As confidentially submitted to the U.S. Securities and Exchange Commission on January 10, 2018. This draft registration statement has not been filed publicly with the Securities and Exchange Commission and all information contained herein remains confidential.

Registration No. __

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

INX LIMITED

(Exact name of registrant as specified in its charter)

| Gibraltar | 6200 | Not Applicable | ||

| (State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer | ||

| incorporation or organization) | Classification Code Number) | Identification No.) |

1.23 World Trade Center

Bayside Road

Gibraltar, GX11 1AA

Gibraltar

Tel: +350 200 44201

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Puglisi & Associates

850 Library Avenue, Suite 204

Newark, Delaware

+1 302 738 6680

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Mark S. Selinger, Esq. Lee A. Schneider, Esq. McDermott Will & Emery LLP 340 Madison Avenue New York, NY 10173 +1 212 547 5400 |

Yuval Horn, Adv. Roy Ribon, Adv. Horn & Co. Law Offices Amot Investments Tower 2 Weizmann Street, 24th Floor Tel Aviv 6423902, Israel +972 3 637 8200 |

Aaron Payas, CFA Hassans International Law Firm 57/63 Line Wall Road P.O. Box 199 Gibraltar GX11 1AA +350 200 79000 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered | Amount to be registered | Proposed maximum offering price per Token(2) | Proposed maximum aggregate offering price(2) | Amount of registration fee(3) | ||||||||||||

| INX Token (1) | 130,000,000 | $ | $ | $ | ||||||||||||

| (1) | Described more fully on page 66. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (3) | Calculated pursuant to Rule 457(o) based on an estimate of the proposed maximum aggregate offering price. |

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the Securities and Exchange Commission has declared this registration statement effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any state or jurisdiction where such offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION | DATED __, 2018 |

INX LIMITED

130,000,000 INX Tokens

This is our initial public offering. We are offering 130,000,000 INX Tokens, (the “INX Tokens” or “Tokens”). Each INX Token will entitle its holder to a pro rata distribution of 20% of our annual net cash flow from operating activities, payable on an annual basis, subject to certain exclusions and minimum distribution requirements. See “Description of INX Tokens.”

There is currently no public market for the INX Token and no guarantee can be provided whether such a market will be established. We expect an initial public offering price of $__ per Token. The initial public offering price was arbitrarily determined by our Board of Directors.

We are an emerging growth company, as defined in the U.S. Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”) and, as such, have elected to comply with certain reduced public company reporting requirements.

Purchasing INX Tokens involves a high degree of risk. See “Risk Factors” beginning on page 10 of this prospectus.

| Per Token | Total | |||||||

| Initial public offering price (1) | $ | $ | ||||||

| Proceeds to us (before expenses) | $ | $ | ||||||

| (1) | INX Tokens offered pursuant to this prospectus may be sold by our Company and distributed from time to time by our officers and directors directly to one or more purchasers. Our officers and directors will not receive any direct compensation for sales of INX Tokens. However, we reserve the right to engage broker-dealers who are FINRA members (“Selling Agents”) to participate in the offer and sale of our INX Tokens and to pay to such Selling Agents cash commissions of up to 7% of the gross proceeds from the sales of INX Tokens placed by them. In addition, INX Tokens may be offered for sale outside of the United States to non-U.S. persons by A-Labs Finance and Advisory Ltd. (“A-Labs”). Please refer to the section entitled “Plan of Distribution” for additional information. |

None of the United States Securities and Exchange Commission, the Gibraltar Financial Services Commission, or any state securities commission or other jurisdiction has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

We expect to deliver the INX Tokens to the purchasers in this offering on or about __, 2018.

The date of this prospectus is __, 2018.

i

Until and including __, 2018 (25 days after the date of this prospectus), all dealers that buy, sell, or trade INX Tokens, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to unsold allotments or subscriptions.

You should rely only on the information contained in this prospectus and any related free-writing prospectus that we authorize to be distributed to you. We have not authorized any person, including any underwriter, to provide you with information different from that contained in this prospectus or any related free-writing prospectus that we authorize to be distributed to you. This prospectus is not an offer to sell, nor is it seeking an offer to buy, the INX Tokens in any state where the offer or sale is not permitted. The information in this prospectus speaks only as of the date of this prospectus unless the information specifically indicates that another date applies, regardless of the time of delivery of this prospectus or of any sale of the INX Tokens offered hereby. Our business, financial condition, results of operations, and prospects may have changed since that date. We do not take any responsibility for, nor do we provide any assurance as to the reliability of, any information other than the information in this prospectus and any free writing prospectus prepared by us or on our behalf. Neither the delivery of this prospectus nor the sale of INX Tokens means that information contained in this prospectus is correct after the date of this prospectus.

Market data and certain industry data and forecasts used throughout this prospectus were obtained from sources we believe to be reliable, including market research databases, publicly available information, reports of governmental agencies, and industry publications and surveys. We have relied on certain data from third party sources, including internal surveys, industry forecasts, and market research, which we believe to be reliable based on our management’s knowledge of the industry. While we are not aware of any misstatements regarding the industry data presented in this prospectus, our estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under the heading “Risk Factors” and elsewhere in this prospectus.

Our financial statements are prepared and presented in accordance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or IASB. Our historical results do not necessarily indicate our expected results for any future periods.

Certain figures included in this prospectus have been subject to rounding adjustments. Accordingly, figures shown as totals in certain tables may not be an arithmetic aggregation of the figures that precede them.

Unless derived from our financial statements or otherwise noted, the terms “dollar,” “U.S. dollar,” “US$,” “USD,” and “$” refer to U.S. dollars, the lawful currency of the United States.

ii

This is only a summary of the prospectus and does not contain or summarize all of the information contained in this prospectus which is material and/or which may be important to you. You should read this entire prospectus, including “Risk Factors,” before making an investment decision about the INX Tokens.

Definitions used in this prospectus can be found in the section of entitled “Glossary of Defined Terms”.

Unless otherwise stated in this prospectus, references to:

| ● | “we,” “us,” “Company,” “our company” or “INX” are to INX Limited and its wholly owned subsidiaries; |

| ● | “INX Tokens,” “Tokens” or “our Tokens” are to INX Tokens as more fully described at page 66; |

| ● | “Companies Act” refers to Gibraltar Companies Act 2014; |

Overview

We are developing a regulated platform for trading blockchain assets and their derivatives (the “INX Exchange”). When fully operational, the INX Exchange is expected to offer professional traders and other institutional investors a trading platform with regulatory transparency and traditional marketplace practices, supported by a significant cash reserve. The INX Exchange is expected to offer both centralized and peer-to-peer professional trading services, with an INX subsidiary company serving as a central counterparty clearing house, and a suite of marketplace features and trading products, including the ability to take short positions and trade derivatives such as futures, options, and swaps.

The INX Exchange will utilize established practices common in other regulated financial services markets, such as traditional trading, clearing, and settlement procedures, regulatory compliance, capital and liquidity reserves and operational transparency. Additionally, when parties cannot locate matches for their proposed trades on the INX Exchange, we intend to offer liquidity through other alternative trading systems or through direct sales.

