UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

__________________________

FORM 10-K

__________________________

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2022

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from_____to_____

Commission File Number 001-38636

__________________________

(Exact name of registrant as specified in its charter)

__________________________

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of Principal Executive Offices) | (Zip Code) | |||||||

+41 21 695 30 00

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | ☒ | ||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant was approximately $501 million based on the closing price of its shares of Common Stock, par value $0.001 per share, on the Nasdaq Global Select Market on June 30, 2022, the last business day of the registrant’s second fiscal quarter.

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☒ No ☐

As of February 8, 2023, the registrant had 64,842,997 shares of common stock, $0.001 par value, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Table of Contents

| Page | ||||||||

| Item 9C. | ||||||||

3

BASIS OF PRESENTATION

Unless the context otherwise requires, references to “Garrett,” “we,” “us,” “our,” and “the Company” in this Annual Report on Form 10-K refer to Garrett Motion Inc. and its subsidiaries.

The accompanying consolidated financial statements of Garrett reflect the consolidated results of operations, financial position and cash flows of Garrett, in conformity with accounting principles generally accepted in the United States of America (“U.S. GAAP” or "GAAP").

Throughout this Annual Report on Form 10-K, we reference certain industry sources. While we believe the compound annual growth rate (“CAGR”) and other projections of the industry sources referenced in this Annual Report on Form 10-K are reasonable, forecasts based upon such data involve inherent uncertainties, and actual outcomes are subject to change based upon various factors beyond our control. All data from industry sources is provided as of the latest practicable date prior to the filing of this Annual Report on Form 10-K and may be subject to change.

4

| CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS | ||

This Annual Report on Form 10-K (this "Annual Report") contains forward-looking statements. We intend such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended ("the Securities Act"). All statements other than statements of historical fact contained in this Annual Report, including without limitation statements regarding our future results of operations and financial position, expectations regarding the growth of the turbocharger and electric vehicle markets and other industry trends, the sufficiency of our cash and cash equivalents, anticipated sources and uses of cash, anticipated investments in our business, our business strategy, pending litigation, anticipated interest expense, and the plans and objectives of management for future operations and capital expenditures are forward-looking statements. These statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. In some cases, you can identify forward-looking statements by terms such as “may,” “will,” “should,” “expect,” “plan,” “anticipate,” “could,” “intend,” “target,” “project,” “contemplate,” “believe,” “estimate,” “predict,” “potential,” or “continue” or the negative of these terms or other similar expressions. The forward-looking statements in this Annual Report are only predictions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition and results of operations. These forward-looking statements speak only as of the date of this Annual Report and are subject to a number of important factors that could cause actual results to differ materially from those in the forward-looking statements, including the factors described in Part I, Item 1A. “Risk Factors,” of this Annual Report and in our other filings with the Securities and Exchange Commission (the "SEC").

You should read this Annual Report and the documents that we reference herein completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements. Except as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained herein, whether as a result of any new information, future events, changed circumstances or otherwise.

5

PART I

Item 1. Business

Our Company

Garrett designs, manufactures and sells highly engineered turbocharger and electric-boosting technologies for light and commercial vehicle original equipment manufacturers (“OEMs”) and the global vehicle independent aftermarket as well as automotive software solutions. These OEMs, in turn, ship to consumers globally. We are a global technology leader with significant expertise in delivering products for internal combustion engines ("ICE") using gasoline, diesel, natural gas and electrified powertrains (hybrid and fuel cell). Additionally, we are currently in the development stage of turbochargers for internal combustion engines using hydrogen as fuel and other highly engineered components for zero emission vehicles. These products are key enablers for fuel (and/or energy) economy and emissions standards compliance.

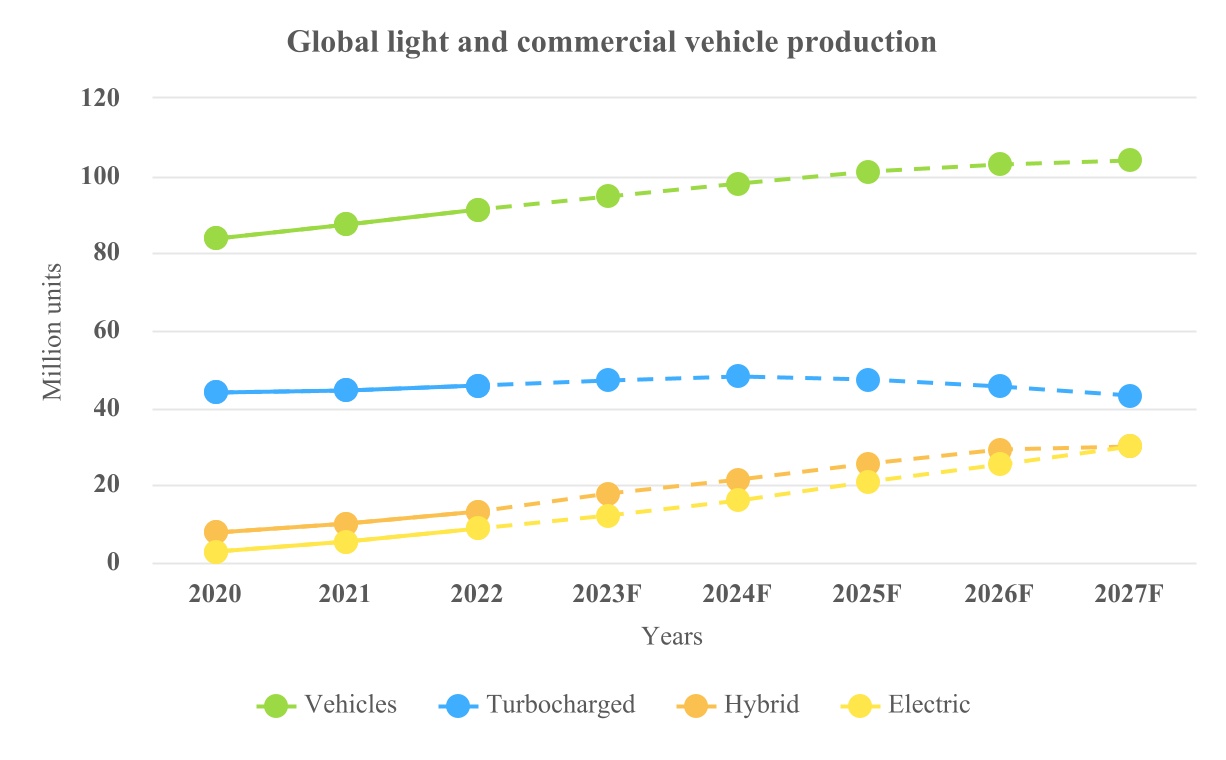

The turbocharger industry is expected to increase from approximately 46 million units in 2022 to approximately 48 million units by 2024, then gradually plateau and drop to approximately 41 million units by 2028, according to S&P ("S&P", formerly IHS) for light vehicles and Knibb, Gormezano and Partners ("KGP") and Power Systems Research ("PSR") for on-highway and off-highway commercial vehicles. The turbocharger industry growth is mainly driven in the short and medium term by an expected increase in the penetration of hybrid vehicles, from approximately 13 million hybrid cars globally in 2022 to an anticipated 29 million hybrid cars globally in 2026.

