UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

FOR THE FISCAL YEAR ENDED DECEMBER 31 , 2023

| or | |||||

| FOR THE TRANSITION PERIOD FROM ___________ TO __________ | |||||

| COMMISSION FILE NUMBER | |||||

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | ||||

(Address of principal executive offices) (Zip code)

Registrant's telephone number, including area code: (724 ) 271-7600

Securities registered pursuant to Section 12(b) of the Act

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated Filer | ☐ | Emerging Growth Company | ||||||||||||||||||||||||||

| Non-Accelerated Filer | ☐ | Smaller Reporting Company | |||||||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of common stock held by non-affiliates of the registrant as of June 30, 2023: $4.1 billion

The number of shares of common stock outstanding (in thousands), as of January 31, 2024: 433,661

DOCUMENTS INCORPORATED BY REFERENCE

EQUITRANS MIDSTREAM CORPORATION

Table of Contents

| Page No. | ||||||||

| PART I | ||||||||

| PART II | ||||||||

| PART III | ||||||||

| PART IV | ||||||||

3

EQUITRANS MIDSTREAM CORPORATION

Glossary of Commonly Used Terms, Abbreviations and Measurements

2021 Water Services Agreement – that certain mixed-use water services agreement entered into on October 22, 2021 by the Company and EQT (as defined below), as subsequently amended, which became effective on March 1, 2022.

Allowance for Funds Used During Construction (AFUDC) – carrying costs for the construction of certain long-lived regulated assets are capitalized and amortized over the related assets' estimated useful lives. The capitalized amount for construction of regulated assets includes interest cost and a designated cost of equity for financing the construction of these regulated assets.

Amended EQM Credit Facility – that certain Third Amended and Restated Credit Agreement, dated as of October 31, 2018, among EQM, as borrower, Wells Fargo Bank, National Association, as the administrative agent, swing line lender, and a letter of credit (L/C) issuer, the lenders party thereto from time to time and any other persons party thereto from time to time (as amended by that certain First Amendment to Third Amended and Restated Credit Agreement, dated as of March 30, 2020, by that certain Second Amendment to Third Amended and Restated Credit Agreement, dated April 16, 2021, by that certain Third Amendment to the Third Amended and Restated Credit Agreement, dated as of April 22, 2022, by that certain Fourth Amendment to Third Amended and Restated Credit Agreement, dated as of October 6, 2023, by that certain Fifth Amendment to Third Amended and Restated Credit Agreement, dated as of February 15, 2024, and as may be further amended, restated, amended and restated, supplemented or otherwise modified from time to time). For the avoidance of doubt, any reference to the Amended EQM Credit Facility as of any particular date shall mean the Amended EQM Credit Facility as in effect on such date.

Annual Revenue Commitments (ARC or ARCs) – contractual term in a water services agreement that obligates the customer to pay for a fixed amount of water services annually.

Appalachian Basin – the area of the United States composed of those portions of West Virginia, Pennsylvania, Ohio, Maryland, Kentucky and Virginia that lie in the Appalachian Mountains.

associated gas – natural gas that is produced as a byproduct of principally oil production activities.

British thermal unit – a measure of the amount of energy required to raise the temperature of one pound of water one-degree Fahrenheit.

Code – the U.S. Internal Revenue Code of 1986, as amended, and the regulations and interpretations promulgated thereunder.

delivery point – the point where gas is delivered into a downstream gathering system or transmission pipeline.

Distribution – the distribution of 80.1% of the then-outstanding shares of common stock, no par value, of Equitrans Midstream Corporation (Equitrans Midstream common stock) to EQT shareholders of record as of the close of business on November 1, 2018.

EQGP – EQGP Holdings, LP and its subsidiaries. EQGP is a wholly owned subsidiary of Equitrans Midstream Corporation.

EQM – EQM Midstream Partners, LP and its subsidiaries. EQM is a wholly owned subsidiary of Equitrans Midstream Corporation.

EQM Merger – On June 17, 2020, pursuant to that certain Agreement and Plan of Merger, dated as of February 26, 2020, by and among the Company, EQM LP LLC (formerly, EQM LP Corporation), a wholly owned subsidiary of the Company (EQM LP), LS Merger Sub, LLC, a wholly owned subsidiary of EQM LP (Merger Sub), EQM and EQGP Services, LLC (the EQM General Partner), Merger Sub merged with and into EQM, with EQM continuing and surviving as an indirect, wholly owned subsidiary of the Company.

EQT – EQT Corporation (NYSE: EQT) and its subsidiaries.

EQT Global GGA – that certain Gas Gathering and Compression Agreement entered into on February 26, 2020 (the EQT Global GGA Effective Date) by the Company with EQT and certain affiliates of EQT for the provision of certain gas gathering services to EQT in the Marcellus and Utica Shales of Pennsylvania and West Virginia, as subsequently amended.

Equitrans Midstream Preferred Shares – the Equitrans Midstream Corporation Series A Perpetual Convertible Preferred Shares, no par value.

4

firm contracts – contracts for gathering, transmission, storage and water services that reserve an agreed upon amount of pipeline or storage capacity regardless of the capacity used by the customer during each month, and generally obligate the customer to pay a fixed, monthly charge.

firm reservation fee revenues – contractually obligated revenues that include fixed monthly charges under firm contracts and fixed volumetric charges under MVC (as defined below) and ARC (as defined above) contracts.

gas – natural gas.

liquefied natural gas (LNG) – natural gas that has been cooled to minus 161 degrees Celsius for transportation, typically by ship. The cooling process reduces the volume of natural gas by 600 times.

local distribution company (LDC or LDCs) – a company involved in the delivery of natural gas to consumers within a specific geographic area.

Minimum volume commitments (MVC or MVCs) – contracts for gathering or water services that obligate the customer to pay for a fixed amount of volumes daily, monthly, annually or over the life of the contract.

Mountain Valley Pipeline (MVP) – an estimated 300-mile, 42-inch diameter natural gas interstate pipeline with a targeted capacity of 2.0 Bcf per day that is designed to span from the Company's existing transmission and storage system in Wetzel County, West Virginia to Pittsylvania County, Virginia, providing access to the growing Southeast demand markets.

Mountain Valley Pipeline, LLC (MVP Joint Venture) – a joint venture formed among the Company and, as applicable, affiliates of each of NextEra Energy, Inc., Consolidated Edison, Inc. (Con Edison), AltaGas Ltd. and RGC Resources, Inc. (RGC) for purposes of the MVP and the MVP Southgate (as defined below) projects.

MVP Southgate – an estimated 31-mile, 30-inch diameter natural gas interstate pipeline with a targeted capacity of 550,000 dekatherms per day that is designed to span from the terminus of the MVP in Pittsylvania County, Virginia to planned new delivery points in Rockingham County, North Carolina.

natural gas liquids (NGLs) – those hydrocarbons in natural gas that are separated from the gas as liquids through the process of absorption, condensation, adsorption or other methods in gas processing plants. Natural gas liquids include ethane, propane, pentane, butane and iso-butane.

play – a proven geological formation that contains commercial amounts of hydrocarbons.

Preferred Interest – the preferred interest that the Company has in EQT Energy Supply, LLC (EES), a subsidiary of EQT.

Proxy Statement – the Company's definitive proxy statement relating to the 2024 annual meeting of shareholders to be filed with the Securities and Exchange Commission.

Rager Mountain natural gas storage field incident – that certain venting of natural gas in 2022 at a storage well (well 2244) at Equitrans, L.P.'s Rager Mountain natural gas storage facility, located in Jackson Township, a remote section of Cambria County, Pennsylvania, which venting was successfully halted on November 19, 2022.

reservoir – a porous and permeable underground formation containing an individual and separate natural accumulation of producible hydrocarbons (crude oil and/or natural gas) which is confined by impermeable rock or water barriers and is characterized by a single natural pressure system.