As part of our INX Exchange platform, we have created the INX Token, which is offered pursuant to this prospectus. After the INX Exchange is operational, holders of INX Tokens who have been duly identified through know-your-customer and anti-money laundering (“KYC/AML”) procedures will be entitled to certain rights. INX Token holders will be able to use the INX Token to pay INX Exchange transaction fees at a discount to other methods of payment or to post collateral on the INX Exchange at a more favorable ratio than other forms of collateral. Holders of INX Tokens will also be entitled to receive a pro rata distribution of 20% of our annual net cash flow from operating activities, payable on an annual basis, subject to certain exclusions and minimum distribution requirements. Further, in addition to a cash reserve to be comprised of a significant portion of the proceeds of this offering, we plan to maintain a capital reserve and liquidity fund of up to 110 million INX Tokens, consisting of 45 million INX Tokens created but not previously sold by the Company to the public and 20% of the INX Tokens received by the Company as payment of transaction fees, up to an additional 65 million INX Tokens. The Company may sell a portion of INX Tokens it receives as payment of transaction fees in future offerings to raise additional financing and to help maintain a public float of INX Tokens. See “Description of INX Tokens”.

One of our U.S. subsidiaries intends to file applications for registration as a broker-dealer and as an alternative trading system with FINRA and another U.S. subsidiary intends to register as a designated contract market and swap execution facility with the CFTC. Our subsidiary in Gibraltar intends to apply to the Gibraltar Financial Services Commission for a license under the Financial Services (Distributed Ledger Technology Providers) Regulations 2017 for its European-based operations.

1

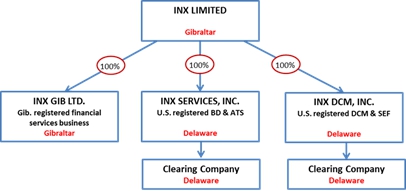

Corporate Information and Structure of INX

We are a Gibraltar private company limited by shares, incorporated on November 27, 2017. The majority of our issued share capital is held by Triple-V (1999) Ltd, an entity wholly owned by Shy Datika, our Chief Executive Officer and Chairman of the Board of Directors (see – “Principal Shareholders”) and the balance of our issued share capital is held by our employees, lenders and other service providers. We plan to have the following wholly-owned subsidiaries:

| ● | INX Services, Inc., a Delaware corporation, which will be a registered broker-dealer and an alternative trading system. INX Services, Inc. will form a wholly-owned Delaware subsidiary which will serve as a clearing company; |

| ● | INX DCM, Inc., which will be incorporated in Delaware and will act as a designated contract market and swap execution facility. INX DCM, Inc. will form a wholly-owned Delaware subsidiary which will serve as a clearing company; and |

| ● | INX GIB Ltd., which will be incorporated in Gibraltar as a private company limited by shares and will offer the Company’s services and products to the European market. We intend to apply to the Gibraltar Financial Services Commission for a license under the Financial Services (Distributed Ledger Technology Providers) Regulations 2017 for its European-based operations. |

INX Limited’s registered office is located at 1.23 World Trade Center, Bayside Road, Gibraltar, GX11 1AA, Gibraltar, and its telephone number is +350 200 44201. After the INX Exchange becomes fully operational, INX Limited intends to relocate its principal office to New York, NY.

Industry Overview

Background & Current Market

Blockchain assets, also known as “tokens” or “coins,” have experienced rapid growth since first introduced in 2009 with the launch of Bitcoin. As of December 31, 2017, blockchain assets had a total market capitalization of over $570 billion. Blockchain assets historically have not been issued by governments, banks or similar organizations but rather are collectively maintained by a decentralized user base, accessed through software, which also governs the blockchain asset’s creation, movement, and ownership. This lack of a single point of data collection is believed to enhance the security of traditional blockchain networks and blockchain assets.

The blockchain market has grown dramatically. As of December 31, 2017, approximately $4 billion in the aggregate had been raised through offerings of blockchain assets, many of which are initial coin offerings (“ICOs”), and over 120 blockchain asset exchanges provide basic buy and sell services for one or more blockchain assets. As of December 31, 2017, 56 exchanges of blockchain assets average daily trading volumes over $20,000,000 and 25 exchanges of blockchain assets average daily trading volume over $100,000,000. As of December 31, 2017, top blockchain asset exchanges, based on USD 24-hour volume, include Binance, Bitfinex, Bithumb, BitMEX, Bittrex, GDAX, HitBTC, OKEx, and Poloniex.

There has been growing institutional interest in operating regulated blockchain asset exchanges and utilizing blockchain assets in bank financing practices. In January 2017, UBS, BNY Mellon, Deutsche Bank, Santander, NEX and blockchain startup Clearmatics announced their own blockchain asset issuances with the intent to incorporate blockchain assets in currency-related transactions, encourage regulation by central banks and create fiat-like asset-collateralized networks on custom blockchain platforms. In December 2017, Bank of America was awarded a patent for an automated digital currency exchange system. On December 18, 2017, the Chicago Board of Exchange began trading in bitcoin futures, and was joined shortly thereafter by CME Group, also offering bitcoin futures.

2

The significant growth of the blockchain asset market and the lack of regulated trading in blockchain assets have triggered an increase in governmental scrutiny. On July 25, 2017, the Securities and Exchange Commission issued a Report of Investigation pursuant to Section 21(a) of the Securities Exchange Act of 1934 (the “Exchange Act”) that found that sales of tokens by a virtual organization known as The DAO (a “decentralized autonomous organization”) violated the federal securities laws by participating in the unregistered sale of securities. The SEC also has cautioned brokers, dealers and other market participants that (i) allow for payments in virtual currencies, (ii) allow customers to purchase virtual currencies on margin, or (iii) otherwise use virtual currencies to facilitate securities transactions to exercise particular caution, including ensuring that their virtual currency activities do not undermine their know-your-customer and anti-money laundering obligations.

Finally, recognizing that not all blockchain assets may be securities, the CFTC has stated that virtual currencies, like bitcoin, may be commodities that are within the purview of the CFTC. Because of the uncertainty built into a “facts and circumstances” analysis, as well as general regulatory uncertainty worldwide, companies have begun to structure their blockchain assets as securities and conduct sales of their blockchain assets as registered securities offerings. As blockchain assets take on the attributes of securities and market makers expand the breadth of blockchain asset trading products into spot, futures and derivative trading instruments, the need and demand for a regulated blockchain asset trading solution continues to grow.