In 2022, a significant increase in battery electric vehicle (“BEV”) production has been observed in Europe and China, with BEV representing, respectively, 8% and 18% of light vehicles produced. In China, renewed sales incentives, especially in Tier 2 and Tier 3 cities, as well as non-financial incentives such as more generous license-plate quotas for major metropolitan areas, have bolstered Chinese BEV penetration. In the long-term, the proposal in the European Union ("E.U.") for all new cars to be zero-emission at tail pipe by 2035, as well as local regulations, could drive a further increase of BEV penetration in Europe beyond currently forecasted levels. In the United States of America ("US" or "United States"), the tightening of CO2/mileage targets is expected to drive higher turbo penetration in the short to medium-term. The President of the United States signed an executive order with the goal of making half of all new vehicles sold in 2030 zero-emissions vehicles, including battery electric, plug-in hybrid electric, or fuel cell electric vehicles, which is expected to accelerate the electrification trend in the mid-to-long term. Garrett's portfolio for hybrid powertrains includes new electric boosting solutions that leverage our unique technologies for electrical high speed boosting machinery. Garrett's product portfolio also includes fuel cell compressors for which we are developing the third generation. We are well positioned to take advantage of growing opportunities especially in the application of commercial vehicles. In China, the roadmap released by the China Society of Automotive Engineers, Energy-saving and New Energy Vehicle Technology Roadmap 2.0, outlines a technology path for the next ten years that aims to find a balance between fuel consumption improvement for hybrids and the introduction of electric vehicles. In that context, the turbocharger industry is expected to keep contributing to fuel economy optimization of gasoline, diesel vehicles and hybrid vehicles.

In the short to medium term, we continue to believe that turbocharger demand will grow as turbochargers remain one of the most cost-efficient levers to improve the fuel efficiency of gasoline, diesel and hybrid vehicles. In 2021, Garrett won the prestigious Automotive News PACE™ award for the industry's first E-turbo that successfully launched in 2022. The unique high speed electric motor technology developed for this product came from Garrett's fuel cell compressors that are required by fuel cell vehicles. Additionally, this technology also offers opportunities for new products to support all types of electrified drivetrains. In the commercial vehicle industry, we expect a slower transition to BEVs due to the requirements of specific applications and associated range and charging time constraints, which translates into more resilient turbocharger demand, as most commercial vehicles are turbocharged. In addition, low or zero emission alternative fuels for ICE, like natural gas or hydrogen, are expected to gain momentum in coming years, supporting continued turbocharger demand. Growth in the turbocharger industry is expected globally, with special mention for high-growth regions in Asia, where rising income levels continue to drive long-term automotive demand. While these positive factors do not isolate the turbocharger industry from fluctuations in global vehicle production volumes, such factors may assist in mitigating the negative impact of macroeconomic cycles. In addition, approximately 30% of our revenue comes from commercial vehicle and aftermarket sales that are less sensitive to the trend of electrification.

Emergence from Chapter 11

On September 20, 2020 (the “Petition Date”), the Company and certain of its subsidiaries (collectively, the “Debtors”) each filed a voluntary petition for relief under chapter 11 of title 11 of the United States Code (the “Bankruptcy Code”) in the United States Bankruptcy Court for the Southern District of New York (the “Bankruptcy Court”). The

6

Debtors’ chapter 11 cases (the “Chapter 11 Cases”) were jointly administered under the caption “In re: Garrett Motion Inc., 20-12212.” On April 20, 2021, the Debtors filed the Revised Amended Plan of Reorganization (the “Plan”). On April 26, 2021, the Bankruptcy Court entered an order (the “Confirmation Order”) among other things, confirming the Plan. On April 30, 2021 (the “Effective Date”), the conditions to the effectiveness of the Plan were satisfied or waived and the Company emerged from bankruptcy (the "Emergence").

Macroeconomic disruptions

The automotive industry continues to be impacted by uncertainty due to worldwide semiconductor shortages, the Covid-19 pandemic, governmental responses to the pandemic including the lockdown measures in China, and geopolitical tensions. The semiconductor shortage is expected to continue into 2023 although to a lesser extent compared to the previous year, and production levels may be reduced further should Covid-related lockdown measures persist or extend. The evolution of geopolitical conflicts and the consequent energy shortage in Europe, especially during the winter season, may further expose supply related challenges for the automotive industry while adding inflationary pressure and triggering recessionary scenarios. The Company continues to review production levels at OEM plants and closely monitor supply-chain disruptions related to logistics and component shortages in order to minimize the impact of the bottleneck in supply and mitigate any potential disruption in production. Additionally, we have in place procedures for the monitoring of supplier risks and we believe we have substantially addressed such risks with manageable economic impacts including use of premium freight or adjusted payment terms that are limited in time. We have prepared contingency plans for multiple scenarios that we believe will allow us to react swiftly to changes in customer demand while protecting Garrett’s long-term growth potential. See "- Risks Relating to our Business - Volatility in the cost and availability of raw materials, components, energy and transportation, in addition to disruptions in the supply chain, including supplier insolvency, has increased, and may continue to increase, the cost of our products and services, and may impact our ability to meet commitments to customers and cause us to incur significant liabilities." - in Item 1A - Risk Factors of this Annual Report.

Analyst consensus for the full year 2022 estimates growth of approximately 6% in global light vehicle production and approximately 15% drop in commercial vehicle production. As for the turbocharger industry, a 5% increase for the combined light and commercial vehicle turbocharger industry volume occurred in 2022. In 2023, 4% growth is expected by S&P for light vehicle production, and commercial vehicles are expected by KGP and PSR to grow at 5%. We have prepared contingency plans for multiple scenarios that we believe will allow us to react swiftly to changes in customer demand while protecting Garrett’s long-term growth potential. The supplies needed for our operations were generally available throughout 2022. In limited circumstances, certain suppliers experienced financial distress during 2022, resulting in supply disruptions. However, we had implemented new procedures in 2021 for monitoring of supplier risks associated with Covid-19 and we believe we have substantially addressed such risks with manageable economic impacts including use of premium freight or adjusted payment terms that are limited in time. As the global supply chain restarts, it is possible that additional supply constraints will appear for the industry. In addition, we sustained cost control measures and cash management actions in 2022 including:

•Postponing capital expenditures;

•Optimizing working capital requirements;

•Lowering discretionary spending;

•Flexing organizational costs by implementing short-term working schemes;

•Reducing temporary workforce and contract service workers; and

•Restricting external hiring.

The following charts show our percentage of revenues by geographic region and product line for the years ended December 31, 2022, 2021 and 2020, and the percentage changes from the prior years.

7

Revenue Summary

| By Geography | ||

| North America | Europe | Asia | Other | ||||||||||||||||||||

•We are a global business that generated revenues of approximately $3.6 billion in 2022.

•In 2022, our OEM sales contributed approximately 86% of our revenues while our aftermarket and other products contributed 14%.

