|

|

By Geography |

|

|

|

|

|

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

|

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

or

|

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number

(Exact name of registrant as specified in its charter)

|

|

|

|

|

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

|

|

|

|

|

(Address of Principal Executive Offices) |

|

(Zip Code) |

+

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

|

None |

None |

None |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.001 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

☐ |

|

|

☒ |

|

Non-accelerated filer |

☐ |

|

Smaller reporting company |

|

|

Emerging growth company |

|

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes

The aggregate market value of the common stock held by non-affiliates of the registrant was approximately $

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes ☐ No ☐

As of February 4, 2021, the registrant had

Table of Contents

|

|

|

Page |

|

PART I |

|

|

|

Item 1. |

9 |

|

|

Item 1A. |

25 |

|

|

Item 1B. |

44 |

|

|

Item 2. |

44 |

|

|

Item 3. |

44 |

|

|

Item 4. |

46 |

|

|

PART II |

|

|

|

Item 5. |

47 |

|

|

Item 6. |

49 |

|

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

53 |

|

Item 7A. |

69 |

|

|

Item 8. |

70 |

|

|

|

75 |

|

|

|

Consolidated and Combined Statements of Comprehensive Income |

76 |

|

|

77 |

|

|

|

78 |

|

|

|

79 |

|

|

|

80 |

|

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

131 |

|

Item 9A. |

131 |

|

|

Item 9B. |

131 |

|

|

PART III |

|

|

|

Item 10. |

132 |

|

|

Item 11. |

137 |

|

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

168 |

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

173 |

|

Item 14. |

174 |

|

|

PART IV |

|

|

|

Item 15. |

175 |

|

|

Item 16. |

178 |

|

|

179 |

||

2

EXPLANATORY NOTE

On September 20, 2020 (the “Petition Date”), Garrett Motion Inc. (the “Company”) and certain of its subsidiaries (collectively, the “Debtors”) each filed a voluntary petition for relief under chapter 11 of title 11 of the United States Code (the “Bankruptcy Code”) in the United States Bankruptcy Court for the Southern District of New York (the “Bankruptcy Court”). The Debtors’ chapter 11 cases (the “Chapter 11 Cases”) are being jointly administered under the caption “In re: Garrett Motion Inc., 20-12212.”

On the Petition Date, the Debtors entered into a Restructuring Support Agreement (as amended, restated, supplemented or otherwise modified from time to time, the “RSA”) with consenting lenders (the “Consenting Lenders”) holding, in the aggregate, approximately 61% of the aggregate outstanding principal amount of loans under that certain Credit Agreement, dated as of September 27, 2018, (as amended, restated, supplemented or otherwise modified from time to time, the “Prepetition Credit Agreement”) by and among the Company, as Holdings, Garrett LX III S.à r.l., as Lux Borrower, Garrett Borrowing LLC, as U.S. Co-Borrower, Garrett Motion S.à r.l., as Swiss Borrower, the Lenders and Issuing Banks party thereto and JPMorgan Chase Bank, N.A., as Administrative Agent. Pursuant to the RSA, the Consenting Lenders and the Debtors agreed to the principal terms of a financial restructuring, to be implemented through a plan of reorganization under the Bankruptcy Code, and which could include the sale of all or substantially all of the assets of certain Debtors and of the stock of certain Debtors and other subsidiaries, as further described below. On January 6, 2021, the Debtors and Consenting Lenders holding no less than a majority of the aggregate outstanding principal amount of loans under the Prepetition Credit Agreement then held by all Consenting Lenders entered into Amendment No. 1 to the Restructuring Support Agreement (the “Amendment”), which, among other things, extended certain milestones contained in the RSA.

On the Petition Date, certain of the Debtors also entered into a share and asset purchase agreement (as amended, restated, supplemented or otherwise modified from time to time, the “Stalking Horse Purchase Agreement”) with AMP Intermediate B.V. (the “Stalking Horse Bidder”) and AMP U.S. Holdings, LLC, each affiliates of KPS Capital Partners, LP (“KPS”), pursuant to which the Stalking Horse Bidder agreed to purchase, subject to the terms and conditions contained therein, substantially all of the assets of the Debtors. The Stalking Horse Purchase Agreement constituted a “stalking horse” bid that was subject to higher and better offers by third parties in accordance with the bidding procedures approved by the Bankruptcy Court in an order entered by the Bankruptcy Court after hearings on October 21, 2020 and October 23, 2020 (the “Bidding Procedures Order”). The Bidding Procedures Order permitted third parties to submit competing proposals for the purchase and/or reorganization of the Debtors and approved stalking horse protections for the Stalking Horse Bidder.

On October 6, 2020, the Bankruptcy Court entered an order granting interim approval of the Debtors’ entry into a Senior Secured Super-Priority Debtor-in-Possession Credit Agreement (the “DIP Credit Agreement”), with the lenders party thereto (the “DIP Lenders”) and Citibank N.A. as administrative agent (the “DIP Agent”). On October 9, 2020 (the “Closing Date”), the Company, the DIP Agent and the DIP Lenders entered into the DIP Credit Agreement. The DIP Credit Agreement provides for a senior secured, super-priority term loan (the “DIP Term Loan Facility”) in the principal amount of $200 million, $100 million of which was funded on the Closing Date and $100 million of which was subsequently funded on October 26, 2020, following entry of the Bankruptcy Court’s final order approving the DIP Term Loan Facility on October 23, 2020. The proceeds of the DIP Term Loan Facility are to be used by the Debtors to (a) pay certain costs, premiums, fees and expenses related to the Chapter 11 Cases, (b) make payments pursuant to any interim or final order entered by the Bankruptcy Court pursuant to any “first day” motions permitting the payment by the Debtors of any prepetition amounts then due and owing, (c) make certain adequate protection payments in accordance with the DIP Credit Agreement and (d) fund working capital needs of the Debtors and their subsidiaries to the extent permitted by the DIP Credit Agreement. On October 12, 2020, the Company, the DIP Agent and the DIP Lenders entered into the First Amendment to the DIP Credit Agreement (the “First DIP Amendment”). The First DIP Amendment eliminates the obligation for the Company to pay certain fees to the DIP Lenders in connection with certain prepayment events under the DIP Credit Agreement.

In accordance with the Bidding Procedures Order, the Debtors held an auction (the “Auction”) at which they solicited and received higher and better offers from KPS and from a consortium made up of Owl Creek Asset Management, L.P., Warlander Asset Management, L.P., Jefferies LLC, Bardin Hill Opportunistic Credit Master Fund LP, Marathon Asset Management L.P., and Cetus Capital VI, L.P., or affiliates thereof (collectively, the “OWJ Group”). In addition to the bids received at the Auction from KPS and the OWJ Group, the Debtors also received a transaction proposal in parallel from Centerbridge Partners, L.P., Oaktree Capital Management, L.P., Honeywell International Inc. and certain other investors and parties (collectively, the “CO Group”). The Auction was completed on January 8, 2021, at which point the Debtors filed with the Bankruptcy Court (i) an auction notice noting that a bid received from KPS was the successful bid at the Auction but that the Debtors were still considering the proposal from the CO Group, (ii) a plan of reorganization (as may be amended, restated, supplemented or otherwise modified from time to time, the “Plan”) and (iii) a related disclosure statement (as may be amended, restated, supplemented or otherwise modified from time to time, (the “Disclosure Statement”).

