain the CSRC’s approval for our offering or if the CSRC or any other PRC government authorities promulgates any interpretation or implements rules that would require us to obtain CSRC or other governmental approvals for our offering, we may face adverse actions or sanctions by the CSRC or other PRC regulatory agencies. In any such event, these regulatory agencies may impose fines and penalties on our operations in China, limit our operating privileges in China, delay or restrict the repatriation of the proceeds from our offerings into the PRC, restrictions on or prohibition of the payments or remittance of dividends by our subsidiaries in China, or other actions that could have a material and adverse effect on our business, reputation, financial condition, results of operations, prospects, as well as the trading price of the Class A Ordinary Shares. The CSRC or other PRC regulatory agencies may also take actions requiring us, or making it advisable for us, to halt our offering before settlement and delivery of the Class A Ordinary Shares that we are offering. Consequently, if you engage in market trading or other activities in anticipation of and prior to settlement and delivery, you would be doing so at the risk that the settlement and delivery may not occur. In addition, if the CSRC or other regulatory agencies later promulgate new rules or explanations requiring us to obtain their approvals for our offering, we may be unable to obtain waivers of such approval requirements. Any uncertainties or negative publicity regarding such approval requirements could materially and adversely affect the trading price of our Class A Ordinary Shares.

| 11 |

| Table of Contents |

Recently, the PRC government adopted a series of regulatory actions and issued statements to regulate business operations in China with little advance notice, including cracking down on illegal activities in the securities market, adopting new measures to extend the scope of cybersecurity reviews, and expanding the efforts in anti-monopoly enforcement. As of the date of this annual report, as advised by our PRC counsel, Jingtian & Gongcheng LLP, we and our subsidiaries, (1) are not subject to permission requirements from the CAC or any other entity that is required to approve of our PRC subsidiaries’ operations, and (2) have not received or were denied such permissions by any PRC authorities. Nevertheless, the General Office of the Central Committee of the Communist Party of China and the General Office of the State Council jointly issued the “Opinions on Severely Cracking Down on Illegal Securities Activities According to Law,” or the Opinions, which were made available to the public on July 6, 2021. The Opinions emphasized the need to strengthen the administration over illegal securities activities, and the need to strengthen the supervision over overseas listings by Chinese companies. Given the current PRC regulatory environment, it is uncertain when and whether we or our PRC subsidiaries, will be required to obtain permission from the PRC government to list on U.S. exchanges in the future, and even when such permission is obtained, whether it will be denied or rescinded. We have been closely monitoring regulatory developments in China regarding any necessary approvals from the CSRC or other PRC governmental authorities required for overseas listings. As of the date of this annual report, we have not received any inquiry, notice, warning, sanctions or regulatory objection to this offering from the CSRC or other PRC governmental authorities. However, there remains significant uncertainty as to the enactment, interpretation and implementation of regulatory requirements related to overseas securities offerings and other capital markets activities.

On February 17, 2023, the CSRC promulgated the Trial Administrative Measures of Overseas Securities Offering and Listing by Domestic Companies (the “Trial Measures”), which will take effect on March 31, 2023. The Trial Measures clarified and emphasized several aspects, which include but are not limited to: (1) comprehensive determination of the “indirect overseas offering and listing by PRC domestic companies” in compliance with the principle of “substance over form” and particularly, an issuer will be required to go through the filing procedures under the Trial Measures if the following criteria are met at the same time: a) 50% or more of the issuer’s operating revenue, total profit, total assets or net assets as documented in its audited consolidated financial statements for the most recent accounting year is accounted for by PRC domestic companies, and b) the main parts of the issuer’s business activities are conducted in mainland China, or its main places of business are located in mainland China, or the senior managers in charge of its business operation and management are mostly Chinese citizens or domiciled in mainland China; (2) exemptions from immediate filing requirements for issuers that a) have already been listed or registered but not yet listed in foreign securities markets, including U.S. markets, prior to the effective date of the Trial Measures, and b) are not required to re-perform the regulatory procedures with the relevant overseas regulatory authority or the overseas stock exchange, c) whose such overseas securities offering or listing shall be completed before September 30, 2023, provided however that such issuers shall carry out filing procedures as required if they conduct refinancing or are involved in other circumstances that require filing with the CSRC; (3) a negative list of types of issuers banned from listing or offering overseas, such as (a) issuers whose listing or offering overseas have been recognized by the State Council of the PRC as possible threats to national security, (b) issuers whose affiliates have been recently convicted of bribery and corruption, (c) issuers under ongoing criminal investigations, and (d) issuers under major disputes regarding equity ownership; (4) issuers’ compliance with web security, data security, and other national security laws and regulations; (5) issuers’ filing and reporting obligations, such as obligation to file with the CSRC after it submits an application for initial public offering to overseas regulators, and obligation after offering or listing overseas to report to the CSRC material events including change of control or voluntary or forced delisting of the issuer; and (6) the CSRC’s authority to fine both issuers and their shareholders between 1 and 10 million RMB for failure to comply with the Trial Measures, including failure to comply with filing obligations or committing fraud and misrepresentation. As of the date of this annual report, as advised by our PRC counsel, Jingtian & Gongcheng LLP, for any future follow-on offerings of our securities, we should submit filing materials to the CSRC within three working days after the completion of such offering. The required filing materials shall include, but not be limited to, (1) filing report and relevant commitment letter and (2) legal opinions by our local counsel.