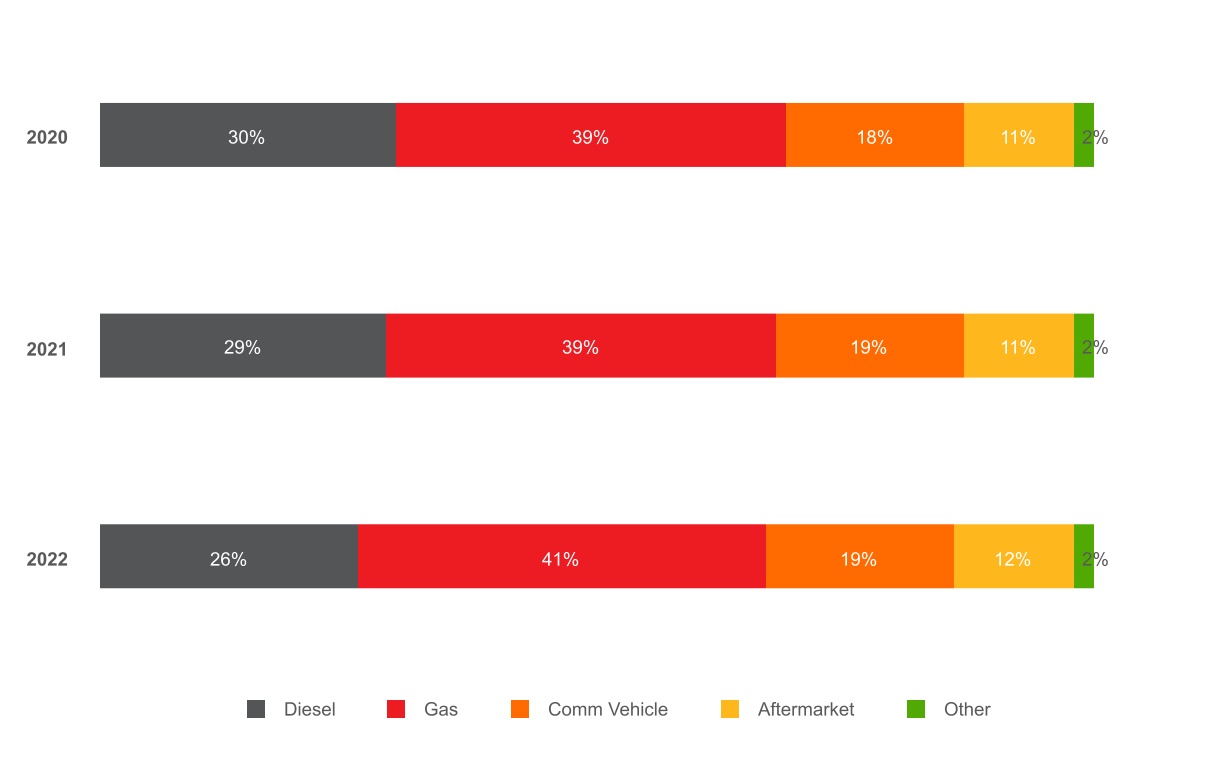

•Amongst OEM sales, light vehicle products (products for passenger cars, SUVs, light trucks, and other products) accounted for approximately 78% of our revenues. Commercial vehicle products (products for on-highway trucks and off-highway trucks, construction, agriculture and power-generation machines) accounted for 22%.

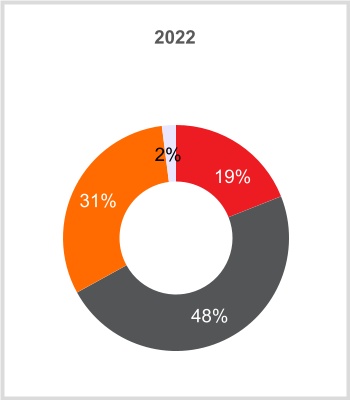

•Approximately 48% of our 2022 revenues came from sales shipped from Europe, 31% from sales shipped from Asia and 19% from sales shipped from North America. For more information, see Note 27, Concentrations, of the Notes to our Consolidated Financial Statements.

8

Our Industry

We currently compete in the global turbocharger industry for gasoline, diesel and natural gas engines, in the electric-boosting industry for electrified (hybrid and fuel cell) vehicle powertrains and in the emerging connected vehicle software industry. As vehicles become more electrified, our electric-boosting products use principles similar to our turbochargers to further optimize air intake and thus further enhance performance, fuel economy and exhaust emissions with the help of an integrated high-speed electric motor. By using a turbocharger or electric-boosting technology, an OEM can deploy smaller, lighter powertrains with better fuel economy and exhaust emissions while delivering the same power and acceleration as larger, heavier powertrains. As such, turbochargers have become one of the most highly effective technologies for helping global OEMs meet increasingly stricter emission standards. At the same time, we have developed unique technological competencies, which we aim to continue leveraging to solve our customers’ energy related challenges in the electrification evolution related to ICE, hybrids and electric powertrains. We are developing solutions and increasing our research and development ("R&D") spend, focusing more than 50% of total R&D expenditure in 2023 on electrification technologies like fuel cell compressors for a broad range of stack power (40kW to 250kW) and high value electric vehicle components. We are also continuing to develop Model Predictive Controls ("MPC") algorithms and cybersecurity software solutions that leverage our knowledge of vehicle powertrains and experience working closely with OEM manufacturers.

Global Turbocharger Industry

The global turbocharger industry includes turbochargers for new light and commercial vehicles as well as turbochargers for replacement use in the global aftermarket. According to S&P, KGP and PSR, the global turbocharger industry consisted of approximately 46 million turbocharged vehicles with an estimated total value of approximately $10 billion in 2022. Within the global turbocharger industry in 2022, light vehicles accounted for approximately 86% of total unit volume and commercial vehicles accounted for the remaining 14%.

S&P, KGP and PSR project that the turbocharger production volume will peak in 2024 and return to 2022 levels by 2026, driven mainly by turbochargers for light vehicle gasoline engines and continued slow growth for commercial vehicles, offset by a decline in diesel turbochargers given a decline in diesel powertrains, particularly for light vehicles. This annual sales estimate would add 230 million new turbocharged vehicles on the road globally between 2023 and 2027.

Key trends affecting our industry

Current global economic conditions due to Covid-19 and geopolitical conflicts have adversely affected and may continue to adversely affect many industries including the automotive sector. Chip shortages and rising raw material prices and inflation also had significant impacts on the automotive industry, making it unable to serve the recovery in demand. Consequently, S&P reduced its light vehicle production volume forecast for 2023 from approximately 91 million units that they forecasted in 2021 to between 80 to 88 million units in their January 2023 light vehicle industry production volume forecast.

Growth in overall vehicle production. After an increase of 3% in light vehicle production and 1% in commercial vehicle production in 2021, a stronger growth was expected in 2022. However, supply chain disruptions, driven by shortages in semiconductors and the continuous impact of Covid-19 particularly in China, affected vehicle production in 2022 resulting in flat volumes versus 2021. For 2023, S&P, KGP and PSR expect limited growth in light vehicle production and growth in commercial vehicle production of approximately 6%. However, significant uncertainty level remains with further Covid-19 waves, continued supply chain disruptions and geopolitical tensions. The shift from pure gasoline and diesel ICE to hybridized powertrains is expected to continue in response to increasingly strict fuel efficiency and regulatory standards. In parallel, the share of pure electric vehicles is expected to continue to increase from a low base as technology and supporting infrastructure continue to improve.

Global vehicle fuel efficiency and emissions standards. OEMs are facing increasingly strict constraints for vehicle fuel efficiency and emissions standards globally. Regulatory authorities in key vehicle regions such as the United States, the European Union, China, Japan, and Korea have instituted regulations that require sustained and significant reductions in greenhouse gas (including CO2 and NOx) and particulate matter vehicle emissions. OEMs are required to evaluate and adopt various solutions to address these stricter standards. Turbochargers allow OEMs to reduce engine size without sacrificing vehicle performance, thereby increasing fuel efficiency and decreasing harmful emissions. Furthermore, turbochargers allow more precise “air control” over both engine intake and exhaust conditions such as gas pressures, flows and temperatures, enabling optimization of the combustion process. This combustion optimization is critical to engine efficiency, exhaust emissions, power and transient response and enables such concepts as exhaust gas recirculation for diesel engines and Miller-cycle operation for gasoline engines. Consequently, we believe turbocharging will continue to be

9

a key technology for automakers to meet future tough fuel economy and emissions standards without sacrificing performance.

Turbocharger penetration. The utilization of turbochargers and electric-boosting technologies on vehicle powertrain systems is one of the most cost-effective solutions to address stricter standards, and OEMs are increasing their adoption of these technologies. S&P, KGP and PSR expect total turbocharger penetration to increase globally from approximately 46 million units in 2022 to approximately 48 million units by 2024; after this year, the turbocharger penetration will plateau then start decreasing based on current expectations on hybrid solutions adopted by different OEMs, reaching the same volumes from 2022 in 2026. S&P forecasts turbocharger penetration growth for gasoline turbochargers, expecting an increase in light vehicles from approximately 47% in 2022 to 51% in 2025.

