Filed Pursuant to Rule 424(b)(4)

Registration Statement No. 333-232594

Prospectus

5,000,000 Shares

![]()

BORR DRILLING LIMITED

Common Shares

This is the initial public offering in the United States of 5,000,000 common shares, par value $0.05 per share (“Shares”), of Borr Drilling Limited, a Bermuda exempted company limited by shares (the “Offering”).

Prior to this Offering, there has been no public market in the United States for our Shares. Our Shares are listed on the Oslo Børs under the symbol “BDRILL” and have been approved for listing on the New York Stock Exchange (“NYSE”) under the symbol “BORR.” The initial public offering price of our Shares is $9.30. On July 30, 2019, the closing price of our Shares on the Oslo Børs was 82.36 Norwegian Kroner, or NOK, per share, which was equivalent to approximately $9.40 per share based upon the Bloomberg Composite Rate of NOK 8.76 to $1.00 in effect on that date.

We are an “emerging growth company” as that term is defined in the Jumpstart Our Business Startups Act of 2012 and as such, will be eligible for reduced public company reporting requirements.

INVESTING IN OUR SHARES INVOLVES RISKS. SEE “RISK FACTORS” BEGINNING ON PAGE 13.

Neither the United States Securities and Exchange Commission nor any state securities commission or other regulatory body has approved or disapproved of these securities, or determined if this Prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

No offer or invitation to subscribe for Shares may be made to the public in Bermuda.

PRICE $9.30 PER SHARE

Per Share |

Total |

|||||

Initial public offering price |

$ | 9.300 | $ | 46,500,000 | ||

Underwriting discount(1) |

$ | 0.515 | $ | 2,575,000 | ||

Proceeds, before expenses, to Borr Drilling |

$ | 8.785 | $ | 43,925,000 | ||

| (1) | See the section entitled “Underwriting” for additional disclosure regarding underwriting compensation payable by us. |

We have also granted the underwriters an option for a period of 30 days to purchase up to 750,000 additional Shares on the same terms as set forth above. See “Underwriting.”

The underwriters expect to deliver the Shares against payment in U.S. dollars in New York, New York on or about August 2, 2019.

|

Goldman Sachs & Co. LLC

|

DNB Markets

|

|

BTIG

|

Citigroup

|

Danske Markets

|

Evercore ISI

|

Fearnley Securities

|

Prospectus dated July 31, 2019.

TABLE OF CONTENTS

Page |

|||

You should rely only on the information contained in this Prospectus (as defined below) and any related free writing prospectus that we authorize to be distributed to you. We and the underwriters have not authorized any person to provide you with information different from that contained in this Prospectus or any related free writing prospectus authorized to be distributed to you. This Prospectus is not an offer to sell, nor is it seeking an offer to buy, Shares in any state or other jurisdiction where such offer or sale is not permitted. The information in this Prospectus speaks only as of the date of this Prospectus unless the information specifically indicates that another date applies, regardless of the time of delivery of this Prospectus or of any sale of the securities offered hereby.

Neither we nor any of the underwriters has done anything that would permit this Offering or possession or distribution of this Prospectus, or any filed free writing prospectus, in any jurisdiction other than in the United States. Persons outside the United States who come into possession of this Prospectus or any filed free writing prospectus must inform themselves about, and observe any restrictions relating to, this Offering of the Shares and the distribution of this Prospectus or any filed free writing prospectus outside of the United States.

This Prospectus contains forward-looking statements that are subject to a number of risks and uncertainties, many of which are beyond our control. See the sections entitled “Risk Factors” and “Note Regarding Forward-Looking Statements.”

i

Until August 25, 2019 (the 25th day after the date of this Prospectus), all dealers that buy, sell or trade Shares, whether or not participating in this Offering, may be required to deliver a prospectus. This is in addition to the obligation of dealers to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

Shares may be offered or sold in Bermuda only in compliance with the provisions of the Investment Business Act of 2003 and the Exchange Control Act 1972, and related regulations of Bermuda which regulate the sale of securities in Bermuda. In addition, specific permission is required from the Bermuda Monetary Authority, or the BMA, pursuant to the provisions of the Exchange Control Act 1972 and related regulations, for all issuances and transfers of securities of Bermuda companies, other than in cases where the BMA has granted a general permission. The BMA in its policy dated June 1, 2005 provides that where any equity securities of a Bermuda company, including our common shares, are listed on an appointed stock exchange, general permission is given for the issue and subsequent transfer of any securities of a company from and/or to a nonresident, for as long as any equities securities of such company remain so listed. The NYSE is deemed to be an appointed stock exchange under Bermuda law.

Approvals or permissions given by the Bermuda Monetary Authority do not constitute a guarantee by the Bermuda Monetary Authority as to our performance or our creditworthiness. In granting such permission, the BMA accepts no responsibility for our financial soundness or the correctness of any of the statements made or opinions expressed in this Prospectus. This Prospectus does not need to be filed with the Registrar of Companies in Bermuda in accordance with Part III of the Companies Act 1981 of Bermuda, as amended (the “Companies Act”) pursuant to provisions incorporated therein following the enactment of the Companies Amendment Act 2013. Such provisions state that a prospectus in respect of the offer of shares in a Bermuda company whose equities are listed on an appointed stock exchange under Bermuda law does not need to be filed in Bermuda, so long as the company in question complies with the requirements of such appointed stock exchange in relation thereto.

ii

NOTE ON THE PRESENTATION OF INFORMATION

Unless otherwise indicated, information presented in this Prospectus which forms part of this registration statement on Form F-1 (this “Prospectus”) assumes that the underwriters’ option to purchase additional Shares is not exercised.

Throughout this Prospectus, unless the context otherwise requires, (i) references to “Borr Drilling Limited,” “Borr Drilling,” the “Company,” the “Registrant,” “we,” “us,” “Group,” “our” and words of similar import refer to Borr Drilling Limited and its consolidated subsidiaries, (ii) references to our “Board” or “Board of Directors” refer to the board of directors of Borr Drilling Limited as constituted at any point in time and “Director” or “Directors” refers to a member or members of the Board, as applicable, (iii) references to “Borr Drilling Management Dubai” and “Borr Drilling Management UK” refer to our subsidiaries Borr Drilling Management DMCC and Borr Drilling Management (UK) Ltd, respectively, (iv) references to our “Memorandum,” each provision thereof a “Clause,” or the “Bye-Laws,” each provision thereof a “Bye-Law,” refer to the memorandum of association and the amended and restated bye-laws of Borr Drilling Limited, respectively, each as in effect from time to time, (v) references to “Magni” or “Magni Partners” refers to Magni Partners (Bermuda) Limited, (vi) references to “Taran” refer to Taran Holdings Limited, (vii) references to “Ubon” refer to Ubon Partners AS, (viii) references to “Drew” refer to Drew Holdings Limited, (ix) references to our “DNB Revolving Credit Facility” or “DNB RCF” refer to our historical revolving credit facility with DNB Bank ASA, (x) references to our “Guarantee Facility” refer to our historical guarantee facility with DNB Bank ASA, (xi) references to our “DC Revolving Credit Facility” or “DC RCF” refer to our historical revolving credit and guarantee facility with Danske Bank A/S and Citigroup Global Markets Limited, (xii) references to our “Bridge Facility” or “Bridge RCF” refer to our historical revolving credit facility with Danske Bank A/S and DNB Bank ASA, (xiii) references to our “Hayfin Facility” refer to our term loan facility with Hayfin Services LLP, among others, (xiv) references to our “Syndicated Facility” or “Syndicated RCF” refer to our senior secured credit facilities with DNB Bank ASA, Danske Bank, Citibank N.A., Jersey Branch and Goldman Sachs Bank USA, (xv) references to our “New Bridge Facility” or “New Bridge RCF” refer to our senior secured revolving credit facility with DNB Bank ASA and Danske Bank, (xvi) references to our “Convertible Bonds” refer to our $350.0 million convertible bonds due 2023, (xvii) references to our “jack-up rigs” shall be deemed to include our semi-submersible rig (as the context may require) and (xviii) references to our “Reverse Share Split” refer to the conversion of each of our Shares into 0.20 Shares, resulting in a reverse share split at a ratio of 5-for-1. Unless otherwise indicated, all Share and per Share data in this Prospectus is adjusted to give effect to our Reverse Share Split and is approximate due to rounding.