3

On January 11, 2021, the Debtors, having determined that the proposal from the CO Group was a higher and better proposal than the successful bid of KPS at the Auction, entered into a Plan Support Agreement with the CO Group (as amended, restated, supplemented or otherwise modified from time to time, the “PSA”) and announced their intention to pursue a restructuring transaction with the CO Group (the “Transaction”). As a result of the entry into the PSA, (i) the Debtors filed a supplemental auction notice with the Bankruptcy Court on January 11, 2021 describing the Debtors’ determination to proceed with the Transaction, (ii) the Debtors filed a revised Plan to implement the Transaction and a related revised Disclosure Statement with the Bankruptcy Court on January 22, 2021 and (iii) the Stalking Horse Purchase Agreement became terminable, following which, on January 15, 2021, the Stalking Horse Bidder terminated the Stalking Horse Purchase Agreement and the Debtors subsequently paid a termination payment of $63 million and an expense reimbursement payment of $15.7 million to the Stalking Horse Bidder pursuant to the terms of the Stalking Horse Purchase Agreement and the Bidding Procedures Order.

In accordance with the terms of the PSA, on January 22, 2021, the Debtors’ entered into an Equity Backstop Commitment Agreement (the “EBCA”) with certain members of the CO Group (the “Equity Backstop Parties”), pursuant to which, among other things, the Company will conduct the rights offering contemplated by the PSA (the “Rights Offering”) and each Equity Backstop Party committed to (i) exercise its rights, as a stockholder of the Company, to purchase in the Rights Offering shares of the convertible Series A preferred stock of the Company to be offered in the Rights Offering (the “Series A Preferred Stock”) and (ii) purchase, on a pro rata basis (in accordance with percentages set forth in the EBCA), shares of Series A Preferred Stock which were offered but not subscribed for in the Rights Offering.

On February 15, 2021, the Debtors and the CO Group agreed with certain of the Consenting Lenders to amend and restate the PSA so as to, among other things, add certain of the Consenting Lenders as parties thereto supporting the Plan.

The Debtors’ entry into and performance and obligations under the PSA and the EBCA are subject to approval by the Bankruptcy Court and other customary closing conditions. On February 9, 2021, the official committee of equity securities holders (the “Equity Committee”) filed an objection to the Debtors’ motion seeking authority to enter into and perform under the PSA and the ECBA. A hearing on the matter is scheduled to take place in the Bankruptcy Court on February 16, 2021. There can be no assurances that the Debtors will obtain the approval of the Bankruptcy Court and complete the Transaction.

On January 24, 2021, representatives of the Equity Committee submitted a restructuring term sheet for a proposed plan of reorganization sponsored by Atlantic Park. The Equity Committee subsequently filed with the Bankruptcy Court on February 5, 2021, a proposed plan of reorganization and related disclosure statement with respect to such transaction (as reflected in the proposed plan of reorganization filed with the Bankruptcy Court, the “Atlantic Park Proposal”). The transactions contemplated under the Atlantic Park Proposal have been proposed as an alternative to the transactions contemplated under the Plan. In connection with the Atlantic Park Proposal, the Equity Committee filed a motion with the Bankruptcy Court seeking to modify the Debtors’ exclusive periods to file and solicit votes on a Chapter 11 plan. The Equity Committee’s motion is scheduled to be heard by the Bankruptcy Court on February 16, 2021. The Company has significant concerns with the feasibility of the Atlantic Park Proposal and has concluded that at this time the transactions contemplated under the Atlantic Park Proposal are not reasonably likely to lead to a higher and better alternative plan of reorganization as compared to the Plan. The Equity Committee has also filed a revised proposed plan of reorganization and disclosure statement in connection with the Atlantic Park Proposal with the Bankruptcy Court on February 15, 2021.

The disclosures in this Annual Report on Form 10-K should be read in the context of the Chapter 11 Cases. All documents filed with the Bankruptcy Court are available for inspection at the Office of the Clerk of the Bankruptcy Court or online (a) for a fee on the Bankruptcy Court’s website at www.ecf.uscourts.gov and (b) free of charge on the website of the Debtors’ claims and noticing agent, Kurtzman Carson Consultants LLC at http://www.kccllc.net/garrettmotion.

See Note 2 Reorganization and Chapter 11 Proceedings of the Notes to the Company’s Condensed Consolidated and Combined Financial Statements for additional information regarding the Chapter 11 Cases, the RSA, the Stalking Horse Purchase Agreement, the PSA, the ECBA, the Transaction and the DIP Credit Agreement.

4

BASIS OF PRESENTATION

On October 1, 2018, Garrett Motion Inc. became an independent publicly-traded company through a pro rata distribution (the “Distribution”) by Honeywell International Inc. (“Former Parent” or “Honeywell”) of 100% of the then-outstanding shares of Garrett to Honeywell’s stockholders (the “Spin-Off”). Each Honeywell stockholder of record received one share of Garrett common stock for every 10 shares of Honeywell common stock held on the record date.

Unless the context otherwise requires, references to “Garrett,” “we,” “us,” “our,” and “the Company” in this Annual Report on Form 10-K refer to Garrett Motion Inc. and its subsidiaries following the Spin-Off.

This Annual Report on Form 10-K contains financial information that was derived partially from the consolidated financial statements and accounting records of Honeywell. The accompanying consolidated and combined financial statements of Garrett (“Consolidated and Combined Financial Statements”) reflect the consolidated and combined historical results of operations, financial position and cash flows of Garrett, for periods following the Spin-Off, and the Transportation Systems Business, for all periods prior to the Spin-Off, as it was historically managed in conformity with accounting principles generally accepted in the United States of America (“U.S. GAAP”). Therefore, the historical consolidated and combined financial information may not be indicative of our future performance and does not necessarily reflect what our consolidated and combined results of operations, financial condition and cash flows would have been had the Business operated as a separate, publicly traded company during the entirety of the periods presented, particularly because of changes that we have experienced, and expect to continue to experience in the future, as a result of our separation from Honeywell, including changes in the financing, cash management, operations, cost structure and personnel needs of our business.

Throughout this Annual Report on Form 10-K, we reference certain industry sources. While we believe the compound annual growth rate (“CAGR”) and other projections of the industry sources referenced in this Annual Report on Form 10-K are reasonable, forecasts based upon such data involve inherent uncertainties, and actual outcomes are subject to change based upon various factors beyond our control. All data from industry sources is provided as of the latest practicable date prior to the filing of this Annual Report on Form 10-K and may be subject to change.

5

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements. We intend such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended. All statements other than statements of historical fact contained in this Annual Report, including without limitation statements regarding our future results of operations and financial position, the consequences and outcome of the Chapter 11 Cases, other potential claims against the Debtors related to the Chapter 11 Cases, the completion of the Transaction (including our global settlement with Honeywell), the impact of the delisting of our common stock from the New York Stock Exchange, the anticipated impact of the novel coronavirus (“COVID-19”) pandemic on our business, results of operations and financial position, expectations regarding the growth of the turbocharger and electric vehicle markets and other industry trends, the sufficiency of our cash and cash equivalents, anticipated sources and uses of cash, anticipated investments in our business, our business strategy, pending litigation, anticipated payments under our agreements with Honeywell, if our global settlement with Honeywell is not approved by the Bankruptcy Court, and the expected timing of those payments, anticipated interest expense, and the plans and objectives of management for future operations and capital expenditures are forward-looking statements. These statements involve known and unknown risks, uncertainties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. In some cases, you can identify forward-looking statements by terms such as “may,” “will,” “should,” “expect,” “plan,” “anticipate,” “could,” “intend,” “target,” “project,” “contemplate,” “believe,” “estimate,” “predict,” “potential,” or “continue” or the negative of these terms or other similar expressions. The forward-looking statements in this Annual Report are only predictions. We have based these forward-looking statements largely on our current expectations and projections about future events and financial trends that we believe may affect our business, financial condition and results of operations. These forward-looking statements speak only as of the date of this Annual Report and are subject to a number of important factors that could cause actual results to differ materially from those in the forward-looking statements, including the factors described in Part I, Item 1A. “Risk Factors,” of this Annual Report on Form 10-K and in our other filings with the Securities and Exchange Commission.