Medium-Term Powertrain Trends

Note - Years 2020 - 2022 represent actual data and years 2023 - 2027 represent forecasted data.

Source: S&P, KGP, PSR

Engine size and complexity. In order to address stricter fuel economy standards, OEMs have used turbochargers to reduce the average engine size on their vehicles over time without compromising performance. Stricter pollutants emissions standards (primarily for NOx and particulates) have driven higher turbocharger adoption as well, which we believe will continue in the future, with a predicted total automotive turbocharger production volume CAGR of 1% between 2022 and 2025, in an industry with a predicted total automobile production volume CAGR of approximately 3% over the same period, in each case according to S&P, KGP and PSR.

Electrification. To address stricter fuel economy standards, OEMs also have been increasing the electrification of their vehicle offerings, primarily with the addition of hybrid vehicles, which have powertrains equipped with a gasoline or diesel internal combustion engine in combination with an electric motor. S&P estimates that hybrid vehicles produced globally will grow from a total of approximately 17.4 million vehicles in 2023 to 28.6 million vehicles by 2026, representing a CAGR of 17%. The electrified powertrain of hybrid vehicles enables the usage of highly synergistic electric-boosting technologies which augment standard turbochargers with electrically assisted boosting and electrical-generation capability. Furthermore, the application of electric boosting extends the requirement for engineering collaboration with OEMs to include electrical integration, software controls, and advanced sensing. Overall, this move to electric boosting further increases the role and value of turbocharging in improving vehicle fuel economy and exhaust emissions.

10

Battery electric and fuel cell technologies. OEMs are investing in full BEVs to comply with increasingly tight regulatory targets across regions. S&P, KGP and PSR expect that BEVs will compose 26% of total light and commercial vehicle production globally by 2026. Consumer adoption hinges on future "cost of range”, tightly linked to the energy capacity of the battery, but also how well that energy is used. Energy efficiency increases (including how to best address thermal management challenges), battery price (and consequently vehicle price), weight reduction through increases in power density, and shorter recharging times are all critical problems to solve. As OEMs strive to solve these issues, they are increasing investment in hydrogen fuel cell powered electric vehicles for demanding applications requiring long range, especially in the commercial vehicle space. These vehicles, like battery electric vehicles, have fully electric motor powertrains, but they rely on the hydrogen fuel cell to generate the required electricity. The hydrogen fuel cell also requires advanced electric-boosting technology to run efficiently and optimize range and cost of ownership. We are investing to address selected challenges raised by the electrification trend, where our differentiated technology can bring benefits related to lighter, more compact and more energy efficient components for electric vehicles.

Connected vehicles, software and controls. In addition to powertrain evolution, the connected vehicle industry is growing rapidly. Our MPC algorithms, predictive maintenance, diagnostics and cybersecurity tools address this industry. We expect their adoption will increase as advanced driver assistance features increase requirements for vehicle functional safety. Simultaneously, our cybersecurity solutions protect those vehicles against outside interference to ensure correct functionality.

Vehicle ownership in China, India and other high-growth regions. Vehicle ownership in China, India and other emerging regions remains well below ownership levels in developed areas and will be a key driver of future vehicle production. At the same time, these regions are following the lead of developed countries by instituting stricter emission standards. Growth in production volume and greater penetration by large global OEMs in these regions, along with evolving emission standards and increasing fuel economy and vehicle performance demands, is driving increasing turbocharger penetration in high-growth regions.

Our Competitive Strengths

We believe that we differentiate ourselves through the following competitive strengths:

Global and broad industry leadership

We are a global leader in the $10 billion OEM turbocharger industry. We believe we will continue to benefit from the increased adoption of turbochargers, as well as our global technology leadership, comprehensive portfolio, continuous product innovation and our deep-seated relationships with all global OEMs.

Light Vehicles

•Gasoline: The global adoption of turbochargers by OEMs on gasoline engines has increased rapidly from approximately 14% in 2013 to approximately 47% in 2022 and is forecasted by S&P to increase to 51% by 2025. In addition to the volume growth, tightening of CO2 regulations is driving a technology shift, moving away from standard waste gate technology to variable geometry turbo ("VNT") which is a premium technology that offers us technological competitive advantages. In 2016, we launched our first high volume VNT gasoline application, and this technology is expected to experience increased adoption in years to come. According to forecast by S&P, VNT should represent 10% of global turbo gasoline production by 2027, with 25% in Europe and 18% in China. In 2028, forecasted penetration maintains the same at a global level, with 25% in Europe and 19% in China. A key to our strategy for gasoline growth is thus to leverage our technology strengths in high-temperature materials and variable geometry as well as our scale, global footprint and in-market capabilities to meet the volume on technology demands of global OEMs.

•Diesel: We have a long history of technology leadership in diesel engine turbochargers. Despite diesel industry weakness for some vehicle segments, the majority of our diesel turbochargers revenue comes from heavier and bigger vehicles like SUVs, pickup trucks and light commercial vehicles (such as delivery vans), which remain a stable part of the diesel industry. Diesel maintains a unique advantage in terms of fuel consumption, hence cost of ownership, and towing capacity makes it the powertrain of choice for heavier vehicle applications. Diesel also remains essential for OEMs to meet their CO2 fleet average regulatory target going forward, as diesel vehicles produce less CO2 on average than gasoline vehicles.

•Electrified vehicles: We provide a comprehensive portfolio of turbocharger and electric-boosting technologies to manufacturers of hybrid-electric and fuel cell vehicles. OEMs have increased their adoption of these

11

electrified technologies given regulatory standards and consumer demands driving an expected CAGR globally of approximately 25% from 2022 to 2026, according to S&P. Similar to turbochargers for gasoline and diesel engines, turbochargers for hybrid vehicles are an essential component of maximizing fuel efficiency and overall engine performance. Our products provide OEMs with solutions that further optimize engine performance and position us well to serve OEMs as they add more electrified vehicles into their fleets.

Commercial vehicles. Our Company traces its roots to the 1950s when we helped develop a turbocharged commercial vehicle for Caterpillar. We have maintained our strategic relationship with key commercial vehicle OEMs for over 60 years as well as industry-leading positions across both on- and off-highway use. Our products improve engine performance and lower emissions on trucks, buses, agriculture equipment, construction equipment and mining equipment with engine sizes ranging 1.8L to 105L.

High-growth regions. We have a strong track record serving global and local OEMs, including customers in China and India, with an in-market and for-market strategy. We operate two R&D centers and three manufacturing facilities in these high-growth regions that serve light and commercial vehicle OEMs. Our local presence in high-growth regions has helped us win business with key international and domestic Chinese and Indian OEMs, and we grew significantly faster than the vehicle production in these regions between 2013 and 2022.

Strong and collaborative relationships with leading OEMs globally

We supply our products to more than 60 OEMs globally. Our top ten customers accounted for approximately 59% of net sales and our largest customer represented approximately 12% of our net sales in 2022. With over 60 years in the turbocharger industry, we have developed strong capabilities working with all major OEMs. We consistently meet their stringent design, performance and quality standards while achieving capacity and delivery timelines that are critical for customer success. Our track record of successful collaborations, as demonstrated by our strong client base and our ability to successfully launch multiple product applications annually, is well recognized. Our regional research, development and manufacturing capabilities are a key advantage in helping us to supply OEMs as they expand geographically and shift towards standardized engines and vehicle platforms globally.

Global aftermarket platform

Our Garrett aftermarket brand has strong recognition across distributors and garages globally, and is known for boosting performance, quality and reliability. We operate through a distribution network of more than 250 distributors covering 165 countries. Our aftermarket business has historically provided a stable stream of revenue supported by our large installed base, currently estimated at over 120 million vehicles. As turbocharger penetration rates continue to increase, we expect that our installed base and aftermarket opportunities will continue to grow.