Identified problems in the current blockchain asset platform or exchange markets include the following:

| ● | Pre-trade and post-trade services are limited. Clients of some of the current blockchain exchanges cannot continually manage blotter, reports, credit, position, technical analysis and investment tools during pre-trade actions and receive trade confirmations, reporting and access to pricing data during post-trade actions. This lack of transparency results in lower pricing performance, inefficiencies and ultimately higher trading risks. |

| ● | Lack of Trading History. Most blockchain asset exchanges do not or cannot present the entire history of trades to exchange participants in a manner that would be requested by a regulator. This lack of trading history does not allow regulatory agencies to effectively monitor transactions. |

| ● | Lack of Regulation. Lack of regulation of blockchain asset exchanges and blockchain asset trades leads to low customer and public confidence in both the exchanges and blockchain assets traded. Without regulation, blockchain asset exchanges assume less responsibility for what takes place on their platforms as compared to regulated exchanges. For example, blockchain asset exchanges are generally unable to verify the legitimate origin of funds in a trade and therefore cannot confirm that the trades are not in violation of anti-money laundering laws. In addition, current blockchain asset exchanges do not provide traditional trading protections, such as trading collateral capital and liquidity reserves, making professional traders unable or reluctant to conduct derivative trading on these exchanges. |

| ● | Lack of Clearing House. The clearing and settlement processes of current blockchain asset exchanges do not occur through traditional, regulated channels. Blockchain asset trading exchanges lack separate clearing houses which are an essential component of regulated trading marketplaces and help ensure the integrity of trades. The current blockchain asset markets settle trades, clear trades, collect and maintain margin monies, regulate delivery, and report trading data with no allocated capital to guarantee settlement. This results in higher clearing and settlement risk. |

| ● | No Physical Delivery for Short Trades. Physical delivery of underlying assets between parties to a short transaction helps ensure the completion of the transactions, regardless of other activities that are being conducted on the same exchange for other clients. Current blockchain asset marketplaces allow clients to leverage their trades by not possessing the assets being traded, known as a “naked” short sale, resulting in potential disruption of trading activity on the exchange or the weakening of the exchange’s financial stability due to the costs incurred by the exchange to cover naked short sales. |

| ● | Lack of Technological Capability. The trading platforms of blockchain asset exchanges generally do not have the technological capability to handle the large trading volumes or capture trades for multiple simultaneous trading requests without disruption or significant errors. The technology of many blockchain asset exchanges was not developed to handle the dramatic growth in demand to engage in blockchain trades and the market has witnessed exchange outages, sometimes for many hours, pricing errors, lack of user access to their funds, and other service related complaints. |

3

| ● | Lack of Pricing Transparency. There is no clear market standard for fees for trading blockchain assets. This is particularly true in the retail market where the pricing of blockchain assets may be affected by significant transaction fees. In addition, many unregulated exchanges do not clarify their fees, creating ambiguity with respect to the final price of trades. |

| ● | Significant Arbitrage. Arbitrage trading exploits the price differences of identical or similar financial instruments on different markets or in different forms. The pricing discrepancies among blockchain asset trading exchanges encourage arbitrage trading, which creates market inefficiencies and undermines the credibility of the exchanges. Lack of pricing transparency, and difficulties accessing these exchanges, exacerbates this problem. |

These weaknesses in current blockchain asset trading platforms reveal a significant opportunity in the blockchain asset industry for exchange providers with operations and services that provide functionality, transparency and collateralized trading platforms similar to those of regulated trading marketplaces.

Our Solution: A Single Regulated Integrated Platform of Exchange for Blockchain Assets

We believe that the only comprehensive solution to the issues that we have identified, and to the shortcomings of the current marketplace, is the development of a new, blockchain based marketplace that is subject to governmental oversight. We are designing our platform to provide the following solutions to the problems identified above, which we believe will make the INX Exchange an attractive choice for blockchain trading:

| ● | Robust Pre-Trade and Post-Trade Services. We are designing the INX Exchange to permit clients to continually manage blotter, reports, credit, position, technical analysis and investment tools during pre-trade actions and receive trade confirmations, reporting and access to pricing data during post-trade actions. In addition, where parties do not locate matches for their proposed trades on our system, we plan to obtain liquidity through other ATSs or through direct sales. We expect that these attributes will allow greater pricing performance and lower trading risks. |

| ● | Historical Trading Record. We plan to implement KYC/AML procedures from the first recorded transaction on the INX Exchange and provide transparency so that clients have the ability to review all activities taken by them, and believe that this accessibility will supplement the transparency of blockchain assets. |

| ● | Regulation. We believe that regulatory oversight of the INX Exchange will instill greater confidence in the INX Exchange compared to unregulated blockchain asset exchanges. As the ownership of blockchain assets becomes more commonplace and more professional traders enter the blockchain market, we believe that clients will expect regulatory safeguards, comparable to the current fiat and stock exchanges, when making blockchain trades. |

| ● | Clearing House. We plan to create separate clearing houses for trading activities on our exchange which will facilitate transactions on our platform while providing regulatory agencies with access to monitor and supervise transactions on our exchange. |

| ● | Cash Reserve Fund; Capital Reserve and Liquidity Fund. We plan to establish a cash reserve fund comprised of a portion of the proceeds of this offering. In addition, we plan to establish a significant capital reserve and liquidity fund of up to 110 million INX Tokens, comprised of 45 million INX Tokens created but not previously sold by the Company to the public, and 20% of the INX Tokens received by the Company as payment for transaction fees, up to an additional 65 million INX Tokens. We believe that this fund will allow the INX Exchange to cover shortfalls in transactions, thereby introducing an important, additional layer of comfort for the investors, traders and clients. |

| ● | Allowing Physical Delivery and Short Trading. We believe that the INX Exchange’s requirement of physical delivery in short and derivatives transactions improves exchange participants’ risk management abilities and will result in increased trade volumes and greater diversity in the financial instruments utilized for blockchain assets. We believe that hedge transactions, accompanied with physical delivery, will therefore be an incentive for trading on the INX Exchange. |

4

| ● | Our Robust Technology. We intend to develop technology for the INX Exchange to support high volumes of traffic to enable rapid trading activity. We believe that our technology will help alleviate the current outages that have taken place on other blockchain asset exchanges, help improve market liquidity, decrease bid-ask spreads and enhance market efficiencies. |

| ● | Transparent Pricing. We plan to set transparent trading fees that will be available to market participants prior to entering into a transaction. As a result, the cost of trading on our exchange will have a limited effect on the pricing of blockchain assets, which will be a function of the parties’ orders. |

| ● | Fixed Rates; Arbitrage Prevention. We plan to establish fixed rates for the blockchain assets traded on the INX Exchange, which rates will be available to all market participants. We also plan to implement procedures that will enable easy access to our trading system, which, together with pricing transparency, should decrease exposure to arbitrage trading and enhance the efficiency of the trading market. Further, the Company will not engage in proprietary trading on its own platform (or any other platform) and will not act as a market maker. |

Our Development Plan

We are designing our trading platform to provide clients with a cross-asset, multi-currency non-biased execution trading solution and to function as broker, execution, and clearing agent. Our goal in the development of the INX platform is to offer professionals in the financial services community a comprehensive, interactive platform that allows for seamless integrated trading, real-time risk management and reporting and administration tools. The INX Exchange will permit trading of multiple blockchain assets, including trades in spot, futures and derivative forms. The INX Exchange is expected to offer both centralized and peer-to-peer professional trading with an INX subsidiary company serving as a central counterparty clearing house. This trading platform will help our customers automate and coordinate front-office trading functions, middle-office risk management and reporting functions, and back-office accounting functions.

We are developing our system in modules to allow for a phased roll out of features in accordance with regulatory approvals that we receive and the technological development of the INX Exchange. See “Business— Phases of Development.”

