Table of Contents

Index to Financial Statements

Filed pursuant to Rule 424(b)(3)

Registration Statement No. 333-228389

PROSPECTUS

Apergy Corporation

Offer to Exchange

$300,000,000 aggregate principal amount of its 6.375% Senior Notes due 2026 (the “exchange notes”), which have been registered under the Securities Act of 1933, as amended (the “Securities Act”), for any and all of its outstanding 6.375% Senior Notes due 2026 (the “outstanding notes” and such transaction, the “exchange offer”)

We are conducting the exchange offer in order to provide you with an opportunity to exchange your unregistered outstanding notes for the exchange notes that have been registered under the Securities Act.

The Exchange Offer

| • | We will exchange all unregistered outstanding notes that are validly tendered and not validly withdrawn for an equal principal amount of exchange notes that are registered under the Securities Act. |

| • | You may withdraw tenders of outstanding notes at any time prior to the expiration of the exchange offer. |

| • | The exchange offer expires at 11:59 p.m., New York City time, on December 19, 2018, unless extended (the “expiration date”). We do not currently intend to extend the expiration date. |

| • | The exchange of outstanding notes for exchange notes in the exchange offer will not constitute a taxable exchange or other taxable event for U.S. federal income tax purposes. See the discussion under the caption “Summary of Material United States Federal Income Tax Consequences” for more information. You should consult your own tax advisor as to the particular tax consequences to you of the exchange offer, as well as the tax consequences of the ownership and disposition of outstanding notes or exchange notes. |

| • | The terms of the exchange notes to be issued in the exchange offer are substantially identical to the outstanding notes, except that the exchange notes will be registered under the Securities Act, do not have any transfer restrictions and do not have registration rights or additional interest provisions. |

Results of the Exchange Offer

| • | Except as prohibited by applicable law, the exchange notes may be sold in the over-the-counter market, in negotiated transactions or through a combination of such methods. |

| • | We will not receive any proceeds from the exchange offer. |

There is no established trading market for the exchange notes or the outstanding notes and we do not intend to list the exchange notes or the outstanding notes on any securities exchange.

All untendered outstanding notes will remain outstanding and continue to be subject to the restrictions on transfer set forth in the outstanding notes and in the Indenture (as defined herein). In general, the outstanding notes may not be offered or sold, unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offer, we do not currently anticipate that we will register the outstanding notes under the Securities Act.

Each broker-dealer that receives exchange notes for its own account in the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of those exchange notes. The letter of transmittal states that by so acknowledging and delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for outstanding notes where the broker-dealer acquired such outstanding notes as a result of market-making or other trading activities. We have agreed to keep effective the registration statement of which this prospectus is a part until 180 days after the completion of the exchange offer. See “Plan of Distribution.”

See “Risk Factors” beginning on page 12 for a discussion of certain risks that you should consider before participating in the exchange offer.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is November 21 , 2018.

Table of Contents

Index to Financial Statements

Unless otherwise indicated or context otherwise requires, all references in this prospectus to “Apergy Corporation,” “Apergy,” “the Company,” “we,” “us,” “our” and “our company” refer (i) prior to the Separation (as defined herein), to the Apergy businesses, consisting of entities, assets and liabilities, conducting the upstream oil and gas business within Dover’s Energy segment and (ii) after the Separation, to Apergy Corporation and its consolidated subsidiaries.

References in this prospectus to “Dover” refer to Dover Corporation, a Delaware corporation and its consolidated subsidiaries (other than Apergy Corporation and its combined subsidiaries), unless the context otherwise requires or as otherwise specified herein.

This prospectus incorporates or references important business and financial information about Apergy that is not included in or delivered with this prospectus. This information is available without charge to any person to whom this prospectus is delivered, upon written or oral request. Written requests should be sent to:

Apergy Corporation

2445 Technology Forest Blvd

Building 4, 12th Floor

The Woodlands, Texas 77381

Attn: David Skipper

Oral requests should be made by telephoning (713) 230-8031.

To ensure timely delivery, you should make your request to us no later than December 12, 2018, which is five business days prior to the expiration date of the exchange offer.

i

Table of Contents

Index to Financial Statements

CAUTIONARY STATEMENT CONCERNING FORWARD-LOOKING STATEMENTS

This prospectus contains “forward-looking statements” within the meaning of the safe harbors from liability established by the Private Securities Litigation Reform Act of 1995. Forward-looking statements are usually related to future events and anticipated revenues, earnings, cash flows or other aspects of our operations or operating results. Forward-looking statements are often identified by the words “believe,” “anticipate,” “expect,” “may,” “intend,” “foresee,” “guidance,” “estimate,” “potential,” “outlook,” “plan,” “should,” “will,” “would,” “could,” “target,” “forecast” and similar expressions, including the negative thereof. The absence of these words, however, does not mean that the statements are not forward-looking statements. Forward-looking statements are based on our current expectations, beliefs and assumptions concerning future developments and business conditions and their potential effect on us. While management believes that these forward-looking statements are reasonable as and when made, there can be no assurance that future developments affecting us will be those that we anticipate.

All of our forward-looking statements involve risk, uncertainties (some of which are significant or beyond our control) and assumptions that could cause actual results to materially differ from our historical experience and our present expectations or projections. Known material factors that could cause actual results to materially differ from those contemplated in the forward-looking statements include those set forth in this prospectus under the heading entitled “Risk Factors,” which are summarized as follows:

| • | Demand for our products and services, which is affected by changes in the price of, and demand for, crude oil and natural gas in domestic and international markets; |

| • | Our ability to successfully compete with other companies in our industry; |

| • | Our ability to develop and implement new technologies and services, as well as our ability to protect and maintain critical intellectual property assets; |

| • | Cost inflation and availability of raw materials; |

| • | Changes in federal, state and local legislation and regulations relating to hydraulic fracturing or oil and gas development and the potential for related litigation or restrictions on our customers; |

| • | Our ability to successfully execute our capital allocation and acquisition programs; |

| • | Potential liabilities arising out of the installation or use of our products; |

| • | Continuing consolidation within our customers’ industry; |

| • | A failure of our information technology infrastructure or any significant breach of security; |

| • | Changes in environmental and health and safety laws and regulations which may increase our costs, limit the demand for our products and services or restrict our operations; |

| • | Risks relating to our existing international operations and expansion into new geographical markets; |

| • | Changes in domestic and foreign governmental public policies, risks associated with entry into emerging markets, changes in statutory tax rates and unanticipated outcomes with respect to tax audits; |

| • | Failure to attract, retain and develop personnel for key management; |

| • | The impact of our indebtedness on our financial position and operating flexibility; |

| • | The impact of tariffs and other trade measures on our business; |

| • | Credit risks related to our customer base or the loss of significant customers; |

| • | Deterioration in future expected profitability or cash flows and its effect on our goodwill; |

| • | Disruptions in the political, regulatory, economic and social conditions of the countries in which we conduct business; |

1

Table of Contents

Index to Financial Statements

| • | Fluctuations in currency markets worldwide; and |

| • | Increased compliance costs for us and our customers due to changes in climate change legislation and other regulatory initiatives. |

We undertake no obligation to publicly update or revise any of our forward-looking statements after the date they are made, whether as a result of new information, future events or otherwise, except to the extent required by law.

WHERE YOU CAN FIND MORE INFORMATION

We are required to file annual, quarterly and current reports, proxy statements and other information with the SEC. Our SEC filings are available to the public on the SEC’s website at http://www.sec.gov.