Highly-engineered portfolio with continuous product innovation

We have led the revolution in turbocharging technology over the last 60 years and maintain a leading technology portfolio of approximately 1,700 patents and patents pending. We have a globally deployed team of more than 1,220 engineers across five R&D centers and 11 close-to-customer engineering centers. Our engineers have led the mainstream commercialization of several leading turbocharger innovations, including variable geometry turbines, dual-boost compressors, ball-bearing rotors, electrically actuated controls and air-bearing electric compressors for hydrogen fuel cells. We maintain a culture of continuous product innovation, introducing about ten new technologies per year and upgrading our existing key product lines approximately every 3 years. Outside of our turbocharger product lines, we apply this culture of continuous innovation to meet the needs of our customers in new areas, particularly in connected automotive technologies. We are developing solutions and increasing our R&D spend, focusing more than 50% of total R&D expenditure in 2023 on electrification technologies like fuel cell compressors for a broad range of stack power (40kW to 250kW) and high value electric vehicle components. We are also continuing to develop MPC algorithms and cybersecurity software solutions that leverage our knowledge of vehicle powertrains and experience working closely with OEM manufacturers.

Global and low cost manufacturing footprint with operational excellence

Our geographic footprint locates R&D, engineering and manufacturing capabilities close to our customers, enabling us to tailor technologies and products for the specific vehicle types sold in each geographic industry. In all regions where we operate, we leverage low-cost sourcing through our robust supplier development program, which continually works to develop new suppliers that are able to meet our specific quality, productivity and cost requirements. We now source more than two-thirds of our materials from low-cost countries and believe our high-quality, low-cost supplier network to be a

12

significant competitive advantage. We have invested heavily to bring differentiated local capabilities to our customers in high-growth regions, including China and India.

In 2022, we manufactured more than 87% of our products in low-cost countries, including seven manufacturing facilities in China, India, Mexico, Romania and Slovakia. We have a long-standing culture of lean manufacturing excellence and continuous productivity improvement. We believe global uniformity and operational excellence across facilities is a key competitive advantage in our industry given that OEM engine platforms are often designed centrally but manufactured locally, requiring suppliers to meet the exact same specifications across all locations.

Our Growth Strategies

Garrett invests in innovative technologies that address the needs of our customers in the ongoing auto industry transformation. This continued investment into differentiated technology, coupled with our relentless focus on customer relations and our global capabilities, allows us to drive the following business strategies:

Strengthen industry leadership across powertrain technologies

We are focused on strengthening our industry position in light vehicles:

•Gasoline turbochargers, which historically lagged adoption of diesel turbochargers, are expected to increase at a 2.1% annual CAGR from 2022 to 2025, according to S&P. We expect to benefit from this higher growth given the gasoline platforms we have been awarded over the past several years. We have launched the first modern 1.5L VNT gasoline application with a major OEM and we expect to see increasing adoption of this technology in years to come. Key to our strategy for gasoline growth is our plan to leverage our technology strengths in high temperature materials and variable geometry technologies as well as our scale, global footprint and in-region capabilities to meet the volume demands of global OEMs.

•We believe growth in our share of the diesel turbochargers industry will be driven by new product introductions focused on emissions-enforcement technologies and supported by our favorable positioning with large vehicles and high-growth regions within this industry. The more stringent emissions standards require greater turbocharger technology content such as variable geometry, 2-stage systems, advanced bearings and materials which increase our content per vehicle.

Leverage our differentiated technology to solve key challenges in electrification

We stand to benefit from the increased adoption of hybrid-electric and fuel cell vehicles and the increased need for turbochargers associated with increased sales volumes for these engine types. S&P estimates that the global production of electrified vehicles (ranging from mild-hybrids to plugin-hybrids to battery and fuel cell electric vehicles) will increase from approximately 22 million vehicles in 2022 to approximately 60 million vehicles by 2027, representing an annualized growth rate of approximately 18%. OEMs will need to further improve engine performance for their increasingly hybrid electrified offerings, and our comprehensive portfolio of turbocharger and electric-boosting technologies are designed to help OEMs do so. We expect to continue to invest in product innovations and new technologies and believe that we are well positioned to continue to be a technology-leader in the propulsion of electrified vehicles. As we keep strengthening our electrical know-how, we believe our capabilities and technological expertise can be pivoted in the electrification arena for selected electric powertrain opportunities.

Increase industry position in high-growth regions

In 2022, after a steep drop in the first quarter due to strict lockdowns, vehicle production in China continued to experience further challenges through the third quarter from supply chain disruptions caused by shortage of semiconductor components whereas fourth quarter recovery partly compensated for the decline in the first three quarters, with a 4% full year growth, aligned to average growth in the other regions. S&P expects vehicle production in China to be stable next year. We plan to continue to strengthen our relationships with OEMs in high-growth, emerging regions by demonstrating our technology leadership through our local research, development and manufacturing capabilities. We expect our local footprint to continue to provide a strong competitive edge in high-growth regions due to our ability to work closely with OEMs throughout all stages of the product lifecycle including aftermarket support. For example, in China, our research center in Shanghai, our manufacturing facilities in Wuhan and Shanghai and our 1,042 employees support our differentiated end-to-end capabilities and we believe will continue to support key platform wins in the Chinese market. Our operations in China are expected to continue to benefit us as OEMs build global platforms in low cost regions. Our

13

commitment to providing high-touch technology support to OEMs has allowed us to be recognized as a local player in other key high-growth regions, such as India.

Grow our aftermarket business

We have an opportunity to strengthen our global network of more than 250 distributors in 165 countries by deepening our channel penetration, leveraging our well-recognized Garrett brand, utilizing new online technologies for customer engagement and sales, and widening the product portfolio. Installer Connect, a global web-based platform providing self-service tools aimed at connecting garage technicians generated more than 15 thousand additional technicians certified, and our Turbo Service Replacement website attracted more than 800 thousand visitors. Additionally, the Garrett Web Racing & Performance section of our website attracted more than 1.4 million visitors in 2022.

Research, Development and Intellectual Property

We maintain technical engineering centers in major automotive production regions of the world to develop and provide advanced products, process and manufacturing support to all of our manufacturing sites, and to provide our customers with local engineering capabilities and design developments on a global basis. As of December 31, 2022, we employed approximately 1,260 engineers. Our total R&D expenses were $153 million, $136 million and $111 million for the years ended December 31, 2022, 2021 and 2020, respectively, with more than 50% of our total R&D spend in 2022 focused on electrification technologies. Additionally, the Company incurred engineering-related expenses which are also included in Cost of goods sold of $11 million, $22 million, and $13 million for the years ended December 31, 2022, 2021 and 2020, respectively.

We currently hold approximately 1,700 patents and patents pending. Our current patents are expected to expire between 2023 and 2041. While no individual patent or group of patents, taken alone, is considered material to our business, taken in the aggregate, these patents provide meaningful protection for our intellectual property.

Materials

The most significant raw materials we use to manufacture our products are grey iron, aluminum, stainless steel and a nickel-, iron- and chromium-based alloy. As of December 31, 2022, we have not experienced any significant shortage of raw materials and we or our suppliers (on our behalf) do not typically carry inventories of such raw materials in excess of those reasonably required to meet our production and shipping schedules.

Customers

Our global customer base includes nine of the ten largest light vehicle OEMs and nine of the ten largest commercial vehicle engine makers. Our ten largest applications in 2022 were with six different OEMs. OEM sales were approximately 86% of our 2022 revenues while our aftermarket and other products contributed 14%.

Our largest customer is Bayerische Motoren Werke AG (“BMW”). In 2022, 2021 and 2020, BMW accounted for 12%, 13%, and 11%, respectively, of our total sales. In 2022, 2021 and 2020, our sales to Ford Motor Company (“Ford”) were 10%, 10%, and 10%, respectively, of our total sales.