We have currently developed the INX Token. After the INX Exchange is operational, holders of INX Tokens who have been duly identified through KYC/AML procedures will be entitled to certain rights. INX Token holders will be able to use the INX Token to pay INX Exchange transaction fees at a discount to other methods of payment or to post collateral on the INX Exchange at a more favorable ratio than other forms of collateral. Holders of INX Tokens will also be entitled to receive a pro rata distribution of 20% of our annual net cash flow from operating activities, payable on an annual basis, subject to certain exclusions and minimum distribution requirements. Further, in addition to a cash reserve to be comprised of a significant portion of the proceeds of this offering, we plan to maintain a capital reserve and liquidity fund of up to 110 million INX Tokens, consisting of 45 million INX Tokens created but not previously sold by the Company to the public and 20% of the INX Tokens received by the Company as payment of transaction fees, up to an additional 65 million INX Tokens .. The Company may sell a portion of INX Tokens it receives as payment of transaction fees in future offerings to raise additional financing and to help maintain a public float of INX Tokens. See “Description of INX Tokens”.

Our Growth Strategies

We believe that our operational capabilities will strengthen and expand as the INX Exchange completes each phase of development. This will enable us to launch several growth strategies, including the following.

| ● | Active expansion of institutional blockchain asset trading and large-scale block transactions. The Company plans to promote the INX Exchange with institutional and other accredited investors such as family offices, hedge funds and others who require a platform that allows blockchain asset derivative trading and large-scale block transactions. |

| ● | Monetize market data and connectivity. We plan to serve as a hub for blockchain asset traders, institutional investors, commercial banks and individuals trading blockchain asset derivatives. As we attract more clients, we expect that we will accumulate non-proprietary big-data relating to trading behavior and related market statistics. We plan to use this data for internal use and as a product to be sold to institutional investors and trade analysts. |

| ● | Strategic opportunities. Upon completion of development phases, we plan to pursue strategic alliances with commercial banks and other licensed and regulated blockchain asset exchanges for the expansion of our business. In addition, we believe that a part of our future growth strategy will include the acquisitions and integration of other blockchain service providers under the INX Exchange’s regulated processes. |

5

| ● | The INX Token. Use of the INX Token is intended to create a “virtuous cycle”. Holders of INX Tokens will be entitled to a distribution based on our annual net cash flow from operating activities, subject to certain exclusions and minimum distribution requirements. Our profit share model makes these INX Token holders beneficiaries of the growth and success of the Company’s operations. This in turn increases the value of the INX Token and its acceptance as a method of payment and as collateral on the INX Exchange, which may be done at a discount to other methods of payment or at a more favorable ratio than other forms of collateral. |

| ● | Single integrated platform. We believe that the INX Exchange’s ability to provide customers with a single integrated platform to access an array of services and features preferred by participants in the financial services community will attract high volume traders who need a multifunctional trading platform. Our competitive position is also bolstered by the breadth of workflow functionalities we offer across the entire transaction lifecycle, including pre-trade, trade and post-trade services. |

Competition

We face intense competition in the blockchain asset trading market on a global level. While we are not aware of any blockchain asset exchange that currently provides the services we expect the INX Exchange to provide, the market for trading blockchain assets has generated considerable interest and is continually evolving with new entrants to the market. In addition, established financial institutions have expressed interest in operating regulated blockchain asset exchanges and utilizing blockchain assets in bank financing practices. See “Business— Competition.”

Risk Factors

Our business is subject to numerous risks, as more fully described in the section titled “Risk Factors” immediately following this prospectus summary. You should read and carefully consider these risks and all of the other information in this prospectus, including the financial statements and the related notes included elsewhere in this prospectus, before deciding whether to invest in INX Tokens. In particular, such risks include, but are not limited to, the following:

| ● | We may not be able to develop the INX Exchange as contemplated or at all. |

| ● | Blockchain networks represent a new and rapidly changing industry and there remains relatively limited use of blockchain networks and blockchain assets. |

| ● | Blockchain technology is an emerging technology that is novel and untested. |

| ● | The legal framework of regulations applicable to blockchain technologies, virtual currencies, tokens and token offerings is uncertain. |

| ● | Tax authorities may disagree with our tax positions with regard to the Company, its business and the INX Token and may ask us to revise these positions in a manner that could adversely affect you. |

| ● | The prices of blockchain assets are extremely volatile and fluctuations in the price of blockchain assets could materially affect our profits. |

| ● | Our company has no operating history. | |

| ● | There is currently no trading market for our INX Tokens and, if a trading market were to develop, the price of the INX Tokens may be volatile. |

| ● | We expect to face intense competition from other companies. |

| ● | We may not receive regulatory approval in the various jurisdictions in which we plan to operate our businesses. |

| ● | We may not be able to prevent illegal activity from occurring over our exchange. |

| ● | Our securities business and related clearing operations expose us to material default and liquidity risk. |

| ● | We rely on third party contractors for the design, development and implementation of our exchange infrastructure. |

| ● | Systems failures or capacity constraints could materially harm our ability to conduct our operations and execute our business strategy. |

| ● | We may be a target of cyber-attacks and other cyber security risks. |

6

| ● | Valuation of the INX Token is difficult. |

| ● | There can be no assurance that we will be able to distribute any funds to INX Token holders. |

| ● | The tax characterization of Tokens is uncertain and you must seek your own tax advice in connection with purchasing Tokens. |

Implications of Our Emerging Growth Company and Foreign Private Issuer Status

As a company with less than $1.07 billion in revenue for our year ending December 31, 2017, we qualify as an “emerging growth company” under Section 2(a) of the Securities Act of 1933, as amended, (the “Securities Act”), as modified by the U.S. Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). As an emerging growth company, we may take advantage of certain exemptions from reporting requirements that generally apply to public companies, including the auditor attestation requirements with respect to internal control over financial reporting under Section 404 of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”), compliance with new standards adopted by the Public Company Accounting Oversight Board (the “PCAOB”) requiring communication of critical audit matters in the independent public accounting firm report on our annual financial statements, exemption from say-on-pay, say-on-frequency, and say-on-golden parachute voting requirements, and reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements.

We will remain an emerging growth company until the earliest of: (i) the last day of our fiscal year during which we have total annual gross revenue of at least $1.07 billion; (ii) the last day of our fiscal year following the fifth anniversary of the completion of this offering; (iii) the date on which we have, during the previous three-year period, issued more than $1.0 billion in non-convertible debt; or (iv) the date on which we are deemed to be a “large accelerated filer” under the Securities Exchange Act of 1934, as amended. Once we cease to be an emerging growth company, we will not be entitled to the exemptions provided in the JOBS Act.

