UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number

(Exact name of Registrant as specified in its charter)

|

||

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

|

|

|

|

|

|

|

|

|

|

||

(Address of principal executive offices) |

|

(Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

|

Trading Symbol(s) |

|

Name of each exchange on which registered |

|

|

|

|

* Not for trading, but only in connection with the registration of American Depositary Shares representing such Ordinary Shares pursuant to the requirements of the U.S. Securities and Exchange Commission.

Securities registered pursuant to Section 12(g) of the Act:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

Accelerated filer |

Smaller reporting company |

|

|

|

|

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐ Yes

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 2023, the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $

As of February 29, 2024 the number of outstanding ordinary shares, par value £0.003 per share, of the registrant was

Table of Contents

|

|

|

Page |

|

|

|

|

|

|

|

|

|

|

|

|

Item 1. |

|

5 |

|

|

|

|

|

Item 1A. |

|

35 |

|

|

|

|

|

Item 1B. |

|

84 |

|

|

|

|

|

Item 1C. |

|

84 |

|

|

|

|

|

Item 2. |

|

85 |

|

|

|

|

|

Item 3. |

|

85 |

|

|

|

|

|

Item 4. |

|

86 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 5. |

|

87 |

|

|

|

|

|

Item 6. |

|

87 |

|

|

|

|

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

88 |

|

|

|

|

Item 7A. |

|

98 |

|

|

|

|

|

Item 8. |

|

98 |

|

|

|

|

|

Item 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

99 |

|

|

|

|

Item 9A. |

|

99 |

|

|

|

|

|

Item 9B. |

|

100 |

|

|

|

|

|

Item 9C. |

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

|

100 |

|

|

|

|

|

|

|

|

|

|

|

|

Item 10. |

|

101 |

|

|

|

|

|

Item 11. |

|

106 |

|

|

|

|

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

112 |

|

|

|

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

|

113 |

|

|

|

|

Item 14. |

|

114 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Item 15. |

|

116 |

|

|

|

|

|

Item 16. |

|

119 |

|

|

|

|

|

|

|

||

CERTAIN DEFINITIONS

Unless otherwise indicated and except where the context otherwise requires, references in this Annual Report on Form 10-K (defined below) to:

1

2

GENERAL INFORMATION

In this Annual Report on Form 10‑K (“Annual Report”), “Mereo,” the “Group,” the “Company,” “we,” “us” and “our” refer to Mereo BioPharma Group plc and its consolidated subsidiaries, except where the context otherwise requires. “Mereo,” the Mereo logo and other trademarks, trade names or service marks of Mereo appearing in this Annual Report are the property of Mereo.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements that involve risks and uncertainties, as well as assumptions that, if they never materialize or prove incorrect, could cause our results to differ materially from those expressed or implied by such forward-looking statements. We make such forward-looking statements pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995 and other federal securities laws. All statements other than statements of historical facts contained in this Annual Report are forward-looking statements. In some cases, you can identify forward-looking statements by words such as “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “intend,” “expect” or the negative of these words or other comparable terminology.

Any forward-looking statements in this Annual Report reflect our current views with respect to future events or to our future financial performance and involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by these forward-looking statements. Factors that may cause actual results to differ materially from current expectations include, among other things, those listed under Part I, Item 1A. Risk Factors and elsewhere in this Annual Report. Given these uncertainties, you should not place undue reliance on these forward-looking statements. Except as required by law, we assume no obligation to update or revise these forward-looking statements for any reason, even if new information becomes available in the future.

This Annual Report also contains estimates, projections and other information concerning our industry, our business, and the markets for certain diseases, including data regarding the estimated size of those markets, and the incidence and prevalence of certain medical conditions. Information that is based on estimates, forecasts, projections, market research or similar methodologies is inherently subject to uncertainties and actual events or circumstances may differ materially from events and circumstances reflected in this information. Unless otherwise expressly stated, we obtained this industry, business, market and other data from reports, research surveys, studies and similar data prepared by third parties, industry, medical and general publications, government data and similar sources.

SUMMARY RISK FACTORS

You should carefully consider the risks and uncertainties described below, together with the other information contained in this Annual Report, before making any investment decision. Any of the following risks and uncertainties could have a material adverse effect on our business, prospects, results of operations and financial condition. The market price of our ADSs could decline due to any of these risks and uncertainties, and you could lose all or part of your investment. The risks described below are those that we currently believe may materially affect us. We may face additional risks and uncertainties not currently known to us or that we currently deem to be immaterial.

3

4

Item 1. Business

Overview

We are a biopharmaceutical company focused on the development of innovative therapeutics for rare diseases. We have developed a portfolio of late-stage clinical product candidates. Our two rare disease product candidates are setrusumab for the treatment of osteogenesis imperfecta (OI) and alvelestat primarily for the treatment of severe alpha-1 antitrypsin deficiency-associated lung disease (AATD-LD). Setrusumab has received orphan designation for OI from the European Medicines Agency (EMA) and the U.S. Food and Drug Administration (FDA), PRIME designation from the EMA and has rare pediatric disease designation from the FDA. Alvelestat has received U.S. Orphan Drug Designation for the treatment of AATD and Fast Track designation for the treatment of AATD-LD.

Our strategy is to selectively acquire and develop product candidates for rare diseases that have already received significant investment from large pharmaceutical and biotechnology companies and that have substantial pre-clinical, clinical and manufacturing data packages. Since our formation in March 2015, we have successfully executed on this strategy by acquiring six clinical-stage product candidates of which four were in rare diseases and oncology. Four of our six clinical-stage product candidates were acquired from large pharmaceutical companies and two were acquired in the Merger. We have successfully completed large, randomized Phase 2 clinical trials for four of our product candidates and the Phase 1b portion of a Phase 1b/2 for a fifth product candidate.

Rare diseases represent an attractive development and, in some cases, commercialization opportunity for us since they typically have high unmet medical need and can utilize regulatory pathways that facilitate acceleration to approval and to the potential market. Development of products for rare diseases involve close collaboration with key opinion leaders and investigators, and close coordination with patient organizations. Rare disease patients are typically treated at a limited number of specialized sites which helps identification of the patient population and enables a small, targeted sales infrastructure to commercialize the products in key markets.

Our Strategy

We intend to become a leading biopharmaceutical company developing innovative therapeutics that aim to improve outcomes for patients with rare diseases. The key elements of our strategy to achieve this goal include:

5

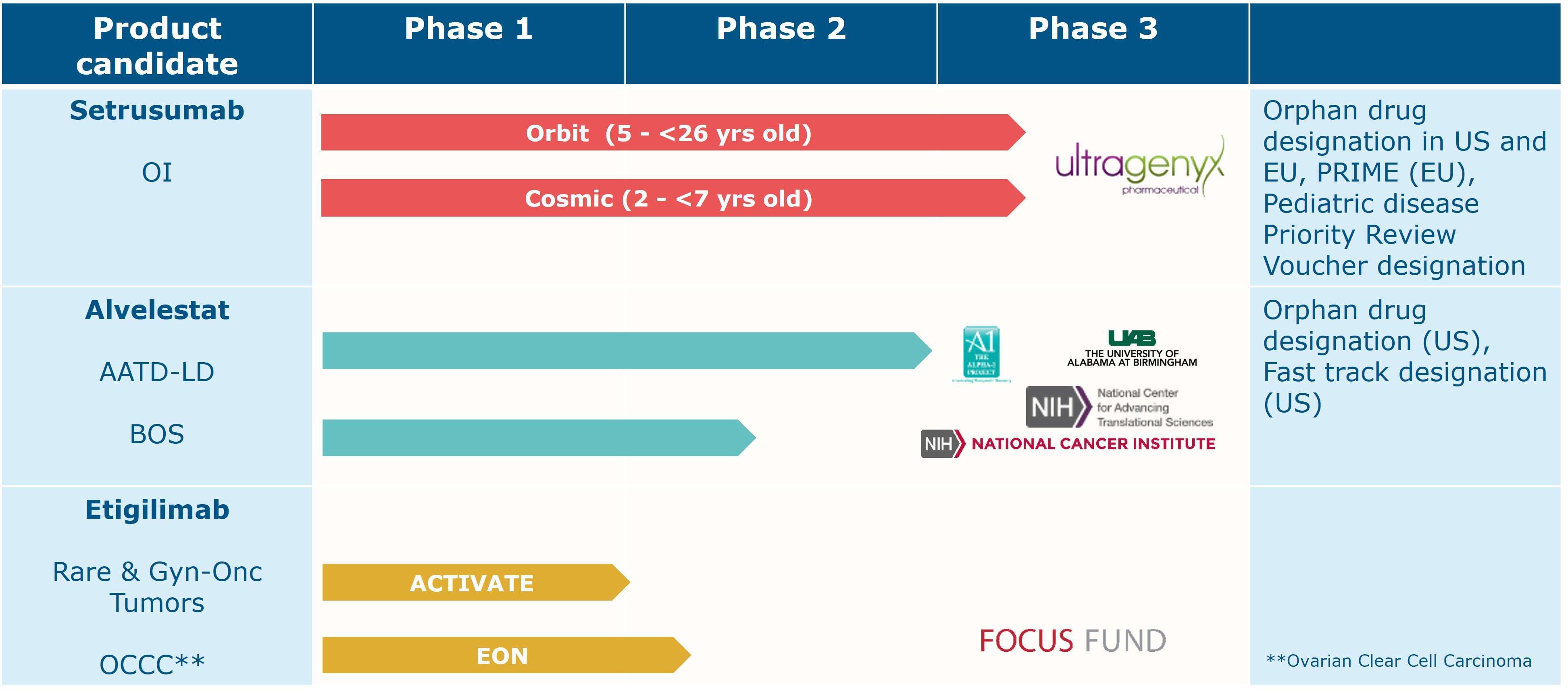

Our Pipeline

The following table summarizes our pipeline for our product candidates. We have global commercial rights to alvelestat, etigilimab and acumapimod and commercial rights to setrusumab in Europe and the U.K. We granted Ultragenyx an exclusive license to develop and commercialize setrusumab in the U.S. and rest of the world, and we have licensed global rights for navicixizumab to Feng Biosciences (formerly OncXerna) and global rights for leflutrozole to ReproNovo.

Core Rare Disease Product Candidates

Setrusumab (BPS-804/UX143) for the Treatment of Osteogenesis Imperfecta

Overview

In collaboration with Ultragenyx, we are developing setrusumab for the treatment of OI, a rare genetic disease, which is caused by variants in the COL1A1 or COL1A2 genes, which results in bones that can break easily and is commonly known as brittle bone disease. Setrusumab is a novel, intravenously administered antibody that is designed to inhibit sclerostin, a protein that inhibits the activity of bone-forming cells, known as osteoblasts. We believe that by blocking sclerostin, setrusumab has the potential to induce or increase osteoblast function and maturation of these cells, and to inhibit bone-resorption through osteoclasts, increasing overall bone mass and thereby reducing fractures in OI patients.

Background of Osteogenesis Imperfecta

OI is a genetic disorder characterized by fragile bones and reduced bone mass, resulting in bones that break easily, loose joints and weakened teeth. In severe cases, patients may experience hundreds of fractures in a lifetime. In addition, people with OI often suffer from muscle weakness, early hearing loss, fatigue, curved bones, scoliosis (curved spine), brittle teeth, respiratory problems and short stature. The disease can be extremely debilitating and even fatal in newborn infants with a severe form of the disease. OI is a rare condition that affects an estimated 60,000 people in the U.S. and Europe, according to estimates by Orphanet.

There are eight recognized forms of OI, designated type I through type VIII. Type I is cited to be the least severe form, although patients can still have many fractures and other physical manifestations of the disease, while Type II is the most severe and frequently causes death at or shortly after birth. OI Type I is the most prevalent and estimated to occur in approximately 50% to 60% of OI patients. Type III and Type IV patients may be wheelchair bound and typically have many fractures through their lifetime. Type III and Type IV patients may also have short stature, scoliosis and hearing loss by the time they are young adults. OI is typically diagnosed at birth with most patients being born with a blue or gray tint to the sclera, the part of the eye that is usually white.

6

Current Treatment Landscape for Osteogenesis Imperfecta

There are no therapies approved by the FDA or EMA for the treatment of OI. The only treatments available to OI patients are the acute management of fractures as they occur and drugs such as bisphosphonates which are typically used to treat osteoporosis and are not approved for OI but are commonly used off-label in children. Bisphosphonates slow down the rate at which osteoclasts resorb bone. These anti-resorptives include Aredia (pamidronate), Fosamax (alendronate) and Reclast (zoledronic acid). Bisphosphonates have not consistently been shown to reduce fractures in OI adult patients and the effect of long-term therapy with these drugs remains unclear in both adults and children.

Current treatment of OI is directed towards management of fractures with casting or surgical fixation. Following either of these, physical therapy will often be required. Preventative surgeries, such as intramedullary, or in-bone, rodding fixation are also undertaken. Supportive care for the disease involves surgery to correct deformities, internal splinting of bones with metal rods, bracing to support weak limbs and decrease pain, physical therapy and muscle strengthening and aerobic conditioning to improve bone mass and strength.

Our Approach

Our product for treating OI is setrusumab, a fully human monoclonal antibody that is designed to inhibit sclerostin. Sclerostin is produced in osteocytes, which are mature bone cells that are thought to be the mechanoreceptor cells that regulate the activity of bone-building osteoblasts and bone-resorbing osteoclasts. Sclerostin inhibits the activity of osteoblasts. We believe that by blocking sclerostin, setrusumab has the potential to induce or increase osteoblast activity and maturation of these cells, increasing overall bone mass, and thereby reducing fractures in OI patients.

In 2016, we obtained orphan drug designation in OI for setrusumab in the U.S. and the EU and, in November 2017, the program was accepted into the Priority Medicines scheme (“PRIME”) of the EMA. In September 2020 we received rare pediatric disease designation for setrusumab in OI from the FDA. See “—Government Regulation—Foreign Government Regulation.”

Clinical Development of Setrusumab

Prior to our acquisition of setrusumab, Novartis conducted four clinical trials in 106 patients and healthy volunteers. In 2019 we completed a Phase 2b dose-finding study (ASTEROID) study of setrusumab in 112 adult patients with Type I, III and IV OI. Following the 12-month dosing part of the trial, patients were followed for a further twelve months to examine the off-effects of setrusumab. The results of this Phase 2b trial supported the progression of setrusumab into a pivotal study in OI. Setrusumab was safe and well-tolerated in the study. There were no cardiac-related safety concerns observed in the study.

Top-line Data from Setrusumab Phase 2 Portion of Phase 2/3 Orbit Study

In June 2023, we along with our partner, Ultragenyx, announced successful completion of the Phase 2 portion of the pivotal Phase 2/3 Orbit study in 24 pediatric and young adult patients (5 to <26 years old) for setrusumab in OI, which compared two different doses of setrusumab, 20 and 40 mg/kg, to determine the optimal dose for the Phase 3. The primary endpoint of the Phase 2 study was circulating levels of P1NP, a biomarker reflective of bone formation. The study also evaluated numerous other endpoints, including bone mineral density (“BMD”) and annualized fracture rates, PK and safety. Across all patients evaluated at both doses, these data showed statistically significant increases in levels of serum P1NP, a sensitive marker of bone formation, and substantial and significant improvement in BMD by three months. An increase in lumbar spine BMD from baseline of 9.4% at 20 mg/kg (n=10) was observed, with a substantial mean change in the Z-score of +0.65 from -2.12 (n=11) at baseline. There was no significant difference between the two doses tested, accordingly, the 20 mg/kg was selected as the Phase 3 dose. The changes observed in BMD in these younger patients at 3 months are equivalent to the changes following 12 months treatment with setrusumab in adult patients reported from the Phase 2b ASTEROID study. The 24 patients from the Phase 2 portion of the ORBIT study are continuing to receive setrusumab treatment in an open-label extension study.

