Exhibit 99.1

Altus Midstream Company October 2018

Disclaimer FORWARD LOOKING STATEMENTS The information in this presentation and the oral statements made in connection therewith include “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of present or historical fact included in this presentation, regarding Apache Corporation’s (“Apache”) business, operations, and future financial and operating performance and forecasts, and Kayne Anderson Acquisition Corp.’s (“KAAC”) proposed business combination transaction with a wholly owned subsidiary of Apache involving certain midstream assets currently owned by Apache (the “business combination”), KAAC’s ability to consummate the business combination, the benefits of the business combination, and KAAC’s future financial performance following the business combination, as well as KAAC’s strategy, future operations and financial position, estimated revenues and losses, projected costs, prospects, plans and objectives of management are forward-looking statements. When used in this presentation, including any oral statements made in connection therewith, the words “could,” “should,” “will,” “may,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project,” the negative of such terms and other similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. These forward-looking statements are based on management’s current expectations and assumptions about future events and are based on currently available information as to the outcome and timing of future events. Except as otherwise required by applicable law, KAAC and Apache disclaim any duty to update any forward-looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this presentation. KAAC and Apache caution you that these forward-looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond the control of KAAC and Apache, incident to the development, production, gathering, transportation and sale of oil, natural gas and natural gas liquids. These risks include, but are not limited to, commodity price volatility, low prices for oil and/or natural gas, global economic conditions, uncertainties inherent in the joint venture pipeline options referred to herein, inflation, increased operating costs, construction delays and cost over-runs, lack of availability of equipment, supplies, services and qualified personnel, processing volumes and pipeline throughput, uncertainties related to new technologies, geographical concentration of operations, environmental risks, weather risks, security risks, drilling and other operating risks, regulatory changes, regulatory risks (including if KAAC were to become an investment company in the future), the uncertainty inherent in estimating oil and natural gas reserves and in projecting future rates of production, reductions in cash flow, lack of access to capital, KAAC’s ability to satisfy future cash obligations, restrictions in existing or future debt agreements or structured or other financing arrangements, the timing of development expenditures, managing growth and integration of acquisitions, and failure to realize expected value creation from acquisitions. Should one or more of the risks or uncertainties described in this presentation and the oral statements made in connection therewith occur, or should underlying assumptions prove incorrect, actual results and plans could differ materially from those expressed in any forward-looking statements. Additional information concerning these and other factors that may impact KAAC’s operations and projections can be found in its periodic filings with the Securities and Exchange Commission (the “SEC”), including its Annual Report on Form 10-K for the fiscal year ended December 31, 2017. KAAC’s SEC filings are available publicly on the SEC’s website at www.sec.gov. NO OFFER OR SOLICITATION This presentation is for informational purposes only and shall not constitute an offer to sell or the solicitation of an offer to buy any securities pursuant to the proposed business combination or otherwise, nor shall there be any sale of securities in any jurisdiction in which the offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act. RESERVE INFORMATION Reserve engineering is a process of estimating underground accumulations of hydrocarbons that cannot be measured in an exact way. The accuracy of any reserve estimate depends on the quality of available data, the interpretation of such data, and price and cost assumptions made by reserve engineers. In addition, the results of drilling, testing, and production activities may justify revisions of estimates that were made previously. If significant, such revisions could impact Apache’s strategy and change the schedule of any further production and development drilling. Accordingly, reserve estimates may differ significantly from the quantities of oil and natural gas that are ultimately recovered. Estimated Ultimate Recoveries, or “EURs,” refers to estimates of the sum of total gross remaining proved reserves per well as of a given date and cumulative production prior to such given date for developed wells. These quantities do not necessarily constitute or represent reserves as defined by the SEC and are not intended to be representative of all anticipated future well results. USE OF PROJECTIONS This presentation contains projections for Apache and KAAC, including with respect to its EBITDA, capital expenditures and distributable cash flow. KAAC’s independent auditors have not audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this presentation, and accordingly, have not expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this presentation. These projections are for illustrative purposes only and should not be relied upon as being necessarily indicative of future results. In this presentation, certain of the above-mentioned projected information has been repeated for purposes of providing comparisons with historical data. The assumptions and estimates underlying the projected information are inherently uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the projected information. Even if the assumptions and estimates are correct, projections are inherently uncertain due to a number of factors outside KAAC’s control. Accordingly, there can be no assurance that the projected results are indicative of the future performance of KAAC after completion of the business combination or that actual results will not differ materially from those presented in the projected information. Inclusions of the projected information in this presentation should not be regarded as a representation by any person that the results contained in the projected information will be achieved. 2 Disclaimer FORWARD LOOKING STATEMENTS The information in this presentation and the oral statements made in connection therewith include “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended. All statements, other than statements of present or historical fact included in this presentation, regarding Apache Corporation’s (“Apache”) business, operations, and future financial and operating performance and forecasts, and Kayne Anderson Acquisition Corp.’s (“KAAC”) proposed business combination transaction with a wholly owned subsidiary of Apache involving certain midstream assets currently owned by Apache (the “business combination”), KAAC’s ability to consummate the business combination, the benefits of the business combination, and KAAC’s future financial performance following the business combination, as well as KAAC’s strategy, future operations and financial position, estimated revenues and losses, projected costs, prospects, plans and objectives of management are forward-looking statements. When used in this presentation, including any oral statements made in connection therewith, the words “could,” “should,” “will,” “may,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project,” the negative of such terms and other similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. These forward-looking statements are based on management’s current expectations and assumptions about future events and are based on currently available information as to the outcome and timing of future events. Except as otherwise required by applicable law, KAAC and Apache disclaim any duty to update any forward-looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this presentation. KAAC and Apache caution you that these forward-looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond the control of KAAC and Apache, incident to the development, production, gathering, transportation and sale of oil, natural gas and natural gas liquids. These risks include, but are not limited to, commodity price volatility, low prices for oil and/or natural gas, global economic conditions, uncertainties inherent in the joint venture pipeline options referred to herein, inflation, increased operating costs, construction delays and cost over-runs, lack of availability of equipment, supplies, services and qualified personnel, processing volumes and pipeline throughput, uncertainties related to new technologies, geographical concentration of operations, environmental risks, weather risks, security risks, drilling and other operating risks, regulatory changes, regulatory risks (including if KAAC were to become an investment company in the future), the uncertainty inherent in estimating oil and natural gas reserves and in projecting future rates of production, reductions in cash flow, lack of access to capital, KAAC’s ability to satisfy future cash obligations, restrictions in existing or future debt agreements or structured or other financing arrangements, the timing of development expenditures, managing growth and integration of acquisitions, and failure to realize expected value creation from acquisitions. Should one or more of the risks or uncertainties described in this presentation and the oral statements made in connection therewith occur, or should underlying assumptions prove incorrect, actual results and plans could differ materially from those expressed in any forward-looking statements. Additional information concerning these and other factors that may impact KAAC’s operations and projections can be found in its periodic filings with the Securities and Exchange Commission (the “SEC”), including its Annual Report on Form 10-K for the fiscal year ended December 31, 2017. KAAC’s SEC filings are available publicly on the SEC’s website at www.sec.gov. NO OFFER OR SOLICITATION This presentation is for informational purposes only and shall not constitute an offer to sell or the solicitation of an offer to buy any securities pursuant to the proposed business combination or otherwise, nor shall there be any sale of securities in any jurisdiction in which the offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of any such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act. RESERVE INFORMATION Reserve engineering is a process of estimating underground accumulations of hydrocarbons that cannot be measured in an exact way. The accuracy of any reserve estimate depends on the quality of available data, the interpretation of such data, and price and cost assumptions made by reserve engineers. In addition, the results of drilling, testing, and production activities may justify revisions of estimates that were made previously. If significant, such revisions could impact Apache’s strategy and change the schedule of any further production and development drilling. Accordingly, reserve estimates may differ significantly from the quantities of oil and natural gas that are ultimately recovered. Estimated Ultimate Recoveries, or “EURs,” refers to estimates of the sum of total gross remaining proved reserves per well as of a given date and cumulative production prior to such given date for developed wells. These quantities do not necessarily constitute or represent reserves as defined by the SEC and are not intended to be representative of all anticipated future well results. USE OF PROJECTIONS This presentation contains projections for Apache and KAAC, including with respect to its EBITDA, capital expenditures and distributable cash flow. KAAC’s independent auditors have not audited, reviewed, compiled or performed any procedures with respect to the projections for the purpose of their inclusion in this presentation, and accordingly, have not expressed an opinion or provided any other form of assurance with respect thereto for the purpose of this presentation. These projections are for illustrative purposes only and should not be relied upon as being necessarily indicative of future results. In this presentation, certain of the above-mentioned projected information has been repeated for purposes of providing comparisons with historical data. The assumptions and estimates underlying the projected information are inherently uncertain and are subject to a wide variety of significant business, economic and competitive risks and uncertainties that could cause actual results to differ materially from those contained in the projected information. Even if the assumptions and estimates are correct, projections are inherently uncertain due to a number of factors outside KAAC’s control. Accordingly, there can be no assurance that the projected results are indicative of the future performance of KAAC after completion of the business combination or that actual results will not differ materially from those presented in the projected information. Inclusions of the projected information in this presentation should not be regarded as a representation by any person that the results contained in the projected information will be achieved. 2

Disclaimer USE OF NON-GAAP FINANCIAL MEASURES This presentation includes non-GAAP financial measures, including EBITDA and distributable cash flow of KAAC. KAAC believes EBITDA and distributable cash flow are useful because they allow KAAC to more effectively evaluate its operating performance and compare the results of its operations from period to period and against its peers without regard to financing methods or capital structure. KAAC does not consider these non-GAAP measures in isolation or as an alternative to similar financial measures determined in accordance with GAAP. The computations of EBITDA and distributable cash flow may not be comparable to other similarly titled measures of other companies. KAAC excludes certain items from net (loss) income in arriving at EBITDA and distributable cash flow because these amounts can vary substantially from company to company within its industry depending upon accounting methods and book values of assets, capital structures and the method by which the assets were acquired. EBITDA and distributable cash flow should not be considered an alternative to, or more meaningful than, net income as determined in accordance with GAAP or as indicators of operating performance. Certain items excluded from EBITDA and distributable cash flow are significant components in understanding and assessing a company’s financial performance, such as a company’s cost of capital and tax structure, as well as the historic costs of depreciable assets, none of which are components of EBITDA or distributable cash flow. KAAC’s presentation of EBITDA and distributable cash flow should not be construed as an inference that its results will be unaffected by unusual or non-recurring terms. INDUSTRY AND MARKET DATA This presentation has been prepared by KAAC and Apache and includes market data and other statistical information from sources believed by KAAC and Apache to be reliable, including independent industry publications, governmental publications or other published independent sources. Some data is also based on the good faith estimates of KAAC and Apache, which are derived from their review of internal sources as well as the independent sources described above. Although KAAC and Apache believe these sources are reliable, they have not independently verified the information and cannot guarantee its accuracy and completeness. TRADEMARKS AND TRADE NAMES KAAC and Apache own or have rights to various trademarks, service marks, and trade names that they use in connection with the operation of their respective businesses. This presentation also contains trademarks, service marks, and trade names of third parties, which are the property of their respective owners. The use or display of third parties’ trademarks, service marks, trade names, or products in this presentation is not intended to, and does not imply, a relationship with KAAC or Apache, or an endorsement or sponsorship by or of KAAC or Apache. Solely for convenience, the trademarks, service marks, and trade names referred to in this presentation may appear without the ®, TM, or SM symbols, but such references are not intended to indicate, in any way, that KAAC or Apache will not assert, to the fullest extent under applicable law, their rights or the right of the applicable licensor to these trademarks, service marks, and trade names. “ALPINE HIGH” and are trademarks of Apache Corporation. IMPORTANT INFORMATION FOR INVESTORS AND STOCKHOLDERS In connection with the proposed business combination, KAAC has filed a preliminary proxy statement with the SEC. The definitive proxy statement and other relevant documents will be sent or given to the stockholders of KAAC and will contain important information about the proposed business combination and related matters. KAAC stockholders and other interested persons are advised to read, when available, the proxy statement in connection with KAAC’s solicitation of proxies for the special meeting of stockholders to be held to approve the business combination because the proxy statement will contain important information about the proposed business combination. When available, the definitive proxy statement will be mailed to KAAC stockholders as of a record date to be established for voting on the business combination. Stockholders will also be able to obtain copies of the proxy statement, without charge, once available, at the SEC’s website at www.sec.gov. In addition, stockholders will be able to obtain free copies of the proxy statement by directing a request to: Kayne Anderson Acquisition Corp., 811 Main Street, Suite 1400, Houston, Texas 77002, email: thart@kaynecapital.com, Attn: Terry Hart. PARTICIPANTS IN SOLICITATION KAAC, Apache and their respective directors and officers may be deemed participants in the solicitation of proxies of KAAC’s stockholders in connection with the proposed business combination. KAAC stockholders and other interested persons may obtain, without charge, more detailed information regarding the directors and officers of KAAC in KAAC’s Annual Report on Form 10-K for the year ended December 31, 2017 filed with the SEC on March 27, 2018 and the proposed directors and officers of KAAC in KAAC’s definitive proxy statement, when it becomes available. Additional information will be available in the definitive proxy statement when it becomes available. 3 Disclaimer USE OF NON-GAAP FINANCIAL MEASURES This presentation includes non-GAAP financial measures, including EBITDA and distributable cash flow of KAAC. KAAC believes EBITDA and distributable cash flow are useful because they allow KAAC to more effectively evaluate its operating performance and compare the results of its operations from period to period and against its peers without regard to financing methods or capital structure. KAAC does not consider these non-GAAP measures in isolation or as an alternative to similar financial measures determined in accordance with GAAP. The computations of EBITDA and distributable cash flow may not be comparable to other similarly titled measures of other companies. KAAC excludes certain items from net (loss) income in arriving at EBITDA and distributable cash flow because these amounts can vary substantially from company to company within its industry depending upon accounting methods and book values of assets, capital structures and the method by which the assets were acquired. EBITDA and distributable cash flow should not be considered an alternative to, or more meaningful than, net income as determined in accordance with GAAP or as indicators of operating performance. Certain items excluded from EBITDA and distributable cash flow are significant components in understanding and assessing a company’s financial performance, such as a company’s cost of capital and tax structure, as well as the historic costs of depreciable assets, none of which are components of EBITDA or distributable cash flow. KAAC’s presentation of EBITDA and distributable cash flow should not be construed as an inference that its results will be unaffected by unusual or non-recurring terms. INDUSTRY AND MARKET DATA This presentation has been prepared by KAAC and Apache and includes market data and other statistical information from sources believed by KAAC and Apache to be reliable, including independent industry publications, governmental publications or other published independent sources. Some data is also based on the good faith estimates of KAAC and Apache, which are derived from their review of internal sources as well as the independent sources described above. Although KAAC and Apache believe these sources are reliable, they have not independently verified the information and cannot guarantee its accuracy and completeness. TRADEMARKS AND TRADE NAMES KAAC and Apache own or have rights to various trademarks, service marks, and trade names that they use in connection with the operation of their respective businesses. This presentation also contains trademarks, service marks, and trade names of third parties, which are the property of their respective owners. The use or display of third parties’ trademarks, service marks, trade names, or products in this presentation is not intended to, and does not imply, a relationship with KAAC or Apache, or an endorsement or sponsorship by or of KAAC or Apache. Solely for convenience, the trademarks, service marks, and trade names referred to in this presentation may appear without the ®, TM, or SM symbols, but such references are not intended to indicate, in any way, that KAAC or Apache will not assert, to the fullest extent under applicable law, their rights or the right of the applicable licensor to these trademarks, service marks, and trade names. “ALPINE HIGH” and are trademarks of Apache Corporation. IMPORTANT INFORMATION FOR INVESTORS AND STOCKHOLDERS In connection with the proposed business combination, KAAC has filed a preliminary proxy statement with the SEC. The definitive proxy statement and other relevant documents will be sent or given to the stockholders of KAAC and will contain important information about the proposed business combination and related matters. KAAC stockholders and other interested persons are advised to read, when available, the proxy statement in connection with KAAC’s solicitation of proxies for the special meeting of stockholders to be held to approve the business combination because the proxy statement will contain important information about the proposed business combination. When available, the definitive proxy statement will be mailed to KAAC stockholders as of a record date to be established for voting on the business combination. Stockholders will also be able to obtain copies of the proxy statement, without charge, once available, at the SEC’s website at www.sec.gov. In addition, stockholders will be able to obtain free copies of the proxy statement by directing a request to: Kayne Anderson Acquisition Corp., 811 Main Street, Suite 1400, Houston, Texas 77002, email: thart@kaynecapital.com, Attn: Terry Hart. PARTICIPANTS IN SOLICITATION KAAC, Apache and their respective directors and officers may be deemed participants in the solicitation of proxies of KAAC’s stockholders in connection with the proposed business combination. KAAC stockholders and other interested persons may obtain, without charge, more detailed information regarding the directors and officers of KAAC in KAAC’s Annual Report on Form 10-K for the year ended December 31, 2017 filed with the SEC on March 27, 2018 and the proposed directors and officers of KAAC in KAAC’s definitive proxy statement, when it becomes available. Additional information will be available in the definitive proxy statement when it becomes available. 3