Upon completion of this offering, we will also be subject to the reporting requirements of the Securities Exchange Act of 1934, as amended, (the “Exchange Act”), that are applicable to “foreign private issuers,” and under those requirements we will file reports with the Securities and Exchange Commission (the “SEC”). As a foreign private issuer we are exempt from certain rules and regulations under the Exchange Act, that are applicable to other public companies that are not foreign private issuers. For example, we will not be required to issue quarterly reports, proxy statements that comply with the requirements applicable to U.S. domestic reporting companies, or individual executive compensation information that is as detailed as that required of U.S. domestic reporting companies. We will also have four months after the end of each fiscal year to file our annual report with the SEC and will not be required to file current reports as frequently or promptly as U.S. domestic reporting companies. We may also present financial statements pursuant to International Financial Reporting Standards (“IFRS”), instead of pursuant to U.S. generally accepted accounting principles (“U.S. GAAP” or “GAAP”). Our executive officers, directors, and principal shareholders will be exempt from the requirements to report transactions in our equity securities and from the short-swing profit liability provisions contained in Section 16 of the Exchange Act. As a foreign private issuer, we will also not be subject to the requirements of Regulation FD (Fair Disclosure) promulgated under the Exchange Act.

We may choose to take advantage of any, some, or all of the exemptions available to us as an emerging growth company or as a foreign private issuer. We have taken advantage of reduced reporting requirements in this prospectus.

Accordingly, the information contained in this prospectus may be different from the information you receive from other public companies in which you hold stock. Please see the section of this prospectus titled “Risk Factors—Risks Relating to our Incorporation in Gibraltar” for a description of exemptions that apply to emerging growth companies and foreign private issuers.

7

THE OFFERING

| Security Offered | INX Token (the “INX Token”), an ERC20 compliant token. | |

| Token ticker on the INX Exchange | INX | |

| Total Tokens issued in this offering | 130,000,000 Tokens | |

| Total Tokens to be outstanding (and not held by INX Limited) immediately after this offering | 147,626,562 Tokens | |

| Use of Proceeds |

We intend to use the net proceeds raised from the sale of INX Tokens in this offering as follows: $18 million for the operation of the INX Exchange, including continued development of the INX Exchange (see “Business—Phases of Development”), marketing and improvement of security measures. The balance of the net proceeds will be used to establish and capitalize a cash reserve fund for the INX Exchange, which will satisfy regulatory requirements. See “Use of Proceeds”

| |

| Termination of the Offering | The offering will terminate upon the earlier to occur of: (i) the sale of all of the 130,000,000 Tokens being offered, or (ii) 365 days after this registration statement is declared effective by the SEC. | |

| Uses of the INX Token on the INX Exchange |

(1) Payment of transaction fees at an average discount of 20% as compared to fees paid using other methods of payment;

(2) Deposit as a portion of collateral for short positions at a more favorable ratio than other forms of collateral. | |

| Distributions on INX Tokens | Each INX Token will entitle its holder to a pro rata distribution of 20% of our annual net cash flow from operating activities, payable on an annual basis, subject to certain exclusions and minimum distribution requirements. See “Description of INX Tokens.” | |

| Capital Reserve & Liquidity Fund | 45,000,000 INX Tokens will be set aside in a capital reserve and liquidity fund. Additional Tokens will be contributed to the reserve as INX Tokens are received by the Company in payment of INX Exchange transaction fees, up to a maximum of 110,000,000 INX Tokens. | |

| Tokens Reserved for Employee Issuances | 7,373,438 INX Tokens have been reserved for future sale and issuance to employees of the Company. | |

| Total Tokens; Mining | 200,000,000 INX Tokens have been created. There is no mining of INX Tokens and there is no other means of creating new INX Tokens. | |

| Transfer Agent | Computershare Limited |

8

SUMMARY FINANCIAL DATA

The following summary statement of comprehensive loss for the period from September 1, 2017 (inception of the Company) to December 31, 2017 and the summary balance sheet data as of December 31, 2017 should be read together with our audited financial statements and accompanying notes, as well as the information provided in this prospectus. Our historical results are not necessarily indicative of the results that may be expected in the future.

Summary Statement of Comprehensive Loss

From September 1, 2017 (inception) through December 31, 2017 (USD in thousands) | ||||

| Operating expenses: | ||||

| General and administrative | 586 | |||

| Loss from operations | 586 | |||

| Fair value adjustment of INX Token liability | 50 | |||

| Finance expenses | 1 | |||

| Net Loss | 637 | |||

Summary Balance Sheet Data

| December 31, | ||||

| 2017 | ||||

| Total Assets | 517 | |||

| Working Capital | 62 | |||

| Total Liabilities | 455 | |||

| Total shareholders’ equity | 62 | |||

9

Investing in INX Tokens involves a high degree of risk. You should carefully consider the risks we describe below, along with all of the other information set forth in this prospectus, including the section entitled “Cautionary Note Regarding Forward-Looking Statements” and our financial statements and the related notes beginning on page F-1, before deciding to purchase INX Tokens. The risks and uncertainties described below are those significant risk factors, currently known and specific to us, that we believe are relevant to an investment in INX Tokens. If any of these risks materialize, our business, results of operations or financial condition could suffer, the price of INX Tokens could decline substantially and you could lose part or all of your investment. Additional risks and uncertainties not currently known to us or that we now deem immaterial may also harm us and adversely affect your investment in INX Tokens.

You may lose all monies that you spend purchasing INX Tokens. If you are uncertain as to our business and operations or you are not prepared to lose all monies that you spend purchasing INX Tokens, we strongly urge you not to purchase any INX Tokens. We recommend you consult legal, financial, tax and other professional advisors or experts for further guidance before participating in the offering of our INX Token as further detailed in this prospectus. Further, we recommend you consult independent legal advice in respect of the legality of your participation in the INX Token sale.

We do not recommend that you purchase INX Tokens unless you have prior experience with cryptographic tokens, blockchain-based software and distributed ledger technology and unless you have received independent professional advice.

RISKS RELATED TO BLOCKCHAIN ASSETS

Blockchain is a nascent and rapidly changing technology and there remains relatively small use of blockchain networks and blockchain assets in the retail and commercial marketplace. The slowing or stopping of the development or acceptance of blockchain networks may adversely affect an investment in our Company.

The development of blockchain networks is a new and rapidly evolving industry that is subject to a high degree of uncertainty. Factors affecting the further development of the blockchain industry include:

| ● | continued worldwide growth in the adoption and use of blockchain networks and assets; |

| ● | the maintenance and development of the open-source software protocol of blockchain networks; |

| ● | changes in consumer demographics and public tastes and preferences; |

| ● | the popularity or acceptance of the Bitcoin or Ethereum networks; |

| ● | the availability and popularity of other forms or methods of buying and selling goods and services, including new means of using fiat currencies; |

| ● | government and quasi-government regulation of blockchain networks and assets, including any restrictions on access, operation and use of blockchain networks and assets; and |

| ● | the general economic environment and conditions relating to blockchain networks and assets. |

Our business model is dependent on continued investment in and development of the blockchain industry and related technologies. If investments in the blockchain industry become less attractive to investors or innovators and developers, or if blockchain networks and assets do not gain public acceptance or are not adopted and used by a substantial number of individuals, companies and other entities, it could have a material adverse impact on our prospects and our operations.

The application of distributed ledger technology is novel and untested and may contain inherent flaws or limitations.

Blockchain is an emerging technology that offers new capabilities which are not fully proven in use. There are limited examples of the application of distributed ledger technology. In most cases, software used by blockchain asset issuing entities will be in an early development stage and still unproven.