References in this Prospectus to our “Financing Arrangements” refer to our Hayfin Facility, Syndicated RCF, New Bridge RCF, Convertible Bonds and shipyard delivery financing arrangements described more fully herein, collectively, including the agreements and other terms governing our Hayfin Facility, Syndicated RCF, New Bridge RCF, Convertible Bonds and delivery financing arrangements, respectively.

References in this Prospectus (i) to the “SEC” refer to the United States Securities and Exchange Commission and (ii) to “U.S. GAAP” refer to the generally accepted accounting principles in the United States as in effect at any point in time.

References in this Prospectus to “Keppel” and “PPL” refer to the shipyards Keppel FELS Limited and PPL Shipyard Pte Ltd., respectively, including their respective subsidiaries and affiliates as the context may require.

References in this Prospectus to “NDC,” “Total,” “ExxonMobil,” “Perenco,” “TAQA,” “BW Energy,” “ONGC,” “Spirit Energy,” “Tulip,” “BP,” “Shell” and “Chevron” refer to our key customers the National Drilling Company, Total S.A., Exxon Mobil Corporation, Perenco S.A., Abu Dhabi National Energy Company PJSC, BW Offshore Limited, the Oil and Natural Gas Corporation, Spirit Energy Limited, Tulip Oil Holding B.V., BP plc, Royal Dutch Shell plc and Chevron Corporation, respectively, including their respective subsidiaries and affiliates as the context may require.

References in this Prospectus to “ABS” refer to the American Bureau of Shipping.

Unless otherwise indicated, all references to “U.S.$” and “$” in this Prospectus are to, and amounts are presented in, U.S. dollars. All references to “€,” “EUR,” or “Euros” are to the single currency of the European Monetary Union, all references to “£,” “Pounds” or “GBP” are to pounds sterling and all references to “NOK” are to Norwegian Kroner.

iii

In this Prospectus, we present certain market and industry data. When furnishing the information set out in this Prospectus, including the industry information and data presented in the section entitled “Industry Overview,” we have used certain statistical and graphical information obtained from Rystad Energy, an independent energy research and business intelligence company. See “Experts.” Rystad Energy has advised us that the statistical and graphical information presented in this Prospectus is drawn from its database and other sources. We do not have any knowledge that the information provided by Rystad Energy is inaccurate in any material respect. Rystad Energy has further advised us that: (a) certain of the information provided is based on estimates or subjective judgments, (b) the information in the databases of other offshore drilling data collection agencies may differ from the information in Rystad Energy’s database and (c) while Rystad Energy has taken reasonable care in the compilation of the statistical and graphical information and believes it to be accurate and correct, data collection is subject to limited audit and validation procedures. Other information contained in this Prospectus regarding our industry and the markets in which we operate is based on our own internal estimates and research. This information is based on third party services which we believe to be reliable. Unless otherwise indicated, the basis for any statements regarding our competitive position in this Prospectus is based on our own assessment and knowledge of the market in which we operate. Where information sourced from Rystad Energy is presented, the source of such information is identified. Forward-looking information obtained from third party sources, including Rystad Energy, is subject to the same qualifications and the uncertainties regarding the other forward-looking statements in this Prospectus.

Market data and statistics are inherently predictive and subject to uncertainty and do not necessarily reflect actual market conditions. Such statistics are based on market research, which, itself, is based on sampling and subjective judgments by both the researchers and the respondents, including judgments about what types of products and transactions should be included in the relevant market. As a result, investors should be aware that statistics, statements and other information relating to markets, market sizes, market shares, market positions and other industry data set forth in this Prospectus, including in the section entitled “Industry Overview” (and projections, assumptions and estimates based on such data) may not be reliable indicators of our future performance and the future performance of the offshore drilling industry. See the sections entitled “Risk Factors” and “Note Regarding Forward-Looking Statements.”

iv

The following summary is qualified in its entirety by, and should be read in conjunction with, the more detailed information and financial statements appearing elsewhere in this Prospectus. In addition to this summary, we urge you to read the entire prospectus carefully before deciding whether to buy our Shares. You should carefully consider, among other things, our consolidated financial statements and the related notes and sections entitled “Risk Factors,” “Note Regarding Forward-Looking Statements,” “Selected Consolidated Financial and Other Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” as well as the audited consolidated financial statements of Borr Drilling Limited as of and for the years ended December 31, 2018 and 2017, the unaudited condensed consolidated interim financial statements of Borr Drilling Limited as of March 31, 2019 and for the three months ended March 31, 2019 and 2018, and the audited consolidated financial statements of Paragon Offshore Limited for its predecessor for the period from January 1, 2017, to July 18, 2017 and its successor for the periods from July 18, 2017, to December 31, 2017, and from January 1, 2018, to March 29, 2018, which are included elsewhere in this Prospectus, before making an investment decision.

OUR COMPANY

We are an offshore shallow-water drilling contractor providing worldwide offshore drilling services to the oil and gas industry. Our primary business is the ownership, contracting and operation of jack-up rigs for operations in shallow-water areas (i.e., in water depths up to approximately 400 feet), including the provision of related equipment and work crews to conduct oil and gas drilling and workover operations for exploration and production customers. We own 27 rigs, including 26 jack-up rigs and one semi-submersible rig, with an additional eight jack-up rigs scheduled to be delivered by the end of 2020. Upon delivery of these newbuild jack-up rigs, we will have a fleet of 30 premium jack-up rigs, which refers to rigs delivered from the yard in 2001 or later.

We aim to become a preferred operator of jack-up rigs within the jack-up drilling market. The shallow-water market is our operational focus as we expect demand will recover sooner than in the mid- and deepwater segments of the contract drilling market. We contract our jack-up rigs and offshore employees primarily on a dayrate basis to drill wells for our customers, including integrated oil companies, state-owned national oil companies and independent oil and gas companies. During 2018, our top five customers by revenue were subsidiaries of NDC, TAQA, BW Energy, Spirit Energy and Total. During the first quarter of 2019, our top five customers by revenue were subsidiaries of NDC, TAQA, Perenco, Total and Tulip. A dayrate drilling contract generally extends over a period of time covering either the drilling of a single well or group of wells or covering a stated term. Our Total Contract Backlog was $383.2 million as of June 30, 2019 and $377.5 million as of December 31, 2018. We currently operate in significant oil-producing geographies throughout the world, including the North Sea, the Middle East, Mexico, West Africa and Southeast Asia. We intend to operate our business with a competitive cost base, driven by a strong and experienced organizational culture and a carefully managed capital structure.

From our initial acquisition of rigs in early 2017, we have expanded rapidly into one of the world’s largest international offshore jack-up drilling contractors by number of jack-up rigs. The following chart illustrates the development in our fleet since our inception:

As of and for the Six Months Ended June 30, |

As of and for the Year Ended December 31, |

||||||||

2019 |

2018 |

2017 |

|||||||

Total Fleet as of January 1 |

27 | 13 | 0 | ||||||

Jack-up Rigs Acquired(1) |

— | 23 | 12 | ||||||

Newbuild Jack-up Rigs Delivered from Shipyards |

2 | 9 | 1 | ||||||

Jack-up Rigs Disposed of |

2 | 18 | 0 | ||||||

Total Fleet as of the end of Period |

27 | 27 | 13 | ||||||

Newbuild Jack-up Rigs not yet Delivered as of the End of Period |

8 | 9 | 13 | ||||||

Jack-up Rigs Committed to be Sold as of the End of Period |

1 | — | — | ||||||

Total Fleet, including Newbuild Rigs not yet Delivered, as of the end of Period |

35 | 36 | 26 | ||||||

| (1) | Includes acquisition of one semi-submersible rig in 2018. |

1

Our operating revenues, net (loss) and Adjusted EBITDA for the year ended December 31, 2018 were $164.9 million, $(190.9) million and $(65.8) million, respectively, and for the three months ended March 31, 2019 were $51.9 million, $(56.4) million and $(15.3) million, respectively. Adjusted EBITDA is a non-GAAP measure. For a definition of Adjusted EBITDA and a reconciliation of Adjusted EBITDA to the most directly comparable financial measure of net loss under U.S. GAAP, see “—Summary Consolidated Financial and Other Data.”