Additional data from the Phase 2 portion of the Phase 2/3 Orbit study were reported at the annual ASBMR meeting in October 2023 and demonstrated that treatment with setrusumab significantly reduced incidence of fractures in patients with OI with at least 6 months of follow-up and continued to demonstrate ongoing and meaningful improvements in lumbar spine bone BMD. As of the cut-off date and following at least six months of treatment with setrusumab, the annualized fracture rate across all 24 patients in the Phase 2 portion of the study was reduced by 67%. The median annualized fracture rate of 0.72 in the two years prior to treatment was reduced to 0.00 (n=24, p=0.042) during the mean treatment duration period of nine months. These fractures excluded fractures of the fingers, toes, skull and face consistent with the Phase 3 study design. In the two years prior to treatment with setrusumab all patients experienced at least one fracture. Following initiation of treatment with setrusumab, 20 patients experienced no radiographic-confirmed fractures, and 4 patients experienced 7 radiographic-confirmed fractures in 5 separate events. Two of these fractures occurred within the first two months of treatment, a time in which setrusumab-induced increases in BMD may have been suboptimal in reducing fractures.

7

At the six-month timepoint, treatment with setrusumab resulted in a mean increase in lumbar spine BMD from baseline of 13% at 20 mg/kg (n=11) and 16% at 40 mg/kg (n=8), which represented the same substantial mean improvement in Z-score of +0.85 for both dose groups at 6 months compared to a combined mean baseline Z-score of –1.68. The small apparent difference in BMD change from baseline is likely related to differences in patients assigned to the two treated groups. There was no statistically significant difference in BMD percent change or Z-score change from baseline between the 20 and 40 mg/kg dosing cohorts. As of the data cut-off for our October 2023 announcement, there were no treatment-related serious adverse events observed in the study.

The 24 patients from the Phase 2 portion of the Orbit study are continuing to receive setrusumab treatment at 20 mg/kg in an open label extension study. Additional longer-term Phase 2 data from the Orbit study are expected in the second half of 2024.

Phase 3 Orbit and Cosmic Studies

The Phase 3 portion of the Orbit study is enrolling approximately 150 patients (aged 5 - <26 years old) at 50 sites across 12 countries and is expected to complete enrollment around the end of the first quarter of 2024. Patients are randomized 2:1 to receive setrusumab (20 mg/kg) or placebo, respectively, with a primary efficacy endpoint of a reduction in annualized clinical fracture rate, excluding fingers, toes, skull and face.

A second study, Cosmic, a Phase 3 open-label study in younger children (aged 2 - < 7 years old) is enrolling approximately 60 patients, with enrollment expected to complete around the end of the first quarter of 2024. The Cosmic study is an active-controlled study evaluating the effect of setrusumab compared to intravenous bisphosphonates (IV-BP) therapy (randomized 1:1) on annualized total fracture rate.

We believe the Orbit and Cosmic trials, if successful, will support U.S. and European regulatory filings for the potential approval of setrusumab for the treatment of osteogenesis imperfecta.

Alvelestat (MPH-966) for the Treatment of Severe Alpha-1 Antitrypsin Deficiency (AATD)-Associated Lung Disease:

Overview

We are developing alvelestat for the treatment of severe AATD-associated Lung Disease (AATD-LD). AATD-LD is a potentially life-threatening rare, genetic condition that results in severe debilitating diseases, including early-onset pulmonary emphysema. Alvelestat is a novel, oral small molecule designed to inhibit neutrophil elastase (NE). Scientific data indicate that the increased risk of lung tissue injury in patient with AATD may be due to inadequately controlled NE caused by insufficient alpha-1 antitrypsin (AAT). We believe that by inhibiting NE, alvelestat has the potential to reduce the destruction of lung tissue and stabilize clinical deterioration in patients with severe AATD-LD patients.

Background of Alpha-1-Antitrypsin Deficiency

AATD is a genetic disease. There are estimated to be 50,000 people in North America and 60,000 in Europe with severe AATD, which we define as AATD in patients with serum AAT levels <11mM, (most commonly either a PiZZ genotype or Null/Null genotype). although there are approximately only 10,000 people diagnosed in North America. The major function of AAT in the lungs is to protect the connective tissue from NE released from triggered neutrophils. The lungs are normally defended from NE attack by AAT, which is a highly effective inhibitor of NE. Severe AATD patients produce ineffective or no AAT and are, therefore, unable to defend against NE attack. As a result, severe AATD patients commonly experience degeneration of lung function, such as early-onset pulmonary emphysema, which significantly affects quality of life and life expectancy. They may require oxygen therapy in order to continue their daily lives and the most severe patients may require lung transplantation.

AATD is the result of a mutation of the SERPINA1 gene. Most people with severe AATD inherit two copies of the defective PiZ allele, or gene variant, of the SERPINA1 gene, resulting in a PiZZ genotype. Patients with a PiZZ genotype have approximately 15% of normal AAT levels. Individuals who inherit two copies of the Null allele, resulting in a Null/Null genotype, do not produce any AAT. These two groups are at very high risk of developing lung disease. AATD patients with the PiZZ genotype experience loss of lung tissue as measured by lung density on computed tomographic (CT) scanning, a decline in FEV1, a standard measure of exhalation and poor quality of life. Respiratory disease can progress to need for chronic oxygen therapy, lung transplant and death. The annual mortality rate in this genotype estimated to be 4%. Given that individuals with the Null/Null genotype do not produce any AAT, we believe that they are likely to experience an even greater annual decline in FEV1.

Current Treatment Landscape for Alpha-1 Antitrypsin Deficiency

AATD patients are monitored by pulmonary functions tests, including spirometry. Treatment involves bronchodilators and inhaled corticosteroid medications and pulmonary rehabilitation, with increased intensity of therapy guided by disease severity. Surgical options include lung volume reduction surgery and lung transplantation. Both are highly invasive, and transplantation is only an option for a portion of patients with end-stage disease despite optimal therapy.

8

Augmentation therapy is available for AATD, using a partially purified plasma preparation highly enriched for AAT that is administered weekly by intravenous infusion. This therapy was first approved by the FDA in the 1980s based on its biochemical efficacy, meaning its ability to raise blood levels of AAT, but not based on clinical outcome data. Several observational studies have suggested that AAT augmentation therapy may slow the rate of decline in lung function in a subgroup of AATD patients with moderate-to-severe airflow obstruction, but not for those with earlier stages of lung disease. In a randomized, controlled trial of augmentation therapy, patients had some reduction in the progression of emphysema, as assessed by measuring lung density using computed tomography. The study did not show significant slowing in the decline in FEV1.

We believe that current therapies for AATD are inadequate. Surgical options are limited to a few patients, are highly invasive, have variable results, and do not address the underlying pathology of AATD. AAT augmentation therapy, while FDA approved, was not approved on the basis of clinical outcome data. Benefit has not been demonstrated in patients with earlier stages of lung disease where there is an unmet need to reduce progression of irreversible lung tissue loss. In Europe Regulatory approval was on efficacy based on slowing of CT density decline, without effects on other measures such as FEV1 or patient-reported outcomes. Further, AAT augmentation therapy is generally not reimbursed and thus is not currently available to patients in several jurisdictions, including some key European markets. In addition, AAT augmentation therapy requires potentially inconvenient weekly intravenous infusions.

Our Approach

Our product candidate for treating severe AATD is alvelestat, a potent, specific oral small molecule that is designed to inhibit NE. We believe that by inhibiting NE, alvelestat has the potential to reduce the enzymatic destruction of lung tissue. Furthermore, we believe that convenient oral dosing of alvelestat could provide a significant advantage compared to the current treatments for AATD of surgery or weekly intravenous AAT augmentation therapy. Alvelestat is not being investigated for treatment of the hepatic disease which is due to the damaging effect of accumulated abnormal ZZ protein in the liver, rather than the protein deficiency. Liver disease occurs in approximately 10% cases of severe AATD, predominantly in children.

Alvelestat has received U.S. Orphan Drug Designation for the treatment of AATD and Fast Track designation in AATD-LD.

Clinical Development of Alvelestat

Prior to our license of alvelestat, AstraZeneca conducted 12 clinical trials involving 1,776 subjects, including trials in COPD, bronchiectasis and cystic fibrosis. Although these trials were conducted in diseases other than AATD, we believe the data demonstrated potential clinical benefit and biomarker evidence of treatment effect for AATD patients. These trials created a safety database of 1,149 subjects treated with alvelestat.