Scope 1 emissions – direct greenhouse gas emissions from owned or controlled sources.

Scope 2 emissions – indirect greenhouse gas emissions from the generation of purchased energy.

Separation – the separation of EQT's midstream business, which was composed of the assets and liabilities of EQT's separately-operated natural gas gathering, transmission and storage and water services operations of EQT, from EQT's upstream business, which was composed of the natural gas, oil and natural gas liquids development, production and sales and commercial operations of EQT, which occurred on the Separation Date.

Separation Date – November 12, 2018.

throughput – the volume of natural gas transported or passing through a pipeline, plant, terminal or other facility during a particular period.

5

wellhead – the equipment at the surface of a well used to control the well's pressure and the point at which the hydrocarbons and water exit the ground.

working gas – the volume of natural gas in the storage reservoir that can be extracted during the normal operation of the storage facility.

Unless the context otherwise requires, a reference to a "Note" herein refers to the accompanying Notes to the consolidated financial statements contained in Part II, "Item 8. Financial Statements and Supplementary Data" of this Annual Report on Form 10-K and all references to "we," "us," "our" and "the Company" refer to Equitrans Midstream Corporation and its subsidiaries.

| Abbreviations | Measurements | ||||

AROs – asset retirement obligations | Btu = one British thermal unit | ||||

ASC – Accounting Standards Codification | BBtu = billion British thermal units | ||||

ASU – Accounting Standards Update | Bcf = billion cubic feet | ||||

CERCLA – Comprehensive Environmental Response, Compensation and Liability Act | Mcf = thousand cubic feet | ||||

DOT – United States Department of Transportation | MMBtu = million British thermal units | ||||

EPA – United States Environmental Protection Agency | MMcf = million cubic feet | ||||

FASB – Financial Accounting Standards Board | MMgal = million gallons | ||||

FERC – United States Federal Energy Regulatory Commission | |||||

GAAP – United States Generally Accepted Accounting Principles | |||||

GHG – greenhouse gas | |||||

HCAs – high consequence areas | |||||

IRS – United States Internal Revenue Service | |||||

MCAs – moderate consequence areas | |||||

NAAQS – National Ambient Air Quality Standards | |||||

NEPA – National Environmental Policy Act, as amended | |||||

NGA – Natural Gas Act of 1938, as amended | |||||

NGPA – Natural Gas Policy Act of 1978, as amended | |||||

NYMEX – New York Mercantile Exchange | |||||

NYSE – New York Stock Exchange | |||||

PHMSA – Pipeline and Hazardous Materials Safety Administration of the DOT | |||||

RCRA – Resource Conservation and Recovery Act | |||||

SEC – United States Securities and Exchange Commission | |||||

6

EQUITRANS MIDSTREAM CORPORATION

Cautionary Statements

Disclosures in this Annual Report on Form 10-K contain certain forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (the Exchange Act), and Section 27A of the Securities Act of 1933, as amended (the Securities Act). Statements that do not relate strictly to historical or current facts are forward-looking and usually identified by the use of words such as "aim," "anticipate," "approximate," "aspire," "assume," "believe," "budget," "continue," "could," "design," "estimate," "expect," "focused," "forecast," "goal," "guidance," "intend," "may," "objective," "opportunity," "outlook," "plan," "position," "potential," "predict," "project," "pursue," "scheduled," "seek," "should," "strategy," "strive," "target," "view," "will," or "would" and other words of similar meaning in connection with any discussion of future operating or financial matters. Without limiting the generality of the foregoing, forward-looking statements contained in this Annual Report on Form 10-K include the matters discussed in the sections captioned "Developments, Market Trends and Competitive Conditions" in Part I, "Item 1. Business" and "Outlook" in Part II, "Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations," and the expectations of plans, strategies, objectives, and growth and anticipated financial and operational performance of Equitrans Midstream Corporation (together with its subsidiaries, Equitrans Midstream or the Company), including the following and/or statements with respect thereto, as applicable:

•guidance and any changes in such guidance in respect of the Company’s gathering, transmission and storage and water services revenue and volume, including the anticipated effects associated with the EQT Global GGA;

•projected revenue (including from firm reservation fees) and volumes, gathering rates, deferred revenues, expenses and contract liabilities, and the effects on liquidity, leverage, projected revenue, deferred revenue and contract liabilities associated with the EQT Global GGA and the MVP project (including changes in timing for such project);

•the ultimate gathering MVC fee relief, and timing thereof, provided to EQT under the EQT Global GGA and related agreements, and timing of step ups in MVC thereunder;

•the Company's ability to de-lever and timing and means thereof;

•the ultimate financial, business, reputational and/or operational impacts resulting, directly or indirectly, from the Rager Mountain natural gas storage field incident;

•the weighted average contract life of gathering, transmission and storage contracts;

•infrastructure programs (including the targeted or ultimate timing, cost, capacity and sources of funding with respect to gathering, transmission and storage and water projects);

•the outcome of the Company's Board of Directors' strategic process with respect to the Company;

•the cost to construct or restore right-of-way for, capacity of, shippers for, timing and durability of regulatory approvals and concluding litigation, final design (including project scope, expansions, extensions or refinements and capital related thereto), ability and timing to contract additional capacity on, mitigate emissions from, targeted in-service dates of, and completion (including potential timing of such completion) of current, planned or in-service projects or assets, in each case as applicable;

•the effect of the Fiscal Responsibility Act of 2023 on the MVP Joint Venture's ability to complete the MVP project;

•the ability to construct, complete and place in service the MVP project;

•the targeted timing and cost of completing, the MVP project (and risks related thereto), the realizability of the MVP performance award program, and the degree to which, if at all, the MVP PSU Amendment (as defined in Note 8) fosters the Company completing the MVP project safely and in compliance with environmental standards;

•the targeted total MVP project cost and schedule, including the timing for contractual obligations to commence, and the ability to continue construction, potential receipt of in-service authorization, and the realizability of the perceived benefits of the MVP project;

•finalizing the scope of the MVP Southgate and the ability to permit, construct, complete and place in service the MVP Southgate;

•the targeted total project cost and timing for completing (and ability to complete) MVP Southgate, including the satisfaction, if any, of conditions precedent with respect to the relevant precedent agreements, timing for forecasted

7

capital expenditures related thereto, and the realizability of the perceived benefits of the amended project, design, scope and provisions included in the relevant precedent agreements, and any potential extensions of the terms of the precedent agreements;

•the MVP Joint Venture's ability to execute any additional agreements for firm capacity for the MVP Southgate;

•the realizability of all or any portion of the Henry Hub cash bonus payment under the EQT Global GGA;

•the potential for future bipartisan support for, and the potential timing for, additional federal energy infrastructure permitting reform legislation to be enacted;

•the ultimate terms, partner relationships and structure of the MVP Joint Venture and ownership interests therein;

•the impact of changes in assumptions and estimates relating to the potential completion and full in-service timing of the MVP project (as well as changes in such timing) on, among other things, the fair value of the Henry Hub cash bonus payment provision of the EQT Global GGA, gathering rates, the amount of gathering MVC fee relief and the estimated transaction price allocated to the Company's remaining performance obligations under certain contracts with firm reservation fees and MVCs;

•the Company's ability to identify and complete opportunities to optimize its existing asset base and/or expansion projects in the Company's operating areas and in areas that would provide access to new markets;

•the Company's ability to bring, and targeted timing for bringing, in-service extensions and expansions of its mixed-use water system, and realize benefits therefrom in accordance with its strategy for its water services business segment;

•the Company's ability to identify and complete acquisitions and other strategic transactions, including joint ventures, effectively integrate transactions into the Company's operations, and achieve synergies, system optionality, accretion and other benefits associated with transactions, including through increased scale;

•the potential for the MVP project, EQM's leverage, customer credit ratings changes, defaults, acquisitions, dispositions and financings to impact EQM's credit ratings and the potential scope of any such impacts;