We have filed with the SEC a registration statement on Form S-4 relating to the securities covered by this prospectus. This prospectus is a part of the registration statement and does not contain all of the information in the registration statement. Whenever a reference is made in this prospectus to a contract or other document of ours, please be aware that the reference is only a summary and that you should refer to the exhibits that are a part of the registration statement for a copy of the contract or other document. You may access a copy of the registration statement through the SEC’s website.

2

Table of Contents

Index to Financial Statements

This summary highlights selected information appearing elsewhere in this prospectus and is, therefore, qualified in its entirety by the more detailed information appearing elsewhere in this prospectus. It may not contain all the information that is important to you. We urge you to read carefully this entire prospectus and the other documents to which it refers to understand fully the terms of the exchange notes and the exchange offer. You should pay special attention to “Risk Factors” and “Cautionary Statement Concerning Forward-Looking Statements.”

Our Business

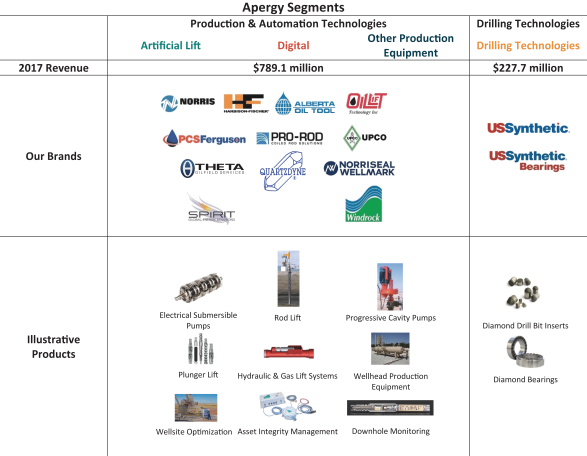

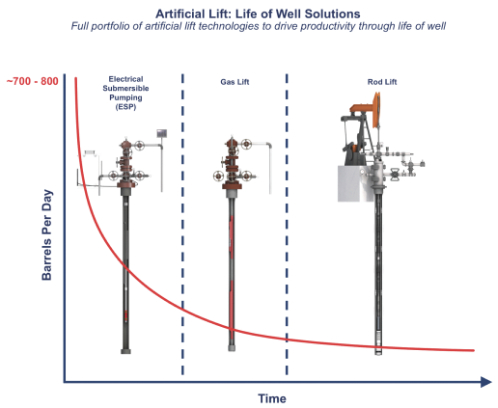

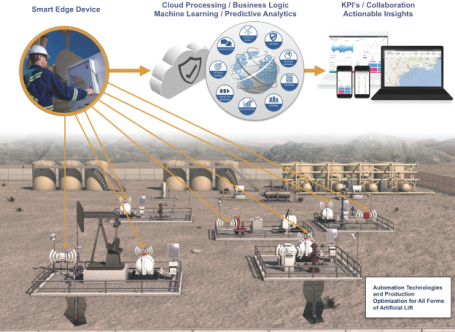

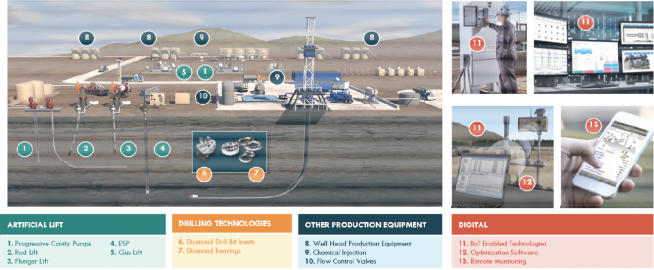

We are a leading provider of highly engineered equipment and technologies that help companies drill for and produce oil and gas safely and efficiently around the world. Our products provide efficient functioning throughout the lifecycle of a well—from drilling to completion to production. We report our results of operations in the following reporting segments: Production & Automation Technologies; and Drilling Technologies. Our Production & Automation Technologies segment offerings consist of artificial lift equipment and solutions, including rod pumping systems, electric submersible pump systems, progressive cavity pumps and drive systems and plunger lifts, as well as a full automation and digital offering consisting of equipment, software and Industrial Internet of Things solutions for downhole monitoring, wellsite productivity enhancement and asset integrity management. Our Drilling Technologies segment offering provides market leading polycrystalline diamond cutters and bearings that result in cost effective and efficient drilling. See “Our Business and Properties.”

Separation and Distribution

On April 18, 2018, the Dover Corporation (“Dover”) Board of Directors approved the separation of entities conducting its upstream oil and gas energy business within Dover’s Energy segment (the “Separation”) into an independent, publicly traded company named Apergy Corporation. In accordance with the separation and distribution agreement, the two companies were separated by Dover distributing to Dover’s stockholders all 77,339,828 shares of common stock of Apergy on May 9, 2018. Each Dover stockholder received one share of Apergy stock for every two shares of Dover stock held at the close of business on the record date of April 30, 2018. In conjunction with the Separation, Dover received a private letter ruling from the Internal Revenue Service (the “IRS”) to the effect that, based on certain facts, assumptions, representations and undertakings set forth in the ruling, for U.S. federal income tax purposes, the distribution of Apergy common stock was not taxable to Dover or U.S. holders of Dover common stock, except in respect to cash received in lieu of fractional share interests. Following the Separation, Dover retained no ownership interest in Apergy, and each company, as of May 9, 2018, has separate public ownership, boards of directors and management. On May 9, 2018, Apergy common stock began “regular-way” trading on the New York Stock Exchange under the “APY” symbol. See “Certain Relationships and Related Person Transactions.”

Corporate Information

Apergy Corporation was incorporated in Delaware on October 10, 2017, under the name Wellsite Corporation and was renamed Apergy Corporation on February 2, 2018. Apergy was formed for the purpose of holding entities, assets and liabilities used in conducting Dover’s upstream oil and gas business within Dover’s Energy segment prior to the Separation. The address of our principal executive offices is 2445 Technology Forest Blvd, Building 4, 12th Floor, The Woodlands, Texas 77381. Our telephone number is (281) 403-5772.

We also maintain an internet site at www.apergy.com. Our website and the information contained therein or connected thereto shall not be deemed to be incorporated herein, and you should not rely on any such information in deciding whether or not to participate in the exchange offer.

3

Table of Contents

Index to Financial Statements

The Exchange Offer

| General |

In connection with the private offering of the outstanding notes, we entered into a registration rights agreement with the initial purchasers in such offering pursuant to which we agreed, among other things, to deliver this prospectus to you and to use commercially reasonable efforts to complete the exchange offer within one year after the date of original issuance of the outstanding notes. You are entitled to exchange in the exchange offer your outstanding notes for the exchange notes that are identical in all material respects to the outstanding notes except: |

| • | the exchange notes have been registered under the Securities Act; |

| • | the exchange notes are not entitled to any registration rights which are applicable to the outstanding notes under the registration rights agreement; and |

| • | the additional interest provision of the registration rights agreement is not applicable. |

| The Exchange Offer |

We are offering to exchange $300.0 million aggregate principal amount of 6.375% Senior Notes due 2026 that have been registered under the Securities Act for any and all of our existing restricted 6.375% Senior Notes due 2026. |

| You may only exchange outstanding notes in minimum denominations of $2,000 and integral multiples of $1,000 in excess thereof. |

| Resale |

Based on an interpretation by the staff of the SEC set forth in no-action letters issued to third parties, we believe that the exchange notes issued pursuant to the exchange offer in exchange for the outstanding notes may be offered for resale, resold and otherwise transferred by you (unless you are our “affiliate” within the meaning of Rule 405 under the Securities Act) without compliance with the registration and prospectus delivery provisions of the Securities Act, provided that: |

| • | you are acquiring the exchange notes in the ordinary course of your business; and |

| • | you have not engaged in, do not intend to engage in, and have no arrangement or understanding with any person to participate in, a distribution of the exchange notes. |

| If you are a broker-dealer and receive exchange notes for your own account in exchange for outstanding notes that you acquired as a result of market-making activities or other trading activities, you must acknowledge that you will deliver this prospectus in connection with any resale of the exchange notes and that you are not our affiliate. See “Plan of Distribution.” |

