Exhibit 99.2

CHINA SXT PHARMACEUTICALS, INC.

CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE SIX MONTHS ENDED SEPTEMBER 30, 2022 AND 2021

(UNAUDITED)

CHINA SXT PHARMACEUTICALS, INC.

INDEX TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

F-1

CHINA SXT PHARMACEUTICALS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS

(IN U.S. DOLLARS, EXCEPT FOR NUMBER OF SHARES DATA)

| September 30, 2022 (Unaudited) |

March 31, 2022 |

|||||||

| ASSETS | ||||||||

| Current Assets | ||||||||

| Cash and cash equivalents | $ | $ | ||||||

| Restricted cash | ||||||||

| Accounts receivable, net | ||||||||

| Notes receivable | ||||||||

| Inventories | ||||||||

| Advance to suppliers | ||||||||

| Loan receivable and accrued interest | ||||||||

| Amounts due from related parties | ||||||||

| Prepayments, receivables and other current assets | ||||||||

| Total Current Assets | ||||||||

| Property, plant and equipment, net | ||||||||

| Construction in progress | ||||||||

| Intangible assets, net | ||||||||

| Long-term deposit | ||||||||

| Total Non-current Assets | ||||||||

| TOTAL ASSETS | $ | $ | ||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY | ||||||||

| Current Liabilities | ||||||||

| Bank loans – current portion | $ | $ | ||||||

| Short-term convertible note | ||||||||

| Accounts payable | ||||||||

| Refund liabilities | ||||||||

| Advance from customers | ||||||||

| Amounts due to related parties | ||||||||

| Accrued expenses and other liabilities | ||||||||

| Taxes payable | ||||||||

| Total Current Liabilities | ||||||||

| Total Non-current Liabilities | ||||||||

| TOTAL LIABILITIES | ||||||||

| SHAREHOLDERS’ EQUITY | ||||||||

| Additional paid-in capital | ||||||||

| Accumulated deficits | ( |

) | ( |

) | ||||

| Accumulated other comprehensive income | ( |

) | ||||||

| Total Shareholders’ Equity | ||||||||

| TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY | $ | $ | ||||||

| * | Retrospectively restated for effect of reverse stock split on February 22, 2021 and May 19, 2022. |

The accompanying notes are an integral part of these interim condensed consolidated financial statements.

F-2

CHINA SXT PHARMACEUTICALS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF INCOME/(LOSS) AND COMPREHENSIVE INCOME/(LOSS)

(IN U.S. DOLLARS, EXCEPT SHARES DATA)

(UNAUDITED)

| For the six months ended September 30, |

||||||||

| 2022 (Unaudited) |

2021 (Unaudited) |

|||||||

| Revenues | $ | $ | ||||||

| Revenues generated from third parties | ||||||||

| Revenue generated from related parties | ||||||||

| Cost of revenues | ( |

) | ( |

) | ||||

| Gross profit | ||||||||

| Operating expenses: | ||||||||

| Selling and marketing | ( |

) | ( |

) | ||||

| General and administrative | ( |

) | ( |

) | ||||

| Total operating expenses | ( |

) | ( |

) | ||||

| Operating Loss | ( |

) | ( |

) | ||||

| Other income (expenses): | ||||||||

| Interest income (expense), net | ( |

) | ||||||

| Other income, net | ||||||||

| Total other income (expenses), net | ( |

) | ||||||

| Income (Loss) before income taxes | ( |

) | ( |

) | ||||

| Income tax provision | - | ( |

) | |||||

| Net loss | ( |

) | ( |

) | ||||

| Other comprehensive income (loss): | ||||||||

| Foreign currency translation adjustment | ( |

) | ||||||

| Comprehensive loss | ( |

) | ( |

) | ||||

| Earnings per ordinary share | ||||||||

| $ | ( |

) | $ | ( |

) | |||

| Weighted average number of ordinary shares outstanding | ||||||||

| * |

The accompanying notes are an integral part of these interim condensed consolidated financial statements.

F-3

CHINA SXT PHARMACEUTICALS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY

FOR THE SIX MONTHS ENDED SEPTEMBER 30, 2021 and 2020

(IN U.S. DOLLARS, EXCEPT SHARES DATA)

(UNAUDITED)

| Shares* | Amount | Additional

| Retained | Accumulated | Total equity | |||||||||||||||||||

| Balance as of March 31, 2021 | $ | $ | $ | ( | ) | $ | $ | |||||||||||||||||

| Net loss | - | ( | ) | ( | ) | |||||||||||||||||||

| Shares issued as employee incentives | ||||||||||||||||||||||||

| Unearned employee compensation | - | ( | ) | ( | ) | |||||||||||||||||||

| Shares to be cancelled | ( | ) | ||||||||||||||||||||||

| Foreign currency translation gain | - | |||||||||||||||||||||||

| Balance as of September 30, 2021 (Unaudited) | $ | $ | $ | ( | ) | $ | $ | |||||||||||||||||

| Balance as of March 31, 2022 | $ | $ | $ | ( | ) | $ | $ | |||||||||||||||||

| Net loss | - | - | - | ( | ) | - | ( | ) | ||||||||||||||||

| Shares issued as employee incentives | - | - | ||||||||||||||||||||||

| Share issued due to reverse-split round up | - | - | - | - | - | |||||||||||||||||||

| Shares issued for convertible notes | ||||||||||||||||||||||||

| Foreign currency translation gain | - | ( | ) | ( | ) | |||||||||||||||||||

| Balance as of September 30, 2022 (Unaudited) | $ | $ | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||

| * |

| ** | 36,943 ordinary shares related to the employee incentives plan were cancelled on October 29, 2021. |

The accompanying notes are an integral part of these interim condensed consolidated financial statements.

F-4

CHINA SXT PHARMACEUTICALS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(IN U.S. DOLLARS)

(UNAUDITED)

| For the six months ended September 30, |

||||||||

| 2022 (Unaudited) |

2021 (Unaudited) |

|||||||

| Cash Flows from Operating Activities: | ||||||||

| Net loss from operations | $ | ( |

) | $ | ( |

) | ||

| Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||

| Convertible note - Accretion of financing cost | ||||||||

| Bad debt provision | ( |

) | ||||||

| Depreciation and amortization expenses | ||||||||

| Equity incentive plan | ||||||||

| Changes in operating assets and liabilities: | ||||||||

| Accounts receivable | ( |

) | ||||||

| Note receivable | ||||||||

| Inventory | ||||||||

| Advance to suppliers | ( |

) | ( |

) | ||||

| Prepayments, receivables and other assets | ( |

) | ||||||

| Deferred cost | ||||||||

| Accounts payable and accrual | ||||||||

| Advance from customers | ( |

) | ( |

) | ||||

| Taxes payable | ||||||||

| Accrued expenses and other current liabilities | ||||||||

| Net cash used in operating activities | ( |

) | ( |

) | ||||

| Cash Flows from Investing Activities: | ||||||||

| Purchase of property, plant and equipment | ( |

) | ( |

) | ||||

| Other receivable - Huangshan Panjie | - | |||||||

| Deposits for investment | ( |

) | ||||||

| Net cash provided by (used in) investing activities | ( |

) | ||||||

| Cash Flows from Financing Activities: | ||||||||

| Bank borrowings | ( |

) | ( |

) | ||||

| Payment to related parties | ( |

) | ( |

) | ||||

| Net cash provided by (used in) financing activities | ( |

) | ( |

) | ||||

| Effect of exchange rate changes on cash and cash equivalents and restricted cash | ( |

) | ||||||

| Net increase (decrease) in cash, cash equivalents and restricted cash | ( |

) | ( |

) | ||||

| Cash, cash equivalents and restricted cash at the beginning of period | ||||||||

| Cash, cash equivalents and restricted cash at the end of period | $ | $ | ||||||

| Supplemental disclosures of cash flows information: | ||||||||

| Cash paid for income taxes | $ | $ | ||||||

| Cash paid for interest expense | $ | $ | ||||||

| Non-cash transactions: | ||||||||

| Issuance of shares for equity incentive plan | $ | $ | ||||||

| Issuance of shares for convertible notes principal and interest settlement | $ | $ | ||||||

The accompanying notes are an integral part of these interim condensed consolidated financial statements.