Our common shares have traded on the Oslo Børs since August 2017, under the symbol “BDRILL.”

OUR FLEET

We believe that we have one of the most modern jack-up fleets in the offshore drilling industry. Our drilling fleet consists of 27 rigs, of which four are standard jack-up rigs, 22 are premium jack-up rigs and one is a semi-submersible rig. In addition, we have agreed to purchase eight additional premium jack-up rigs to be delivered prior to the end of 2020. Premium jack-up rigs means rigs delivered from the yard in 2001 or later and which are suitable for operations in water depths up to 400 feet with an independent leg cantilever design. The majority of our rigs were built after 2013 and as of June 30, 2019, the average age of our premium fleet (excluding our four standard jack-up rigs and our semi-submersible rig) and of our entire fleet (excluding newbuilds not yet delivered) is 4.2 years and 9.7 years, respectively. As of the date of the last expected delivery of the newbuild jack-up rigs we have agreed to purchase, which is in 2020, the average age of our premium fleet (excluding our four standard jack-up rigs and our semi-submersible rig) and of our entire fleet will be 4.3 years and 8.8 years, respectively, which we believe to be among the lowest average fleet age in the industry (both currently and as of the date of our last expected delivery).

As of June 30, 2019, we had 26 total jack-up rigs, of which 11 rigs were “warm stacked,” which means the rigs, including our newbuild jack-up rigs which have been delivered but not yet been activated, are kept ready for redeployment and retain a maintenance crew, and three rigs were “cold stacked,” which means the rigs are stored in a harbor, shipyard or a designated offshore area and the crew is reassigned to an active rig or dismissed. We have entered into an agreement to sell one of our cold stacked jack-up rigs, the “Eir,” and we expect the sale to be completed by the end of the first quarter of 2020, subject to certain conditions. We believe that well-planned and well-managed stacking will significantly reduce reactivation cost and the cost of mobilization of a rig towards a contract. We are therefore focusing on securing cost efficiencies during stacking while limiting future risk from premature reactivation. This means concentrating stacked rigs in as few locations as possible to be able to share crew, running reduced but sufficient maintenance programs on equipment and preserving critical equipment.

We intend to prioritize the deployment of our currently contracted premium jack-up rigs. Reactivation of our premium jack-up rigs that are stacked will be undertaken for select contract opportunities. However, a stacked rig will only be reactivated if the achievable dayrate supports the reactivation and subsequent operating costs in a sensible way. Between April 1, 2018 and June 30, 2019, we signed 15 new contracts for drilling services, including nine with new customers. Our ability to keep our jack-up rigs operational when under contract, or Technical Utilization, for the year ended December 31, 2018 was 99.3% and for the six months ended June 30, 2019 was 99.0%, and the proportion of the potential full contractual dayrate that each contracted jack-up rig actually earns each day, or Economic Utilization, for the year ended December 31, 2018 was 97.9% and for the six months ended June 30, 2019 was 95.2%.

Each rig in our fleet is certified by ABS, enabling universal recognition of our equipment as qualified for international operations.

OUR COMPETITIVE STRENGTHS

We believe that our competitive strengths include:

One of the youngest and largest offshore drilling contractors

We have one of the youngest and largest fleets in the jack-up drilling market. The majority of our rigs were built after 2013 and, as of June 30, 2019, the average age of our premium fleet (excluding our four standard jack-up rigs, our semi-submersible rig and newbuilds not yet delivered) is 4.2 years and of our entire fleet (excluding newbuilds not yet delivered) is 9.7 years (implying an average building year of 2010),

2

respectively, which we believe is among the lowest average fleet age in the industry. New and modern rigs that offer technically capable, operationally flexible, safe and reliable contracting are increasingly preferred by customers. We expect to compete for and secure new drilling contracts from new tenders as well as privately negotiated transactions, which we estimate represent approximately half of new contract opportunities. We believe, based on our young fleet and growing operational track record, that we will be better placed to secure new drilling contracts as offshore drilling demand rises than our competitors who operate older, less modern fleets.

Largely uniform and modern fleet with available capacity to expand customer base

Because our fleet is one of the youngest and largest and the drilling equipment on, and operating capability of, our jack-up rigs is largely uniform, we have the capacity to bid for multiple contracts simultaneously, including those requiring active employment of multiple rigs over the same period, as in the case of our operations for Pemex (as defined below) in Mexico. We have acquired (including newbuilds not yet delivered) a fleet of largely premium jack-up rigs from shipyards with a reputation for quality and reliability. Moreover, due to the uniformity of the jack-up rigs in our fleet, we have been able to achieve operational and administrative efficiencies.

We have activated a number of our jack-up rigs since late 2018 based on firm contract opportunities, which we believe confirms our expectation that industry conditions in the jack-up drilling market will continue to improve. We believe that we are well-placed to capitalize on these improving trends as we seek to establish ourselves as one of the preferred providers in the industry. As of June 30, 2019, we have 11 rigs warm stacked and available for contracting as well as an additional eight jack-up rigs under construction which are also available for contracting.

Commitment to safety and the environment

We are focused on developing a strong Quality, Health, Safety and Environment (“QHSE”) culture and performance history. We believe that the combination of quality jack-up rigs and experienced and skilled employees contributes to the safety and effectiveness of our operations. Since the 2010 Deepwater Horizon Incident (as defined below) (to which we were not a party), there has been an increased focus on offshore drilling QHSE issues by regulators as well as by the industry. As a result, companies exploring for or producing oil and/or natural gas (“E&P Companies”) have imposed increasingly stringent QHSE rules on their contractors, especially when working on challenging wells and operations where the QHSE risks are higher. Our commitment to strong QHSE culture and performance is reflected in our Technical Utilization rate of 99.3% in 2018 and 99.0% for the six months ended June 30, 2019, and our excellent safety record in the same period. We believe our focus on providing safe and efficient drilling services will enhance our growth prospects as we work toward becoming one of the preferred providers in the industry.

Strong and diverse customer relationships

We have strong relationships with our customers rooted in our employees’ expertise, reputation and history in the offshore drilling industry, as well as our growing operational track record and the quality of our fleet. Our customers are oil and gas exploration and production companies, including integrated oil companies, state-owned national oil companies and independent oil and gas companies. For the year ended December 31, 2018, our five largest customers in terms of revenue were NDC, TAQA, BW Energy, Spirit Energy and Total. We believe that we are responsive and flexible in addressing our customers’ specific needs and seek collaborative solutions to achieve customer objectives. We focus on strong operational performance and close alignment with our customers’ interests, which we believe provides us with a competitive advantage and will contribute to contracting success and rig utilization.

Management team and Board members with extensive experience in the drilling industry

Our executive management team and Board have extensive experience in the oil and gas industry in general and in the drilling industry in particular. In addition, the members of our executive management team are knowledgeable operating and financial executives with extensive experience with companies operating in the jack-up drilling market. The members of our executive management team and Board have held and

3

currently hold leadership positions at prominent offshore drilling and oilfield services companies, including Schlumberger Limited, Marine Drilling Companies, Inc., Seadrill Limited, North Atlantic Drilling Ltd., TODCO and Archer Limited, and have relationships which complement one another and have assisted, and continue to assist, in our development.

Effective acquisition history

We acquired our jack-up rigs at what we believe are historically attractive prices, including through four major acquisitions since early 2017. The average purchase price of our rigs is significantly lower than the historical construction cost of comparable rigs. We acquired our jack-up rigs at a substantial discount to their cost when originally ordered. We have acquired the majority of our newbuild jack-up rigs by raising equity in the financial markets and by entering into delivery financing arrangements provided by the shipyards. In contrast to many of our competitors who built and owned their fleet prior to 2014, we entered the jack-up drilling market at what we believe to be an attractive price point. Although we have incurred net losses as we commence operations, we believe we are well placed, with a young and modern fleet, to capitalize on any upturn in the jack-up drilling market.