4

Table of Contents

Index to Financial Statements

| Any holder of outstanding notes who: |

| • | is our affiliate; |

| • | does not acquire exchange notes in the ordinary course of its business; or |

| • | tenders its outstanding notes in the exchange offer with the intention to participate, or for the purpose of participating, in a distribution of exchange notes, |

| cannot rely on the position of the staff of the SEC enunciated in Morgan Stanley & Co. Incorporated (available June 5, 1991) and Exxon Capital Holdings Corporation (available May 13, 1988), as interpreted in Shearman & Sterling (available July 2, 1993), or similar no-action letters and, in the absence of an exemption therefrom, must comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale of the exchange notes. |

| Our belief that the exchange notes may be offered for resale without compliance with the registration or prospectus delivery provisions of the Securities Act is based on interpretations of the SEC for other exchange offers that the SEC expressed in some of its no-action letters to other issuers in exchange offers like ours. We cannot guarantee that the SEC would make a similar decision about our exchange offer. If our belief is wrong, or if you cannot truthfully make the representations mentioned above, and you transfer any exchange note issued to you in the exchange offer without meeting the registration and prospectus delivery requirements of the Securities Act, or without an exemption from such requirements, you could incur liability under the Securities Act. We are not indemnifying you for any such liability. |

| Expiration Date |

The exchange offer will expire at 11:59 p.m., New York City time, on December 19, 2018, unless extended by us. We do not currently intend to extend the expiration date. |

| Withdrawal |

You may withdraw the tender of your outstanding notes at any time prior to the expiration of the exchange offer. We will return to you any of your outstanding notes that are not accepted for any reason for exchange, without expense to you, promptly after the expiration or termination of the exchange offer. |

| Conditions to the Exchange Offer |

The exchange offer is subject to customary conditions. We reserve the right to waive any defects, irregularities or conditions to exchange as to particular outstanding notes. See “The Exchange Offer—Conditions to the Exchange Offer.” |

| Procedures for Tendering Outstanding Notes |

If you wish to participate in the exchange offer, you must either: |

| • | complete, sign and date the accompanying letter of transmittal, or a facsimile of the letter of transmittal, in accordance with the |

5

Table of Contents

Index to Financial Statements

| instructions contained in this prospectus and the letter of transmittal, and mail or deliver such letter of transmittal or facsimile thereof to the exchange agent at the address set forth on the cover page of the letter of transmittal; or |

| • | if you hold outstanding notes through the Depository Trust Company (“DTC”), comply with DTC’s Automated Tender Offer Program procedures described in this prospectus, by which you will agree to be bound by the letter of transmittal. |

| By signing, or agreeing to be bound by, the letter of transmittal, you will represent to us that, among other things: |

| • | you are acquiring the exchange notes in the ordinary course of your business; |

| • | you have no arrangement or understanding with any person to participate in the distribution of the exchange notes; |

| • | you are not our “affiliate” within the meaning of Rule 405 under the Securities Act; |

| • | you are not engaged in, and do not intend to engage in, a distribution of the exchange notes; and |

| • | if you are a broker-dealer that will receive exchange notes for your own account in exchange for outstanding notes that were acquired as a result of market-making activities, you will deliver a prospectus, as required by law, in connection with any resale of such exchange notes. |

| Guaranteed Delivery Procedures |

None. |

| Special Procedures for Beneficial Owners |

If you are a beneficial owner of outstanding notes that are registered in the name of a broker, dealer, commercial bank, trust company or other nominee, and you wish to tender those outstanding notes in the exchange offer, you should contact the registered holder promptly and instruct the registered holder to tender those outstanding notes on your behalf. If you wish to tender on your own behalf, you must, prior to completing and executing the letter of transmittal and delivering your outstanding notes, either make appropriate arrangements to register ownership of the outstanding notes in your name or obtain a properly completed bond power from the registered holder. The transfer of registered ownership may take considerable time and may not be able to be completed prior to the expiration date. |

| Effect on Holders of Outstanding Notes |

As a result of the making of the exchange offer, and upon acceptance for exchange of all validly tendered outstanding notes pursuant to the terms of the exchange offer, we will have fulfilled a covenant under the registration rights agreement. Accordingly, there will be no increase in the applicable interest rate on the outstanding notes under |

6

Table of Contents

Index to Financial Statements

| the circumstances described in the registration rights agreement. If you do not tender your outstanding notes in the exchange offer, you will continue to be entitled to all the rights and limitations applicable to the outstanding notes as set forth in the Indenture, except we will not have any further obligation to you to provide for the exchange and registration of untendered outstanding notes under the registration rights agreement. To the extent that outstanding notes are tendered and accepted in the exchange offer, the trading market for outstanding notes that are not so tendered and accepted could be adversely affected. |

| Consequences of Failure to Exchange |

All untendered outstanding notes will remain outstanding and continue to be subject to the restrictions on transfer set forth in the outstanding notes and in the Indenture. In general, the outstanding notes may not be offered or sold unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offer, we do not currently anticipate that we will register the outstanding notes under the Securities Act. |

| United States Federal Income Tax Consequences |

The exchange of outstanding notes for exchange notes in the exchange offer will not constitute a taxable exchange or other taxable event for U.S. federal income tax purposes. See “Summary of Material United States Federal Income Tax Consequences.” You should consult your own tax advisor as to the particular tax consequences to you of the exchange offer, as well as the tax consequences of the ownership and disposition of outstanding notes or exchange notes. |

| Use of Proceeds |

We will not receive any proceeds from the issuance of the exchange notes in the exchange offer. See “Use of Proceeds.” |

| Exchange Agent |

Wells Fargo Bank, National Association is the exchange agent for the exchange offer. Any questions and requests for assistance, requests for additional copies of this prospectus or of the letter of transmittal should be directed to the exchange agent. The address and telephone number of the exchange agent are set forth in the section captioned “The Exchange Offer—Exchange Agent.” |

7

Table of Contents

Index to Financial Statements

The Exchange Notes

The terms of the exchange notes and those of the outstanding notes are substantially identical, except that the transfer restrictions and registration rights relating to the outstanding notes do not apply to the exchange notes. For a more detailed description of the terms of the notes and the guarantees, see “Description of the Exchange Notes.” When we use the term “notes” in this prospectus, the term includes the outstanding notes and the exchange notes, as applicable.