Introduction 4 Introduction 4

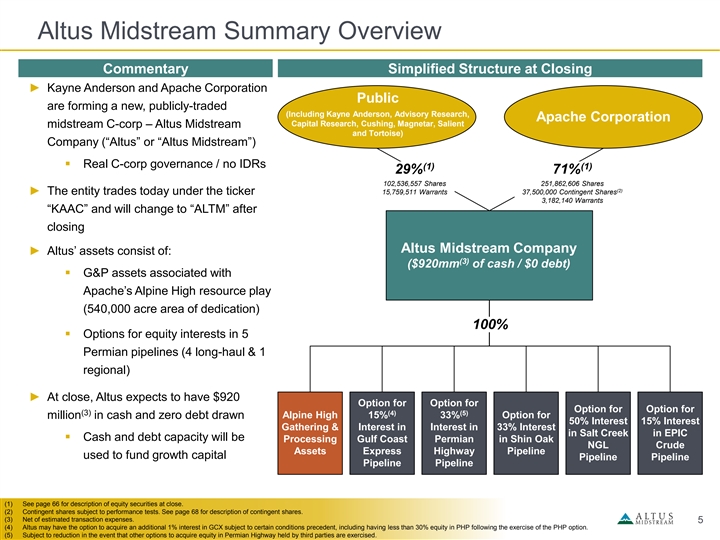

Altus Midstream Summary Overview Commentary Simplified Structure at Closing ► Kayne Anderson and Apache Corporation Public are forming a new, publicly-traded (Including Kayne Anderson, Advisory Research, Apache Corporation Capital Research, Cushing, Magnetar, Salient midstream C-corp – Altus Midstream and Tortoise) Company (“Altus” or “Altus Midstream”) § Real C-corp governance / no IDRs (1) (1) 29% 71% 102,536,557 Shares 251,862,606 Shares (2) 15,759,511 Warrants 37,500,000 Contingent Shares ► The entity trades today under the ticker 3,182,140 Warrants “KAAC” and will change to “ALTM” after closing Altus Midstream Company ► Altus’ assets consist of: (3) ($920mm of cash / $0 debt) § G&P assets associated with Apache’s Alpine High resource play (540,000 acre area of dedication) 100% § Options for equity interests in 5 Permian pipelines (4 long-haul & 1 regional) ► At close, Altus expects to have $920 Option for Option for Option for Option for (3) (4) (5) Alpine High 15% 33% Option for million in cash and zero debt drawn 50% Interest 15% Interest Gathering & Interest in Interest in 33% Interest in Salt Creek in EPIC § Cash and debt capacity will be Processing Gulf Coast Permian in Shin Oak NGL Crude Assets Express Highway Pipeline used to fund growth capital Pipeline Pipeline Pipeline Pipeline (1) See page 66 for description of equity securities at close. (2) Contingent shares subject to performance tests. See page 68 for description of contingent shares. (3) Net of estimated transaction expenses. 5 (4) Altus may have the option to acquire an additional 1% interest in GCX subject to certain conditions precedent, including having less than 30% equity in PHP following the exercise of the PHP option. (5) Subject to reduction in the event that other options to acquire equity in Permian Highway held by third parties are exercised. Altus Midstream Summary Overview Commentary Simplified Structure at Closing ► Kayne Anderson and Apache Corporation Public are forming a new, publicly-traded (Including Kayne Anderson, Advisory Research, Apache Corporation Capital Research, Cushing, Magnetar, Salient midstream C-corp – Altus Midstream and Tortoise) Company (“Altus” or “Altus Midstream”) § Real C-corp governance / no IDRs (1) (1) 29% 71% 102,536,557 Shares 251,862,606 Shares (2) 15,759,511 Warrants 37,500,000 Contingent Shares ► The entity trades today under the ticker 3,182,140 Warrants “KAAC” and will change to “ALTM” after closing Altus Midstream Company ► Altus’ assets consist of: (3) ($920mm of cash / $0 debt) § G&P assets associated with Apache’s Alpine High resource play (540,000 acre area of dedication) 100% § Options for equity interests in 5 Permian pipelines (4 long-haul & 1 regional) ► At close, Altus expects to have $920 Option for Option for Option for Option for (3) (4) (5) Alpine High 15% 33% Option for million in cash and zero debt drawn 50% Interest 15% Interest Gathering & Interest in Interest in 33% Interest in Salt Creek in EPIC § Cash and debt capacity will be Processing Gulf Coast Permian in Shin Oak NGL Crude Assets Express Highway Pipeline used to fund growth capital Pipeline Pipeline Pipeline Pipeline (1) See page 66 for description of equity securities at close. (2) Contingent shares subject to performance tests. See page 68 for description of contingent shares. (3) Net of estimated transaction expenses. 5 (4) Altus may have the option to acquire an additional 1% interest in GCX subject to certain conditions precedent, including having less than 30% equity in PHP following the exercise of the PHP option. (5) Subject to reduction in the event that other options to acquire equity in Permian Highway held by third parties are exercised.

New Way to Invest in Midstream…and it’s in the Permian! Sponsor controls production & development Super-system with large contiguous acreage dedication Pure-play Permian Integrated Permian to Gulf Coast midstream value chain JV pipelines provide diversity and long term contracts C-corp structure with an alignment of interests Conservative balance sheet; self-financing 6 New Way to Invest in Midstream…and it’s in the Permian! Sponsor controls production & development Super-system with large contiguous acreage dedication Pure-play Permian Integrated Permian to Gulf Coast midstream value chain JV pipelines provide diversity and long term contracts C-corp structure with an alignment of interests Conservative balance sheet; self-financing 6

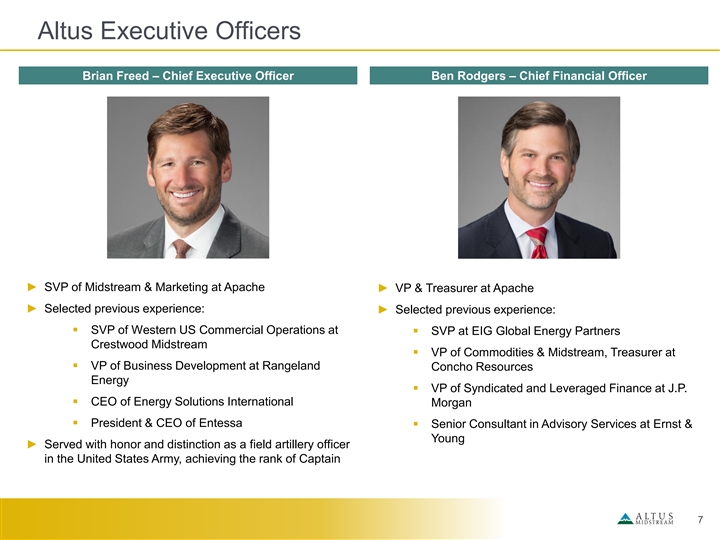

Altus Executive Officers Brian Freed – Chief Executive Officer Ben Rodgers – Chief Financial Officer ► SVP of Midstream & Marketing at Apache ► VP & Treasurer at Apache ► Selected previous experience: ► Selected previous experience: § SVP of Western US Commercial Operations at § SVP at EIG Global Energy Partners Crestwood Midstream § VP of Commodities & Midstream, Treasurer at § VP of Business Development at Rangeland Concho Resources Energy § VP of Syndicated and Leveraged Finance at J.P. § CEO of Energy Solutions International Morgan § President & CEO of Entessa § Senior Consultant in Advisory Services at Ernst & Young ► Served with honor and distinction as a field artillery officer in the United States Army, achieving the rank of Captain 7 Altus Executive Officers Brian Freed – Chief Executive Officer Ben Rodgers – Chief Financial Officer ► SVP of Midstream & Marketing at Apache ► VP & Treasurer at Apache ► Selected previous experience: ► Selected previous experience: § SVP of Western US Commercial Operations at § SVP at EIG Global Energy Partners Crestwood Midstream § VP of Commodities & Midstream, Treasurer at § VP of Business Development at Rangeland Concho Resources Energy § VP of Syndicated and Leveraged Finance at J.P. § CEO of Energy Solutions International Morgan § President & CEO of Entessa § Senior Consultant in Advisory Services at Ernst & Young ► Served with honor and distinction as a field artillery officer in the United States Army, achieving the rank of Captain 7

Other Presenters / Key Team Members ► Member of the Advisory Board at EV Private Equity Navneet Behl ► Member of team for all exploration completions for all unconventional plays within EOG from 2005 to 2014 th Apache VP of Operations of NAM ► Alpine High is the 4 unconventional play start-up, previous ones being Barnett Johnson County, Barnett Extension Counties and Eagle Ford Oil Play Unconventional Resources ► Over 24 years of experience in the petroleum industry ► Founding member of the executive leadership team that oversaw the formation of Coral Energy Bob Bourne ► Former SVP of Business Development at American Midstream Partners Apache VP, Business Development ► Former Principal of Costar Midstream LLC – Midstream and Marketing ► Former CEO of Gas Solutions ► Former Managing Director of investment banking and head of Securities and Research at Tudor, Pickering, Holt & Co. Mark Meyer ► Former President, Co-founder of upstream-oriented equity strategies at RR Advisors Apache SVP of Energy Technology ► Previously Lead E&P analyst at Simmons & Company International and Goldman Sachs Strategies ► Various reservoir, production and drilling engineering assignments with Exxon, Chevron and Union Texas ► Former VP of Business Development at Crestwood Midstream Jonathan Greenberg ► Former Equity Research Analyst and Private Equity Associate at Kayne Anderson Capital Advisors Apache Manager of Midstream Asset Strategy ► Former Investment Banking Analyst at Deutsche Bank ► Former Head of Navarro Midstream (midstream division of Lewis Energy) Pete Kirsch ► Former SVP of EH&S and Compliance Services at Enable Midstream Apache Region Manager, ► Former SVP of Operations & Engineering at CenterPoint Energy Midstream Operations ► Approximately 30 years experience in midstream space ► Managing Partner at Kayne Anderson Capital Advisors Kevin McCarthy KAAC Chairman ► CEO of Kayne Anderson’s closed-end funds (KYN and KMF) Altus Midstream Director ► Former Global Head of Energy Investment Banking at UBS ► 35+ years of energy industry experience Bob Purgason ► 20+ years at Williams in various senior positions in NGLs, gas marketing, operations, M&A and major project development KAAC CEO ► Former COO of Chesapeake Midstream until its sale to Williams in 2015 Altus Midstream Director ► Former COO of Crosstex Energy 8 Other Presenters / Key Team Members ► Member of the Advisory Board at EV Private Equity Navneet Behl ► Member of team for all exploration completions for all unconventional plays within EOG from 2005 to 2014 th Apache VP of Operations of NAM ► Alpine High is the 4 unconventional play start-up, previous ones being Barnett Johnson County, Barnett Extension Counties and Eagle Ford Oil Play Unconventional Resources ► Over 24 years of experience in the petroleum industry ► Founding member of the executive leadership team that oversaw the formation of Coral Energy Bob Bourne ► Former SVP of Business Development at American Midstream Partners Apache VP, Business Development ► Former Principal of Costar Midstream LLC – Midstream and Marketing ► Former CEO of Gas Solutions ► Former Managing Director of investment banking and head of Securities and Research at Tudor, Pickering, Holt & Co. Mark Meyer ► Former President, Co-founder of upstream-oriented equity strategies at RR Advisors Apache SVP of Energy Technology ► Previously Lead E&P analyst at Simmons & Company International and Goldman Sachs Strategies ► Various reservoir, production and drilling engineering assignments with Exxon, Chevron and Union Texas ► Former VP of Business Development at Crestwood Midstream Jonathan Greenberg ► Former Equity Research Analyst and Private Equity Associate at Kayne Anderson Capital Advisors Apache Manager of Midstream Asset Strategy ► Former Investment Banking Analyst at Deutsche Bank ► Former Head of Navarro Midstream (midstream division of Lewis Energy) Pete Kirsch ► Former SVP of EH&S and Compliance Services at Enable Midstream Apache Region Manager, ► Former SVP of Operations & Engineering at CenterPoint Energy Midstream Operations ► Approximately 30 years experience in midstream space ► Managing Partner at Kayne Anderson Capital Advisors Kevin McCarthy KAAC Chairman ► CEO of Kayne Anderson’s closed-end funds (KYN and KMF) Altus Midstream Director ► Former Global Head of Energy Investment Banking at UBS ► 35+ years of energy industry experience Bob Purgason ► 20+ years at Williams in various senior positions in NGLs, gas marketing, operations, M&A and major project development KAAC CEO ► Former COO of Chesapeake Midstream until its sale to Williams in 2015 Altus Midstream Director ► Former COO of Crosstex Energy 8