F-5

CHINA SXT PHARMACEUTICALS, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

NOTE 1 – ORGANIZATION AND PRINCIPAL ACTITIVIES

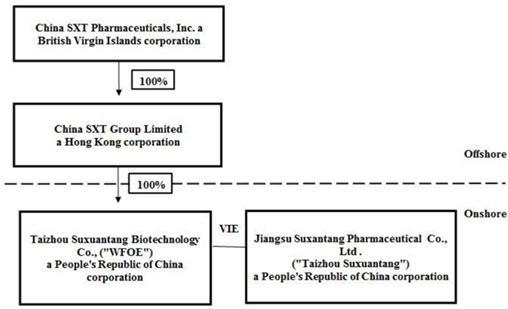

China SXT Pharmaceutical, Inc. (“SXT” or the “Company”) is a holding company incorporated in British Virgin Islands on July 4, 2017. The Company focuses on the research, development, manufacture, marketing and sales of traditional Chinese medicine pieces (the “TCMP”), through its variable interest entity (“VIE”), Jiangsu Suxuantang Pharmaceutical Co., Ltd, (“Taizhou Suxuantang”) in China. The Company currently sells three types of TCMP products: Advanced TCMP, Fine TCMP and Regular TCMP, and TCM Homologous Supplements (“TCMHS”) products. We currently have a product portfolio of 19 advanced TCMPs, 10 Fine TCMPs, 235 Regular TCMPs and 4 TCMHS solid beverage products that address a wide variety of diseases and medical indications. Most of our products are sold on a prescription basis across China. The Company’s principal executive offices are located in Taizhou, Jiangsu province, China.

Restructuring and Share Issuance

On July 4, 2017, we were incorporated in the British

Virgin Islands by issuance of

On July 21, 2017, our wholly owned subsidiary China SXT Group Limited (“SXT HK”) was incorporated in Hong Kong. China SXT Group Limited in turn holds all the capital stocks of Taizhou Suxantang Biotechnology Co. Ltd. (“WFOE”), a wholly foreign owned enterprise incorporated in China on October 13, 2017. On the same day, Taizhou Suxuantang and its shareholders entered into such a series of contractual arrangements, also known as VIE Agreements.

The discussion and presentation of financial statements herein assumes the completion of the Restructuring, which is accounted for retroactively as if the aforementioned transactions had become effective as of the beginning of the first period presented in the accompanying condensed consolidated financial statements.

F-6

NOTE 1 – ORGANIZATION AND PRINCIPAL ACTITIVIES (CONTINUED)

The following diagram illustrates our corporate structure, including our subsidiary and condensed consolidated variable interest entity as of the date of the financial statements assuming the completion of our Restructuring:

VIE Agreements with Taizhou Suxuantang

Due to PRC legal restrictions on foreign ownership in the pharmaceutical sector, neither the Company nor our subsidiaries own any equity interest in Taizhou Suxuantang. Instead, the Company controls and receives the economic benefits of Taizhou Suxuantang’s business operations through a series of contractual arrangements. WFOE, Taizhou Suxuantang and its shareholders entered into such a series of contractual arrangements, also known as VIE Agreements, on October 13, 2017. The VIE agreements are designed to provide WFOE with the power, rights and obligations equivalent in all material respects to those it would possess as the sole equity holder of Taizhou Suxuantang, including absolute control rights and the rights to the assets, property and revenue of Taizhou Suxuantang.

According to the Exclusive Business Cooperation Agreement between WFOE and Taizhou Suxuantang, which is one of the VIE Agreements that was also entered into on October 13, 2017, Taizhou Suxuantang is obligated to pay service fees to WFOE approximately equal to the net income of Taizhou Suxuantang.

Each of the VIE Agreements is described in detail below:

Exclusive Business Cooperation Agreement

Pursuant to the Exclusive Business Cooperation Agreement between Taizhou Suxuantang and WFOE, WFOE provides Taizhou Suxuantang with technical support, consulting services and other management services relating to its day-to-day business operations and management, on an exclusive basis, utilizing its advantages in technology, human resources, and information. Additionally, Taizhou Suxuantang granted an irrevocable and exclusive option to WFOE to purchase from Taizhou Suxuantang, any or all of Taizhou Suxuantang’s assets at the lowest purchase price permitted under the PRC laws. Should WFOE exercise such option, the parties shall enter into a separate asset transfer or similar agreement. For services rendered to Taizhou Suxuantang by WFOE under this agreement, WFOE is entitled to collect a service fee calculated based on the time of services rendered multiplied by the corresponding rate, plus the amount of the services fees or ratio decided by the board of directors of WFOE based on the value of services rendered by WFOE and the actual income of Taizhou Suxuantang from time to time, which is approximately equal to the net income of Taizhou Suxuantang.

F-7

NOTE 1 – ORGANIZATION AND PRINCIPAL ACTITIVIES (CONTINUED)

The Exclusive Business Cooperation Agreement shall remain in effect for ten years unless it is terminated by WFOE with 30-day prior notice. Taizhou Suxuantang does not have the right to terminate the agreement unilaterally. WFOE may unilaterally extend the term of this agreement with prior written notice.

The CEO and president of WFOE, Mr. Feng Zhou, is currently managing Taizhou Suxuantang pursuant to the terms of the Exclusive Business Cooperation Agreement. WFOE has absolute authority relating to the management of Taizhou Suxuantang, including but not limited to decisions with regard to expenses, salary raises and bonuses, hiring, firing and other operational functions. The Exclusive Business Cooperation Agreement does not prohibit related party transactions. The audit committee is required to review and approve in advance any related party transactions, including transactions involving WFOE or Taizhou Suxuantang.

Share Pledge Agreement

Under the Share Pledge Agreement among WFOE and

Feng Zhou, Ziqun Zhou, and Di Zhou, who together hold

The Share Pledge Agreement shall be effective until all payments due under the Exclusive Business Cooperation Agreement have been paid by Taizhou Suxuantang. WFOE shall cancel or terminate the Share Pledge Agreement upon with no additional expense.

The purposes of the Share Pledge Agreement are to (1) guarantee the performance of Taizhou Suxuantang’s obligations under the Exclusive Business Cooperation Agreement, (2) make sure the shareholders of Taizhou Suxuantang shall not transfer or assign the pledged equity interests, or create or allow any encumbrance that would prejudice WFOE’s interests without WFOE’s prior written consent and (3) provide WFOE control over Taizhou Suxuantang. Under the Exclusive Option Agreement (described below), WFOE may exercise its option to acquire the equity interests in Taizhou Suxuantang any time to the extent permitted by the PRC Law. In the event Taizhou Suxuantang breaches its contractual obligations under the Exclusive Business Cooperation Agreement, WFOE will be entitled to foreclose on the Taizhou Suxuantang Shareholders’ equity interests in Taizhou Suxuantang and may (1) exercise its option to purchase or designate third parties to purchase part or all of their equity interests in Taizhou Suxuantang and in this situation, WFOE may terminate the VIE agreements after acquisition of all equity interests in Taizhou Suxuantang or form a new VIE structure with the third parties designated by WFOE; or (2) dispose the pledged equity interests and be paid in priority out of the proceeds from the disposal in which case the VIE structure will be terminated.

F-8

NOTE 1 – ORGANIZATION AND PRINCIPAL ACTITIVIES (CONTINUED)

Exclusive Option Agreement

Under the Exclusive Option Agreement, the Taizhou

Suxuantang Shareholders irrevocably granted WFOE (or its designee) an exclusive option to purchase, to the extent permitted under PRC

law, once or at multiple times, at any time, part or all of their equity interests in Taizhou Suxuantang at the exercise price of RMB

Under the Exclusive Option Agreement, WFOE may at any time under any circumstances, purchase, or have its designated person to purchase, at its discretion, to the extent permitted under PRC law, all or part of the shareholders’ equity interests in Taizhou Suxuantang.