•the effect and outcome of contractual disputes, litigation and other proceedings, including regulatory investigations and proceedings;

•the potential effects of any consolidation of or effected by upstream gas producers, including acquisitions of midstream assets, whether in or outside of the Appalachian Basin;

•the potential for, timing, amount and effect of future issuances or repurchases of the Company's securities;

•the effects of conversion, if at all, of the Equitrans Midstream Preferred Shares (as defined herein);

•the effects of seasonality;

•expected cash flows, cash flow profile (and support therefor from certain contract structures) and MVCs, including those associated with the EQT Global GGA, and the potential impacts thereon of the commission and in-service timing (or absence thereof) and cost of the MVP project;

•projected capital contributions and capital and operating expenditures, including the amount and timing of reimbursable capital expenditures, capital budget and sources of funds for capital expenditures;

•the Company's ability to recoup replacement and related costs;

•future dividend amounts, timing and rates;

•statements regarding macroeconomic factors' effects on the Company's business, including future commodity prices, the impact of MVP in-service on commodity prices or natural gas volumes in the Appalachian Basin, and takeaway capacity constraints in the Appalachian Basin;

•beliefs regarding future decisions of customers in respect of production growth, curtailing natural gas production, timing of turning wells in line, rig and completion activity and related impacts on the Company's business, and the effect, if any, on such future decisions should the MVP be brought in-service, as well as the potential for increased volumes to flow to the Company's gathering and transmission system to supply the MVP following in-service;

8

•the Company's liquidity and financing position and requirements, including sources, availability and sufficiency;

•statements regarding future interest rates and/or reference rates and the potential impacts thereof;

•the ability of the Company's subsidiaries (some of which are not wholly owned) to service debt under, and comply with the covenants contained in, their respective credit agreements;

•the MVP Joint Venture's ability to raise project-level debt, and the anticipated proceeds that the Company expects to receive therefrom;

•expectations regarding natural gas and water volumes in the Company's areas of operations;

•the Company's ability to achieve anticipated benefits associated with the execution of the EQT Global GGA and other commercial agreements;

•the Company's ability to position itself for a lower carbon economy, achieve, and create value from, its environmental, social and governance (ESG) and sustainability initiatives, targets and aspirations (including targets and aspirations set forth in its climate policy) and respond, and impacts of responding, to increasing stakeholder scrutiny in these areas;

•the effectiveness of the Company's information technology and operational technology systems and practices to detect and defend against evolving cyberattacks on United States critical infrastructure;

•the effects and associated cost of compliance with existing or new government regulations including any quantification of potential impacts of regulatory matters related to climate change on the Company; and

•future tax rates, status and position.

The forward-looking statements included in this Annual Report on Form 10-K involve risks and uncertainties that could cause actual results to differ materially from projected results. Accordingly, investors should not place undue reliance on forward-looking statements as a prediction of actual results. The Company has based these forward-looking statements on management's current expectations and assumptions about future events. While the Company considers these expectations and assumptions to be reasonable, they are inherently subject to significant business, economic, competitive, regulatory, judicial, construction and other risks and uncertainties, many of which are difficult to predict and are beyond the Company's control, including, as it pertains to the MVP project, risks and uncertainties such as the physical construction conditions, including steep slopes and any further unexpected geological impediments, continued crew availability, ability to meet contractor draw down plans, and productivity realizable, project opposition, the receipt of certain time of year and other variances and approvals, if applicable, and weather. The risks and uncertainties that may affect the operations, performance and results of the Company's business and forward-looking statements include, but are not limited to, those set forth under Part I, "Item 1A. Risk Factors," and elsewhere in this Annual Report on Form 10-K.

Any forward-looking statement speaks only as of the date on which such statement is made and the Company does not intend to correct or update any forward-looking statement, unless required by securities law, whether as a result of new information, future events or otherwise. As forward-looking statements involve significant risks and uncertainties, caution should be exercised against placing undue reliance on such statements.

PART I

Item 1. Business

Overview of Operations and the Company

Equitrans Midstream is one of the largest natural gas gatherers in the U.S. and holds a significant transmission footprint in the Appalachian Basin. Equitrans Midstream, a Pennsylvania corporation, became an independent, publicly traded company on November 12, 2018 and its common stock trades on the New York Stock Exchange under the symbol "ETRN". The Company provides midstream services to its customers in Pennsylvania, West Virginia and Ohio through its three primary assets: the gathering system, which includes predominantly dry gas gathering systems of high-pressure gathering lines; the transmission system, which includes FERC-regulated interstate pipelines and storage systems; and the water network, which primarily consists of water pipelines, storage and other facilities that support well completion and produced water handling activities.

As of December 31, 2023, the Company provided a majority of its natural gas gathering, transmission and storage services and water services under long-term contracts that generally include firm reservation fee revenues. For the year ended December 31,

9

2023, approximately 70% of the Company's operating revenues were generated from firm reservation fee revenues. Generally, the Company is focused on utilizing contract structures reflecting long-term firm capacity, MVC or ARC commitments which are intended to provide support to its cash flow profile. The percentage of the Company's operating revenues that are generated by firm reservation fees (as well as the Company's revenue generally) may vary year to year depending on various factors, including customer volumes and the rates realizable under the Company's contracts, including the EQT Global GGA (defined below) which provides for periodic gathering MVC fee declines through January 1, 2028 (with the fees then remaining fixed throughout the remaining term). Additionally, as discussed below, in connection with MVP full in-service the EQT Global GGA provides for more significant potential gathering MVC fee declines in certain contract years.

The Company's operations are focused primarily in southwestern Pennsylvania, northern West Virginia and southeastern Ohio, which are prolific resource development areas in the natural gas shale plays known as the Marcellus and Utica Shales. These regions are also the primary operating areas of EQT, the Company's largest customer, which was one of the largest natural gas producers in the United States based on average daily sales volumes as of December 31, 2023. EQT accounted for approximately 61% of the Company's revenues for the year ended December 31, 2023.

EQT Global GGA. On February 26, 2020 (the EQT Global GGA Effective Date), the Company entered into a Gas Gathering and Compression Agreement (as subsequently amended, the EQT Global GGA) with EQT and certain affiliates of EQT for the provision by the Company of certain gas gathering services to EQT in the Marcellus and Utica Shales of Pennsylvania and West Virginia. The EQT Global GGA is intended to, among other things, incentivize combo and return-to-pad drilling by EQT. Pursuant to the EQT Global GGA, EQT is subject to an initial annual MVC of 3.0 Bcf per day that gradually steps up to 4.0 Bcf per day through December 2031 following the full in-service date of the MVP and the dedication of a substantial majority of EQT's core acreage in southwestern Pennsylvania and West Virginia. The EQT Global GGA runs from the EQT Global GGA Effective Date through December 31, 2035, and will renew annually thereafter unless terminated by EQT or the Company pursuant to its terms. Pursuant to the EQT Global GGA, the Company has certain obligations to build connections to connect EQT wells to its gathering system, which are subject to limitations, including geographical in relation to the dedicated area, as well as the distance of such connections to the Company's then-existing gathering system, which have provided and could further provide capital efficiencies to EQM. In addition to the fees related to gathering services, the EQT Global GGA provides for potential cash bonus payments payable by EQT to the Company during the period beginning on the first day of the calendar quarter in which the MVP full in-service date occurs through the calendar quarter ending December 31, 2024 (the Henry Hub cash bonus payment provision). The potential cash bonus payments are conditioned upon the quarterly average of certain Henry Hub natural gas prices exceeding certain price thresholds.