Phase 2 Clinical Trials in AATD

In May 2022, we successfully completed a Phase 2, placebo-controlled, 12-week, dose-ranging, proof-of-concept clinical trial (ASTRAEUS) in 99 patients with AATD-LD in the U.S and the EU which demonstrated statistically significant changes in neutrophil elastase activity and biomarkers of disease severity at different time points up to 12 weeks. We enrolled only adult patients with PiZZ or Null/Null genotypes or rare genotypes with severe deficiency of alpha-1 antitrypsin (<11 microMolar) with confirmed emphysema, who had not received AAT augmentation therapy or had undergone a wash-out period following AAT augmentation therapy. The study examined two doses of alvelestat (120 mg and 240 mg) compared to placebo with three primary endpoints along the pathogenic pathway of lung disease in AATD patients. These primary endpoints were plasma desmosine (a biomarker of protease-driven elastin breakdown), Aα-Val360, a specific biomarker of NE proteolytic activity, and neutrophil elastase activity in blood. Secondary endpoints were safety, exacerbation frequency, and pharmacokinetics. Exploratory endpoints were St. Georges Respiratory Questionnaire (SGRQ) which is a patient-reported outcome of Respiratory Health Status and lung function tests, including FEV1.

We subsequently announced additional Phase 2 data from this study in October 2022 demonstrating the association of biomarker responders in alvelestat-treated patients to improvement in the activity domain of the St George’s Respiratory Questionnaire, but not in patients treated with placebo.

No new safety signals were detected in patients with AATD-LD compared to the previous studies conducted by AstraZeneca. The most frequent adverse event was headache which was more frequently observed at the higher doses of alvelestat (120 mg and 240 mg) used in AATD-LD than at the lower doses used in previous studies in COPD, bronchiectasis and cystic fibrosis. There was evidence of tolerance to headache being induced, and we intend to use a dose-escalation regime for initiation of treatment in future trials. Monitoring for Adverse Events of Special Interest (AESIs) documented a single treatment-emergent adverse event (TEAE) of liver function abnormality (raised hepatic transaminases, without meeting Hy’s Law) and one AESI of prolonged QTc, in which study-drug stopping criteria were met were reported in the ASTRAEUS trial. Both events fully resolved on study drug cessation.

9

In October 2023, the University of Alabama at Birmingham (UAB) and Mereo reported on the ATALANTa study, a multi-center, double-blind, placebo-controlled, proof-of-concept investigator-led study run by Professor Mark Dransfield, Director of the Division of Pulmonary, Allergy and Critical Care, UAB, in collaboration with Mereo. ATALANTa investigated the safety and efficacy of alvelestat 120 mg, or matched placebo, twice daily, for 12 weeks in a broad range of individuals with AATD-LD, including those with less severe phenotypes (Pi*SZ) and earlier stage patients than were enrolled in the Company-sponsored ASTRAEUS Phase 2 study, and those receiving augmentation therapy. The study randomized 63 patients, 32 in the 120 mg alvelestat arm (44% on augmentation therapy) and 31 in the placebo arm (48% on augmentation therapy). The results demonstrated with the 120 mg dose of alvelestat (the lower dose used in the Phase 2 ASTRAEUS study) are consistent with those observed in ASTRAEUS on blood neutrophil elastase activity and changes in the disease-activity biomarkers, desmosine and Aα-val360. The data demonstrate that the 120 mg dose of alvelestat is safe on top of augmentation and support Mereo’s selection of the 240 mg dose to be studied in the planned Phase 3 pivotal trial. Exploratory endpoints in ATALANTa demonstrated statistically significant improvement in SGRQ Activity score (p=0.0106 versus placebo) and a trend to improvement in SGRQ Total score at 12 weeks in patients not receiving augmentation therapy and having earlier stage lung disease (based on their FEV1). The ATALANTa and ASTRAEUS data support the use of the SGRQ Total score in the planed Phase 3 pivotal trial and inclusion of patients with earlier stages of lung disease. Safety in ATALANTa was consistent with the known alvelestat profile and there were no liver or QTc AESIs documented.

Planned Phase 3 Clinical Trial in AATD

In March 2023, we announced the outcome of the end-of-Phase 2 discussions with the FDA and the EMA (Scientific Advice) and the guidance on the Phase 3 endpoints received from both Regulatory Agencies. In the EU, the Company received guidance that lung density by computed tomography (CT) scan with a relaxed p value (p<0.1) may be sufficient for full regulatory approval. In the U.S., following additional FDA interactions in the second half of 2023, the Company has aligned on St George’s Respiratory questionnaire Total score as the primary endpoint, with a functional assessment as a key secondary endpoint, which, if successful, is expected to support submissions for full regulatory approval in the U.S. Inclusion of patients with earlier and later stage lung disease progression in the planned registrational study could increase the addressable patient population for alvelestat. Based on the guidance from the FDA and the EMA, the Company is designing a single, global, Phase 3 study evaluating the 240 mg dose of alvelestat versus placebo in approximately 220 patients with AATD-LD with two independent primary endpoints to support applications for full marketing approvals in both the U.S. and EU.

The Company continues to evaluate non-dilutive financing options for the development and potential commercialization of alvelestat in AATD-LD while continuing to progress the program to maintain the planned Phase 3 timelines.

Phase 1b/2 Clinical Trial in Bronchiolitis Obliterans Syndrome (“BOS”)

BOS is a rare progressive, fibrosing disease of the lungs affecting approximately 6% of the estimated 12,000 stem cell transplants a year in the U.S., often as part of graft versus host disease. For lung transplants, approximately 50% of the patients develop BOS by 5 years, which is the leading cause of retransplant and mortality. There are an estimated 10,000 people living with lung transplant and BOS in the U.S. and Europe. BOS is characterized by neutrophil infiltration in the lung, excess neutrophil elastase and inflammation. The pathology of BOS in stem cell transplant and lung transplant is overlapping.

As BOS is driven by elevated neutrophils in the lung and excess NE activity, leading to lung damage through elastin breakdown in the tissue and progressive fibrosis, and ultimately respiratory failure we believe our approach using alvelestat to inhibit NE has significant advantages. By inhibiting NE, we believe alvelestat will reduce the accelerating effects of NE-driven inflammation on BOS leading to increased success rate of SCT and lung transplant. The investigator-led clinical program is designed to generate data on clinical endpoints that would potentially support registration and reimbursement in SCT.

An investigator-sponsored open-label Phase1b/2 study in Bronchiolitis Obliterans Syndrome (BOS) following allogeneic stem cell transplant is being conducted. The study uses within patient dose escalation from 60 mg BID up to 240 mg BID, over the initial 8 weeks of study, with treatment continued for up to 6 months. Interim results from 7 patients enrolled in the Phase 1b study were reported in December 2021 showing stabilization or improvement in lung function measured by Forced Expiratory Volume in 1 second, (FEV1) in 6 of 7 patients, and supportive biomarker responses. Evaluation of the clinical and safety data from 10 patients in the Phase 1b supported the dose to be progressed and expansion into the Phase 2 portion of the study which was initiated in the second half of 2022. No safety signals have been detected in this study.

Etigilimab (MPH-313) for the Treatment of Advanced Solid Tumors

Overview

10

Etigilimab is an antibody against TIGIT (T-cell immunoreceptor with Ig and ITIM domains). TIGIT is a next generation checkpoint receptor shown to block T-cell activation and the body’s natural anti-cancer immune response. Etigilimab is an IgG1 monoclonal antibody which binds to the human TIGIT receptor on immune cells with a goal of improving the activation and effectiveness of T-cell and NK cell anti-tumor activity.

We acquired etigilimab in the Merger with Mereo BioPharma 5 (formerly OncoMed Pharmaceuticals, Inc.) in 2019.

Clinical Development of Etigilimab

Our oncology product candidate, etigilimab (an anti-TIGIT antibody), has completed a Phase 1a dose escalation clinical trial in 23 patients with advanced solid tumors and has been evaluated in a Phase 1b study in combination with nivolumab in select tumor types.

In 2023, we completed the Phase 1b portion of an open label Phase1b/2 basket study (the ACTIVATE study) evaluating etigilimab in combination with nivolumab in three rare tumors, two specific subtypes of soft-tissue sarcomas, uveal melanoma and testicular germ cell cancer, three gynecological carcinomas, cervical, endometrial and ovarian carcinomas and any solid tumor with high mutation burden, all in the recurrent/metastatic setting.