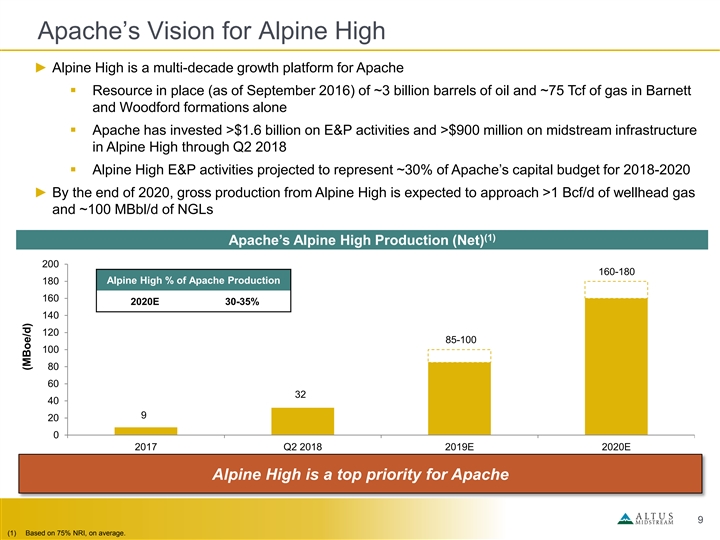

Apache’s Vision for Alpine High ► Alpine High is a multi-decade growth platform for Apache § Resource in place (as of September 2016) of ~3 billion barrels of oil and ~75 Tcf of gas in Barnett and Woodford formations alone § Apache has invested >$1.6 billion on E&P activities and >$900 million on midstream infrastructure in Alpine High through Q2 2018 § Alpine High E&P activities projected to represent ~30% of Apache’s capital budget for 2018-2020 ► By the end of 2020, gross production from Alpine High is expected to approach >1 Bcf/d of wellhead gas and ~100 MBbl/d of NGLs (1) Apache’s Alpine High Production (Net) 200 160-180 Alpine High % of Apache Production 180 160 2020E 30-35% 140 120 85-100 100 80 60 32 40 9 20 0 2017 Q2 2018 2019E 2020E Alpine High is a top priority for Apache 9 (1) Based on 75% NRI, on average. (MBoe/d) Apache’s Vision for Alpine High ► Alpine High is a multi-decade growth platform for Apache § Resource in place (as of September 2016) of ~3 billion barrels of oil and ~75 Tcf of gas in Barnett and Woodford formations alone § Apache has invested >$1.6 billion on E&P activities and >$900 million on midstream infrastructure in Alpine High through Q2 2018 § Alpine High E&P activities projected to represent ~30% of Apache’s capital budget for 2018-2020 ► By the end of 2020, gross production from Alpine High is expected to approach >1 Bcf/d of wellhead gas and ~100 MBbl/d of NGLs (1) Apache’s Alpine High Production (Net) 200 160-180 Alpine High % of Apache Production 180 160 2020E 30-35% 140 120 85-100 100 80 60 32 40 9 20 0 2017 Q2 2018 2019E 2020E Alpine High is a top priority for Apache 9 (1) Based on 75% NRI, on average. (MBoe/d)

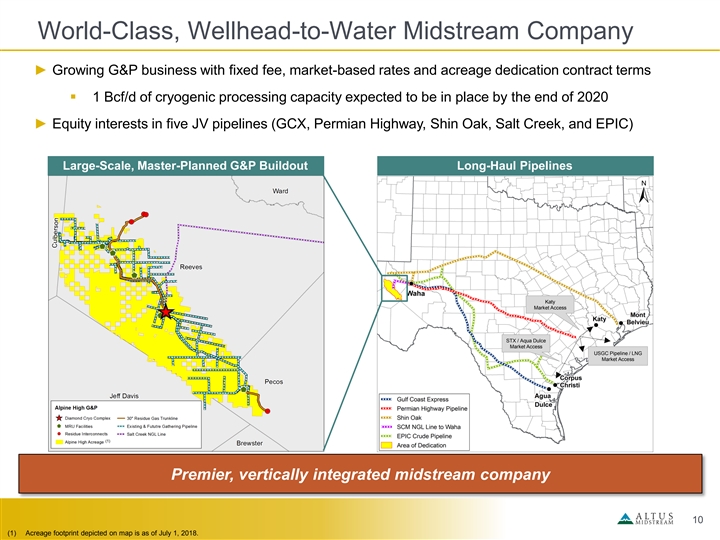

World-Class, Wellhead-to-Water Midstream Company ► Growing G&P business with fixed fee, market-based rates and acreage dedication contract terms § 1 Bcf/d of cryogenic processing capacity expected to be in place by the end of 2020 ► Equity interests in five JV pipelines (GCX, Permian Highway, Shin Oak, Salt Creek, and EPIC) Large-Scale, Master-Planned G&P Buildout Long-Haul Pipelines Katy Market Access STX / Aqua Dulce Market Access USGC Pipeline / LNG Market Access (1) Premier, vertically integrated midstream company 10 (1) Acreage footprint depicted on map is as of July 1, 2018. World-Class, Wellhead-to-Water Midstream Company ► Growing G&P business with fixed fee, market-based rates and acreage dedication contract terms § 1 Bcf/d of cryogenic processing capacity expected to be in place by the end of 2020 ► Equity interests in five JV pipelines (GCX, Permian Highway, Shin Oak, Salt Creek, and EPIC) Large-Scale, Master-Planned G&P Buildout Long-Haul Pipelines Katy Market Access STX / Aqua Dulce Market Access USGC Pipeline / LNG Market Access (1) Premier, vertically integrated midstream company 10 (1) Acreage footprint depicted on map is as of July 1, 2018.

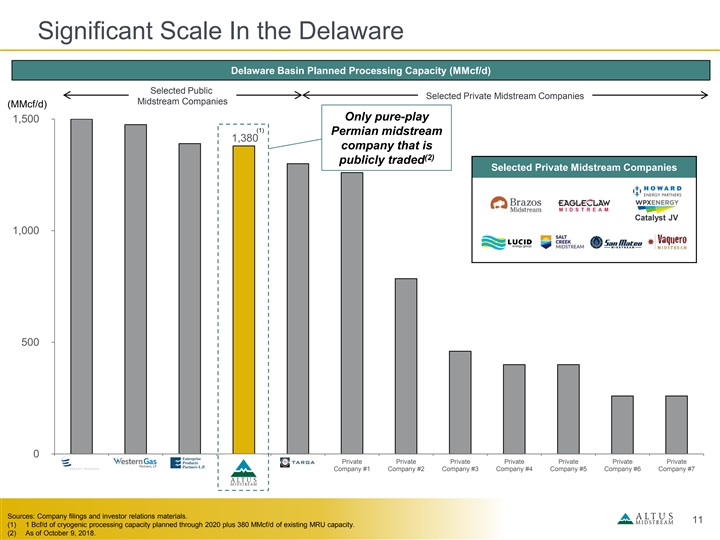

Significant Scale In the Delaware Delaware Basin Planned Processing Capacity (MMcf/d) Selected Public Selected Private Midstream Companies Midstream Companies (MMcf/d) Only pure-play 1,500 (1) Permian midstream 1,380 company that is (2) publicly traded Selected Private Midstream Companies Catalyst JV 1,000 500 0 ETE WES EPD Altus TRGP Private Private Private Private Private Private Private Company #1 Company #2 Company #3 Company #4 Company #5 Company #6 Company #7 Sources: Company filings and investor relations materials. 11 (1) 1 Bcf/d of cryogenic processing capacity planned through 2020 plus 380 MMcf/d of existing MRU capacity. (2) As of October 9, 2018. Significant Scale In the Delaware Delaware Basin Planned Processing Capacity (MMcf/d) Selected Public Selected Private Midstream Companies Midstream Companies (MMcf/d) Only pure-play 1,500 (1) Permian midstream 1,380 company that is (2) publicly traded Selected Private Midstream Companies Catalyst JV 1,000 500 0 ETE WES EPD Altus TRGP Private Private Private Private Private Private Private Company #1 Company #2 Company #3 Company #4 Company #5 Company #6 Company #7 Sources: Company filings and investor relations materials. 11 (1) 1 Bcf/d of cryogenic processing capacity planned through 2020 plus 380 MMcf/d of existing MRU capacity. (2) As of October 9, 2018.

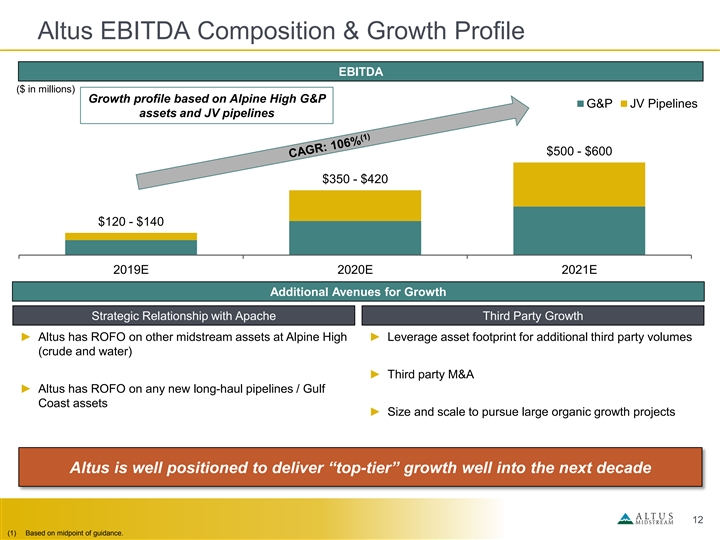

Altus EBITDA Composition & Growth Profile EBITDA ($ in millions) Growth profile based on Alpine High G&P G&P JV Pipelines assets and JV pipelines $500 - $600 $350 - $420 $120 - $140 2019E 2020E 2021E Additional Avenues for Growth Strategic Relationship with Apache Third Party Growth ► Altus has ROFO on other midstream assets at Alpine High ► Leverage asset footprint for additional third party volumes (crude and water) ► Third party M&A ► Altus has ROFO on any new long-haul pipelines / Gulf Coast assets ► Size and scale to pursue large organic growth projects Altus is well positioned to deliver “top-tier” growth well into the next decade 12 (1) Based on midpoint of guidance. Altus EBITDA Composition & Growth Profile EBITDA ($ in millions) Growth profile based on Alpine High G&P G&P JV Pipelines assets and JV pipelines $500 - $600 $350 - $420 $120 - $140 2019E 2020E 2021E Additional Avenues for Growth Strategic Relationship with Apache Third Party Growth ► Altus has ROFO on other midstream assets at Alpine High ► Leverage asset footprint for additional third party volumes (crude and water) ► Third party M&A ► Altus has ROFO on any new long-haul pipelines / Gulf Coast assets ► Size and scale to pursue large organic growth projects Altus is well positioned to deliver “top-tier” growth well into the next decade 12 (1) Based on midpoint of guidance.

Investment Merits ► Independent E&P with 64-year operating history and global footprint Premier E&P ► Dedicated to long-term development plan for Alpine High Sponsor ► Transaction achieves Apache’s desire to create a fully integrated midstream company (1) ► ~340,000 contiguous net acres; multi-decade inventory of drilling locations Exposure to World-Class ► More than 5,000 vertical feet of stacked pay Resource at Alpine High ► Alpine High expected to comprise 30-35% of Apache’s total production by 2020 ► Pure-play Permian public midstream company Unique Public Investment ► Exposure to full midstream value chain from Permian to the Gulf Coast Opportunity ► Depth of upstream inventory supports decades of robust cash flow growth ► Clear alignment of interests (C-corp governance / no incentive distribution rights) Differentiated, Simplified ► No leverage at formation; no need to issue common equity Corporate Structure ► Retaining and reinvesting cash flow in the business through 2020 13 (1) Acreage as of July 1, 2018. Investment Merits ► Independent E&P with 64-year operating history and global footprint Premier E&P ► Dedicated to long-term development plan for Alpine High Sponsor ► Transaction achieves Apache’s desire to create a fully integrated midstream company (1) ► ~340,000 contiguous net acres; multi-decade inventory of drilling locations Exposure to World-Class ► More than 5,000 vertical feet of stacked pay Resource at Alpine High ► Alpine High expected to comprise 30-35% of Apache’s total production by 2020 ► Pure-play Permian public midstream company Unique Public Investment ► Exposure to full midstream value chain from Permian to the Gulf Coast Opportunity ► Depth of upstream inventory supports decades of robust cash flow growth ► Clear alignment of interests (C-corp governance / no incentive distribution rights) Differentiated, Simplified ► No leverage at formation; no need to issue common equity Corporate Structure ► Retaining and reinvesting cash flow in the business through 2020 13 (1) Acreage as of July 1, 2018.