Under the EQT Global GGA, the performance obligation is to provide daily MVC capacity and as such the total consideration is allocated proportionally to the daily MVC over the life of the contract. In periods that the gathering MVC revenue billed will exceed the allocated consideration, the excess will be deferred to the contract liability and recognized in revenue when the performance obligation has been satisfied. While the 3.0 Bcf per day MVC capacity became effective on April 1, 2020, additional daily MVC capacity and the associated gathering MVC fees payable by EQT to the Company as set forth in the EQT Global GGA are conditioned upon the full in-service date of the MVP. The performance obligation, the allocation of the total consideration over the life of the contract and the gathering MVC fees payable by EQT under the contract have been in the past, and in the future could be, affected by changes in the timing of the full in-service date of the MVP.

Under the EQT Global GGA, the gathering MVC fee periodically declines through January 1, 2028 (with the fees then remaining fixed throughout the remaining term). Before January 1, 2026, beginning the first day of the quarter in which the full in-service date of the MVP occurs under the EQT Global GGA, the gathering MVC fees payable by EQT to the Company are subject to more significant potential declines for certain contract years as set forth in the EQT Global GGA, which, prior to EQT's exercise of the EQT Cash Option (defined below), provided for estimated aggregate fee relief of up to approximately $270 million in the first twelve-month period, up to approximately $230 million in the second twelve-month period and up to approximately $35 million in the third twelve-month period. Given that the MVP full in-service date did not occur by January 1, 2022, on July 8, 2022, EQT irrevocably elected under the EQT Global GGA to forgo up to approximately $145 million of the potential gathering MVC fee relief in such first twelve-month period and up to approximately $90 million of the potential gathering MVC fee relief in such second twelve-month period in exchange for a cash payment from the Company to EQT in the amount of approximately $195.8 million (the EQT Cash Option). As a result of EQT exercising the EQT Cash Option (and payment by the Company thereof), the maximum aggregate potential fee relief applicable under the EQT Global GGA in such first twelve-month period and such second twelve-month period was reduced to be up to approximately $125 million and depending on the ultimate in-service date of the MVP, up to approximately $140 million, respectively. The gathering MVC fees and potential declines are subject to certain provisions related to inflation adjustment in accordance with the terms of the EQT Global GGA. Additionally, the EQT Global GGA provides for a fee credit to the gathering rate for certain gathered volumes that also receive separate transmission services under certain transmission contracts.

10

See also "Our exposure to commodity price risk may increase in the future and NYMEX Henry Hub futures prices affect the fair value, and may affect the realizability, of potential cash payments to us by EQT pursuant to the EQT Global GGA.” included in Part I, "Item 1A. Risk Factors" of this Annual Report on Form 10-K for a discussion of factors affecting the estimated fair value of the derivative asset attributable to the Henry Hub cash bonus payment provision.

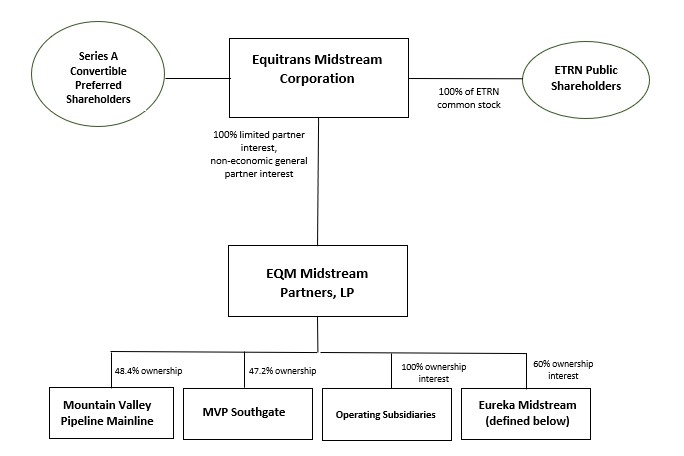

The following diagram depicts the Company's organizational and ownership structure as of December 31, 2023:

11

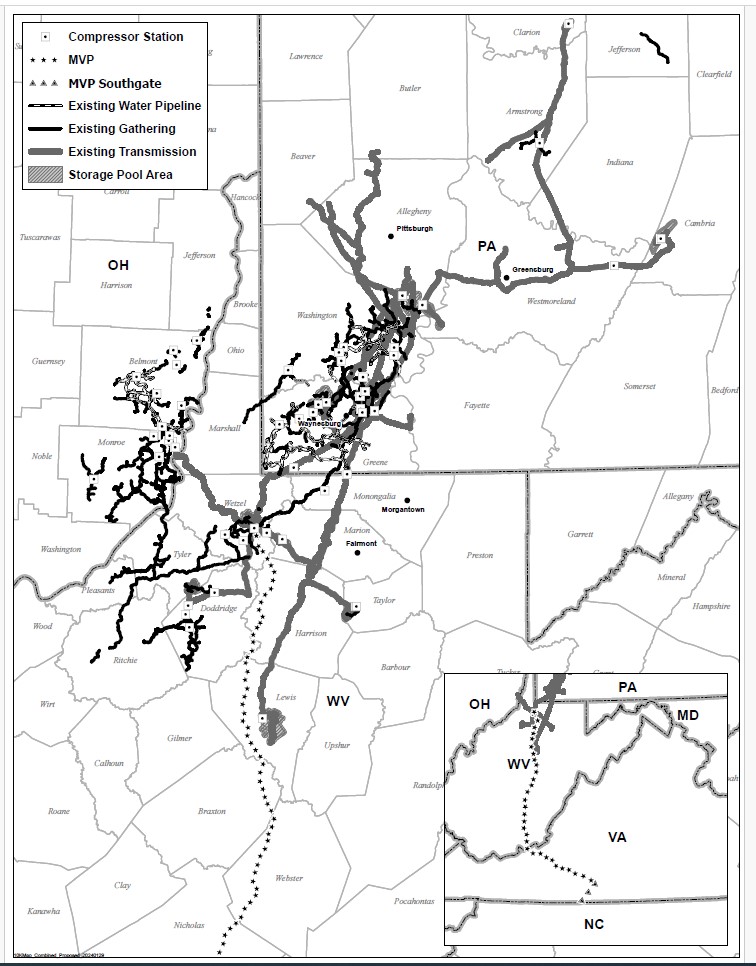

The following is a map of the Company's gathering, transmission and storage and water services operations as of December 31, 2023. Also included are the MVP and MVP Southgate routes, which projects are discussed under "Developments, Market Trends and Competitive Conditions" in Part I, "Item 1. Business" of this Annual Report on Form 10-K.

12

Business Segments

The Company reports its operations in three segments that reflect its three lines of business: Gathering, Transmission and Water. These segments include all of the Company's operations.

The Company's three business segments correspond to the Company's three primary assets: the gathering system, transmission and storage system and water service system. The following table summarizes the composition of the Company's operating revenues by business segment.

| Years Ended December 31, | |||||||||||||||||

| 2023 | 2022 | 2021 | |||||||||||||||

| Gathering operating revenues | 62 | % | 66 | % | 66 | % | |||||||||||

| Transmission operating revenues | 32 | % | 30 | % | 30 | % | |||||||||||

| Water operating revenues | 6 | % | 4 | % | 4 | % | |||||||||||

The Company's largest customer, EQT, accounted for approximately 61%, 61% and 59% of the Company's total revenues for the years ended December 31, 2023, 2022 and 2021, respectively.

Gathering Customers. For the year ended December 31, 2023, EQT accounted for approximately 59% of Gathering's throughput and approximately 62% of Gathering's revenues. Subject to certain exceptions and limitations, as of December 31, 2023, Gathering (inclusive of acreage dedications to Eureka Midstream Holdings, LLC (Eureka Midstream), a joint venture in which the Company is the operator and has a 60% interest) had significant acreage dedications through which the Company has the right to elect to gather all natural gas produced from wells under dedicated areas in (i) Pennsylvania pursuant to agreements with EQT, including the EQT Global GGA, and agreements with certain other third parties, (ii) West Virginia pursuant to agreements with EQT, including the EQT Global GGA, and agreements with certain other third parties, and (iii) Ohio pursuant to agreements with various third parties.