You should read this Annual Report and the documents that we reference herein completely and with the understanding that our actual future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements. Except as required by applicable law, we do not plan to publicly update or revise any forward-looking statements contained herein, whether as a result of any new information, future events, changed circumstances or otherwise.

6

Summary Risk Factors

Our business is subject to numerous risks and uncertainties, including those described in Part I Item 1A. “Risk Factors” in this Annual Report on Form 10-K. You should carefully consider these risks and uncertainties when investing in our common stock. The principal risks and uncertainties affecting our business include the following:

|

|

• |

the ability to obtain Bankruptcy Court approval in the Chapter 11 Cases with respect to the Debtors’ motions, the outcome of the Bankruptcy Court’s rulings in the Chapter 11 Cases and the outcome of the Chapter 11 Cases in general, including the length of time the Debtors will operate in the Chapter 11 Cases and the ability to obtain Bankruptcy Court approval of the adequacy of the Debtors’ Disclosure Statement and confirmation of the Debtors’ Plan; |

|

|

• |

restrictions on our operations as a result of the Chapter 11 Cases, the PSA and the DIP Credit Agreement; |

|

|

• |

ability to complete a restructuring transaction (including in accordance with the PSA and the ECBA) or realize adequate consideration for such transaction or complete a global settlement with Honeywell for spin-off related claims (including in accordance with the PSA) with the approval of the Bankruptcy Court; |

|

|

• |

the potential adverse effects of extended operation during the Chapter 11 Cases on our business, financial condition, results of operations and liquidity, including potential loss of customers and suppliers, management and other key personnel; |

|

|

• |

the availability of additional financing to maintain our operations if the DIP Term Loan Facility should become unavailable or insufficient; |

|

|

• |

the potential to experience increased levels of employee attrition as a result of the Chapter 11 Cases; |

|

|

• |

ability to utilize our net operating loss carryforwards in future years; |

|

|

• |

the delisting of our common stock from NYSE and resulting potential for limited liquidity and increased price volatility of our common stock; |

|

|

• |

other litigation and the inherent risks involved in a bankruptcy process, including the possibility of converting to a proceeding under Chapter 7 of the Bankruptcy Code; |

|

|

• |

the effect of the Chapter 11 Cases on the trading price and liquidity of our securities; |

|

|

• |

changes in the automotive industry and economic or competitive conditions; |

|

|

• |

our ability to develop new technologies and products, and the development of either effective alternative turbochargers or new replacement technologies; |

|

|

• |

any failure to protect our intellectual property or allegations that we have infringed the intellectual property of others; and our ability to license necessary intellectual property from third parties; |

|

|

• |

potential material losses and costs as a result of any warranty claims and product liability actions brought against us; |

|

|

• |

any significant failure or inability to comply with the specifications and manufacturing requirements of our original equipment manufacturer customers or by increases or decreases to the inventory levels maintained by our customers; |

|

|

• |

changes in the volume of products we produce and market demand for such products and prices we charge and the margins we realize from our sales of our products; |

|

|

• |

any loss of or a significant reduction in purchases by our largest customers, material nonpayment or nonperformance by any our key customers, and difficulty collecting receivables; |

|

|

• |

inaccuracies in estimates of volumes of awarded business; |

|

|

• |

work stoppages, other disruptions or the need to relocate any of our facilities; |

|

|

• |

supplier dependency; |

7

|

|

• |

any failure to meet our minimum delivery requirements under our supply agreements; |

|

|

• |

any failure to increase productivity or successfully execute repositioning projects or manage our workforce; |

|

|

• |

potential material environmental liabilities and hazards; |

|

|

• |

natural disasters and physical impacts of climate change; |

|

|

• |

pandemics, including without limitation the COVID-19 pandemic, and effects on our workforce and supply chain; |

|

|

• |

technical difficulties or failures, including cybersecurity risks; |

|

|

• |

the outcome of and costs associated with pending and potential material litigation matters, including our pending lawsuit against Honeywell; |

|

|

• |

changes in legislation or government regulations or policies, including with respect to CO2 reduction targets in Europe as part of the Green Deal objectives or other similar changes which may contribute to a proportionately higher level of battery electric vehicles; |

|

|

• |

risks related to international operations and our investment in foreign markets, including risks related to the withdrawal of the United Kingdom from the European Union; |

|

|

• |

the terms of our indebtedness and our ability to access capital markets; |

|

|

• |

unforeseen adverse tax effects; |

|

|

• |

our leveraged capital structure and liabilities to Honeywell may pose significant challenges to our overall strategic and financial flexibility and have a material adverse effect on our business, liquidity position and financial position; and |

|

|

• |

inability to recruit and retain qualified personnel. |

8

Part I

Item 1. Business

Our Company

Our Company designs, manufactures and sells highly engineered turbocharger and electric-boosting technologies for light and commercial vehicle original equipment manufacturers (“OEMs”) and the global vehicle independent aftermarket as well as automotive software solutions. These OEMs in turn ship to consumers globally. We are a global technology leader with significant expertise in delivering products across gasoline, diesel, natural gas and electric (hybrid and fuel cell) powertrains. These products are key enablers for fuel economy and emission standards compliance.

Our products are highly engineered for each individual powertrain platform, requiring close collaboration with our customers in the earliest years of powertrain and new vehicle design. Our turbocharging and electric-boosting products enable our customers to improve vehicle performance while addressing continually evolving and converging regulations that mandate significant increases in fuel efficiency and reductions in exhaust emissions worldwide.

We offer light vehicle gasoline, light vehicle diesel and commercial vehicle turbochargers that enhance vehicle performance, fuel economy and drivability. A turbocharger provides an engine with a controlled and pressurized air intake, which intensifies and improves the combustion of fuel to increase the amount of power sent through the transmission and to improve the efficiency and exhaust emissions of the engine. Market penetration of light vehicles with a turbocharger is expected to increase from approximately 51% in 2020 to approximately 55% by 2025, according to IHS Markit (“IHS”), which we believe will allow the turbocharger market to grow at a faster rate than overall automobile production.

Building on our expertise in turbocharger technology, we have also developed electric-boosting technologies targeted for use in electrified powertrains, primarily hybrid and fuel cell vehicles. Our products include electric turbochargers and electric compressors that provide more responsive driving and optimized fuel economy in electrified vehicles. Our early-stage and collaborative relationships with our global OEM customer base have enabled us to increase our knowledge of customer needs for vehicle safety, predictive maintenance, and advanced controllers to develop new connected and software-enabled products.

In addition, we have emerging opportunities in technologies, products and services that support the growing connected vehicle market, which include software focused on automotive cybersecurity and integrated vehicle health management (“IVHM”). Our focus is developing solutions for enhancing cybersecurity of connected vehicles, as well as in-vehicle monitoring to provide maintenance diagnostics, which reduce vehicle downtime and repair costs. For example, our Intrusion Detection and Prevention System uses anomaly detection technology that functions like virus detection software to perform real-time data analysis to ensure every message received by a car’s computer is valid. Our IVHM tools detect intermittent faults and anomalies within complex vehicle systems to provide a more thorough understanding of the real-time health of a vehicle system and enable customers to fix faults before they actually occur. We are collaborating with tier-one suppliers on automotive cybersecurity software solutions and with several major OEMs on IVHM technologies.