Questions? 14 Questions? 14

Altus Midstream Overview – Gathering & Processing 15 Altus Midstream Overview – Gathering & Processing 15

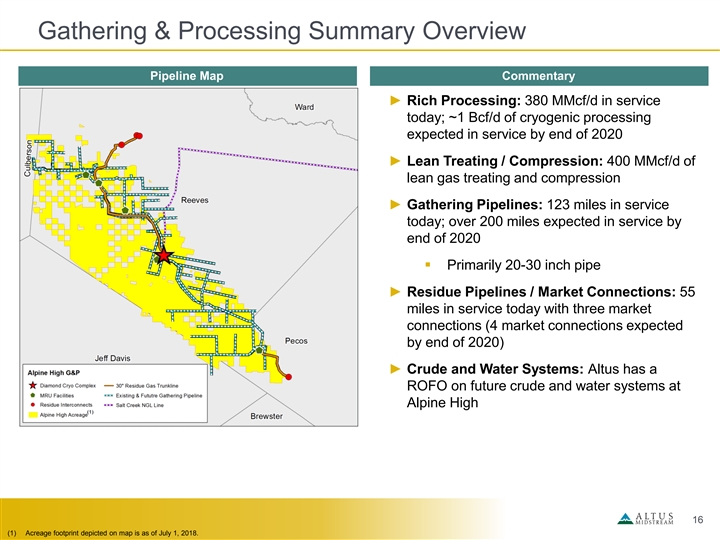

Gathering & Processing Summary Overview Pipeline Map Commentary ► Rich Processing: 380 MMcf/d in service today; ~1 Bcf/d of cryogenic processing expected in service by end of 2020 ► Lean Treating / Compression: 400 MMcf/d of lean gas treating and compression ► Gathering Pipelines: 123 miles in service today; over 200 miles expected in service by end of 2020 § Primarily 20-30 inch pipe ► Residue Pipelines / Market Connections: 55 miles in service today with three market connections (4 market connections expected by end of 2020) ► Crude and Water Systems: Altus has a ROFO on future crude and water systems at Alpine High (1) 16 (1) Acreage footprint depicted on map is as of July 1, 2018. Gathering & Processing Summary Overview Pipeline Map Commentary ► Rich Processing: 380 MMcf/d in service today; ~1 Bcf/d of cryogenic processing expected in service by end of 2020 ► Lean Treating / Compression: 400 MMcf/d of lean gas treating and compression ► Gathering Pipelines: 123 miles in service today; over 200 miles expected in service by end of 2020 § Primarily 20-30 inch pipe ► Residue Pipelines / Market Connections: 55 miles in service today with three market connections (4 market connections expected by end of 2020) ► Crude and Water Systems: Altus has a ROFO on future crude and water systems at Alpine High (1) 16 (1) Acreage footprint depicted on map is as of July 1, 2018.

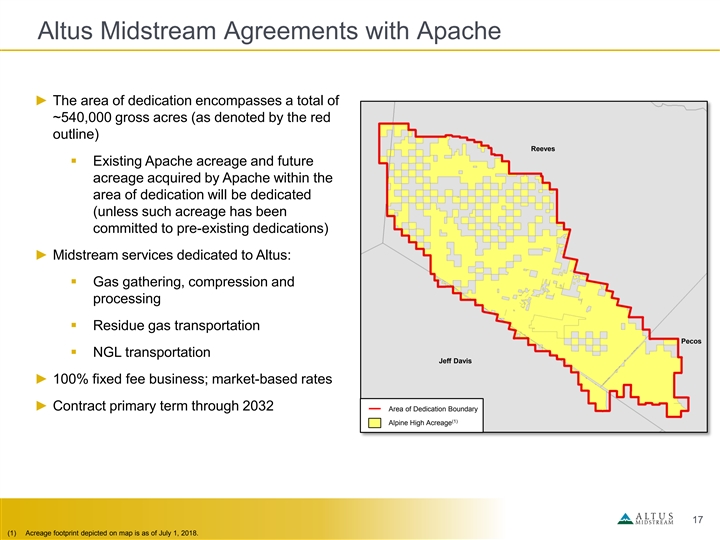

Altus Midstream Agreements with Apache ► The area of dedication encompasses a total of ~540,000 gross acres (as denoted by the red outline) Reeves § Existing Apache acreage and future acreage acquired by Apache within the area of dedication will be dedicated (unless such acreage has been committed to pre-existing dedications) ► Midstream services dedicated to Altus: § Gas gathering, compression and processing § Residue gas transportation Pecos § NGL transportation Jeff Davis ► 100% fixed fee business; market-based rates ► Contract primary term through 2032 Area of Dedication Boundary (1) Alpine High Acreage 17 (1) Acreage footprint depicted on map is as of July 1, 2018. Altus Midstream Agreements with Apache ► The area of dedication encompasses a total of ~540,000 gross acres (as denoted by the red outline) Reeves § Existing Apache acreage and future acreage acquired by Apache within the area of dedication will be dedicated (unless such acreage has been committed to pre-existing dedications) ► Midstream services dedicated to Altus: § Gas gathering, compression and processing § Residue gas transportation Pecos § NGL transportation Jeff Davis ► 100% fixed fee business; market-based rates ► Contract primary term through 2032 Area of Dedication Boundary (1) Alpine High Acreage 17 (1) Acreage footprint depicted on map is as of July 1, 2018.

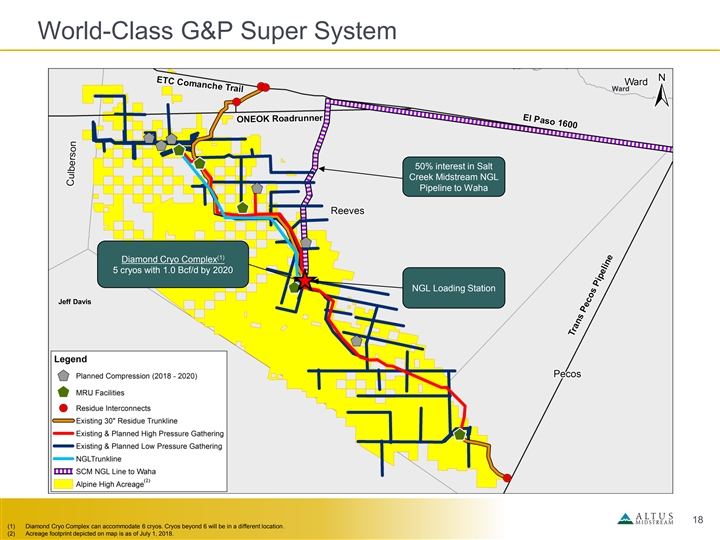

World-Class G&P Super System Ward 50% interest in Salt Creek Midstream NGL Pipeline to Waha (1) Diamond Cryo Complex 5 cryos with 1.0 Bcf/d by 2020 NGL Loading Station Jeff Davis (2) 18 (1) Diamond Cryo Complex can accommodate 6 cryos. Cryos beyond 6 will be in a different location. (2) Acreage footprint depicted on map is as of July 1, 2018. World-Class G&P Super System Ward 50% interest in Salt Creek Midstream NGL Pipeline to Waha (1) Diamond Cryo Complex 5 cryos with 1.0 Bcf/d by 2020 NGL Loading Station Jeff Davis (2) 18 (1) Diamond Cryo Complex can accommodate 6 cryos. Cryos beyond 6 will be in a different location. (2) Acreage footprint depicted on map is as of July 1, 2018.

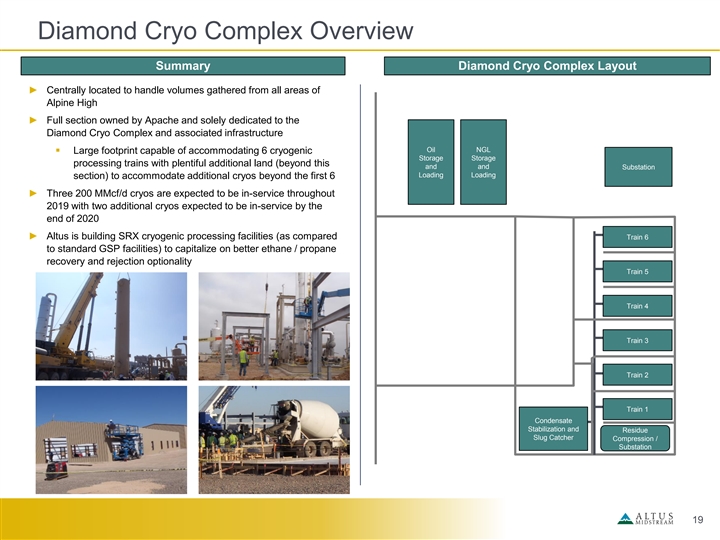

Diamond Cryo Complex Overview Summary Diamond Cryo Complex Layout ► Centrally located to handle volumes gathered from all areas of Alpine High ► Full section owned by Apache and solely dedicated to the Diamond Cryo Complex and associated infrastructure Oil NGL § Large footprint capable of accommodating 6 cryogenic Storage Storage processing trains with plentiful additional land (beyond this and and Substation Loading Loading section) to accommodate additional cryos beyond the first 6 ► Three 200 MMcf/d cryos are expected to be in-service throughout 2019 with two additional cryos expected to be in-service by the end of 2020 ► Altus is building SRX cryogenic processing facilities (as compared Train 6 to standard GSP facilities) to capitalize on better ethane / propane recovery and rejection optionality Train 5 Train 4 Train 3 Train 2 Train 1 Condensate Stabilization and Residue Slug Catcher Compression / Substation 19 Diamond Cryo Complex Overview Summary Diamond Cryo Complex Layout ► Centrally located to handle volumes gathered from all areas of Alpine High ► Full section owned by Apache and solely dedicated to the Diamond Cryo Complex and associated infrastructure Oil NGL § Large footprint capable of accommodating 6 cryogenic Storage Storage processing trains with plentiful additional land (beyond this and and Substation Loading Loading section) to accommodate additional cryos beyond the first 6 ► Three 200 MMcf/d cryos are expected to be in-service throughout 2019 with two additional cryos expected to be in-service by the end of 2020 ► Altus is building SRX cryogenic processing facilities (as compared Train 6 to standard GSP facilities) to capitalize on better ethane / propane recovery and rejection optionality Train 5 Train 4 Train 3 Train 2 Train 1 Condensate Stabilization and Residue Slug Catcher Compression / Substation 19

Diamond Cryo Complex: Cryo Train #1 Amine Unit Cryo Unit Area Refrigeration Dehy Unit Compression Hot Oil Pumps Hot Oil Heaters Thermal Oxidizer Instrument Air Pkg MCC Bldgs Main N/S Rack 20 Diamond Cryo Complex: Cryo Train #1 Amine Unit Cryo Unit Area Refrigeration Dehy Unit Compression Hot Oil Pumps Hot Oil Heaters Thermal Oxidizer Instrument Air Pkg MCC Bldgs Main N/S Rack 20

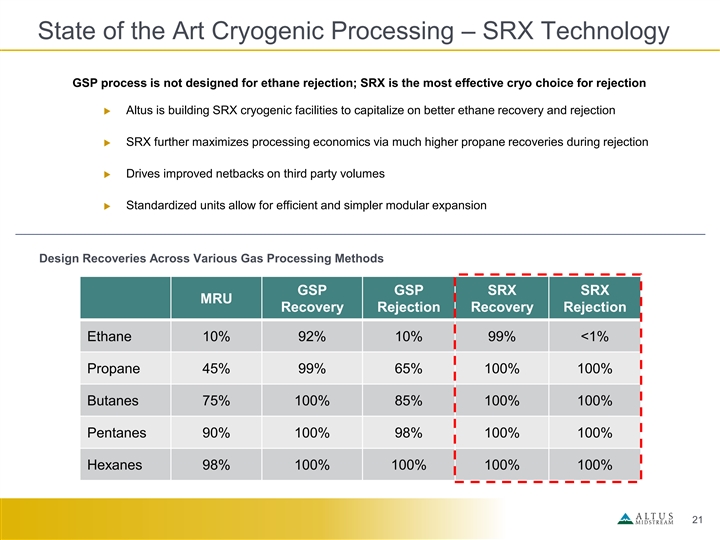

State of the Art Cryogenic Processing – SRX Technology GSP process is not designed for ethane rejection; SRX is the most effective cryo choice for rejection u Altus is building SRX cryogenic facilities to capitalize on better ethane recovery and rejection u SRX further maximizes processing economics via much higher propane recoveries during rejection u Drives improved netbacks on third party volumes u Standardized units allow for efficient and simpler modular expansion Design Recoveries Across Various Gas Processing Methods GSP GSP SRX SRX MRU Recovery Rejection Recovery Rejection Ethane 10% 92% 10% 99% <1% Propane 45% 99% 65% 100% 100% Butanes 75% 100% 85% 100% 100% Pentanes 90% 100% 98% 100% 100% Hexanes 98% 100% 100% 100% 100% 21 State of the Art Cryogenic Processing – SRX Technology GSP process is not designed for ethane rejection; SRX is the most effective cryo choice for rejection u Altus is building SRX cryogenic facilities to capitalize on better ethane recovery and rejection u SRX further maximizes processing economics via much higher propane recoveries during rejection u Drives improved netbacks on third party volumes u Standardized units allow for efficient and simpler modular expansion Design Recoveries Across Various Gas Processing Methods GSP GSP SRX SRX MRU Recovery Rejection Recovery Rejection Ethane 10% 92% 10% 99% <1% Propane 45% 99% 65% 100% 100% Butanes 75% 100% 85% 100% 100% Pentanes 90% 100% 98% 100% 100% Hexanes 98% 100% 100% 100% 100% 21