| Issuer |

Apergy Corporation |

| Securities Offered |

$300,000,000 aggregate principal amount of exchange notes. |

| Maturity Date |

May 1, 2026. |

| Indenture |

We will issue the exchange notes under the Indenture, dated as of May 3, 2018, as amended and supplemented (the “Indenture”), between us and Wells Fargo Bank, National Association, as trustee (the “Trustee”). |

| Interest Rate |

6.375% per year. |

| Interest Payment Dates |

May 1 and November 1 of each year. |

| Guarantees |

The exchange notes will be guaranteed, jointly and severally, by all existing and future direct and indirect 100% owned domestic subsidiaries of Apergy that incur or that guarantee any obligations under our senior secured credit facilities (the “Senior Secured Credit Facilities”) (the “Guarantors”) or certain series of capital markets debt securities (other than the notes) of Apergy or any Guarantor. See “Description of the Exchange Notes—Guarantees.” |

| All of our existing direct and indirect 100% owned domestic subsidiaries (other than certain immaterial subsidiaries) will guarantee the exchange notes. In the future, additional subsidiaries may not guarantee the notes and guarantees provided may be released in certain circumstances. See “Risk Factors—Risks Related to Holding the Exchange Notes—Claims of holders of the notes will be structurally subordinated to all obligations of our existing and future subsidiaries that do not become Guarantors of the notes.” In the event of a bankruptcy, liquidation, reorganization or similar proceeding of any of these non-Guarantor subsidiaries, the non-Guarantor subsidiaries will pay the holders of their debt and their trade creditors before they will be able to distribute any of their assets to Apergy or a Guarantor. As a result, all of the existing and future liabilities of our non-Guarantor subsidiaries, including any claims of trade creditors, will be effectively senior to the notes. The Indenture does not limit the amount of liabilities that are not considered indebtedness that may be incurred by Apergy or its restricted subsidiaries, including the non-Guarantor subsidiaries. |

8

Table of Contents

Index to Financial Statements

| Ranking |

The exchange notes and guarantees will constitute senior indebtedness of Apergy and the Guarantors and will rank: |

| • | pari passu in right of payment with any existing and future senior indebtedness of Apergy and the Guarantors, including under the Senior Secured Credit Facilities; |

| • | senior in right of payment to any future subordinated indebtedness of Apergy and the Guarantors; |

| • | effectively subordinated to all of Apergy’s and the Guarantors’ existing and future secured indebtedness, including the Senior Secured Credit Facilities, to the extent of the value of the collateral securing such indebtedness; and |

| • | structurally subordinated to all existing and future indebtedness and other claims and liabilities, including preferred stock, of Apergy’s subsidiaries that will not guarantee the notes (other than indebtedness and liabilities owed to Apergy or one of the Guarantors). |

| As of September 30, 2018, the notes and related guarantees were effectively subordinated to approximately $395.0 million (excluding any original issue discount and deferred financing costs) principal amount of senior secured indebtedness, to the extent of the collateral securing such senior secured indebtedness, such indebtedness consisting solely of approximately $395.0 million (excluding any original issue discount and deferred financing costs) of borrowings under term loan B facility (the “Term Loan Facility”) of the Senior Secured Credit Facilities. |

| As of September 30, 2018, we were able to incur approximately an additional $244.5 million of indebtedness under the senior secured revolving credit facility (the “Revolving Credit Facility”) of the Senior Secured Credit Facilities. |

| See “Description of the Exchange Notes—Ranking.” |

| Optional Redemption |

Except as described below, Apergy cannot redeem the notes before May 1, 2021. Thereafter, Apergy may redeem some or all of the notes at any time at the redemption prices listed under “Description of the Exchange Notes—Optional Redemption,” plus accrued and unpaid interest up to, but excluding, the redemption date. |

| At any time and from time to time prior to May 1, 2021, Apergy may redeem some or all of the exchange notes at a price equal to 100% of the aggregate principal amount thereof plus the make-whole premium described under “Description of the Exchange Notes—Optional Redemption,” plus accrued and unpaid interest up to, but excluding, the redemption date. |

| At any time and from time to time prior to May 1, 2021, Apergy may redeem up to 35% of the aggregate principal amount of the notes at a |

9

Table of Contents

Index to Financial Statements

| redemption price of 106.375% of the aggregate principal amount thereof, plus accrued and unpaid interest up to, but excluding, the redemption date, with the net proceeds of certain equity offerings if at least 65% of the aggregate principal amount of notes issued remains outstanding afterward and Apergy redeems the notes within 180 days of completing the equity offering. |

| Change of Control Offer |

If a Change of Control Repurchase Event (as defined under “Description of the Exchange Notes”) occurs, Apergy will be required to make an offer to purchase all of the notes at a price in cash equal to 101% of the aggregate principal amount thereof plus accrued and unpaid interest up to, but excluding, the repurchase date. See “Description of the Exchange Notes—Repurchase at the Option of Holders—Change of control repurchase events.” |

| Asset Sale Proceeds |

If Apergy or any of its restricted subsidiaries engages in certain asset sales, Apergy will be required under certain circumstances to make an offer to purchase the notes at 100% of the principal amount thereof, plus accrued and unpaid interest up to, but excluding, the repurchase date. See “Description of the Exchange Notes—Repurchase at the Option of Holders—Asset sales.” |

| Covenants |

The Indenture limits the ability of Apergy and its restricted subsidiaries to, among other things: |

| • | pay dividends or distributions, repurchase equity, prepay subordinated indebtedness and make other restricted payments; |

| • | incur additional indebtedness or issue certain preferred shares; |

| • | make certain investments; |

| • | sell or transfer certain assets; |

| • | incur liens on assets; |

| • | merge, consolidate or sell all or substantially all of its assets; |

| • | enter into transactions with affiliates; |

| • | designate our subsidiaries as unrestricted subsidiaries; and |

| • | create or cause to exist certain restrictions on the ability of non-Guarantor restricted subsidiaries to pay dividends or make other payments to us. |

| These covenants are subject to important exceptions and qualifications. Following the first date on which (i) the notes have an investment grade rating, (ii) no default has occurred and is continuing under the Indenture and (iii) Apergy has delivered an officer’s certificate to the Trustee certifying that the conditions set forth in clauses (i) and (ii) above are satisfied, Apergy and its restricted subsidiaries will not be subject to certain of these covenants and the obligation to grant further guarantees will be terminated. See “Description of the Exchange Notes—Certain Covenants.” |

10

Table of Contents

Index to Financial Statements

| No Prior Market |

The exchange notes will be new securities for which there is currently no market. We do not intend to apply for a listing of the exchange notes on any securities exchange or to arrange for the inclusion of the exchange notes on any automated dealer quotation system. Accordingly, there can be no assurance as to the development or liquidity of any market for the exchange notes. Accordingly, we cannot assure you that a liquid market for the exchange notes will develop or be maintained. |

| Risk Factors |

You should consider carefully all of the information set forth in this prospectus prior to exchanging your outstanding notes. In particular, we urge you to consider carefully the factors set forth under the heading “Risk Factors.” |

11

Table of Contents

Index to Financial Statements

You should carefully consider the risk factors set forth below as well as the other information contained in this prospectus. Any of the following risks could materially and adversely affect our business, financial condition, operating results or cash flow; however, these risks are not our only risks. In such a case, the trading price of the notes could decline or we may not be able to make payments of interest and principal on the notes, and you may lose all or part of your original investment.

Risks Related to Apergy’s Business

Trends in oil and natural gas prices may affect the drilling and production activity, profitability and financial stability of Apergy’s customers and therefore the demand for, and profitability of, Apergy’s products and services, which could have a material adverse effect on Apergy’s business, results of operations and financial condition.

