UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

| (Mark One) | |||||

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended March 31 , 2021

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from __________________ to __________________

Commission File No.: 1-4850

| DXC TECHNOLOGY COMPANY | ||

| (Exact name of registrant as specified in its charter) | ||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||

| (Address of principal executive offices) | (zip code) | |||||||||||||

Registrant's telephone number, including area code: (703 ) 245-9675

| Securities registered pursuant to Section 12(b) of the Act: | ||||||||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Securities registered pursuant to Section 12(g) of the Act: None | ||||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x Yes o No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

x | Accelerated Filer | o | ||||||||||||||||||

| Non-accelerated Filer | o | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes x No

The aggregate market value of the registrant's common stock held by non-affiliates of the registrant on September 30, 2020, the last business day of the registrant's most recently completed second fiscal quarter, based upon the closing price of a share of the registrant’s common stock on that date, was $4,531,553,903 .

DOCUMENTS INCORPORATED BY REFERENCE

TABLE OF CONTENTS

| Item | Page | ||||||||||

| 1. | |||||||||||

| 1A. | |||||||||||

| 1B. | |||||||||||

| 2. | |||||||||||

| 3. | |||||||||||

| 4. | |||||||||||

| 5. | |||||||||||

| 6. | |||||||||||

| 7. | |||||||||||

| 7A. | |||||||||||

| 8. | |||||||||||

| 9. | |||||||||||

| 9A. | |||||||||||

| 9B. | |||||||||||

| 10. | |||||||||||

| 11. | |||||||||||

| 12. | |||||||||||

| 13. | |||||||||||

| 14. | |||||||||||

| PART IV | |||||||||||

| 15. | |||||||||||

| 16. | |||||||||||

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

All statements and assumptions contained in this Annual Report on Form 10-K and in the documents incorporated by reference that do not directly and exclusively relate to historical facts constitute “forward-looking statements.” Forward-looking statements often include words such as “anticipates,” “believes,” “estimates,” “expects,” “forecast,” “goal,” “intends,” “objective,” “plans,” “projects,” “strategy,” “target,” and “will” and words and terms of similar substance in discussions of future operating or financial performance. These statements represent current expectations and beliefs, and no assurance can be given that the results described in such statements will be achieved.

Forward-looking statements include, among other things, statements with respect to our financial condition, results of operations, cash flows, business strategies, operating efficiencies or synergies, divestitures, competitive position, growth opportunities, share repurchases, dividend payments, plans and objectives of management and other matters. Such statements are subject to numerous assumptions, risks, uncertainties and other factors that could cause actual results to differ materially from those described in such statements, many of which are outside of our control. Furthermore, many of these risks and uncertainties are currently amplified by and may continue to be amplified by or may, in the future, be amplified by, the coronavirus disease 2019 (“COVID-19”) crisis and the impact of varying private and governmental responses that affect our customers, employees, vendors and the economies and communities where they operate.

Important factors that could cause actual results to differ materially from those described in forward-looking statements include, but are not limited to:

•the uncertainty of the magnitude, duration, geographic reach of the COVID-19 crisis, its impact on the global economy, and the impact of current and potential travel restrictions, stay-at-home orders, and economic restrictions implemented to address the crisis;

•the effects of macroeconomic and geopolitical trends and events;

•our inability to succeed in our strategic objectives;

•our inability to succeed in our strategic transactions;

•the risk of liability or damage to our reputation resulting from security incidents, including breaches, cyber-attacks insider threats, disclosure of sensitive data or failure to comply with data protection laws and regulations in a rapidly evolving regulatory environment; in each case, whether deliberate or accidental.

•our inability to develop and expand our service offerings to address emerging business demands and technological trends, including our inability to sell differentiated services up the Enterprise Technology Stack;

•the risks associated with our international operations;

•our credit rating and ability to manage working capital, refinance and raise additional capital for future needs;

•the competitive pressures faced by our business;

•our inability to accurately estimate the cost of services, and the completion timeline, of contracts;

•execution risks by us and our suppliers, customers, and partners;

•our inability to retain and hire key personnel and maintain relationships with key partners;

•our inability to comply with governmental regulations or the adoption of new laws or regulations;

•our inability to achieve the expected benefits of our restructuring plans;

•inadvertent infringement of third-party intellectual property rights or our inability to protect our own intellectual property assets;

•our inability to remediate any material weakness and maintain effective internal control over financial reporting;

•potential losses due to asset impairment charges;

•our inability to pay dividends or repurchase shares of our common stock;

•pending investigations, claims and disputes and any adverse impact on our profitability and liquidity;

•disruptions in the credit markets, including disruptions that reduce our customers' access to credit and increase the costs to our customers of obtaining credit;

•our failure to bid on projects effectively;

•financial difficulties of our customers and our inability to collect receivables;

•our inability to maintain and grow our customer relationships over time and to comply with customer contracts or government contracting regulations or requirements;

•changes in tax laws and any adverse impact on our effective tax rate;

•risks following the merger of Computer Sciences Corporation ("CSC") and Enterprise Services business of Hewlett Packard Enterprise Company's ("HPES") businesses, including anticipated tax treatment, unforeseen liabilities and future capital expenditures;

1

•risks following the spin-off of our former U.S. Public Sector business and its related mergers with Vencore Holding Corp. and KeyPoint Government Solutions to form Perspecta Inc. (the "USPS"); and

•the other factors described under Item 1A. “Risk Factors.”

No assurance can be given that any goal or plan set forth in any forward-looking statement can or will be achieved, and readers are cautioned not to place undue reliance on such statements, which speak only as of the date they are made. Any forward-looking statement made by us in this Annual Report on Form 10-K speaks only as of the date on which this Annual Report on Form 10-K was first filed. We do not undertake any obligation to update or release any revisions to any forward-looking statement or to report any events or circumstances after the date of this report or to reflect the occurrence of unanticipated events, except as required by law.

Throughout this report, we refer to DXC Technology Company, together with its consolidated subsidiaries, as “we,” “us,” “our,” “DXC,” or the “Company.” In order to make this report easier to read, we also refer throughout to (i) our Consolidated Financial Statements as our “financial statements,” (ii) our Consolidated Statements of Operations as our “statements of operations,” (iii) our Consolidated Statement of Comprehensive (Loss) Income as the "statements of comprehensive income,"(iv) our Consolidated Balance Sheets as our “balance sheets” and (v) our Consolidated Statements of Cash Flows as our “statements of cash flows.” In addition, references throughout to numbered “Notes” refer to the numbered Notes to our Financial Statements that we include in the Financial Statements section of this report.

PART I

ITEM 1. BUSINESS

Overview

DXC, a Nevada corporation, is a global IT services market leader. Our more than 130,000 people in 70-plus countries help our global customers, over half of today’s fortune 500 companies, run mission-critical systems with the latest technology innovations across our Enterprise Technology Stack.

Our customers trust DXC to innovate and deliver transformative solutions for new levels of performance, profitability, competitiveness, and customer experience.

DXC was formed on April 1, 2017 by the merger of CSC and HPES (the "HPES Merger").

Transformation Journey

The DXC “Transformation Journey” strategy focuses on building stronger relationships with customers, its people, and unlocking value across the Enterprise Technology Stack.