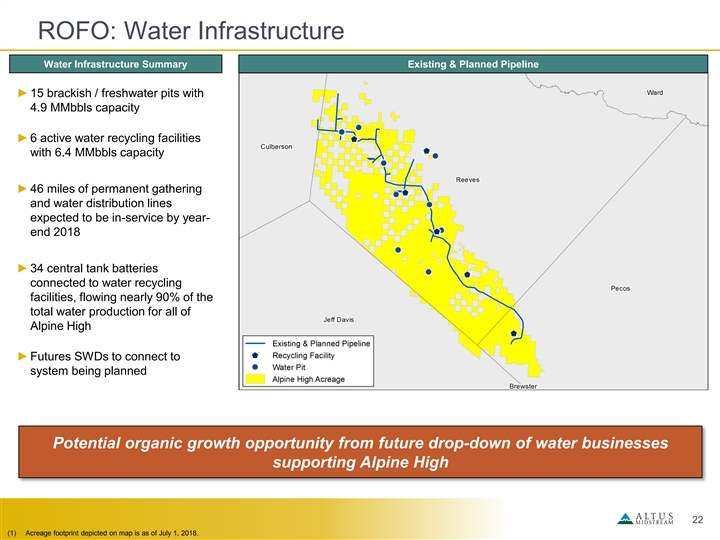

ROFO: Water Infrastructure Water Infrastructure Summary Existing & Planned Pipeline ►15 brackish / freshwater pits with 4.9 MMbbls capacity ►6 active water recycling facilities with 6.4 MMbbls capacity ►46 miles of permanent gathering and water distribution lines expected to be in-service by year- end 2018 ►34 central tank batteries connected to water recycling facilities, flowing nearly 90% of the total water production for all of Alpine High ► Futures SWDs to connect to system being planned (1) Potential organic growth opportunity from future drop-down of water businesses supporting Alpine High 22 (1) Acreage footprint depicted on map is as of July 1, 2018. ROFO: Water Infrastructure Water Infrastructure Summary Existing & Planned Pipeline ►15 brackish / freshwater pits with 4.9 MMbbls capacity ►6 active water recycling facilities with 6.4 MMbbls capacity ►46 miles of permanent gathering and water distribution lines expected to be in-service by year- end 2018 ►34 central tank batteries connected to water recycling facilities, flowing nearly 90% of the total water production for all of Alpine High ► Futures SWDs to connect to system being planned (1) Potential organic growth opportunity from future drop-down of water businesses supporting Alpine High 22 (1) Acreage footprint depicted on map is as of July 1, 2018.

Other ROFO Opportunities ► Altus will have a right of first offer on additional equity options ► Altus will have a right of first offer to develop a crude oil gathering system § Firm space on EPIC through acreage dedication with Saragosa terminal near Alpine High ► ~1.7 million acre area of mutual interest (approximately 10 miles surrounding the Alpine High area of dedication), providing Altus with first right to participate in midstream opportunities originated by Apache 23 Other ROFO Opportunities ► Altus will have a right of first offer on additional equity options ► Altus will have a right of first offer to develop a crude oil gathering system § Firm space on EPIC through acreage dedication with Saragosa terminal near Alpine High ► ~1.7 million acre area of mutual interest (approximately 10 miles surrounding the Alpine High area of dedication), providing Altus with first right to participate in midstream opportunities originated by Apache 23

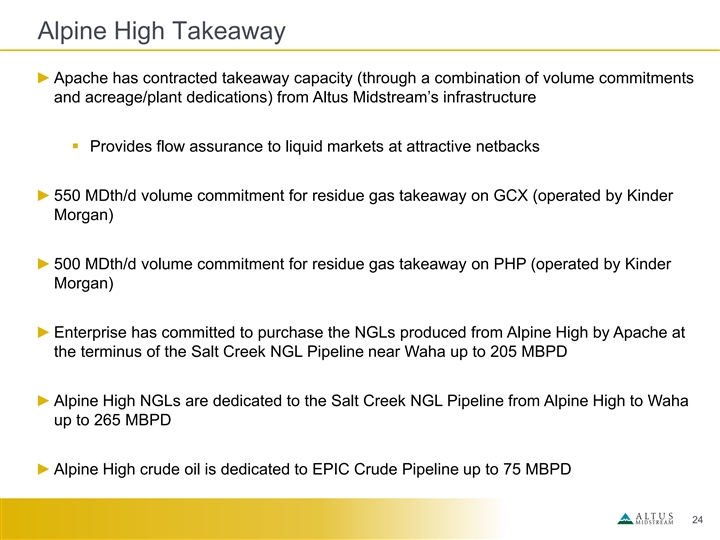

Alpine High Takeaway ► Apache has contracted takeaway capacity (through a combination of volume commitments and acreage/plant dedications) from Altus Midstream’s infrastructure § Provides flow assurance to liquid markets at attractive netbacks ► 550 MDth/d volume commitment for residue gas takeaway on GCX (operated by Kinder Morgan) ► 500 MDth/d volume commitment for residue gas takeaway on PHP (operated by Kinder Morgan) ► Enterprise has committed to purchase the NGLs produced from Alpine High by Apache at the terminus of the Salt Creek NGL Pipeline near Waha up to 205 MBPD ► Alpine High NGLs are dedicated to the Salt Creek NGL Pipeline from Alpine High to Waha up to 265 MBPD ► Alpine High crude oil is dedicated to EPIC Crude Pipeline up to 75 MBPD 24 Alpine High Takeaway ► Apache has contracted takeaway capacity (through a combination of volume commitments and acreage/plant dedications) from Altus Midstream’s infrastructure § Provides flow assurance to liquid markets at attractive netbacks ► 550 MDth/d volume commitment for residue gas takeaway on GCX (operated by Kinder Morgan) ► 500 MDth/d volume commitment for residue gas takeaway on PHP (operated by Kinder Morgan) ► Enterprise has committed to purchase the NGLs produced from Alpine High by Apache at the terminus of the Salt Creek NGL Pipeline near Waha up to 205 MBPD ► Alpine High NGLs are dedicated to the Salt Creek NGL Pipeline from Alpine High to Waha up to 265 MBPD ► Alpine High crude oil is dedicated to EPIC Crude Pipeline up to 75 MBPD 24

Questions? 25 Questions? 25

Altus Midstream Overview – JV Pipelines 26 Altus Midstream Overview – JV Pipelines 26

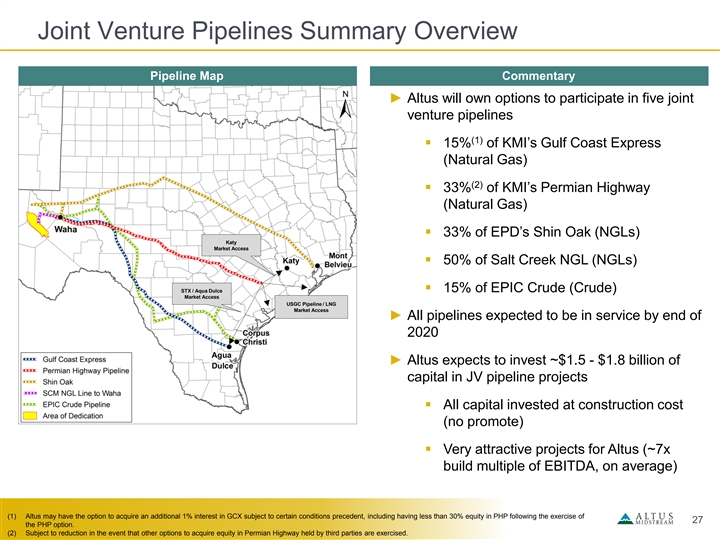

Joint Venture Pipelines Summary Overview Pipeline Map Commentary ► Altus will own options to participate in five joint venture pipelines (1) § 15% of KMI’s Gulf Coast Express (Natural Gas) (2) § 33% of KMI’s Permian Highway (Natural Gas) § 33% of EPD’s Shin Oak (NGLs) Katy Market Access § 50% of Salt Creek NGL (NGLs) § 15% of EPIC Crude (Crude) STX / Aqua Dulce Market Access USGC Pipeline / LNG Market Access ► All pipelines expected to be in service by end of 2020 ► Altus expects to invest ~$1.5 - $1.8 billion of capital in JV pipeline projects § All capital invested at construction cost (no promote) § Very attractive projects for Altus (~7x build multiple of EBITDA, on average) (1) Altus may have the option to acquire an additional 1% interest in GCX subject to certain conditions precedent, including having less than 30% equity in PHP following the exercise of 27 the PHP option. (2) Subject to reduction in the event that other options to acquire equity in Permian Highway held by third parties are exercised. Joint Venture Pipelines Summary Overview Pipeline Map Commentary ► Altus will own options to participate in five joint venture pipelines (1) § 15% of KMI’s Gulf Coast Express (Natural Gas) (2) § 33% of KMI’s Permian Highway (Natural Gas) § 33% of EPD’s Shin Oak (NGLs) Katy Market Access § 50% of Salt Creek NGL (NGLs) § 15% of EPIC Crude (Crude) STX / Aqua Dulce Market Access USGC Pipeline / LNG Market Access ► All pipelines expected to be in service by end of 2020 ► Altus expects to invest ~$1.5 - $1.8 billion of capital in JV pipeline projects § All capital invested at construction cost (no promote) § Very attractive projects for Altus (~7x build multiple of EBITDA, on average) (1) Altus may have the option to acquire an additional 1% interest in GCX subject to certain conditions precedent, including having less than 30% equity in PHP following the exercise of 27 the PHP option. (2) Subject to reduction in the event that other options to acquire equity in Permian Highway held by third parties are exercised.

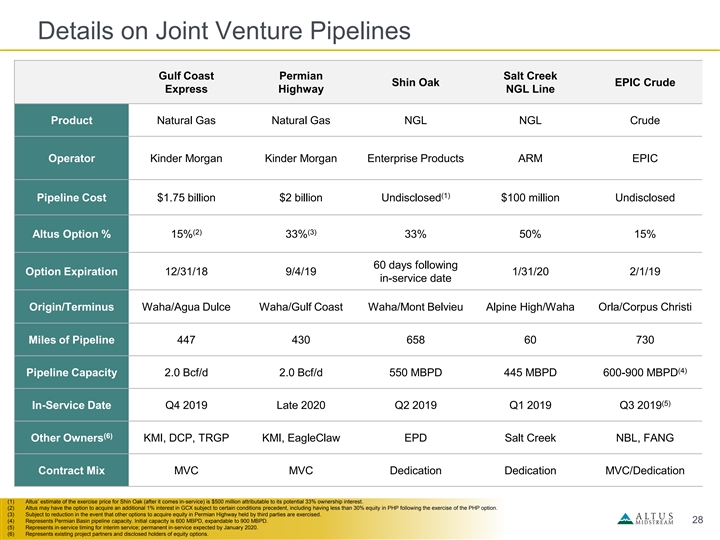

Details on Joint Venture Pipelines Gulf Coast Permian Salt Creek Shin Oak EPIC Crude Express Highway NGL Line Product Natural Gas Natural Gas NGL NGL Crude Operator Kinder Morgan Kinder Morgan Enterprise Products ARM EPIC (1) Pipeline Cost $1.75 billion $2 billion Undisclosed $100 million Undisclosed (2) (3) Altus Option % 15% 33% 33% 50% 15% 60 days following Option Expiration 12/31/18 9/4/19 1/31/20 2/1/19 in-service date Origin/Terminus Waha/Agua Dulce Waha/Gulf Coast Waha/Mont Belvieu Alpine High/Waha Orla/Corpus Christi Miles of Pipeline 447 430 658 60 730 (4) Pipeline Capacity 2.0 Bcf/d 2.0 Bcf/d 550 MBPD 445 MBPD 600-900 MBPD (5) In-Service Date Q4 2019 Late 2020 Q2 2019 Q1 2019 Q3 2019 (6) Other Owners KMI, DCP, TRGP KMI, EagleClaw EPD Salt Creek NBL, FANG Contract Mix MVC MVC Dedication Dedication MVC/Dedication (1) Altus’ estimate of the exercise price for Shin Oak (after it comes in-service) is $500 million attributable to its potential 33% ownership interest. (2) Altus may have the option to acquire an additional 1% interest in GCX subject to certain conditions precedent, including having less than 30% equity in PHP following the exercise of the PHP option. (3) Subject to reduction in the event that other options to acquire equity in Permian Highway held by third parties are exercised. (4) Represents Permian Basin pipeline capacity. Initial capacity is 600 MBPD, expandable to 900 MBPD. 28 (5) Represents in-service timing for interim service; permanent in-service expected by January 2020. (6) Represents existing project partners and disclosed holders of equity options. Details on Joint Venture Pipelines Gulf Coast Permian Salt Creek Shin Oak EPIC Crude Express Highway NGL Line Product Natural Gas Natural Gas NGL NGL Crude Operator Kinder Morgan Kinder Morgan Enterprise Products ARM EPIC (1) Pipeline Cost $1.75 billion $2 billion Undisclosed $100 million Undisclosed (2) (3) Altus Option % 15% 33% 33% 50% 15% 60 days following Option Expiration 12/31/18 9/4/19 1/31/20 2/1/19 in-service date Origin/Terminus Waha/Agua Dulce Waha/Gulf Coast Waha/Mont Belvieu Alpine High/Waha Orla/Corpus Christi Miles of Pipeline 447 430 658 60 730 (4) Pipeline Capacity 2.0 Bcf/d 2.0 Bcf/d 550 MBPD 445 MBPD 600-900 MBPD (5) In-Service Date Q4 2019 Late 2020 Q2 2019 Q1 2019 Q3 2019 (6) Other Owners KMI, DCP, TRGP KMI, EagleClaw EPD Salt Creek NBL, FANG Contract Mix MVC MVC Dedication Dedication MVC/Dedication (1) Altus’ estimate of the exercise price for Shin Oak (after it comes in-service) is $500 million attributable to its potential 33% ownership interest. (2) Altus may have the option to acquire an additional 1% interest in GCX subject to certain conditions precedent, including having less than 30% equity in PHP following the exercise of the PHP option. (3) Subject to reduction in the event that other options to acquire equity in Permian Highway held by third parties are exercised. (4) Represents Permian Basin pipeline capacity. Initial capacity is 600 MBPD, expandable to 900 MBPD. 28 (5) Represents in-service timing for interim service; permanent in-service expected by January 2020. (6) Represents existing project partners and disclosed holders of equity options.