The creation and operation of a digital system for the public trading of blockchain assets utilizing a distributed ledger will be subject to potential technical, legal and regulatory constraints. There is no warranty that the process for receiving, use and ownership of blockchain assets will be uninterrupted or error-free and there is an inherent risk that the software, network, blockchain assets and related technologies and theories could contain undiscovered technical flaws or weaknesses, the cryptographic security measures that authenticate transactions and the distributed ledger could be compromised, and breakdowns and trading halts could cause the partial or complete inability to use or loss of blockchain assets.

10

Risks associated with the distributed ledger technology could affect the market for blockchain assets which could have a materially adverse effect on an investment in the Company.

The open-source structure of blockchain software means that blockchain networks may be susceptible to developments by users or contributors that could damage the reputation of those blockchain assets. Blockchain networks may be the target of malicious cyberattacks or may contain exploitable flaws, which may result in security breaches and the loss or theft of blockchain assets.

Most blockchain networks operate based on some form of open-source software. An open source project is not represented, maintained or monitored by an official organization or authority.

The open-source nature of blockchain network software means that it may be difficult for a blockchain asset issuer or its contributors to maintain or develop blockchain networks. Developers and other contributors to blockchain network protocols are generally not directly compensated for their contributions in maintaining and developing the protocol. If the awards of blockchain assets for solving blocks and transaction fees for recording transactions are not sufficiently high to incentivize miners, miners may respond in a way that reduces confidence in the blockchain network. Instead, most blockchain networks provide that miners receive awards and transaction fees for recording transactions and maintaining the blockchain network. Such fees are generally paid in the blockchain asset of that network.

If the awards and fees paid for maintenance of a network are not sufficiently high to incentivize miners, miners may respond in a way that reduces confidence in the blockchain network. To the extent that any miners cease to record transactions in solved blocks, transactions that do not include the payment of a transaction fee will not be recorded on the blockchain until a block is solved by a miner who does not require the payment of transaction fees. Any widespread delays in the recording of transactions could result in a loss of confidence in the blockchain network and its assets.

Blockchain networks may also be the target of malicious attacks seeking to identify and exploit weaknesses in the software. Third parties not affiliated with the issuer may introduce weaknesses or bugs into the core infrastructure elements of the blockchain network and open-source code which may result in the loss or theft of blockchain assets.

Such events may result in a loss of trust in the security and operation of blockchain networks and a decline in user activity which could have a negative impact on the Company.

The prices of blockchain assets are extremely volatile. Fluctuations in the price of Bitcoin, Ether and/or other blockchain assets could materially and adversely affect the Company.

The prices of blockchain assets such as Bitcoin and Ether have historically been subject to dramatic fluctuations and are highly volatile, and the market price of other blockchain assets may also be highly volatile. As relatively new products and technologies, blockchain assets have only recently become accepted as a means of payment for goods and services, and such acceptance and use remains limited. Conversely, a significant portion of demand for blockchain assets is generated by speculators and investors seeking to profit from the short- or long-term holding of blockchain assets. A lack of expansion, or a contraction of adoption and use of blockchain assets, may result in increased volatility or a reduction in the price of blockchain assets.

Several additional factors may influence the market price of blockchain assets, including, but not limited to:

| ● | Global blockchain asset supply; | |

| ● | Global blockchain asset demand, which can be influenced by the growth of retail merchants’ and commercial businesses’ acceptance of blockchain assets like virtual currencies as payment for goods and services, the security of online blockchain asset exchanges and digital wallets that hold blockchain assets, the perception that the use and holding of blockchain assets is safe and secure, and the regulatory restrictions on their use; | |

| ● | Changes in the software, software requirements or hardware requirements underlying the blockchain networks; | |

| ● | Changes in the rights, obligations, incentives, or rewards for the various participants in blockchain networks; | |

| ● | Investors’ expectations with respect to the rate of inflation; | |

| ● | Interest rates; | |

|

|

● | Currency exchange rates, including the rates at which blockchain assets may be exchanged for fiat currencies; |

| ● | Fiat currency withdrawal and deposit policies of blockchain asset exchanges and liquidity on such exchanges; | |

| ● | Interruptions in service or other failures of major blockchain asset exchanges; | |

| ● | Investment and trading activities of large investors, including private and registered funds, that may directly or indirectly invest in blockchain networks or blockchain assets; |

11

| ● | Monetary policies of governments, trade restrictions, currency devaluations and revaluations; | |

| ● | Regulatory measures, if any, that affect the use of blockchain assets; |

| ● | The maintenance and development of the open-source software utilized in blockchain networks; | |

| ● | Global or regional political, economic or financial events and situations; or | |

| ● | Expectations among blockchain network participants that the value of such blockchain assets will soon change. |

A decrease in the price of a single blockchain asset may cause volatility in the entire blockchain industry and may affect other blockchain assets. For example, a security breach that affects investor or user confidence in Ether or Bitcoin may affect the industry as a whole and may also cause the price of other blockchain assets to fluctuate.

The value of blockchain assets and fluctuations in the price of blockchain assets could materially and adversely affect our business and investment in the Company.

The regulatory regimes governing blockchain technologies, virtual currencies, tokens and token offerings are uncertain, and new regulations or policies may materially adversely affect the development of blockchain networks and the use of blockchain assets.

Initially, it was unclear how distributed ledger technologies, blockchain assets and the businesses and activities utilizing such technologies and assets would fit into the current web of government regulation. As blockchain networks and blockchain assets have grown in popularity and in market size, international, federal, state and local regulatory agencies have begun to clarify their position regarding the sale, purchase and ownership of blockchain assets.

Regulation of blockchain networks remains in its early stages but it is likely to evolve significantly. Such evolution is subject to uncertainty and may vary significantly among jurisdictions. Various legislative and executive bodies in the United States and in other countries have shown that they intend to adopt legislation or take enforcement actions, which may severely impact the development and growth of blockchain networks and the adoption and use of blockchain assets.

New or changing laws and regulations or interpretations of existing laws and regulations, in the United States or elsewhere, may materially and adversely impact the value of blockchain assets, the liquidity and market price of blockchain assets, the ability to access marketplaces or exchanges on which to trade blockchain assets, and the structure, rights and transferability of blockchain assets. Governments may seek to ban transactions in blockchain assets altogether. See “Business—Regulatory Oversight of Blockchain Assets.” The Company may be prevented from entering, or it may be required to cease operations in, a jurisdiction that makes it illegal or commercially unviable or undesirable to operate in such jurisdiction. Enforcement, or the threat of enforcement, may also drive a critical mass of participants and trading activity away from regulated markets such as the INX Exchange and toward unregulated exchanges.

Although it is impossible to predict the positions that will be taken by certain governments, any regulatory changes in affecting blockchain assets could be substantial and materially adverse to the development and growth of our business and investment in the Company.

The blockchain asset trading ledger is publicly available which may give rise to privacy concerns.