The oil and gas industry is cyclical in nature and experiences periodic downturns of varying length and severity. Most recently, the oil and gas industry experienced a significant downturn in 2015 and 2016. Apergy’s ability to manage periodic industry downturns is important to its business, results and prospects. Demand for Apergy’s energy products and services is sensitive to the level of drilling and production activity of, and the corresponding capital spending by, oil and natural gas companies. The level of drilling and production activity is directly affected by trends in oil and natural gas prices, which are influenced by numerous factors affecting the supply and demand for oil and gas, including:

| • | worldwide economic activity; |

| • | the level of exploration and production activity; |

| • | interest rates and the cost of capital; |

| • | environmental regulation; |

| • | federal, state and foreign policies regarding exploration and development of oil and gas; |

| • | the ability and/or desire of the Organization of the Petroleum Exporting Countries (“OPEC”) and other major producers to set and maintain production levels and pricing; |

| • | governmental regulations regarding future oil and gas exploration and production; |

| • | the cost of exploring and producing oil and gas; |

| • | the pace of adoption and cost of developing alternative energy sources; |

| • | the availability, expiration date and price of onshore and offshore leases; |

| • | the discovery rate of new oil and gas reserves in onshore and offshore areas; |

| • | the success of drilling for oil and gas in unconventional resource plays such as shale formations; |

| • | alternative opportunities to invest in onshore exploration and production opportunities; |

| • | domestic and global political and economic uncertainty, socio-political unrest and instability, terrorism or hostilities; |

| • | technological advances; and |

| • | weather conditions. |

Oil and gas prices and the level of drilling and production activity have been characterized by significant volatility in recent years. In particular, the prices of oil and natural gas were highly volatile in 2014 and 2015 and declined dramatically. Prices of oil began to recover in late 2016, but there can be no assurance that increases

12

Table of Contents

Index to Financial Statements

will continue. Apergy expects continued volatility in both crude oil and natural gas prices, as well as in the level of drilling and production related activities. Even the perception of longer-term lower oil and natural gas prices can reduce or defer major capital expenditures by Apergy’s customers in the oil and gas industry. A significant downturn in the industry could result in the reduction in demand for Apergy’s products and services, and could have a material adverse effect on Apergy’s business, results of operations, financial condition and cash flows.

Apergy might be unable to compete successfully with other companies in its industry.

The markets in which Apergy operates are highly competitive. The principal competitive factors in Apergy’s markets are customer service, product quality and performance, price, breadth of product offering, market expertise and innovation. In some of Apergy’s product and service offerings, it competes with the oil and natural gas industry’s largest oilfield service providers. These large national and multi-national companies may have longer operating histories, greater financial, technical, and other resources, greater brand recognition, and a stronger presence in geographic markets than Apergy. In addition, Apergy competes with many smaller companies capable of competing effectively on a regional or local basis. Apergy’s competitors may be able to respond more quickly to new or emerging technologies and services, and changes in customer requirements. Many contracts are awarded on a bid basis, which further increases competition based on price. As a result of competition, Apergy may lose market share or be unable to maintain or increase prices for its present services, or to acquire additional business opportunities, which could have a material adverse effect on Apergy’s business, results of operations, financial condition and cash flows.

If Apergy is unable to develop new products and technologies, its competitive position may be impaired, which could materially and adversely affect its sales and market share.

The markets in which Apergy operates are characterized by changing technologies and introductions of new products and services. As a result, Apergy’s success is dependent upon its ability to develop or acquire new services and products on a cost-effective basis, to introduce them into the marketplace in a timely manner and to protect and maintain critical intellectual property assets related to these developments. Difficulties or delays in research, development or production of new products and technologies, or failure to gain market acceptance of new products and technologies, may significantly reduce future revenues and materially and adversely affect Apergy’s competitive position. While Apergy intends to continue committing substantial financial resources and effort to the development of new services and products, Apergy may not be able to successfully differentiate its services and products from those of its competitors. Apergy’s customers may not consider its proposed services and products to be of value to them or may not view them as superior to Apergy’s competitors’ services and products. In addition, competitors or customers may develop new technologies, which address similar or improved solutions to Apergy’s existing technology. Further, Apergy may not be able to adapt to evolving markets and technologies, develop new products, achieve and maintain technological advantages or protect technological advantages through intellectual property rights. If Apergy does not compete successfully, its business, results of operations, financial condition and cash flows could be materially adversely affected.

Apergy could lose customers or generate lower revenue, operating profits and cash flows if there are significant increases in the cost of raw materials or if Apergy is unable to obtain raw materials.

Apergy purchases raw materials, sub-assemblies and components for use in its manufacturing operations, which exposes Apergy to volatility in prices for certain commodities. Significant price increases for these commodities could adversely affect Apergy’s operating profits. While Apergy generally attempts to mitigate the impact of increased raw material prices by endeavoring to make strategic purchasing decisions, broaden its supplier base and pass along increased costs to customers, there may be a time delay between the increased raw material prices and the ability to increase the prices of products, or Apergy may be unable to increase the prices of products due to a competitor’s pricing pressure or other factors. In addition, while raw materials are generally available now, the inability to obtain necessary raw materials could affect Apergy’s ability to meet customer commitments and satisfy market demand for certain products. Certain of Apergy’s product lines depend on a

13

Table of Contents

Index to Financial Statements

limited number of third-party suppliers and vendors. The ability of these third parties to deliver raw materials may be affected by events beyond Apergy’s control. Consequently, a significant price increase in raw materials, or their unavailability, may result in a loss of customers and adversely impact Apergy’s business, results of operations, financial condition and cash flows.

Federal, state and local legislative and regulatory initiatives relating to hydraulic fracturing and the potential for related litigation could result in increased costs and additional operating restrictions or delays for Apergy’s customers, which could reduce demand for Apergy’s products and negatively impact Apergy’s business, financial condition and results of operations.

Environmental laws and regulations could limit Apergy’s customers’ exploration and production activities. Although Apergy does not directly engage in hydraulic fracturing activities, it provides products and services to hydraulic fracturing operators in the oil and natural gas industry. Hydraulic fracturing is a widely used industry production technique that is used to recover oil and/or natural gas from dense subsurface rock formations. The process involves the injection of water, proppants and chemicals, under pressure, into the formation to fracture the surrounding rock and stimulate production. The hydraulic fracturing process is typically regulated by state or local governmental authorities. However, the practice of hydraulic fracturing has become controversial in some areas and is undergoing increased scrutiny. Several federal agencies, regulatory authorities, and legislative entities are investigating the potential environmental impacts of hydraulic fracturing and whether additional regulation may be necessary. The U.S. Congress has from time to time considered, but has not yet adopted, legislation to provide for federal regulation of hydraulic fracturing and to require disclosure of the chemicals used in the process. The U.S. Environmental Protection Agency (“EPA”) has issued a number of regulations in recent years that may affect hydraulic fracturing; however, the current administration has more generally indicated an interest in scaling back or rescinding regulations that inhibit the development of the U.S. oil and gas industry. It is difficult to predict the extent to which proposed regulations will be implemented or the outcome of any related litigation.

In addition, various state and local governments have implemented, or are considering, increased regulatory oversight of hydraulic fracturing through additional permitting requirements, operational restrictions, disclosure requirements and temporary or permanent bans on hydraulic fracturing in certain areas such as environmentally sensitive watersheds. For example, many states have imposed disclosure requirements on hydraulic fracturing well owners and operators regarding the chemicals used in hydraulic fracturing. Some local governments have adopted and others may seek to adopt ordinances prohibiting or regulating the time, place and manner of drilling activities in general or hydraulic fracturing activities within their jurisdictions. Concerns have been raised that hydraulic fracturing may also contribute to seismic activity and in response to these concerns, regulators in some states, including Texas, are seeking to impose additional requirements. Increased regulation and attention given to induced seismicity could lead to greater opposition to, and litigation concerning, oil and natural gas activities utilizing hydraulic fracturing or injection wells for waste disposal.