The Phase 1b portion of the ACTIVATE study enrolled 76 patients in total. Data from this study were presented at several major medical conferences (ASCO, 2022; ESMO, 2023). The trial evaluated objective response rate as a primary endpoint and safety, duration of response, pharmacokinetics, anti-drug antibodies, progression-free disease and other endpoints as secondary endpoints. Objective responses were reported for patients with gynecological cancers, rare tumors, and soft-tissue sarcoma with 7 patients remaining on study for at least 335 days. The combination of etigilimab and nivolumab was generally well tolerated with a safety profile qualitatively similar to that of nivolumab alone. The main drug-related safety findings included rash, pruritis, fatigue and headache and the number of Grade 3 events was seven. No Grade 4 or Grade 5 events were reported. Additionally, we have found several intratumoral biomarkers (PVR, TIGIT, and CD226+/CD8 T cells) that, with further testing, might be predictive of response to treatment. At this time, the Company has no plans to conduct and directly fund further clinical studies of etigilimab.

In April 2021, the Company entered into partnership with Cancer Focus Fund for a Phase 1b/2 study of etigilimab in Clear Cell Ovarian Cancer to be conducted at The University of Texas MD Anderson Cancer Center. The Phase 1b/2 study is being financed by Cancer Focus Fund. Clear cell ovarian cancer is a rare cancer that accounts for approximately 5 to 10% of all ovarian carcinomas in North America. Enrollment is continuing in this investigator-led Phase 1b/2 study of etigilimab plus nivolumab (the EON study) and based on encouraging data from the first 10 patients enrolled, the study has been expanded to enroll an additional 10 patients in the Phase 2 portion of the study.

Our Non-Core Partnered Programs

Following completion of successful Phase 1b or Phase 2 studies the products below are programs which we have successfully partnered.

Navicixizumab (OMP-305B83) for Treatment of Ovarian Cancer

Navicixizumab (“Navi”) is a bispecific antibody that inhibits delta-like ligand 4 (DLL4) and vascular endothelial growth factor (VEGF).

We acquired Navi in the Merger. In January 2020, we out-licensed Navi to Feng Biosciences (formerly OncXerna). See “- Material Agreements-Licensing Agreement for Navicixizumab.” In addition, Navi is the subject of the CVR Agreement which sets forth certain rights and obligations of us with respect to Navi. See “—Material Agreements—CVR Agreement Between Us and Computershare—The NAVI Milestones.”

Leflutrozole (BGS-649)

Leflutrozole is an oral inhibitor of aromatase. Excess aromatase in fat tissue reduces testosterone, LH and FSH, leading to HH. In Phase 2 trials, leflutrozole normalized testosterone, increased LH and FSH, improved total sperm count, and was reported to be well-tolerated.

In December 2023, we entered into an exclusive global license agreement with ReproNovo for the development and commercialization of leflutrozole, a non-steroidal aromatase inhibitor. See "—Material Agreements—Licensing Agreement for Leflutrozole". Under the terms of the License Agreement, ReproNovo, a reproductive medicine company, is responsible for all future development and commercialization of leflutrozole. Mereo received an upfront payment and will be eligible to receive up to $64.3

11

million in future clinical, regulatory and commercial milestones as well as tiered mid-single digit royalties on global annual net sales of leflutrozole.

Our Non-Core Programs Available for Partnering

Following completion of a successful Phase 2 study, we intend to out-license or sell the following program.

Acumapimod (BCT-197) for the Treatment of AECOPD

Acumapimod is a p38 MAP kinase inhibitor therapy for treatment during severe acute exacerbations of COPD (AECOPD). In a Phase 2 trial, acumapimod given over 5 days in patients hospitalized with AECOPD demonstrated a statistically significant reduction in re-hospitalization for treatment failure and recurrent exacerbations. Acumapimod was reported to be safe and well tolerated. Following meetings with FDA and EMA a global Phase 3 registrational program has been designed.

We intend to out-license or sell acumapimod to third parties for the further development of acumapimod recognizing the need for greater resources to take this product candidate to market.

Material Agreements

Licensing Agreement with Ultragenyx for setrusumab

On December 17, 2020, we announced that we entered into a license and collaboration agreement with Ultragenyx, for setrusumab for OI. Under the terms of the agreement, Ultragenyx will lead future global development of setrusumab in both pediatric and adult patients. We granted Ultragenyx an exclusive license to develop and commercialize setrusumab in the U.S. and rest of the world, excluding Europe, where we retain commercial rights. Each party will be responsible for post-marketing commitments in their respective territories. Under the terms of the agreement, Ultragenyx made an upfront payment of $50 million to Mereo and a $9.0 million payment during the year ended December 31, 2023 upon achievement of a clinical milestone. Ultragenyx will pay up to $254 million in additional development, regulatory and commercial milestones and tiered double digit percentage royalties to us on net sales outside of Europe and we will pay a fixed double digit percentage royalty to Ultragenyx on net sales in Europe. Under the terms of our 2015 agreement with Novartis, we will pay Novartis a percentage of proceeds, subject to certain deductions, and we will receive a substantial majority of the payments from Ultragenyx.

Licensing Agreement with AstraZeneca

In October 2017, we announced that we entered into an exclusive license and option agreement (the “License Agreement”), to obtain from AstraZeneca an exclusive worldwide, sub-licensable license under AstraZeneca’s intellectual property rights relating to certain product candidates containing a NE inhibitor, including product candidates that contain alvelestat, with an option to acquire such intellectual property rights following commencement of a pivotal trial and payment of related milestone payments (the “Option”), together with the acquisition of certain related assets.

Upon entering into the License Agreement, we made a payment of $3.0 million and issued 490,798 ordinary shares to AstraZeneca, for an aggregate upfront payment equal to $5.0 million. In connection with certain development and regulatory milestones, we have agreed to make payments of up to $115.5 million in the aggregate and issue additional ordinary shares (or ADS equivalent) to AstraZeneca for licensed product candidates containing alvelestat. In addition, we have agreed to make payments to AstraZeneca based on specified commercial milestones of the product candidate. In the event that we sub-license alvelestat, we have also agreed to pay a specified percentage of sublicensing revenue to AstraZeneca. Otherwise, we have agreed to make royalty payments to AstraZeneca equal to ascending specified percentages of tiered annual worldwide net sales by us or our affiliates of licensed product candidates (subject to certain reductions), ranging from the high single digits to low double digits. Royalties will be payable on a licensed product-by-licensed product and country-by-country basis until the later of ten years after the first commercial sale of such licensed product in such country and expiration of the last patent covering such licensed product in such country that would be sufficient to prevent generic entry. Under the License Agreement, we may freely grant sub-licenses to affiliates upon notice to AstraZeneca and we must obtain AstraZeneca’s consent, not be unreasonably withheld, to grant sub-licenses to a third party. We have agreed to use commercially reasonable efforts to develop and commercialize at least one licensed product. In addition, we are generally responsible for costs related to the development and commercialization of the licensed products under the License Agreement.

The License Agreement will expire on the expiry of the last-to-expire royalty term with respect to all licensed product candidates. Upon the expiration of the royalty term for a licensed product in a particular country, the licenses to us for such product in such country will become fully paid and irrevocable. Prior to exercise of the Option, if at all, we may terminate the License

12

Agreement upon prior written notice. Either party may terminate the agreement upon prior written notice for the other party’s material breach that remains uncured for a specified period of time or insolvency. AstraZeneca agreed not to assert any AstraZeneca intellectual property rights that were included in the scope of the License Agreement against us.

Licensing Agreement for Navicixizumab

On January 13, 2020, we entered into a global license agreement with Feng Biosciences (formerly OncXerna) for the development and commercialization of navicixizumab, an anti-DLL4/VEGF bispecific antibody, which, at the time, was being evaluated in a Phase 1b study in combination with paclitaxel in patients with advanced heavily pretreated ovarian cancer. Navicixizumab previously completed a Phase 1a monotherapy study in patients with various types of refractory solid tumors and is one of two product candidates we acquired through the Merger.