The Company provides gathering services in two manners: firm service and interruptible service. Firm service contracts are typically long-term and often include firm reservation fees, which are fixed, monthly charges for the guaranteed reservation of pipeline access. Revenues under firm reservation fees also include fixed volumetric charges under MVCs. As of December 31, 2023, the gathering system had total contracted firm reservation capacity (including contracted MVCs) of approximately 7.7 Bcf per day (inclusive of Eureka Midstream contracted capacity), which included contracted firm reservation capacity of approximately 1.8 Bcf per day associated with the Company's high-pressure header pipelines. Including future capacity expected from expansion projects that are not yet fully constructed or not yet fully in-service for which the Company has executed firm contracts, the gathering system had total contracted firm reservation capacity (including contracted MVCs) of approximately 8.8 Bcf per day (inclusive of Eureka Midstream contracted capacity) as of December 31, 2023, which included contracted firm reservation capacity of approximately 1.9 Bcf per day associated with the Company's high-pressure header pipelines. Volumetric-based fees can also be charged under firm contracts for each firm volume gathered, as well as for volumes gathered in excess of the firm contracted volume. Based on total projected contractual revenues, including projected contractual revenues from future capacity expected from expansion projects that are not yet fully constructed or not yet fully in-service for which the Company has executed firm contracts, the Company's firm gathering contracts had a weighted average remaining term of approximately 13 years as of December 31, 2023.

Interruptible service contracts include volumetric-based fees, which are charges for the volume of natural gas gathered and generally do not guarantee access to the pipeline. These contracts can be short- or long-term. To the extent that capacity reserved by customers with firm service contracts is not fully used or excess capacity exists, the gathering system can allocate capacity to interruptible services.

The Company generally does not take title to the natural gas gathered for its customers but retains a percentage of wellhead gas receipts to recover natural gas used to fuel certain of its compressor stations and meet other requirements on the Company's gathering systems.

Transmission Customers. For the year ended December 31, 2023, EQT accounted for approximately 61% of Transmission's throughput and approximately 51% of Transmission's revenues. As of December 31, 2023, Transmission had an acreage dedication from EQT through which the Company had the right to elect to transport all gas produced from wells drilled by EQT under dedicated areas in Allegheny, Washington and Greene Counties in Pennsylvania and Wetzel, Marion, Taylor, Tyler, Doddridge, Harrison and Lewis Counties in West Virginia. The Company's other customers include LDCs, marketers, producers and commercial and industrial users. The Company's transmission and storage system provides customers with

13

access to markets in Pennsylvania, West Virginia and Ohio and to the Mid-Atlantic, Northeastern, Midwestern and Gulf Coast markets through interconnect points with major interstate pipelines.

The Company provides transmission and storage services in two manners: firm service and interruptible service. Firm service contracts are typically long-term and often include firm reservation fees, which are fixed, monthly charges for the guaranteed reservation of pipeline and storage capacity. Volumetric-based fees can also be charged under firm contracts for firm volume transported or stored, as well as for volumes transported or stored in excess of the firm contracted volume. As of December 31, 2023, the Company had firm capacity subscribed under firm transmission contracts of approximately 5.8 Bcf per day, which includes future capacity expected from expansion projects that are not yet fully constructed or not yet fully in-service for which the Company has executed firm transmission contracts and excludes approximately 2.6 Bcf per day of firm capacity commitments associated with the MVP and MVP Southgate projects. As of December 31, 2023, the Company had firm storage capacity of approximately 29.8 Bcf subscribed under firm storage contracts. Based on total projected contractual revenues, including projected contractual revenues from future capacity expected from expansion projects that are not yet fully constructed or not yet fully in-service for which the Company has executed firm contracts, the Company's firm transmission and storage contracts had a weighted average remaining term of approximately 12 years as of December 31, 2023.

Interruptible service contracts include volumetric-based fees, which are charges for the volume of natural gas transported or stored and generally do not guarantee access to the pipeline or storage facility. These contracts can be short- or long-term. To the extent that capacity reserved by customers with firm service contracts is not fully used or excess capacity exists, the transmission and storage systems can allocate capacity to interruptible services.

The Company generally does not take title to the natural gas transported or stored for its customers but retains a percentage of gas receipts to recover natural gas used to fuel its compressor stations and meet other requirements of the Company's transmission and storage systems.

As of December 31, 2023, approximately 97% of Transmission's contracted firm transmission capacity was subscribed by customers under negotiated rate agreements under its tariff. As of December 31, 2023, Transmission had minimal contracted firm transmission capacity subscribed at discounted rates and recourse rates under its tariff. See also "FERC Regulation" under "Regulatory Environment" below and "Our and the MVP Joint Venture's natural gas gathering, transmission and storage services, as applicable, are subject to extensive regulation by federal, state and local regulatory authorities. Changes in or additional regulatory measures adopted by such authorities, and related litigation, could have a material adverse effect on our business, financial condition, results of operations, liquidity and ability to pay dividends.” included in Part I, "Item 1A. Risk Factors" of this Annual Report on Form 10-K for additional information.

Water Customers. For the year ended December 31, 2023, EQT accounted for approximately 96% of Water's revenues. The Company has the exclusive right to provide fluid handling services to certain EQT-operated wells through 2029 (and thereafter such right will continue on a month-to-month basis) within areas of dedication in Belmont County, Ohio, including the delivery of fresh water for well completion operations and the collection and recycling or disposal of flowback and produced water. The Company also provides water services to other customers operating in the Marcellus and Utica Shales.

The Company's Assets

Gathering Assets. As of December 31, 2023, the gathering system, inclusive of Eureka Midstream's gathering system, included approximately 1,220 miles of high-pressure gathering lines, 138 compressor units with compression of approximately 491,000 horsepower and multiple interconnect points with the Company's transmission and storage system and to other interstate pipelines.

Transmission and Storage Assets. As of December 31, 2023, the transmission and storage system included approximately 940 miles of FERC-regulated, interstate pipelines that have interconnect points to seven interstate pipelines and multiple LDCs. As of December 31, 2023, the transmission and storage system was supported by 42 compressor units, with total throughput capacity of approximately 4.4 Bcf per day and compression of approximately 135,000 horsepower, and 18 associated natural gas storage reservoirs, which had a peak withdrawal capacity of approximately 820 MMcf per day and a working gas capacity of approximately 43 Bcf.

Water Assets. As of December 31, 2023, the fresh water systems included approximately 201 miles of pipeline that deliver fresh water from local municipal water authorities, the Monongahela River, the Ohio River, local reservoirs and several regional waterways. In addition, as of December 31, 2023, the fresh water systems consisted of permanent, buried pipelines, surface pipelines, 17 fresh water impoundment facilities, as well as pumping stations, which support water transportation throughout the systems, and take point facilities and measurement facilities, which support well completion activities. During 2023, the Company completed the majority of the main trunkline pipelines on the mixed water system including a pipeline that connects its two mixed water storage facilities. As of December 31, 2023, the mixed water system included approximately 53 miles of

14

buried pipeline and two water storage facilities with 350,000 barrels of capacity, as well as two interconnects with the Company’s existing Pennsylvania fresh water systems and provides services to producers in southwestern Pennsylvania. The Company plans to continue to expand its mixed water system in 2024, including the completion of a pipeline to serve a producer in West Virginia and a water pipeline, scheduled to be completed in the first quarter of 2025, to interconnect with the same producer's Pennsylvania mixed water network.