2

Key transformation journey priorities include:

•Inspire and Take Care of our People – Ensuring the health and safety of our people is a top priority, especially in the current environment

Continuing to bring in new technology, account and delivery talent across the world, and making investments that recognize and reward our people

•Focus on Customers – Strengthening our customer relationships and ensuring we are proactively delivering for customers

•Optimize Cost – Optimizing value to better serve our customers by eliminating confusion and complexity

•Seize the Market – Seizing the market opportunity by cross-selling and expanding what we do with our customers across the Enterprise Technology Stack

•Unlock Value to Strengthen Balance Sheet – Unlocking value by pursuing strategic alternatives, rationalizing our portfolio, and strengthening our balance sheet through our commitment to running a long-term sustainable business

The Company will continue to focus on execution of its strategy in the next fiscal year, with a continued focus on our people, revenue stabilization, cost optimization and winning in the market. While the Company has already disclosed that it completed the sale of two businesses that comprised the Strategic Alternatives plan, the Company will continue its portfolio shaping efforts and divest assets that the Company does not believe are well integrated with its enterprise technology stack and its strategic direction so it can focus on its strategy.

Important Acquisitions and Divestitures

During fiscal 2021, DXC completed the sale of its U.S. State and Local Health and Human Services business ("HHS" or the "HHS Business") to Veritas Capital Fund Management, L.L.C. ("Veritas Capital") to form Gainwell Technologies. The sale was accomplished by the cash purchase of all equity interests and assets attributable to the HHS Business together with future services to be provided by the Company for a total enterprise value of $5.0 billion, subject to net working capital adjustments and assumed liabilities.

On July 17, 2020, DXC entered into a purchase agreement with Dedalus Holding S.p.A. ("Dedalus"), a company organized under the laws of Italy, pursuant to which Dedalus will acquire DXC’s healthcare provider software business (the "HPS" or the "HPS Business"). The sale was completed on April 1, 2021, for a purchase price of €462 million (approximately $543 million) (the "HPS Sale").

During fiscal 2020, DXC completed the acquisition of Luxoft Holding, Inc., a global scale digital service provider whose offerings encompass strategic consulting, custom software development, and digital solution engineering services. We also completed other acquisitions during fiscal 2020 to complement our offerings and to provide opportunities for future growth.

See Note 2 - "Acquisitions" and Note 3 - "Divestitures" for further information on acquisitions and divestitures.

3

Segments and Services

Our reportable segments are Global Business Services ("GBS") and Global Infrastructure Services ("GIS").

Global Business Services

GBS provides innovative technology solutions that help our customers address key business challenges and accelerate transformations tailored to each customer’s industry and specific objectives. GBS offerings include:

•Analytics and Engineering. Our portfolio of analytics services and extensive partner ecosystem help customers gain rapid insights, automate operations, and accelerate their transformation journeys. We provide software engineering and solutions that enable businesses to run and manage their mission-critical functions, transform their operations, and develop new ways of doing business.

•Applications. We use advanced technologies and methods to accelerate the creation, modernization, delivery and maintenance of high-quality, secure applications allowing customers to innovate faster while reducing risk, time to market, and total cost of ownership, across industries. Our vertical-specific IP includes solutions for insurance, banking and capital markets, and automotive among others.

•Business process services. Include integration and optimization of front and back office processes, and agile process automation. This helps companies to reduce cost and minimize business disruption, human error, and operational risk while improving customer experiences.

Global Infrastructure Services

GIS provides a portfolio of technology offerings that deliver predictable outcomes and measurable results while reducing business risk and operational costs for customers. GIS offerings include:

•Cloud and Security. We help customers to rapidly modernize by adapting legacy apps to cloud, migrate the right workloads, and securely manage their multi-cloud environments. Our security solutions help predict attacks, proactively respond to threats, ensure compliance and protect data, applications and infrastructure.

•IT Outsourcing ("ITO"). Our ITO services support infrastructure, applications, and workplace IT operations, including hardware, software, physical/virtual end-user devices, collaboration tools, and IT support services. We help customers securely optimize operations to ensure continuity of their systems and respond to new business and workplace demands while achieving cost takeout, all with limited resources, expertise, and budget.

•Modern Workplace. Services to fit our customer’s employee, business and IT needs from intelligent collaboration, modern device management, digital support services, Internet of Things ("IoT") and mobility services, providing a consumer-like, digital experience.

See Note 20 - "Segment and Geographic Information" for additional information related to our reportable segments, including the disclosure of segment revenues, segment profit, and financial information by geographic area.

Sales and Marketing

We market and sell our services to customers through our direct sales force, operating out of locations around the world. Our customers include commercial businesses of many sizes and in many industries and public sector enterprises. No individual customer exceeded 10% of our consolidated revenues for fiscal 2021, fiscal 2020, or fiscal 2019.

Seasonality

General economic conditions have an impact on our business and financial results. The markets in which we sell our solutions, services and productions occasionally experience weak economic conditions that may negatively affect sales. We also experience some seasonal trends in the sale of our services. For example, contract awards and certain revenue are often tied to the timing of our customers' fiscal year-ends, and we also experience seasonality related to our own fiscal year-end selling activities.

4

Competition

The IT and professional services markets we compete in are highly competitive and are not dominated by a single company or a small number of companies. A substantial number of companies offer services that overlap and are competitive with those we offer. In addition, the increased importance of offshore labor centers has brought several foreign-based competitors into our markets.

Our competitors include:

•large multinational enterprises that offer some or all of the services and solutions that we offer;

•smaller companies that offer focused services and solutions similar to those that we offer;

•offshore service providers in lower-cost locations, particularly in India that sell directly to end-users;

•solution or service providers that compete with us in a specific industry segment or service area; and

•in-house functions of corporations that use their own resources rather than engaging an outside IT services provider.

The principal methods of competition in the markets for our solutions and services include:

•vision and strategic advisory ability;

•integrated solutions capabilities;

•performance and reliability;

•global and diverse talent;

•delivery excellence and ongoing support;

•responsiveness to customer needs;

•competitive pricing of services;

•technical and industry expertise;

•reputation and experience;

•quality of solutions and services; and

•financial stability and strong corporate governance.

Our ability to obtain new business and retain existing business is dependent upon the following:

•technology, industry and systems know-how with an independent perspective on best solutions across software, hardware, and service providers;

•ability to offer improved strategic frameworks and technical solutions;

•investments in our services and solutions;

•focus on responsiveness to proactively address customer needs, quality of services and competitive prices;

•successful management of our relationships with leading strategic and solution partners in hardware, networking, cloud, applications and software;

•project management experience and capabilities, including delivery;

•end-to-end spectrum of IT and professional services we provide; and

•financial stability and strong corporate governance.

Intellectual Property

We rely on a combination of trade secrets, patents, copyrights, and trademarks, as well as contractual protections to protect our business interests. While our technical services and products are not generally dependent upon patent protection, we do selectively seek patent protection for certain inventions likely to be incorporated into products and services or where obtaining such proprietary rights will improve our competitive position.

As our patent portfolio has been built over time, the remaining terms of the individual patents across the patent portfolio vary. We believe that our patents and patent applications are important for maintaining the competitive differentiation of our solutions and services and enhancing our freedom to sell solutions and services in markets in which we choose to participate. No single patent is in itself essential to our company as a whole or to any business segment.

5

Additionally, we own or have rights to various trademarks, service marks, and trade names that are used in the operation of our business. We also own or have the rights to copyrights that protect the content of our products and other proprietary materials.