The distributed ledger used to record transfers of ownership of blockchain assets is generally available to the public and stores the complete trading history from inception of the issuance of the respective blockchain asset. The blockchain assets are represented by ledger balances and secured by cryptographic key pairs and only the public-key-derived wallet address is exposed to the public on the distributed ledger. The personal identity information necessary to associate a public key representing a given block of digital securities with the owner of those securities being maintained in a separate database that is not exposed to the public.

As such, transparent trading data, other than holder identity, with respect to blockchain assets will be publicly available. This may make it more difficult for holders of blockchain assets to execute certain trading strategies. Security breaches with respect to the holders’ personal identity information database could result in theft of the information necessary to link personal identity with public keys, and thus the stolen information could be used to determine the affected holder’s complete trading history. Concerns over these issues may limit adoption of this novel trading system by a range of potential investors, reducing liquidity of blockchain assets.

There are also a number of data protection, security, privacy and other government- and industry-specific requirements that are implicated by utilizing a distributed ledger. If blockchain networks are unable to satisfy data protection, security, privacy, and other government-and industry-specific requirements, their growth could be harmed.

Blockchain transactions are irrevocable and stolen or incorrectly transferred blockchain assets may be irretrievable. As a result, any incorrectly executed blockchain asset transactions could adversely affect an investment in the Company.

Blockchain asset transactions are not, from an administrative perspective, reversible without the consent and active participation of the recipient of the transaction or, in theory, control or consent of a majority of the processing power on such blockchain asset’s network. Once a transaction has been verified and recorded in a block that is added to the blockchain, an incorrect transfer of blockchain assets or a theft of blockchain assets generally will not be reversible. The risk of such loss could limit the adoption of blockchain assets and adversely affect an investment in the Company.

12

RISKS RELATED TO OUR COMPANY’S OPERATIONS

Our ability to develop the INX Exchange faces operational, technology and regulatory challenges and we may not be able to develop the INX Exchange as contemplated or at all.

Our proposed platform is complex and its creation requires the integration of multiple technologies and the development of new software. We may not be able to develop the INX Exchange as contemplated by our business model or at all. Any events or circumstances which adversely affect the Company or any of our affiliated operating entities may have a corresponding adverse effect on our development of the INX Exchange, including but not limited to the development, structuring and launch of the INX Exchange. Such adverse effects would correspondingly have an impact on the utility, liquidity, and the trading price of INX Tokens.

The development and maintenance of the INX Exchange could lead to unanticipated and substantial costs, delays or other operational or financial difficulties. There can be no assurance that we will have the financial and technological resources necessary to complete the development of the INX Exchange if its development costs more than we have estimated or requires technology and expertise that we do not have and cannot develop.

Moreover, even if we are able to develop the INX Exchange as contemplated, we may not be able to develop the platform on a timely basis, and our platform design and technology may be incompatible with new or emerging forms of blockchain assets or related technologies and consequently not be a viable trading vehicle for these blockchain assets. Any of these factors could materially adversely affect our ability to commercialize and generate any revenue from our proposed INX Exchange.

Further, there can be no assurance that our platform will gain the acceptance of regulators, customers or other market participants. Because blockchain asset trading is in its early stages, it is difficult to predict the future regulatory oversight that we may face or future preferences and requirements of blockchain asset traders. Failure to achieve acceptance from any or all of these constituents could impede our ability to develop and sustain a commercial business.

We have no operating history.

We are a recently formed company established under the laws of Gibraltar with minimal activity and no historical operating results, and we will not commence operations of the INX Exchange until obtaining funding through this offering. Because we lack an operating history, you have no basis upon which to evaluate our ability to achieve our business objective. Our proposed operations are subject to all business risks associated with a new enterprise. The likelihood of our creation of a viable business must be considered in light of the problems, expenses, difficulties, complications, and delays frequently encountered in connection with the inception of a business operating in a relatively new, highly competitive, and developing industry. There can be no assurance that we will ever generate any operating activity or develop and operate the business as planned. If we are unsuccessful at executing on our business plan, our business, prospects, and results of operations may be materially adversely affected and investors may lose all or a substantial portion of their investment.

We expect to face intense competition from other companies and if we are not able to successfully compete, our business, financial condition and operating results will be materially harmed.

We expect to encounter competition in all aspects of our business, including from entities having substantially greater capital and resources, offering a wide range of products and services and in some cases operating under a different and possibly less stringent regulatory regime.

We will also face competition from other futures, securities and securities option exchanges; over-the-counter markets (OTC); clearing organizations; large industry participants; swap execution facilities; alternative trade execution facilities; technology firms, including electronic trading system developers, and others. Many of our competitors and potential competitors have greater financial, marketing, technological and personnel resources than we do. In addition, many of our competitors may offer a wider range of bundled services, have broader name recognition, and have larger customer bases than we do.

13

New entrants may enter the market with alternative methods of providing trade execution and related services, and existing competitors often launch new initiatives.

Our ability to develop competitive advantages will require continued enhancements to our products, investment in the development of our services, additional marketing activities and enhanced customer support services. There can be no assurance that we will have resources to make sufficient investments in the development of our services, that our competitors will not devote significantly more resources to competing services or that we will otherwise be successful in developing market share. If competitors offer superior services, our market share could be affected and this would adversely impact our business and results of operations.

Failure to keep up with rapid changes in industry-leading technology, products and services could negatively impact our results of operations.

The institutional financial services industry is subject to rapid technological change and evolving industry standards. User demands become greater and more sophisticated as the dissemination of products and information to customers increases. If we are unable to anticipate and respond to the demand for new services, products and technologies, innovate in a timely and cost-effective manner and adapt to technological advancements and changing standards, we may be unable to compete effectively, which could have a material adverse effect on our business. Many of our competitors have significantly greater resources than we do to fund research and development initiatives. Moreover, the development of technology-based services is a complex and time-consuming process. New products and enhancements to existing products can require long development and testing periods. Significant delays in new product releases, failure to meet key deadlines, or significant problems in creating new products could negatively impact our revenues and profits.

We may not receive regulatory approval in the various jurisdictions in which we plan to operate our businesses.

We are seeking or we plan to seek registrations with the SEC, FINRA, the CFTC and various other regulatory bodies both in the U.S. and in other countries. If we fail to qualify for registrations under any of these authorities, we may be unable to execute our business plan as a provider of financial services. This would have a broad impact on us and could have a material adverse effect on our businesses, financial condition, results operations and prospects and, as a result, investors could lose all or most of their investment. In addition, any such action could also cause us significant reputational harm, which, in turn, could seriously harm the Company.

Firms in the financial services industry have experienced increased scrutiny in recent years. Such regulatory or other actions may lead to penalties, fines, disbarment and other sanctions which could place restrictions or limitations on our operations and otherwise have a material adverse effect on our businesses.

The securities markets and the brokerage industry in which we operate are subject to extensive, evolving regulation that imposes significant costs and competitive burdens that could materially impact our business.

Most aspects of our broker-dealer operations will be highly regulated, including regulated oversight over sales and reporting practices, operational compliance, capital requirements and licensing of employees. Accordingly, we face the risk of significant intervention by regulatory authorities such as the SEC and FINRA in the U.S. and their equivalents in other countries.