Developments, Market Trends and Competitive Conditions

The Company's strategically located and integrated assets overlay core acreage in the Appalachian Basin. The location of the Company's assets allows its producer customers to access major demand markets in the U.S. The Company is one of the largest natural gas gatherers in the U.S., and its largest customer, EQT, was one of the largest natural gas producers in the U.S. based on average daily sales volumes as of December 31, 2023 and EQT's public senior debt had investment grade credit ratings from Standard & Poor's Global Ratings (S&P), Fitch Ratings (Fitch) and Moody's Investors Service (Moody's) as of that date. For the year ended December 31, 2023, approximately 70% of the Company's operating revenues were generated from firm reservation fee revenues. Generally, the Company is focused on utilizing contract structures reflecting long-term firm capacity, MVC or ARC commitments which are intended to provide support to its cash flow profile. The percentage of the Company's operating revenues that are generated by firm reservation fees (as well as the Company's revenues generally) may vary year to year depending on various factors, including customer volumes and the rates realizable under the Company's contracts, including the EQT Global GGA which provides for periodic gathering MVC fee declines through January 1, 2028 (with the fee then remaining fixed throughout the remaining term). Additionally, as discussed above under "Overview of the Company and Operations" in Part 1, "Item 1. Business" of this Annual Report on Form 10-K, in connection with MVP full in-service the EQT Global GGA provides for more significant potential gathering MVC fee declines in certain contract years.

The Company's principal strategic aim is to achieve greater scale and scope, enhance the durability of its financial strength and to continue to work to position itself for a lower carbon economy.

The Company's standalone strategy reflects its continued pursuit of organic growth projects, including completing and placing in service the MVP, focusing on identifying opportunities to use its existing assets to deepen and grow its customer relationships at optimized levels of capital spending and taking into account the Company’s leverage, and continuing to prudently invest resources in its sustainability-oriented initiatives. The Company’s strategy also reflects its continued focus on achieving a strong balance sheet, and given the Company’s size, operating footprint and other factors considering inorganic opportunities, such as to extend the Company’s operations into the southeast United States and new, key demand markets, such as the Gulf of Mexico LNG export market.

In conjunction with the Company working to execute on its standalone strategy, the Company’s Board of Directors has been engaged in a process with third parties that have expressed interest in strategic transactions involving the Company. The board has engaged outside advisors and the process is ongoing. There is no assurance that such process will result in the execution, approval or completion of any specific transaction or outcome.

The Company expects that the MVP, together with the Hammerhead pipeline and Equitrans, L.P. Expansion Project (EEP), will primarily drive the Company's near-term organic growth, as discussed in further detail below. In particular, the Company believes that the MVP, among other benefits, will allow for greater natural gas production in the southwestern Appalachian Basin (and/or result in increased volumes flowing to the Company's gathering and transmission system given the Company's belief in the system's current unique positioning to provide the supply path to MVP). In addition, the Company continues to focus on de-levering its balance sheet (which the Company views as a critical strategic objective), including in connection with the MVP.

•Mountain Valley Pipeline. The MVP is being constructed by a joint venture among the Company and affiliates of each of NextEra Energy, Inc. (NEE), Consolidated Edison, Inc. (Con Edison), AltaGas Ltd. and RGC Resources, Inc. (RGC). As of December 31, 2023, the Company owned an approximate 48.4% interest in the MVP project and will operate the MVP. The MVP is an estimated 300-mile, 42-inch diameter natural gas interstate pipeline with a targeted capacity of 2.0 Bcf per day that is designed to span from the Company's existing transmission and storage system in Wetzel County, West Virginia to Pittsylvania County, Virginia, which will provide access to the growing southeast demand markets once it is placed in-service. The MVP Joint Venture has secured a total of 2.0 Bcf per day of firm capacity commitments at 20-year terms. Additional shippers have expressed interest in the MVP project and the MVP Joint Venture is evaluating an expansion opportunity that could add approximately 0.5 Bcf per day of capacity through the installation of incremental compression.

In October 2017, the FERC issued the Certificate of Public Convenience and Necessity for the MVP. In the first quarter of 2018, the MVP Joint Venture received limited notice to proceed with certain construction activities from the FERC and commenced construction. However, the MVP project was repeatedly, significantly delayed and subject to cost increases because of legal and regulatory setbacks, particularly in respect of litigation in the U.S. Court of Appeals

15

for the Fourth Circuit (Fourth Circuit). Notwithstanding such prior setbacks, the MVP Joint Venture continued to engage in pursuing the authorizations necessary to complete the MVP project, including on February 28, 2023, the U.S. Department of the Interior’s Fish and Wildlife Service (FWS) issuing a new Biological Opinion and Incidental Take Statement (2023 BiOp) for the MVP project and in May 2023, the U.S. Forest Service and Bureau of Land Management issuing authorizations related to MVP’s segment in the Jefferson National Forest (JNF).

On June 3, 2023, the President of the United States signed into law the Fiscal Responsibility Act of 2023 that, among other things, ratified and approved all permits and authorizations necessary for the construction and initial operation of the MVP, directed the applicable federal officials and agencies to maintain such authorizations, required the Secretary of the Army to issue not later than June 24, 2023 all permits or verifications necessary to complete construction of the MVP and allow for the MVP’s operation and maintenance, and divested courts of jurisdiction to review agency actions on approvals necessary for MVP construction and initial operation.

Thereafter, certain necessary authorizations were issued to the MVP Joint Venture, and the FERC authorized the MVP Joint Venture to resume all construction activities in all MVP project locations. After the Fourth Circuit issued a stay halting MVP project construction in the JNF and a stay of the 2023 BiOp, the U.S. Supreme Court vacated the stays on July 27, 2023. The MVP Joint Venture recommenced forward construction activity in August 2023.

Since then, the MVP Joint Venture has made substantial progress on completing the MVP. As of February 15, 2024, the MVP Joint Venture, among other things, has completed:

•approximately 300 miles of pipeline installed (less than 4 miles remaining to install);

•415 crossings (13 remaining);

•the hydrotesting of approximately 180 miles (approximately 125 miles remain to be tested, inclusive of interconnect piping);

•the purging and packing of the pipeline through to the second compressor station (total of approximately 77 miles);

•the commissioning of two of three MVP compressor stations; and

•restoration of a substantial portion of the pipeline right of way, with the remaining approximately 112 miles of pipeline restoration to occur following MVP in-service.

Forward progress slowed at the end of 2023 through early 2024 as a result of unforeseen challenging construction conditions, combined with unexpected and substantially adverse winter weather conditions throughout much of January 2024. As a result, the MVP Joint Venture retained a higher than planned contractor headcount through January into February to maintain the right of way and address weather-induced issues and also to be in a position to improve forward progress as soon as conditions became more favorable. While productivity has since improved at the end of January and into February 2024, the combined effect of these unforeseen challenges significantly slowed the previously anticipated pace of construction and adversely affected project cost. As a result, the Company is targeting MVP project completion and commissioning in the second quarter of 2024, at a total estimated project cost ranging from approximately $7.57 billion to approximately $7.63 billion (excluding allowance for funds used during construction (AFUDC)).

Based on such targeted completion timing and following in-service authorization from the FERC, the Company expects that MVP and MVP-related firm capacity contractual obligations would commence on June 1, 2024 (with certain MVC step ups and more significant gathering MVC fee declines under the EQT Global GGA commencing April 1, 2024).

As the MVP Joint Venture continues to diligently work towards responsibly completing the MVP project, it will

continue to prioritize the safety of its workforce, communities, and assets, and the project's compliance with applicable

environmental standards and regulations.

The targeted completion timing and cost, and accordingly the commencement of MVP and MVP-related firm capacity contractual obligations are subject to many factors, including the physical construction conditions, weather and productivity, many of which are beyond the Company's control.

16

Further adverse developments however, whatever the cause, affecting the MVP project could further increase project

costs and/or further delay completion or in-service of the project, and adversely affect the Company, including its

leverage levels and potential liquidity. See also "Expanding our business by constructing new midstream

assets subjects us to construction, business, economic, competitive, regulatory, judicial, environmental, political and

legal uncertainties that are beyond our control." included in Part I, "Item 1A. Risk Factors" of this Annual Report on

Form 10-K. See also Part II, "Item 3. Legal Proceedings" of this Annual Report on Form 10-K.