In addition to developing our intellectual property portfolio, we license intellectual property rights from third parties as we deem appropriate. We have also granted and plan to continue to grant licenses to others under our intellectual property rights when we consider these arrangements to be in our interest. These license arrangements include a number of cross-licenses with third parties.

Environmental Regulation

Our operations are subject to regulation under various federal, state, local, and foreign laws concerning the environment and sustainability, including laws addressing the discharge of pollutants into the air and water, the management and disposal of hazardous substances and wastes, and the clean-up of contaminated sites. Environmental costs and accruals are presently not material to our operations, cash flows or financial position; and, we do not currently anticipate material capital expenditures for environmental control facilities. However, we could incur substantial costs including clean-up costs, fines and civil or criminal sanctions and third-party damage or personal injury claims if we were to violate or become liable under existing and future environmental laws or legislation.

Human Capital Management

As a leading global information technology services company, we attract highly skilled and educated people. As of March 31, 2021, we employed approximately 134,000 people worldwide. At DXC our people are our number one asset - ensuring they feel valued and respected.

Value of Employee Engagement

We value our people and take various actions for employee engagement. We assess employee engagement at least annually through a global engagement survey. During the past year, 77% of our people participated in the survey, which resulted in an Employee Engagement Index measuring 72%. Based on feedback received through periodic engagement surveys, management has implemented several initiatives to improve the employee experience from rewards and recognition, communications and process improvement. Various platforms like Global Talent Management, Coaching & Mentoring, Career Development programs, and global recognition are also used to improve employee experiences and engagement.

Management During COVID-19

We are committed to keeping our people safe and well. DXC employees are equipped and enabled to work virtually and flexibly from home today and continue to deliver results for our customers. Science and data will remain the drivers of our approach as we continue to navigate through COVID-19, and ensure the safety and well-being of our people. We will remain flexible and ready to react quickly if required to deliver for our customers. We recognize that this is an opportunity for DXC to change the employee experience in an impactful way.

Training and Education

We view professional development as a corporate responsibility — a strategic investment in our employees’ and the company’s future. Through our global learning management ecosystem, we offer hundreds of learning programs as well as a career development system to help employees reach their potential. Providing ways to learn, grow, and explore new and challenging opportunities contribute to our ability to retain a motivated, knowledgeable workforce. Assessing employee abilities and contributions is a cornerstone of development at DXC. Our self-directed learning culture encourages employees to learn at their own pace and in a learning environment of their preference. Key to our people development is the role managers play – we remain focused on equipping and enabling our people leaders to ensure our people have leaders that guide and support them in their development and success.

6

Inclusion & Diversity

We are committed to an Inclusive and Diverse workforce. The DXC Global Diversity and Non-Discrimination Policy guides our engagement in management and hiring practices that promote diversity and inclusion.

Human Rights

We are committed to the protection and advancement of human rights and to ensuring that our operations in communities around the world function with integrity. DXC is firmly committed to preventing the exploitation of vulnerable groups. Our main human rights–related focus areas are promoting good practice through our large and diverse global supply chain and supporting a diverse and inclusive corporate culture.

Available Information

We use our corporate website, www.dxc.technology, as a routine channel for distribution of important information, including detailed company information, financial news, SEC filings, Annual Reports, historical stock information and links to a recent earnings call webcast. DXC’s Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, all amendments to those reports, and the Proxy Statements for our Annual Meetings of Stockholders are made available, free of charge, on our corporate website as soon as reasonably practicable after such reports have been filed with or furnished to the SEC. They are also available through the SEC at www.sec.gov/edgar/searchedgar/companysearch.html. Our corporate governance guidelines, Board of Directors' committee charters (including the charters of the Audit Committee, Compensation Committee, Nominating/Corporate Governance Committee and Risk Committee) and code of ethics entitled "Code of Business Conduct" are also available on our website. The information on our website is not incorporated by reference into, and is not a part of, this report.

7

Information About Our Executive Officers

| Name | Age | Year First Elected as Officer | Term as an Officer | Position Held with the Registrant as of the filing date | Family Relationship | |||||||||||||||||||||||||||

| Michael J. Salvino | 55 | 2019 | Indefinite | President and Chief Executive Officer | None | |||||||||||||||||||||||||||

| Kenneth P. Sharp | 50 | 2020 | Indefinite | Executive Vice President and Chief Financial Officer | None | |||||||||||||||||||||||||||

| William L. Deckelman, Jr. | 63 | 2017 | Indefinite | Executive Vice President and General Counsel | None | |||||||||||||||||||||||||||

| Mary E. Finch | 51 | 2019 | Indefinite | Executive Vice President and Chief Human Resources Officer | None | |||||||||||||||||||||||||||

| Vinod Bagal | 55 | 2019 | Indefinite | Executive Vice President, Global Delivery and Transformation | None | |||||||||||||||||||||||||||

| Neil A. Manna | 58 | 2017 | Indefinite | Senior Vice President, Corporate Controller and Principal Accounting Officer | None | |||||||||||||||||||||||||||

Business Experience of Executive Officers

Michael J. Salvino became the President and Chief Executive Officer of DXC in September 2019 and has been a member of the Board of Directors of DXC since May 2019. Prior to joining DXC, Mr. Salvino served as managing director of Carrick Capital Partners from 2016 to 2019, where he was directly involved with Carrick's portfolio companies and in sourcing new investments, growing and managing large scale tech-enabled services businesses, specifically business process outsourcing, security and machine learning. Prior to his tenure at Carrick, from 2009 to 2016, Mr. Salvino served as group chief executive of Accenture Operations, where he led a team of more than 100,000 consulting and outsourcing professionals focused on providing business process outsourcing, infrastructure, security and cloud services to deliver business value and drive productivity and digital improvements for clients. Prior to that, he held leadership roles in the HR outsourcing business at Hewitt Associates Inc. and as president of the Americas Region at Exult Inc. Mr. Salvino is a board member of the Atrium Health Foundation, the largest healthcare system in the Carolinas, where he serves on the Investment Oversight Committee for both the hospital and the foundation. Mr. Salvino graduated from Marietta College with a Bachelor of Science degree in industrial engineering. He serves on the Marietta College Board of Trustees and is also a member of the Board of Visitors of the Duke University Pratt School of Engineering.

Kenneth P. Sharp became the Executive Vice President and Chief Financial Officer of DXC in November 2020. Prior to joining DXC, Mr. Sharp served as Vice President and Chief Financial Officer, Defense Systems Sector for Northrop Grumman (“NOC”) from June 2018 to November 2020. From January 2016 to June 2018, Mr. Sharp served as Senior Vice President, Finance of Orbital ATK (subsequently purchased by NOC). Prior to that, he served as Senior Vice President, Chief Accounting Officer and Corporate Controller of Leidos, Inc. (formerly SAIC, Inc.). Before joining Leidos, Mr. Sharp spent a decade at CSC, the predecessor company to DXC and eight years at Ernst & Young. Mr. Sharp also served in the United States Marine Corps.

William L. Deckelman, Jr. serves as Executive Vice President and General Counsel of DXC since September 2020. He previously served as Executive Vice President, General Counsel and Secretary of DXC since the completion of the HPES Merger. Prior to that, Mr. Deckelman served as Executive Vice President, General Counsel and Secretary of CSC. Mr. Deckelman joined CSC in January 2008 and served as Vice President, General Counsel and Secretary from 2008 to 2012, as Executive Vice President and General Counsel from 2012 to 2014, and as Executive Vice President, General Counsel and Secretary from August 2014 until the completion of the HPES Merger. Prior to joining CSC, Mr. Deckelman served as Executive Vice President and General Counsel of Affiliated Computer Services Inc. from 2000 to 2008, served as a director from 2000 to 2003, and previously held various executive positions there from 1989 to 1995.