The adoption of new laws or regulations at the federal, state, or local levels imposing reporting obligations on, or otherwise limiting or delaying, the hydraulic fracturing process could make it more difficult to complete oil and gas wells, increase Apergy’s customers’ costs of compliance and doing business, and otherwise adversely affect the hydraulic fracturing services they perform, which could negatively impact demand for Apergy’s products and services. In addition, heightened political, regulatory and public scrutiny of hydraulic fracturing practices, including lawsuits, could expose Apergy or its customers to increased legal and regulatory proceedings, which could be time-consuming, costly or result in substantial legal liability or significant reputational harm. Apergy could be directly affected by adverse litigation, or indirectly affected if the cost of compliance or the risks of liability limit the ability or willingness of Apergy’s customers to operate. Such costs and scrutiny could directly or indirectly, through reduced demand for Apergy’s products and services, have a material adverse effect on its business, results of operations, financial condition and cash flows.

14

Table of Contents

Index to Financial Statements

Apergy’s growth and results of operations may be adversely affected if it is unsuccessful in its capital allocation and acquisition program.

If Apergy fails to allocate its capital appropriately, in respect of either its acquisition program or organic growth in its operations, it could be overexposed in certain markets and geographies and unable to expand into adjacent products or markets. Apergy expects to pursue a strategy of acquiring value creating, add-on businesses that broaden its existing position and global reach thereby complementing its existing businesses. However, there can be no assurance that Apergy will be able to continue to find suitable businesses to purchase, that Apergy will be able to acquire such businesses on acceptable terms, or that all closing conditions will be satisfied with respect to any pending acquisition. If Apergy is unsuccessful in its acquisition efforts, then its ability to continue to grow could be adversely affected. In addition, Apergy faces the risk that a completed acquisition may underperform relative to expectations. Apergy may not achieve the synergies originally anticipated, may become exposed to unexpected liabilities or may not be able to sufficiently integrate completed acquisitions into its current business and growth model. These factors could potentially have an adverse impact on Apergy’s business, results of operations, financial condition and cash flows.

Apergy’s products are used in operations that are subject to potential hazards inherent in the oil and natural gas industry and, as a result, Apergy is exposed to potential liabilities that may affect its financial condition and reputation.

Apergy’s products are used in potentially hazardous drilling, completion and production applications in the oil and natural gas industry where an accident or a failure of a product can potentially have catastrophic consequences. Risks inherent to these applications, such as equipment malfunctions and failures, equipment misuse and defects, explosions, blowouts and uncontrollable flows of oil, natural gas or well fluids and natural disasters can cause personal injury, loss of life, suspension of operations, damage to formations, damage to facilities, business interruption and damage to or destruction of property, surface water and drinking water resources, equipment and the environment. In addition, Apergy provides certain services that could cause, contribute to or be implicated in these events. If Apergy’s products or services fail to meet specifications or are involved in accidents or failures, Apergy could face warranty, contract or other litigation claims, which could expose Apergy to substantial liability for personal injury, wrongful death, property damage, loss of oil and natural gas production, and pollution and other environmental damages. Apergy may agree to indemnify its customers against specific risks and liabilities. While Apergy currently maintains insurance protection against some of these risks, and seeks to obtain indemnity agreements from its customers requiring them to hold Apergy harmless from some of these risks, Apergy’s current insurance and contractual indemnity protection may not be sufficient or effective enough to protect it under all circumstances or against all risks. The defense of these lawsuits may require significant expenses and divert management’s attention, and Apergy may be required to pay damages that could adversely affect its business, results of operations, financial condition and cash flows. In addition, the frequency and severity of such incidents could affect insurability and relationships with customers, employees and regulators. In particular, Apergy’s customers may elect not to purchase its products or services if they view its safety record as unacceptable, which could cause Apergy to lose customers and substantial revenues.

Apergy’s customers’ industries are undergoing continuing consolidation that may impact Apergy’s results of operations.

The oil and gas industry is rapidly consolidating and, as a result, some of Apergy’s largest customers have consolidated and are using their size and purchasing power to seek economies of scale and pricing concessions. This consolidation may result in reduced capital spending by some of Apergy’s customers or the acquisition of one or more of Apergy’s primary customers, which may lead to decreased demand for Apergy’s products and services. Apergy cannot assure you that it will be able to maintain its level of sales to a customer that has consolidated or replace that revenue with increased business activity with other customers. As a result, the acquisition of one or more of Apergy’s primary customers may have a significant negative impact on Apergy’s

15

Table of Contents

Index to Financial Statements

business, results of operations, financial condition or cash flows. Apergy is unable to predict what effect consolidations in the industry may have on price, capital spending by its customers, its selling strategies, its competitive position, its ability to retain customers or its ability to negotiate favorable agreements with its customers.

Apergy is subject to information technology, cybersecurity and privacy risks.

Apergy depends on various information technologies throughout its company to store and process information and support its business activities. Apergy also manufactures and sells hardware and software to provide monitoring, controls and optimization of customer critical assets in oil and gas production and distribution. Apergy also provides services to maintain these systems and to enable higher return through their business and technical domain knowledge. Additionally, Apergy’s operations rely upon partners, vendors and other third-party providers of information technology software and services. If these technologies, systems, products or services are damaged, cease to function properly, are breached due to employee error, malfeasance, system errors, or other vulnerabilities, or are subject to cybersecurity attacks, such as those involving unauthorized access, malicious software and/or other intrusions, including by criminals, nation states or insiders, Apergy or its partners, vendors or other third parties could experience production downtimes, operational delays, other detrimental impacts on its operations or ability to provide products and services to its customers, the compromising of confidential, proprietary or otherwise protected information, including personal and customer data, destruction, corruption, or theft of data, security breaches, other manipulation, disruption, misappropriation or improper use of its systems or networks, financial losses from remedial actions, loss of business or potential liability, adverse media coverage, legal claims or legal proceedings, including regulatory investigations and actions, and/or damage to its reputation. While Apergy attempts to mitigate these risks by employing a number of measures, including employee training, technical security controls and maintenance of backup and protective systems, Apergy’s and its partners’, vendors’ and other third-parties’ systems, networks, products and services remain potentially vulnerable to known or unknown cybersecurity attacks and other threats, any of which could have a material adverse effect on Apergy’s business, results of operations, financial condition and cash flows.

Apergy and its customers are subject to extensive environmental and health and safety laws and regulations that may increase Apergy’s costs, limit the demand for Apergy’s products and services or restrict Apergy’s operations. In addition, future regulations, or more stringent enforcement of existing regulations, could increase those costs and liabilities, which could adversely affect Apergy’s results of operations.

Apergy’s operations and the operations of its customers are subject to numerous and complex federal, state, local and foreign laws and regulations relating to the protection of human health, safety and the environment. These laws and regulations affect Apergy’s customers by limiting or curtailing their exploration, drilling and production activities, the products and services Apergy designs, markets and sells and the facilities where Apergy manufactures its products. For example, Apergy’s operations and the operations of its customers are subject to numerous and complex laws and regulations that, among other things: may regulate the management and disposal of hazardous and non-hazardous wastes; may require acquisition of environmental permits related to its operations; may restrict the types, quantities and concentrations of various materials that can be released into the environment; may limit or prohibit operation activities in certain ecologically sensitive and other protected areas; may regulate specific health and safety criteria addressing worker protection; may require compliance with operational and equipment standards; may impose testing, reporting and record-keeping requirements; and may require remedial measures to mitigate pollution from former and ongoing operations. Sanctions for noncompliance with such laws and regulations may include revocation of permits, corrective action orders, administrative or civil penalties, criminal prosecution and the imposition of injunctions to prohibit certain activities or force future compliance.