On November 4, 2019, Con Edison exercised an option to cap its investment in the construction of the MVP project at approximately $530 million (excluding AFUDC). On May 4, 2023, RGC exercised an option for the Company to fund RGC's portion of future capital contributions with respect to the MVP project, which funding the Company commenced in June 2023 and will continue through the full in-service date of the MVP. The Company and NEE are obligated, and RGC, prior to the exercise of its option described above had opted, to fund the shortfall in Con Edison's capital contributions on a pro rata basis. Following RGC's exercise of its option, the Company is also funding RGC's portion of Con Edison's shortfall. Such funding by the Company in respect of the Con Edison shortfall and RGC's portion of capital contributions has and will correspondingly increase the Company's interests in the MVP project and decrease Con Edison's and RGC's respective interest, as applicable, in the MVP project. If the project were to be completed in the second quarter of 2024 and at a total project cost ranging from approximately $7.57 billion to approximately $7.63 billion (excluding AFUDC), the Company expects its equity ownership in the MVP project would progressively increase from approximately 48.4% to approximately 49.0%.

Through December 31, 2023, the Company had funded approximately $3.4 billion to the MVP Joint Venture for the MVP project. If the MVP project were to be completed in the second quarter of 2024 at a total project cost ranging from approximately $7.57 billion to approximately $7.63 billion (excluding AFUDC), the Company expects it would make total capital contributions to the MVP Joint Venture in 2024 of approximately $540 million to $575 million primarily related to forward construction, and expects that it would incur a total of approximately $4.0 billion over the project's construction, inclusive of approximately $245 million in excess of the Company's ownership interest.

•Wellhead Gathering Expansion Projects and Hammerhead Pipeline. During the year ended December 31, 2023, the Company invested approximately $267.7 million in gathering projects (inclusive of capital expenditures related to the noncontrolling interest in Eureka Midstream). For 2024, the Company expects to invest approximately $225 million to $275 million in gathering projects (inclusive of expected capital expenditures of approximately $15 million related to the noncontrolling interest in Eureka Midstream). The primary projects include infrastructure expansion and optimization in core development areas in the Marcellus and Utica Shales in southwestern Pennsylvania, southeastern Ohio and northern West Virginia for EQT, Range Resources Corporation (Range Resources) and other producers. The Company has seen and expects that it will continue to see the benefits of return-to-pad drilling and system integrations in 2024, and estimates gathering capital expenditures required to maintain flat gathered volumes in a given year would be between approximately $200 million and $250 million for 2024.

The Hammerhead pipeline is a 1.6 Bcf per day gathering header pipeline that is primarily designed to connect natural gas produced in Pennsylvania and West Virginia to the MVP, Texas Eastern Transmission and Eastern Gas Transmission, is supported by a 20-year term, 1.2 Bcf per day, firm capacity commitment from EQT, and cost approximately $540 million. The Company expects Hammerhead pipeline full commercial in-service to commence in conjunction with full MVP in-service and is focused on obtaining additional firm capacity commitments and/or additional interruptible volumes for the pipeline. During the fourth quarter of 2023, the Company provided firm and interruptible volumes from the Company's Hammerhead Gathering agreement with EQT and expects to continue the interruptible volumes up to the full commercial in-service date of the Hammerhead pipeline when firm commitments will commence.

The Company also has an agreement with a producer customer to install approximately 32,000 horsepower booster compression to existing facilities. The project is backed by a long-term firm commitment and is expected to be in-service in the first quarter of 2024. The majority of spend on the project was incurred in 2023.

•Transmission Projects. During the year ended December 31, 2023, the Company invested approximately $84.2 million in transmission projects. For 2024, the Company expects to invest approximately $75 million to $85 million in transmission projects, including approximately $40 million to complete the Company's Ohio Valley Connector expansion project (OVCX). The Company expects OVCX will increase deliverability on the Company's existing Ohio Valley Connector pipeline (OVC) by approximately 350 MMcf per day, create new receipt and delivery transportation paths, and enhance long-term reliability. The project is primarily supported by new long-term firm capacity commitments of 330 MMcf per day, as well as an extension of approximately 1.0 Bcf per day of existing contracted mainline capacity for EQT. OVCX is designed to meet growing demand in key markets in the mid-continent and gulf

17

coast through existing interconnects with long-haul pipelines in Clarington, Ohio. On January 20, 2023, the FERC issued the Final Environmental Impact Statement for the project. On June 15, 2023, the FERC issued the Certificate of Public Convenience and Necessity for OVCX. On July 31, 2023, the FERC issued the Notice to Proceed and the Company commenced construction during the third quarter of 2023. The Company expects to invest a total of approximately $160 million in the project and is targeting the incremental capacity to be placed in-service during the second quarter of 2024. The OVCX project, as well as the Company's successful open season in 2023 for the available transmission capacity that was subject of the one-time transmission customer's contract buyout during the first quarter of 2023, is consistent with the Company's ongoing efforts to optimize existing assets and achieve capital efficiency.

The Company's EEP project is designed to provide north-to-south capacity on the mainline Equitrans, L.P. system, including primarily for deliveries to the MVP. A portion of the EEP commenced operations with interruptible service in the third quarter of 2019. The EEP provides capacity of approximately 600 MMcf per day and offers access to several markets through interconnects with Texas Eastern Transmission, Eastern Gas Transmission and Columbia Gas Transmission. In connection with MVP full in-service, firm transportation agreements for 550 MMcf per day of capacity will commence under 20-year terms.

•MVP Southgate Project. In December 2023, the MVP Joint Venture announced an amended MVP Southgate project in lieu of the original project. The amended project would extend approximately 31 miles from the terminus of the MVP in Pittsylvania County, Virginia to planned new delivery points in Rockingham County, North Carolina using 30-inch diameter pipe. The MVP Southgate project, which was announced in April 2018, previously contemplated an approximate 75-mile interstate pipeline that was approved by the FERC to extend from the MVP at Pittsylvania County, Virginia to new delivery points in Rockingham and Alamance Counties, North Carolina. The Company is expected to operate the MVP Southgate project and owned a 47.2% interest in the MVP Southgate project as of December 31, 2023. The amended MVP Southgate is estimated to cost a total of approximately $370 million, excluding AFUDC and certain costs incurred for purposes of the original project. The Company expects to fund its proportionate share through capital contributions made to the MVP Joint Venture.

The MVP Joint Venture has entered into precedent agreements with each of Public Service Company of North Carolina, Inc. (PSNC), and Duke Energy Carolinas, LLC (Duke), which precedent agreements contemplate the amended project (in lieu of the original project). In contrast to the original, lengthier project, which traversed 155 water crossings and required an additional compressor station (the permit application for which was denied by the Virginia State Air Pollution Control Board in 2021), the amended project would include substantially fewer water crossings (all of which would be evaluated for boring) and would not require a new compressor station. The new precedent agreements, among other things, collectively provide for 550,000 Dth per day of firm capacity commitments (whereas the original project was supported by a 300,000 Dth per day firm capacity commitment with PSNC, which has been superseded by the new precedent agreement with PSNC), are each for 20-year terms (subject to two potential five-year extensions), and describe certain conditions precedent to the parties’ respective obligations regarding MVP Southgate (including, among others, that both precedent agreements remain in full force and effect). Given the court-related construction stops experienced on MVP, the new precedent agreements also incorporate certain spending and termination protections which may be exercised in certain circumstances in accordance with the terms of the precedent agreements, including in connection with a delay, stay or vacatur of certain governmental authorizations. The MVP Joint Venture recently completed an open season for the MVP Southgate project and expects to finalize the project scope in the coming months. The targeted completion timing for the project is June 2028, with the majority of the capital spend expected to occur in 2027.