Supply Relationships with Our Customers

We typically supply products to our OEM customers through “open” purchase orders, which are generally governed by terms and conditions negotiated with each OEM. Although the terms and conditions vary from customer to customer, they typically contemplate a relationship under which our customers are not required to purchase a minimum amount of product from us. These relationships typically extend over the life of the related engine platform. Prices are negotiated with respect to each business award, which may be subject to adjustments under certain circumstances, such as commodity or foreign exchange escalation/de-escalation clauses or for cost reductions achieved by us. The terms and conditions typically provide that we are subject to a warranty on the products supplied. We may also be obligated to share in all or a part of recall costs if the OEM recalls its vehicles for defects attributable to our products.

Individual purchase orders are terminable for cause or non-performance and, in most cases, upon our insolvency and certain change of control events. In addition, many of our OEM customers have the option to terminate for convenience on certain programs, which permits our customers to impose pressure on pricing during the life of the vehicle program, and issue purchase contracts for less than the duration of the vehicle program, which potentially reduces our profit margins and increases the risk of our losing future sales under those purchase contracts. We manufacture, and ship based on customer

14

release schedules, normally provided on a weekly basis, which can vary due to cyclical automobile production or inventory levels throughout the supply chain.

Although customer programs typically extend to future periods, and although there is an expectation that we will supply certain levels of OEM production during such future periods, customer agreements including applicable terms and conditions do not necessarily constitute firm orders. Firm orders are generally limited to specific and authorized customer purchase order releases placed with our manufacturing and distribution centers for actual production and order fulfilment. Firm orders are typically fulfilled as promptly as possible from the conversion of available raw materials, sub-components and work-in-process inventory for OEM orders and from current on-hand finished goods inventory for aftermarket orders. The dollar amount of such purchase order releases on hand and not processed at any point in time is not believed to be significant based upon the time frame involved.

Regulatory and Environmental Compliance

We are subject to the requirements of environmental and health and safety laws and regulations in each country in which we operate. These include, among other things, laws regulating air emissions, water discharge, hazardous materials and waste management. We have an environmental management structure designed to facilitate and support our compliance with these requirements globally. Although it is our intent to comply with all such requirements and regulations, we cannot provide assurance that we are at all times in compliance. Environmental requirements are complex, change frequently and have tended to become more stringent over time. Accordingly, we cannot assure that environmental requirements will not change or become more stringent over time or that our eventual environmental costs and liabilities will not be material.

Certain environmental laws assess liability on current or previous owners or operators of real property for the cost of removal or remediation of hazardous substances. At this time, we are involved in various stages of investigation and cleanup related to environmental remediation matters at certain of our present and former facilities. In addition, there may be soil or groundwater contamination at several of our properties resulting from historical, ongoing or nearby activities.

As of December 31, 2022, the undiscounted reserve for environmental investigation and remediation was $17 million. We do not currently possess sufficient information to reasonably estimate the amounts of environmental liabilities to be recorded upon future completion of studies, litigation or settlements, and we cannot determine either the timing or the amount of the ultimate costs associated with environmental matters, which could be material to our consolidated results of operations and operating cash flows in the periods recognized or paid. However, considering our past experience and existing reserves, we do not expect that environmental matters will have a material adverse effect on our consolidated financial position.

Corporate Responsibility

Our Sustainability Approach

Garrett’s mission to enable cleaner, more efficient and connected vehicles is at the heart of our contribution to society. Our engineering expertise and transformative technologies help optimize fuel efficiency, reduce harmful emissions and manage growing vehicle complexity, all of which are critical areas on the road to a clean transportation future.

Our corporate sustainability framework, called WeCare4, starts from our mission to enable cleaner, more efficient vehicles by spearheading technology development and continuing to deliver industry-first innovations. It is built on two main pillars - investing in a culture of innovation and operating responsibly to ensure long-term impact.

We embed sustainability in our governance structure. Our Sustainability Committee, composed of the CEO and several members of Garrett’s senior leadership team, is sponsored by our Chief Technology Officer and oversees our sustainability strategy development, definition and deployment. Our Board of Directors, including its committees, provide Board oversight of our environment, social and governance ("ESG") activities, corporate responsibility and sustainability strategy. Primary responsibility at Board level for reviewing and reporting to the full Board on our sustainability programs and policies, as well as our corporate citizen commitments, resides with the Nominating & Governance Committee.

Garrett articulates its commitments to social and environmental considerations in the communities in which it operates in the Company’s Code of Business Conduct, which can be found on our website at www.garrettmotion.com under "About Us – Corporate – Sustainability". The Company published its fiscal year 2021 Sustainability Report in 2022, the content of which is not incorporated by reference into this Annual Report or in any other report or document we file with the SEC.

15

Human Capital

At Garrett, we place a high value on developing the right working environment and the right skillsets to advance our performance culture, support our growth strategy and ensure that the world at large can continue to benefit from breakthroughs in sustainable mobility. We invest in creating an inclusive, stimulating, and safe work environment where our employees can deliver their workplace best every day. As of December 31, 2022, we employed approximately 7,300 permanent employees and 2,000 temporary and contract workers globally.

Diversity, equity and inclusion

Diversity and Inclusion is one of Garrett’s four fundamentals. As such, we strive to ensure that our employees are each involved, supported, respected and connected. Embracing diverse thoughts and ideas through inclusion leads to a competitive advantage in the market, increased innovation as we generate new and better ideas, and customer-centric decision making. We pride ourselves that diversity is represented from the top of the organization, for example 25 different nationalities are represented in our senior management team and they bring with them a wide variety of different backgrounds and experiences. Overall, in our global workforce we have representation of approximately 60 different nationalities. As of December 31, 2022, Garrett's Board of Directors had 33% female representation.

In 2022, the Company continued to strengthen and develop its approach to diversity, equity and inclusion. Actions during the year included:

•Regular reporting and review of existing diversity and inclusion metrics and initiatives

•Work by 14 Diversity and Inclusion Champions in key countries to develop local Diversity and Inclusion initiatives suitable for the local context while aligning with the global strategy

•Holding Garrett’s annual Diversity and Inclusion Week in November based on the themes of Beyond Bias.

16

The percentage of female employees in Garrett was 21.8% in 2022. The percentage of female employees in Senior Management roles was 19.0% in 2022. Over the past four years, Garrett increased the percentage of female employees in Garrett by 5.8% (from 20.6% to 21.8%) and by 13.8% in Senior Management over the same four year period (from 16.7% to 19.0%).

The table below shows the evolution of our gender diversity representation over the last four years and our 2025 ambition:

| 2019 | 2020 | 2021 | 2022 | 2025 Ambition | ||||||||||||||||||||||||||||

| % Women in total workforce | 20.6% | 20.8% | 22.2% | 21.8% | 25.0% | |||||||||||||||||||||||||||

| % Women in Senior Management | 16.7% | 19.5% | 20.0% | 19.0% | 25.0% | |||||||||||||||||||||||||||

Talent Management

At Garrett, we encourage our employees to develop their skills and capabilities through a comprehensive Performance and Talent Management system. From annual goal-setting and performance reviews to learning opportunities for employees and leaders, the Company helps its people align their professional experience with the Company’s business objectives and encourages them to take ownership of their development and career paths.

Our learning environment offers employees access to more than 1,000 online trainings that address a wide range of functional competencies, technical skills, and human skills. Learning can be self-paced, while the Company’s growing online peer-to-peer learning communities also allow employees to easily access courses specific to their function and to share materials and ideas on topics of interest. A variety of instructor led virtual programs were deployed during 2022 to support employees' development and a number of dedicated programs for emerging and experienced leaders were successfully held. Approximately 80,000 hours of online training was delivered during 2022.