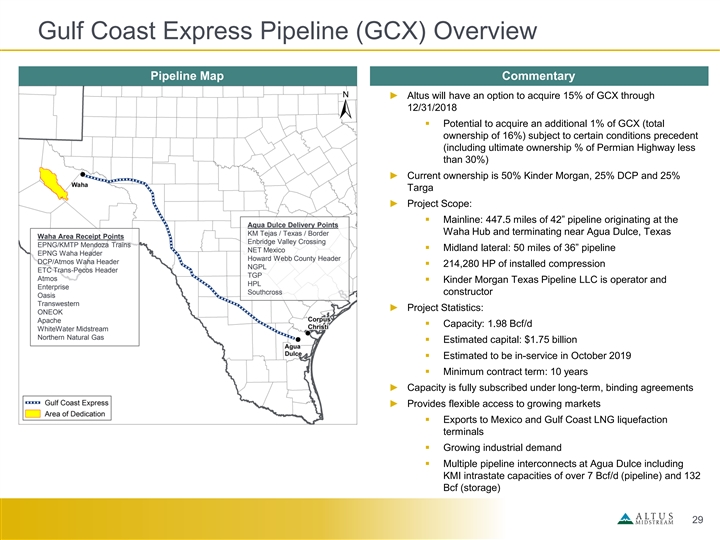

Gulf Coast Express Pipeline (GCX) Overview Pipeline Map Commentary ► Altus will have an option to acquire 15% of GCX through 12/31/2018 § Potential to acquire an additional 1% of GCX (total ownership of 16%) subject to certain conditions precedent (including ultimate ownership % of Permian Highway less than 30%) ► Current ownership is 50% Kinder Morgan, 25% DCP and 25% Targa ► Project Scope: § Mainline: 447.5 miles of 42” pipeline originating at the Aqua Dulce Delivery Points Waha Hub and terminating near Agua Dulce, Texas KM Tejas / Texas / Border Waha Area Receipt Points Enbridge Valley Crossing EPNG/KMTP Mendoza Trains § Midland lateral: 50 miles of 36” pipeline NET Mexico EPNG Waha Header Howard Webb County Header DCP/Atmos Waha Header § 214,280 HP of installed compression NGPL ETC Trans-Pecos Header TGP Atmos § Kinder Morgan Texas Pipeline LLC is operator and HPL Enterprise Southcross constructor Oasis Transwestern ► Project Statistics: ONEOK Apache § Capacity: 1.98 Bcf/d WhiteWater Midstream Northern Natural Gas § Estimated capital: $1.75 billion § Estimated to be in-service in October 2019 § Minimum contract term: 10 years ► Capacity is fully subscribed under long-term, binding agreements ► Provides flexible access to growing markets § Exports to Mexico and Gulf Coast LNG liquefaction terminals § Growing industrial demand § Multiple pipeline interconnects at Agua Dulce including KMI intrastate capacities of over 7 Bcf/d (pipeline) and 132 Bcf (storage) 29 Gulf Coast Express Pipeline (GCX) Overview Pipeline Map Commentary ► Altus will have an option to acquire 15% of GCX through 12/31/2018 § Potential to acquire an additional 1% of GCX (total ownership of 16%) subject to certain conditions precedent (including ultimate ownership % of Permian Highway less than 30%) ► Current ownership is 50% Kinder Morgan, 25% DCP and 25% Targa ► Project Scope: § Mainline: 447.5 miles of 42” pipeline originating at the Aqua Dulce Delivery Points Waha Hub and terminating near Agua Dulce, Texas KM Tejas / Texas / Border Waha Area Receipt Points Enbridge Valley Crossing EPNG/KMTP Mendoza Trains § Midland lateral: 50 miles of 36” pipeline NET Mexico EPNG Waha Header Howard Webb County Header DCP/Atmos Waha Header § 214,280 HP of installed compression NGPL ETC Trans-Pecos Header TGP Atmos § Kinder Morgan Texas Pipeline LLC is operator and HPL Enterprise Southcross constructor Oasis Transwestern ► Project Statistics: ONEOK Apache § Capacity: 1.98 Bcf/d WhiteWater Midstream Northern Natural Gas § Estimated capital: $1.75 billion § Estimated to be in-service in October 2019 § Minimum contract term: 10 years ► Capacity is fully subscribed under long-term, binding agreements ► Provides flexible access to growing markets § Exports to Mexico and Gulf Coast LNG liquefaction terminals § Growing industrial demand § Multiple pipeline interconnects at Agua Dulce including KMI intrastate capacities of over 7 Bcf/d (pipeline) and 132 Bcf (storage) 29

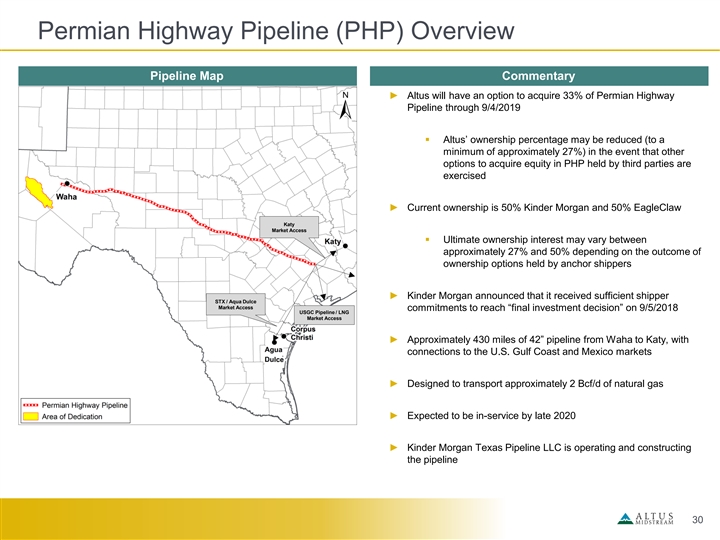

Permian Highway Pipeline (PHP) Overview Pipeline Map Commentary ► Altus will have an option to acquire 33% of Permian Highway Pipeline through 9/4/2019 § Altus’ ownership percentage may be reduced (to a minimum of approximately 27%) in the event that other options to acquire equity in PHP held by third parties are exercised ► Current ownership is 50% Kinder Morgan and 50% EagleClaw Katy Market Access § Ultimate ownership interest may vary between approximately 27% and 50% depending on the outcome of ownership options held by anchor shippers ► Kinder Morgan announced that it received sufficient shipper STX / Aqua Dulce Market Access commitments to reach “final investment decision” on 9/5/2018 USGC Pipeline / LNG Market Access ► Approximately 430 miles of 42” pipeline from Waha to Katy, with connections to the U.S. Gulf Coast and Mexico markets ► Designed to transport approximately 2 Bcf/d of natural gas ► Expected to be in-service by late 2020 ► Kinder Morgan Texas Pipeline LLC is operating and constructing the pipeline 30 Permian Highway Pipeline (PHP) Overview Pipeline Map Commentary ► Altus will have an option to acquire 33% of Permian Highway Pipeline through 9/4/2019 § Altus’ ownership percentage may be reduced (to a minimum of approximately 27%) in the event that other options to acquire equity in PHP held by third parties are exercised ► Current ownership is 50% Kinder Morgan and 50% EagleClaw Katy Market Access § Ultimate ownership interest may vary between approximately 27% and 50% depending on the outcome of ownership options held by anchor shippers ► Kinder Morgan announced that it received sufficient shipper STX / Aqua Dulce Market Access commitments to reach “final investment decision” on 9/5/2018 USGC Pipeline / LNG Market Access ► Approximately 430 miles of 42” pipeline from Waha to Katy, with connections to the U.S. Gulf Coast and Mexico markets ► Designed to transport approximately 2 Bcf/d of natural gas ► Expected to be in-service by late 2020 ► Kinder Morgan Texas Pipeline LLC is operating and constructing the pipeline 30

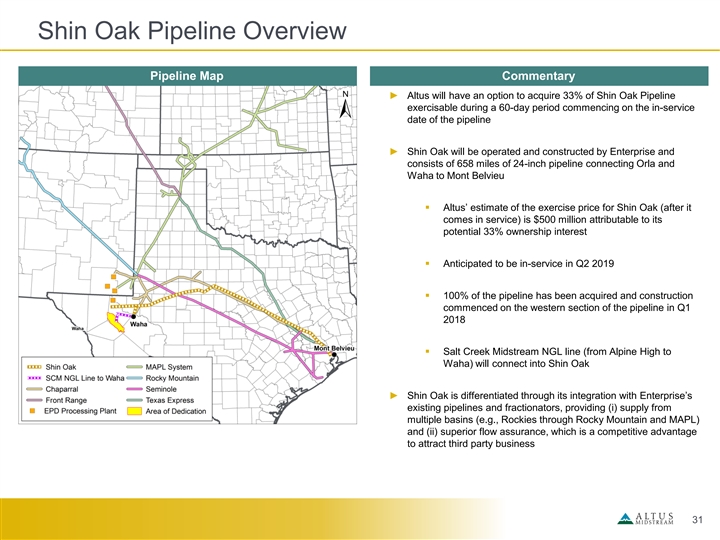

Shin Oak Pipeline Overview Pipeline Map Commentary ► Altus will have an option to acquire 33% of Shin Oak Pipeline exercisable during a 60-day period commencing on the in-service date of the pipeline ► Shin Oak will be operated and constructed by Enterprise and consists of 658 miles of 24-inch pipeline connecting Orla and Waha to Mont Belvieu § Altus’ estimate of the exercise price for Shin Oak (after it comes in service) is $500 million attributable to its potential 33% ownership interest § Anticipated to be in-service in Q2 2019 § 100% of the pipeline has been acquired and construction commenced on the western section of the pipeline in Q1 2018 § Salt Creek Midstream NGL line (from Alpine High to Waha) will connect into Shin Oak ► Shin Oak is differentiated through its integration with Enterprise’s existing pipelines and fractionators, providing (i) supply from multiple basins (e.g., Rockies through Rocky Mountain and MAPL) and (ii) superior flow assurance, which is a competitive advantage to attract third party business 31 Shin Oak Pipeline Overview Pipeline Map Commentary ► Altus will have an option to acquire 33% of Shin Oak Pipeline exercisable during a 60-day period commencing on the in-service date of the pipeline ► Shin Oak will be operated and constructed by Enterprise and consists of 658 miles of 24-inch pipeline connecting Orla and Waha to Mont Belvieu § Altus’ estimate of the exercise price for Shin Oak (after it comes in service) is $500 million attributable to its potential 33% ownership interest § Anticipated to be in-service in Q2 2019 § 100% of the pipeline has been acquired and construction commenced on the western section of the pipeline in Q1 2018 § Salt Creek Midstream NGL line (from Alpine High to Waha) will connect into Shin Oak ► Shin Oak is differentiated through its integration with Enterprise’s existing pipelines and fractionators, providing (i) supply from multiple basins (e.g., Rockies through Rocky Mountain and MAPL) and (ii) superior flow assurance, which is a competitive advantage to attract third party business 31

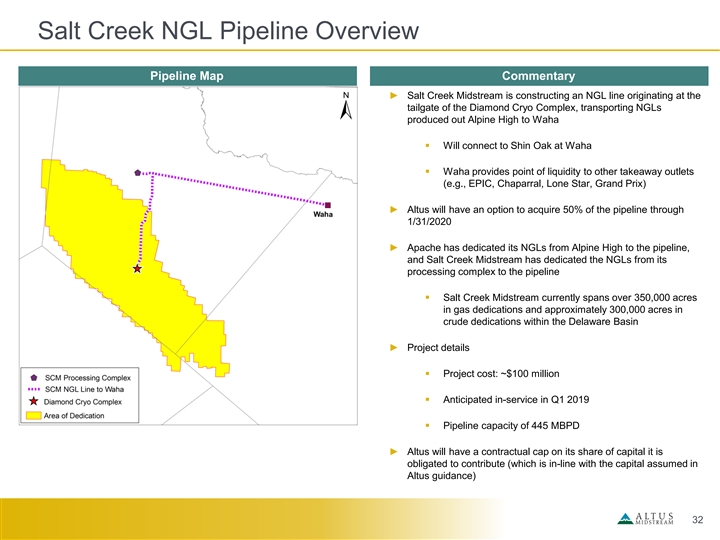

Salt Creek NGL Pipeline Overview Pipeline Map Commentary ► Salt Creek Midstream is constructing an NGL line originating at the tailgate of the Diamond Cryo Complex, transporting NGLs produced out Alpine High to Waha § Will connect to Shin Oak at Waha § Waha provides point of liquidity to other takeaway outlets (e.g., EPIC, Chaparral, Lone Star, Grand Prix) ► Altus will have an option to acquire 50% of the pipeline through 1/31/2020 ► Apache has dedicated its NGLs from Alpine High to the pipeline, and Salt Creek Midstream has dedicated the NGLs from its processing complex to the pipeline § Salt Creek Midstream currently spans over 350,000 acres in gas dedications and approximately 300,000 acres in crude dedications within the Delaware Basin ► Project details § Project cost: ~$100 million § Anticipated in-service in Q1 2019 § Pipeline capacity of 445 MBPD ► Altus will have a contractual cap on its share of capital it is obligated to contribute (which is in-line with the capital assumed in Altus guidance) 32 Salt Creek NGL Pipeline Overview Pipeline Map Commentary ► Salt Creek Midstream is constructing an NGL line originating at the tailgate of the Diamond Cryo Complex, transporting NGLs produced out Alpine High to Waha § Will connect to Shin Oak at Waha § Waha provides point of liquidity to other takeaway outlets (e.g., EPIC, Chaparral, Lone Star, Grand Prix) ► Altus will have an option to acquire 50% of the pipeline through 1/31/2020 ► Apache has dedicated its NGLs from Alpine High to the pipeline, and Salt Creek Midstream has dedicated the NGLs from its processing complex to the pipeline § Salt Creek Midstream currently spans over 350,000 acres in gas dedications and approximately 300,000 acres in crude dedications within the Delaware Basin ► Project details § Project cost: ~$100 million § Anticipated in-service in Q1 2019 § Pipeline capacity of 445 MBPD ► Altus will have a contractual cap on its share of capital it is obligated to contribute (which is in-line with the capital assumed in Altus guidance) 32