This Agreement shall remain effective until all equity interests held by Taizhou Suxuantang Shareholders in Taizhou Suxuantang have been transferred or assigned to WFOE and/or any other person designated by WFOE in accordance with this Agreement.

Power of Attorney

Under the Power of Attorney, the Taizhou Suxuantang Shareholders authorize WFOE to act on their behalf as their exclusive agent and attorney with respect to all rights as shareholders, including but not limited to: (a) attending shareholders’ meetings; (b) exercising all the shareholder’s rights, including voting, that shareholders are entitled to under the laws of China and the Articles of Association, including but not limited to the sale or transfer or pledge or disposition of shares in part or in whole; and (c) designating and appointing on behalf of shareholders the legal representative, the executive director, supervisor, the chief executive officer and other senior management members of Taizhou Suxuantang.

Although it is not explicitly stipulated in the Power of Attorney, the term of the Power of Attorney shall be the same as the term of that of the Exclusive Option Agreement.

This Power of Attorney is coupled with an interest and shall be irrevocable and continuously valid for each shareholder from the date it is executed until the date he/she no longer is a shareholder of Taizhou Suxuantang.

The Exclusive Option Agreement, together with the Share Pledge Agreement and the Power of Attorney enable WFOE to exercise effective control over Taizhou Suxuantang.

Basis of presentation and principles of consolidation

The accompany unaudited condensed consolidated financial statements of the Company has been prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”). The accompanying condensed consolidated financial statements include our accounts and those of our wholly owned subsidiaries and VIE. Accordingly, all intercompany balances and transactions have been eliminated through the consolidation process.

In the opinion of management, these unaudited condensed consolidated interim financial statements reflect all adjustments, consisting of normal recurring adjustments, which are necessary to present fairly, in all material respects, the Company’s condensed consolidated financial position, results of operations, cash flows and changes in equity for the interim periods presented. These unaudited condensed financial statements do not include certain information and footnote disclosures as required by the U.S. GAAP for complete annual financial statements. Therefore, these unaudited condensed consolidated interim financial statements should be read in conjunction with the financial statements and related notes included in the Company’s first initial offering Registration Statement on Form 20-F for the year ended March 31, 2022 and 2021.

The VIE, Taizhou Suxuantang is owned by three shareholders, each of which act as the Company’s nominee shareholder. For the consolidated VIEs, the Company’s management made evaluations of the relationships between the Company and the VIE and the economic benefit flow of contractual arrangements with Taizhou Suxuantang. In connection with such evaluation, management also took into account the fact that, as a result of such contractual arrangements, the Company control the shareholders’ voting interests in these VIEs. As a result of such evaluation, management concluded that the Company is the primary beneficiary of the consolidated VIEs, Taizhou Suxuantang. The Company does not have any VIEs that are not consolidated in the financial statements.

F-9

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES

Risks in relation to the VIE structure

It is possible that the Company’s operation of certain of its operations and businesses through its VIE could be found by PRC authorities to be in violation of PRC law and regulations prohibiting or restricting foreign ownership of companies that engage in such operations and businesses. While the Company’s management considers the possibility of such a finding by PRC regulatory authorities under current law and regulations to be remote. On January 19, 2015, the Ministry of Commerce of the PRC, or (the “MOFCOM”) released on its Website for public comment a proposed PRC law (the “Draft FIE Law”) that appears to include VIE within the scope of entities that could be considered to be foreign invested enterprises (or “FIEs”) that would be subject to restrictions under existing PRC law on foreign investment in certain categories of industry. Specifically, the Draft FIE Law introduces the concept of “actual control” for determining whether an entity is considered to be an FIE. In addition to control through direct or indirect ownership or equity, the Draft FIE Law includes control through contractual arrangements within the definition of “actual control.” If the Draft FIE Law was passed by the People’s Congress of the PRC and went into effect in its current form and as a result the Company’s VIE could become explicitly subject to the current restrictions on foreign investment in certain categories of industry. The Draft FIE Law includes provisions that would exempt from the definition of foreign invested enterprises entities where the ultimate controlling shareholders are either entities organized under PRC law or individuals who are PRC citizens. The Draft FIE Law is silent as to what type of enforcement action might be taken against existing VIEs that operate in restricted or prohibited industries and are not controlled by entities organized under PRC law or individuals who are PRC citizens. If a finding were made by PRC authorities, under existing law and regulations or under the Draft FIE Law if it becomes effective, about the Company’s operation of certain of its operations and businesses through its VIEs, regulatory authorities with jurisdiction over the licensing and operation of such operations and businesses would have broad discretion in dealing with such a violation, including levying fines, confiscating the Company’s income, revoking the business or operating licenses of the affected businesses, requiring the Company to restructure its ownership structure or operations, or requiring the Company to discontinue all or any portion of its operations. Any of these actions could cause significant disruption to the Company’s business operations and have a severe adverse impact on the Company’s cash flows, financial position and operating performance.

In addition, it is possible that the contracts among Taizhou Suxuantang, WFOE, and the nominee shareholders of Taizhou Suxuantang would not be enforceable in China if PRC government authorities or courts were to find that such contracts contravene PRC laws and regulations or are otherwise not enforceable for public policy reasons. In the event that the Company was unable to enforce these contractual arrangements, the Company would not be able to exert effective control over the VIEs. Consequently, the VIEs’ results of operations, assets and liabilities would not be included in the Company’s condensed consolidated financial statements. If such were the case, the Company’s cash flows, financial position, and operating performance would be materially adversely affected. The Company’s contractual arrangements Taizhou Suxuantang, WFOE, and the nominee shareholders of Taizhou Suxuantang are approved and in place. Management believes that such contracts are enforceable and considers the possibility remote that PRC regulatory authorities with jurisdiction over the Company’s operations and contractual relationships would find the contracts to be unenforceable.

The Company’s operations and businesses rely on the operations and businesses of its VIEs, which hold certain recognized revenue-producing assets. The VIEs also have an assembled workforce, focused primarily on research and development, whose costs are expensed as incurred. The Company’s operations and businesses may be adversely impacted if the Company loses the ability to use and enjoy assets held by its VIE.

F-10

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Foreign currency translation

Transactions denominated in currencies other than the functional currency are translated into the functional currency at the exchange rates prevailing at the dates of the transaction. Monetary assets and liabilities denominated in currencies other than the functional currency are translated into the functional currency using the applicable exchange rates at the balance sheet dates. The resulting exchange differences are recorded in the statement of operations.

The reporting and functional currencies of the Company and SXT HK are the United States Dollars (“US$”) and the accompanying financial statements have been expressed in US$. In addition, the WFOE and the VIE maintain their books and records in their respective local currency, Renminbi (“RMB”), which is also the respective functional currency for each subsidiary and VIE as they are the primary currency of the economic environment in which each subsidiary operates.

In general, for consolidation purposes, assets, and liabilities of its subsidiaries whose functional currency is not the US$ are translated into US$, in accordance with ASC Topic 830-30, “Translation of Financial Statement”, using the exchange rate on the balance sheet date. Revenues and expenses are translated at average rates prevailing during the period. The gains and losses resulting from translation of financial statements of a foreign subsidiary are recorded as a separate component of accumulated other comprehensive income within the statement of stockholders’ equity. Other equity items are translated using the exchange rates on the transaction date.

Translation of amounts from the local currencies of the Company into US$ has been made at the following exchange rates for the respective periods:

September 30, | March

31, | September 30, | ||||||||||

| Balance sheet items, except for equity accounts | ||||||||||||

| Items in the statements of income(loss) and comprehensive income(loss), and statements of cash flows | ||||||||||||

Use of estimates

The preparation of condensed consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates. On an ongoing basis, management reviews these estimates and assumptions using the currently available information.