OUR BUSINESS STRATEGIES

Through our premium jack-up rigs, we intend to meet our primary business objective of becoming a preferred operator in the jack-up drilling market while also maximizing return to our shareholders. To achieve this, our strategies include the following:

Deploy high-quality rigs to service a growing industry

We have acquired one of the leading jack-up fleets in the industry with capacity to service existing and future client needs. Tender activity in the jack-up drilling market has been increasing sharply since the second quarter of 2018, which we believe indicates the industry is recovering from the challenges it has faced over the last five years. We believe that shallow-water drilling, such as that performed by our jack-up rigs, has a shorter lifecycle between exploration and first oil and lower capital expenditure than other forms of drilling performed by mobile offshore drilling units, such as drillships. We believe this makes shallow-water drilling more attractive than deep-water projects in the current economic and industry climates. Major E&P Companies have experienced falling production coupled with rising cash flows since late 2016 and as a result of these factors, we anticipate an increase in shallow-water drilling among E&P and other companies. In addition to tender activity in which we participate through bidding, we also compete for new contract opportunities through privately negotiated transactions, including private tenders and direct negotiations with customers, which we estimate represent approximately half of new contract opportunities. We believe our footprint in the industry is growing. Between April 1, 2018, and June 30, 2019, we signed 15 new contracts for drilling services with an aggregate value of approximately $439 million, including nine with new customers. During this period, we also signed two extensions and have had four options exercised. As of June 30, 2019, 16 of our 27 rigs are under contract (including our semi-submersible rig).

Become a preferred provider in the industry

We have established strong and long-term relationships with key participants and customers in the offshore drilling industry, including through our acquisition of Paragon Offshore Limited, the hiring of experienced personnel and contracts signed since our inception, and we will seek to deepen and strengthen these relationships as part of our strategy. This involves identifying value add services for our customers (such as integrated well contracts) and, as an example of this, we have signed a non-exclusive Collaboration Agreement (as defined below) with Schlumberger Oilfield Holdings Ltd., a wholly owned subsidiary of Schlumberger Limited, who is our principal shareholder (“Schlumberger”), to offer such services. For more information on our relationship with Schlumberger, please see the section entitled “Certain Relationships and Related Party Transactions.” We also plan to continue to hire employees with long track-records in the industry and extensive contacts with potential key customers to further improve customer relationships. Based on our largely premium and uniform fleet, our experienced team and a solid industry network, we believe that we are well-positioned to capitalize on improving trends as we seek to establish ourselves as a preferred provider to these customers.

4

Establish high-quality, cost-efficient operations

We intend to be a leading offshore shallow-water drilling company by operating with a competitive cost base while continuing to grow our reputation as a high quality contractor. Our key objective is to deliver the best operations possible—both in terms of Technical Utilization and QHSE culture and performance—while also maximizing deployment of our rigs and maintaining a competitive cost structure.

To facilitate our strategy, we have acquired one of the most modern and uniform fleets in the industry, with experienced and skilled individuals across the organization and on our Board. We expect to have an advantage not only with regard to operating expenditures as a result of our largely standardized fleet, but also with regard to financing costs when compared to many of our industry peers.

Establish and offer integrated services

We are planning to offer integrated drilling/well services together with Schlumberger and have been tendering our services on this basis for some contract tenders. Integrated drilling services offer all services and equipment (and in some cases, material procurement) in a single contract. We believe this model is more economically feasible and thus attractive for smaller E&P Companies operating offshore, as the model could reduce the number of contracts required for a project from above ten to two or three. Significant cost saving potential is evident in the model. As a result, project management could become simpler, cheaper and more efficient for customers with integrated drilling services. Further, this could lead to improved well design, better selection and more efficient operators of rig equipment and technology.

We expect our collaboration agreement with Schlumberger, while not exclusive to either party, to enable us to offer integrated well services by providing a combination of services, technology, equipment and rigs that we expect to yield a significant value proposition. An example is the recent contract awarded to us in Mexico, where we, Schlumberger and local partners will work together to deliver integrated drilling services to Pemex.

Maintain financial discipline

We intend to manage our balance sheet by maintaining a suitable proportion of equity and debt, depending on our contract backlog and market outlook. In the future, we may consider adding leverage against our contract backlog or to finance growth or other accretive activities. We will also aim to distribute dividends to shareholders whenever we have excess cash flows and are permitted to do so under our Financing Arrangements.

RISK FACTORS

We face a number of risks associated with our business and industry and must overcome a variety of challenges to utilize our competitive strengths and implement our business strategies. These risks relate to, among others, changes in the jack-up drilling market, including supply and demand, utilization rates, dayrates, customer drilling programs and commodity prices; a downturn in the global economy; hazards inherent in our industry and operations resulting in liability for personal injury or loss of life, damage to or destruction of property and equipment, pollution or environmental damage; inability to comply with covenants in certain of our debt arrangements; and inability to successfully employ our jack-up rigs. Investing in our Shares involves substantial risk. You should carefully consider those risks described in the section entitled “Risk Factors” and the other information in this Prospectus before deciding whether to invest in our Shares.

RECENT DEVELOPMENTS

New Local Partner Relationship

In February 2019, we, along with a local partner in Mexico, Proyectos Globales de Energia y Servicos CME, S.A. DE C.V. (“CME”), successfully tendered for a contract to provide integrated well services to Petroleos Mexicanos (“Pemex”). On March 20, 2019, one of our subsidiaries and one of CME’s subsidiaries entered into a contract for the provision of integrated well services to Pemex (the “Pemex Contract”). In June 2019, we finalized the Mexican JV (as defined below) structure and expect to commence operations under the Pemex Contract in early August 2019. Please see the sections entitled “Business—Joint Venture, Partner and Agency Relationships—Mexico” and “—Our Fleet” for further information.

5

Refinancing of Historical Financing Arrangements

During the first half of 2019, we refinanced our historical revolving credit facilities, including our DNB RCF, Guarantee Facility, DC RCF and Bridge RCF. Following the signing of our Hayfin Facility, Syndicated Facility and New Bridge Facility agreements on June 25, 2019, which collectively provided $645 million in financing, we paid in full the outstanding balances due under our DNB RCF, Guarantee Facility, DC RCF and Bridge RCF, respectively, which were subsequently cancelled. Please see the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Our Existing Indebtedness” for more information.

Reverse Share Split

We have effected a conversion of each of our Shares into 0.20 Shares, resulting in a reverse share split at a ratio of 5-for-1. Our post-Reverse Share Split Shares began to trade on the Oslo Børs on June 26, 2019. Unless otherwise indicated, all Share and per Share data in this Prospectus is adjusted to give effect to our Reverse Share Split and is approximate due to rounding.

As of March 31, 2019, there were 525,341,755 Shares issued and outstanding, representing a per share net tangible book value of $2.71. Immediately after our Reverse Share Split, the number of issued and outstanding Shares decreased to 105,068,351, not accounting for fractional shares, representing a per share net tangible book value of $13.55.

Acquisition of Keppel’s Hull B378

In March 2019, we entered into an assignment agreement with BOTL Lease Co. Ltd. (the “Original Owner”) for the assignment of the rights and obligations under a construction contract to take delivery of one KFELS Super B Bigfoot premium jack-up rig identified as Keppel’s Hull No. B378 from Keppel for a purchase price of $122.1 million. The construction contract was, at the same time, novated to our subsidiary, Borr Jack-Up XXXII Inc., and amended. We took delivery of the jack-up rig on May 9, 2019 and the rig was subsequently renamed “Thor.”

To finance the rig purchase we entered into a $120.0 million senior secured term loan facilities agreement, consisting of two facilities (Facility A and Facility B) of $60.0 million each, which we refer to as our Bridge Facility. The facilities had a maturity date of September 30, 2019. Following the signing of our Hayfin Facility, Syndicated Facility and New Bridge Facility agreements on June 25, 2019, which collectively provided $645 million in financing, we paid the outstanding balance due under our Bridge Facility, which was subsequently cancelled.