8

Mary E. Finch was appointed as Executive Vice President and Chief Human Resources Officer of DXC in October 2019. Ms. Finch previously served as Executive Vice President and Chief Human Resources Officer of AECOM from September 2015 to October 2019. Prior to that, she served at Accenture as Senior Managing Director from September 2013 to August 2015 and as Managing Director Human Resources from January 2001 to September 2013, where she held various roles across the company including COO of Human Resources where she drove global delivery of HR services, overseeing operations supporting approximately 320,000 employees across 56 countries and multiple Accenture businesses. Ms. Finch also served as VP Human Resources of Abilizer Solutions Inc. from 2000 to 2001.

Vinod Bagal was appointed as Executive Vice President, Global Delivery and Transformation of DXC in October 2019. Prior to joining DXC, Mr. Bagal served at Cognizant Technology Solutions as Senior Vice President - Global Multi-Service Integration and North America Delivery and as Senior Vice President - Global Technology Consulting and Multi-Service Integration from September 2014 to October 2019, where he led the transformation of Cognizant's client delivery organization to position it for the next wave of professional services demands. From 1994 to 2014, Mr. Bagal held a series of leadership roles at Accenture.

Neil A. Manna has served as Senior Vice President, Corporate Controller and Principal Accounting Officer of DXC since the completion of the HPES Merger. He also served as Acting Chief Financial Officer of DXC from October 2020 until November 2020. Mr. Manna previously served as Principal Accounting Officer, Vice President and Controller of CSC. Mr. Manna joined CSC in June 2016. Prior to joining CSC, he served as the Chief Accounting Officer and Senior Vice President of CA Technologies (formerly Computer Associates, Inc.) from December 2008 to June 2016. He served as Principal Accounting Officer and Vice President of Worldwide Accounting for RealNetworks, Inc. from July 2007 to November 2008. He is a Certified Public Accountant and holds a Bachelor’s degree in Accounting and a Master’s degree in Business Administration.

9

Item 1A.RISK FACTORS

Our operations and financial results are subject to various risks and uncertainties, which may materially and adversely affect our business, financial condition, and results of operations, and the actual outcome of matters as to which forward-looking statements are made in this Annual Report. In such case, the trading price for DXC common stock could decline, and you could lose all or part of your investment. Past performance may not be a reliable indicator of future financial performance and historical trends should not be used to anticipate results or trends in future periods. Future performance and historical trends may be adversely affected by the aforementioned risks, and other variables and risks and uncertainties not currently known or that are currently expected to be immaterial may also materially and adversely affect our business, financial condition, and results of operations or the price of our common stock in the future.

Risk Factor Summary

The following is a summary of the risk factors our business faces. The list below is not exhaustive, and investors should read this "Risk Factors" section in full. Some of the risks we face include:

Risks Related to Our Business

•Our business and financial results have been adversely affected and could continue to be materially adversely affected by the COVID-19 crisis.

•We may not succeed in our strategic objectives and our strategic transactions may prove unsuccessful.

•We could be held liable for damages, our reputation could suffer, or we may experience service interruptions, from security breaches, cyber-attacks or disclosure of confidential information or personal data.

•Our ability to continue to develop and expand our service offerings to address emerging business demands and technological trends, including our ability to sell differentiated services up the Enterprise Technology Stack, may impact our future growth.

•Our ability to compete in certain markets we serve is dependent on our ability to continue to expand our capacity in certain offshore locations. However, as our presence in these locations increases, we are exposed to risks inherent to these locations which may adversely affect our revenue and profitability.

•Our credit rating and ability to manage working capital, refinance and raise additional capital for future needs could adversely affect our liquidity, capital position, borrowing, cost and access to capital markets.

•We have indebtedness, which could have a material adverse effect on our business, financial condition and results of operations.

•Our primary markets are highly competitive. If we are unable to compete in these highly competitive markets, our results of operations may be materially and adversely affected.

•If we are unable to accurately estimate the cost of services and the timeline for completion of contracts, the profitability of our contracts may be materially and adversely affected.

•Performance under contracts, including those on which we have partnered with third parties, may be adversely affected if we or the third parties fail to deliver on commitments or otherwise breach obligations to our customers.

•Our ability to provide customers with competitive services is dependent on our ability to attract and retain qualified personnel.

•Our international operations are exposed to risks, including fluctuations in exchange rates.

•Our business operations are subject to various and changing federal, state, local and foreign laws and regulations that could result in costs or sanctions that adversely affect our business.

10

•We may not achieve some or all of the expected benefits of our restructuring plans and our restructuring may adversely affect our business.

•We may inadvertently infringe on the intellectual property rights of others and our inability to procure third-party licenses may result in decreased revenue or increased costs.

•We may be exposed to negative publicity and other potential risks if we are unable to achieve and maintain effective internal controls over financial reporting.

•We have identified a material weakness in our internal control over financial reporting. Without effective internal control over financial reporting, we may fail to detect or prevent a material misstatement in our financial statements, which could materially harm our business, our reputation and our stock price.

•We could suffer additional losses due to asset impairment charges.

•We may not be able to pay dividends or repurchase shares of our common stock.

•Pending litigations may have a material and adverse impact on our profitability and liquidity.

•We may be adversely affected by disruptions in the credit markets, including disruptions that reduce our customers' access to credit and increase the costs to our customers of obtaining credit, and our hedging program is subject to counterparty default risk.

•We derive significant revenues and profit from contracts awarded through costly competitive bidding processes, and we may not achieve revenue and profit objectives if we fail to bid on these projects effectively.

•If our customers experience financial difficulties, we may not be able to collect our receivables.

•If we are unable to maintain and grow our customer relationships over time or to comply with customer contracts or government contracting regulations or requirements, our operating results and cash flows will suffer.

•Recent U.S. tax legislation may materially affect our financial condition, results of operations and cash flows, and changes in our tax rates could affect our future results.

Risks Related to Our Strategic Transactions

•We could have an indemnification obligation to HPE if the stock distribution in connection with the HPES business separation were determined not to qualify for tax-free treatment.

•If the HPES Merger does not qualify as a reorganization under Section 368(a) of the Code, CSC's former stockholders may incur significant tax liabilities.

•We assumed certain material pension benefit obligations following the HPES Merger. These liabilities and future funding obligations could restrict our cash available for operations, capital expenditures and other requirements.

•The USPS Separation and Mergers and NPS Separation could result in substantial tax liability to DXC and our stockholders.

11

Risks Related to Our Business

Our business and financial results have been adversely affected and could continue to be materially adversely affected by the COVID-19 crisis.

The COVID-19 crisis has caused disruptions in global economies, financial and commodities markets and rapid shifts in governmental and public health policies in the countries where we operate or our customers are located or the industries in which we and our customers compete. The COVID-19 crisis and the actions taken by governments, businesses and individuals to curtail the spread of the disease have negatively impacted, and are expected to continue to negatively impact our business, results of operations, cash flows and financial condition. The extent of such impact will depend on future developments, including the duration and spread of COVID-19, the speed at which the vaccine is distributed, the number of individuals in general who agree to receive the vaccine along with the number of our employees receiving the vaccine. In addition, the recent COVID-19 strain mutations may also hamper the vaccine's effectiveness.