Changes in facts and circumstances may cause the Company to revise its estimates. The Company bases its estimates on historical experience and on various other assumptions that are believed to be reasonable, the results of which form the basis for making judgments about the carrying values of assets and liabilities. The following are some of the areas requiring significant judgments and estimates as of September 30, 2022 and March 31, 2022: determinations of the useful lives of long-lived assets, estimates of allowances for doubtful accounts, sales return rate, valuation assumptions in performing asset impairment tests of long-lived assets and determinations of fair value of convertible notes (liability component, etc.) and warrants.

F-11

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Fair values of financial instruments

ASC Topic 825, Financial Instruments (“Topic 825”) requires disclosure of fair value information of financial instruments, whether recognized in the balance sheets, for which it is practicable to estimate that value. In cases where quoted market prices are not available, fair values are based on estimates using present value or other valuation techniques. Those techniques are significantly affected by the assumptions used, including the discount rate and estimates of future cash flows. In that regard, the derived fair value estimates cannot be substantiated by comparison to independent markets and, in many cases, could not be realized in immediate settlement of the instruments. Topic 825 excludes certain financial instruments and all nonfinancial assets and liabilities from its disclosure requirements. Accordingly, the aggregate fair value amounts do not represent the underlying value of the Company.

| ● | Level 1 - inputs to the valuation methodology are quoted prices (unadjusted) for identical assets or liabilities in active markets. |

| ● | Level 2 - inputs to the valuation methodology include quoted prices for similar assets and liabilities inactive markets, and inputs that are observable for the assets or liability, either directly or indirectly, for substantially the full term of the financial instruments. |

| ● | Level 3 - inputs to the valuation methodology are unobservable and significant to the fair value. |

As of September 30, 2022 and March 31, 2022, financial instruments of the Company primarily comprised of cash and cash equivalents, restricted cash, accounts receivables, loan receivable and accrued interest, due from related parties, prepayments, receivables and other current assets (exclude prepayments and deposits), bank loans (current and non-current portion), accounts payable, amounts due to related parties and accrued expenses and other liabilities. The carrying amounts of these financial instruments approximated their fair values because of their generally short maturities.

Cash and cash equivalents

The Company considers all highly liquid investment instruments with an original maturity of three months or less from the date of purchase to be cash equivalents. The Company maintains most of the bank accounts in the PRC. Cash balances in bank accounts in PRC are not insured by the Federal Deposit Insurance Corporation or other programs.

Restricted cash

Restricted cash is cash held as collateral for transactions and a loan the Company has entered.

In November 2016, the FASB issued Accounting Standards Update No. 2016-18, Statement of Cash Flows (Topic 230): Restricted Cash, which requires companies to include amounts generally described as restricted cash and restricted cash equivalents in cash and cash equivalents when reconciling beginning-of-period and end-of-period total amounts presented in the statement of cash flows. The Company adopted the new standard effective April 1, 2018, using the retrospective transition method.

The ending balance of restricted cash presented on the face of the

condensed consolidated balance sheets as of September 30, 2022 and March 31, 2022 were and $

Accounts receivable

Accounts receivable are recorded at the invoiced

amount less an allowance for any uncollectible accounts and do not bear interest, which are due on demand. Management reviews the adequacy

of the allowance for doubtful accounts on an ongoing basis, using historical collection trends and aging of receivables. Management also

periodically evaluates individual customer’s financial condition, credit history, and the current economic conditions to adjust

in the allowance when it is considered necessary. Account balances are charged off against the allowance after all means of collection

have been exhausted and the potential for recovery is considered remote. As of September 30, 2022 and March 31, 2022, the Company assessed

the recoverability of its accounts receivable and record an allowance of $

Inventories

Inventories primarily include raw materials and finished goods.

Inventories are stated at the lower of cost or

net realizable value. Cost is determined by the weighted-average method. Raw material cost is based on purchase costs while work-in-progress

and finished goods comprise direct materials, direct labor and an allocation of manufacturing overhead costs. Net realizable value represents

the anticipated selling price, net of distribution cost, less estimated costs to completion for inventories. As of September 30, 2022

and March 31, 2022, the Company assessed the net realizable value of its inventories and record a provision of $

F-12

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Advance to suppliers

Advance to suppliers represent amounts advanced to suppliers for future purchases of raw materials and for other services. The suppliers usually require advance payments when the Company makes purchase or orders service, and the advanced payments will be utilized to offset the Company’s future payments.

Property, plant and equipment, net

Property and equipment are stated at cost. The straight-line depreciation method is used to compute depreciation over the estimated useful lives of the assets, as follows:

Residual | Useful Lives | |||||

| Machinery | % | |||||

| Electric equipment | % | |||||

| Office equipment | % | |||||

| Vehicles | % | |||||

| Leasehold improvement cost | % | |||||

The Company reviews property, plant and equipment for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. An asset is considered impaired if its carrying amount exceeds the future net undiscounted cash flows that the asset is expected to generate. If such asset is considered to be impaired, the impairment recognized is the amount by which the carrying amount of the asset, if any, exceeds its fair value determined using a discounted cash flow model. For the six months ended September 30, 2022 and 2021, there was no impairment of property, plant and equipment.

Costs of repairs and maintenance are expensed as incurred and asset improvements are capitalized. The cost and related accumulated depreciation and amortization of assets disposed of or retired are removed from the accounts, and any resulting gain or loss is reflected in the condensed consolidated income statements.

Intangible assets, net

Intangible assets are stated at cost less accumulated amortization. Intangible assets represented the trademark registered in the PRC and purchased software which are amortized on a straight-line basis over a useful life of 10 years.

The Company follows ASC Topic 350 in accounting for intangible assets, which requires impairment losses to be recorded when indicators of impairment are present and the undiscounted cash flows estimated to be generated by the assets are less than the assets’ carrying amounts. For the six months ended September 30, 2022 and 2021, the Company record no impairment of intangible assets.

F-13

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Construction in process

Construction in process records the cost of construction work, which is not yet completed. A construction in process item is not depreciated until the asset is placed in service.

Construction in process respects unfinished factory, workshop, and retail outlet. Construction in process will be transferred to leasehold improvement when it is finished. Depreciation is recorded starting at the time when assets are ready for the intended use.

Impairment of long-lived assets

Long-lived assets primarily include property, plant and equipment and intangible assets. In accordance with the provision of ASC Topic 360-10-5, “Impairment or Disposal of Long-Lived Assets”, the Company generally conducts its annual impairment evaluation to its long-lived assets, usually in the fourth quarter of each year, or more frequently if indicators of impairment exist, such as a significant sustained change in the business climate. The recoverability of long-lived assets is measured at the reporting unit level, which is an operating segment or one level below an operating segment. If the total of the expected undiscounted future net cash flows is less than the carrying amount of the asset, a loss is recognized for the difference between the fair value and carrying amount of the asset. The Company record no impairment charge for the six months ended September 30, 2022 and 2021, respectively.

Convertible note, net

ASC 470, Debt, requires the liability and equity components of convertible debt instruments that may be settled in cash upon conversion to be separately accounted for in a manner that reflects the issuer’s nonconvertible debt borrowing rate. ASC 470-20 requires that the initial proceeds from the sale of these notes be allocated between a liability component and an equity component in a manner that reflects interest expense at the interest rate of similar nonconvertible debt that could have been issued by the Company at such time. We measured the estimated fair value of the debt component of our convertible notes as of the issuance date based on our nonconvertible debt borrowing rate. The equity components of the convertible senior notes have been reflected within additional paid-in capital in our audited consolidated balance sheet, and the resulting debt discount is amortized over the period during which the convertible notes are expected to be outstanding (through the maturity date) as additional non-cash interest expense.

Upon repurchase of convertible debt instruments, ASC 470-20 requires the issuer to allocate total settlement consideration, inclusive of transaction costs, amongst the liability and equity components of the instrument based on the fair value of the liability component immediately prior to repurchase. The difference between the settlement consideration allocated to the liability component and the net carrying value of the liability component, including unamortized debt issuance costs, would be recognized as gain (loss) on extinguishment of debt in our audited consolidated statements of operations. The remaining settlement consideration allocated to the equity component would be recognized as a reduction of additional paid-in capital in our audited consolidated balance sheets

Revenue recognition

The Company adopted ASC Topic 606 Revenue from Contracts with Customers (“ASC 606”), on April 1, 2018, using the modified retrospective method.