Sale of Jack-up Rigs

In May 2019, we entered into sale agreements for the sale of the “Eir,” “Baug” and “Paragon C20051,” none of which were operating or on contract, for cash consideration of $3.0 million each. The jack-up rigs have been sold with a contractual obligation not to be used for drilling purposes and so retired from the international jack-up fleet. The sales of “Baug” and “Paragon C20051” were completed in May 2019 for cash consideration of $6.0 million and the sale of “Eir” is expected to be completed by the end of the first quarter of 2020, subject to certain conditions. We have recorded an impairment of $11.4 million in the first quarter of 2019 in connection with our entry into an agreement for the sale of the “Eir.” These divestments bring the total number of jack-up rigs divested by us and retired from the international jack-up fleet to 20 since the beginning of 2018.

COMPANY INFORMATION

Borr Drilling Limited was incorporated by Taran Holdings Limited on August 8, 2016, pursuant to the Companies Act, as an exempted company limited by shares and registered in the Bermuda register of companies with the name “Magni Drilling Limited.” On December 16, 2016, we changed our name to Borr Drilling Limited. On December 19, 2016, our Shares were introduced to the Norwegian OTC market and on August 30, 2017, our Shares were listed on the Oslo Børs under the symbol “BDRILL.” Our principal executive offices are located at S. E. Pearman Building, 2nd Floor, 9 Par-la-Ville Road, Hamilton HM11, Bermuda and our telephone number is +1 (441) 737-0152.

6

OTHER INFORMATION

Because we are incorporated under the laws of Bermuda, you may encounter difficulty protecting your interests as shareholders, and your ability to protect your rights through the U.S. federal court system may be limited. Please refer to the sections entitled “Risk Factors” and “Enforceability of Civil Liabilities Against Foreign Persons” for more information.

7

THE OFFERING

Since we are a holding company with no material assets other than the shares of our subsidiaries through which we conduct our operations, our ability to pay dividends will depend on our subsidiaries distributing their earnings and cash flow to us. Furthermore, the covenants in our New Bridge Facility agreement require the approval of our lenders prior to the distribution of any dividends and the covenants in our Syndicated Facility agreement subject dividends to certain conditions which if not met would require the approval of our lenders prior to the distribution of any dividend.

We have not paid dividends to our shareholders since incorporation. We aim to distribute a portion of our future earnings from operations, if any, to our shareholders from time to time as determined by our Board. Any dividends declared in the future will be at

8

the sole discretion of our Board and will depend upon earnings, market prospects, current capital expenditure programs and investment opportunities.

9

SUMMARY CONSOLIDATED FINANCIAL AND OTHER DATA

Our summary consolidated statement of operations and other financial data for the years ended December 31, 2018 and 2017 and our summary consolidated balance sheet data as of December 31, 2018 and 2017 have been derived from our audited consolidated financial statements as of and for the years ended December 31, 2018 and 2017, which are included elsewhere in this Prospectus (the “Consolidated Financial Statements”). Our summary consolidated statement of operations and other financial data for the three months ended March 31, 2019 and 2018 and our summary consolidated balance sheet data as of March 31, 2019 have been derived from our unaudited condensed consolidated financial statements as of March 31, 2019 and for the three months ended March 31, 2019 and 2018, which are included elsewhere in this Prospectus (the “Interim Financial Statements”).

Our Consolidated Financial Statements and Interim Financial Statements are prepared and presented in accordance with U.S. GAAP. Our historical results are not necessarily indicative of results expected for future periods.

The following table should be read in conjunction with the sections entitled “Capitalization” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our Consolidated Financial Statements and Interim Financial Statements and notes thereto, which are included herein. Our Consolidated Financial Statements and Interim Financial Statements are maintained in U.S. dollars. We refer you to the notes to our Consolidated Financial Statements and Interim Financial Statements for a discussion of the basis on which our Consolidated Financial Statements and Interim Financial Statements are prepared, respectively.

We have effected a conversion of each of our Shares into 0.20 Shares, resulting in a reverse share split at a ratio of 5-for-1. Our post-Reverse Share Split Shares began to trade on the Oslo Børs on June 26, 2019. The table below reflects our Reverse Share Split. Unless otherwise indicated, all Share and per Share data in this Prospectus is adjusted to give effect to our Reverse Share Split and is approximate due to rounding.