We use regular talent reviews to strengthen the Company’s internal development processes and to calibrate assessment of individual performance. Twice per year we hold succession planning meetings up to and including the executive level, during which the bench-strength of teams are scrutinized and development plans for their talent are reviewed. Ahead of both annual and mid-year performance reviews, leaders hold calibration meetings to ensure that assessment ratings are consistent and fair amongst peer groups.

Be well, work well

Health and Safety

World-class health and safety considerations are integrated into Garrett’s procedures and processes. Our management system aligns with the global standard ISO 45001 (and ISO 14001 and ISO 50 001) and provides protection of human health and safety during normal and emergency situations. Compliance with our standards and local regulatory requirements is monitored through a company-wide self-assessment process assured through annual audits. In 2022 we supplemented this with a rolling 4-year compliance audit against local regulations by a global service provider. The timely development and implementation of process improvement and corrective action plans are closely monitored.

As the Covid-19 pandemic started to recede in the first quarter of 2022, through government and international action, we transitioned to more normal working with continued support for the health and well being of our employees. This transition is now complete with the emergence of China from their zero-Covid policy.

Our safety performance was maintained in our Total Case Incident Rate (“TCIR”). TCIR is measured as the number of recordable injuries and illnesses multiplied by 200,000 and then that number is divided by the total number of hours worked by employees, TCIR was 0.12 in 2022, which is consistent with the TCIR in the previous three years.

Compensation and benefits

Garrett’s rewards programs are rooted in our “Be well, work well” principle, and aim to support employees in achieving the right work-life balance. We invest significant time and resources in establishing compensation programs that are both competitive and equitable. We constantly evaluate our positions for market competitiveness and adjust when necessary with the goal of ensuring the retention of top talent and continuation of equitable pay practices.

17

As part of our commitment to the well-being of our employees, the Company offers an Employee Assistance Program. It is an external counselling service designed to assist employees with personal, family, or workplace matters. This service is confidential and is also available to each employee’s dependents.

In late 2020, the Company made a number of well-being resources available to all its connected employees, including useful tools and techniques for managing mental and physical health, in addition to dedicated online events. These remained in place throughout 2021 and 2022.

Employee feedback, representation, and retention

Garrett’s Performance and Talent Management system aims to ensure that two-way dialogue is ongoing between employees and managers, punctuated by both an annual and a mid-year review, which provides employees the opportunity to express their opinions and ideas in terms of their development goals and career aspirations.

Garrett’s strategy is to build positive, direct, business-focused working relationships with all employees in order to drive business results. The Company respects employees’ rights and their wish to be part of employee representative bodies including unions, work councils and employee forums. The Company understands the value of collective bargaining in its labor and employee relations strategy and the importance of trust in its working relationships. Approximately 40% of the Company’s permanent employees (including both full-time and part-time employees) are represented by unions and works councils under current collective bargaining agreements.

The Company closely monitors employee turnover to measure retention and define improvement actions as and where necessary. As of December 31, 2022, the Company’s annual voluntary turnover for 2022 was 13.6%, which reflects the trends of the current global marketplace for talent. Garrett has developed a full set of actions to maximize retention that are carried out at both a global and local level, with line managers as well as functional leaders held accountable for their employee turnover performance. We intend to continue to work diligently on this area to mitigate against the challenges of a highly competitive global marketplace for talent.

Educating future innovators

Garrett places a high value on STEM research and learning opportunities that provide young people with the skills needed to develop the future of sustainable mobility. The Company sponsors higher education institutes in several countries to further critical research in technical areas and provide students with opportunities to study STEM programs.

Garrett’s Internship Programs enable students to connect theoretical knowledge with practical responsibilities in the spirit of ‘living laboratories’ during which they are encouraged to take ownership of business projects and define tactics to meet the project goals. In 2022, Garrett offered 261 internships in 11 countries, which is twice as many compared to 2021 (approximately 37% in Engineering, 32% in Integrated Supply Chain, 12% in IT and the remainder in Finance, HR, Marketing and Sales, Legal and Internal Audit).

Garrett runs a Graduate Program which in 2022 provided 25 graduates in 2 countries to gain experience and exposure to Garrett’s cutting-edge technologies while at the same time building their leadership skills in a fast-paced and professional work environment.

The Company sponsors Formula SAE and Formula Student teams in several countries providing the students in the racing team with leadership coaching, technical guidance, parts for the vehicle and financial support. Our engineers and leaders take part on Formula Student and Formula SAE races as judges and technical support. In 2022, the Company sponsored the European BEST Engineering Competition, the biggest international technical competition in Central Europe, where Garrett defined an assignment for over 50 students on a case study comparing pros and cons for a cooling unit with conventional pump and radial impeller driven compressor.

Garrett supports the local Universities globally with master thesis projects, class speakers and technical sharing events and is involved in the community supporting STEM activities for high schools worldwide. The Company continues to enhance the engagement with global organizations at the university focused on diversity students increasing intern and full time recruiting. Garrett works closely with leading Universities globally on over 10 collaboration projects that push the envelope of technical innovation.

18

Seasonality

Our business is typically moderately seasonal. Our primary North American customers historically reduce production during the month of July and halt operations for approximately one week in December; our European customers generally reduce production during the months of July and August and for one week in December; and our Chinese customers often reduce production during the period surrounding the Chinese New Year. Shut-down periods in the rest of the world generally vary by country. In addition, automotive production is traditionally reduced in the months of July, August and September due to the launch of parts production for new vehicle models. Accordingly, our results reflect this seasonality. Our sales predictability in the short term might also be impacted by sudden changes in customer demand, driven by our OEM customers’ supply chain management.

We also typically experience seasonality in cash flow, as a relatively small portion of our full year cash flow is typically generated in the first quarter of the year and a relatively large portion in the last quarter. This seasonality in cash flow is mostly caused by timing of supplier payments for capital expenditures, changes in working capital balances related to the sales seasonality discussed above, and incentive payments.

Cybersecurity

Cybersecurity and protection of our data is a top priority across the entire organization. To that end, we take a holistic approach to securing our data and business systems from attack, compromise or loss. The Company's cybersecurity objective is to protect Garrett data privacy, information theft, and protection from external and insider cyber threats. This includes the combination of leading technologies, policies, and procedures, and the Company’s Security Operation Center (“SOC”).

The Company's SOC provides visibility across all information technology assets and includes proactive cyber security Threat Detection Technology to facilities the identification of misconfigurations to mitigate threats and prevent data loss. As part of the Company’s holistic approach to cybersecurity, there are incremental programs and technology associated with threat hunting, vulnerability scanning and threat detection and response technology. We continually evaluate risks, threats, intelligence feeds and vulnerabilities to adapt, mitigate or respond as necessary to preserve a secure state. Combining technology, processes, and threat intelligence we deliver specific and timely education and training to the organization, including mandatory training for all employees.

While Garrett focuses heavily on prevention and detection, response and recovery plans, service agreements and partner engagements are in place should there be a need for us to respond to an attack. There have been no material cybersecurity events during the year ended December 31, 2022.

Additional Information

Our Annual Reports on Form 10-K, including this Annual Report, our Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, as well as all amendments and other reports filed with or furnished to the SEC, are also available free of charge on our internet site at https://www.garrettmotion.com as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The contents of our internet site are not incorporated by reference into this Annual Report. The SEC maintains a website at SEC.gov that contains reports, proxy and information statements, and other information regarding issuers that file with the SEC, including our Company.

Item 1A. Risk Factors

You should carefully consider all of the information in this Annual Report on Form 10-K and each of the risks described below, which we believe are the principal risks we face. Any of the following risks could materially and adversely affect our business, financial condition and results of operations and the actual outcome of matters as to which forward-looking statements are made in this Annual Report on Form 10-K. Other events that we do not currently anticipate or that we currently deem immaterial may also affect our business, prospects, financial condition and results of operations.