Our comprehensive portfolio of turbocharger, electric-boosting and connected vehicle technologies is supported by our five research and development (“R&D”) centers, 11 close-to-customer engineering facilities and 13 factories, which are strategically located around the world. Our operations in each region have self-sufficient sales, engineering and production capabilities, making us a nimble local competitor, while our standardized manufacturing processes, global supply chain, worldwide technology R&D and size enable us to deliver the scale benefits, technology leadership, cross-regional support and extensive resources of a global enterprise. In high-growth regions, including China and India, we have established a local footprint, which has helped us secure strong positions with in-region OEM customers who demand localized engineering and manufacturing content but also require the capabilities and track record of a global leader.

We also sell our technologies in the global aftermarket through our distribution network of more than 200 distributors covering 160 countries. Through this network, we provide approximately 5,300 part-numbers and products to service garages across the globe. Garrett is a leading brand in the independent aftermarket for both service replacement turbochargers as well as high-end performance and racing turbochargers. We estimate that over 110 million vehicles on the road today utilize our products, further supporting our global aftermarket business.

9

Leading technology, continuous innovation, product performance and OEM engineering collaboration are central to our customer value proposition and a core part of our culture and heritage. In 1962, we introduced a turbocharger for a mass-produced passenger vehicle. Since then, we have introduced many other notable technologies in mass-production vehicles, such as turbochargers with variable geometry turbines, dual-boost compressors, ball-bearing rotors and electronically actuated controls, all of which vastly improve engine response when accelerating at low speeds and increase power at higher speeds and enable significant improvements in overall engine fuel economy and exhaust emissions for both gasoline and diesel engines. Our portfolio today includes approximately 1,600 patents and patents pending.

Reorganization and Chapter 11 Proceedings

On the Petition Date, the Debtors each entered into the RSA and filed a voluntary petition for relief under the Bankruptcy Code in the Bankruptcy Court. The Chapter 11 Cases are being jointly administered under the caption “In re: Garrett Motion Inc., 20-12212.”

On the Petition Date, certain of the Debtors also entered into the Stalking Horse Purchase Agreement with the Stalking Horse Bidder and AMP U.S. Holdings, LLC, each affiliates of KPS, pursuant to which the Stalking Horse Bidder agreed to purchase, subject to the terms and conditions contained therein, substantially all of the assets of the Debtors. The Stalking Horse Purchase Agreement constituted a “stalking horse” bid that was subject to higher and better offers by third parties in accordance with the bidding procedures approved by the Bankruptcy Court in the Bidding Procedures Order. The Bidding Procedures Order permitted third parties to submit competing proposals for the purchase and/or reorganization of the Debtors and approved stalking horse protections for the Stalking Horse Bidder.

On the Petition Date, we were notified by the New York Stock Exchange (the “NYSE”) that, as a result of the Chapter 11 Cases, and in accordance with Section 802.01D of the NYSE Listed Company Manual, that NYSE had commenced proceedings to delist our common stock from the NYSE. The NYSE indefinitely suspended trading of our common stock on September 21, 2020. We determined not to appeal the NYSE’s determination. On October 8, 2020, the NYSE filed a Form 25-NSE with the Securities and Exchange Commission, which removed our common stock from listing and registration on the NYSE effective as of the opening of business on October 19, 2020. The delisting of our common stock from NYSE has and could continue to limit the liquidity of our common stock, increase the volatility in the price of our common stock, and hinder our ability to raise capital.

In accordance with the Bidding Procedures Order, the Debtors held the Auction at which they solicited and received higher and better offers from KPS and the OWJ Group. In addition to the bids received at the Auction from KPS and the OWJ Group, the Debtors also received a transaction proposal in parallel from the CO Group. The Auction was completed on January 8, 2021, at which point the Debtors filed with the Bankruptcy Court (i) an auction notice noting that a bid received from KPS was the successful bid at the Auction but that the Debtors were still considering the proposal from the CO Group, (ii) the Plan and Disclosure Statement. On January 11, 2021, the Debtors, having determined that the proposal from the CO Group was a higher and better proposal than the successful bid of KPS at the Auction, entered into the PSA and announced their intention to pursue a restructuring transaction with the CO Group. As a result of the entry into the PSA, (i) the Debtors filed a supplemental auction notice with the Bankruptcy Court on January 11, 2021 describing the Debtors’ determination to proceed with the Transaction, (ii) the Debtors filed a revised Plan and related revised Disclosure Statement with the Bankruptcy Court on January 22, 2021 to implement the Transaction and (iii) the Stalking Horse Purchase Agreement became terminable, following which, on January 15, 2021, the Stalking Horse Bidder terminated the Stalking Horse Purchase Agreement and the Debtors subsequently paid a termination payment of $63 million and an expense reimbursement payment of $15.7 million to the Stalking Horse Bidder pursuant to the terms of the Stalking Horse Purchase Agreement and the Bidding Procedures Order.

Under the terms of the PSA and the Transaction, the Plan, if confirmed by the Bankruptcy Court, will include a global settlement with Honeywell providing for (a) the full and final satisfaction, settlement, release, and discharge of all liabilities under or related to the indemnification and reimbursement agreement with Honeywell entered into on September 12, 2018 (the “Honeywell Indemnity Agreement”), that certain Indemnification Guarantee Agreement, dated as of September 27, 2018 (as amended, restated, amended and restated, supplemented, or otherwise modified from time to time), by and among Honeywell ASASCO 2 Inc. as payee, Garrett ASASCO as payor, and certain subsidiary guarantors as defined therein (the “Guarantee Agreement,” and together with the Honeywell Indemnity Agreement, the “Indemnity Agreements”) and the tax matters agreement with Honeywell, dated September 12, 2018 (the “Tax Matters Agreement”) and (b) the dismissal with prejudice of the lawsuits against Honeywell relating to the Honeywell Indemnity Agreement and the Tax Matters Agreement (the “Honeywell Litigation”) in exchange for (x) a $375 million cash payment by the company at emergence from chapter 11 (“Emergence”) and (y) new Series B Preferred Stock issued by the Company payable in installments of $35 million in 2022, and $100 million annually 2023-2030 (the “Series B Preferred Stock”).

10

In accordance with the terms of the PSA, on January 22, 2021, the Debtors’ entered into the EBCA with the Equity Backstop Parties, pursuant to which, among other things, the Company will conduct the Rights Offering and each Equity Backstop Party committed to (i) exercise its rights, as a stockholder of the Company, to purchase in the Rights Offering shares of the Series A Preferred Stock and (ii) purchase, on a pro rata basis (in accordance with percentages set forth in the EBCA), shares of Series A Preferred Stock which were offered but not subscribed for in the Rights Offering.

On February 15, 2021, the Debtors and the CO Group agreed with certain of the Consenting Lenders to amend and restate the PSA so as to, among other things, add certain of the Consenting Lenders as parties thereto supporting the Plan.

The Debtors’ entry into and performance and obligations under the PSA and the EBCA are subject to approval by the Bankruptcy Court and other customary closing conditions. On February 9, 2021, the Equity Committee filed an objection to the Debtors’ motion seeking authority to enter into and perform under the PSA and the ECBA. A hearing on the matter is scheduled to take place in the Bankruptcy Court on February 16, 2021. There can be no assurances that the Debtors will obtain the approval of the Bankruptcy Court and complete the Transaction.