Revenue is recognized when control of promised

goods is transferred to the Company’s customers in an amount of consideration of which the Company expect to be entitled to in exchange

for the goods, and the Company can reasonably estimates return provision for the goods. The product return provisions are estimated based

on (1) historical rates, (2) specific identification of outstanding returns not yet received from customers and outstanding discounts

and claims and (3) estimated returns, discounts and claims expected, but not yet finalized with customers. As of September 30, 2022 and

March 31, 2022, sales return provision recorded in refund liabilities were $

For the six months ended September 30, 2022 and 2021, the Company did not have any significant incremental costs of obtaining contracts with customers incurred or costs incurred in fulfilling contracts with customers within the scope of ASC Topic 606, that shall be recognized as an asset and amortized to expenses in a pattern that matches the timing of the revenue recognition of the related contract.

The Company does not have amounts of contract

assets since revenue is recognized as control of goods is transferred. The contract liabilities consist of advance payments from customers.

The contract liabilities are reported in a net position on a customer-by-customer basis at the end of each reporting period. All contract

liabilities are included in advance from customers in the condensed consolidated balance sheets. As of September 30, 2022 and March 31,

2022, the Company record advance from customers of $

Cost of revenue

Cost of revenue consists primarily of cost of materials, direct labors, overhead, and other related incidental expenses that are directly attributable to the Company’s principal operations.

F-14

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Market development fees

Market development fees relate mainly to market development and advertisements

of our pharmaceutical products. For the six months ended September 30, 2022 and 2021, marketing and advertising expenses are $

Income Taxes

Current income tax expenses are provided for in accordance with the laws of the relevant taxing authorities. As part of the process of preparing the condensed consolidated financial statements, the Company is required to estimate its income taxes in each of the jurisdictions in which it operates. The Company accounts for income taxes using the liability method, under which deferred income taxes are recognized for future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax bases. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. The effect on deferred taxes of a change in tax rates is recognized as income or expense in the period that includes the enactment date. Valuation allowance is provided on deferred tax assets to the extent that it is more likely than not that the asset will not be realizable in the foreseeable future.

The Company adopts ASC 740-10-25 “Income Taxes” which prescribes a more likely than not threshold for financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return. It also provides guidance on derecognition of income tax assets and liabilities, classification of current and deferred income tax assets and liabilities, accounting for interest and penalties associated with tax positions, accounting for income taxes in interim periods and income tax disclosures. The Company did not have significant unrecognized uncertain tax positions or any unrecognized liabilities, interest or penalties associated with unrecognized tax benefit as of September 30, 2022 and March 31, 2022.

Comprehensive income (loss)

Comprehensive income includes net income and foreign

currency adjustments. Comprehensive income is reported in the condensed consolidated statements of operations and comprehensive income.

Accumulated other comprehensive income, as presented on the balance sheets are the cumulative foreign currency translation adjustments.

As of September 30, 2022 and March 31, 2021, the balance of accumulated other comprehensive income amounted to $(

Leases

Leases are classified as either capital or operating leases. Leases that transfer substantially all the benefits and risks incidental to the ownership of assets are accounted for as if there was an acquisition of an asset and incurrence of an obligation at the inception of the lease. All other leases are accounted for as operating leases wherein rental payments are recognized in the condensed consolidated income statements on a straight-line basis over the lease terms. The Company had no capital leases for the six months ended September 30, 2022 and 2021, respectively.

Segment reporting

Operating segments are reported in a manner consistent with the internal reporting provided to the chief operating decision-maker, which is a strategic committee comprised of members of the Company’s management team. In the respective periods presented, the Company had one single operating and reportable segment, namely the manufacture and distribution of TCMP. Although TCMP consist of different business units of the Company, information provided to the chief operating decision-maker is at the revenue level and the Company does not allocate operating costs or assets across business units, as the chief operating decision-maker does not use such information to allocate resources or evaluate the performance of the business units. As the Company’s long-lived assets are substantially all located in the PRC and substantially all of the Company’s revenue is derived from within the PRC, no geographical information is presented.

F-15

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Significant risks and uncertainties

Credit risk

Assets that potentially subject the Company to

significant concentration of credit risk primarily consist of cash and cash equivalents, restricted cash, accounts receivable, other receivables,

advances to suppliers, loan receivable and accrued interest, and amounts due from related parties. The maximum exposure of such assets

to credit risk is their carrying amount as at the balance sheet dates. As of September 30, 2022 and March 31, 2022 the Company held cash

and cash equivalents of $

The Company conducts credit evaluations of its customers and suppliers

and generally does not require collateral or other security from them. The Company establishes an accounting policy for allowance for

doubtful accounts on the individual customer’s financial condition, credit history, and the current economic conditions. As of September

30, 2022 and March 31, 2022, the Company record allowances of $

Liquidity risk

The Company is also exposed to liquidity risk which is risk that it is unable to provide sufficient capital resources and liquidity to meet its commitments and business needs. Liabilities that potentially subject the Company to significant concentration of liquidity risk primarily consist of bank loans (current and non-current portion), accounts payable, amounts due to related parties, and accrued expenses and other liabilities. Liquidity risk is controlled by the application of financial position analysis and monitoring procedures. When necessary, the Company will turn to other financial institutions and the owners to obtain short-term funding to meet the liquidity shortage.

Foreign currency risk

The Company has significant operating activities in China, thus has assets and liabilities are denominated in RMB, which is not freely convertible into foreign currencies. All foreign exchange transactions take place either through the Peoples’ Bank of China (“PBOC”) or other authorized financial institutions at exchange rates quoted by PBOC. Approval of foreign currency payments by the PBOC or other regulatory institutions requires submitting a payment application form together with suppliers ‘invoices and signed contracts”. The value of RMB is subject to changes in central government policies and to international economic and political developments affecting supply and demand in the China Foreign Exchange Trading System market. Where there is a significant change in value of RMB, the gains and losses resulting from translation of financial statements of a foreign subsidiary will be significantly affected.

F-16

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Significant risks and uncertainties (continued)

Concentration risk

Significant customers and suppliers are those that account for greater than 10% of the Company’s revenues and purchases, respectively. The loss of any of the Company’s significant supplier or the failure to purchase key raw material could have a material adverse effect on our business, consolidated results of operations and financial condition

During the six months ended September 30, 2022,

there are two customers generated sales which accounted for over

For

the six months ended | ||||||||

2022 | 2021 | |||||||

| Customer A | % | % | ||||||

| Customer B | % | % | ||||||

| Customer C (related party customer) | % | % | ||||||

As of September 30, 2022 and March 31, 2022, the Company

had accounts receivable balances from

| As of | ||||||||

September 30, | March

31, | |||||||

| Customer D (related party customer) | | % | % | |||||

During the six months ended September 30, 2022 and 2021, there were one and three suppliers which accounted for over 10% of total purchase for that period, respectively. The details are as follows:

| For the six months ended September 30, | ||||||||

2022 (Unaudited) | 2021 (Unaudited) | |||||||

| Supplier A | % | - | % | |||||

| Supplier B | % | % | ||||||

| Supplier C | % | % | ||||||

| Supplier D | % | % | ||||||

As of September 30, 2022 and March 31, 2022, the Company

had accounts payable balances from three and three suppliers which accounted for over

| As of | ||||||||

| September 30, 2022 (Unaudited) | March 31, 2022 | |||||||

| Supplier A | % | - | % | |||||

| Supplier B | % | % | ||||||

| Supplier D | % | % | ||||||

| Supplier E | % | % | ||||||

Recently issued accounting standards

The Jumpstart Our Business Startups Act (“JOBS Act”) provides that an emerging growth company (“EGC”) as defined therein can take advantage of an extended transition period for complying with new or revised accounting standards. This allows an EGC to delay adoption of certain accounting standards until those standards would otherwise apply to private companies. The Company has adopted the extended transition period.