Risks Relating to our Business:

Volatility in the cost and availability of raw materials, components, energy and transportation, in addition to disruptions in the supply chain, including supplier insolvency, has increased, and may continue to increase, the cost of our products and services, and may impact our ability to meet commitments to customers and cause us to incur significant liabilities.

19

We have experienced, and may continue to experience, volatility in the cost and availability of raw materials, components, energy and transportation as a result of a broad range of factors beyond our control including, but not limited to, pandemics, general inflation and geopolitical tensions caused by armed conflict. If we are unable to pass through increased costs of raw materials, components, energy and transportation to our customers, or are otherwise unable to mitigate these cost increases, this could have an adverse effect on our results of operations and financial condition. Furthermore, if we are unable to overcome significant disruptions in the supply chain, such as those caused by the shortage of semiconductor chips and global logistical constraints currently impacting the automotive industry, it could adversely impact our business.

Short- or long-term capacity constraints, insufficient quality control, financial distress or significant changes in business conditions at any point in our supply chain could disrupt our operations and adversely affect our financial performance, particularly when the affected suppliers and vendors are the sole sources of products that we require or that have unique capabilities, or when our customers have directed us to use those specific suppliers and vendors. A significant portion of our supply chain is located in mainland China. Our ability to manage inventory and meet delivery requirements may be constrained by our suppliers’ inability to scale production and adjust delivery of long-lead time products during times of volatile demand. If our third-party manufacturers fail to deliver products, parts and components of sufficient quality on time and at reasonable prices, we could have difficulties fulfilling our orders on similar terms or at all, sales and profits could decline, and our commercial reputation could be damaged. If we fail to adequately assess the creditworthiness and operational reliability of existing or future suppliers, our suppliers become insolvent, if there is any unanticipated deterioration in their creditworthiness and operational reliability, or if they do not perform or adhere to our existing or future contractual arrangements, any resulting increase in non performance by them, our inability to otherwise obtain the supplies or our inability to enforce the terms of the contract or seek other remedies could have a material adverse effect on our financial condition and results of operations. Changes or additions to our supply chain require considerable time and resources and involve significant risks and uncertainties. Our inability to fill our supply needs would jeopardize our ability to fulfil obligations under commercial contracts, and could result in reduced sales and profits, contract penalties or terminations, and damage to customer relationships.

The Company relies on sales to major customers as well as a network of independent dealers to manage the distribution of its products, and we could be adversely impacted by the loss of any of our such major customers or dealers, changes in their requirements for our products or changes in their financial condition.

Changes in our business relationships with any of our major customers or in the timing, size and continuation of their various programs could have a material adverse impact on us. The loss of any of these customers, the loss of business with respect to one or more of their vehicle models on which we have high component content, or a significant decline in the production levels of such vehicles would negatively impact our business, results of operations and financial condition. Pricing pressure from our customers also poses certain risks. Inability on our part to offset pricing concessions with cost reductions would adversely affect our profitability. We are continually bidding on new business with these customers, as well as seeking to diversify our customer base, but there is no assurance that our efforts will be successful. Further, to the extent that the financial condition of our largest customers deteriorates, including possible bankruptcies, mergers or liquidations, or their sales otherwise decline, our financial position and results of operations could be adversely affected.

If our dealers are unsuccessful with their sales and business operations, it could have an adverse effect on overall sales and revenue. We rely on the capability of our independent dealers to develop and implement effective sales plans to create demand among purchasers for the equipment and related products and services that the dealers purchase from us. If our dealers are not successful in these endeavors, then we will be unable to grow our sales and revenue, which would have an adverse effect on our financial condition. In addition, the dealer channel’s ability to support and service precision technology solutions and emerging power solutions may affect customers’ acceptance and adoption rates of these products.

Dealers may have trouble funding their day-to-day cash flow needs and paying their obligations due to adverse business conditions resulting from negative economic effects or other factors. Dealers may exit relationships with us or we may seek to terminate relationships with certain dealers if they are unable to meet customer needs. The unplanned loss of any of our dealers could lead to inadequate market coverage, negative customer impressions of us, and may adversely impact our ability to collect receivables that are associated with that dealer.

We may not be able to successfully negotiate favorable pricing terms with our customers, which may adversely affect our results of operations.

There is substantial and continuing pressure on OEMs to reduce costs, including the costs of the products we supply. We negotiate sales prices annually with our automotive customers. Our customer supply agreements generally require step-

20

downs in component pricing over the period of production. In addition, our customers often reserve the right to terminate their supply contracts at any time, which enhances their ability to obtain price reductions. OEMs have also exercised significant influence over their suppliers, including us, because the automotive component supply industry is highly competitive and serves a limited number of customers. Based on these factors, our status as a Tier I supplier (one that supplies vehicle components directly to manufacturers) and the fact that our customers’ product programs typically last a number of years and are anticipated to encompass large volumes, our customers are able to negotiate favorable pricing, and any cost-cutting initiatives that our customers adopt generally will result in increased downward pressure on our pricing. Any resulting impacts to our sales levels and margins, could over time significantly reduce our revenues and adversely affect our competitive standing and prospects. Additionally, large commercial settlements with our customers may adversely affect our results of operations.

The automotive industry is evolving and if we are unable, or perceived as unable, to respond appropriately to such evolution, our financial condition and results of operation could be adversely impacted.

The sales and margins of our business are directly impacted by government regulations, including safety, performance and product certification regulations, particularly with respect to emissions, fuel economy and energy efficiency standards for motor vehicles. Increased public awareness and concern regarding global climate change may result in more regional and/or federal requirements to reduce or mitigate the effects of greenhouse gas emissions. While such requirements can promote increased demand for our turbochargers and other products, several markets in which we operate are undertaking efforts to more strictly regulate or ban vehicles powered by certain older-generation diesel engines. If such efforts are pursued more broadly throughout the market than we have anticipated, such efforts may impact demand for our aftermarket products. Changes in demand and emerging needs of customers that are not perceived adequately in advance and/or incorporated in the product development process (e.g., demand for eco-compatible products) may result in lower sales volumes and consequently affect our results of operations.

Even if overall automotive sales and production remain stable, changes in regulations and consumer preferences may shift consumer demand away from the types of vehicles we prioritize or towards the types of vehicles where our products generate smaller profit margins. A decrease in consumer demand for the specific types of vehicles that have traditionally included our turbocharger products, such as a decrease in demand for diesel-fueled vehicles in favor of gasoline-fueled vehicles, or lower-than-expected consumer demand for specific types of vehicles where we anticipate providing significant components as part of our strategic growth plan, such as a decrease in demand for vehicles utilizing electric-hybrid and fuel cell powertrains in favor of full battery electric vehicles, could have a significant effect on our business. If we are unable to anticipate significant changes in consumer sentiment, or if consumer demand for certain vehicle types changes more than we expect, our results of operations and financial condition could be adversely affected. Furthermore, if we are unable to maintain our competitive advantage through innovation, if we do not sustain our ability to meet customer requirements relative to technology, or we fail to be awarded new business, there could be a material adverse effect on our results of operations, financial condition and future business prospects.

Sales in our aftermarket operations are also directly related to consumer demand and spending for automotive aftermarket products, which may be affected by additional factors such as the average useful life of OEM parts and components, severity of regional weather conditions, highway and roadway infrastructure deterioration and the average number of miles vehicles are driven by owners. Improvements in technology and product quality are extending the longevity of vehicle component parts, which may result in delayed or reduced aftermarket sales. Our results of operations and financial condition could be adversely affected if we fail to respond in a timely and appropriate manner to changes in the demand for our aftermarket products.