On January 24, 2021, representatives of the Equity Committee submitted a restructuring term sheet for the Atlantic Park Proposal. The Equity Committee subsequently filed with the Bankruptcy Court on February 5, 2021, a proposed plan of reorganization and related disclosure statement with respect to the Atlantic Park Proposal. The transactions contemplated under the Atlantic Park Proposal have been proposed as an alternative to the transactions contemplated under the Plan. In connection with the Atlantic Park Proposal, the Equity Committee filed a motion with the Bankruptcy Court seeking to modify the Debtors’ exclusive periods to file and solicit votes on a Chapter 11 plan. The Equity Committee’s motion is scheduled to be heard by the Bankruptcy Court on February 16, 2021. The Company has significant concerns with the feasibility of the Atlantic Park Proposal and has concluded that at this time the transactions contemplated under the Atlantic Park Proposal are not reasonably likely to lead to a higher and better alternative plan of reorganization as compared to the Plan.

For additional information regarding the Chapter 11 Cases, reorganization, the PSA, the ECBA and the Transaction, see “Explanatory Note” and Note 2, Reorganization and Chapter 11 Proceedings of the Notes to the Consolidated and Combined Financial Statements.

Impact of COVID-19 Pandemic

The ongoing global COVID-19 pandemic has created unparalleled challenges for the auto industry in the short-term. In the three months ended March 31, 2020, our manufacturing facility in Wuhan, China was shut down for six weeks in February and March and we saw diminished production in our Shanghai, China facility for that same time period, which adversely impacted our net sales for the period. During the second quarter, our facilities in China re-opened, however our manufacturing facilities in Mexicali, Mexico and Pune, India were shut down for five weeks and our manufacturing facilities in Europe operated at reduced capacity. During this time, we implemented a set of hygiene and safety measures that complied with, and in many places exceeded local regulations in order to protect our employees while maintaining commitments vis-a-vis our customers. This combined with the fast recovery observed in all geographies has enabled us to ramp up production in most of our production sites to normal levels in the third quarter of 2020. This trend has been confirmed in the fourth quarter, despite the resurgence of infection rates in U.S. and European Union. If the COVID-19 pandemic drives new lockdown measures impacting our manufacturing facilities, our facilities may be forced to shut down or operate at reduced capacity again. Additional or continued facilities closures or reductions in operation could significantly reduce our production volumes and have a material adverse impact on our business, results of operations and financial condition.

Analyst consensus for the full year 2020 anticipates a 17% decrease in global light vehicle production, and for a 10% decline in commercial vehicle production, a larger drop than during the financial crisis in 2008 and 2009. In 2021, a partial recovery is expected with a rebound of light vehicle production of 14% and commercial vehicles of 6%. As a result, we estimate that a contraction of approximately 13% for the combined light and commercial vehicle turbocharger industry volume occurred in 2020 and we expect a rebound of 13% in 2021. We have prepared contingency plans for multiple scenarios that we believe will allow us to react swiftly to changes in customer demand while protecting Garrett’s long-term growth potential. The supplies needed for our operations were generally available throughout 2020. In limited circumstances, certain suppliers experienced financial distress during 2020, resulting in supply disruptions. However, during 2020, we implemented new procedures for monitoring of supplier risks associated with COVID-19 and the Chapter 11 Cases and believe we have substantially addressed such risks with manageable economic impacts

11

including use of Premium Freight or adjusted payment terms that are limited in time. In addition, we have implemented cost control measures and cash management actions, including:

|

|

• |

Postponing capital expenditures; |

|

|

• |

Optimizing working capital requirements; |

|

|

• |

Lowering discretionary spending; |

|

|

• |

Flexing organizational costs by implementing short-term working schemes; |

|

|

• |

Reducing temporary workforce and contract service workers; and |

|

|

• |

Restricting external hiring. |

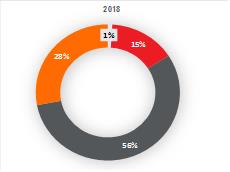

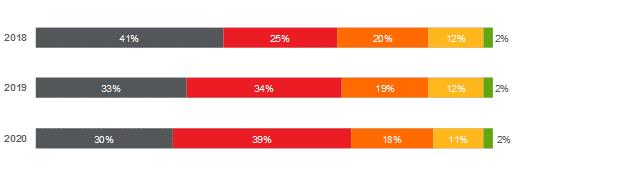

The following charts show our percentage of revenues by geographic region and product line for the years ended December 31, 2020, 2019 and 2018 and the percentage change from the prior year comparable period.

Revenue Summary

|

|

By Geography |

|

|

|

|

|

|

By Product-line |

|

|

|

|

• |

We are a global business that generated revenues of approximately $3 billion in 2020. |

|

|

• |

In 2020, light vehicle products (products for passenger cars, SUVs, light trucks, and other products) accounted for approximately 69% of our revenues. Commercial vehicle products (products for on-highway trucks and off-highway trucks, construction, agriculture and power-generation machines) accounted for 18%. |

12

|

|

• |

In 2020, our OEM sales contributed approximately 87% of our revenues while our aftermarket and other products contributed 13%. |

|

|

• |

Approximately 51% of our 2020 revenues came from sales shipped from Europe, 33% from sales shipped from Asia and 15% from sales shipped from North America. For more information, see Note 26 Concentrations of the Notes to our Consolidated and Combined Financial Statements. |

Our Industry

We compete in the global turbocharger market for gasoline, diesel and natural gas engines; in the electric- boosting market for electrified (hybrid and fuel cell) vehicle powertrains; and in the emerging connected vehicle software market. As vehicles become more electrified, our electric-boosting products use principles similar to our turbochargers to further optimize air intake and thus further enhance performance, fuel economy and exhaust emissions with the help of an integrated high-speed electric motor. By using a turbocharger or electric-boosting technology, an OEM can deploy smaller, lighter powertrains with better fuel economy and exhaust emissions while delivering the same power and acceleration as larger, heavier powertrains. As such, turbochargers have become one of the most highly effective technologies for helping global OEMs meet increasingly stricter emission standards.

Global Turbocharger market

The global turbocharger market includes turbochargers for new light and commercial vehicles as well as turbochargers for replacement use in the global aftermarket. According to IHS and other experts, the global turbocharger market consisted of approximately 44 million unit sales with an estimated total value of approximately $10 billion in 2020. Within the global turbocharger market, light vehicles accounted for approximately 90% of total unit volume and commercial vehicles accounted for the remaining 10%.

Consultants project that the turbocharger production volume will grow at a CAGR of approximately 3% from 2019 through 2025, driven mainly by turbochargers for light vehicle gasoline engines and continued slow growth for commercial vehicles, offset by a decline in diesel turbochargers given a decline in diesel powertrains, particularly for light vehicles. This annual sales estimate would add approximately 372 million new turbocharged vehicles on the road globally between 2019 and 2025.

Key trends affecting our industry

Current global economic conditions due to COVID-19 have adversely affected and may continue to adversely affect many industries including the Automotive sector. Analysts estimate that automotive industry revenue dropped 11% in 2020, compared to 2019, according to Standard & Poor’s Capital IQ. According to the same dataset, other industries that drive, in particular, Off-Highway commercial vehicle turbo demand, such as Oil and Gas (24%), Railroads (16%) or Marine (2%) recorded drops in industry revenue over the same period. Global GDP growth, while restarting in second half of 2020 on the back of global government stimulus programs, will remain 5 percentage points below pre-crisis forecasts at least until 2023, according to the OECD. Consequently, IHS reduced its light vehicle production volume forecast for 2025 from 102 million units that they forecasted in 2019 to 95 million units in their January 2021 light vehicle industry production volume forecast. While this resets the volume outlook for the automotive industry, the underlying growth drivers for the turbo industry remain unchanged: Growth in the overall vehicle industry (albeit from a lower base), increasingly tight fuel efficiency and emission standards, and growing turbocharger penetration.