Under the terms of the license agreement, Feng Biosciences received an exclusive worldwide license to develop and commercialize Navi. We received an upfront payment of $4.0 million and in February 2022 we received an additional payment of $2.0 million, following satisfaction of a milestone. Feng Biosciences will be responsible for all future research, development and commercialization of Navi. Additionally, we will be eligible to receive up to $300 million in future clinical, regulatory and commercial milestones, tiered royalties ranging from the mid-single-digit to sub-teen percentages on global annual net sales of Navi, as well as a negotiated percentage of sublicensing revenues from certain sublicensees.

As a consequence of the license agreement with Feng Biosciences, and in accordance with the terms and conditions of the CVR Agreement, holders of CVRs pursuant to the CVR Agreement will be entitled to receive certain eligible cash milestone payments made to us under the license agreement relating to the development and commercialization of Navi. See “—CVR Agreement Between Us and Computershare.”

In February 2022, we received a milestone payment of $2.0 million (£1.5 million) under the Navi License Agreement with Feng Biosciences. An associated payment was made to the former shareholders of Mereo BioPharma 5, Inc. under the CVR Agreement of a total of $0.9 million (£0.7 million), after deductions of costs, charges and expenditures.

In the fourth quarter of 2023, Feng Biosciences completed a restructuring, recapitalization and closed on a refinancing. Feng Biosciences is a clinical stage therapeutics company advancing precision medicine for people with cancer. The company will continue to utilize its XernaTM platform to progress navicixizumab.

Licensing Agreement for Leflutrozole

In December 2023, we entered into an exclusive global license agreement with ReproNovo for the development and commercialization of leflutrozole, a non-steroidal aromatase inhibitor. Under the terms of the License Agreement, ReproNovo, a reproductive medicine company, is responsible for all future development and commercialization of leflutrozole. Mereo received an upfront payment and will be eligible to receive up to $64.3 million in future clinical, regulatory and commercial milestones as well as tiered mid-single digit royalties on global annual net sales of leflutrozole.

CVR Agreement Between Us and Computershare

Following the closing of the Merger, OncoMed’s stockholders received, in exchange for each outstanding share of OncoMed common stock owned immediately prior to the closing of the Merger (except for any dissenting shares): (1) a number of our ADSs determined by reference to an exchange ratio, and (2) one CVR, representing the right to receive contingent payments if specified milestones are achieved within agreed time periods, subject to and in accordance with the terms and conditions of the Contingent Value Rights Agreement (the Mereo “CVR Agreement”), dated April 23, 2019, by and among Computershare, as rights agent, and us.

Except in limited circumstances, the CVRs may not be transferred, pledged, hypothecated, encumbered, assigned or otherwise disposed of.

Milestone Events and Payments

The CVR milestones relate to Mereo BioPharma 5 (formerly OncoMed)’s etigilimab and navicixizumab product candidates, though the milestone relevant to etigilimab can no longer be achieved and no payments will become due or payable to CVR holders in relation to etigilimab.

The contingent payments would become payable to the rights agent, for subsequent distribution to the holders of the CVRs, upon the achievement of a milestone relating to NAVI. If a milestone relating to NAVI occurs at any time prior to the fifth anniversary of the closing of the Merger, being April 23, 2024, and on each such occurrence, then, thirty days following the achievement thereof,

13

we are obligated to notify the rights agent and pay the amounts owed pursuant to the NAVI Agreement (as defined in the CVR Agreement).

The NAVI Milestones

The receipt of the upfront milestone payment of $4.0 million by us under the Navi License Agreement with Feng Biosciences (formerly OncXerna) in January 2020 resulted in a payment to CVR holders of approximately 1.2 cents per CVR, a total of approximately $0.5 million, after deductions of costs, charges and expenditures.

The receipt of the milestone payment of $2.0 million by us under the Navi License Agreement with Feng Biosciences (formerly OncXerna) in February 2022 resulted in a payment to CVR holders of approximately 2.3 cents per CVR, a total of approximately $0.9 million, after deductions of costs, charges and expenditures.

Novartis Agreements

In July 2015, three of our wholly-owned subsidiaries, Mereo BioPharma 3 Limited, Mereo BioPharma 2 Limited, and Mereo BioPharma 1 Limited (the “Subsidiaries”), entered into asset purchase agreements (the “Purchase Agreements”), to acquire from Novartis rights to setrusumab, acumapimod, and leflutrozole (the “Compounds”), respectively, and certain related assets (together with the Compounds, the “Novartis Assets”).

Under the Purchase Agreements, we have agreed to make tiered royalty payments to Novartis based on annual worldwide net sales of product candidates that include the Compounds (the “Acquired Novartis Product Candidates”), at percentages ranging from the high single digits to low double digits. In the event that the parties agree or it is otherwise determined in accordance with the Purchase Agreements that we require third-party intellectual property rights to exploit the Acquired Novartis Product Candidates, we are entitled to offset a specified percentage of amounts paid to such third parties in consideration for such intellectual property rights against the royalties due to Novartis. The royalty payments are payable for a period of ten years after the first commercial sale of an Acquired Novartis Product. We further agreed that in the event of a change in control that involves the transfer, license, assignment or lease of all or substantially all of a Subsidiary’s assets, including a Compound and related assets, we will pay Novartis a percentage of the proceeds of such transaction, with the majority of the proceeds being retained by us. No payment, however, is required with respect to any transaction of Mereo BioPharma Group plc involving its equity interests, a merger or consolidation of it, or a sale of any of its assets.

We also entered into a sublicense agreement with Novartis (the “Sublicense Agreement”), pursuant to which Novartis granted us an exclusive, worldwide, royalty-bearing sublicense for certain therapeutic antibody product candidates directed against sclerostin (the “Antibody Product Candidates”), including setrusumab. Under the Sublicense Agreement, we have agreed to pay Novartis royalties in the low single digits on worldwide net sales of Antibody Product Candidates. Royalties will be payable on a country-by-country basis until the later of expiration of the last valid claim of the licensed patents covering the Antibody Product Candidates in a country and ten years after the first commercial sale of the Antibody Product Candidates in such country, with a maximum royalty term of 12 years after the first commercial sale of the Antibody Product Candidates in such country. We have also agreed to pay Novartis up to $3.25 million in development and regulatory milestones, of which $0.8 million was paid in 2023, and to use commercially reasonable efforts to develop and commercialize an Antibody Product. The Sublicense Agreement will expire on the earlier of the termination of the agreement under which Novartis is granting us a sublicense (the “Original License Agreement”) and, on a product-by-product and country-by-country basis, the expiration of the royalty term with respect to such Antibody Product Candidate in such country. The Original License Agreement has a perpetual term and may be terminated for breach or upon a change in control of the licensing party. We may terminate the Sublicense Agreement upon written notice to Novartis and either party may terminate the Sublicense Agreement for the other party’s uncured material breach or bankruptcy.

Novartis Loan Note

On February 10, 2020, we entered into a £3.8 million convertible loan note instrument with Novartis pursuant to which we issued 3,841,479 unsecured convertible loan notes (the “Novartis Loan Note”) with a maturity date of February 10, 2023, and warrants to purchase 1,449,614 ordinary shares, exercisable until February 2025.

On February 10, 2023, we amended the Novartis Loan Note, extending the maturity date to February 10, 2025. Pursuant to the amendment and a new warrant instrument, interest accrued to the amendment date was paid in cash, and warrants to purchase 2,000,000 ordinary shares at an exercise price of £0.150 per ordinary share were issued and are exercisable until February 10, 2028.

Cooperation Agreement with Rubric Capital Management LP

14

On October 28, 2022, Mereo entered into a cooperation agreement (the “Cooperation Agreement”) with Rubric Capital Management LP, the Company’s largest shareholder. Pursuant to the Cooperation Agreement, four new directors, Dr. Annalisa Jenkins, Dr. Daniel Shames, Mr. Marc Yoskowitz and Mr. Justin Roberts, were subsequently appointed to the Company’s Board of Directors on November 10, 2022. Concurrent with these appointments taking effect, directors Dr. Peter Fellner, Dr. Brian Schwartz, Dr. Abdul Mullick and Ms. Anne Hyland resigned from the Board.