Negative impacts that have occurred, or may occur in the future, include disruptions or restrictions on our employees’ ability to work effectively, as well as temporary closures of our facilities or the facilities of our customers or our subcontractors, or the requirements to deliver our services remotely. A significant portion of our application outsourcing and software development activities is in India, which is currently experiencing a high rate of COVID-19 infections. Continued public health threat and government responses could materially adversely affect our operations and the delivery of our services. Negative impacts from COVID-19 could potentially affect our ability to perform under our contracts with customers. Cost increases may not be recoverable from customers or covered by insurance, which could impact our profitability. If a business interruption occurs and we are unsuccessful in our continuing efforts to minimize the impact of these events, our business, results of operations, financial position, and cash flows could be materially adversely affected.

In addition, the COVID-19 crisis has resulted in a widespread global health crisis that is adversely affecting the economies and financial markets of many countries, which could result in an economic downturn that may negatively affect demand for our services, including the financial failure of some of our customers. This economic downturn, depending upon its severity and duration, could also lead to the deterioration of worldwide credit and financial markets that could limit our customers’ ability or willingness to pay us in a timely manner and our ability to obtain external financing to fund our operations and capital expenditures, result in losses on our holdings of cash and investments due to failures of financial institutions and other parties, and result in a higher rate of losses on our accounts receivables due to credit defaults.

Our financial results may also be materially and adversely impacted by a variety of factors related to COVID-19 that have not yet been determined, including potential impairments of goodwill and other assets, and changes to our contingent liabilities, for which actual amounts may materially exceed management estimates and our calculation of global tax liabilities. Even after the COVID-19 crisis has subsided, depending upon its duration and potential recurrence, and the governmental policies in response thereto, we may continue to experience materially adverse impacts to our business as a result of its global economic impact, including any recession that may occur or be continuing as a result.

We continue to evaluate the extent to which the COVID-19 crisis has impacted us and our employees, customers and suppliers and the extent to which it and other emerging developments will impact us and our employees, customers and suppliers in the future. We caution investors that any of the factors mentioned above could have material and adverse impacts on our current and future business, results of operations, cash flows and financial condition.

To the extent the COVID-19 crisis and the resulting economic disruption continue to adversely affect our business and financial results, it may also have the effect of heightening many of the other risks described in this “Risk Factors” section, such as those relating to our level of indebtedness, our ability to generate sufficient cash flows to service our indebtedness and to comply with the covenants contained in the agreements that govern our indebtedness and our counterparty credit risk.

12

We may not succeed in our strategic objectives, which could adversely affect our business, financial condition, results of operations and cash flows.

Our transformation journey focuses on our customers, optimizing costs and seizing the market. Our strategic priorities include an initiative to assist DXC customers across a broader range of their information technology needs, which we refer to as “the enterprise technology stack.” We may not be able to implement our strategic priorities and progress on our transformation journey in accordance with our expectations for a variety of reasons, including failure to execute on our plans in a timely fashion, lack of adequate skills, ineffective management, inadequate incentives, customer resistance to new initiatives, inability to control costs or maintain competitive offerings. We also cannot be certain that executing on our strategy will generate the benefits we expect. If we fail to execute successfully on our strategic priorities, or if we pursue strategic priorities that prove to be unsuccessful, our business, financial position, results of operations and cash flows may be materially and adversely affected.

We could be held liable for damages, our reputation could suffer, or we may experience service interruptions, from security breaches, cyber-attacks, other security incidents or disclosure of confidential information or personal data, which could cause significant financial loss.

As a provider of IT services to private and public sector customers operating in a number of industries and countries, we store and process increasingly large amounts of data for our customers, including sensitive and personally identifiable information. We also manage IT infrastructure of our own and of customers. We possess valuable proprietary information, including copyrights, trade secrets and other intellectual property and we collect and store certain personal and financial information from customers and employees. Our security measures designed to identify and protect against security incidents may fail to detect, prevent or adequately respond to a future threat incident. Security incidents can result from unintentional events or deliberate attacks by insiders such as employees, contractors or service providers or third parties, including criminals, competitors, nation-states, and hacktivists. These incidents can result in significant disruption to our business through an impact on our operations or those of our clients, employees, vendors or other partners; loss of data (including proprietary, confidential or otherwise sensitive or valuable information) for us, our clients, employees, vendors or partners; reputational damage, injury to customer relationships, liability (whether contractual or otherwise) for any of the above, including monetary damages; remediation costs; regulatory actions from regulators; any of which, or a combination of which, could have a material impact on our results of operations or financial condition. The regulatory environment related to information security and data privacy is evolving rapidly and the Company will need to expend time and resources to ensure compliance with these evolving regulations, and failure to understand and comply with these regulations can have an impact on the Company, its results of operations, and financial condition.

The continued occurrence of high-profile data breaches and cyber-attacks, including by nation-state actors, reflects an external environment that is increasingly hostile to information and corporate security. Like other companies, we face an evolving array of information security and data security threats that pose risks to us and our customers. We can also be harmed by attacks on third parties, such as denial-of-service attacks. We see regular unauthorized efforts to access our systems, which we evaluate for severity and frequency. For example, in July 2020, certain systems of our subsidiary, Xchanging, experienced a ransomware attack. While incidents experienced thus far have not resulted in significant disruption to our business, it is possible that we could suffer a severe attack or incident, with potentially material and adverse effects on our business, reputation, customer relations, results of operations or financial condition.

In the event of a security incident, we could be exposed to regulatory actions, customer attrition due to reputational concerns or otherwise, containment and remediation expenses, and claims brought by our customers or others for breaching contractual confidentiality and security provisions or data protection or privacy laws. We must expend capital and other resources to protect against security incidents, including attempted security breaches and cyber-attacks and to alleviate problems caused by successful breaches or attacks. The cost, potential monetary damages, and operational consequences of responding to security incidents and implementing remediation measures could be significant and may be in excess of insurance policy limits or be not covered by our insurance at all.

13

We rely on internal and external information and technological systems to manage our operations and are exposed to risk of loss resulting from security incidents, including breaches in the security or other failures of these systems. Security incidents such as through an advanced persistent threat attack, or the accidental loss, inadvertent disclosure or unapproved dissemination of proprietary information or sensitive or confidential data about us, or our customers, could expose us to risk of loss of this information, regulatory scrutiny, actions and penalties, extensive contractual liability and other litigation, reputational harm, and a loss of customer confidence, which could potentially have an adverse impact on future business with current and potential customers. Moreover, failure to maintain effective internal accounting controls related to data security breaches and cybersecurity in general could impact our ability to produce timely and accurate financial statements and could subject us to regulatory scrutiny.

Advances in computer capabilities, new discoveries in the field of cryptography or other events or developments may result in a compromise or breach of the algorithms that we use to protect our data and that of customers, including sensitive customer transaction data. A party, whether an insider or third party operating outside the Company, who is able to circumvent our security measures or those of our contractors, partners or vendors could access our systems and misappropriate proprietary information, the confidential data of our customers, employees or business partners or cause interruption in our or their operations.