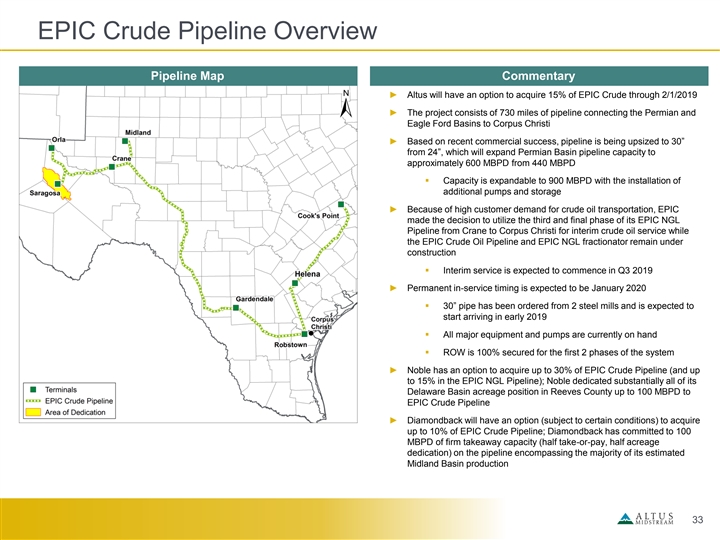

EPIC Crude Pipeline Overview Pipeline Map Commentary ► Altus will have an option to acquire 15% of EPIC Crude through 2/1/2019 ► The project consists of 730 miles of pipeline connecting the Permian and Eagle Ford Basins to Corpus Christi ► Based on recent commercial success, pipeline is being upsized to 30” from 24”, which will expand Permian Basin pipeline capacity to approximately 600 MBPD from 440 MBPD § Capacity is expandable to 900 MBPD with the installation of additional pumps and storage ► Because of high customer demand for crude oil transportation, EPIC made the decision to utilize the third and final phase of its EPIC NGL Pipeline from Crane to Corpus Christi for interim crude oil service while the EPIC Crude Oil Pipeline and EPIC NGL fractionator remain under construction § Interim service is expected to commence in Q3 2019 ► Permanent in-service timing is expected to be January 2020 § 30” pipe has been ordered from 2 steel mills and is expected to start arriving in early 2019 § All major equipment and pumps are currently on hand § ROW is 100% secured for the first 2 phases of the system ► Noble has an option to acquire up to 30% of EPIC Crude Pipeline (and up to 15% in the EPIC NGL Pipeline); Noble dedicated substantially all of its Delaware Basin acreage position in Reeves County up to 100 MBPD to EPIC Crude Pipeline ► Diamondback will have an option (subject to certain conditions) to acquire up to 10% of EPIC Crude Pipeline; Diamondback has committed to 100 MBPD of firm takeaway capacity (half take-or-pay, half acreage dedication) on the pipeline encompassing the majority of its estimated Midland Basin production 33 EPIC Crude Pipeline Overview Pipeline Map Commentary ► Altus will have an option to acquire 15% of EPIC Crude through 2/1/2019 ► The project consists of 730 miles of pipeline connecting the Permian and Eagle Ford Basins to Corpus Christi ► Based on recent commercial success, pipeline is being upsized to 30” from 24”, which will expand Permian Basin pipeline capacity to approximately 600 MBPD from 440 MBPD § Capacity is expandable to 900 MBPD with the installation of additional pumps and storage ► Because of high customer demand for crude oil transportation, EPIC made the decision to utilize the third and final phase of its EPIC NGL Pipeline from Crane to Corpus Christi for interim crude oil service while the EPIC Crude Oil Pipeline and EPIC NGL fractionator remain under construction § Interim service is expected to commence in Q3 2019 ► Permanent in-service timing is expected to be January 2020 § 30” pipe has been ordered from 2 steel mills and is expected to start arriving in early 2019 § All major equipment and pumps are currently on hand § ROW is 100% secured for the first 2 phases of the system ► Noble has an option to acquire up to 30% of EPIC Crude Pipeline (and up to 15% in the EPIC NGL Pipeline); Noble dedicated substantially all of its Delaware Basin acreage position in Reeves County up to 100 MBPD to EPIC Crude Pipeline ► Diamondback will have an option (subject to certain conditions) to acquire up to 10% of EPIC Crude Pipeline; Diamondback has committed to 100 MBPD of firm takeaway capacity (half take-or-pay, half acreage dedication) on the pipeline encompassing the majority of its estimated Midland Basin production 33

Questions? 34 Questions? 34

Alpine High Overview 35 Alpine High Overview 35

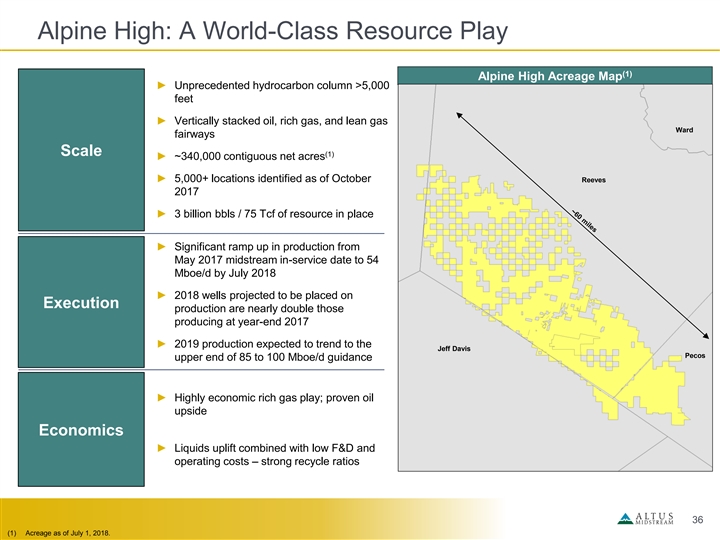

Alpine High: A World-Class Resource Play (1) Alpine High Acreage Map ► Unprecedented hydrocarbon column >5,000 feet ► Vertically stacked oil, rich gas, and lean gas Ward fairways Scale (1) ► ~340,000 contiguous net acres ► 5,000+ locations identified as of October Reeves 2017 ► 3 billion bbls / 75 Tcf of resource in place ► Significant ramp up in production from May 2017 midstream in-service date to 54 Mboe/d by July 2018 ► 2018 wells projected to be placed on Execution production are nearly double those producing at year-end 2017 ► 2019 production expected to trend to the Jeff Davis Pecos upper end of 85 to 100 Mboe/d guidance ► Highly economic rich gas play; proven oil upside Economics ► Liquids uplift combined with low F&D and operating costs – strong recycle ratios 36 (1) Acreage as of July 1, 2018. Alpine High: A World-Class Resource Play (1) Alpine High Acreage Map ► Unprecedented hydrocarbon column >5,000 feet ► Vertically stacked oil, rich gas, and lean gas Ward fairways Scale (1) ► ~340,000 contiguous net acres ► 5,000+ locations identified as of October Reeves 2017 ► 3 billion bbls / 75 Tcf of resource in place ► Significant ramp up in production from May 2017 midstream in-service date to 54 Mboe/d by July 2018 ► 2018 wells projected to be placed on Execution production are nearly double those producing at year-end 2017 ► 2019 production expected to trend to the Jeff Davis Pecos upper end of 85 to 100 Mboe/d guidance ► Highly economic rich gas play; proven oil upside Economics ► Liquids uplift combined with low F&D and operating costs – strong recycle ratios 36 (1) Acreage as of July 1, 2018.

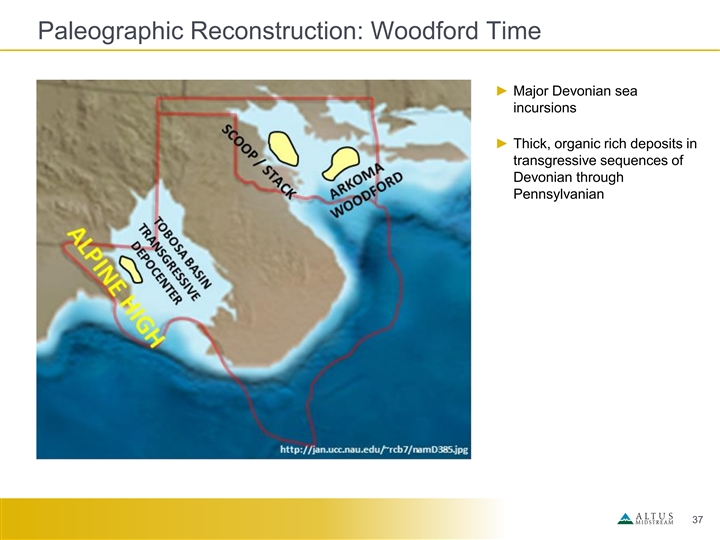

Paleographic Reconstruction: Woodford Time ► Major Devonian sea incursions ► Thick, organic rich deposits in transgressive sequences of Devonian through Pennsylvanian 37 Paleographic Reconstruction: Woodford Time ► Major Devonian sea incursions ► Thick, organic rich deposits in transgressive sequences of Devonian through Pennsylvanian 37

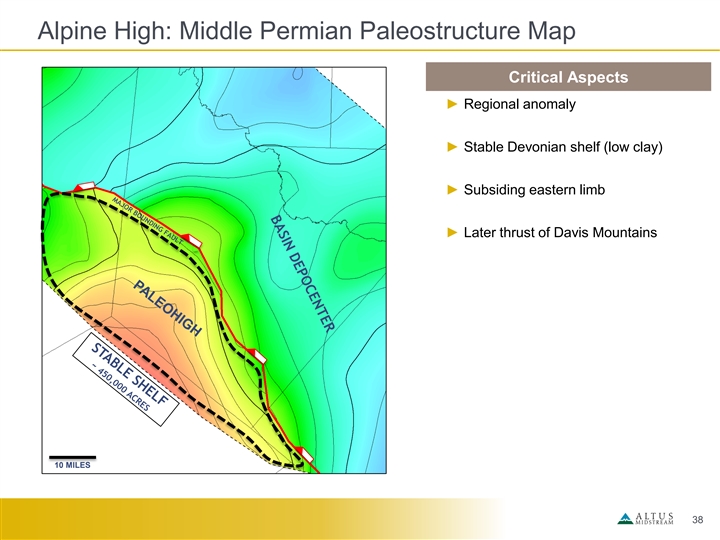

Alpine High: Middle Permian Paleostructure Map Critical Aspects ► Regional anomaly ► Stable Devonian shelf (low clay) ► Subsiding eastern limb ► Later thrust of Davis Mountains 10 MILES 38 Alpine High: Middle Permian Paleostructure Map Critical Aspects ► Regional anomaly ► Stable Devonian shelf (low clay) ► Subsiding eastern limb ► Later thrust of Davis Mountains 10 MILES 38

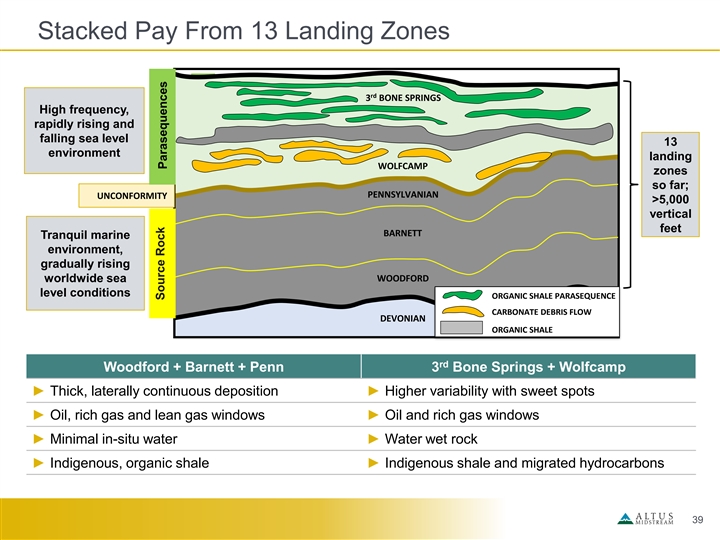

Stacked Pay From 13 Landing Zones rd 3 BONE SPRINGS High frequency, rapidly rising and falling sea level 13 environment landing WOLFCAMP zones so far; PENNSYLVANIAN UNCONFORMITY >5,000 vertical feet BARNETT Tranquil marine environment, gradually rising worldwide sea WOODFORD level conditions ORGANIC SHALE PARASEQUENCE CARBONATE DEBRIS FLOW DEVONIAN ORGANIC SHALE rd Woodford + Barnett + Penn 3 Bone Springs + Wolfcamp ► Thick, laterally continuous deposition ► Higher variability with sweet spots ► Oil, rich gas and lean gas windows ► Oil and rich gas windows ► Minimal in-situ water ► Water wet rock ► Indigenous, organic shale ► Indigenous shale and migrated hydrocarbons 39 Source Rock Parasequences Source Rock Parasequences Stacked Pay From 13 Landing Zones rd 3 BONE SPRINGS High frequency, rapidly rising and falling sea level 13 environment landing WOLFCAMP zones so far; PENNSYLVANIAN UNCONFORMITY >5,000 vertical feet BARNETT Tranquil marine environment, gradually rising worldwide sea WOODFORD level conditions ORGANIC SHALE PARASEQUENCE CARBONATE DEBRIS FLOW DEVONIAN ORGANIC SHALE rd Woodford + Barnett + Penn 3 Bone Springs + Wolfcamp ► Thick, laterally continuous deposition ► Higher variability with sweet spots ► Oil, rich gas and lean gas windows ► Oil and rich gas windows ► Minimal in-situ water ► Water wet rock ► Indigenous, organic shale ► Indigenous shale and migrated hydrocarbons 39 Source Rock Parasequences Source Rock Parasequences