For the Three Months Ended March 31 |

For the Year Ended December 31, |

|||||||||||

2019 |

2018 |

2018 |

2017 |

|||||||||

(in $ millions, except per share data) |

||||||||||||

SUMMARY CONSOLIDATED STATEMENTS OF OPERATIONS DATA: |

||||||||||||

Operating revenues |

$ | 51.9 | $ | 10.6 | $ | 164.9 | $ | 0.1 | ||||

Gain from bargain purchase |

— | 38.1 | 38.1 | — | ||||||||

Gain on disposals |

— | — | 18.8 | — | ||||||||

Operating expenses |

(109.9 | ) |

(62.8 | ) |

(353.2 | ) |

(109.8 | ) |

||||

Operating loss |

(58.0 | ) |

(14.1 | ) |

(131.4 | ) |

(109.7 | ) |

||||

Total other income (expenses), net |

1.8 | (19.7 | ) |

(57.0 | ) |

21.7 | ||||||

Income tax expense |

(0.2 | ) |

— | (2.5 | ) |

— | ||||||

Net loss |

(56.4 | ) |

(33.8 | ) |

(190.9 | ) |

(88.0 | ) |

||||

Other comprehensive gain (loss) |

(7.3 | ) |

— | 0.6 | (6.2 | ) |

||||||

Total comprehensive loss |

$ | (63.7 | ) |

$ | (33.8 | ) |

$ | (190.3 | ) |

$ | (94.2 | ) |

Net loss per common share: |

||||||||||||

Basic |

(0.52 | ) |

(0.35 | ) |

(1.85 | ) |

(1.70 | ) |

||||

Diluted |

(0.52 | ) |

(0.35 | ) |

(1.85 | ) |

(1.70 | ) |

||||

Common shares outstanding |

105,068,351 | 105,068,351 | 105,068,351 | 95,264 | ||||||||

Weighted average common shares outstanding |

105,068,351 | 102,877,501 | 102,877,501 | 51,726,288 | ||||||||

10

As of March 31 |

As of December 31, |

||||||||

2019 |

2018 |

2017 |

|||||||

(in $ millions) |

|||||||||

SUMMARY BALANCE SHEET DATA: |

|||||||||

Cash and cash equivalents |

$ | 29.4 | $ | 27.9 | $ | 164.0 | |||

Restricted cash |

29.4 | 63.4 | 39.1 | ||||||

Other current assets |

150.7 | 117.3 | 22.4 | ||||||

Jack-up drilling rigs |

2,416.1 | 2,278.1 | 783.3 | ||||||

Newbuildings |

432.5 | 361.8 | 642.7 | ||||||

Marketable securities |

— | 31.0 | 20.7 | ||||||

Other long-term assets |

40.3 | 34.2 | — | ||||||

Total assets |

3,098.4 | 2,913.7 | 1,672.3 | ||||||

Trade accounts payable |

14.7 | 9.6 | 9.6 | ||||||

Accruals and other current liabilities |

109.6 | 106.5 | 11.5 | ||||||

Long-term debt (including current portion) |

1,415.4 | 1,174.6 | 87.0 | ||||||

Onerous contracts |

71.3 | 81.5 | 71.3 | ||||||

Other liabilities |

15.6 | 8.0 | — | ||||||

Total liabilities |

1,626.6 | 1,380.2 | 179.4 | ||||||

Total equity |

$ | 1,471.8 | $ | 1,533.5 | $ | 1,492.9 | |||

For the Three Months Ended March 31, |

For the Year Ended December 31, |

|||||||||||

2019 |

2018 |

2018 |

2017 |

|||||||||

(in $ millions) |

||||||||||||

CASH FLOW DATA: |

||||||||||||

Net Cash Provided by / (Used in) Operating Activities |

$ | (13.9 | ) |

$ | (45.4 | ) |

$ | (135.2 | ) |

$ | (184.8 | ) |

Net Cash Provided by / (Used in) Investing Activities |

(172.1 | ) |

(198.8 | ) |

(560.1 | ) |

(1,256.5 | ) |

||||

Net Cash Provided by / (Used in) Financing Activities |

153.5 | 147.6 | 583.5 | 1,506.3 | ||||||||

As of and for the Three Months Ended March 31, |

As of and for the Year Ended December 31, |

|||||||||||

2019 |

2018 |

2018 |

2017 |

|||||||||

OTHER FINANCIAL AND OPERATIONAL DATA: |

||||||||||||

Adjusted EBITDA(1) (in $ millions) |

$ | (15.3 | ) |

$ | (40.0 | ) |

$ | (65.8 | ) |

$ | (61.8 | ) |

Total Contract Backlog(2) (in $ millions) |

451.2 | 206.7 | 377.5 | 28.5 | ||||||||

Technical Utilization(3) (in %) |

98.8 | % |

91.9 | % |

99.3 | % |

— | |||||

Economic Utilization(4) (in %) |

95.7 | % |

86.1 | % |

97.9 | % |

— | |||||

TRIF(5) (number of incidents) |

1.20 | 1.66 | 1.54 | — | ||||||||

| (1) | Adjusted EBITDA is a non-GAAP financial measure and as used herein represents net loss adjusted for: depreciation and impairment of non-current assets, amortization of contract backlog, interest income, interest capitalized to newbuildings, foreign exchange loss, net, other financial expenses, interest expense, gross, change in unrealized (loss)/gain on Call Spread Transactions (as defined below), (loss)/gain on forward contracts, gain from bargain purchase and income tax expense. We present Adjusted EBITDA because we believe that it and other similar measures are widely used by certain investors, securities analysts and other interested parties as supplemental measures of performance. We believe Adjusted EBITDA provides meaningful information about the performance of our business and therefore we use it to supplement our U.S. GAAP reporting. Moreover, our management uses Adjusted EBITDA in presentations to our Board to provide a consistent basis to measure operating performance of our business, as a measure for planning and forecasting overall expectations, for evaluation of actual results against such expectations and in communications with our shareholders, lenders, bondholders, rating agencies and others concerning our financial performance. We believe that Adjusted EBITDA improves the comparability of year-to-year results and is representative of our underlying performance, although Adjusted EBITDA has significant limitations, including not reflecting our cash requirements for capital or deferred costs, rig reactivation costs, newbuild rig activation costs contractual commitments, taxes, working |

11

capital or debt service. Non-GAAP financial measures may not be comparable to similarly titled measures of other companies and have limitations as analytical tools and should not be considered in isolation or as a substitute for analysis of our operating results as reported under U.S. GAAP. The following table sets forth a reconciliation of Adjusted EBITDA to net loss for the three months ended March 31, 2019 and 2018 and the years ended December 31, 2018 and 2017:

For the Three Months Ended March 31, |

For the Year Ended December 31, |

|||||||||||

2019 |

2018 |

2018 |

2017 |

|||||||||

(in $ millions) |

||||||||||||

Net loss |

$ | (56.4 | ) |

$ | (33.8 | ) |

$ | (190.9 | ) |

$ | (88.0 | ) |

Depreciation and impairment of non-current assets |

23.9 | 12.2 | 79.5 | 47.9 | ||||||||

Amortization of contract backlog* |

7.4 | — | 24.2 | — | ||||||||

Interest income |

(0.3 | ) |

(0.5 | ) |

(1.2 | ) |

(3.2 | ) |

||||

Interest capitalized to newbuildings |

(5.8 | ) |

(2.7 | ) |

(23.4 | ) |

— | |||||

Foreign exchange loss, net |

(0.2 | ) |

0.2 | 1.1 | 0.3 | |||||||

Other financial expenses |

0.8 | — | 3.5 | — | ||||||||

Interest expense, gross |

18.8 | 2.7 | 37.1 | 0.5 | ||||||||

Change in unrealized (loss)/gain on Call Spread Transactions |

(3.6 | ) |

— | 25.7 | — | |||||||

(Loss)/gain on forward contracts |

(11.5 | ) |

20.0 | 14.2 | (19.3 | ) |

||||||

Gain from bargain purchase |

— | (38.1 | ) |

(38.1 | ) |

— | ||||||

Income tax expense |

0.2 | — | 2.5 | — | ||||||||

Adjusted EBITDA |

$ | (15.3 | ) |

$ | (40.0 | ) |

$ | (65.8 | ) |

$ | (61.8 | ) |

| * | Amortization of the fair market value of existing contracts at the time of the initial acquisition. |

See the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations—How We Evaluate Our Business—Financial Measures—Adjusted EBITDA.”

| (2) | Our Total Contract Backlog includes only firm commitments for contract drilling services represented by definitive agreements. Total Contract Backlog (in $ millions) is calculated as the maximum contract drilling dayrate revenue that can be earned from a drilling contract based on the contracted operating dayrate. Total Contract Backlog excludes revenue resulting from mobilization and demobilization fees, contract preparation, capital or upgrade reimbursement, recharges, bonuses and other revenue sources and is not adjusted for planned out-of-service periods during the contract period. The contract period excludes additional periods that may result from the future exercise of extension options under our contracts, and such extension periods are included only when such options are exercised. The contract operating dayrate may temporarily change due to, among other factors, mobilization, weather or repairs. As used in this Prospectus, Total Contract Backlog (in $ millions) is not the same measure as the acquired contract backlog presented in our Consolidated Financial Statements and Interim Financial Statements. Please see Notes 2 and 14 to our Consolidated Financial Statements and Notes 3 and 11 to our Interim Financial Statements for further information. See the section entitled “Business—Customers and Contract Backlog.” |

| (3) | Technical Utilization is the efficiency with which we perform well operations without stoppage due to mechanical, procedural or other operational events that result in down, or zero, revenue time. Technical Utilization is calculated as the technical utilization of each rig in operation for the period, divided by the number of rigs in operation for the period, with the technical utilization for each rig calculated as the total number of hours during which such rig generated dayrate revenue, divided by the maximum number of hours during which such rig could have generated dayrate revenue, expressed as a percentage measured for the period. We have not provided Technical Utilization data for the year ended December 31, 2017 because only one of our jack-up rigs was in operation for approximately one day at the end of December 2017. See “Business—History and Development—Acquisition from Transocean” for more information. Technical Utilization is calculated only with respect to rigs in operation for the relevant period and is not calculated on a fleet-wide basis. Technical Utilization is a measure of efficiency of rigs in operation and is not a measurement of utilization of our fleet overall. |

| (4) | Economic Utilization is the dayrate revenue efficiency of our operational rigs and reflects the proportion of the potential full contractual dayrate that each jack-up rig actually earns each day. Economic Utilization is affected by reduced rates for standby time, repair time or other planned out-of-service periods. Economic Utilization is calculated as the economic utilization of each rig in operation for the period, divided by the number of rigs in operation for the period, with the economic utilization of each rig calculated as the total revenue, excluding bonuses, as a proportion of the full operating dayrate multiplied by the number of days on contract in the period. We have not provided Economic Utilization data for the year ended December 31, 2017 because only one of our jack-up rigs was in operation for approximately one day at the end of December 2017. See “Business—History and Development—Acquisition from Transocean” for more information. Economic Utilization is calculated only with respect to rigs in operation for the relevant period and is not calculated on a fleet-wide basis. Economic Utilization is a measure of efficiency of rigs in operation and is not a measurement of utilization of our fleet overall. |

| (5) | Total recordable incident frequency (“TRIF”) is a measure of the rate of recordable workplace injuries. TRIF, as defined by the International Association of Drilling Contractors, is derived by multiplying the number of recordable injuries during the twelve-month period prior to the specified date by 1,000,000 and dividing this value by the total hours worked in that period by the total number of employees. An incident is considered “recordable” if it results in medical treatment over certain defined thresholds (such as receipt of prescription medication or stitches to close a wound) as well as incidents requiring the injured person to spend time away from work. We have not provided TRIF data for the year ended December 31, 2017 because only one of our jack-up rigs was in operation for approximately one day at the end of December 2017. See “Business—History and Development—Acquisition from Transocean” for more information. |

12

An investment in our Shares involves significant risks. You should carefully consider all of the information in this Prospectus, including the risks and uncertainties described below, before making an investment in our Shares. Any of the following risks could have a material adverse effect on our business, financial condition and results of operations. In any such case, the market price of our Shares could decline, and you may lose part or all of your investment.

RISK FACTORS RELATED TO OUR INDUSTRY

The jack-up drilling market historically has been highly cyclical, with periods of low demand and/or over-supply that could result in adverse effects on our business.