Manufacturing

We do not own or operate manufacturing facilities for the production of our product candidates, nor do we have plans to develop our own manufacturing operations in the foreseeable future. We have entered into manufacturing agreements with a number of drug substance, drug product, and other manufacturers and suppliers for alvelestat, etigilimab and acumapimod and we intend to enter into additional manufacturing agreements as necessary. Following our license of alvelestat, we acquired certain clinical trial materials and we subsequently outsourced production of further clinical supplies to our own manufacturing suppliers. We also outsource certain product formulation trials. We expect that drug product pre- validation and validation batches will be manufactured to satisfy regulatory requirements where we progress product candidates to late-stage trials.

We intend to enter into contractual relationships for the manufacture of commercial supplies for setrusumab, alvelestat and etigilimab, if approved for commercial sale. Any batches of product candidates for commercialization will need to be manufactured in facilities, and by processes, that comply with the requirements of the FDA, the EMA, and the regulatory agencies of other jurisdictions in which we are seeking approval. We employ internal resources to manage our manufacturing contractors and ensure they are compliant with current good manufacturing practices.

Commercialization, Sales and Marketing

We do not have our own marketing, sales, or distribution capabilities. In order to commercialize our product candidates, if approved for commercial sale, we must either develop a sales and marketing infrastructure or collaborate with third parties that have sales and marketing experience. In December 2020, we entered into a license and collaboration agreement with Ultragenyx for setrusumab. For our other current and future product candidates we intend to take strategic decisions on whether to further develop them, potentially through to approval, directly commercializing globally or in certain territories, or to seek a partner for further development, co-development and/or commercialization. For product candidates we intend to commercialize or co-commercialize, we must either establish a sales and marketing organization with technical expertise and supporting distribution capabilities in major markets or potentially outsource aspects of these functions to third parties or partners.

Competition

We compete directly with other biopharmaceutical and pharmaceutical companies that focus on the treatment of OI, AATD, solid tumors and AECOPD. We may also face competition from academic research institutions, governmental agencies and other various public and private research institutions. We expect to face increasingly intense competition as new technologies become available. Any product candidates, including setrusumab, alvelestat, etigilimab and acumapimod that we or our partners successfully develop and commercialize will compete with existing therapies and new therapies that may become available in the future.

We consider setrusumab’s current closest potential competitors in development for the treatment of OI to be Amgen and UCB’s anti-sclerostin antibody, romosozumab (Evenity), which was approved for osteoporosis in the U.S. in April 2019 and in December 2019 in Europe. In addition, Jiangsu Hengrui has commenced Phase 1 development of an anti-sclerostin antibody for osteoporosis in China, and Transcenta Holding has licensed the Chinese rights to the anti-sclerostin antibody blosozumab from Eli Lilly and Company (“Lilly”) and plans to develop it for osteoporosis. Baylor College of Medicine has conducted a Phase 1 open label trial of fresolimumab, a TGF-B inhibitor, in adult OI patients, and Sanofi is conducting a Phase 1 trial of SAR439459, a related TGF-B inhibitor, in adult OI patients. Amgen has also terminated a Phase 3 study and an open label extension study of denosumab (Prolia) an anti-resorptive agent in pediatric patients with OI.

We consider alvelestat’s current closest potential competitors for the treatment of severe AATD to be alpha-1- proteinase inhibitors that are administered intravenously in AAT augmentation therapy. Currently, there are four inhibitors on the market in the U.S. and the EU: Prolastin-C from Grifols, S.A. (“Grifols”), Aralast from Shire plc, now a subsidiary of Takeda Pharmaceutical Company Ltd (“Shire”), Zemaira from CSL Limited (“CSL”), and Glassia from Kamada Ltd. (“Kamada”). Kamada is also developing an inhaled version of augmentation therapy which is in Phase 3 and has a recombinant alpha-1 antitrypsin in early development. InhibRx, Inc. (“InhibRx”) (pending acquisition by Sanofi) has initiated a Phase 2 registrational trial of INBRX-101, a recombinant human alpha-1 antitrypsin Fc fusion protein (rhAAT-Fc) for replacement therapy. Apic Bio, Inc. (“Apic Bio”) is in the early stages of developing a dual function vector (df-AAV) gene-therapy approach for AATD silencing the mutant Z-AAT protein and augmenting wildtype M-AAT production. Wave Life Sciences has initiated a Phase 1 study of RNA base-editing oligonucleotide (WVE-0006) to

15

restore wild-type protein in lung and liver disease, a program that has been recently partnered with GSK. Intellia Therapeutics has initiated a Phase 1 study with a CRISPR/Cas9 -based insertion of normal SERPINA1 gene, targeting lung disease (NTLA-3001). Peak Bio acquired an oral NE inhibitor, PHP-303 from Ph Pharma in March 2022 and recently announced a merger with Akari Pharmaceuticals. Vertex Pharmaceuticals Inc. (“Vertex”) has two small molecule corrector programs for AATD in Phase 1 trials following Phase 2 trials with two other molecules with the same mechanism of action that were discontinued due to toxicity and efficacy. Biomarin Pharmaceutical Inc. is in early stages of development of a small molecule corrector (BMN 349). There are no therapies with regulatory approval for Bronchiolitis Obliterans Syndrome (“BOS”) following SCT or lung transplant. We consider alvelestat’s closest potential competitors to be the Janus Kinase (JAK1) inhibitor, itacitinib, and JAK2 inhibitor, ruxolitinib, (Incyte Corporation) in Phase 1/Phase2 studies in lung transplant-associated and SCT-associated BOS, respectively; AI Therapeutics inhaled formulation of sirolimus (LAM-001) in Phase 1 for BOS in lung transplant; Isopogen allogeneic bone marrow derived Mesenchymal Stem Cells for Chronic Lung Allograft Dysfunction (CLAD) in Phase 1 (NCT02709343 ); and liposomal inhaled cyclosporin-A (Zambon) in Phase 2 in BOS following SCT and in Phase 3 global pivotal trials in BOS associated with lung transplant.

We consider etigilimab’s current closest potential competitors to include other anti-TIGIT agents being developed by companies including Roche, Merck, iTeos and GSK, Beigene, Arcus/Gilead and Compugen amongst others. In addition, there are other combinations of existing cancer therapies available commercially for example, Yervoy and Opdivo and Opdivo or Keytruda in combination with chemotherapeutic targeted agents. There are a number of bispecific antibodies with an anti-TIGIT arm in development including a Phase 3 program in NSCLC being developed by AstraZeneca. There are also a number of other agents in development to other immuno-oncology targets that could compete with an anti-TIGIT approach, for example anti-LAG3.

For acumapimod, although we are not aware of any approved therapies for the treatment of AECOPD, there are a wide range of established therapies available for the treatment of COPD as well as a number of product candidates in development. We consider acumapimod’s current closest potential competitor for the treatment of AECOPD to be Verona Pharma’s (“Verona”) nebulized and inhaled ensifentrine (RPL554), a PDE3 / PDE4 dual inhibitor that is currently being developed as a bronchodilator and anti-inflammatory agent for COPD, Asthma and Cystic Fibrosis patients. In 2022, Verona announced positive results (FEV1 and AECOPD exacerbation frequency) from two Phase 3 trials (ENHANCE-1 and ENHANCE-2) in COPD. The FDA has assigned a Prescription Drug User Fee Act (“PDUFA”) target action date for ensifentrine of June 26, 2024. Pulmatrix, Inc. (“Pulmatrix”) has PUR1800, a narrow-spectrum kinase inhibitor (NSKI) that completed a Phase 1b trial in COPD. In addition to Pulmatrix, there are several compounds, which directly or indirectly target the p38 MAP Kinase pathway in clinical development by Poolbeg Pharma Plc (“Poolbeg), Fulcrum Therapeutics Inc (“Fulcrum”), GEn1E Lifesciences Inc (“GEn1E Lifesciences”), CervoMed Inc (“CervoMed”), Kinarus AG (“Kinarus”), Neurokine Therapeutics (“Neurokine”), and Inovio Pharmaceuticals Inc (“Inovio”), among others, for therapeutic indications outside the COPD setting.

We may face increasing competition for additional new product acquisitions from pharmaceutical companies as new companies emerge with a similar business model and other more established companies focus on acquiring product candidates to develop their pipelines. Many of our competitors have significantly greater name recognition, financial, manufacturing, marketing, drug development, technical and human resources than we do. Mergers and acquisitions in the biopharmaceutical and pharmaceutical industries may result in even more resources being concentrated among a smaller number of our competitors. Smaller or early stage companies may also prove to be significant competitors, particularly through collaborative arrangements with large and established companies. These competitors also compete with us in recruiting and retaining top qualified scientific and management personnel, establishing clinical trial sites and patient registration for clinical trials and in acquiring technologies complementary to, or necessary for, our programs.