Growth in overall vehicle production. After a decrease of 17% in Light Vehicle production and 10% in Commercial Vehicle production in 2020, consultants expect a stabilization in 2021. The global automotive industry is expected to reach pre-crisis volumes in 2022-2023. The shift from pure gasoline and diesel internal combustion engines to hybridized powertrains is expected to continue in response to increasingly strict fuel efficiency and regulatory standards. In parallel, the share of pure electric vehicles is expected to continue to increase from a low base as technology and supporting infrastructure continue to improve.

Global vehicle fuel efficiency and emissions standards. OEMs are facing increasingly strict constraints for vehicle fuel efficiency and emissions standards globally. Regulatory authorities in key vehicle markets such as the United States, the European Union, China, Japan, and Korea have instituted regulations that require sustained and significant improvements in CO2, NOx and particulate matter vehicle emissions. OEMs are required to evaluate and adopt various

13

solutions to address these stricter standards. Turbochargers allow OEMs to reduce engine size without sacrificing vehicle performance, thereby increasing fuel efficiency and decreasing harmful emissions. Furthermore, turbochargers allow more precise “air control” over both engine intake and exhaust conditions such as gas pressures, flows and temperatures, enabling optimization of the combustion process. This combustion optimization is critical to engine efficiency, exhaust emissions, power and transient response and enables such concepts as exhaust gas recirculation for diesel engines and Miller-cycle operation for gasoline engines. Consequently, we believe turbocharging will continue to be a key technology for automakers to meet future tough fuel economy and emissions standards without sacrificing performance.

Turbocharger penetration. The utilization of turbochargers and electric-boosting technologies on vehicle powertrain systems is one of the most cost-effective solutions to address stricter standards, and OEMs are increasing their adoption of these technologies. IHS and other industry sources expect total turbocharger penetration to increase globally from approximately 53% in 2020 to approximately 56% by 2025. IHS forecasts particularly strong turbocharger penetration growth for gasoline turbochargers, expecting an increase from approximately 44% in 2020 to 56% in 2025.

Medium-Term Powertrain Trends

Source: IHS

Engine size and complexity. In order to address stricter fuel economy standards, OEMs have used turbochargers to reduce the average engine size on their vehicles over time without compromising performance. Stricter pollutants emissions standards (primarily for NOx and particulates) have driven higher turbocharger adoption as well, which we believe will continue in the future, with a predicted total automotive turbocharger sales volume CAGR of 3% between 2019 and 2025, in an industry with a predicted total automobile sales volume CAGR of approximately 1% over the same period, in each case according to IHS and other industry sources. In addition, increasingly demanding fuel economy standards require continuous increases in turbocharger technology content (e.g., variable geometry, electronic actuation, multiple stages, ball bearings, electrical control, etc.) which results in steady increases in average turbocharger content per vehicle.

Powertrain electrification. To address stricter fuel economy standards, OEMs also have been increasing the electrification of their vehicle offerings, primarily with the addition of hybrid vehicles, which have powertrains equipped with a gasoline or diesel internal combustion engine in combination with an electric motor. IHS estimates that hybrid vehicles globally will grow from a total of approximately 5.3 million vehicles in 2019 to 29.5 million vehicles by 2025, representing a CAGR of 33%. The electrified powertrain of hybrid vehicles enables the usage of highly synergistic electric-boosting technologies which augment standard turbochargers with electrically assisted boosting and electrical-generation capability. Furthermore, the application of electric boosting extends the requirement for engineering collaboration with OEMs to include electrical integration, software controls, and advanced sensing. Overall, this move to electric boosting further increases the role and value of turbocharging in improving vehicle fuel economy and exhaust emissions.

OEMs are also investing in full battery-electric vehicles to comply with increasingly tight regulatory targets across regions. IHS and other industry sources expect that they will compose 10% of total light and commercial vehicle production globally by 2025. Consumer adoption hinges on future battery cost – hence vehicle price - reductions,

14

increases in power density – hence driving range, and shorter recharging times. As OEMs strive to solve these issues, they are increasing investment in hydrogen fuel cell powered electric vehicles for demanding applications requiring long range, especially in the commercial vehicle space. These vehicles, like battery electric vehicles, have fully electric motor powertrains, but they rely on the hydrogen fuel cell to generate the required electricity. The hydrogen fuel cell also requires advanced electric-boosting technology for optimization of size and efficiency.

Connected vehicles, autonomous vehicles, and shared vehicles. In addition to powertrain evolution, the market for connected vehicle services is growing rapidly. According to Strategy&, a consulting firm, this market is expected to grow 34% per annum from approximately $8 billion in 2020 to approximately $35 billion in 2025. Our IVHM, predictive maintenance, diagnostics and cybersecurity tools address this market. Their adoption should increase as advanced driver assistance features and ultimately autonomous driving increase requirements for vehicle functional safety. Simultaneously, our cybersecurity solutions protect those vehicles against outside interference to ensure correct functionality.

Vehicle ownership in China and other high-growth markets. Vehicle ownership in China and other emerging markets remains well below ownership levels in developed markets and will be a key driver of future vehicle production. At the same time, these markets are following the lead of developed countries by instituting stricter emission standards. Growth in production volume and greater penetration by large global OEMs in these markets, along with evolving emission standards and increasing fuel economy and vehicle performance demands, is driving increasing turbocharger penetration in high-growth regions.

Our Competitive Strengths

We believe that we differentiate ourselves through the following competitive strengths:

Global and broad market leadership

We are a global leader in the $10 billion turbocharger industry. We believe we will continue to benefit from the increased adoption of turbochargers, as well as our global technology leadership, comprehensive portfolio, continuous product innovation and our deep-seated relationships with all global OEMs. We maintain a leadership position across all vehicle types, engine types and regions, including:

Light Vehicles.

|

|

• |

Gasoline: The global adoption of turbochargers by OEMs on gasoline engines has increased rapidly from approximately 14% in 2013 to approximately 40% in 2019 and is forecasted by IHS to increase to 56% by 2025. We have launched a leading modern 1.5L variable geometry turbo (“VNT”) gasoline application, which we believe to be among the first with a major OEM, and we expect to see increasing adoption of this technology in years to come. Key to our strategy for gasoline growth is to leverage our technology strengths in high-temperature materials and variable geometry as well as our scale, global footprint and in-market capabilities to meet the volume demands of global OEMs. |

|

|

• |

Diesel: We have a long history of technology leadership in diesel engine turbochargers. Despite diesel market weakness for some vehicle segments, the majority of our diesel turbochargers revenue comes from heavier and bigger vehicles like SUVs, pickup trucks and light commercial vehicles (such as delivery vans), which remain a stable part of the diesel market. Diesel maintains a unique advantage in terms of fuel consumption, hence cost of ownership, and towing capacity makes it still the powertrain of choice for heavier vehicle applications. Diesel also remains essential for OEMs to meet their CO2 fleet average regulatory target going forward, as diesel vehicles produce approximately 10-15% less CO2, on average, than gasoline vehicles. |

|

|

• |

Electrified vehicles. We provide a comprehensive portfolio of turbocharger and electric-boosting technologies to manufacturers of hybrid-electric and fuel cell vehicles. OEMs have increased their adoption of these electrified technologies given regulatory standards and consumer demands driving an expected CAGR globally of approximately 33% from 2019 to 2025, according to IHS. Similar to turbochargers for gasoline and diesel engines, turbochargers for hybrid vehicles are an essential component of maximizing fuel efficiency and overall engine performance. Our products provide OEMs with solutions that further optimize engine performance and position us well to serve OEMs as they add more electrified vehicles into their fleets. |

15

Commercial vehicles. Our Company traces its roots to the 1950s when we helped develop a turbocharged commercial vehicle for Caterpillar. We have maintained our strategic relationship with key commercial vehicle OEMs for over 60 years as well as market-leading positions across the commercial vehicle markets for both on- and off-highway use. Our products improve engine performance and lower emissions on trucks, buses, agriculture equipment, construction equipment and mining equipment with engine sizes ranging 1.8L to 105L.