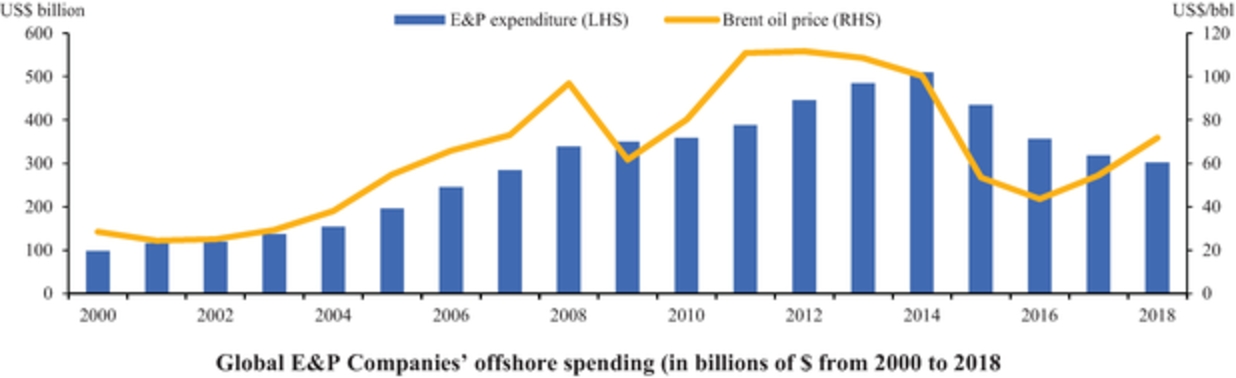

The jack-up drilling market historically has been highly cyclical and is primarily related to the demand for jack-up rigs and the available supply of jack-up rigs. Demand for jack-up rigs is directly related to the regional and worldwide levels of offshore exploration and development spending by oil and gas companies, which is beyond our control. It is not unusual for jack-up rigs to be unutilized or underutilized for significant periods of time and subsequently resume full or near full utilization when business cycles change. During historical industry periods of high utilization and high dayrates, industry participants ordered the construction of new jack-up rigs, which has resulted in an over-supply of jack-up rigs worldwide. During periods of supply and demand imbalance, jack-up rigs are frequently contracted at or near cash breakeven operating rates for extended periods of time until dayrates increase when the supply/demand balance is restored. Offshore exploration and development spending may fluctuate substantially from year-to-year and from region-to-region.

The significant decline in oil and gas prices and resulting reduction in spending by customers, together with the increase in supply of jack-up rigs in recent years, has resulted in an oversupply of jack-up rigs and a decline in utilization and dayrates, a situation which may persist for many years.

A prolonged period of reduced demand and/or excess jack-up rig supply may require us to idle or dispose of additional jack-up rigs or to enter into low dayrate contracts or contracts with unfavorable terms. For more information on our jack-up rig disposal policy, see the section entitled “Business—Our Fleet.” There can be no assurance that the demand for jack-up rigs will increase in the future. Any further decline or if there is not an improvement in demand for jack-up rigs could have a material adverse effect on our business, financial condition and results of operations.

The offshore contract drilling industry is highly competitive, with periods of excess rig availability which reduce dayrates and could result in adverse effects on our business.

Our industry is highly competitive, and our contracts are traditionally awarded on a competitive bid basis. Pricing, rig age, safety records and competency are key factors in determining which qualified contractor is awarded a job. Competitive factors include: rig availability, rig location, rig operating features and technical capabilities, pricing, workforce experience, operating efficiency, condition of equipment, contractor experience in a specific area, reputation and customer relationships. If we are not able to compete successfully, our revenues and profitability may be impacted, which could have a material adverse effect on our business, financial condition and results of operations.

The supply of offshore drilling rigs, including jack-up rigs, has increased significantly in recent years. Delivery of newbuild drilling rigs will continue to increase rig supply in coming years and could curtail a strengthening, or trigger a further reduction, in utilization and dayrates. Approximately 13 newbuild jack-up rigs (of which nine were delivered to us) were delivered during 2018, representing an approximate 3% increase in the total worldwide fleet of competitive offshore drilling rigs since the end of 2017. As of June 12, 2019, there were approximately 62 newbuild jack-up rigs reported to be on order or under construction to be delivered no later than the end of 2020. Most of the newbuild jack-up rigs to be delivered no later than the end of 2020, including the eight newbuild jack-up rigs we have agreed to purchase, do not have drilling contracts in place. In addition, the supply of marketed offshore drilling rigs could further increase due to depressed market conditions resulting in an increase in uncontracted rigs as existing contracts expire. There is no assurance that the market in general or a geographic region in particular will be able to fully absorb the supply of new rigs in future periods. Any continued oversupply of drilling rigs could have a material adverse effect on our business, financial condition and results of operations.

13

The success of our business largely depends on the level of activity in the oil and gas industry, which can be significantly affected by volatile oil and natural gas prices.

The success of our business largely depends on the level of activity in offshore oil and natural gas exploration, development and production, which may be affected by conditions in the worldwide economy. Oil and natural gas prices, and market expectations of potential changes in these prices, significantly affect the level of drilling activity. Historically, when drilling activity and operator capital spending decline, utilization and dayrates also decline and drilling may be reduced or discontinued, resulting in an oversupply of drilling rigs. Oil and natural gas prices have historically been volatile, and oil prices have declined significantly since mid-2014 with prices in excess of $100 per barrel (as defined below), causing operators to reduce capital spending and cancel or defer existing programs, substantially reducing the opportunities for new drilling contracts. Oil prices have rebounded from the 12-year lows experienced during early 2016, and in 2017 experienced the first increase in average prices since 2014, with prices ranging from a low of $44 to a high of $67 per barrel. Oil prices experienced both increases and declines throughout 2018 and remained generally volatile, with prices ranging from a low of $50.47 to a high of $86.29 per barrel, according to Bloomberg. Oil prices have averaged approximately $66 per barrel during the first six months of 2019, around 23% higher than the cost of oil at the end of 2018, which was $54 per barrel. Oil prices increased gradually from January until April, reaching $75 per barrel, however, fell sharply toward the end of May and first half of June, dropping below $60 per barrel on June 12, 2019. In recent weeks, oil prices have increased. As of July 25, 2019, the price of oil was $63.13 per barrel. While oil prices have improved against historic lows, they have not improved to a level that supports increased rig demand which sufficiently absorbs existing rig supply and generates a meaningful increase in dayrates. We expect insufficient demand to continue as long as oil prices and rig supply remain at current levels. A lack of a meaningful and sustained recovery in oil and natural gas prices, continued volatility in prices or further price reductions, may cause our customers to maintain historically low levels or further reduce their overall level of activity, in which case demand for our services may decline and our results of operations may be adversely affected through lower rig utilization and/or low dayrates. Numerous factors may affect oil and natural gas prices and the level of demand for our services, including:

| • | regional and global economic conditions and changes therein; |

| • | oil and natural gas supply and demand; |

| • | expectations regarding future energy prices; |

| • | the ability of the Organization of the Petroleum Exporting Countries (“OPEC”) to reach further agreements to set and maintain production levels and pricing and to implement existing and future agreements; |

| • | the level of production by non-OPEC countries; |

| • | capital allocation decisions by our customers, including the relative economics of offshore development versus onshore prospects; |

| • | tax policy; |

| • | advances in exploration and development technology; |

| • | costs associated with exploring for, developing, producing and delivering oil and natural gas; |

| • | the rate of discovery of new oil and gas reserves and the rate of decline of existing oil and gas reserves; |

| • | trade policies and sanctions imposed on oil-producing countries or the lifting of such sanctions; |

| • | laws and government regulations that limit, restrict or prohibit exploration and development of oil and natural gas in various jurisdictions, or materially increase the cost of such exploration and development; |

| • | the further development or success of shale technology to exploit oil and gas reserves; |

| • | available pipeline and other oil and gas transportation capacity; |

| • | the development and exploitation of alternative fuels; |

14

| • | laws and regulations relating to environmental matters, including those addressing alternative energy sources and the risks of global climate change; |

| • | changes in tax laws, regulations and policies; |

| • | merger, acquisition and divestiture activity among E&P Companies; |

| • | the availability of, and access to, suitable locations from which our customers can explore and produce hydrocarbons; |

| • | activities by non-governmental organizations to restrict the exploration, development and production of oil and gas in light of environmental considerations; |

| • | disruption to exploration and development activities due to hurricanes and other severe weather conditions and the risk thereof; |

| • | natural disasters or incidents resulting from operating hazards inherent in offshore drilling, such as oil spills; |

| • | the worldwide social and political environment, including uncertainty or instability resulting from changes in political leadership and environmental policies, changes in geopolitical-social views toward fossil fuels and renewable energy and changes in investors’ expectations regarding environmental, social and governance (ESG) matters; and |

| • | the worldwide military and political environment, including uncertainty or instability resulting from an escalation or additional outbreak of armed hostilities or other crises in oil or natural gas producing areas of the Middle East or geographic areas in which we operate, or acts of terrorism. |