Experienced computer programmers, hackers or insiders may be able to penetrate our network security and misappropriate or compromise our confidential information or that of third parties, create system disruptions or cause shutdowns. Computer programmers and hackers have deployed and may continue to develop and deploy ransomware, malware and other malicious software programs through phishing and other methods that attack our products or otherwise exploit any security vulnerabilities of these products. In addition, sophisticated hardware and operating system software and applications produced or procured from third parties may contain defects in design or manufacture, including “bugs” and other problems that could unexpectedly interfere with the security and operation of our systems, or harm those of third parties with whom we may interact. The costs to eliminate or alleviate cyber or other security problems, including ransomware, malware, bugs, malicious software programs and other security vulnerabilities, could be significant, and our efforts to address these problems may not be successful and could result in interruptions, delays, cessation of service and loss of existing or potential customers, which may impede our sales, distribution or other critical functions.

Increasing cybersecurity, data privacy and information security obligations around the world could also impose additional regulatory pressures on our customers’ businesses and, indirectly, on our operations, or lead to inquiries or enforcement actions. In the United States, we are seeing increasing obligations and expectations from federal and non-federal customers. In response, some of our customers have sought, and may continue to seek, to contractually impose certain strict data privacy and information security obligations on us. Some of our customer contracts may not limit our liability for the loss of confidential information. If we are unable to adequately address these concerns, our business and results of operations could suffer.

14

Compliance with new privacy and security laws, requirements and regulations may result in cost increases due to expanded compliance obligations, potential systems changes, the development of additional administrative processes and increased enforcement actions, litigation, fines and penalties. The regulatory landscape in these areas continues to evolve rapidly, and there is a risk that the Company could fail to address or comply with the fast changing regulatory environment, which could lead to regulatory or other actions which result in material liability for the Company. For example, in 2020, the California Consumer Privacy Act (“CCPA”) came into force and provides new data privacy rights for California consumers and new operational requirements for covered companies. The CCPA also includes a private right of action for certain data breaches that is expected to increase data breach litigation. Failure to comply with the CCPA could result in civil penalties of $2,500 for each violation or $7,500 for each intentional violation. Additionally, a new privacy law, the California Privacy Rights Act (“CPRA”), was approved by California voters in the November 3, 2020 election. The CPRA, which takes effect on January 1, 2023 and significantly modifies the CCPA, potentially results in further uncertainty and could require us to incur additional costs and expenses in an effort to comply. Some observers have noted the CCPA and CPRA could mark the beginning of a trend toward more stringent privacy legislation in the United States, which could also increase our potential liability and adversely affect our business. For example, the CCPA has encouraged “copycat” laws in other states across the country, such as in Virginia, New Hampshire, Illinois and Nebraska. This legislation may add additional complexity, variation in requirements, restrictions and potential legal risk, require additional investment in resources to compliance programs, and could impact strategies and availability of previously useful data and could result in increased compliance costs and/or changes in business practices and policies.

In addition, the data protection landscape in the European Union (“EU”) is continually evolving, resulting in possible significant operational costs for internal compliance and risks to our business. The EU adopted the General Data Protection Regulation (“GDPR”), which became effective in May 2018, and contains numerous requirements and changes from previously existing EU laws, including more robust obligations on data processors and heavier documentation requirements for data protection compliance programs by companies.

Among other requirements, the GDPR regulates the transfer of personal data subject to the GDPR to third countries that have not been found to provide adequate protection to such personal data, including the United States. Recent legal developments in Europe have created complexity and uncertainty regarding such transfers. For instance, on July 16, 2020, the Court of Justice of the European Union (the “CJEU”) invalidated the EU-U.S. Privacy Shield Framework (the “Privacy Shield”) under which personal data could be transferred from the EEA to U.S. entities who had self-certified under the Privacy Shield scheme. While the CJEU upheld the adequacy of the standard contractual clauses (a standard form of contract approved by the European Commission as an adequate personal data transfer mechanism and potential alternative to the Privacy Shield), it made clear that reliance on such clauses alone may not necessarily be sufficient in all circumstances. Use of the standard contractual clauses must now be assessed on a case-by-case basis taking into account the legal regime applicable in the destination country, including, in particular, applicable surveillance laws and rights of individuals, and additional measures and/or contractual provisions may need to be put in place; however, the nature of these additional measures is currently uncertain. The CJEU went on to state that if a competent supervisory authority believes that the standard contractual clauses cannot be complied with in the destination country and that the required level of protection cannot be secured by other means, such supervisory authority is under an obligation to suspend or prohibit that transfer.

Failure to comply with the GDPR could result in penalties for noncompliance (including possible fines of up to the greater of €20 million and 4% of our global annual turnover for the preceding financial year for the most serious violations, as well as the right to compensation for financial or non-financial damages claimed by individuals under Article 82 of the GDPR).

Further, in March 2017, the United Kingdom (“U.K.”) formally notified the European Council of its intention to leave the EU pursuant to Article 50 of the Treaty on European Union (“Brexit”). The U.K. ceased to be an EU Member State on January 31, 2020, but enacted a Data Protection Act substantially implementing the GDPR, effective in May 2018, which was further amended to align more substantially with the GDPR following Brexit. It is unclear how U.K. data protection laws or regulations will develop in the medium to longer term. Since the beginning of 2021 we must comply with both the GDPR and the U.K. GDPR, with each regime having the ability to fine up to the greater of €20 million (in the case of the GDPR) or £17 million (in the case of the U.K. GDPR) and 4% of total annual revenue.

15

While we strive to comply with all applicable data protection laws and regulations, as well as internal privacy policies, any failure or perceived failure to comply or any misappropriation, loss or other unauthorized disclosure of sensitive or confidential information may result in proceedings or actions against us by government or other entities, private lawsuits against us (including class actions) or the loss of customers, which could potentially have an adverse effect on our business, reputation and results of operations.

Portions of our infrastructure also may experience interruptions, delays or cessations of service or produce errors in connection with systems integration or migration work that takes place from time to time. We may not be successful in implementing new systems and transitioning data, which could cause business disruptions and be expensive, time-consuming, disruptive and resource intensive. Such disruptions could adversely impact our ability to fulfill orders and respond to customer requests and interrupt other processes. Delayed sales, lower margins or lost customers resulting from these disruptions could reduce our revenues, increase our expenses, damage our reputation, and adversely affect our stock price.

Our strategic transactions may prove unsuccessful and our profitability may be materially and adversely affected.

At any given time, we may be engaged in discussions or negotiations with respect to one or more transactions, including acquisitions, divestitures or spin-offs, strategic partnerships or other transaction involving one or more of our businesses. Any of these transactions could be material to our business, financial condition, results of operations and cash flows. We may ultimately determine not to proceed with any transaction for commercial, financial, strategic or other reasons. As a result, we may not realize benefits expected from exploring one or more strategic transactions, may realize benefits further in the future or those benefits may ultimately be significantly smaller than anticipated, which could adversely affect our business, financial condition, results of operations and cash flows.

In addition, we may fail to complete transactions. Closing transactions is subject to uncertainties and risks, including the risk that we may be unable to satisfy conditions to closing, such as regulatory and financing conditions and the absence of material adverse changes to our business.

For acquisitions, our inability to successfully integrate the operations we acquire and leverage these operations to generate substantial cost savings, as well as our inability to avoid revenue erosion and earnings decline, could have a material adverse effect on our results of operations, cash flows and financial position. In order to achieve successful acquisitions, we will need to:

•integrate the operations and business cultures, as well as the accounting, financial controls, management information, technology, human resources and other administrative systems, of acquired businesses with existing operations and systems;

•maintain third-party relationships previously established by acquired companies;

•attract and retain senior management and key personnel at acquired businesses; and

•manage new business lines, as well as acquisition-related workload.