Compliance with regulations may require us and our customers to dedicate significant financial and operational resources that could result in some participants leaving our markets or decreasing their trading activity, which would negatively affect our profitability. We expect to continue to incur significant costs to comply with the extensive regulations that apply to our business.

See “Business—Regulation of Our Market” for a description of potential regulation of our business.

As we expand our business, we may be exposed to increased and different types of regulatory requirements. We may become subject to new regulations or changes in the interpretation or enforcement of existing regulations, which may adversely affect our business. Also, regulatory changes that impact how our customers conduct their business may impact our business and results of operations. The U.S. federal government and other governments outside of the United States may implement new or revised regulatory requirements for the financial services industry. Any changes to the regulatory rules could cause us to expend more significant compliance, business and technology resources, incur additional operational costs and create additional regulatory exposure.

14

If we fail to comply with applicable laws, rules or regulations, we may be subject to censure, fines, cease-and-desist orders, suspension of our business, removal of personnel or other sanctions, including revocation of our broker-dealer registrations, our designations as a contract market and derivatives clearing organization.

The extent to which blockchain assets are used to fund criminal or terrorist enterprises or launder the proceeds of illegal activities could materially impact our business.

The potential, or perceived potential, for anonymity in transfers of bitcoin and similar blockchain assets, as well as the decentralized nature of blockchain networks, has led some terrorist groups and other criminals to solicit bitcoins and other blockchain assets for capital raising purposes. As blockchain assets have grown in both popularity and market size, the U.S. Congress and a number of U.S. federal and state agencies have been examining the operations of blockchain assets, their users and exchanges, concerning the use of blockchain assets for the purpose of laundering the proceeds of illegal activities or funding criminal or terrorist enterprises.

In addition to the current market, new blockchain networks or similar technologies may be developed to provide more anonymity and less traceability. There is also the potential that other blockchain asset exchanges may court such illicit activity by not adhering to know-your-customer and anti-money laundering practices.

We may not be able to prevent illegal activity from occurring over our exchange. The use of blockchain assets for illegal purposes, or the perception of such use, over our exchange or on other exchanges could result in significant legal and financial exposure, damage to our reputation, damage to the reputation of blockchain assets and a loss of confidence in the services provided by our exchange and the blockchain asset community as a whole. This could result in regulatory penalties which could have an adverse effect on our business.

We may not have sufficient cash flow from operating activities, cash on hand and the ability to obtain borrowing capacity to finance required capital expenditures, fund strategic initiatives and meet our other cash needs. These obligations require a significant amount of cash, and we may need additional funds, which may not be readily available.

The viability of our business will be dependent on the availability of adequate capital to develop and maintain our business and meet our regulatory capital requirements. We will need to continue to invest in our operations for the foreseeable future to carry out our business plan. If the INX Exchange does not attract clients and does not achieve the expected operating results, we will need to seek additional financing or revise our business plan. Our ability to borrow additional funds may be impacted by financial lending institutions’ ability or willingness to lend to us on commercially acceptable terms.

Low levels of operating cash flow together with limited access to capital or credit in the future could have an impact on our ability to meet our regulatory capital requirements, invest in our software and infrastructure, engage in strategic initiatives, make acquisitions or strategic investments in other companies, react to changing economic and business conditions, repay our outstanding debt, or make dividend payments. Such outcomes could have an adverse effect on our business, financial condition and operating results.

Our securities business and related clearing operations expose us to material default and liquidity risk.

We plan to self-clear blockchain asset transactions. Our clearing house operations will expose us to counterparties with differing risk profiles. We plan to guarantee transactions submitted by our clearing firms with counterparties in the financial industry, including brokers and dealers, commercial banks, investment banks, mutual and hedge funds, and other institutional customers.

We could be adversely impacted by the financial distress or failure of one or more of our clearing firms. We may be required to finance our clients’ unsettled positions and we could be held responsible for the defaults of our clients. Default by our clients may also give rise to our incurring penalties imposed by execution venues, regulatory authorities and clearing and settlement organizations.

Regulatory agencies have recently required clearing and settlement organizations to increase the level of margin deposit requirements and they may continue to do so in the future. Growth in trading activity may lead to higher regulatory capital requirements. We cannot assure you that these capital requirements will be sufficient to protect market participants from a default or that we will not be adversely affected in the event of a significant default.

Broker-dealers are also subject to regulatory capital requirements promulgated by the applicable regulatory and exchange authorities of the countries in which they operate. The failure to maintain required regulatory capital may lead to suspension or revocation of a broker-dealer registration and suspension or expulsion by a regulatory body. If existing cash together with cash from operations are not sufficient, we may need to reject orders from clients and we may ultimately breach regulatory capital requirements.

15

Furthermore, if our broker-dealer subsidiaries are subject to new or modified regulatory capital rules or requirements, or fines, penalties or sanctions due to increased or more stringent enforcement, it could materially limit or reduce the liquidity we may need to expand or even maintain our then-present levels of business, which could have a material adverse effect on our business, results of operations and financial condition.

Our commitment to maintain a cash reserve fund and other regulatory requirements may limit our profits and our ability to make distributions to Token holders.

Our plan is to establish a cash reserve fund to facilitate coverage of our clearing house and settlement operations. We intend that a portion of the proceeds raised by this offering will be used to fund the cash reserve fund. Additional payments into the cash reserve fund may impact profits of the Company and reduce the total amount that is returned to Token holders. Amounts reserved or released from the fund will be used to cover losses and cannot be used to develop the company and its business.

In addition, our ability to withdraw capital from the cash reserve fund may be subject to regulatory restrictions. We may become subject to capital requirements in the United States or other foreign jurisdictions in which we may enter. Such regulations may require us to accumulate capital reserves in our subsidiaries which could limit our ability to develop our business processes or to disburse funds to our INX Token holders. If we fail to maintain the required levels of capital, we may be required to suspend our broker-dealer operations during the period that we are not in compliance with capital requirements.

If our capital reserves, including the cash reserve fund, are insufficient to meet internal or regulatory requirements, or if they are insufficient to cover our future liabilities, we may be required to raise additional capital. Any one or all of these outcomes may have a material effect on our business.

We may experience systems failures or capacity constraints that could materially harm our ability to conduct our operations and execute our business strategy.

We will be heavily dependent on the capacity, reliability and security of the computer and communications systems and software supporting our operations. We plan to receive and/or process a large portion of our trade orders through electronic means, such as through public and private communications networks. Our systems, or those of our third party providers, may fail or be shut down or, due to capacity constraints, may operate slowly, causing one or more of the following to occur:

| ● | unanticipated disruptions in service to our customers; |

| ● | slower response times and delays in our customers’ trade execution and processing; |

| ● | failed settlement of trades; |

| ● | incomplete or inaccurate accounting, recording or processing of trades; |

| ● | financial losses; |

| ● | security breaches; |

| ● | litigation or other customer claims; |

| ● | loss of customers; and |

| ● | regulatory sanctions. |

If any of our systems do not operate properly, are compromised or are disabled, including as a result of system failure, employee or customer error or misuse of our systems, we could suffer financial loss, liability to customers, regulatory intervention or reputational damage that could affect demand by current and potential users of our market.