The FERC previously conditioned its authorization on MVP Southgate being built and made available for service by June 18, 2023. On June 15, 2023, the MVP Joint Venture filed a request with the FERC for an extension of time to June 18, 2026, to complete MVP Southgate, which the FERC granted on December 19, 2023. Project opponents filed a request for rehearing of the FERC's December 19, 2023 order. On February 20, 2024, the FERC denied the rehearing request. The MVP Joint Venture is evaluating the permitting and regulatory roadmap for the project, including requesting an updated completion due date.

•Water Operations. During the year ended December 31, 2023, the Company invested approximately $45.7 million in its water infrastructure, primarily to continue to construct the initial mixed-use water system buildout. The Company placed portions of the initial mixed-use water system in service during 2022 and its second above ground water storage facility into service in July 2023, which brings its total water storage capacity to 350,000 barrels. During 2023, the Company completed the majority of the main trunkline pipelines on the mixed water system, including a pipeline that connects its two mixed water storage facilities. In May 2023, the Company executed an agreement with a producer customer to provide mixed-use water delivery service. The 10-year agreement is backed by a minimum volume commitment. For 2024, the Company expects to invest approximately $25 million to $35 million in its water operations, primarily related to the continued construction of its mixed-use water system buildout.

18

See "Sustainability and Corporate Responsibility" in Part II, "Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations" of this Annual Report on Form 10-K for a discussion of the Company's continued focus on sustainability matters which the Company believes will help to distinctively position the Company and create value.

Competitive Conditions. Key competitors for new natural gas gathering systems include companies that own major natural gas pipelines, independent gas gatherers and integrated energy companies. When compared to the Company or its customers, some of the Company's competitors have operations in multiple natural gas producing basins, have greater capital resources and access to, or control of, larger natural gas supplies. Natural gas producers that develop their own gas gathering systems or acquire such systems may also compete with the Company depending on the location of such systems relative to the Company's assets and existing agreements.

Competition for natural gas transmission and storage is primarily based on rates, customer commitment levels, timing, performance, commercial terms, reliability, service levels, location, reputation and fuel efficiencies. The Company's principal competitors in its transmission and storage market include companies that own major natural gas pipelines in the Marcellus and Utica Shales. In addition, the Company competes with companies that are building high-pressure gathering facilities that are able to transport natural gas to interstate pipelines without being subject to FERC jurisdiction. Major natural gas transmission companies that compete with the Company also have storage facilities connected to their transmission systems that compete with certain of the Company's storage facilities.

Key competition for water services includes natural gas producers that develop their own water distribution systems in lieu of employing the Company's water services assets and other natural gas midstream companies that offer water services. The Company's ability to attract customers to its water service business depends on its ability to evaluate and select suitable projects and to consummate transactions in a highly competitive environment.

Further, natural gas as a fuel competes with other forms of energy available to end-users, including coal, certain liquid fuels and, increasingly, renewable and alternative energy. Demand for renewable and alternative energy is increasing generally with changes in consumer preferences, governmental clean energy policies, and as renewable and alternative energy becomes more cost competitive with traditional fuels (including by technological advancement, legislation or government subsidies, as well as traditional supply and demand dynamics) and more widely available. Continued increases in the demand for renewable and alternative energy at the expense of natural gas (or increases in the demand for other sources of energy, particularly if prices for natural gas are elevated relative to other forms of energy as fuel) could lead to a reduction in demand for natural gas gathering, transmission and storage, and water services.

See also “Increased competition from other companies that provide gathering, transmission and storage, and water services, or from alternative fuel or energy sources, could negatively impact demand for our services, which could adversely affect our financial results.” included in Part I, "Item 1A. Risk Factors" of this Annual Report on Form 10-K.

Regulatory Environment

FERC Regulation. The Company's interstate natural gas transmission and storage operations are regulated by the FERC under the Natural Gas Act of 1938, as amended (NGA), the Natural Gas Policy Act of 1978, as amended (NGPA), and the regulations, rules and policies promulgated under those and other statutes. The Company's FERC-regulated operations are pursuant to tariffs approved by the FERC that establish rates (other than market-based rate authority), cost recovery mechanisms and terms and conditions of service to its customers. Generally, the FERC's authority extends to:

•rates and charges for the Company's natural gas transmission and storage services;

•certification and construction of new interstate transmission and storage facilities;

•abandonment of interstate transmission and storage services and facilities;

•maintenance of accounts and records;

•relationships between pipelines and certain affiliates;

•terms and conditions of services and service contracts with customers;

•depreciation and amortization policies;

•acquisitions and dispositions of interstate transmission and storage facilities; and

•initiation and discontinuation of interstate transmission and storage services.

19

The FERC regulates the rates and charges for transmission and storage in interstate commerce. Unless market-based rates have been approved by the FERC, the maximum applicable recourse rates and terms and conditions for service are set forth in the pipeline's FERC-approved tariff. Generally, the maximum filed recourse rates for interstate pipelines are based on the cost of providing service, including the recovery of a return on the pipeline's actual and prudent historical investment costs. Key determinants in the ratemaking process include the depreciated capital costs of the facilities, the costs of providing service, the allowed rate of return and income tax allowance, as well as volume throughput and contractual capacity commitment assumptions.

Interstate pipelines may not charge rates or impose terms and conditions of service that, upon review by the FERC, are found to be unjust or unreasonable, unduly discriminatory or preferential. Rate design and the allocation of costs also can affect a pipeline's profitability. While the ratemaking process establishes the maximum rate that can be charged, interstate pipelines such as the Company's transmission and storage system are permitted to discount their firm and interruptible rates without further FERC authorization down to a specified minimum level, provided they do not unduly discriminate. In addition, pipelines are allowed to negotiate different rates with their customers, under certain circumstances. Changes to rates or terms and conditions of service, and contracts can be proposed by a pipeline company under Section 4 of the NGA, or the existing interstate transmission and storage rates, terms and conditions of service and/or contracts may be challenged by a complaint filed by interested persons including customers, state agencies or the FERC under Section 5 of the NGA. Rate increases proposed by a pipeline may be allowed to become effective subject to refund and/or a period of suspension, while rates or terms and conditions of service that are the subject of a complaint under Section 5 of the NGA are subject to prospective change by the FERC. Rate increases proposed by a regulated interstate pipeline may be challenged and such increases may ultimately be rejected by the FERC.

The Company's interstate pipeline may also use negotiated rates that could involve rates above or below the recourse rate or rates that are subject to a different rate structure than the rates specified in the Company's interstate pipeline tariffs, provided that the affected customers are willing to agree to such rates and that the FERC has approved the negotiated rate agreement. A prerequisite for allowing the negotiated rates is that negotiated rate customers must have had the option to take service under the pipeline's recourse rates. As of December 31, 2023, approximately 97% of the system's contracted firm transmission capacity was subscribed by customers under negotiated rate agreements under its tariff. Some negotiated rate transactions are designed to fix the negotiated rate for the term of the firm transportation agreement and the fixed rate is generally not subject to adjustment for increased or decreased costs occurring during the contract term.

The FERC’s regulations also extend to the terms and conditions set forth in agreements for transmission and storage services executed between interstate pipelines and their customers. These service agreements are required to conform, in all material respects, with the form of service agreements set forth in the pipeline's FERC-approved tariff. Non-conforming agreements must be filed with and accepted by the FERC. In the event that the FERC finds that an agreement is materially non-conforming, in whole or in part, it could reject, or require the Company to seek modification of, the agreement, or alternatively require the Company to modify its tariff so that the non-conforming provisions are generally available to all customers or class of customers.

The FERC’s jurisdiction also extends to the certification and construction of new interstate transmission and storage facilities, including, but not limited to, acquisitions, facility replacements and upgrades, expansions, and abandonment of facilities and services. Prior to commencing construction of new or existing interstate transmission and storage facilities, an interstate pipeline must obtain (except in certain circumstances, such as where the activity is permitted under the FERC’s regulations or is authorized under the operator’s existing blanket certificate issued by the FERC) a certificate authorizing the construction, or file to amend its existing certificate, from the FERC.