Some environmental laws and regulations provide for joint and several strict liability for remediation of spills and releases of hazardous substances. In addition, Apergy or its customers may be subject to claims alleging personal injury or property damage as a result of alleged exposure to hazardous substances, as well as

16

Table of Contents

Index to Financial Statements

damage to natural resources. These laws and regulations may expose Apergy or its customers to liability for the conduct of or conditions caused by others, or for Apergy’s acts or for the acts of Apergy’s customers that were in compliance with all applicable laws and regulations at the time such acts were performed. Any of these laws and regulations could result in claims, fines or expenditures that could be material to Apergy’s business, results of operations, financial condition and cash flows.

Environmental laws and regulations, and the interpretation and enforcement thereof, change frequently, and have tended to become more stringent over time. New laws and regulations may have a material adverse effect on Apergy’s customers by limiting or curtailing their exploration, drilling and production activities, which may adversely affect Apergy’s operations by limiting demand for Apergy’s products and services. Additionally, the implementation of new laws and regulations may have a material adverse effect on Apergy’s operating results by requiring Apergy to modify its operations or products or shut down some or all of its facilities.

Apergy is subject to risks relating to existing international operations and expansion into new geographical markets.

Approximately 24%, 26% and 25% of Apergy’s revenues for 2017, 2016 and 2015, respectively, were derived outside the U.S. Apergy continues to focus on penetrating global markets as part of its overall growth strategy and expects sales from outside the U.S. to continue to represent a significant portion of its revenues. Apergy’s international operations and its global expansion strategy are subject to general risks related to such operations, including:

| • | political, social and economic instability and disruptions; |

| • | government export controls, economic sanctions, embargoes or trade restrictions; |

| • | the imposition of duties and tariffs and other trade barriers; |

| • | limitations on ownership and on repatriation or dividend of earnings; |

| • | transportation delays and interruptions; |

| • | labor unrest and current and changing regulatory environments; |

| • | increased compliance costs, including costs associated with disclosure requirements and related due diligence; |

| • | difficulties in staffing and managing multi-national operations; |

| • | limitations on Apergy’s ability to enforce legal rights and remedies; and |

| • | access to or control of networks and confidential information due to local government controls and vulnerability of local networks to cyber risks. |

If Apergy is unable to successfully manage the risks associated with expanding its global business or adequately manage operational risks of its existing international operations, the risks could have a material adverse effect on Apergy’s growth strategy involving expansion into new geographical markets, its reputation, its business, results of operations, financial condition and cash flows.

New tariffs and other trade measures could adversely affect our consolidated results of operations, financial position and cash flows.

Recently, the U.S. government imposed tariffs on steel and aluminum and a broad range of other products imported into the U.S. In response to the tariffs imposed by the U.S. government, the European Union, Canada, Mexico and China have announced tariffs on U.S. goods and services. The new tariffs have increased our manufacturing and material costs and any further trade restrictions, retaliatory trade measures and additional tariffs implemented could result in higher input costs to our products. We may not be able to fully mitigate the

17

Table of Contents

Index to Financial Statements

impact of these increased costs or pass price increases on to our customers. While tariffs and other retaliatory trade measures imposed by other countries on U.S. goods have not yet had a significant impact on our business or results of operations, we cannot predict further developments, and such existing or future tariffs could have a material adverse effect on our consolidated results of operations, financial position and cash flows.

Apergy’s business, profitability and reputation could be adversely affected by domestic and foreign governmental and public policy changes, risks associated with emerging markets, changes in statutory tax rates and laws, including recently enacted U.S. tax reform legislation, and unanticipated outcomes with respect to tax audits.

Apergy’s domestic and international sales and operations are subject to risks associated with changes in laws, regulations and policies (including environmental and employment regulations, export/import laws, tax policies such as export subsidy programs and research and experimentation credits, carbon emission regulations and other similar programs). Failure to comply with any of the foregoing could result in civil and criminal, monetary and non-monetary penalties, as well as damage to Apergy’s reputation. In addition, Apergy cannot provide assurance that its costs of complying with new and evolving regulatory reporting requirements and current or future laws, including environmental protection, employment, data security, data privacy and health and safety laws, will not exceed Apergy’s estimates. In addition, Apergy has made investments in certain countries, including Argentina, Australia, Bahrain, Colombia, Oman and Kenya, and may in the future invest in other countries, any of which may carry high levels of currency, political, compliance, or economic risk. While these risks or the impact of these risks are difficult to predict, any one or more of them could adversely affect Apergy’s business, profitability and reputation.

Apergy is subject to taxation in a number of jurisdictions. Accordingly, Apergy’s effective tax rate is impacted by changes in the mix among earnings in countries with differing statutory tax rates, changes in the valuation allowance of deferred tax assets, disagreements with taxing authorities with respect to the interpretation of tax laws and changes in tax laws. The amount of income taxes and other taxes paid could be adversely impacted by changes in statutory tax rates and laws (which have been and may in the future be under active consideration in various jurisdictions) and are subject to ongoing audits by domestic and international authorities. For example, the U.S. bill commonly referred to as the Tax Cuts and Jobs Act (“Tax Reform Act”), which was enacted on December 22, 2017, significantly changes U.S. tax law by, among other things, imposing a repatriation tax on deemed repatriated earnings of foreign subsidiaries and imposing limitations on the ability to deduct interest expense. If changes in statutory tax rates or laws or audits result in assessments different from amounts estimated, then Apergy’s business, results of operations, financial condition and cash flows may be adversely affected. In addition, changes in tax laws could have an adverse effect on our customers, resulting in lower demand for our products and services.

Failure to attract, retain and develop personnel for key management could have an adverse effect on Apergy’s results of operations, financial condition and cash flows.

Apergy’s growth, profitability and effectiveness in conducting its operations and executing its strategic plans depend in part on its ability to attract, retain and develop qualified personnel, align them with appropriate opportunities for key management positions and support for strategic initiatives. Additionally, during periods of increased investment in the oil and gas industry, competition to hire may increase and the availability of qualified personnel may be reduced. If Apergy is unsuccessful in its efforts to attract and retain qualified personnel, its business, results of operations, financial condition and cash flows could be adversely affected, its market share and competitive position could be adversely affected and/or Apergy could miss opportunities for growth and efficiencies.

The credit risks of Apergy’s customer base could result in losses.

Many of Apergy’s customers are oil and gas companies that have faced or may in the future face liquidity constraints during adverse commodity price environments like the recent industry downturn. These customers

18

Table of Contents

Index to Financial Statements

impact Apergy’s overall exposure to credit risk as they are also affected by prolonged changes in economic and industry conditions. If a significant number of Apergy’s customers experience a prolonged business decline or disruptions, Apergy may incur increased exposure to credit risk and bad debts.

Apergy’s revenue, operating profits and cash flows could be adversely affected if it is unable to protect or obtain patent and other intellectual property rights.

Apergy owns patents, trademarks, licenses and other forms of intellectual property related to its products and continuously invests in research and development that may result in innovations and general intellectual property rights. Apergy employs various measures to develop, maintain and protect its intellectual property rights. These measures may not be effective in capturing intellectual property rights, and they may not prevent Apergy’s intellectual property from being challenged, invalidated, or circumvented, particularly in countries where intellectual property rights are not highly developed or protected. Unauthorized use of Apergy’s intellectual property rights could adversely impact its competitive position and have a negative impact on its business, results of operations, financial condition and cash flows.

Climate change legislation and regulatory initiatives could result in increased compliance costs for Apergy and its customers.