The PRC government has significant authority to intervene or influence the China operations of an offshore holding company, such as ours, at any time. The PRC government may exert more control over offerings conducted overseas and/or foreign investment in China-based issuers. If the PRC government exerts more oversight and control over offerings that are conducted overseas and/or foreign investment in China-based issuers and we were to be subject to such oversight and control, it may result in a material adverse change to our business operations, significantly limit or completely hinder our ability to offer or continue to offer securities to investors, and cause the ordinary shares to significantly decline in value or become worthless.

Our business, prospects, financial condition, and results of operations may be influenced to a significant degree by political, economic, and social conditions in China generally. The PRC government has significant authority to intervene or influence the China operations of an offshore holding company at any time, which could result in a material adverse change to our operations and the value of the ordinary shares.

Furthermore, given recent statements by the Chinese government indicating an intent to exert more oversight and control over offerings that are conducted overseas, although we are currently not required to obtain permission from any of the PRC federal or local government and has not received any denial to list on the U.S. exchange, it is uncertain whether or when we might be required to obtain permission from the PRC government to list on U.S. exchanges in the future. Even if such permission is obtained, it is uncertain whether it will be later denied or rescinded, which could significantly limit or completely hinder our ability to offer or continue to offer our securities to investors and result in a material adverse change to our business operations, and damage our reputation, therefore, cause the value of our shares to significantly decline or be worthless.

We have limited insurance coverage for our operations in China.

The insurance industry in China is still at an early stage of development. Insurance companies in China offer limited insurance products. We have determined that the risks of disruption or liability from our business, the loss or damage to our property, including our facilities, equipment and office furniture, the cost of insuring for these risks, and the difficulties associated with acquiring such insurance on commercially reasonable terms make it impractical for us to have such insurance. As a result, we do not have any business liability, disruption, litigation or property insurance coverage for our operations in China except for insurance on some company owned vehicles. Any uninsured occurrence of loss or damage to property, or litigation or business disruption may result in the incurrence of substantial costs and the diversion of resources, which could have an adverse effect on our operating results.

| 12 |

| Table of Contents |

It may be difficult for overseas shareholders and/or regulators to conduct investigation or collect evidence within China.

Shareholder claims or regulatory investigation that are common in the United States generally are difficult to pursue as a matter of law or practicality in China. For example, in China, there are significant legal and other obstacles to providing information needed for regulatory investigations or litigation initiated outside China. Although the authorities in China may establish a regulatory cooperation mechanism with the securities regulatory authorities of another country or region to implement cross-border supervision and administration, such cooperation with the securities regulatory authorities in the Unities States may not be efficient in the absence of mutual and practical cooperation mechanism. Furthermore, according to Article 177 of the PRC Securities Law, or Article 177, which became effective in March 2020, no overseas securities regulator is allowed to directly conduct investigation or evidence collection activities within the territory of the PRC. While detailed interpretation of or implementation rules under Article 177 have yet to be promulgated, the inability for an overseas securities regulator to directly conduct investigation or evidence collection activities within China may further increase difficulties faced by you in protecting your interests.