Existing contractual restrictions may limit our ability to engage in certain integration activities for varying periods. We may not be successful in meeting these or any other challenges encountered in connection with historical and future acquisitions. Even if we successfully integrate, we cannot predict with certainty if or when these cost and revenue synergies, growth opportunities and benefits will occur, or the extent to which they actually will be achieved. In addition, the quantification of previously announced synergies expected to result from an acquisition is based on significant estimates and assumptions that are subjective in nature and inherently uncertain. Realization of any benefits and synergies could be affected by a number of factors beyond our control, including, without limitation, general economic conditions, increased operating costs, regulatory developments and other risks. In addition, future acquisitions could require dilutive issuances of equity securities and/or the assumption of contingent liabilities. The occurrence of any of these events could adversely affect our business, financial condition and results of operations.

16

Divestiture transactions, such as the USPS Separation, the sale of HHS business to Veritas Capital or the sale of the HPS business to Dedalus, also involve significant challenges and risks, including:

•the potential loss of key customers, suppliers, vendors and other key business partners;

•declining employee morale and retention issues affecting employees, which may result from changes in compensation, or changes in management, reporting relationships, future prospects or perceived expectations;

•difficulty making new and strategic hires of new employees;

•diversion of management time and a shift of focus from operating the businesses to transaction execution considerations;

•customers delaying or deferring decisions or ending their relationships;

•the need to provide transition services, which may result in stranded costs and the diversion of resources and focus;

•the need to separate operations, systems (including accounting, management, information, human resource and other administrative systems), technologies, products and personnel, which is an inherently risky and potentially lengthy and costly process;

•the inefficiencies and lack of control that may result if such separation is delayed or not implemented effectively, and unforeseen difficulties and expenditures that may arise as a result including potentially significant stranded costs;

•our desire to maintain an investment grade credit rating may cause us to use cash proceeds, if any, from any divestitures or other strategic transactions that we might otherwise have used for other purposes in order to reduce our financial leverage;

•the inability to obtain necessary regulatory approvals or otherwise satisfy conditions required in order consummate any such transactions;

•our dependence on accounting, financial reporting, operating metrics and similar systems, controls and processes of divested businesses could lead to challenges in preparing our consolidated financial statements or maintaining effective financial control over financial reporting; and

•including contractual terms limiting our ability to compete for or perform certain contracts or services.

We have also entered into and intend to identify and enter into additional strategic partnerships with other industry participants that will allow us to expand our business. However, we may be unable to identify attractive strategic partnership candidates or complete these partnerships on terms favorable to us. In addition, if we are unable to successfully implement our partnership strategies or our strategic partners do not fulfill their obligations or otherwise prove disadvantageous to our business, our investments in these partnerships and our anticipated business expansion could be adversely affected.

Our ability to continue to develop and expand our service offerings to address emerging business demands and technological trends, including our ability to sell differentiated services up the Enterprise Technology Stack, may impact our future growth. If we are not successful in meeting these business challenges, our results of operations and cash flows may be materially and adversely affected.

Our ability to implement solutions for our customers, incorporating new developments and improvements in technology that translate into productivity improvements for our customers, and our ability to develop digital and other new service offerings that meet current and prospective customers' needs, as well as evolving industry standards, are critical to our success. The markets we serve are highly competitive and characterized by rapid technological change which has resulted in deflationary pressure in the price of services which in turn can adversely impact our margins. Our competitors may develop solutions or services that make our offerings obsolete or may force us to decrease prices on our services which can result in lower margins. Our ability to develop and implement up to date solutions utilizing new technologies that meet evolving customer needs in digital cloud, information technology outsourcing, consulting, industry software and solutions, and application services markets, and in areas such as artificial intelligence, automation, Internet of Things and as-a-service solutions, in a timely or cost-effective manner, will impact our ability to retain and attract customers and our future revenue growth and earnings. If we are unable to continue to execute our strategy and build our business across the Enterprise Technology Stack in a highly competitive and rapidly evolving environment or if we are unable to commercialize such services and solutions, expand and scale them with sufficient speed and versatility, our growth, productivity objectives and profit margins could be negatively affected.

17

Technological developments may materially affect the cost and use of technology by our customers. Some of these technologies have reduced and replaced some of our traditional services and solutions and may continue to do so in the future. This has caused, and may in the future cause, customers to delay spending under existing contracts and engagements and to delay entering into new contracts while they evaluate new technologies. Such delays can negatively impact our results of operations if the pace and level of spending on new technologies by some of our customers is not sufficient to make up any shortfall by other customers. Our growth strategy focuses on responding to these types of developments by driving innovation that will enable us to expand our business into new growth areas. If we do not sufficiently invest in new technology and adapt to industry developments, or evolve and expand our business at sufficient speed and scale, or if we do not make the right strategic investments to respond to these developments and successfully drive innovation, our services and solutions, our results of operations, and our ability to develop and maintain a competitive advantage and to execute on our growth strategy could be negatively affected.

Our ability to compete in certain markets we serve is dependent on our ability to continue to expand our capacity in certain offshore locations. However, as our presence in these locations increases, we are exposed to risks inherent to these locations which may adversely affect our revenue and profitability.

A significant portion of our application outsourcing and software development activities has been shifted to India and we plan to continue to expand our presence there and in other lower-cost locations. As a result, we are exposed to the risks inherent in operating in India or other locations, including (1) the current high rate of COVID-19 infections and government responses, including renewed lockdowns,(2) a highly competitive labor market for skilled workers which may result in significant increases in labor costs, as well as shortages of qualified workers in the future and (3) the possibility that the U.S. Federal Government or the European Union may enact legislation that creates significant disincentives for customers to locate certain of their operations offshore, which would reduce the demand for the services we provide in such locations and may adversely impact our cost structure and profitability. In addition, India has experienced, and other countries may experience, political instability, civil unrest and hostilities with neighboring countries. Negative or uncertain political climates in countries or locations where we operate, such as Ukraine and Russia, including but not limited to, military activity or civil hostilities, criminal activities and other acts of violence, infrastructure disruption, natural disasters or other conditions could adversely affect our operations.

We are subject to the U.S. Foreign Corrupt Practices Act of 1977, as amended ("FCPA") and similar anti-bribery laws in other jurisdictions. We pursue opportunities in certain parts of the world that experience government corruption and in certain circumstances, compliance with anti-bribery laws may conflict with local customs and practices. Our internal policies mandate compliance with all applicable anti-bribery laws. We require our employees, partners, subcontractors, agents, and others to comply with the FCPA and other anti-bribery laws. There is no assurance that our policies or procedures will protect us against liability under the FCPA or other laws for actions taken by our employees and intermediaries. If we are found to be liable for FCPA violations (either due to our own acts or our omissions, or due to the acts or omissions of others), we could suffer from severe criminal or civil penalties or other sanctions, which could have a material adverse effect on our reputation, business, results of operations or cash flows. In addition, detecting, investigating and resolving actual or alleged violations of the FCPA or other anti-bribery violations is expensive and could consume significant time and attention of our senior management.

18

Our credit rating and ability to manage working capital, refinance and raise additional capital for future needs, could adversely affect our liquidity, capital position, borrowing, cost, and access to capital markets.