Despite significant declines in capital spending and cancelled or deferred drilling programs by many operators since 2015, oil and gas production has not yet been reduced by amounts sufficient to result in a rebound in pricing to levels seen prior to the current downturn, and we may not see sufficient supply reductions or a resulting rebound in pricing for an extended period of time or at all. Further, any agreements of OPEC and certain non-OPEC countries to freeze and/or cut production may not be fully realized. The lack of actual production cuts or freezes, or the perceived risk that OPEC countries may not comply with such agreements, may result in depressed oil and gas prices for an extended period of time. In addition, higher oil and gas prices may not necessarily translate into increased activity, and even during periods of high oil and gas prices, customers may cancel or curtail their drilling programs, or reduce their levels of capital expenditures for exploration and production for a variety of reasons, including their lack of success in exploration efforts. Any increase or reduction in drilling activity by our customers may not be uniform across different geographic regions. Locations where costs of drilling and production are relatively higher may be subject to greater reductions in activity or may recover more slowly. Such variation between regions may lead to the relocation of drilling rigs, concentrating drilling rigs in regions with relatively fewer reductions in activity leading to greater competition.

Advances in onshore exploration and development technologies, particularly with respect to onshore shale, could also result in our customers allocating more of their capital expenditure budgets to onshore exploration and production activities and less to offshore activities.

Moreover, there has historically been a strong link between the development of the world economy and the demand for energy, including oil and gas. An extended period of adverse development in the outlook for the world economy could also reduce the overall demand for oil and gas and for our services.

These factors could impact our revenues and profits and as a result limit our future growth prospects. Any significant decline in dayrates or utilization of our rigs could have a material adverse effect on our business, financial condition and results of operations. In addition, these risks could increase instability in the financial and insurance markets and make it more difficult for us to access capital and obtain insurance coverage that we consider adequate or are otherwise required by our contracts.

Down-cycles in the jack-up drilling industry and other factors may affect the market value of our jack-up rigs and the newbuild rigs we have agreed to purchase.

Consumer demand in the shallow-water offshore drilling market, or the jack-up drilling market, has been adversely impacted by trends in the price of oil since 2014 and has not yet recovered. As trends in the price of oil impact the spending plans of our customers, they may also affect the book or market values of our

15

jack-up rigs. The price of Brent crude oil fell from a high of $115.19 per barrel on June 19, 2014, to a low of $26.01 on January 20, 2016, and was $50.57 on December 31, 2018, and $63.39 on July 25, 2019. Although oil prices have recovered from historic lows, they remain generally volatile. If oil prices do not stabilize at favorable levels or we experience further oil price down-cycles, we expect customer demand will continue to be negatively affected. If the offshore drilling industry suffers adverse developments due to the price of oil in the future, the fair market value of our existing and newbuild jack-up rigs may decline. In addition, the fair market value of the jack-up rigs that we currently own, have agreed to acquire, or may acquire in the future, may decrease depending on a number of factors, including:

| • | the general economic and market conditions affecting the offshore contract drilling industry, including competition from other offshore contract drilling companies; |

| • | the types, sizes and ages of our jack-up rigs; |

| • | the supply and demand for our jack-up rigs; |

| • | the costs of newbuild jack-up rigs; |

| • | prevailing drilling services contract dayrates; |

| • | government or other regulations; and |

| • | technological advances. |

If jack-up rig values fall significantly, we may have to record an impairment in our financial statements, which could affect our results of operations. Certain of our competitors in the offshore drilling industry may have a larger or more diverse fleet and a more favorable capitalization than we do, which could allow them to better withstand any impairment recorded for their own fleets or the effects of a commodity price down-cycle. Additionally, if we sell one or more of our jack-up rigs at a time when drilling rig prices have fallen, we may incur a loss on disposal and a reduction in earnings, which may cause us to breach the covenants in certain of our finance agreements. Under certain of our Financing Arrangements, we are required to comply with loan-to-value or minimum-value-clauses, which could require us to post additional collateral or prepay a portion of the outstanding borrowings should the value of the jack-up rigs securing borrowings under each of such agreements decrease below required levels. If we are unable to comply with the covenants in certain of our financing agreements and we are unable to get a waiver, a default could occur under the terms of those agreements.

Our operations involve risks due their international nature.

We operate in various regions throughout the world. As a result of our international operations, we may be exposed to political and other uncertainties, including risks of:

| • | terrorist acts; |

| • | armed hostilities, war and civil disturbances; |

| • | acts of piracy, which have historically affected marine assets; |

| • | significant governmental influence over many aspects of local economies; |

| • | the seizure, nationalization or expropriation of property or equipment; |

| • | uncertainty of outcome in court proceedings in any jurisdiction where we may be subject to claims; |

| • | the repudiation, nullification, modification or renegotiation of contracts; |

| • | limitations on insurance coverage, such as war risk coverage, in certain areas; |

| • | political unrest; |

| • | monetary policy and foreign currency fluctuations and devaluations; |

| • | an inability to repatriate income or capital; |

| • | complications associated with repairing and replacing equipment in remote locations; |

| • | import-export quotas, wage and price controls, and the imposition of trade barriers; |

16

| • | imposition of, or changes in, local content laws and their enforcement, particularly in West Africa and Southeast Asia, where the legislatures are active in developing new legislation; |

| • | sanctions or trade embargoes; |

| • | compliance with various jurisdictional regulatory or financial requirements; |

| • | compliance with and changes to tax laws and interpretations; |

| • | other forms of government regulation and economic conditions that are beyond our control; and |

| • | government corruption. |

It is difficult to predict whether, and if so, when the risks referred to above may come to fruition and the impact thereof. Failure to comply with, or adapt to, applicable laws and regulations or other disturbances as they occur may subject us to criminal sanctions, civil remedies or other increases in costs, including fines, the denial of export privileges, injunctions, seizures of assets or the inability to otherwise remove our jack-up rig from the country in which it operates.

RISK FACTORS RELATED TO OUR BUSINESS

We may not be able to renew contracts which expire and our customers may seek to cancel or renegotiate their contracts, particularly in response to unfavorable industry conditions.

Many jack-up drilling contracts are short-term, and oil and natural gas companies tend to reduce activity levels quickly in response to declining oil and natural gas prices. Our jack-up drilling contracts typically range from three to twenty-four months, although this period may be longer in certain jurisdictions, including the Middle East. During oil price down-cycles, our customers may be unwilling to commit to long-term contracts. Short-term drilling contracts do not provide the stability or visibility of revenue that we would otherwise receive with long-term drilling contracts.

In addition, in difficult market conditions, some of our customers may seek to terminate their agreements with us or to renegotiate our contracts using various techniques, including threatening breaches of contract and applying commercial pressure. Some of our customers have the right to terminate their drilling contracts without cause upon the payment of an early termination fee or compensation for costs incurred up to termination. The general principle is that any such early termination payment, where applicable, shall compensate us for lost revenues less operating expenses for the remaining contract period; however, in some cases, any such payments may not fully compensate us for the loss of the drilling contract. Under certain circumstances our contracts may permit customers to terminate contracts early without any termination payment as a result of non-performance, periods of downtime or impaired performance caused by equipment or operational issues (typically after a specified remedial period), or sustained periods of downtime due to force majeure events beyond our control. In addition, state-owned oil company customers may have special termination rights by law.