Numerous proposals have been made and are likely to continue to be made at various levels of government to monitor and limit emissions of greenhouse gases (“GHG”). Past sessions of the U.S. Congress considered, but did not enact, legislation to address climate change. The EPA and other federal agencies under the previous administration issued regulations that aim to reduce GHG emissions; however, the current administration has more generally indicated an interest in scaling back or rescinding regulations addressing GHG emissions, including those affecting the U.S. oil and gas industry. It is difficult to predict the extent to which such policies will be implemented or the outcome of any related litigation. Any regulation of GHG emissions could result in increased compliance costs or additional operating restrictions for Apergy or its customers and limit or curtail exploration, drilling and production activities of Apergy’s customers, which could directly or indirectly, through reduced demand for Apergy’s products and services, adversely affect Apergy’s business, results of operations, financial condition and cash flows.

The loss of a significant customer could have an adverse impact on Apergy’s financial results.

Apergy’s customers represent some of the largest operators in the oil and gas drilling and production markets, including major integrated, large independent and foreign national oil and gas companies, as well as oil field equipment and service providers. In 2017, Apergy’s top 10 customers represented approximately 34% of total revenues, and no single customer accounted for more than 10% of Apergy’s revenues. While Apergy is not dependent on any one customer or group of customers, the loss of one or more of Apergy’s significant customers could have an adverse effect on its business, results of operations, financial condition and cash flows.

Apergy’s results may be impacted by current domestic and international economic conditions and uncertainties.

Apergy may be adversely affected by disruptions in the financial markets or declines in economic activity both domestically and internationally in those countries in which it operates. These circumstances will also impact Apergy’s suppliers and customers in various ways which could have an impact on Apergy’s business operations, particularly if global credit markets are not operating efficiently and effectively to support industrial commerce.

Apergy is subject to risk due to the volatility of global energy prices and regulations that impact drilling and production, with overall demand for Apergy’s products and services impacted by depletion rates, global economic conditions and related energy demands.

19

Table of Contents

Index to Financial Statements

Negative changes in worldwide economic and capital market conditions are beyond Apergy’s control, are highly unpredictable and can have an adverse effect on Apergy’s business, results of operations, financial condition, cash flows and cost of capital.

A significant decline in the future economic outlook of Apergy’s business and expected future cash flows could result in goodwill or intangible asset impairment charges, which would negatively impact its results of operations.

Apergy has significant goodwill and intangible assets. The valuation and classification of these assets and the assignment of useful lives involve significant judgments and the use of estimates. The testing of goodwill and intangibles for impairment requires significant use of judgment and assumptions, particularly as it relates to the determination of fair market value. A decrease in the long-term economic outlook and future cash flows of Apergy’s business could significantly impact asset values and potentially result in the impairment of intangible assets, including goodwill. Although fair values currently exceed carrying values for each reporting unit, the value of Apergy’s business was unfavorably impacted by the steep declines in revenue and order rates during 2015 and 2016 as drilling and production activity fell due to unfavorable oil prices and lower U.S. rig counts. Future economic declines could result in charges relating to impairments that could have a material adverse effect on Apergy’s results of operations in future periods.

Apergy’s reputation, ability to do business and results of operations may be impaired by improper conduct by any of its employees, agents or business partners.

While Apergy strives to maintain high standards, Apergy cannot provide assurance that its internal controls and compliance systems will always protect it from acts committed by its employees, agents or business partners that would violate U.S. and/or non-U.S. laws or fail to protect Apergy’s confidential information, including the laws governing payments to government officials, bribery, fraud, anti-kickback and false claims, competition, export and import compliance, money laundering and data privacy, as well as the improper use of proprietary information or social media. Any such violations of law or improper actions could subject Apergy to civil or criminal investigations in the U.S. and in other jurisdictions, could lead to substantial civil or criminal, monetary and non-monetary penalties and related stockholder lawsuits, could lead to increased costs of compliance and could damage Apergy’s reputation, its business, results of operations, financial condition and cash flows.

Apergy’s exposure to exchange rate fluctuations on cross-border transactions and the translation of local currency results into U.S. dollars could negatively impact its results of operations.

A portion of our business is transacted and/or denominated in foreign currencies, and fluctuations in currency exchange rates could have a significant impact on our reported results of operations, financial condition and cash flows, which are presented in U.S. dollars. Cross-border transactions, both with external parties and intercompany relationships, result in increased exposure to foreign exchange effects. Although the impact of foreign currency fluctuations on our results of operations has historically not been material, significant changes in currency exchange rates, principally the Canadian Dollar, Australian Dollar and Colombian Peso, could cause fluctuations in the reported results of Apergy’s business that could negatively affect its results of operations. Additionally, the strengthening of the U.S. dollar potentially exposes Apergy to competitive threats from lower cost producers in other countries and could result in unfavorable translation effects as the results of foreign locations are translated into U.S. dollars for reporting purposes.

Customer requirements and new regulations may increase Apergy’s expenses and impact the availability of certain raw materials, which could adversely affect its revenue and operating profits.

Apergy’s business uses parts or materials that are impacted by the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) requirement for disclosure of the use of “conflict minerals” mined in the Democratic Republic of the Congo and adjoining countries. It is possible that some of Apergy’s

20

Table of Contents

Index to Financial Statements

customers will require “conflict free” metals in products purchased from Apergy. Apergy is in the process of determining the country of origin of certain metals used by its business, as required by the Dodd-Frank Act. The supply chain due diligence and verification of sources may require several years to complete based on the current availability of smelter origin information and the number of vendors. Apergy may not be able to complete the process in the time frame required because of the complexity of its supply chain. Other governmental social responsibility regulations also may impact Apergy’s suppliers, manufacturing operations and operating profits.

The need to find alternative sources for certain raw materials or products because of customer requirements and regulations may impact Apergy’s ability to secure adequate supplies of raw materials or parts, lead to supply shortages, or adversely impact the prices at which its business can procure compliant goods.

Adverse and unusual weather conditions could have an adverse impact on Apergy’s business.

Apergy’s business could be materially and adversely affected by severe weather conditions. Hurricanes, tropical storms, flash floods, blizzards, cold weather and other severe weather conditions could result in evacuation of personnel, curtailment of services, damage to equipment and facilities, interruption in transportation of products and materials, and loss of productivity. For example, certain of Apergy’s manufactured products and components are manufactured at a single facility, and disruptions in operations or damage to any such facilities could reduce Apergy’s ability to produce products and satisfy customer demand. If Apergy’s customers are unable to operate or are required to reduce operations due to severe weather conditions, and as a result curtail purchases of Apergy’s products and services, Apergy’s business could be adversely affected.

Risks Related to the Separation

Apergy may not achieve some or all of the expected benefits of the Separation, and the Separation may adversely affect Apergy’s business.

Apergy may not be able to achieve the full strategic and financial benefits expected to result from the Separation, or such benefits may be delayed or not occur at all. The Separation is expected to provide the following benefits, among others:

| • | The Separation will allow Apergy to more effectively pursue its own distinct operating priorities and strategies, and will enable the management of Apergy to pursue separate opportunities for long-term growth and profitability and to recruit, retain and motivate employees pursuant to compensation policies which are appropriate for their respective lines of business. |

| • | The Separation will permit Apergy to concentrate its financial resources solely on its own operations, providing greater flexibility to invest capital in its business in a time and manner appropriate for its distinct strategy and business needs. |

| • | The Separation will enable investors to evaluate the merits, performance and future prospects of Apergy’s businesses and to invest in Apergy separately based on these distinct characteristics. |

| • | The Separation created an independent equity structure that will afford Apergy direct access to capital markets and will facilitate the ability to capitalize on its unique growth opportunities and effect future acquisitions utilizing, among other types of consideration, shares of its common stock. |