We currently maintain investment grade credit ratings with Moody's Investors Service, Fitch Rating Services, and Standard & Poor's Ratings Services. Our credit ratings are based upon information furnished by us or obtained by a rating agency from its own sources and are subject to revision, suspension or withdrawal by one or more rating agencies at any time. Rating agencies may review the ratings assigned to us due to developments that are beyond our control, including potential new standards requiring the agencies to reassess rating practices and methodologies. Ratings agencies may consider changes in credit ratings based on changes in expectations about future profitability and cash flows even if short-term liquidity expectations are not negatively impacted. If changes in our credit ratings were to occur, it could result in higher interest costs under certain of our credit facilities. It would also cause our future borrowing costs to increase and limit our access to capital markets. For example, we currently fund a portion of our working capital requirements in the U.S. and European commercial paper markets. Any downgrade below our current rating would, absent changes to current market liquidity, substantially reduce or eliminate our ability to access that source of funding and could otherwise negatively impact the perception of our company by lenders and other third parties. In addition, certain of our major contracts provide customers with a right of termination in certain circumstances in the event of a rating downgrade below investment grade. There can be no assurance that we will be able to maintain our credit ratings, and any additional actual or anticipated changes or downgrades in our credit ratings, including any announcement that our ratings are under review for a downgrade, may have a negative impact on our liquidity, capital position and access to capital markets.

Our liquidity is a function of our ability to successfully generate cash flows from a combination of efficient operations and continuing operating improvements, access to capital markets and funding from third parties. In addition, like many multinational regulated enterprises, our operations are subject to a variety of tax, foreign exchange and regulatory capital requirements in different jurisdictions that have the effect of limiting, delaying or increasing the cost of moving cash between jurisdictions or using our cash for certain purposes. Our ability to maintain sufficient liquidity going forward is subject to the general liquidity of and on-going changes in the credit markets as well as general economic, financial, competitive, legislative, regulatory and other market factors that are beyond our control. An increase in our borrowing costs, limitations on our ability to access the global capital and credit markets or a reduction in our liquidity can adversely affect our financial condition and results of operations.

Information regarding our credit ratings is included in Part II, Item 7 of this Annual Report on Form 10-K under the caption "Liquidity and Capital Resources."

19

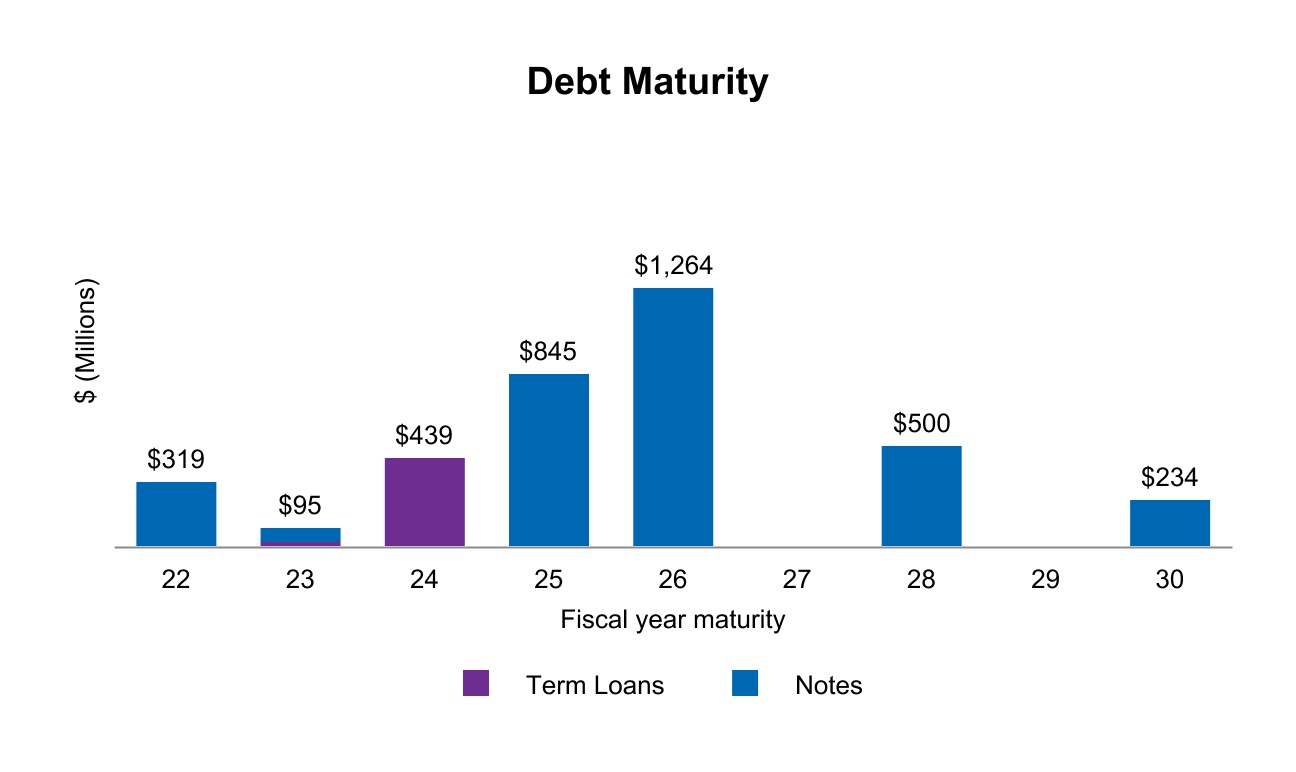

We have indebtedness, which could have a material adverse effect on our business, financial condition and results of operations.

We have indebtedness totaling approximately $5.5 billion as of March 31, 2021 (including capital lease obligations). We may incur substantial additional indebtedness in the future for many reasons, including to fund acquisitions. Our existing indebtedness, together with the incurrence of additional indebtedness and the restrictive covenants contained in, or expected to be contained in the documents evidencing such indebtedness, could have significant consequences on our future operations, including:

•events of default if we fail to comply with the financial and other covenants contained in the agreements governing our debt instruments, which could, if material and not cured, result in all of our debt becoming immediately due and payable or require us to negotiate an amendment to financial or other covenants that could cause us to incur additional fees and expenses;

•subjecting us to the risk of increased sensitivity to interest rate increases in our outstanding variable-rate

indebtedness that could cause our debt service obligations to increase significantly;

•increasing the risk of a future credit ratings downgrade of our debt, which could increase future debt costs

and limit the future availability for debt financing;

•debt service may reduce the availability of our cash flow to fund working capital, capital expenditures, acquisitions and other general corporate purposes, and limiting our ability to obtain additional financing for these purposes;

•placing us at a competitive disadvantage compared to less leveraged competitors;

•increasing our vulnerability to the impact of adverse economic and industry conditions; and

•causing us to reduce or eliminate our return of cash to our stockholders, including via dividends and share repurchases.

In addition, we could be unable to refinance our outstanding indebtedness on reasonable terms or at all.

Our ability to meet our payment and other obligations under our debt instruments depends on our ability to generate significant cash flow in the future. This, to some extent, is subject to general economic, financial, competitive, legislative and regulatory factors as well as other factors that are beyond our control. There can be no assurance that our business will generate sufficient cash flow from operations, or that current or future borrowings will be sufficient to meet our current debt obligations and to fund other liquidity needs.