Our principal business operation is conducted in the PRC. In the event that the U.S. regulators carry out investigation on us and there is a need to conduct investigation or collect evidence within the territory of the PRC, the U.S. regulators may not be able to carry out such investigation or evidence collection directly in the PRC under the PRC laws. The U.S. regulators may consider cross-border cooperation with securities regulatory authority of the PRC by way of judicial assistance, diplomatic channels or regulatory cooperation mechanism established with the securities regulatory authority of the PRC.

PRC regulations relating to the establishment of offshore special purpose companies by PRC residents may subject our PRC resident beneficial owners or our PRC subsidiary to liability or penalties, limit our ability to inject capital into our PRC subsidiary, limit our PRC subsidiary’s ability to increase their registered capital or distribute profits to us, or may otherwise adversely affect us.

In July 2014, SAFE promulgated the Circular on Relevant Issues Concerning Foreign Exchange Control on Domestic Residents’ Offshore Investment and Financing and Roundtrip Investment Through Special Purpose Vehicles, or SAFE Circular 37, to replace the Notice on Relevant Issues Concerning Foreign Exchange Administration for Domestic Residents’ Financing and Roundtrip Investment Through Offshore Special Purpose Vehicles, or SAFE Circular 75, which ceased to be effective upon the promulgation of SAFE Circular 37. SAFE Circular 37 requires PRC residents (including PRC individuals and PRC corporate entities) to register with SAFE or its local branches in connection with their direct or indirect offshore investment activities. SAFE Circular 37 is applicable to our shareholders who are PRC residents and may be applicable to any offshore acquisitions that we make in the future.

Under SAFE Circular 37, PRC residents who make, or have prior to the implementation of SAFE Circular 37 made, direct or indirect investments in offshore SPVs will be required to register such investments with the SAFE or its local branches. In addition, any PRC resident who is a direct or indirect shareholder of a SPV is required to update its filed registration with the local branch of SAFE with respect to that SPV, to reflect any material change. Moreover, any subsidiary of such SPV in China is required to urge the PRC resident shareholders to update their registration with the local branch of SAFE. If any PRC shareholder of such SPV fails to make the required registration or to update the previously filed registration, the subsidiary of such SPV in China may be prohibited from distributing its profits or the proceeds from any capital reduction, share transfer or liquidation to the SPV, and the SPV may also be prohibited from making additional capital contributions into its subsidiary in China. On February 13, 2015, the SAFE promulgated a Notice on Further Simplifying and Improving Foreign Exchange Administration Policy on Direct Investment, or SAFE Notice 13, which became effective on June 1, 2015. Under SAFE Notice 13, applications for foreign exchange registration of inbound foreign direct investments and outbound overseas direct investments, including those required under SAFE Circular 37, will be filed with qualified banks instead of the SAFE. The qualified banks will directly examine the applications and accept registrations under the supervision of the SAFE.

| 13 |

| Table of Contents |

We cannot assure you that all of our shareholders that may be subject to SAFE regulations have completed all necessary registrations with the local SAFE branch or qualified banks as required by SAFE Circular 37, and we cannot assure you that these individuals may continue to make required filings or updates in a timely manner, or at all. We can provide no assurance that we are or will in the future continue to be informed of identities of all PRC residents holding direct or indirect interest in our company. Any failure or inability by such individuals to comply with the SAFE regulations may subject us to fines or legal sanctions, such as restrictions on our cross-border investment activities or our PRC subsidiary’s ability to distribute dividends to, or obtain foreign exchange-denominated loans from, our company or prevent us from making distributions or paying dividends. As a result, our business operations and our ability to make distributions to you could be materially and adversely affected.

Furthermore, as these foreign exchange regulations are still relatively new and their interpretation and implementation has been constantly evolving, it is unclear how these regulations, and any future regulation concerning offshore or cross-border transactions, will be interpreted, amended and implemented by the relevant government authorities. For example, we may be subject to a more stringent review and approval process with respect to our foreign exchange activities, such as remittance of dividends and foreign-currency-denominated borrowings, which may adversely affect our financial condition and results of operations. In addition, if we decide to acquire a PRC domestic company, we cannot assure you that we or the owners of such company, as the case may be, will be able to obtain the necessary approvals or complete the necessary filings and registrations required by the foreign exchange regulations. This may restrict our ability to implement our acquisition strategy and could adversely affect our business and prospects.

Our results and financial conditions are highly susceptible to changes in the PRC’s political, economic and social conditions as our revenue is currently wholly derived from our operations in the PRC.