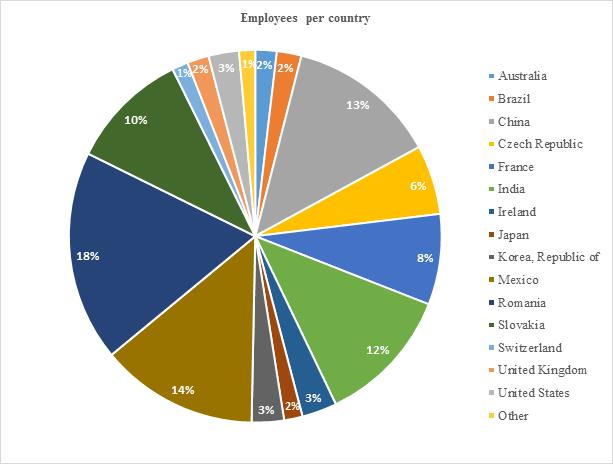

High-growth regions. We have a strong track record serving global and emerging OEMs, including customers in China and India, with an in-market, for-market strategy and operate full R&D and three manufacturing facilities in the high-growth regions that serve light and commercial vehicle OEMs. Our local presence in high-growth regions has helped us win business with key international and domestic Chinese OEMs, and we grew significantly faster than the vehicle production in these regions between 2013 and 2019.

Strong and collaborative relationships with leading OEMs globally

We supply our products to more than 60 OEMs globally. Our top ten customers accounted for approximately 56% of net sales and our largest customer represented approximately 10% of our net sales in 2020. With over 60 years in the turbocharger industry, we have developed strong capabilities working with all major OEMs. We consistently meet their stringent design, performance and quality standards while achieving capacity and delivery timelines that are critical for customer success. Our track record of successful collaborations, as demonstrated by our strong client base and our ability to successfully launch approximately 100 product applications annually, is well recognized. For example, we received a 2017 Automotive News PACE™ Innovation Partnership Award in supporting Volkswagen’s first launch of an industry-leading VNT turbocharged gasoline engine, which is just one example of our strong collaborative relationships with OEMs. Our regional research, development and manufacturing capabilities are a key advantage in helping us to supply OEMs as they expand geographically and shift towards standardized engines and vehicle platforms globally.

Global aftermarket platform

We have an estimated installed base of over 110 million vehicles that utilize our products through our global network of more than 200 distributors covering 160 countries. Our Garrett aftermarket brand has strong recognition across distributors and garages globally, and is known for boosting performance, quality and reliability. Our aftermarket business has historically provided a stable stream of revenue supported by our large installed base. As turbo penetration rates continue to increase, we expect that our installed base and aftermarket opportunity will grow.

Highly-engineered portfolio with continuous product innovation

We have led the revolution in turbocharging technology over the last 60 years and maintain a leading technology portfolio of approximately 1,600 patents and patents pending. We have a globally deployed team of more than 1,250 engineers across five R&D centers and 11 close-to-customer engineering centers. Our engineers have led the mainstream commercialization of several leading turbocharger innovations, including variable geometry turbines, dual-boost compressors, ball-bearing rotors, electrically actuated controls and air-bearing electric compressors for hydrogen fuel cells. We maintain a culture of continuous product innovation, introducing about ten new technologies per year and upgrading our existing key product lines approximately every 3 years. Outside of our turbocharger product lines, we apply this culture of continuous innovation to meet the needs of our customers in new areas, particularly in connected automotive technologies. We are developing solutions, including IVHM and cybersecurity software solutions, that leverage our knowledge of vehicle powertrains and experience working closely with OEM manufacturers.

Global and low cost manufacturing footprint with operational excellence

Our geographic footprint locates R&D, engineering and manufacturing capabilities close to our customers, enabling us to tailor technologies and products for the specific vehicle types sold in each geographic market. In all regions where we operate, we leverage low-cost sourcing through our robust supplier development program, which continually works to develop new suppliers that are able to meet our specific quality, productivity and cost requirements. We now source more than two-thirds of our materials from low-cost countries and believe our high-quality, low-cost supplier network to be a significant competitive advantage. We have invested heavily to bring differentiated local capabilities to our customers in high-growth regions, including China and India.

16

In 2020 we manufactured more than 87% of our products in low-cost countries, including seven manufacturing facilities in China, India, Mexico, Romania and Slovakia. We have a long-standing culture of lean manufacturing excellence and continuous productivity improvement. We believe global uniformity and operational excellence across facilities is a key competitive advantage in our industry given that OEM engine platforms are often designed centrally but manufactured locally, requiring suppliers to meet the exact same specifications across all locations.

Our Growth Strategies

The Debtors, including Garrett, filed for relief under chapter 11 of the Bankruptcy Code in September 2020, primarily with the intent to restructure our balance sheet. Given the Company’s operational performance prior to the Petition Date, our day-to-day operations have been largely unaffected. If we are able to timely restructure our balance sheet, and accordingly emerge from the Chapter 11 Cases, Garrett expects to continue to invest in innovative technologies that address the needs of our customers in the ongoing auto industry transformation. This continued investment into differentiated technology, coupled with our relentless focus on deep customer relations and our global capabilities, will allow us to drive the following business strategies:

Strengthen market leadership across core powertrain technologies

We are focused on strengthening our market position in light vehicles:

|

|

• |

Gasoline turbochargers, which historically lagged adoption of diesel turbochargers, are expected to grow at an 6% annual CAGR from 2019 to 2025, according to IHS, exceeding the growth of diesel turbochargers. We expect to benefit from this higher growth given the gasoline platforms we have been awarded over the past several years. We have launched the first modern 1.5L VNT gasoline application with a major OEM and we expect to see increasing adoption of this technology in years to come. Key to our strategy for gasoline growth is our plan to leverage our technology strengths in high temperature materials and variable geometry technologies as well as our scale, global footprint and in-region capabilities to meet the volume demands of global OEMs. |

|

|

• |

We believe growth in our share of the diesel turbochargers market will be driven by new product introductions focused on emissions-enforcement technologies and supported by our favorable positioning with large vehicles and high-growth regions within this market. The more stringent emissions standards require higher turbocharger technology content such as variable geometry, 2-stage systems, advanced bearings and materials which increase our content per vehicle. We expect to grow our commercial vehicle business through new product introductions and targeted platform wins with key on-highway customers and underserved OEMs. |

Strengthen our penetration of electrified vehicle boosting technologies

We stand to benefit from the increased adoption of hybrid-electric and fuel cell vehicles and the increased need for turbochargers associated with increased sales volumes for these engine types. IHS estimates that the global production of electrified vehicles will increase from approximately 7 million vehicles in 2019 to approximately 42 million vehicles by 2025, representing an annualized growth rate of approximately 34%. OEMs will need to further improve engine performance for their increasingly electrified offerings, and our comprehensive portfolio of turbocharger and electric-boosting technologies are designed to help OEMs do so. We expect to continue to invest in product innovations and new technologies and believe that we are well positioned to continue to be a technology-leader in the propulsion of electrified vehicles.