F-17

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES (CONTINUED)

Recently issued accounting standards (continued)

In February 2016, the FASB issued ASU No. 2016-02, Leases, or ASU 2016-02, which modifies lease accounting for lessees to increase transparency and comparability by recording lease assets and liabilities for operating leases and disclosing key information about leasing arrangements. In July 2018, the FASB issued ASU No. 2018-10, Codification Improvements to Topic 842, Leases, or ASU 2018-10, to supersede ASU 2016-02. In addition, the FASB issued ASU No. 2018-11, Leases (Topic 842): Targeted Improvements, that provide entities with an additional (and optional) transition method to adopt the new leases standard. Under this new transition method, an entity initially applies the new leases standard at the adoption date and recognizes a cumulative-effect adjustment to the opening balance of retained earnings in the period of adoption. Consequently, an entity’s reporting for the comparative periods presented in the financial statements in which it adopts the new leases standard will continue to be in accordance with current GAAP (Topic ASC 840, Leases). In June 2020, the FASB issued ASU No. 2020-05, Revenue from Contracts with Customers (Topic 606) and Leases (Topic 842): Effective Dates for Certain Entities, which amended the effective date of Topic 842, Leases. ASC 842 is now effective for private companies and nonprofit organizations annual reporting periods beginning after December 15, 2021. This was done to provide these organizations with accounting relief during the COVID-19 global pandemic. The amendments in these ASUs are effective for the Company’s fiscal years and interim periods within those fiscal years beginning December 15, 2022. Early adoption is permitted. The Company is evaluating the effects, if any, of the adoption of this guidance on the financial position, results of operations and cash flows.

In June 2016, the FASB issued ASU No. 2016-13, Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments, or ASU 2016-13. This ASU is intended to improve financial reporting by requiring timelier recording of credit losses on loans and other financial instruments held by financial institutions and other organizations. This ASU requires the measurement of all expected credit losses for financial assets held at the reporting date based on historical experience, current conditions, and reasonable and supportable forecasts. This ASU requires enhanced disclosures to help investors and other financial statement users better understand significant estimates and judgments used in estimating credit losses, as well as the credit quality and underwriting standards of the Company’s portfolio. These disclosures include qualitative and quantitative requirements that provide additional information about the amounts recorded in the financial statements. In November 2018, the FASB issued ASU No. 2018-19, Codification Improvements to Topic 326, Financial Instruments—Credit Losses, which clarifies that receivables arising from operating leases should be accounted for in accordance with ASC 842, Leases (“ASC 842”) instead of ASC Subtopic 326-20. In November 2019, the FASB issued ASU No. 2019-10, Financial Instruments—Credit Losses (Topic 326), Derivatives and Hedging (Topic 815), and Leases (Topic 842): Effective Dates, which amended the effective date of ASU 2016-13. The amendments in these ASUs are effective for the Company’s fiscal years and interim periods within those fiscal years beginning December 15, 2022. Early adoption is permitted. The Company is evaluating the effects, if any, of the adoption of this guidance on the financial position, results of operations and cash flows.

In December 2019, the FASB issued ASU 2019-12, Simplifying the Accounting for Income Taxes, as part of its Simplification Initiative to reduce the cost and complexity in accounting for income taxes. This standard removes certain exceptions related to the approach for intra period tax allocation, the methodology for calculating income taxes in an interim period and the recognition of deferred tax liabilities for outside basis differences. It also amends other aspects of the guidance to help simplify and promote consistent application of GAAP. The amendments in these ASUs are effective for the Company’s fiscal years, and interim periods within those fiscal years beginning April 1, 2022. The Company adopted this guidance on April 1, 2022 and the adoption of this guidance had immaterial impact on the Company’s consolidated financial statements.

In March 2020, the FASB issued ASU 2020-04, “Reference Rate Reform (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting” and issued a subsequent amendment which refines the scope of the ASU and clarifies some of its guidance as part of the FASB’s monitoring of global reference rate reform activities in January 2021 within ASU 2021-01 (collectively, including ASU 2020-04, “ASC 848”). ASC 848 provides optional expedients and exceptions for applying U.S. GAAP on contract modifications and hedge accounting to contracts, hedging relationships, and other transactions that reference LIBOR or another reference rate expected to be discontinued because of reference rate reform, if certain criteria are met. These optional expedients and exceptions provided in ASC 848 are effective for the Company from January 1, 2020 through December 31, 2022. The Company has elected the optional expedients for certain existing interest rate swaps that are designated as cash flow hedges, which did not have a material impact on the financial position, results of operations and cash flows. The Company is evaluating the effects, if any, of the potential election of the other optional expedients and exceptions provided in this guidance on the financial position, results of operations and cash flows.

In August 2020, the FASB issued ASU 2020-06, “Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging — Contracts in Entity’s Own Equity (Subtopic 815-40): Accounting for Convertible Instruments and Contracts in an Entity’s Own Equity”, which simplifies an issuer’s accounting for certain convertible instruments and the application of derivatives scope exception for contracts in an entity’s own equity. This guidance also addresses how convertible instruments are accounted for in the diluted earnings per share calculation and required enhanced disclosures about the terms of convertible instruments and contracts in an entity’s own equity. The new guidance is required to be applied either retrospectively to financial instruments outstanding as of the beginning of the first comparable reporting period for each prior reporting period presented or retrospectively with the cumulative effect of the change to be recognized as an adjustment to the opening balance of retained earnings at the date of adoption. This guidance is effective for the Company for the year ending March 31, 2023 and interim reporting periods during the year ending March 31, 2023. Early adoption is permitted. The Company is evaluating the effects, if any, of the adoption of this guidance on the financial position, results of operations and cash flows.

The Company does not believe other recently issued but not yet effective accounting statements, if recently adopted, would have a material effect on the Company’s condensed consolidated balance sheets, statements of comprehensive income (loss) and statements of cash flows.

F-18

NOTE 3 – ACCOUNTS RECEIVABLE

Accounts receivable consisted of the following as of September 30, 2022 and March 31, 2022:

| September 30, 2022 (Unaudited) | March 31, 2022 | |||||||

| Accounts receivable – third parties | $ | $ | ||||||

| Accounts receivable – related parties | ||||||||

| Total accounts receivable, gross | ||||||||

| Less: allowance for doubtful accounts | ( | ) | ( | ) | ||||

| Accounts receivable, net | $ | $ | ||||||

NOTE 4 – INVENTORIES

Inventories as of September 30, 2022 and March 31, 2022 consisted of the following:

September 30, | March

31, | |||||||

| Raw materials | $ | $ | ||||||

| Finished goods | ||||||||

| Provision for inventory | ( | ) | ( | ) | ||||

| Total inventories, net | $ | $ | ||||||

NOTE 5 – LOAN RECEIVABLE AND ACCRUED INTEREST

September 30, | March

31, | |||||||

| Loan receivable - RH Holdings Management (HK) Limited | $ | $ | ||||||

| Accrued interest | ||||||||

| Total | $ | $ | ||||||

Short-term loan of $

F-19

NOTE 6 – PREPAYMENTS, RECEIVABLES AND OTHER ASSETS

Prepayments, receivables and other assets consisted of the following as of September 30, 2022 and March 31, 2022:

| September 30, 2022 (Unaudited) | March 31, 2022 | |||||||

| Receivable from a third-party company | $ | $ | ||||||

| Others | ||||||||

| Total prepayments, receivables and other assets | ||||||||

| Less: allowance for doubtful accounts | ||||||||

| Prepayments, receivables and other assets, net | $ | $ | ||||||

In June 2019, Taizhou Suxuantang entered into

a limited partnership agreement with Huangshan Panjie Investment Management Co., Ltd. (the “Fund” or “Huangshan Panjie”).