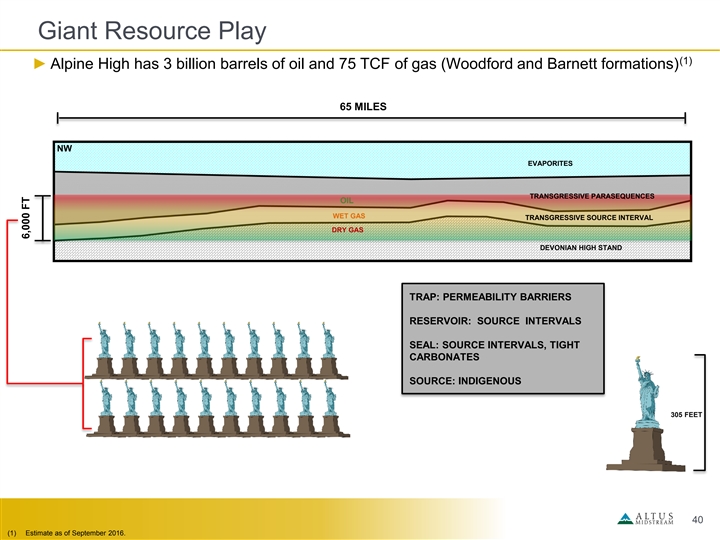

Giant Resource Play (1) ► Alpine High has 3 billion barrels of oil and 75 TCF of gas (Woodford and Barnett formations) 65 MILES NW EVAPORITES TRANSGRESSIVE PARASEQUENCES OIL WET GAS TRANSGRESSIVE SOURCE INTERVAL DRY GAS DEVONIAN HIGH STAND TRAP: PERMEABILITY BARRIERS RESERVOIR: SOURCE INTERVALS SEAL: SOURCE INTERVALS, TIGHT CARBONATES SOURCE: INDIGENOUS 305 FEET 40 (1) Estimate as of September 2016. 6,000 FT Giant Resource Play (1) ► Alpine High has 3 billion barrels of oil and 75 TCF of gas (Woodford and Barnett formations) 65 MILES NW EVAPORITES TRANSGRESSIVE PARASEQUENCES OIL WET GAS TRANSGRESSIVE SOURCE INTERVAL DRY GAS DEVONIAN HIGH STAND TRAP: PERMEABILITY BARRIERS RESERVOIR: SOURCE INTERVALS SEAL: SOURCE INTERVALS, TIGHT CARBONATES SOURCE: INDIGENOUS 305 FEET 40 (1) Estimate as of September 2016. 6,000 FT

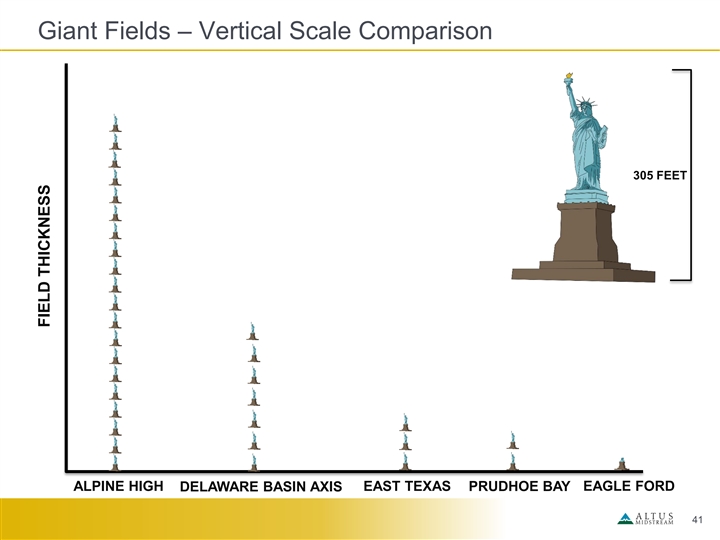

Giant Fields – Vertical Scale Comparison 305 FEET ALPINE HIGH EAST TEXAS PRUDHOE BAY EAGLE FORD DELAWARE BASIN AXIS 41 FIELD THICKNESS Giant Fields – Vertical Scale Comparison 305 FEET ALPINE HIGH EAST TEXAS PRUDHOE BAY EAGLE FORD DELAWARE BASIN AXIS 41 FIELD THICKNESS

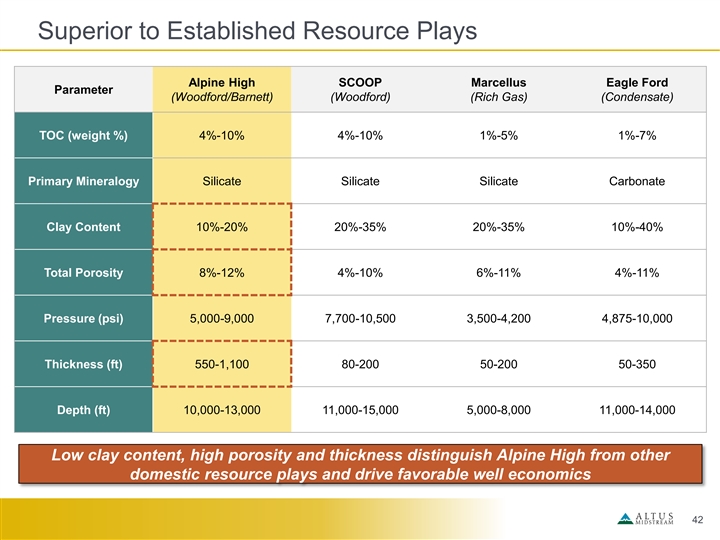

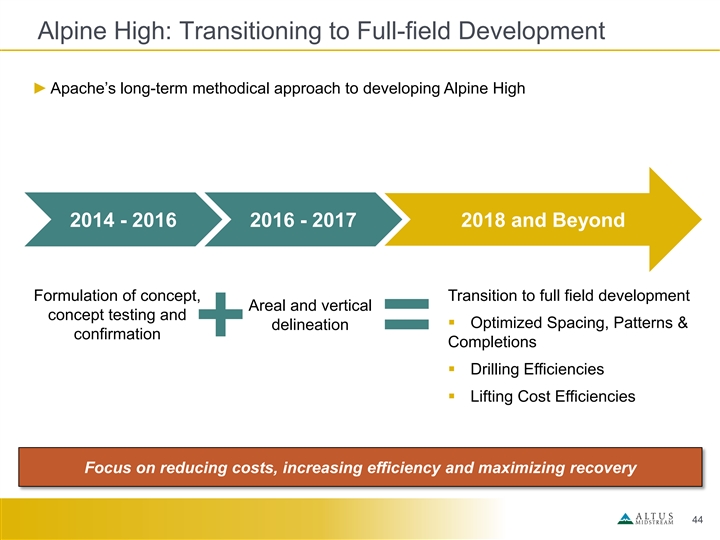

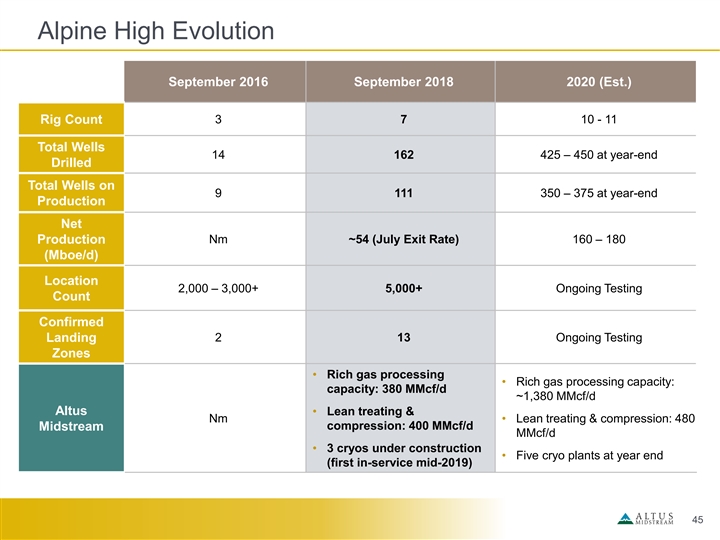

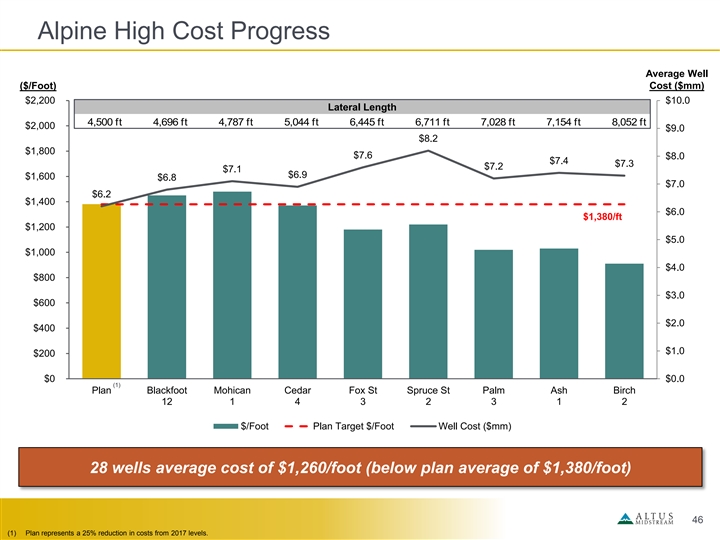

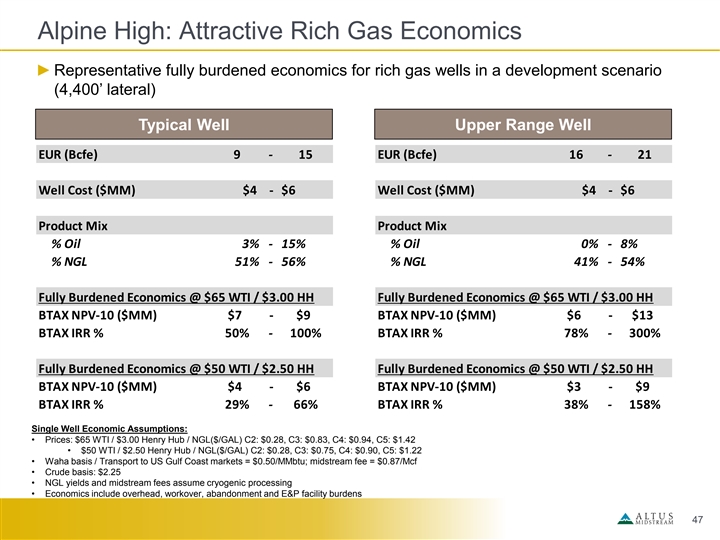

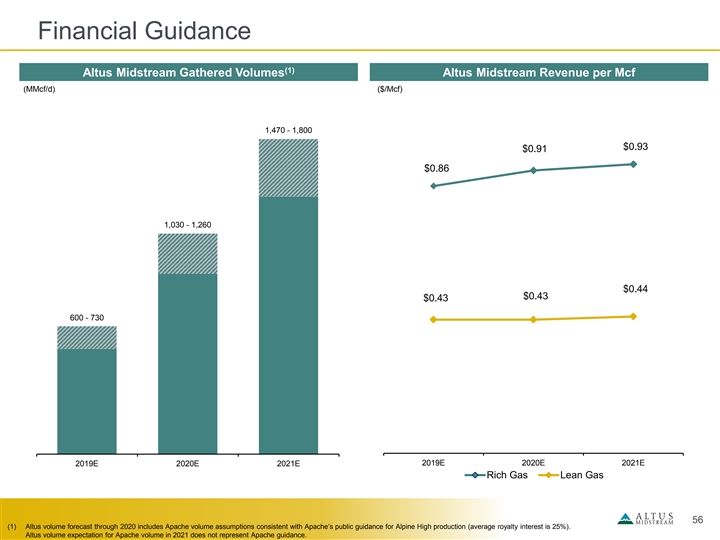

Superior to Established Resource Plays Alpine High SCOOP Marcellus Eagle Ford Parameter (Woodford/Barnett) (Woodford) (Rich Gas) (Condensate) TOC (weight %) 4%-10% 4%-10% 1%-5% 1%-7% Primary Mineralogy Silicate Silicate Silicate Carbonate Clay Content 10%-20% 20%-35% 20%-35% 10%-40% Total Porosity 8%-12% 4%-10% 6%-11% 4%-11% Pressure (psi) 5,000-9,000 7,700-10,500 3,500-4,200 4,875-10,000 Thickness (ft) 550-1,100 80-200 50-200 50-350 Depth (ft) 10,000-13,000 11,000-15,000 5,000-8,000 11,000-14,000 Low clay content, high porosity and thickness distinguish Alpine High from other domestic resource plays and drive favorable well economics 42 Superior to Established Resource Plays Alpine High SCOOP Marcellus Eagle Ford Parameter (Woodford/Barnett) (Woodford) (Rich Gas) (Condensate) TOC (weight %) 4%-10% 4%-10% 1%-5% 1%-7% Primary Mineralogy Silicate Silicate Silicate Carbonate Clay Content 10%-20% 20%-35% 20%-35% 10%-40% Total Porosity 8%-12% 4%-10% 6%-11% 4%-11% Pressure (psi) 5,000-9,000 7,700-10,500 3,500-4,200 4,875-10,000 Thickness (ft) 550-1,100 80-200 50-200 50-350 Depth (ft) 10,000-13,000 11,000-15,000 5,000-8,000 11,000-14,000 Low clay content, high porosity and thickness distinguish Alpine High from other domestic resource plays and drive favorable well economics 42