Increase market position in high-growth regions

In 2020, after a steep drop in the first quarter due to strict lockdowns, vehicle production in China has experienced a very strong rebound which has partly compensated for the decline in the first quarter, with a full year drop of 5%, compared to 20%+ in other regions. IHS expects vehicle production in China to be stable next year. We plan to continue to strengthen our relationships with OEMs in high-growth, emerging regions by demonstrating our technology leadership through our local research, development and manufacturing capabilities. Our local footprint is expected to continue to provide a strong competitive edge in high-growth regions due to our ability to work closely with OEMs throughout all stages of the product lifecycle including aftermarket support. For example, in China, our research

17

center in Shanghai, our manufacturing facilities in Wuhan and Shanghai and our more than 984 employees support our differentiated end-to-end capabilities and we believe will continue to support key platform wins in the Chinese market. Our operations in China are expected to continue to benefit us as OEMs build global platforms in low cost regions. Our commitment to providing high-touch technology support to OEMs has allowed us to be recognized as a local player in other key high-growth regions, such as India.

Grow our aftermarket business

We have an opportunity to strengthen our global network of more than 200 distributors in 160 countries by deepening our channel penetration, leveraging our well-recognized Garrett brand, utilizing new online technologies for customer engagement and sales, and widening the product portfolio. For example, in 2019 we launched a global web-based platform providing self-service tools aimed at connecting garage technicians. In 2020 the platform attracted 170 thousand visitors and 22,000 registered garage technicians who used the platform to complete Garrett self-learning and certification steps.

Drive continuous product innovation across connected vehicles

We are actively investing in software and services that leverage our capabilities in powertrains, vehicle performance management, and electrical/mechanical design to capitalize on the growth relating to connected vehicles. More than 85% of passenger vehicles sold in Europe and the United States and almost 50% of vehicles sold in China in 2020 were estimated to be connected in some way to the Internet according to Strategy&, a consultancy firm. According to the same report, that number is expected to reach 100% in Europe and the United States and >90% in China by 2025. Building on the software and connected vehicle capabilities of our Former Parent, we have assembled a team of engineers, software and technical experts and have opened new design centers in North America, India and Czech Republic. We continue to conduct research to determine key areas of the market where we are best positioned to leverage our existing technology platforms and capabilities to serve our customers. We execute a portion of our connectivity investment in collaboration with OEMs and other Tier 1 suppliers and have multiple early-stage trials with customers underway.

Research, Development and Intellectual Property

We maintain technical engineering centers in major automotive production regions of the world to develop and provide advanced products, process and manufacturing support to all of our manufacturing sites, and to provide our customers with local engineering capabilities and design developments on a global basis. As of December 31, 2020, we employed approximately 1,250 engineers. Our total R&D expenses were $111 million, $129 million and $128 million for the years ended December 31, 2020, 2019 and 2018, respectively. Additionally, the Company incurs engineering-related expenses which are also included in Cost of goods sold of $

We currently hold approximately 1,600 patents and patents pending. Our current patents are expected to expire between 2021 and 2040. While no individual patent or group of patents, taken alone, is considered material to our business, taken in the aggregate, these patents provide meaningful protection for our intellectual property.

Materials

The most significant raw materials we use to manufacture our products are grey iron, aluminum, stainless steel and a nickel-, iron- and chromium-based alloy. As of December 31, 2020, we have not experienced any significant shortage of raw materials and normally do not carry inventories of such raw materials in excess of those reasonably required to meet our production and shipping schedules.

Customers

Our global customer base includes nine of the ten largest light vehicle OEMs and nine of the ten largest commercial vehicle engine makers.

18

Our ten largest applications in 2020 were with seven different OEMs. OEM sales were approximately 87% of our 2020 revenues while our aftermarket and other products contributed 13%.

Our largest customer is Ford Motor Company (“Ford”). In 2020, 2019 and 2018, Ford accounted for 10%, 12%, and 13%, respectively, of our total sales.

Supply Relationships with Our Customers

We typically supply products to our OEM customers through “open” purchase orders, which are generally governed by terms and conditions negotiated with each OEM. Although the terms and conditions vary from customer to customer, they typically contemplate a relationship under which our customers are not required to purchase a minimum amount of product from us. These relationships typically extend over the life of the related engine platform. Prices are negotiated with respect to each business award, which may be subject to adjustments under certain circumstances, such as commodity or foreign exchange escalation/de-escalation clauses or for cost reductions achieved by us. The terms and conditions typically provide that we are subject to a warranty on the products supplied. We may also be obligated to share in all or a part of recall costs if the OEM recalls its vehicles for defects attributable to our products.

Individual purchase orders are terminable for cause or non-performance and, in most cases, upon our insolvency and certain change of control events. In addition, many of our OEM customers have the option to terminate for convenience on certain programs, which permits our customers to impose pressure on pricing during the life of the vehicle program, and issue purchase contracts for less than the duration of the vehicle program, which potentially reduces our profit margins and increases the risk of our losing future sales under those purchase contracts. We manufacture, and ship based on customer release schedules, normally provided on a weekly basis, which can vary due to cyclical automobile production or inventory levels throughout the supply chain.

Although customer programs typically extend to future periods, and although there is an expectation that we will supply certain levels of OEM production during such future periods, customer agreements including applicable terms and conditions do not necessarily constitute firm orders. Firm orders are generally limited to specific and authorized customer purchase order releases placed with our manufacturing and distribution centers for actual production and order fulfillment. Firm orders are typically fulfilled as promptly as possible from the conversion of available raw materials, sub-components and work-in-process inventory for OEM orders and from current on-hand finished goods inventory for aftermarket orders. The dollar amount of such purchase order releases on hand and not processed at any point in time is not believed to be significant based upon the time frame involved.

Regulatory and Environmental Compliance

We are subject to the requirements of environmental and health and safety laws and regulations in each country in which we operate. These include, among other things, laws regulating air emissions, water discharge, hazardous materials and waste management. We have an environmental management structure designed to facilitate and support our compliance with these requirements globally. Although it is our intent to comply with all such requirements and regulations, we cannot provide assurance that we are at all times in compliance. Environmental requirements are complex, change frequently and have tended to become more stringent over time. Accordingly, we cannot assure that environmental requirements will not change or become more stringent over time or that our eventual environmental costs and liabilities will not be material.

Certain environmental laws assess liability on current or previous owners or operators of real property for the cost of removal or remediation of hazardous substances. At this time, we are involved in various stages of investigation and cleanup related to environmental remediation matters at certain of our present and former facilities. In addition, there may be soil or groundwater contamination at several of our properties resulting from historical, ongoing or nearby activities.

As of December 31, 2020, the undiscounted reserve for environmental investigation and remediation was approximately $15.6 million. We do not currently possess sufficient information to reasonably estimate the amounts of environmental liabilities to be recorded upon future completion of studies, litigation or settlements, and we cannot determine either the timing or the amount of the ultimate costs associated with environmental matters, which could be material to our consolidated and combined results of operations and operating cash flows in the periods recognized or

19

paid. However, considering our past experience and existing reserves, we do not expect that environmental matters will have a material adverse effect on our consolidated and combined financial position.

Additionally, pursuant to the Honeywell Indemnity Agreement, Garrett ASASCO is obligated to make payments to Honeywell in amounts equal to