The company is committed to contribute $

NOTE 7 – PROPERTY, PLANT AND EQUIPMENT

Property, plant and equipment consisted of the following as of September 30, 2022 and March 31, 2022:

September 30,

| March

31, | |||||||

| Machinery | $ | $ | ||||||

| Vehicles | ||||||||

| Office equipment | ||||||||

| Electric equipment | ||||||||

| Leasehold improvement | ||||||||

| Total property plant and equipment, at cost | ||||||||

| Less: accumulated depreciation | ( | ) | ( | ) | ||||

| Total property, plant and equipment, net | $ | $ | ||||||

Depreciation expenses were $

NOTE 8 – INTANGIBLE ASSETS, NET

Intangible assets consisted of the following as of September 30, 2022 and March 31, 2022:

| September 30, 2022 (Unaudited) | March 31, 2022 | |||||||

| Trademark | $ | $ | ||||||

| Software | ||||||||

| Total intangible assets, at cost | ||||||||

| Less: accumulated amortization | ( | ) | ( | ) | ||||

| Total intangible assets, net | $ | $ | ||||||

Amortization expense were $

F-20

NOTE 9 – CONSTRUCTION IN PROCESS

Construction in process consist of the following as of September 30, 2022 and March 31, 2022:

September 30, | March 31, | |||||||

| Factory | $ | $ | ||||||

| Retail outlet | ||||||||

| $ | $ | |||||||

NOTE 10 – LONG-TERM DEPOSIT

Long-term deposit consisted of cash deposit of

RMB

NOTE 11 – BANK LOANS

Bank loans consisted of the following as of September 30, 2022 and March 31, 2022:

September 30,

| March

31, | |||||||

| Car loans – current portion | $ | - | $ | |||||

Two car loans of $

NOTE 12 – CONVERTIBLE NOTES

On March 16, 2022, the Company entered into a

Securities Purchase Agreement (the “Purchase Agreement”) with an institutional investor (“Investor”) pursuant

to which the Company issued an unsecured convertible promissory note with a 12-months maturity (the “2022 Convertible Note”)

to Investor. The 2022 Convertible Note has the original principal amount of $

F-21

NOTE 12 – CONVERTIBLE NOTES (CONTINUED)

Material Terms of the Convertible Note:

| ● | Interest accrues on the outstanding balance of the Note at 6% per annum from the Purchase Price Date until the same is paid in full. All interest calculations hereunder shall be computed on the basis of a 360-day year comprised of twelve (12) thirty (30) day months, shall compound daily and shall be payable in accordance with the terms of this Note. |

| ● | Upon the occurrence of a Trigger Event, Investor may increase the outstanding balance payable under the Note by 12% or 5%, depending on the nature of such event. If the Company fails to cure the Trigger Event within the required five trading days, the Triger Event will automatically become an event of default and interest will accrue at the lesser of 22% per annum or the maximum rate permitted by applicable law. |

| ● | Subject to adjustment as set forth in this Note, the price at which Lender has the right to convert all or any portion of the Outstanding Balance into Ordinary Shares is $0.30 per share (the “Lender Conversion Price”). |

| ● | Lender has the right at any time after the date that is six (6) months from the Purchase Price Date until the Outstanding Balance has been paid in full, at its election, to convert (“Conversion”) all or any portion of the Outstanding Balance into fully paid and non-assessable Ordinary Shares, par value $0.0001 (the “Ordinary Shares”), of Borrower (“Conversion Shares”) as per the following conversion formula: the number of Conversion Shares equals the amount being converted (the “Conversion Amount”) divided by the Conversion Price; provided, however, that in the event the Floor Price is higher than the Conversion Price, Borrower may, subject to applicable Nasdaq listing rules, either agree to lower the Floor Price (as defined below) to be equal to the applicable Conversion Price or satisfy the Conversion in cash. |

In accounting for the issuance of the 2022 Convertible

Note, the Company separated the 2022 Convertible Note into liability and equity components. The carrying amount of the equity component

representing the conversion option was $

Debt issuance costs related to the 2022 Convertible

Note comprised of commissions paid to third party placement agent, lawyers, and warrants value of $

Net carrying amount of the liability component Convertible Notes dated as of September 30, 2022 was as follows:

Principal

| Unamortized

| Net

carrying | ||||||||||

| Convertible Notes - short-term | $ | ( | ) | $ | ||||||||

Net carrying amount of the liability component Convertible Note dated as of March 31, 2022 was as follows:

| Principal outstanding | Unamortized issuance cost | Net carrying value | ||||||||||

| Convertible Note - short-term | $ | ( | ) | $ | ||||||||

F-22

NOTE 12 – CONVERTIBLE NOTES (CONTINUED)

Net carrying amount of the equity component of the Convertible Note as of September 30, 2022 and March 31, 2022 were as follows:

| Amount allocated to conversion option | Issuance cost | Equity component, net | ||||||||||

| Convertible Note – equity portion | $ | ( | ) | $ | ||||||||

Amortization of issuance cost, debt discount and interest cost for the six months ended September 30, 2022 were as follows:

| Issuance costs and debt discount | Convertible interest | Total | ||||||||||

| Convertible Notes | $ | $ | $ | |||||||||

For the six months ended September 30, 2022,

The effective interest rate to derive the liability

component fair value is

NOTE 13 – REFUND LIABILITY

Refund liabilities represents the accrued liability for sales return based on the sales and the Company’s estimate of sale return rate.

Estimates of discretionary authorized returns, discounts and claims are based on (1) historical rates, (2) specific identification of outstanding returns not yet received from customers and outstanding discounts and claims and (3) estimated returns, discounts and claims expected, but not yet finalized with customers. Actual returns, discounts and claims in any future period are inherently uncertain and thus may differ from estimates recorded. If actual or expected future returns, discounts or claims were significantly greater or lower than the reserves established, a reduction or increase to net revenues would be recorded in the period in which such determination was made.

The estimated cost of inventory for product returns

of $

NOTE 14 – ACCRUED EXPENSES AND OTHER LIABILITIES

Accrued expenses and other liabilities consisted of the following as of September 30, 2022 and March 31, 2022:

| September 30, 2022 (Unaudited) |

March 31, 2022 |

|||||||

| Accrued payroll and welfare | $ | $ | ||||||

| Other payable for leasehold improvements | ||||||||

| Accrued professional service expenses | ||||||||

| Other current liabilities | ||||||||

| Total | $ | $ | ||||||

As of September 30, 2022 and March 31, 2022, the balances of other current liabilities represented amounts due to suppliers for operating expenses and to staff who paid for operating expenses on behalf of the Company.

F-23

NOTE 15 – SHAREHOLDERS’ EQUITY

Ordinary shares

The Company is authorized to issue unlimited shares

of $

On December 31, 2018, the Company completed the

closing of its initial public offering of

On January 10, 2019, the Underwriter exercise

the warrants in connection with the initial public offering and

For the year ended March 31, 2020,

For the year ended March 31, 2021,

For the six months ended September 30, 2022,

Warrant

In connection with the certain convertible notes issued on May 2, 2019, the Company issued a warrant on January 18, 2021 to Mr. Jian Ke for purchase of 1,000,000 ordinary shares (12,500 ordinary shares retrospectively restated for effect of reverse stock split on February 22, 2021 and May 19, 2022) (the “warrants”). The warrants carry a term of four years and shall be exercisable at $0.3843 per share ($30.744 per share retrospectively restated for effect of reverse stock split on February 22, 2021 and May 19, 2022). Management determined that the warrants are equity instruments because the warrants are both a) indexed to its own stock; and b) classified in stockholders’ equity. The warrants were recorded at their fair value on the date of grant as a component of stockholders’ equity. As of March 31, 2022, the total number of warrants outstanding was 250,000 (12,500 retrospectively restated for effect of reverse stock split on February 22, 2021 and May 19, 2022) with weighted average remaining life of 4 years.