The key competitive factors affecting the success of setrusumab, alvelestat, etigilimab and acumapimod, if approved, are likely to be their efficacy, safety, dosing convenience, price, the effectiveness of companion diagnostics in guiding the use of related therapeutics, the level of generic competition and the availability of reimbursement from government and other third-party payors.

Our commercial opportunity could be reduced or eliminated if our competitors develop and commercialize product candidates that are safer, more effective, less expensive, more convenient or easier to administer or have fewer or less severe side effects than any product candidates that we may develop. Our competitors may also obtain FDA, EMA or other regulatory approval for their product candidates more rapidly than we may obtain approval for our own product candidates, which could result in our competitors establishing a strong market position before we are able to enter the market. Even if setrusumab, alvelestat, etigilimab, or acumapimod achieve marketing approval, they may be priced at a significant premium over competing product candidates if any have been approved by then, potentially reducing our market opportunity. For more information, see “Item 1A. Risk Factors—Risks Related to Commercialization—We operate in a highly competitive and rapidly changing industry, which may result in others acquiring, developing, or commercializing competing product candidates before or more successfully than we or our partners do.”

Intellectual Property

16

We have acquired or exclusively licensed our intellectual property portfolio from Mereo BioPharma 5 (formerly OncoMed), Novartis and AstraZeneca. We strive to protect and enhance the proprietary technologies, inventions and improvements that we believe are important to our business, including seeking, maintaining and defending patent rights, whether developed internally or acquired or licensed from third parties. Our policy is to seek to protect our proprietary position by, among other methods, pursuing and obtaining patent protection in the U.S. and in jurisdictions outside of the U.S. related to our proprietary technology, inventions, improvements, platforms and our product candidates that are important to the development and implementation of our business.

Our intellectual property is held by our wholly owned subsidiaries. As of December 31, 2023, our patent portfolio comprises approximately 607 issued patents and approximately 92 pending patent applications on a global basis.

Individual patents extend for varying periods depending on the date of filing of the patent application or the date of patent issuance and the legal term of patents in the countries in which they are obtained. Generally, patents issued for regularly filed applications in the U.S. are granted a term of 20 years from the earliest effective non-provisional filing date. In addition, in certain instances, a patent term can be extended to recapture a portion of the USPTO delay in issuing the patent as well as a portion of the term effectively lost as a result of the FDA regulatory review period. However, as to the FDA component, the restoration period cannot be longer than five years and the total patent term including the restoration period must not exceed 14 years following FDA approval. The duration of foreign patents varies in accordance with provisions of applicable local law, but typically the duration of foreign issued patents is also 20 years from the earliest effective filing date.

However, the actual protection afforded by a given patent varies on a product-by-product basis and from country to country, dependent on many factors, including the type of patent, the scope of its coverage, the availability of regulatory-related extensions, the availability of legal remedies in a particular country and the validity and enforceability of the patent.

In addition to patent protection, we also rely upon trademarks, trade secrets and know-how, and continuing technological innovation, to develop and maintain our competitive position. We seek to protect our proprietary information, in part, using confidentiality agreements with our collaborators, employees and consultants and invention assignment agreements with our employees. We also have confidentiality agreements or invention assignment agreements with our collaborators and selected consultants. These agreements are designed to protect our proprietary information and, in the case of the invention assignment agreements, to grant us ownership of technologies that are developed through a relationship with a third party. These agreements may be breached, and we may not have adequate remedies for any breach. In addition, our trade secrets may otherwise become known or be independently discovered by competitors. To the extent that our collaborators, employees and consultants use intellectual property owned by others in their work for us, disputes may arise as to the rights in related or resulting know-how and inventions.

Our commercial success will also depend in part on not infringing upon the proprietary rights of third parties. It is uncertain whether the issuance of any third-party patent would require us to alter our development or commercial strategies, or our product candidates or processes, obtain licenses or cease certain activities. Our breach of any license agreements or failure to obtain a license to proprietary rights that we may require to develop or commercialize our product candidates may have an adverse impact on us. If third parties have prepared and filed patent applications prior to March 16, 2013, in the U.S, that also claim technology to which we have rights, we may have to participate in interference proceedings in the USPTO, to determine priority of invention. For more information, please see “Item 1A. Risk Factors—Risks Related to Intellectual Property.”

Setrusumab (BPS-804/UX143)

As of December 31, 2023, we have 127 patents globally (including four issued U.S. patents) and 24 patent applications globally (including a pending U.S. patent application) relating to setrusumab and its use for the treatment of OI. A first patent family includes three issued U.S. patents and 86 corresponding issued foreign patents that relate to the setrusumab antibody, nucleic acids encoding setrusumab, processes for producing setrusumab, and setrusumab’s use as a medicament. Patents emanating from this first patent family expire in 2028 (not accounting for any available patent term extension). We also have two additional patent families, including an issued U.S. patent and 37 issued foreign patents that relate to methods of using anti-sclerostin antibodies, including setrusumab, for the treatment of OI. Patents emanating from these additional patent families expire in 2037 (not accounting for any available patent term extension). Beyond these patents and patent applications, we jointly own with Ultragenyx one additional patent family relating to dosing regimens for the use of anti-sclerostin antibodies, including setrusumab, in the treatment of OI; we expect any patents emanating from this patent family to expire in 2042 (not accounting for any available patent term extension). In December 2020, we entered into a license and collaboration agreement with Ultragenyx for setrusumab for OI, under which Ultragenyx have exclusive rights under all setrusumab patent families outside of Europe. See “—Licensing Agreement with Ultragenyx for setrusumab.”

17

On February 3, 2023, Ultragenyx, Mereo BioPharma 3 Limited, UCB Pharma SA (“UCB”) and Amgen Inc. (“Amgen”) entered into a non-exclusive worldwide, royalty-free license to research, develop, and commercialize setrusumab in osteogenesis imperfecta under certain UCB/Amgen-owned patent rights related to anti-sclerostin compounds and their uses.

Alvelestat (MPH-966)

As of December 31, 2023, our patent portfolio relating to our product candidate alvelestat consisted of three issued U.S. patents, no pending U.S. patent applications, 36 issued or allowed foreign patents and two pending foreign patent applications. These patents have all been licensed under our agreement with AstraZeneca. See “—Material Agreements—Licensing Agreement with AstraZeneca.” These issued patents and patent applications, if issued, include claims directed to 2-pyridone derivatives as NE inhibitors and their uses as well as claims to polymorphs of the tosylate salt of a 5-pyrazolyl-2-pyridone derivative, with expected expiry dates between 2024 and 2030.

Our patent portfolio relating to our product candidate alvelestat also includes one pending international patent application filed under the PCT, three pending U.S. patent applications, two U.S. provisional patent applications, two granted foreign patents and sixteen pending foreign patent applications which have been filed subsequent to the license agreement with AstraZeneca. These patent applications, if issued, include claims directed to dosing regimens of alvelestat, methods of treatment using alvelestat, and dosage forms of alvelestat with expected expiry dates between 2040 and 2044.

Etigilimab (MPH-313)

As of December 31, 2023, our patent portfolio relating to our product candidate etigilimab consisted of four granted U.S. patents and two pending U.S. patent applications, as well as corresponding patent applications in major foreign jurisdictions.

The patent portfolio relating to our product candidate etigilimab contains one core patent family that covers the product per se as well as medical uses thereof. This patent family currently consists of two granted U.S. patents, sixty-one granted or allowed foreign patents and twelve pending foreign patent applications. Patents that issue from this core family are generally expected to expire in 2036.

The portfolio also includes a second patent family that relates to specific methods of treatment using etigilimab. This patent family currently consists of two granted U.S. patents, one U.S. pending patent application, and 8 granted or allowed foreign patents and 5 pending foreign patent applications. Any patents that issue from this family are generally expected to expire in 2037.

The portfolio also includes two PCT patent applications. Any patents that issue from these families are generally expected to expire in 2042.

Navicixizumab (OMP-305B83)