The fair value of this Warrants was $

F-24

NOTE 15 – SHAREHOLDERS’ EQUITY (CONTINUED)

2021 Reverse stock split

On January 23, 2021,

2021 Equity incentive plan

In September 2021, the Company adopted a share

incentive plan (the “2021 Equity Incentive Plan”), which provides for the granting of share incentives, including incentive

share options (“ISOs”), restricted shares and any other form of award pursuant to the Equity Incentive Plan, to members of

the board, and employees of the Company. The Company reserved

Under the 2021 Equity Incentive Plan, the exercise

price of an option may be amended or adjusted at the discretion of the compensation committee, the determination of which would be final,

binding and conclusive.

The 2022 Public Offering

On January 18, 2022, the Company entered into

an underwriting agreement (the “Underwriting Agreement”) with Aegis Capital Corp. (the “Underwriter”), pursuant

to which the Company agreed to sell to the Underwriter, in a firm commitment public offering (the “Offering”)

The Pre-funded Warrants have an exercise price

of $

Pursuant to the 2022 Public Offering, the Company

issued

F-25

NOTE 15 – SHAREHOLDERS’ EQUITY (CONTINUED)

2022 Equity incentive plan

In September 2021, the Company adopted a share incentive plan (the “2022 Equity Incentive Plan”), which provides for the granting of share incentives, including incentive share options (“ISOs”), restricted shares and any other form of award pursuant to the Equity Incentive Plan, to members of the board, and employees of the Company. The vesting schedule, time and condition to exercise options is determined by the Company’s compensation committee. The term of the options may not exceed ten years from the date of the grant.

Under the 2022 Equity Incentive Plan, the exercise

price of an option may be amended or adjusted at the discretion of the compensation committee, the determination of which would be final,

binding and conclusive.

Pursuant to the 2022 Equity Incentive Plan, the Company issued 6,094,180 ordinary shares (304,709 shares retrospectively restated for effect of reverse stock split on May 19, 2022) to its management on June 6, 2022.

2022 Reverse stock split

On May 10, 2022,

F-26

NOTE 16 – INCOME TAXES

| (a) | Corporate Income Taxes |

Under the current laws of the British Virgin Islands

(“BVI”), the Company is not subject to tax on its income or capital gains. In addition, upon payments of dividends by the

Company to its shareholders, no BVI withholding tax is imposed. The Company’s subsidiaries incorporated in Hong Kong were subject

to the Hong Kong profits tax rate at

For the six months ended September 30, 2022 and 2021, income tax expenses consisted of the following:

For

the six months ended | ||||||||

2022 | 2021 | |||||||

| Current income tax provision | $ | $ | ||||||

| Deferred income tax provision | ||||||||

| Total income tax expense | $ | $ | ||||||

| (b) | Deferred Tax Assets |

Deferred income tax was measured using the enacted income tax rates for the periods in which they are expected to be reversed. Significant components of the Company’s deferred income tax assets and liabilities consist of follows:

| September 30, 2022 (Unaudited) | March 31, 2022 | |||||||

| Tax loss carry forward | $ | $ | ||||||

| Allowance for doubtful account - accounts receivable | ||||||||

| Impairment provision for inventory | ||||||||

| Allowance for deferred tax assets | ( | ) | ( | ) | ||||

| Total | $ | $ | - | |||||

The Company evaluates the level of authority for each uncertain tax position (including the potential application of interest and penalties) based on the technical merits, and measures the unrecognized benefits associated with the tax positions. For the six months ended September 30, 2022 and 2021, the Company had no unrecognized tax benefits.

The Company does not anticipate any significant increase to its asset for unrecognized tax benefit within the next 12 months. The Company will classify interest and penalties related to income tax matters, if any, in income tax expense.

F-27

NOTE 17 – RELATED PARTY TRANSACTIONS

Nature of relationships with related parties

| Name of related parties | Relationship with the Company | |

| Feng Zhou | ||

| Jianping Zhou | ||

| Xiaodong Pan | ||

| Taizhou Jiutian Pharmaceutical Co. Ltd. | ||

| Jiangsu Health Pharmaceutical Investment Co., Ltd. | ||

| Taizhou Su Xuan Tang Chinese Medicine Clinic | ||

| Taizhou Su Xuan Tang Chinese hospital Co., Ltd. | ||

| Jiangsu Sutaitang Online Commercial Co., Ltd. |

Related party balances

a. The amounts due from related parties as of September 30, 2022 and March 31, 2022 were as follows:

September 30, | March

31, | |||||||

| Jiangsu Health Pharmaceutical Investment Co., Ltd. | $ | $ | ||||||

| Taizhou Jiutian Pharmaceutical Co. Ltd. | ||||||||

| Taizhou Su Xuan Tang Chinese Medicine Clinic | ||||||||

| Total | $ | $ | ||||||

For the six months ended September 30, 2022, the Company provided working capital to support the operations of its related parties when needed. The amounts due from related parties were unsecured, due on demand, and interest free. The Company expected to collect these amounts from its related parties before March 31, 2023.

b. The amounts due to related parties as of September 30, 2022 and March 31, 2022 were as follows:

September 30, | March

31, | |||||||

| Jiangsu Health Pharmaceutical Investment Co., Ltd. | $ | $ | ||||||

| Jianping Zhou | ||||||||

| Jiangsu Sutaitang Online Commercial Co., Ltd. | ||||||||

| Feng Zhou | ||||||||

| Xiaodong Pan | ||||||||

| Total | $ | $ | ||||||

Related party transactions

For the six months ended September 30, 2022 and

2021, the Company generated revenues of $

For the six months ended September 30, 2022 and

2021, the Company generated revenues of $

For the six months ended September 30, 2022 and

2021, the Company generated revenue of $

For the six months ended September 30, 2022, the

Company repaid $

F-28

NOTE 18 – GUARANTEE

On April 12, 2021, Taizhou Suxuantang signed a

financial guarantee agreement with Jiangsu Changjiang Commercial Bank for Taizhou Jiutian Pharmaceutical Co. Ltd. in borrowing of $

On October 28, 2013, Taizhou Suxuantang signed

a financial guarantee agreement with Fenlan Xu for Jianping Zhou in borrowing of $

The Company has not made any payment under the above guarantee agreements for the six months ended September 30, 2022 and 2021.

NOTE 19 – COMMITMENT

The following table sets forth the Company’s operating lease commitment as of September 30, 2022:

| Office Rental | For the period ended September 30, | |||

| 2023 | $ | |||

| 2024 | ||||

| 2025 | ||||

| 2026 | ||||

| 2027 | ||||

| Thereafter | ||||

| Total | $ | |||

From time to time, the Company is involved in various legal proceedings, claims and other disputes arising from commercial operations, employees, and other matters which, in general, are subject to uncertainties and in which the outcomes are not predictable. The Company determines whether an estimated loss from a contingency should be accrued by assessing whether a loss is deemed probable and can be reasonably estimated. Although the Company can give no assurances about the resolution of pending claims, litigation or other disputes and the effect such outcomes may have on the Company, the Company believes that any ultimate liability resulting from the outcome of such proceedings, to the extent not otherwise provided or covered by insurance, will not have a material adverse effect on our condensed consolidated financial position or results of operations or liquidity. As of September 30, 2022 and March 31, 2022, Company had no pending legal proceedings.

NOTE 20 – SUBSEQUENT EVENTS

Securities purchase agreement

On September 22, 2022, the Company entered into

certain securities purchase agreement (the “SPA”) with Zhijun Xiao, a non-affiliate non-U.S. person (the “Investor”),

pursuant to which Mr. Xiao agreed to purchase

Securities purchase agreement

On December 19, 2022, the Company entered into

a securities purchase agreement (the “Purchase Agreement”) with Streeterville Capital, LLC, a Utah limited liability company

(the “Investor”), pursuant to which the Company issued the Investor an unsecured promissory note on December 19, 2022 in the

original principal amount of $

The Note bears interest at a rate of

The Company issued

The Company evaluated all events and transactions that occurred after September 30, 2022 up through the date the Company issued these financial statements on February 24, 2023 and concluded that no other material subsequent events.

F-29